Marginal Effects for Probit and Tobit with Endogeneity

Kirill S. EvdokimovUniversitat Pompeu Fabra and Barcelona School of Economics: kirill.evdokimov@upf.edu.Ilze KalninaNorth Carolina State University: ikalnin@ncsu.edu.Andrei

ZeleneevUniversity College London: a.zeleneev@ucl.ac.uk.

Evdokimov gratefully acknowledges the support from the Spanish MCIN/AEI via

grants RYC2020-030623-I, PID2019-107352GB-I00, and Severo Ochoa Programme

CEX2019-000915-S.

(This version: June 22, 2023)

Abstract

When evaluating partial effects, it is important to distinguish between

structural endogeneity and measurement errors. In contrast to linear models,

these two sources of endogeneity affect partial effects differently in

nonlinear models. We study this issue focusing on the Instrumental Variable

(IV) Probit and Tobit models. We show that even when a valid IV is

available, failing to differentiate between the two types of endogeneity can

lead to either under- or over-estimation of the partial effects. We develop

simple estimators of the bounds on the partial effects and provide easy to

implement confidence intervals that correctly account for both types of

endogeneity. We illustrate the methods in a Monte Carlo simulation and an

empirical application.

Keywords: (Average) Partial Effects, Instrumental Variable, Control

Variable, Errors-in-Variables, Counterfactuals

1 Introduction

Probit and Tobit are some of the most popular nonlinear models in applied

economics. When a covariate is endogenous, IV-Probit and IV-Tobit models are

used for instrumental variable (IV) estimation of the coefficients (Smith and

Blundell, 1986, Rivers and

Vuong, 1988).111For example, in Stata, these estimators are ivprobit and ivtobit.

A covariate can be endogenous for two reasons. First, the covariate can be

correlated with the individual’s unobserved characteristics (unobserved

heterogeneity). Second, mismeasurement of the covariate

(Errors-in-Variables, EiV) also results in endogeneity. We will refer to

these two types of endogeneity as the “structural” endogeneity and the EiV. In many empirical

settings both sources of endogeneity need to be addressed simultaneously.

The goal of this paper is to characterize the partial effects in the classic

IV-Probit and IV-Tobit models, allowing for both types of endogeneity, and

to emphasize the importance of distinguishing between the two types. We

provide the expressions for the partial effects and average partial effects

that correctly account for the two kinds of endogeneity. Although the two

sources of endogeneity cannot be precisely distinguished using the observed

data, we use the constraints of the model to obtain bounds on the amounts of

endogeneity that can be attributed to each source. We use these bounds to

provide simple estimators of the bounds on the partial and average partial

effects, allowing for both types of endogeneity. We also provide

corresponding valid confidence intervals that are easy to calculate.

In nonlinear models, the need to differentiate between the two kinds of

endogeneity arises because structural endogeneity and EiV play different

roles. In particular, partial effects of covariates are averaged with

respect to the distribution of the individual unobserved heterogeneity. On

the other hand, one aims to remove the impact of the measurement errors,

since they are not properties of individuals but a deficiency in the

measurement process. Thus, even though the IV-Probit and IV-Tobit methods

consistently estimate the coefficients on all regressors regardless of the

source of endogeneity, the effects of the covariates on the outcomes are

only partially identified, since the distribution of the unobserved

heterogeneity is partially identified. The width of the identified set

depends on how hard it is to disentangle structural endogeneity and EiV for

the data at hand. Importantly, we find that naively ignoring the distinction

between the two types of endogeneity can result in both under- and

over-estimation of the magnitude of the partial effects by these IV

estimators.222Wooldridge (2010), page 586, alludes to the

potential importance of the sources of endogeneity for the partial effects

in IV-Probit, but does not elaborate.

IV-Probit and IV-Tobit can be interpreted as control variable estimators.

Partial effects in general control variable models were considered by Blundell and

Powell (2003), Chesher (2003), Imbens and

Newey (2009), and Wooldridge (2005, 2015), among

others. In nonlinear models, accounting for both types of endogeneity is

difficult, see, e.g., Schennach (2022), and it is not clear how to

characterize the bounds on the partial effects in practice. Recently, Chesher

et al. (2023) studied IV methods for the Tobit models relaxing

the first stage specification assumptions, but did not consider EiV.

