Identifiability of causal graphs under nonadditive conditionally parametric causal models

Abstract

Causal discovery from observational data is a rather challenging, often impossible, task. However, an estimation of the causal structure is possible under certain assumptions on the data-generation process. Numerous commonly used methods rely on the additivity of noise in the structural equation models. Additivity implies that the variance or the tail of the effect, given the causes, is invariant; thus, the cause only affects the mean. However, the tail or other characteristics of the random variable can provide different information regarding the causal structure. Such cases have received very little attention in the literature thus far.

Previous studies have revealed that the causal graph is identifiable under different models, such as linear non-Gaussian, post-nonlinear, or quadratic variance functional models. In this study, we introduce a new class of models called the conditional parametric causal models (CPCM), where the cause affects different characteristics of the effect. We use sufficient statistics to reveal the identifiability of the CPCM models in the exponential family of conditional distributions. Moreover, we propose an algorithm for estimating the causal structure from a random sample from the CPCM. The empirical properties of the methodology are studied for various datasets, including an application on the expenditure behavior of residents of the Philippines.

Keywords: causal discovery, structural causal models, identifiability, causality from variance and tail, exponential family

1 Introduction

Having knowledge regarding causal relationships rather than statistical associations enables us to predict the effects of actions that perturb an observed system (Pearl and Mackenzie, 2019). Determining causal structures is a fundamental problem in numerous scientific fields. However, several data-generating processes can produce the same observational distribution. Observing the system after interventions is a reliable means to identify the causal structure, but in numerous real-life scenarios, interventions can be too expensive, unethical (Greenland et al., 1999), or impossible to observe. Hence, estimating the causal structure from observational data has become an important topic in recent years.

In the last few years, much effort has been put into developing a mathematical background for a “language” of causal inference (Pearl, 2009). The theory stands on the structural causal model (SCM) for random variables , with structural equations in the form , where are the causal functions belonging to a certain subclass of real functions , represent the direct causes of , and are independent noise variables. The SCM is an important mathematical concept, and the fundamental goal of causal discovery is to estimate the causal structure (causal graph associated with SCM) or the direct causes of a certain variable of interest. However, estimating the causal structure is impossible without strong assumptions on the class (Peters et al., 2017).

The extant literature in the field presents numerous methods and consequent results for causal inference under different assumptions on the SCM (Glymour et al., 2019). If we observe several environments after different interventions, the assumptions can be much less restrictive (Peters et al., 2016). If we aim to discover causal relations based only on an observed random sample, the assumptions are usually more strict—assuming linear structure or additive noise (Peters et al., 2014).

The additivity assumption () implies that affects only the mean of . One well-known approach that enables more general effects of the covariates is post-nonlinear model (PNL; Zhang and Hyvärinen, 2010). This model potentially allows an effect of on the variance of , but it does not allow arbitrary relations. Quadratic variance function (QVF) models introduced in Park and Raskutti (2017) consider the variance to be a quadratic function of the mean, and location-scale models defined in Immer et al. (2022) allow arbitrary effect on the variance. However, these models assume a fixed tail and fixed higher moments.

In this paper, we develop a framework where can arbitrarily affect the mean, variance, tail, or other characteristics of . However, a caution have to be taken because if affects in a certain manner, the causal structure will become unidentifiable (several causal structures can produce the same distribution of X). We expose the assumptions that are reasonable in order to obtain an identifiable causal structure.

Example 1.

A useful model that allows an arbitrary effect on the variance as well as on the mean is for some functions , in which case the structural equation has the form

| (1) |

The central limit theorem can justify (1) if X is an appropriate sum of independent events.

Example 2.

In certain applications, it may be reasonable to assume

where is the function that describes the tail behaviour. Such a model is common when represents extreme events (Coles, 2001).

In Section 2, we introduce a causal model (we call it the conditionally parametric causal model or CPCM) where the structural equation has the following form:

| (2) |

where is a known distribution function with a vector of parameters . We restrict our focus mostly to the case in which belongs to the exponential family of continuous distributions when sufficient statistics can be used. Section 3 provides the identifiability results of the causal structure in the bivariate case. Assuming (2), is it possible to infer the causal structure based only on observational data? In Section 4, we discuss the multivariate extension. In Section 5, we propose an algorithm for estimating the causal graph under assumption (2). In Section 6, we proceed to a short simulation study, and in Section 7 we illustrate our methodology on a dataset concerning income and expenditure of residents of Philippines.

We provide three appendices: Appendix A contains proofs of the theorems and lemmas presented in the paper. Appendix B contains detailed definitions and explanations for a few concepts that were omitted from the main part of the paper for the sake of clarity. Appendix C presents some details about the simulation study and the application.

1.1 Setup and notation

We borrow the notations of Spirtes et al. (2001) and introduce the notation of graphical causal models. A directed acyclic graph (DAG) contains a finite set of vertices (nodes) and a set of directed edges between distinct vertices. We assume that there exists no directed cycle or multiple edges.

Let be two distinct nodes of . We say that is a parent of if there exists an edge from to in , and we note . Moreover, such is called a child of , with notation . We say that is an ancestor of , if there exists a directed path from to in , notation . In the other direction, we say that is a non-descendant of , if , notation . In addition, we say that the node is a source node if , notation . We omit the argument if evident from the context.

We use capital for distributions and small for densities. Consider a random vector over some probability space with distribution . With a slight abuse of notation, we identify the vertices with the variables . We denote for . We focus on the case in which X has a continuous joint density function with respect to the Lebesgue measure.

The distribution is Markov with respect to if for are disjoint subsets of the vertices and represents a d-separation in (Verma and Pearl, 2013). On the other hand, if for all disjoint subsets of the vertices hold , we say that the distribution is faithful with respect to . A distribution satisfies causal minimality with respect to if it is Markov with respect to , but not to any proper subgraph of . Moreover, it can be shown that faithfulness implies causal minimality (Peters et al., 2017, Proposition 6.35). Two graphs are Markov equivalent if the set of distributions that are Markov with respect to is the same. We denote the Markov equivalency class of as the following set . A set of variables X is said to be causally sufficient if there is no hidden common cause that causes more than one variable in X (Spirtes, 2010). The main concept in causal inference is the SCM (Verma and Pearl, 2013), defined in the following manner.

Definition 1 (SCM).

The random vector follows the SCM with DAG if for each the variable arises from the following structural equation:

where is jointly independent and are measurable functions.

The SCM uniquely defines a distribution of X that can be decomposed into a product of conditional densities or causal Markov kernels (Peters et al., 2017, Definition 6.21)

| (3) |

where represents the conditional density function of the random variable conditioned on its parents . Note that every distribution that is Markov with respect to can be decomposed into (3).

A core concept in causal inference is the identifiability of the causal structure. It is straightforward to compute if the DAG and the Markov kernels (3) are given. However, we deal with the opposite problem, where is given (or a random sample from ) and we want to infer .

Consider the SCM from Definition 1 with conditional densities that satisfy (3). Let , where is the set of all DAGs over and assume that , where is the subset of all conditional density functions. Let . The given pair generates the density .

Definition 2.

We say that the pair is identifiable in if there does not exist a pair , , such that . We say that the class is identifiable over if every pair is identifiable in .

1.2 Related work

Several papers address the problem of the identifiability of the causal structure (for a review, see Glymour et al. (2019)). Shimizu et al. (2006) show identifiability for the linear non-Gaussian additive models (LiNGaM), where for non-Gaussian noise variables . Bühlmann et al. (2014) explore causal additive models (CAM) of the form for smooth functions . Hoyer et al. (2009) and Peters et al. (2014) develop a framework for additive noise models (ANM), where . Under certain (not too restrictive) conditions on , the authors show the identifiability of such models (Peters et al., 2014, Corollary 31) and propose an algorithm estimating (for a review on ANM, see Mooij et al. (2016)). All these frameworks assume that the variance of does not depend on . This is a crucial aspect of the identifiability results.

Zhang and Hyvärinen (2009) consider the following PNL model

with an invertible link function . Here, potentially for the special choice . The PNL causal model a rather general form (the former two are its special cases). However, it is identifiable under certain technical assumptions and with a few exceptions (Zhang and Hyvärinen, 2010).

Park and Raskutti (2015, 2017) reveal identifiability in models in which is a quadratic function of . If has a Poisson or binomial distribution, such a condition is satisfied. They also provide an algorithm based on comparing dispersions for estimating a DAG in polynomial time. Other algorithms have also been proposed, with comparable speed and different assumptions on the conditional densities (Gao et al., 2020). Galanti et al. (2020) consider the neural SCM with representation where and are assumed to be neural networks.

