Time-Average Stochastic Optimization with Non-convex Decision Set and its Convergence

Abstract

This paper considers time-average stochastic optimization, where a time average decision vector, an average of decision vectors chosen in every time step from a time-varying (possibly non-convex) set, minimizes a convex objective function and satisfies convex constraints. This formulation has applications in networking and operations research. In general, time-average stochastic optimization can be solved by a Lyapunov optimization technique. This paper shows that the technique exhibits a transient phase and a steady state phase. When the problem has a unique vector of Lagrange multipliers, the convergence time can be improved. By starting the time average in the steady state the convergence times become under a locally-polyhedral assumption and under a locally-non-polyhedral assumption, where denotes the proximity to the optimal objective cost. Simulations suggest that the results may hold more generally without the unique Lagrange multiplier assumption.

I Introduction

Stochastic network optimization can be used to design dynamic algorithms that optimally control communication networks [1]. The framework has several unique properties which do not exist in a traditional convex optimization setting. In particular, the framework allows for a time-varying and possibly non-convex decision set. For example, it can treat a packet switch that makes binary scheduling decisions, or a wireless system with randomly varying channels and decision sets.

This paper considers time-average stochastic optimization, which is useful for example problems of network utility maximization [2, 3, 4, 5], energy minimization [6, 7], and quality of information maximization [8].

Time is slotted. Define to be a finite or countable infinite sample space of random states. Let denote a random state at time . Random state is assumed to be independent and identically distributed (i.i.d.) across time slots. The steady state probability of is denoted by . Let and be any positive integers. Each slot , decision vector is chosen from a decision set . Define as the time average vector:

The goal is to make decisions over time to solve:

| Minimize | (1) | ||||

| Subject to | |||||

Here it is assumed that is a closed and bounded subset of for each . Let be a closed and bounded set that contains , and and are convex functions from to , where denotes a convex hull of set . Results in [1] imply that the optimal point can be achieved with an ergodic policy for which the limiting time average expectation exists.

Solving formulation (1) using the stochastic network optimization framework does not require any statistical knowledge of the random states. However, if the steady state probabilities are known, the optimal objective cost of formulation (1) is identical the optimal cost of the following problem:

| Minimize | (2) | ||||

| Subject to | |||||

where . Note that for any and any sets and .

Formulation (2) is convex; however, its optimal solution may not be in any of the sets . In fact, determining whether is a member of may already be a difficult task. This illustrates that traditional and state-of-the-art techniques for solving convex optimization cannot be applied directly to solve problem (1). Nevertheless, their convergence times are compelling to be mentioned for a purpose of comparison.

The convergence time of an algorithm is usually measured as a function of an -approximation to the optimal solution. For a convex optimization problem, several techniques utilizing a time average solution [9, 10, 11] have convergence time. For unconstrained optimization without restricted strong convexity property, the optimal first-order method [12, 13] has convergence time, while the gradient and subgradient methods have respectively and convergence time [14]. For constrained optimization, two algorithms developed in [15, 16] have convergence time; however, the results rely on special structures of their formulation. All of these results are for convex optimization problems, which is not formulation (1).

This paper considers a drift-plus-penalty algorithm, developed in [1], that solves formulation (1). The algorithm is shown to have convergence time in [17]. Note that a deterministic version of formulation (1) and its corresponding algorithm are studied in [18].

Inspired by the analysis in [19], the drift-plus-penalty algorithm is shown to have a transient phase and a steady state phase. These phases can be analyzed in two cases that depend on the structure of a dual function. The first case is when a dual function satisfies a locally-polyhedral assumption and the expected transient time is . The second case is when the dual function satisfies a locally-non-polyhedral assumption and the expected transient time is . Then, under a uniqueness assumption on Lagrange multipliers, if the time average starts in the steady state, a solution converges in and time slots under the locally-polyhedral and locally-non-polyhedral assumptions respectively. Simulations suggest these results may hold more generally without the uniqueness assumption.

The paper is organized as follows. Section II constructs an algorithm solving problem (1). The behavior and properties of the algorithm are analyzed in Section III. Section IV analyzes the transient phase and the steady state phase under the locally-polyhedral assumption. Results under the locally-non-polyhedral assumption are provided in Section V. Simulations are performed in Section VI.

II Time-Average Stochastic Optimization

A solution to problem (1) can be obtained through an auxiliary problem, which is formulated in such a way that its optimal solution is also an optimal solution to the time-average problem. To formulate this auxiliary problem, an additional set and mild assumptions are defined. First of all, it can be shown that is compact.

