Drift-implicit Euler scheme for sandwiched processes

driven by Hölder noises

2Department of Business and Management Science, NHH Norwegian School of Economics, Bergen

3Department of Probability Theory, Statistics and Actuarial Mathematics, Taras Shevchenko National University of Kyiv

)

Abstract

In this paper, we analyze the drift-implicit (or backward) Euler numerical scheme for a class of stochastic differential equations with unbounded drift driven by an arbitrary -Hölder continuous process, . We prove that, under some mild moment assumptions on the Hölder constant of the noise, the -rate of convergence is equal to . To exemplify, we consider numerical schemes for the generalized Cox–Ingersoll-Ross and Tsallis–Stariolo–Borland models. The results are illustrated by simulations.

Keywords: sandwiched process, unbounded drift, Hölder continuous noise, numerical scheme

MSC 2020: 60H10; 60H35; 60G22; 91G30

Introduction

We analyze the drift-implicit (also known as backward) Euler numerical scheme for stochastic differential equations (SDEs) of the form

| (0.1) |

where is a general -Hölder continuous noise, , and the drift is unbounded and has one of the following two properties:

-

(A)

has an explosive growth of the type as , where is a given Hölder continuous function of the same order as and ;

-

(B)

has an explosive growth of the type as and an explosive decrease of the type as , where and are given Hölder continuous functions of the same order as such that , , and .

The SDEs of this type were extensively studied in [14]. It was shown that the properties (A) or (B), along with some relatively weak additional assumptions, ensure that the solution to (0.1) is bounded from below (one-sided sandwich case) by the function in the setting (A), i.e.

| (0.2) |

or stays between and (two-sided sandwich case) in the setting (B), i.e.

| (0.3) |

We emphasize that the SDE type (0.1) includes and generalizes several widespread stochastic models. For example, the process given by

where is -Hölder continuous with , fits into the setting (B) and can be regarded as a natural extension of the Tsallis–Stariolo–Borland (TSB) model employed in biophysics (for more details on the standard Brownian TSB model see e.g. [15, Subsection 2.3] or [16, Chapter 3 and Chapter 8]). Another important example is

| (0.4) |

where is -Hölder continuous, , and . It can be shown (see [14, Subsection 4.2]) that, if , stochastic process satisfies the SDE

| (0.5) |

where and the integral w.r.t. exists as a pathwise limit of Riemann-Stieltjes integral sums. Equations of the type (0.5) are used in finance in the standard Brownian setting and are called Chan–-Karolyi–-Longstaff–-Sanders (CKLS) or constant elasticity of variance (CEV) model (see, e.g., [4, 8, 9]). If , the equation (0.5) is also known as the Cox–Ingersoll–Ross (CIR) equation, see , e.g., [10, 11, 12].

In this work, we develop a numerical approximation (both pathwise and in ) for sandwiched processes (0.1) which is similar to the drift-implicit (also known as backward) Euler scheme constructed for the classical Cox-Ingersoll-Ross process in [2, 3, 13] and extended to the case of the fractional Brownian motion with in [18, 21, 22]. In this drift-implicit scheme, in order to generate , one has to solve the equation of the type

| (0.6) |

with respect to which is in general a more computationally heavy problem in comparison to the standard Euler-type techniques (see e.g. [14, Section 5]). However, this drift-implicit numerical method also has a substantial advantage: the approximation maintains the property of being sandwiched, i.e., for all points of the partition

in the setting (A) and

in the case (B). Having this in mind, we shall say that the drift-implicit scheme is sandwich preserving.

We note that a similar approximation scheme was studied in [21] and [18, 22] for processes of the type (0.4) driven by a fractional Brownian motion with . Our work can be seen as an extension of those. However, we emphasize that our results have several elements of novelty. In particular, the paper [21] discusses only pathwise convergence and not convergence in . The approach of [18] and [22] is very noise specific as both use Malliavin calculus techniques in the spirit of [19, Proposition 3.4] to estimate inverse moments of the considered process (which turns out to be crucial to control explosive growth of the drift). As a result, two limitations appear: a restrictive condition involving the time horizon (see e.g. [18, Eq. (8) and Remark 3.1]) and sensitivity to the choice of the noise, i.e. their method cannot be applied directly for drivers other then fBm with . This lack of flexibility in terms of the choice of the noise is a crucial disadvantage in e.g. finance where modern empirical studies justify the use of fBm with extremely low Hurst index () [7] or even drivers with time-varying roughness [1]. Our approach makes use of [14, Theorem 3.2] based on the pathwise calculus and allows us to obtain strong convergence with no limitations on for a substantially larger class of noises. In fact, we require only Hölder continuity of the noise and some moment condition on the corresponding Hölder coefficient which is often satisfied and shared by e.g. all Hölder continuous Gaussian processes.

