Cost of diffusion: nonlinearity and giant fluctuations

Satya N. Majumdar1, Francesco Mori2, Pierpaolo Vivo31 LPTMS, CNRS, Univ. Paris-Sud, Université Paris-Saclay, 91405 Orsay, France

2 Rudolf Peierls Centre for Theoretical Physics,

University of Oxford, Oxford, United Kingdom

3 Department of Mathematics, King’s College London, London WC2R 2LS, United Kingdom

Abstract

We introduce a simple model of diffusive jump process where a fee is charged for each jump. The nonlinear cost function is such that slow jumps incur a flat fee, while for fast jumps the cost is proportional to the velocity of the jump. The model – inspired by the way taxi meters work – exhibits a very rich behavior. The cost for trajectories of equal length and equal duration exhibits giant fluctuations at a critical value of the scaled distance travelled. Furthermore, the full distribution of the cost until the target is reached exhibits an interesting “freezing” transition in the large-deviation regime. All the analytical results are corroborated by numerical simulations. Our results also apply to elastic systems near the depinning transition, when driven by a random force.

††preprint: APS/123-QED

Introduction - For more than a century, simple stochastic processes like the random walk have been successfully used to model a variety of phenomena across disciplines berg_book ; biology ; Bouchaud05 . For instance, the motion of bacteria in space berg_book ; biology and the evolution of the price of a stock in finance Bouchaud05 can be approximated as a sequence of jumps between states, which take place according to some probabilistic rule.

In many different contexts, it is natural to associate a (possibly non-linear) cost – or a reward – to the “change of state” of a stochastic process – often with unexpected or paradoxical consequences. For instance, the energy consumption

of bacteria changes depending on the environment they move in berg_book . Wireless devices absorb different amounts of energy when they switch between activity states (‘off’, ‘idle’, ‘transmit’ or ‘receive’) wireless ; wireless2 . In biochemical reactions, it is often convenient to label secondary reaction products as cost/reward of an underlying primary process stochasticreaction for bookkeeping purposes. The bonus-malus vehicle insurance premium changes depending on the number of claims made in the previous year markovreward4 . In software development, the so-called “technical debt” is the cost of additional rework caused by prioritizing an easy solution now instead of a better design approach that would delay the release of the product technicaldebt . In a variety of situations where random factors are present that affect the change of state of a system, computing the total cost (or reward) of a trajectory may prove very challenging.

In Mathematics and Engineering, stochastic processes with associated costs have been investigated in the framework of Markov reward models howard_book ; markovreward ; rew . Recently, the joint distribution of displacement and cost has also been investigated in Ref. costlevy for random walks in a random environment until a first-passage event. Moreover, optimal control theory has been applied in Ref. debruyne21 to minimize the cost of random walks with resetting. However, the impact of a nonlinear cost function on the cost fluctuations, both in the typical and in the large deviation regime, remains largely unexplored.

An everyday example where nonlinear costs lead to unexpected consequences is that of taxi fares. Indeed, taxi rides in a busy city typically consist of a mixture of fast excursions, and slow steps due, e.g., to congestion or traffic lights. The fare charged to a passenger is automatically computed by the taxi meter, which follows a fairly universal and simple recipe Eastaway . Each city council determines a changeover speed – based on a statistical analysis of the typical local traffic conditions. If the taxi moves faster than , the meter ticks according to the space covered, while if the taxi moves slower than , the meter ticks according to the time elapsed. This way, the driver gets compensated even when the taxi barely moves due to heavy traffic. For example, according to London’s Tariff I rate TFL the meter should charge pence for every 105.4 metres covered, or 22.7 seconds elapsed (whichever is reached first). One of the surprising consequences of the non-linear nature of the taxi fare structure is the so-called taxi paradoxEastaway , whereby two taxis starting together from and arriving together at may charge very different fares depending on their individual patterns of slow vs. fast chunks in their trajectories.

In this Letter, we study a simple but general model of diffusion, inspired by the taxi paradox, where the nonlinear nature of the costs associated to each jump gives rise to a rich and nontrivial behavior. In particular, we will consider two scenarios: fixing both the total distance and the number of steps (Ensemble (i)), or fixing the target location but allowing the number of steps to get there to fluctuate (Ensemble (ii)). In Ensemble (i), the cost has a finite and non-monotonic variance, which is maximal at some critical value of the scaled distance . In Ensemble (ii), we show that the cost variance displays a rich behavior when changing the speed threshold , including ‘giant’ fluctuations of the total cost. In this latter setting, the large deviations of the hitting cost displays an unexpected ‘freezing’ transition in the low-cost regime. Our results show that associating a nonlinear cost to the evolution of a random walk leads to very rich and unexpected phenomena.

