Potts models in the continuum. Uniqueness and exponential decay in the restricted ensembles

Abstract

In this paper we study a continuum version of the Potts model, where particles are points in , , with a spin which may take possible values. Particles with different spins repel each other via a Kac pair potential of range , . In mean field, for any inverse temperature there is a value of the chemical potential at which distinct phases coexist. We introduce a restricted ensemble for each mean field pure phase which is defined so that the empirical particles densities are close to the mean field values. Then, in the spirit of the Dobrushin Shlosman theory, [9], we prove that while the Dobrushin high-temperatures uniqueness condition does not hold, yet a finite size condition is verified for small enough which implies uniqueness and exponential decay of correlations. In a second paper, [8], we will use such a result to implement the Pirogov-Sinai scheme proving coexistence of extremal DLR measures.

1 Introduction

In this paper we consider a continuum version of the classical Potts model, namely a system of point particles in where each particle has a spin , , and particles with different spins repel each other, this being the only interaction present. When this is a simple version of the famous Widom-Rowlinson model which has been the first system where phase transitions in the continuum have been rigorously proved, [15], and for and at very low temperature, a phase coexistence between the symmetric phases for continuum Potts models was established in [11].

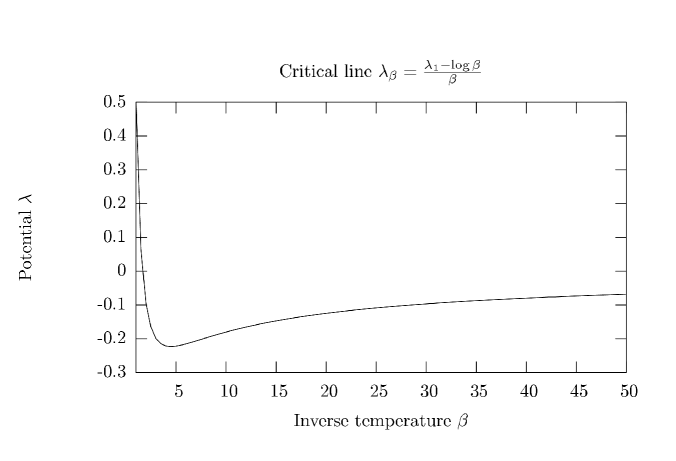

The mean field version of the continuum Potts model has been recently studied in [10]. The phase diagram has an interesting structure. In the -plane, the inverse temperature, the chemical potential, there is a critical curve, see Figure 1, above which (i.e. “large”), there is segregation, namely there are pure phases, each one characterized by having “a most populated species” (of particles with same spin). Instead, below the critical curve there is only one phase, the disordered one where the spin densities are all equal. The behavior on the critical curve depends on . If there is only the disordered phase while if there is coexistence, namely there are phases, the “ordered phases” where there is a spin density larger than all the others and the disordered phase as well.

An analogous phenomenon occurs in the mean field lattice Potts model where at a critical temperature there is a first order phase transition with coexistence of phases if , but in the continuum there is an extra phenomenon occurring at the transition, namely the total particles density has a strictly positive jump when going from the disordered to an ordered phase. This can be seen as an example of interplay between magnetic and elastic properties and interpreted as a magneto-striction effect, as the appearance of a net magnetization is accompanied by an increase of density and thus a decrease of inter-particles distances.

Our purpose is to prove that the above picture remains valid if mean field is replaced by a finite range interaction. Let , , , , a finite configuration of particles. We suppose that their energy is

| (1.1) |

where

| (1.2) |

, a Kac scaling parameter, a smooth probability kernel supported by . (Observe that is independent of the particles labeling).

To motivate the above choice recall that the mean field energy density (mean field energy over volume) is

| (1.3) |

where is the density of particles with spin . Then

| (1.4) |

Thus is the integral of the mean field free energy density, where the latter is computed using the empirical averages . If is small one may think that (1.1) “simulates mean field”. Indeed we will prove in [8] that

Theorem 1.1.

For any , and there is such that for any there exist and mutually distinct, extremal DLR measures at .

To keep the statement simple we have not reported all the information we have on the structure of the DLR measures referring to [8] for the full result. In particular we know that the particles densities are close to their mean field values (for small). The proof of Theorem 1.1 follows the Pirogov-Sinai strategy which is based on the introduction of “restricted ensembles” where the original phase space of the system is restricted by constraints which impose local closeness to one of the putative pure phases, in our case local closeness of empirical averages to the mean field values in a pure phase. We need a full control of such “restricted ensembles” and then a general machinery applies giving the desired phase transition. As a difference with the classical Pirogov-Sinai theory, here the small parameter is the inverse interaction range instead of the temperature, as we are “perturbing” mean field instead of the ground states, see for instance the LMP model, [13], where these ideas have been applied to prove phase transitions for particles systems in the continuum with Kac potentials.

In the typical applications of Pirogov-Sinai, restricted ensembles are studied using cluster expansion which yields a complete analyticity (in the Dobrushin-Shlosman sense, [9]) characterization of the system. Namely constraining the system into a restricted ensemble raises the effective temperature and the state enjoys the characteristics of high temperature systems. An analogous effect has been found in the Ising model with Kac potentials, [7], [5], and in the LMP model, in both the high-temperatures Dobrushin uniqueness condition has been proved to hold. This is a “finite size” condition, and the Dobrushin uniqueness theorem states that if such a condition is verified, then there is a unique DLR state. The importance of the result is that the condition involves only the analysis of the system in a finite box: loosely speaking it is a contraction property which states that compared with the variations of the boundary conditions, the Gibbs measure has strictly smaller changes, all this being quantified using the Wasserstein distance. Dobrushin’s high temperatures means that the size of the box [where the conditional measures are compared] can be chosen small (a single spin in the Ising case) or a small cube in LMP so that there is no self interaction in Ising or a negligible interaction among particles of the box (in LMP) and the main part of the energy is due to the interaction with the boundary conditions. The measure and its variations are then quite explicit and it is possible to check the validity of the above contraction property.

As explained by Dobrushin and Shlosman, one expects that when lowering the temperature the above high temperature property eventually fails, the point however being that it could be regained if we look at systems still in a finite box but with a larger size, eventually divergent as approaching the critical temperature. The problem is that if the finite size condition involves a large box then self interactions are important and it is difficult to check whether the condition is verified.

While it is generally believed that the above picture is correct, there are however not many examples where it has been rigorously established. Unlike Ising with Kac potentials and LMP, in an interval of values of the temperature, where the high temperature Dobrushin condition is valid in restricted ensembles, in the continuum Potts model we are considering there is numerical evidence (at least) that it is not verified. We will prove here that a finite size condition (involving some large boxes where self interaction is important) is verified in our restricted ensembles and then prove using the disagreement percolation techniques introduced in [2], [3], that our finite size condition implies uniqueness and exponential decay of correlations and all the properties needed to implement Pirogov-Sinai, a task accomplished in [8].

Part I Model and main results

2 Mean field

The “multi-canonical” mean field free energy is

| (2.1) |

where represents the density of particles with spin and the inverse temperature, to underline dependence on we may add it as a subscript. The “canonical” mean field free energy is instead

| (2.2) |

and the mean field free energy is the convex envelope of . , and , the chemical potential, are defined by adding the term , where in the case of , .

Observe that for any ,

| (2.3) |

so that if the graph of has a horizontal segment, then for any , has also a horizontal segment when , , which reduces the analysis of phase transitions to a single temperature, object of the following considerations.

As shown in [12] (see the proof of Theorem A.1 therein), the variational problem (2.2) is actually reduced to a two-dimensional problem because:

Lemma 2.1.

| (2.4) |

The analysis of (2.4) yields:

Theorem 2.2.

Let and . Then there are such that coincides with in the complement of and it is a straight line in . As a consequence there is such that has the whole interval as minimizers, it is strictly convex in the complement and .

We will next discuss the structure of the minimizers of .

Theorem 2.3.

