Online Bayesian changepoint detection for network Poisson processes with community structure

Abstract

Network point processes often exhibit latent structure that govern the behaviour of the sub-processes. It is not always reasonable to assume that this latent structure is static, and detecting when and how this driving structure changes is often of interest. In this paper, we introduce a novel online methodology for detecting changes within the latent structure of a network point process. We focus on block-homogeneous Poisson processes, where latent node memberships determine the rates of the edge processes. We propose a scalable variational procedure which can be applied on large networks in an online fashion via a Bayesian forgetting factor applied to sequential variational approximations to the posterior distribution. The proposed framework is tested on simulated and real-world data, and it rapidly and accurately detects changes to the latent edge process rates, and to the latent node group memberships, both in an online manner. In particular, in an application on the Santander Cycles bike-sharing network in central London, we detect changes within the network related to holiday periods and lockdown restrictions between 2019 and 2020.

Keywords — network point process, online variational inference, stochastic blockmodel, streaming data.

1 Introduction

Network data describe complex relationships between a large number of entities, called nodes, linked via edges. In particular, much of such data is continuous-time valued and dynamic in nature, with nodes often exhibiting a latent community structure that drives interactions (Amini et al., 2013). By allowing temporal point processes to exist on the edges of the network, and not solely focusing on the adjacency matrix, such interaction data can be more accurately understood. Common examples of these network structures include email exchanges within a company (Klimt and Yang, 2004) or posts on a social media platform (Paranjape et al., 2017), where employer hierarchy or political leanings, respectively, could drive connections between individuals. Furthermore, it is not always reasonable to assume that such structure is static. In the case of email exchanges, a change in an employee’s role within their organisation would alter the latent community structure of the network. Similarly, in social networks, a sporting or political event would likely affect the frequency of interactions only between users with particular characteristics and topics of interest. Detecting such changepoints is crucial in many real-world applications, such as in the context of computer networks, where modifications of network structure can signify malicious behaviour (see, for example, Hallgren et al., 2023). The detection of such changes in an online manner will be the focus of this paper.

Much of the original work on network models focused on simple, binary connections between nodes. One of the most common of these modelling approaches is the Stochastic Block Model (SBM; Holland et al., 1983), which models connections between nodes via a latent community structure on a network. This model has undergone significant development, with theoretical results extending to include node degree heterogeneity (Karrer and Newman, 2011; Amini et al., 2013; Gao et al., 2018), valued edges (Mariadassou et al., 2010), dynamic community structure in discrete time (Matias and Miele, 2017; Yang et al., 2011; Xu and Hero, 2014), and missing data (Mariadassou and Tabouy, 2020); refer to Lee and Wilkinson (2019) for a comprehensive review. In spite of their simplicity, SBMs can be used to consistently estimate and approximate much more complex network objects, such as exchangeable random graphs and their associated graphons, and thus provide a good approximation for any exchangable random graph model (Airoldi et al., 2013). However, most of these advancements are based on aggregated, discrete time data.

There are several statistical methods for analysing dynamic networks, normally defined as graphs with time-evolving edge-connections. Interested readers are referred to Holme (2015) for a review. However, most of this methodology does not capture instantaneous interactions, but relies instead on aggregations (see, for example, Shlomovich et al., 2022). To combat this, Matias et al. (2018) developed a model for recurrent interaction events, which they call the semiparametric stochastic block model. In this framework, interactions are modelled by a conditional inhomogeneous Poisson process, with intensities depending solely on the latent group memberships of the interacting individuals. Perry and Wolfe (2013) uses a Cox multiplicative intensity model with covariates to model the point processes observed on each edge. Sanna Passino and Heard (2023) models the edge-specific processes via mutually exciting processes with intensities depending only on node-specific parameters. These methodologies handle complex temporal data, but they are offline methods, and work only in the case of a static latent network structure. Attempts have been made at capturing networks with a dynamic latent structure, but attention has focused on discrete time data, such as binary or weighted edges. Matias and Miele (2017) proposed a method for frequentist inference for a model which extends the SBM to allow for dynamic group memberships. In that work, the dynamics of the groups are modelled by a discrete time Markov chain. Heard et al. (2010) developed a two-stage offline method for anomaly detection in dynamic graphs. However, to the best of our knowledge, there currently exists no methodology for online detection of changepoints in the context of continuous-time network data.

The recent work of Fang et al. (2024) represents the first attempt at online estimation and community detection of a network point process. The authors build upon the foundation laid by Matias et al. (2018) and extend it to an online setting, but maintain the assumption of a static latent structure. While Fang et al. (2024) do offer suggestions as to how their framework could be extended to incorporate latent dynamics, the methodology developed therein requires knowing both the adjacency matrix and the number of latent groups a priori.

In this work, we propose a novel online Bayesian changepoint detection algorithm for network point processes with a latent community structure among the nodes. Our methodology is based on utilising forgetting factors within a Bayesian context to sequentially update the variational approximation to the posterior distribution of the model parameters when new data are observed within a stream. We focus on what we will refer to as a dynamic Bayesian block-homogeneous network Poisson process, where dynamic refers to the fact that the latent structure of the network is time-varying. As an added benefit, our method is able to accurately infer the community structure and obtain a piecewise recovery of the conditional intensity function when we consider inhomogeneous Poisson processes on the edges. Extensions to our method are also proposed to simultaneously infer both the adjacency matrix of the network and the number of latent groups in an online manner, and handle cases where new groups are created or existing groups are merged into one another.

The remainder of this article is structured as follows: Section 2 describes the dynamic Bayesian block-homogeneous Poisson process model used in this work, and the possible local and global changes to the network structure occurring on such a network model. Section 3 discusses the proposed online variational Bayesian inference approach via Bayesian forgetting factor, which is used to sequentially approximate the posterior distribution on the stream. The performance of the proposed inferential procedure is then tested in Section 4 on simulated data, and on real-world data from the Santander Cycles bike-sharing network in Section 5, followed by a discussion.

2 Bayesian dynamic block homogeneous Poisson process

2.1 The model

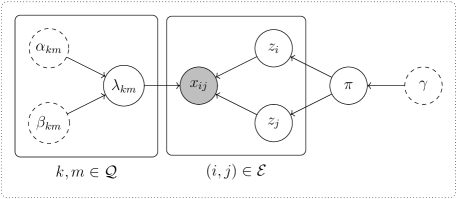

We consider a stochastic process on a network, which produces dyadic interaction data between a set of nodes observed over time. Let be a graph, where the set corresponds to nodes, whereas the edge set contains pairs representing interactions between nodes in . In particular, we write if there is a connection from node to node . Furthermore, we denote the set of all possible edges between nodes as . The graph could be equivalently represented via its adjacency matrix such that , where denotes the indicator function.

We assume that each node belongs to a group , where and we let be a priori independent and identically distributed with where , such that for all , and . We also associate to a binary vector , with , and we write to denote the matrix of group memberships. Under a Bayesian framework, we place a Dirichlet prior distribution on with parameter .

We observe a marked point process on the network, consisting of a stream of triplets , denoting directed interactions from node to node at time , where for . The associated edge-specific counting process is denoted by , where

| (2.1) |

If , for the entire observation period. In this work, we model the counting process as a Poisson process with rate , conditional on and on the node group memberships and . Also, we place independent conjugate gamma prior distributions on the event rates . In summary, the full model can be expressed as follows:

| (2.2) | |||||

| (2.3) | |||||

| (2.4) | |||||

| (2.5) | |||||

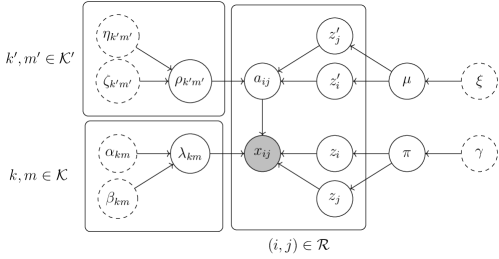

where , and . Note that in (2.2), we use that for a homogeneous Poisson process with rate , the number of counts for that process on an interval of length is Poisson distributed with rate . The model in Equation (2.2) is known as block homogeneous Poisson process (BHPP; Fang et al., 2024), and it is represented in graphical model form in Figure 1.

Under the BHPP, the expected waiting time between events across the entire network is , as described in the following proposition.

Proposition 1.

Let be a directed graph with no isolated nodes. If on each edge lives a homogeneous Poisson process with rate , only dependent upon node memberships , then the expected waiting time between arrivals for the full network counting process is .

Proof.