The model -

Consider a one-dimensional walker whose position at discrete time evolves according to

(1)

starting from the origin , with drawn independently from a probability density function (pdf) with positive support. To each jump, we associate a cost that increases according to the law

(2)

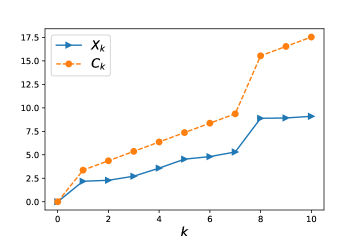

where is a function of . The final position reached after steps is , and the total cost due is . For a typical realization of the process, see Fig. 1. Clearly, and are correlated random variables, whose joint statistics is of interest here.

We further assume that the jumps are positive and exponentially distributed with mean value , i.e., that . For simplicity, we set . Inspired by the taxi paradox described above, we consider the nonlinear cost function , with a positive constant, and the Heaviside step function. This function is such that jumps shorter than the critical size in one unit of time (slower jumps) incur a unit fee, whereas longer (faster) jumps are more costly, with the fee being proportional to the length (velocity) of the jump. Thus, in our model there are two parameters, and .

Figure 1: Typical realization of a random walk with cost function . The cost up to step is a nonlinear function of the random jumps.

Main results (Ensemble (i)) - Due to the nonlinear nature of the cost function, even after fixing the total distance and the number of steps , the total cost remains random, as expressed by the taxi paradox. For large , the average cost grows with the total distance as

(3)

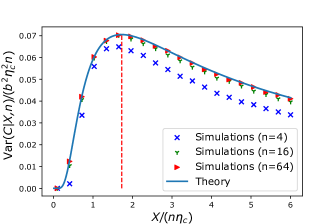

where . To quantify the cost fluctuations around the average, we first compute the cost variance conditioned on the value of after exactly steps. In particular, in the late-time limit , with fixed, we find that the variance takes the scaling form

(4)

where

(5)

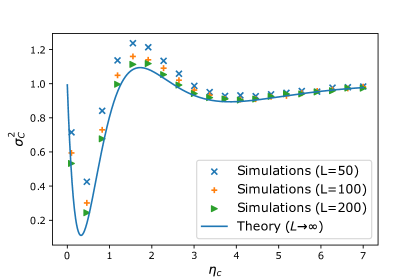

is a positive, non-monotonic scaling function. This scaling function is shown in Fig. 2 and it is in perfect agreement with numerical simulations. Note that the variance has a single maximum at the point . This scaling function has asymptotic behaviors for small and for large .

Figure 2: Scaled cost variance conditioned on the final position as a function of . The continuous blue line corresponds to the analytical scaling function in Eq. (5) (valid for ). The symbols display the results of numerical simulations with samples and different values of . The vertical dashed line highlights the maximum at .

To understand the non-monotonic behavior of the variance, consider two opposite limits: (that is large) and ( small). In the former case, when is fixed to be large,

in a typical trajectory, most of the jumps are big, i.e, the configuration is dominated

by “space-like” runs only (i.e., ) and hence the cost can be written as . Consequently, since both and are fixed the fluctuations of are severely constrained for large . This decrease in the cost fluctuations is hence consequence of the linearity of for large (see supplemental for a discussion on the nonlinear case). In the latter case , a typical trajectory is dominated by only “time-like” runs and once again the cost fluctuations from one trajectory to another are expected to be small, as the precise length of each jump will not significantly alter the fee charged per jump. Thus these two ‘phases’ are like ‘pure’ phases. As one increases the ‘control parameter’ , one first crosses over

from a ‘time-like’ pure phase

to a ‘mixed’ phase, characterized by a larger entropy (i.e. a larger number of possible arrangements of individual jumps eventually landing to the same final spot after jumps). Upon further increasing , the conditional variance undergoes a second crossover

from the ‘mixed’ phase to a ‘space-like’ pure phase. At the special value , the cost fluctuations are maximal (the most unfair scenario for taxi passengers).