Very recently, location-scale models of the form have received some attention. Immer et al. (2022) revealed that bivariate non-identifiable location-scale models must satisfy a certain differential equation. Strobl and Lasko (2022) considered the multivariate extension and estimating patient-specific root causes. Khemakhem et al. (2021) revealed more detailed identifiability results under Gaussian noise in the bivariate case using autoregressive flows. Xu et al. (2022) considered a more restricted location-scale model that divides the range of the predictor variable into a finite set of bins and then fitting an additive model in each bin.

Further, several different algorithms for estimating causal graphs have been proposed, working with different assumptions (Janzing and Schölkopf, 2010; Nowzohour and Bühlmann, 2016; Marx and Vreeken, 2019; Tagasovska et al., 2020). They are often based on Kolmogorov complexity or independence between certain functions in a deterministic scenario. We provide more details about a few of these relevant methods in Section 5.

A few authors assume that causal Markov kernels lie in a parametric family of distributions. Janzing et al. (2009) consider the case in which the density of lies in a second-order exponential family and the variables are a mixture of discrete and continuous random variables. Park and Park (2019) concentrate on a specific subclass of model (2), where lies in a discrete family of generalized hypergeometric distributions—that is, the family of random variables in which the mean and variance have a polynomial relationship. To the best of our knowledge, there does not exist any study in the literature, that provides identifiability results in the case in which lies in a general class of the continuous exponential family. This is the focus of this paper.

2 Definitions of causal models

Recall that the general SCM corresponds to equations , , where are jointly independent noise variables. In this section, we discuss appropriate assumptions on the conditional distribution , where the causes potentially affect the variance or the tail of the effect. First, we introduce the model in the bivariate case.

2.1 Bivariate case of conditionally parametric causal model

In the following account, we consider that belongs to a known parametric family of distributions, and the cause affects only the parameters of the distribution, not the form itself.

In (unrestricted) SCM with the causal graph and the structural equation , we can, without loss of generality, assume that is uniformly distributed. This notion follows the idea of generating random variables in computer software. As long as we do not restrict , we can write , where is uniformly distributed and is the new structural equation. Inferring the distribution of and the function is an equivalent task. Therefore, we assume .

The following definition describes that if then has the conditional distribution with parameters for some .

Definition 3.

We define the bivariate conditionally parametric causal model (bivariate ) with graph by two assignments

| (♥) |

where are noise variables, is uniformly distributed, and is the quantile function with parameters .

We assume that represents measurable non-constant functions on the support of . If is continuous, we additionally assume that is continuous on the support of .

We put no restrictions on the marginal distribution of the cause. Note that we implicitly assume causal minimality, since we assume that are non-constant.

Example 1 (Continued).

The previous example can be understood as a model where the cause affects the mean and variance.

Example 2 (Continued).

Suppose admits the model ( ♥ ‣ 3) with graph , with being the Pareto quantile function 222The density has the form .. This model corresponds to If is small, then the tail of is large and extremes occur more frequently. Note that if for , then the -th moment of does not exist.

We provide another scenario in which (♥ ‣ 3) can be appealing. Consider a situation, in which we are interested in studying waiting times, such as the time until a patient’s death. Then, assuming is the exponential distribution can be reasonable, as using an exponential model is a common practice in statistics and survival analysis. Some might argue that assuming a specific distribution for the effect might be unrealistic, unless there are reasons to believe in such a situation. However, it can be more realistic (or, more importantly, more interpretable) than the additivity of noise (ANM) or similar structural restrictions, which are rather useful for causal discovery.

2.2 Asymmetrical -causal models and

We define a class of models, where we place different assumptions on and and generalize the model from (♥ ‣ 3).

2.2.1 Motivation

In model-based approaches for causal discovery (approaches such as ANM or post-nonlinear models), we assume some form of . Assume that , where is a subset of all conditional distributions. For example, in CPCM, is a known parametric family of conditional distributions. In ANM, consists of all conditional distributions that arise as the sum of a function of the cause and a noise. If is sufficiently small, we can hope for the identifiability of .

In what follows, we discuss a different set of assumptions that is more general and can be asymmetrical for and for . Instead of restricting , we restrict either , or , where are (not necessarily equal) subsets of all conditional distributions (selecting different causal models). We substantiate this by the following example.

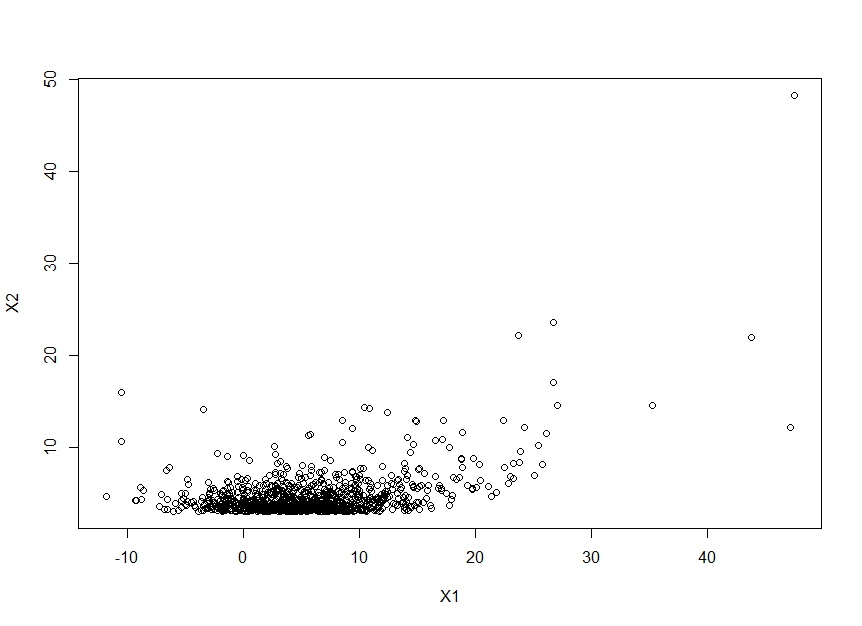

Suppose we observe data such as that in Figure 1. Here, is non-negative, and has full support. Selecting an appropriate restriction of can be tricky, since needs to be non-negative if . On the other hand, needs to have full support in the case in which .

Instead of restricting , we divide our assumptions into two cases. If , then we assume ; if , then we assume , where consists of non-negative distributions and consists of distributions with full support.

Note that this is a generalization of classical model-based approaches since they make the implicit choice . In the following account, we create a framework that enables asymmetrical assumptions.

2.2.2 Definition

Consider a class of bivariate SCMs, which are denoted by . For example, can denote all SCM that follow ANM or can denote all SCM that follow (♥ ‣ 3).

Definition 4.

Let and be two classes of bivariate SCMs with non-empty causal graphs. We say that the pair of random variables follows the asymmetrical causal model, if one of the following conditions holds:

-

•

the pair follows the SCM from with the causal graph , or

-

•

the pair follows the SCM from with the causal graph .

This definition allows different assumptions on each case of the causal structure. For example, if one variable is discrete and the second is continuous, we can assume ANM in one direction and the discrete QVF DAG model (Park and Raskutti, 2015) in the other. In the remainder of the paper, we focus on the continuous CPCM case.

Let and be two continuous distribution functions with parameters, respectively. Let and be two classes of SCMs that arise from the CPCM model (♥ ‣ 3) with and , respectively. We rephrase Definition 4 for this case. A pair of dependent random variables follows the asymmetrical causal model (we call it ), if either

| () |

where are measurable non-constant continuous functions as in (♥ ‣ 3). Note that the model is a special case of the asymmetrical -causal model, where .

3 Identifiability results

In this section, we are interested in ascertaining whether it is possible to infer a causal graph from a joint distribution under the assumptions presented in the previous section. First, we rephrase the notion of identifiability from Definition 2.

Definition 5 (Identifiability).

Let be a distribution that has been generated according to the asymmetrical ( causal model. We say that the causal graph is identifiable from the joint distribution (equivalently, that the model is identifiable) if exactly one of the bullet points from Definition 4 can generate distribution .

Specifically, let be a distribution that has been generated according to the model ( ♥ ‣ 3) with graph . We say that the causal graph is identifiable from the joint distribution if there does not exist and a pair of random variables , where is uniformly distributed, such that the model generates the same distribution .

