Investigation of finite-sample properties of robust location and scale estimators

Abstract

When the experimental data set is contaminated, we usually employ robust alternatives to common location and scale estimators such as the sample median and Hodges-Lehmann estimators for location and the sample median absolute deviation and Shamos estimators for scale. It is well known that these estimators have high positive asymptotic breakdown points and are Fisher-consistent as the sample size tends to infinity. To the best of our knowledge, the finite-sample properties of these estimators, depending on the sample size, have not well been studied in the literature.

In this paper, we fill this gap by providing their closed-form finite-sample breakdown points and calculating the unbiasing factors and relative efficiencies of the robust estimators through the extensive Monte Carlo simulations up to the sample size 100. The numerical study shows that the unbiasing factor improves the finite-sample performance significantly. In addition, we provide the predicted values for the unbiasing factors obtained by using the least squares method which can be used for the case of sample size more than 100.

KEYWORDS: breakdown, unbiasedness, robustness, relative efficiency

1 Introduction

Estimation of the location and scale parameters of a distribution, such as the mean and standard deviation of a normal population, is a common and important problem in the various branches of science and engineering including: biomedical, chemical, materials, mechanical and industrial engineering, etc. The quality of the data plays an important role in estimating these parameters. In practice, the experimental data are often contaminated due to the measurement errors, the volatile operating conditions, etc. Thus, robust estimations are advocated as alternatives to commonly used location and scale estimators (e.g., the sample mean and sample standard deviation) for estimating these parameters. For example, for the case where some of the observations are contaminated by outliers, we usually adopt the sample median and Hodges-Lehmann (Hodges and Lehmann,, 1963) estimators for location and the sample median absolute deviation (Hampel,, 1974) and Shamos (Shamos,, 1976) estimators for scale, because these estimators have a large breakdown point and perform well in either the presence or absence of outliers.

The breakdown point is a common criterion for measuring the robustness of an estimator. The larger the breakdown point of an estimator, the more robust it is. The finite-sample breakdown point based on the idea of Hodges, Jr., (1967) is defined as the maximum proportion of incorrect or arbitrarily observations that an estimator can deal with without making an egregiously incorrect value. The breakdown point of an estimator is a measure of its resistance to data contamination (Wilcox,, 2016). For example, the breakdown points of the sample mean and the sample median are 0 and , respectively. Given that the breakdown point can generally be written as a function of the sample size, we provide the finite-sample breakdown points for the various location and scale estimators mentioned above. It is shown that when the sample sizes are small, they are noticeably different from the asymptotic breakdown point, which is the limit of the finite-sample breakdown point when the sample size tends to infinity.

It deserves mentioning that for a robust scale estimation, the sample median absolute deviation (MAD) and Shamos estimators not only have positive asymptotic breakdown points, but also are Fisher-consistent (Fisher,, 1922) as the sample size goes to infinity. However, when the sample size is small, they have serious biases and thus provide inappropriate estimation. Some bias-correction techniques are commonly adopted to improve the finite-sample performance of these estimators. For instance, Williams, (2011) studied the finite-sample correction factors through computer simulations for several simple robust estimators of the standard deviation of a normal population, which include the MAD, interquartile range, shortest half interval, and median moving range. Later on, under the normal distribution, Hayes, (2014) obtained the finite-sample bias-correction factors of the MAD for scale. They have shown that finite-sample bias-correction factors can significantly eliminate systematic biases of these robust estimators, especially when the sample size is small.

To the best of our knowledge, finite-sample properties of the MAD and Shamos estimators have received little attention in the literature except for some references covering topics for small sample sizes. This observation motivates us to employ the extensive Monte Carlo simulations to obtain the empirical biases of these estimators. Given that the empirical variance of an estimator is one of the important metrics for evaluating an estimator, we also obtain the values of the finite-sample variances of the median, Hodges-Lehmann (HL), MAD and Shamos estimators under the standard normal distribution, which are not fully provided in the statistics literature. Numerical results show that the unbiasing factor improves the finite-sample performance of the estimator significantly. In addition, we provide the predicted values for the unbiasing factors obtained by the least squares method which can be used for the case of the sample size more than 100.

The rest of this paper is organized as follows. In Section 2, we derive the finite-sample breakdown points for robust location estimators and robust scale estimators, respectively. Through the extensive Monte Carlo simulations, we calculate the empirical biases of the MAD and Shamos estimators in Section 3 and the finite-sample variances of the median, HL, MAD, and Shamos estimators in Section 4. An example is provided to illustrate the application of the proposed methods to statistical quality control charts for averages and standard deviations in Section 5. Some concluding remarks are given in Section 6.

2 Finite-sample breakdown point

In this section, we introduce the definitions of the bias and breakdown of an estimator using Definition 1.6.1 of Hettmansperger and McKean, (2010) and Section 2 of Hampel et al., (1986), which is based on the idea of Hodges, Jr., (1967). According to these definitions, we derive the explicit finite-sample breakdown points of the robust estimators for location and scale parameters.

Definition 1 (Bias).

Let be a realization of a sample . We denote the corrupted sample of any of the observations as

The bias of an estimator is defined as

where the is taken over all possible corrected observations with being fixed at their original observations in the realization of .

If makes an arbitrarily large value (say, ), we say that the estimator has broken down.

Definition 2 (Breakdown).

We define the finite-sample breakdown as

| (1) |

This approach to breakdown is called -replacement breakdown because observations are replaced by corrupted values. For more details, readers are referred to (Donoho and Huber,, 1983), Subsection 2.2a of Hampel et al., (1986), and Subsection 1.6.1 of Hettmansperger and McKean, (2010). The sample median and HL estimators for robust location estimation are considered in Subsection 2.1 and the MAD and Shamos estimators for robust scale estimation are in Subsection 2.2.

2.1 Robust location estimators

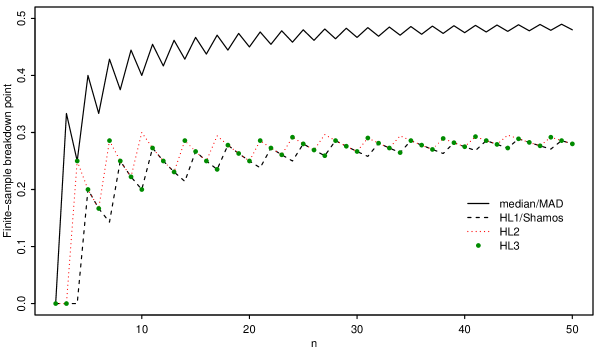

It is well known that the asymptotic breakdown point of the sample median is 1/2; see, for example, Example 2 in Section 2.2 of Hampel et al., (1986). For the HL estimator, the asymptotic breakdown point is given by ; see Example 8 of Section 2.3 of Hampel et al., (1986) for more details. Note that the sample median and HL estimators are in closed-forms and are location-equivariant in the sense that

However, in many cases, the finite-sample breakdown points can be noticeably different from the asymptotic breakdown point, especially when the sample size is small. For instance, when , we observe from Equation (2) that the finite-sample breakdown point for the median is 0.4, which is different from its asymptotic breakdown point of 0.5. This motivates the need for further investigating the finite-sample properties of these robust estimators.

Suppose that we have a sample, . If the sample size is given by an odd number (say, ), the median can be resistant to corrupted observations. Thus, the finite-sample breakdown point of the median with is given by . Next, if the sample size is given by an even number (say, ), then the median can be resistant to corrupted observations which gives . Let be the floor function. That is, is the largest integer not exceeding . Then we have for and for so that the finite-sample breakdown point can be written by the single formula for both odd and even cases. The finite-sample breakdown point of the median is thus given by

| (2) |

It should be noted that Equation (1.6.1) of Hettmansperger and McKean, (2010) defines the finite-sample breakdown point to be According to this definition, the finite-sample breakdown point of the median is given by which is always greater than for any odd value of . For example, with . Also, for the sample mean, is always , not zero. For example, with although its asymptotic breakdown point is zero. On the other hand, based on the finite-sample breakdown point in Equation (1), we have with for the median and always for the sample mean. It deserves mentioning that there are several variants of the breakdown point. We refer the interested readers to Remark 1 in Section 2.2 of Hampel et al., (1986) and Chapter 11 of Huber and Ronchetti, (2009) for more details. In this paper, we follow Equation (1) in Definition 2 to define the finite-sample breakdown.

Using the fact that can be rewritten as where , we have

Thus, the asymptotic breakdown point of the median is obtained by taking the limit of the finite-sample breakdown point as , which provides that .

The HL estimator (Hodges and Lehmann,, 1963) is defined as the median of all pairwise averages of the sample observations and is given by

Note that the median of all pairwise averages can be calculated for the three cases: (i) , (ii) , and (iii) , where . We denoted these three versions as

respectively. Note that each of the paired averages where and is called a Walsh average (Walsh,, 1949). In what follows, we first derive the finite-sample breakdown point for the and then use a similar approach to derive the finite-sample breakdown points for and . It is noteworthy that all three versions are asymptotically equivalent as mentioned in Example 3.7 of Huber and Ronchetti, (2009) although they are practically different with a sample of finite size.

