Beyond Discretization: Learning the Optimal Solution Path

Qiran Dong Paul Grigas Vishal Gupta

University of California, Berkeley University of California, Berkeley University of Southern California

Abstract

Many applications require minimizing a family of optimization problems indexed by some hyperparameter to obtain an entire solution path. Traditional approaches proceed by discretizing and solving a series of optimization problems. We propose an alternative approach that parameterizes the solution path with a set of basis functions and solves a single stochastic optimization problem to learn the entire solution path. Our method offers substantial complexity improvements over discretization. When using constant-step size SGD, the uniform error of our learned solution path relative to the true path exhibits linear convergence to a constant related to the expressiveness of the basis. When the true solution path lies in the span of the basis, this constant is zero. We also prove stronger results for special cases common in machine learning: When and the solution path is -times differentiable, constant step-size SGD learns a path with uniform error after at most iterations, and when the solution path is analytic, it only requires . By comparison, the best-known discretization schemes in these settings require at least discretization points (and even more gradient calls). Finally, we propose an adaptive variant of our method that sequentially adds basis functions and demonstrate strong numerical performance through experiments.

1 Introduction

Many decision-making applications entail solving a family of parametrized optimization problems:

| (1) |

where is an arbitrary set of parameters indexing the problems. (We assume Equation 1 admits an optimal solution for each .) In such applications, we often seek to compute the entire solution path in order to present experts with a portfolio of possible solutions to compare and assess tradeoffs.

As an example, consider the -norm fair facility location problem (Gupta et al., 2023), which minimizes facility opening costs while incorporating -regularization to promote fairness across socioeconomic groups. Since there is no obvious choice for , we might prefer computing solutions for all and allowing experts to (qualitatively) assess the resulting solutions. Many other applications entail navigating similar tradeoffs, including upweighting the minority class in binary classification to tradeoff Type I and II errors or aggregating features to increase interpretability at the expense of accuracy. In each case, we seek the entire solution path because selecting the “best” solution requires weighing a variety of criteria, some of which may be qualitative. These settings differ from classical hyperparameter tuning where there is a clear auxiliary criterion (like out-of-sample performance), and it would be enough to identify the single such that optimizes this criteria.

The most common approach to learning the entire solution path is discretization: discretize , solve Equation 1 at each grid point, and interpolate the resulting solutions. With enough grid points, interpolated solutions are approximately optimal along the entire path. Several authors have sought to determine the minimal the number of discretization points needed to achieve a target level of accuracy, usually under minimal assumptions on . Giesen et al. (2010) considers convex optimization problems over the unit simplex when and show that learning the solution path to accuracy requires at least grid points. Giesen et al. (2012) consider the case where is concave in and and show only points are needed. More recently, Ndiaye et al. (2019) relate the required number of points to the regularity of , arguing that if is uniformly convex of order , one requires points.

A potential criticism of this line of research is that the computational complexity of these methods depends not only on the number of grid points but also depends on the amount of work per grid point, e.g., as measured by the number of gradient calls used by a first-order method. Generally speaking, these methods do not share much information across grid points, at most warm-starting subsequent optimization problems. However, gradient evaluations at nearby grid points contain useful information for optimizing the current grid point, and leveraging this information presents an opportunity to reduce the total work.

1.1 Our Contributions

We propose a novel, simple algorithmic procedure to learn the solution path that applies to an arbitrary set . The key idea is to replace the family of problems in (1) with a single stochastic optimization problem. This stochastic optimization problem depends on two user-specified components: a distribution over values of and a collection of basis functions , . We then seek to approximate as a linear combination of basis functions, , where and is an approximate solution to

| (2) |

In contrast to discretization schemes which only leverage local information, (stochastic) gradient evaluations of Equation 2 inform global structure. Moreover, through a suitable choice of basis functions, we can naturally accomodate complex sets in contrast to earlier work that only treats . Finally, any stochastic optimization routine can be used on Equation 2 beyond just SGD (see, e.g., Lan (2020); Bottou et al. (2018), among others).

Despite its simplicity, our approach can approximate the solution path to higher accuracy than discretization with fewer gradient evaluations. See Figure 1 for a sample of our numerical results on weighted binary classification using SGD to solve Equation 2. We prove this behavior is typical. Loosely,

-

i)

When using constant step-size SGD to solve Equation 2, we prove that the uniform error of our learned path to the true path exhibits linear convergence to an irreducible constant that is proportional to the expressiveness of the basis (Theorem 3.4). This behavior is already visible in Figure 1.

The proof of this result utilizes ideas from the convergence of SGD under various “growth conditions” of the gradient (Bottou et al., 2018; Nguyen et al., 2018; Vaswani et al., 2019; Liu et al., 2024; Bertsekas, 1996). See Khaled and Richtárik (2020) for a summary and comparison of these various conditions. Our contribution to this literature is to relate the expressiveness of the basis to a relaxed, weak-growth condition of Gower et al. (2019, Lemma 2.4). Indeed, we show that under some assumptions, Equation 2 always satisfies this relaxed weak-growth condition, and if the solution path lies in the span of the basis, it satisfies the weak-growth condition of Vaswani et al. (2019). This allows us to leverage results from those works to establish Theorem 3.4.

In special cases, we can leverage a priori knowledge of the structure of to prove stronger results. For example, suppose , and we use Legendre polynomials as our basis. We prove that

-

ii)

If the solution path is -times differentiable, then using polynomials ensures that after gradient calls, we obtain an -approximation to the solution path (Theorem 4.3).

For comparison, Ndiaye et al. (2019) implies that when is strongly-convex, discretization requires at least points. Hence, even if the optimization problem at each grid point can be solved with gradient evaluation, our approach requires asymptotically fewer evaluations whenever . If is large, the savings is substantive.

-

iii)

If the solution path is analytic (), then using basis polynomials ensures that after iterations, we obtain an -approximation to the solution path (Theorem 4.5).

This is almost exponentially less work than discretization.

These specialized results strongly suggest that in the general setting our approach should be competitive as long as we use enough basis functions. This observation motivates a natural heuristic in which we adaptively add basis functions whenever the stochastic optimization routine (e.g., SGD) stalls (see Algorithm 1 and Section 5 for details). We illustrate this idea in Figure 1 (orange line) where we can see that by progressively adding functions we drive the uniform error to zero rapidly.

1.2 Other Related Work

There are some works that consider the total computational work to learn a solution path, typically focusing on a specific choice of . See, e.g., Tibshirani (1996); Cortes and Vapnik (1995); Rosset (2004); Rosset and Zhu (2007); Friedman et al. (2010); Osborne et al. (2000); Hastie et al. (2004); Efron et al. (2004); Mairal and Yu (2012); Tibshirani and Taylor (2011); Ndiaye and Takeuchi (2021) for results on LASSO and regularized SVM; Park and Hastie (2007); Bao et al. (2019) for results on -regularization. Liu and Grigas (2023) study a regularization path setting from an ordinary differential equations perspective using second-order methods. Overall, our work is similar to this larger stream in that we focus on total computational cost, but, unlike this stream, we develop a general-purpose framework with minimal assumptions on .

2 Model Setup and Preliminaries

We denote the -norm by throughout. We focus on the case of smooth, strongly convex functions:

Assumption 2.1 (Uniform Smoothness and Strong Convexity).

There are constants such that, for all , is -strongly convex and -smooth, i.e., for all ,

For any candidate solution path , we define the solution path error of by

An -solution path is a solution path such that . Finally, given any vector of coefficients and basis functions , we define to be the solution path error of .

As mentioned, our method depends on two user-chosen parameters: a distribution over and a series of basis functions , for . We require some minor assumptions on these choices:

Assumption 2.2.

(Distribution, Basis Functions, and Linear Independence).

-

i)

It is easy to generate i.i.d. samples from .

-

ii)

It is easy to compute for any , and .

-

iii)

There does not exist with such that holds -almost everywhere.

This last condition is a linear independence assumption. If violated, one can remove a function without affecting the span of the basis on the support of .

Given , we define the minimal solution path error for this basis by

We also define the following auxiliary constants:

| (3) | ||||

In words, is a uniform bound on the largest eigenvalue of the positive semidefinite matrix , and is the smallest eigenvalue of the corresponding expected matrix. By construction, . Under Assumption 2.2, both constants are strictly positive.

Lemma 2.3 (Positive Spectral Values).

If Assumption 2.2 holds, then .

We can now state our first key result which relates the suboptimality of a feasible solution in Equation 2 to its solution path error. Define

Theorem 2.4 (Relating Suboptimality to Solution Path Error).