In the remainder of the section, we answer the following question: Under what conditions is the causal graph identifiable? We begin with the case.

3.1 Identifiability in

We consider only continuous random variables, but similar results can also be derived for discrete random variables.

First, we deal with the important Gaussian case. Recall that in the additive Gaussian model, where , , the identifiability holds if and only if is non-linear (Hoyer et al., 2009). We provide a different result with both mean and variance as functions of the cause. A similar result is found in (Khemakhem et al., 2021, Theorem 1) in the context of autoregressive flows and where a sufficient condition for identifiability is provided. Another similar problem is studied in Immer et al. (2022) and Strobl and Lasko (2022), both of which show identifiability in location-scale models.

Theorem 1 (Gaussian case).

Let admit the model ( ♥ ‣ 3) with graph and the Gaussian distribution function with parameters . 333Just like in Example 1, this can be rewritten as .

Let be the density of that is absolutely continuous with full support . Let be two times differentiable. Then, the causal graph is identifiable from the joint distribution if and only if there do not exist , , such that

| (4) |

for all and

| (5) |

where represents an equality up to a constant (here, is a valid density function if and only if ). Specifically, if is constant (case ), then the causal graph is identifiable, unless is linear and is the Gaussian density.

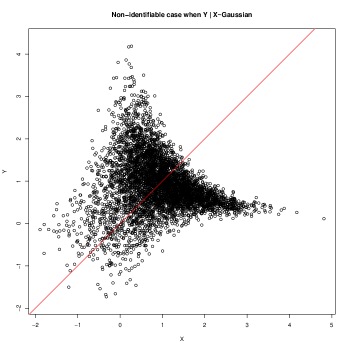

The proof is provided in Appendix A.1. Moreover, a distribution of an unidentifiable Gaussian case with can be found in Appendix A.1, Figure 4.

Theorem 1 indicates that the non-identifiability holds only in the “special case,” when are linear and quadratic, respectively. Note that natural parameters of a Gaussian distribution are , and sufficient statistics of the Gaussian distribution have a linear and quadratic form (for the definition of the exponential family, natural parameter and sufficient statistic, see Appendix B.1). We show that such connections between non-identifiability and sufficient statistics hold in the more general context of the exponential family.

Proposition 1 (General case, one parameter).

Let . Let admit the model ( ♥ ‣ 3) with graph , where lies in the exponential family of distributions with a sufficient statistic , where is continuous. If there do not exist , such that

| (6) |

then the causal graph is identifiable.

Note that the causal graph in (♥ ‣ 3) is trivially identifiable if and have different supports.

Proof.

We first show that if the causal graph is not identifiable, then (6) holds for some .

If the graph is not identifiable, there exists a function , such that causal models , and generate the same joint distribution. Decomposing the joint density yields

| (8) |

Since lies in the exponential family of distributions, we use the notation from Appendix B.1 and rewrite this as

and analogously for . Then, the second equality in (8) becomes

| (9) |

where the second equation is the logarithmic transformation of the first equation after dividing both sides by and . Since the left side is in the additive form, Lemma 1 directly yields (6) (to see this without Lemma 1, apply to (9) and fix such that . We get . Integrating this equality with respect to yields (6). However, using Lemma 1, we do not need to assume the differentiability of ).

Proposition 1 indicates that the only case in which the model is not identifiable is when has a uniquely given functional form (unique up to a linear transformation) and the density of the cause is uniquely given (unique up to one additional parameter ). Note that it is only a sufficient, not a necessary, condition for identifiability since some specific choices of and can still lead to identifiable cases. We show the usage of Proposition 1 for a Pareto model.

Consequence 1.

3.2 Identifiability in models

Similar sufficient conditions as in Proposition 1 can be derived for a more general case, when has several parameters and for the . The following theorem reveals that the model is “typically” identifiable.

Theorem 2.

Let follow the defined as in ( ‣ 2.2.2), where lie in the exponential family of continuous distributions and , are the corresponding sufficient statistics with a nontrivial intersection of their support .

The causal graph is identifiable if is not a linear combination of on —that is, if cannot be written as

| (11) |

for all and for some constants , .

The proof is provided in Appendix A.3. Note that condition (11) is sufficient, but not necessary for identifiability. Similar to that in the Gaussian (Theorem 1) or Pareto cases (Consequence 1), in order to obtain a necessary condition, the distribution of the cause also needs to be restricted.

The following example illustrates the usage of Theorem 2 on Gamma and Beta distributions.

Consequence 2.

-

•

Let admit the model ( ♥ ‣ 3) with graph , where is a Gamma distribution with parameters . If there do not exist constants , such that

then the causal graph is identifiable.

-

•

Let admit the , as in ( ‣ 2.2.2), where is the Gamma distribution function with parameters and is the Beta distribution function with parameters . If there do not exist constants , , such that for all the following holds:

then the causal graph is identifiable.

4 Multivariate case

We move the theory to the case with more than two variables . We assume causal sufficiency (all relevant variables have been observed) and causal minimality. However, we do not assume faithfulness. It is straightforward to generalize the asymmetric causal model to the multivariate case, in which we assume that each variable arises under the model.

To be more rigorous, we define a multivariate CPCM as a generalization of ( ‣ 2.2.2).

Definition 6.

Let be distribution functions with parameters, respectively. We define an asymmetrical causal model ( for short) as a collection of equations:

we assume that the corresponding causal graph is acyclic. is a collection of jointly independent uniformly distributed random variables. are continuous non-constant functions in any of their arguments.

If for some quantile function and for all , we call such a model .

Simply said, we assume that is distributed according to distribution with parameters . We assume all are known, apart from the source variables. Note that defined in Section 2.2.2 is a special case of Definition 6, since we allow the source variable to be arbitrarily distributed.

The question of the identifiability of in the multivariate case is in order. Here, it is not satisfactory to consider the identifiability of each pair of separately. Each pair needs to have an identifiable causal relation conditioned on other variables . Such an observation was first made by Peters et al. (2014) in the context of additive noise models. We now provide a more precise statement in the context of .

Definition 7.

We say that the is pairwise identifiable, if for all , , such that and , there exists , which satisfies that a bivariate model defined as is identifiable (in the sense of Definition 5), where and , .

Lemma 1.

Let be generated by the pairwise identifiable with DAG . Then, is identifiable from the joint distribution.

The proof is provided in Appendix A.5. It is an application of Theorem 28 in Peters et al. (2014). An important special case arises when we assume (conditional) normality.

Consequence 3 (Multivariate Gaussian case).

Suppose that follow with a Gaussian distribution function . This corresponds to for all and for some functions . In other words, we assume that the data-generation process has the following form:

Potentially, source nodes can have arbitrary distributions. Combining Theorem 1 and Lemma 1, the causal graph is identifiable if the functions , , are not in the form (4) in any of their arguments.

5 Methods for inference

5.1 Related work

There are numerous algorithms that can be utilized to estimate the causal graph from observational data, each requiring different assumptions, guarantees, and outputs (see Glymour et al. (2019), or Chapter 4 in Peters et al. (2017) for a review). In the following three paragraphs, we describe three main approaches in the recent literature.

Identifiable model-based methods such as LiNGaM (Shimizu et al., 2006), RESIT (Peters et al., 2014), PNL (Zhang and Hyvärinen, 2010), GHD DAG (Park and Park, 2019; Park and Raskutti, 2017), HECI (Xu et al., 2022), and LOCI (Immer et al., 2022) exploit the fact that we cannot fit a certain model in both causal directions. This is also the approach adopted in this paper. For practical evaluation, we need to measure how well the model fits the data. One possibility is to test the independence between the cause and the estimated noise. The second possibility is to use a maximum likelihood approach. In both cases, the choice of the model is rather important.

Score-based methods (Chickering, 2002; Nowzohour and Bühlmann, 2016) are popular for distinguishing between the DAGs in the Markov equivalence class. Denote the space of DAGs on nodes by and let be a score function. Function assigns each DAG a score that evaluates the overall fit. The goal is then to find , which is typically an NP-hard problem (Chickering et al., 2004). However, under an appropriately selected and additional assumptions, algorithms with polynomial time complexity were proposed (Rajendran et al., 2021). Nevertheless, the choice of is crucial since the graph that minimizes can differ from the true data-generating mechanism.

Other methods based on algorithmic mutual information (Janzing and Schölkopf, 2010; Tagasovska et al., 2020) or information-geometric approaches (Janzing and Schölkopf, 2010) are popular, particularly in computer science. They are based on a different paradigm of independence (based on Kolmogorov complexity or independence between certain functions in a deterministic scenario). Often, they are implemented only in the bivariate case. In the simulations in Section 6.2, we compare our method with several previously mentioned methods.