The basic idea of how to derive the finite-sample breakdown point for the HL estimators was proposed by Ouyang et al., (2019), but they did not provide explicit formulae. In this paper, we provide the method of how to derive the explicit formulae. Suppose that we make of the observations arbitrarily large, where . Notice that there are paired average terms in the HL3 estimator: , where . Because the HL3 estimator is the median of the values, the finite-sample breakdown point cannot be greater than due to Equation (2). If we make of the observations arbitrarily large, then the number of arbitrarily large paired averages becomes . These two facts provide the following relationship

which is equivalent to . The finite-sample breakdown point of the is then given by , where

| (3) |

To obtain an explicit formula for Equation (3), we let . Since , is decreasing for . The roots of are given by

Since is an integer and , we have , that is, Then we have the closed-form finite-sample breakdown point of the

| (4) |

The asymptotic breakdown point of is given by . Using where , we can rewrite Equation (4) as

where and . Thus, we have .

In the case of the estimator, there are Walsh averages. Since the estimator is the median of the Walsh averages, the finite-sample breakdown point cannot be greater than due to Equation (2) again. If we make observations arbitrarily large with , then there are arbitrarily large Walsh averages. Thus, the following inequality holds

which is equivalent to In a similar way as done for Equation (3), we let be the largest integer satisfying the above, where . For convenience, we let . Then is decreasing for due to and the roots of are given by . Thus, using the similar argument to that used for the case, we have Then we have the closed-form finite-sample breakdown point of the

| (5) |

It should be noted that we also have .

Similar to the case of the , we obtain that the closed-form finite-sample breakdown point of the estimator is given by

| (6) |

2.2 Robust scale estimators

For robust scale estimation, we consider the MAD (Hampel,, 1974) and the Shamos estimator (Shamos,, 1976). The MAD is given by

| (7) |

where and is needed to make this estimator Fisher-consistent (Fisher,, 1922) for the standard deviation under the normal distribution. For more details, see Example 4 in Section 2.3 of Hampel et al., (1986) and Rousseeuw and Croux, (1992, 1993). This resembles the median and its finite-sample breakdown point is the same as that of the median in (2). The Shamos estimator is given by

| (8) |

where is needed to make this estimator Fisher-consistent for the standard deviation under the normal distribution (Lèvy-Leduc et al.,, 2011).

Of particular note is that the Shamos estimator resembles the HL1 estimator by replacing the Walsh averages by pairwise differences. Thus, its finite-sample breakdown point is the same as that of the HL1 estimator in (5). In the case of the HL estimator, the median is calculated for , , and , but the median in the Shamos estimator is calculated only for because for . Note that the MAD and Shamos estimators are in a closed-form and are scale-equivariant in the sense that

As afore-mentioned, we also provide the values the finite-sample breakdown points of the Shamos estimator in Table 2 and the plot of these values in Figure 1.

3 Empirical biases

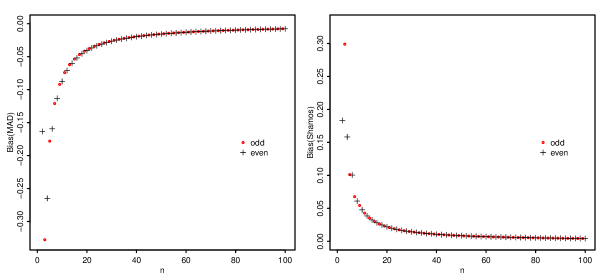

As mentioned above, the MAD in (7) and the Shamos estimator in (8) are Fisher-consistent for the standard deviation under the normal distribution, that is, as the sample size goes to infinity, it converges to the standard deviation under the normal distribution, . However, due to the cost of sampling and measurements in practical applications, we often need to find parameter estimates from data with small sample sizes; see, for example, Williams, (2011), whereas these estimates have serious biases, especially when the sample sizes are small. To the best of our knowledge, an empirical investigation of finite sample correction factors of these estimates has not been well studied in the literature. This observation motivates us to obtain the unbiasing factors for the MAD and Shamos estimators through the Monte Carlo simulation methods (Rousseeuw and Croux,, 1992). In what follows, we discuss how to conduct simulations under two cases: and .

For the case when , we generated a sample of size from the standard normal distribution, , and calculated the MAD and Shamos estimates. We repeated this simulation ten million times () to obtain the empirical biases of these two estimators. These values are provided in Table 3 and can also be seen in Figure 2. It is clear that an empirically unbiased MAD is given by

where is the empirical bias of the under the standard normal distribution. Similarly, an empirically unbiased Shamos estimator is given by

where is the empirical bias of the Shamos estimator under the standard normal distribution.

For the case when , we suggested to use the methods proposed by Hayes, (2014) and Williams, (2011). To be more specific, Hayes, (2014) suggested the use of and Williams, (2011) suggested the use of . Similarly, we can estimate using and . These suggestions are quite reasonable, because the MAD in (7) and Shamos in (8) are Fisher-consistent, and and converge to zero as goes to infinity.

Using the methods proposed by Hayes, (2014) and Williams, (2011), we obtained the least squares estimate as follows:

and

respectively. In a similar fashion, the least squares estimate using Hayes, (2014) and Williams, (2011) is given by

| and | ||||

respectively. The empirical biases of the MAD and Shamos estimators are provided in Table 4 for . We observed that the estimated biases are very accurate up to the fourth decimal point. Note that Hayes, (2014) and Williams, (2011) estimated for the case of odd and even values of separately. However, as one expects, for a large value of , the gain in precision may not be noticeable as shown in Figure 2.

It is well known that the sample standard deviation is not unbiased under the normal distribution. To make it unbiased, the unbiasing factor is widely used in engineering statistics including control charting so that is unbiased, where is given by

| (9) |

It is worth mentioning that this notation was originally used in ASTM E11, (1976) and it has since then been a standard notation in the engineering statistics literature.

We suggest to use and notations for the unbiasing factors of the MAD and Shamos estimators, respectively. Consequently, we can obtain the unbiased MAD and Shamos estimators for any value of given by

| (10) |

where and .

4 Empirical variances and relative efficiencies

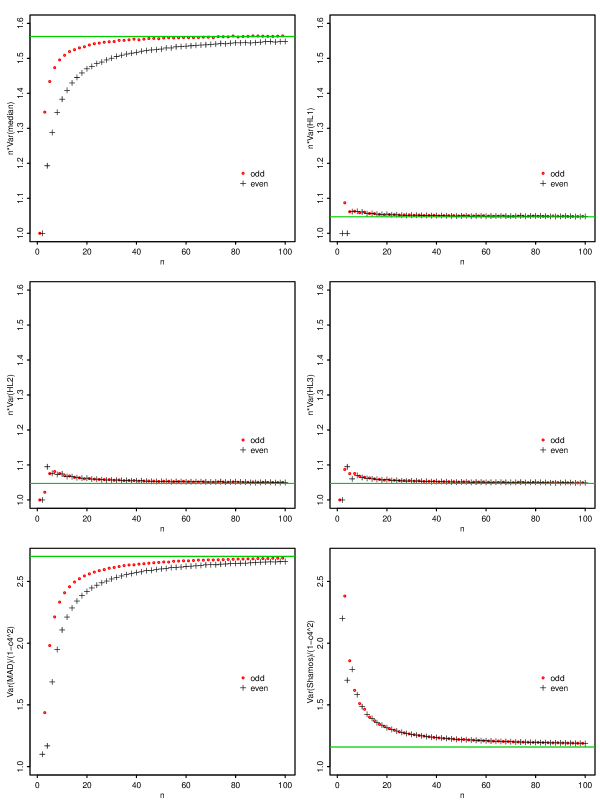

In this section, through the extensive Monte Carlo simulations, we calculate the finite-sample variances of the median, Hodges-Lehmann (HL1, HL2, HL3), MAD and Shamos estimators under the standard normal distribution. We generated a sample of size from the standard normal distribution and calculated their empirical variances for a given value of . We repeated this simulation ten million times () to obtain the empirical variance for each of .

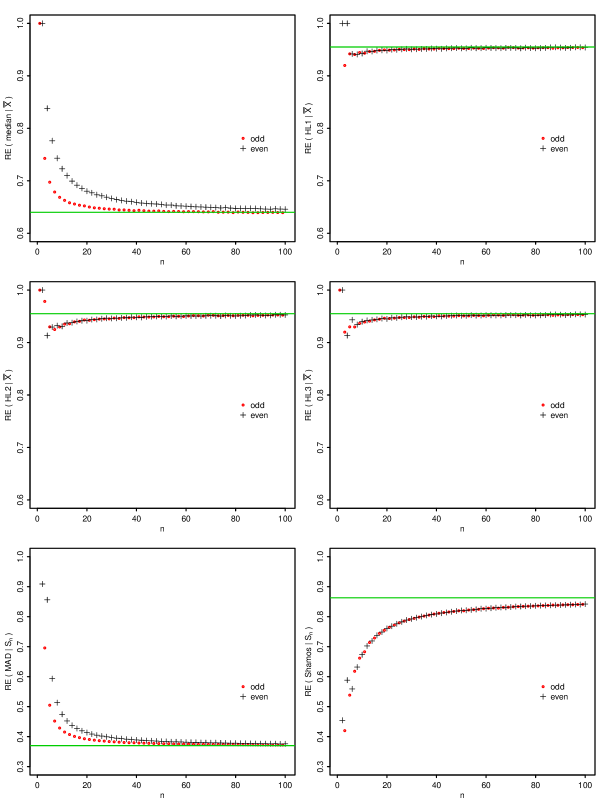

It should be noted that the values of the asymptotic relative efficiency (ARE) of various estimators are known. Here, the ARE is defined as the limit of the relative efficiency (RE) as goes to infinity. The RE of with respect to is defined as

where is often a reference or baseline estimator. Then the ARE is given by

For example, under the normal distribution, we have , , , and , where is the sample mean and is the sample standard deviation. For more details, see Serfling, (2011) and Lèvy-Leduc et al., (2011).