Let , and as in Theorem 2.2. Then has minimizers denoted by , . For , and for all not equal to . Instead for all and

| (2.5) |

Finally for any the Hessian matrix is strictly positive, namely there is such that for any vector ,

| (2.6) |

The minimizers satisfy the mean field equation

| (2.7) |

The Hessian has the explicit form:

| (2.8) |

3 Restricted ensembles

The purpose of this paper is to study the system in restricted ensembles defined by restricting the phase space to particles configurations which are “close to a mean field equilibrium phase”. Unfortunately the requests from the Pirogov-Sinai theory will complicate the picture, but let us do it gradually and start by defining notions as local equilibrium and “coarse grained” variables, adapted to the present context.

3.1 Geometrical notions

We discretize by introducing cells of size , the mesh parameter will be specified in the next paragraph.

The partition

, , denotes the partition of into the cubes ( and the cartesian components of and ), calling the cube which contains .

A set is -measurable if it is union of cubes in and denotes the union of all cubes in ( the complement of ) which are connected to , two sets being connected if their closures have non empty intersection. Analogously, is the union of all cubes in which are connected to .

A function is -measurable if its inverse images are -measurable sets.

The basic scales

There are four main lengths in our analysis: . More precisely let , and verify

| (3.1) |

(the precise meaning of the inequality will become clear in the course of the proofs), then

| (3.2) |

with the additional request that is an integer multiple of which is an an integer multiple of which is an integer multiple of . The partition is coarser than if each cube of the former is union of cubes of the latter, we will then also say that is finer than . This happens if and only if is an integer multiple of , thus is finer than which is finer than which is finer than .

We will need that

| (3.3) |

Eventually we define, for any -measurable region , :

| (3.4) |

where is the volume of the region , thus is the number of blocks inside .

The accuracy parameter

Finally, the parameter in (3.1) is not related to a length, it defines an “accuracy parameter”

| (3.5) |

whose role will be specified next.

3.2 Local equilibrium

A particles configuration is a sequence such that for any compact set and any ,

| (3.6) |

We then associate to any such the empirical densities

| (3.7) |

as functions on and the “local phase indicators” first for any ( below as in Theorem 2.3)

| (3.8) |

and then for any particles configuration as above,

| (3.9) |

With and as in (3.5) and (3.2), we then define

| (3.10) |

is the restricted phase space and the configurations in are said to be in local equilibrium in the phase . Their restrictions to a -measurable set is denoted by and we will study (in the simplest case) the Gibbs measure with Hamiltonian as in (1.4) on the phase space restricted to . As mentioned in the beginning of this section to apply Pirogov-Sinai we will need to complicate the picture, by adding a “polymer structure” to the phase space and by modifying the Hamiltonian .

3.3 Polymer configurations

A polymer is a pair , , the spatial support of , is a bounded, connected -measurable region and , its specification, a -measurable function on with values in . In the applications of Pirogov-Sinai, will be contours and not as general as above, to keep it simple we skip all that sticking to the above definition. We tacitly fix in the sequel and the corresponding phase space and define:

Polymer weights

The weight of is a function , , (dependence on is not made explicit in ) which depends on the restriction of to and which satisfies the bound

| (3.11) |

Polymer configurations and weights

We denote by sequences of polymers with the restriction that any two polymers and , , are mutually disconnected (i.e. the closures of their spatial supports do not intersect and they are therefore at least at mutual distance ). The collection of all such sequences is denoted by and , a -measurable region, the subset of made by sequences whose elements have all sp in ; subset of with the further request that sp is not connected to . If is a finite sequence we define its weight as

| (3.12) |

3.4 The interpolated Hamiltonian

Pirogov-Sinai applications also require to change the Hamiltonian. Let be a bounded, -measurable region, , then the “reference Hamiltonian” in is

| (3.13) |

where is the chemical potential introduced in Theorem 2.2, is defined in Subsection 3.1, in (3.7).

For any we then define the “interpolated Hamiltonian”

| (3.14) |

where , and

| (3.15) |

as in (1.1) with such that . Since and , interpolates between the true and the reference Hamiltonians.

As we will see in [8], enters in the analysis of the finite volume corrections to the pressure, a key step in the implementation of the Pirogov-Sinai strategy.

3.5 DLR measures

The finite volume Gibbs measure in , a bounded, -measurable region, with boundary condition , is the following probability on

| (3.16) |

where the free measure is

| (3.17) |

and where the partition function is the normalization factor which makes the above a probability. In (3.16) the boundary conditions only involve particles configurations, to define the DLR measures we also need to condition on the outside polymers.

DLR measures

Given , , we call the collection of all pairs where denotes the restriction of to . We then define the probability on by

| (3.18) |

A probability on is DLR if the two properties below hold.

it verifies the Peierls bound: for any ,

| (3.19) |

for any bounded, -measurable region the conditional probability of given that the particles configurations in is and that is as given by (3.18).

A few remarks on the above definitions: the Gibbs measures satisfy the Peierls bound (3.19). Indeed given any in such that sp is not connected to sp for any , then, for any ,

and (3.19) follows from (3.11). On the other hand we have not specified all the properties of the weights as they arise in the applications (to the continuum Potts model) so that in the present context wild things may happen. For instance weights still compatible with (3.11) may be such that whenever sp contains , a bounded, simply connected measurable set, then unless sp. If the weights had such a property then there are sequences of finite volume Gibbs measures whose limits are not supported by . Thus a support property like (3.19) is necessary in the present context.

3.6 Main result

We fix , the statements below being valid for any such and for all small enough. We will employ the following notion: agrees with in ( a -measurable set) if all such that the closure of sp intersects are also in and viceversa and moreover

| (3.20) |

Theorem 3.1.

For all small enough there is a unique DLR measure and there are constants and such that the following holds. For any bounded, -measurable regions and and any boundary conditions and there is a coupling of and such that if is any -measurable subset of :

| (3.21) |

3.7 A finite size condition

The proof of Theorem 3.1 follows the Dobrushin Shlosman approach: we first introduce and verify a finite size condition and then prove that this implies uniqueness and exponential decay. In this subsection we describe the former step. Let be a -measurable, connected region contained in where is obtained by taking a cube , then considering and finally . All the bounds we will write must be uniform in such a class. Notice that the diameter of is which for small is much larger than the interaction range, in this sense is “large” and we are away from the Dobrushin’s high temperatures uniqueness scenario.

Our finite size condition involves only Gibbs measures without polymers: namely the probability on defined for any given as follows

| (3.22) |

We want to compare two such measures with different boundary conditions and , thus introducing the product space whose elements are denoted by . The finite size condition requires that there is a coupling of and with the property that the event we define below has a “large probability”.

Notation

Let and with as in Theorem 5.1 below. Call and define a partition of into the intervals , ,…,, .

Definition 3.2.

The function and the set .

We denote by

| (3.23) |

Given and , we define the function , as follows.

If then .

If and , then .

If and , call , then if for some , we set , otherwise we set .

The set , , is defined as the whole space if and otherwise by

| (3.24) |

In section 7.4, we will use Theorem 3.3 below with and . Recalling the definition of in (3.4), we state:

Theorem 3.3.

For any integer there exist and such that for all and for any with , for any and as above, there is a coupling of and such that with and defined above,

| (3.25) |

The proof of Theorem 3.3 is given in Part II of this paper. It consists of three parts, in the first one we use a step of the renormalization group to describe the marginal of over the variables . Their distribution is proved to be Gibbsian with an effective Hamiltonian at the inverse effective temperature . In a second part we study the ground states of the effective Hamiltonians, proving exponential decay from the boundary conditions. In a third and final part we bound the Wasserstein distance between the Gibbs measures by approximating the latter to Gaussian distributions describing fluctuations around the ground states characterized in the previous step.

3.8 Disagreement percolation

The finite size condition established in Theorem 3.3 is used to construct the coupling of Theorem 3.1. The proof uses the ideas introduced by van der Berg and Maes in their disagreement percolation paper, [3]. The proof given in Part III of this paper consists of two steps. In the first one we introduce set-valued stopping times, called stopping sets, and prove that monotone sequences of stopping sets define couplings of the Gibbs measures and that if the sequence stops, then in the last set there is agreement. In the second and last step we prove that the probability that the sequence stops late is related to a percolation event which is then shown to have exponentially small probability.

Part II The finite size condition

4 Effective Hamiltonians

We will use the following notations.

