Normalized Power Prior Bayesian Analysis

Abstract

The elicitation of power priors, based on the availability of historical data, is realized by raising the likelihood function of the historical data to a fractional power , which quantifies the degree of discounting of the historical information in making inference with the current data. When is not pre-specified and is treated as random, it can be estimated from the data using Bayesian updating paradigm. However, in the original form of the joint power prior Bayesian approach, certain positive constants before the likelihood of the historical data could be multiplied when different settings of sufficient statistics are employed. This would change the power priors with different constants, and hence the likelihood principle is violated.

In this article, we investigate a normalized power prior approach which obeys the likelihood principle and is a modified form of the joint power prior. The optimality properties of the normalized power prior in the sense of minimizing the weighted Kullback-Leibler divergence is investigated. By examining the posteriors of several commonly used distributions, we show that the discrepancy between the historical and the current data can be well quantified by the power parameter under the normalized power prior setting. Efficient algorithms to compute the scale factor is also proposed. In addition, we illustrate the use of the normalized power prior Bayesian analysis with three data examples, and provide an implementation with an R package NPP.

keywords:

Bayesian analysis, historical data, joint power prior, normalized power prior, Kullback-Leibler divergence1 Introduction

In applying statistics to real experiments, it is common that the sample size in the current study is inadequate to provide enough precision for parameter estimation, while plenty of the historical data or data from similar research settings are available. For example, when design a clinical study, historical data of the standard care might be available from other clinical studies or a patient registry. Due to the nature of sequential information updating, it is natural to use a Bayesian approach with an informative prior on the model parameters to incorporate these historical data. Though the current and historical data are usually assumed to follow distributions from the same family, the population parameters may change somewhat over different time and/or experimental settings. How to adaptively incorporate the historical data considering the data heterogeneity becomes a major concern for the informative prior elicitation.

To address this issue, [1], and thereafter [2], [3], and [4] proposed the concept of power priors, based on the availability of historical data. The basic idea is to raise the likelihood function based on the historical data to a power parameter that controls the influence of the historical data. Its relationship with hierarchical models is also shown by [5]. For a comprehensive review of the power prior, we refer the readers to the seminar article [6]. The power parameter can be prefixed according to external information. It is also possible to search for a reasonable level of information borrowing from the prior-data conflict via sensitivity analysis according to certain criteria. For example, [7] suggested the use of deviance information criterion [8] or the logarithm of pseudo-marginal likelihood. The choice of would depend on the criterion of interest.

[3] and [2] generalized the power prior with a fixed to a random by introducing the joint power priors. They specified a joint prior distribution directly for both and , the parameters in consideration, in which an independent proper prior for was considered in addition to the original form of the power prior. Hypothetically, when the initial prior for is vague, the magnitude of borrowing would be mostly determined by the heterogeneity between the historical and the current data. However, under the joint power priors, the posterior distributions vary with the constants before the historical likelihood functions, which violates the likelihood principle [9]. It raises a critical question regarding which likelihood function should be used in practice. For example, the likelihood function based on the raw data and the likelihood function based on the sufficient statistics could differ by a multiplicative constant. This would likely yield different posteriors. Therefore, it may not be appropriate [10]. Furthermore, the power parameter has a tendency to be close to zero empirically, which suggests that much of a historical data may not be used in decision making [11].

In this article, we investigate a modified power prior which was initially proposed by [12] for a random . It is named as the normalized power prior since it includes a scale factor. The normalized power prior obeys the likelihood principle. As a result, the posteriors can quantify the compatibility between the current and historical data automatically, and hence control the influence of historical data on the current study in a more sensible way.

The goals of this work are threefold. First, we review the joint power prior and the normalized power prior that have been proposed in literature. We aim to show that the joint power prior may not be appropriate for a random . Second, we carry out a comprehensive study on properties of the normalized power prior both theoretically and numerically, shed light on the posterior behavior in response to the data compatibility. Finally, we design efficient computational algorithms and provide practical implementations along with three data examples.

2 A Normalized Power Prior Approach

2.1 The Normalized Power Prior

Suppose that is the parameter (vector or scalar) of interest and is the likelihood function of based on the historical data . In this article, we assume that the historical data and current data are independent random samples. Furthermore, denote by the initial prior for . Given the power parameter , [3] defined the power prior of for the current study as

| (2.1) |

The power parameter , a scalar in , measures the influence of historical information on the current study.

The power prior in (2.1) was initially elicited for a fixed . As the value of is not necessarily pre-determined and typically unknown in practice, the full Bayesian approach extends the case to a random by assigning a reasonable initial prior on it. A natural prior for would be a distribution since . [3] constructed the joint power prior of as

| (2.2) |

with the posterior, given the current data , as

| (2.3) |

where denotes the parameter space of . The prior in (2.2) is constructed by directly assigning a prior for jointly [6]. However, if we integrate out in (2.2) we have , which does not equal to . This meant that the initial prior for is updated after one observes the historical data alone. Moreover, in the posterior (2.3), any constant before cannot be canceled out between the numerator and the denominator. This could yield different posteriors if different forms of the likelihood functions are used. For example, the likelihood based on the raw data and the likelihood based on the distribution of sufficient statistics could result in different posteriors. Also, the prior in (2.2) could be improper. Once the historical information is available, a prior elicited from such information would better be proper. Propriety conditions for four commonly used classes of regression models can be found in [3] and [2].

Alternatively, one can first specify a conditional prior distribution on given , then specify a marginal distribution for . The normalizing constant in the first step is therefore a function of . Since is a parameter, this scale factor should not be ignored. Therefore, a modified power prior formulation, called the normalized power prior, was proposed by [12] which included this scale factor. Consequently, for , the normalized power prior is

| (2.4) |

in the region of such that the denominator of (2.4) is finite.

When , the prior in (2.4) is always proper given that is proper, whereas it is not necessarily the case for that of the joint power prior (2.2). More importantly, multiplying the likelihood function in (2.2) by an arbitrary positive constant, which could be a function of , may change the joint power prior, whereas the constant is canceled out in the normalized power prior in (2.4).

Using the current data to update the prior distribution in (2.4), we derive the joint posterior distribution for as

Integrating out from the expression above, the marginal posterior distribution of can be expressed as

| (2.5) |

If we integrate out in (2.4), we obtain a new prior for , a prior that is updated by the historical information,

| (2.6) |

With historical data appropriately incorporated, (2.6) can be viewed as an informative prior for the Bayesian analysis to the current data. Consequently, the posterior distribution of can be written as

Below we describe some variations of the normalized power prior. A primary extension deals with the presence of multiple historical studies. Similar to [3], the prior defined in (2.4) can be easily generalized. Suppose there are historical studies, denote by the historical data for the study, and . The power parameter for each historical study can be different, and we can further assume they follow the same independent initial prior. Let , the normalized power prior of the form (2.4) can be generalized to

This framework would accommodate the potential heterogeneity among historical data sets from different sources or collected at different time points. Data collected over a long period may be divided into several historical data sets to ensure the homogeneity within each data. Examples of implementing the power prior approach using multiple historical studies can be found in [12], [13], [14] and [15].