Physical applications - Nonlinear functions similar to ,

composed of a constant and a linear part, naturally emerge in disparate areas of

physics. An elementary example is that of static friction: in order to move a block

in contact with a substrate one has to overcome a threshold force due to

static adhesion. Then, applying a force for a fixed time interval ,

the velocity of the block is given by

where now depends on the block mass and VMT2012 . The function

is the velocity-force characteristic describing the response of the system

to an applied force and, up to a global shift by , is identical to the cost

function per unit time in our taxi model. A natural question is: what is the average

response when the block is subject to a random applied force drawn from,

say, ? To measure this average (over random force) response, one

needs to repeat the experiment times, by applying a random force drawn

independently for each sample from . Then is precisely the mean force per sample, and is the mean velocity of the block per sample. Thus, the number of steps

in the taxi problem plays the role of the number of samples here. Consequently,

for large , the scaling function in Eq.

(3) describes precisely the average response characteristic, while

in Eqs. (4) and (5) describe the

fluctuations of the response around its average.

More generally, our results can be extended to a wide variety of disordered

systems when an extended object/manifold such as an elastic string or a polymer is

driven by a random force in a spatially inhomogeneous medium. These

systems undergo a depinning transition when a force is applied: below the

depinning threshold , the manifold is pinned by the disorder and its velocity

vanishes, while above the threshold, the velocity-force relation follows a power-law

scaling with the depinning exponent pascal2000 ; Duemmer2005 ; Reichhardt2016 . For example, when a DNA chain

translocates through a nanopore by applying a pulling force via optical tweezer, the

exponent menais18 , while for a harmonic elastic string in

-dimensions one gets Duemmer2005 . Other examples

include vortices in type-II superconductors Blatter1994 and colloidal crystals

Pertsinidis2008 . To analyse the velocity-force characteristic for such an

elastic string driven by a random force, we need to generalise our method

presented above for to for arbitrary

. In supplemental , we have computed exactly both the average

velocity-force response characteristic and its fluctuations for arbitrary .

Our results show that the associated scaling functions and

depend continuously on .

Main results (Ensemble (ii)) - It is also natural to estimate the distribution of the hitting cost to be paid to reach a given location , irrespective of the time required. First-passage or hitting properties redner_book ; Brayreview ; BrownianFunctionals are important in several applications, from chemical reactions hanggi90 to insurance policies avram08 . Note that in this second setting, the number of steps is a random variable. We find that for large the distribution of takes the large-deviation form

(6)

where the rate function reads

(7)

and satisfies

(8)

The rate function is supported over and has the following asymptotic behaviors supplemental

(9)

where and are given below (see Eq. (11)).

Thus, in the typical regime, the cost fluctuates around the typical value , where , with variance , where

(10)

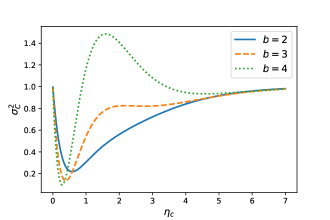

It turns out that the cost variance has a surprisingly rich behavior as a function of the parameters and . First, for both and the scaled variance tends to the limiting value (see Fig. 3). This counter-intuitive result can be understood as follows. For , all of the steps are time-like and hence the cost , where is the number of steps. The distribution of the number of steps needed – given the target location – is Poisson, for (see supplemental for the derivation). Therefore, . On the other hand, for , all of the steps are space-like and hence , where is the final position. Thus, we obtain again .

For intermediate values of , the behavior of depends on . For small values of , has a unique minimum as a function of (see supplemental ). Interestingly, above the critical value (that we computed numerically with Mathematica), develops a second minimum and a maximum (see Fig. 3). This behavior can be qualitatively understood as follows: for slightly above zero, most of the step are still space-like. Therefore, , hence the variance , implying that initially must decrease linearly as increases from zero. As increases further, ‘time-like’ steps become more and more abundant. The cost fluctuations start increasing again with increasing and become maximal at some . These ‘giant’ fluctuations reflect the perfect mixing of time-like and space-like steps, which can be arranged in the maximal number of different ways to cover the distance . Increasing further beyond the maximum leads the cost fluctuations to subside, as the pure “time-like” phase settles in.

Figure 3: Variance of the hitting cost as a function of for increasing values of .

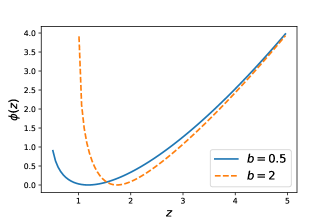

The behavior of the lowest edge of the support of is also very interesting. First, the edge itself depends on whether is smaller or larger than . More precisely, for , while for .

Around the lower edge, we have the following behavior for

(11)

with solution of and . Therefore, the rate function attains a finite value at the lower edge of its support, , if , whereas it diverges logarithmically at the lower edge of its support, , if . A plot of the full rate function computed by solving Eq. (7) and Eq. (8) numerically with Mathematica, along with the asymptotic behaviors above is included in Fig. 4 for different values of and .