Let with . Suppose that has connected components. As we have no isolated nodes, the number of edges is minimised with and if is even, or and , if is odd. Without loss of generality, assume and call the rate of the full network Poisson process . By superposition, it follows or , for even and odd, respectively, and so the expected waiting time , is bounded as . ∎

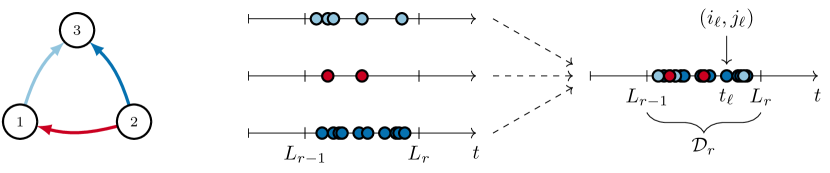

The aim of the present paper is to provide an online algorithm for detecting changepoints; such an algorithm must be able to perform inference at each iteration before the arrival of any new data. A consequence of Proposition 1 is that for networks of increasing size, this becomes infeasible for large when observing all events as they arrive, as an online algorithm would need to be at least as fast. This motivates a further assumption that data arrives as a stream of batched counts rather than a stream of continuous-valued event times. Let the batches be observed at times , where for . Each data batch takes the form

| (2.6) |

We consider the case of a constant time between batches, so that for all . Also, we denote the complete set of data available at time as . This setup is illustrated in Figure 2.

Initially, we assume that both the adjacency matrix and the number of latent groups are known a priori, similar to the setup in Fang et al. (2024). However, we note that assuming this knowledge is limiting in practical applications, since these quantities are usually unknown. Therefore, Sections 3.5 and 3.6 discuss extensions of the BHPP model and corresponding inference procedures with an unknown adjacency matrix and an unknown number of groups.

2.2 Changes to the network

In real-world applications, it is unrealistic to assume that the latent group memberships and rate matrix are constant across the entire observation period. Our objective is therefore to develop a framework which could be used to detect global and local changes to the model parameters.

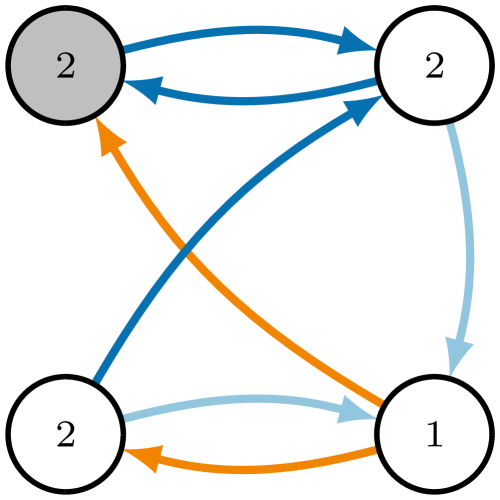

For local changes, we consider modifications to the latent group structure, allowing for any nodes to change their group membership at any time . In contrast to the approach of Matias and Miele (2017), in which the membership of node over the observation window behaves according to a discrete-time, irreducible and aperiodic Markov chain, we place no model on how or when nodes change and allow for any (finite) number of changes in a given interval. Furthermore, we allow for changes in continuous time, again in contrast to the discrete-time formulation of Matias and Miele (2017). Our main objective is only to detect if and when nodes have changed memberships, not to estimate the underlying group membership switching process. Figure 3 illustrates the effect of a single node switch in the case of nodes.

For global changes, we consider jumps in the intensity between any groups at some time of the form (). Again, we are interested in assessing if the block-specific intensity has changed, and we do not estimate or posit assumptions on the mechanism that leads to such changes.

3 An online variational Bayesian estimation procedure

We present an online inference procedure for tracking the time-evolving latent structure and parameters of the BHPP model described in Section 2.1. We focus first on the set-up where the full edge set and the number of latent groups is known, as in Fang et al. (2024). Next, we consider when is unknown, and then we move to the case of an unknown number of groups, using a Bayesian nonparametric approach.

3.1 Variational Bayesian approximation

Variational Bayesian (VB) inference has the objective to approximate a posterior distribution when it is not analytically tractable (Wang and Blei, 2019), offering a faster estimation approach when compared to Markov Chain Monte Carlo methods (Blei et al., 2017). This makes it more suited to the requirements of an online learning framework. We adopt the terminology of Blei et al. (2017) in distinguishing between local latent variables , that scale with the number of nodes, and global latent variables , whose dimension, written , does not change with .

In a variational approach, one posits a family of distributions on the parameter space , and seeks to select the component closest to the true posterior in the sense of the Kullback-Leibler (KL) divergence, where denotes the observed data. A mathematically convenient choice for is the mean-field variational family, the set of factorisable distributions of the form

| (3.1) |

The approximating distribution is then given as

| (3.2) |

Despite every taking a simple product structure, the solution to (3.2) is usually not available analytically. A popular method for approximating the global minimum of the KL-divergence is the Coordinate Ascent Variational Inference (CAVI) algorithm (Bishop, 2006; Blei et al., 2017), which iteratively updates each component of while keeping the others fixed. Letting denote the -dimensional vector of latent variables , CAVI proceeds as follows:

| (3.3) |

for until some convergence criterion is met. Under the mean-field variational approximation, (3.3) has the following solution (Bishop, 2006):

| (3.4) |

where the notation used to denote the expectation with respect to all components of except (Blei et al., 2017). As per convention with variational inference algorithms, we will drop the subscript on for notational convenience, and take the argument of the variational component to index it (see, for example, Blei et al., 2017).

It should be noted that CAVI is only guaranteed to achieve a local minimum, and hence is sensitive to intialisation (Zhang and Zhou, 2020; Blei et al., 2017). Furthermore, with , updates in (3.4) have an explicit ordering. The ordering of the updates can also have implications on the convergence properties of the algorithm (Ray and Szabó, 2022), similarly to Gibbs sampling (see, for example, van Dyk and Park, 2008).

3.2 Online VB for the dynamic BHPP

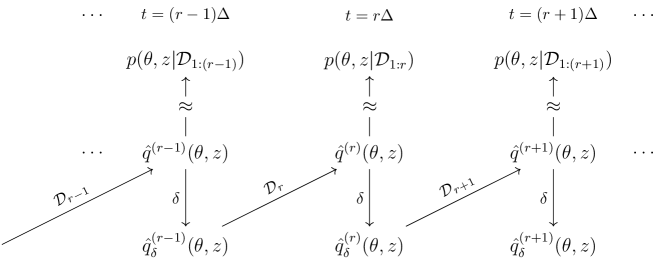

Upon receiving the latest batch at time , the aim of the online algorithm is to update the estimates of the BHPP parameters based on the entire history of the process. To ensure finite and constant complexity and memory, a truly online algorithm should be single pass (see, for example Bifet et al., 2018): each data batch should be inspected only once, and summaries of previous data batches are used in conjunction with to update parameter estimates.

The prior-posterior distribution updates within a Bayesian framework offers a natural way to propagate information forward in time. The posterior distribution at time contains the information that was learned from . A naive approach therefore is to pass this through as the new prior distribution for the update at time . However, this will perform poorly in the case of changing latent structure. As the number of batches increases, the new prior distributions become more concentrated around the current best estimates. This results in an updated posterior distribution that is largely dominated by its prior distribution (corresponding to the posterior distribution up to the previous batch) and which is increasingly insensitive to new data and changes in the data generating process.

We therefore propose to flatten the posterior obtained at , via temperature parameters, at the point of passing it through as the prior distribution for the update at . This flattening step is in effect down-weighting previous observations and can therefore be considered as a Bayesian analogue of the forgetting factor procedure that has been widely used in frequentist online literature (see, for example, Haykin, 2002; Bodenham and Adams, 2017). In this way, the parameter estimates are quicker to respond to changes in the latent rate structure.

Due to the independence of counts from a Poisson process within non-overlapping time windows, the posterior density at step under the BHPP model factorises as

| (3.5) |

where the prior distributions are chosen to be conjugate, as per (2.3) and (2.5). From (3.5), the posterior distribution at step can be interpreted as the prior for the posterior distribution at step .

The posterior density in (3.5) is not available in closed form and, due to the marginal density being unavailable, can only be evaluated up to a normalising constant. We thus consider the VB approach with the mean-field variational family, deploying the CAVI algorithm to compute approximate posterior distributions. Denoting the approximate posterior at step by , we pass through as the prior for step the tempered density

| (3.6) | ||||

| (3.7) |

controlled by the Bayesian forgetting factor (BFF) . Here, is a normalising constant to ensure a valid density. This procedure is visualised in Figure 4.

