Statistical estimation of the Oscillating Brownian Motion

Abstract

We study the asymptotic behavior of estimators of a two-valued, discontinuous diffusion coefficient in a Stochastic Differential Equation, called an Oscillating Brownian Motion. Using the relation of the latter process with the Skew Brownian Motion, we propose two natural consistent estimators, which are variants of the integrated volatility estimator and take the occupation times into account. We show the stable convergence of the renormalized errors’ estimations toward some Gaussian mixture, possibly corrected by a term that depends on the local time. These limits stem from the lack of ergodicity as well as the behavior of the local time at zero of the process. We test both estimators on simulated processes, finding a complete agreement with the theoretical predictions.

Keywords: Oscillating Brownian Motion, Gaussian mixture, local time, occupation time, Arcsine distribution, Skew Brownian Motion

1 Introduction

Diffusion processes with discontinuous coefficients attract more and more attention for simulation and modelling purposes (see references in [23]). Many domains are actually concerned, such as geophysics [31], population ecology [5, 4], finance [6, 28], … among others. From a theoretical point of view, diffusions with discontinuous coefficients are an instance of Stochastic Differential Equations (SDE) with local time — also called skew diffusion — for which many results are contained in the work of J.-F. Le Gall [20].

Estimation come together with simulation and modelling, as models need to be calibrated. This article deals with the parametric estimation of the coefficients of a one-dimensional SDE of type

| (1.1) |

where is a Brownian motion and takes two values according to the sign of , when the process is observed at discrete times , up to a time . In a first part, we consider that (1.1) contains no drift (). The solution to (1.1) is called an Oscillating Brownian Motion (OBM). This process was studied by J. Keilson and J.A. Wellner in [18] who give some of its main properties and close form expressions for its density and occupation time.

We provide two very simple estimators which generalize the integrated volatility (or averaged squared) estimator (in finance, is called the volatility when represents the logarithm of the price of an asset). For two processes , we set

with . The quantity is an approximation of the occupation time of on the positive axis up to time . Our estimator of is then , where is the positive part of . A similar estimator is defined for . Although an analytic form is known for the density, this estimator is simpler to implement than the Maximum Likelihood Estimator. Besides, it also applies when , while explicit expressions for the density become cumbersome, at best [21, 29].

We show first that is a consistent estimator of . Yet it is asymptotically biased. We also prove that converges stably to a mixture of Gaussian distributions (in which, unsurprisingly, the occupation time of the positive side appears) plus an explicit term giving the bias.

When estimating , the actual size of the “useful” sample is proportional to the occupation time of . Therefore, a dependence on the occupation time is to be expected in any reasonable estimator. The law of the occupation time for the OBM follows an arcsine type distribution, which generalizes the one of the Brownian motion. Since these laws carry much mass close to the extremes, this amounts to say that many trajectories of this process spend most of the time on the same side of . Therefore, with a high probability, either or is only based on few observations. This affects our central limit theorem as well as the quality of the estimation of , meaning that the limit law will not be a Gaussian one, as one would expect from the approximation of quadratic variation, but a Gaussian mixture displaying heavy tails.

Another tool of importance in this framework, strictly connected with the occupation time, is the local time. Given a stochastic process , its local time at a point , denoted by , represents the time spent by at , properly re-scaled. It has a fundamental role in the study of SDEs with discontinuous coefficients. Intuitively, the local time appears when dealing with discontinuous coefficients because it helps to quantify what happens locally at the discontinuity. A Lamperti’s type transform applied with the help of the Itô-Tanaka formula shows that is intimately related to the Skew Brownian Motion (SBM, see [10, 24]) , the solution to the SDE

In the present paper, the local time plays an important role for two reasons. First, because we use the transform to apply some convergence results which extend to the SBM some results of J. Jacod on the asymptotic behavior of quantities of type . Second, because the local time itself appears in the limit of the above quantities. Actually, the asymptotic bias is related to the local time.

We then provide a second simple estimator of , defined as which is also consistent. We show that converges stably to a Gaussian mixture. The asymptotic bias observed in is removed through the introduction of the quadratic term which is related to the local time. The variance of the former limit is not larger than the one of the latter.