Assumption 1

There exists a vector in the interior of that satisfies for all .

In convex optimization, Assumption 1 is a Slater condition, which is a sufficient condition for strong duality [20].

Define the extended set that is a closed, bounded, and convex subset of and contains . Set can be , but it can be defined as a hyper-rectangle set to simplify a later algorithm. Define as the Euclidean norm.

Assumption 2

Functions and for are convex and Lipschitz continuous on the extended set , so there are constants and for that for any :

| (3) | ||||

| (4) |

II-A Auxiliary formulation

For function of vector , define an average of function values as

Recall that problem (1) can be achieved with an ergodic policy for which the limiting time average expectation exists. The time average stochastic optimization (1) is solved by considering an auxiliary formulation, which is formulated in terms of well defined limiting expectations “for simplicity.”

| Minimize | (5) | ||||

| Subject to | |||||

This formulation introduces the auxiliary vector . The second constraint ties and together, so the original objective function and constraints of problem (1) are preserved in problem (5). Let be the optimal objective cost of problem (1).

Theorem 1

Proof:

Let be the optimal objective cost of the auxiliary problem (5). We show that .

Let be an optimal solution, generated by an ergodic policy, to problem (1) such that:

Consider a solution to problem (5) as follows:

It is easy to see that this solution satisfies the last two constraints of problem (5). For the first constraint, it follows from Lipschitz continuous that for

Therefore, this solution is feasible, and the objective cost of problem (5) is

This implies that .

Alternatively, let be an optimal solution to problem (5) such that:

Consider a solution to problem (1) as follows:

It is easy to see that the solution satisfies the last constraint of problem (1). For the first constraint, the convexity of implies that for

Hence, this solution is feasible. The objective cost of problem (1) follows from the convexity of that

This implies that . Thus, combining the above results, we have that . ∎

II-B Lyapunov optimization

The auxiliary problem (5) can be solved by the Lyapunov optimization technique [1]. Define and to be virtual queues of constraints and with update dynamics:

| (6) | |||||

| (7) |

where operator is the projection to a corresponding non-negative orthant.

For ease of notations, let , , and respectively be the vectors of virtual queues , , and functions .

Define Lyapunov function (8) and Lyapunov drift (9) as

| (8) | ||||

| (9) |

Let notation denote the transpose of vector . Define .

Lemma 1

For every , the Lyapunov drift is upper bounded by

| (10) |

II-C Drift-plus-penalty algorithm

Let and be the initial condition of and respectively. Every time step, the Lyapunov optimization technique observes the current realization of random state before choosing decisions and that minimize the right-hand-side of (11). The drift-plus-penalty algorithm is summarized in Algorithm 1.

III Behaviors of Drift-Plus-Penalty Algorithm

Starting from , Algorithm 1 reaches the steady state when vector concentrates around a specific set (defined in Section III-A). The transient phase is the period before this concentration.

III-A Embedded Formulation

A convex optimization problem, called embedded formulation, is considered. This idea is inspired by [19].

| Minimize | (12) | ||||

| Subject to | |||||

This formulation has a dual problem, whose properties are used in convergence analysis. Let and be the vectors of dual variables associated with the first and second constraints of problem (12). The Lagrangian is defined as

The dual function of problem (12) is

| (13) |

where is defined in (14) and all of the minimums take the same value.

| (14) |

Define the solution to the infimum in (14) as

| (15) | ||||

| (16) |

Finally, the dual problem of formulation (12) is

| Maximize | (17) | |||

| Subject to |

Problem (17) has an optimal solution that may not be unique. A set of these optimal solutions, which are vectors of Lagrange multipliers, can be used to analyze the expected transient time. However, to simplify the proofs and notations, the uniqueness assumption is assumed. Let denote a concatenation vector of and .

Assumption 3

Dual problem (17) has a unique vector of Lagrange multipliers denoted by .

This assumption is assumed throughout Section IV and Section V. Note that this is a mild assumption when practical systems are considered, e.g., [19, 5]. Furthermore, simulation results in Section VI evince that this assumption may not be needed.

To prove the main result of this section, a useful property of is derived. Define .

Lemma 2

For any and , it holds that

| (18) |

The following lemma ties the virtual queues of Algorithm 1 to the Lagrange multipliers. Given the generated result of Algorithm 1, define as a concatenation of vectors and .