The paper is organized as follows. Section 1 describes the setting in detail and contains some necessary statements on the properties of the sandwiched processes. In Section 2, we give the convergence results in the setting (B) which turns out to be a bit simpler then (A) due to boundedness of the process. Section 3 extends the scheme to the setting (A). In Section 4, we give some examples and simulations; in particular we show that in some cases (e.g. for the generalized TSB and CIR models) equations (0.6) can be solved explicitly which drastically improves the computational efficiency of the algorithm.

1 Preliminaries and assumptions

Fix and define

| (1.1) | ||||||

where , are such that , .

Throughout the paper, we will be dealing with a stochastic differential equation of the form

| (1.2) |

The noise is always assumed to satisfy the following conditions:

-

(Z1)

a.s.;

-

(Z2)

has a.s. -Hölder continuous paths, , i.e. there exists a positive random variable such that

Given the noise satisfying (Z1)–(Z2), the initial value and the drift satisfy one of the two lists of assumptions given below.

Assumptions A.

(One-sided sandwich case) There exists a -Hölder continuous function : with being the same as in (Z2) such that

-

(A1)

is deterministic and ,

-

(A2)

: is continuous and for any

where and are some given constants and is from (Z2),

-

(A3)

where , are some given constants and with being from (Z2),

-

(A4)

the partial derivative with respect to the spacial variable exists, is continuous and bounded from above, i.e.

for some .

Assumptions B.

(Two-sided sandwich case) There exist -Hölder continuous functions , : , , , with being the same as in (Z2) such that

-

(B1)

is deterministic and ,

-

(B2)

: is continuous and for any

where and are some given constants and is from (Z2),

-

(B3)

where , are some given constants and with being from (Z2),

-

(B4)

the partial derivative with respect to the spacial variable exists, is continuous and bounded from above, i.e.

for some .

Both Assumptions A and B along with (Z1)–(Z2) ensure that the SDE (1.2) has a unique solution. In the theorem below, we provide some relevant results related to sandwiched processes (see [14, Theorems 2.3, 2.5, 2.6, 3.1 and 3.2]).

Theorem 1.1.

Let be a stochastic process satisfying (Z1)–(Z2).

-

1)

If the initial value and the drift satisfy assumptions (A1)–(A3), then the SDE has a unique strong pathwise solution such that for all

(1.3) Moreover, there exist deterministic constants , , and depending only on , the shape of and , such that for all the estimate (1.3) can be refined as follows:

(1.4) where is from (Z2) and is from (A3). In particular, if is such that

(1.5) for some , then

and, if

(1.6) for some , then

-

2)

If the initial value and the drift satisfy assumptions (B1)–(B3), then the SDE has a unique strong pathwise solution such that for all

(1.7) Moreover, there exist deterministic constants and depending only on , the shape of and , such that for all the estimate (1.7) can be refined as follows:

(1.8) where is from (Z2) and is from (B3). In particular, if can be chosen in such a way that

(1.9) for some , then

Remark 1.2.

Remark 1.3.

Due to the property (1.7), the setting described in Assumptions B will be referred to as the two-sided sandwich case since the solution is “sandwiched” between and a.s. Similarly, the property (1.3) justifies the name one-sided sandwich case for the setting corresponding to Assumptions A. In both cases A and B, the solution to (1.2) will be referred to as a sandwiched process.

Remark 1.4.

Note that assumptions (A4) and (B4) are not required for Theorem 1.1 to hold and will be used later on.

In what follows, conditions (1.5), (1.6) and (1.9) will play an important role since the -convergence of the approximation scheme will directly follow from the integrability of . However it should be noted that these conditions are not very restricting as indicated in the following example.

Example 1.5.

(Hölder Gaussian noises) Let be an arbitrary Hölder continuous Gaussian process satisfying (Z1)–(Z2). In this case, by [6], the random variable from (Z2) can be chosen to have moments of all orders.

We now complete the Section with some examples of the sandwiched processes.

Example 1.6.

(Generalized CIR and CKLS/CEV models) Let , satisfy (Z1)–(Z2) with and , , , be given. Then, by Theorem 1.1, 1), the SDE of the form

| (1.10) |

has a unique positive solution. Moreover, it can be shown (see [14, Subsection 4.2]) that, if , stochastic process , , a.s. satisfies the SDE of the form

| (1.11) |

where and the integral w.r.t. exists a.s. as a pathwise limit of Riemann-Stieltjes integral sums. As mentioned already, the (1.11) appears in finance in the standard Brownian setting and is called Chan–Karolyi–Longstaff–Sanders (CKLS) or constant elasticity of variance (CEV) model (see e.g. [4, 8, 9]). If (i.e. when ), the equation (1.11) is also known as the Cox-Ingersoll-Ross (CIR) equation [10, 11, 12].

