Lower Bounds on the Rate of Convergence for Accept-Reject-Based Markov Chains

Abstract

To avoid poor empirical performance in Metropolis-Hastings and other accept-reject-based algorithms practitioners often tune them by trial and error. Lower bounds on the convergence rate are developed in both total variation and Wasserstein distances in order to identify how the simulations will fail so these settings can be avoided, providing guidance on tuning. Particular attention is paid to using the lower bounds to study the convergence complexity of accept-reject-based Markov chains and to constrain the rate of convergence for geometrically ergodic Markov chains.

The theory is applied in several settings. For example, if the target density concentrates with a parameter (e.g. posterior concentration, Laplace approximations), it is demonstrated that the convergence rate of a Metropolis-Hastings chain can tend to exponentially fast if the tuning parameters do not depend carefully on . This is demonstrated with Bayesian logistic regression with Zellner’s g-prior when the dimension and sample increase in such a way that size and flat prior Bayesian logistic regression as .

1 Introduction

Metropolis-Hastings algorithms [23, 35, 56] are foundational to the use of Markov chain Monte Carlo (MCMC) methods in statistical applications [10]. Metropolis-Hastings requires the choice of a proposal distribution and this choice is crucial to the efficacy of the resulting sampling algorithm. The choice of tuning parameters for the proposal distribution prompted ground-breaking research into optimal scaling [48] and adaptive MCMC methods [20]. Nevertheless, in many applications this remains a difficult task and is often accomplished by trial and error. A significant goal here is to provide further guidance on this task, especially in high-dimensional settings.

Metropolis-Hastings Markov chains are an instance of accept-reject-based (ARB) Markov chains, which require a proposal distribution and either accept or reject a proposal at each step. While Metropolis-Hastings chains are the most widely used and studied ARB chains, others are of practical importance or theoretical interest. This includes, among others, non-reversible Metropolis-Hastings [8], Barker’s algorithm [6], portkey Barker’s algorithm [60], and the Lazy-Metropolis-Hastings algorithm [32]. The main difference between varieties of ARB chains is the definition of the acceptance probability, but the choice of a proposal remains crucial for the efficacy of the associated sampling algorithm. Indeed, there has been recent interest in the optimal scaling problem for more general ARB chains [1].

Under standard regularity conditions, ARB chains converge to their target distribution and thus will eventually produce a representative sample from it. If the proposal is not well chosen, then this convergence can take prohibitively long. In fact, one goal is to provide a general tool for identifying when an ARB chain will fail to produce a representative sample within any reasonable amount of time. This is achieved by developing novel lower bounds on the convergence rate. These lower bounds have wide application to aid in choosing proposal distributions and tuning parameters to avoid poor convergence behavior.

General lower bounds on the convergence rate have not been previously investigated for ARB chains outside of some Metropolis-Hastings independence samplers [11, 45, 64]. Others have instead focused on upper bounding the spectral gap using the conductance [2, 9, 22, 25, 26, 33, 52, 66, 67]. An upper bound on the spectral gap lower bounds the convergence rate but requires a reversible Markov chain [18, 33], which is not assumed in the development of the general lower bounds below.

Most commonly, the convergence of ARB chains has been measured with total variation [51, 55]. However, recently, the Wasserstein distances [30, 62, 63] from optimal transportation have been used in the convergence analysis of high-dimensional MCMC algorithms [13, 14, 22, 40, 41]. The interest in Wasserstein distances mainly is due to the observation that Wasserstein distances may enjoy improved scaling properties in high dimensions compared to the total variation distance. The new lower bounds are similar whether total variation or a Wasserstein distance is used, but the conditions required for lower bounding the Wasserstein distances are slightly stronger than those for total variation. In particular, the Wasserstein lower bounds show when the chain has poor convergence properties in total variation, then it will often do so in Wasserstein distances.

Convergence rate analysis of MCMC chains on general state spaces largely has centered on establishing upper bounds on the convergence rate [27, 51] or, failing that, in establishing qualitative properties such as geometric ergodicity, which ensures an exponential convergence rate to the target distribution in either total variation or Wasserstein distances [21, 28, 36, 51, 55]. There has been important work establishing geometric ergodicity for Metropolis-Hastings chains [e.g. 24, 34, 47], but, even though there is some recent work for a specific random-walk Metropolis-Hastings chain [3], it has not yet produced much understanding of their quantitative rates of convergence. The lower bounds developed here allow the exponential rate of convergence to be bounded below and hence, in conjunction with the existing approaches, will help provide a clearer picture of the quantitative convergence properties of geometrically ergodic ARB chains.

Convergence complexity of MCMC algorithms with respect to the dimension and sample size has been of significant recent interest [7, 11, 15, 26, 40, 41, 68, 69, 71]. Lower bounds can be used to study conditions on the tuning parameters which imply the convergence rate rapidly tends to with the dimension and sample size even in the setting where the chain is geometrically ergodic for fixed and . This can then be used to choose the scaling so that the poor high-dimensional convergence properties might be avoided. One implication of the theory developed below is that the scaling should be chosen explicitly as a function of both and , with the details dependent upon the setting, since if they are chosen otherwise, the resulting ARB chain can have poor convergence properties. In comparison, optimal scaling results are derived in the setting where the dimension , but the explicit scaling dependence on is often infeasible to compute.

Throughout, the theory is illustrated with straightforward examples, some of which concern ARB chains that are not versions of Metropolis-Hastings. However, several significant, practically relevant applications of Metropolis-Hastings are also studied. One application concerns a class of Metropolis-Hastings algorithms using a general Gaussian proposal which in special cases is the proposal used in independence samplers, random-walk Metropolis-Hastings (RWMH) [55], Metropolis-adjusted Langevin algorithm (MALA) [43, 46], and other variants such as Riemannian manifold MALA [19].

The lower bounds are also studied for random walk Metropolis-Hastings algorithm with log-concave target densities. In particular, an application to RWMH for Bayesian logistic with Zellner’s g-prior is studied as . In this example, the convergence rate can tend to exponentially fast if the scaling does not depend carefully on and . More general target densities are studied under conditions which imply they concentrate towards their maximum point with (e.g. Bayesian posterior concentration, Laplace approximations) as . Once again, if the tuning parameters do not depend on , the convergence rate can tend to rapidly as . As an application of the general result, flat prior Bayesian logistic regression is studied as only .

The remainder is organized as follows. Section 2 provides a formal definition of ARB Markov chains and some relevant background. Total variation lower bounds are studied in Section 3, including a comparison with conductance methods. Applications of the theoretical results are considered in Section 4. Then Section 5 presents lower bounds in Wasserstein distances. Final remarks are given in Section 6. Most proofs are deferred to the appendices.