Under Assumptions 2.2 and 2.1, for any , we have

This bound decomposes into two terms, one proportional to , which represents the suboptimality of and the other proportional to , which measures the maximal expressiveness of the basis. By solving Equation 2 to greater accuracy, we can drive down the first term, but we will not affect the second term. To reduce the second term, we must add basis functions to obtain a better quality approximation.

Theorem 2.4 shows any algorithm for solving Equation 2 can be used to approximate the solution path. In the next section, we argue that when is small, constant step-size SGD for Equation 2 exhibits linear convergence to a constant proportional to , making it an ideal algorithm to study.

3 SGD to Learn the Solution Path

In this section, we apply constant step-size SGD to solve Equation 2. The key idea is to show that Equation 2 satisfies a certain growth condition and apply Gower et al. (2019, Theorem 3.1). One minor detail is that Gower et al. (2019) proves their result under a stronger “expected smoothness” condition for the setting where the objective Equation 2 is a finite sum. However, the result holds more generally under a weaker condition (Eq. (9) of their work). Hence, for clarity, we first restate this condition and the more general result.

The following definition is motivated by Gower et al. (2019, Lemma 2.4):

Definition 3.1 (Relaxed Weak Growth Condition (RWGC)).

Consider a family of functions , , and . Let . Then, and are said to satisfy the relaxed weak growth condition with constants and , if for all ,

When , Definition 3.1 recovers the weak growth condition of Vaswani et al. (2019). In this case, the variance of the stochastic gradients goes to zero as we approach an optimal solution. Hence, at optimality, not only is the expectation of the gradient zero, but it is zero almost surely in . For regression problems, this condition corresponds to interpolation.

Definition 3.1 is implied by a standard second moment condition on the gradients (take ). However, the most interesting cases are when is small relative to and . (This will be the case for Equation 2. See Section 3.1.)

We then have the following theorem.

Theorem 3.2 (Gower et al. (2019)).

Suppose that the RWGC holds for the family of functions , and that is -strongly convex for some for some . Consider the SGD algorithm, initialized at , with iterations

where is a random sample and parametrizes the step-size. Then for all , we have

In other words, constant step-size SGD under the RWGC exhibits a “fast” linear convergence in expectation up to a constant that is directly proportional to , after which it stalls. When , we exactly recover the result of Vaswani et al. (2019). To keep the exposition self-contained, we provide a proof in the appendix.

3.1 Solving Equation 2 with SGD

We next prove that Equation 2 satisfies RWGC, and in particular, that the “” term depends on , the minimal solution path error of the basis. To our knowledge, we are the first to make this observation.

Define

| (4a) | ||||

| (4b) | ||||

Lemma 3.3 (Equation 2 satisfies RWGC).

Suppose that Assumptions 2.2 and 2.1 hold and recall the constants defined in Equation 3. Then, the family of functions and the function , defined in Equation 4, satisfy the relaxed weak growth condition (RWGC) with constants and . Namely, for all ,

In addition, is -strongly convex.

We now combine Theorems 2.4, 3.2 and 3.3 to yield our main result: a bound on the expected solution path error for constant step-size SGD. Recall constant step-size SGD in this setting yields the iteration

where

and . We assume that the gradient is easily computable for any and .

We then have:

Theorem 3.4 (Expected Solution Path Error Convergence for SGD).

Under Assumptions 2.2 and 2.1, consider applying SGD to Equation 2 with a constant step-size parameterized by . Then, after iterations, the expected solution path error is at most

In particular, when , then for ,

When , then for any and ,

Theorem 3.4 highlights the role of the basis functions in our results. First we see that as , the expected solution path error plateaus at a constant proportional to . As mentioned, measures the expressiveness of the basis, and we expect to be small as we add more basis functions. We interpret as a condition number for Equation 2, which also depends on the choice of basis through Equation 3. This constant increases as we grow the basis. Finaly, the iteration complexity scales linearly with this condition number. Thus, an “ideal” basis must navigate this tradeoff between and .

Fortunately, there exists a rich theory on function approximation that studies the relationship between basis functions, uniform error, and eigenspectra. In the next section we leverage this theory to provide a comparison of our method with existing discretization techniques in a specialized setting.

4 Specialized Results for

We next leverage results from function approximation theory to bound the number of basis functions needed to achieve a target solution path error. We focus on the case as it facilitates simple comparisons to existing results and elucidates key intuition.

We use a simple basis: we approximate each component of by the first Legendre polynomials. Hence the total number of basis functions is . Recall, the Legendre polynomials form an orthogonal basis on with respect to the uniform distribution, i.e., , where and are the and Legendre polynomial, respectively. Since we approximate each component separately, the matrix is block-diagonal, with d blocks of size .

For this basis, depending on the value of implied by the choice of , let refer to the constants (3). We can bound the constant :

Lemma 4.1 ( for Legendre Polynomials).

Take and to be the uniform distribution on . Then, for the above basis,

Notice, that this constant is independent of and grows mildly with . This is not true of all polynomial bases. One can check empirically that for the monomial basis, grows exponentially fast in .

Bounding depends on the properties . As a first example,

Lemma 4.2 ( for -Differentiable Solution Paths).

Let . Suppose Assumption 2.1 holds and that there exists an integer and constant such that for all , has derivatives and the derivative is -Lipschitz continuous. Then, for any , for the basis described above,

The proof of Lemma 4.2 is constructive; we exhibit a polynomial with the given solution path error.

Combining these lemmas with Theorem 3.4 allows us to calculate the requisite basis size and number of iterations needed to achieve a target solution-path error:

Theorem 4.3 (SGD for -differentiable Solution Paths).

Let , be the uniform distribution on . Then, under the conditions of Lemma 4.2, if we use polynomials in the previous basis, and run constant-step size SGD for iterations, the resulting iterate satisfies .

For clarity, both big “Oh” terms should be interpreted as , and both suppress constants not depending on (but possibly depending on ). Loosely, the theorem establishes that the “smoother” is (i.e. larger ), the fewer iterations required by our method to achieve a target tolerance.

Recall, Ndiaye et al. (2019) established that for strongly convex functions, discretization requires at least points. One might expect the number of gradient evaluations per point to scale like . Hence, if , our approach requires asymptotically less work. The larger , the larger the savings.

This gap is particularly striking . As a second example, suppose is analytic on , i.e, its Taylor Series is absolutely convergent on this interval.

Lemma 4.4 ( for Analytic Solution Paths).

Suppose Assumption 2.1 holds and that for each , is analytic on the interval . Then, there exist constants and such that for any , with the basis described above,

The proof is again constructive. The constants and pertain to the analytic continuation of to the complex plane. Importantly, the solution path error now dies geometrically fast (like ). Using this faster decay rate yields,

Theorem 4.5 (SGD for Analytic Solution Paths).

Let , and be the uniform distribution on . Then, under the conditions of Lemma 4.4, if we use polynomials in the previous basis, and run constant-step size SGD for iterations, the resulting iterate satisfies .

Again, the big “Oh” hides constants that do not depend on . Compared to Ndiaye et al. (2019), the amount of work almost exponentially smaller.

5 An Adaptive Algorithm

Although the previous section’s specialized results provide theoretical insight, they do not suggest practical algorithms. Picking the number of basis apriori from approximation theory is difficult. This challenge motivates our algorithm Algorithm 1, where the number of basis functions is determined “on the fly.” To implement Algorithm 1, one needs to specify i) a sequence of basis functions ii) a distribution and iii) a criterion for deciding when to add a new basis function. We next discuss these choices.

Although any basis and distribution can be used in Algorithm 1, we suggest making these choices in concert. In our experiments we focus on sequences of polynomials that are orthogonal with respect to . The Legendre polynomials and the uniform distribution on is one such pair, but there are many canonical examples including Hermite polynomials with the normal distribution and Laguerre polynomials with the exponential distribution. There are performance-optimized implementations of these families in standard software (see, e.g., scipy.special). Although polynomials map to , by approximating each dimension separately as in Section 4, we can extend these polynomials to a basis for . Finally, polynomials are uniform function approximators for Lipschitz functions. Thus, the class is highly expressive.

Two other advantages of orthogonal polynomials in Algorithm 1 are: i) Extending the basis does not require altering existing basis functions. This is unlike, e.g., cubic splines or adding nodes to a neural network, where the addition of a new spline point affects previous bases. ii) Intuitively, orthogonality suggests that if is near optimal in the iteration, then is likely to be close to optimal in the iteration. Thus, we benefit from warmstarts.

We next discuss the criterion for adding a new basis function. One approach is to empirically approximate the objective of Equation 2 using a hold-out validation set, and add a basis function when performance stalls. This approach requires additional functional evaluations and samples . In our experiments, we explore an alternate criterion motivated by the RWGC. Specifically, if is near-optimal, the upperbound on the second moment of the gradient in RWGC is approximately constant. Thus, we add a basis function when second moment of the gradient averaged over recent iterations has plateaued. This allows us to reuse gradients and additional function evaluations.