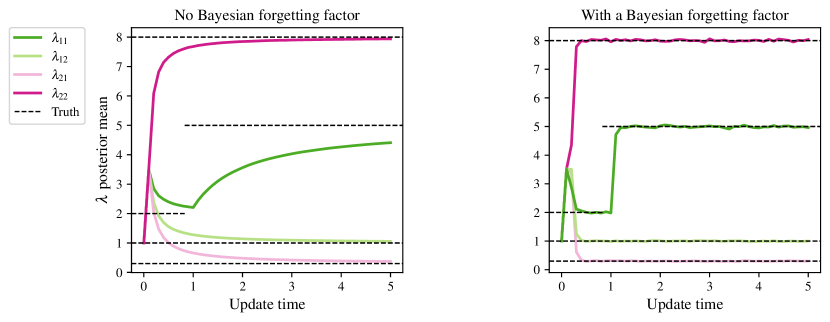

The effect of the BFF in down-weighting previous data and placing greater emphasis on the latest batch is illustrated in Figure 5. A fully-connected network is simulated on the time interval with nodes and groups. An instantaneous rate change in is made at . The left panel of Figure 5 shows the results for naive approach (without a forgetting factor), whereas the right panel includes a BFF and demonstrates a much faster response to the change and quicker convergence of the posterior mean to the true value.

3.3 Online CAVI updates

We assume that each component of (3.6) takes the same form of its corresponding complete conditional distribution under the standard BHPP model in (2.2)–(2.5), raised to a power and normalised:

Here, and are normalising constants, ensuring that the densities are valid, and are temperature parameters specific to each class of latent variables. Suppose that data is observed on the interval , for , and denote the count on edge during this interval by . Under the prior structure in (3.6), it is shown in Appendix A that the CAVI sequential updates are:

-

1.

for all where are defined as:

(3.8) (3.9) -

2.

for all where , with , satisfies the relation:

(3.10) -

3.

where is defined as:

(3.11)

Here is the digamma function. Note that the parameters , are jointly optimised via a fixed point solver for (3.10), iteratively moving through the rows of the matrix until convergence. The fixed point solver is initialised at the -th step by using the value of outputted from the -th step as the starting point, which also partially circumvents the problem of label switching (Jasra et al., 2005).

Algorithm 1 describes the full inference procedure based upon the updates in equations (3.9)–(3.11).

3.4 Detecting changepoints

In this work, we aim to detect two types of changepoints: changes in the point process rates and changes in the group memberships.

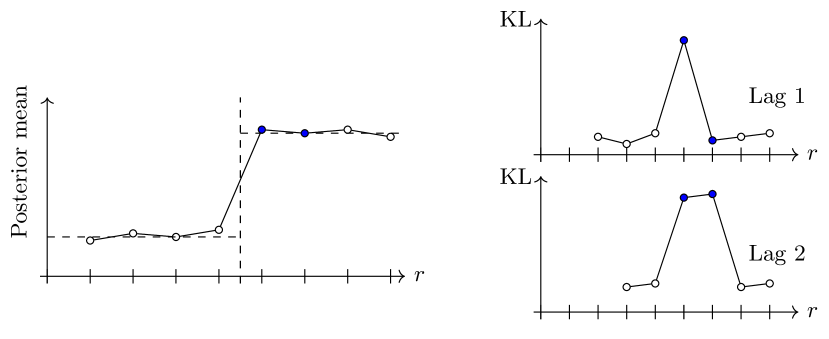

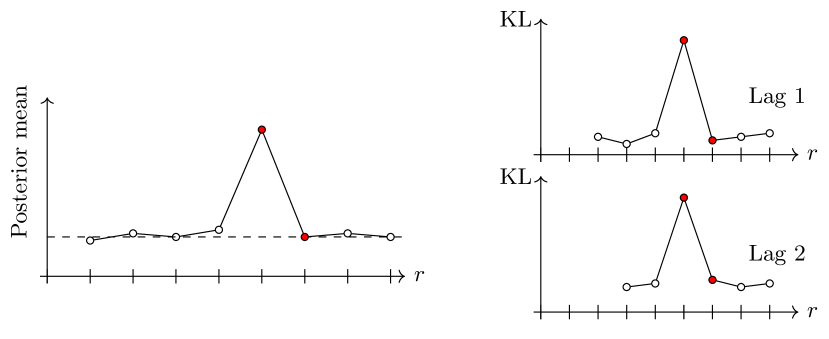

To detect changes in the point process rates, we compute the KL-divergence between the approximate posteriors and , for , where is a lag parameter. We compare the current approximation with estimates beyond that of the previous update, up to a maximal lag of , to avoid incorrectly flagging outliers as changes. Figure 6(a) illustrates the behaviour of the KL-divergence for a lag of 1 and a lag of 2. In Figure 6(b), we see that using only a lag of 1 would result in the false identification of a change. There is a trade-off to be made between confidence and speed of detection. We found that a maximal lag of provided a good balance.

To compute the KL-divergence, we note that is gamma distributed for all . For two random variables and with probability distributions and respectively, their KL-divergence is:

| (3.12) |

Two burn-in times are required to make use of the KL-divergence. In particular, iterations are needed for the algorithm to converge from initialisation, and further steps needed to obtain enough samples to flag changes. During the initial steps, stationarity is assumed. After steps, we propose to use the median absolute deviation (MAD) to evaluate the presence of a changepoint, as it is robust to outliers (Leys et al., 2013). In general, for a dataset , the MAD is defined as

| (3.13) |

where denotes the median of the elements in a set. An observation is classified as an outlier if , for a choice of threshold .

In our proposed methodology, the elements in the set are the realised values of the KL-divergence between different gamma distributions, approximating the posterior distributions for the parameters at different time windows. In particular, we write and construct . A changepoint is flagged at if for all , we have:

| (3.14) |

It must be remarked that if we choose a maximal lag of , we can only flag a changepoint a minimum of time steps after the changepoint has occurred.

We now consider whether the stream must be reset post change. Suppose a change to the latent rate occurs at some time , and that pre-change , whereas post-change, for and . Pre-change, our algorithm provides two consecutive CAVI estimates and , with shapes and rates and , respectively, and post-change, we have CAVI estimates and with shapes and rates and . For ease of analysis, we suppose that , and .

We consider the ratio of the KL-divergences between consecutive estimates pre and post-change, and expand as to get

| (3.15) |

Similarly, taking yields

| (3.16) |

Observation of (3.15) indicates that to first order the ratio depends upon only the relative size of the difference between their rates, that is , and not directly upon the magnitude of . This is not problematic only if the magnitude of changes linearly with . Also, (3.16) shows that the ratio depends directly on the magnitude of the scale . It follows that after the identification of a changepoint at , , the stream of realised KL-divergence values must be discarded, and the algorithm wait a further steps to obtain enough samples for the new set which is used to detect any subsequent changes. A further benefit of consider a maximal lag is that more KL-divergence samples are obtained for the same number of observations.

To detect changes in the group memberships, the approximation to the posterior of the latent group memberships in (3.10) provides a node-level vector ( of group membership probabilities. Computing provides a group assignment for node , and by comparing assignments between runs, one has a natural way of flagging changes. However, this approach is unsatisfactory as it does not account for the magnitude of the change in probability. The KL-divergence also cannot be used for flagging group changes, since is only defined only when for all values in the support of . Instead, we utilise the Jensen-Shannon divergence (JS; Lin, 1991), defined for two distributions as

| (3.17) |

where is a 50-50 mixture distribution of and . The JS-divergence is symmetric in its arguments, and avoids the undefined values encountered with the KL-divergence. For , where denotes the -dimensional simplex, the JS-divergence between discrete random variables and , with probability mass functions and respectively, takes the following form:

| (3.18) |

The MAD is then used to detect changes to the stream of logged values, but with two additional requirements on the group probabilities:

| (3.19) | ||||

| (3.20) |

If the MAD condition and both (3.19) and (3.20) are met, then a changepoint is flagged. The conditions (3.19) and (3.20) ensure that changes are flagged only if the most likely group assignment changes after a window of steps where the most likely group assignment was stable. It should noted that for this stream, as the probabilities are constrained to sum to 1, we do not reset these values after a changepoint is detected.