2 Accept-reject-based Markov chains

Let be a nonempty measurable space and the Borel sigma algebra on . Suppose is a probability measure on supported on a nonempty measurable set with density with respect to a sigma-finite measure on . The support of is so for each , . Assume for each , and is strictly positive (e.g., Lebesgue measure) meaning for nonempty, measurable open sets , . While this general setting will suffice for most of the work, at various points more specific assumptions on will be required.

For each , suppose that is a proposal distribution on having density with respect to . If , define the acceptance probability by

Let denote the Dirac measure at the point . The accept-reject-based Markov kernel is defined on for and measurable sets as

Let denote the set of positive integers. The Markov kernel for iteration time with is defined recursively by

where .

It is assumed that is such that is invariant for . Invariance is often ensured through a detailed balance (i.e., reversibility) condition, but this is not required in general. For example, detailed balance does not hold for non-reversible Metropolis-Hastings yet is invariant [8]. Of course, detailed balance holds for Metropolis-Hastings (MH) where

| (1) |

Define the total variation distance between probability measures on by where is the set of Borel measurable functions . It is well-known that if is -irreducible, aperiodic, and Harris recurrent, the ARB Markov chain converges in total variation, as , to the invariant distribution [55, 56] and hence will eventually produce a representative sample from . Section 3 considers measuring this convergence with the total variation norm, while Section 5 considers doing so with Wasserstein distances from optimal transportation.

3 Total variation lower bounds

3.1 Lower bounds

Previously, a lower bound in the total variation distance was shown for the Metropolis-Hastings independence sampler [64, Lemma 1]. A similar argument provides a lower bound for general ARB chains.

Theorem 1.

For every and every ,

Although it has been suppressed here, often depends on the sample size and the dimension ; for example, consider the setting where is a Bayesian posterior density. If as or , then the total variation lower bound will approach 1 and the ARB Markov chain will be ineffective in that regime. However, once this has been identified, the proposal can often be chosen so as to avoid the difficulties.

Of course, can be difficult to calculate analytically. However, this is often unnecessary since it typically suffices to study an upper bound for it. If a finer understanding is required, it is straightforward to use Monte Carlo sampling to produce a functional estimate of . Both of these approaches will be illustrated in several examples later. Consider the following simple example of a non-reversible Metropolis-Hastings Markov chain [8, Section 4.3].

Example 1.

For , let be the Euclidean space of dimension . Denote the standard -norms by . Denote the Gaussian distribution on with mean and symmetric, positive-definite covariance matrix by . For , consider the Crank-Nicolson proposal so that the proposal has the standard Gaussian density as its invariant density, which is denoted . Suppose is a Gaussian density of the distribution with . For ,

Define

and then defines a valid non-reversible Metropolis-Hastings Markov chain [8, Section 4.1] since

If and are the acceptance probabilities for non-reversible MH and the usual MH with the same proposal, respectively, then

For large , the lower bounds of Theorem 1 will be similar for both Markov chains. However, for small values of , the lower bound for non-reversible MH can be appreciably smaller than the lower bound for MH.

In general, it is difficult to compare ARB Markov chains based on lower bounds. However, there are some settings where it may be informative.

Proposition 1.

Let and be ARB kernels with acceptance functions and , respectively. If for all , then

If (perhaps as ), then the lower bound for both and will tend to 1. Of course, if , then it may still be the case that . That is, might avoid poor convergence properties while does not.

Example 2.

Consider the portkey Barker’s kernel [60] where if is symmetric so that , then

| (2) |

Notice that Barker’s [6] algorithm is recovered if .

It is well-known that Metropolis-Hastings is more efficient than Barker’s in the Peskun sense [39] so that the variance of the asymptotic normal distribution for a sample mean will be larger if the Monte Carlo sample is produced using Barker’s algorithm. However, the asymptotic variance is only greater by a factor of 2 [32] and there are some settings where portkey Barker’s is preferred [60].

Notice that if the same proposal density is used for Metropolis-Hastings and portkey Barker’s, then

and hence, by Proposition 1,

The lower bound for portkey Barker’s cannot be better than the lower bound for Metropolis-Hastings.

3.2 Geometric ergodicity

The kernel is -geometrically ergodic if there is a and a function such that for every and every ,

There has been substantial effort put into establishing the existence of for some ARB Markov chains [see, e.g., 24, 34, 46, 47], but, outside of the Metropolis-Hastings independence sampler [64], these efforts have not yielded any constraints on .

Theorem 2.

If is -geometrically ergodic, then

Example 3.

Let and consider the following Gaussian densities

Set

and consider a random walk MH kernel with a Gaussian proposal centered at the previous step and scale matrix . This RWMH is geometrically ergodic [24], but only the existence of has been established.

3.3 Comparison with conductance methods

In this section, the ARB Markov kernel is assumed to be reversible with respect to . Let denote the Lebesgue spaces with respect to a measure . Conductance can be used to lower bound the convergence rate and this is compared to the techniques used above. If a Markov kernel satisfies

then it is said to have a spectral gap. For measurable sets with , define

and define the conductance [33]. The conductance can be used to upper bound the spectral gap [33, Theorem 2.1]:

Since is a reversible Markov kernel, there is an equivalence between a spectral gap and geometric convergence in total variation [18, Theorem 2.1]. Specifically, there is a such that for every probability measure with , there is a constant such that

if and only if there is a spectral gap with . Under these conditions, the convergence rate can be lower bounded by the conductance so that

Under further conditions on the function , the conductance will also lower bound the convergence rate if is geometrically ergodic [18, Proposition 2.1 (ii), Theorem 2.1].

For sets with , to move from to , the Metropolis-Hastings kernel must accept and [22, Proposition 2.16]

Proposition 2.

Assume is a nonempty metric space. Let be a ARB Markov kernel with an upper semicontinuous acceptance probability . Then

4 Applications using Metropolis-Hastings

4.1 Gaussian proposals for Metropolis-Hastings

Suppose , is a positive-definite, symmetric matrix, and . Let the proposal distribution be . For specific choices of and , this is the proposal used in many popular Metropolis-Hastings algorithms. For example, if and , then RWMH results but if is not the identity, then a Riemannian manifold RWMH algorithm is obtained [19]. Of course, if is a constant vector, then an independence sampler results. If is differentiable, , and , then this is the proposal used in MALA [46]. A general covariance and defines the proposal used in Riemannian manifold MALA [19]. The following result lower bounds the convergence rate of a Metropolis-Hastings kernel independently of .

Proposition 3.

Let and the proposal distribution be . The Metropolis-Hastings acceptance probability satisfies

Even though the bound in Proposition 3 is not sharp, it results in general restrictions on the magnitude of the tuning parameter in that it forces to be small in order to avoid poor convergence properties. This suggests, that MH algorithms can have convergence rates with a poor dimension dependence, especially if the tuning parameter is not chosen carefully.