6 Numerical Experiments

We next empirically compare i) our approach using a fixed, large basis (denoted LSP for “Learning the Solution Path”) ii) our adaptive Algorithm 1 (denoted ALSP for “Adaptive LSP” and iii) uniform discretization, a natural benchmark. We aim to show that both our approaches not only outperform the benchmark but that the qualitative insights from our theoretical results hold for more general optimization procedures than constant step-size SGD. We also provide preliminary results on how the choice of basis affects performance.

We choose uniform discretization for our benchmark in lieu of other schemes (like geometric spacing) because i) it matches the theoretical lower bound from (Ndiaye et al., 2019) and ii) we see it as most intuitive for learning the solution path with small uniform error. Specifically, for various , we consider a uniform spacing of size in each dimension of , and run (warm-started) gradient descent for iterations. The constant here is calibrated in an oracle fashion to achieve a solution-path error of (see Section B.1 for details) giving the benchmark a small advantage.

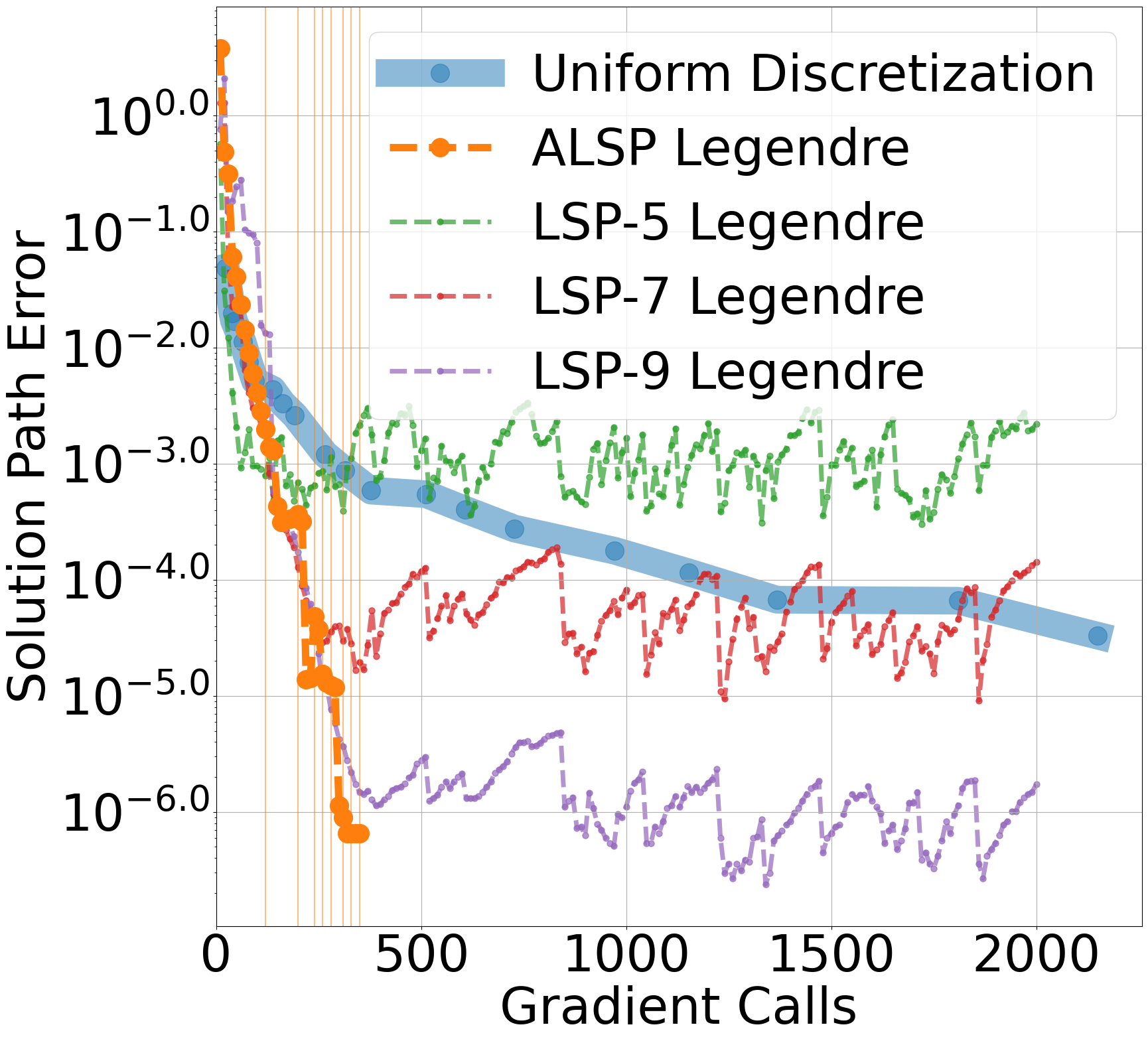

6.1 Weighted Binary Classification

We consider a binary classification problem using a randomly selected subset of cases from the highly imbalanced Law School Admission Bar Passage dataset (Wightman, 1998). Of the cases, there are positive instances and negatives. Standard logistic regression predicts positives with a false positive rate of . When identifying students likely to fail is key, the default classifier may not be useful. Reweighting cases is a standard approach to improve false positive rate at the cost of overall accuracy.

We take

where and denote the log-likelihood on the positive and negative classes respectively. Specifically, letting for denote the data,

and similarly for .

The hyperparameter controls the weight placed on each class. We use (scaled and shifted) Legendre polynomials with a distribution.

The ground truth is computed via iterations of (warm-started) gradient descent over a uniform grid of points. Solution path error is approximated by the uniform error over this grid.

For LSP, we run SGD using torch.optim.SGD. In lieu of a constant learning rate, we dynamically reduce the learning rate according to the Distance Diagnostic of Pesme et al. (2020, Section 4). This dynamic updating is more reflective of practice. We use the suggested parameters from Pesme et al. (2020) with the exception of , which we tune by examining the performance after iterations. (We take ) For ALSP, we initialize the algorithm with polynomials and stop it after adding polynomials.