4.1 General notation for Part II

By default in this section is a connected, -measurable region contained in , see Subsection 3.7, and regions in are all -measurable. To discretize we will use the lattice . Thus in the sequel is the basic mesh. We define

| (4.1) |

The basic variables are the densities , , (by default variables denoted by are non negative densities). Call the set of all such that has integer values, so that is the range of values of the densities when , , ; being defined in (3.7).

To have lighter notation we will use the label for a pair , , writing , if and sometimes shorthand for and for .

denotes the Euclidean space of vectors with the usual scalar product . By an abuse of notation we also denote by the Hilbert space with above replaced by .

4.2 The effective Hamiltonian

The effective Hamiltonian , , , is defined by the equality

| (4.2) |

as in (3.14), so that is the effective inverse temperature. The Gibbs measure with Hamiltonian , inverse temperature and free measure the counting measure on is then the marginal over the variables of the Gibbs measure defined in (3.22).

Since and is small, the effective temperature vanishes as , and the analysis of the Gibbs measure becomes intimately related to the study of the ground states of . This will be the argument of the next section, in this one we determine . In this subsection we describe its main terms and state the main theorem; in the successive ones we give the proof.

The LP term.

The main contribution to the effective Hamiltonian will be the Lebowitz-Penrose free energy functional, the LP term in the title of the paragraph. This is

| (4.3) |

where we employ the usual vector notation: if is a matrix, a vector in ,

| (4.4) |

calling the vector if and otherwise. In (4.3)

| (4.5) |

The normalization is such that is a probability kernel. The term in (4.3) is “the entropy minus the chemical potential energy”:

| (4.6) |

When , is just the usual LP free energy and for this reason we call the LP term. Notice that if , then the bulk terms of which are proportional to cancel, this will play an important role in the study of the ground states.

The one body effective potential.

This term is due to second order terms in the Stirling formula when computing the entropy contribution. It has the form:

| (4.7) |

The many-body effective potential.

This term denoted by , takes into account variations of the potential energy inside the elementary cells which have been neglected in the LP term. The dependence of on is very simple, it is in fact a polynomial of order , a suitable positive integer. The coefficients of the polynomial are described next, they have a simpler form once we use Poisson polynomials. We denote by , , , the Poisson polynomial of order and, by an abuse of notation we write

| (4.8) |

We shorthand , , and call ; meaning that there is such that . Given we denote by , with positive integers, calling . We finally call and denote by the function equal to and to when , respectively ; below is a positive number . Then has the form:

| (4.9) |

are coefficients which may depend on but only if , in such a case they only depend on . The main features of the coefficients (whose dependence on is not made explicit) is that:

| (4.10) |

and

| (4.11) |

where is a constant independent of and .

Theorem 4.1.

For any there are , and coefficients as above such that for all small enough

| (4.12) |

with the remainder

| (4.13) |

Recall that in this section is a subset of thus , a constant, if we wanted larger volumes we would have to increase , namely to include more body-potentials and longer interaction range, the expansion in Theorem 4.1 being highly non uniform in . The proof which follows closely the one in [13] of a similar result, is given in the remaining subsections.

4.3 Derivation of the LP term

We fix arbitrarily , call , introduce a set of labels whose elements are denoted by , where , ; the coordinate functions on are , and respectively equal to the first, second and third entry in . We then define for (meaning ) the probability measures on as and call , remembering that this measure as well as the index set depend on the initial choice of , as this is momentarily fixed we are not making it explicit. We obviously have:

| (4.14) |

where on the r.h.s. should be thought of as a -labeled configuration of particles (the label specifying also the cube where the particle is) which is identified to the integration variable relative to the measure : thus the dependence on is hidden in the structure of the probability . The bracket on the r.h.s. is equal to

| (4.15) |

Then, recalling the Stirling formula:

| (4.16) |

we can estimate as follows

| (4.17) |

where and is equal to the r.h.s. of (4.7) with .

Proof of (4.13) for .

We now show that defined in (4.17) above satisfies the bound (4.13):

where we used the fact that , since . From this, we get

| (4.18) |

Call the energy defined with replaced by , then depends only on the densities and which in (4.14) are fixed equal to and , hence

| (4.19) |

Collecting all the above terms we thus identify in (4.14)

| (4.20) |

4.4 Cluster expansion

To estimate the r.h.s. of (4.20) we use cluster expansion. Call a set of unordered pairs , , then defines a graph structure with vertices and edges . We call diagrams the connected sets in , their collection. Call and the spaces of all possible diagrams and of all possible which appear when varying . Let

| (4.21) |

then, since is a product measure,

| (4.22) |

(4.22) is derived from (4.20) by writing

where the labels include both the particles in and those of outside . After expanding the product we then get (4.22), details are omitted.

The basic condition for cluster expansion which we have in the present context, involves the elementary diagrams namely and states that given any

| (4.23) |

(4.23) is proved by observing that the densities are bounded and that (4.21) yields for

| (4.24) |

“Cluster expansion” then applies for any small enough and the following holds (for any ).

Notation. We give a graph structure by calling vertices the diagrams and edges the pairs and which have non empty intersection, as sets in .

Denote by , , positive, integer valued functions, calling “the multiplicity” of . We restrict to where

| (4.25) |

and shorthand when sp.

Cluster expansion tells us that given any for all small enough there are coefficients , , such that

| (4.26) |

and, for any ,

| (4.27) |

where is the number of edges in . The coefficients have the following explicit expression:

| (4.28) |

where thinking of in (4.26) as a function of the weights ,

| (4.29) |

( being bounded coefficients independent of ). As said, all the above follows from the general theory (of cluster expansion) using the condition (4.23), see for instance [16].

4.5 Identification of the many body potential

We will next use (4.27) to truncate the sum in (4.26) identifying the remainder with the term and recognizing in the finite sum the Hamiltonian , for this we will use the explicit representation of the terms of the expansion provided by (4.28)–(4.29).

Calling , by (4.27), for any ,

Since , there is such that and we can then choose so large that

| (4.30) |

thus (4.13) is satisfied and

| (4.31) |

The dependence on is hidden in the space , on which the functions are defined. Theorem 4.1 will be proved once we show that the r.h.s. of (4.31) can be written as the r.h.s. of (4.9).

We rewrite the r.h.s. of (4.31) by first summing over all in “the same equivalence class” and then summing over all equivalence classes. Before defining the equivalence we observe that if is a one to one map of onto itself, then extends naturally to a map of onto itself by letting be the diagram with vertices , , and edges , the edges of . We then call if there is a one to one map from onto such that , for all ; for all .

Calling the equivalence class of , i.e. the set of all , we define the average weight

| (4.32) |

Notice that if sp consists only of such that then for all . If instead there are labels in sp such that then is a non trivial average. Actually the averages involve the labels in each triple , , with . Calling the number of such that ,

| (4.33) |

where is the Poisson polynomial and . We then have

| (4.34) |

We next interchange the sums: for any sequence , , let

| (4.35) |

then

| (4.36) |

thus identifying in Theorem 4.1 in terms of :

| (4.37) |

recalling the remark before (4.33), indeed the l.h.s. depends on only via .

Of course we still need to prove that the function defined via (4.37) satisfies the bounds stated in (4.10)–(4.11). Since the coefficients in (4.28), are bounded, say

| (4.38) |

we just need to bound . The definition of involves product of terms for each edge of the diagram which we bound using (4.24). The bound obtained in this way is the same for all so that the bound for is the same as for . To fix up the combinatorics, we proceed as follows. For any we define a graph structure on sp introducing a node for each element of sp which is then given the label , thus different nodes may have the same label. Edges in are the union of all the edges present in all the diagrams such that . Each edge is then given a multiplicity equal to the sum of all over the diagrams which contain the given edge. With this definition any gives rise to the same as we are only recording the coordinates and of .

To proceed with the bound we assign a “weight” to any node in . Having (4.24)in mind, we assign to each edge a weight , where the multiplicity of the edge. We have thus assigned a weight to equal to the product of the weights of its nodes and of its edges and, with reference to (4.35) and recalling (4.38)

| (4.39) |

Recalling that is the number of such that , is also the number of nodes in with label . Thus, calling the number of nodes in with label , , and ,

| (4.40) |

(4.37) then yields

| (4.41) |

By (4.35) the terms to consider have such that . Then if diam, being the sites appearing in , because the weight of the edges in are proportional to .

