Identification and estimation of causal effects in the presence of confounded principal strata

Abstract

The principal stratification has become a popular tool to address a broad class of causal inference questions, particularly in dealing with non-compliance and truncation-by-death problems. The causal effects within principal strata which are determined by joint potential values of the intermediate variable, also known as the principal causal effects, are often of interest in these studies. Analyses of principal causal effects from observed data in the literature mostly rely on ignorability of the treatment assignment, which requires practitioners to accurately measure as many as covariates so that all possible confounding sources are captured. However, collecting all potential confounders in observational studies is often difficult and costly, the ignorability assumption may thus be questionable. In this paper, by leveraging available negative controls that have been increasingly used to deal with uncontrolled confounding, we consider identification and estimation of causal effects when the treatment and principal strata are confounded by unobserved variables. Specifically, we show that the principal causal effects can be nonparametrically identified by invoking a pair of negative controls that are both required not to directly affect the outcome. We then relax this assumption and establish identification of principal causal effects under various semiparametric or parametric models. We also propose an estimation method of principal causal effects. Extensive simulation studies show good performance of the proposed approach and a real data application from the National Longitudinal Survey of Young Men is used for illustration.

Keywords: Causal Inference; Negative Control; Non-compliance; Principal Stratification; Unmeasured Confounding.

1 Introduction

Many scientific problems are concerned with evaluating the causal effect of a treatment on an outcome in the presence of an intermediate variable. Direct comparisons conditional on observed values of the intermediate variable are usually not causally interpretable. Frangakis and Rubin, (2002) propose the principal stratification framework and define principal causal effects that can effectively compare different treatment assignments in such settings. The principal stratification is defined by joint potential values of the intermediate variable under each treatment level being compared, which is not affected by treatment assignment, and hence it can be viewed as a pretreatment covariate to classify individuals into subpopulations. Principal causal effects that are defined as potential outcome contrasts within principal strata thus exhibit clear scientific interpretations in many practical studies (VanderWeele,, 2011). For instance, in non-compliance problems, the intermediate variable is the actual treatment received, the principal stratification represents the compliance status, and the treatment assignment plays the role of an instrumental variable in identifying the complier average causal effect (Angrist et al.,, 1996). In truncation-by-death problems, the intermediate variable denotes survival status, and a meaningful parameter termed survivor average causal effect is defined as the effect among the subgroup who would survive under both treatment levels (Rubin et al.,, 2006; Zhang et al.,, 2009; Ding et al.,, 2011).

Analysis of principal causal effects from observed data is challenging, because principal stratification is often viewed as an unobserved confounder between the intermediate and outcome variables. Most works in the literature rely on the ignorability of treatment assignment, which states that the distributions of potential values of intermediate and outcome variables do not vary across the treatment assignment given observed covariates. This assumption essentially requires that observed covariates account for all possible confounding factors between the treatment and post-treatment variables. Since the principal causal effects are defined on the latent principal strata, one can only establish large sample bounds or conduct sensitivity analysis for principal causal effects under the ignorability assumption (Zhang and Rubin,, 2003; Lee,, 2009; Long and Hudgens,, 2013), but fails to obtain identifiability results without additional assumptions. Previous literature has used an auxiliary variable that satisfies some conditional independence conditions to address the identification issues (Ding et al.,, 2011; Jiang et al.,, 2016; Ding and Lu,, 2017; Wang et al.,, 2017; Luo et al.,, 2021). However, as can happen in observational studies, one may not sufficiently collect the pretreatment covariates. The existence of unmeasured variables may render the ignorability assumption invalid and thus the traditional causal estimates in principal stratification analysis can be biased.

As far as we know, there has not been much discussion on principal causal effects when the ignorability assumption fails. Several authors have considered the setting where the potential values of the intermediate variable are correlated with the treatment assignment even after conditioning on observed covariates. In other words, the treatment and the intermediate variable are confounded by unmeasured factors in this setting. Schwartz et al., (2012) present model-based approaches for assessing the sensitivity of complier average causal effect estimates in non-compliance problems when there exists unmeasured confounding in the treatment arms. Kédagni, (2021) discusses similar problems and provides identifiability results by using a proxy for the confounded treatment assignment under some tail restrictions for the potential outcome distributions. Deng et al., (2021) study truncation-by-death problems and establish identification of the conditional average treatment effects for always-survivors given observed covariates by employing an auxiliary variable whose distribution is informative of principal strata. However, because the conditional distributions of principal strata given covariates are not identified, the survivor average causal effect is generally not identifiable in their setting.

To overcome these limitations, we establish identification of principal causal effects by leveraging a pair of negative control variables. In the absence of intermediate variables, many researchers have employed a negative control exposure and a negative control outcome to identify the average causal effects when unobserved confounders exist (Miao et al.,, 2018; Shi et al.,, 2020; Miao et al.,, 2020; Cui et al.,, 2020). However, the principal causal effects may be of more interest in the presence of an intermediate variable. For instance, in truncation-by-death problems, individuals may die before their outcome variables are measured, and hence the outcomes for dead individuals are not well defined. Then the survivor average causal effect is more scientifically meaningful in these studies (Rubin et al.,, 2006; Tchetgen Tchetgen,, 2014). While the identification and estimation of average causal effects within the negative control framework have been well studied in the literature, it remains uncultivated in studies where an intermediate variable exists and principal causal effects are of interest.

In this paper, we develop identification and estimation of principal causal effect in the presence of unmeasured confounders. Specifically, we first introduce a confounding bridge function that links negative controls and the intermediate variable to identify proportions of the principal strata. We then establish nonparametric identification of principal causal effects by assuming that the negative controls have no direct effect on the outcome. We next relax this assumption and show alternative identifiability results based on semiparametric and parametric models. Finally, we provide an estimation method and discuss the asymptotic properties. We evaluate the performance of the proposed estimator with simulation studies and a real data application.