In Corollary 3.8, we also generalize these convergence results in presence of a bounded drift term. We prove that the estimators mentioned above converge to analogous limit random variables, depending on the occupation time of the SDE under study. Unlike for the OBM, the limit law is not explicit for SDEs with general drift, since the law of the occupation time is not know, if not in special cases (see e.g. [37, 38, 17]).

The novelty of the paper lies in the treatment of a discontinuous diffusion coefficient. This implies a drastic difference with the case of regular coefficients, as the situation cannot be reduced to a Brownian one (the measure of the SBM being singular with respect to the one of the Brownian motion [20]). This explains the presence of an asymptotic bias for , which is removed by a correction (leading to ) which involves only a fraction of order of the observations.

Besides, the framework is not the one of ergodic processes, like for many estimators, but of null recurrent ones. On the last point, our study does not fit the situations considered e.g., in [11, 12, 1].

With respect to many estimators constructed for diffusion processes, the lack of ergodicity of the process explains the presence of a mixed normal distribution in the limit. For diffusions, asymptotic convergence involving a mixture of normal distributions (with different type of limits) is already observed in the works of F. Florens-Zmirou [9] for non-parametric estimation, and of J. Jacod [15, 14], from which we borrow and adapt the general treatment. The core of our proof requires the adaptation to the SBM of some results on the convergence toward the local time given in [14].

Content of the paper

In Section 2 we define the Oscillating Brownian Motion (OBM) and recall some useful properties. In Section 3 we define our estimators and state precisely the convergence theorems. These results are then proved is Section 4. In Section 5 we consider the Oscillating Random Walk, a discrete process that can be used to construct the OBM, and study an estimator on this discrete process. Section 6 is devoted to the implementation of the estimators of the OBM, and contains numerical experiments showing the good behavior of the estimators in practice.

Notations

For notational convenience, we work on the time interval . Our results can be extended to a general time interval via a space-time re-scaling (see Remark 3.7). Throughout the paper, we use the following notation for convergence of random variables: in probability; in law; stable in law; denotes equality in law. The Lebesgue measure is written . The positive and negative parts of are denoted by , . For any continuous semimartingale , we write for its quadratic variation process. For we define the (symmetric) local time of at as the process , with (See [33, Corollary VI.1.9, p. 227])

When we do not specify , we mean the local time at : .

For fixed , we consider the discretization of given by . For any process , we write . For any processes we also set the “discrete bracket”

We also write .

2 Oscillating Brownian Motion

For two parameters , we define the diffusion coefficient as follows:

| (2.1) |

Let be a Brownian motion with its (completed) natural filtration on a probability space . From now on, we denote by the unique strong solution to

| (2.2) |

Strong existence and uniqueness of is granted by the results of [20]. Following the terminology of [18], we call an Oscillating Brownian Motion (OBM)

We recall some known properties of , proved in [18].

For , let be the density of in , with initial condition . In [18] explicit formulas for the transition density are given. In particular, when ,

Integrating the previous equations we obtain

| (2.3) |

where is the cumulative density function of the standard Gaussian. The law of the occupation time of is also computed in [18]. Let the occupation time of be defined as

| (2.4) |

The distribution of , with a.s., is explicit. The scaling holds, and

| (2.5) |

This generalizes the arcsine law for the occupation time of the Brownian Motion. The occupation time on is easily computed from since obviously, for any .

We introduce the process , setting for . It follows from the Itô-Tanaka formula that is a Skew Brownian Motion (SBM, see [24]), meaning that satisfies the following SDE:

| (2.6) |

where is a Brownian Motion, is the symmetric local time of at , and the coefficient is given by

| (2.7) |

We write from now on BM for Brownian Motion, SBM for Skew Brownian Motion, OBM for Oscillating Brownian Motion. The local times of and are related by

| (2.8) |

(see [24] for a special case from which we easily recover this formula).