Note that with a random sample of size from the standard normal distribution, we have and , where is given in (9). Thus, we have

| and | ||||

for a large value of . We provided these values for each of in Tables 5 and 6 and also plotted these values in Figure 4.

For the case when , we suggest to estimate these values based on Hayes, (2014) or Williams, (2011) as we did the biases in the previous section. We suggest the following models to obtain these values for :

| and | ||||

One can also use the method based on Williams, (2011). For brevity, we used the method based on Hayes, (2014). To estimate these values for , we obtained the empirical REs in Table 7 for , , , , , , . We observe from Figure 4 that it is reasonable to estimate the values for the median and MAD in the case of odd and even values of separately. Using the large values of , we can estimate the above coefficients. For this reason, we use the simulation results in Tables 6 and 7. Then the least squares estimates based on the method of Hayes, (2014) are given by

| and | ||||

In Tables 8 and 9, we also calculated the REs of the afore-mentioned estimators for using the above empirical variances. For , we can easily obtain the REs using the above estimated variances. It should be noted that the REs of the median, HL2 and HL3 are exactly one for . When , the median, HL2 and HL3 are essentially the same as the sample mean.

Another noticeable result is that the RE of the HL1 is exactly one especially for . When , the HL1 is the median of , , , , and . Then this is the same as the median of , , , , and , where are order statistics. Because

| and | |||

we have

Thus, the RE of the HL1 should be exactly one. In this case, as expected, the finite-sample breakdown is zero as provided in Table 2.

It should be noted that the and are unbiased for under the normal distribution, but their square values are not unbiased for . Using the empirical and estimated variances, we can obtain the unbiased versions as follows. For convenience, we denote and , where the variances are obtained using a sample of size from the standard normal distribution as mentioned earlier. Since the MAD and Shamos estimators are scale-equivariant, we have and with a sample from the normal distribution . It is immediate from Equation (10) that and . Considering , we have

| and | ||||

Thus, the following estimators are unbiased for under the normal distribution

5 Example

In this section, we provide an example to illustrate the application of the proposed methods to statistical quality control charts (Shewhart,, 1926) for averages and standard deviations. For more details, see Section 3.8 of ASTM E11, (2018). Three-sigma control limits are most widely used to set the upper and lower control limits in statistical control charts due to Shewhart, (1931).

We briefly introduce how to construct the statistical control charts and then propose robust alternatives using the proposed methods. In general, the construction of statistical quality control charts is involved with two phases: Phase-I and Phase-II (Vining,, 2009; Montgomery,, 2013). In Phase-I, the goal is to establish reliable control limits with a clean set of process data. In Phase-II, using the control limits obtained in Phase-I, we monitor the process by comparing the statistic for each successive subgroup as future observations are collected. The Phase-II control charts are based on the estimates in Phase-I and the performance of the Phase-II control chart relies on the accuracy of the Phase-I estimate. Thus, if the Phase-I control limits are estimated with a corrupted data set, this can produce an adverse effect in Phase-II. It is well known that the sample mean and standard deviations are highly sensitive to data contamination and can even be destroyed by a single corrupted value (Rousseeuw,, 1991). Thus, the conventional control charts based on these statistics are very sensitive to contamination. This problem can be easily overcome by using the proposed robust methods.

As an illustration, we deal with the control limits of the conventional control charts for averages and standard deviations. Suppose that the mean and standard deviation are given by and with a sample of size . Then the parameters of the control limits of the chart are given by (UCL) and (LCL). We assume that we have subgroups which is of size . Let be the th sample, where and and be its realization. Let and be the sample mean and standard deviation of the th sample, respectively. Then the estimates of are given by , where , , and ; see ASQC and ANSI, (1972) for the notation . Note that an estimate of is given by since is an estimate of .

As obtained in (10), the unbiased MAD and Shamos estimators for any value of are given by

respectively. For convenience, we let and . Let and be the MAD and Shamos estimates of the th sample, respectively. Then robust analogues of can be obtained as

where and .

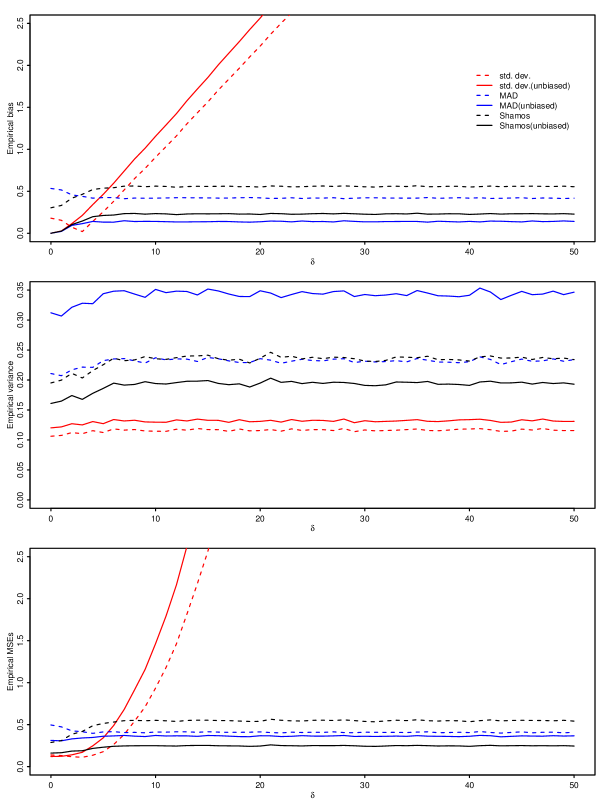

As mentioned above, the conventional limits are very sensitive to data contamination. For example, when there are outlying observations, the control limits are moved outward from the center line, which makes it difficult to monitor any out-of-control signal. Since the three-sigma plays an important role in constructing the charts, we investigate the estimates of . To this end, we carry out a simulation. We assume that are normally distributed with where and and there are subgroups which are all of size . We repeated this simulation ten thousand times.

To investigate the robust properties of the proposed methods, we corrupted the observation by adding to , where . We provide the empirical biases, variances and mean square errors of the estimates of in Table 1 and Figure 3. For brevity, we provide the results only for in the table. In the figure, the solid lines denote the unbiased estimates after the finite-sample correction. From the results, if there is no contamination (), the unbiased/original standard deviations clearly perform the best. The unbiased version is slightly better than the original standard deviation. Thus, the unbiasing factor, , improves the bias and MSE. However, if there exists data contamination, the unbiased/original standard deviations started to break down as the corruption level increases. We also observe the unbiasing factor, , does not improve either the bias or the MSE unless is very small.

On the other hand, the robust alternatives (MAD and Shamos) do not break down with the considered corruption as expected. We also note that the unbiasing factors, and , could help the bias and MSE decrease even when there is contamination. Especially, the original Shamos estimator is much improved with the unbiasing factor . Note that the MSE of the unbiased standard deviation is , while that of the unbiased Shamos is when there is no contamination. This shows that the two estimators are quite comparable even when there is no contamination. In summary, the unbiased Shamos is the best choice in this illustrative example.

| standard | unbiased | unbiased | unbiased | ||||

| deviation | std. dev. | MAD | MAD | Shamos | Shamos | ||

| Empirical Biases | |||||||

| 0 | 0.00036 | 0.00044 | 0.30333 | ||||

| 10 | 0.90590 | 1.15528 | 0.14111 | 0.56179 | 0.23454 | ||

| 20 | 2.22951 | 2.56340 | 0.13713 | 0.54997 | 0.22381 | ||

| 30 | 3.57069 | 3.99020 | 0.13610 | 0.55349 | 0.22700 | ||

| 40 | 4.91276 | 5.41796 | 0.14145 | 0.55059 | 0.22436 | ||

| 50 | 6.25617 | 6.84714 | 0.14119 | 0.55455 | 0.22796 | ||

| Empirical Variances | |||||||

| 0 | 0.10623 | 0.12023 | 0.21083 | 0.31212 | 0.19514 | 0.16093 | |

| 10 | 0.11460 | 0.12970 | 0.23713 | 0.35106 | 0.23538 | 0.19411 | |

| 20 | 0.11573 | 0.13098 | 0.23563 | 0.34884 | 0.23632 | 0.19489 | |

| 30 | 0.11673 | 0.13211 | 0.23140 | 0.34258 | 0.23159 | 0.19099 | |

| 40 | 0.11833 | 0.13392 | 0.23053 | 0.34129 | 0.23157 | 0.19098 | |

| 50 | 0.11572 | 0.13097 | 0.23405 | 0.34649 | 0.23397 | 0.19295 | |

| Empirical MSEs | |||||||

| 0 | 0.13853 | 0.12023 | 0.49600 | 0.31212 | 0.28715 | 0.16093 | |

| 10 | 0.93526 | 1.46437 | 0.41219 | 0.37097 | 0.55099 | 0.24912 | |

| 20 | 5.08646 | 6.70198 | 0.41344 | 0.36764 | 0.53879 | 0.24498 | |

| 30 | 12.86655 | 16.05382 | 0.40993 | 0.36110 | 0.53794 | 0.24252 | |

| 40 | 24.25359 | 29.48825 | 0.40536 | 0.36130 | 0.53472 | 0.24131 | |

| 50 | 39.25542 | 47.01434 | 0.40905 | 0.36643 | 0.54149 | 0.24492 | |

6 Concluding remarks

In this paper, we studied the finite-sample properties of the sample median and Hodges-Lehmann estimators for location and the MAD and Shamos estimators for scale. We obtained the closed-form finite-sample breakdown points of these estimators for the population parameters. We also calculated the unbiasing factors and relative efficiencies of the MAD and the Shamos estimators for the scale parameter through the extensive Monte Carlo simulations up to the sample size of 100. The numerical study showed that the unbiasing factor significantly improves the finite-sample performance of these estimators under consideration. In addition, we provided the predicted values for the unbiasing factors obtained by using the least squares method which can be used for the case of sample size more than 100. To facilitate the implementation of the proposed methods into various application fields, Park and Wang, (2019) developed the R package library which is published in the CRAN (R Core Team,, 2019).