To prove (4.11) we fix and restrict the sum in (4.41) to . For each such we can then define a tree structure in with root , a first generation made by all nodes connected to the root, second generation made by the nodes connected to those of the first generation and so forth. To recover the original graph we may also have to add edges connecting individuals of the same generation and also attribute to each edge its multiplicity, as explained earlier. We then have

| (4.42) |

Define a new weight by changing the weights of the edges into

while the weights of the node are unchanged. Then

| (4.43) |

The weight of the root of the tree cancels with the prefactor . We upper bound the sum on the r.h.s. if we regard a multiple edge with multiplicity as distinct edges originating from a same node and also regard edges between nodes in the same generation as edges into the next generation (thus dropping the constraint that the arrival node is the same as the arrival node of another edge), each node added in this way getting an extra weight . In this way we have an independent branching and since

we then get (4.11), details are omitted. Theorem 4.1 is proved. ∎

5 Ground states of the effective Hamiltonian

In this section we study the ground states of the main term in the effective Hamiltonian , which, with reference to (4.12), is

| (5.1) |

While originally defined in Subsection 4.1, it is convenient here to extend the range of values of to an interval of the real line. We thus call

The ground states in the title are then the minimizers of as a function on with regarded as a parameter.

Let be the function defined as in Definition 3.2 but with the set in (3.23) replaced with the set

| (5.2) |

Our main result is the following theorem:

Theorem 5.1.

There are and positive such that for any and for all small enough the following holds. For any there is a unique minimizer of . Let , be as above and and the minimizers with and , then for any :

-

•

(i) If , .

-

•

(ii) If , , with same bound for .

Existence of a minimizer follows from being a smooth function on a compact set of the Euclidean space. Uniqueness and exponential decay are more difficult and the proof will take the whole section. The basic ingredient is that (the Hessian matrix of the derivatives w.r.t. the variables ) computed on the minimizer in the constraint space is positive and “quasi diagonal”, which would then give the required uniqueness and exponential decay if we had . This is however not necessarily the case because the minimum could be reached on the boundaries of the domain of definition, which, on the other hand, is necessary to ensure convexity. We will solve the problem by relaxing the constraint and then studying the limit when the cutoff is reconstructed.

5.1 Extra notation and definitions

The basic notation are those established in Subsection 4.1, here we add a few new ones specific to this section:

We will write where, recalling (4.12),

| (5.3) |

To evidentiate some of the variables in , say those in , we write , where and are the restrictions of to and respectively to .

It will be convenient to relax the constraint by enlarging into

| (5.4) |

where has been chosen such that

We then introduce a cutoff parameter (which will eventually vanish), call , and define for any , the function on as

| (5.5) | |||||

Since [] is a continuous function of which varies on a compact set, it has a minimizer denoted by [], and we will later see that this minimizer is unique. We call its extension to the whole , by setting on . Here is the density associated to via (3.7) with , thus of course depends on .

For any -measurable set we write for any differentiable and -measurable function

| (5.6) |

5.2 A-priori estimates

In this subsection we prove some a-priori bounds on . When we loose the bound valid at but, as we will see, we have the great simplification to know that for small enough, minimizers are critical points, thus satisfying , and .

Lemma 5.2.

There is a constant such that for all and for any minimizer of the following holds: for all and all ,

| (5.7) |

In particular, if then for all small enough, any minimizer of is also a critical point.

Proof. We denote by

Then for all ,

and since vanishes on :

and, calling ,

and in conclusion

| (5.8) |

and (5.7) follows because and are bounded proportionally to the cardinality of .

By choosing so small that , we conclude that is in the interior of and is thus a critical point. ∎

Lemma 5.3.

converges by subsequences and any limit point is a minimizer of .

Proof. Convergence by subsequences follows from compactness and by (5.7) any limit point is in . Now for any , we get and by taking along a convergent subsequence . ∎

A minimizer of is not necessarily a critical point, i.e. , the equality may fail if the minimizer is on the boundary of the constraint. In such a case however, the gradient if different from zero “must be directed along the normal pointing toward the interior”.

Lemma 5.4.

Any minimizer of , is “a critical point” in the following sense:

If for some , (strictly!), then

| (5.9) |

If instead , then

| (5.10) |

5.3 Convexity and uniqueness

Convexity is a key ingredient in our analysis:

Theorem 5.5.

Proof. Recalling (5.3) and denoting by below the diagonal matrix with entries

and get a lower bound by dropping the last term thus reducing the proof to the case . Extend and as equal to 0 outside and set

where is defined in (4.1). Then,

recalling(2.8), by (2.6) the curly bracket is non negative as well as .

Since for each

then

Thus

Recalling (A.2), (A.3) and using (4.9)–(4.11) we get

Thus

(5.11) is then proved recalling the assumption .

∎

Theorem 5.6.

Proof. We interpolate by setting , , then calling we have

By (5.7) for small enough and for as well, so that by (5.11)

Moreover . In fact, if and is a minimizer of , by Lemma 5.2 (for small enough) is also a critical point and . If and a minimizer of then by Lemma 5.4, which, for the same reason, holds if is a critical point of in the sense of Lemma 5.4.

∎

Corollary 5.7.

For any and small enough the minimizer of is unique, same holds at for . For (and small enough) there is a unique critical point in the space ; such a critical point minimizes . Analogously, when there is a unique critical point in the sense of Lemma 5.4. Such a critical point minimizes . The minimizer of , , converges as to the minimizer of .

Proof. From Lemma 5.2 it follows that any minimizer of is also a critical point and verifies (5.7), so for all and all , and we can apply Theorem 5.6 to the matrix . If we assume that there are two minimizers, then (5.12) gives a contradiction. The proofs in the case follows by using Lemma 5.3.∎

5.4 Perfect boundary conditions

In this subsection we restrict to “perfect boundary conditions”, by this meaning that we study

| (5.13) |

namely we replace in the LP term of the effective Hamiltonian, see (4.12), by the mean field equilibrium value. is then defined by adding to the term given by (5.5). All the previous considerations obviously apply to and .

Theorem 5.8.

For any small enough and for all small enough, the minimizer of minimizes as well and it is such that

| (5.14) |

a constant.

Proof. Since is a minimizer of , . Then if (5.14) holds, and by Corollary 5.7 is a minimizer of . We thus have only to prove (5.14) for all small enough. Consider first the simplified problem with .

Case

Recalling (4.3), if , then by an explicit computation, for all ,

| (5.15) |

where if and if . is a solution of (5.15) and therefore also a solution of (with ). By Corollary 5.7 it is then the unique minimizer of and (5.14) is proved (for ).

Proof of (5.14).

Call

; for all small enough denote by the minimizer of , so that . Suppose that

| (5.16) |

Obviously while because of the above analysis with . Then

| (5.17) |

On the other hand by differentiating we get

| (5.18) |

By Lemma 5.2 and Theorem 5.5 for all small enough, is symmetric and positive definite, then by Theorem A.3 the inverse is well defined and bounded as an operator on , and we thus get from (5.18)

| (5.19) |

which by (5.17) yields (5.14). (5.19) also implies that . Notice that (5.19) implies (5.16), but unfortunately the argument is circular as it started by supposing the validity of (5.16). To avoid the impasse we start from the equation in the unknown

| (5.20) |

where is considered as a “known term” such that for all . From what said before, (5.20) has a unique solution called and

| (5.21) |

Since is Lipschitz in (we omit the details) the ordinary differential equation

| (5.22) |

has a unique solution . Then, by (5.20),

| (5.23) |

Since , as well, hence by Corollary 5.7, and by (5.22) it is differentiable with continuous derivative. (5.16) thus holds and the theorem proved. ∎

5.5 Exponential decay

This subsection concludes our analysis with the following main theorem, Theorem 5.1 will be proved in the Subsection 5.6 as a corollary, taking as a neighborhood of in and .

Theorem 5.9.