3 Main results

3.1 The stable convergence

Before stating our results, we need to recall the notion of stable convergence, which was introduced by A. Rényi [32]. We refer to [16] or [15] for a detailed exposition. Let a sequence of -valued random variables defined on the same probability space . Let be an -valued random variable defined on an extension, . We then say that converges stably to (and write ) if:

for all bounded continuous functions on and all bounded random variables Y on (or, equivalently, for all as above and all functions which are bounded and Lipschitz). This notion of convergence is stronger than convergence in law, but weaker than convergence in probability. We use in this paper the following crucial result: for random variables , (), and ,

3.2 Estimators for the parameters the Oscillating Brownian motion

Let us assume that we observe the process solution to (2.2) at the discrete times . We want to estimate from these observations.

A natural estimator for the occupation time defined in (2.4) is given by the Riemann sums (see Section 4.4):

| (3.1) |

We define now as

| (3.2) |

which we show to be a consistent estimator for . Similarly, we set

Finally, we define our estimator of the vector as

Theorem 3.1.

Let be solution of (2.2) with a.s., and defined in (3.2). Then

-

(i)

The estimator is consistent:

-

(ii)

There exists an extension of carrying a Brownian motion independent from such that

(3.3) The stable limit in the above result depends on the path of through its local time and its occupation time . By identifying the distribution of the limit, we can rewrite (3.3) as a convergence in distribution involving elementary random variables as

(3.4) where , are mutually independent, , and follows the modified arcsine law (2.5) with density

Remark 3.2.

Remark 3.3.

Remark 3.4.

We assume a.s. because we need to visit both and . This happens a.s. in any right neighborhood of if the diffusion starts from . If the initial condition is not , we shall wait for the first time at which the process reaches , say , and consider the (random) interval .

We define now a different estimator for by

| (3.5) |

Theorem 3.5.

Let be solution of (2.2) with a.s., and defined in (3.5). The following convergence holds for :

where is a BM independent of on an extension of . We can rewrite such convergence as follows:

| (3.6) |

where are mutually independent, and follows the modified arcsine law with density given by (2.5), with .

Remark 3.6.

Comparing Theorems 3.1 and 3.5, we see that an asymptotic bias is present in , but not in . This bias has the same order ( as the “natural fluctuations” of the estimator. Because the local time is positive, it is more likely that underestimates . For a more quantitative comparison between the convergence of the two estimators, see Remark 4.18. In Section 6, we compare the two estimators in practice.

Remark 3.7.

Theorem 3.5 gives the asymptotic behavior for an estimator of in the presence of high frequency data, yet with fixed time horizon . The OBM enjoys a scaling property: if is an OBM issued from , then is an OBM issued form , for any constant (see [33, Exercise IX.1.17, p. 374]). Using this fact, we can easily generalize Theorem 3.5 to the case of data on a time interval for some fixed . We set

| (3.7) |

The estimator is consistent and we have the following convergence:

where is a BM independent of on an extension of the underlying probability space. The limiting random variable follows the law given in (3.6), which actually does not depend on .

A slightly different approach is to imagine that our data are not in high frequency, but that we observe the process at regular time intervals, for a long time. In this case it is more reasonable to consider an OBM , construct an estimator depending on , and then take the limit in long time. We set

Using again Theorem 3.5 and the diffusive scaling of the OBM, we have the following convergence:

The limit distribution is again the law given in (3.6). Theorem (3.1) can also be generalized to high frequency data on an interval and to equally spaced data in long time, using the diffusive scaling and (4.19)-(4.20). For example, analogously to (3.7), we define

Again, the limit law does not change and is the one given in (3.4).

3.3 A generalization to OBM with drift

We consider now a wider class of processes, adding a drift term to equation (2.2). Formally, let now be the strong solution to

| (3.8) |

with , defined in (2.1) and measurable and bounded. Again, strong existence and uniqueness of the solution to (3.8) is ensured by the results of [20].

Corollary 3.8.

The following convergence holds for :

where is a BM independent of on an extension of the underlying probability space. We can rewrite such convergence as follows:

where are mutually independent, and .

Remark 3.9.

Unlike for the OBM, the limit law is not explicit in Corollary 3.8, since the law of the occupation time of the positive axes is not know in general (See e.g., [19, 37, 17, 38]). On the other hand, some information on the law of can be obtained, at least in some special cases, via Laplace transform.

We also stress that this dependence on the occupation time is due the actual sample size of the data giving us useful information. Indeed, when estimating , the number of intervals that we can use is proportional to the occupation time of . Analogously for the negative part.

