fixltx2e

Dependent Random Partitions by

Shrinking Toward an Anchor

Abstract

Although exchangeable processes from Bayesian nonparametrics have been used as a generating mechanism for random partition models, we deviate from this paradigm to explicitly incorporate clustering information in the formulation our random partition model. Our shrinkage partition distribution takes any partition distribution and shrinks its probability mass toward an anchor partition. We show how this provides a framework to model hierarchically-dependent and temporally-dependent random partitions. The shrinkage parameters control the degree of dependence, accommodating at its extremes both independence and complete equality. Since a priori knowledge of items may vary, our formulation allows the degree of shrinkage toward the anchor to be item-specific. Our random partition model has a tractable normalizing constant which allows for standard Markov chain Monte Carlo algorithms for posterior sampling. We prove intuitive theoretical properties for our distribution and compare it to related partition distributions. We show that our model provides better out-of-sample fit in a real data application.

Keywords: Bayesian nonparametrics; Chinese restaurant process; Dirichlet process mixture model; Hierarchically dependent partitions; Temporally dependent partitions.

1 Introduction

Random partition models are flexible Bayesian prior distributions which accommodate heterogeneity and the borrowing of strength by postulating that data or parameters are generated from latent clusters. Exchangeable random partition models arise from Bayesian nonparametric (BNP) models, which are extremely flexible and often involve rich modeling techniques applied to specific problems. For the sake of introducing key ideas, we start with a very simple BNP model. The sampling model for data is , which is conditioned on an item-specific parameter. In practice, the sampling model may depend on other parameters which are treated in the usual Bayesian fashion, but here we focus on the prior distribution for . Specifically, we assume that are independent and identically distributed from an unknown discrete random measure . The prior for is the de Finetti mixing measure , an infinite-dimensional prior distribution, e.g., the Dirichlet process prior (ferguson1973bayesian). Notationally, we write and . This model can be enhanced in a variety of ways, e.g., additional parameters could be added to the sampling model or prior distributions could be placed on parameters of .

The discrete nature of yields ties among with positive probability, implying a partition of into subsets such that items and belong to the same subset if and only if . We let denote the common value of the ’s for the items in subset . A partition defines a clustering of items, and we interchangeably use the terms partition and clustering and the terms subset and cluster.

In many applications, interest lies in making inference on the partition or flexibly borrowing strength in the estimation of the ’s. That is, the random measure itself may not be of interest and is merely used as a vehicle for inducing a clustering structure. In these situations, the random measure can be integrated over its prior , resulting in an exchangeable partition distribution:

| (1) | ||||

where is the centering distribution of . The probability mass function of an exchangeable partition distribution is a function of an exchangeable partition probability function (EPPF) (pitman1995exchangeable). Thus, under the exchangeability assumption, the items being clustered are indistinguishable from one another. When is the Dirichlet process, for example, the resulting is the Ewens distribution (ewens1972sampling; pitman1995exchangeable), that is, the partition distribution of the Chinese restaurant process (CRP).

In the presence of additional information that ought to influence the partition, the exchangeability constraint is untenable and researchers have developed nonexchangeable random partition models that are not obtained by marginalizing over a random measure . Examples include muller2011product, blei2011distance, airoldi2014generalized, and dahl2017random which use covariates or distances to influence a partition distribution.

Some have sought partition distributions which directly incorporate prior knowledge on the partition itself. Rather than incorporating covariates or distances in a partition distribution, one might wish to use a “best guess” as to the value of the partition, yet may not be completely certain and therefore may be unwilling to fix the partition on this value. Instead, a modeler may wish to use a partition distribution that is anchored on this “best guess” but yet allow for deviations from the anchor partition. The nature of these deviations is governed by a baseline partition distribution, and a shrinkage parameter controls how much the baseline partition distribution is pulled toward the anchor partition.

We introduce a partition distribution with a shrinkage parameter that governs the concentration of probability mass between two competing elements, a baseline partition distribution , and an anchor partition . We call our distribution the shrinkage partition (SP) distribution. Our approach builds on the pioneering work of smith2020demand’s location scale partition (LSP) and paganin2020centered’s centered partition process (CPP). Our SP distribution and both the LSP and CPP distributions are influenced by an anchor partition (called the “location” partition and the “centered” partition in their respective papers). However, the LSP depends on the arbitrary ordering of the data and the distribution of deviations from the anchor partition is immutable and intrinsically embedded, which limits modeling flexibility. Both our SP distribution and the CPP allow for any baseline partition distribution, but the probability mass function of the CPP is only specified up to the normalizing constant. The nature of the combinatorics makes the normalizing constant intractable, so the shrinkage parameter must be fixed using a computationally intensive cross-validation procedure and posterior inference hyperparameters (e.g., the shrinkage parameter) is not practically feasible.