According to the application of the proposed methods to statistical quality control charts for averages and standard deviations, it would be useful to develop robustified alternatives to traditional Shewhart-type control charts because its control limits are also constructed based on the unbiased estimators under the normal distribution. We obtained the empirical and estimated biases of several commonly used robust estimators under the normal distribution, which can be widely used for bias-corrections of the estimates of the parameters. For other parametric models, one can obtain empirical and estimated biases with appropriate robust estimators as suggested in this paper. Given that the breakdown point used in this paper does not depend on a probability model as pointed out in Subsection 2.2a of Hampel et al., (1986), it is of particular interest to obtain biases and relative efficiencies under other parametric models.

Acknowledgment

The authors greatly appreciate the reviewers for their thoughtful comments and suggestions, which have significantly improved the quality of this manuscript. This work was supported by the National Research Foundation of Korea (NRF) grant funded by the Korea government (No. NRF-2017R1A2B4004169).

References

- ASQC and ANSI, (1972) ASQC and ANSI (1972). ASQC (ANSI Standards: A1-1971 (Z1.5-1971), Definitions, Symbols, Formulas, and Tables for Control Charts (approved Nov. 18, 1971). American National Standards Institute, Milwaukee, Wisconsin.

- ASTM E11, (1976) ASTM E11 (1976). Manual on Presentation of Data and Control Chart Analysis. American Society for Testing and Materials, Philadelphia, PA, 4th edition.

- ASTM E11, (2018) ASTM E11 (2018). Manual on Presentation of Data and Control Chart Analysis. American Society for Testing and Materials, West Conshohocken, PA, 9th edition. S. N. Luko (Ed.).

- Donoho and Huber, (1983) Donoho, D. and Huber, P. J. (1983). The notion of breakdown point. In A Festschrift for Erich L. Lehmann, Wadsworth Statist./Probab. Ser., pages 157–184. Wadsworth, Belmont, CA.

- Fisher, (1922) Fisher, R. A. (1922). On the mathematical foundations of theoretical statistics. Philosophical Transactions of the Royal Society of London. Series A, Containing Papers of a Mathematical or Physical Character, 222:309–368.

- Hampel, (1974) Hampel, F. R. (1974). The influence curve and its role in robust estimation. Journal of the American Statistical Association, 69:383–393.

- Hampel et al., (1986) Hampel, F. R., Ronchetti, E., Rousseeuw, P. J., and Stahel, W. A. (1986). Robust Statistics: The Approach Based on Influence Functions. John Wiley & Sons, New York.

- Hayes, (2014) Hayes, K. (2014). Finite-sample bias-correction factors for the median absolute deviation. Communications in Statistics: Simulation and Computation, 43:2205–2212.

- Hettmansperger and McKean, (2010) Hettmansperger, T. P. and McKean, J. W. (2010). Robust Nonparametric Statistical Methods. Chapman & Hall/CRC, Boca Raton, FL, 2nd edition.

- Hodges and Lehmann, (1963) Hodges, J. L. and Lehmann, E. L. (1963). Estimates of location based on rank tests. Annals of Mathematical Statistics, 34:598–611.

- Hodges, Jr., (1967) Hodges, Jr., J. L. (1967). Efficiency in normal samples and tolerance of extreme values for some estimates of location. In Proceedings of the Fifth Berkeley Symposium on Mathematical Statistics and Probability, volume 1, pages 163–186, Berkeley. University of California Press.

- Huber and Ronchetti, (2009) Huber, P. J. and Ronchetti, E. M. (2009). Robust Statistics. John Wiley & Sons, New York, 2nd edition.

- Lèvy-Leduc et al., (2011) Lèvy-Leduc, C., Boistard, H., Moulines, E., Taqqu, M. S., and Reisen, V. A. (2011). Large sample behaviour of some well-known robust estimators under long-range dependence. Statistics, 45:59–71.

- Montgomery, (2013) Montgomery, D. C. (2013). Statistical Quality Control: An Modern Introduction. John Wiley & Sons, 7th edition.

- Ouyang et al., (2019) Ouyang, L., Park, C., Byun, J.-H., and Leeds, M. (2019). Robust design in the case of data contamination and model departure. In Lio, Y., Ng, H., Tsai, T. R., and Chen, D. G., editors, Statistical Quality Technologies: Theory and Practice (ICSA Book Series in Statistics), pages 347–373. Springer, Cham.

- Park and Wang, (2019) Park, C. and Wang, M. (2019). rQCC: Robust quality control chart. https://cran.r-project.org/web/packages/rQCC/. R package version 0.19.8.2.

- R Core Team, (2019) R Core Team (2019). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Rousseeuw, (1991) Rousseeuw, P. (1991). Tutorial to robust statistics. Journal of Chemometrics, 5:1 – 20.

- Rousseeuw and Croux, (1993) Rousseeuw, P. and Croux, C. (1993). Alternatives to the median absolute deviation. Journal of the American Statistical Association, 88:1273–1283.

- Rousseeuw and Croux, (1992) Rousseeuw, P. J. and Croux, C. (1992). Explicit scale estimators with high breakdown point. In Dodge, Y., editor, -Statistical Analysis and Related Methods, pages 77–92. North-Holland,.

- Serfling, (2011) Serfling, R. J. (2011). Asymptotic relative efficiency in estimation. In Lovric, M., editor, Encyclopedia of Statistical Science, Part I, pages 68–82. Springer-Verlag, Berlin.

- Shamos, (1976) Shamos, M. I. (1976). Geometry and statistics: Problems at the interface. In Traub, J. F., editor, Algorithms and Complexity: New Directions and Recent Results, pages 251–280. Academic Press, New York.

- Shewhart, (1926) Shewhart, W. A. (1926). Quality control charts. Bell Systems Technical Journal, pages 593–603.

- Shewhart, (1931) Shewhart, W. A. (1931). Economic Control of Quality of Manufactured Product. Van Nostrand Reinhold, Princeton, NJ. Republished in 1981 by the American Society for Quality Control, Milwaukee, Wisconsin.

- Vining, (2009) Vining, G. (2009). Technical advice: Phase I and Phase II control charts. Quality Engineering, 21(4):478–479.

- Walsh, (1949) Walsh, J. E. (1949). Some significance tests for the median which are valid under very general conditions. The Annals of Mathematical Statistics, 20:54–81.

- Wilcox, (2016) Wilcox, R. R. (2016). Introduction to Robust Estimation and Hypothesis Testing. Academic Press, Loncon, United Kingdom, 4th edition.

- Williams, (2011) Williams, D. C. (2011). Finite sample correction factors for several simple robust estimators of normal standard deviation. Journal of Statistical Computation and Simulation, 81:1697–1702.