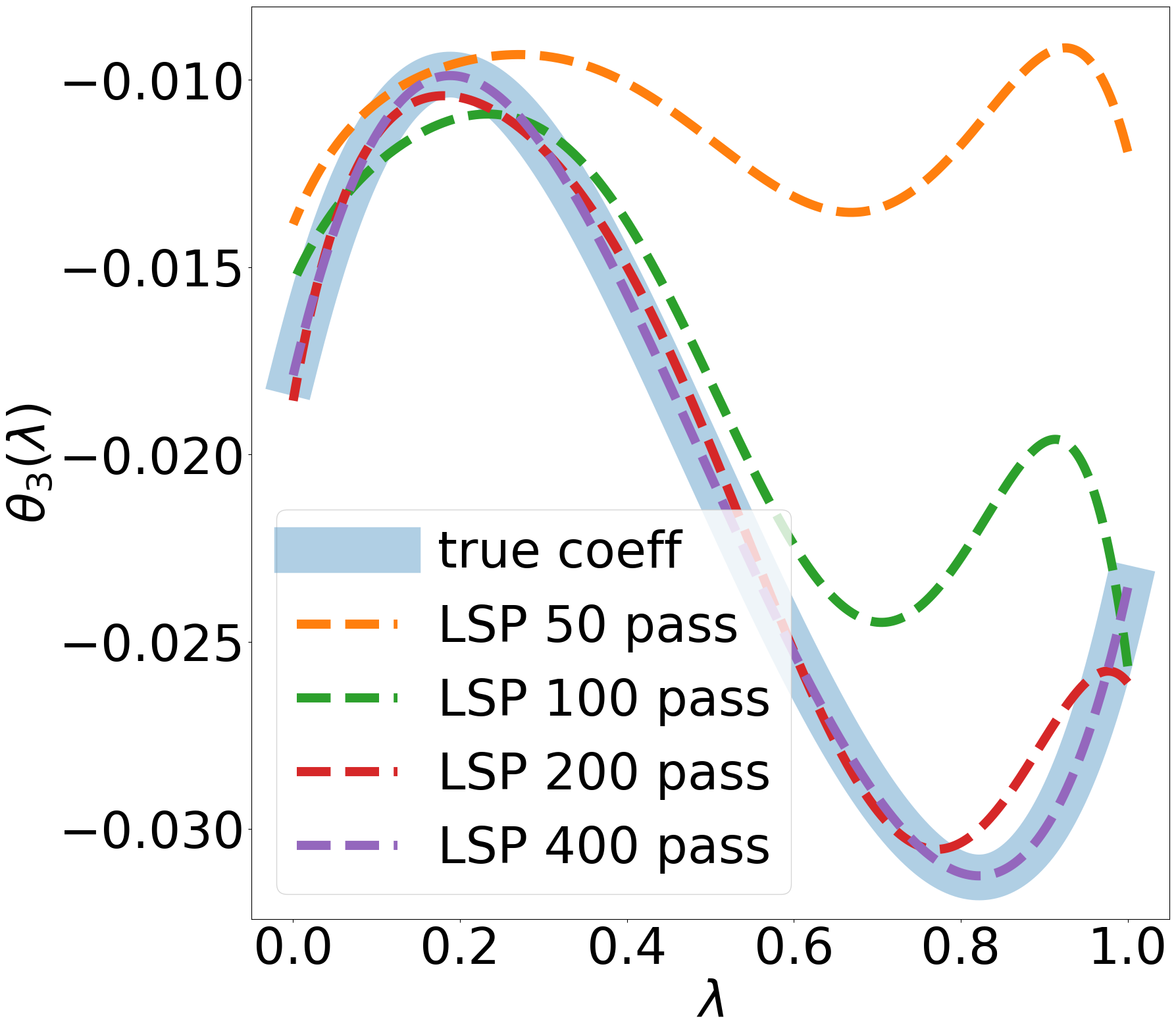

Figure 1 in the introduction shows the performance for LSP. As we can see, LSP methods converge rapidly to an irreducible error, and this error decreases as we add basis functions. Our adaptive method converges rapidly. This performance is resonated by Figure 2, where we plot the coefficient profile for when using polynomials. The approximation improves as we increase the number of iterations, and eventually become closely aligned with the true solution path.

Practically, this experiment suggests that when the region of is compact, taking to be uniform paired with a polynomial basis is favorable. The polynomial basis can then be taken to be orthogonal to as discussed in Section 5.

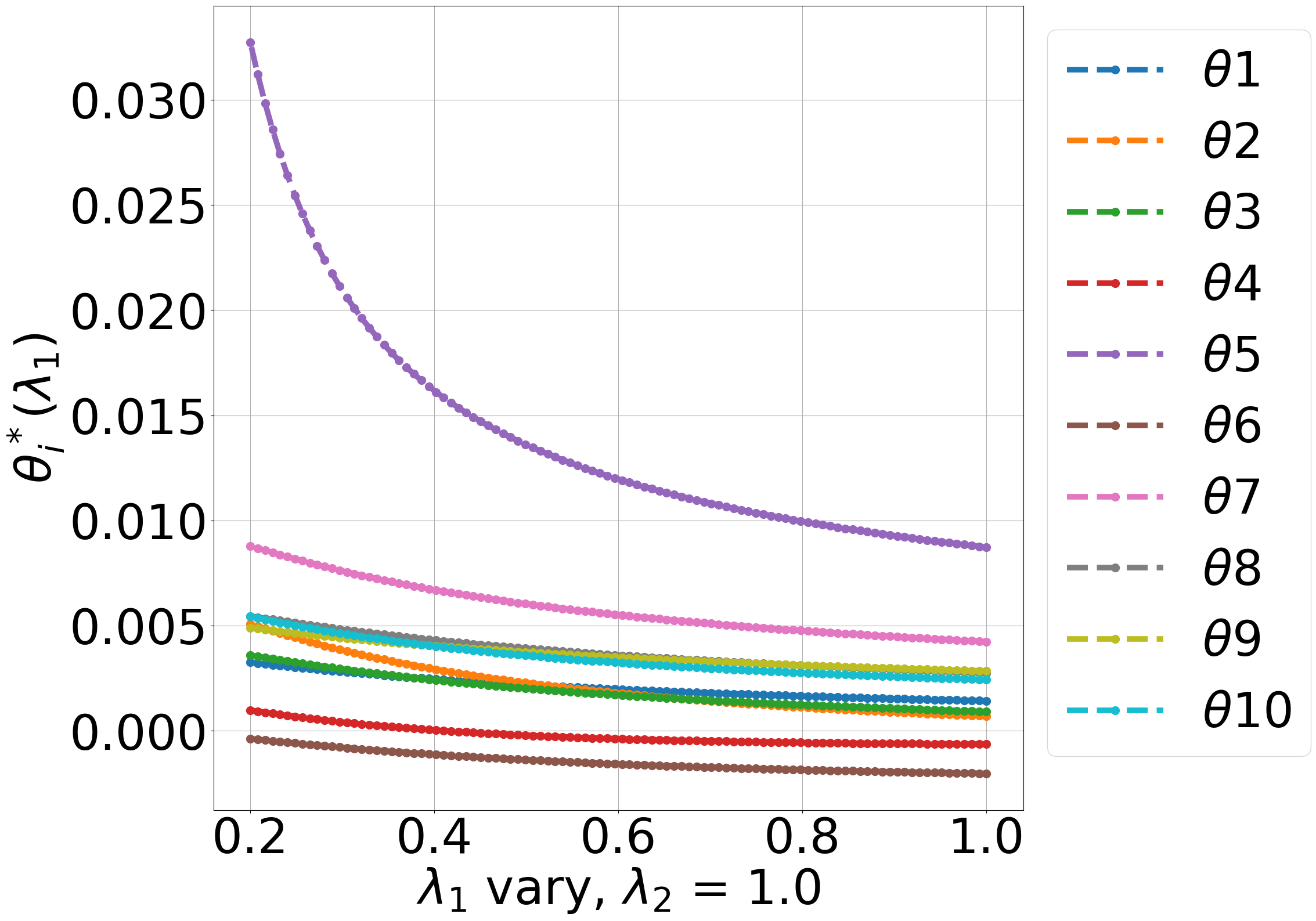

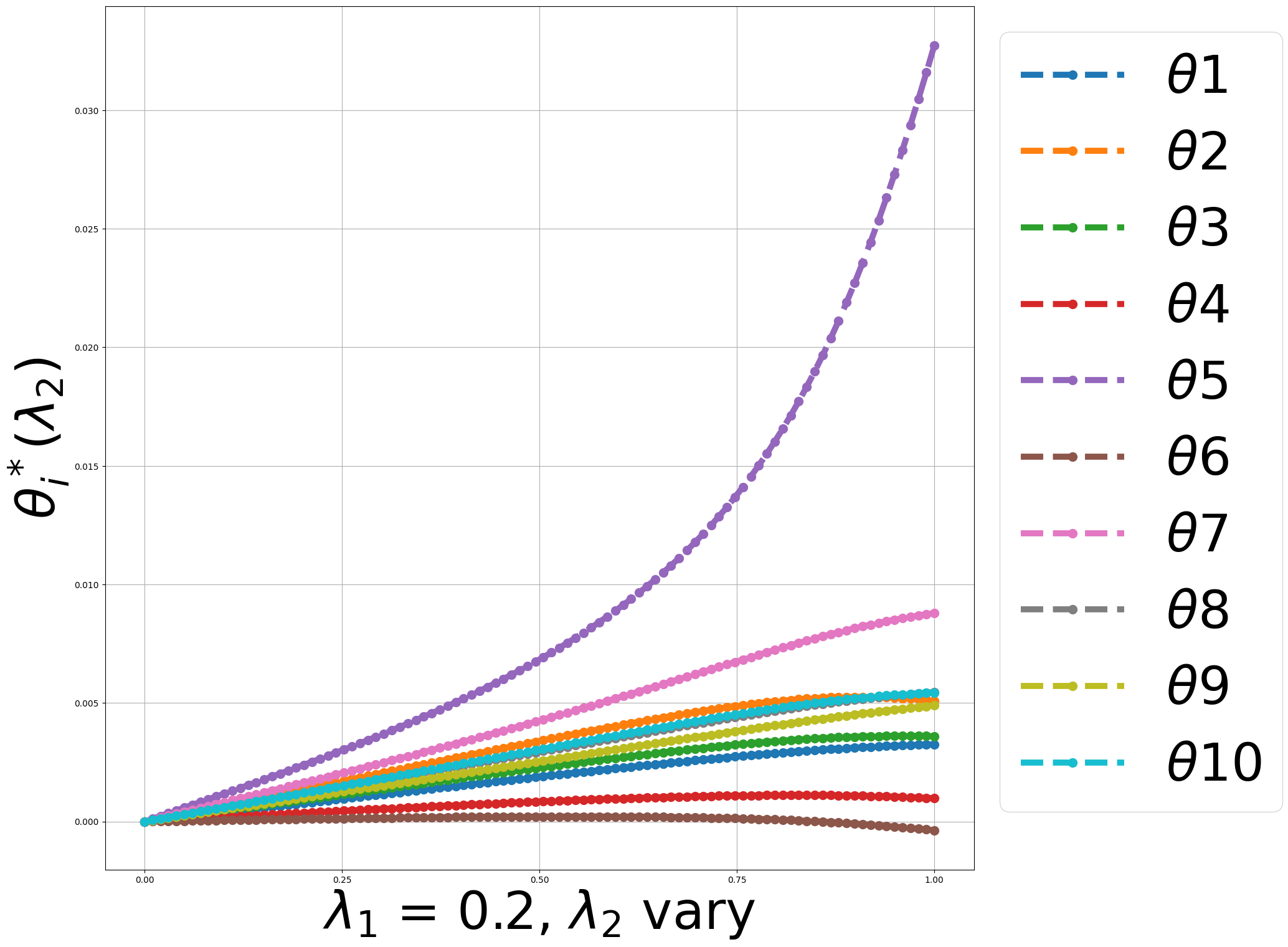

6.2 Portfolio Allocation

We next consider a portfolio allocation problem calibrated to real data where represents the weights on different asset classes. Namely, let and be the mean and covariance matrix of the returns of the different asset classes. We fit these parameters to the monthly return data from Aug. 2014 to July 2024 using the Fama-French 10 Industry index dataset.111https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html

