On stochastic integrals with controlled growth of their containing range

Nikolai Dokuchaev

Department of Mathematics & Statistics,

Curtin University,

GPO Box U1987, Perth, 6845 Western Australia

Abstract

This short note suggests special examples of stochastic Itô integrals with controlled growth of their containing range. The integrands for this integrals are presented

explicitly. The construction does not involve neither stopping times nor forecasting or calculation of the conditional expectations of a contingent claim.

Key words: stochastic integrals, Itô calculus, containing range

The paper considers stochastic processes represented as stochastic Itô integrals (possibly, with a drift term). Usually, these integrals have unlimited range of possible values.

However, there are special cases of integrals with limited range. These integrals can be obtained, for instance, as conditional expectations of random variables with

limited range, or via restriction of the integration interval by a random Markov stopping times preventing the range growth. These approaches may be inconvenient in some cases.

For example, calculation of a condition expectation is essentially a forecast of a contingent claim depending on the future values, and this procedure can be difficult.

Besides, one would need to specify first this contingent claims. On the other hand, restriction of the integration interval by stopping times

leads to stochastic integrals with some paths being frozen at that stopping times. Obviously, this feature could be undesirable.

The present paper suggests special examples of stochastic Itô integrals with controlled growth of their containing range. The integrands for this integrals are presented

explicitly. The paper uses an original approach does not involve neither stopping times nor forecasting or calculation of the conditional expectations of a contingent claim. This approach does not involve neither forecasting nor calculation of the conditional expectations of a contingent claim.

2 The main result

We are also given a standard complete probability space and a

right-continuous filtration of complete -algebras of

events. In addition, we are given an one-dimensional Wiener

process , that is a Wiener

process adapted to and such that and that is independent from if .

Consider a continuous time one-dimensional random

process

such that

Here and are bounded real-valued one-dimensional -adapted processes.

Let be a real valued random -adapted process

that is integrable on any finite time interval. For simplicity, we assume that for any .

Let be the filtration of complete -algebras of

events generated by the process .

It can be noted that, since the process is adapted

to the filtration generated by , it follows that is also the filtration generated by the process ; see e.g. Remark 1.1 in [5], p.10, or

Proposition 7.1 in [9], where this was shown for a log-normal types

of processes which was rather technical.

Theorem 2.1

Consider processes and defined for as

(1)

and

(2)

In this case,

(3)

Then

Clearly, the process is bounded uniformly in all almost surely on any finite time interval and -adapted. Hence the stochastic integral (1)

is well defined and is bounded uniformly in all almost surely on any finite time interval.

Representation (2) in Theorem 2.1 implies that the boundaries for the range of the stochastic integral are defined by the choice of the process .

Respectively, Theorem 2.1 allows to construct stochastic processes with preselected on a given time interval

time depending boundaries for their range.

Proof of Theorem 2.1 follows from this and

from (5).

Remark 2.3

Consider the case where .

In this case, it follows from the proof above that, for any -adapted

process , there exists a -adapted process such that

and that

the integral

has a limited range in . To see this, it suffices to

select and observe that and that

3 Some modifications

The approach demonstrated above allows many modifications.

Let us provide one of possible modifications,

Theorem 3.1

Consider a process defined as

(6)

where . Further, let a process be defined as the stochastic integral

(7)

Then can be represented as

(8)

Clearly, the process is bounded uniformly in all almost surely on any finite time interval and -adapted. Hence the stochastic integral (7)

is well defined.

Representation (8) in Theorem 3.1 implies that the boundaries for the range of the stochastic integral are defined by the choice of the process .

Respectively, Theorem 3.1 allows to construct stochastic processes with preselected on a given time interval

time depending boundaries for their range.

Corollary 3.2

Let be fixed, and let be a integrable function.

Let .

Then

Proof of Lemma 3.1.

Let be defined as the solution of the Itô equation

By the Itô formula,

In particular, we have that

Direct differentiation gives that

Hence

Let and . We have that

It follows that

where . We have that

Hence for any and .