Figure 4: Rate function describing the large deviations of the hitting cost, evaluated by solving Eq. (7) and Eq. (8) numerically with Mathematica for and (continuous line) and and (dashed line).

Interestingly, the lower edge “freezes” to the value for . To understand this freezing transition, we notice that the lower edge is related to the minimal possible cost by . In supplemental , we show that if , i.e., when space-like configurations are sufficiently inexpensive, the cost is minimized by a single long jump of length , corresponding to (and hence ). On the other hand, for , the minimal cost is attained with time-like steps of length leading to .

Derivations - We focus on the probability that a random walker that has reached position after exactly steps with a total cost (Ensemble (i)). This quantity can be formally written as

(12)

where the average is performed over the variables . Taking the double Laplace transform yields supplemental , where

(13)

The distribution of the final position alone is easily obtained as for an exponential jump distribution. Thus, the -th moment of , conditioned on the total displacement , can be obtained by Laplace inversion supplemental , leading to the exact expressions for the average and variance of the cost in Eqs. (39) and (42) of supplemental . The fact that the conditional variance is nonzero embodies the taxi paradox described earlier, as different trajectories reaching the same spot after the same number of steps ( time) may indeed charge different amounts!

Conclusions and Outlook - Motivated by the taxi paradox,

we have introduced and solved exactly a simple model for diffusion with a nonlinear cost associated to each

jump. Our results exhibit unexpected phenomena, including giant fluctuations of the

cost and a freezing transition in the large deviation regime of the total cost. We expect that our results should

apply generally to arbitrary jump

distributions with a finite variance. We have shown that our results can be directly applied

to a variety of physical systems where an extended object is pulled by a random force in

a disordered medium.

In future works, it would be interesting to investigate fat-tailed jump

distributions such as Lévy walks, which are of central importance in

finance and biology ZDK2015 . In particular, very fat-tailed jump

distribution will display condensation phenomena, where a single jump dominates the trajectory Majumdar2005 . It

would be relevant to investigate the impact of a nonlinear cost on such setting. Moreover, one may consider cost

functions that penalize short jumps and rewards instead long excursions with a flat fee – a pattern commonly found in

public transportation pricing models, where monthly passes are typically cheaper than collecting single ride tickets.

Acknowledgements - This work was supported by a Leverhulme Trust International Professorship grant [number

LIP-202-014]. For the purpose of Open Access, the authors have applied a CC BY public copyright licence to any Author

Accepted Manuscript version arising from this submission.

References

(1) H. C. Berg. Random Walks in Biology. (Princeton University Press, 2018).

(2) E. A. Codling, M. J. Plank, and S. Benhamou. Random walk models in biology. J. R. Soc. Interface 5, 813 (2008).

(3) J.-P. Bouchaud. The subtle nature of financial random walks. Chaos 15, 026104 (2005).

(4) P. J. M. Havinga and G. J. M. Smit. Energy-Efficient Wireless Networking for Multimedia Applications. Wireless Communications and Mobile

Computing 1, 165-184 (2001).

(5)

L. Cloth, J.-P. Katoen, M. Khattri, and R. Pulungan. Model checking Markov reward models with impulse rewards. 2005 International Conference on Dependable Systems and Networks (DSN’05), Yokohama, Japan, pp. 722-731, doi: 10.1109/DSN.2005.64 (2005)

(6)

A. Angius and A. Horváth. Analysis of stochastic reaction networks with Markov reward models. In Proceedings of the 9th International Conference on Computational Methods in Systems Biology (CMSB ’11). Association for Computing Machinery, New York, NY, USA, 45–54. https://doi.org/10.1145/2037509.2037517 (2011).

(7) G. Amico, J. Janssen, and R. Manca. Discrete Time Markov Reward Processes a Motor Car Insurance Example. Technology and Investment 1 (2), 135-142. doi: 10.4236/ti.2010.12016 (2010).

(8) V. Lenarduzzi, T. Besker, D. Taibi, A. Martini, and F. Arcelli Fontana.

A systematic literature review on Technical Debt prioritization: Strategies, processes, factors, and tools.

Journal of Systems and Software 171, 110827 (2021). https://doi.org/10.1016/j.jss.2020.110827.

(9) R. Howard. Dynamic Probabilistic Systems. Vol. 1-2 (Wiley, New York, 1971).

(10) L. Tan, K. Mahdaviani, and A. Khisti. Markov Rewards Processes with Impulse Rewards and Absorbing States. Preprint arXiv [arXiv:2105.00330] (2021).