We then solve

Here the first term represents the (negative) expected return, the second represents the risk (variance) and the third is a smoothed version regularization to induce sparsity. Namely, The parameters and control the tradeoffs in these multiple objectives.

Ground truth is computed over a grid.

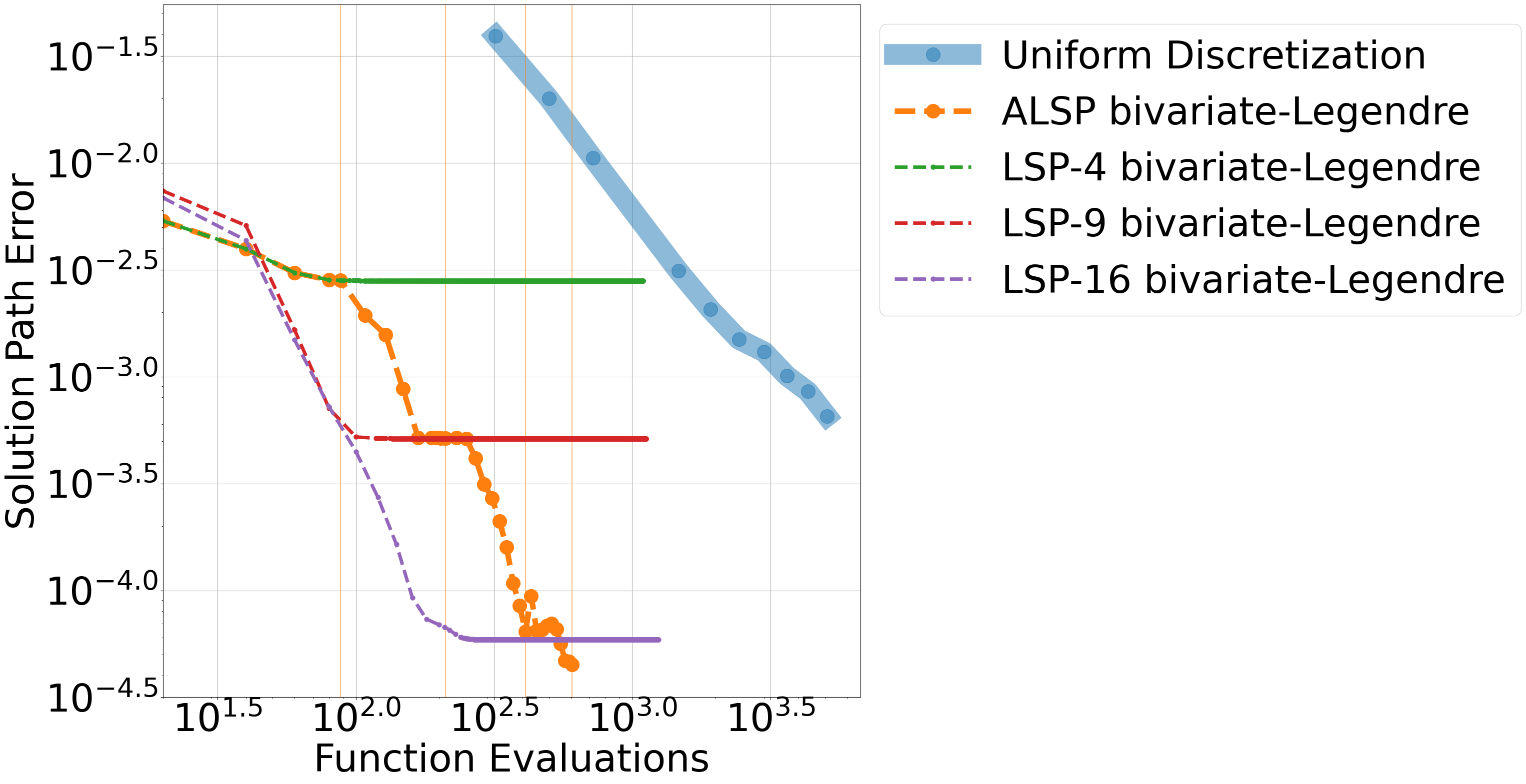

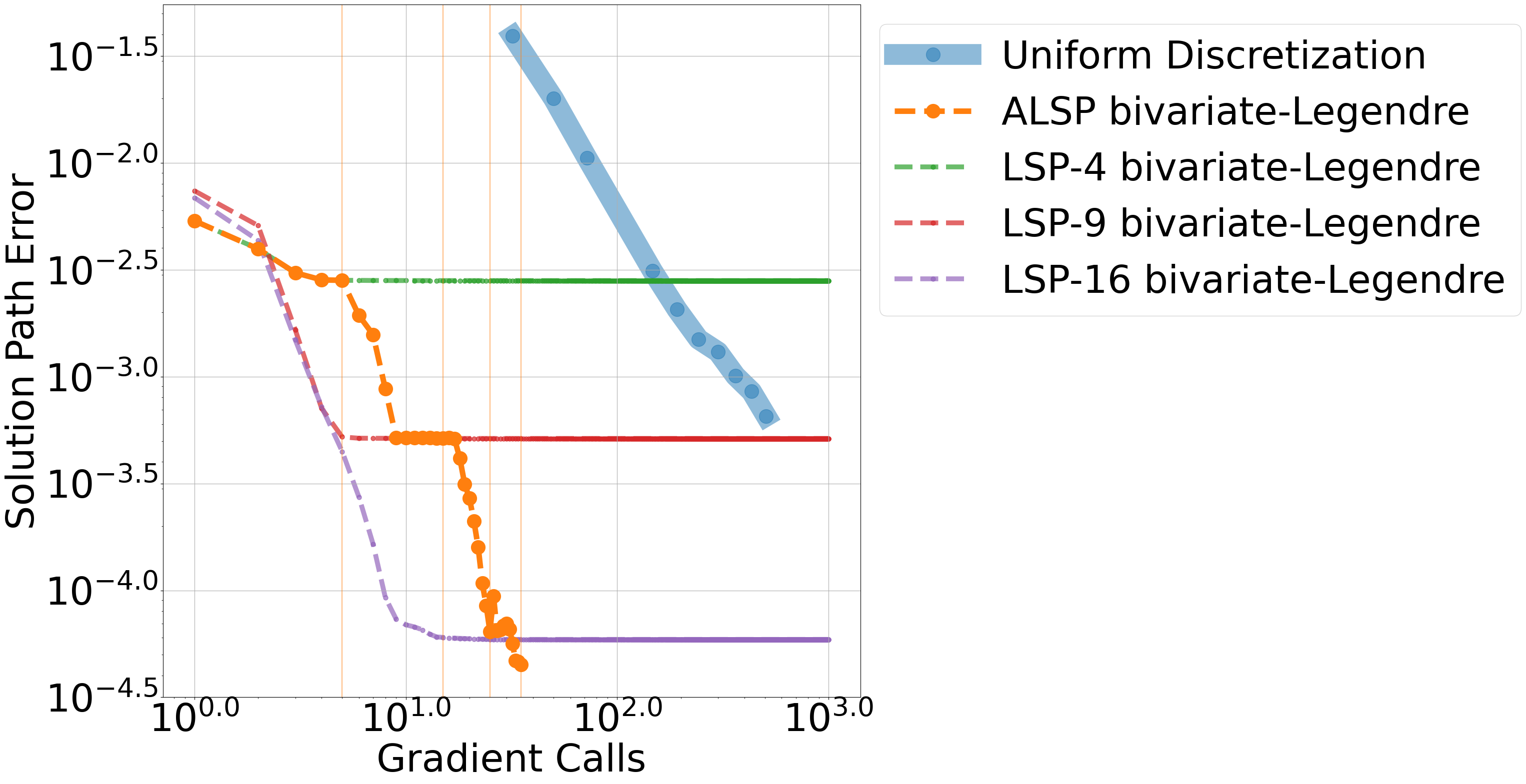

We focus on bivariate-Legendre polynomials for our basis, scaled and shifted to be orthogonal to uniform distribution on . We initialize with ALSP with 2 polynomials in each dimension, and iterate by adding one polynomial in each dimension, so that , after which we stop.