In contrast, our SP distribution has several desirable properties. First, the SP has a tractable normalizing constant, so standard Markov chain Monte Carlo (MCMC) techniques can be used for posterior inference on hyperparameters (e.g., shrinkage and concentration parameters). Second, the SP does not depend on the order in which data is observed, making the data analysis invariant to what may be an arbitrary ordering. Third, the SP allows for any baseline partition distribution to govern the distribution of partitions informed by the anchor partition. Fourth, prior knowledge about the clustering of items may be different across the items and our SP is unique in allowing differential shrinkage toward the anchor.

Further, whereas the LSP and CPP were introduced as prior distributions for a single partition in situations where the modeler has a prior guess as to the value of the partition, we note that our formulation — in addition to being suitable for this case — also permits building models for dependent random partitions. page2022dependent was the first to directly model temporally-dependent partitions that are evenly spaced in time. Our approach adds flexibility, permitting modeling temporally-dependent random partitions that are not necessarily observed on a uniformly-spaced grid. Further, our SP permits not only temporal dependence, but other forms of dependence. Whereas hierarchical modeling of means and variances is common in Bayesian data analysis, we believe that our SP is the first to allow hierarchically-dependent partitions. Indeed, song2023clustering recently used our SP distribution as a basis for their innovative hierarchical bi-clustering model of mouse-tracking data. As contemporaneous work, paganin2023informed and dombowsky2023product are two recent pre-prints on dependent random partitions.

The SP distribution scales well in the number of items being clustered. It has properties that one would expect in a partition distribution, such as the ability to control the distribution of the number of subsets, influence the distribution of cluster sizes, and generally behaves like other partition distributions in the literature, with the added feature of shrinking toward an anchor partition. Software implementing our SP distribution is available as an R package (https://github.com/dbdahl/gourd-package).

The remainder of the paper is organized as follows. In Section 2, we review the LSP and CPP and put them in common notation for ease in understanding the novelty of our SP distribution, which is detailed in Section 3. Properties of the SP distribution are detailed in Section 4 and models for dependent partition models based on the SP distribution are discussed in Section 5. An empirical study in Section 6 shows that our SP distribution, based on 10-fold cross validation, compares favorably to the LSP and CPP for a single partition and that our SP can be used for hierarchically-dependent and temporally-dependent partitions to improve performance beyond what is possible with models that ignore dependence among partitions.

2 Existing Distributions Indexed by a Partition

Our shrinkage partition distribution itself was inspired by paganin2020centered’s CPP and smith2020demand’s LSP. A key parameter in all three distributions is what we term the anchor partition , a partition of the integers which represents the a priori estimate of the population partition. The anchor partition plays the same role as the “centered” partition in the CPP and the “location” partition in the LSP. As noted by dahl2021discussion, words like “centered” or “location” may be misnomers. We use the term “anchor” to suggest that the probability distribution is “tethered to” — but not “centered on” or “located at” — the anchor partition . How closely the partition distribution reflects is a function of what we term the shrinkage parameter .

In this paper the anchor partition is expressed in terms of cluster labels such that two items have the same label (i.e., ) if and only if they belong to the same subset in the anchor partition. Likewise, we use to denote the vector of cluster labels of a random partition. Cluster labels are assumed to be in canonical form, i.e., cluster label “1” is used for the first item (and all items clustered with it), cluster label “2” is used for the next item (and all items clustered with it) that is not clustered with the first item, etc.

Studying the probability mass function of each distribution helps one see the similarities with our SP distribution, and what motivated us to develop our new partition distribution. For the sake of comparison, we express each distribution in common notation.

2.1 Centered Partition Process

The CPP of paganin2020centered is formed from a baseline partition distribution and a distance function which measures the discrepancy between two partitions. The probability mass function of the CPP is:

| (2) |

where is a univariate shrinkage parameter controlling the magnitude of the penalty for discrepancy with the anchor partition . The baseline partition distribution will likely depend on other parameters (e.g., the Ewens distribution has a concentration parameter) but we suppress them here for simplicity. Note that reduces to the baseline partition distribution as . Conversely, as , all probability concentrates on the anchor partition , i.e. . While any distance function for partitions could be used, paganin2020centered focus on the variation of information (meilua2007comparing; wade2018bayesian). We use the notation for a partition whose distribution is the CPP with anchor partition , shrinkage parameter , distance function , and baseline distribution .

A key challenge with the CPP is that the probability mass function in (2) is only specified up to proportionality. While the normalizing constant can theoretically be obtained through enumeration of all possible partitions of items, the number of possible partitions of items (as given by the Bell number) quickly makes enumeration infeasible beyond 20 or so items. The lack of a normalizing constant precludes posterior inference on other parameters associated with the baseline distribution (e.g., a concentration parameter). Further, as a practical matter, the shrinkage parameter must be fixed for data analysis, making the CPP unsuitable for modeling dependent partitions.