(11) A. Gouberman and M. Siegle. Markov Reward Models and Markov Decision Processes in Discrete and Continuous Time: Performance Evaluation and Optimization. In: Remke, A., Stoelinga, M. (eds) Stochastic Model Checking. Rigorous Dependability Analysis Using Model Checking Techniques for Stochastic Systems. ROCKS 2012. Lecture Notes in Computer Science, vol 8453. Springer, Berlin, Heidelberg (2014). https://doi.org/10.1007/978-3-662-45489-3_6

(12) A. Bianchi, G. Cristadoro, and G. Pozzoli. Ladder Costs for Random Walks in Lévy media. Preprint [arXiv:2206.02271] (2022).

(13) B. De Bruyne and F. Mori. Resetting in Stochastic Optimal Control. Preprint [arXiv:2112.11416] (2021).

(14) R. Eastaway and J. Wyndham. How long is a piece of string? : More hidden mathematics of everyday life. (Pavilion Books, 2005).

(17) A. Vanossi, N. Manini, and E. Tosatti.

Static and dynamic friction in sliding colloidal monolayers.

Proc. Natl. Acad. Sci. U.S.A. 109, 16429 (2012).

(18) C. Pascal, T. Giamarchi, and P. Le Doussal.

Creep and

depinning in disordered media. Phys. Rev. B 62, 6241 (2000).

(19) O. Duemmer and W. Krauth. Critical exponents of the

driven elastic string in a disordered medium. Phys. Rev. E 71, 061601 (2005).

(20) C. Reichhardt and C. J. O. Reichhardt. Depinning and

nonequilibrium dynamic phases of particle assemblies driven over random and ordered

substrates: a review. Rep. Prog. Phys. 80, 026501 (2016).

(21) T. Menais. Polymer translocation under a pulling force: Scaling arguments and threshold forces. Phys. Rev. E 97, 022501 (2018).

(22) G. Blatter, M. V. Feigel’man, V. B. Geshkenbein, A. I. Larkin, and V. M. Vinokur. Vortices in high-temperature superconductors. Rev. Mod. Phys. 66, 1125 (1994).

(23) A. Pertsinidis and X. S. Ling. Statics and dynamics of 2D colloidal crystals in a random pinning

potential. Phys. Rev. Lett. 100, 028303 (2008).

(24) S. Redner. A guide to first-passage processes. (Cambridge University Press, Cambridge, 2001).

(25) A. J. Bray, S. N. Majumdar, and G. Schehr. Persistence and First-Passage Properties in Non-equilibrium Systems. Adv. in Phys. 62, 225-361 (2013).

(26) S. N. Majumdar. Brownian Functionals in Physics and Computer Science. Current Science 89, 2076 (2005).

(27) P. Hänggi, P. Talkner, and M. Borkovec. Reaction-rate theory: fifty years after Kramers. Rev. Mod. Phys. 62, 251 (1990).

(28) F. Avram, Z. Palmowski, and M. R. Pistorius. Exit problem of a two-dimensional risk process from the quadrant: exact and asymptotic results. Ann. Appl. Probab. 18, 2421 (2008).

(29) V. Zaburdaev, S. Denisov, and J. Klafter. Lévy walks.

Rev. Mod. Phys. 87, 483 (2015).

(30) S. N. Majumdar, M. R. Evans, and R. K. P. Zia. Nature of the condensate in mass transport models. Phys. Rev. Lett. 94, 180601 (2005).

I Supplemental Material

Consider a random walk (jump process) in discrete time and continuous space, where each jump

length is a positive independent and identically distributed (IID) variable drawn from a continuous PDF (normalized to unity).

Let us denote the cumulative distribution

(14)

Let and denote the position and cost after steps, i.e.,

(15)

where is the non-linear cost associated to each jump.

Below, we consider two different ensembles where the underlying random variables are different, and then demonstrate how

the statistics of total cost in the two models are related to each other.

I.1 Ensemble (i)

In this Ensemble, the cost and the position are random variables, but

the number of steps is fixed. Let denote the joint distribution of and , given fixed .

It is useful to write this joint distribution explicitly by integrating over the underlying jump lengths.

One obtains

(16)

where all the integrals (here and below) run between and . We emphasize that in this ensemble and are random variables and is fixed. This means that

when we integrate over and for any , we should get . This is easily verified from

Eq. (16), since is normalized to unity for each .

