Statistical Inference for the Rough Homogenization Limit of Multiscale Fractional Ornstein-Uhlenbeck Processes

Abstract

Most real-world systems exhibit a multiscale behaviour that needs to be taken into consideration when fitting the effective dynamics to data sampled at a given scale. In the case of stochastic multiscale systems driven by Brownian motion, it has been shown that in order for the Maximum Likelihood Estimators of the parameters of the limiting dynamics to be consistent, data needs to be subsampled at an appropriate rate. Recent advances in extracting effective dynamics for fractional multiscale systems make the same question relevant in the fractional diffusion setting. We study the problem of parameter estimation of the diffusion coefficient in this context. In particular, we consider the multiscale fractional Ornstein-Uhlenbeck system (fractional kinetic Brownian motion) and we provide convergence results for the Maximum Likelihood Estimator of the diffusion coefficient of the limiting dynamics, using multiscale data. To do so, we derive asymptotic bounds for the spectral norm of the inverse covariance matrix of fractional Gaussian noise.

Keywords: multiscale fractional Ornstein-Uhlenbeck processes, spectral norm, fractional Gaussian Noise

1 Introduction

Real-world systems often exhibit a multiscale behaviour. A typical example of that is the weather, where atmospheric dynamics take place at the scale of seconds but it is only their aggregate effect that will determine their long-term dynamics [14]. In order to effectively study the behaviour of such systems, scientists often build mathematical models that match the dynamics of the system at a given scale. This is usually done by re-scaling each component of the multiscale model appropriately using a change of variables, e.g., in the time or space dimension, or a change of units so that a unit of the quantity of interest in the model leads to meaningful dynamics in each of the components and then taking appropriate limits with respect to the scaling parameter. The techniques used are similar, irrespective of the underlying mathematical model (e.g. Ordinary, Partial or Stochastic Differential Equation) – see [25] for a detailed discussion.

Stochastic Differential Equations (SDEs) are powerful models that capture many characteristics of stochastic systems arising in many different areas, while also allowing for a rigorous study of their behaviour. For a stochastic system that exhibits multiscale behaviour, there are two types of behaviour of multiscale SDEs that are of interest. The first one, corresponding to what is referred to as the ‘averaging’ case, may be expressed in general as

| (1) |

where and are independent Brownian motions. In this case, the first-order term in the expansion of the dynamics of the ‘slow variable’ with respect to the scale separation parameter only depends on averages over the ‘fast variable’ and provides a good approximation of its long-term dynamics.

The second case, referred to as the ‘homogenization’ case, arises when the first-order term of the expansion disappears and the long-term dynamics are approximated by higher order terms. The general form may be written as

| (2) |

where averaged over goes to and contributes to the diffusion coefficient of the limiting dynamics through a Central Limit Theorem type of behaviour. In both cases, it is possible to show [24] that, under appropriate conditions, the slow variable converges in law as to the solution of

| (3) |

for some drift term and diffusion coefficient depending on the dynamics of the multiscaled systems (1) and (1). The later model comes in very handy for practitioners as not only it reduces the dimensionality of the problem – as the fast variable disappears – but it also provides a coarse-grained model for the slow dynamics, expressed on a single scale.

The question that naturally arises in this scenario is whether it is possible to fit the coarse-grained model (3) to multiscale data generated by systems (1) or (1). Ṫhis problem was first studied in [24] for a particular version of (1), where they showed that the Maximum Likelihood Estimators (MLE) for the effective drift and diffusion coefficient are asymptotically biased when evaluated at multiscaled data unless the data is subsampled at an appropriate rate. More specifically, they showed that if observations from the multiscale process are sampled at rate then the MLE for the effective drift and diffusion coefficients evaluated on a discretised path are asymptotically unbiased if , i.e. if the sampling rate is between the two characteristic time-scales of the system. In [18], the results of [24] for the drift estimation are extended to more general multiscale models. In particular, the authors prove that the MLE for the drift of the limiting process (3) evaluated at multiscale data is asymptotically unbiased in the averaging case (1) whereas for the homogenised equation (1) it is biased unless the sampling is again performed at an -dependent rate of for . This is not at all unexpected as the appearance of higher frequency terms leads to the multiscale dynamics dominating in the finer scales. In [26], by focusing on the particular case of a multiscale system of Ornstein-Uhlenbeck processes, they show that the MLEs for the drift and diffusion coefficients will be asymptotically unbiased for and respectively, with optimal sampling rate achieved at for the drift and for the diffusion coefficient. They also show that in the averaging case, the MLEs for both the drift and diffusion coefficients are unbiased.

