How Accurate is inv(A)*b?

Abstract.

Several widely-used textbooks lead the reader to believe that solving a linear system of equations by multiplying by a computed inverse inv(A) is inaccurate. Virtually all other textbooks on numerical analysis and numerical linear algebra advise against using computed inverses without stating whether this is accurate or not. In fact, under reasonable assumptions on how the inverse is computed, x=inv(A)*b is as accurate as the solution computed by the best backward-stable solvers. This fact is not new, but obviously obscure. We review the literature on the accuracy of this computation and present a self-contained numerical analysis of it.

1. Introduction

Can you accurately compute the solution to a linear equation by first computing an approximation to and then multiplying by (x=inv(A)*b in Matlab)?

Unfortunately, most of the literature provides a misleading answer to this question. Many textbooks, including recent and widely-used ones, mislead the reader to think that x=inv(A)*b is less accurate than x=A\b, which computes the factorization of with partial pivoting and then solves for using the factors [6, p. 31], [10, p. 53], [7, p. 50], [11, p. 77], [2, p. 166], [13, pp. 184, 235, and 246]. Other textbooks warn against using a computed inverse for performance reasons without saying anything about accuracy. If you still dare use x=inv(A)*b in Matlab code, Matlab’s analyzer issues a wrong and misleading warning [9].

As far as we can tell, only two sources in the literature present a correct analysis of this question. One is almost 50 years old [16, pp. 128–129], and is therefore hard to obtain and somewhat hard to read. The other is recent, but relegates this analysis to the solution of an exercise, rather than including it in the 27-page chapter on the matrix inverse [8, p. 559; see also p. 260]; even though the analysis there shows that x=inv(A)*b is as accurate as x=A\b, the text ends by stating that “multiplying by an explicit inverse is simply not a good way to solve a linear system”. The reader must pay careful attention to the analysis if he or she is to answer our question correctly.

Our aim in this article is to clarify to researchers (and perhaps also to educators and students) the numerical properties of a solution to that is obtained by multiplying by a computed inverse. We do not present new results; we present results that are known, but not as much as they should be.

Computing the inverse requires more arithmetic operations than computing an factorization. We do not address the question of computational efficiency, but we do note that there is evidence that using the inverse is sometimes preferable from the performance perspective [3].

It also appears that explicit inverses are sometimes used when the inverse must be applied in hardware, as in some MIMO radios [5, 15]. The numerical analysis in the literature and in this paper does not apply as-is to these computations, because hardware implementations typically use fixed-point arithmetic rather than floating point. Still, the analysis that we present here provides guiding principles to all implementations (e.g., to solve for the rows of the inverse using a backward-stable solver), and it may also provide a template for an analysis of fixed-point implementations or alternative inversion algorithms.

The rest of this paper is organized as follows. Section 2 presents the naive numerical analysis that probably led many authors to claim that x=inv(A)*b is inaccurate; the analysis is correct, but the error bound that it yields is too loose. Section 3 presents a much tighter analysis, due to Wilkinson; Higham later showed that this bound holds even in the componentwise sense. Section 4 explains another aspect of computed inverses that is not widely appreciated: that they are typically good for applying either from the left or from the right, but not both. Even when x=inv(A)*b is accurate, x is usually not backward stable; Section 5 discusses conditions under which x is also backward stable. To help the reader fully understand all of these results, Section 6 demonstrates them using simple numerical experiments. We present concluding remarks in Section 7.

2. A Loose Bound

Why did the inverse acquire its bad reputation? Good inversion methods produce a computed inverse that is, at best, conditionally accurate,

| (2.1) |

We cannot hope for an unconditional bound of on the relative forward error. Some inversion methods guarantee conditional accuracy (for example, computing the inverse column by column using a backward stable linear solver). In particular, lapack’s xGETRI satisfies (2.1), and also a componentwise conditional bound [8, p. 268]. That is, each entry in the computed inverse that xGETRI produces is conditionally accurate. It appears that Matlab’s inv function also satisfies (2.1).

Let’s try to use (2.1) to obtain a bound on the forward error . Multiplying by in floating point produces that satisfies for some with . Denoting , we have

so

| (2.2) | |||||

Unless is so ill conditioned that the left-hand side of (2.1) is larger than (any constant would do), . Therefore,

| (2.3) |

In contrast, solving using a backward stable solver such as one based on the factorization (or on an factorization with partial pivoting provided there is no growth) yields for which

| (2.4) |

3. Tightening the Bound

The bound (2.3) is loose because of a single term, , which we used to bound the norm of . The other term in the bound, , is tight.

The key insight is that rows of tend to lie mostly in the directions of left singular vectors of that are associated with small singular values. The smaller the singular value of , the stronger the influence of the corresponding singular vector (or singular subspace) on the rows of . Therefore, the norm of the product of and is much smaller than the product of the norms; shrinks the strong directions of the error matrix . This explains why the norm of is small. This relationship between the singular vectors of and depends on a backward stability criterion on , which we define and analyze below.