Unlike our previous experiment, to showcase that the qualitative insights of our theory hold for other algorithms other than SGD, we use torch.optim.BFGS for LSP, ALSP and uniform discretization (for a fair comparison). Unlike SGD, BFGS uses both function and gradient evaluations. We restrict it to use only function calls per gradient step so that the total work is still proportional to number of gradient calls.

As in our previous experiment, we see that LSP rapidly converges to an irreducible error and then plateaus. By contrast, ALSP seems to make continued progress as we add polynomials. Both method substantively outperform uniform discretization.

The improved performance over uniform discretization is partially attributable to the increased dimension of (because discretization suffers the curse of dimensionality), but is also because (traditionally) discretization interpolates solutions in a piecewise constant fashion. In this example, is very smooth. See Figure 5 in Appendix. Hence, polynomial can learn to interpolate values very fast, while uniform discretization needs a great deal more resolution.

7 Conclusion

We propose a new method for learning the optimal solution path of a family of problems by reframing it as a single stochastic optimization problem over a linear combination of pre-specified basis functions. Compared to discretization schemes, our method offers flexibility and scalability by taking a global perspective on the solution path. When using sufficiently large bases, we prove our problem satisfies a certain relaxed weak-growth condition that strongly allows us to solve the single optimization problm very efficiently. Theoretical results in special cases and numerical experiments in more general settings support these findings.

Future research might more carefully examine the interplay between the parameterization of the family of problems and choice of basis. One might also consider other universal function approximators (like deep neural networks or forests of trees) within this context.

References

- Bao et al. (2019) R. Bao, B. Gu, and H. Huang. Efficient approximate solution path algorithm for order weight l_1-norm with accuracy guarantee. In 2019 IEEE International Conference on Data Mining (ICDM), pages 958–963. IEEE, 2019.

- Bertsekas (1996) D. Bertsekas. Neuro-dynamic programming. Athena Scientific, 1996.

- Bottou et al. (2018) L. Bottou, F. E. Curtis, and J. Nocedal. Optimization methods for large-scale machine learning. SIAM review, 60(2):223–311, 2018.

- Cortes and Vapnik (1995) C. Cortes and V. Vapnik. Support-vector networks. Machine Learning, 20:273–297, 1995.

- Efron et al. (2004) B. Efron, T. Hastie, I. Johnstone, and R. Tibshirani. Least angle regression. 2004.

- Friedman et al. (2010) J. Friedman, T. Hastie, and R. Tibshirani. Regularization paths for generalized linear models via coordinate descent. Journal of Statistical Software, 33(1):1, 2010.

- Giesen et al. (2010) J. Giesen, M. Jaggi, and S. Laue. Approximating parameterized convex optimization problems. pages 524–535, 09 2010. ISBN 978-3-642-15774-5. doi: 10.1007/978-3-642-15775-2“˙45.

- Giesen et al. (2012) J. Giesen, S. Laue, J. Mueller, and S. Swiercy. Approximating concavely parameterized optimization problems. Advances in Neural Information Processing Systems, 3:2105–2113, 01 2012.

- Gower et al. (2019) R. M. Gower, N. Loizou, X. Qian, A. Sailanbayev, E. Shulgin, and P. Richtárik. Sgd: General analysis and improved rates. In International conference on machine learning, pages 5200–5209. PMLR, 2019.

- Gupta et al. (2023) S. Gupta, J. Moondra, and M. Singh. Which lp norm is the fairest? approximations for fair facility location across all” p”. In Proceedings of the 24th ACM Conference on Economics and Computation, pages 817–817, 2023.

- Hastie et al. (2004) T. Hastie, S. Rosset, R. Tibshirani, and J. Zhu. The entire regularization path for the support vector machine. Journal of Machine Learning Research, 5(Oct):1391–1415, 2004.

- Khaled and Richtárik (2020) A. Khaled and P. Richtárik. Better theory for sgd in the nonconvex world. arXiv preprint arXiv:2002.03329, 2020.

- Lan (2020) G. Lan. First-order and Stochastic Optimization Methods for Machine Learning, volume 1. Springer, 2020.

- Liu et al. (2024) C. Liu, D. Drusvyatskiy, M. Belkin, D. Davis, and Y. Ma. Aiming towards the minimizers: fast convergence of sgd for overparametrized problems. Advances in neural information processing systems, 36, 2024.

- Liu and Grigas (2023) H. Liu and P. Grigas. New methods for parametric optimization via differential equations. arXiv preprint arXiv:2306.08812, 2023.

- Mairal and Yu (2012) J. Mairal and B. Yu. Complexity analysis of the lasso regularization path. In Proceedings of the 29th International Coference on International Conference on Machine Learning, pages 1835–1842, 2012.

- Ndiaye and Takeuchi (2021) E. Ndiaye and I. Takeuchi. Continuation path with linear convergence rate. arXiv preprint arXiv:2112.05104, 2021.

- Ndiaye et al. (2019) E. Ndiaye, T. Le, O. Fercoq, J. Salmon, and I. Takeuchi. Safe grid search with optimal complexity. In International Conference on Machine Learning, pages 4771–4780. PMLR, 2019.

- Nguyen et al. (2018) L. Nguyen, P. H. Nguyen, M. Dijk, P. Richtárik, K. Scheinberg, and M. Takác. Sgd and hogwild! convergence without the bounded gradients assumption. In International Conference on Machine Learning, pages 3750–3758. PMLR, 2018.

- Osborne et al. (2000) M. R. Osborne, B. Presnell, and B. A. Turlach. A new approach to variable selection in least squares problems. IMA Journal of Numerical Analysis, 20(3):389–403, 2000.

- Park and Hastie (2007) M. Y. Park and T. Hastie. L1-Regularization Path Algorithm for Generalized Linear Models. Journal of the Royal Statistical Society Series B: Statistical Methodology, 69(4):659–677, 08 2007. ISSN 1369-7412.

- Pesme et al. (2020) S. Pesme, A. Dieuleveut, and N. Flammarion. On convergence-diagnostic based step sizes for stochastic gradient descent. In International Conference on Machine Learning, pages 7641–7651. PMLR, 2020.

- Rosset (2004) S. Rosset. Following curved regularized optimization solution paths. Advances in Neural Information Processing Systems, 17, 2004.

- Rosset and Zhu (2007) S. Rosset and J. Zhu. Piecewise linear regularized solution paths. The Annals of Statistics, pages 1012–1030, 2007.

- Tibshirani (1996) R. Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society Series B: Statistical Methodology, 58(1):267–288, 1996.

- Tibshirani and Taylor (2011) R. J. Tibshirani and J. Taylor. The solution path of the generalized lasso. The Annals of Statistics, 39(3):1335 – 1371, 2011. doi: 10.1214/11-AOS878. URL https://doi.org/10.1214/11-AOS878.

- Trefethen (2013) L. N. Trefethen. Approximation Theory and Approximation Practice. SIAM, 2013.

- Vaswani et al. (2019) S. Vaswani, F. Bach, and M. Schmidt. Fast and faster convergence of sgd for over-parameterized models and an accelerated perceptron. In The 22nd International Conference on Artificial Intelligence and Statistics, pages 1195–1204. PMLR, 2019.

- Wightman (1998) L. F. Wightman. Lsac national longitudinal bar passage study. lsac research report series. 1998.

Appendix A Omitted Proofs

A.1 Proofs from Section 2

Proof for Lemma 2.3..

Suppose by contradiction that . Then there exists a corresponding eigenvector with such that

This further implies that almost everywhere. By the linear independence assumption in Assumption 2.2, we then must have , but this is a contradiction since is an eigenvector.

For the second statement, notice

where the penultimate inequality follows from Jensen’s inequality and the convexity of the maximal eigenvalue function. ∎

Next, recall the family of functions and the function defined in (4):

Before proceeding, we establish smoothness and strong convexity of these functions.

Proposition A.1 (Uniform Smoothness and Strong Convexity).

The family of functions , over all , is -smooth. Moreover, is -smooth and -strongly convex.