Then the proof of Lemma follows.

The proof of Theorem 3.1 follows from the lemma. The proof of Corollary

3.2 follows from the theorem applied to the corresponding choice of .

Remark 3.5

For the case where ,

similarly Remark 2.3, it can be shown that, that, for any -adapted

process , there exists a -adapted process such that

and that

the integral

has a limited range in . To see this, it suffices to

select and observe that .

4 Possible applications for financial modelling

One of core problem of financial mathematics is the portfolio selection problem.

Application of classical methods of optimal stochastic control for portfolio optimization problems

requires

forecasting of market parameters.

This forecasting is usually difficult.

This problem is related to the open problem of

validation of the so-called technical analysis methods that offer trading

strategies based on historical observations. There are many

different strategies suggested in this framework (see, e.g., [1, 2, 4, 14, 15, 5, 6]

and the references therein. It is

known that mean-reverting market models and market models with bounded range

for the prices generate

some special speculative

opportunities (see, e.g., [3, 4, 7, 8, 10, 13, 16, 17, 18]).

Theorems 2.1-3.1 give a possibility to convert a stock price process

into a processes or that could have features similar to mean-reverting market models and market models with bounded range for the prices.

For this new artificial asset, one can apply strategies from [3, 4, 7, 8, 10, 13].

We leave this for the future research.