3.5 Online VB for the dynamic BHPP with an unknown underlying graph

Until now, it has been assumed that the graph is fully connected. We relax this assumption and extend the framework to the setting where is unknown. Assuming when there is no edge adversely affects estimation of the latent rates; instead of the absence of an event indicating the absence of an edge, it instead just leads to a lower rate estimate. This motivates a method that can take into account the possibility that . The work here builds upon the sparse setup of Matias et al. (2018).

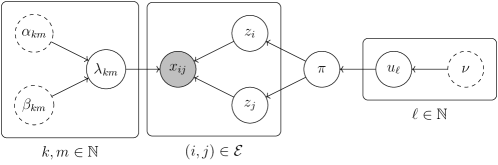

For each , an additional latent variable is introduced. A new latent group membership is assigned to each , and is Bernoulli-distributed conditional upon and , according to a stochastic blockmodel (SBM; Holland et al., 1983). Each captures the probability that is also an element of , and functions to reduce the contribution of edges with no arrivals to the estimates of the underlying rates. The new model is then expressed as:

| (3.21) | |||||

| (3.22) | |||||

| (3.23) | |||||

| (3.24) | |||||

| (3.25) | |||||

| (3.26) | |||||

| (3.27) | |||||

| (3.28) | |||||

We allow the most general setting in which the group structure that governs the rates is separate from that which determines edge connection probabilities. We assume that the graph is static, and so changes to the memberships that drive the edge-processes should not affect the determination of the graph adjacency matrix. The decoupling of the edge-process and edge-connection group memberships ensure this. Furthermore, as has been noted, SBMs provide good approximations to any exchangeable random graph model (Airoldi et al., 2013), and they therefore offer a logical model for the graph generation mechanism. This new model structure is represented in graphical model form in Figure 7.

Given the graph is considered to be static, if for some , then (corresponding to ) with probability one. Otherwise, if then we either have no edge (corresponding to ), or a non-null intensity process with no events in . The difference with the Section 2.1 is that we now have the additional local latent variables, , and , all of which grow with (linearly for and , and quadratically for ).

To implement variational inference, the full conditional distribution must be written down exactly, as per (3.4). Using the fact that inter-arrival times from a Poisson process are exponentially distributed, Matias et al. (2018) shows that the conditional posterior probability of an edge in the case of static takes the form

| (3.29) |

Since is static, the posterior for each should be computed using the full data . Note that the conditional distribution in (3.29) depends on only via the counting process at time .

For the model in (3.21)-(3.28), the true posterior distribution after batches factorises as

| (3.30) |

similarly to the posterior distribution in (3.5). Therefore, inference on this model can be performed in much the same way as inference on the original model. However, as the true conditional posterior for is tractable, the update procedure is slightly different. Unlike Matias et al. (2018), we cannot simply take to be Bernoulli distributed with probability as in (3.29) as is, in general, not static. Instead, to account for variations in over the full observation window, we propose an approximation to the posterior distribution of at , conditional upon , of the form , where

| (3.31) |

Here, and denote the mean of our approximate posterior distribution for and , respectively, at update . At update , we propose a variational approximation of the form , where is as in (3.31) and . A two-step estimation procedure follows naturally, wherein is approximated using CAVI as was done previously, and then is updated using (3.31) and the CAVI approximations to the posteriors of and . Note that since for , for , for and are considered static parameters, forgetting factors for these quantities are not required.

Consider the BHPP model with unknown graph structure, as in (3.21)-(3.28), with global parameters and local parameters , and . At step , we approximate the posterior density by , which is the product of the optimal CAVI solution and the fixed-form approximation of (3.31). For the BHPP model with known graph structure, all latent variables could change, and thus in (3.7) all components were tempered before being passed as the prior for step . However, in the case of an unknown graph structure, as the graph is assumed to be static, only the components of the dynamic latent variables are tempered when constructing the prior for step . We pass through as the prior for step the partially tempered density

| (3.32) | ||||

| (3.33) |

We assume that each component of (3.33) takes the same form as its corresponding complete conditional distribution under the BHPP model with unknown graph structure of (3.21)-(3.28). Additionally, the distributions for , and are raised to a power and normalised. In summary:

Suppose that data is again observed on the interval , for . Under the prior structure in (3.33), the CAVI sequential updates take the form:

-

1.

where for all we define and as

(3.34) (3.35) -

2.

where for all , we define and as

(3.36) -

3.

for all where , with , satisfies the relation:

(3.37) (3.38) -

4.

for all where , with , satisfies the relation:

(3.39) (3.40) -

5.

where for all , we define as:

(3.41) -

6.

where for all , we define as:

(3.42) -

7.

, where is defined in (3.31).

3.6 Online VB for the dynamic BHPP with an unknown number of groups

In real-world applications, the number of groups is usually unknown, and it must be estimated from the observed data. To address this issue, we adopt a Bayesian non-parametric approach, proposing a Dirichlet process prior (Ferguson, 1973) on the group memberships. In particular, we replace the Dirichlet prior distributions in (2.5) and (3.27) with a Griffiths-Engen-McCloskey (GEM; Pitman, 2002) prior distribution, with parameter , written . This prior distribution corresponds to an infinite limit of a Dirichlet distribution: , where is the vector of ones of length . The full model becomes:

| (3.43) | |||||

| (3.44) | |||||

| (3.45) | |||||

| (3.46) | |||||

where represents an infinite sequence such that for all and . The GEM prior distribution also corresponds to the distribution of proportions obtained under a stick-breaking representation (Sethuraman, 1994) of a Dirichlet process. Therefore, the proportions can be reparametrised as a product of variables drawn from independent beta distributions, as follows:

| (3.47) |

This decomposition is particularly useful to derive an online variational inference algorithm for the BHPP model with GEM priors (GEM-BHPP), following Blei and Jordan (2006). In particular, within a mean-field approximation for the posterior distribution , a variational approximation is posited directly on , rather than . This approximation is truncated at a level , implying that for , effectively resulting in an -dimensional probability vector from (3.47). It should be pointed out how this approach differs from the model set-up we considered earlier. In the GEM-BHPP, we make no truncation in the model set-up, but rather only in the variational approximation to it. This is in contrast to the method we presented in Sections 2.1, wherein one would be using a finite-dimensional Dirichlet distribution directly in the prior structure.

We introduce the notation , , and , for . If we define , for all and and , for all , the first iteration takes the form of the model specified in (3.43)–(3.46). Using this notation, we can formulate our inference procedure based on the same process of sequential CAVI updates.

Consider the GEM-BHPP model in (3.46)–(3.43) with a stick-breaking reparametrisation of as in 3.47, global parameters and local parameters . The posterior distribution is approximated by the optimal CAVI solution . Similarly to (3.7), this CAVI approximation is tempered to form , taking the following product form:

| (3.48) |

This tempered density is then passed through as the prior for step . We assume that each component of (3.48) takes the same form of its corresponding complete conditional distribution under the GEM-BHPP model in (3.43)–(3.46), raised to a power and normalised:

| (3.49) | |||||

| (3.50) | |||||

| (3.51) |

where and are normalising constants, ensuring that the densities are valid, and are temperature parameters specific to each class of latent variables. Suppose that data is observed on the interval , for , and denote the count on edge during this interval by . Under the prior structure in (3.48), the CAVI sequential updates then take the form

-

1.

for all where are defined as:

(3.52) (3.53) -

2.

for all where , with , satisfies the relation:

(3.54) (3.55) -

3.

for all where and are defined as:

(3.56)

A subtle problem arises with the updates in (3.53). In the case that the truncation parameter, , is larger than the true number of groups, the update procedure will allocate some groups zero nodes. If is one such group, then for all for every after the algorithm has converged, up until a change occurs. For , it follows from the rate update in (3.53) that for all , and thus that the posterior mean of and diverges. This divergence causes problems in (3.55) where this mean appears. To circumvent this problem, we must replace with the set . That is, we introduce a specific forgetting factor for each group-to-group rate. For each, , we initially set , but monitor the sum with increasing . Then, for all such that , we set , where is some threshold. This intervention prevents the exponential decay of to 0 as . Once the threshold is exceeded, the relevant BFFs are returned to . Experimentation found that is a good choice for .