Appendix: Tables and Figures

| median and MAD | HL1 and Shamos | HL2 | HL3 | ||

|---|---|---|---|---|---|

| 2 | 0.0000000 | 0.0000000 | 0.0000000 | 0.0000000 | |

| 3 | 0.3333333 | 0.0000000 | 0.0000000 | 0.0000000 | |

| 4 | 0.2500000 | 0.0000000 | 0.2500000 | 0.2500000 | |

| 5 | 0.4000000 | 0.2000000 | 0.2000000 | 0.2000000 | |

| 6 | 0.3333333 | 0.1666667 | 0.1666667 | 0.1666667 | |

| 7 | 0.4285714 | 0.1428571 | 0.2857143 | 0.2857143 | |

| 8 | 0.3750000 | 0.2500000 | 0.2500000 | 0.2500000 | |

| 9 | 0.4444444 | 0.2222222 | 0.2222222 | 0.2222222 | |

| 10 | 0.4000000 | 0.2000000 | 0.3000000 | 0.2000000 | |

| 11 | 0.4545455 | 0.2727273 | 0.2727273 | 0.2727273 | |

| 12 | 0.4166667 | 0.2500000 | 0.2500000 | 0.2500000 | |

| 13 | 0.4615385 | 0.2307692 | 0.2307692 | 0.2307692 | |

| 14 | 0.4285714 | 0.2142857 | 0.2857143 | 0.2857143 | |

| 15 | 0.4666667 | 0.2666667 | 0.2666667 | 0.2666667 | |

| 16 | 0.4375000 | 0.2500000 | 0.2500000 | 0.2500000 | |

| 17 | 0.4705882 | 0.2352941 | 0.2941176 | 0.2352941 | |

| 18 | 0.4444444 | 0.2777778 | 0.2777778 | 0.2777778 | |

| 19 | 0.4736842 | 0.2631579 | 0.2631579 | 0.2631579 | |

| 20 | 0.4500000 | 0.2500000 | 0.2500000 | 0.2500000 | |

| 21 | 0.4761905 | 0.2380952 | 0.2857143 | 0.2857143 | |

| 22 | 0.4545455 | 0.2727273 | 0.2727273 | 0.2727273 | |

| 23 | 0.4782609 | 0.2608696 | 0.2608696 | 0.2608696 | |

| 24 | 0.4583333 | 0.2500000 | 0.2916667 | 0.2916667 | |

| 25 | 0.4800000 | 0.2800000 | 0.2800000 | 0.2800000 | |

| 26 | 0.4615385 | 0.2692308 | 0.2692308 | 0.2692308 | |

| 27 | 0.4814815 | 0.2592593 | 0.2962963 | 0.2592593 | |

| 28 | 0.4642857 | 0.2857143 | 0.2857143 | 0.2857143 | |

| 29 | 0.4827586 | 0.2758621 | 0.2758621 | 0.2758621 | |

| 30 | 0.4666667 | 0.2666667 | 0.2666667 | 0.2666667 | |

| 31 | 0.4838710 | 0.2580645 | 0.2903226 | 0.2903226 | |

| 32 | 0.4687500 | 0.2812500 | 0.2812500 | 0.2812500 | |

| 33 | 0.4848485 | 0.2727273 | 0.2727273 | 0.2727273 | |

| 34 | 0.4705882 | 0.2647059 | 0.2941176 | 0.2647059 | |

| 35 | 0.4857143 | 0.2857143 | 0.2857143 | 0.2857143 | |

| 36 | 0.4722222 | 0.2777778 | 0.2777778 | 0.2777778 | |

| 37 | 0.4864865 | 0.2702703 | 0.2702703 | 0.2702703 | |

| 38 | 0.4736842 | 0.2631579 | 0.2894737 | 0.2894737 | |

| 39 | 0.4871795 | 0.2820513 | 0.2820513 | 0.2820513 | |

| 40 | 0.4750000 | 0.2750000 | 0.2750000 | 0.2750000 | |

| 41 | 0.4878049 | 0.2682927 | 0.2926829 | 0.2926829 | |

| 42 | 0.4761905 | 0.2857143 | 0.2857143 | 0.2857143 | |

| 43 | 0.4883721 | 0.2790698 | 0.2790698 | 0.2790698 | |

| 44 | 0.4772727 | 0.2727273 | 0.2954545 | 0.2727273 | |

| 45 | 0.4888889 | 0.2888889 | 0.2888889 | 0.2888889 | |

| 46 | 0.4782609 | 0.2826087 | 0.2826087 | 0.2826087 | |

| 47 | 0.4893617 | 0.2765957 | 0.2765957 | 0.2765957 | |

| 48 | 0.4791667 | 0.2708333 | 0.2916667 | 0.2916667 | |

| 49 | 0.4897959 | 0.2857143 | 0.2857143 | 0.2857143 | |

| 50 | 0.4800000 | 0.2800000 | 0.2800000 | 0.2800000 |

| MAD | Shamos | MAD | Shamos | |||||

|---|---|---|---|---|---|---|---|---|

| 1 | NA | NA | 51 | |||||

| 2 | 52 | |||||||

| 3 | 53 | |||||||

| 4 | 54 | |||||||

| 5 | 55 | |||||||

| 6 | 56 | |||||||

| 7 | 57 | |||||||

| 8 | 58 | |||||||

| 9 | 59 | |||||||

| 10 | 60 | |||||||

| 11 | 61 | |||||||

| 12 | 62 | |||||||

| 13 | 63 | |||||||

| 14 | 64 | |||||||

| 15 | 65 | |||||||

| 16 | 66 | |||||||

| 17 | 67 | |||||||

| 18 | 68 | |||||||

| 19 | 69 | |||||||

| 20 | 70 | |||||||

| 21 | 71 | |||||||

| 22 | 72 | |||||||

| 23 | 73 | |||||||

| 24 | 74 | |||||||

| 25 | 75 | |||||||

| 26 | 76 | |||||||

| 27 | 77 | |||||||

| 28 | 78 | |||||||

| 29 | 79 | |||||||

| 30 | 80 | |||||||

| 31 | 81 | |||||||

| 32 | 82 | |||||||

| 33 | 83 | |||||||

| 34 | 84 | |||||||

| 35 | 85 | |||||||

| 36 | 86 | |||||||

| 37 | 87 | |||||||

| 38 | 88 | |||||||

| 39 | 89 | |||||||

| 40 | 90 | |||||||

| 41 | 91 | |||||||

| 42 | 92 | |||||||

| 43 | 93 | |||||||

| 44 | 94 | |||||||

| 45 | 95 | |||||||

| 46 | 96 | |||||||

| 47 | 97 | |||||||

| 48 | 98 | |||||||

| 49 | 99 | |||||||

| 50 | 100 |

| MAD | (Hayes) | (Williams) | Shamos | (Hayes) | (Williams) | |||

|---|---|---|---|---|---|---|---|---|

| 109 | 0.0038374 | 0.0038377 | 0.0038425 | |||||

| 110 | 0.0037996 | 0.0038025 | 0.0038073 | |||||

| 119 | 0.0034984 | 0.0035124 | 0.0035170 | |||||

| 120 | 0.0034691 | 0.0034828 | 0.0034875 | |||||

| 129 | 0.0032441 | 0.0032379 | 0.0032422 | |||||

| 130 | 0.0032241 | 0.0032127 | 0.0032170 | |||||

| 139 | 0.0029854 | 0.0030031 | 0.0030070 | |||||

| 140 | 0.0029548 | 0.0029815 | 0.0029854 | |||||

| 149 | 0.0028230 | 0.0028002 | 0.0028036 | |||||

| 150 | 0.0028080 | 0.0027814 | 0.0027847 | |||||

| 159 | 0.0026355 | 0.0026229 | 0.0026258 | |||||

| 160 | 0.0026154 | 0.0026064 | 0.0026093 | |||||

| 169 | 0.0024503 | 0.0024667 | 0.0024692 | |||||

| 170 | 0.0024402 | 0.0024521 | 0.0024545 | |||||

| 179 | 0.0023257 | 0.0023281 | 0.0023301 | |||||

| 180 | 0.0023122 | 0.0023151 | 0.0023170 | |||||

| 189 | 0.0021780 | 0.0022042 | 0.0022058 | |||||

| 190 | 0.0021673 | 0.0021925 | 0.0021941 | |||||

| 199 | 0.0020904 | 0.0020928 | 0.0020940 | |||||

| 200 | 0.0020786 | 0.0020823 | 0.0020835 | |||||

| 249 | 0.0016628 | 0.0016708 | 0.0016704 | |||||

| 250 | 0.0016562 | 0.0016641 | 0.0016636 | |||||

| 299 | 0.0013875 | 0.0013904 | 0.0013889 | |||||