5.2 Algorithm for CPCM using independence testing

Our CPCM methodology is based on selecting an appropriate model (in our case, reduced to a choice of ) and a measure of a model fit. In the following subsections, we measure the model fit by exploiting the principle of independence between the cause and the mechanism. Algorithms such as RESIT (Peters et al., 2014), CAM (Bühlmann et al., 2014), PNL (Zhang and Hyvärinen, 2009), and LOCI (Immer et al., 2022) are special cases or only small modifications of our framework.

Recall that the general SCM corresponds to equations , , where are jointly independent noise variables. We define the invertible functional causal model (IFCM) as an acyclic SCM, such that there exist functions for which , . IFCM is strictly broader than all previously mentioned models (e.g., the post-nonlinear model where satisfy , for invertible).

5.2.1 Main steps of the algorithm

A causal graph is said to be plausible under the causal model if the joint distribution can be generated under model with such a graph. The algorithm in Table 1 describes the main steps to test the plausibility. If one direction is plausible and the other is not, we consider the former as a final estimate. Problems arise if both directions have the same plausibility. If both directions are plausible, it suggests an unidentifiable setup (or we have insufficient data). If both directions are unplausible, it suggests that certain assumptions are not fulfilled or that our estimate (resp ) is not appropriate.

| General IFCM | |

|---|---|

| Test for independence between and . | Test for independence between and . |

| If not rejected, return an empty graph. | If not rejected, return an empty graph. |

| In direction : | In direction : |

| 1) Estimate function | 1) Estimate . |

| 2) Compute . | 2) Use probability transform |

| 3) Test an independence between and . | 3) Test an independence between and . |

| Direction is plausible if the test from step 3 | Direction is plausible if the test from step 3 |

| is not rejected. | is not rejected. |

| Repeat for the other direction . | Repeat for the other direction using . |

The estimation of without additional assumptions is rather difficult and has to be based on a more restricted model. Under CPCM, this reduces to an estimation of in the first step. This can be done using any machine learning algorithm, such as GAM, GAMLSS, random forest, or neural networks. For the third step (test of independence), we can use a kernel-based HSIC test (Pfister et al., 2018) or a copula-based test (Genest et al., 2019).

If follow with an identifiable causal graph, it is easy to show that our proposed estimation of the causal graph is consistent—that is, the true causal graph is recovered with probability tending to one as the number of data tends to infinity. Mooij et al. (2016) show that, if follows an additive noise model, then the estimation of the causal graph (using a suitable regression method and HSIC) is consistent. Sun and Schulte (2023) consider an analogous result in the context of location-scale models. It is straightforward to show the analogous results for CPCM, with the assumption that the estimator is suitable. Let be a random sample from . For a given function , define and for an estimator let . Then, we say that the estimator is suitable, if

where the expectation is taken with respect to the distribution of the random sample. This property was shown for a few special cases in certain classical estimators such as GAM (Green and Silverman, 1994) or GAMLSS (Stasinopoulos and Rigby, 2007).

Generalizing this approach for the multivariate case with variables is straightforward. For each , we estimate for all and compute the probability transform . Then, we can test independence between and conclude that is plausible if this test is not rejected. However, in the multivariate case, several graphs can be plausible, which can be inconvenient in practice. The score-based algorithm can overcome this nuisance, as we describe below.

5.3 Score-based algorithm for CPCM

The algorithm for CPCM using the independence test presented in the previous subsection does not always provide an output. The possibility of rejecting the independence test in all directions can be considered a safety net, therebyshielding us against unfulfilled assumptions or unidentifiable cases. Nevertheless, we may still want to obtain an estimation of the graph.

Following the ideas of Nowzohour and Bühlmann (2016) and Peters et al. (2014), we use the following penalized independence score:

where represents some measure of independence, and are noise estimations obtained by estimating and putting such as in step 1 and step 2 in the algorithm in Section 5.2.

With regard to choice of , we use minus the logarithm of the p-value of the copula-based independence test (Genest et al., 2019) and . These choices appear to work well in practice, but we do not provide any theoretical justification of their optimality. In the bivariate case, we test the independence between and and if rejected, we select the graph with the lowest score . In doing so, we do not have to select an appropriate .

Another natural choice for the score function is based on log-likelihood or Akaike information criterion (AIC), as in Nowzohour and Bühlmann (2016). Comparison of these choices of in simple models have been studied (Sun and Schulte, 2023), and it appears that selecting an independence-based score function is more robust against model misspecification and typically a better choice. We do not comment on this further in this paper.

The main disadvantage of the proposed method is that we have to go through all graphs , which is possible only for , since the number of DAGs grows superexponentially with dimension (Chickering et al., 2004). Several modifications can be used in order to speed up the process. In this regard, greedy algorithms have been proposed (Chickering, 2002; Rajendran et al., 2021); however, this is beyond the scope of this paper. Our algorithm is relatively standard and is only a slight modification of classical algorithms. Hence, in Section 6, we provide only a short simulation study to highlight the results of Section 3.

5.4 Model selection, overfitting, and problems in practice

Model selection (choice of or and if we opt for our CPCM framework) is a crucial step in our approach. The choice of a model is a common problem in classical statistics; however, it is more subtle in causal discovery. Here, should be viewed as a metric for the “complexity” of SCM. We mention some of the problems that arise in practice. We also discuss them in detail in our application.

-

•

Choosing with too many parameters ( is large): Even if the theory suggests that it is not possible to fit a in both causal directions, this is only an asymptotic result that is no longer valid for a finite number of data. If we select with numerous parameters to estimate, our data will be fitted perfectly and we will not reject the wrong causal graph. However, by selecting an overly simple , our assumptions may not be fulfilled and we may end up rejecting the correct causal graph.

-

•

Several choices of and multiple testing: The choice of should ideally be based on prior knowledge of the data-generation process. Examining the marginal distributions of and can be useful, although it is questionable how much marginal distributions can help select an appropriate model for the conditional distribution. Comparing many different s can lead to multiple testing problems, and we should be careful with data-driven estimation of , as the following lemma suggests:

Lemma 1.

Let be a distribution function with one parameter () belonging to the exponential family with the corresponding sufficient statistic . Suppose that the joint distribution is generated according to model ( ♥ ‣ 3) with graph .

Then, there exists such that the model ( ♥ ‣ 3) with graph also generates . In other words, there exists such that the causal graph in is not identifiable from the joint distribution.

The proof (provided in Appendix A.6) is based on the specific choice of , such that its sufficient statistic is equal to (where is the parameter from the original model ). Lemma 1 indicates that a data-driven estimation of can be problematic. However, such would lead to a rather non-standard distribution.

-

•

Different complexity between models: We recommend selecting the same in both directions (if reasonable) or at least attempting to choose with the same number of parameters . If we select, say, with one parameter and with five parameters (), it will create a bias toward one direction because the model with more parameters will fit the data more easily. We refer to this as an “unfair game.”

In our implementation, we use GAM (Wood et al., 2016) estimation of . With regard to the independence test, we use Hoeffding D-test (Herwartz and Maxand, 2020) in the bivariate case, copula-based independence test (Kojadinovic and Holmes, 2009) in the multivariate case with , and HSIC (Zhang et al., 2011) when (for a review of different tests and their comparisons, see Genest et al. (2019)).

6 Simulations

The R code with the implementations of the algorithms presented in the previous section and the code for the simulations and the application can be found in the supplementary package or https://github.com/jurobodik/Causal_CPCM.git.

In this section, we illustrate our methodology under controlled conditions. We first consider the bivariate case in which causes . We select different distribution functions in the CPCM model, different forms of , and different distributions of . We recreate a few of the theoretical results presented in Section 2.