By integrating over , we can easily compute the marginal distribution as

(17)

For example, for positive exponential distribution, , it is easy to see

that is given by (taking Laplace transform of Eq. (17) with respect to and inverting)

(18)

which is normalized to unity, . Knowing this marginal distribution,

one can compute the conditional distribution of , given and as

(19)

One then computes the mean and the variance of from this conditional distribution for fixed and , i.e,.

(20)

(21)

These quantities will be computed below.

I.2 Ensemble (ii)

In this second ensemble, the random variables are and , but the final position is kept fixed at . Let denote the joint distribution of and , for fixed .

One can again express this joint distribution by integrating over the underlying random jumps as

(22)

where is the cumulative distribution defined in Eq. (14). Note that for a generic

, the two distributions respectively in Eqs. (16) and (22) differ

from each other only in the last jump . Eq. (22) can be understood as follows.

Once the walker has made complete jumps, it has to reach in the last jump. So, the

length of the last jump has a different distribution from the preceding ones due to the constraint of reaching . In fact, the statistical weight attached to this last jump

is since the last jump would have been ‘completed’ after .

This is a standard computation in renewal processes. The important thing is to check whether it satisfies

the correct normalization. To check this normalization, we first integrate Eq. (22)

over to get the marginal PDF as

(23)

Let us now take the Laplace transform with respect to to write

(24)

where is the Laplace

transform of the jump distribution.

It is easy to see, using integration by parts, that

Inverting with respect to , we get our desired normalization

(28)

Thus, Eq. (22) is an appropriately normalized joint distribution for the two random variables

and , with fixed . The marginal distribution of for fixed is then obtained

by summing over the random variable

(29)

Finally, we compute the mean cost and its variance for fixed in Ensemble (ii) as

(30)

(31)

I.3 Relationship between the two ensembles

In this section, we will be using the notation (instead of ) for Ensemble (ii) to indicate the fixed total distance in order to compare the two ensembles. The two JPDF’s, namely in Eq. (16) and in

Eq. (22), are different from each other for generic . This is natural

because the random variables in the two ensembles are different. Hence, for generic ,

there is no simple relation between the moments of the total cost in the two Ensembles.

In particular, the

two variances in Eq. (21) and in Eq. (31) have

no reasons to be related to each other.

However,

for the special case of exponential jump distribution , it is clear that

and hence, in this case, Eqs. (16)

and (22) coincide exactly and we have

(32)

Thus for the special exponential distribution , the two joint

distributions and coincide,

although the underlying random variables in the two ensembles are quite different.

To see how the cost moments in the two Ensembles may be related in this special case, we first compute

the marginal distribution in Ensemble (ii).

Substituting and using in Eq. (26) we get

(33)

which, upon inversion, gives the Poisson distribution for

However, once again, one should remember

that the

underlying random variable is in , while it is the

continuous variable in . Using the two identities

and for this exponential jump distribution, it then follows from Eqs. (20)

and (30) that

(36)

Using , then gives the precise relation between the mean costs

in the two Ensembles

(37)

As a useful check of this exact relation, note that the average total cost in Ensemble (i) is (see Eq. (13) in the main text, and derivation below)

(38)

valid for all and all . Substituting this result on the right hand side

of Eq. (37) and summing over exactly, we get

(39)

Now, for large , this leads to

(40)

which coincides exactly (replacing by ) with as stated

just before Eq. (10) in the main text. This is a useful check.

In an identical way, the -th moment of the cost in the two ensembles are also related via

(41)

Consequently, the variances in the two ensembles are also related, but the relationship is not as simple

as the moments in Eq. (41). One has to compute the first and the second moment in each ensembles

(which are related via Eq. (41)), and then compute for

the variance. In other words, the precise relation between the two variances is

(42)

I.4 Ensemble (i): Calculation of the conditional average and variance of the total cost

In this Section, we compute the average and the variance of the total cost charged in Ensemble (i) for an excursion that reaches in exactly steps. We consider again the exponential jump pdf .

We start from the probability (given ) in Eq. (16) that reads

(43)

where denotes the average over the jump variables ’s. We next take the Laplace transform with respect to and

(44)

where

(45)

Here, we used the fact that in Laplace space, all -integrals decouple, and are identical to each other.

Then, taking the -th

derivative of with respect to and setting ,

one gets the

Laplace transform (with respect to ) of the -th moment of the cost

(46)

For example, for and we get after simple algebra from (46) the two expressions

(47)

(48)

Then, we can invert the Laplace transforms (47) and (48) with respect to using

(49)

(50)

Using these Laplace-inversion formulae, we invert Eqs. (47) and (48)

to compute and

explicitly. Next we divide by the marginal distribution

(51)

to compute

and .