One of the main criticisms of the subsampling at a constant rate approach is that it implicitly assumes knowledge of the scale separation variable , which is usually unrealistic. This led to alternative approaches that either depend on transforming the data [17] or aim to extract an adaptive sampling rate directly from the data [15]. Another alternative approach that is similar in spirit to subsampling is applying a kernel smoother to the multiscale data [1, 19, 2]. This avoids the need of subsampling at an appropriate rate at the cost of having to find an appropriate kernel bandwidth which turns out to be a very similar problem, although there is some numerical evidence that the later can be more robust against a sub-optimal choice [1].

Recently, there has been significant progress in understanding averaging and homogenisation limits for multiscale systems driven by fractional Brownian motion (fractional diffusion), making it possible to extract the effective dynamics of systems that exhibit long-term dependencies even at the fine scale. For example, averaging and homogenisation limits in the context of fractional multiscale diffusions can be found in [13] and [8], respectively. In this paper, we aim to address the question of fitting the limiting dynamics to the observed data in this context for the first time. Similarly to the SDE case, we expect the most interesting behaviour to arise when components of the multiscale process contribute in the limit to components of different roughness, which corresponds to the case where the slow dynamics are approximated by the second order term in the expansion with respect to the scale separation variable .

We consider the simplest possible problem that exhibits an interesting behaviour, which is the fractional Ornstein-Uhlenbeck process where a ’rough homogenisation’ limit exists and is a scaled fractional Brownian motion [9], also called the fractional kinetic Brownian motion model, described by the following multiscale system :

| (4) |

where represents a fractional Brownian motion with Hurst parameter and is a stationary fractional Ornstein-Uhlenbeck process. Indeed, in [9], the authors prove that

in the -norm, where is the slow variable in the solution to (1).

Similar to [24], we study the behaviour of the Maximum Likelihood Estimator (MLE) of for the diffusion parameter of the limiting equation when evaluated on multiscale data. We assume access to continuous paths of the multiscale system (1) and we consider the behaviour of estimators given data sampled at any constant rate . As before, we find that in order for the estimator to be unbiased, we need to sample at an -dependent rate in between the two time-scales of the system (1): . In particular, we show that the MLE for vanishes to almost surely if no subsampling is performed. On the other hand, we show that if subsampling is performed at an appropriate rate convergence to for in an appropriate interval is ensured in the -norm. We will assume that the observational time horizon is arbitrary but fixed to a finite quantity.

As simple as it may seem, this model requires the development of a new methodology to address the problem. Existing results in the literature on parameter estimation for multiscale systems heavily rely on the Markovianity of the processes involved. Here, the fast and slow processes in the multiscale equations, as well as the effective limit, depart from the Markovian regime. Thus, instead of using the generators of the processes to draw convergence results of the estimators, we derive convergence rates for the covariance matrix of the increments in the slow processes with respect to the spectral norm and the size of the discretisation.

1.1 Notation

We will denote by and the slow and fast variables of the multiscale system respectively, where will always be the observable part. We will also use without the index to denote the random variable whose distribution is the limiting distribution of . We assume that sample paths are observed continuously over a finite time horizon , where is an arbitrary number. We will denote the sampling rate of the observations by , so that is the number of observations gathered. Thus, the following two limits are equivalent

| (5) |

We will denote by the scale separation parameter. In other words, it is the characteristic time scale of the fast-varying part of the system, i.e. when measured in the same units, per unitary time elapsed in the slow variables the dynamics of the fast variables evolve by units of time. We will assume that is small, i.e. . Moreover, similar to [24] we will set for some , aiming to find the range of that will result to an unbiased estimator. Thus, is also equivalent to the limits in (5).

We will denote by the covariance matrix of the following random vector

so that is a discretisation of a fractional Gaussian Noise of size over an interval . In general, we will use the notation to denote the vector of increments of size over an interval of any stochastic .

All the processes considered along the paper are assumed to be real-valued stochastic processes defined on the same probability space . We define the following norms on these stochastic processes. For any and any fixed value of we define the -norm to be the standard norm

from which we drop any reference to since the probability space will always be the same one.