4 Simulation studies

We evaluate the online changepoint detection algorithm of Section 3 using simulated data. Four simulation studies are conducted. Unless otherwise stated, we consider a network with nodes and latent groups, initialised with . For convenience, we define the intra-inter-group rate matrix

| (4.1) |

The update interval is set to time units throughout, and every experiment is repeated 50 times, with the results averaged. We cycle 3 times over the CAVI and fixed point equations. All hyperparameters are initialised as 1, except for and , which are initialised uniformly on and , respectively. For all , is initialised as , and as , when is known, and as when we infer the number of groups at a truncation level of . Unless otherwise stated, is set to be 2 and and to 10. In Section 4.1, we examine membership and rate recovery in the case that and are known when a varying proportion of nodes swap between the two groups. In Section 4.2, membership recovery is investigated when is known, but changes throughout the observation window. In Section 4.3, we consider two the effect of a decreasing lag between two instantaneous changes to when both and are known. Finally, in Section 4.4, the effect of increasing sparsity in case of known but unknown is examined.

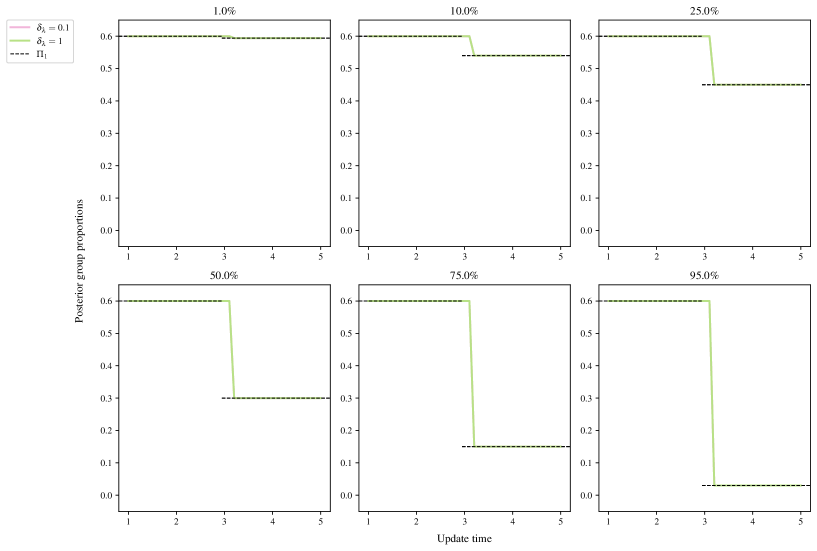

4.1 Latent group membership recovery

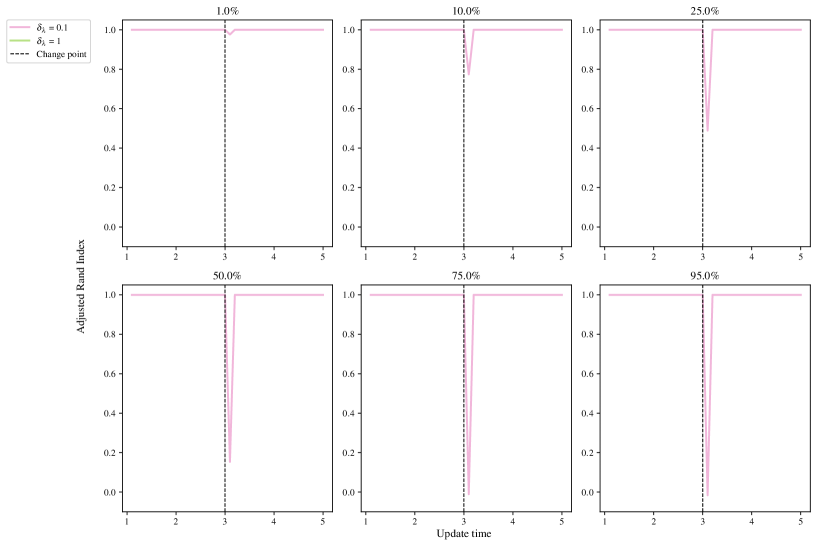

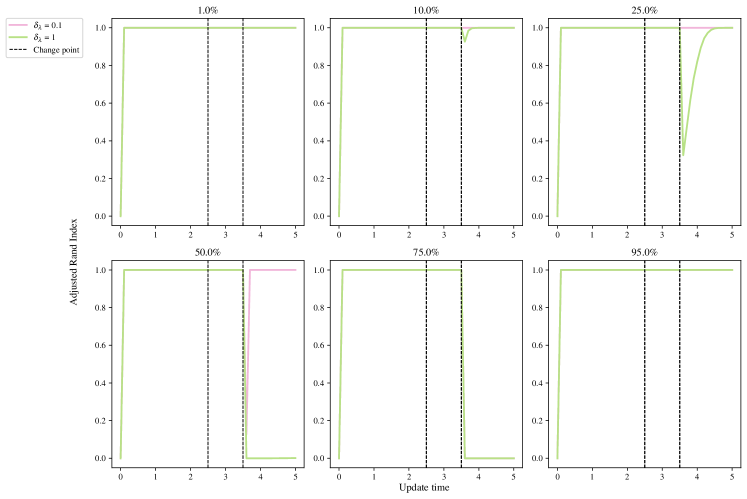

The first experiment takes a fully-connected network with rate matrix as given in (4.1). At time , of nodes from group 1 swap to group 2, with . To evaluate latent membership recovery, the inferred group memberships at time are compared to the true memberships using the adjusted rand index (ARI, Hubert and Arabie, 1985). The ARI takes values between and , with a value of indicating perfect agreement (up to label switching), random agreement, and complete disagreement. By computing the ARI at each update, rather than taking an average over , we can examine the smoothness of recovery, and the reaction of the algorithm to changepoints.

Figure 9(a) shows the inference procedure is stable across all values of , where the plots begin from steps. The ARI is steady before and after the change except for the step immediately after the change. Figure 9(b) shows that the algorithm quickly converges to the true proportions, both with and without a BFF.

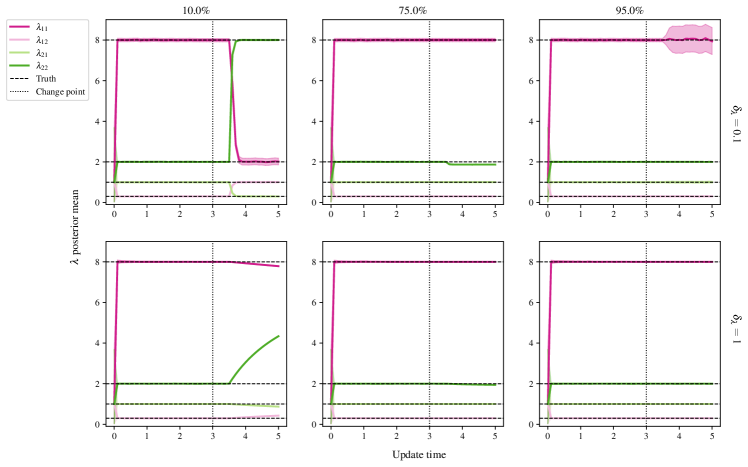

4.2 Number of groups recovery

We consider a fully connected network with two group membership changes: all nodes merging into group 1 at , followed by the creation of a new group at . Specifically, at , of the nodes in group 1 remain, while the remainder create group 2. We again consider , with as the rate matrix, and ARI as our performance metric. We set here, which corresponds to taking the argmax of each .

Figure 11 shows that the inference correctly groups the nodes in all cases pre-merger and between the merger and creation, both with and without a BFF. Using a BFF, the algorithm is seen to maintain a high ARI after the creation of a new group, in all cases except when . The application without the BFF also fails in this case, but additionally it fails for , and is slower to converge to the new groups when and 10.

For cases where 50% of nodes or less remain in group 1, the algorithm converges to the correct proportions, but with label-switching. This is observed in Figure 11, where the rates are seen to swap in the 10% panel for the case of a BFF.

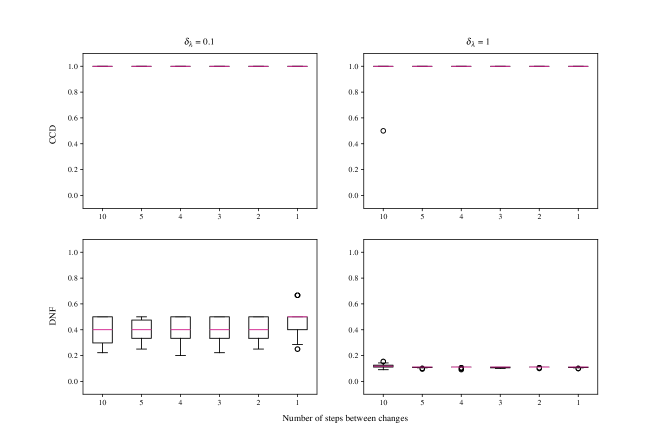

4.3 Detection of changes to the matrix of rates

On a fully connected network, we examine sequential changes to the rate matrix with decreasing time between the changes. The rate matrix maps as

with the first change at and the second at . For each run, took a value in . Here we do not reset the stream after a flagged change to the latent rates as we control their relative magnitude and wish to examine the performance of the algorithm with small latency between changes.