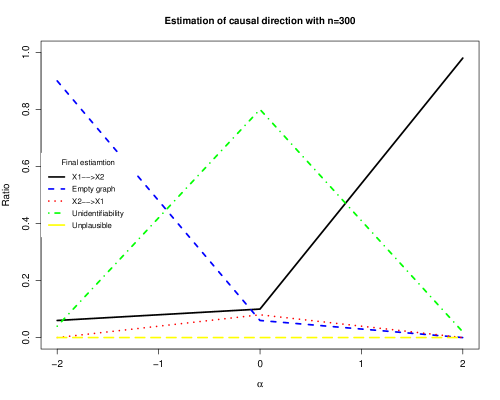

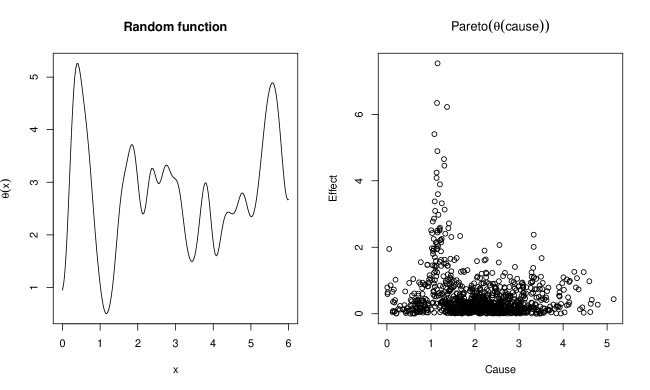

6.1 Pareto case following Example 2 and Consequence 1

Consider the Pareto distribution function ; functions are defined similarly as in (10). Specifically, we choose and for some hyper-parameter . This represents the distortion from the unidentifiable case. If , we are in the unidentifiable case described in Consequence 1. If , Consequence 1 suggests that we should be able to distinguish between the cause and the effect. If , then is almost constant (function is close to zero function on ) and are (close to) independent.

For the size of the dataset and , we simulate data as described above. Using our algorithm from Section 5.2, we obtain an estimate of the causal graph. After averaging results from 100 repetitions, we obtain the results described in Figure 2. The resulting numbers are as expected: if , then both directions tend to be plausible. If , we tend to estimate the correct direction ; if , then we tend to estimate an empty graph since are (close to) independent.

6.2 The Gaussian case and comparison with baseline methods

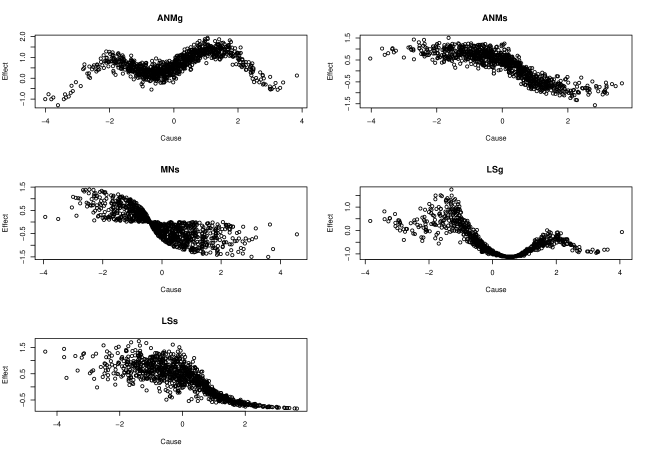

For simulated data, we use the benchmark dataset introduced in Tagasovska et al. (2020). The dataset consists of additive and location-scale Gaussian pairs of the form , where , . In one setup (LSg), we consider and as nonlinear functions simulated using Gaussian processes with Gaussian kernel with bandwidth one (Rasmussen and Williams, 2005). In the second setup (LSs), we consider and as sigmoids (Bühlmann et al., 2014). Further, nonlinear additive noise models (ANM) are generated as LS with constant and nonlinear multiplicative noise models (MN) are generated as LS with fixed (only with sigmoid functions for ). For each of the five cases (LSg, LSs, ANMg, ANMs, and MNs), we simulate 100 pairs with datapoints.

We compare our method with LOCI (Immer et al., 2022), HECI (Xu et al., 2022), RESIT (Peters et al., 2014), bQCD (Tagasovska et al., 2020), IGCI with Gaussian and uniform reference measures (Janzing and Schölkopf, 2010) and Slope (Marx and Vreeken, 2019). Details can be found in Appendix C. As in Mooij et al. (2016), we use the accuracy for forced decisions as our evaluation metric. The results are presented in Table 2. We conclude that our estimator performs well on all datasets, and provides comparable results with those using LOCI and IGCI (although utilizing the uniform reference measure would lead to much worse results for IGCI).

Note that in the ANM and MN cases, we non-parametrically estimate two parameters while only one is relevant. Therefore, it can happen that we “overfit” (see Section 5.4), and both directions are not rejected. To improve our results, fixing either or could be beneficial (although it may prove challenging to determine this conclusively in practical applications).

| ANMg | ANMs | MNs | LSg | LSs | |

|---|---|---|---|---|---|

| Our CPCM | 100 | 97 | 95 | 99 | 98 |

| LOCI | 100 | 100 | 99 | 91 | 85 |

| HECI | 99 | 43 | 29 | 96 | 54 |

| RESIT | 100 | 100 | 39 | 51 | 11 |

| bQCD | 100 | 79 | 99 | 100 | 98 |

| IGCI (Gauss) | 100 | 99 | 99 | 97 | 100 |

| IGCI (Unif) | 31 | 35 | 12 | 36 | 28 |

| Slope | 22 | 25 | 9 | 12 | 15 |

6.3 Robustness against a misspecification of F

Consider , where , 444 denotes the truncated Gaussian distribution on . Therefore, , with a mean of approximately . and let

| (12) |

where is a non-negative function. In other words, we generate according to (♥ ‣ 3), with being an exponential distribution function. Recall that the exponential distribution is a special case of Gamma distribution with a fixed shape parameter.

The goal of this simulation is to ascertain how the choice of affects the resulting estimate of the causal graph. We consider five different choices for : Gamma with fixed scale, Gamma (with two parameters as in Consequence 2), Pareto, Gaussian with fixed variance, and Gaussian (with two parameters as in Example 1).

We generate variables, according to (12), with different functions, . Then, we apply the CPCM algorithm with different choices of . Table 3 presents the percentage of correctly estimated causal graphs (an average out of 100 repetitions). The results remain more or less good for that are “similar” to the exponential distribution, with respect to the density and support. However, if we select the Gaussian distribution (a uni-modal distribution with different support), our methodology often provides wrong estimates.

| F | Random | |||

|---|---|---|---|---|

| Gamma (fixed scale) | ||||

| Gamma (two parameters) | ||||

| Pareto | ||||

| Gaussian (fixed variance) | ||||

| Gaussian (two parameters) |

7 Application

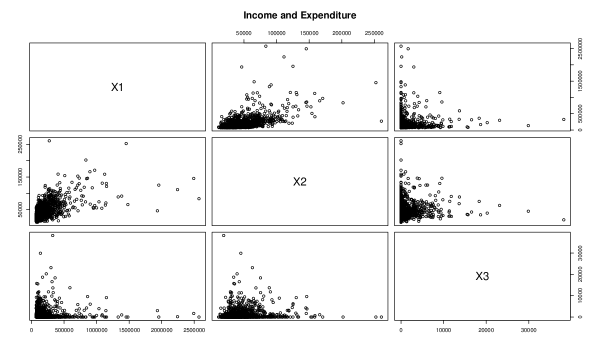

We explain our methodology in detail based on real-world data that describes the expenditure habits of Philippines residents. The Philippine Statistics Authority conducts a nationwide survey of Family Income and Expenditure (Philippine Statistics Authority, 2023) every three years. The dataset (taken from Flores (2018)) contains over 40,000 observations primarily comprising the household income and expenditures of each household. To reduce the size and add homogeneity to the data, we consider only families of size (people living alone) above the poverty line (top 90%, with an income of at least per year). We end up with observations.

We focus on the following variables: Total income (), Food expenditure (), and Alcohol expenditure (). Our objective is to identify the causal relationships among these variables. Intuition gives us that . However, the relationships between alcohol and other variables is not trivial. Drinking habits can impact income and food habits, although income can change the quality of the purchased alcohol. Histograms and pairwise plots of the variables are presented in Appendix C.

7.1 Pairwise discovery

First, we focus on the causal relationship between and (between and ). We apply our methodology following the algorithm presented in Section 5.2. With regard to the choice of and , we select the Gamma distribution for both (model described in Consequence 2). We explain our choice: both marginals of and are Gamma-shaped (see the histograms in Figure 8) and the Gamma is a common choice for this type of data. One may argue that the Pareto distribution is more suitable since the tails of and are heavy-tailed and and are dependent in extremes. One may compare AIC scores in regression with the Gamma and Pareto distributions. The AIC is equal to () for the Gamma (Pareto) distribution in the direction and () for the Gamma (Pareto) distribution in the direction . In this case, the Gamma distribution appears to be a better fit in both directions. However, selecting based on AIC is not appropriate; we must be careful when comparing several choices of (see the discussion in Section 5.4).