III-B -slot convergence

For any positive integer and any starting time , define the -slot average starting at as

This average leads to the following convergence bounds.

Theorem 2

Let be a sequence generated by Algorithm 1. For any positive integer and any starting time , the objective cost converges as

| (20) |

and the constraint violation for every is

| (21) |

Proof:

The proof is in Appendix. ∎

III-C Concentration bound

Theorem 3

Let be a real random process over satisfying

for some positive real-valued , and .

Suppose (with probability ) for some . Then for every time , the following holds:

where and constants , and are:

In this paper, random process is defined to be the distance between and the vector of Lagrange multipliers as for every .

Lemma 4

It holds for every that

Proof:

The first part is proven in two cases.

i) If , the non-expansive projection implies

ii) If , then

Therefore, . Using proves the second part. ∎

IV Locally-polyhedral dual function

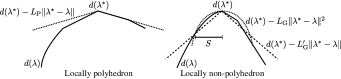

This section analyzes the expected transient time and a convergence result in the steady state. Dual function (13) in this section is assumed to satisfy a locally-polyhedral property, introduced in [19]. This property is illustrated in Figure 1. It holds when and each for are either linear or piece-wise linear.

Assumption 4

Let be the unique Lagrange multiplier vector. There exists such that dual function (13) satisfies, for any ,

| (22) |

Note that, by concavity of the dual function, if inequality (22) holds locally about , it must also hold globally.

IV-A Expected transient time

The progress of at each step can be analyzed. Define

Lemma 5

Lemma 5 implies that proceeds closer to in the next step when the distance between them is at least . This implication means that concentrates around in the steady state. The transient time of Algorithm 1 under the locally-polyhedral assumption is defined as

Also, let be an indicator function whose value is if is true and otherwise.

Lemma 6

Given the initial condition , the expected transient time is at most

Proof:

Recall that . Define random variable as , and . It follows that

where is a given constant (with probability 1). Taking an expectation of both sides gives:

Lemma 6 implies that the expected transient time under the locally-polyhedral assumption is .

IV-B Convergence time in a steady state

Once Algorithm 1 enters the steady state, the following property holds.

Lemma 7

The above lemma implies that, in the steady state, the expected distance and square distance between and the vector of Lagrange multipliers are constant. This phenomenon leads to an improved convergence time when the average is performed in the steady state. A useful result is derived before the main theorem.

Lemma 8

For any times and , it holds that

Proof:

It holds for any that

Using the above equality with leads to

Taking an expectation proves the lemma. ∎

Finally, the convergence in the steady state is analyzed.

Theorem 4

For any time and positive integer , the objective cost converges as

| (30) |

and the constraint violation is upper bounded by

| (31) |

The implication of Theorem 4 is as follows. When the average starts in the steady state, the deviation from the optimal cost is , and the constraint violation is bounded by . By setting , the convergence time is .

V Locally-non-polyhedral dual function

The dual function (13) in Section V is assumed to satisfy a locally-non-polyhedral property, modified from [19]. This property is illustrated in Figure 1.

Assumption 5

Let be the unique Lagrange multiplier vector. The following holds:

i) There exist and such that, whenever and , dual function (13) satisfies

ii) When and , there exist such that dual function (13) satisfies

The progress of at each step can be analyzed. Define

Lemma 9

Proof:

If condition

| (37) |

is true, Lemma 3 implies that

Applying Jensen’s inequality [20] on the left-hand-side yields

When , it follows that

| (38) |

However, condition (37) holds when

| (39) |

because Assumption 5 implies that, when ,

Therefore, condition (37) holds when condition (39) holds. Condition (39) requires that

Thus, inequality (38) holds when . This proves the first part of (36).

Lemma 9 implies that proceeds closer to in the next step when the distance between them is at least . This implication means that concentrates around in the steady state.

V-A Expected transient time

From an initial condition, the transient time of Algorithm 1 under the locally-non-polyhedral assumption is defined as

Lemma 10

When is sufficiently larger that and , given the initial condition , the expected transient time is at most

Proof:

Recall that . Define random variable as , and . It follows that

where is a given constant (with probability 1). Taking an expectation of both sides gives:

V-B Convergence time in a steady state

Once Algorithm 1 enters the steady state, the following property holds.

Lemma 11

When is sufficiently larger that , , and , under Assumptions 3 and 5, for any time , the following holds

| (43) | ||||

| (44) |

where and are:

The convergence results in the steady state are as follows.