2.2 Location-Scale Partition Distribution

We now discuss the location-scale partition (LSP) distribution of smith2020demand. As the name implies, smith2020demand originally expressed their distribution using a location and a scale parameter. For the sake of comparison, we reparameterize the LSP probability mass function (pmf) to use a univariate shrinkage parameter , which is the reciprocal of their original scale parameter. The LSP has a constructive definition, in which a partition is obtained by sequentially allocating items. Let denote the set of unique cluster labels after the item is allocated and, therefore, is the cardinality of that set or, in other words, the number of clusters in the partition after item is allocated. Note that, for the LSP, the order in which items are allocated affects the probability of a partition, making data analysis using the LSP subject to what is often an arbitrary ordering. To overcome this deficiency and to make the comparisons in Section 6 more fair, we generalize the original LSP using a technique of dahl2017random. Specifically, items are allocated in an order given by a permutation of the integers , where the k item allocated is the item in the model or dataset, and a uniform prior is placed on the permutation . Thus the LSP’s modified pmf is:

where by definition and for :

| (3) | ||||

Following dahl2017random, the key to obtaining a normalizing constant for the LSP and our SP distribution comes from sequential allocation. We use the notation for a partition whose distribution is our extension of the LSP, marginalizing over . As with the CPP, as .

Noticeably absent from the LSP are any parameters to control the distribution beyond the anchor partition and the shrinkage parameter . As , the sequential allocation probabilities for a cluster in (3) reduces to a uniform selection among existing clusters and a new cluster. There is no mechanism to control the number of clusters. The LSP’s baseline partition distribution is “hardwired” into its pmf and is obtained when . Note that this partition distribution is a special case of the Jensen-Liu partition (JLP) distribution of jensen2008bayesian and casella2014cluster with mass parameter fixed at .

3 Shrinkage Partition Distribution

3.1 Probability Mass Function

We now present the probability mass function (pmf) of the SP distribution, which incorporates key strengths of both the CPP and the LSP, addresses some of their limitations, and adds modeling flexibility. Like the CPP and the LSP, the SP distribution is formed using an anchor partition . Both the CPP and the LSP use a single, real-valued shrinkage parameter , with larger shrinkage values producing higher concentrations of probability mass for partitions that are close to . Instead of a real-valued shrinkage, the SP distribution uses a vector-valued shrinkage to permit item-specific knowledge and flexibility in how close realizations from the SP distribution are to the anchor partition . That is, is idiosyncratic to the item, although a modeler could simplify ’s structure by making each entry equal or, choose to have items in the particular subset of all share the same shrinkage value (i.e., if ).

Like many other partition distributions, including the LSP, we adopted a sequential allocation construction for the SP distribution, with an important caveat. As it was originally defined, the LSP distribution implicitly uses a fixed permutation , which makes the data analysis dependent on the ordering of the data. In some contexts (e.g., time series), the item order may be meaningful. But most commonly, the permutation would be viewed as a nuisance parameter. Lacking prior knowledge for , we recommend using the uniform distribution on , that is, . Marginalizing over has the effect of making the data analysis invariant to the order of the data. We also place a practical constraint on the baseline partition distribution : it must have an explicit sequential allocation probability function, which we denote as . Thus . The function may be an exchangeable partition probability function (EPPF) from, e.g., the Ewens distribution (ewens1972sampling; pitman1995exchangeable; pitman1996some), but we are not limited to exchangeable priors and only require a sequential allocation rule. We call this sequential allocation rule a “conditional allocation probability function” (CAPF).

The CPP utilizes a distance function between and , such as the Binder loss (binder.1978) or the variation of information (meilua2007comparing; wade2018bayesian). Analogously, the SP’s anchor partition distribution uses a function inspired by the general form of Binder loss (binder.1978; wade2018bayesian; dahl2022search). This function, denoted , rewards allocations which agree with while simultaneously penalizing or rewarding larger clusters. The penalization term is controlled by the grit parameter which influences the number of clusters and the cluster sizes. The function is presented in CAPF form:

| (4) | ||||

for and . Notationally, is the number of clusters in the partition before allocating the item. Varying the grit parameter in (4) favors different configurations, analogous to the different behaviors of Binder and VI losses. Thus, our formulation provides flexibility like the CPP but differs in that a prior can be set on (i.e., the distance function).

The pmf of the SP distribution is:

| (5) |

where

| (6) | ||||

We note that, to simplify notation, we are conditioning on , , and , however, the probabilities defined in (4) – (6) are only conditionally dependent on some elements of these vectors. For a random partition , we use the notation to denote the partition has a SP distribution with an anchor partition , a shrinkage vector , a permutation , and a baseline distribution . When marginalizing over the permutation parameter with a uniform prior, we use the notation .