The assumption of gaussianity of the unobservables simplifies the analysis

of the IV-Probit and IV-Tobit models and allows us to obtain simple bounds

and confidence intervals on the true partial effects that are easy to

implement. It would be important to relax the gaussianity assumption in the

future. At the same time, the simplicity of the proposed approach makes it a

convenient starting point in empirical analysis.

In particular, it allows researchers to gauge the importance of properly

accounting for both types of endogeneity, which is essential given the

ubiquity of both in economics.

The rest of the paper is organized as follows. The analysis of partial

effects in the Probit and Tobit models is virtually identical, thus we first

consider Tobit in Sections 2-3. In Section 4, we explain how the methods apply to the Probit model,

and extend the analysis to cover the average partial effects and other

counterfactuals. Section 5 provides some Monte Carlo simulation

results. Section 6 presents an illustrative empirical

application.

2 The Model

The Tobit model is often used for estimation of economic models with a

“corner solution,” i.e., models where the

outcome variable is forced to be non-negative. The examples of

such dependent variables include the amounts of charitable

contributions, hours worked, or monthly consumption of cigarettes.

First, consider the standard Tobit model with exogenous covariates and

without EiV:

(1)

the individual unobserved heterogeneity has a normal

distribution and is independent

from the covariates and . We use the asterisk to

denote variables that will be affected by the EiV, as we explain in detail

below.

We collect the covariates in a vector , so (1) can be

written as . The standard normal cumulative distribution and density

functions are denoted by and , respectively.333Most of the analysis in Sections 2 and 3

equally applies to the Probit model. For simplicity of exposition, we focus

on the Tobit model for the moment, and then discuss Probit in Section 4.1.

In the Tobit model, one is usually interested in the partial effects

(marginal effects) of covariates on and . For concreteness we consider partial effects of the continuously

distributed covariates.

The partial effect of the covariate on the mean at a

given is

(2)

The partial effect of the covariate on the probability is

(3)

These formulas for the are standard, see, e.g., Wooldridge (2010), for detailed calculations. Most often one considers

the partial effects at the means of the covariates .

When is correlated with and we observe data , the IV-Tobit model can be

estimated using instrumental variables , as proposed by Smith and

Blundell (1986), Newey (1987), and Rivers and

Vuong (1988).

Assume that

(4)

(5)

where is a normal random variable, possibly correlated with :

(6)

The IV-Tobit model in (4)-(6) can be

estimated using a random sample of in two steps, see, e.g., Wooldridge (2010).

First, one estimates in equation (5) by

the the residuals in the regression of

on . Note that we can write , where , and is independent of , , and (and

hence of ). Then, one estimates the standard Tobit model

where are replaced by their estimates .

(Alternatively, the two steps can be combined and all of the parameters can

be estimated simultaneously by the Maximum Likelihood Estimator.) The reason

this approach works is that equation (5) creates a

control variable , and the inclusion of in

the above equation makes exogenous.

To estimate the partial effects, one would plug the estimates and into equations (2)-(3) in place of and .

So far we were assuming that the data has no measurement errors. We now

allow to be mismeasured, i.e., that instead of we observe its noisy measurement :

(7)

We assume that , i.e., the measurement error is classical.

Note that the objects of researchers’ interest do not change: the goal is to

estimate the partial effects (2)-(3). The

structural endogeneity and measurement errors are difficulties that an

estimation procedure needs to overcome. In particular, note that we are

interested in estimation of the effect of on , and

not in the effect of the mismeasured .444This is similar to the linear regression settings, where one would be

interested in the effect of on . The slope

coefficient in the OLS regression of on is not the object

of interest because it is subject to the attenuation bias due to the EiV

(and also possibly due to the endogeneity of ).

3 Analysis of the Model

First, we use the model in equations (4)-(7) to

obtain the model in terms of the observable . Since , we can rewrite (4) as

where . Let . The model in equations (4)-(7) can be written as

(8)

(9)

(14)

The definitions of and imply that

(15)

Note that variables are the analogs of the true

variables that arise due to the

measurement errors . In the absence of measurement errors,

i.e., when , we have , ,

The model in equations (8)-(14) can be estimated by MLE or using the control variable two-step

approach described earlier. Specifically, both approaches will consistently

estimate parameters and the covariance matrix of the

unobservables in equation (14), i.e., , , and . Note that because the

model is nonlinear, the marginal effects (2)-(3) depend not only on but also on . Thus, even though the available data allows immediately estimating , we cannot obtain the marginal effects because we do not know . Naively using an estimate of in place

of would lead to a biased estimate of the partial

effects, since , as implied by

equation (15).