An important extension is based on the partial borrowing power prior [16, 17], in which the historical data can be borrowed only through some common parameters with fixed . For instance, when evaluating cardiovascular risk in new therapies, priors for only a subset of the parameters are constructed based on the historical data [18]. Below we describe the partial borrowing normalized power prior, which is an extension of the partial borrowing power prior. Let be the parameter of interest in the current study, and let be the parameter in a historical study, where is a subset of the common parameters. Now

| (2.7) |

defines the partial borrowing normalized power prior, where and denote the parameter spaces of and , respectively. In this case, the dimensions of and can be different, which is another advantage of using the prior in (2.7).

In addition, for model with latent variables , one can also extend the fixed borrowing to a random under the normalized power prior framework. Denote the distribution of and assume is the parameter of interest, we have two strategies to construct a power prior for when is fixed. One way is to discount directly on the likelihood of expressed as , where denotes the domain of . The normalized power prior is of the form

| (2.8) |

Another borrowing strategy is to discount the likelihood of conditional on , while is not discounted such that the power prior with fixed has the form . [6] named such a prior partial discounting power prior. We propose its counterpart beyond a fixed , the partial discounting normalized power prior, which is formulated as

| (2.9) |

[6] argued that the partial discounting power prior is preferable due to both practical reasons and computational advantages. Both of the (2.8) and (2.9) can be extended to models with random effects, in which the distribution may depend on additional unknown variance parameters.

Finally, we note that in the complex data analysis practice, the extensions described above might be combined. For example, one can consider a partial borrowing normalized power prior with multiple historical data, where the borrowing is carried out only through some selected mutual parameters. Another example is in [18], where the partial borrowing power prior is used in the presence of latent variables. Further variations for specific problems will be explored elsewhere.

2.2 Computational Considerations in the Normalized Power Prior

For the normalized power prior, the only computational effort in addition to that of the joint power prior is to calculate the scale factor . In some models the integral can be calculated analytically up to a normalizing constant, so can be expressed in closed forms. The posterior sample from can be obtained by first sampling from or , then from , where is without the element. It is typically achieved by using a Metropolis-Hastings algorithm [19] for , followed by Gibbs sampling for each .

However, needs to be calculated numerically in some models. General Monte Carlo methods to calculate the normalizing constant in the Bayesian computation can be applied. Since the integrand includes a likelihood function powered to , we consider the following approach, which best tailored to the specific form of the integral. It is based on a variant of the algorithm in [20] and [21] using the idea of path sampling [22]. The key observation is that can be expressed as an integral of the expected log-likelihood of historical data, where the integral is calculated with respect to a bounded one-dimensional parameter. This identity can be written as

| (2.10) |

which is an adaptive version of the results from [20]. Proof is shown in A. For given , the expectation in (2.10) is evaluated with respect to the density . Therefore the integrand can be calculated numerically if we can sample from . This is the prerequisite to implement the power prior with a fixed power parameter; hence no extra condition is required to calculate using (2.10). By choosing an appropriate sequence of we can approximate the integral numerically.

When sampling from the posterior using the normalized power prior, needs to be calculated for every iteration. [21] suggested that the function can be well approximated by linear interpolation. Since is bounded, it is recommended to calculate a sufficiently large number of the for different on a fine grid before the posterior sampling, then use a piecewise linear interpolation at each iteration during the posterior sampling. In addition to the power prior with fixed , the only computational cost is to determine for selected values of as knots. Details of a sampling algorithm is provided in B.

Sampling from the density can be computationally intensive in some models. Therefore the knots should be carefully selected given limited computational budget. A rule of thumb based on our empirical evidence is to select more grid points close to , to account for the larger deviation from piecewise linearity in when . An example is to use with . Recently, [23] noted that is a strictly convex function but not necessarily monotonic. They design primary grid points by prioritizing the region where the derivative is close to , then use a generalized additive model to interpolate values on a larger grid. In practice, one may consider combining the two strategies above by adding some grid points used by [23] into the original design . In addition, when is not monotone, piecewise linear interpolation with limited number of grid points also needs to be cautious, especially around the region where change signs.

2.3 Normalized Power Prior Approach for Exponential Family

In this section we discuss how to make inference on parameter (scalar or vector-valued) in an exponential family, incorporating both the current data and the historical data . Suppose that the data comes from an exponential family with probability density function or probability mass function of the form [24]

| (2.11) |

where the dimension of is no larger than . Here and are real-valued functions of the observation , and are real-valued functions of the parameter . Define . Furthermore, define

| (2.12) |

as the compatibility statistic to measure how compatible a sample is with other samples in providing information about . The density function of the current data can be expressed as

| (2.13) |

where and stands for the compatibility statistic related to the current data . Accordingly, the compatibility statistic and the density function similar to (2.12) and (2.13) for the historical data can be defined as well. The joint posterior of can be written as

| (2.14) |

Integrating out from (2.14), the marginal posterior distribution of is given by

The behavior of the power parameter can be examined from this marginal posterior distribution. Similarly, the marginal posterior distribution of can be derived by integrating out in , but it often does not have a closed form. Instead the posterior distribution of given , and is often in a more familiar form. Therefore we may learn the characteristic of the marginal posterior of by studying the conditional posterior distribution , together with .

In the following subsections we provide three examples of the commonly used distributions, where the posterior marginal density (up to a normalizing constant) of can be expressed in closed forms. It can be extended to many other distributions as well by choosing appropriate initial priors .

2.3.1 Bernoulli Population

Suppose we are interested in making inference on the probability of success from a Bernoulli population with multiple replicates. Assume the total number of successes in the historical and the current data are and respectively, with the corresponding total number of trials and . The joint posterior distribution of and can be easily derived as the result below and the proof is omitted.

Result 1. Assume that the initial prior distribution of follows a distribution, the joint posterior distribution of can be expressed as

where stands for the beta function.

Integrating out in , the marginal posterior distribution of can be expressed as

The conditional posterior distribution of given follows a distribution. However, the marginal posterior distribution of does not have a closed form.

2.3.2 Multinomial Population

As a generalization of the Bernoulli/binomial to categories, in a multinomial population assume we observe historical data and the current data , with each element represents the number of success in that category. Let and . Suppose the parameter of interest is which adds up to 1. We have the following results below.

Result 2. Assume the initial prior of follows a Dirichlet distribution with , the joint posterior of can be expressed as

where stands for the gamma function.

The marginal posterior of can be derived by integrating out as

Similar to the Bernoulli case, the marginal posterior distribution of does not have a closed form. The conditional posterior distribution of given follows a Dirichlet distribution with .

2.3.3 Normal Linear Model and Normal Population

Suppose we are interested in making inference on the regression parameters from a linear model with current data

| (2.15) |

where the dimension of vector is and that of is . Similarly, we assume the historical data has the form , with . Assume that both and are positive definite. Define

Now, let’s consider a conjugate initial prior for as the following. , with , and either has a MVN distribution, which includes the Zellner’s prior [25] or , which is a noninformative prior. Here we assume as a known positive definite matrix. Hence, the initial prior can be written as

| (2.16) |

We have the following theorem whose proof is given in A.

Theorem 2.1.

With the set up above for the normal linear model (2.15) and the initial prior of as in (2.16), suppose the initial prior of is . Then, the following results can be shown.

-

(a)

The normalized power prior distribution of is

where

-

(b)

The marginal posterior density of , given , can be expressed as

where

-

(c)

The conditional posterior distribution of , given , is a multivariate Student t-distribution with location parameters , shape matrix , and the degrees of freedom as

-

(d)

The conditional posterior distribution of , given , follows an inverse-gamma distribution with shape parameter , and scale parameter .