Proof for Proposition A.1..

Fix an arbitrary . Then, for any , , smoothness of is certified by

for any , . To obtain the same conclusions for , we may take expectation over on the above inequalities, and invoke the linearity of expectations as well as the property that

Next, we verify the strong convexity of . Fixing , , for any , define , . Then, by strong convexity of , we have

Take expectation w.r.t. on both sides, we obtain

The second term in the last inequality comes from the Leibniz integral rule and the third term invokes a well-known property of the smallest eigenvalue of a positive definite matrix. ∎

Proof for Theorem 2.4..

First, we prove that is attained at some . Observe that is continuous. Thus, its level set is closed. Furthermore, is bounded. To see this, for any , by strong convexity of ,

| (4) | ||||

Since is arbitrary, for any , ,

Applying the Weierstrass Theorem, there exists s.t.

Next, we prove the main result of the theorem. Again, fix an arbitrary . By -smoothness of ,

| (5) |

Using the identity and triangle inequality on the right-hand side, this inequality becomes

By strong convexity of and definition of ,

So

| (6) |

Next, we bound . Observe that due to the optimality of for each ,

On the other hand, from the optimality of and strong-convexity of ,

Combining this inequality with the previous one shows which implies that

Substitute the above into Equation 6. Take expectation over sample paths on both sides, we conclude that

Rearranging and using the fact that verifies the statement. ∎

A.2 Proofs from Section 3

Proof for Theorem 3.2.

The proof follows the proof of Theorem 3.1 of Gower et al. (2019); we include it for completeness under the assumption of the RWGC Definition 3.1. Let denote the step-size. For , we have

Taking conditional expectations yields

| (7) |

The first inequality above uses the RWGC and the second uses strong convexity. The final inequality holds since and . Furthermore, since , we have ; therefore, by iterating Equation 7 and taking overall expectations, we get

where the second inequality uses the geometric series bound. Recalling that completes the proof.

∎

Proof for Lemma 3.3..

Recall that Proposition A.1 already establishes the smoothness of and smoothness and strong convexity of .

Define

By -smoothness, we have

Using for all , rearranging and recalling the definitions of (Section 2) and (proof of Theorem 2.4) yields

where the second inequality uses optimality of and the third uses that is attained at . Taking expectations on both sides, we get

where we used that the definition of implies that . Multiplying through by completes the proof. ∎

Proof for Theorem 3.4.

Our strategy will be to invoke Lemma 3.3 and apply Theorem 3.2, in conjuction with Theorem 2.4. To that end, notice that the upper bound on the step-size parameter given in Theorem 3.2 becomes . Hence, we need only constrain .

Applying Theorem 3.2 yields

Taking expectation of Theorem 2.4 on both sides and substituting the above, we have

| (8) |

Rearranging yields the first result. We next prove the two bounds on the iteration complexity.

First consider the case . Our goal will be to choose large enough to drive the first term on the right side of (8) to below . To simplify exposition, let . Then, we need to ensure that

We can upper bound the right side using the identity . Hence, it would be sufficient if

Replacing with its definition yields the first case.

For the second case where , (8) reduces to

Given , we need to ensure that

Again using , it would be sufficient if

Replacing with its definition yields the second case.

∎

A.3 Proofs from Section 4

Proof of Lemma 4.1..

As described in the main text, is block-diagonal with blocks of size . Denote this block by and note the elements of are precisely the first Legendre polynomials evaluated at .

Now the matrix is also block diagonal with copies of the matrix . As a consequence, the eigenvectors of are the stacked copies of the eigenvectors of with the same eigenvalues.

Since is a rank-one matrix, it has at most one non-zero eigenvalue, and by inspection, this eigenvalue is with eigenvector . Then,

because the Legendre polynomials achieve their maxima at with a value of .

By a nearly identical argument, we can see that

because by the orthogonality of the Legendre polynomials, the above matrix is diagonal. Hence

∎

Proof for Lemma 4.2.

Our proof is constructive and we will show a slightly stronger result. We will approximate by the its Chebyshev truncation up to degree for each . Letting be the coefficients corresponding to the resulting polynomials, we will show that satisfies the bound in Lemma 4.2, which implies that also satisfies the bound.

Let denote the Chebyshev polynomial of the first kind. For the dimension of the solution path, let denote the coefficient of in the Chebyshev truncation of up to degree .

Since is Lipschitz continuous with constant , it also has bounded variation . Thus, for any and , Trefethen (2013, Theorem 7.2) guarantees that

Then,

Moreover, smoothness of ensures that for any ,

Combine the above and using the definition of -norm, we deduce that

∎

Proof of Theorem 4.3.

As we are only interested in asymptotic behavior as , we will often suppress any constants that do not depend on below. In particular, we will write whenever there exists a constant (not depending on but perhaps depending on and ) such that .

Note that in order to attain a small solution path error, we will need to use a large number of polynomials . Based on Theorem 3.4, our first goal is to choose large enough that

| (9) |

First observe that Lemma 4.2 establishes that the solution path error is at most

| (10) |

Using Lemma 4.1, we can upper bound the right side of Equation 9 by

for some constant not depending on . Hence it suffices to take

polynomials to achieve our target error.

We now seek to bound the iteration count. By Theorem 3.4, the iteration count should exceed

where we have assumed SGD was initialized at and used Equation 10 and (cf. the proof of Lemma 4.1) to simplify.

To complete the proof we need to bound . To this end, we first bound , where is constructed by approximating each component by its Chebyshev truncation to degree for each .

Then,

where the penultimate inequality collects constants and invokes Trefethen (2013, Theorem 7.1) to bound the second summation. Note, for , this last sum is summable, so that .

Furthermore, from the proof of Lemma 4.2, . Hence, since the solution-path error upper bounds the stochastic error, we also have . From strong convexity, this implies that .

Putting it together, we have that

Substituting above shows that it suffices to take iterations as . Given our previous calculation of , this amount to iterations.

∎

Proof for Lemma 4.4.

The proof is very similar to the proof of Lemma 4.2, with the only difference being that we use Theorem 8.2 from (Trefethen, 2013) instead of Theorem 7.2.

Recall that a Bernstein ellipse with radius in the complex plain is the ellipse

Since is analytic, there exists an analytic continuation of to a Bernstein ellipse of radius . The value of generally depends on if has any singularities in the complex plane, but is guaranteed to be larger than . Let be . Finally, let and .

Now, define and as in the proof for Lemma 4.2.

For any and , Theorem 8.2 in (Trefethen, 2013) guarantees that

Plug this result into the last inequality of the proof for Lemma 4.2, we obtain

∎

Proof of Theorem 4.5..

The proof is quite similar to the proof of Theorem 4.3. Again, we only consider asymptotic behavior as and suppress all other constants. Hence, means there exists a constant (not depending on ) such that .

Again, our first goal is to identify a sufficiently large to achieve our target error. By Theorem 3.4 we seek large enough that

Lemma 4.4 shows that there exists an such that

hence it suffice to take large enough that

Solving this equation exactly requires the Lambert-W function. Instead, we take . Then,

for sufficiently small.

Again, to bound the number of iterations, we will need to bound . We again will assume that , and first consider bounding . Recall, is obtained by approximating each component by the Chebyshev truncation of to degree . Then,

Here, the second to last inequaity uses (Trefethen, 2013, Theorem 8.1). Since the last summation is summabble, we again conclude that .

The proof of Lemma 4.4 establishes that . Since solution path error bounds the stochasstic error, we conclude that , and by strong convexity, .

Putting it together, we have that

Substituting into the iteration complexity shows that it suffices to take

iterations, by using our condition on . ∎

Appendix B Implementation Details

B.1 Calibrating Uniform Discretization

To apply uniform discretization in practice on must decide i) the number of grid points to use, and ii) the number of gradient calls to make at each grid point. Loosely speaking, our approach to these two decisions is to first fix a set of desired “target” solution path errors denoted . Then, for each , we determine the number of grid points and gradient calls to approximately achieve a solution path error of .

More specifically, Ndiaye et al. (2019) suggests that to achieve a solution path error of , we require grid points. Thus, for each , we construct a uniform discretization with grid points across every dimension of the hyperparameter space. We denote this grid by . Recall that deterministic gradient descent requires steps to achieve an error of . Motivated by this result, we use gradient calls per grid point. The total number of gradient calls is thus .