Further, applying the CPCM algorithm yields the following estimation: . The p-values of the independence tests were and corresponding to the directions and , respectively. Selecting the Pareto distribution function or even the Gaussian distribution function yields similar results.

Second, we focus on a causal relationship between and (between and ). As for the choice of , the Pareto distribution appears more reasonable since it appears heavy-tailed with a large mass between 0 and 1000 pesos. However, selecting and can potentially lead to an “unfair game” bias (see Section 5.4).

Applying the CPCM algorithm suggests that both directions are unplausible. The p-values of the independence tests were and corresponded to the directions and , respectively. We note that for any pair of Gamma, Gaussian, or Pareto distribution functions, the p-values are always below . This suggests that some assumptions remain unfulfilled. In this case, we believe that causal sufficiency is violated; there is a strong unobserved common cause between these variables. Note that even if both causal graphs were unplausible, direction appeared to be the most probable direction ( for the choice of Gamma distribution).

Finally, we focus on the causal relationship between and (between and ). Using the same principle as that for previous pairs, we obtain an estimation . The p-values of the independence tests were and , which corresponded to the directions and , respectively. We note that selecting the Pareto distribution function or the Gaussian distribution function yields similar results. This result suggests that drinking habits affect food habits.

7.2 Multivariate score-based discovery and results

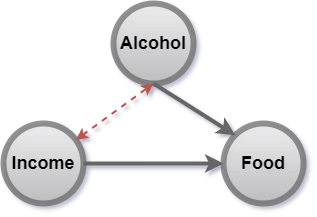

We apply the score-based algorithm presented in Section 5.3 using the Gamma distribution function . The graph with the best score is the one presented in Figure 3. However, this graph is not plausible, as the test of independence between yields a p-value of . The graphs where and are neighbours had slightly worse scores and a p-value of .

Possible feedback loops and common causes are the main reasons why we do not obtain clear independence between the estimated noise variables. Deviations from the assumed model conditions are often observed in real-world scenarios. Despite this, acceptable estimates of the causal relationships can still be derived if the deviations are not excessive.

8 Conclusion and future research

In this study, we introduced a new family of models for causal inference—the CPCM. The main part of the theory consisted of exploring the identifiability of the causal structure under this model. We showed that bivariate CPCM models with distribution function are typically identifiable, except when the parameters of are in the form of a linear combination of its sufficient statistics. Moreover, we showed more detailed characterization of the identifiability in the one-parameter as well as the Gaussian and Pareto cases. We briefly explained the multivariate extensions of these results.

We proposed an algorithm that estimates the causal graph based on the CPCM model and discussed several possible extensions of the algorithm. A short simulation study suggests that the methodology is comparable with other commonly used methods in the Gaussian case. However, our methodology is rather flexible, varying with the choice of . For specific choices of , our methodology can be adapted for detection of causality-in-variance or causality-in-tail and can be used to generalize additive models in various frameworks. We applied our methodology on real-world data and discussed a few possible problems and results.

Our methodology is not meant to be a black-box model for causal discovery. Discussing the choice of models and adapting them for different applications can bring a new perspective on the causal discovery, and future research is required to show how useful our framework is in practice. However, identifying an automatic, data-driven choice of can lead to new and interesting results.

Our framework can also be useful for different causal inference tasks. For example, the invariant-prediction framework (Peters et al., 2016) can be adapted for detecting invariance in a non-additive matter, such as invariance in tails or invariance in variance. This can lead to new directions of research.

Conflict of interest and data availability

R code and the data are available in an online repository or on request from the author.

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Acknowledgements

This study was supported by the Swiss National Science Foundation.

Appendix A Appendix: Proofs

A.1

Theorem 1.

Let admit the model ( ♥ ‣ 3) with graph and the Gaussian distribution function with parameters . Let be the density of that is absolutely continuous with full support . Let be two times differentiable.

Then, the causal graph is identifiable from the joint distribution if and only if there do not exist , , such that

| (4) |

for all and

| (5) |

where represents an equality up to a constant (here, is a valid density function if and only if ). Specifically, if is constant (case ), then the causal graph is identifiable unless is linear and is the Gaussian density.

Proof.

We opt for proving this theorem from scratch, without using Theorem 2. The reader attempt to use Theorem 2. For clarity regarding the indexes, we use the notation .

First, we show that if the causal graph is not identifiable, then and must satisfy (4). Let be the density function of . Since the causal graph is not identifiable, there exist two CPCM models that generate : the CPCM model with and the function and the CPCM model with and the function .

We decompose (corresponding to the direction )

where is the Gaussian density function with parameters . We rewrite this in the other direction:

We take the logarithm of both equations and rewrite them in the following manner:

| (13) |

Calculating on both sides , we obtain

Since this has to hold for all , both sides need to be constant (let us denote this constant by ).

Differential equation has solution for , such that .

Plugging this result into (13) and calculating on both sides , we obtain

| (14) |

Equation (14) is another differential equation with a solution , for some for all .

Next, we show that it is necessary that . If we show , then and are exactly in the form (4). We plug the representations and into (13). Thus, we obtain

We can re-write the last expression as

| (15) |

where

Since the left-hand side of (15) is in additive form, the right side also needs to have an additive representation. However, that is only possible if and . Therefore, we necessarily have and either or . The case corresponds to a constant and, hence, also . We have shown that and have to satisfy (4).

Next, we show that if the causal graph is not identifiable, then the density of has form (5). Plugging the form of and into (13), we obtain

We rewrite

| (16) |

Since this has to hold for all , both sides of (16) need to be constant and we obtain . Hence,

where and . The condition comes from the fact that if and then is not a density function (it is not integrable since for all ).

Finally, we deal with the other direction: we show that if and satisfy (4) and has form (5), then the causal graph is not identifiable. Assume that are given. Define and select , such that . Define . Moreover, define

Note that regardless of the coefficients, these are valid density functions (with one exception when and , which is why we selected ). In case of , this is the classical Gaussian distribution density function.

Using these values, we obtain the equality

or more precisely,

Since this holds for all , we found a valid backward model. The density in (5) uses the notation and . ∎

An example of the joint distribution of with is depicted in Figure 4.

A.2

Consequence 1.

Proof.

For a clarity in the indexes, we use the notation and we assume .

First, we show that if (10) holds, then there exists a backward model that generates the same joint distribution. The joint density can be written as

For the backwards model, define and , where . Then, we can write

Therefore, for all holds , where both correspond to the valid model (♥ ‣ 3), which is what we wanted to prove.

Second, we show the other implication. Assume that the causal graph is not identifiable. Therefore, the joint distribution can be decomposed as

| (17) |

where for all , we have and , where are some non-negative functions and are some density functions defined on .

A sufficient statistic for Pareto distribution is . Proposition 1 implies that the only form of can be a linear function of the logarithm. Thus., we write , for some .

Take the logarithm of (17) and, using the previous notation, we obtain

By simple algebra, we obtain

| (18) |

We show that equality (18) implies and the left side of (18) is constant. Denote the left side of (18) as , and denote . Equality (18) reads as

| (19) |

The only possibility that the right side of (19) is additive is when , in which case Therefore,

In other words, , which is what we wanted to prove. ∎

A.3

Before we prove Theorem 2, we show the following auxiliary lemma.

Lemma 1.

Let and let contain an open interval. Let be non-constant continuous real functions on , such that is additive in —that is, there exist functions and , such that

Then, there exist (not all zero) constants , such that for all . Specifically for , it holds that for some .

Moreover, assume that for some , functions are affinly independent—that is, there exist , such that a matrix

| (20) |

has full rank. Then, for all there exist constants , such that for all .

Proof.

Fix , such that . Then, we have for all

and subtraction of these equalities yields

Defining and yields the first result (with ).

Now, we prove the “Moreover” part. Consider equalities

where are defined, such that matrix (20) has full rank. Subtracting from each equality, the first equality yields

Using matrix formulation, this can be rewritten as

| (21) |

Multiplying both sides by indicates that are nothing else than a linear combination of , which is what we wanted to show. ∎

Theorem 2.

Let follow the defined as in ( ‣ 2.2.2), where and lie in the exponential family of continuous distributions and , are the corresponding sufficient statistics with a nontrivial intersection of their support .

The causal graph is identifiable if is not a linear combination of on —that is, if cannot be written as

| (11) |

for all and for some constants , .

Proof.