3 Optimality Properties of the Normalized Power Prior

In investigating the optimality properties of the normalized power priors, we use the idea of minimizing the weighted Kullback-Leibler (KL) divergence [26] that is similar to, but not the same as in [4].

Recall the definition of the KL divergence,

where and are two densities with respect to Lebesgue measure. In [4], a loss function related to a target density , denoted by , is defined as the convex sum of the KL divergence between and two posterior densities. One is the posterior density without using any historical data, denoted by , and the other is the posterior density with the historical and current data equally weighted, denoted by . The loss is defined as

where the weight for is . It is showed that, when is given, the unique minimizer of is the posterior distribution derived using the power prior, i.e.,

Furthermore, [4] claim that the posterior derived from the joint power prior also minimizes when is random.

We look into the problem from a different angle. Since the prior for without the historical data is with , we further denote the prior for when fully utilizing the historical data as , with . Clearly

| (3.1) |

where is a normalizing constant.

Suppose we have a prior . For any function , define the expected weighted KL divergence between and , and between and as

| (3.2) |

where . We have the following theorem whose proof is given in A.

Theorem 3.2.

Note that the last claim in Theorem 3.2 comes from

The assumption of indicates that the original prior of does not depend on , which is reasonable.

4 Posterior Behavior of the Normalized Power Prior

In this section we investigate the posteriors of both and under different settings of the observed statistics. We show that by using the normalized power prior, the resulting posteriors can respond to the compatibility between and in an expected way. However, the posteriors are sensitive to different forms of the likelihoods under same data and model using the joint power priors.

4.1 Results on the Marginal Posterior Mode of the Power Parameter

Some theoretical results regarding the relationship between the posterior mode of and the compatibility statistic defined in (2.12) are given as follows. Their proofs are given in A.

Theorem 4.3.

Suppose that historical data and current data are two independent random samples from an exponential family given in (2.11). The compatibility statistic for and are and respectively as defined in (2.12). Then the marginal posterior mode of is always under the normalized power prior approach, if

| (4.1) |

for all , where

and

The first term in (4.1) is always non-negative if the prior of is a nondecreasing function. Hence, if one uses uniform prior on , this term is zero. The second term, , is always non-negative by using the property of KL divergence. It is 0 if and only if , which means given and , current data does not contribute to any information for . This could be a rare case. The third term in (4.1) depends on how close and are to each other. When , the third term is zero, and hence the posterior mode of is 1. Since is non-negative, the posterior mode of may also achieve as long as the difference between and is negligible from a practical point of view. On the other hand, for the joint power prior approach, we have the following result.

Theorem 4.4.

Suppose that current data comes from a population with density function , and is a related historical data. Furthermore, suppose that the initial prior is a non-increasing function and the conditional posterior distribution of given is proper for any . Then for any and , if

| (4.2) |

then there exists at least one positive constant such that has mode at under the joint power prior, where .

The assumption in (4.2) is valid in the case that all the integrals are finite positive values when is either 0 or 1. Usually this condition satisfies when is smooth. The proof of this result is also given in the A. For a normal or a Bernoulli population, our research reveals that has mode at in many scenarios regardless of the level of compatibility between and . Note that the results in Theorem 4.4 is not limited to exponential family distributions.

A primary objective of considering as random is to let the posterior inform the compatibility between the historical and the current data, given a vague initial prior on . This allows adaptive borrowing according to the prior-data conflict. Theorem 4.3 indicates that, when the uniform initial prior of is used, the posterior of could potentially suggest borrowing more information from as long as is compatible with . In practice, this has the potential to reduce the sample size required in in the design stage, and to provide estimates with high precision in the analysis stage. Theorem 4.4 shows that, on the other hand, if one considers the joint power prior with an arbitrary likelihood form and a smooth initial prior , it is possible that the posterior of could not inform the data compatibility. This suggests the opposite, meaning that adaptive borrowing might not be true when using the joint power prior; see Section 4.2 for more details.

4.2 Posteriors of Model Parameters

We investigate the posteriors of all model parameters in Bernoulli and normal populations, to illustrate that different forms of the likelihoods could result in different posteriors, which affects the borrowing strength.

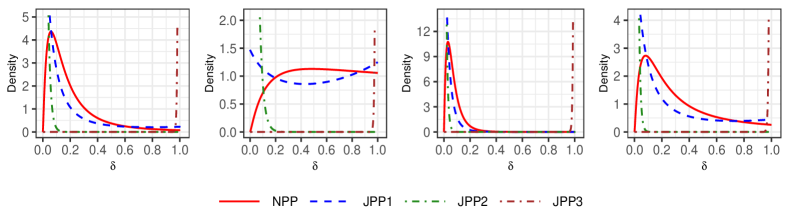

For independent Bernoulli trials, two different forms of the likelihood functions are commonly used. One is based on the product of independent Bernoulli densities such that , and another is based on the sufficient statistic, the summation of the binary outcomes, which follows a binomial distribution , where . Assuming , the corresponding posteriors are

and

respectively. After marginalization we have

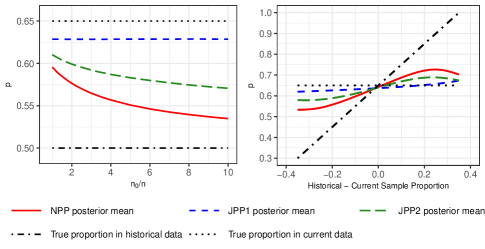

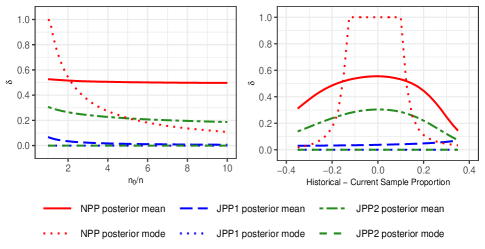

We denote these two scenarios as JPP1 and JPP2 in Figure 1.

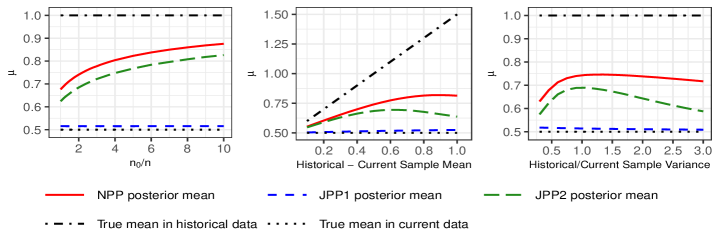

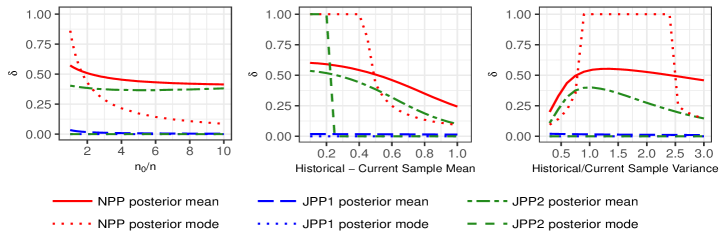

For the normal population, we also consider two different forms of the likelihood functions. One uses the product of independent normal densities

where is the value of the observation in . Another less frequently used form is the density of sufficient statistics , where and are the sample mean and variance of , respectively. Since and , so under the shape-scale parameterization. Then

where .