Example 1.7.

(Generalized TSB model) Let , , , satisfy (Z1)–(Z2) with and . Then, by Theorem 1.1, 2), the SDE of the form

| (1.12) |

has a unique solution such that for all a.s. In the standard Brownian setting, the SDE of the type (1.12) is known as the Tsallis–Stariolo–Borland (TSB) model and is used in biophysics (for more details, see e.g. [15, Subsection 2.3] or [16, Chapter 3 and Chapter 8]).

Example 1.8.

Notation 1.9.

In what follows, denotes any positive deterministic constant that does not depend on the partition and the exact value of which is not relevant. Note that may change from line to line (or even within one line).

2 The approximation scheme for the two-sided sandwich

We will start by considering the numerical scheme for the two-sided sandwich case which turns out to be slightly simpler due to boundedness of . Let the noise satisfy (Z1)–(Z2), and satisfy Assumptions B and be the unique solution of the SDE (1.2). Consider a uniform partition of , , , with the mesh such that

| (2.1) |

where is an upper bound for from (B4). Let us define as follows:

| (2.2) | ||||

where the second expression is considered as an equation with respect to .

Remark 2.1.

Remark 2.2.

The value of for can also be defined via linear interpolation as

In such case all results of this section hold with almost no changes in the proofs.

Remark 2.3.

Before presenting the main results of this section, we require some auxiliary lemmas. First of all, we note that the values , , of the discretized process are bounded away from both and by random variables that do not depend on the partition. Namely, we have the following result that can be regarded as a discrete modification of arguments in [14, Theorem 3.2].

Lemma 2.4.

Proof.

We will prove that

| (2.4) |

by using the pathwise argument (see Remark 1.2). The other inequality can be derived in a similar manner. Recall that, by Assumptions B, and are -Hölder continuous, i.e. there exists such that

Denote also

where is from (B3),

with the constants and also from (B3), and

Note that, with probability 1,

and, furthermore, it is easy to check that , and .

If for a particular , then, by definition of , the bound of the type (2.4) holds automatically. Suppose that there exists such that . Denote by the last point of the partition before on which stays above , i.e.

(note that such point exists since ). Then, for all we have that and therefore, using (B3), we obtain that, with probability 1,

Consider a function such that

It is straightforward to verify that attains its minimum at

and, taking into account the explicit form of ,

Namely, even if , we still have that, with probability 1,

and thus, with probability 1, for any

where . ∎

Remark 2.5.

It is clear that constants and in Lemma 2.4 can be chosen jointly for and , so that the inequalities

and

hold simultaneously with probability 1.

Next, we proceed with a simple property of the sandwiched process in (1.2).

Lemma 2.6.

Let satisfy (Z1)–(Z2) and assumptions (B1)–(B3) hold.

-

1)

There exists a positive random variable such that, with probability 1,

-

2)

If, for some ,

(2.5) where and are from (Z2), is from (B2) and is from (B3), then one can choose such that

Proof.

Denote , . By (1.8),

i.e. with probability 1 , , where

| (2.6) |

and is defined by (1.1). It is evident that , , therefore, using (Z2), (B2) and (1.7), we can write that, with probability 1, for all :

| (2.7) | ||||

where is a positive constant. Now one can put

| (2.8) |

and observe that the definition of , (2.5) and (2.6) imply that

∎

Corollary 2.7.

Under (Z1)–(Z2) and Assumptions B, using Lemma 2.4 and following the proof of Lemma 2.6, it is easy to obtain that there exists a random variable independent of the partition such that with probability 1

| (2.9) |

Furthermore, just like in Lemma 2.6, if (2.5) for some for , then

Finally, just as in Remark 2.5, can be chosen jointly for and , so that

holds simultaneously with (2.9) with probability 1.

Lemma 2.8.

Let satisfy (Z1)–(Z2), Assumptions B hold and the mesh of the partition satisfy (2.1).

-

1)

For any , there exists a positive random variable that does not depend on the partition such that

-

2)

If, additionally,

(2.10) where and are from (Z2), is from (B2) and is from (B3), then one can choose such that , i.e. there exists a deterministic constant that does not depend on the partition such that

Proof.

Fix such that , , is Hölder continuous (for simplicity of notation, we will omit in the brackets). Denote , . Then

| (2.11) | ||||

By the mean value theorem,

with . Using this, we can rewrite (2.11) as follows:

| (2.12) |

where

by (B4) and (2.1).