Remark 3.10.

Remark 3.11.

The scaling property described in Remark 3.7 no longer holds in this situation, so that the estimator can only be used in the “high frequency” setting.

4 Proofs of the convergence theorem

This section is devoted to the proof Theorems 3.1 and 3.5. We first deal with some general approximation results which are well known for diffusions with regular coefficients (see [14, 15, 16]), but not for the framework considered here with discontinuous coefficients (when , the law of the SBM is singular with respect to the one of the BM [20]).

Following [26, 8], we use the connection between the OBM and the SBM through a Lamperti-type transform. Hence, we apply the results of [22] to the convergence of estimators of quadratic variation, covariation and occupation time for these processes. Finally, we use all these results to prove the main Theorems 3.1 and 3.5.

4.1 Approximation results

Let us write

for the Lebesgue integral of a function. In [22], the following approximation result, borrowed from [14], is proved for the SBM solution of (2.6).

Lemma 4.1.

Let be a bounded function such that for and be a SBM of parameter (i.e., the solution to (2.6)). Then for any ,

where is the symmetric local time at of the SBM and

| (4.1) |

Remark 4.2.

In particular, when , is BM and the coefficient in front of the local time is simply . We recover there a special case of a theorem by J. Jacod (see [14], Theorem 4.1).

We prove now an approximation result for the OBM.

Lemma 4.3.

Let be the OBM in (2.2). Let be a bounded function such that for . Then for any ,

where is the local time of and

Proof.

We state now a very special case of Theorem 3.2 in [13], that we apply several times in this work. The version in [13] holds for semimartingales, not only martingales, the processes involved can be multi-dimensional, and the limit process is not necessarily . Anyways, we do not need this general framework here. Stating the theorem only for one-dimensional martingales converging to allows us to keep a simpler notation, which we introduce now: for each càdlàg process we write . Consider a filtered probability space carrying a Brownian motion . The filtration is the natural (completed) one for the Brownian motion. We define the filtration as the “discretization” defined by . We consider a -martingale in , i.e., a process of the form

where each is measurable, square-integrable, and .

Theorem 4.4 (Simplified form of Theorem 3.2 in [13]).

Suppose that

| (4.2) | |||

| (4.3) |

Then converges to in probability as .

Remark 4.5.

In [13] some kind of uniform integrability is assumed in the limit, whereas here we do not ask explicitly for such a condition. The reason is that the uniform integrability assumption is implied by the fact that the limit in (4.2) is .

It is also required that converges to for any bounded martingale orthogonal to on . As we have considered the Brownian motion with its natural (completed) filtration, this set is reduced to the constant ones.

4.2 Scaled quadratic variation of Brownian local time

Let be a BM and its local time at . Let us recall the diffusive scaling property for any (see e.g. [33, Exercise 2.11, p. 244]).

Let be the natural (completed) filtration of .

For , we write .

Lemma 4.6.

Let be the Brownian local time at . The following convergence holds:

We split the proof of this result in the next tree lemmas. We start with the explicit computations on the moments of the Brownian local time.

Lemma 4.7.

For , we set . We have

| (4.4) |

where denotes a standard Gaussian random variable. Besides, the following tail estimates hold for :

| (4.5) |

Remark 4.8.

Proof.

Formula (6) in [35] gives the following expression for the moments of the Brownian local time

To apply Remark 4.2 we need to compute the following integral

Changing the order of integration by Fubini-Tonelli’s theorem,

so (4.4) is proved. We now use the following bound for Gaussian tails: . We apply it twice and find the upper bound for :

For we apply the same inequality:

Now, since for all ,

Hence the result. ∎

We consider now the quadratic sum in Lemma 4.6, and write

In the next two lemmas we prove the convergence of the two summands. Lemma 4.6 follows directly.

Lemma 4.9.

Let be the Brownian local time at . The following convergence holds:

Proof.

We consider now the martingale part.

Lemma 4.10.

With

it holds that .

4.3 Scaled quadratic covariation of skew Brownian motion and its local time

We now give some results on the scaled quadratic covariation between the SBM and its local time. For the Brownian motion with the filtration of Section 2, we consider the strong solution to for and its local time (apart from the results in [20], strong existence for the SBM has been proved first in [10]).