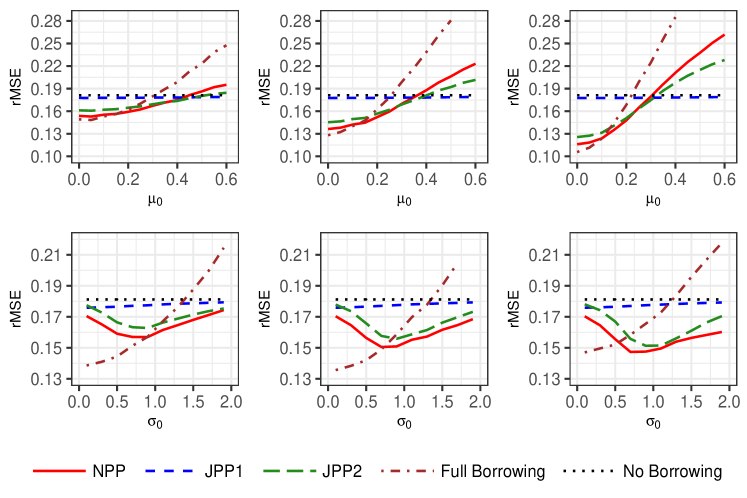

Similar to the Bernoulli case, we can easily derive their joint power priors and the corresponding posteriors denoted as JPP1 and JPP2. As a result, their log posteriors are differed by . In the numerical experiment we use a as the initial prior for , and the reference prior [27] as the initial prior for .

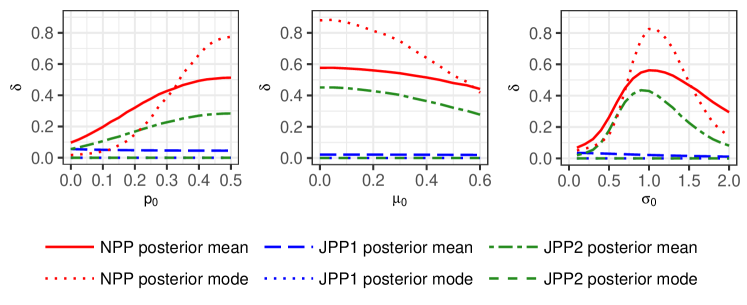

Figure 1 shows how the posteriors of and change with and in data simulated from the Bernoulli population, in which a is used as the initial prior for both and . Figure 2 shows how the posterior of and change with , (for fixed and ), and (for fixed and ) in the normal population.

From both Figures 1 and 2, we observe, under the normalized power prior, the posterior mean of the parameter of interest ( in the Bernoulli population and in the normal population) are sensitive to the change of compatibility between and . As the difference between the observed sample average of and increases, the posterior mean of both and are getting closer to the parameter estimate based on at the beginning, then going back to the parameter estimate based on . For increasing , the posterior mean are getting closer to the parameter estimate based on . Both of the posterior mean and mode of respond to the compatibility between and as expected. In addition, when the two samples are not perfectly homogeneous, the posterior mode of can still attain . This is reasonable because the historical population is subjectively believed to have similarity with the current population with a modest amount of heterogeneous. These findings imply that the power parameter responds to data in a sensible way in the normalized power prior approach.

When using the joint power prior approach, we observe that the posteriors of the parameters , and behave differently with different forms of the likelihoods. Despite a violation of the likelihood principle, the joint power prior might provide moderate adaptive borrowing under certain form of the likelihood. The degree of the adaptive borrowing is less than using the normalized power prior. Under another likelihood form in our illustration, the posteriors suggest almost no borrowing, regardless of how compatible these two samples are.

5 Behavior of the Square Root of Mean Square Error under the Normalized Power Prior

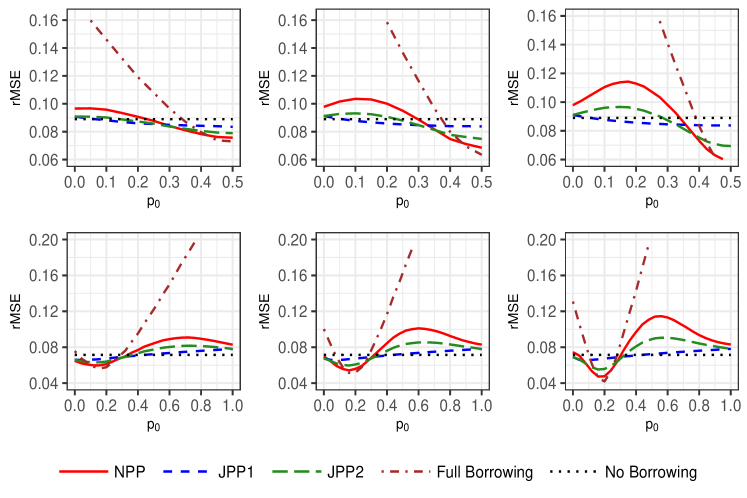

We now investigate the influence of borrowing historical data in parameter estimation using the square root of the mean square error (rMSE) as the criteria. Several different approaches are compared, including the full borrowing (pooling), no borrowing, normalized power prior, and joint power prior. Two different likelihood forms are used for in the joint power priors, with the same notation as in Section 4. The rMSE obtained by the Monte Carlo method, defined as , is used for comparison, where is the number of Monte Carlo samples, is the true parameter and is the estimate in the sample. We choose in all experiments.

5.1 Bernoulli Population

We first compute the rMSE of estimated in independent Bernoulli trials, where is the probability of success in the current population. Suppose the current data comes from a binomial(, ) distribution and the historical data comes from a binomial(, ) distribution, with both and unknown. The posterior mean of is used as the estimate. In the simulation experiment we choose , or , and or . We use the as the initial prior for both and .

Based on the results in Figure 3, the normalized power prior approach yields the rMSE comparable to the full borrowing when the divergence between the current and the historical population is small or mild. As increases from , both the posterior mean and the mode of will decrease on average. The rMSE of the posterior mean of will increase with when is near . As the further increases, the posterior mean and mode of will automatically drop toward (Figure 5), so the rMSE will then decrease and eventually drop to the level comparable to no borrowing. Also, when is small, the rMSE will decrease as increase, which implies when the divergence between the current and the historical populations is mild, incorporating more historical data would result in better estimates using the normalized power prior. However, when is large, the rMSE will increase with in most scenarios. All plots from Figures 3 and 5 indicate that the normalized power prior approach provides adaptive borrowing.

For the joint power prior approaches, the prior with the likelihood expressed as the product of independent Bernoulli densities is similar to no borrowing while using the prior based on a binomial likelihood tends to provide some adaptive borrowing, with less information incorporated than using the normalized power prior. This is consistent with what we observed regarding their posteriors in Section 4.

5.2 Normal Population

We also investigate the rMSE of estimated in a normal population with unknown variance. Suppose that the current and historical samples are from normal and populations respectively, with both mean and variance unknown. Furthermore, the population mean is the parameter of interest, and the posterior mean is used as the estimate of .

It can be shown that the marginal posterior distribution of only depends on , , , and , and so does the rMSE. Therefore we design two simulation settings, with , , , and or under both settings. In the first experiment we fix , the heterogeneity is reflected by varying and therefore . In the second experiment, we fix so is fixed at . We change at various levels resulting in changes in .