2 Notation and assumptions

Assume that there are individuals who are independent and identically sampled from a superpopulation of interest. Let denote a binary treatment assignment with indicating treatment and for control. Let denote an outcome of interest, and let denote a binary intermediate variable. Let denote a vector of covariates observed at baseline. We use the potential outcomes framework and make the stable unit treatment value assumption; that is, there is only one version of potential outcomes and there is no interference between units (Rubin,, 1990). Let and denote the potential values of the intermediate variable and outcome that would be observed under treatment . The observed values and are deterministic functions of the treatment assignment and their respective potential values: and .

Frangakis and Rubin, (2002) define the principal stratification as joint potential values of the intermediate variable under both the treatment and control. We denote the basic principal stratum by and it can be expressed as . Since each of the potential values has two levels, there are four different principal strata in total. For simplicity, we refer to these principal strata, namely, as never-takers (), compliers (), always-takers (), and defiers (), respectively. The causal estimand of interest is the principal causal effect, i.e.,

The principal causal effect conditional on a latent variable is not identifiable without additional assumptions. Here we do not impose the exclusion restriction assumption (Angrist et al.,, 1996) that requires no individual causal effect on the outcome among the subpopulations and , because in many settings with intermediate variables, such as truncation-by-death or surrogate problems (Gilbert and Hudgens,, 2008), the very scientific question of interest is to test whether the principal causal effect or is zero. Under this setup, the identification of in the literature often relies on the following monotonicity assumption.

Assumption 1 (Monotonicity).

.

Monotonicity rules out the existence of the defier group . This assumption may be plausible in some observational studies. For example, in studies evaluating the effect of educational attainment on future earnings, a subject living near a college is likely to receive a higher educational level. The second commonly-used assumption is the treatment ignorability assumption: . This assumption entails that the baseline covariates control for all confounding factors between the treatment and post-treatment variables. However, the ignorability fails in the presence of unmeasured confounding. Let denote an unobserved variable, which together with observed covariates , captures all potential confounding sources between the treatment and variables . We impose the following latent ignorability assumption.

Assumption 2 (Latent ignorability).

(i) ; (ii) .

The type of confounding considered in Assumption 2(i) is termed -confounding by Schwartz et al., (2012). The presence of the unmeasured variable in this assumption brings about dramatic methodological changes and important technical challenges to principal stratification analysis. For example, when the traditional ignorability assumption holds, the inequality can be used to falsify the monotonicity assumption. However, if exists, it is no longer possible to empirically test monotonicity using this inequality. In addition, if we define principal score as the proportion of the principal stratum given observed covariates (Ding and Lu,, 2017), namely, , the presence of impedes identification of . Assumption 2(ii) means that the confounding factors between the treatment and the outcome are fully characterized by the latent principal stratification and observed covariates (Wang et al.,, 2017). Assumption 2 has also been considered by Kédagni, (2021) and Deng et al., (2021).

We next discuss identification of under Assumptions 1 and 2. For simplicity, we define , and hence . It suffices to identify for the identification of . Let . Then under Assumption 2(ii), we have

| (1) |

It can be seen that the identification of depends on that of and . Under Assumptions 1 and 2(i), we have that

where . Because is unobserved, the principal scores in the above equations cannot be identified without additional assumptions. As for the conditional outcome means , only and can be identified under Assumptions 1 and 2(ii) by and . However, the identifiability of other conditional outcome means is not guaranteed, because the observed data and are mixtures of two principal strata:

| (2) | |||

where , , and . In later sections, the conditional probabilities of principal strata given only a subset of covarites may be of interest, and we simply denote them by replacing with in the original notations. For example, . Other notations, such as and , can be similarly interpreted. Due to the presence of unobserved confounders , the weights in (2) are no longer identifiable, which complicates the identification and differs from most of existing results in the literature. In such a case, the large sample bounds or sensitivity analysis for these conditional outcome means cannot be easily obtained without further assumptions and it would be even more difficult to obtain their identifiability results. In the following section, we discuss how to establish the identifiability of principal causal effects based on auxiliary variables.

3 Identification

3.1 Nonparametric identification using a pair of negative controls

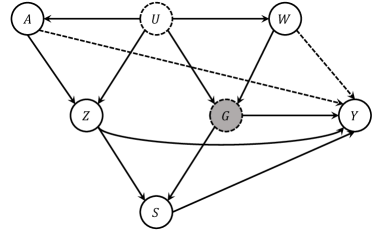

In this section, we establish a nonparametric identification result for principal causal effects through a pair of negative control variables when the ignorability assumption fails. Motivated from the proximal causal inference framework for identifying average treatment effects (Miao et al.,, 2018; Shi et al.,, 2020; Miao et al.,, 2020; Cui et al.,, 2020), we assume that the covariates can be decomposed into such that serves as a negative control exposure, serves as a negative control intermediate variable and accounts for the remaining observed confounders. For convenience, we may use the notation and interchangeably below.

Assumption 3 (Negative control).

Assumption 4 (Confounding bridge).

There exists a function such that almost surely for all .

Assumption 3 implies that the variables are sufficient to account for the confounding between and . The negative control exposure does not directly affect either the intermediate variable or the negative control intermediate variable . Assumption 3 imposes no restrictions on - association or - association, and allows the two negative controls and to be confounded by the unmeasured variable . See Fig. 1 for a graphic illustration. The confounding bridge function in Assumption 4 establishes the connection between the negative control and the intermediate variable . Assumption 4 defines an inverse problem known as the Fredholm integral equation of the first kind. The technical conditions for the existence of a solution are provided in Carrasco et al., (2007). Since the principal stratum is a latent variable, Assumptions 3 and 4, which are used to control for unobserved confounding between treatment and intermediate variables, are not sufficient to nonparametrically identify principal causal effects. We thus impose the following conditional independence condition between the negative controls and potential outcomes given the latent variable and observed covariates .