Example 4.

Suppose is the standard -dimensional Normal distribution, , and consider the Metropolis-Hastings algorithm with proposal . Fix and note that

Thus, for any fixed the acceptance probability will approach 0 for large and hence the convergence rate will approach 1. However, this can be avoided if, for example, . If, instead, is fixed, then the acceptance probability will approach 0 for large . Large values of should be avoided when tuning any of the MH algorithms in this example.

Normal proposal distributions are common in many applications of MH, but the key requirement in the proof of Proposition 3 is the boundedness of the proposal density. Consider using a multivariate -distribution as a proposal instead, specifically . Then, if denotes the usual gamma function,

and the same argument in the proof yields that

As with the example above, this suggests that large values of should be avoided.

4.2 RWMH with log-concave targets

Let and where is the normalizing constant. Consider sampling from with RWMH using a -dimensional Gaussian proposal centered at the current state with variance . In this case, for all ,

More can be said with more assumptions on . Consider the setting where satisfies a strong-convexity requirement. That is, if is a convex set and , the function is -strongly convex if is convex on . Also, let denote the set of subgradients of at the point .

Proposition 4.

Suppose is convex and that, for , is -strongly convex on . If , then, for any ,

There are at least two settings where Proposition 4 yields specifc lower bounds.

Corollary 1.

Suppose is convex and that, for , is -strongly convex on . If is the point which maximizes , then

and hence

Proof.

This is immediate from Proposition 4 with the observation that . ∎

Corollary 2.

Suppose is convex and that, for , is -strongly convex on . If the RWMH kernel is -geometrically ergodic, then

For any fixed value of , the lower bound will increase exponentially as . However, if , then this can be avoided, an observation that agrees with the optimal scaling guidelines [49], but under much weaker conditions on .

An adversarial example using a Gaussian target showed the spectral gap for the RWMH algorithm tends to polynomially fast with the dimension [22]. An adversarial example in a non-toy example where the convergence rate can tend to exponentially in the dimension follows.

Example 5.

(RWMH for Bayesian logistic regression) Suppose, for , and

Consider RWMH with Gaussian proposal centered at the current state, scale , and having the posterior distribution as its invariant distribution. The RWMH is -geometrically ergodic for some unknown [61]. The negative log-likelihood in this model is convex and applying Corollary 2, obtain

4.2.1 Bayesian logistic regression with Zellner’s g-prior

A specific application is considered where both and are allowed to increase and the data-generating mechanism for Bayesian logistic regression with Zellner’s g-prior [70] need not be correct. Let with taking values in and taking values in . Let be a fixed constant and set . If is positive-definite and denotes the sigmoid function, the posterior density is characterized by

Assume are independent and identically distributed random variables with zero mean, unit variance, and a finite fourth moment. Consider RWMH with a Gaussian proposal centered at the current state and scale and invariant density . If as , the following result implies that the convergence rate will exponentially tend to with unless .

Proposition 5.

Let denote the point which maximizes . If in such a way that , then, with probability 1, for all sufficiently large , the acceptance probability for RWMH satisfies

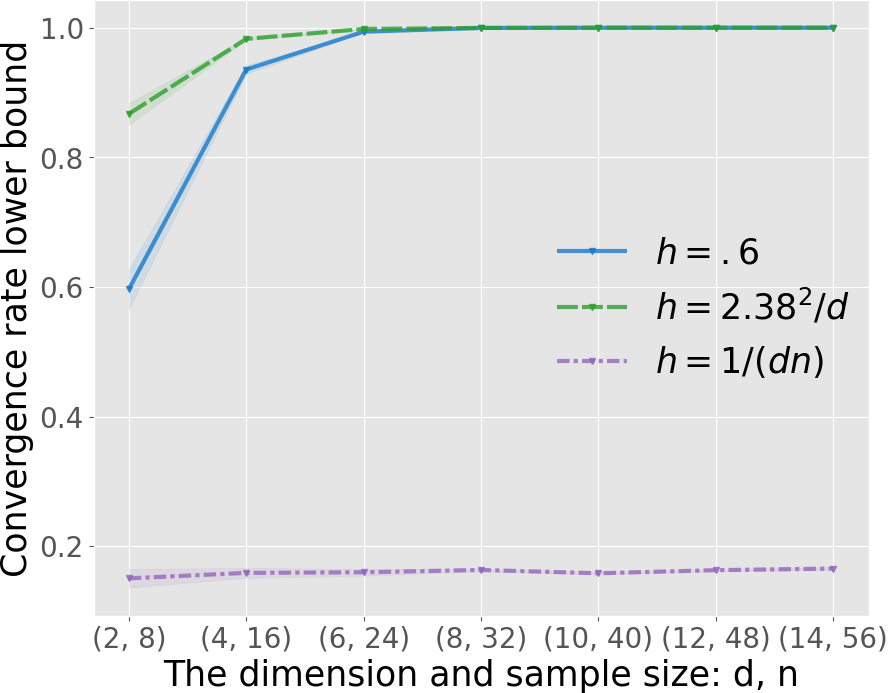

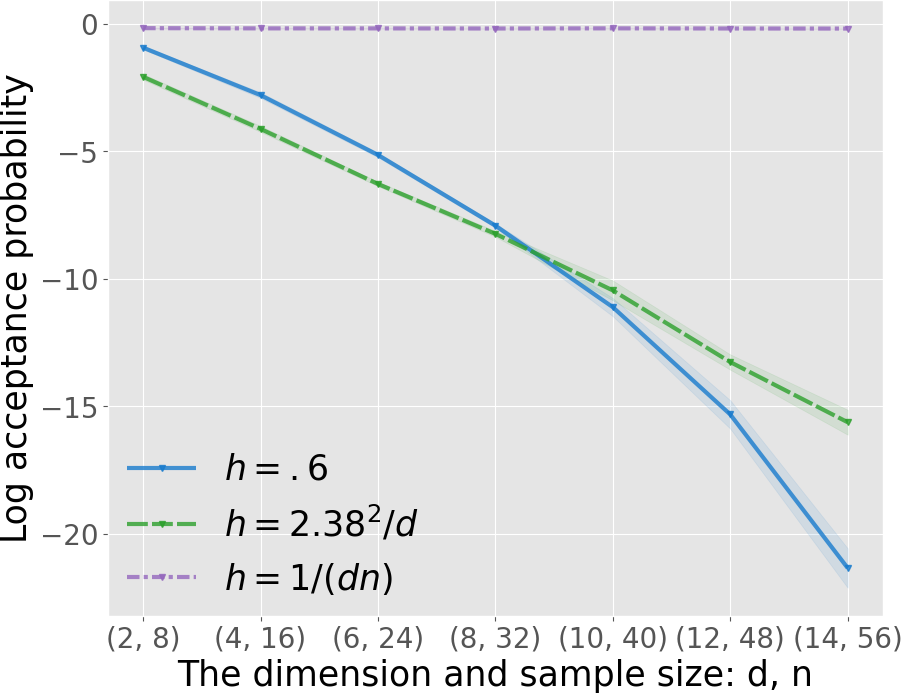

It is useful to empirically investigate the convergence of the RWMH algorithm in this example for different tuning parameters. The acceptance probability at the posterior maximum can be estimated using standard Monte Carlo with samples. Since is log-concave, can be estimated efficiently using gradient descent. In turn, Theorem 1 will be used to estimate the lower bound to the convergence rate. Artificial data will be considered where , , and the data are generated with increasing dimensions and sample sizes , specifically,