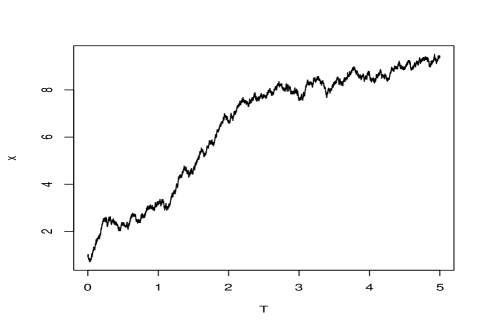

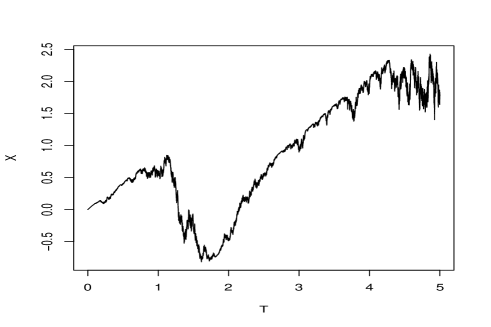

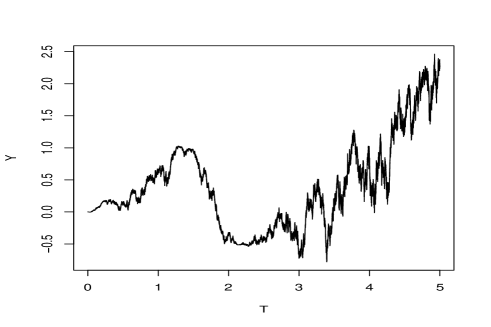

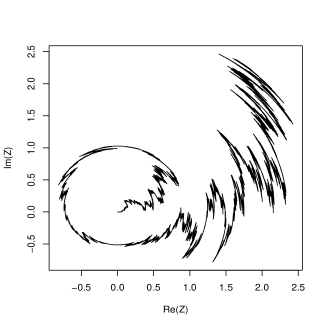

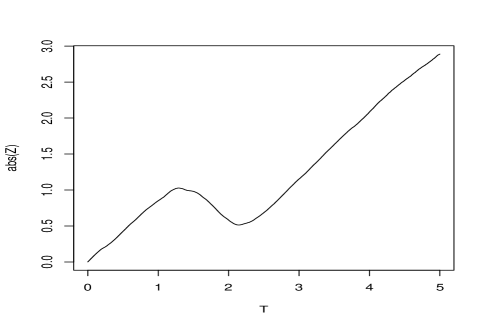

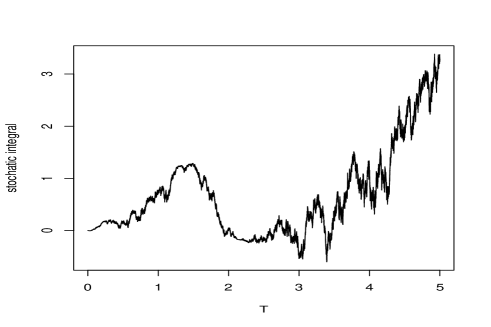

Figures 3-6 shows sample paths of processes

introduced above and obtained via Monte-Carlo simulation

under the assumption that , , , and .

We used natural discretization in time with grid point on the interval .

Calculations were executed using R and RStudio programms.

Figure 1: .

Figure 2: .

Figure 3: .

Figure 4: .

Figure 5: .

Figure 6: .

References

[1]

Barmish, B. Ross, Primbs, A. (2016)

On a new paradigm for stock trading via a model-free feedback controller.

IEEE Transactions on Automatic Control. 61 (3), 662–676.

[2]

Baumann M.H., Grüne, L. (2017)

Simultaneously long short trading in discrete and continuous time.

Systems & Control Letters 99, 85-99.

[3]

Carcanoa, G., Falbo, P. , and S. Stefania. (2005)

Speculative trading in mean reverting markets. European

Journal of Operational Research163, iss. 1, 132–144.

[5]

Dokuchaev, N.G. (2002) Dynamic portfolio strategies:

quantitative methods and empirical rules for incomplete

information. Boston: Kluwer Academic Publishers.

[6]

Dokuchaev, N.G., and A. Savkin (2004) Universal strategies for

diffusion markets

and possibility of

asymptotic arbitrage. Insurance: Mathematics and Economics34, 409-419.

[7]

Dokuchaev, N.G. (2006) Speculative opportunities for currency

exchange under soft peg. Applied Financial Economics Letters2, 371-374.

[9]

Dokuchaev, N. (2007), Mathematical Finance: Core Theory, Problems, and Statistical Algorithms, London: Routledge

[10] Dokuchaev, N. (2012). Mean-reverting discrete time market models:

speculative opportunities and

absence of arbitrage. IMA Journal of Management Mathematics23, 17-27.

[11]

Dokuchaev, N. (2014). Volatility estimation from short time series of stock prices. Journal of Nonparametric Statistics26 (2), pp. 373–384.

[12]

Dokuchaev, N. A pathwise inference method for the parameters of diffusion terms.

Journal of Nonparametric Statistics. In press; accepted 23.06.2017.

[13]

Falbo, P., Frittelli, M., and S. Stefani. (1999) Profitable decision

rules in mean reverting markets, Rapporti di Ricerca del

Dipartimento di Metodi Quantitativi dell’Universit di Brescia, No.

162. Brescia, Italy.

[14]

Hsu, P.-H., and C.-M. Kuan. (2005) Reexaming the profitability of

thechnical analysis with data snooping checks. Journal of

Financial Econometrics3, iss. 4, 606-628.

[15] Hsu, P.-H., M. P. Taylor, Z. Wang. (2016)

Technical trading: Is it still beating the foreign exchange market?

Journal of International Economics 102 188 208

Lo et al [2000]

Lo, A.W., Mamaysky, H., and Wang, Jiang. (2000).

Foundation of technical analysis: computational algorithms,

statistical inference, and empirical implementation. Journal

of Finance55 (4), 1705-1765.

Lorenzoni et al [2007]

Lorenzoni, G., Pizzinga, A., Atherino, R.,

Fernandes, C,, Freire, R.R.. (2007). On the Statistical Validation of

Technical Analysis. Revista Brasileira de Finanças. Vol.

5, No. 1, pp. 1-28.

.

Shiryaev [1999]

Shiryaev, A.N. (1999) Essentials of Stochastic Finance. Facts,

Models, Theory. World Scientific Publishing Co., NJ, 1999.