There are and positive such that the following holds. Let and be the minimizers of , respectively , with . Then for any partition of into two -measurable sets and ,

| (5.24) |

Proof. We follow the interpolation strategy used in the proof of Theorem 5.8. To this end we separate the “interaction part” in writing where is independent of the boundary conditions while

| (5.25) |

where is given by the r.h.s of (4.9) with the sum over restricted to the set .

We then interpolate between the two boundary conditions

| (5.26) |

The analysis done in the previous subsections, applies to as well. Thus the minimizer of is unique, is a critical point, namely and satisfies for all and all , .

We can apply the same proof as the one given in Theorem 5.8. In fact by Theorem 5.5, for all small enough, and for all such that , we have that is symmetric and positive definite, then by Theorem A.3 the inverse is well defined and bounded as an operator on . Thus the equation

| (5.27) |

has a unique solution that we call that is Lipschitz in . This implies that the equation

has a unique solution that coincides with the minimizer . Thus is differentiable in and satisfies

| (5.28) |

By Corollary 5.7, converges by subsequences as to a limit which minimizes , so that

| (5.29) |

We now estimate uniformly in and to prove (5.9) as a consequence of (5.29).

Equations for .

we let

| (5.30) |

so that (5.28) becomes

We also define:

| (5.31) |

is a diagonal matrix whose diagonal elements are

| (5.32) |

To distinguish among large and non large (called small) values of , we introduce a large positive number which will be specified later and, calling the Hilbert space of vectors ,

| (5.33) |

Let be the orthogonal projection on and , thus selects the sites where is large and those where it is small.

Our strategy will be the following: rewrite as linear expressions of to get bounds on (and therefore on ) using knowledge on .

Rewriting in terms of .

Since the matrices are diagonal they commute, giving for instance , i.e.:

| (5.34) |

and symetrically:

| (5.35) |

Using together with (5.34) we get:

| (5.36) |

where is invertible on the range of since is a positive matrix.

Using together with (5.36) and (5.35)we get:

Let

| (5.37) |

so that if is invertible on the range of (as we will prove), then

| (5.38) |

A decomposition of .

Recalling (5.30) and (5.26), after expanding the Poisson polynomials in (4.9) we get,

| (5.39) | |||||

where if and , when . The coefficients satisfy the same bounds as the coefficients of (4.9) (with maybe a different constant).

Shorthand by the sites in which are in , noticing that by definition of there are not terms with .

We then call the sum of minus the second sum on the r.h.s. of (5.39) restricted to sets such that: and any is either in or , , (or both). .

By linearity where and are defined with replaced by and and we will bound differently and using norms for the former and norms for the latter.

Bounds on .

By Theorem A.1 if is large enough and ,

| (5.40) |

Moreover by (A.5)

| (5.41) |

Then applying Theorem A.2,A.3 with as in (5.37) and , is invertible and there is a constant such that . Therefore there is a new constant such that

| (5.42) |

If , and as well, let us then suppose . Then (5.39) yields

| (5.43) |

To bound we go back to (5.36), the same arguments used before prove that as well, so that is bounded as on the r.h.s. of (5.43) (with a new constant ) and is therefore bounded as the first term on the r.h.s. (5.9), we will prove next that is bounded as the second term on the r.h.s. (5.9) which will then be proved.

Bounds on .

Recalling the definition of

| (5.44) |

where and if , and suitable constants.

By Theorem A.2

| (5.45) |

By (5.45) and (5.44), calling and ,

| (5.46) |

By (A.5)

| (5.47) |

and since if and ,

Thus supposing , we get from (5.38)

| (5.48) |

To bound (recall (5.36)) we use (5.47) to get

| (5.49) |

while, using (5.48) and (5.47),

hence

| (5.50) |

∎

5.6 Proof of Theorem 5.1

The proof is a corollary of Theorem 5.9. Indeed given any , call the union of all , . Then if , same notation as in Theorem 5.9, and by (5.9) we are reduced to a sum over . We split the exponent into two equal terms and get

| (5.51) |

The exponent in Theorem 5.1 is thus going to be half the of Theorem 5.9. Using Theorem 5.9 with replaced by , and calling the corresponding minimizer,

and using (5.14)

6 Local Couplings

In this section we prove Theorem 3.3, thus we fix a region , union of a finite number , of cubes of and two boundary conditions , . We also fix a and we consider the two Gibbs measures defined in (3.22) and with state space . The aim is to construct a coupling of these two probabilities such that (3.25) holds. , being a joint distribution, is defined on the product space whose elements are denoted by .

6.1 Definitions and main results

Recalling that is defined in Definition 3.2 we denote by

| (6.1) |

In order to prove Theorem 3.3 we have to find a coupling so that there is such that

| (6.2) |

We define (recall that is the ball of center and radius ),

| (6.3) |

and we observe that , dist.

We denote by

| (6.4) |

and in the sequel we will consider only those such that for all and ,

Given and any subset we will call the restriction to of .

Given a subset , we call the following metric on :

| (6.5) | |||

| (6.6) |

We call the corresponding Wasserstein distance between two measures and in :

| (6.7) | |||||

where the inf runs over all possible joint distributions (couplings) of and .

In Subsection 6.3 we prove the following Theorem.

Theorem 6.1.

Given union of cubes of there is such that for all , , the following holds.

Given any , such that ( defined in (6.3)), the following holds.

Calling , for any two configurations , on , we denote by , .

Let , be the probabilities , conditioned to have the configuration in equal to and occupation numbers in given by .

Then for defined in (6.1)

| (6.8) |

The next result, proved at the end of Subsection 6.6, deals with the Wasserstein distance of the distributions of the occupation numbers that in Theorem 6.1 have been set equal to each other inside . For these variables the metric defined in (6.6) is replaced by

Theorem 6.2.

Given union of cubes of there is such that the following holds. Let , be the marginals of , on the variables defined in (6.4).

Then

| (6.9) |

6.2 Two properties of the Wasserstein distance in an abstract setting

Let be a complete, separable metric space with distance and let be the corresponding Wasserstein distance between two measures and . Thus

| (6.10) |

where the inf runs over all possible joint distributions of and .

Theorem 6.3.

Let be a given positive measure on . Let and be such that for all ,

| (6.11) |

Set

| (6.12) |

Then

| (6.13) |

where, after fixing arbitrarily an element , we have called .

In particular,

| (6.14) |

Proof. Let

is a coupling of and and therefore

having bounded and integrated over the missing variable.

(6.13) is then obtained by writing .

∎

The following estimate is taken from [14]:

Theorem 6.4.

Let be a measurable set, a probability on and the probability conditioned to . Then

| (6.15) |

Proof. Let

where is the probability supported by . Let be any bounded, measurable function on , then

Hence is a coupling and

which proves (6.15). ∎

Eventually, we mention the following elementary property:

Proposition 6.5.

Assume that the distance satisfies . Then for all probability measures and for all

| (6.16) |

Proof.

Without loss of generality we assume . Remarking that , we get for any coupling of

| (6.17) |

and the proposition is proved by taking the infimum over all possible couplings . ∎

Remark 6.6.

The proposition above states that Wasserstein distances associated to very particular distances are finer than the total variation distance . In the following, we will use this property for , remarking that .

6.3 Couplings of multi-canonical measures

Here we prove Theorem 6.1. Recalling that , we fix two boundary conditions , . We have to compare the marginal distributions of , over the configurations in (i.e. well inside ). Since the probabilities , depend only on the restrictions of to where the corresponding occupation numbers in the two measures are all equal to each other. We will thus study couplings of multi-canonical measures, hence the title of the Subsection.

It is now convenient to label the particles. To this purpose we use a multi-index , where is the cube of where the particle is; is its spin and distinguishes among the particles in the same cube with same spin. We call the set of labels

Observe that is determined by and we thus have the same labels for the two measures. Given we denote by a vector configuration with . We then denote by a vector configuration in . Analogously we define . We then call the energy defined in (3.14) and with fixed as above.

Calling

| (6.18) |

we define

| (6.19) |

Remark 6.7.

If is a measurable subset of , then denotes all labels with and the marginal of over the unlabeled configurations is the original multi-canonical measure in .