As a guideline, Corollary 5 says to choose at least when is large enough. This example does not satisfy the required theoretical assumptions for optimal scaling guidelines [49] and hence is anticipated to perform poorly here. It is compared to optimal scaling with , a fixed variance parameter , and scaling with according to Corollary 5. Repeating the simulation times with randomly generated data, Figure 1(a) displays the estimates to these lower bounds using the average within standard error. Figure 1(b) plots the log acceptance probability at the target’s maximum to compare the speed at which the convergence rate tends to 1. According to the theory, optimal scaling and fixed parameter choices should behave poorly as the dimension increases which corresponds with the simulation results shown in Figure 1.

4.3 Lower bounds under concentration

Section 4.2.1 considered lower bounds on RWMH under concentration of a strongly log-concave posterior. If the target density is concentrating to its maximal point with , intuition suggests that the tuning parameters of the Metropolis-Hastings algorithm should also depend on the parameter . In infinitely unbalanced Bayesian logistic regression, proposals which depend on the sample size have been shown to exhibit more appealing convergence complexity when compared to data augmentation Gibbs samplers [26].

Consider target distributions indexed by a parameter such as Bayesian posteriors where is the sample size. Let and . Define the target density by . If the proposal density is bounded so that there is , with possibly depending on or , such that (cf. Section 4.1), then for MH algorithms,

Of course, the best lower bound will result at , a point maximizing .

A Laplace approximation can be used to lower bound the target density at its maximum point. The following result is inspired by previous results on Laplace approximations [31, 57, 58], but unlike high-dimensional Laplace approximations [53, 54], is not required to be differentiable.

Proposition 6.

Suppose there exists at least one which maximizes for each . Assume for some , the dimension and that the following holds for some constants and for all sufficiently large :

1. is -strongly convex for all .

2. The optimal point satisfies the strict optimality condition:

3. The integral is controlled away from the optimum:

Then for any , for all sufficiently large , the density concentrates at with

Moreover, f the proposal density is bounded so that there is , with possibly depending on or , such that , then

Proposition 6 requires the dimension to not grow too fast with . The first assumption is a locally strong convex assumption which ensures sufficient curvature of locally near the maximum point of . Since only a lower bound on the density is required, the need to control higher order derivatives used in high-dimensional Laplace approximations [53, 54] is avoided. The second and third assumptions ensure sufficient decay of away from similar to assumptions made previously [31, 54]. Similar assumptions are also used for Bayesian posterior densities with proper priors when the dimension is fixed [37, Theorem 4].

Example 6.

It is evident from (3) that Proposition 6 can be important when tuning Metropolis-Hastings algorithms used in Bayesian statistics. In particular, if the target density is concentrating at its maximum point and the tuning parameters and do not depend carefully on , then it easily can happen that rapidly. Moreover, it can happen that the geometric convergence rate rapidly.

4.3.1 Flat prior Bayesian logistic regression

Consider flat prior Bayesian logistic regression without assuming correctness of the data generation. Let be independent and identically distributed with and . With the sigmoid function , the posterior density is characterized by

Assumption 1.

Let if and if and define to be the matrix with rows . Suppose:

1. is full column rank.

2. There exists a vector with all components positive such that .

If Assumption 1 holds with probability for all sufficiently large , then both the maximum likelihood estimator (MLE) and the random Bayesian logistic regression posterior density, , exist [12, Theorems 2.1, 3.1].

The Pólya-Gamma Gibbs sampler has been shown to be geometrically ergodic for this model [65], but it remains an open question if Metropolis-Hastings is geometrically ergodic. Since the prior is improper, previous results on posterior concentration [37] do not apply, but the next result shows that the posterior density can indeed concentrate so that Proposition 6 can be applied for MH algorithms with bounded proposals. For the sake of specificity recall the definitions of , , and from Section 4.1 so that the MH algorithms uses a proposal distribution.

Theorem 3.

Assume the following:

-

1.

With probability , Assumption 1 holds for all sufficiently large .

-

2.

The MLE is almost surely consistent to some .

-

3.

with probability .

-

4.

For , if , then with probability .

Then, with probability , for all sufficiently large , there is a so that the MH acceptance probability satisfies

Assumption 1 ensures existence of the posterior density and MLE [12, Theorem 2.1, 3.1]. Consistency of the MLE in Assumption 2 is a well-studied problem and conditions are available when the model is correctly specified [16] or using M-estimation [59, Example 5.40]. Assumption 4 was used previously [37, Theorem 13] and is used to ensure identifiability in generalized linear models [59]. Assumption 2 requires standardization of the features which is often done for numerical stability.

