Cross-validation and Peeling Strategies

for Survival Bump Hunting

using Recursive Peeling Methods

Abstract

We introduce a framework to build a survival/risk bump hunting model with a censored time-to-event response. Our Survival Bump Hunting (SBH) method is based on a recursive peeling procedure that uses a specific survival peeling criterion derived from non/semi-parametric statistics such as the hazards-ratio, the log-rank test or the Nelson–Aalen estimator. To optimize the tuning parameter of the model and validate it, we introduce an objective function based on survival or prediction-error statistics, such as the log-rank test and the concordance error rate. We also describe two alternative cross-validation techniques adapted to the joint task of decision-rule making by recursive peeling and survival estimation. Numerical analyses show the importance of replicated cross-validation and the differences between criteria and techniques in both low and high-dimensional settings. Although several non-parametric survival models exist, none addresses the problem of directly identifying local extrema. We show how SBH efficiently estimates extreme survival/risk subgroups unlike other models. This provides an insight into the behavior of commonly used models and suggests alternatives to be adopted in practice. Finally, our SBH framework was applied to a clinical dataset. In it, we identified subsets of patients characterized by clinical and demographic covariates with a distinct extreme survival outcome, for which tailored medical interventions could be made. An R package PRIMsrc is available on CRAN and GitHub.

Keywords: Exploratory Survival/Risk Analysis, Survival/Risk Estimation & Prediction, Non-Parametric Method, Cross-Validation, Bump Hunting, Rule-Induction Method.

1 Introduction

Non-Parametric Methods for Bump Hunting

The search for data structures in the form of bumps, modes, components, clusters or classes are important as they often reveal underlying phenomena leading to scientific discoveries. It is a difficult and central problem, applicable to virtually all sort of exact and social sciences with practical applications in various fields such as finance, marketing, physics, astronomy and biology.

It is common to treat the task of finding isolated data structures with the help of a response function as in a regression or classification problem or simply a probabilistic model as in a density estimation problem. Among the non-parametric unsupervised methods, this can be done by testing modality [Hartigan_1992, Rozal_1994, Polonik_1995, Burman_2009], using nonparametric mixture models (see e.g. [Bohning_2003] for a review), pattern recognition or clustering. However, beside the limitations or problems encountered by these methods in higher dimensional settings, model fitting e.g. of finite mixture models is challenged by the estimation of the true number of components [Dazard_2010a]. A similar situation exists for clustering procedures where the true number of clusters is unknown. Moreover, unsupervised methods may also fail to capture true data structures simply by ignoring a response if available [Dazard_2010a]. Although non-parametric supervised approaches such as, for instance, decision trees and their ensemble versions [Breiman_1984, Breiman_2001], do not have this drawback, these classification and regression procedures may also perform poorly [Dazard_2010a] since they are designed to work when the true number of classes is fixed or assumed in advance.

Exploratory supervised bump hunting procedures are among the few non-parametric methods that have been proposed to address this problem. These methods seek bump supports (possibly disjoint) of the input space of multi variables where a target function (e.g. a regression or density function) is on average larger (or lower) than its average over the entire input space. They cover tasks such as: (i) Mode(s) Hunting, (ii) Local/Global Extremum(a) Finding, (iii) Subgroup(s) Identification, (iv) Outlier(s) Detection. One known as the Patient Rule Induction Method (PRIM) was initially introduced by Friedman & Fisher [Friedman_1999] and later formalized by Polonik [Polonik_2010]. Essentially, the method is a recursive peeling algorithm that explores the input space to find rectangular solution regions where the response is expected to be larger on average. Some interesting features common and distinct to decision trees such as Classification and Regression Trees (CART) [Breiman_1984] help describe PRIM. As a rule-induction method like CART, PRIM generates simple decision rules describing the solution region of interest. Further, like CART, PRIM is a non-parametric procedure, algorithmic in nature (backwards fitting recursive algorithm), which makes few statistical assumptions about the data. Although PRIM does not explicitly state a model as CART, one can be formulated [Wu_2003, Hastie_2009]. Both algorithms/models have the possibility to recover complex interactions between input variables. Basic difference between the two methods lies in their approach and goal (reviewed in section LABEL:peeling_rule).