The specific values of , , and used in our experiments are recorded in Table 1.

| Weighted Binary Classification | |||

|---|---|---|---|

| Portfolio Allocation |

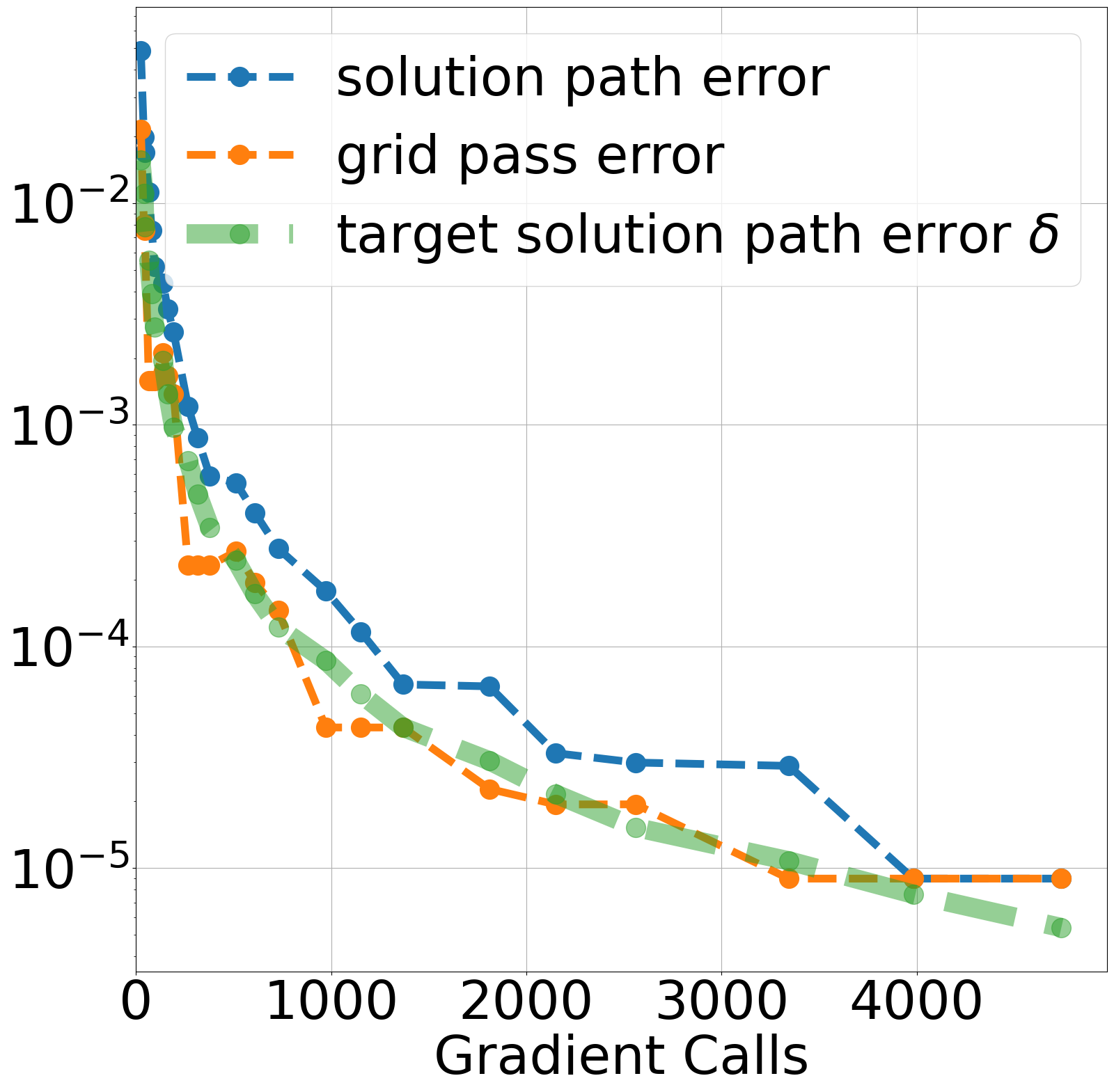

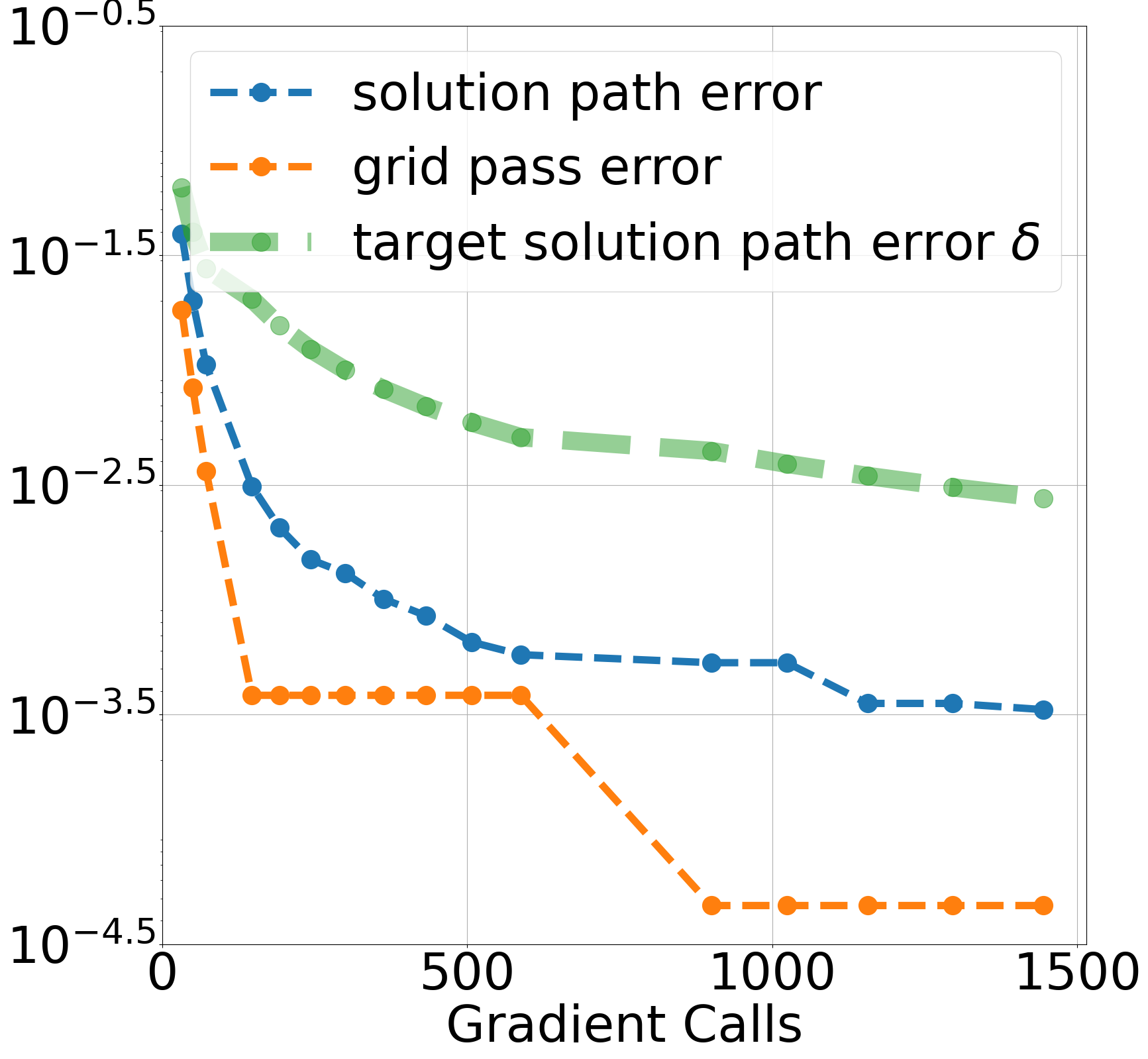

We next argue that this procedure with these constants is roughly efficient. Define the grid pass error as

For comparison, the solution-path error is

Since , the grid pass error is always less than the solution path error.

By comparing the grid pass error, the solution path error, and the target solution path error, we can calibrate the amount of work done at each grid point and the total number of grid points. Specifically, if the grid pass error is much smaller than the solution pass error, it suggests we have allocated too much work to gradient calls at grid points and have insufficient grid points. On the other hand, if the grid pass error is very far from the target solution path error, it suggests we have not allocated enough work to gradient calls at the grid points and have too many grid points. Based on this trade-off, we tune the constants and .

In Figure 4, we compare the solution path error and grid pass error to the target solution path error for our experiments. Figure 4(a) illustrates that in the weighted binary classification experiment with , the discretization scheme performs well, satisfying both objectives as the solution path error and grid pass error closely align with the target solution path error. Figure 4(b) demonstrates that for the portfolio allocation problem, both solution path error and grid pass error are still close to each other, but fall below the target solution path error. This is primarily due to the high precision of BFGS, though only very few gradient calls are performed at each grid.

Appendix C Additional Figures