Lemma 4.11.

For and as above, the following convergence holds:

| (4.7) | |||

| (4.8) | |||

| (4.9) |

We set

| (4.10) |

and write

We prove (4.7) in the next two lemmas. Once (4.7) is proved, (4.8) follows since is a SBM with parameter , while (4.9) follows from a combination of (4.7) and (4.8) since .

Lemma 4.12.

With defined in (4.10), the following convergence holds:

| (4.11) |

Proof.

Lemma 4.13.

With defined by (4.10), the following convergence holds:

4.4 Approximation of occupation time

In this section we extend the result in [30], which is proved for diffusions with smooth coefficients, to the OBM. We consider approximating the occupation time of up to time :

As previously, we suppose that we know the values of on a grid of time lag .

For , we consider

| (4.12) |

The are martingale increments. We write

In the following lemmas we prove the convergence of the two summands.

Remark 4.15.

In [30] it is proved that the estimator times is tight, so the speed of convergence proved there, holding only for smooth coefficients, is faster than the speed proved here. We are actually able to prove that is the speed of convergence for the martingale part also for the OBM (and other diffusions with discontinuous coefficients), but not for the drift part . We would need the central limit theorem giving the speed of convergence corresponding to the law of large numbers proved in Lemma (4.3), but this looks quite hard to get in the case of discontinuous diffusion coefficients. Anyways, for our goal of estimating the parameters of the OBM, the fact that our estimator multiplied with the “diffusive scaling” converges to is enough. Actually, this result depends on a compensation between two terms in Lemma 4.16 which holds for this particular diffusion but for which we do not have results holding for a wider class of SDEs with discontinuous coefficients.

Lemma 4.16.

With defined by (4.12), the following convergence holds:

Proof.

Lemma 4.17.

With defined by (4.12), the following convergence holds:

4.5 Proof of the main results

Proof of Theorem 3.1.

We set

Itô-Tanaka’s formula (see [33]) gives the following equation for the positive and negative part of :

| (4.13) |

Moreover, is a martingale with quadratic variation

It is well known that the quadratic variation of a martingale can be approximated with the sum of squared increments over shrinking partitions. Thus,

| (4.14) |

From (4.13),

The local time is of finite variation, is continuous. Thus as well as converge to almost surely. From (4.14),

| (4.15) |

Recall the definition of in (3.1). Then

From (4.15) and (4.5), , and similarly . Therefore, the vector converges in probability to . The estimator is then consistent.

We consider now the rate of convergence. From (4.13) applied to , we have as in (4.5) that

We consider separately the tree summands. From the central limit theorem for martingales (see for example [15], (5.4.3) or Theorem 5.4.2), since ,

where is a Brownian motion independent of the filtration of . Therefore it is also independent of . Consider now the second summand. The OBM is linked to a SBM solution to (2.6) through . With (2.8) and (4.9) in Lemma 4.11,

Clearly this also holds for , and we obtain the convergence in probability of to .

We use Lemma 4.6 for dealing with the third summand:

| (4.16) |

We obtain, using (3.1),

| (4.17) |

We write now

Recall that and converge almost surely to and . Besides, a.s., because . Therefore, from Theorem 4.14,

| (4.18) |

The statement is now proved, but we would like to get a more explicit expression for the law of the limit random variable. Recall . From Corollary 1.2 in [2], standard computations give that the joint density of is, for , :

We set now

Changing variable in the integration, the joint density of is

| (4.19) |

We also find the joint density of as

| (4.20) |

As we can factorize , and are independent and their laws are explicit. In particular from (2.5), for , ,

and

Let now be a random variable with the same law of , and let be an independent exponential random variable of parameter . From (4.19), (4.20)

Moreover,

where are standard Gaussian random variables independent of and . Therefore the limit law has the expression given in the statement. ∎

Proof of Theorem 3.5.

Using (4.13), we obtain

From the Central Limit Theorem for martingales [15, Theorem 5.4.2] and ,

where is another BM independent of the filtration of . Both and are defined on an extension of with where carries the BM . Moreover,

so because of Lemma 4.11. Finally,

This is the analogous of (4.17) in the proof of Theorem 3.1. From now on the proof follows as in Theorem 3.1, but without the local time part. ∎

Remark 4.18.

