Bivariate compound Poisson risk processes with shocks

(Working version)

Pavlina K. Jordanova

Faculty of Mathematics and Informatics, Konstantin Preslavsky University of Shumen,

115 ”Universitetska” str., 9712 Shumen, Bulgaria.

Corresponding author: pavlina_kj@abv.bg Evelina Veleva

Department of Applied mathematics and Statistics, ”Angel Kanchev” University of Ruse, Bulgaria. Kosto Mitov

Department of Medical Physics, Biophysics, Pre-clinical and Clinical Sciences, Medical University - Pleven, Bulgaria.

Abstract

Contemporary insurance theory is concentrated on models with different types of polices and shock events may influence the payments on some of them. Jordanova [7] considered a model where a shock event contributes to the total claim amount with one and the same value of the claim sizes to different types of polices. Jordanova and Veleva [8] went a step closer to real life situations and allowed a shock event to cause different claim sizes to different types of polices. In that paper the counting process is assumed to be Multinomial. Here it is replaced with different independent homogeneous Poison processes. The bivariate claim counting process is expressed in two different ways. Its marginals and conditional distributions are totaly described. The mean square regression of these processes is computed. The Laplace-Stieltjes transforms and numerical characteristics of the total claim amount processes are obtained. The risk reserve process and the probabilities of ruin in infinite time are discussed. The risk reserve just before the ruin and the deficit (or the severity) at ruin are thoroughly investigated in case when the initial capital is zero. Their means, probability mass functions and probability generating functions are obtained.

Although the model is constructed by a multivariate counting processes, along the paper it is shown that the total claim amount process is stochastically equivalent to a univariate compound Poisson process. These allows us to reduce the considered risk model to a Cramer-Lundberg risk model, to use the corresponding results and to make the conclusions for the new model. Analogous results can be obtained for more types of polices and more types of shock events.

The results are applied in case when the claim sizes are exponentially distributed.

Stochastically equivalent models could be analogously constructed in queuing theory.

1 DESCRIPTION OF THE MODEL AND ITS RELATIONS WITH PREVIOUSLY INVESTIGATED MODELS

The origin of modeling of random processes with common shocks is usually related with the names of Marshal and Olkin [14, 15] or Mardia [13]. They construct different bivariate models with dependent coordinates, where the dependence is caused by a joint summand, or a joint term in the maxima or the minima. The results could be easily transferred to random processes with independent increments. Cossette and Marceau [3] apply such results in risk theory. Jordanova [7] uses merging of compound Poisson processes and investigates a particular case of the model, defined in this work. The difference is that, in that work, in a fixed point of time, if there is a shock event it affects different types of contracts via one and the same claim size. In the insurance model investigated in Jordanova and Veleva [8] the form of the dependence is improved. The claim sizes caused by one and the same shock event on different types of polices can be different. However, in that paper, the counting processes of claim arrivals of different types of polices are described via a Multinomial processes. Here this Multinomial process is replaced with different independent homogeneous Poisson processes (HPPs) and the form of the dependence is the same. More precisely, let , , be mutually independent HPPs with parameters correspondingly , and . By assumption .

The counting processes and of both types of claims are in generally dependent HPP with common shocks, and for all

(1)

Therefore, is a HPP with parameter and is a HPP with parameter .

The total claim amount process is such that for all ,

(2)

(3)

The sequences and , , are mutually independent.

The processes and are in generally dependent.

The definitions of , and mean that we allow the claims to be of two mutually exclusive different types and shock events (like car-crashes) may cause possibly different payments in both polices. The process describes the counts of shock events.

In (3) for any fixed the random variables (r.vs.) are independent identically distributed (i.i.d.) with cumulative distribution function (c.d.f.) . The sequences , and are mutually independent. Without lost of generality the almost sure strictly positive r.v. describes the -th claim amount, () of a certain type , . If the distribution of the claim sizes has mass at zero, the parameters of the corresponding counting HPPs, participating in and , defined in (3), can be changed, and the model can be reduced to the considered here one.