Next, denote

and define . By multiplying both sides of (2.12) by , we obtain that

| (2.13) |

and, expanding the terms in (2.13) one by one, , and taking into account that , we obtain that

Therefore

Observe that, by assumption (B4) and (2.1), for any , ,

whence there exists a constant that does not depend on , or such that

Using this, one can deduce that

Note that , where is defined by (2.6) and is defined via (1.1), hence, by (B2) as well as Lemma 2.6, we can deduce that

In other words, there exists a constant that does not depend on the partition such that

and, since the right-hand side of the relation above does not depend on or , we have

| (2.14) |

It remains to notice that, by (2.6) and (2.8),

whenever (2.10) holds, which finally implies

∎

Now we are ready to proceed to the main results of this subsection.

Theorem 2.9.

Let satisfy (Z1)–(Z2), Assumptions B hold and the mesh of the partition satisfy (2.1).

-

1)

For any , there exists a random variable that does not depend on the partition such that

-

2)

If, additionally,

where and are from (Z2), is from (B2) and is from (B3), then one can choose such that , i.e. there exists a deterministic constant that does not depend on the partition such that

Proof.

Fix such that , , is Hölder continuous (for simplicity of notation, we again omit in the brackets) and consider an arbitrary . Denote

i.e. . Then

where we used Lemma 2.6 to estimate and bound (2.14) to estimate . Therefore

Finally, using the same arguments as in Lemma 2.6 and Lemma 2.8, it is easy to see that the condition

implies that

therefore

for some constant that does not depend on the partition. ∎

Theorem 2.10.

- 1)

-

2)

If, additionally,

(2.15) where and are from (Z2), is from (B2) and is from (B3), then one can choose such that , i.e. there exists a deterministic constant that does not depend on the partition such that

and

3 One-sided sandwich case

The drift-implicit Euler approximation scheme described in Section 2 for the two-sided sandwich can also be adapted for the one-sided setting that corresponds to Assumptions A on the SDE (0.1). However, in the two-sided sandwich case the process was bounded (which was utilized, e.g., in Lemma 2.6) and, moreover, the behaviour of was similar near both and so that it was sufficient to analyze only one of the bounds. In the one-sided case, each , for , is not a bounded random variable, therefore the approach from Section 2 has to be adjusted. For this, we will be using the inequalities (1.4).

Let the noise satisfy (Z1)–(Z2), and satisfy Assumptions A and be the unique solution of the SDE (1.2). In line with Section 2, we consider a uniform partition of , , , with the mesh such that

| (3.1) |

where is an upper bound for from assumption (A4). The backward Euler approximation is defined in a manner similar to (2.2), i.e.

| (3.2) | ||||

where the second expression is considered as an equation with respect to .

Remark 3.1.

Just as in the two-sided sandwich case, each , , is well defined since the equation

has a unique solution w.r.t. such that for any fixed and any . To understand this, note that assumption (A4) together with (3.1) imply that

| (3.3) |

Second, by (A3),

| (3.4) |

Next, by (A2), for any , we have that

i.e.

Using this, (A4) and the mean value theorem, for any positive

whence

| (3.5) |

Existence and uniqueness of the solution then follows from (3.3)–(3.5).

Remark 3.2.

Similarly to the two-sided sandwich case, the value of for can also be defined via linear interpolation with no changes in formulations of the results and almost no variations in the proofs.

Our strategy for proving the convergence of to will be similar to what we have done in section 2. Therefore we will be omitting the details highlighting only the points which are different from the two-sided sandwich case. We start with some useful properties of and .

Lemma 3.3.

Let satisfy (Z1)–(Z2), Assumptions A hold and the mesh of the partition satisfy (3.1). Then there exist deterministic constants , depending only on , the shape of the drift and , such that

where is from assumption (Z2) and is from assumption (A3). Moreover, there exist constants , that also depend only on , the shape of the drift and such that

for all partitions with the mesh satisfying with and being from (A2).

Proof.

The proof of

is identical to the corresponding one in Lemma 2.4 and will be omitted. Let us prove that

Fix for which is Hölder continuous, consider a partition with the mesh satisfying and fix an arbitrary . Assume that (otherwise the claim of the lemma holds automatically). Put

and observe that for any , where is defined via (1.1). Next, by (A2), for any

i.e. there exists a constant that does not depend on the partition such that

| (3.6) |

Next, observe that, for any , we have

Therefore, using (3.6) and

one can write

where is some positive constant that does not depend on the partition.

Now we want to apply the discrete version of the Gronwall inequality from [20, Lemma A.3]. In order to do that, we observe that

and, for any ,

Now, since , we can write that

and, for all ,

Put

with being the greatest integer less than or equal to and observe that, for all ,

Therefore,

and, for all ,

Using a discrete version of the Gronwall inequality, we now obtain that for all

which ends the proof. ∎

Remark 3.4.