The problem with identifying is that the data only

allows identification of the parameters , , and . However, the distribution of the true is governed by

parameters: , , , and . Thus, one cannot

uniquely determine these parameters from the equations (15). In other words, models with different values of

are observationally equivalent: they correspond

to identical distributions of the observables even though they imply different values of

true . Thus, one cannot uniquely determine (i.e.,

point-identify) from the data . Correspondingly, one cannot point-identify

the partial effects, which depend on .

Equations (15) provide restrictions on , which we will use to provide bounds on the possible

values of true , and hence on the values of the

partial effects.

Bounds on

From equations (15) the upper bound on is . We now

obtain the lower bound on . In particular, we look

to find the smallest that satisfies equations (15), Cauchy-Schwarz inequality , and the

non-negativity constraints , , and . Let .

Proposition 1 provides the bounds in terms of the

quantities that can be estimated using the data . Condition guarantees that the denominator in the fraction above

is positive. The proof of Proposition 1 also provides

bounds on and .

Correct Partial Effects

We now use the bounds on from Proposition 1 to obtain the bounds on the partial effects, in

terms of the parameters that can be recovered from data.

For a given ,

the partial effects for the covariate are, as in equations (2)-(3),

(17)

The lower and upper bounds for partial effects for the covariate, , are computed as

(18)

Function in (17) is a monotone function of , so the minimum and maximum in equation (18)

are achieved on the boundaries of interval .

Function in

equation (17) is not monotone in , but the bounds in equation (18)

for can also be simplified. The minimum and

maximum over can be attained only at , at , and, when ,

at .

Thus, one only needs to evaluate at these or points to calculate the minimum and

maximum in equation (18).

Since , naively using

instead of when calculating , would lead to attenuation bias when ,

but would bias away from zero when , i.e., the EiV would make naive over-estimate the partial effects in the latter case. Likewise, for the

probability, naively using

can both under- and over-estimate the true partial effect .

Estimation

Using the standard two-step or MLE approaches described in Section 2, one obtains the estimates of , , , and (and of their variance-covariance

matrix for inference). Then, from equation (16) one

obtains the estimate of .

For a given value of , the estimated partial

effects would be

(19)

Then, the estimated bounds on are

(20)

where the minimum and maximum are easily computed using univariate numerical

optimization. For the partial effects in equation (19), these extrema can also be computed as described

under equation (18).

For example, one often considers the partial effects at the mean values of

covariates taking , where

and are the sample averages. Note

that .

Inference

To provide a simple method for inference about the partial effects, we adopt

a Bonferroni approach (e.g., McCloskey, 2017). This approach

allows us to avoid computational challenges that often arise in the context

of subvector inference in partially identified models. The construction of a

confidence interval for a partial effect proceeds in

two steps:

1.

Pick and construct , a confidence interval for , based on the bounds provided in Proposition 1.

2.

Construct a confidence interval for as the

union , where is a standard confidence interval

for based on in equation (19) for a

given .

We now provide the implementation details for each step.

Step 1. The confidence interval for is constructed based on the bounds given in Proposition 1. As the upper bound, we take , where is the standard error of , and is the quantile of the standard

normal distribution. The lower bound is based on , where

and are the plug-in estimators of the two terms on the right

hand side of equation (16). Note that

and are (generally) jointly asymptotically normal and their

asymptotic variance-covariance matrix can be computed using the delta

method. Then, as the lower bound of , we take . Here and are the standard errors of and , and is the quantile of , where are jointly normal with unit variances and

correlation , and is an estimator of the correlation between and (e.g., see Romano and

Wolf, 2005).

By a standard argument, the confidence interval for

given by

has asymptotic coverage at least for the true . In the numerical illustrations we take .

Step 2. First, the standard is constructed by adding and

subtracting from . The standard error of can be computed

using the delta method. Then we can construct

as

where the minimum and maximum are easily calculated using univariate

numerical optimization over . By the standard

Bonferroni argument, the confidence interval

has asymptotic coverage of at least for the true partial effect .