Sometimes we will also use some norms on the time domain defined on an interval . These will be explicitly denoted as to avoid confusion and they are defined for any real-valued function as

Two further norms will be used along the paper, both of them denoted as . When the argument is a (possibly random) vector it will be the usual Euclidean norm. When the argument is instead a matrix this will denote the spectral norm, which is the norm on a matrix space induced by the corresponding Euclidean norm. For symmetric matrices it may be computed as

see [10].

Another convention we adopt is to use the term to denote a constant that may change from line to line. In other words, two different written in different lines mean proportionality but the exact value may differ from line to line. We will sometimes, for the sake of simplicity, use ’’ to denote less or equal up to a constant, that is is totally equivalent to . On some occasions the constant may depend on some quantity of interest in which case this will be indicated as an argument or subscript.

2 Preliminaries

The two processes of interest will be the fractional Brownian motion and fractional Ornstein-Uhlenbeck process. We start by defining them and stating some of the properties that will play an important role in the rest of the paper.

2.1 Fractional Brownian motion

Definition 2.1.

A fractional Brownian motion of Hurst index is a continuous and centred Gaussian process with covariance function

| (6) |

We denote by the covariance between increments of fractional Brownian motion on a given equispaced partition of an interval with partition size , i.e.

| (7) | ||||

| (8) |

This is independent of which implies that the covariance of increments is stationary. The covariance between two consecutive increments is given by , so they are positively correlated for and negatively correlated for . The former is therefore used to model systems with memory, while the latter will make more sense under the assumption of some intermittent or repulsive behaviour in the underlying model. Moreover, for whereas if . For , we get the independence of Brownian motion increments.

A more intuitive way to illustrate the effect of the parameter on the process is through the Holder continuity of its sample paths. A fractional Brownian Motion with Hurst parameter is (almost surely) -Holder continuous for any . Therefore, values lead to sample paths that are rougher than those of a standard Brownian Motion, whereas values give rise to smoother sample paths.

The most relevant feature of the fractional Brownian Motion for our work is that, for any value it is a non-Markovian process due to its covariance structure –see [20] for a direct argument.

2.2 Fractional Ornstein-Uhlenbeck Process

Definition 2.2.

A fractional Ornstein-Uhlenbeck process is defined as the unique stationary solution to the Langevin equation

| (9) |

which admits the closed formula

Ornstein-Uhlenbeck processes are mean-reverting processes that are well suited to describe perturbations around a given value. Fractional Ornstein-Uhlenbeck processes generalise standard Ornstein-Uhlenbeck processes in the same way as fractional Brownian motion does to a Brownian motion. It includes an additional parameter that allows to control the smoothness of its sample paths.

For (9) to be well defined we need to adopt the technical convention that is a two-sided fractional Brownian motion:

from which we drop the tilde to ease the notation and use just for the two-sided version of it.

The process defined in (9) is a centred Gaussian stationary process that is ergodic [5]. We consider the rescaled fractional Ornstein-Uhlenbeck to be the unique stationary solution to the Langevin equation

| (10) |

which has the same distribution as .

Again the fractional Ornstein-Uhlenbeck process is non-Markovian for any value .

2.3 The kinetic fractional Brownian Motion model.

In this section, we present the main model that we will be concerned with in this paper, namely the kinetic fractional Brownian Motion model, as described in [9, Section 3]. The system is formally defined as follows:

| (11) |

where is a standard fractional Brownian motion with Hurst parameter so that is a stationary fractional Ornstein-Uhlenbeck process, and is some real number (most commonly ). As it is standard in the multiscale systems literature represents the ’slow’ variable of the system and is the environmental/perturbation effect that oscillates at a faster rate, i.e., the ’fast’ variable. This is possibly the simplest model driven by fractional Brownian motion, such that a homogenization type of limit exists, in the sense that converges to an appropriately scaled fractional Brownian motion, in a way made precise in the following:

Thus, similar to [24], it is natural to ask how we can construct robust estimators for , given .

Remark.

We note that the process may be defined by the expression

where the right-hand side is well-defined as a path-wise Riemann integral since has almost surely continuous paths in . It becomes straightforward then that is a Gaussian Process as it is a time integral of an integrable (in the Riemann sense) Gaussian Process.