We look for the origin of the asymptotic bias present in , but not in . Consider first the difference between the approximation of quadratic variation used in the two different estimators:

From (4.13),

From the central limit theorem for martingales [15, Theorem 5.4.2],

Since converges in probability to , using (4.16) we obtain

| (4.21) |

We then see that the asymptotic bias in is related to the bracket .

4.6 Proof of Corollary 3.8: adding a drift term via Girsanov Theorem

Let us start with a remark on the stability of the stable convergence under a Girsanov transform.

Lemma 4.19.

For two probability spaces and , let us define an extension by of of the form

Assume that and carry respectively Brownian motions and with natural (completed) filtrations and . Assume also that and are independent.

On , let be an exponential -martingale which is uniformly integrable. Let be the measure such that .

Suppose now that a sequence on of -measurable random variables converges stably to a random variable on the extension of where and are -random variables on .

Then converges stably to on where is a Brownian motion independent from and (the laws of and are of course changed).

Proof.

Let us write . The Girsanov weight is -measurable and integrable with respect to . Hence, it is easily shown that for any bounded, -measurable random variable and any bounded, continuous function , converges to .

Under , as and are independent and the bracket does not change under a Girsanov transform. This implies that is still a Brownian motion under . Hence the result. ∎

Proof of Corollary 3.8.

Let be solution to with an underlying Brownian motion on . We denote by the filtration of . Thus, is an OBM.

The Girsanov theorem is still valid for discontinuous coefficients [20]. Let us set

Since is bounded, we define a new measure by . Under , the process is solution to for a Brownian motion , .

5 Oscillating Random Walk

In [18] the OBM is constructed also as a limit of discrete processes, called Oscillating Random Walks (ORW), analogously to how the BM is constructed as a limit of Random Walks. The aim of this section is to examplify the phenomena of dependence on the occupation of the limit law, in a simpler framework and with a non-technical proof.

We define the ORW as the following process. Fix . For , we introduce the following random variables:

Now we set and

We consider the re-normalized process

For all , we have the following convergence:

The convergence in probability holds if the processes are constructed as in [34], and is an OBM of parameters , . This means that in this setting we have , but we do not loose in generality because we can always re-scale time and space.

In this appendix, we recover from the observations of for some large an estimator for the parameters of the OBM.

We set , , and introduce the following estimator of :

| (5.1) |

Theorem 5.1.

Let be the estimator defined above. The following convergence holds:

where follows the law in (2.5), is a standard Gaussian and they are independent.

Proof.

When , with probability , and with probability . We can compute the log-likelihood and maximize it as in the statistics of Binomial variables, finding that the maximum likelihood estimator for is in (5.1). In [18] it is proved that

where follows the law in (2.5). This easily implies

| (5.2) |

Conditioning to , we have that follows is a binomial distribution with parameters . We write the event

From Berry-Essen inequality [3, 7], we have

for some constant . Now, from (5.2) and Portmanteau Lemma,

Moreover, . Recalling

we obtain the following convergence

which implies the statement. ∎

6 Empirical evidence

In this section we implement estimators and use them on simulated data. For doing so, we reduce the OBM (2.2) to a SBM (2.6), and we simulate it through the simulation method given in [23]. This method gives the successive positions of the SBM, hence the OBM, on a time grid of size .

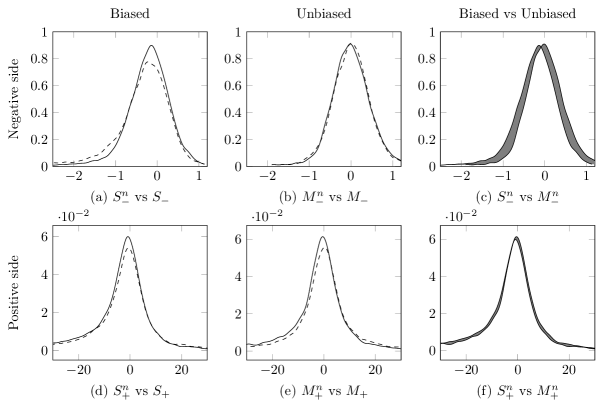

Recall Remark 3.7, in particular estimators , for which we have central limit theorems with the same limit laws of (3.4), (3.6). We use the parameters: , (thus ), , (so that in (2.6), pushing the process to the negative side). In Figure 1, we plot the density of

for realizations of these estimators (meaning the simulation of paths of the OBM). Their empirical densities are compared with the ones of

given in (3.6) and (3.4), with and . The densities of and (which do not depend on ) are obtained by simulation. The occupation time is simulated by inverting its distribution function [19, 25]:

(a), (d) normalized error of the estimators (solid line) and theoretical limits (dashed lines);

(b), (e) normalized error of the estimators (solid line) and theoretical limits (dashed lines);

(c), (f) normalized error of the estimators and normalized error of the estimators .

We see that the limit distribution on the positive side has a larger variance than the one in the negative side. This is due to the sample size, proportional to the occupation time, which is on average larger on the side where the diffusion coefficient is smaller. We also obtain a good agreement of the normalized empirical error with the prediction of the central limit theorem. On the pictures on the right, we observe the difference between biased and non-biased estimator; the grey area is the effect given by the shift to the left of the distribution, caused by the local time term. This shift is more visible when the diffusion coefficient is smaller.

We have also checked that has a distribution close to the one of , which is straightforward since the density of is known (for this, we use P. Lévy’s identity which relates the local time to the supremum of the Brownian motion whose density is explicitly known). The agreement is good.

Finally, the same simulation work can be done using the random walks defined in Section 5 using the simple approach. Again, the numerical results are in good agreements with the theory, although some instabilities appear due to the fact that the occupation time may take small values with high probability.

References

- [1] R. Altmeyer and J. Chorowski. Estimation error for occupation time functionals of stationary Markov processes. ArXiv e-prints, October 2016.

- [2] T. Appuhamillage, V. Bokil, E. Thomann, E. Waymire, and B. Wood. Occupation and local times for skew Brownian motion with applications to dispersion across an interface. Ann. Appl. Probab., 21(1):183–214, 2011.

- [3] Andrew C. Berry. The accuracy of the Gaussian approximation to the sum of independent variates. Trans. Amer. Math. Soc., 49:122–136, 1941.

- [4] R S Cantrell and C Cosner. Diffusion Models for Population Dynamics Incorporating Individual Behavior at Boundaries: Applications to Refuge Design. Theoretical Population Biology, 55(2):189–207, 1999.

- [5] R.S. Cantrell and C. Cosner. Skew Brownian motion: a model for diffusion with interfaces? In Proceedings of the International Conference on Mathematical Models in the Medical and Health Sciences, pages 73–78. Vanderbilt University Press, 1998.

- [6] Marc Decamps, Marc Goovaerts, and Wim Schoutens. Self exciting threshold interest rates models. Int. J. Theor. Appl. Finance, 9(7):1093–1122, 2006.

- [7] Carl-Gustav Esseen. On the Liapounoff limit of error in the theory of probability. Ark. Mat. Astr. Fys., 28A(9):19, 1942.

- [8] Pierre Étoré. On random walk simulation of one-dimensional diffusion processes with discontinuous coefficients. Electron. J. Probab., 11:no. 9, 249–275 (electronic), 2006.

- [9] Daniéle Florens-Zmirou. On estimating the diffusion coefficient from discrete observations. J. Appl. Probab., 30(4):790–804, 1993.

- [10] J. M. Harrison and L. A. Shepp. On skew Brownian motion. Ann. Probab., 9(2):309–313, 1981.

- [11] R. Höpfner and E. Löcherbach. Limit theorems for null recurrent Markov processes. Mem. Amer. Math. Soc., 161(768), 2003.

- [12] Reinhard Höpfner. Asymptotic statistics. De Gruyter Graduate. De Gruyter, Berlin, 2014. With a view to stochastic processes.

- [13] Jean Jacod. On continuous conditional Gaussian martingales and stable convergence in law. In Séminaire de Probabilités, XXXI, volume 1655 of Lecture Notes in Math., pages 232–246. Springer, Berlin, 1997.

- [14] Jean Jacod. Rates of convergence to the local time of a diffusion. Ann. Inst. H. Poincaré Probab. Statist., 34(4):505–544, 1998.