Figures 4 and 5 display the results. The trend of the rMSE in the normalized power prior is generally consistent with the findings in a Bernoulli population. For the joint power prior approaches, the one with the likelihood based on the original data is similar to no borrowing. The one based on the product of densities using sufficient statistics tends to provide some adaptive borrowing, while less information is incorporated than using the normalized power prior. We conclude that the normalized power prior can also provide adaptive borrowing under the normal population.

6 Applications

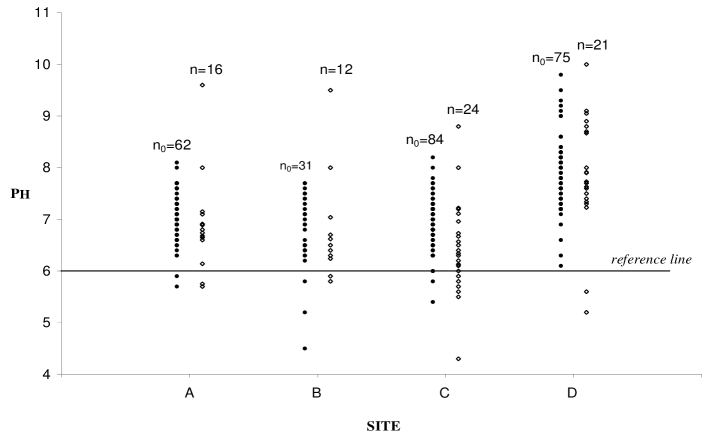

6.1 Water-Quality Assessment

In this example, we use measurements of pH to evaluate impairment of four sites in Virginia individually. pH data collected over a two-year or three-year period are treated as the current data, while pH data collected over the previous nine years represents one single historical data. Of interest is the determination of whether the pH values at a site indicate that the site violates a (lower) standard of more than of the time. For each site, larger sample size is associated with the historical data and smaller with the current data. We apply the normalized power prior approach, a traditional Bayesian approach for current data only using the reference prior, and the joint power prior approaches. Assume that the measurements of water quality follow a normal distribution, and for ease of comparison, the normal model with a simple mean is considered. Since the data is used as an illustration to implement the normalized power prior, other factors, such as spatial and temporal features, are not considered. The current data and historical data are plotted side by side for each site in Figure 6. A violation is evaluated using a Bayesian test of

where is the lower percentile of the distribution for pH.

Site Current Historical Posterior probability of data data (s.d. of ) mean mean Reference Normalized Joint power prior (s.d.) (s.d.) prior power prior (1) (2) (3) A 16 6.91 62 7.05 0.177 0.488 0.385 0.201 0.997 (0.90) (0.47) (0.34) (0.26) (0.31) (0.32) (0.09) B 12 6.78 31 6.73 0.069 0.047 0.051 0.070 0.033 (1.03) (0.71) (0.47) (0.26) (0.30) (0.45) (0.17) C 24 6.43 84 6.95 0.001 0.004 0.003 0.002 0.592 (0.88) (0.49) (0.26) (0.24) (0.25) (0.25) (0.08) D 21 7.87 75 7.88 0.865 0.986 0.959 0.886 1.000 (1.11) (0.67) (0.36) (0.25) (0.30) (0.35) (0.11)

Table 1 summarizes the current and the historical data, and the test results using the reference prior analysis (without incorporating historical data), the normalized power prior, and the joint power prior analyses (with reference prior as the initial prior for , i.e, in Section 2.3.3). Similar to Sections 4 and 5, results from the joint power priors are calculated using different likelihood functions: (1) joint density of sufficient statistics; (2) product of independent normal densities; (3) product of independent normal densities multiply by an arbitrary large constant .

The posterior probability of is calculated based on the posterior of , where is the quantile function of a standard normal distribution. If the significance level is used, the Bayesian test using the reference prior and the current data would only indicate site C as impaired. Here we use the posterior probability of as equivalent to the p-value [28]. Using historical data does lead to different conclusions for site B. The test using normalized power prior results in significance for both sites B & C. The test using joint power prior with likelihood (1) results in significance for site C, and the posterior probability of for site B is very close to . In the case of site B, there are around of historical observations below . Hence our prior opinion of the site is suggestive of impairment. Less information is therefore required to declare impairment relative to a reference prior and the result is a smaller p-value. However, if one uses the likelihood function in case (2) of the joint power prior method, the test result is similar to no borrowing. Furthermore, if we use an arbitrary constant as in case (3) of the joint power prior, results will be completely different. The standard deviations of will become very small, and it is similar to a full borrowing; see Figure 7. We will conclude site B impaired, but site C not, due to the strong influence of the historical data.

Hence, this example shows that the inference results are sensitive to the likelihood form in employing the joint power prior. On the other hand, normalized power prior provides adaptive borrowing in all scenarios. It is more reasonable to conclude that both site B and site C are impaired.

6.2 Noninferiority Trial in Vaccine Development

In a vaccine clinical trial, it is commonly required to demonstrate that the new vaccine does not interfere with other routine recommended vaccines concomitantly. In addition to the phase 3 efficacy and safety trials, a noninferiority trial is commonly designed to demonstrate that the effect (in this example, the response rate) of a routine recommended vaccine (vaccine A) can be preserved when concomitantly used with the experimental vaccine (vaccine B). If the differences in the response rate of vaccine A when concomitantly used with vaccine B and the response rate of using vaccine A alone is within a certain prespecified margin, then we may conclude that they do not interfere each other. The prespecified positive margin , known as the noninferiority margin, reflects the maximum acceptable extent of clinical noninferiority in an experimental treatment.

A simple frequentist approach of conducting such noninferiority test is to calculate the confidence interval of , where and are the response rates for test and control groups respectively. Given a positive noninferiority margin , we conclude that the experimental treatment is not inferior to the control if the lower bound of the confidence interval is greater than . When a Bayesian approach is applied, the confidence interval can be replaced by the credible interval (CI) based on the highest posterior density [29].

However, a problem with either the frequentist or the Bayesian approach using noninformative priors is, when the sample size is too small, the confidence interval or the credible interval will become too wide. Therefore inferiority could be inappropriately concluded. For this reason, historical evidence, especially historical data for the control group, can be incorporated. Examples of Bayesian noninferiority trials design based on power prior can be found in [30] and [31].

We illustrate the use of normalized power prior approach to adaptively borrow data from historical controls in the development of RotaTeq, a live pentavalent rotavirus vaccine. A study was designed to investigate the concomitant use of RotaTeq and some routine pediatric vaccines between 2001-2005 [32]. Specifically, the test was conducted to evaluate the anti-polyribosylribitol phosphate response (a measure of vaccination against invasive disease caused by Haemophilus influenzae type b) to COMVAX (a combination vaccine for Haemophilus influenzae type b and hepatitis B), in concomitant use with RotaTeq. Since our goal is to assess whether the experimental vaccine RotaTeq will affect the response rate of the routine recommended COMVAX or not, the endpoint is the response rate of COMVAX. The per-protocol population included subjects from the test group (COMVAX+RotaTeq) and 592 from the control group (COMVAX+placebo).