2.4 Estimators for

As discussed earlier, our goal is to estimate the diffusion parameter of , given . As in [24], we start by deriving an estimator given sampled at a rate and then replace by corresponding to our observations. Finally, we analyse the convergence of the estimator as , aiming to identify the range of controlling the subsampling rate for which the estimator is consistent.

Since , we use the properties of the fractional Brownian Motion to derive a desired estimator for . The fact that it is Gaussian and has stationary increments allows us to derive an estimator for the diffusion coefficient. First, define the vector of increments of the limiting process as .

Recall that the fractional Gaussian Noise is a stationary centred Gaussian process with covariance function (7) and thus the covariance between any pair and is

Consequently, follows a normal distribution with mean and variance and it follows by a straightforward calculation that the maximum likelihood estimator for given a realisation of is

where , as a superscript of a vector or matrix denotes transpose. Replacing by leads to the following estimtor:

| (12) |

The remainder of the paper focuses on studying the behaviour of this estimator.

Remark.

When we talk about the MLE we are implicitly assuming that a likelihood function is available and thus that has a density with respect to the Lebesgue measure. In other words, as it is a Gaussian vector, that is an invertible matrix. While this is often taken for granted, later in Section 3 we find a strictly positive lower bound for the smallest eigenvalue of . This together with the Spectral Theorem guarantees the existence and provides with a direct construction of .

2.5 Main results

In this section we present the main results of our work pertaining to the convergence of the estimator alongside some newly developed tools necessary for the proofs.

2.5.1 Asymptotic biasedness without subsampling

First, we show that if we sample too finely (in a sense made precise below), the estimator will be biased.

Theorem 2.3.

2.5.2 Consistency with appropriate subsampling

The next result gives the range of for which we can guarantee that the estimator will be consistent, in a sense that is made precise below.

Theorem 2.4.

2.5.3 Auxiliary Tools: asymptotic bounds on the spectral norm of .

A key step in our approach is controlling the spectral norm of the inverse covariance matrix of fractional Gaussian Noise on a equi-spaced grid. While this is a trivial problem in the case of Gaussian noise arising from a standard Brownian Motion as covariance matrices are diagonal, it gets quite complicated when . The problem of bounding the eigenvalues has been studied for covariance operators associated with both fractional Brownian Motion and Gaussian Noise in [6], where explicit asymptotic results were derived for the eigenvalues of the operators both for and . However, for the discretised processes, there is not, to the best of our knowledge, anything similar available in the literature.

Lemma 2.5.

Let be the covariance matrix of a discretised fractional Gaussian Noise process on an equi-spaced grid of points over an interval . It then holds that

where .

Note that there is a qualitative difference in the behaviour of the spectral norm in lemma 2.5, for and . When the spectral norm of the matrix is asymptotically bounded by . However, when it stops decreasing with and does not get any better than .

3 Proof of Lemma 2.5

Throughout this section we will assume that without any loss of generality. We also add the superscript to the covariance matrix to make explicit the dependence of on the size of the grid. Indeed, let be the covariance matrix of a discretised fractional Gaussian noise when observations are taken on an equi-spaced grid of times . Let be the same matrix but when the observations happen instead in the grid . It then holds that

as a consequence of the self-similarity of the fractional Brownian Motion [4], or extracted directly from (7). Since we are interested in an asymptotic bound on any result will also hold for any fixed .

It is a standard linear algebra result that the spectral norm of the inverse covariance matrix is bounded by the reciprocal of the smallest eigenvalue.

Lemma 3.1.

Let be an invertible covariance matrix. It then holds that

where is the smallest eigenvalue of .

The following lemma, while straightforward, allows us to use the probabilistic interpretation of the covariance matrix in order to get a lower bound for the smallest eigenvalue.

Lemma 3.2.

Let be a covariance matrix. If for some and any , then .

Proof.

Let be any eigenvalue of and an associated eigenvector. It then holds that

from which the result stems immediately. ∎

Finally, we note that the quadratic form associated with the covariance matrix of fractional Gaussian noise can also be expressed as the second moment of a Wiener integral with respect to the original fractional Brownian Motion as follows:

| (15) |

where is the simple function .