The constructed confidence interval is asymptotically valid as long as (i)

the first step confidence interval covers the true with probability at least

asymptotically, and (ii) the delta method applies to for the true . Both conditions are satisfied provided that the true is bounded away from zero. Note that in this case is valid even if is equal to (or local to) zero, which

implies that is also valid.

4 Extensions

4.1 Probit

IV-Probit is the same as IV-Tobit except in equation (4). Since Probit is a binary

outcome model, in equation (14) one imposes the

standard normalization . For Probit, we are interested in the

partial effects of covariates on the probability of , which are

given by in equation (3). Similarly to the IV-Tobit model, the IV-Probit model can be estimated by MLE

or by the two-step approach identical to the one described in Section 2, except the second step uses the standard Probit estimator in

place of the Tobit estimator. Then the bounds on are estimated as in equation (20). Confidence intervals for can be computed exactly

as described above.

4.2 Average Partial Effects and other Other Counterfactuals

In addition to the partial effects at a given , researchers are often

interested in the Average Partial Effects

(21)

which are the partial effects averaged with respect

to the distribution of . Define

Note that the distribution of is not directly observable due

to the EiV. Averaging with respect to the

distribution of the observed would result in biased estimators of the APEs. To account for

this, in the Appendix we show that these APEs can be calculated as

(22)

(23)

Hence, for any given value of , these APEs can be

estimated by

Finally, the estimated bounds on the APEs are obtained by finding the

minimum and maximum over . These can be easily

computed numerically, since are smooth

functions of a scalar argument . Our two-step approach to inference also

applies to the APEs with a minimal modification. The only difference is that

in Step 2 the construction of the standard error as usual needs to account for

the sampling variability in both the parameter estimators and the data

entering the expressions for the APEs directly.

It is also straightforward to apply our analysis to other counterfactuals,

including partial effects and APEs of discrete covariates, as well as to the

ordered Probit and two-sided Tobit models. Proposition 1 and the bounds on remain the same, and

hence the estimation and inference procedures remain unchanged, except for

different formulas in equations (17)-(20) corresponding to the counterfactuals of

interest.

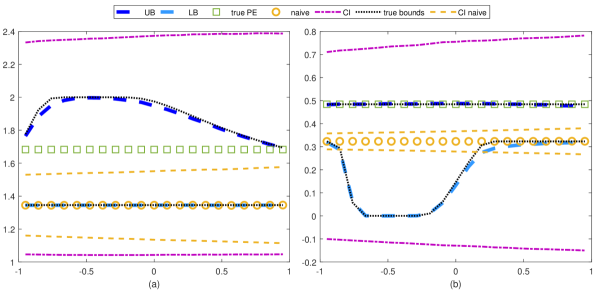

5 Numerical Illustration

We simulate a Tobit model with endogenous and mismeasured ,

as in equations (4)-(7), with , , , and . Figure 1 plots the results for the Partial Effects (PEs) of

at the population mean values of the covariates.

We consider a range of designs corresponding to the true values of on the horizontal axis.

For each , the figure shows the true PE

(“true”), the true (population) bounds

for the PE obtained using Proposition 1

(“true bounds”), as well as the medians

over the Monte Carlo replications of the estimated lower and upper bounds on

the PE (“LB” and “UB”) and the corresponding confidence intervals

(“CI”) based on the two-step IV-Tobit

estimator. The true bounds for the PE are calculated using the point

identified parameters , , , and , see equations (8)-(14). For comparison, we also include the results for the PE

calculated using the standard naive IV-Tobit estimator (“naive”) and the corresponding confidence intervals

(“CI naive”). The “naive” estimators of the partial effects are and , i.e., they replace with in equation (19).

Figure 1: Simulation results for partial effects on: (a) expectations, , and (b) probability, . Values of are on

the horizontal axis.

Figure 1 (a) shows the bounds on , while Figure 1 (b) considers . As expected, the true PE is between the lower and upper

bounds for all values of . By construction, the

“naive” IV-Tobit estimator of coincides with one of the bounds. In both

panels, the “naive” estimates are below

the true values for every , and the

“naive” IV-Tobit confidence intervals do

not include the true PE. In this design, the identified set and the

confidence intervals for the true partial effects are much wider than those

of the “naive” estimator. The relative

width of the identified set and the confidence intervals depends on the

specific parameter values. In contrast to these simulations, in the example

of the next section, the identified set is very narrow and the confidence

intervals for the partial effects have width similar to those of the naive

estimator.