Suppose that we use a backward stable solver to compute the rows of one by one by solving where is row of . Each computed row satisfies

with . Rearranging the equation, we obtain

so . For a componentwise version of this bound and related bounds for other methods of computing , see [8, section 14.3].

This is the key to the conditional accuracy of . Since , the norm of is . We therefore have the following theorem.

Theorem 1.

Let be a linear system with a coefficient matrix that satisfies . Assume that is an approximate inverse of that satisfies . Then the floating-point product of and satisfies

The essence of this analysis appears in Wilkinson’s 1963 monograph [16, pp. 128–129]. Wilkinson did not account for the rounding errors in the multiplication , which are not asymptotically significant, but otherwise his analysis is complete and correct.

4. Left and Right Inverses

In this article, we multiply by the inverse from the left to solve . This implies that the approximate inverse should be a good left inverse. Indeed, we have seen that a with a small left residual guarantees a conditionally accurate solution . Whether is also a good right inverse, in the sense that is small, is irrelevant for solving . If we were trying to solve , we would need a good right inverse.

Wilkinson noted that if rows of are computed using with partial pivoting, then is usually both a good left inverse and a good right inverse, but not always [16, page 113]. Du Croz and Higham show matrices for which this is not the case, but they also note that such matrices are the exception rather than the rule [4].

Other inversion methods tend to produce a matrix that is either a left inverse or a right inverse but not both. A good example is Newton’s method. If one iterates with then converges to a left inverse. If one iterates with then converges to a right inverse.

5. Multiplication by the Inverse is (Sometimes) Backward Stable

The next section presents a simple example in which the computed solution is conditionally accurate but not backward stable. In this section we show that under certain conditions, the solution is also backward stable. The analysis also clarifies in what ways backward stability can be lost.

Suppose that we use a that is a good right inverse, . We can produce such a by solving for its columns using a backward-stable solver. We have

for some with . Here too, the term does not influence the asymptotic upper bound. The assumption that is a good right inverse bounds the other term,

| (5.1) | |||||

The relative backward error is given by the expression [12]. Filling in the bound on the norm of the residual, we obtain

If we assume that is a reasonable enough left inverse so that at least is close to (that is, if the forward error is ), then a solution that has norm close to guarantees backward stability to within . Let be the SVD of , so

where and are the left and right singular vectors of . If , then and is backward stable. If the projection of on is not large but the projection on, say, is large and is close to , the solution is still backward stable, and so on.

Perhaps more importantly, we have now identified the ways in which can fail to be backward stable:

-

(1)

is not a good right inverse, or

-

(2)

is such a poor left inverse that is much smaller than , or

-

(3)

the projection of on the left singular vectors of associated with small singular values is small.

The next section shows an example that satisfies the last condition.

6. Numerical Examples

Let us demonstrate the theory with a small numerical example. We set , and , generate a random matrix with , and generate its inverse. The matrix and the inverse are produced by matrix multiplications, and each multiplication has at least one unitary factor, so both are accurate to within a relative error of about . We also compute an approximate inverse using Matlab’s inv function.

-

[L,dummy,R] = svd(randn(n));

svalues = logspace(log10(sigma_1), log10(sigma_n), n);

S = diag(svalues);

invS = diag(svalues.^-1);

A = L * S * R’;

AccurateInv = R * invS * L’;

V = inv(A);

The approximate inverse is only conditionally accurate, as predicted by (2.1), but its use as a left inverse leads to a conditionally small residual.

-

Gamma = V - AccurateInv;

norm(Gamma) / norm(AccurateInv)

ans = 3.4891e-09

norm(V * A - eye(n))

ans = 1.6976e-08

We now generate a random right hand-side and use the inverse to solve . The result is backward stable to within a relative error of .

-

b = randn(n, 1);

x = R * (invS * (L’ * b));

xv = V * b;

norm(A * xv - b) / (norm(A) * norm(xv) + norm(b))

ans = 8.8078e-16

Obviously, the solution should be conditionally accurate, and it is.

-

norm(xv - x) / norm(x)

ans = 3.102e-09

We now perform a similar experiment, but with a random , which leads to a right-hand side which is nearly orthogonal to the left singular vectors of that correspond to small singular values; now the solution is only conditionally backward stable.

-

x = randn(n, 1);

b = L * (S * (R’ * x));

xv = V * b;

norm(A * xv - b) / (norm(A) * norm(xv) + norm(b))

ans = 2.1352e-10

Theorem 1 predicts that the solution should still be conditionally accurate. It is. Matlab’s backslash operator, which is a linear solver based on Gaussian elimination with partial pivoting, produces a solution with a similar accuracy.