3.1 The Wiener Integral with respect to the fractional Brownian Motion

Before proving lemma 2.5, we first define the space of deterministic integrands of a fractional Brownian Motion, following [16]. Let be the space of -valued step functions on and denote by the closure of for the scalar product

which is an equivalent definition to the natural construction of the Wiener integrands as the span of the increments of (see, for example, [12]). This is to say that, for , the inner product admits the representation

The proof of lemma 2.5, although based on the same idea of studying the integrands of the Wiener integral with respect to a fractional Brownian Motion, is substantially different depending on whether is smaller or bigger than . Therefore, we will carry an independent analysis for each case.

Before proceeding with each case note that in principle none of them would apply to the case . However, in this case the results is trivial as and therefore .

3.2 Case .

When it is possible to re-write the inner product as (see for example [21])

We now introduce some operators on that will provide with some useful representations of functions in .

Definition 3.3.

The fractional integral of order is defined as the operator

The fractional derivative of order and can be expressed as

Lastly, we call the Marchaud fractional derivative of order which may be written as

When , is the inverse operator of in whereas the Marchaud fractional derivative is the adjoint of in , playing the role of a fractional integration by parts –see [23].

Proposition 3.1.

The following relation between the operators hold for :

where extends to the positive real line by setting if .

Proof.

An application of Fubini’s theorem to the left-hand side yields

where the inner integral is computed as follows

∎

It immediately follows that, by taking , we obtain

where

Corolary 3.1.

Let . It then holds that

Thus, for , we get

| (16) |

Proof.

A simple application of Cauchy-Schwardz’s inequality yields

where the last equality follows from proposition 3.1. ∎

It follows from (3) and (16) that we can bound the quadratic form associated to by taking again

| (17) |

Hence, if we can find a bound of the type

| (18) |

it follows from lemmas 3.1 and 3.2 that

| (19) |

as required. We now prove that (18) holds for an appropriate , to be identified. For the following holds:

The Marchaud fractional derivative of order of may be written as

It follows that

| (20) | ||||

| (21) |

where in (20) we take the change of variable and in (21) we expand the square and pull out of the integral the terms without . We denote

We want to find a bound of the form that will allow to conclude the result using (19). Expanding the product of differences, using and the fact that , we get the bound

| (22) |

where the last equality is due to the role of and being interchangeable in . Thus, we only need to bound the terms

After some tedious computations (see Appendix A for the details) it is possible to bound all the terms by expressions of the form when , which is true for the case of interest when .

3.3 Case .

As before, let be the domain of the Wiener integral with respect to fractional Brownian Motion (see, for example, [4] for a thorough exposition of the space ). To construct a lower bound for the norm defined on this space, we can now take advantage of one of the multiple representations this space has, which will in turn allow to write

First, we note that, for (and ), it is possible to write (see [3] Theorem 2.5)

| (25) |

In words, the space of functions in extended to the real line is a subspace of the fractional Sobolev space .

We now use the fact that (see [7] Theorem 6.5) for any compactly supported function defined in the real line

| (26) |

for any .

4 Proof of Theorem 2.3

We now go on to prove theorem 2.3:

Proof.

Recall that and are both defined in the same space . By means of Kolmogorov’s Continuity Theorem (see for example [22]) there exists a set with in which, for every , is a continuous function on in . As a consequence, for each , there exists such that

Let now

| (28) |

It follows from the definition of in (11) that

| (29) |

Putting all together and applying lemma 2.5, we get that

| (30) |

Then, (13) follows for any and by taking . To prove (14), recall that the increments of are identically distributed. An application of Fubini’s theorem yields

where the inequality is due to Cauchy-Schwarz’s inequality together with the stationarity of . Hence, taking expectation in both sides of (28), we get

Note that, we now assume that . Therefore, if

whereas if

The result follows by taking in both sides. ∎

5 Proof of Theorem 2.4

Proof.

We begin by decomposing the estimator as follows

Applying the -norm, we get

| (31) |

The differences may be written as (see [9]). For the first term we have that

| (32) |

Since is a deterministic quantity, we only need to control the -norm of the first quantity. We write

| (33) |

where we used Cauchy-Schwardz’s inequality and the stationarity of the fractional Ornstein-Uhlenbeck process . It follows that

Together with Lemma 2.5, this yields

| (34) |

by just plugging each bound in (5). We use a similar approach to bound the second term of (5). First, we note that

| (35) |

Thus, we now need to control . We write

| (36) |

It follows that

which, again, together with lemma 2.5, yields

by just plugging each bound in (35). Finally, we control the third term of (5), using a Law of Large Numbers type of argument. Since is the covariance matrix of it holds that

Therefore,

Putting everything together we get that, if

while if

Therefore, if convergence is guaranteed provided that , whereas if , we require that . In particular, if for some , convergence will be guaranteed for . ∎

6 Numerical Simulations

In this section, we support some of our theoretical findings with numerical simulations.