From (5), it is clear that the allocation of items to subsets in a partition are sequential. However, the SP distribution is similar in form to the CPP in that the allocation of each item depends on the baseline partition distribution and its compatibility to the anchor partition . The CPP, however, applies this trade-off globally, whereas our SP distribution does so on a sequential, item-by-item basis. At the step, note that there are only possible allocations for . Thus, the normalizing constant needed for (6) is readily computed for any , which easily permits posterior inference on any of the parameters in the SP distribution using standard MCMC techniques.

3.2 Baseline Distributions

The baseline distribution is a key component of the CPP and the SP which affords flexibility to the modeler. Here we discuss a few obvious choices for and emphasize that others may be desired for any given situation. Conditional allocation probability functions are one way to characterize probability mass functions for partition distributions and are used in the SP distribution. CAPFs rely on items being sequentially allocated to clusters in the partition. Although most partition distributions can be viewed as a sequentially allocated process, those that cannot may not have tractable CAPFs. In this section, we examine a few partition distributions that could serve as a baseline distribution for the SP distribution and provide their associated CAPFs.

3.2.1 The Chinese Restaurant Process

The two most common partition distributions are the Ewens (ewens1972sampling; pitman1995exchangeable; pitman1996some) and the Ewens-Pitman (pitman1997two) distributions (also referred to as the one-parameter and two-parameter Chinese restaurant process, respectively). The CAPF for the Ewens-Pitman partition distribution is:

| (7) | ||||

Although this distribution is invariant to item allocation order, we include a permutation parameter in the CAPF for notational consistency. The CAPF of the Ewens distribution can be obtain by setting in (7). Both the Ewens and Ewens-Pitman distributions have the “rich-get-richer” property which can be adjusted to some extent in the Ewens-Pitman distribution through the discount parameter .

3.2.2 The Uniform Partition Distribution

The uniform partition (UP) distribution is exchangeable and is a very simple partition distribution. To be used as a baseline distribution for the SP distribution, its CAPF is needed. To our knowledge, the sequential allocation rule for the uniform partition distribution is not contained in the literature elsewhere and we provide it here.

First, the total number of items to be partitioned, denoted , must be fixed and known. Then at the item’s allocation one must know the number of subsets allocated thus far in the partition (i.e., ) and also the number of items left to allocate (i.e., ). Now consider an extension of the Bell number , defined recursively by the following formulas: and , for all , (the nonnegative integers). We note that is the Bell number; additional information about the extension of the Bell number is included in Appendix LABEL:sec:eBells. The CAPF for the UP distribution is:

| (8) | ||||

for . When , the CAPF for the UP distribution is 1.

3.2.3 The Jensen-Liu Partition Distribution

The Jensen-Liu partition (JLP) distribution was introduced by jensen2008bayesian and later named in casella2014cluster. It places a uniform probability of allocating to any existing cluster and a distinct probability of forming a new cluster. Unlike the previously mentioned distributions in this section, the JLP is not exchangeable. The CAPF for the JLP (endowed with a permutation parameter) is:

| (9) | ||||

3.2.4 Other Possible Baseline Partition Distributions

Beyond those already mentioned, there are many other possible baseline partition distributions. dahl2017random introduces the Ewens-Pitman attraction (EPA) distribution which generalizes Ewens-Pitman distribution when distances (or similarities) between items are known. Using the EPA distribution would allow one to incorporate covariates into the partitioning of items by converting the covariates to similarities between items. Another recent addition to partition distributions is the Allelic partition distribution (betancourt2022prior). This distribution was developed specifically to have the microclustering property (that is, partitions contain many clusters in which there are relatively few items in each). This partition behavior is in stark contrast to the Ewens distribution, which favors large cluster sizes. Product partition models (hartigan1990partition, PPMs) can be used as a baseline in the SP distribution. Suitable extensions of PPMs incorporate covariates (muller2011product; park2010bayesian) or those that add spatial structure with covariates (page2016spatial).

4 Effect of Shrinkage Parameter on SP Distribution

An intuitive way to think about the shrinkage partition (SP) distribution from Section 3 is to view it as a compromise between a baseline partition distribution and the anchor partition . The nature of this compromise is controlled by the shrinkage parameter . In this section, we investigate in more detail how the shrinkage parameter influences the SP distribution.

4.1 Extremes and Smooth Evolution Between Extremes

The degree of compromise between the baseline partition distribution and the anchor partition is governed by the shrinkage parameter . In one extreme case, where each idiosyncratic shrinkage is relatively large, the SP distribution assigns probability mass to partitions that are very similar to the anchor partition and, in the limit, the distribution becomes a point mass distribution at the anchor partition . In the other extreme case, i.e., when the idiosyncratic shrinkages all equal zero, the SP reduces to the baseline distribution and the anchor partition has no influence in the SP’s pmf. We formally present these properties below.

Theorem 1.