If the is not identifiable, then there exist functions and , such that models , and generate the same joint density function. Decompose the joint density as

| (22) |

Since and lie in the exponential family of distributions, we use the notation from Appendix B.1 and rewrite it as

After a logarithmic transformation of both sides of (22), we obtain

| (23) |

Define and . Then, equality (23) reads as

Finally, we use Lemma 1. We know that functions are affinly independent in the sense presented in Lemma 1 (see (26) in Appendix B.1). Therefore, Lemma 1 gives us that are only a linear combination of , which is what we wanted to show. ∎

A.4

Details corresponding to Consequence 2.

The density function of the Gamma distribution with parameters is in the form . The sufficient statistics are .

The density function of the Beta distribution with parameters is in the form . The sufficient statistics are .

A.5

Lemma 1.

Let be generated by the with DAG and with density . Assume that for all , , such that and , there exist , such that a bivariate model defined as is identifiable (in the sense of Definition 5), where and , .

Then, is identifiable from the joint distribution.

Proof.

Let there be two models, with causal graphs , that both generate . From Proposition 29 in Peters et al. (2014) (recall that we assume causal minimality of ), there exist variables , such that

-

•

in and in ,

-

•

.

For this , select in accordance to the condition in the theorem. Below, we use the notation where . Now, we use Lemma 36 and Lemma 37 from (Peters et al., 2014). Since in , we define a bivariate SCM as 555Informally, we consider and .

where and . This is a bivariate CPCM with . However, the same holds for the other direction: Since in , we can also define a bivariate SCM in the following manner:

where and . We obtained a bivariate CPCM with , which is a contradiction with the pairwise identifiability. Hence, . ∎

A.6

Lemma 1.

Let be a distribution function with one parameter () belonging to the exponential family with the corresponding sufficient statistic . Suppose that the joint distribution is generated in accordance with model ( ♥ ‣ 3) with graph .

Then, there exists , such that the model ( ♥ ‣ 3) with graph also generates . In other words, there exists , such that the causal graph in is not identifiable from the joint distribution.

Proof.

The idea of the proof is the following: we select , such that its sufficient statistic is equal to . Let us denote the original model as

where (using notation from Appendix B.1) the conditional density function can be rewritten as

We define from an exponential family in the following manner: consider the sufficient statistic for all in support of and choose and for all in support of . Then, a model where

for a specific choice has the following conditional density function:

Therefore, the joint distribution is equal in both models, since

We found model with graph that generates the same distribution. ∎

Appendix B Theoretical details and detailed definitions

B.1 Exponential family

The exponential family is a set of probability distributions whose probability density function can be expressed in the following form:

| (24) |

where are real functions and is a vector-valued function. We call a sufficient statistic, a base measure, and a normalizing (or partition) function.

Often, form (24) is called a canonical form and

where , is called its reparametrization (natural parameters are a specific form of the reparametrization). We always work only with a canonical form (attention for Gaussian distribution, where the standard form is not in the canonical form).

Numerous important distributions lie in the exponential family of continuous distributions, such as Gaussian, Pareto (with fixed support), log-normal, Gamma, and Beta distributions, to name a few.

Functions in (24) are not uniquely defined. For example, is unique up to a linear transformation.

The support of (defined as ) is fixed and does not depend on . Potentially, do not have to be defined outside of this support; however, we typically overlook this fact (or possibly define for where these functions are not defined). If we assume that is continuous (which is typically the case in this paper), we additionally assume that the support is nontrivial in the sense that it includes an open interval.

Without loss of generality, we always assume that is minimal in the sense that we cannot write using only parameters. Then, are linearly independent in the following sense: there exists , such that matrix

| (25) |

has full rank. Moreover, are affinly independent in the following sense: there exists , such that a matrix

| (26) |

has full rank. In this paper (particularly in Lemma 1), we assume that are affinly independent (i.e., satisfy (26)).

Appendix C Simulations and application details

Plots corresponding to the datasets from Simulations 2 and 3 are presented in Figures 5 and 6. Plots corresponding to the application are drawn in Figures 7 and 8.

C.1 Baselines implementations from Simulations 2

As mentioned earlier, the experiments from Simulations 2 were inspired by Tagasovska et al. (2020) and implementations of other baseline methods are also taken from Tagasovska et al. (2020) and Immer et al. (2022).

For LOCI, we use the default format with neural network estimations and subsequent independence testing (also denoted as ) (Immer et al., 2022). For IGCI, we use the original implementation from Janzing and Schölkopf (2010) with slope-based estimation with Gaussian and uniform reference measures. For RESIT, we use the implementation from Peters et al. (2014) with GP regression and the HSIC independence test with a threshold value of . For the slope algorithm, we use the implementation of Marx and Vreeken (2019), with the local regression included in the fitting process.For comparisons with other methods such as PNL, GPI-MML, ANM, Sloppy, GR-AN, EMD, GRCI, see Section 3.2 in Tagasovska et al. (2020) and Section 5 in Immer et al. (2022).

References

- Bühlmann et al. (2014) P. Bühlmann, J. Peters, and J. Ernest. CAM: Causal additive models, high-dimensional order search and penalized regression. The Annals of Statistics, 42(6):2526–2556, 2014. doi: 10.1214/14-aos1260.

- Chickering (2002) D. M. Chickering. Optimal structure identification with greedy search. Journal of Machine Learning Research, 3:507–554, 2002. doi: 10.1162/153244303321897717.

- Chickering et al. (2004) D. M. Chickering, D. Heckerman, and Ch. Meek. Large-sample learning of bayesian networks is np-hard. Journal of Machine Learning Research, 5:1287–1330, 2004.

- Coles (2001) S. Coles. An Introduction to Statistical Modeling of Extreme Values. Springer Series in Statistics. Springer-Verlag, 2001. ISBN 1-85233-459-2.

- Flores (2018) F. P. Flores. Dataset: Family income and expenditure. https://www.kaggle.com/datasets/grosvenpaul/family-income-and-expenditure, 2018. Accessed: [1.2.2023].

- Galanti et al. (2020) T. Galanti, O. Nabati, and L. Wolf. A critical view of the structural causal model. Preprint, 2020.

- Gao et al. (2020) M. Gao, Y. Ding, and B. Aragam. A polynomial-time algorithm for learning nonparametric causal graphs. In Proceedings of the 34th International Conference on Neural Information Processing Systems, NIPS’20, Red Hook, NY, USA, 2020. Curran Associates Inc. ISBN 9781713829546.

- Genest et al. (2019) C. Genest, J.G. Nešlehová, B. Rémillard, and O.A. Murphy. Testing for independence in arbitrary distributions. Biometrika, 106(1):47–68, 2019. doi: 10.1093/biomet/asy059.

- Glymour et al. (2019) C. Glymour, K. Zhang, and P. Spirtes. Review of causal discovery methods based on graphical models. Frontiers in Genetics, 10, 2019. doi: 10.3389/fgene.2019.00524.

- Green and Silverman (1994) P. Green and B. Silverman. Nonparametric Regression and Generalized Linear Models: A Roughness Penalty Approach. Chapman and Hall/CRC, 1994. ISBN 9780412300400. URL https://www.routledge.com/Nonparametric-Regression-and-Generalized-Linear-Models-A-roughness-penalty/Green-Silverman/p/book/9780412300400.

- Greenland et al. (1999) S. Greenland, J. Pearl, and J.M. Robins. Causal diagrams for epidemiologic research. Epidemiology, 10:37–48, 1999. URL https://pubmed.ncbi.nlm.nih.gov/9888278/.

- Herwartz and Maxand (2020) H. Herwartz and S. Maxand. Nonparametric tests for independence: a review and comparative simulation study with an application to malnutrition data in india. Statistical Papers, 61:2175–2201, 2020. doi: 10.1007/s00362-018-1026-9.

- Hoyer et al. (2009) P. Hoyer, D. Janzing, J.M. Mooij, J. Peters, and B. Schölkopf. Nonlinear causal discovery with additive noise models. In Advances in Neural Information Processing Systems, volume 21. Curran Associates, Inc., 2009. URL https://proceedings.neurips.cc/paper/2008/file/f7664060cc52bc6f3d620bcedc94a4b6-Paper.pdf.

- Immer et al. (2022) A. Immer, Ch. Schultheiss, J. E. Vogt, B. Schölkopf, and P. Bühlmann. On the identifiability and estimation of causal location-scale noise models. arXiv preprint arXiv:2210.09054, 2022.