We evaluate the detection of latent changes using the proportion of changepoints correctly detected (CCD), and the proportion of detections that are not false (DNF), as in Bodenham and Adams (2017). Note that we aggregate across all group-to-group rates. Specifically, if there are changepoints, and we detect , of which are correct, analogous to recall and precision, the authors define:

-

1.

, the proportion of changepoints correctly detected,

-

2.

, the proportion of detections that are not false.

As noted by Bodenham and Adams (2017), CCD and DNF are preferred to their more intuitive counterparts (proportion of missed changepoints and proportion of false detections, respectively) as for the CCD and DNF, values closer to 1 indicate better performance than those closer to 0. Furthermore, these metrics are preferable over average run length metrics ( and ) as we want to capture the number of changes detected and missed.

Suppose and are consecutive true changepoints for , and let the most recently flagged changepoint by the algorithm for be . If the next flag for occurs at , that is is missed, then is classified as a correct detection of . This is common practice in the literature. This approach is adopted by Bodenham and Adams (2017), whereas other authors implement a softmax rule for classification (see, for example, Alanqary et al., 2021; Yamanishi and Takeuchi, 2002; Bodenham and Adams, 2017), adjusting for when multiple changes are flagged in the same window.

In Figure 12, we see the CCD and DNF for each run. The CCD is consistently high for both a BFF and no BFF. This demonstrates that the algorithm consistently flags true changes with and without a BFF. The role of the BFF is shown in the DNF, where we see BFF yielding higher values. Without a BFF, multiple changes are flagged that did not occur.

4.4 Effect of network sparsity

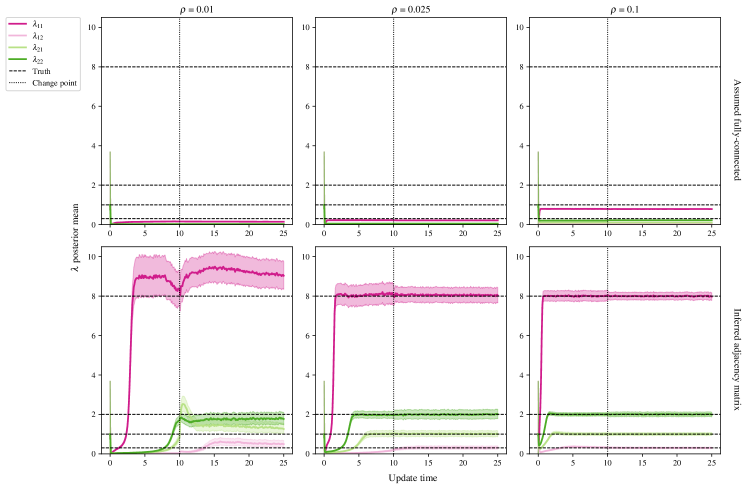

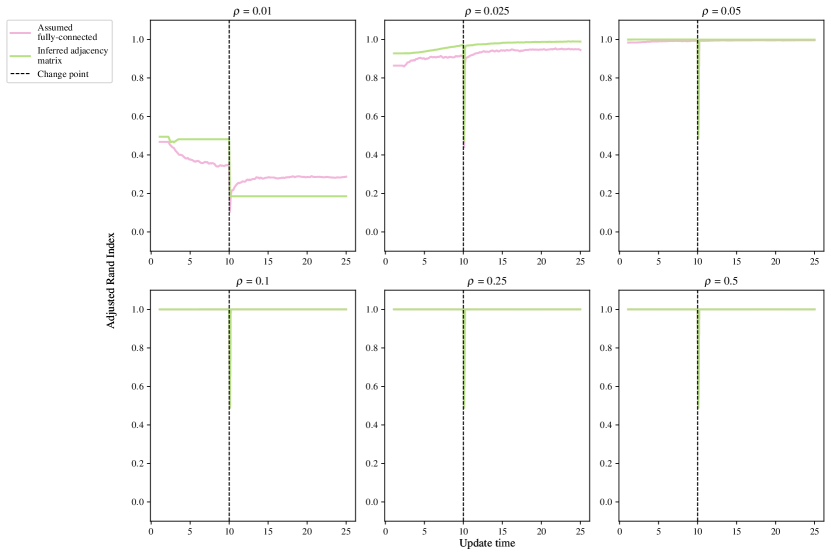

We examine the effect of decreasing network sparsity on changepoint detection. We simulate a network with latent connection groups, letting , the group connection probability, vary over . For the point process groups, we retain the same as before, and again, we set . We simulate on , with , and at , of nodes from group 1 swap to group 2. The inference procedure is run on the simulated network twice, once where the network is assumed fully-connected, and a second time when the adjacency matrix is inferred. Both procedures are run with .

Figure 14 demonstrates the effect of incorrectly assuming that the graph is fully connected: the rates are significantly underestimated. On the other hand, when is inferred, the posterior means are much closer to the true values, even in the case of density. Furthermore, in Figure 14 the mean ARI of the membership recovery is seen to be higher for the inferred adjacency matrix.

5 Application to the Santander Cycles bike-sharing network

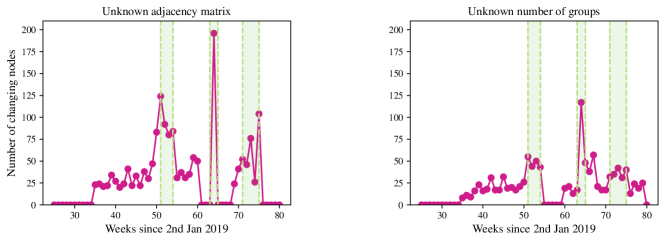

The proposed online changepoint algorithms were tested on Transport for London (TfL) data from the London Santander Cycles bike-sharing network, which is publicly available online (https://cycling.data.tfl.gov.uk/, powered by TfL Open Data). Each datum corresponds to a bike hire, and contains the start and end times of the journey, the IDs of the source and destination stations, the journey duration, a bike ID number, and an unique identifier for the journey. Considering the start and end stations as source and destination nodes, and the timestamp of the end of the journey as an arrival time to the directed edge from source to destination, the data forms a network point process. In this study, the data is aggregated into weekly counts to smooth the intensities of the point processes and weekly periodicities. We select a subset of the data from 2nd January 2019 until 15th July 2020 as this window contains significant COVID-19 related national events that can be used to check the performance of our algorithm. In this time period, unique nodes are observed within weekly time windows, with updates every week time steps.

The online VB algorithm for the dynamic BHPP is run for the separate cases of an unknown graph structure, and an unknown number of groups. The number of groups in the case of an unknown adjacency matrix was set to match the number inferred by the implementation for an unknown number of groups, which was . The adjacency matrix in the case of unknown was set to correspond to a fully connected graph: . We consider the task of detecting changes to the latent group structure of the bike sharing network. We run both algorithms with , , , and , so that changes can be detected only after weeks of observations. We initialise the hyperparameters as described in Section 4.

Figure 15 shows that the algorithms flag multiple changes at each update, but that there are three regions where the number of flagged changes peaks. From left to right, these green regions correspond to the Christmas and New Year period of 2019, the introduction of the first UK COVID-19 lockdown on 19/03/2020, and the subsequent phased easing of restrictions from 01/06/2020. The algorithm reacts to these events, which are likely to cause changes to the network.

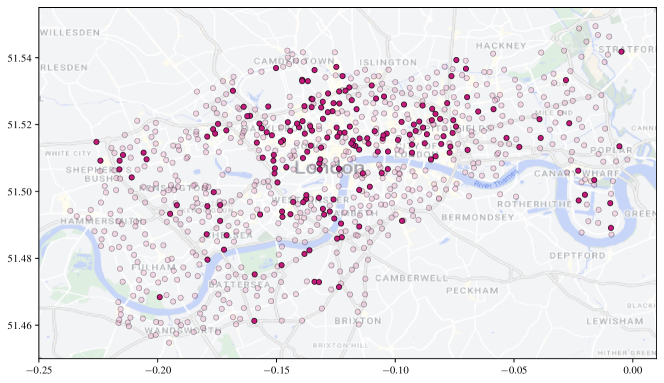

Figure 16 shows that the flagged changes corresponding to the onset of the lockdown are very concentrated around central London, which makes sense as “work from home” orders will have affected the use of these commuting bike stations. Additionally, stations around the Westfield Shopping Centre in Shepherd’s Bush and the Canary Wharf financial district are flagged, representing an expected change due to the government restrictions.