Let be the partition with all items assigned to a single cluster, be the partition with items each assigned to a unique cluster, with , and :

| [Diffusion to the baseline dist’n] | |||

| [Anchor partition consistency] | |||

Recall that and are vectors of cluster labels. When statements such as are made, we imply that they are in the same equivalence class, that is, their cluster labels encode the same partition. The proof of Theorem 1 is given in Appendix LABEL:apx:blc. Between these extreme cases for the shrinkage (zero and infinity) and under certain conditions, the probability of the anchor partition is monotonically increasing in the shrinkage .

Theorem 2.

For any and such that , if and with , and , then .

A proof of Theorem 2 is included in Appendix LABEL:apx:blc. This theorem implies that controls how “close” in probability the SP distribution is to the anchor partition . Additionally, this closeness to is strictly increasing as increases.

Whereas Theorem 2 illustrates monotonically increasing probability for the anchor partition as a function of increasing , in fact the entire distribution is getting closer to a point mass distribution at the anchor partition. Formally, both the Kullback-Leibler divergence and the total variation distance between the SP distribution and a point mass distribution at the anchor partition decreases monotonically with increasing .

Theorem 3.

Consider two partition distributions: i) , a point mass at the anchor partition , and ii) such that with , , and . Then both the Kullback-Leiber divergence and the total variation distance are strictly decreasing as increases.

Although not a true metric, the Kullback-Leiber divergence provides a sense of how relatively “close” two distributions are to each other. This theorem reiterates the concept that the SP distribution is a compromise between the baseline distribution and the anchor partition . When , the SP distribution is identical to , and is at its maximum. Then, as increases, strictly decreases, or in other words, the SP distribution moves away from and toward the point mass distribution at . A proof of Theorem 3 is also included in Appendix LABEL:apx:blc.

Theorems 1, 2, and 3 all provide intuition for the shrinkage parameter, which is reinforced with an illustrative example. Consider the SP distribution in which the permutation is integrated out, , is the Ewens partition distribution with concentration parameter , and . The left plot in Figure 1 shows the evolution of the SP’s probabilities of an anchor partition as a function of increasing . The plot shows the probabilities for the partitions of items that are stacked so that, if a vertical line segment were drawn between 0 and 1 at some value of , then the line segment would be divided into 15 pieces, with the length of each piece representing the probability of one of the partitions. The length of the vertical line segment in the blue region denotes the probability of the anchor partition , which when , is determined solely from the baseline distribution and then converges to as goes to infinity. The plot visually depicts an example of anchor partition consistency, diffusion to the baseline distribution, and the smooth evolution between these two extremes. Also note that the partitions and are shaded in yellow. These partitions are similar to the and therefore have increasing probability for small shrinkage which eventually gives way to the anchor for large .

The upshot of these theorems is that the shrinkage parameter smoothly controls the compromise between a baseline partition distribution and the anchor partition . To some extent, depending on , the SP distribution inherits clustering properties of , which are tempered with the characteristics of the anchor partition .

4.2 Idiosyncratic Shrinkage Parameters

Recall that the SP distribution is parameterized with a vector-valued shrinkage parameter . Whereas the CPP and LSP have only a univariate shrinkage parameter to inform the compromise between the baseline distribution and the anchor partition , our SP distribution allows for idiosyncreatic shrinkages. The allowance of item-specific shrinkages offers unique flexibility in prior elicitation that is consequently not possible in existing distributions. Specifically, consider a data analysis scenario where there is strong prior knowledge regarding the clustering of a few items, but little or no prior knowledge regarding the clustering of the remaining items. In this case, the SP prior may avoid inadvertently imposing prior influence on less-understood relationships by setting corresponding shrinkage values to be relatively small or, at the extreme, itself. Conversely, strong a priori clustering information about a few items can be expressed without fear of unduly affecting items which are not well understood.

For illustration, consider again an SP distribution in which , is integrated out of the model, , and is the Ewens partition distribution with concentration parameter . Recall the scenario in Section 4.1 with the anchor and . Now assume instead there is no prior knowledge about the clustering of the fourth item (but we do have an indication that the first and second items are clustered together and are not clustered with the third item). That is, we are indifferent to , , and , apart from beliefs about the number and size of clusters encoded within the baseline distribution and the grit parameter . In this case, we let and any of these three values for the anchor partition yield exactly the same partition distribution. The evolution of probabilities as increases is illustrated in the right plot of Figure 1. Notice that , , and all retain probability as goes to infinity.

This example displays another key feature of the SP distribution when contains both zero and non-zero values. We highlight that the SP distribution is invariant to the a priori clustering of items with shrinkage parameter set to 0, i.e., . For example, the probabilities for the SP distribution specified in the right pane of Figure 1 would remain unchanged if instead of .

Theorem 4.

If and , where and are anchor partitions such that for every and where and , if and only if , then and are equal in distribution.