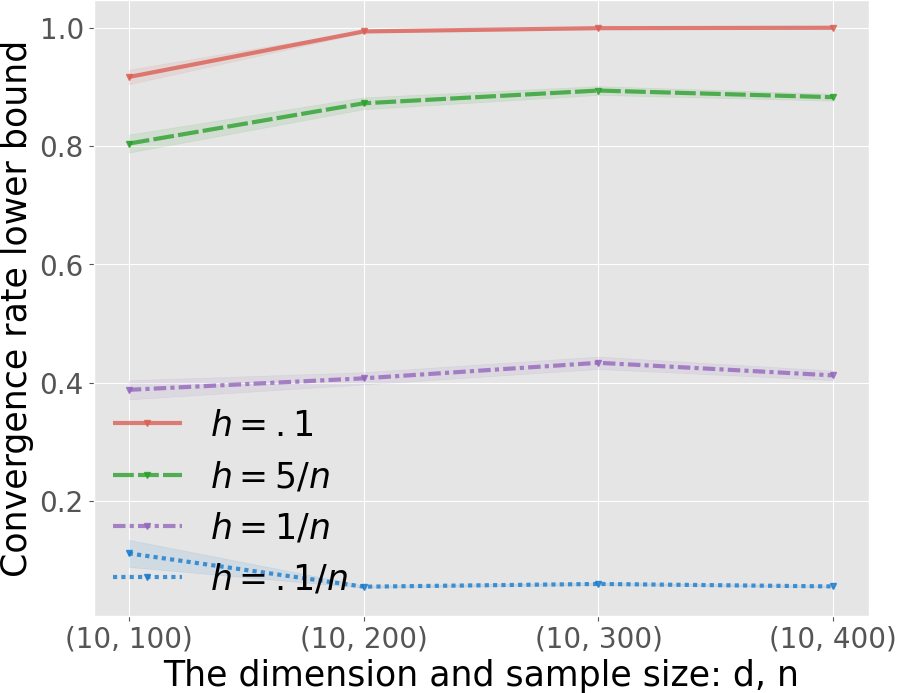

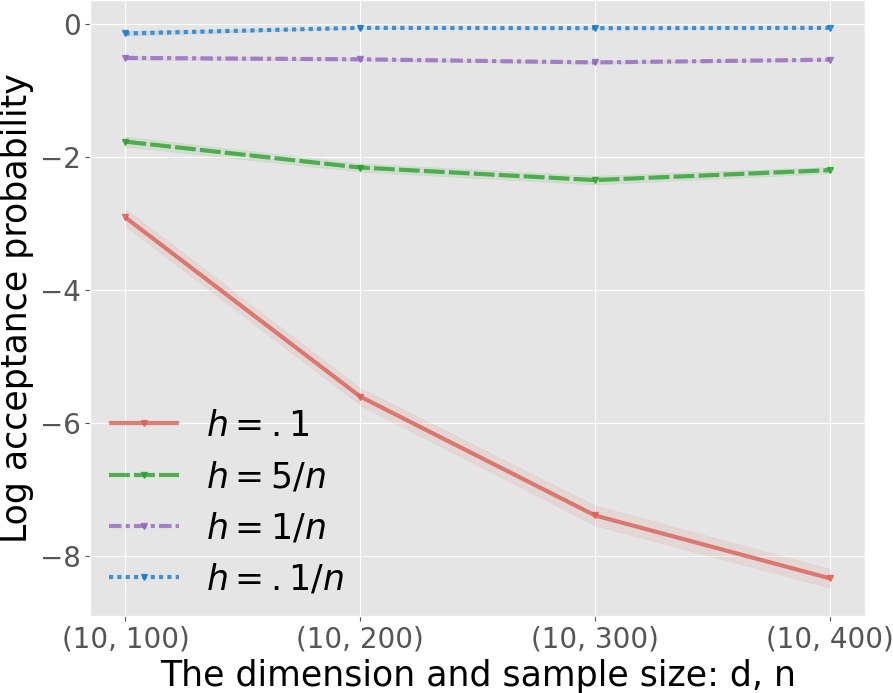

In this example an explicit value for is unavailable, but the robustness of the scaling can be investigated empirically via a standard Monte Carlo estimate of the acceptance probability at the MLE . The estimate will be based on Monte Carlo samples. Consider using MH with a fixed variance parameter , and scaling with , , and . Artificial data is generated with where in fixed dimension and increasing sample sizes . The simulation is replicated times independently. Figure 2(a) shows the total convergence rate lower bound and Figure 2(b) shows the log acceptance probability at the target’s maximum using the average within estimated standard error. It is apparent that scales worse than , but the scaling is not nearly as problematic as the fixed variance parameter which is commonly used in practice.

5 Wasserstein lower bounds

Wasserstein distances have become popular in the convergence analysis of high-dimensional MCMC algorithms due to improved scaling properties in high dimensions compared to the total variation distance. There are lower bounds available for many Wasserstein distances which are analogous to the lower bounds from Section 3 and which can result in similar conclusions if the acceptance probability is not well-behaved.

The Wasserstein lower bounds also yield necessary conditions for Wasserstein geometric ergodicity of ARB chains that are similar to those available for total variation [47]. A result of independent interest establishes the equivalence between the a spectral gap and Wasserstein geometric ergodicity for general reversible Markov chains, complementing existing results for total variation [42].

5.1 Lower bounds

For probability measures , let be the set of all joint probability measures with marginals . With a metric cost function , the -Wasserstein distance of order is

Generally, the metric is the metric on the space.

We consider the following assumption on the target density.

Assumption 2.

Suppose where and . Suppose is a density with respect to Lebesgue measure and suppose .

The Wasserstein distances are required to satisfy the following condition.

Assumption 3.

Suppose for some constant , .

As norms are equivalent on , these cost metrics include any norm on .

For the special case of the Metropolis-Hastings independence sampler there are existing lower bounds for some Wasserstein distances [11]. The above assumptions are enough to ensure lower bounds for the general ARB Markov chain and a wider class of Wasserstein distances.

5.2 Geometric ergodicity

Say is -geometrically ergodic if there is a and a function such that for every and every ,

Compared to the definition of geometric ergodicity in total variation, this requires a metric cost function for the Wasserstein distance of order .

Recall that if the rejection probability cannot be bounded below one, that is, if the acceptance probability satisfies , then a Metropolis-Hastings algorithm fails to be geometrically ergodic [47, Proposition 5.1]. Theorem 5 yields the same in these Wasserstein distances for ARB kernels. There are well known examples where the condition on this happens [34, Example 1], [47, Proposition 5.2].

Proof.

If it were -geometrically ergodic, then, by Theorem 5, , which is a contradiction. ∎

Analogous comparisons can be made to conductance methods as in Section 3.3. In particular, the lower bounds on the spectral gap can also lower bound the exponential convergence rate in the Wasserstein distance. We extend previously developed sufficient conditions for a spectral gap using the Wasserstein distance to an equivalence condition [22, Proposition 2.8]. Note that the assumptions in the following proposition are self-contained and hold for reversible Markov kernels under more general conditions.

Proposition 8.

Let be any probability measure on a Polish space , and let be any Markov kernel on reversible with respect to . For a , the following are equivalent if they hold for every probability measure on with :

(i) The Markov operator has a spectral gap at least .

(ii) There is a depending on such that for every ,

For reversible Metropolis-Hastings under the conditions of Proposition 2, if Proposition 8 (ii) holds, then

Under these conditions, an application of Hölder’s inequality extends this lower bound to Wasserstein distances of order . For probability measures with , if there is a such that for every ,

then as well.

6 Final remarks

The lower bounds studied above can guide practitioners in tuning ARB algorithms, including Metropolis-Hastings algorithms. Particular attention was paid to the convergence complexity of geometrically ergodic ARB chains and it was demonstrated that the tuning parameters should carefully take into account both the sample size and parameter dimension . In particular, RWMH and MALA type algorithms have strong restrictions on the scaling parameter when the target density concentrates with .