It is clear that constants , , and can be chosen jointly for and , so that the inequalities

and

hold simultaneously with probability 1.

Next, corresponding to Lemma 2.6 in the two-sided case, enjoys Hölder continuity with the Hölder constant being integrable provided that has moments of sufficiently high order. This is summarized in the lemma below.

Lemma 3.5.

Let satisfy (Z1)–(Z2) and assumptions (A1)–(A3) hold.

-

1)

There exists a positive random variable such that with probability 1

-

2)

If, for some ,

(3.7) where and are from (Z2), is from (A2) and is from (A3), then one can choose such that

Proof.

By (1.4),

i.e. with probability 1 , , where

| (3.8) |

and is defined in (1.1). Denote and notice that , , since . Thus, using the same arguments as applied in (2.7), we can write that, with probability 1, for any :

where is from (A2). Now, again by (1.4),

hence with probability 1

where is a positive constant. Now one can put

| (3.9) |

and observe that

whenever (3.7) holds. ∎

Corollary 3.6.

Using Lemma 3.3 and following the proof of Lemma 3.5, it is easy to obtain that, for any partition with the mesh satisfying

| (3.10) |

there is a random variable independent of the partition such that with probability 1

| (3.11) |

Furthermore, just like in Lemma 2.6, for

provided that

Finally, such can be chosen jointly for and , so that

holds simultaneously with (3.11) with probability 1.

Lemma 3.7.

Let satisfy (Z1)–(Z2), Assumptions A hold and the mesh of the partition satisfy (3.1).

-

1)

For any , there exists a positive random variable that does not depend on the partition such that

-

2)

If, additionally,

(3.12) where and are from (Z2), is from (A2) and is from (A3), then one can choose such that , i.e. there exists a deterministic constant that does not depend on the partition such that

Proof.

Now we are ready to formulate the two main results of this section.

Theorem 3.8.

Let satisfy (Z1)–(Z2), Assumptions A hold and the mesh of the partition satisfy (3.10).

-

1)

For any , there exists a random variable that does not depend on the partition such that

-

2)

If, additionally,

where and are from (Z2), is from (A2) and is from (A3), then one can choose such that , i.e. there exists a deterministic constant that does not depend on the partition such that

Proof.

Theorem 3.9.

Let satisfy (Z1)–(Z2), Assumptions A hold and the mesh of the partition satisfy (3.10).

-

1)

For any , there exists a random variable that does not depend on the partition such that

-

2)

If, additionally,

(3.14) where and are from (Z2), is from (A2) and is from (A3), then one can choose such that , i.e. there exists a deterministic constant that does not depend on the partition such that

Proof.

The proof is similar to Theorem 2.10 and is omitted. ∎

4 Examples and simulations

The algorithms presented in (2.2) and (3.2) imply that, in order to generate , one has to solve an equation that potentially can be challenging from the computational point of view. However, in some cases that are relevant for applications this equation has a simple explicit solution.

Regarding the numerical examples that follow, we remark that:

-

1)

all the simulations are performed in the R programming language on the system with Intel Core i9-9900K CPU and 64 Gb RAM;

-

2)

in order to simulate paths of fractional Brownian motion, R package somebm is used;

-

3)

in Example 4.3, discrete samples of the multifractional Brownian motion (mBm) values are simulated using the Cholesky decomposition of the corresponding covariance matrix (for covariance structure of the mBm, see e.g. [5, Proposition 4]) and the R package nleqslv is used for solving (2.2) numerically.

Example 4.1.

(Generalized CIR processes) Let , satisfy (Z1)–(Z2) with , , , , be given and satisfy the SDE of the form

| (4.1) |

This process fits into the framework of Section 3 and the equation for from (3.2) reads as follows:

It is easy to see that it has a unique positive solution

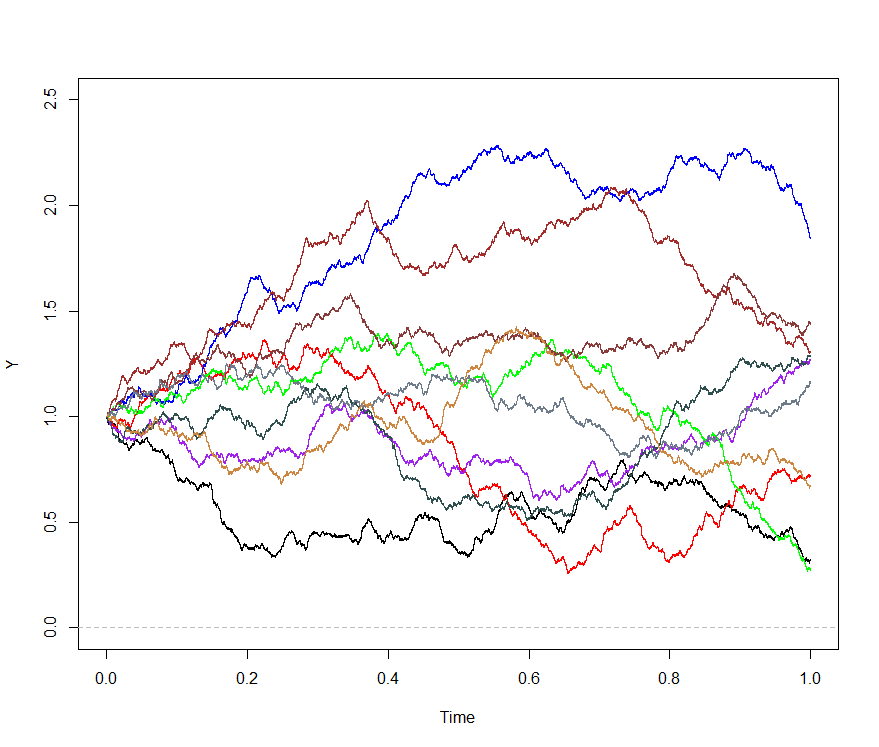

Fig. 1 contains 10 sample paths of the process (4.1) driven by a fractional Brownian motion with . In all simulation we take , and . Based on 10000 simulations, the average time for simulating one path is 0.005388308 seconds.

Note that the drift-implicit Euler scheme for (4.1) driven by the fractional Brownian motion was the main subject of [18] and [22] but in both these works the convergence of to is established only on with being small (see e.g. [18, Eq. (8) and Remark 3.1]). Our results fill this gap and convergence holds on arbitrary for any model parameters.

Example 4.2.

(Sandwiched process of the TSB type) Consider a sandwiched SDE of the form

| (4.2) |

where satisfies (Z1)–(Z2) with . This equation fits into the framework of Section 3 and the scheme (2.2) leads to cubic equations of the form

| (4.3) |

where

Note this equation can be solved explicitly using, e.g., the celebrated Cardano method. Namely, define

and put

where among possible complex values of and one should take those for which . Then the three roots of the cubic equation (4.3) are

and is equal to the root which belongs to (note that there is exactly one root in that interval).

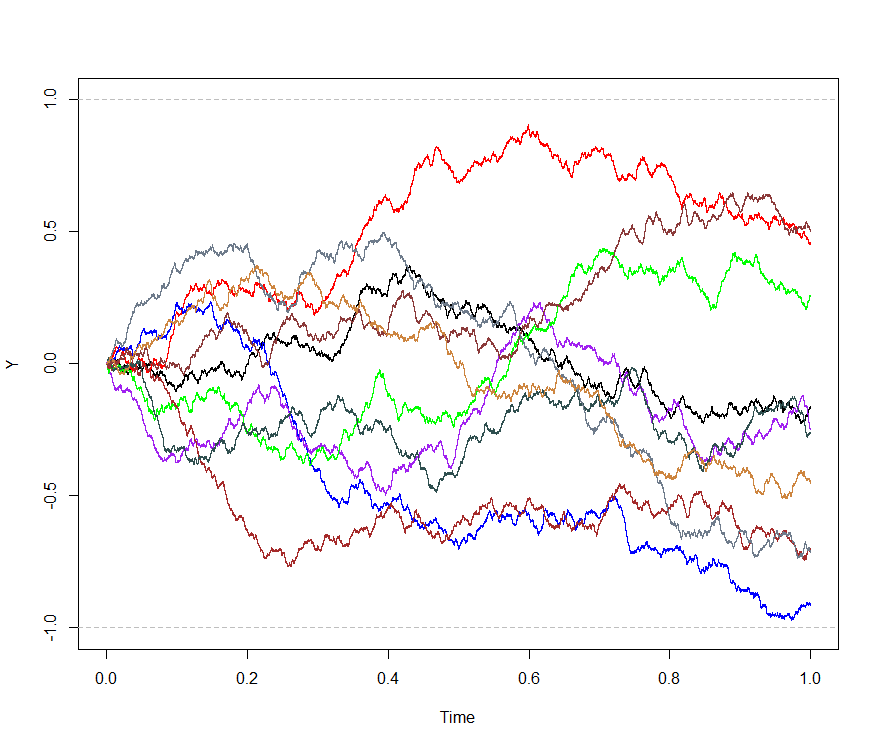

Fig. 2 contains 10 sample paths of the process (4.2) driven by a fractional Brownian motion with . In all simulation we take , and , , (this case corresponds to the TSB equation described in Example 1.7). Simulation is performed by direct implementation of the Cardano’s method in R; based on 10000 simulations, the average time for simulating one path is 0.03700142 seconds.