-

norm((A\b) - x) / norm(x)

ans = 4.0801e-09

norm(xv - x) / norm(x)

ans = 4.5699e-09

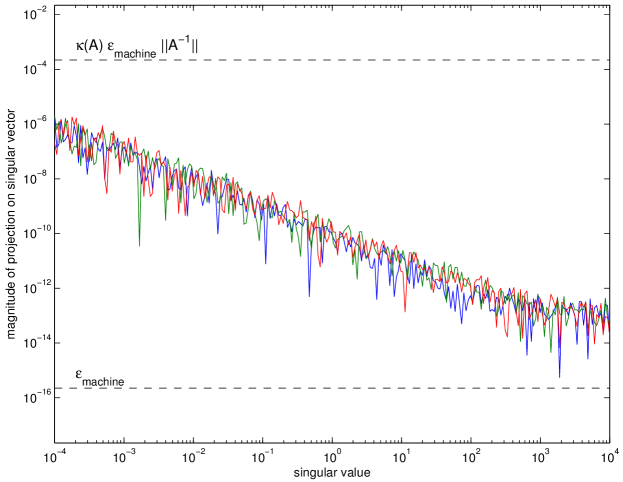

The magic is in the special structure of rows of . Figure 6.1 displays this structure graphically. We can see that a row of is almost orthogonal to the left singular vectors of associated with large singular values, and that the magnitude of the projections increases with decreasing singular values. If we produce an approximate inverse with the same magnitude of error as in inv(A) but with a random error matrix, it will not solve conditionally accurately.

-

BadInv = AccurateInv + norm(Gamma) * randn(n);

xv = BadInv * b;

norm(A * xv - b) / (norm(A) * norm(xv) + norm(b))

ans = 0.075727norm(xv - x) / norm(x)

ans = 0.83552

7. Closing Remarks

Solving a linear system of equations using a computed inverse produces a conditionally accurate solution, subject to an easy to satisfy condition on the computation of . Using Gaussian elimination with partial pivoting or a factorization produces a solution with errors that have the same order of magnitude as those produced by .

If the right-hand side does not have any special relationship to the left singular subspaces of , then the solution produced by is also backward stable (under a slightly different technical condition on ), and hence as good as a solution produced by GEPP or . As far as we know, this result is new.

If is close to orthogonal to the left singular subspaces of corresponding to small singular values, then the solution produced by is conditionally accurate, but usually not backward stable. Whether this is a significant defect or not depends on the application. In most applications, it is not a serious problem.

One difficulty with a conditionally-accurate solution that is not backward stable is that it does not come with a certificate of conditional accuracy. We normally take a small backward error to be such a certificate.

There might be applications that require a backward stable solution rather than an accurate one. Strangely, this is exactly the case with the computation of itself; the analysis in this paper relies on rows being computed in a backward-stable way, not on their forward accuracy. We are not aware of other cases where this is important.

References

- [1] David H. Bailey and Helaman R. P. Ferguson. A Strassen-Newton algorithm for high-speed parallelizable matrix inversion. In Proceedings of the 1988 ACM/IEEE conference on Supercomputing, pages 419–424, 1988.

- [2] S. D. Conte and Carl de Boor. Elementary Numerical Analysis: An Algorithmic Approach. McGraw-Hill Book Company, third edition, 1980.

- [3] Adi Ditkowski, Gadi Fibich, and Nir Gavish. Efficient solution of using . Journal of Scientific Computing, 32:29–44, 2007.

- [4] Jeremy J. Du Croz and Nicholas J. Higham. Stability of methods for matrix inversion. IMA Journal of Numerical Analysis, 12(1):1–19, 1992.

- [5] Stefan Eberli, Davide Cescato, and Wolfgang Fichtner. Divide-and-conquer matrix inversion for linear MMSE detection in SDR MIMO receivers. In Proceedings of the 26th Norchip Conference, pages 162–167. IEEE, 2008.

- [6] George E. Forsythe, Michael A. Malcolm, and Cleve B. Moler. Computer Methods for Mathematical Computations. Prentice-Hall, Inc., 1977.

- [7] Michael T. Heath. Scientific Computing: An Introductory Survey. The McGraw-Hill Companies, 1997.

- [8] Nicholas J. Higham. Accuracy and Stability of Numerical Algorithms. SIAM, second edition, 2002.

- [9] The MathWorks, Inc. M-Lint: Matlab’s code analyzer, 2010. Release 2010b.

- [10] Cleve Moler. Numerical Computing with MATLAB. SIAM, 2004.

- [11] Dianne P. O’Leary. Scientific Computing with Case Studies. SIAM, 2009.

- [12] J. L. Rigal and J. Gaches. On the compatibility of a given solution with the data of a linear system. J. ACM, 14:543–548, July 1967.

- [13] G. W. Stewart. Matrix Algorithms. Volume I: Basic Decompositions. SIAM, 1998.

- [14] V. Strassen. Gaussian elimination is not optimal. Numererische Mathematik, 13:354–355, 1969.

- [15] C. Studer, S. Fateh, and D. Seethaler. ASIC implementation of soft-input soft-output MIMO detection using MMSE parallel interference cancellation. IEEE Journal of Solid-State Circuits, 46:1754–1765, 2011.

- [16] J. H. Wilkinson. Rounding Errors in Algebraic Processes. Prentice Hall, Inc., 1963.