To date, only a few extensions of the original PRIM work have been done: This includes a Bayesian model-assisted formulation of PRIM [Wu_2003], a boosted version of PRIM based on Adaboost [Wang_2004], an extension of PRIM to censored responses [LeBlanc_2002, LeBlanc_2005] and to discrete variables [Il-Gyo_2008]. Although PRIM is intrinsically multivariate, it was uncertain from the original work how the algorithm would perform in ultra high-dimension where collinearity [Friedman_1999, Fan_2008] and sparsity abound. So, recently, an interesting body of work studied when and why the Principal Component space can be used effectively to optimize the response-predictor relationship in bump hunting. This was first addressed in [Dazard_2010a], where the computational details of such an approach were laid out for high-dimensional settings. Further, focusing on the properties of PRIM, authors demonstrated using basic geometrical arguments how the PC rotation of the predictor space alone can generate “improved” bump estimates [Diaz_2015a, Diaz_2015b]. These developments have important implications for general supervised learning theory and practical applications. In fact, [Dazard_2010a] first used a sparse PC rotation for improving bump hunting in the context of high dimensional genomic predictors and later showed how this approach can be used to find additional heterogeneity in terms of survival outcomes for colon cancer patients ([Dazard_2012a]).

Model Development and Validation in Discovery-Based Research

The primary problem encountered in discovery-based research has been non-reproducible results. For instance, early biomarker discovery studies using modern high-throughput datasets with large number of features have often been characterized by false or exaggerated claims and eventually disappointment when original results could not be reproduced in an independent study [Simon_2003, Michiels_2005, Dobbin_2005, Ein-Dor_2005, Shi_2006, Dupuy_2007, Subramanian_2010, Leek_2010, Haibe-Kains_2013]. Sadly, these results have been published even in high-profile journals and considered to provide definitive conclusions for both clinical care and biology. The problems of model reliability and reproducibility have usually been characterized by issues of severe model over-fitting, biased model parameter estimates and under-estimated errors. This has been attributed to a lack of proper rules to assess the analytical validity of studies simply because they were either under-developed or not routinely/correctly applied [Ntzani_2003, Ransohoff_2004]. This problem first received the attention of statisticians (see for instance reviews on guidelines and checklists [Baker_2002, Dupuy_2007, McShane_2013b]) as well as editors and US regulators lately [McShane_2013a].

Meanwhile, considerable development work has been done in the fields of feature selection, predictive model building and model validation to resolve the aforementioned issues. Recent developments include strategies such as variable/feature selection, dimension reduction, coefficient shrinkage and regularization. The challenge is obviously more acute in the context of high-dimensional data where the number of variables greatly exceeds the number of observations (so-called paradigm), since usually only a small number of variables truly enter in the model, while the large majority of them just contribute to noise. This noisy situation is even more complicated by the multicollinearity and spurious correlation between variables as well as the endogeneity between variables and model residual errors (see e.g. [Fan_2014] for a recent review).

A common situation where model reliability and reproducibility arise is when, for instance, model performance estimates are calculated from the same data that was used for model building, eventually resulting in initially promising results, but often non-reproducible [Ambroise_2002, Simon_2003, Hastie_2009]. These so-called “resubstitution estimates” are severely (optimistically) biased. Another problematic situation is when not all the steps of model building (such as pre-selection, creation of the prediction rule and parameter tuning) are internal to the cross-validation procedure, thereby creating a selection bias [Ambroise_2002, Varma_2006, Hastie_2009]. In addition, findings might not be reproducible even when proper independent sample and validation procedures are used. Problems may arise simply because cross-validated estimates are well-known to have large variance, a situation that is obviously more prevalent when few independent observations or small sample size are used [Efron_1983, Markatou_2005, Dobbin_2007].

Predictive Survival/Risk Modeling by Rule-Induction Methods

One important application of survival/risk modeling is to identify and segregate samples for predictive diagnostic and/or prognosis purposes. Direct applications include the stratification of patients by diagnostic and/or prognostic groups and/or responsiveness to treatment. Therefore, survival modeling is usually performed to predict/classify patients into risk or responder groups (not to predict exact survival time) from which one usually derives survival/risk functions estimates (e.g. by Kaplan–Meier estimates). However, for the reasons mentioned above, Kaplan–Meier estimates for the risk groups computed on the same set of data used to develop the survival model may be very biased [Varma_2006, Molinaro_2005].

In the context of a time-to-event outcome, regression survival trees have proven to be useful. Several developments have been made for fitting decision trees to non-informative censored survival times [Gordon_1985, Ciampi_1986, Segal_1988, Davis_1989, LeBlanc_1992, LeBlanc_1993, Ahn_1994]. Although regression survival trees are powerful techniques to understand for instance patient outcome and for forming multiple prognostic groups, often times interest focuses only on estimating extreme survival/risk groups. In this respect, survival bump hunting aims not at estimating the survival/risk probability function over the entire variable space, but at searching regions where this probability is larger (or smaller) than its average over the entire space.