We will use the Dobrushin high-temperature techniques which allow to reduce to a comparison of the conditional probabilities of a single variable .

Proposition 6.8 (Dobrushin high-temperature theorem).

There is such that the following holds. For all , , all and all and

| (6.21) |

where

Proof. The probabilities to compare have the form

while

where and hence

Remark 6.9.

From the proof above, we see that the r.h.s of (6.21) is actually proportionnal to . In other terms, the effective temperature of the system is of order and thus very high indeed.

Corollary 6.10.

With defined by (6.20), there is such that for all small enough the following holds:

| (6.22) |

Proof. For and as in Proposition 6.8 we call (which is the r.h.s. of (6.21)). Then there is such that for all small enough the following holds:

The first inequality follows from the Dobrushin high-temperature theorem (Proposition 6.8) while the second one is obvious once (which is satisfied for all small enough). ∎

6.4 Taylor expansion

In this subsection we consider the marginal of on the variables , , . By an abuse of notation we denote also the marginal with .

The following holds:

Proposition 6.11.

Proof. By (4.13) there is such that

| (6.26) |

By (6.26) and Theorem 6.3, there is a (different) constant such that

| (6.27) |

Hence the triangular inequality implies (6.25).∎

We will bound by using the triangular inequality to replace the two measures by their Taylor approximants.

We first prove the following result true for any -measurable region .

Theorem 6.12.

For any , calling , the following holds.

There are and that verifies (6.29) below, so that, calling the minimizer of

| (6.28) |

We bound the partition function as follows, with a small constant to be chosen later:

so that

Remark now that

with , and . Choosing such that , i.e.

| (6.29) |

which is always possible (see (3.3)), we get as . The Theorem is now proved with , which is always possible for small enough.∎

We call the minimizer of , . We then let

| (6.30) |

Proposition 6.13.

For all , ,

| (6.31) |

where are the probabilities conditioned to , .

Analogously to (6.3) we define the following subset of .

| (6.32) |

and we observe that , dist. We also have

Lemma 6.14.

Let be as in Theorem 5.1. Then for all .

Proof. Let , by definition of , if then . Assume then that . By (6.32) and (6.3) there is such that , thus and therefore . By definition of we then have that and also that with where is given by . Then , that implies that . ∎

Recalling that is the minimizer of , , we observe that in general the gradient of (see (5.6) for notation), evaluated at does not vanishes in all . However, by Theorem 5.1 and Lemmas 5.4, 6.14 it follows that .

being defined by Theorem 4.1, we set and define

| (6.33) |

Thus in while for all and . We denote by the common value, thus

| (6.34) |

We also define the matrix with entries:

| (6.35) |

Observe that . We denote by the two matrices restricted to which are then equal; their common entries are then

| (6.36) |

We define for

| (6.37) |

and the probabilities

| (6.38) |

where is the characteristic function of the set :

The following holds:

Proposition 6.15.

For all , , and for all if is small enough the following holds:

| (6.39) |

Proof. We Taylor expand and we call the third order.

| (6.40) |

Observe that in and for a suitable constant

and conclude that the right hand side of the above inequality is estimated by as soon as satisfies

| (6.41) |

Since and , by applying Theorem 6.3 with and we get that

| (6.42) |

From Lemma 6.14 and (i) of Theorem 5.1 we get that given any for small enough.

By applying Theorem 6.3 with and we get that

| (6.43) |

By using the triangular inequality we then get (6.39).∎

6.5 Quadratic approximation in continuous variables

In this subsection we consider the conditional probabilities , , . Since , and recalling (6.34) and (6.36), we have that

| (6.44) |

where is the matrix restricted to and where, as usual, is the sum over of the numerator on the right hand side of (6.44).

We compare the probabilities with measures with the same energy but with continuous state space. To define these measures we start by setting some notations.

By convenience we consider the variables , thus . Since , defined in (6.44) have support on , the variables are such that

| (6.45) |

where is the integer part of ( as in Theorem 6.12).

We call with

| (6.46) |

and we denote by . In this new variables the boundary conditions become

| (6.47) |

By an abuse of notation we call the distribution of the variables under the probabilities defined in (6.44), thus

| (6.48) |

where is the sum over of the numerator.

We next introduce variables which take values in the interval of the real line:

| (6.49) |

and we call

| (6.50) |

We next define the probabilities measures on as

| (6.51) |

where and is the integral of the numerator.

Proposition 6.16.

For all , recalling (6.47) the following holds:

| (6.52) |

Proof. Given we call we define as

| (6.53) |

and the following probabilities on

| (6.54) |

By continuity there is a point such that

| (6.55) |

Therefore

| (6.56) |

where is the vector defined as the gradient of with respect to the variables and is the norm of the vector .

Since then

| (6.57) |

For small , thus by Theorem 6.3 and the triangular inequality we get

| (6.58) |

We now observe that at any coupling of and we can associate a coupling of and by setting

To prove that is indeed a coupling of and we compute for any function on

Thus

| (6.59) |

We next observe that

Taking the over the coupling in the above inequality and using (6.59), we get that , thus (6.58) implies (6.52). ∎

6.6 Gaussian approximation

We now extend the measures on to a measures , , on the full Euclidean space, thus , are the Gaussian measure defined by the r.h.s. of (6.51) without the last characteristic function.

Thus letting ,

| (6.60) |

with the integral of the numerator.

The following holds:

Proposition 6.17.

There is such that the following holds:

| (6.61) |

Proof. By the Chebischev’s inequality, and recalling that , there is such that

By (6.29) there is such that

| (6.62) |

Since is equal to the probability conditioned to the set , by using Theorem 6.4 and the triangular inequality, we get (6.61). ∎

We are thus left with the estimate of that we do next.

Proposition 6.18.

There is such that the following holds:

| (6.63) |

Proof. We first observe that from the definition of the Wasserstein distance

| (6.64) |

where is the restriction of to , namely . Thus the inf on the r.h.s. of (6.64) can be restricted to all couplings of the marginals on the set of the probabilities , .

We next call the matrix with entries , , , , , denotes the restriction to of .

Then remark that marginals of Gaussian variables are Gaussian themselves, so we get:

| (6.66) |

We use that the Wasserstein distance is related to the variational distance via the following relation

| (6.67) |

where

| (6.68) |

We now prove that

| (6.69) |

To prove (6.69) we interpolate defining , . Then, shorthanding ,

| (6.70) |

Using Cauchy-Schwartz the r.h.s. is bounded by

| (6.71) |

hence (6.69).

To estimate , we apply Theorem A.1 with , the identity matrix, and with , observing that whenever . Thus from (A.10) and (A.5), using that , , (6.47) and (6.45) we get that there are and , such that for all and since dist

Thus this inequality together with (6.67) and (6.69) implies (6.63). ∎

Proof of Theorem 6.2. Recalling the definition (6.38) of the probabilities , and the conditional probabilities defined in (6.44), from Propositions 6.16, 6.17, 6.18 we get that for all , ,

Thus, there is a coupling of the conditional probabilities , such that

| (6.72) |

We define for all

We then define a coupling of the measures by letting

| (6.73) |

From (6.27), (6.72) and Theorem 6.12 it follows that

| (6.74) |

Observe that (6.74) implies that

| (6.75) |

Then, (6.75), Propositions 6.11, 6.13, 6.15 implies (6.9). ∎

6.7 Proof of Theorem 3.3

We need to construct a coupling such that (6.2) holds.

Recall and that for any two configurations , on we denote by , . From Theorem 6.1 we have that, for any , there is a coupling of the two conditional Gibbs measures , such that

| (6.76) |

Given and , we define a coupling of , , by setting

From Theorem 6.2 there is a coupling of , such that

| (6.77) |

Then the final coupling is defined as follows:

| (6.78) |

Thus from (6.76) and (6.77) we get

| (6.79) |

To complete the proof of (6.2) we need to show that

| (6.80) |

Since in the set on the l.h.s. of (6.80), , by using (6.27) we have

| (6.81) |

From Theorem 6.12 and (ii) of Theorem 5.1 it follows that for all and for or ,

| (6.82) |

Part III Disagreement percolation

In this part we fix , a bounded -measurable region , ; and stand for the measures and . They are obtained by conditioning measures and which could be either DLR measures or Gibbs measures with . We will first construct a coupling of and and, with the help of such a coupling, we will then define a coupling of and proving that it satisfies the requirements of Theorem 3.1. The notation which are most used in this part are reported below.