Assumption 5.

.

Under Assumption 5, we can view the observed variables and as proxies of , the role of which resembles the usual instrumental variables that preclude direct effects on the outcome (Angrist et al.,, 1996); see Fig. 1 for an illustration. Similar assumptions have been widely used in principal stratification literature (Ding et al.,, 2011; Jiang et al.,, 2016; Wang et al.,, 2017; Luo et al.,, 2021). In the next subsection, we shall consider to relax this assumption based on semiparametric or parameric models.

Theorem 1.

Suppose that Assumptions 1, 2(i), 3 and 4 hold. Then the conditional probabilities of principal strata are identified by

| (3) |

Under additional Assumptions 2(ii) and 5, the principal causal effects are identifiable if for any , the functions in the following two vectors

| (4) |

are respectively linearly independent.

The identifiability result (3) in Theorem 1 links the confounding bridge function with the conditional probabilities of principal strata given observed variables . With an additional completeness condition, the bridge function in Assumption 4 can be equivalently characterized by a solution to an equation based on observed variables (see Lemma S2 in the supplementary materials). Note that Assumption 4 only requires the existence of solutions to the integral equation. Theorem 1 implies that even if is not unique, all solutions to Assumption 4 must result in an identical value of each conditional proportion of the principal stratification.

In the absence of unmeasured confounding, Ding et al., (2011) and Wang et al., (2017) use only one proxy variable whose distribution is informative of principal stratum to establish nonparametric identification. When the principal strata are confounded by the unmeasured variable , Theorem 1 shows that principal causal effects can also be identified with two proxy variables. The conditions in (4) are similar to the relevance assumption in instrumental variable analyses (Angrist et al.,, 1996), which requires the association between the negative control exposure and principal stratum . Because the weights ’s are identified according to (3), the linear independence conditions among functions in each vector of (4) are in principle testable based on observed data.

3.2 Identification under semiparametric or parametric models

In this section, we relax Assumption 5 to some extent and discuss the identifiability of principal causal effects under semiparametric or parametric models.

Assumption 6.

,

Assumption 6 is notably weaker than Assumption 5 by requiring only one substitutional variable for the principal stratum , which allows negative control exposure to directly affect the outcome. This is in parallel to the usual assumption for the identifiability of principal causal effects when unmeasured confounding is absent (Ding et al.,, 2011; Jiang et al.,, 2016; Wang et al.,, 2017; Luo et al.,, 2021). We consider a semiparametric linear model for to facilitate identification of principal causal effects under Assumption 6.

Theorem 2.

One may further relax Assumption 6 by considering the following model,

| (6) |

which allows the outcome to be affected by all observed covariates , including the negative control intermediate variable . The above semiparametric linear model (6) has also been considered in Ding et al., (2011) and Luo et al., (2021). As shown in the supplementary material, the parameters in (6) are identifiable under some regularity conditions. This means that we can identify the conditional outcome mean . However, since the proportions of principal strata are not identifiable under the assumptions in Theorem 2, the parameter expressed in (1) cannot be identified unless additional conditions exist. Below we consider parametric models that would make it possible to identify the principal causal effects even if Assumption 6 were violated.

Proposition 1.

As implied by the latent ignorability assumption, the association may occur in the presence of unobserved confounder , so the coefficient in the model for after (7) may not be zero. The ordinal model in (7) is compatible with monotonicity assumption and can be rewritten in the following form under this assumption:

| (8) |

where . In fact, we model the distribution of potential values of the intermediate variable using a generalized linear model, which is similar in spirit to the marginal and nested structural mean models proposed by Robins et al., (2000). Under such parametric models, Proposition 1 shows that we can identify the conditional proportions of the principal strata given all observed covariates. This is a stronger result than that in Theorem 1, where only the conditional proportions of principal strata given covariates are identifiable. With this result, we can consider another weaker version of Assumption 5, which is in parallel to Assumption 6.

Assumption 7.

.

This condition is similar to the “selection on types” assumption considered in Kédagni, (2021), which entails that the negative control exposure has no direct effect on the outcome . We next consider identification of principal causal effects under the ordinal model (7) and other various conditions.

Theorem 3.

Under Assumptions 1–4 and the model parameterization in Proposition 1, the following statements hold:

-

(i)

with additional Assumption 5, the principal causal effects are identified if for any , the functions in the vectors and are respectively linearly independent.

-

(ii)

with additional Assumption 6, the principal causal effects are identified if for any , the functions in the vectors and are respectively linearly independent.

-

(iii)

with additional Assumption 7, the principal causal effects are identified if for any , the functions in the vectors and are respectively linearly independent.

-

(iv)

with the additional model (6), the principal causal effects are identified if the functions in the vectors and are respectively linearly independent.

In contrast to Theorem 1, Theorem 3 shows that under the parametric models in Proposition 1, the principal causal effects are always identifiable as long as certain linear independence conditions are satisfied, albeit Assumption 5 may partially or completely fails. Besides, since the functions are identifiable based on Proposition 1, those linear independence conditions in Theorem 3 are testable from observed data.

4 Estimation

While the nonparametric identification results provide useful insight, nonparametric estimation, however, is often not practical especially when the number of covariates is large due to the curse of dimensionality. We consider parametric working models for estimation of principal causal effects in this section.

Model 1 (Bridge function).

The bridge function is known up to a finite-dimensional parameter .