- [15] Jean Jacod and Philip Protter. Discretization of processes, volume 67 of Stochastic Modelling and Applied Probability. Springer, Heidelberg, 2012.

- [16] Jean Jacod and Albert N. Shiryaev. Limit theorems for stochastic processes, volume 288 of Grundlehren der Mathematischen Wissenschaften. Springer-Verlag, Berlin, second edition, 2003.

- [17] Yuji Kasahara and Yuko Yano. On a generalized arc-sine law for one-dimensional diffusion processes. Osaka J. Math., 42(1):1–10, 2005.

- [18] Julian Keilson and Jon A. Wellner. Oscillating Brownian motion. J. Appl. Probability, 15(2):300–310, 1978.

- [19] John Lamperti. An occupation time theorem for a class of stochastic processes. Trans. Amer. Math. Soc., 88:380–387, 1958.

- [20] J.-F. Le Gall. One-dimensional stochastic differential equations involving the local times of the unknown process. Stochastic Analysis. Lecture Notes Math., 1095:51–82, 1985.

- [21] A. Lejay, Lenôtre, and G. Pichot. One-dimensional skew diffusions: explicit expressions of densities and resolvent kernel, 2015. Preprint.

- [22] A. Lejay, E. Mordecki, and S. Torres. Convergence of estimators for the skew Brownian motion with application to maximum likelihood estimation, 2017. In preparation.

- [23] A. Lejay and G. Pichot. Simulating diffusion processes in discontinuous media: a numerical scheme with constant time steps. Journal of Computational Physics, 231:7299–7314, 2012.

- [24] Antoine Lejay. On the constructions of the skew Brownian motion. Probab. Surv., 3:413–466, 2006.

- [25] Antoine Lejay. Simulation of a stochastic process in a discontinuous layered medium. Electron. Commun. Probab., 16:764–774, 2011.

- [26] Antoine Lejay and Miguel Martinez. A scheme for simulating one-dimensional diffusion processes with discontinuous coefficients. Ann. Appl. Probab., 16(1):107–139, 2006.

- [27] Paul Lévy. Sur certains processus stochastiques homogènes. Compositio Math., 7:283–339, 1939.

- [28] Alex Lipton and Artur Sepp. Filling the gaps. Risk Magazine, pages 66–71, 2011-10.

- [29] S. Mazzonetto. On the Exact Simulation of (Skew) Brownian Diffusion with Discontinuous Drift. Phd thesis, Postdam University & Université Lille 1, 2016.

- [30] Hoang-Long Ngo and Shigeyoshi Ogawa. On the discrete approximation of occupation time of diffusion processes. Electron. J. Stat., 5:1374–1393, 2011.

- [31] J. M. Ramirez, E. A. Thomann, and E. C. Waymire. Advection–dispersion across interfaces. Statist. Sci., 28(4):487–509, 2013.

- [32] Alfréd Rényi. On stable sequences of events. Sankhyā Ser. A, 25:293 302, 1963.

- [33] Daniel Revuz and Marc Yor. Continuous martingales and Brownian motion, volume 293 of Grundlehren der Mathematischen Wissenschaften. Springer-Verlag, Berlin, 3 edition, 1999.

- [34] Charles Stone. Limit theorems for random walks, birth and death processes, and diffusion processes. Illinois J. Math., 7:638–660, 1963.

- [35] Lajos Takács. On the local time of the Brownian motion. Ann. Appl. Probab., 5(3):741–756, 1995.

- [36] J. B. Walsh. A diffusion with discontinuous local time. In Temps locaux, volume 52-53, pages 37–45. Société Mathématique de France, 1978.

- [37] Shinzo Watanabe. Generalized arc-sine laws for one-dimensional diffusion processes and random walks. In Stochastic analysis (Ithaca, NY, 1993), volume 57 of Proc. Sympos. Pure Math., pages 157–172. Amer. Math. Soc., Providence, RI, 1995.

- [38] Shinzo Watanabe, Kouji Yano, and Yuko Yano. A density formula for the law of time spent on the positive side of one-dimensional diffusion processes. J. Math. Kyoto Univ., 45(4):781–806, 2005.