| 300 | 0.0013822 | 0.0013858 | 0.0013842 | |||||

| 349 | 0.0012033 | 0.0011906 | 0.0011884 | |||||

| 350 | 0.0012013 | 0.0011872 | 0.0011849 | |||||

| 399 | 0.0010331 | 0.0010410 | 0.0010383 | |||||

| 400 | 0.0010287 | 0.0010384 | 0.0010357 | |||||

| 449 | 0.0009196 | 0.0009248 | 0.0009217 | |||||

| 450 | 0.0009170 | 0.0009227 | 0.0009197 | |||||

| 499 | 0.0008413 | 0.0008319 | 0.0008286 | |||||

| 500 | 0.0008389 | 0.0008303 | 0.0008270 |

| median | HL1 | HL2 | HL3 | MAD | Shamos | |||

|---|---|---|---|---|---|---|---|---|

| 1 | 1.0000 | NA | 1.0000 | 1.0000 | NA | NA | ||

| 2 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.1000 | 2.2001 | ||

| 3 | 1.3463 | 1.0871 | 1.0221 | 1.0871 | 1.4372 | 2.3812 | ||

| 4 | 1.1930 | 1.0000 | 1.0949 | 1.0949 | 1.1680 | 1.6996 | ||

| 5 | 1.4339 | 1.0617 | 1.0754 | 1.0754 | 1.9809 | 1.8573 | ||

| 6 | 1.2882 | 1.0619 | 1.0759 | 1.0602 | 1.6859 | 1.7883 | ||

| 7 | 1.4736 | 1.0630 | 1.0814 | 1.0756 | 2.2125 | 1.6180 | ||

| 8 | 1.3459 | 1.0628 | 1.0728 | 1.0705 | 1.9486 | 1.5824 | ||

| 9 | 1.4957 | 1.0588 | 1.0756 | 1.0678 | 2.3326 | 1.5109 | ||

| 10 | 1.3833 | 1.0608 | 1.0743 | 1.0641 | 2.1072 | 1.4855 | ||

| 11 | 1.5088 | 1.0602 | 1.0693 | 1.0649 | 2.4082 | 1.4643 | ||

| 12 | 1.4087 | 1.0560 | 1.0670 | 1.0614 | 2.2112 | 1.4234 | ||

| 13 | 1.5195 | 1.0567 | 1.0685 | 1.0629 | 2.4570 | 1.4008 | ||

| 14 | 1.4298 | 1.0565 | 1.0663 | 1.0603 | 2.2848 | 1.3905 | ||

| 15 | 1.5249 | 1.0562 | 1.0645 | 1.0603 | 2.4952 | 1.3719 | ||

| 16 | 1.4457 | 1.0547 | 1.0637 | 1.0590 | 2.3412 | 1.3554 | ||

| 17 | 1.5302 | 1.0541 | 1.0633 | 1.0587 | 2.5217 | 1.3434 | ||

| 18 | 1.4585 | 1.0540 | 1.0621 | 1.0574 | 2.3846 | 1.3355 | ||

| 19 | 1.5333 | 1.0532 | 1.0605 | 1.0567 | 2.5447 | 1.3249 | ||

| 20 | 1.4702 | 1.0545 | 1.0620 | 1.0581 | 2.4185 | 1.3146 | ||

| 21 | 1.5383 | 1.0536 | 1.0611 | 1.0573 | 2.5611 | 1.3079 | ||

| 22 | 1.4770 | 1.0527 | 1.0596 | 1.0557 | 2.4475 | 1.3015 | ||

| 23 | 1.5420 | 1.0532 | 1.0597 | 1.0564 | 2.5758 | 1.2953 | ||

| 24 | 1.4850 | 1.0529 | 1.0594 | 1.0560 | 2.4699 | 1.2883 | ||

| 25 | 1.5438 | 1.0521 | 1.0586 | 1.0553 | 2.5873 | 1.2825 | ||

| 26 | 1.4896 | 1.0518 | 1.0578 | 1.0545 | 2.4886 | 1.2776 | ||

| 27 | 1.5462 | 1.0526 | 1.0582 | 1.0553 | 2.5960 | 1.2731 | ||

| 28 | 1.4954 | 1.0511 | 1.0567 | 1.0538 | 2.5030 | 1.2676 | ||

| 29 | 1.5476 | 1.0525 | 1.0581 | 1.0552 | 2.6070 | 1.2650 | ||

| 30 | 1.5005 | 1.0518 | 1.0571 | 1.0543 | 2.5199 | 1.2616 | ||

| 31 | 1.5482 | 1.0514 | 1.0564 | 1.0538 | 2.6132 | 1.2586 | ||

| 32 | 1.5057 | 1.0517 | 1.0567 | 1.0541 | 2.5335 | 1.2552 | ||

| 33 | 1.5516 | 1.0521 | 1.0571 | 1.0545 | 2.6208 | 1.2519 | ||

| 34 | 1.5091 | 1.0512 | 1.0560 | 1.0534 | 2.5442 | 1.2493 | ||

| 35 | 1.5515 | 1.0508 | 1.0554 | 1.0530 | 2.6285 | 1.2466 | ||

| 36 | 1.5123 | 1.0512 | 1.0557 | 1.0534 | 2.5545 | 1.2433 | ||

| 37 | 1.5531 | 1.0512 | 1.0556 | 1.0534 | 2.6332 | 1.2415 | ||

| 38 | 1.5148 | 1.0502 | 1.0545 | 1.0522 | 2.5637 | 1.2393 | ||

| 39 | 1.5550 | 1.0513 | 1.0555 | 1.0533 | 2.6344 | 1.2364 | ||

| 40 | 1.5173 | 1.0507 | 1.0547 | 1.0526 | 2.5720 | 1.2357 | ||

| 41 | 1.5532 | 1.0498 | 1.0539 | 1.0518 | 2.6403 | 1.2325 | ||

| 42 | 1.5206 | 1.0510 | 1.0549 | 1.0528 | 2.5780 | 1.2315 | ||

| 43 | 1.5552 | 1.0504 | 1.0541 | 1.0522 | 2.6436 | 1.2287 | ||

| 44 | 1.5224 | 1.0500 | 1.0537 | 1.0518 | 2.5869 | 1.2284 | ||

| 45 | 1.5568 | 1.0504 | 1.0541 | 1.0522 | 2.6477 | 1.2260 | ||

| 46 | 1.5240 | 1.0496 | 1.0533 | 1.0514 | 2.5904 | 1.2248 | ||

| 47 | 1.5570 | 1.0504 | 1.0539 | 1.0521 | 2.6511 | 1.2232 | ||

| 48 | 1.5249 | 1.0493 | 1.0528 | 1.0510 | 2.5960 | 1.2214 | ||

| 49 | 1.5562 | 1.0495 | 1.0529 | 1.0512 | 2.6537 | 1.2199 | ||

| 50 | 1.5267 | 1.0499 | 1.0532 | 1.0514 | 2.6014 | 1.2184 |

| median | HL1 | HL2 | HL3 | MAD | Shamos | |||

|---|---|---|---|---|---|---|---|---|

| 51 | 1.5583 | 1.0502 | 1.0534 | 1.0517 | 2.6577 | 1.2199 | ||

| 52 | 1.5298 | 1.0499 | 1.0532 | 1.0515 | 2.6053 | 1.2174 | ||

| 53 | 1.5592 | 1.0501 | 1.0533 | 1.0517 | 2.6568 | 1.2160 | ||

| 54 | 1.5298 | 1.0489 | 1.0519 | 1.0503 | 2.6125 | 1.2156 | ||

| 55 | 1.5584 | 1.0493 | 1.0523 | 1.0508 | 2.6631 | 1.2144 | ||

| 56 | 1.5330 | 1.0497 | 1.0527 | 1.0512 | 2.6139 | 1.2132 | ||

| 57 | 1.5589 | 1.0496 | 1.0526 | 1.0510 | 2.6649 | 1.2126 | ||

| 58 | 1.5337 | 1.0495 | 1.0524 | 1.0509 | 2.6161 | 1.2098 | ||

| 59 | 1.5598 | 1.0501 | 1.0530 | 1.0515 | 2.6671 | 1.2095 | ||

| 60 | 1.5349 | 1.0489 | 1.0517 | 1.0503 | 2.6219 | 1.2095 | ||

| 61 | 1.5594 | 1.0492 | 1.0519 | 1.0505 | 2.6667 | 1.2073 | ||

| 62 | 1.5361 | 1.0492 | 1.0520 | 1.0505 | 2.6235 | 1.2071 | ||

| 63 | 1.5594 | 1.0485 | 1.0512 | 1.0498 | 2.6695 | 1.2064 | ||

| 64 | 1.5373 | 1.0494 | 1.0521 | 1.0507 | 2.6260 | 1.2050 | ||

| 65 | 1.5598 | 1.0488 | 1.0514 | 1.0500 | 2.6731 | 1.2067 | ||

| 66 | 1.5380 | 1.0496 | 1.0521 | 1.0508 | 2.6297 | 1.2036 | ||

| 67 | 1.5606 | 1.0494 | 1.0519 | 1.0506 | 2.6722 | 1.2034 | ||

| 68 | 1.5389 | 1.0491 | 1.0516 | 1.0503 | 2.6341 | 1.2030 | ||

| 69 | 1.5607 | 1.0479 | 1.0504 | 1.0491 | 2.6748 | 1.2025 | ||

| 70 | 1.5399 | 1.0490 | 1.0514 | 1.0502 | 2.6351 | 1.2016 | ||

| 71 | 1.5595 | 1.0482 | 1.0506 | 1.0494 | 2.6738 | 1.2005 | ||

| 72 | 1.5410 | 1.0491 | 1.0515 | 1.0503 | 2.6351 | 1.1993 | ||