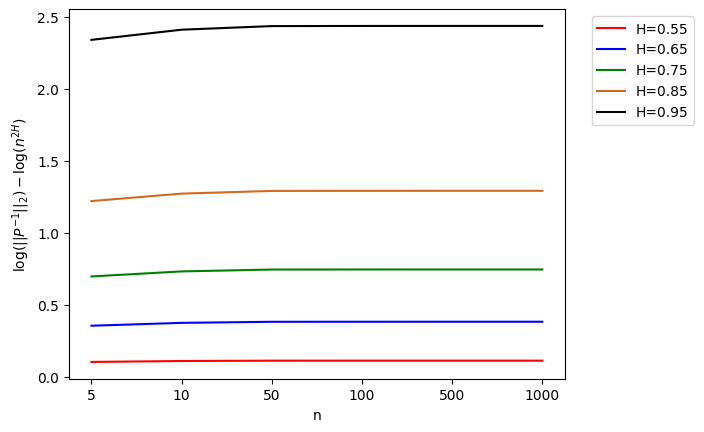

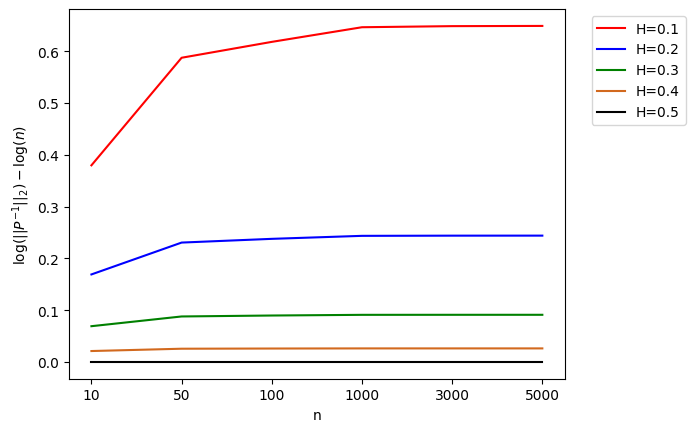

6.1 Asymptotic order of

As mentioned before the bounds found in lemma 2.5 simply upper bound the asymptotic behaviour of . To see how sharp these are we conduct a numerical experiment in which we compare them to the actual values for different in the logarithmic scale.

In Figure 1 we perform this experiment for values , where the asymptotic bound is . In Figure 2 analogous results are shown for values when the bound is . In both cases, we see that the ratio seems to behave as a constant as becomes large suggesting that the order of the bounds is sharp.