Main notation and definitions.

We call

| (6.83) |

Given a measurable subset of and , we call its restriction to . Namely if , then

| (6.84) |

We will say that we vary in if we change leaving invariant.

We denote by the product space,

| (6.85) |

Given a subset and , we call its restriction to .

We call the -algebra of all Borel sets in and for any measurable set in we call the -algebra of all Borel sets such that does not vary when we change in .

7 Construction of the coupling

The target of this section is to construct a “good” coupling of and . The basic idea is to implement the disagreement percolation technique used in van der Berg and Maes, [3], Butta et al., [6], Lebowitz et al,[13]. The first step is to introduce a sequence of random sets , which is done in the next subsection. We will then introduce the notion of “stopping sets” and “strong Markov couplings” showing that the sets are indeed stopping sets and, using the strong Markov coupling property, we will finally get the desired coupling of and .

7.1 The sequence

We will define here for each a decreasing sequence of -measurable sets , which are therefore set valued random variables. We set and for , define , thus the sequence is defined once we specify the “screening sets” . Screening sets are defined iteratively with the help of the notion of “good” and “bad cubes”.

After defining in an arbitrary fashion an order among the cubes of , for any -measurable set , we start the definition by calling bad all the cubes of . We then select among these the first one (according to the pre-definite order) which intersects a polymer (i.e. either , or ), if there is no such cube we then take the first cube in . Call the cube selected with such a rule. We then define and call bad all cubes of if intersects a polymer. If not, we say that a cube is good if and if

| (7.1) |

otherwise is called bad. In this way each cube of is classified as good or bad and therefore all cubes of are classified as good or bad. We then select in in the same way we had selected in , and the cubes of are then classified as good or bad by the same rule used for those of . By iteration we then define a sequence which becomes eventually constant, as it stops changing at if has no bad cube or if is empty. Since has cubes, is certainly constant after , but maybe even earlier. In Appendix B we will prove:

Theorem 7.1.

If the sequence stops at and is non empty, then

| (7.2) |

and

| (7.3) |

7.2 Stopping sets

The random variables are “stopping sets” and the sequence is decreasing, , in the following sense.

-

•

, a measurable subset of , is the algebra of all Borel sets such that does not change if we vary in .

-

•

A random variable with values in the measurable subsets of is called a stopping set if for all ,

(7.4) -

•

Two stopping sets and are such that if

7.3 Strong Markov couplings

A coupling of and is called strong Markov in , a stopping set, if the measure

| (7.5) |

is also a coupling of and for all couplings of , and .

Theorem 7.2.

Given any stopping set , let be a coupling of and which is strong Markov in , Then any coupling defined by (7.5) is strong Markov in provided the stopping set is such that ,

Proof. We have to prove that for any family of couplings , the probability defined as

| (7.6) |

is a coupling of and . We thus take a function and we prove that , where , , is the expectation of under , respectively .

Using that is a stopping set we get

We now rewrite by using its definition (7.5) and since we get

| (7.7) |

Observe that (recalling )

| (7.8) |

We insert (7.8) in (7.7) and we get

The Theorem is proved.∎

7.4 Construction of couplings

We use the sequence of decreasing stopping sets (in the order ) and Theorem 7.2 to construct a sequence of couplings of and , the desired coupling will then be , where . The sequence is defined iteratively by setting equal to the product coupling: which, as it can be easily checked, is strong Markov in . Then for any we set

| (7.9) |

where is the marginal of over and , , is the coupling of , and defined next. We distinguish three cases according to the values of .

-

•

If is such that either , or , or both, then is the product coupling: .

-

•

If is such that and then , namely is the coupling supported by the diagonal.

-

•

Finally let be such that but . Call , . Let be the product of the marginal distributions of and over . Let be the coupling defined in Theorem 3.3 and letting , we denote by the characteristic function of the set .

Then we define

By Theorem 7.1 the second case above occurs if and only if all cubes of are good, while in the third case there are bad cubes in so that is non empty. The proof that cubes are good with large probability will be based on Theorem 3.3 and the following lemma:

Lemma 7.3.

Suppose and that the third case above is verified, namely is such that and . Suppose also that . Let in , then is good if for all , as in (3.2).

Proof. The proof follows from the definitions of good cubes and because for all , . ∎

8 Probability estimates.

Recall from the beginning of Part III that and are obtained by conditioning to the configurations outside the measures and which are either DLR measures or Gibbs measures with . Thus if is the coupling of and defined in Subsection 7.4, we obtain a coupling of by writing

| (8.1) |

We will prove here that there is a constant such that for all small enough, for any -measurable subset of :

| (8.2) |

This proves that and agree in , in the sense of (3.20), with probability from which Theorem 3.1 follows. Indeed if and are two DLR measures, by the arbitrariness of and , (8.2) shows that , hence that there is a unique DLR measure. If instead and are two Gibbs measures and , , then (8.2) yields (3.21).

8.1 Reduction to a percolation event

Denote by the union of all bad cubes contained in and of the cubes in with a polymer, namely those cubes such that , in . Since by its definition any screening set is connected to a bad cube and since any bad cube in is necessarily contained in a screening set, it follows that if then it is connected to .

Since the event in (8.2) is bounded by

| (8.3) |

, it is therefore also bounded by the event that the bad cubes percolate from to . Hence, denoting in the sequel by a connected, -measurable subset of ,

| (8.4) |

We write , the union of cubes of “type ”. Cubes of type 1 are those with a polymer, namely is type 1 if there is in such that . is type 2 (also called unsuccessful) if , say in , is bad and all cubes of are without polymers (in the above sense). Cubes of type 3 are the remaining ones, they are therefore in the union of all with connected to a type 1 bad cube. Then calling ,

| (8.5) |

Since ,

| (8.6) |

Therefore and

| (8.7) |

We are thus reduced to estimate for any ,

| (8.8) |

8.2 Peierls estimates

We bound here where is some given set in . Thus each cube is either contained in sp, or in sp, (or both). Thus

| (8.9) |

where . Let , disjoint cubes of , then, since and satisfy the Peierls estimates,

| (8.10) |

for all small enough. Thus

| (8.11) |

8.3 Probability of unsuccessful cubes

We will bound here . Given any we define

| (8.12) |

| (8.13) |

will be specified later. We are going to prove that for all ,

| (8.14) |

where is the expectation with respect to . Since and , we then get from (8.14),

| (8.15) |

Recalling (8.1), we set and for ,

| (8.16) |

calling the expectation w.r.t. . We have , hence by (7.9),

| (8.17) |

where . The last integral is equal to 1 if , while, if this is not the case, by (3.25)

| (8.18) |

We then get from (8.17),

| (8.19) |

We choose

| (8.20) |

so that the on the r.h.s. of (8.19) is 1 which thus proves (8.14) and (8.15).

8.4 Proof of Theorem 3.1

As we have shown at the beginning of this Section, Theorem 3.1 follows from (8.2) that we prove here.

Part IV Appendices

Appendix A Operators on Euclidean spaces

For the sake of completeness we recall here some elementary properties of operators on finite dimensional Hilbert spaces used in the previous sections. We call the real Hilbert space of vectors with scalar product

| (A.1) |

where above ranges in a finite index set on which a distance is defined (in our applications stands for a pair , with , and either or , being a fixed -measurable bounded subset of . Operators on are identified to matrices by setting . We write ,

| (A.2) |

Recall that

| (A.3) |

The first inequality in (A.3) is obvious. To prove the second one we write

In Theorem A.1 below we consider matrices of the form , thus including (after restricting to ) and , the matrix considered in (5.37). With in mind these two applications we will suppose the diagonal elements of strictly positive and large.

Theorem A.1.