A natural example of an insurance interpretation of this model is as follows. For , is the part of the claim size which is due to the customer for -th standard insurance policy of type exclusively the common shocks. Analogously for . The r.v. models the part of the claim size which have to be paid to the customer due to some common shock. Jordanova and Veleva [8] give and example when the random elements with describe health insurances, is for car insurance. Then, is the total claim amount up to time , which is due to customers for having some healthy problems, not related with car-crashes. The r.v. models the total claim amount up to time , which is due to healthy problems, caused by car-crashes. The r.v. is for the total claim amount up to time , which is due to some car problems which are not related with car-crashes, for example car-thefts. And finally, the r.v.

is the total claim amount up to time , which is due to some car problems which are related with car-crashes.

Therefore, the random process is the total claim amount processes for the insurance events caused by ”healthy problems”, is the amount paid to customers for events caused by ”problems with cars”.

As usually the risk reserve process is defined via the equality

(4)

where is the initial capital and is the premium income rate per unit time.

The time of ruin when the initial capital is will be denoted by

(5)

The probability for ruin in ”infinite horizon” and initial capital is

(6)

and the corresponding survival probability is .

All random elements discussed here are assumed to be measurable with respect to one the same probability space with natural filtration born by the considered processes. The letter is a notation for probability generating function (p.g.f.). Analogously, the letter means Laplace-Stieltjes transform (LST).

2 THE BIVARIATE COUNTING PROCESS

Poisson and compound Poisson processes are very well investigated in the scientific literature. See for example Kingman [9], or Sundt and Vernic [17]. In multivariate case we have two types of compound Poisson processes. The I type means ”with equal number of summands”. The type ”II” is its opposite. Let us now derive the compound Poisson presentation of the first type of the bivariate counting process , defined in (1). In order to formulate our results we will define a random vector with probability mass function (p.m.f.)

(7)

and zero otherwise. Here , , and . By assumption the random vectors are i.i.d. with p.m.f. (7).

Denote by, a HPP with , and parameter , and by

(8)

Here and and are independent. In our example the random process counts the number of the insurance events caused by healthy problems. The random process counts the number of the insurance events caused by problems with cars.

In the next theorem we show that the bivariate counting process

is a particular case of a multivariate homogeneous in time compound Poisson process with equal number of summands, i.e. of type I, in the sense of Sundt and Vernic [17, 18].

Theorem 1. The bivariate counting processes and coincide in the sense of their finite dimensional distributions.

Proof: The processes and have homogeneous and independent additive increments and they start from the coordinate beginning. Therefore, in order to prove their stochastic equivalence it is enough to prove equality of their univariate time intersections. Due to the uniqueness of the correspondence between the probability laws and their p.g.fs. it is enough to derive equality between the p.g.fs.

The definition of p.g.fs., (1), the multiplicative property of p.g.f. and the well-known formula for the p.g.f. of the Poisson distribution entail that for all ,

By the definition (30), the formula for double expectations and the definition of Poisson distribution

By the multiplicative property of p.g.fs. and the fact that the random vectors are i.i.d. we have

(9)

Now, by using (7) we obtain the p.g.f. of .

Therefore, the fact that is a HPP with parameter and the Maclaurin series leads us to

which is exactly . The uniqueness of the correspondence between p.g.fs. and the probability distribution completes the proof.

Note 1. For all the distribution of the time intersections of the bivariate counting process , defined in (1) are determined via the following p.g.fs.,

They are called bivariate Poisson distributions, and for any fixed , they are very well investigated in the scientific literature. See for example Kocherlakota and Kocherlakota [12] who show that for ,

and this probability mass function (p.m.f.) is equal to otherwise.

Thus, for or , and

and this p.m.f. is equal to otherwise.

Their correlation does not depend on and is

Theorem 2. For or , and the mean square regression of the bivariate couunting processes is

Proof: Without lost of generality let us assume that . Then,

Note 2. The process is a Markov chain with -matrix

It is a univariate compound Poisson process. For all , its time intersections satisfy the equalities

It is determined via the distribution of its time intersections which have the following p.g.fs.,

It is easy to see that as far as and , thus

3 STOCHASTICALLY EQUIVALENT PRESENTATIONS OF THE TOTAL CLAIM AMOUNT PROCESS

The process has a compound Poisson of type I presentation.