Lower bounds on the convergence rate appear to be available for other sampling algorithms such as Hamiltonian Monte Carlo, component-wise MCMC (e.g. Metropolis-within-Gibbs), and some adaptive MCMC algorithms, but these are beyond the scope of the current work.

7 Supplementary material and code availability

The Python package ”mhlb” and the code used for the simulations and plots are made available for download at https://github.com/austindavidbrown/lower-bounds-for-Metropolis-Hastings.

8 Acknowledgements

We thank Riddhiman Bhattacharya, Qian Qin, and Dootika Vats for their helpful comments on an earlier draft. Jones was partially supported by NSF grant DMS-2152746.

References

- Agrawal et al. [2021] Sanket Agrawal, Dootika Vats, Krzysztof Łatuszyński, and Gareth O. Roberts. Optimal scaling of MCMC beyond Metropolis. To appear in Advances in Applied Probability, 2021.

- Andrieu and Vihola [2015] Christophe Andrieu and Matti Vihola. Convergence properties of pseudo-marginal Markov chain Monte Carlo algorithms. The Annals of Applied Probability, 25(2):1030 – 1077, 2015.

- Andrieu et al. [2022] Christophe Andrieu, Anthony Lee, Sam Power, and Andi Q. Wang. Explicit convergence bounds for Metropolis Markov chains: isoperimetry, spectral gaps and profiles. preprint arXiv:2211.08959, 2022.

- Bach [2010] Francis Bach. Self-concordant analysis for logistic regression. Electronic Journal of Statistics, 4:384 – 414, 2010.

- Bai and Yin [1993] Z. D. Bai and Y. Q. Yin. Limit of the smallest eigenvalue of a large dimensional sample covariance matrix. The Annals of Probability, 21(3):1275 – 1294, 1993.

- Barker [1964] A. A. Barker. Monte Carlo calculations of the radial distribution functions for a proton-electron plasma. Australian Journal of Physics, 18:119–132, 1964.

- Belloni and Chernozhukov [2009] Alexandre Belloni and Victor Chernozhukov. On the computational complexity of MCMC-based estimators in large samples. The Annals of Statistics, 37(4):2011–2055, 2009.

- Bierkens [2015] Joris Bierkens. Non-reversible Metropolis-Hastings. Statistics and Computing, 26(6):1213–1228, 2015.

- Bou-Rabee and Eberle [2020] Nawaf Bou-Rabee and Andreas Eberle. Markov chain Monte Carlo methods, 2020.

- Brooks et al. [2011] Stephen P. Brooks, Andrew Gelman, Galin L. Jones, and Xiao-Li Meng (Ed). Handbook of Markov Chain Monte Carlo. Chapman & Hall, London, 2011.

- Brown and Jones [2022] Austin Brown and Galin L. Jones. Exact convergence analysis for Metropolis-Hastings independence samplers in Wasserstein distances. preprint arXiv:2111.10406, 2022.

- Chen and Shao [2000] Ming-Hui Chen and Q. Shao. Propriety of posterior distribution for dichotomous quantal response models. Proceedings of the American Mathematical Society, 129(1):293 – 302, 2000.

- Dalalyan [2017] Arnak S. Dalalyan. Theoretical guarantees for approximate sampling from smooth and log-concave densities. Journal of the Royal Statistical Society, Series B, 79:651–676, 2017.

- Durmus and Moulines [2015] Alain Durmus and Éric Moulines. Quantitative bounds of convergence for geometrically ergodic Markov chain in the Wasserstein distance with application to the Metropolis adjusted Langevin algorithm. Statistics and Computing, 25:5–19, 2015.

- Ekvall and Jones [2021] Karl Oskar Ekvall and Galin L. Jones. Convergence analysis of a collapsed Gibbs sampler for Bayesian vector autoregressions. Electronic Journal of Statistics, 15:691 – 721, 2021.

- Fahrmeir and Kaufmann [1985] Ludwig Fahrmeir and Heinz Kaufmann. Consistency and asymptotic normality of the maximum likelihood estimator in generalized linear models. The Annals of Statistics, 13(1):342 – 368, 1985.

- Folland [1999] Gerald B. Folland. Real Analysis: Modern Techniques and Their Applications. Wiley, 2 edition, 1999.

- Fort et al. [2003] G. Fort, E. Moulines, Gareth O. Roberts, and J. S. Rosenthal. On the geometric ergodicity of hybrid samplers. Journal of Applied Probability, 40(1):123–146, 2003.

- Girolami and Calderhead [2011] Mark Girolami and Ben Calderhead. Riemann manifold Langevin and Hamiltonian Monte Carlo methods. Journal of the Royal Statistical Society. Series B (Statistical Methodology), 73(2):123–214, 2011.

- Haario et al. [2001] Heikki Haario, Eero Saksman, and Johanna Tamminen. An adaptive Metropolis algorithm. Bernoulli, 7(2):223 – 242, 2001.

- Hairer and Mattingly [2011] Martin Hairer and Jonathan C. Mattingly. Yet another look at Harris’ ergodic theorem for Markov chains. Seminar on Stochastic Analysis, Random Fields and Applications VI, 63, 2011.

- Hairer et al. [2014] Martin Hairer, Andrew M. Stuart, and Sebastian J. Vollmer. Spectral gaps for a Metropolis–Hastings algorithm in infinite dimensions. The Annals of Applied Probability, 24:2455–2490, 2014.

- Hastings [1970] W. K. Hastings. Monte Carlo sampling methods using Markov chains and their applications. Biometrika, 57(1), 1970.

- Jarner and Hansen [2000] Søren F. Jarner and Ernst Hansen. Geometric ergodicity of Metropolis algorithms. Stochastic Processes and their Applications, 85:341–361, 2000.

- Jarner and Yuen [2004] Søren F. Jarner and Wai Kong Yuen. Conductance bounds on the convergence rate of Metropolis algorithms on unbounded state spaces. Advances in Applied Probability, 36:243–266, 2004.

- Johndrow et al. [2019] James E. Johndrow, Aaron Smith, Natesh Pillai, and David B. Dunson. MCMC for imbalanced categorical data. Journal of the American Statistical Association, 114(527):1394–1403, 2019.

- Jones and Hobert [2001] Galin L. Jones and James P. Hobert. Honest exploration of intractable probability distributions via Markov chain Monte Carlo. Statistical Science, 16:312–334, 2001.

- Jones and Hobert [2004] Galin L. Jones and James P. Hobert. Sufficient burn-in for Gibbs samplers for a hierarchical random effects model. The Annals of Statistics, 32(2):784 – 817, 2004.

- Kallenberg [2021] Olav Kallenberg. Foundations of Modern Probability. Springer, Cham, 3 edition, 2021.

- Kantorovich and Rubinstein [1957] L. V. Kantorovich and G. S. Rubinstein. On a function space in certain extremal problems. Dokl. Akad. Nauk USSR, 115(6):1058–1061, 1957.