Since COMVAX was used for a few years, data from historical trials with similar features can be incorporated. Table 2 provides a summary of the available datasets [32]. We pool the four historical data sets, and applying (1) non-informative Bayesian analysis with Jeffrey’s prior; (2) joint power prior with the likelihood written as the product of Bernoulli densities, denoted as JPP1; (3) joint power prior with likelihood written as the binomial density, denoted as JPP2; (4) normalized power prior. Results are summarized in Table 3.

Study Study Years N Responders Response Rate Historical Studies Study 1 1992-1993 576 417 72.4% Study 2 1993-1995 111 90 81.1% Study 3 1993-1995 62 49 79.9% Study 4 1997-2000 487 376 77.2% Current Study Control 2001-2005 592 426 72.0% Test 2001-2005 558 415 74.4%

Since the normalized power prior incorporates the most information from the control group of the historical studies, its 95% CI of is the shortest. On the other hand, using the joint power prior with the product of Bernoulli densities as the likelihood results in almost no borrowing, while using a binomial density as the likelihood will slightly improves the borrowing. Since the average response rate in historical controls are slightly larger than that of the current control, the estimated response rate of the control group is the largest under the normalized power prior. This will result in a more conservative decision making when concluding noninferiority. Under a commonly used noninferiority margin , we can conclude noninferiority under all approaches, but in very rare cases, when a smaller margin is chosen, say , the noninferiority might be questionable when considering more historical information with a normalized power prior.

The posterior distribution of is skewed, therefore the posterior mean is not close to the posterior mode of . In the normalized power prior approach, the posterior mean of is , indicating that on average, approximately subjects are borrowed from the historical data. On the other hand, if one considers the power prior with a fixed for ease of interpretation, the posterior mode and posterior mean of can serve as the guided values, since they provide some useful information regarding the data compatibility. For example, considering a fixed in practice might be anti-conservative, while a fixed might be too conservative from the prior-data conflict point of view.

| Prior | CI for | Mode of | ||

|---|---|---|---|---|

| Jeffrey’s Prior | 71.92 | - | - | |

| JPP1 | 71.93 | 0.001 | 0 | |

| JPP2 | 72.68 | 0.166 | 0 | |

| NPP | 73.50 | 0.482 | 0.181 |

6.3 Diagnostic Test Evaluation

The U.S. Food and Drug Administration (FDA) has released a guidance222the complete version of the guidance can be freely downloaded at: https://www.fda.gov/media/71512/download [Accessed 03 June 2019]. for the use of Bayesian methods in medical device clinical trials. This guidance specifies that the power prior could be one of the methodologies to borrow strength from other studies. In this example, the proposed normalized power prior is applied to evaluate the diagnostic test for spontaneous preterm delivery (SPD). The binary diagnostic test may result in one of the four possible outcomes: true positive (Cell 1), false positive (Cell 2), false negative (Cell 3) and true negative (Cell 4); see Table 4. Let denote the cell probabilities and let denote the corresponding number of subjects in Table 4. The sensitivity and specificity of a test can be expressed in terms of the cell probabilities as

respectively, where stands for disease status and stands for test status.

| Disease status | ||||

|---|---|---|---|---|

| Yes | No | |||

| Test positive | Cell 1 (TP) | Cell 2 (FP) | ||

| Test negative | Cell 3 (FN) | Cell 4 (TN) | ||

A simple frequentist approach to evaluate such binary test is to compute the 95% confidence intervals of and , denoted by and . Then we compare the lower bounds and to the value of 50% which is the sensitivity and specificity of a random test. We may conclude that the diagnostic test outweighs a random test on the diseased group if is greater than 50%. Similarly, the diagnostic test outweighs a random test on non-diseased group if is greater than 50%.

In practice, however, the diseased group’s data are difficult to collect leading to a relatively small . As a result, the confidence interval of tends to be too wide to make any conclusions. For the purpose of this agreement, the sequential Bayesian updating and the power prior can be used to incorporate the historical/external information.

A diagnostic test based on a medical device (PartoSure Test-P160052) was developed to aid in rapidly assess the risk of spontaneous preterm delivery within 7 days from the time of diagnosis in pre-pregnant women with signs and symptoms333the dataset used in this example is freely available at: https://www.accessdata.fda.gov/cdrh_docs/pdf16/P160052C.pdf [Accessed 03 June 2019].. Table 5 lists the dataset of 686 subjects from the US study and the dataset of 511 subjects from the European study. The test was approved by FDA based on the US study, so the European study is regarded as the external information in this example. The joint power prior (with the full multinomial likelihood), the normalized power prior, no borrowing and full borrowing are applied, with Jeffrey’s prior as the initial prior for . Table 6 summarizes the results. It is found that the posterior mean under the power prior is always between the posterior mean of no borrowing and full borrowing. Also, the result of using joint power prior is close to the one of no borrowing since only of the external information is incorporated on average. Using the normalized power prior will on average increase the involved external information to , making its result closer to the full borrowing. In practice, the posterior mean of (e.g, and ) could be important to clinicians because it not only reflects the information amount that is borrowed, but also indicates the average sample size (e.g., and ) that is incorporated. The joint power prior suggests very little borrowing while the normalized power prior suggests a moderate level of borrowing. In general, these two data sets are compatible since they have similar sensitivity ( and ) and specificity ( and ). The value obtained by the normalized power prior is more persuasive and reflects the data compatibility.

US study Disease status European study Disease status Yes No Total Yes No Total Test positive 3 11 14 Test positive 9 20 29 Test negative 3 669 672 Test negative 9 473 482 Total 6 680 686 Total 18 493 511

Prior 95% CI for (%) 95% CI for (%) Mode of Fixed 50.04 (16.67, 82.80) 98.31 (97.32, 99.22) - - Fixed 49.85 (31.40, 68.70) 97.32 (96.38, 98.17) - - JPP 49.98 (18.94, 83.05) 98.24 (97.27, 99.18) 0.044 0 NPP 49.88 (21.60, 78.84) 98.02 (96.93, 99.00) 0.216 0.085

7 Summary and Discussion

As a general class of the informative priors for Bayesian inference, the power prior provides a framework to incorporate data from alternative sources, whose influence on statistical inference can be adjusted according to its availability and its discrepancy between the current data. It is semi-automatic, in the sense that it takes the form of raising the likelihood function based on the historical data to a fractional power regardless of the specific form of heterogeneity. As a consequence of using more data, the power prior has advantages in terms of the estimation with small sample sizes. When we do not have enough knowledge to model such heterogeneity and cannot specify a fixed power parameter in advance, a power prior with a random is especially attractive in practice.

In this article we provide a framework of using the normalized power prior approach, in which the degree of borrowing is dynamically adjusted through the prior-data conflict. The subjective information about the difference in two populations can be incorporated by adjusting the hyperparameters in the prior for , and the discrepancy between the two samples is automatically taken into account through a random . Theoretical justification is provided based on the weighted KL divergence. The controlling role of the power parameter in the normalized power prior is adjusted automatically based on the congruence between the historical and the current samples and their sample sizes; this is shown using both the analytical and numerical results. On the other hand, we revisit some undesirable properties of using the joint power prior for a random ; this is shown by theoretical justifications and graphical examples. Efficient algorithms for posterior sampling using the normalized power prior are also discussed and implemented.