A proof of Theorem 4 is provided in Appendix LABEL:apx:blc. Essentially, it says that an item with a shrinkage parameter of zero can be placed into any cluster in the anchor partition without affecting the probabilities of the SP distribution. This fits nicely with an intuitive Bayesian interpretation of having a shrinkage parameter set to zero and relieves the modeler from making an arbitrary choice that could affect the analysis.

The behavior of the SP distribution is demonstrated in the right plot in Figure 1, and gives rise to what we refer to as “limiting partitions.” The definition of a limiting partition is:

Definition 1.

Let with for scalars . A partition which has non-zero probability as is a limiting partition.

When one or more idiosyncratic shrinkage parameters are set to zero and assuming , the SP distribution does not reduce to a point mass at as becomes large. However, remains a limiting partition, and if at least two items have then the number of limiting partitions is less than the number that are possible under . In the limit, this allows the SP distribution to force some items to be clustered and other items to be separated, and leave the remaining items to be randomly clustered according to . The following theorem, whose proof is in the appendix, characterizes the limiting partitions.

Theorem 5.

Consider any baseline distribution , anchor partition and fixed partition , such that and . For any with either 0 or 1, and , define to be the set of index pairs such that , , and . If for all index pairs in , then is a limiting partition of .

One interesting quantity of the SP distribution is the number of limiting partitions which exist. We know the number of possible partitions for items with no constraints is the Bell number, and on the other extreme, there is only one partition (a point mass) when all values in go to infinity. However, when only some elements in go to infinity, the number of limiting partitions is between those two extremes. Theorem 6, whose proof is found in Appendix LABEL:apx:blc, gives the number of limiting partitions.

Theorem 6.

Let , with for all possible and , where is either 0 or 1 and . Let be the number of items with shrinkage equal to zero. Let be the number of clusters in having at least one item with . As , the number of limiting partitions in the SP distribution is —an extension of the Bell numbers from Section 3.2.2.

5 Dependent Random Partitions

5.1 Hierarchically-Dependent Random Partitions

Over the past several decades, Bayesian hierarchical models have been used extensively with a great deal of success. Dependence among datasets can be induced between similar populations by placing a common prior distribution on parameters of interest, e.g., means and variances, and then placing a hyperprior distribution on the hyperparameters of the common prior distribution. Using our SP distribution, these same principles can be applied to dependent partitions. Specifically, consider separate collections of data, each with the same items to be clustered, and let , …, be the latent partitions. We can “borrow strength” in the estimation of these partitions through the following hierarchical model:

| (10) |

A standard choice for might be the CRP, however, any partition distribution could be used. Likewise any choice could be made for , e.g., another CRP or a SP distribution with a “best guess” anchor partition. Standard MCMC techniques can be used for posterior inference because the normalizing constant of the SP distribution is available.

The default choice for the shrinkage parameter might be with a prior on the scalar . A more sophisticated prior could easily be adapted, such as, , with . Here would permit each partition to have varying degrees of dependence among the collection of the partitions. The point is that the degree of dependence among , …, is governed by the shrinkage parameter . As with typical Bayesian hierarchical models, the model in (10) allows the extremes of independence and exact equality among the partitions , …, by setting or , respectively.

The hierarchy shown in (10) using the SP distribution is simple and can be expanded upon. For example, while analyzing neuroimaging data, song2023clustering generalizes the basic hierarchical structure we propose here. In particular, they use an early version of our SP distribution in an innovative model to simultaneously cluster in two domains, namely, bi-clustering subjects and conditions.

5.2 Temporally-Dependent Random Partitions

Modeling dependent partitions over time is also very natural using our SP partition distribution. Again, assume we are partitioning the same items and we have partitions , …, . Recently page2022dependent presented a model to induce temporal dependence in partitions. They argue that dependency should be placed directly on the partition as opposed to much of the literature, which attempts to induce dependence on an underlying random measure. We follow that same philosophy and model dependence directly on the partitions using our SP distribution. A basic time dependent model is:

| (11) |

for . For SP distribution models with data that are evenly spaced in time, we envision setting with a common parameter over time. However, unlike page2022dependent, our framework is not restricted to data analysis involving equally-spaced time points. For example, the model is easily modified by parameterizing the shrinkage to be time-dependent, e.g., , where is the difference in time between time and time .

6 Empirical Demonstration: Return to Education

In this section, we illustrate various uses of our shrinkage partition distribution, demonstrate the dependent partition models from the previous section, and compare results from related partition distributions. Consider a regression model studying the relationship between earnings and education attainment. The data were obtained from IPUMS CPS (ipums). In March of each year, a cross-section of individuals from the 50 United States and the District of Columbia (D.C.) are surveyed regarding their employment and demographic information. Data with harmonized variables are available from the years 1994 to 2020. Applying sensible filters for our application (e.g., only including working individuals) yields 139,555 observations. For simplicity, sampling weights are ignored for this demonstration.