After lengthy but straightforward algebra, this leads to the following exact results for the conditional mean and the variance

(52)

(53)

as given in the main text. Taking the scaling limit , , with fixed, we obtain

(54)

(55)

with

(56)

(57)

as given in the main text.

I.5 Ensemble (ii): Poisson distribution for the number of steps needed, given a target location at

We start from the joint distribution of the jumps and the number of steps, given the fixed final location

(58)

Taking the Laplace transform w.r.t. , and integrating over the jumps, we get for the Laplace transform of the marginal distribution of the number of steps given the target location at

(59)

Inverting the Laplace transform, we get the Poisson distribution with parameter

(60)

for as claimed in the main text.

I.6 Ensemble (ii): Asymptotics of

Consider that our random process stops when the target location is reached. Let denote the jump lengths in a typical configuration, where of course the number of steps to reach is now a random variable.

The joint distribution of the jump lengths, the number of steps and the total cost – given the target position is given by

(61)

Marginalizing over and , and taking the Laplace transform with respect to and , we get

(62)

where we used the standard geometric series, and is defined in Eq. (12) of the main text.

Taking the inverse Laplace transform over only, we get for the Laplace transform of the hitting cost distribution

(63)

where is a Bromwich contour.

Assuming the large deviation form , how do we extract the rate function from the large- asymptotic behavior of ? The answer is provided by the Legendre-Fenchel theory as follows.

(64)

where in the first step we have used the large deviation ansatz for , and then we changed variables . For large , we can evaluate the last integral via a saddle point method

(65)

which should be compared with the predicted large deviation behavior

(66)

where the value is that for which the integrand in (63) has a pole, namely .

Comparing (65) and (66), we get by Legendre-Fenchel inversion that

(67)

namely Eq. (7) of the main text, after the identification .

We now investigate the behavior of the critical equation (8) of the main text

(68)

providing the location of the pole of Eq. (63) after the identification . We first analyze it in the limit . In this limit, the critical equation reduces to

(69)

as the only nonzero root. Introducing a Taylor expansion ansatz for small into (68) and expanding for small , we get

(70)

Equating the two coefficients to zero, we get

(71)

(72)

Now, from Eq. (6) of the main text we get

(73)

(74)

where the maximum is attained at , where

(75)

which corresponds to the quadratic minimum (central regime of eq. (9) in the main text).

Coming back to , in the quadratic regime

(76)

which shows that the typical fluctuations of the hitting cost are Gaussian with mean and variance that can be read off from (76) as

(77)

(78)

with given in Eq. (10) of the main text. The variance is shown in Fig. 5 for different values of . As a function of , the variance exhibits the rich behavior described in the main text.

Figure 5: Variance of the hitting cost as a function of for and increasing values of . Simulations are done averaging over trajectories that stop as soon as they cross the target spot . In solid blue, the theoretical prediction in Eq. (10) of the main text.

We now analyze the critical equation (68) in the limit . We can first try to match the second and third term of the equation

(79)

but this can only hold true if the leading asymptotics of the fourth term (evaluated at ) turns out to be smaller than the asymptotics of the second (or third) term evaluated at . Otherwise the initial assumption that the leading asymptotics be given by the second/third term of Eq. (68) would be internally inconsistent.

So, we need to have , which implies . In this sub-case, setting (where is a correction term), inserting this ansatz back into (68) we obtain

(80)

for large . For , we have for large , which satisfies the equation (80) self-consistently to leading order. Hence

(81)

when .

Now, from Eq. (6) of the main text we get

(82)

(83)

where the maximum is attained at that is solution of

(84)

Hence

(85)

as . Therefore, for , we find that

(86)

and .

We now turn to the sub-case . In this case, the “matching” of terms in (79) would be inconsistent. So, we need to match the second and fourth term in the critical equation (68)

(87)

where we can determine the correction term (to leading order in ) by substituting (87) into (68)

(88)

(89)

Lumping together the leading terms () on the left hand side, we need to have

(90)

from which

(91)

Substituting into Eq. (6) of the main text

(92)

(93)

where the maximum is attained at that is solution of

(94)

Hence

(95)

which diverges logarithmically as . Thus, for , we find

(96)

and .