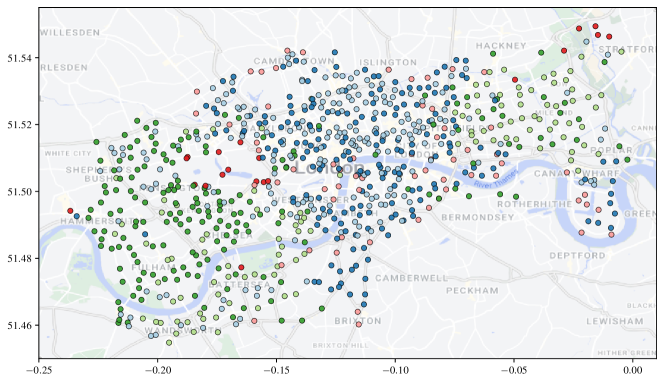

Furthermore, Figure 17 displays an example clustering from the dynamic BHPP model with unknown number of groups at update point 50. There is some spatial clustering to the nodes, but each cluster contains mainly nodes with similar activity patterns. For example, the dark and light blue clusters represent popular nodes in central London and the Canary Wharf financial district, which are mainly used by commuters into these areas. Similarly, the light and dark green clusters are nodes in West and East London (with the dark green cluster mostly covering West London, and the light green East London and the areas of Battersea and Wandsworth (south of the river Thames). The pink cluster is around the boundary between the blue and green regions. A notable exception is represented by the red cluster, representing the most popular stations within the network, mainly used for leisure around Hyde Park and the Queen Elizabeth Olympic Park in Stratford. In addition, the red cluster also contains two additional stations in Battersea Park and Ravenscourt Park (west of Hammersmith).

6 Conclusion and discussion

We have presented a novel online Bayesian inference framework for detecting changes to the latent structure of a block-homogeneous Poisson process in which data arrives as batches in an event stream. Our methodology is scalable, and leverages a Bayesian forgetting factor framework to flag changes to the latent community structure and edge-process rates. The framework is extended to the cases where the adjacency matrix or the number of latent groups are unknown a priori. When tested on both real and simulated data, our methodology is seen to detect latent structure accurately and with minimal latency.

There are numerous ways in which this work could be extended. In particular, the frameworks for an unknown graph structure and unknown number of latent groups can readily be integrated to handle the case where neither is known a priori. It would also be of interest to incorporate seasonality into the model, perhaps within an online framework with longer memory.

A further challenge would be to adapt the framework to allow for nodes to enter or leave the network during observation. Similarly, the adjacency matrix is assumed static in our methodology, and so an extension would allow for this to be dynamic, although this would likely cause identifiability issues in the case where there are also changes to the latent rates.

Acknowledgements

Joshua Corneck acknowledges funding from the Engineering and Physical Sciences Research Council (EPSRC), grant number EP/S023151/1. Ed Cohen acknowledges funding from the EPSRC NeST Programme, grant number EP/X002195/1. Francesco Sanna Passino acknowledges funding from the EPSRC, grant number EP/Y002113/1.

Code

Python code to implement the methodologies proposed in this article and reproduce the results is available in the Github repository joshcorneck/dynamicBHPP.

References

- Airoldi et al. (2013) Airoldi, E. M., Costa, T. B., and Chan, S. H. (2013) Stochastic blockmodel approximation of a graphon: Theory and consistent estimation. In Advances in Neural Information Processing Systems (eds. C. Burges, L. Bottou, M. Welling, Z. Ghahramani and K. Weinberger), vol. 26. Curran Associates, Inc.

- Alanqary et al. (2021) Alanqary, A., Alomar, A. O., and Shah, D. (2021) Change point detection via multivariate singular spectrum analysis. In Advances in Neural Information Processing Systems (eds. A. Beygelzimer, Y. Dauphin, P. Liang and J. W. Vaughan).

- Amini et al. (2013) Amini, A. A., Chen, A., Bickel, P. J., and Levina, E. (2013) Pseudo-likelihood methods for community detection in large sparse networks. The Annals of Statistics, 41, 2097–2122.

- Bifet et al. (2018) Bifet, A., Gavaldà, R., Holmes, G., and Pfahringer, B. (2018) Machine Learning for Data Streams: with Practical Examples in MOA. Adaptive Computation and Machine Learning series. MIT Press.

- Bishop (2006) Bishop, C. M. (2006) Pattern Recognition and Machine Learning (Information Science and Statistics). Berlin, Heidelberg: Springer-Verlag.

- Blei and Jordan (2006) Blei, D. M. and Jordan, M. I. (2006) Variational inference for Dirichlet process mixtures. Bayesian Analysis, 1, 121–143.

- Blei et al. (2017) Blei, D. M., Kucukelbir, A., and McAuliffe, J. D. (2017) Variational inference: A review for statisticians. Journal of the American Statistical Association, 112, 859–877.

- Bodenham and Adams (2017) Bodenham, D. A. and Adams, N. M. (2017) Continuous monitoring for changepoints in data streams using adaptive estimation. Statistics and Computing, 27, 1257–1270.

- Fang et al. (2024) Fang, G., Ward, O. G., and Zheng, T. (2024) Online estimation and community detection of network point processes for event streams. Statistics and Computing, 34.

- Ferguson (1973) Ferguson, T. S. (1973) A Bayesian analysis of some nonparametric problems. The Annals of Statistics, 1, 209–230.

- Gao et al. (2018) Gao, C., Ma, Z., Zhang, A. Y., and Zhou, H. H. (2018) Community detection in degree-corrected block models. The Annals of Statistics, 46, 2153–2185.

- Hallgren et al. (2023) Hallgren, K. L., Heard, N. A., and Turcotte, M. J. M. (2023) Changepoint detection on a graph of time series. Bayesian Analysis, 1–28.

- Haykin (2002) Haykin, S. (2002) Adaptive filter theory. Upper Saddle River, NJ: Prentice Hall, 4th edn.

- Heard et al. (2010) Heard, N. A., Weston, D. J., Platanioti, K., and Hand, D. J. (2010) Bayesian anomaly detection methods for social networks. The Annals of Applied Statistics, 4, 645–662.

- Holland et al. (1983) Holland, P. W., Laskey, K. B., and Leinhardt, S. (1983) Stochastic blockmodels: First steps. Social Networks, 5, 109–137.

- Holme (2015) Holme, P. (2015) Modern temporal network theory: a colloquium. The European Physical Journal B, 88, 234.

- Hubert and Arabie (1985) Hubert, L. J. and Arabie, P. (1985) Comparing partitions. Journal of Classification, 2, 193–218.

- Jasra et al. (2005) Jasra, A., Holmes, C. C., and Stephens, D. A. (2005) Markov Chain Monte Carlo methods and the label switching problem in Bayesian mixture modeling. Statistical Science, 20, 50–67.

- Karrer and Newman (2011) Karrer, B. and Newman, M. E. J. (2011) Stochastic blockmodels and community structure in networks. Physical Review E, 83, 016107.

- Klimt and Yang (2004) Klimt, B. and Yang, Y. (2004) The Enron corpus: A new dataset for email classification research. In Machine Learning: ECML 2004 (eds. J.-F. Boulicaut, F. Esposito, F. Giannotti and D. Pedreschi), 217–226. Berlin, Heidelberg: Springer Berlin Heidelberg.

- Lee and Wilkinson (2019) Lee, C. and Wilkinson, D. J. (2019) A review of stochastic block models and extensions for graph clustering. Applied Network Science, 4, 1–50.

- Leys et al. (2013) Leys, C., Ley, C., Klein, O., Bernard, P., and Licata, L. (2013) Detecting outliers: Do not use standard deviation around the mean, use absolute deviation around the median. Journal of Experimental Social Psychology, 49, 764–766.

- Lin (1991) Lin, J. (1991) Divergence measures based on the Shannon entropy. IEEE Transactions on Information Theory, 37, 145–151.

- Mariadassou et al. (2010) Mariadassou, M., Robin, S., and Vacher, C. (2010) Uncovering latent structure in valued graphs: A variational approach. The Annals of Applied Statistics, 4.

- Mariadassou and Tabouy (2020) Mariadassou, M. and Tabouy, T. (2020) Consistency and asymptotic normality of stochastic block models estimators from sampled data. The Electronic Journal of Statistics, 14, 3672–3704.