Also, one possible drawback of decision trees is that the data splits at an exponential rate as the space undergo partitioning (typically by binary splits) as opposed to a more patient rate in decision boxes (typically by controlled quantile). In this sense, bump hunting by recursive peeling may be a more efficient way of learning from the data. With the exception of the work of LeBlanc et al. on Adaptive Risk Group Refinement [LeBlanc_2005], it has not been studied whether decision boxes, obtained from box-structured recursive peelings, would yield better estimates for constructing prognostic groups than their tree-structured counterparts.

Although resampling methods are often useful in assessing the prediction accuracy of classifier models, they are not directly applicable for predictive survival modeling applications. Simon et al. have reviewed the literature of such applications and identified serious deficiencies in the validation of survival risk models [Dupuy_2007, Subramanian_2010, Simon_2011]. They noted for instance that in order to utilize the cross-validation approach developed for classification problems, some studies have dichotomized their survival or disease-free survival data …. The problem on how to cross-validate the estimation of survival distributions (e.g. by Kaplan–Meier curves) is not obvious [Simon_2011]. In addition, beside Subramanian and Simon’s initial study on the usefulness of resampling methods for assessing survival prediction models in high-dimensional data [Subramanian_2011], no comparative study has been done for rule-induction methods and specifically recursive peeling methods such as our “Patient Recursive Survival Peeling” method (see section LABEL:survestimation).

Contribution and Scope

Our survival/risk bump hunting model is built upon the regular bump hunting framework, which we extended to accommodate a possibly censored time-to-event type of response. To build our survival/risk bump hunting model, we first describe our “Patient Recursive Survival Peeling” (PRSP) method, a non-parametric recursive peeling procedure, derived from a rule-induction method, namely the Patient Rule Induction Method (PRIM), which we have extended to allow for survival/risk response, possibly censored. In the process, we describe what appropriate survival estimator and statistic may be used as a peeling criteria to fit our survival/risk bump hunting model.

One of the critiques made in the original PRIM work was the lack of validation procedure and measures of significance of solution regions. So, our objective was also to develop a validation procedure for the purpose of model tuning by means of an optimization criterion of model parameters tuning and a resampling technique amenable to the joint task of decision rule making by recursive peeling (i.e. decision-box) and survival estimation. Specifically, we describe here two alternative, possibly repeated, -fold cross-validation techniques adapted to the task, namely the “Replicated Combined CV” (RCCV) and “Replicated Averaged CV” (RACV). Moreover, we show how to use survival end-points/prediction statistics for the specific goal of model peeling length optimization by cross-validation.

Results support the claim that optimal survival bump hunting models may be reached using appropriate combination of criterion and technique under certain situations, for which we provide guidelines. Finally, we show empirical results from a real dataset application and from simulated data in low- and high-dimension, illustrating the efficiency of our cross-validation and peeling strategies and the adequacy of our survival bump hunting framework in comparison to other available non-parametric survival models.

We do not describe nor discus the specific treatment of dimension-reduction or variable selection in high-dimensional settings for the only reason that the focus of this study is on cross-validation and peeling strategies. Even though the issue of model unreliability is known to be more severe when there is a large number of variables to choose from [Simon_2003], it is known to persist even in low-dimensional setting [Subramanian_2013]. So, we posit that the framework described here is relevant and applicable to both low and high-dimensional situations. Nevertheless, the method does include cross-validation procedures to control model size (# covariates) in addition to model complexity (# peeling steps). It has been tested in multiple () low and high-dimensional situations where and even (see abstract of application article [Dazard_2016a] and our example datasets in our R package PRIMsrc [Dazard_2015a]) and we show empirical analyses in high-dimensional simulated datasets where .

2 Survival Bump Hunting for Exploratory Survival Analysis

2.1 Bump Hunting Model

2.1.1 Notation - Goal

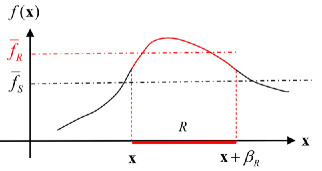

The formal setup of bump hunting is as follows [see also Friedman_1999, Polonik_2010]. Let us consider a supervised problem with a univariate output (response) random variable, denoted . Further, let us consider a -dimensional random vector of support , also called input space, in an Euclidean space. Let us denote the input variables by , of joint probability density function and by the target function to be optimized (e.g. any regression function or e.g. the p.m.f or p.d.f ).

Briefly, the goal in bump hunting is to find a sub-space or region of the input space within which the average value of is expected to be significantly larger (or smaller) than its average value over the entire input space (Figure 1). In addition, one wishes that the corresponding support (mass) of , say , be not too small, that is, greater than a minimal support threshold, say .