We acknowledge when is considered random and estimated with a Bayesian approach, the normalized power prior is more appropriate. The violation of likelihood principle under the joint power prior was discussed in [12] and [10]. However, a comprehensive study on the joint power prior and the normalized power prior is not available in literature. As a result, the joint power priors with random were still used afterwards, for example, [33], [13], [30], and [34]. This might partially due to the fact that the undesirable behavior of the joint power priors were not fully studied and recognized. Although under certain likelihood forms, the joint power priors would provide limited adaptive borrowing, its mechanism is unclear. We conclude that the joint power prior is not recommended with a random .

On the other hand, the power prior with fixed is widely used in both clinical trial design and observational studies. It can be viewed as a special case of the normalized power prior with initial prior of coming from a degenerate distribution. We conjecture that a similar sensitivity analysis used in a power prior with fixed [6] might be carried out to search for the initial prior of in the normalized power prior context. Since the normalized power prior generalizes the power prior with fixed, most inferential results in power prior with fixed could be easily adopted. Further studies will be carried out elsewhere.

Disclaimer

This article represents the views of the authors and should not be construed to represent FDA’s views or policies.

Acknowledgements

We warmly thank the anonymous referees and the associate editor for helpful comments and suggestions that lead to an improved article. This work is partially supported by “the Fundamental Research Funds for the Central Universities” in UIBE(CXTD11-05) and a research grant by College of Business at University of Texas at San Antonio.

References

- Ibrahim and Chen [1998] J. G. Ibrahim, M.-H. Chen, Prior distributions and bayesian computation for proportional hazards models, Sankhya: The Indian Journal of Statistics, Series B (1998) 48–64.

- Chen et al. [2000] M.-H. Chen, J. G. Ibrahim, Q.-M. Shao, Power prior distributions for generalized linear models, Journal of Statistical Planning and Inference 84 (2000) 121–137.

- Ibrahim and Chen [2000] J. G. Ibrahim, M.-H. Chen, Power prior distributions for regression models, Statistical Science 15 (2000) 46–60.

- Ibrahim et al. [2003] J. G. Ibrahim, M.-H. Chen, D. Sinha, On optimality properties of the power prior, Journal of the American Statistical Association 98 (2003) 204–213.

- Chen and Ibrahim [2006] M.-H. Chen, J. G. Ibrahim, The relationship between the power prior and hierarchical models, Bayesian Analysis 1 (2006) 551–574.

- Ibrahim et al. [2015] J. G. Ibrahim, M.-H. Chen, Y. Gwon, F. Chen, The power prior: Theory and applications, Statistics in Medicine 34 (2015) 3724–3749.

- Ibrahim et al. [2012] J. G. Ibrahim, M.-H. Chen, H. Chu, Bayesian methods in clinical trials: a bayesian analysis of ecog trials e1684 and e1690, BMC Medical Research Methodology 12 (2012) 183.

- Spiegelhalter et al. [2002] D. J. Spiegelhalter, N. G. Best, B. P. Carlin, A. Van Der Linde, Bayesian measures of model complexity and fit, Journal of the Royal Statistical Society: Series B 64 (2002) 583–639.

- Birnbaum [1962] A. Birnbaum, On the foundations of statistical inference, Journal of the American Statistical Association 57 (1962) 269–306.

- Neuenschwander et al. [2009] B. Neuenschwander, M. Branson, D. J. Spiegelhalter, A note on the power prior, Statistics in Medicine 28 (2009) 3562–3566.

- Neelon and O’Malley [2010] B. Neelon, A. O’Malley, Bayesian analysis using power priors with application to pediatric quality of care, Journal of Biometrics & Biostatistics 1 (2010) 103.

- Duan et al. [2006] Y. Duan, K. Ye, E. P. Smith, Evaluating water quality using power priors to incorporate historical information, Environmetrics 17 (2006) 95–106.

- Gamalo et al. [2014] M. A. Gamalo, R. C. Tiwari, L. M. LaVange, Bayesian approach to the design and analysis of non-inferiority trials for anti-infective products, Pharmaceutical Statistics 13 (2014) 25–40.

- Gravestock and Held [2019] I. Gravestock, L. Held, Power priors based on multiple historical studies for binary outcomes, Biometrical Journal (2019) 1201–1218.

- Banbeta et al. [2019] A. Banbeta, J. van Rosmalen, D. Dejardin, E. Lesaffre, Modified power prior with multiple historical trials for binary endpoints, Statistics in Medicine 38 (2019) 1147–1169.

- Ibrahim et al. [2012] J. G. Ibrahim, M.-H. Chen, H. A. Xia, T. Liu, Bayesian meta-experimental design: Evaluating cardiovascular risk in new antidiabetic therapies to treat type 2 diabetes, Biometrics 68 (2012) 578–586.

- Chen et al. [2014a] M.-H. Chen, J. G. Ibrahim, D. Zeng, K. Hu, C. Jia, Bayesian design of superiority clinical trials for recurrent events data with applications to bleeding and transfusion events in myelodyplastic syndrome, Biometrics 70 (2014a) 1003–1013.

- Chen et al. [2014b] M.-H. Chen, J. G. Ibrahim, H. A. Xia, T. Liu, V. Hennessey, Bayesian sequential meta-analysis design in evaluating cardiovascular risk in a new antidiabetic drug development program, Statistics in Medicine 33 (2014b) 1600–1618.

- Chib and Greenberg [1995] S. Chib, E. Greenberg, Understanding the metropolis-hastings algorithm, The American Statistician 49 (1995) 327–335.

- Friel and Pettitt [2008] N. Friel, A. N. Pettitt, Marginal likelihood estimation via power posteriors, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 70 (2008) 589–607.

- Van Rosmalen et al. [2018] J. Van Rosmalen, D. Dejardin, Y. van Norden, B. Löwenberg, E. Lesaffre, Including historical data in the analysis of clinical trials: Is it worth the effort?, Statistical Methods in Medical Research 27 (2018) 3167–3182.

- Gelman and Meng [1998] A. Gelman, X.-L. Meng, Simulating normalizing constants: From importance sampling to bridge sampling to path sampling, Statistical Science 13 (1998) 163–185.

- Carvalho and Ibrahim [2020] L. M. Carvalho, J. G. Ibrahim, On the normalized power prior, arXiv:2004.14912 v1 (2020) 1–31.

- Casella and Berger [2002] G. Casella, R. L. Berger, Statistical Inference, 2nd ed., Duxbury Pacific Grove, CA, 2002.

- Zellner [1986] A. Zellner, On Assessing Prior Distributions and Bayesian Regression Analysis with g-Prior Distributions, Elsevier, New York., 1986.

- Kullback and Leibler [1951] S. Kullback, R. A. Leibler, On information and sufficiency, The Annals of Mathematical Statistics 22 (1951) 79–86.

- Berger and Bernardo [1992] J. O. Berger, J. M. Bernardo, On the development of reference priors, 1992.

- Berger [2013] J. O. Berger, Statistical Decision Theory and Bayesian Analysis, Springer Science & Business Media, 2013.

- Gamalo et al. [2011] M. A. Gamalo, R. Wu, R. C. Tiwari, Bayesian approach to noninferiority trials for proportions, Journal of Biopharmaceutical Statistics 21 (2011) 902–919.

- Lin et al. [2016] J. Lin, M. Gamalo-Siebers, R. Tiwari, Non-inferiority and networks: Inferring efficacy from a web of data, Pharmaceutical Statistics 15 (2016) 54–67.