| 73 | 1.5622 | 1.0492 | 1.0515 | 1.0503 | 2.6754 | 1.1993 | ||

| 74 | 1.5426 | 1.0498 | 1.0521 | 1.0510 | 2.6395 | 1.1990 | ||

| 75 | 1.5619 | 1.0489 | 1.0512 | 1.0500 | 2.6763 | 1.1985 | ||

| 76 | 1.5415 | 1.0486 | 1.0509 | 1.0497 | 2.6411 | 1.1975 | ||

| 77 | 1.5616 | 1.0485 | 1.0508 | 1.0496 | 2.6780 | 1.1975 | ||

| 78 | 1.5434 | 1.0494 | 1.0516 | 1.0505 | 2.6453 | 1.1971 | ||

| 79 | 1.5639 | 1.0493 | 1.0515 | 1.0504 | 2.6794 | 1.1968 | ||

| 80 | 1.5445 | 1.0497 | 1.0519 | 1.0508 | 2.6453 | 1.1958 | ||

| 81 | 1.5612 | 1.0486 | 1.0507 | 1.0496 | 2.6815 | 1.1960 | ||

| 82 | 1.5444 | 1.0494 | 1.0515 | 1.0504 | 2.6472 | 1.1947 | ||

| 83 | 1.5626 | 1.0484 | 1.0505 | 1.0494 | 2.6815 | 1.1947 | ||

| 84 | 1.5449 | 1.0490 | 1.0511 | 1.0500 | 2.6475 | 1.1939 | ||

| 85 | 1.5630 | 1.0484 | 1.0504 | 1.0494 | 2.6831 | 1.1938 | ||

| 86 | 1.5441 | 1.0479 | 1.0499 | 1.0489 | 2.6505 | 1.1931 | ||

| 87 | 1.5643 | 1.0495 | 1.0514 | 1.0504 | 2.6830 | 1.1923 | ||

| 88 | 1.5448 | 1.0478 | 1.0497 | 1.0487 | 2.6535 | 1.1929 | ||

| 89 | 1.5640 | 1.0487 | 1.0506 | 1.0496 | 2.6857 | 1.1931 | ||

| 90 | 1.5463 | 1.0483 | 1.0503 | 1.0493 | 2.6562 | 1.1920 | ||

| 91 | 1.5634 | 1.0486 | 1.0505 | 1.0495 | 2.6853 | 1.1914 | ||

| 92 | 1.5477 | 1.0491 | 1.0509 | 1.0500 | 2.6567 | 1.1913 | ||

| 93 | 1.5631 | 1.0481 | 1.0500 | 1.0490 | 2.6859 | 1.1906 | ||

| 94 | 1.5482 | 1.0488 | 1.0507 | 1.0497 | 2.6584 | 1.1907 | ||

| 95 | 1.5629 | 1.0481 | 1.0499 | 1.0490 | 2.6878 | 1.1905 | ||

| 96 | 1.5466 | 1.0477 | 1.0495 | 1.0486 | 2.6576 | 1.1894 | ||

| 97 | 1.5636 | 1.0480 | 1.0498 | 1.0489 | 2.6881 | 1.1895 | ||

| 98 | 1.5477 | 1.0477 | 1.0495 | 1.0486 | 2.6613 | 1.1899 | ||

| 99 | 1.5642 | 1.0483 | 1.0501 | 1.0492 | 2.6888 | 1.1887 | ||

| 100 | 1.5484 | 1.0481 | 1.0498 | 1.0489 | 2.6604 | 1.1874 |

| median | HL1 | HL2 | HL3 | MAD | Shamos | |||

|---|---|---|---|---|---|---|---|---|

| 109 | 1.5655 | 1.0490 | 1.0506 | 1.0498 | 2.6889 | 1.1857 | ||

| 110 | 1.5508 | 1.0484 | 1.0500 | 1.0492 | 2.6657 | 1.1856 | ||

| 119 | 1.5651 | 1.0478 | 1.0492 | 1.0485 | 2.6936 | 1.1830 | ||

| 120 | 1.5526 | 1.0478 | 1.0493 | 1.0486 | 2.6717 | 1.1836 | ||

| 129 | 1.5661 | 1.0477 | 1.0490 | 1.0483 | 2.6953 | 1.1809 | ||

| 130 | 1.5541 | 1.0478 | 1.0492 | 1.0485 | 2.6727 | 1.1804 | ||

| 139 | 1.5671 | 1.0491 | 1.0503 | 1.0497 | 2.6963 | 1.1792 | ||

| 140 | 1.5567 | 1.0495 | 1.0508 | 1.0502 | 2.6770 | 1.1794 | ||

| 149 | 1.5666 | 1.0484 | 1.0496 | 1.0490 | 2.7008 | 1.1789 | ||

| 150 | 1.5566 | 1.0484 | 1.0496 | 1.0490 | 2.6815 | 1.1788 | ||

| 159 | 1.5673 | 1.0484 | 1.0495 | 1.0490 | 2.7006 | 1.1768 | ||

| 160 | 1.5584 | 1.0485 | 1.0495 | 1.0490 | 2.6827 | 1.1765 | ||

| 169 | 1.5661 | 1.0474 | 1.0485 | 1.0479 | 2.7012 | 1.1757 | ||

| 170 | 1.5578 | 1.0476 | 1.0486 | 1.0481 | 2.6861 | 1.1755 | ||

| 179 | 1.5676 | 1.0477 | 1.0487 | 1.0482 | 2.7038 | 1.1750 | ||

| 180 | 1.5590 | 1.0480 | 1.0490 | 1.0485 | 2.6889 | 1.1750 | ||

| 189 | 1.5663 | 1.0473 | 1.0483 | 1.0478 | 2.7043 | 1.1743 | ||

| 190 | 1.5584 | 1.0473 | 1.0482 | 1.0478 | 2.6903 | 1.1741 | ||

| 199 | 1.5681 | 1.0481 | 1.0490 | 1.0486 | 2.7049 | 1.1741 | ||

| 200 | 1.5608 | 1.0482 | 1.0491 | 1.0486 | 2.6904 | 1.1732 | ||

| 249 | 1.5679 | 1.0472 | 1.0479 | 1.0476 | 2.7083 | 1.1705 | ||

| 250 | 1.5623 | 1.0479 | 1.0486 | 1.0483 | 2.6977 | 1.1709 | ||

| 299 | 1.5689 | 1.0477 | 1.0483 | 1.0480 | 2.7084 | 1.1673 | ||

| 300 | 1.5642 | 1.0479 | 1.0485 | 1.0482 | 2.6986 | 1.1670 | ||

| 349 | 1.5700 | 1.0479 | 1.0484 | 1.0481 | 2.7131 | 1.1673 | ||

| 350 | 1.5654 | 1.0479 | 1.0484 | 1.0481 | 2.7049 | 1.1675 | ||

| 399 | 1.5691 | 1.0475 | 1.0479 | 1.0477 | 2.7126 | 1.1650 | ||

| 400 | 1.5646 | 1.0469 | 1.0474 | 1.0472 | 2.7072 | 1.1651 | ||

| 449 | 1.5694 | 1.0474 | 1.0478 | 1.0476 | 2.7125 | 1.1639 | ||

| 450 | 1.5659 | 1.0475 | 1.0479 | 1.0477 | 2.7056 | 1.1645 | ||

| 499 | 1.5701 | 1.0475 | 1.0479 | 1.0477 | 2.7147 | 1.1637 | ||

| 500 | 1.5674 | 1.0482 | 1.0486 | 1.0484 | 2.7101 | 1.1646 |

| median | HL1 | HL2 | HL3 | MAD | Shamos | |||

|---|---|---|---|---|---|---|---|---|

| 1 | 1.0000 | NA | 1.0000 | 1.0000 | NA | NA | ||

| 2 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 0.9091 | 0.4545 | ||

| 3 | 0.7427 | 0.9199 | 0.9784 | 0.9199 | 0.6958 | 0.4199 | ||

| 4 | 0.8382 | 1.0000 | 0.9133 | 0.9133 | 0.8562 | 0.5884 | ||

| 5 | 0.6974 | 0.9419 | 0.9299 | 0.9299 | 0.5048 | 0.5384 | ||

| 6 | 0.7763 | 0.9417 | 0.9295 | 0.9432 | 0.5932 | 0.5592 | ||

| 7 | 0.6786 | 0.9407 | 0.9248 | 0.9297 | 0.4520 | 0.6180 | ||

| 8 | 0.7430 | 0.9409 | 0.9322 | 0.9342 | 0.5132 | 0.6320 | ||

| 9 | 0.6686 | 0.9445 | 0.9297 | 0.9365 | 0.4287 | 0.6618 | ||

| 10 | 0.7229 | 0.9426 | 0.9308 | 0.9398 | 0.4746 | 0.6732 | ||

| 11 | 0.6628 | 0.9432 | 0.9352 | 0.9391 | 0.4153 | 0.6829 | ||

| 12 | 0.7098 | 0.9470 | 0.9372 | 0.9422 | 0.4522 | 0.7026 | ||

| 13 | 0.6581 | 0.9464 | 0.9359 | 0.9408 | 0.4070 | 0.7139 | ||

| 14 | 0.6994 | 0.9465 | 0.9378 | 0.9432 | 0.4377 | 0.7192 | ||

| 15 | 0.6558 | 0.9468 | 0.9394 | 0.9432 | 0.4008 | 0.7289 | ||

| 16 | 0.6917 | 0.9482 | 0.9402 | 0.9443 | 0.4271 | 0.7378 | ||

| 17 | 0.6535 | 0.9486 | 0.9405 | 0.9445 | 0.3966 | 0.7444 | ||

| 18 | 0.6856 | 0.9487 | 0.9415 | 0.9457 | 0.4194 | 0.7488 | ||

| 19 | 0.6522 | 0.9495 | 0.9430 | 0.9463 | 0.3930 | 0.7547 | ||