We can now analyze the behavior exactly on the transition line, namely when exactly. In this case, the critical equation (68) reads

(97)

Matching again the second and third term of the equation

(98)

and assuming therefore , the correction term satisfies

(99)

(100)

and assuming the behavior of the correction term, we get in the limit the self-consistency conditions for the constants and

(101)

(102)

where in the last step we expanded and neglected sub-leading terms for large . In the limit , the terms in parentheses in Eq. (102) must vanish, leading to the trascendental equations

(103)

and

(104)

Since , one finds and . Therefore, we find that the solution of Eq. (68), can be written as, for

(105)

Inserting this result into the equation for the rate function (Eq. (6) of the main text), we find that for small

(106)

Performing the maximization over , we obtain that, for ,

(107)

Thus, for the critical case , we find

(108)

and , as reported in the main text.

What remains to be done is to analyze the behavior as of the critical equation (68). As , the dominant terms to be matched are

(109)

which works self-consistently in (68), as the first and second terms ( and ) would then cancel out exactly, while the last term () would go to zero as .

Substituting into Eq. (6) of the main text

(110)

where the maximum is attained at that is solution of

(111)

from which

(112)

as (corresponding to the asymptotics ).

I.7 Ensemble (ii): Configuration of minimal cost and the freezing transition

In this Section, we identify the trajectories that minimize the total cost for Ensemble (ii) in the limit . This minimization will allow us to understand the freezing transition of the lower edge of the rate function around Eq. (11) of the main text. Indeed, the lower edge is related to the minimal cost by the relation .

Assuming that the trajectory of minimal cost is composed of jumps of the same length , we have that the total cost is

(113)

where is the single-step cost function. The total cost can be rewritten as

(114)

Minimizing the cost with respect to , we find that for the minimal cost is

(115)

corresponding to a single jump () of length . In other words, if space-like jump are sufficiently cheap (i.e., if is small), the minimal cost is attained by a single long jump. On the other hand, for we find

(116)

corresponding to time-like steps of maximal length . This explains the freezing transition of the lower edge .

II Generalized cost function

As explained in the main text, our results can be applied to a range of physical systems that

typically undergo a depinning transition when driven by an external force. In these systems, an extended

object such as an elastic string in a disordered medium is dragged by an external force , it remains immobile for

, and starts sliding with a constant velocity with

when the applied force exceeds the threshold value . The exponent depends

on the system. When a random force (say, exponentially distributed)

is now applied to such an extended object, it is natural to investigate what the sample averaged velocity-force

characteristic looks like. Fluctuations around this average response is also important to understand.

Out taxi random walk model is precisely suitable to address this question. In this model we

had chosen the cost function to be . To apply

our results to the randomly forced elastic string mentioned above, we just need to generalize our computations

to the case where is arbitrary.

In this section, we present an exact computation for the class of cost functions

(117)

for arbitrary , thus generalizing our previous result for

. Note that we have included the constant shift in Eq. (117) in order to compare

to the taxi random walk model for . In the physics examples mentioned above, one does not need

this extra factor. However, the contribution of this extra factor in is just in the total cost

and it does not affect the variance.

We will focus here on Ensemble (i), i.e., fixing and and investigate the first two moments of

the cost.

Analogously to the case , the -th moment of the cost can be computed by

first evaluating (see Eq. (46))

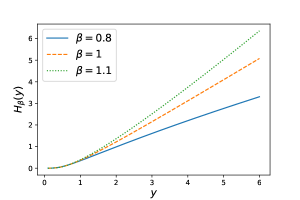

Note that by setting we recover the result in Eq. (52). In the limit , with fixed the average cost can be written as

(124)

where

(125)

This scaling function is shown in Fig. (6). In physical systems, the shift factor in Eq. (124) will not be there and for large , the scaling function

then describes precisely the average velocity-force characteristic (per sample) when

the extended object is driven by an external random force drawn from an exponential

distribution .

Figure 6: Scaling functions (left panel) and (right panel), respectively given in Eqs. (125) and (129), as a function of for different values of .

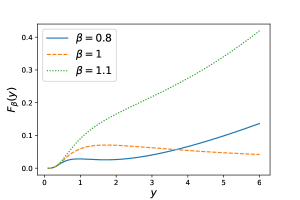

We next focus on the cost variance. Following the same procedure as

above and using the Laplace inversion formula in Eq. (49), we find

(126)

Taking the limit , with fixed we find

(127)

where

(128)

Note that for we recover the result in Eq. (57). The scaling function is plotted in Fig. (6) and

has asymptotic behaviors

(129)

In the large- limit the cost of the cost variance grows as for . However,

only for ,

the prefactor of the leading term for large vanishes exactly and the first nonzero term turns

out to be ,

leading to vanishing fluctuations for large . As explained in the main text, this is a consequence of the

linearity of for large in the case .