To gain some intuition about the shape of the bounds in Figure 1,

notice that when , measurement error in

introduces a negative correlation between and . Thus,

observing is only consistent with , but not with , i.e., implies

positive correlation due to the structural endogeneity. On the other hand,

observing can be explained both by the effect of EiV combined

with , and by without any EiV. Thus, when it is harder to disentangle

structural endogeneity and EiV. As a consequence, the true and the estimated

correct bounds on the PEs in Figure 1 are wider for the negative

values of .

6 Empirical Illustration

We illustrate the proposed methods in the estimation of the Tobit and Probit

models for women’s labor force participation. We use the classic data set

from Mroz (1987) who estimates Tobit and related models to explain

married women’s hours of work. The data contains 753 women, 428 of which

report working non-zero hours. For Tobit, the dependent variable is the

number of hours worked (hours), and for Probit, the dependent

variable is working at some point during the year (). In both

models, the covariates are age, education, experience, experience squared,

nonwife income in thousands (nwifeinc), number of children less

than six years of age, number of children between 6 and 18 inclusive, and an

intercept. Husband’s years of schooling, huseduc, are used as an

instrument for nwifeinc. This specification is used in, e.g., Wooldridge (2010). Nonwife income could be correlated with the unobserved

characteristics (structural endogeneity), and income variables are also

known to be frequently mismeasured.

Tobit

IV-Tobit

CI for IV-Tobit

[LB, UB]

CI

nwifeinc

-5.33

-19.0

[ -39.6, 1.68 ]

[ -19.1, -19.0 ]

[ -41.6, 2.44 ]

educ

48.7

70.3

[ 29.0, 112 ]

[ 70.3, 70.8 ]

[ 26.9, 117 ]

exper

79.5

74.9

[ 51.6, 98.2 ]

[ 74.9, 75.4 ]

[ 50.3, 102 ]

exper2

-1.13

-1.14

[ -1.82, -0.468 ]

[ -1.15, -1.14 ]

[ -1.89, -0.444 ]

age

-32.9

-28.2

[ -39.3, -17.2 ]

[ -28.4, -28.2 ]

[ -40.6, -16.8 ]

Table 1: Tobit. Partial Effects on Expectation.

Tobit

IV-Tobit

CI for IV-Tobit

[LB, UB]

CI

nwifeinc

-0.303

-1.06

[ -2.16, 0.043 ]

[ -1.10, -1.06 ]

[ -2.65, 0.157 ]

educ

2.77

3.92

[ 1.75, 6.10 ]

[ 3.92, 4.08 ]

[ 1.33, 7.48 ]

exper

4.52

4.18

[ 2.77, 5.59 ]

[ 4.18, 4.34 ]

[ 2.51, 6.51 ]

exper2

-0.064

-0.064

[ -0.102, -0.026 ]

[ -0.066, -0.064 ]

[ -0.121, -0.022 ]

age

-1.87

-1.58

[ -2.26, -0.890 ]

[ -1.64, -1.58 ]

[ -2.60, -0.834 ]

Table 2: Tobit. Partial Effects on Probability. All numbers are multiplied by 100.

Probit

IV-Probit

CI for IV-Probit

[LB, UB]

CI

nwifeinc

-0.470

-1.39

[ -2.67, -0.104 ]

[ -1.49, -1.39 ]

[ -3.29, 0.079 ]

educ

5.11

6.41

[ 3.96, 8.86 ]

[ 6.41, 6.87 ]

[ 2.98, 10.8 ]

exper

4.82

4.38

[ 2.68, 6.08 ]

[ 4.38, 4.70 ]

[ 2.49, 6.82 ]

exper2

-0.074

-0.073

[ -0.118, -0.028 ]

[ -0.079, -0.073 ]

[ -0.137, -0.024 ]

age

-2.06

-1.69

[ -2.58, -0.804 ]

[ -1.81, -1.69 ]

[ -2.87, -0.784 ]

Table 3: Probit. Partial Effects on Probability. All numbers are multiplied by 100.

Tables 1-2

contain the results on partial effects for Tobit. Table 1 contains the results on partial effects on

expectation, , while Table 2

contains partial effects on probability, . All partial

effects are evaluated at the mean values of covariates. In both tables, the

first column (“Tobit”) provides the partial effects for

different covariates in the standard Tobit MLE where all covariates are

assumed to be exogenous.