| 20 | 0.6802 | 0.9483 | 0.9416 | 0.9451 | 0.4135 | 0.7607 | ||

| 21 | 0.6501 | 0.9491 | 0.9424 | 0.9458 | 0.3905 | 0.7646 | ||

| 22 | 0.6770 | 0.9499 | 0.9437 | 0.9472 | 0.4086 | 0.7684 | ||

| 23 | 0.6485 | 0.9495 | 0.9437 | 0.9466 | 0.3882 | 0.7720 | ||

| 24 | 0.6734 | 0.9498 | 0.9440 | 0.9470 | 0.4049 | 0.7762 | ||

| 25 | 0.6478 | 0.9504 | 0.9447 | 0.9476 | 0.3865 | 0.7798 | ||

| 26 | 0.6713 | 0.9507 | 0.9454 | 0.9483 | 0.4018 | 0.7827 | ||

| 27 | 0.6468 | 0.9501 | 0.9450 | 0.9476 | 0.3852 | 0.7855 | ||

| 28 | 0.6687 | 0.9514 | 0.9463 | 0.9490 | 0.3995 | 0.7889 | ||

| 29 | 0.6462 | 0.9501 | 0.9451 | 0.9477 | 0.3836 | 0.7905 | ||

| 30 | 0.6664 | 0.9507 | 0.9459 | 0.9485 | 0.3968 | 0.7926 | ||

| 31 | 0.6459 | 0.9511 | 0.9466 | 0.9489 | 0.3827 | 0.7945 | ||

| 32 | 0.6641 | 0.9508 | 0.9463 | 0.9486 | 0.3947 | 0.7967 | ||

| 33 | 0.6445 | 0.9505 | 0.9460 | 0.9483 | 0.3816 | 0.7988 | ||

| 34 | 0.6627 | 0.9513 | 0.9470 | 0.9493 | 0.3931 | 0.8004 | ||

| 35 | 0.6445 | 0.9516 | 0.9475 | 0.9496 | 0.3804 | 0.8022 | ||

| 36 | 0.6612 | 0.9513 | 0.9472 | 0.9493 | 0.3915 | 0.8043 | ||

| 37 | 0.6439 | 0.9513 | 0.9473 | 0.9493 | 0.3798 | 0.8055 | ||

| 38 | 0.6601 | 0.9522 | 0.9483 | 0.9504 | 0.3901 | 0.8069 | ||

| 39 | 0.6431 | 0.9512 | 0.9475 | 0.9494 | 0.3796 | 0.8088 | ||

| 40 | 0.6591 | 0.9518 | 0.9481 | 0.9500 | 0.3888 | 0.8093 | ||

| 41 | 0.6438 | 0.9525 | 0.9489 | 0.9507 | 0.3787 | 0.8113 | ||

| 42 | 0.6576 | 0.9515 | 0.9479 | 0.9498 | 0.3879 | 0.8120 | ||

| 43 | 0.6430 | 0.9521 | 0.9486 | 0.9504 | 0.3783 | 0.8138 | ||

| 44 | 0.6569 | 0.9524 | 0.9490 | 0.9508 | 0.3866 | 0.8141 | ||

| 45 | 0.6423 | 0.9520 | 0.9487 | 0.9504 | 0.3777 | 0.8157 | ||

| 46 | 0.6562 | 0.9527 | 0.9494 | 0.9511 | 0.3860 | 0.8164 | ||

| 47 | 0.6422 | 0.9520 | 0.9489 | 0.9505 | 0.3772 | 0.8175 | ||

| 48 | 0.6558 | 0.9530 | 0.9499 | 0.9515 | 0.3852 | 0.8187 | ||

| 49 | 0.6426 | 0.9529 | 0.9497 | 0.9513 | 0.3768 | 0.8197 | ||

| 50 | 0.6550 | 0.9525 | 0.9495 | 0.9511 | 0.3844 | 0.8208 |

| median | HL1 | HL2 | HL3 | MAD | Shamos | |||

|---|---|---|---|---|---|---|---|---|

| 51 | 0.6417 | 0.9522 | 0.9493 | 0.9508 | 0.3763 | 0.8197 | ||

| 52 | 0.6537 | 0.9525 | 0.9495 | 0.9510 | 0.3838 | 0.8214 | ||

| 53 | 0.6414 | 0.9523 | 0.9494 | 0.9509 | 0.3764 | 0.8223 | ||

| 54 | 0.6537 | 0.9534 | 0.9506 | 0.9521 | 0.3828 | 0.8226 | ||

| 55 | 0.6417 | 0.9530 | 0.9503 | 0.9517 | 0.3755 | 0.8234 | ||

| 56 | 0.6523 | 0.9527 | 0.9499 | 0.9513 | 0.3826 | 0.8243 | ||

| 57 | 0.6415 | 0.9528 | 0.9501 | 0.9514 | 0.3752 | 0.8247 | ||

| 58 | 0.6520 | 0.9528 | 0.9502 | 0.9515 | 0.3822 | 0.8266 | ||

| 59 | 0.6411 | 0.9523 | 0.9497 | 0.9510 | 0.3749 | 0.8268 | ||

| 60 | 0.6515 | 0.9534 | 0.9508 | 0.9521 | 0.3814 | 0.8268 | ||

| 61 | 0.6413 | 0.9531 | 0.9506 | 0.9519 | 0.3750 | 0.8283 | ||

| 62 | 0.6510 | 0.9531 | 0.9506 | 0.9519 | 0.3812 | 0.8284 | ||

| 63 | 0.6413 | 0.9538 | 0.9513 | 0.9526 | 0.3746 | 0.8289 | ||

| 64 | 0.6505 | 0.9529 | 0.9505 | 0.9517 | 0.3808 | 0.8299 | ||

| 65 | 0.6411 | 0.9535 | 0.9511 | 0.9523 | 0.3741 | 0.8287 | ||

| 66 | 0.6502 | 0.9528 | 0.9505 | 0.9516 | 0.3803 | 0.8308 | ||

| 67 | 0.6408 | 0.9529 | 0.9507 | 0.9518 | 0.3742 | 0.8310 | ||

| 68 | 0.6498 | 0.9532 | 0.9509 | 0.9521 | 0.3796 | 0.8312 | ||

| 69 | 0.6408 | 0.9543 | 0.9520 | 0.9532 | 0.3739 | 0.8316 | ||

| 70 | 0.6494 | 0.9533 | 0.9511 | 0.9522 | 0.3795 | 0.8323 | ||

| 71 | 0.6412 | 0.9540 | 0.9518 | 0.9529 | 0.3740 | 0.8330 | ||

| 72 | 0.6489 | 0.9532 | 0.9510 | 0.9521 | 0.3795 | 0.8338 | ||

| 73 | 0.6401 | 0.9532 | 0.9510 | 0.9521 | 0.3738 | 0.8338 | ||

| 74 | 0.6483 | 0.9525 | 0.9504 | 0.9515 | 0.3789 | 0.8341 | ||

| 75 | 0.6402 | 0.9534 | 0.9513 | 0.9524 | 0.3736 | 0.8344 | ||

| 76 | 0.6487 | 0.9536 | 0.9516 | 0.9526 | 0.3786 | 0.8351 | ||

| 77 | 0.6404 | 0.9537 | 0.9517 | 0.9527 | 0.3734 | 0.8351 | ||

| 78 | 0.6479 | 0.9529 | 0.9509 | 0.9520 | 0.3780 | 0.8353 | ||

| 79 | 0.6394 | 0.9530 | 0.9510 | 0.9520 | 0.3732 | 0.8355 | ||

| 80 | 0.6475 | 0.9526 | 0.9507 | 0.9517 | 0.3780 | 0.8363 | ||

| 81 | 0.6405 | 0.9537 | 0.9517 | 0.9527 | 0.3729 | 0.8361 | ||

| 82 | 0.6475 | 0.9529 | 0.9510 | 0.9520 | 0.3778 | 0.8370 | ||

| 83 | 0.6400 | 0.9538 | 0.9520 | 0.9529 | 0.3729 | 0.8370 | ||

| 84 | 0.6473 | 0.9533 | 0.9514 | 0.9523 | 0.3777 | 0.8376 | ||

| 85 | 0.6398 | 0.9539 | 0.9520 | 0.9529 | 0.3727 | 0.8376 | ||

| 86 | 0.6476 | 0.9543 | 0.9525 | 0.9534 | 0.3773 | 0.8381 | ||

| 87 | 0.6393 | 0.9529 | 0.9511 | 0.9520 | 0.3727 | 0.8387 | ||

| 88 | 0.6473 | 0.9544 | 0.9526 | 0.9535 | 0.3769 | 0.8383 | ||

| 89 | 0.6394 | 0.9536 | 0.9518 | 0.9527 | 0.3723 | 0.8382 | ||

| 90 | 0.6467 | 0.9539 | 0.9521 | 0.9530 | 0.3765 | 0.8389 | ||

| 91 | 0.6396 | 0.9536 | 0.9519 | 0.9528 | 0.3724 | 0.8394 | ||

| 92 | 0.6461 | 0.9532 | 0.9515 | 0.9524 | 0.3764 | 0.8394 | ||

| 93 | 0.6398 | 0.9541 | 0.9524 | 0.9533 | 0.3723 | 0.8399 | ||

| 94 | 0.6459 | 0.9535 | 0.9518 | 0.9526 | 0.3762 | 0.8399 | ||

| 95 | 0.6398 | 0.9541 | 0.9524 | 0.9533 | 0.3721 | 0.8400 | ||

| 96 | 0.6466 | 0.9545 | 0.9529 | 0.9537 | 0.3763 | 0.8407 | ||

| 97 | 0.6396 | 0.9542 | 0.9526 | 0.9534 | 0.3720 | 0.8407 | ||

| 98 | 0.6461 | 0.9545 | 0.9529 | 0.9537 | 0.3757 | 0.8404 | ||

| 99 | 0.6393 | 0.9539 | 0.9523 | 0.9531 | 0.3719 | 0.8412 | ||

| 100 | 0.6458 | 0.9541 | 0.9525 | 0.9533 | 0.3759 | 0.8422 |