- Janzing and Schölkopf (2010) D. Janzing and B. Schölkopf. Causal inference using the algorithmic markov condition. IEEE Transactions on Information Theory, 56(10):5168–5194, 2010. doi: 10.1109/TIT.2010.2060095.

- Janzing et al. (2009) D. Janzing, X. Sun, and B. Schoelkopf. Distinguishing cause and effect via second order exponential models. ArXiv e-prints (0910.5561), 2009. doi: 10.48550/ARXIV.0910.5561.

- Khemakhem et al. (2021) I. Khemakhem, R. Monti, R. Leech, and A.Hyvarinen. Causal autoregressive flows. In Proceedings of The 24th International Conference on Artificial Intelligence and Statistics, volume 130 of Proceedings of Machine Learning Research, pages 3520–3528. PMLR, 2021. URL https://proceedings.mlr.press/v130/khemakhem21a.html.

- Kojadinovic and Holmes (2009) I. Kojadinovic and M. Holmes. Tests of independence among continuous random vectors based on cramér-von mises functionals of the empirical copula process. Journal of Multivariate Analysis, 100:1137–1154, 2009. doi: 10.1016/j.jmva.2008.10.013.

- Marx and Vreeken (2019) A. Marx and J. Vreeken. Telling cause from effect using mdl-based local and global regression. Knowledge and Information Systems, 60(3):1277–1305, 2019. doi: 10.1007/s10115-018-1286-7.

- Mooij et al. (2016) J.M. Mooij, J. Peters, D. Janzing, J. Zscheischler, and B. Schölkopf. Distinguishing cause from effect using observational data: Methods and benchmarks. Journal of Machine Learning Research, 17(1):1103–1204, 2016.

- Nowzohour and Bühlmann (2016) Ch. Nowzohour and P. Bühlmann. Score-based causal learning in additive noise models. Statistics: A Journal of Theoretical and Applied Statistics, 50(3):471–485, 2016. doi: 10.1080/02331888.2015.1060237.

- Park and Park (2019) G. Park and H. Park. Identifiability of generalized hypergeometric distribution (ghd) directed acyclic graphical models. In Proceedings of the Twenty-Second International Conference on Artificial Intelligence and Statistics, volume 89 of Proceedings of Machine Learning Research, pages 158–166. PMLR, 2019. URL https://proceedings.mlr.press/v89/park19a.html.

- Park and Raskutti (2015) G. Park and G. Raskutti. Learning large-scale poisson dag models based on overdispersion scoring. In Advances in Neural Information Processing Systems, volume 28. Curran Associates, Inc., 2015. URL https://proceedings.neurips.cc/paper/2015/file/fccb60fb512d13df5083790d64c4d5dd-Paper.pdf.

- Park and Raskutti (2017) G. Park and G. Raskutti. Learning quadratic variance function (qvf) dag models via overdispersion scoring (ods). Journal of Machine Learning Research, 18(1):8300–8342, 2017.

- Pearl (2009) J. Pearl. Causality: Models, Reasoning and Inference. Cambridge University Press, 2009. ISBN 978-0521895606.

- Pearl and Mackenzie (2019) J. Pearl and D. Mackenzie. The Book of Why. Penguin Books, 2019. URL http://bayes.cs.ucla.edu/WHY/.

- Peters et al. (2014) J. Peters, J.M. Mooij, and B. Schölkopf. Causal discovery with continuous additive noise models. Journal of Machine Learning Research, 15:2009–2053, 2014.

- Peters et al. (2016) J. Peters, P. Bühlmann, and N. Meinshausen. Causal inference by using invariant prediction: identification and confidence intervals. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 78(5):947–1012, 2016. URL https://doi.org/10.1111/rssb.12167.

- Peters et al. (2017) J. Peters, D. Janzing, and B. Schölkopf. Elements of Causal Inference: Foundations and Learning Algorithms. The MIT Press, 2017. ISBN 0262037319. URL https://library.oapen.org/bitstream/id/056a11be-ce3a-44b9-8987-a6c68fce8d9b/11283.pdf.

- Pfister et al. (2018) N. Pfister, P. Bühlmann, B. Schölkopf, and J. Peters. Kernel-based tests for joint independence. Journal of the Royal Statistical Society Series B, 80(1):5–31, 2018. doi: 10.1111/rssb.12235.

- Philippine Statistics Authority (2023) Philippine Statistics Authority. Family income and expenditure survey (fies), 2023. URL https://psa.gov.ph/content/family-income-and-expenditure-survey-fies-0. Accessed: [1.2.2023].

- Rajendran et al. (2021) G. Rajendran, B. Kivva, M. Gao, and B. Aragam. Structure learning in polynomial time: Greedy algorithms, bregman information, and exponential families. NeurIPS, Conference Paper 7430, 2021. doi: 10.48550/arXiv.2110.04719.

- Rasmussen and Williams (2005) C. E. Rasmussen and C. K. I. Williams. Gaussian Processes for Machine Learning. The MIT Press, 2005. ISBN 9780262256834. doi: 10.7551/mitpress/3206.001.0001.

- Shimizu et al. (2006) S. Shimizu, P. Hoyer, A. Hyvärinen, and A. Kerminen. A linear non-gaussian acyclic model for causal discovery. Journal of Machine Learning Research, 7:2003–2030, 2006.

- Spirtes (2010) P. Spirtes. Introduction to causal inference. Journal of Machine Learning Research, 11(54):1643–1662, 2010. URL http://jmlr.org/papers/v11/spirtes10a.html.

- Spirtes et al. (2001) P. Spirtes, C. Glymour, and R. Scheines. Causation, Prediction, and Search, 2nd Edition, volume 1. The MIT Press, 1 edition, 2001. URL https://EconPapers.repec.org/RePEc:mtp:titles:0262194406.

- Stasinopoulos and Rigby (2007) D.M. Stasinopoulos and R.A. Rigby. Generalized additive models for location scale and shape (gamlss) in r. Journal of Statistical Software, 23(7):1–46, 2007. doi: 10.18637/jss.v023.i07.

- Strobl and Lasko (2022) E.V. Strobl and T. A. Lasko. Identifying patient-specific root causes with the heteroscedastic noise model. arXiv preprint arXiv:2205.13085, 2022.

- Sun and Schulte (2023) X. Sun and O. Schulte. Cause-effect inference in location-scale noise models: Maximum likelihood vs. independence testing, arXiv preprint 2301.12930, 2023.

- Tagasovska et al. (2020) N. Tagasovska, V. Chavez-Demoulin, and T. Vatter. Distinguishing cause from effect using quantiles: Bivariate quantile causal discovery. In Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 9311–9323, 2020. URL https://proceedings.mlr.press/v119/tagasovska20a.html.

- Verma and Pearl (2013) T. S. Verma and J. Pearl. On the equivalence of causal models. Computing Research Repository, 2013. URL http://arxiv.org/abs/1304.1108.

- Wood et al. (2016) S. N. Wood, N. Pya, and B. Säfken. Smoothing parameter and model selection for general smooth models. Journal of the American Statistical Association, 111(516):1548–1563, 2016. doi: 10.1080/01621459.2016.1180986.

- Xu et al. (2022) S. Xu, O. A. Mian, A. Marx, and J. Vreeken. Inferring cause and effect in the presence of heteroscedastic noise. In Proceedings of the 39th International Conference on Machine Learning, volume 162, pages 24615–24630, 2022. URL https://proceedings.mlr.press/v162/xu22f.html.

- Zhang and Hyvärinen (2009) K. Zhang and A. Hyvärinen. On the identifiability of the post-nonlinear causal model. In Proceedings of the Twenty-Fifth Conference on Uncertainty in Artificial Intelligence, UAI ’09, pages 647–655. AUAI Press, 2009. ISBN 9780974903958.

- Zhang and Hyvärinen (2010) K. Zhang and A. Hyvärinen. Distinguishing causes from effects using nonlinear acyclic causal models. In Proceedings of Workshop on Causality: Objectives and Assessment at NIPS 2008, volume 6 of Proceedings of Machine Learning Research, pages 157–164. PMLR, 2010. URL https://proceedings.mlr.press/v6/zhang10a.html.

- Zhang et al. (2011) K. Zhang, J. Peters, D. Janzing, and B. Schölkopf. Kernel-based conditional independence test and application in causal discovery. In Proceedings of the Twenty-Seventh Conference on Uncertainty in Artificial Intelligence, UAI’11, pages 804–813. AUAI Press, 2011. ISBN 9780974903972.