The remaining columns are based on the two-step IV-Tobit estimator, where

huseduc is used to instrument for the endogenous nwifeinc.

The second column (“IV-Tobit”) contains the naive

estimators of the partial effects, followed by the confidence

intervals (column “CI for IV-Tobit”). Column

“[LB, UB]” provides the proposed estimated bounds

for the partial effects that account for both types of endogeneity. The last

column contains the corresponding confidence intervals for the partial

effects.

In both Tables 1 and 2, we observe that the confidence intervals for

the correct partial effects at the mean are only slightly wider than the

naive ones of IV-Tobit. In particular, using the correct inference approach

does not change any of the conclusions about the effects of the variables

being statistically significant.

Table 3 contains the corresponding results

for Probit. Again, the confidence intervals for the correct partial effects

are not much wider than the naive ones. Unlike the Tobit case, not all

conclusions about the statistical significance of the partial effects are

preserved, as the partial effect of nonwife income becomes statistically insignificant. Hence, if we base our analysis only on

the binary outcome model, properly accounting for the roles of measurement

error and structural endogeneity can reverse the conclusion that the partial

effect of nonwife income is statistically significantly different from zero.

References

Blundell and

Powell (2003)Blundell, R. and J. L. Powell (2003): “Endogeneity in

Nonparametric and Semiparametric Regression Models,” in Advances in

Economics and Econometrics, ed. by M. Dewatripont, L. P. Hansen, and S. J.

Turnovsky, 312–357.

Chesher (2003)Chesher, A. (2003): “Identification in Nonseparable Models,”

Econometrica, 71, 1405–1441.

Chesher

et al. (2023)Chesher, A., D. Kim, and A. M. Rosen (2023): “IV methods for

Tobit models,” Tech. rep., University College London.

Imbens and

Newey (2009)Imbens, G. and W. Newey (2009): “Identification and Estimation

of Triangular Simultaneous Equations Models without Additivity,”

Econometrica, 77, 1481–1512.

McCloskey (2017)McCloskey, A. (2017): “Bonferroni-based size-correction for

nonstandard testing problems,” Journal of Econometrics, 200, 17–35.

Mroz (1987)Mroz, T. A. (1987): “The Sensitivity of an Empirical Model of

Married Women’s Hours of Work to Economic and Statistical Assumptions,”

Econometrica, 55, 765.

Newey (1987)Newey, W. K. (1987): “Efficient estimation of limited

dependent variable models with endogenous explanatory variables,”

Journal of Econometrics, 36, 231–250.

Rivers and

Vuong (1988)Rivers, D. and Q. H. Vuong (1988): “Limited Information

Estimators And Exogeneity Tests For Simultaneous Probit Models,”

Journal of Econometrics, 39, 347–366.

Romano and

Wolf (2005)Romano, J. P. and M. Wolf (2005): “Stepwise Multiple Testing

as Formalized Data Snooping,” Econometrica, 73, 1237–1282.

Schennach (2022)Schennach, S. (2022): “Measurement Systems,” Journal of

Economic Literature, 60, 1223–1263.

Smith and

Blundell (1986)Smith, R. J. and R. W. Blundell (1986): “An Exogeneity Test

for a Simultaneous Equation Tobit Model with an Application to Labor Supply,”

Econometrica, 54, 679.

Wooldridge (2005)Wooldridge, J. M. (2005): “Unobserved Heterogeneity and

Estimation of Average Partial Effects,” in Identification and Inference

for Econometric Models: Essays in Honor of Thomas Rothenberg, ed. by

D. Andrews and J. Stock, Cambridge University Press, 27–55.

Wooldridge (2010)

——— (2010): Econometric Analysis of

Cross Section and Panel Data, Second Edition, The MIT Press.

Wooldridge (2015)

——— (2015): “Control Function Methods

in Applied Econometrics,” Journal of Human Resources, 50, 420–445.

Appendix

Proof of Proposition 1. Note that

combined with equation (15)

implies

Since , the denominator in this

fraction is positive. Since , let

Then

(24)

Note that

Thus, in equation (24) can be equivalently written as

where the fraction is always non-negative, ensuring that . Finally, equation (15)

implies that is bounded between

and .