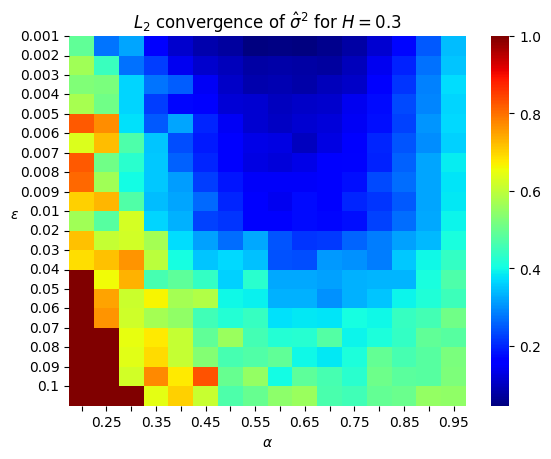

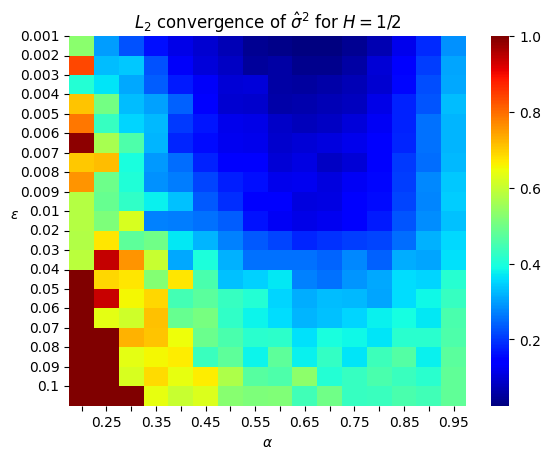

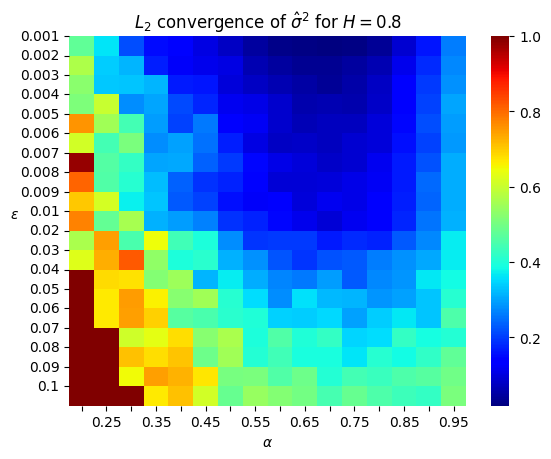

6.2 -convergence of the multiscaled MLE.

We here simulate as when for different values of . To do so we set and simulate sample paths of the solution to (11) over to then compute . For each combination of and the error is estimated through an empirical mean over 100 realisations of coming from 100 different sample paths.

In Figures 3, 4 and 5 the same experiment is repeated for and respectively. The mean error observed is plotted on a colour palette where the darker blue areas correspond to smaller errors and hence faster convergence, whereas warmer colours represent larger errors or slower convergence regimes.

Numerical simulations seem to suggest that convergence occurs for values . Although this matches our findings for it hints that the result for could be extended to values . However, our approach cannot be extended any further as some obstructions appear when trying to prove this analytically, as mentioned at the end of Section 3.3.

Another interesting observation is that the value seems to optimise the convergence. While this seems to extend across all values of we have only been able to prove this analytically in the case using a different bound for the errors than the one in Section 5.

Appendix A Calculation of bounds for and in Proof 2.5

We include here the details of how the bounds for the different terms of the norm of are calculated in the proof of lemma 2.5 when .

A.1 Bound for

We first deal with the terms :

where the first inequality is due to the Mean Value Theorem applied to both terms of the integrand and the last equality holds since . Note that within this term the role of and is still interchangeable. Therefore, we only need to analyse now the terms corresponding to and the term , since the terms are the same.

| (37) | ||||

where the geometric sum in (37) is bounded as before and the integrand integrates to a constant as .

We now bound the terms corresponding to :

where again the integral is just a constant as .

A.2 Bound for

We use similar techniques to the ones used for , noting that more care should be taken as the role of and will no longer be interchangeable as appears multiplying . We first split the sum as follows:

and we bound each term separately. For the first one we can proceed as follows:

Note that, for in , it holds that

Therefore,

For the remaining terms, we use the following procedure:

References

- Abdulle et al., [2021] Abdulle, A., Garegnani, G., Pavliotis, G. A., Stuart, A. M., and Zanoni, A. (2021). Drift estimation of multiscale diffusions based on filtered data. Foundations of Computational Mathematics., 23:33–84.

- Abdulle et al., [2022] Abdulle, A., Pavliotis, G. A., and Zanoni, A. (2022). Eigenfunction martingale estimating functions and filtered data for drift estimation of discretely observed multiscale diffusions. Statistics and Computing., 32(34).

- Bardina and Jolis, [2006] Bardina, X. and Jolis, M. (2006). Multiple fractional integral with hurst parameter less than 1/2. Stochastic Processes and their Applications, 116(3):463–479.

- Biagini et al., [2010] Biagini, F., Hu, Y., Oksendal, B., and Zhang, T. (2010). Multidimensional Stochastic Processes as Rough Paths: Theory and Applications. Cambridge University Press.

- Cheridito et al., [2003] Cheridito, P., Kawaguchi, H., and Maejima, M. (2003). Fractional ornstein-uhlenbeck processes. Electronic Journal of Probability, 8:1–14.