In both Examples 4.1 and 4.2, equations for computing could be explicitly solved but the Hölder continuity of the noise could not be less then . The next example shows that the drift-implicit Euler scheme can be applied in the rough case as well.

Example 4.3.

(Sandwiched process driven by multifractional Brownian motion) Consider the sandwiched SDE of the form

| (4.4) |

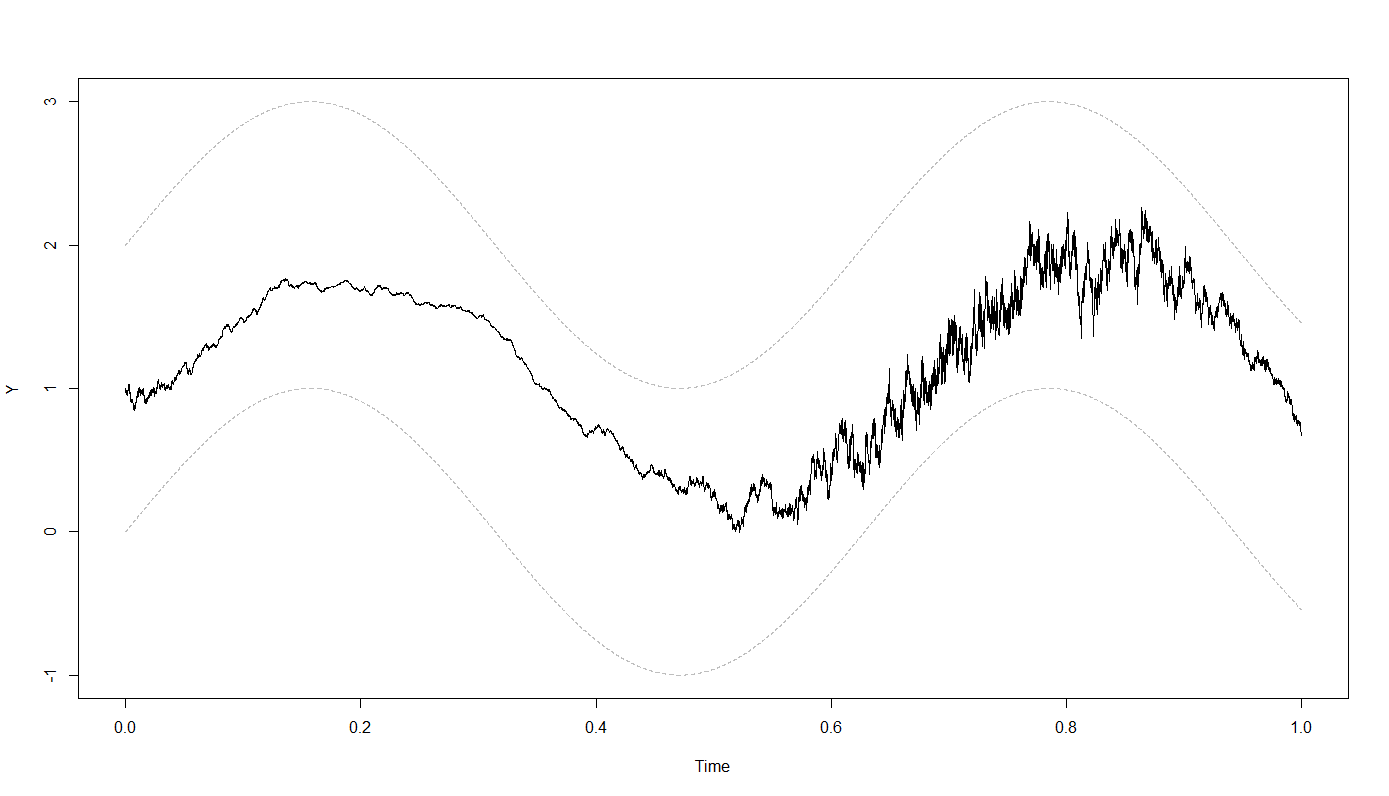

In this case, Theorem 1.1 guarantees existence and uniqueness of the solution for -Hölder with (note that this equation fits the framework of Example 1.8 from Section 1). On Fig. 3, one can see paths of the process (4.4) with , , driven by multifractional Brownian motion (mBm) with functional Hurst parameter (note that the lowest value of the functional Hurst parameter is ). For more details on mBm, see [5] as well as [17, Lemma 3.1] for results on Hölder continuity of its paths. Based on 10000 simulations, the average time for simulating one path is 0.4968714 seconds.