Theorem 3. The bivariate total claim amount process , described in (3) is a bivariate compound Poisson process of type I. It is stochastically equivalent (in the sense of finite dimensional distributions) to the process , where

(10)

Here , , is a vector with distribution (7), and is a HPP with parameter . The random process , and the sequences , , , and are mutually independent.

Proof: Consider . The definition of Laplace-Stieltjes transforms (LSTs), (3), the multiplicative property of LSTs, and the formula for the LSTs of compound Poisson distribution entail

In the last equality we have used the definitions (10). The uniqueness of the correspondence between the probability laws and their LSTs entails the equality in distribution of the univariate time intersections of , described in (3), and those of the process . These processes have homogeneous and independent additive increments and they start from the coordinate beginning. Therefore, the last entails their stochastic equivalence in the sense of finite dimensional distributions.

Corollary 1. For all the distribution of the time intersections , of the bivariate process defined in (3) are determined via the following LSTs,

i)

If , , then, ,

ii)

If , , then,

iii)

;

iv)

v)

The correlation does not depend on . More precisely

Corollary 2. The time intersections

of the compound Poisson process , possess the following properties:

i)

their distributions are determined via the following Laplace-Stieltjes transforms

ii)

;

iii)

4 STOCHASTICALLY EQUIVALENT RISK MODELS

In this section, first it is shown that the risk reserve process , defined in (4), is a classical compound Poisson risk process. Then, by using the results about the Cramer-Lundberg risk model, the corresponding characteristics of and probabilities for ruin in infinite time are obtained. More precisely,

Corollary 2 entails that the risk process, described in (4) is stochastically equivalent to the process

(11)

where , and . Let us denote by . By assumption . Then,

By using these notations we obtain the well-known formula for the safety loading in the Cramer-Lundberg risk model,

(12)

The corresponding net profit condition is

(13)

For the general results about the Cramer-Lundberg risk model see for example Rolski et al. [16], Asmussen and Albrecher [1], Grandell [6] or Gerber [4] among others.

If the net profit condition (13) is satisfied, then the Cramer-Lundberg presentation (11) of the risk process allows us to conclude that it possesses the following properties.

If we denote by , by , , and by , then

, and

Now, we have the compound geometric form, for the Laplace-Stieltes transform of . For ,

(16)

Given that is finite, let us denote by the absolute value of the deficit at ruin. This r.v. has an integrated tail distribution

with mean value

and the Laplace-Stieltes transform

As far as the distribution of coincides with the integrated tail distribution of the mixture of the distributions of , and , it is a mixture of the corresponding integrated tail distributions of , and . The corresponding weights are

Theorem 4. If , , and the random vector has the distribution

(17)

then the integrated tail distribution of is the mixture with c.d.f.

The last means that if the r.vs. have the integrated tail distribution correspondingly of , , and , and if the r.vs. are independent of , then

The proof follows by the total probability formula.

In this way

where the r.vs. are independent and identically distributed, and they are independent on . The r.v. is Geometrically distributed over the natural numbers (, ), with parameter

Now, we have obtained the Beekmans convolution series [2] or Pollaczek-Khinchin formula [11]

The expected time of ruin, given that the ruin occur and the initial capital is is

The joint distribution of the deficit at ruin and - the risk surplus just before the ruin, when is

In case when the initial capital is positive, when we replace c.d.f. of in the well known formulae for , see for example Gerber and Shiu (1997) [5] or Klugman, Panjer and Willmot (2012) [10],

By the main properties of the Cramer-Lundberg risk model, which could be found in any textbook on Risk theory, we have that if the Cramer-Lundberg exponent exists, which in this case is the same, as if a positive solution of the equation

exists, then

.