Let be the vector of the natural logarithm of the average hourly earnings for individuals in state () in year (with corresponding to the year 1994 and ). Let be a matrix of covariates containing a column of ones for the intercept and the following mutually-exclusive dummy variables related to educational attainment: high school graduate, some college, or at least a bachelors degree. The matrix consists of non-education related covariates: age, age, hours worked weekly (weeklyhrs), weeklyhrs, and the following dummy variables: male, white, Hispanic, in a union, and married. We consider the regression model , where the elements of are independent and identically distributed normal with mean zero and precision . Conditional independence is assumed across states and years. Note that and lack a subscript and are therefore common across all states.

Interest lies especially in estimating the state-year specific regression coefficients regarding educational attainment. Some state-year combinations have sufficient data (e.g., California has at least 497 observations per year), but some have limited data (e.g., D.C. has a year with only 20 observations) such that estimating parameters would be very imprecise. One solution is to combine data from small states, although such combinations may be ad hoc. Instead, in a given year , we obtain parsimony and flexibility by postulating that the states are clustered by ties among for . Let be the clustering induced by these ties, where if and only if . For notational convenience, we label the first item , use consecutive integers for the unique cluster labels in , and let be the unique values for the regression coefficients. Let be the matrices obtained by vertically stacking the matrices for all such that . Likewise, define by vertically stacking matrices for all such that and let be the corresponding vector from concatenating for all such that .

The joint sampling model for data is:

| (12) |

where

| (13) |

where is an identity matrix and represents a multivariate normal distribution with mean and precision matrix .

We use the following joint prior distribution for the other parameters as the product of independent distributions. The prior of the precision in the sampling distribution is gamma with shape and rate , making the prior expected standard deviation equal a preliminary guess of 0.361 obtained by exploratory data analysis. The regression coefficient vector has a normal prior distribution with mean and precision . Based on preliminary explorations using ordinary least squares, the priors for the cluster-specific regression coefficients are independent and identically distributed normal with mean and precision is .

As the probability mass function of the shrinkage partition distribution is available in closed form, the full suite of standard MCMC algorithms are available to sample from the posterior distribution. Our approach for updating the cluster labels is a Pólya urn Gibbs sampler based on neal2000markov’s Algorithm 8. One caveat is that the SP distribution is not exchangeable, so its full pmf — or, at least, the part of the pmf involving the current item and any item allocated after it according to the permutation — must be computed.

Recall that we have years and therefore partitions . We now discuss three specifications for the joint prior distribution for . We first consider independent random partitions in Section 6.1 and use this model as a means to compare the SP distribution with the CPP and the LSP. We then consider hierarchically and temporally dependent random partitions in Sections 6.2 and LABEL:sec:temporal, respectively.

6.1 Independent Partitions Model

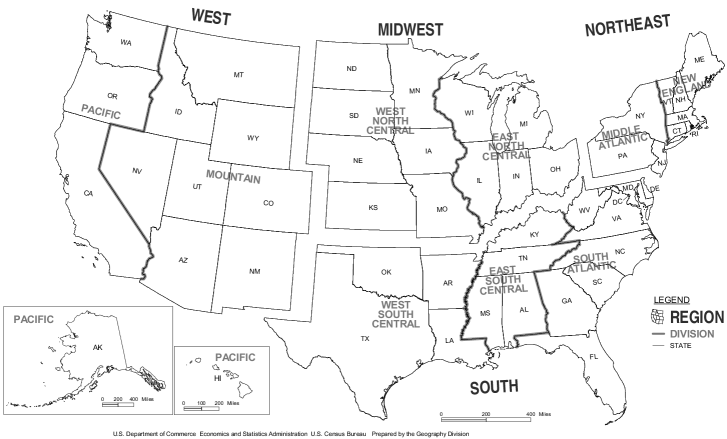

In this section, we consider various prior distributions for of the form . One’s best guess for an unknown partition may be the partition given by the four US Census Regions, shown in Figure 2. Indeed, at one extreme, one may wish to fix to be these regions, effectively using a point-mass distribution on the regions. At the other extreme, one may disregard the regions and specify, for example, that or .

We entertain compromises between these extremes. In this subsection, we fix to be the anchor partition given by the U.S. Census Bureau regions and consider several partition distributions informed by this “best guess” partition . Specifically, we consider the shrinkage partition (SP) distribution, the centered partition process (CPP), and the location-scale partition (LSP) distribution. Recall that the normalizing constant is not known for the CPP and hence the shrinkage value must be fixed to use standard MCMC methods to fit the model. In this subsection, for the sake of comparison with the CPP, we also fix the shrinkage for the SP and LSP. The specifics of how influences each distributional family differ and it is not clear how to calibrate an for each distributional family such that the influence of is commensurate. Instead, we consider a distribution-specific grid of values for and only present results for the best-fitting model of each distributional family. Specifically, we compare the following prior partition distributions: i. “Location-Scale Partition”: using our extension to make the analysis invariant to observation order, ii. “Centered Partition Process – VI”: , iii. “Centered Partition Process – Binder”: , iv. “Shrinkage Partition – Common”: with , v. “Shrinkage Partition – Idiosyncratic”: with having elements equal to for all states, except for Maryland, Delaware, District of Columbia, Montana, North Dakota, and South Dakota. These states with are on the borders of regions and it is reasonable to be less confident in the allocation to their particular region in the anchor partition . Note that, for the sake of comparison, we fix the concentration parameter at for the CRP baseline distribution. In practice, one might treat as random when using our SP distribution since it has a tractable normalizing constant.