Model 2 (Treatment and negative control intermediate variable).

The treatment model is known up to a finite-dimensional parameter , and the negative control intermediate variable model is known up to a finite-dimensional parameter .

Model 3 (Outcome).

The conditional outcome mean function is known up to a finite-dimensional parameter .

Note that in Model 3 should be compatible with the requirements in Theorems 1-3. For example, under the conditions in Theorem 1 or 3(i), we consider a parametric form for that is only related to the covariate , but should not be dependent on and . Given the above parameterizations in Models 1–3, we are now ready to provide a three-step procedure for estimation of the principal causal effects.

In the first step, we aim to estimate the conditional probabilities considered in Theorem 1. The expression in (3) implies that for estimation of , we only need to estimate the parameters and that are in the bridge function and negative control intermediate variable model , respectively. Under Assumptions 3, 4, and the completeness condition, we have the following equation (see Lemma S2 in the supplementary material for details):

We then obtain an estimator by solving the following estimating equations

| (9) |

where for some generic variable , and is an arbitrary vector of functions with dimension no smaller than that of . If the dimension of the user-specified function is larger than that of , we may adopt the generalized method of moments (Hansen,, 1982) to estimate . We next obtain the estimators and in Model 2 by maximum likelihood estimation. With the parameter estimates and , we can finally obtain the estimators based on (3). The calculation of the estimated probabilities involves integral equations with respect to the distribution , which may be numerically approximated to circumvent computational difficulties. Consequently, we have a plug-in estimator of defined in (2) and an estimator of as follows:

In addition, if the model assumptions in Proposition 1 hold, we can further estimate the conditional probabilities given fully observed covariates and ; the estimation details are relegated to the supplementary material for space cosiderations. As noted by Theorems 1–3, the estimation of principal causal effects requires different conditional probabilities of principal strata, depending on which assumptions are imposed. For example, Theorem 1 requires , whereas Theorem 3 requires . For simplicity, we denote these conditional probabilities by a unified notation with in Theorems 1–2 and in Theorem 3. The notations and are equipped with similar meanings.

In the second step, we aim to estimate the parameters for and in the outcome Model 3. To derive an estimator for , we observe the following moment constraints by invoking the monotonicity assumption:

| (10) | ||||

We emphasize here that the specifications of in Model 3 may not always depend on all the observed covariates due to identifiability concerns; see also the discussions below Model 3. With the above moment constraints, we can apply the generalized method of moments again to obtain a consistent estimator for . The estimation of is similar, because we have another pair of moment constraints:

| (11) | ||||

Finally, in view of (1), we can obtain our proposed estimator for the principal causal effect as follows:

Using empirical process theories, one can show that the resulting estimator is consistent and asymptotically normally distributed.

5 Simulation studies

We conduct simulation studies to investigate the finite sample performance of the proposed estimators in this section. We consider the following data-generating mechanism:

-

(a).

We generate covariates from

-

(b).

We generate the binary treatment from a Bernoulli distribution with .

-

(c).

Given , we generate from the following joint normal distribution

To guarantee , we set and For simplicity, we assume that is linear in by setting

-

(d).

Define , and we generate the principal stratum from the following ordered probit model:

-

(e).

The outcome is finally generated from the following conditional normal distribution:

The true values of parameters are set as follows:

-

(a).

, , , , .

-

(b).

, , .

-

(c).

, , , , , , , , , , , , .

-

(d).

, , , . Since controls for magnitude of unobserved confounding, we consider 6 different values, i.e., .

-

(e).

, , , , , , , . We consider 4 settings for : , , and , which corresponds to different identifying assumptions.

| Case | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Bias | Sd | CP | Bias | Sd | CP | Bias | Sd | CP | ||||||