If additionally

then

If the distributions of , , , and are all subexponential and , , , and are all finite, then

5 Exponential claim sizes

Let us now suppose that , are independent and exponentially distributed with means correspondingly , . Then,

Now, we have the compound geometric form, for the Laplace-Stieltes transform (LST) of . For ,

(23)

As far as the integrated tail distribution of the Exponential distribution is again Exponential distribution with the same parameter, the integrated tail distribution of has a LST

(24)

(25)

(26)

Now we need to observe only that

is the LST of the integrated tail distribution of . Let us suppose that a r.v. has such probability law, and is independent of and . Then

The mean value of is,

In this case it is a mixture of two Exponential and the integrated tail distribution of a Hypoexponential distribution. Moreover,

If , then for ,

and this c.d.f. is equal to , otherwise. The corresponding probability density function is

If , then has the integrated tail distribution of r.v. More precisely for ,

and this c.d.f. is equal to , otherwise.

The last means that when ,

where

(30)

with p.d.f.

, when and , otherwise,

and with p.d.f. , when and , otherwise.

Thus, when ,

(32)

This is equivalent to

(33)

where the r.v. is Geometrically distributed over the natural numbers (, ), with parameter

, are i.i.d. random vectors with distribution defined in (17) with corresponding , and , defined in (19). All these random elements are assumed to be independent.

If , then, for ,

and , otherwise.

This is equivalent to

(35)

where the r.v. is Geometrically distributed over the natural numbers, with parameter

, are i.i.d. random vectors with distribution defined in (17) with corresponding , and , defined in (19). For , . The last vector is defined in (30). For , , and . All these random elements are assumed to be independent.

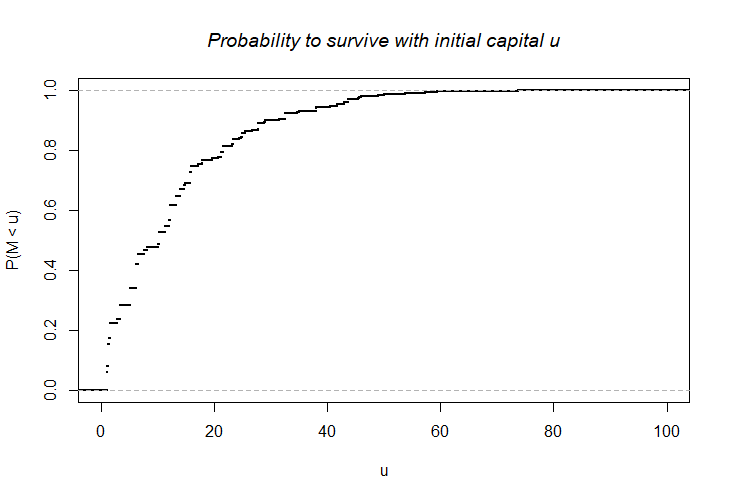

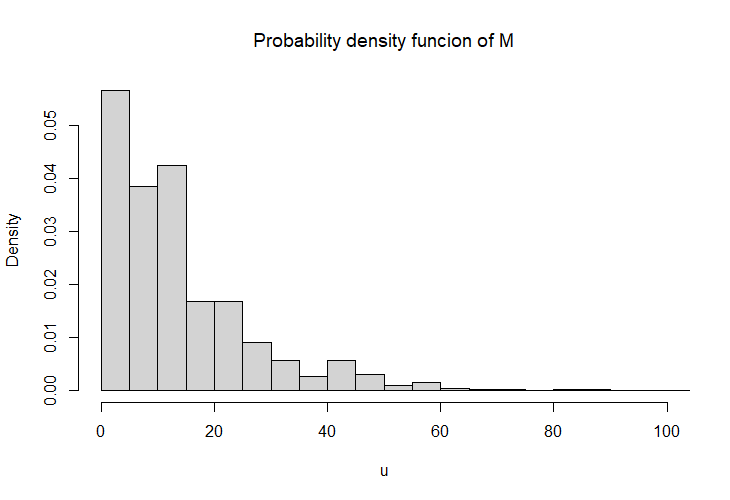

Formula (35) allows us to simulate independent observations on without generating all sample paths of the risk process and to plot the probability to survive, which is actually estimated via the empirical c.d.f. of . Moreover, we can estimate also its derivative, which coincides with the probability density function of .