Let with , a diagonal matrix, and suppose there are , and such that the following holds (recall the definition of the norm given in (A.3)).

| (A.4) |

The diagonal elements of are such that for every . Finally whenever . Then if is large enough,

| (A.5) |

Proof. By (A.3), . On the other hand and for so large that the sum on the r.h.s. of (A.6) below converges and

| (A.6) |

as seen by multiplying the r.h.s. of (A.6) from the left by : we then get which is equal to 1 after writing and after telescopic cancellations. Thus (A.6) holds and

| (A.7) |

hence, recalling (A.3), we get the first inequality in (A.5). We write

Since , by (A.6)

hence the second inequality in (A.5).

∎

In the next two theorems we consider a matrix with small norm, it represents in our applications the matrix which by Theorem A.1 has indeed a small norm (if is large).

Theorem A.2.

Let ; suppose symmetric, for all ; and . Then is invertible and

| (A.8) |

Suppose further that

| (A.9) |

then

| (A.10) |

Proof. By the integration by parts formula,

| (A.11) |

Since ,

| (A.12) |

Then is well defined and equal to ; (A.8) also follows.

Calling the vector with components ,

| (A.13) |

By (A.12),

| (A.14) |

By a Taylor expansion:

| (A.15) |

hence using (A.9),

| (A.16) |

∎

Theorem A.3.

Let as in Theorem A.2; call the diagonal part of , , and suppose that . Then

| (A.17) |

∎

Appendix B Proof of Theorem 7.1

In the sequel cubes are always cubes in and a cube is called “older” than if there is such that and . We will prove the theorem as a consequence of the following property:

Property P. Let be a good cube, , the cubes older than which intersect . If either is empty or if all are good, then .

Before proving Property P, we will use it to prove Theorem 7.1. Suppose that for some , is non empty and that all cubes in are good (thus the sequence stops at ). Let be a cube in , and at distance from . Then intersects only cubes of , which are by assumption good; then by Property P, , hence (7.2). (7.3) holds because all cubes of are good.

We start the proof of Property P by introducing a new function , . We set outside and at all which are in bad cubes. The definition of on the good cubes is given iteratively in . We thus suppose to have already defined on all cubes of and have to define it on . Let thus and . We set if , otherwise

| (B.1) |

To compute the value of , , , we need to look at all sequences such that: , is older than , and to know whether the cubes are good or bad. In principle the sequence may be arbitrarily long but in fact it is not:

Lemma 1. Let be a good cube, , then the value of depends only on whether the cubes are good or bad, where is the collection of cubes older than which intersect .

Proof. Since any ball of radius intersects at most cubes of the partition , then any sequence as above consists at most of elements. ∎

Since , then

| either or | (B.2) |

We will next prove:

Lemma 2. Let be a good cube, , then, if ,

| (B.3) |

Proof. The proof is by induction on the “age” of the cubes. We thus suppose that the above statements holds for all cubes of . Let be a good cube in , then the above properties hold by the definition of the function and of good cubes. ∎

Property P is then an immediate consequence of Lemma 2 and (B.2).

Appendix C Mean field

In this appendix we prove Theorems 2.2 and 2.3. Our approach is based on the recent works [12, 10], having in mind that in [12] the total density was set to , the temperature being the free parameter, while here we fix the (inverse) temperature , the total density being the free parameter. The two approaches are equivalent, see (2.3).

To achieve our goal, we will need Lemmas C.1, C.2, C.3, C.4 and C.5 below. The first lemma is an essential property relating the total density to the corresponding constrained minimizer in a one-to-one way. The second and third lemmas respectively deal with the first and second derivatives of the free energy. They show in particular that the sign of the second derivative depends on the roots of some peculiar second degree polynomial. The fourth lemma studies the locations of these roots, while the fifth and last lemma gives a general condition for a piecewise-convex function to have a common tangent at two different points.

The section is organized as follows. We first give some notations and reformulate known results, before stating our auxiliary lemmas. Then we prove Theorems 2.2 and 2.3, while the proofs of lemmas are deferred to the end of the present section.

Notations

For any , we will denote by the density vector defined as follows:

| (C.1) |

Notice that and rewrite (2.4) as follows:

| (C.2) |

Now, remarking that , we adapt a result from [10, 12]. Namely, recalling Theorem A.1 in [12] or section 3 in [10], and comparing (C.3) and (C.4) below with (A.10) and (A.22) in [12], we know that for any there exists a threshold

| (C.3) |

such that

-

•

for all , the function reaches its minimum at ;

-

•

for all , the function reaches its minimum at , defined as the largest solution of the equation where

(C.4) -

•

at , the function reaches its minimum at and at .

The statement above means that we have

| (C.5) |

First of all, we will see that

Lemma C.1 (Monotony of and ).

The functions and are both increasing respectively on and , where . They satisfy the relations and .

Moreover

Lemma C.2.

| (C.6) |

| (C.7) |

Lemma C.3.

| (C.8) | ||||

| (C.9) |

where denotes the roots of the second degree polynomial given by

According to Lemma C.3, the convexity properties of will follow from the position of the roots of with respect to . We will actually prove the lemma below

Lemma C.4 (Roots of ).

The roots of the polynomial are such that and

-

•

for any , and for all , ;

-

•

for any , there exists a unique such that . Moreover, on and on .

Eventually, the following fact will be helpful to analyze the convex envelope of :

Lemma C.5.

Let and be convex functions with continuous second derivatives. If and if , then there exists a common tangent to their respective graphs .

We are now ready to prove our theorems.

Proof of Theorem 2.2. By (C.8), is strictly convex. Let us now study the convexity of . Fixing we remark that Lemma C.1 implies and so that Lemma C.4 gives:

-

•

for all , ;

-

•

if then ;

-

•

if , if and if , where .

Therefore, (C.9) shows that if then is strictly convex on , while if then is strictly concave on and strictly convex on .

Let us analyze the convex envelope of .

- •

-

•

If we first have to deal with the concave part of . We introduce the function defined by

Since , is convex and has continuous second derivatives. Moreover, on , the graph of is a line located above the graph of (concavity of ); since the latter intersects the (convex) graph of , the graph of and the graph of intersect at some point with abscisse . Besides, the concavity of implies , while the convexity of implies . Thus Lemma C.2 shows that Lemma C.5 applies to and defined above.

In any case, Lemma C.5 implies that there exists a line which is simultaneously tangent to the disordered branch of (at some point ) and to the ordered branch of (at some other point ). The function being strictly convex outside , the graph of its convex envelope necessarily coincides with (resp. with the graph of ) inside (resp. outside) . Denoting by the slope of , the convex envelope of is horizontal on and strictly convex outside this segment of minimizers. ∎

Proof of Theorem 2.3. If is a minimizer of , then is a minimizer of so that . If , then ; if , then there exists such that , where exchanges the first and the coordinates. Reciprocally, the above vectors are all minimizers of . Moreover,

thus proving (2.5).

We now show the second part of Theorem 2.3 dealing with the Hessian of . Straightforward computations show:

Since is a minimizer, is semi-definite positive. Actually, is definite positive, or else the third order corrections in the Taylor–Lagrange formula would contradict the extremality of :

Taking an orthonormal basis of eigenvectors, the estimate (2.6) holds with the smallest eigenvalue of .∎

This section ends with the proofs of Lemma C.1, Lemma C.2, Lemma C.3, Lemma C.4 and Lemma C.5 which are stated at the beginning of the section and used in the proofs above.

We now show that is always positive:

We see immediately that for all , so that increases on . On this subinterval, is thus minimal at where it takes the value

which increases with , vanishes at , and is strictly positive for all . From this it follows that is strictly positive on , which implies that is strictly increasing with . Since goes to when , Lemma C.1 is proved.∎

Proof of Lemma C.2.

Using (C.11) and recalling that , we have for all :

| (C.12) | ||||

| (C.13) |

From (C.4), we know that , thus

| (C.14) |

From Lemma C.1, as thus (C.7) follows from (C.10) - (C.13). Similarly, as , thus (C.6) follows by taking limits in (C.10) and (C.14). ∎

Proof of Lemma C.3.

First notice that (C.8) follows from (C.10). Using (C.12) we get:

where we used ( by abusing notations) and (from (C.4)). This achieves the proof of (C.9).∎

Proof of Lemma C.4.

-

•

roots of