| (i) | 0.6 | 7.5 | 96.2 | 2.4 | 39.8 | 95.8 | 2.8 | 28.6 | 95.0 | |||||

| (ii) | 0.5 | 8.0 | 95.8 | 0.1 | 46.3 | 96.4 | 0.7 | 21.9 | 95.8 | |||||

| (iii) | 1.0 | 12.5 | 95.6 | 7.8 | 48.5 | 94.0 | 3.3 | 21.6 | 94.4 | |||||

| (iv) | 0.2 | 12.6 | 95.8 | 1.1 | 50.3 | 96.8 | 0.9 | 23.4 | 95.2 | |||||

| Bias | Sd | CP | Bias | Sd | CP | Bias | Sd | CP | ||||||

| (i) | 0.4 | 3.5 | 94.4 | 1.6 | 18.9 | 96.6 | 0.7 | 12.9 | 94.8 | |||||

| (ii) | 0.4 | 3.8 | 94.6 | 1.0 | 21.9 | 96.4 | 0.3 | 9.6 | 95.8 | |||||

| (iii) | 1.2 | 5.3 | 95.8 | 4.9 | 20.8 | 96.0 | 0.1 | 9.5 | 95.6 | |||||

| (iv) | 1.0 | 5.3 | 96.4 | 3.7 | 21.8 | 96.0 | 0.3 | 10.1 | 96.6 | |||||

| Bias | Sd | CP | Bias | Sd | CP | Bias | Sd | CP | ||||||

| (i) | 0.5 | 5.5 | 95.2 | 8.2 | 44.8 | 93.6 | 6.6 | 25.0 | 94.4 | |||||

| (ii) | 0.5 | 5.9 | 95.8 | 8.3 | 51.0 | 94.8 | 3.2 | 19.0 | 94.8 | |||||

| (iii) | 0.6 | 6.8 | 96.6 | 11.1 | 47.0 | 93.8 | 3.5 | 20.9 | 93.4 | |||||

| (iv) | 0.5 | 6.8 | 96.4 | 6.4 | 51.0 | 96.2 | 2.2 | 22.4 | 95.4 | |||||

| Bias | Sd | CP | Bias | Sd | CP | Bias | Sd | CP | ||||||

| (i) | 0.4 | 2.6 | 95.0 | 5.1 | 21.8 | 94.4 | 0.1 | 11.8 | 95.4 | |||||

| (ii) | 0.4 | 2.8 | 94.6 | 4.8 | 24.6 | 94.4 | 0.2 | 8.6 | 95.6 | |||||

| (iii) | 0.7 | 3.2 | 95.2 | 7.1 | 21.6 | 94.0 | 0.4 | 8.8 | 94.4 | |||||

| (iv) | 0.6 | 3.2 | 95.2 | 6.0 | 23.2 | 94.2 | 0.0 | 9.3 | 95.4 | |||||

-

•

Sd: empirical standard error. CP: 95% coverage probability.

Under the above data generating mechanism, the bridge function with the following form is compatible with Assumption 4 (see supplementary materials for details):

We thus model the bridge function in Model 1 with this parametric form and specify all correct parametric models in Model 2. We estimate the bridge function by solving the estimating equation (9) with the user-specified functions . It is worth pointing out that our data-generating mechanism also satisfies the model assumptions in Proposition 1, and we can consistently estimate the probabilities and using the method given in the supplementary material. We investigate the performance of the proposed estimators under various values of , which represent different conditional independence conditions between and the outcome . For the four different settings in (e), we consider estimation of principal causal effects with four different correct parametric forms in Model 3, respectively. For example, the setting implies that Assumption 5 holds, and we specify the working model ; if , then the outcome can be affected by all covariates, and we employ the linear model given in (6). For simplicity, we refer to these four different estimation procedures as cases (i)–(iv), respectively.

For each value of , we consider sample size and . Table 1 reports the bias, standard error and coverage probabilities of 95% confidence intervals averaged across 500 replications with and . The corresponding results for other values of are provided in the supplementary material. The results in all the settings are similar. It can be found that our method has negligible biases with smaller variances as the sample size increases. Estimators of and are more stable than that of . This may be because the estimation of requires solving the joint estimating equations (10) and (11) rather than only one of them. The proposed estimators have coverage probabilities close to the nominal level in all scenarios. All these results demonstrate the consistency of our proposed estimators.

6 Application to Return to Schooling

We illustrate our approach by reanalyzing the dataset from the National Longitudinal Survey of Young Men (Card,, 1993; Tan,, 2006). This cohort study includes 3,010 men who were aged - when first interviewed in 1966, with follow-up surveys continued until 1976. We are interested in estimating the causal effect of education on earnings, which might be confounded by unobserved preferences for students’ abilities and family costs (Kédagni,, 2021).

The treatment is an indicator of living near a four-year college. Following Tan, (2006), we choose the educational experience beyond high school as the intermediate variable . The outcome is the log wage in the year 1976, ranging from 4.6 to 7.8. We consider the average parental education years as the negative control exposure , because parents’ education years are highly correlated with whether their children have the chance to live close to a college. We use the intelligence quotient (IQ) scores as the negative control intermediate variable , because IQ is related to students’ learning abilities, and students with higher IQ are more likely to enter college. The data set also includes the following covariates : race, age, scores on the Knowledge of the World of Work test, a categorical variable indicating whether children living with both parents, single mom, or step-parents, and several geographic variables summarizing living areas in the past. The missing covariates are imputed via the -Nearest Neighbor algorithm with (Franzin et al.,, 2017).

Monotonicity is plausible because living near a college would make an individual more likely to receive higher education. Following Jiang et al., (2022), we do not invoke the exclusion restriction assumption that living near a college can affect the earnings only through education. In fact, we can evaluate the validity of this assumption by applying the proposed approach in this paper. We employ similar model parameterizations as used in simulation studies, and our analyses here are also conducted under the cases (i)–(iv) that represent different conditional independence assumptions for the outcome model.

| Case | |||

|---|---|---|---|

| (i) | 0.07 (0.07, 0.81) | 0.68 (1.85, 0.25) | 0.86 (2.83, 0.32) |

| (ii) | 0.06 (0.09, 0.77) | 0.13 (0.45, 0.59) | 0.02 (0.56, 0.16) |

| (iii) | 0.18 (0.55, 0.80) | 0.87 ( 0.05, 1.93) | 0.07 (0.91, 0.23) |

| (iv) | 0.18 (0.56, 0.78) | 0.85 ( 0.00, 1.88) | 0.07 (0.89, 0.26) |

Table 2 shows the point estimates and their associated 95% confidence intervals obtained via the nonparametric bootstrap method. We first observe that the results in cases (iii) and (iv) are very close. Compared with them, the corresponding results in cases (i) and (ii) are completely different. Because the outcome model in cases (i) and (ii) do not include the proxy variable as a predictor, the empirical findings may indicate misspecifications of outcome models in these two cases. Thus, the results in cases (iii) and (iv), where the IQ score is allowed to directly affect the wage , are more credible. Based on these results, we find that both the 95% confidence intervals for and cover zero, which implies no significant evidence of violating the exclusion restriction. The estimate of is positive and its corresponding confidence interval does not cover zero. This implies that education has a significantly positive effect on earnings, which is consistent with previous analyses (Tan,, 2006; Jiang et al.,, 2022; Kédagni,, 2021).

7 Discussion

With the aid of a pair of negative controls, we have established identification and estimation of principal causal effects when the treatment and principal strata are confounded by unmeasured variables. The availability of negative control variables is crucial for the proposed approach. Although it is generally not possible to test the negative control assumptions via observed data without additional assumptions, the existence of such variables is practically reasonable in the empirical example presented in this paper and similar situations where two or more proxies of unmeasured variables may be available (Miao et al.,, 2018; Shi et al.,, 2020; Miao et al.,, 2020; Cui et al.,, 2020).