- Matias and Miele (2017) Matias, C. and Miele, V. (2017) Statistical clustering of temporal networks through a dynamic stochastic block model. Journal of the Royal Statistical Society. Series B (Statistical Methodology), 79, 1119–1141.

- Matias et al. (2018) Matias, C., Rebafka, T., and Villers, F. (2018) A semiparametric extension of the stochastic block model for longitudinal networks. Biometrika, 105, 665–680.

- Paranjape et al. (2017) Paranjape, A., Benson, A. R., and Leskovec, J. (2017) Motifs in temporal networks. In Proceedings of the Tenth ACM International Conference on Web Search and Data Mining, WSDM ’17, 601–610. New York, NY, USA: Association for Computing Machinery.

- Perry and Wolfe (2013) Perry, P. O. and Wolfe, P. J. (2013) Point process modelling for directed interaction networks. Journal of the Royal Statistical Society Series B: Statistical Methodology, 75, 821–849.

- Pitman (2002) Pitman, J. (2002) Combinatorial stochastic processes (Technical Report 621). Department of Statistics. University of California at Berkeley, Berkeley, CA.

- Ray and Szabó (2022) Ray, K. and Szabó, B. (2022) Variational Bayes for high-dimensional linear regression with sparse priors. Journal of the American Statistical Association, 117, 1270–1281.

- Sanna Passino and Heard (2023) Sanna Passino, F. and Heard, N. A. (2023) Mutually exciting point process graphs for modeling dynamic networks. Journal of Computational and Graphical Statistics, 32, 116–130.

- Sethuraman (1994) Sethuraman, J. (1994) A constructive definition of Dirichlet priors. Statistica Sinica, 639–650.

- Shlomovich et al. (2022) Shlomovich, L., Cohen, E. A. K., and Adams, N. (2022) A parameter estimation method for multivariate binned Hawkes processes. Statistics and Computing, 32, 98.

- van Dyk and Park (2008) van Dyk, D. A. and Park, T. (2008) Partially collapsed Gibbs samplers. Journal of the American Statistical Association, 103, 790–796.

- Wang and Blei (2019) Wang, Y. and Blei, D. M. (2019) Frequentist consistency of variational Bayes. Journal of the American Statistical Association, 114, 1147–1161.

- Xu and Hero (2014) Xu, K. and Hero, A. (2014) Dynamic stochastic blockmodels for time-evolving social networks. IEEE Journal of Selected Topics in Signal Processing, 8, 552–562.

- Yamanishi and Takeuchi (2002) Yamanishi, K. and Takeuchi, J. (2002) A unifying framework for detecting outliers and change points from non-stationary time series data. In Proceedings of the Eighth ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, KDD ’02, 676–681. New York, NY, USA: Association for Computing Machinery.

- Yang et al. (2011) Yang, T., Chi, Y., Zhu, S., Gong, Y., and Jin, R. (2011) Detecting communities and their evolutions in dynamic social networks - a Bayesian approach. Machine Learning, 82, 157–189.

- Zhang and Zhou (2020) Zhang, A. Y. and Zhou, H. H. (2020) Theoretical and computational guarantees of mean field variational inference for community detection. The Annals of Statistics, 48, 2575–2598.

Appendix A Derivation of CAVI updates

Here we derive the CAVI approximating distributions for each parameter at the th update. In deriving these expressions, we assume no ordering for the parameter updates, and will use a superscript of for all parameters but for the one whose expression is then being derived.

A.1 Approximation of

Ignoring any terms that do not contain , we can derive the expectation as follows:

| (A.1) | ||||

| (A.2) | ||||

| (A.3) | ||||

| (A.4) | ||||

| (A.5) | ||||

| (A.6) | ||||

| (A.7) |

Taking the exponential, it follows that the optimal choice of under a CAVI approximation is , where

| (A.8) | ||||

| (A.9) | ||||

| (A.10) |

for and .

A.2 Approximation of

Ignoring any terms that do not contain , we compute the expectation as:

| (A.11) | ||||

| (A.12) |

Using the distributions derived for , we see that the optional CAVI approximation is to take , where

| (A.13) |

for .

A.3 Approximation of

Ignoring any terms that do not contain , we derive the expectation as follows:

| (A.14) | ||||

| (A.15) | ||||

| (A.16) | ||||

| (A.17) | ||||

| (A.18) |

Using the distributions derived for , it follows that the optimal CAVI approximation is to take , where

| (A.19) | ||||

| (A.20) |

for .

Appendix B Derivation of CAVI updates for an unknown adjacency matrix

Here we derive the CAVI approximating distributions for each parameter at the th update. In deriving these expressions, we assume no ordering for the parameter updates, and will use a superscript of for all parameters but for the one whose expression is then being derived.

B.1 Approximation of

Ignoring any terms that do not contain , we derive the expectation as:

| (B.1) | ||||

| (B.2) | ||||

| (B.3) | ||||

| (B.4) | ||||

| (B.5) | ||||

| (B.6) | ||||

| (B.7) | ||||

| (B.8) | ||||

| (B.9) |

Taking the exponential, and using the distributions derived for and the assumed form for , it follows that the optimal CAVI approximation is to take , where

| (B.10) | ||||

| (B.11) | ||||

| (B.12) | ||||

| (B.13) |

for and .

B.2 Approximation of

Ignoring any terms that do not contain , we can derive the expectation as follows:

| (B.14) | ||||

| (B.15) | ||||

| (B.16) | ||||

| (B.17) | ||||

| (B.18) |

Using the distributions derived for and assumed form for , we see that the optimal CAVI approximating distribution is with

| (B.19) | ||||

| (B.20) |

for .

B.3 Approximation of

Ignoring any terms that do not contain , we derive the expectation as:

| (B.21) | ||||

| (B.22) | ||||

| (B.23) | ||||

| (B.24) | ||||

| (B.25) |

Taking the exponential and computing expectations with respect to the derived distributions for and the assumed form for , it follows that the optimal CAVI approximation takes , with

| (B.26) | ||||

| (B.27) |

for .

B.4 Approximation of

Ignoring any terms that do not contain , we derive the expectation as:

| (B.28) | ||||

| (B.29) | ||||

| (B.30) |

Using the derived forms for , we see that the optimal CAVI choice is , where

for .

B.5 Approximation of

Ignoring any terms that do not contain , we compute the necessary expectation as:

| (B.31) | ||||

| (B.32) | ||||

| (B.33) |

Taking the exponential, and using the derived form for , we see that the optimal CAVI distribution is , where

| (B.34) |

for .

B.6 Approximation of

Ignoring terms that do not contain , we derive the expectation as:

| (B.35) | |||

| (B.36) | |||

| (B.37) | |||

| (B.38) | |||

| (B.39) | |||

| (B.40) | |||

| (B.41) | |||

| (B.42) |

Taking the exponential, and using the distributions derived for and the assumed form of , it follows that the optimal CAVI choice of is , where

| (B.43) | |||

| (B.44) | |||

| (B.45) | |||

| (B.46) | |||

| (B.47) |

for and .

Appendix C Derivation of CAVI updates for the Dirichlet process prior

Under our model specification, the term for can be rewritten using indicators as

| (C.1) |

The joint loglikelihood then becomes

| (C.2) | ||||

| (C.3) | ||||

| (C.4) |

C.1 Approximation of

Recalling that , it follows that . We can thus compute the necessary expectation as:

| (C.5) | ||||

| (C.6) | ||||

| (C.7) | ||||

| (C.8) | ||||

| (C.9) | ||||

| (C.10) |

Using the distributions derived for and , it follows that the optimal CAVI distribution is , with

| (C.11) | ||||

| (C.12) | ||||

| (C.13) | ||||

| (C.14) |

for and .

C.2 Approximation of

Recall that , and so . This truncation removes the need for an infinite sum. In this way, we can compute the expectation for the CAVI approximation as:

| (C.15) | ||||

| (C.16) | ||||

| (C.17) | ||||

| (C.18) |

Using the derived distributions for , it follows that the optimal CAVI approximation is , where

| (C.19) | ||||

| (C.20) |

for .

C.3 Approximation of

Again, using that , we have and , for , the required expectation becomes:

| (C.21) | ||||

| (C.22) | ||||

| (C.23) | ||||

| (C.24) |

where we have used the derived forms for to compute the indicator expectations. It follows that the optimal CAVI approximation is , where

| (C.25) | ||||

| (C.26) |

for .