- Kass et al. [1990] Robert E. Kass, Luke Tierney, and Joseph B. Kadane. The validity of posterior expansions based on Laplace’s method. Bayesian and Likelihood Methods in Statistics and Econometrics, pages 473–488, 1990.

- Łatuszyńki and Roberts [2013] K. Łatuszyńki and G. O. Roberts. CLTs and asymptotic variance of time-sampled Markov chains. Methodology and Computing in Applied Probability, 15:237–247, 2013.

- Lawler and Sokal [1988] Gregory F. Lawler and Alan D. Sokal. Bounds on the spectrum for Markov chains and Markov processes: A generalization of Cheeger’s inequality. Transactions of the American Mathematical Society, 309(2):557–580, 1988.

- Mengersen and Tweedie [1996] Kerrie L. Mengersen and Richard L. Tweedie. Rates of convergence of the Hastings and Metropolis algorithms. The Annals of Statistics, 24:101–121, 1996.

- Metropolis et al. [1953] N. Metropolis, A. W. Rosenbluth, M. N. Rosenbluth, A. H. Teller, and E. Teller. Equations of state calculations by fast computing machine. Journal of Chemical Physics, 21, 1953.

- Meyn and Tweedie [2009] Sean P. Meyn and Richard L. Tweedie. Markov Chains and Stochastic Stability. Cambridge University Press, USA, 2 edition, 2009.

- Miller [2021] Jeffrey W. Miller. Asymptotic normality, concentration, and coverage of generalized posteriors. Journal of Machine Learning Research, 22:1–53, 2021.

- Nesterov [2018] Yurii Nesterov. Lectures on Convex Optimization. Springer International Publishing, 2 edition, 2018.

- Peskun [1973] P. Peskun. Optimum Monte Carlo sampling using Markov chains. Biometrika, 89:745–754, 1973.

- Qin and Hobert [2019] Qian Qin and James P Hobert. Convergence complexity analysis of Albert and Chib’s algorithm for Bayesian probit regression. Annals of Statistics, 47:2320–2347, 2019.

- Rajaratnam and Sparks [2015] Bala Rajaratnam and Doug Sparks. MCMC-based inference in the era of big data: A fundamental analysis of the convergence complexity of high-dimensional chains. preprint arXiv:1508.00947, 2015.

- Roberts and Rosenthal [1997] Gareth O. Roberts and Jeffrey S. Rosenthal. Geometric ergodicity and hybrid Markov chains. Electronic Communications in Probability, 2:13–25, 1997.

- Roberts and Rosenthal [1998a] Gareth O. Roberts and Jeffrey S. Rosenthal. Optimal scaling of discrete approximations to Langevin diffusions. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 60(1):255––268, 1998a.

- Roberts and Rosenthal [1998b] Gareth O. Roberts and Jeffrey S Rosenthal. Optimal scaling of discrete approximations to Langevin diffusions. Journal of the Royal Statistical Society: Series B, 60:255–268, 1998b.

- Roberts and Rosenthal [2011] Gareth O. Roberts and Jeffrey S. Rosenthal. Quantitative non-geometric convergence bounds for independence samplers. Methodology and Computing in Applied Probability volume, 13:391––403, 2011.

- Roberts and Tweedie [1996a] Gareth O. Roberts and Richard L. Tweedie. Exponential convergence of Langevin distributions and their discrete approximations. Bernoulli, 2(4):341–363, 1996a.

- Roberts and Tweedie [1996b] Gareth O. Roberts and Richard L. Tweedie. Geometric convergence and central limit theorems for multidimensional Hastings and Metropolis algorithms. Biometrika, 83:95–110, 1996b.

- Roberts et al. [1997a] Gareth O. Roberts, A. Gelman, and W. R. Gilks. Weak convergence and optimal scaling of random walk metropolis algorithms. The Annals of Applied Probability, 7(1):110–120, 1997a.

- Roberts et al. [1997b] Gareth O. Roberts, Andrew Gelman, and W. R. Gilks. Weak convergence and optimal scaling of random walk Metropolis algorithms. The Annals of Applied Probability, 7(1):110 – 120, 1997b.

- Roberts et al. [1997c] Gareth O. Roberts, Andrew Gelman, and Walter R Gilks. Weak convergence and optimal scaling of random walk Metropolis algorithms. Annals of Applied Probability, 7:110–120, 1997c.

- Rosenthal [1995] Jeffrey S. Rosenthal. Minorization conditions and convergence rates for Markov chain Monte Carlo. Journal of the American Statistical Association, 90:558–566, 1995.

- Schmidler and Woodard [2011] Scott C. Schmidler and Dawn B. Woodard. Lower bounds on the convergence rates of adaptive MCMC methods. Technical Report, Duke University, 2011.

- Shun and McCullagh [1995] Zhenming Shun and Peter McCullagh. Laplace approximation of high dimensional integrals. Journal of the Royal Statistical Society. Series B (Methodological), 57(4):749–760, 1995.

- Tang and Reid [2021] Yanbo Tang and Nancy Reid. Laplace and saddlepoint approximations in high dimensions. preprint arXiv:2107.10885, 2021.

- Tierney [1994] Luke Tierney. Markov chains for exploring posterior distributions. The Annals of Statistics, 22:1701–1728, 1994.

- Tierney [1998] Luke Tierney. A note on Metropolis-Hastings kernels for general state spaces. The Annals of Applied Probability, 8:1–9, 1998.

- Tierney and Kadane [1986] Luke Tierney and Joseph B. Kadane. Accurate approximations for posterior moments and marginal densities. Journal of the American Statistical Association, 81(393):82–86, 1986.

- Tierney et al. [1989] Luke Tierney, Robert E. Kass, and Joseph B. Kadane. Approximate marginal densities of nonlinear functions. Biometrika, 76(3):425–433, 1989.

- Vaart [1998] A. W. van der Vaart. Asymptotic Statistics. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, 1998.

- Vats et al. [2022] D. Vats, F. B. Gonçalves, K. Łatuszyńki, and G. O. Roberts. Efficient Bernoulli factory Markov chain Monte Carlo for intractable posteriors. Biometrika, 109:369–385, 2022.

- Vats et al. [2019] Dootika Vats, James M. Flegal, and Galin L. Jones. Multivariate output analysis for Markov chain Monte Carlo. Biometrika, 106:321–337, 2019.

- Villani [2003] Cédric Villani. Topics in Optimal Transportation. Graduate studies in mathematics. American Mathematical Society, 2003.

- Villani [2009] Cédric Villani. Optimal Transport: Old and New. Springer Berlin, Heidelberg, 1 edition, 2009.