The proposed methods may be improved or extended in several directions. First, we consider parametric methods to solve integral equations involved in our estimation procedure. One may also consider nonparametric estimation techniques to obtain the solutions (Newey and Powell,, 2003; Chen and Pouzo,, 2012; Li et al.,, 2021). Second, we relax the commonly-used ignorability assumption by allowing unmeasured confounders between the treatment and principal strata, and it is possible to further relax this assumption and consider the setting where Assumption 2(ii) fails. Third, our identifiability results rely on the monotonicity assumption which may not hold in some real applications. In principle, one can conduct sensitivity analysis to assess the principal causal effects of violations of monotonicity assumption (Ding and Lu,, 2017). Finally, it is also of interest to develop doubly robust estimators for the principal causal effects as provided by Cui et al., (2020) for average treatment effects. The study of these issues is beyond the scope of this paper and we leave them as future research topics.

References

- Angrist et al., (1996) Angrist, J. D., Imbens, G. W., and Rubin, D. B. (1996). Identification of causal effects using instrumental variables. Journal of the American Statistical Association, 91(434):444–455.

- Card, (1993) Card, D. (1993). Using geographic variation in college proximity to estimate the return to schooling. Technical report, National Bureau of Economic Research.

- Carrasco et al., (2007) Carrasco, M., Florens, J.-P., and Renault, E. (2007). Linear inverse problems in structural econometrics estimation based on spectral decomposition and regularization. Handbook of Econometrics, 6:5633–5751.

- Chen and Pouzo, (2012) Chen, X. and Pouzo, D. (2012). Estimation of nonparametric conditional moment models with possibly nonsmooth generalized residuals. Econometrica, 80(1):277–321.

- Cui et al., (2020) Cui, Y., Pu, H., Shi, X., Miao, W., and Tchetgen Tchetgen, E. J. (2020). Semiparametric proximal causal inference. arXiv: 2011.08411.

- Deng et al., (2021) Deng, Y., Guo, Y., Chang, Y., and Zhou, X.-H. (2021). Identification and estimation of the heterogeneous survivor average causal effect in observational studies. arXiv: 2109.13623v3.

- Ding et al., (2011) Ding, P., Geng, Z., Yan, W., and Zhou, X.-H. (2011). Identifiability and estimation of causal effects by principal stratification with outcomes truncated by death. Journal of the American Statistical Association, 106(496):1578–1591.

- Ding and Lu, (2017) Ding, P. and Lu, J. (2017). Principal stratification analysis using principal scores. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 79(3):757–777.

- Frangakis and Rubin, (2002) Frangakis, C. E. and Rubin, D. B. (2002). Principal stratification in causal inference. Biometrics, 58(1):21–29.

- Franzin et al., (2017) Franzin, A., Sambo, F., and Di Camillo, B. (2017). Bnstruct: an r package for bayesian network structure learning in the presence of missing data. Bioinformatics, 33(8):1250–1252.

- Gilbert and Hudgens, (2008) Gilbert, P. B. and Hudgens, M. G. (2008). Evaluating candidate principal surrogate endpoints. Biometrics, 64(4):1146–1154.

- Hansen, (1982) Hansen, L. P. (1982). Large sample properties of generalized method of moments estimators. Econometrica, 50:1029–1054.

- Jiang et al., (2016) Jiang, Z., Ding, P., and Geng, Z. (2016). Principal causal effect identification and surrogate end point evaluation by multiple trials. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 78(4):829–848.

- Jiang et al., (2022) Jiang, Z., Yang, S., and Ding, P. (2022). Multiply robust estimation of causal effects under principal ignorability. Journal of the Royal Statistical Society: Series B (Statistical Methodology). doi:10.1111/rssb.12538.

- Kédagni, (2021) Kédagni, D. (2021). Identifying treatment effects in the presence of confounded types. Journal of Econometrics, doi: 10.1016/j.jeconom.2021.01.012.

- Lee, (2009) Lee, D. S. (2009). Training, wages, and sample selection: Estimating sharp bounds on treatment effects. The Review of Economic Studies, 76(3):1071–1102.

- Li et al., (2021) Li, W., Miao, W., and Tchetgen Tchetgen, E. J. (2021). Nonparametric inference about mean functionals of nonignorable nonresponse data without identifying the joint distribution. arXiv: 2110.05776v2.

- Long and Hudgens, (2013) Long, D. M. and Hudgens, M. G. (2013). Sharpening bounds on principal effects with covariates. Biometrics, 69(4):812–819.

- Luo et al., (2021) Luo, S., Li, W., and He, Y. (2021). Causal inference with outcomes truncated by death in multiarm studies. Biometrics. doi: 10.1111/biom.13554.

- Miao et al., (2018) Miao, W., Geng, Z., and Tchetgen Tchetgen, E. J. (2018). Identifying causal effects with proxy variables of an unmeasured confounder. Biometrika, 105(4):987–993.

- Miao et al., (2020) Miao, W., Shi, X., and Tchetgen Tchetgen, E. J. (2020). A confounding bridge approach for double negative control inference on causal effects. arXiv: 1808.04945.

- Newey and Powell, (2003) Newey, W. K. and Powell, J. L. (2003). Instrumental variable estimation of nonparametric models. Econometrica, 71(5):1565–1578.

- Robins et al., (2000) Robins, J. M., Hernan, M. A., and Brumback, B. (2000). Marginal structural models and causal inference in epidemiology. Epidemiology, 11(5):550–560.