To assess fit, we performed 10-fold cross validation as follows. The dataset was divided into 10 equally-sized, mutually-exclusive, and exhaustive subsets (shards). For each fold, one of the 10 shards was held out as the test dataset for a model fit with the other 9 shards. For each fold, 55,000 MCMC iterations were run, the first 5,000 were discarded as burn-in, and 1-in-10 thinning was applied for convenience. For each MCMC iteration, the permutation received ten Metropolis update attempts based on uniformly sampling ten items from and randomly shuffling them.

To assess fit, we use the out-of-sample log-likelihood, defined as the sum of the Monte Carlo estimate of the expectation of the log-likelihood contribution for each observation when it was part of the held-out shard. Models with larger values for the out-of-sample log-likelihood indicate a better fit. Results are summarized in Table 1, where the models are ordered with the best performing at the top. The “Shrinkage Partition Distribution – Idiosyncratic” model produces the best model fit by a wide margin. None of the 95% Monte Carlo confidence intervals overlap except for the “Shrinkage Partition Distribution – Common” and “Centered Partition Process – VI” cases. Each of the SP, CPP, and LSP models improve upon the one extreme of the CRP (which ignores the region information) and the other extreme of fixing the partition at the anchor partition . The CPU time for the full data analysis for each model is included in the table. All the timing metrics were computed on a server with 256 GB of RAM and with Intel Xeon Gold 6330 2.00GHz CPUs.

| Prior Partition Distribution | Out-of-Sample Fit | CPU Time |

|---|---|---|

| Shrinkage Partition Distribution – Idiosyncratic | ||

| Shrinkage Partition Distribution – Common | ||

| Centered Partition Process – VI | ||

| Location-Scale Partition | ||

| Centered Partition Process – Binder | ||

| Fixed Partition of | ||

| Chinese Restaurant Process |

6.2 Hierarchically-Dependent Random Partitions

The model in the previous subsection assumed a priori independence among the partitions . Note that we are repeatedly clustering the same items and one might expect an improvement by allowing the “borrowing of strength” in partition estimation. In this subsection, we demonstrate the Bayesian hierarchical model presented in Section 5.1. This illustrates that, in a very intuitive way, dependent partition models can be formulated in the same way as other Bayesian hierarchical models. We show that our model produces a large improvement in the out-of-sample log-likelihood when compared to the models in the previous subsection.

Consider the following model with the same likelihood as defined in (12) and (13), with a hierarchical prior for the partitions given in (10), with both and baseline distribution chosen to be . Of course, and could be specified separately or come from other distributional families, and it would still be straightforward to make inference on their hyperparameters. The key to this flexibility is that the SP distribution has a tractable normalizing constant, which allows for posterior inference on the anchor partition using standard MCMC techniques. Likewise, the tractable normalizing constant also readily permits posterior inference on the shrinkage parameter and other hyperparameters. In this demonstration, we set with the prior on being a gamma distribution with shape and rate . On the grit parameter , we place a beta prior with shapes and .

We again use the same 10-fold out-of-sample fit measure with the same sampling, burn-in, and thinning set-up as in the previous subsection, except, for every MCMC iteration, we attempted 200 updates for the permutation based on uniformly selecting five items. Although the acceptance rate for an individual Metropolis proposal to update the permutation was only 0.009, the ordering of 57% of the items changed per MCMC iteration. Because of the stickiness associated with the permutation , we repeated the whole exercise five times with randomly selected starting values for the permutation and then combined the samples after burn-in. The out-of-sample fit was , a substantial improvement of about 262 units from the best model fit from the independence models in Section 6.1. This improvement is even more impressive when recognizing that the region information in Figure 2 was not incorporated in this (and the subsequent) model. The CPU time for the model was approximately 4.28 hours; about a third of that time was used to update the anchor partition, a third on the permutation, and the last third all the other parameters.

The prior and posterior distributions of and are included in Figure LABEL:fig:shrinkage. The figure shows that posterior learning on these two parameters is occurring. The plot on the right-hand-side of Figure LABEL:fig:shrinkage shows the SALSO estimate (dahl2022search) anchor partition . The color intensity in the plot represents the posterior probability that two states are co-clustered (with red indicating 1 and white indicating 0). It is interesting that there are four very distinct clusters, not unlike the Census Bureau regions in Figure 2.