Theorem 5

When is sufficiently large that , and , then for any time and any positive integer , the objective cost converges as

| (47) |

and the constraint violation is upper bounded by

| (48) |

VI Simulation

VI-A Staggered Time Averages

In order to take advantage of the improved convergence times, computing time averages must be started in the steady state phase shortly after the transient time. To achieve this performance without knowing the end of the transient phase, time averages can be restarted over successive frames whose frame lengths increase geometrically. For example, if one triggers a restart at times for integers , then a restart is guaranteed to occur within a factor of 2 of the time of the actual end of the transient phase.

VI-B Results

This section illustrates the convergence times of the drift-plus-penalty Algorithm 1 under locally-polyhedron and locally-non-polyhedron assumptions. Let , and . A formulation is

| Minimize | (51) | |||

| Subject to | ||||

where function will be given for different cases.

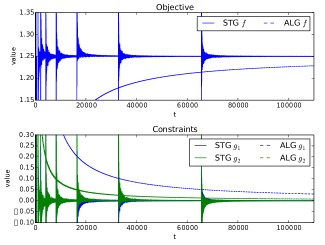

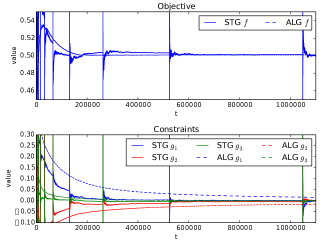

Under locally-polyhedron assumption, let be the objective function of problem (51). In this setting, the optimal value is where . Figure 2 shows the values of objective and constraint functions of time-averaged solutions. It is easy to see the improved convergence time from the staggered time averages (STG) compared to the convergence time of Algorithm 1 (ALG).

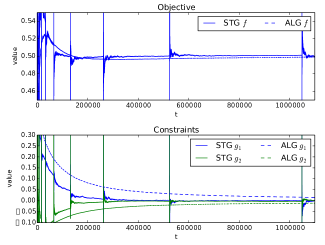

Under locally-non-polyhedral assumption, let be the objective function of problem (51). Note that the optimal value of this problem is where . Figure 3 shows the values of objective and constraint functions of time-averaged solutions. It can be seen from the constraints plot that the staggered time averages converges faster than Algorithm 1. This illustrates the different between convergence times and .

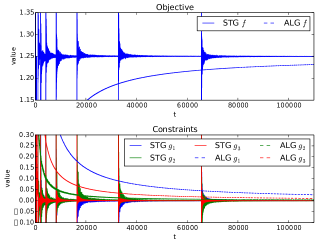

Figure 4 illustrates the convergence time of problem 51 with and additional constraint . The dual function of this formulation has non-unique vector of Lagrange multipliers. The Comparison of Figures 4 and 2 shows that there is no difference in the order of convergence time.

Figure 5 illustrates the convergence time of problem 51 with and additional constraint . The dual function of this formulation has non-unique vector of Lagrange multipliers. The Comparison of Figures 5 and 3 shows that there is no difference in the order of convergence time.

VII Conclusion

We consider the time-average stochastic optimization problem with a non-convex decision set. The problem can be solved using the drift-plus-penalty algorithm, which converges in . After we analyze the transient and steady state phases of the algorithm, the convergence time can be improved by performing time average in the steady state. we prove that the improved convergence time is under the locally-polyhedral assumption and is under the locally-non-polyhedral assumption.

Appendix

The convergence time of the objective cost as a function of vectors is firstly proven. This proof requires the following theorem proven in [1].

Theorem 6

There exists a randomized policy that only depends on such that for all :

Lemma 12

Let be a sequence generated by Algorithm 1. For any positive integer and starting time , it holds that

Proof:

Since decision minimizes the right-hand-side of (11), the following holds for any other decisions including the randomized policy in Theorem 6:

Taking the conditional expectation of the above bound gives

where the last inequality uses properties of the randomized policy in Theorem 6.

Taking expectation and using iterated expectation leads to

Summing from to yields

Dividing by , using the convexity of , and rearranging terms proves the lemma. ∎

The constraint violation as a function of vectors is the following.

Lemma 13

Let be a sequence generated by Algorithm 1. For any positive integer and starting time , it holds for that

Proof:

Dynamic (6) implies that . Taking expectation gives . Summing from to yields . Dividing by , using the convexity of , and rearranging terms proves the lemma. ∎

The following result is used to translates the results in Lemmas 12 and 13 to the bounds as functions of vectors .