- Rubin, (1990) Rubin, D. B. (1990). Comment: Neyman (1923) and causal inference in experiments and observational studies. Statistical Science, 5(4):472–480.

- Rubin et al., (2006) Rubin, D. B. et al. (2006). Causal inference through potential outcomes and principal stratification: application to studies with “censoring” due to death. Statistical Science, 21(3):299–309.

- Schwartz et al., (2012) Schwartz, S., Li, F., and Reiter, J. P. (2012). Sensitivity analysis for unmeasured confounding in principal stratification settings with binary variables. Statistics in Medicine, 31(10):949–962.

- Shi et al., (2020) Shi, X., Miao, W., Nelson, J. C., and Tchetgen Tchetgen, E. J. (2020). Multiply robust causal inference with double-negative control adjustment for categorical unmeasured confounding. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 82(2):521–540.

- Tan, (2006) Tan, Z. (2006). Regression and weighting methods for causal inference using instrumental variables. Journal of the American Statistical Association, 101(476):1607–1618.

- Tchetgen Tchetgen, (2014) Tchetgen Tchetgen, E. J. (2014). Identification and estimation of survivor average causal effects. Statistics in Medicine, 33(21):3601–3628.

- VanderWeele, (2011) VanderWeele, T. J. (2011). Principal stratification–uses and limitations. The International Journal of Biostatistics, 7(1):1–14.

- Wang et al., (2017) Wang, L., Zhou, X.-H., and Richardson, T. S. (2017). Identification and estimation of causal effects with outcomes truncated by death. Biometrika, 104(3):597–612.

- Zhang and Rubin, (2003) Zhang, J. L. and Rubin, D. B. (2003). Estimation of causal effects via principal stratification when some outcomes are truncated by “death”. Journal of Educational and Behavioral Statistics, 28(4):353–368.

- Zhang et al., (2009) Zhang, J. L., Rubin, D. B., and Mealli, F. (2009). Likelihood-based analysis of causal effects of job-training programs using principal stratification. Journal of the American Statistical Association, 104(485):166–176.

Supplementary Material

In the supplementary material, we provide proofs of theorems and claims in the main paper. We also provide additional details for the estimation and simulation studies.

Appendix S1 Proofs of propositions and theorems

S1.1 The proof of expression (1)

Proof.

By the Law of Iterated Expectation (LIE), we have

| (S12) |

Given Assumption 2(ii), we have

Combining these two pieces, we have

∎

S1.2 Lemmas

We first prove the first conclusion in Theorem 1, which is summarized as the following lemma.

Lemma S1.

Proof.

Lemma S2.

S1.3 The proof of Theorems 1-2

Proof.

Given the conditions in Lemma S1, we know that the weights and are identifiable for all . Under monotonicity assumption, the causal estimands and can be identified by

We next show that and are also identifiable. For simplicity, we omit the proof of and . Applying LIE to get

| (S15) |

- 1.

- 2.

Given the identifiability of and , we show that and can be identified from the view of (S12). Specifically, we have

for Moreover, given Assumptions 2(ii) and 5 or 6, we have

Therefore, for , we have

Similarly, and are also identifiable. ∎

S1.4 The identifiability of (6)

In this section, we show the identifiability of (6).

Proof.

By the LIE, we have

Given the conditions in Lemma S1, we know that the proportions of principal strata for all are identifiable. If the functions

is linearly independen, we then can identify , , , and . Subsequently, and are also identifiable. Similarly, and are also identifiable. ∎

S1.5 The proof of Proposition 1

Proof.

First, we can identify and from the observed data based on normal distribution. Next, we consider the identifiablity of , , , and . Given equation (7) in main text, we have that

where . The above equalities indicate (8) holds. According to Lemma S1, we can nonparametriclly identify the distribution . Also,

Since are linearly independent, then we can use probit regression to identify all the parameters. ∎

S1.6 The proof of Theorem 3

Proof.

Given the conditions in Proposition 1, we know that the proportions of principal strata for all are identifiable. Also, under Assumption 1, we know that the causal estimands or can be identified by

We then show that and are also identifiable. We omit the proof of and due to the similarity. Applying LIE to get

| (S16) |

- 1.

- 2.

- 3.

- 4.

Given the identifiability of and , we can identify and from (S12). Similarly, we can identify and .

∎

Appendix S2 Estimation details

S2.1 Estimation details about Model 1

S2.2 Estimation details about Proposition 1

If we assume the conditions in Proposition 1 hold, that is, the conditional distribution in Model 2 is normal distributed and equation (8) holds, we can further estimate the weights and . In order to ensure the linearly independent condition in Proposition 1, we suggest adding higher-order polynomial, square, or interaction terms to the conditional expectation of the conditional distribution , especially in the case of linear regression. After obtaining as shown in the main text, there are some approaches to estimate the parameters in equation (8). For example, we can use GMM again to solve through the following moment constraints,

or we can directly derive the specific form of the right hand of the above estimating equation, and then use Probit regression to solve for . Under monotonicity assumption 1, we can estimate by plugging into equation (8):

We then find the estimate of as follows:

Appendix S3 Simulation details

S3.1 Simulation details about bridge function in Section 5

-

1.

We first present the specific form of the conditional density function . Since , where and the specific form of is

-

2.

We next present the specific form of the latent distribution is as follows,

And thus,

(S17) - 3.

S3.2 Simulation details about other models

-

1.

We now present the specific form of . Since , where and the specific form of is

-

2.

The specific form of :

For simplicity, we let , where

-

3.