Such simulation study was performed with sample size and parameters , , , , , , and . Then, , and . Both plots are given on Figure 1.

Figure 1: Estimators of the probability to survive (left) and its derivative (right)

6 CONCLUSIONS

Analogous conclusions could be done for mathematical models of insurance businesses with more types of claims, more types of polices, and more types of shock event. The idea is to reduce them to the classical compound Poisson risk model.

Although the model is constructed by a multivariate counting processes, along the paper it is shown that the total claim amount process is stochastically equivalent to a univariate compound Poisson process. These allows us to reduce the considered risk model to a Cramer-Lundberg risk model, to use the corresponding results and to make the conclusions for the new model.

These results give us a different approach for estimation of the probability of ultimate ruin and its derivative.

Analogous results can be applied in queuing theory.

7 ACKNOWLEDGMENTS

The first author is partially supported by the project RD-08-144/01.03.2022 from the Scientific Research Fund in Konstantin Preslavsky University of Shumen, Bulgaria. Evelina Veleva thanks to the project No 2022-FNSE-04, financed by ”Scientific research” Fund of Ruse University.

References

[1] Asmussen, S., Albrecher, H. Ruin probabilities, Advansed Series on Statistical Science & Applied Probability, vol. 14, (2010) World Scientific.

[2] Beekman, J.A., Collective risk results, Transactions of the Society of Actuaries, vol.20, pp. 182–199, (1968).

[3] Cossette, H., Marceau, H., The discrete-time risk model with correlated classes of business, Insurance: Mathematics and Economics, vol.26(2), pp. 133–149, (2000).

[4] Gerber, H.U., An introduction to mathematical risk theory, SS Heubner Foundation Monograph Series, Monograph No. 8, (1979) University of Michigan.

[5] Gerber, H.U., Shiu, E.S.W., The joint distribution of the time of ruin, the surplus immediately before ruin, and the deficit at ruin, Insurance: Mathematics and Economics, vol. 21(2), pp. 129-137 (1997).

[6] Grandell, J., Aspects of risk theory, Springer Series in Statistics, (1992) Springer Verlag.

[7] Jordanova, P., Merging of bivariate Compound Poisson risk processes with shocks, MATTEX 2018 Conference proceedings,

vol. 1, pp. 49–56, (1988).

[8] Jordanova, P., Veleva, E., Merging of bivariate Binomial risk processes with shocks, AIP Conference Proceedings,

vol. …, pp. …–…, (2021).

[9] Kingman, J. F. C., Poisson Processes, Oxford studies in probability, (1991) Clanderon press, Oxford.

[10] Klugman, S. A., Pnjer, H., H., and Willmot, G. E., Loss models: from data to decision, (2012) John Wiley & Sons.

[11] Khinchine, A.Y., Mathematical theory of a stationary queue, Matematicheskii Sbornik, vol. 39(4):7384 (1932) (in russian).

[12] Kocherlakota, S., Kocherlakota, K., Bivariate Discrete Distributions, (1992) Marcel Dekker, New York.

[13] Mardia, K., V., Families of Bivariate Distributions, (1970) Charles Griffin and Sons, London.

[14] Marshall, A.W., Olkin, I., A multivariate exponential distribution, Journal of the the Americn Statistical Association,

vol.62, pp. 30–44, (1967).

[15] Marshall, A.W., Olkin, I., Families of multivariate distributions, Journal of the the Americn Statistical Association,

vol.83, pp. 834–841, (1988).

[16] Rolski, T., Schmidli, H., Schmidt, V., Teugels, J., Stochastic processes for insurance and finance, vol. 505 (1998) John Wiley and Sons.

[17] Sundt, B., Vernic, R., Recursions for convolutions and compound distributions with insurance applications, (2009) Springer Science & Business Media.

[18] Vernic, R., On the Evaluation of the Distribution of a General Multivariate Colleacite Model: Recursions versus Fast Fourier Transform, Risks, vol.6(3), 87, pp. 1–14, (2018), MDPI.