- Wang [2022] Guanyang Wang. Exact convergence analysis of the independent Metropolis-Hastings algorithms. Bernoulli, 28(3):2012 – 2033, 2022.

- Wang and Roy [2018] Xin Wang and Vivekananda Roy. Geometric ergodicity of Pólya-gamma Gibbs sampler for Bayesian logistic regression with a flat prior. Electronic Journal of Statistics, 12(2):3295 – 3311, 2018.

- Woodard et al. [2009] Dawn Woodard, Scott Schmidler, and Mark Huber. Sufficient conditions for torpid mixing of parallel and simulated tempering. Electronic Journal of Probability, 14:780 – 804, 2009.

- Woodard [2015] Dawn B. Woodard. A lower bound on the mixing time of uniformly ergodic Markov chains in terms of the spectral radius. preprint arXiv:1405.0028, 2015.

- Yang and Rosenthal [2017] Jun Yang and Jeffrey S. Rosenthal. Complexity results for MCMC derived from quantitative bounds. preprint arXiv:1708.00829, 2017.

- Yang et al. [2016] Yun Yang, Martin J. Wainwright, and Michael I. Jordan. On the computational complexity of high-dimensional Bayesian variable selection. Annals of Statistics, 44:2497–2532, 2016.

- Zellner [1986] Arnold Zellner. On assessing prior distributions and Bayesian regression analysis with g-prior distributions. Bayesian Inference and Decision Techniques: Essays in Honor of Bruno de Finetti, pages 233–243, 1986.

- Zhuo and Gao [2021] Bumeng Zhuo and Chao Gao. Mixing time of Metropolis-Hastings for Bayesian community detection. Journal of Machine Learning Research, 22(10):1–89, 2021.

Appendix A Proofs for Section 3

Proof of Theorem 1.

Fix and let . Then

Applying this recursively we obtain for

and, since is a Lebesgue density on , .

Let be the set of functions . Notice that and, since is a Lebesgue density on , . Thus,

∎

Proof of Proposition 2.

Fix . By regularity of [29, Lemma 1.36], we can find a sequence of open balls with radius centered at such that

We can choose large enough so that . Since and , then by assumption on the support of and since is strictly positive, then

For , and so,

| (4) |

Choose a sequence such that

Since , then . By upper semicontinuity of and taking the limit superior of (4), we have

Since this holds for every , the desired result follows by taking the infimum. ∎

Appendix B Proofs for Section 4

Proof of Proposition 3.

For all , ,

and hence

| (5) |

∎

Proof of Proposition 4.

By the subgradient inequality [38, Corollary 3.2.1], for every and ,

Thus,

and a routine calculation involving completing the square yields the claim. ∎

Proof of Proposition 5.

To apply Proposition 4, it will be shown that with probability 1, for sufficiently large , the target density is strongly convex.

Proof of Proposition 6.

Take sufficiently large so that the each of the assumptions hold. After changing the variables, obtain the decomposition

| (6) | ||||

| (7) |

Consider the first integral (6). Since the closed ball is convex, for all , by the subgradient inequality [38, Lemma 3.2.3],

This implies

Consider the second integral (7). We have

Combining these results,

Since ,

The desired result follows at once. ∎

Proof of Theorem 3.

The proof will show the conditions of Proposition 6 hold with probability for large enough . Using Assumption 1, with probability , assume is sufficiently large so that the posterior density and the MLE exist. Define

and write where . The first step is to develop sufficient curvature of the target density at . Denote the th derivative matrix or tensor of the function by . Recall that is the sigmoid function. For every ,

and

Since with probability , by the strong law of large numbers [17, Theorem 10.13], almost surely,

By Assumption 4, for any , , with probability ,

Since expectations preserve strict inequalities, there is a sufficiently small so that for any , ,

Combining these results, for all , with probability ,

for all sufficiently large . By Assumption 3, with probability and , so by the mean value theorem, almost surely,

For all , with probability , for all sufficiently large,

| (8) |

For the remainder of this argument, assume is sufficiently large so that (8) holds with probability and the remainder of the proof is taken to hold with probability without reference. Since , for all and ,

It is immediate that [4, Proposition 1 (6)] for and all ,

Since closed balls are convex, is strongly convex on the closed ball [38, Theorem 2.1.11]. Thus, the local strong convexity condition (1) in Proposition 6 holds.

Since [4, Proposition 1 (3)]

Using (8) and the fact that , obtain, for all with ,

Hence, for all with ,

Thus, for , the strict optimality condition (2) in Proposition 6 holds.

The required control of the integral (3) in Proposition 6 also holds since

∎

Appendix C Proofs for Section 5

Proof of Theorem 4.

We will first construct a suitable Lipschitz function. Fix , and fix . Define the function by . We have for every ,

Therefore, is a bounded Lipschitz function with respect to the distance and the Lipschitz constant is . By assumption there exists such that . Then, using the fact that , we obtain

| (9) |

Fix a positive integer . Then, for each and each , we obtain the lower bound

We now apply this lower bound multiple times:

| (10) |

The final step follows from the fact that . Combining (9) and (10), we then have the lower bound,

| (11) |

The case where is trivial so we assume this is finite. We then have by the Kantovorich-Rubinstein theorem [62, Theorem 1.14] and the lower bound in (11),

If , then taking the limit of , completes the proof. Suppose then that . Maximizing this lower bound with respect to yields . We then have

This completes the proof for the norm and by assumption, .

Finally, let be a coupling for and . Using Hölder’s inequality [17, Theorem 6.2] with ,

Taking the infimum over completes the proof. ∎

Proof of Proposition 8.

It will suffice to show (ii) implies (i) [18, Theorem 2.1]. Condition (ii) implies convergence in the bounded Lipschitz norm, that is,

The following proof is similar to that of an existing result [22, Proposition 2.8]. Let and let be a non-negative, bounded, Lipschitz with Lispchitz constant . We can assume on some positive probability of so that . Then we can define so that . The function is Lipschitz since for ,

Define the probability measure by and so . We have constructed so that

By (ii), there is a constant such that

By reversibility, . We then have

Now let be a bounded, Lipschitz function with Lipschitz constant . Denote the positive and negative parts of by . There are then constants such that

This holds for arbitrary and so applying [22, Lemma 2.9],

Now let be a bounded, lower semicontinuous function with . The approximation is Lipschitz continuous, uniformly bounded and pointwise. Now by the dominated convergence theorem [17, Theorem 2.24], pointwise. By the dominated convergence theorem and since is bounded and Lipschitz,

Now let with . By [29, Lemma 1.37], we can choose a sequence of bounded, continuous functions converging to in . By reversibility and Jensen’s inequality,

So, if in , then in as well. Therefore, since is bounded and lower semicontinuous, after taking limits, we conclude

The condition can be extended to all of by shifting and thus this holds for all of . ∎