The specific form of ,

S3.3 Additional simulation results

| Case | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Bias | Sd | CP | Bias | Sd | CP | Bias | Sd | CP | ||||||

| (i) | 0.9 | 12.4 | 94.8 | 1.5 | 42.7 | 96.2 | 1.0 | 35.3 | 96.0 | |||||

| (ii) | 0.5 | 13.7 | 95.8 | 3.1 | 51.4 | 97.8 | 2.1 | 29.3 | 97.6 | |||||

| (iii) | 7.2 | 28.8 | 97.0 | 18.9 | 67.4 | 96.0 | 4.1 | 28.0 | 94.6 | |||||

| (iv) | 3.4 | 33.1 | 95.8 | 5.9 | 71.8 | 97.4 | 0.3 | 31.3 | 95.6 | |||||

| Bias | Sd | CP | Bias | Sd | CP | Bias | Sd | CP | ||||||

| (i) | 0.2 | 5.5 | 95.6 | 0.2 | 21.0 | 96.0 | 0.6 | 14.9 | 95.0 | |||||

| (ii) | 0.1 | 6.0 | 95.4 | 1.1 | 24.1 | 96.0 | 0.5 | 11.5 | 95.4 | |||||

| (iii) | 3.2 | 13.5 | 96.6 | 7.1 | 31.9 | 97.2 | 0.2 | 12.3 | 94.6 | |||||

| (iv) | 2.1 | 13.9 | 96.2 | 4.0 | 32.2 | 96.2 | 0.6 | 12.6 | 95.0 | |||||

| Bias | Sd | CP | Bias | Sd | CP | Bias | Sd | CP | ||||||

| (i) | 0.8 | 9.7 | 95.0 | 2.1 | 40.9 | 96.4 | 2.0 | 30.2 | 95.8 | |||||

| (ii) | 0.6 | 10.2 | 95.2 | 0.6 | 47.4 | 96.8 | 0.0 | 24.2 | 96.8 | |||||

| (iii) | 2.6 | 17.9 | 95.4 | 10.9 | 54.1 | 95.2 | 3.2 | 22.9 | 94.8 | |||||

| (iv) | 1.1 | 18.7 | 96.6 | 3.0 | 56.5 | 97.6 | 0.4 | 26.5 | 96.2 | |||||

| Bias | Sd | CP | Bias | Sd | CP | Bias | Sd | CP | ||||||

| (i) | 0.3 | 4.2 | 94.0 | 0.2 | 19.4 | 95.8 | 0.9 | 13.7 | 94.0 | |||||

| (ii) | 0.2 | 4.7 | 95.2 | 0.6 | 22.5 | 95.6 | 0.6 | 9.9 | 96.6 | |||||

| (iii) | 1.7 | 7.8 | 96.0 | 4.8 | 24.0 | 95.4 | 0.1 | 10.3 | 95.8 | |||||

| (iv) | 1.2 | 8.0 | 95.8 | 3.0 | 24.6 | 95.6 | 0.6 | 10.6 | 96.6 | |||||

| Case | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Bias | Sd | CP | Bias | Sd | CP | Bias | Sd | CP | ||||||

| (i) | 0.6 | 6.5 | 95.0 | 3.5 | 41.4 | 95.8 | 3.8 | 26.6 | 93.8 | |||||

| (ii) | 0.5 | 7.0 | 96.0 | 1.7 | 47.5 | 96.0 | 1.4 | 20.2 | 96.0 | |||||

| (iii) | 0.6 | 9.6 | 96.2 | 7.5 | 45.5 | 95.8 | 2.8 | 20.9 | 94.2 | |||||

| (iv) | 0.3 | 9.6 | 95.8 | 1.9 | 48.8 | 97.0 | 1.0 | 22.1 | 96.0 | |||||

| Bias | Sd | CP | Bias | Sd | CP | Bias | Sd | CP | ||||||

| (i) | 0.3 | 3.2 | 94.8 | 1.7 | 19.3 | 95.8 | 0.8 | 12.4 | 95.4 | |||||

| (ii) | 0.3 | 3.5 | 93.6 | 1.2 | 22.2 | 96.0 | 0.2 | 8.8 | 95.4 | |||||

| (iii) | 0.7 | 4.3 | 94.4 | 4.0 | 20.1 | 93.4 | 0.1 | 9.1 | 95.8 | |||||

| (iv) | 0.6 | 4.3 | 94.0 | 3.2 | 21.3 | 94.4 | 0.3 | 9.5 | 96.4 | |||||

| Bias | Sd | CP | Bias | Sd | CP | Bias | Sd | CP | ||||||

| (i) | 0.5 | 6.0 | 95.0 | 4.6 | 41.4 | 94.8 | 5.2 | 25.5 | 94.8 | |||||

| (ii) | 0.4 | 6.5 | 95.4 | 4.2 | 47.2 | 95.0 | 2.2 | 19.4 | 96.0 | |||||

| (iii) | 0.5 | 8.0 | 97.0 | 8.2 | 44.7 | 95.0 | 3.2 | 20.2 | 94.2 | |||||

| (iv) | 0.4 | 8.0 | 96.6 | 2.9 | 47.9 | 96.8 | 1.4 | 21.8 | 96.4 | |||||

| Bias | Sd | CP | Bias | Sd | CP | Bias | Sd | CP | ||||||

| (i) | 0.3 | 2.8 | 94.6 | 3.0 | 21.0 | 94.4 | 0.3 | 12.3 | 94.0 | |||||

| (ii) | 0.3 | 3.1 | 94.2 | 2.7 | 24.2 | 95.0 | 0.0 | 8.7 | 95.0 | |||||

| (iii) | 0.7 | 3.6 | 94.4 | 5.2 | 21.2 | 92.6 | 0.1 | 9.0 | 95.0 | |||||

| (iv) | 0.6 | 3.7 | 94.6 | 4.0 | 22.4 | 93.6 | 0.3 | 9.5 | 95.4 | |||||