- Chigansky and Kleptsyna, [2018] Chigansky, P. and Kleptsyna, M. (2018). Exact asymptotics in eigenproblems for fractional brownian covariance operators. Stochastic Processes and their Applications, 128(6):2007–2059.

- Di Nezza et al., [2012] Di Nezza, E., Palatucci, G., and Vadinoci, E. (2012). Hitchhiker‘s guide to the fractional sobolev spaces. Bulletin des Sciences Mathematiques, 136(5):521–573.

- Gehringer and Li, [2021] Gehringer, J. and Li, X.-M. (2021). Rough homogenisation with fractional dynamics. Springer Proceedings of Mathematics and Statistics: Geometry and Invariance in Stochastic Dynamics, 379:137–168.

- Gehringer and Li, [2022] Gehringer, J. and Li, X.-M. (2022). Functional limit theorems for the fractional ornstein-uhlenbeck process. Journal of Theoretical Probability, 35:426–456.

- Horn and Johnson, [1985] Horn, R. A. and Johnson, C. R. (1985). Matrix Analysis. Cambridge University Press, Cambridge.

- Isserlis, [1918] Isserlis, L. (1918). On a formula for the product-moment coefficient of any order of a normal frequency distribution in any number of variables. Biometrika, 12(1/2):134–139.

- Jolis, [2007] Jolis, M. (2007). On the wiener integral with respect to fractional brownian motion on an interval. Journal of Mathematical Analysis and Applications, 330(2):1115–1127.

- Li and Sieber, [2022] Li, X.-M. and Sieber, J. (2022). Slow-fast systems with fractional environments and dynamics. Annals of Applied Probability, 32(5):3964–4003.

- Majda et al., [2001] Majda, A. J., Timofeyev, I., and Venden Eijnden, E. (2001). A mathematical framework for stochastic climate models. Communications on Pure and Applied Mathematics, LIV:0891–0974.

- Manikas and Papavasiliou, [2019] Manikas, T. and Papavasiliou, A. (2019). Diffusion parameter estimation for the homogenized equation. Multiscale Modeling & Simulation, 17(2):675–695.

- Nualart, [2010] Nualart, D. (2010). The Malliavin Calculus and Related Topics. Springer Berlin, Heidelberg.

- Olhede et al., [2010] Olhede, S. C., Sykulski, A. M., and Pavliotis, G. A. (2010). Frequency domain estimation of integrated volatility for ito processes in the presence of market-microstructure noise. Multiscale Modeling & Simulation, 8(2):0891–0974.

- Papavasiliou et al., [2009] Papavasiliou, A., Pavliotis, G. A., and Stuart, A. M. (2009). Maximum likelihood drift estimation for multiscale systems. Stochastic Processes and their Applications, 119(10):3173–3210.

- Pavliotis et al., [2024] Pavliotis, G. A., Reich, S., and Zanoni, A. (2024). Filtered data based estimators for stochastic processes driven by colored noise. https://arxiv.org/pdf/2312.15975.

- Phuoc Huy, [2003] Phuoc Huy, D. (2003). A remark on non-markov property of a fractional brownian motion. Vietnam Journal of Mathematics., 31(2):237–240.

- Pipiras and Taqqu, [2000] Pipiras, V. and Taqqu, M. S. (2000). Integration questions related to fractional brownian motion. Probability Theory and Related Fields, 118:251–291.

- Revuz and Yor, [1999] Revuz, D. and Yor, M. (1999). Continuous Martingales and Brownian Motion. Springer.

- Samko et al., [1993] Samko, S. G., Kilbas, A. A., and Marichev, O. I. (1993). Fractional Integrals and Derivatives: Theory and Applications. Gordon and Breach Science Publishers.

- Stuart and Pavliotis, [2007] Stuart, A. M. and Pavliotis, G. A. (2007). Parameter estimation for multiscale diffusions. Journal of Statistical Physics, 137(4):741–781.

- Stuart and Pavliotis, [2008] Stuart, A. M. and Pavliotis, G. A. (2008). Multiscale methods: averaging and homogenization. Springer, New York.

- Zhang and Papavasiliou, [2018] Zhang, F. and Papavasiliou, A. (2018). Maximum likelihood estimation for multiscale ornstein-uhlenbeck processes. Stochastics, 90(6):807–835.