Acknowledgements

The present research is carried out within the frame and support of the ToppForsk project nr. 274410 of the Research Council of Norway with title STORM: Stochastics for Time-Space Risk Models. The second author was supported by Japan Science and Technology Agency CREST JPMJCR21.

References

- [1] Alfi, V., Coccetti, F., Petri, A., and Pietronero, L. Roughness and finite size effect in the NYSE stock-price fluctuations. The European physical journal. B 55, 2 (2007), 135–142.

- [2] Alfonsi, A. On the discretization schemes for the CIR (and Bessel squared) processes. Monte Carlo Methods Appl. 11, 4 (2005), 355–384.

- [3] Alfonsi, A. Strong order one convergence of a drift implicit Euler scheme: application to the CIR process. Statist. Probab. Lett. 83, 2 (2013), 602–607.

- [4] Andersen, L. B. G., and Piterbarg, V. V. Moment explosions in stochastic volatility models. Finance and Stochastics 11, 1 (Sept. 2006), 29–50.

- [5] Ayache, A., Cohen, S., and Vehel, J. L. The covariance structure of multifractional Brownian motion, with application to long range dependence. In 2000 IEEE International Conference on Acoustics, Speech, and Signal Processing. Proceedings (Cat. No.00CH37100) (2002), IEEE.

- [6] Azmoodeh, E., Sottinen, T., Viitasaari, L., and Yazigi, A. Necessary and sufficient conditions for Hölder continuity of Gaussian processes. Statistics & Probability Letters 94 (2014), 230 – 235.

- [7] Bayer, C., Friz, P., and Gatheral, J. Pricing under rough volatility. Quant. Finance 16, 6 (2016), 887–904.

- [8] Chan, K. C., Karolyi, G. A., Longstaff, F. A., and Sanders, A. B. An empirical comparison of alternative models of the short-term interest rate. The journal of finance 47, 3 (1992), 1209–1227.

- [9] Cox, J. C. The constant elasticity of variance option pricing model. The Journal of Portfolio Management 23, 5 (1996), 15–17.

- [10] Cox, J. C., Ingersoll, J. E., and Ross, S. A. A re-examination of traditional hypotheses about the term structure of interest rates. The Journal of Finance 36, 4 (Sept. 1981), 769–799.

- [11] Cox, J. C., Ingersoll, J. E., and Ross, S. A. An intertemporal general equilibrium model of asset prices. Econometrica 53, 2 (Mar. 1985), 363.

- [12] Cox, J. C., Ingersoll, J. E., and Ross, S. A. A theory of the term structure of interest rates. Econometrica 53, 2 (Mar. 1985), 385.

- [13] Dereich, S., Neuenkirch, A., and Szpruch, L. An Euler-type method for the strong approximation of the Cox–Ingersoll–Ross process. Proceedings of the Royal Society A. Mathematical, physical, and engineering sciences 468, 2140 (2012), 1105–1115.

- [14] Di Nunno, G., Mishura, Y., and Yurchenko-Tytarenko, A. Sandwiched SDEs with unbounded drift driven by Hölder noises. ArXiv 2012.11465 (2020).

- [15] Domingo, D., d’Onofrio, A., and Flandoli, F. Properties of bounded stochastic processes employed in biophysics. Stochastic Analysis and Applications 38, 2 (Dec. 2019), 277–306.

- [16] d’Onofrio, A., Ed. Bounded Noises in Physics, Biology, and Engineering. Springer New York, 2013.

- [17] Dozzi, M., Kozachenko, Y., Mishura, Y., and Ralchenko, K. Asymptotic growth of trajectories of multifractional Brownian motion, with statistical applications to drift parameter estimation. Statistical inference for stochastic processes 21, 1 (2018), 21–52.

- [18] Hong, J., Huang, C., Kamrani, M., and Wang, X. Optimal strong convergence rate of a backward Euler type scheme for the Cox–Ingersoll–Ross model driven by fractional Brownian motion. Stochastic Processes and their Applications 130, 5 (2020), 2675 – 2692.

- [19] Hu, Y., Nualart, D., and Song, X. A singular stochastic differential equation driven by fractional Brownian motion. Statistics & Probability Letters 78, 14 (Oct. 2008), 2075–2085.

- [20] Kruse, R. Strong and weak approximation of semilinear stochastic evolution equations. Springer International Publishing, 2014.

- [21] Kubilius, K., and Medžiūnas, A. Positive solutions of the fractional SDEs with non-Lipschitz diffusion coefficient. Mathematics 9, 1 (2020).

- [22] Zhang, S.-Q., and Yuan, C. Stochastic differential equations driven by fractional Brownian motion with locally Lipschitz drift and their implicit Euler approximation. Proceedings of the Royal Society of Edinburgh: Section A Mathematics (2020), 1–27.