- Li et al. [2018] W. Li, M.-H. Chen, X. Wang, D. K. Dey, Bayesian design of non-inferiority clinical trials via the bayes factor, Statistics in Biosciences 10 (2018) 439–459.

- Liu [2018] G. F. Liu, A dynamic power prior for borrowing historical data in noninferiority trials with binary endpoint, Pharmaceutical Statistics 17 (2018) 61–73.

- Zhao et al. [2014] Y. Zhao, J. Zalkikar, R. C. Tiwari, L. M. LaVange, A bayesian approach for benefit-risk assessment, Statistics in Biopharmaceutical Research 6 (2014) 326–337.

- Zhang et al. [2019] J. Zhang, C.-W. Ko, L. Nie, Y. Chen, R. C. Tiwari, Bayesian hierarchical methods for meta-analysis combining randomized-controlled and single-arm studies, Statistical Methods in Medical Research 28 (2019) 1293–1310.

- Gelman et al. [2013] A. Gelman, J. B. Carlin, H. S. Stern, D. B. Dunson, A. Vehtari, D. B. Rubin, Bayesian Data Analysis, 3rd ed., Chapman and Hall/CRC, 2013.

- Carpenter et al. [2017] B. Carpenter, A. Gelman, M. D. Hoffman, D. Lee, B. Goodrich, M. Betancourt, M. Brubaker, J. Guo, P. Li, A. Riddell, Stan: A probabilistic programming language, Journal of Statistical Software 76 (2017) 1–32.

Appendix A Proofs and Theorems

Proof of Identity (2.10):

Taking derivative of

with respect to we have:

So the equation (2.10) can be obtained by

integrating with respect to .

Proof of Theorem 2.1: To prove the Theorem 2.1, we first state two simple identities of linear algebra and multivariate integral without proof. For positive-definite matrices and , and vectors , , and ,

| (A.1) |

On the other hand, for being a positive-definite matrix, and vectors, with positive constants , and where ,

| (A.2) |

For the current data , the likelihood function of using (2.15) can be written as

where is defined in Section 2.3.3. Accordingly, adding subscript to data and all other quantities except for the parameters would give similar form to .

- (a)

-

(b)

Since

where is defined in Theorem 2.1 (b), and

where , using the normalized power prior in (a), the posterior is of the form

Marginalizing out, we obtain

where . Plugging in we get (b).

-

(c)

Integrating out from the joint posterior, we have

where and are defined above in the proof of part (b). The conditional distribution of given satisfies

where This is the kernel of a multivariate Student t-distribution with parameters specified in Theorem 2.1 (c).

-

(d)

Using Gaussian integral we can marginalize out from the joint posterior, then

where is defined in the proof of part (b). Conditional on , is an inverse-gamma kernel with parameters specified in Theorem 2.1 (d).

Proof of Theorem 3.2:

The quantity in (3.2) can be written as

| (A.3) |

where

| (A.4) |

is defined in (3.1), and is the denominator in (A.4). The second term of (A) in the last line is not related to , and the inside KL divergence in the first term is clearly minimized when .

Proof of Theorem 4.3:

Applying the property of the KL divergence between two distributions,

with equality held if and only if , we conclude that

| (A.5) |

with equality held if and only if . In (A), is a marginal density that does not depend on and hence its related term is 0 since both and are proper.

In order to show that the marginal posterior mode of is 1, it is sufficient to show that the derivative of in (2.5) is non-negative. Using certain algebra similar to the proof of identity (2.10), we obtain

| (A.6) |

Since we are dealing with the exponential family with the form (2.11) and (2.13), considering the likelihood ratio we have

| (A.7) |

Proof of Theorem 4.4:

Suppose that is an arbitrary positive constant. We take the likelihood function of the form , then and . For the original joint power prior, the marginal posterior distribution of can be rewritten as

| (A.8) |

To prove that the marginal posterior mode of is , it is sufficient to show that the derivative of with respect to is non-positive for any .

The derivative contains two parts. The first part is the derivative on . If is non-increasing as described in the theorem, this part is non-positive. The second part is the derivative in the integral part in (A). An equivalent condition to guarantee this part non-positive is

| (A.9) |

assuming that the derivative and integral are interchangeable.

If we take

then the sufficient condition in (A) for the marginal posterior mode of being is met for any .

Appendix B MCMC Sampling Scheme

B.1 Algorithm for Posterior Sampling

Here we describe an algorithm in detail that is applicable in models when is free of any numerical integration, and the full conditional for each is readily available.

Let denote the parameters of interest in the model, and is with the element removed. The initial prior can be chosen so that the full conditional posterior of each , the , can be sampled directly using the Gibbs sampler [Gelman et al., 2013]. However, neither the full conditional posterior nor the marginal posterior is readily available. Given that is known up to a normalizing constant, the Metropolis-Hastings algorithm [Chib and Greenberg, 1995] is implemented. Here we illustrate the use of a random-walk Metropolis-Hastings algorithm with Gaussian proposals for , which converges well empirically. Let denotes the proposal distribution for in the current iteration, given its value in the previous iteration is . The algorithm proceeds as follows:

-

Step 0:

Choose the initial values for the parameters and , set the tuning constant as , and iteration index .

-

Step 1:

The Metropolis-Hastings step. Simulate and . Compute and the acceptance probability . After applying a change of variable, we have

Then set , if . Otherwise, set .

-

Step 2:

The Gibbs sampling step. For , independently sample from its full conditional posterior .

-

Step 3:

Increase by , and repeat steps and until the states have reached the equilibrium distribution of the Markov chain.

Since , an independent proposal from a beta distribution might also provide good convergence. In such cases, the proposal distribution will be the same beta distribution evaluated at and in the nominator and denominator respectively.

B.2 Algorithm to Compute the Scale Factor

Here we describe an algorithm in detail when the scale factor in the denominator, needs to be calculated numerically. From identity (2.10), , so we only need to calculate the one-dimensional integral.

MCMC samples from with fixed can be easily drawn, since the target density is expressed explicitly up to a normalizing constant. A fast implementation with RStan [Carpenter et al., 2017] and parallel programming is applicable, by including the fixed in the target statement. We develop the following algorithm to calculate the scale factor up to a true constant. It is an adaptive version of the path sampling based on the results in Van Rosmalen et al. [2018].

-

Step 0:

Choose a set of different numbers as knots between and , and another knot at , with sufficiently large. Sort them in ascending order . Let , (), and . Choose , the number of MCMC samples in a run when sampling from . Initialize .

-

Step 1:

Generate samples from using an appropriate MCMC algorithm. Denote the sample as .

-

Step 2:

Calculate .

-

Step 3:

Calculate .

-

Step 4:

Increase by . If then repeat Steps 1 to 3.

The output is a vector of values, , for selected knots.

Finally, for that is not on the knots, it is efficient to linearly interpolate based on its nearest two values on the knots [Van Rosmalen et al., 2018]. The interpolation can be done quite fast at every iteration when sampling from the posterior using a normalized power prior, so the algorithm similar to the one described in B.1 can be applied. Compared to the joint power prior, the extra computational cost is to calculate on the selected knots, with the capability of parallel computation. Both of the algorithms in B.1 and B.2 are implemented in R package NPP.