Lemma 14

Let be a sequence generated by Algorithm 1. For any positive integer and starting time , it holds that

Proof:

Dynamic (7) implies that . Summing from to yields . Dividing by and rearranging terms proves the lemma. ∎

Finally, Lemma 2 is proven.

References

- [1] M. J. Neely, “Stochastic network optimization with application to communication and queueing systems,” Synthesis Lectures on Communication Networks, vol. 3, no. 1, 2010.

- [2] M. J. Neely, E. Modiano, and C. Li, “Fairness and optimal stochastic control for heterogeneous networks,” Networking, IEEE/ACM Transactions on, vol. 16, no. 2, Apr. 2008.

- [3] L. Georgiadis, M. J. Neely, and L. Tassiulas, “Resource allocation and cross-layer control in wireless networks,” Foundations and Trends in Networking, Apr. 2006.

- [4] A. Stolyar, “Greedy primal-dual algorithm for dynamic resource allocation in complex networks,” Queueing Systems, vol. vol. 54, no. 3, pp. 203-220, 2006.

- [5] A. Eryilmaz and R. Srikant, “Fair resource allocation in wireless networks using queue-length-based scheduling and congestion control,” Networking, IEEE/ACM Transactions on, vol. 15, no. 6, Dec. 2007.

- [6] M. J. Neely, “Energy optimal control for time-varying wireless networks,” Information Theory, IEEE Transactions on, Jul. 2006.

- [7] L. Lin, X. Lin, and N. B. Shroff, “Low-complexity and distributed energy minimization in multi-hop wireless networks,” Proc. IEEE INFOCOM, 2007.

- [8] S. Supittayapornpong and M. J. Neely, “Quality of information maximization for wireless networks via a fully separable quadratic policy,” Networking, IEEE/ACM Transactions on, 2014.

- [9] Y. Nesterov, “Primal-dual subgradient methods for convex problems,” Mathematical Programming, vol. 120, no. 1, 2009.

- [10] A. Nedić and A. Ozdaglar, “Approximate primal solutions and rate analysis for dual subgradient methods,” SIAM Journal on Optimization, vol. 19, no. 4, 2009.

- [11] M. J. Neely, “Distributed and secure computation of convex programs over a network of connected processors,” DCDIS Conf., Guelph, Ontario, Jul. 2005.

- [12] Y. Nesterov, Introductory Lectures on Convex Optimization: A Basic Course (Applied Optimization). Springer Netherlands, 2004.

- [13] P. Tseng, “On accelerated proximal gradient methods for convex-concave optimization,” submitted to SIAM Journal on Optimization, 2008.

- [14] S. Boyd and L. Vandenberghe, Convex Optimization. New York, NY, USA: Cambridge University Press, 2004.

- [15] E. Wei and A. Ozdaglar, “On the o(1/k) convergence of asynchronous distributed alternating direction method of multipliers,” arXiv:1307.8254, Jul. 2013.

- [16] A. Beck, A. Nedić, A. Ozdaglar, and M. Teboulle, “An o(1/k) gradient method for network resource allocation problems,” Control of Network Systems, IEEE Transactions on, vol. 1, no. 1, Mar. 2014.

- [17] M. J. Neely, “A simple convergence time analysis of drift-plus-penalty for stochastic optimization and convex program,” arXiv:1412.0791v1 [math.OC], Dec. 2014.

- [18] S. Supittayapornpong and M. J. Neely, “Time-average optimization with nonconvex decision set and its convergence,” in CDC, 2014 Proceedings IEEE, Dec. 2014.

- [19] L. Huang and M. J. Neely, “Delay reduction via lagrange multipliers in stochastic network optimization,” Automatic Control, IEEE Transactions on, vol. 56, no. 4, Apr. 2011.

- [20] D. Bertsekas, A. Nedić, and A. Ozdaglar, Convex Analysis and Optimization. Athena Scientific, 2003.

- [21] M. J. Neely, “Energy-aware wireless scheduling with near optimal backlog and convergence time tradeoffs,” in INFOCOM, 2015 Proceedings IEEE, Apr. 2015, to appear.

- [22] S. Asmussen, Applied Probability and Queues, ser. Applications of mathematics. New York: Springer, 2003.

- [23] S. M. Ross, Stochastic Processes (Wiley Series in Probability and Statistics), 2nd ed. Wiley, Feb. 1995.