Self-exciting price impact

via negative resilience in

stochastic order books

Abstract

Most of the existing literature on optimal trade execution in limit order book models assumes that resilience is positive. But negative resilience also has a natural interpretation, as it models self-exciting behaviour of the price impact, where trading activities of the large investor stimulate other market participants to trade in the same direction. In the paper we discuss several new qualitative effects on optimal trade execution that arise when we allow resilience to take negative values. We do this in a framework where both market depth and resilience are stochastic processes.

Keywords: optimal trade execution; limit order book; stochastic market depth; stochastic resilience; negative resilience; quadratic BSDE; infinite-variation execution strategy; semimartingale execution strategy.

2020 MSC: Primary: 91G10; 93E20; 60H10. Secondary: 60G99.

Introduction

In an illiquid financial market large orders have a substantial adverse effect on the realized prices. It is, therefore, reasonable to divide a large order into smaller ones when an investor faces the task of closing a large position in an illiquid market. The scientific literature on optimal trade execution problems deals with the optimization of such trading schedules. The inputs are time horizon , size (shares of a stock) of the financial position to be closed until time and model of the price impact.

The literature on optimal trade execution takes price impact as exogenously given. Depending on how the price impact is modeled the majority of current literature can be naturally divided into two groups.

In the first group of models, execution strategies have absolutely continuous paths , and the price impact at any time depends only on the derivative at time . In particular, the price impact at time is independent of all orders executed at times prior to and does not influence the impact of the orders executed at times after . Essentially, what is modeled in this approach is only market depth, and the price impact is purely instantaneous in the sense described above.111This, instantaneous, impact is alternatively called temporary impact. There can also be a permanent component in the price impact, but it has no effect on determining optimal execution strategies. In the literature, such models are often called the Almgren-Chriss type models; see, e.g., [9, 10, 11] and references therein.

In the second group of models, trades induce a transient price impact that decays over time due to resilience effects of the price. In such models, the execution price at time is influenced in a nontrivial way by orders filled at times prior to , and the execution at time in turn influences the execution prices of subsequent orders. Essentially, there are now two quantities to be modeled separately: market depth and resilience. Such models are inspired by a limit order book interpretation. The pioneering work Obizhaeva and Wang [34] models the price impact via a block-shaped limit order book (which translates into a constant market depth), where the impact decays exponentially at a constant rate. Mathematically, it is this rate that is called resilience.222From this perspective, the models within the first group are essentially models with infinite resilience, whereas the models in the second group are models with finite resilience. Our model in this paper falls into this second group.

As explained above, there is a clear qualitative difference between the models in the first and in the second group. Moreover, this translates into qualitative differences in the optimal execution strategies. One of the facets worth mentioning in this respect is that, as opposed to absolutely continuous strategies in the first group of models, optimal strategies in the second group are càdlàg and usually exhibit jumps333The exceptions are Graewe and Horst [27] and Horst and Xia [29], where optimal strategies are absolutely continuous, although the models belong to the second group according to our classification. The reason is that jumps are strongly penalized by the form of the functionals that are optimized in [27] and [29]. (in a sense, jumps at certain times allow to better exploit finite resilience).

Most of the existing literature within the second group of models assumes that resilience is positive. The explanation is that the impact of the trade should decay over time. But negative resilience also has a natural interpretation, as it models self-exciting behaviour of the price impact, where trading activities of the large investor stimulate other market participants to trade in the same direction. From this viewpoint, it seems reasonable to expect that there are (particularly unstable) periods in financial markets when the resilience is negative. In this paper we discuss several new qualitative effects in optimal trade execution that can arise when we allow the resilience to take negative values.

In practice, resilience is difficult to estimate from real data (cf. Section 7.3 in Roch [37]), and we are not aware of any empirical study of whether the resilience can be negative. On the other hand, there recently appeared many papers on trade execution that model self-excitement of price impact in different ways, while, as explained above, negative resilience is an alternative way of modeling this effect. As in Cayé and Muhle-Karbe [21] and in Fu et al. [24], we motivate self-exciting price impact by the following reasons. Imagine, for instance, a large trader performing extensive selling. Firstly, a continued selling pressure makes it more and more difficult to find counterparties. Secondly, such an extensive selling by the large trader may trigger stop-loss strategies by other market participants, where they start selling in anticipation of further decrease in the price. Thirdly, extensive selling may also attract predatory traders that employ front-running strategies. In each case, we obtain an increased price impact for subsequent trades.

For existing approaches to self-exciting price impact, see Alfonsi and Blanc [4], Cartea et al. [20], Cayé and Muhle-Karbe [21], Fu et al. [24] and references therein. We now explain that, mathematically, all these approaches and ours are pairwise substantially different. In [21] the framework is of the Almgren–Chriss type, and self-excitement is produced by the trades of the large trader in a way that the price impact coefficient depends on the trading activity of the large trader. In [4] the orders of the large trader incur price impact like in the Obizhaeva–Wang model (with positive resilience), while the orders of other market participants are modeled by Hawkes processes with self-exciting jump intensities. That is, in contrast to the previously mentioned approach, self-excitement is produced by the trades of other market participants. [20] again use Hawkes processes but in a quite different way: they consider an execution model where the large trader places limit orders whose fill rates depend on mutually exciting “influential” market order flows. [24] consider liquidation games between several large traders (and the corresponding mean-field limit as well as the single player subcase) with a self-exciting order flow. In a sense, self-excitement in [24] is “more endogenous” than in the other mentioned approaches (including ours, where the resilience process is exogenously given), as in [24] there appear “child orders” triggered by the large traders’ trading activity, and as the strategies in [24] come out as Nash equilibria in the game. In our approach self-excitement is produced by the trades of the large trader at time instances when the resilience is negative in the Obizhaeva-Wang type model where both market depth and resilience are stochastic processes (differently from [20] and like in the other mentioned approaches, the large trader trades with market orders).

Despite the differences in the set-up, it is interesting to observe the following qualitative similarity in the strategies that may result from our approach and from the one in [24]. Below we, in particular, discuss that, in our framework, it is never optimal to overshoot the execution target whenever the resilience is positive, but it can be optimal to overshoot the target if we allow the resilience to take negative values. In other words, in our framework, the possibility to overshoot the target is a qualitative effect of self-excitation via negative resilience. In the same vein, in the single player benchmark model for [24] without self-excitation, which goes back to Graewe and Horst [27], it is not optimal to overshoot the execution target (this is observed in Theorem 2.2 of Horst and Kivman [28]), whereas the resulting strategies in the model with self-excitation in [24] do sometimes overshoot the target (cf. Figure 1 or Figure 2 in [24]).

We now briefly describe our framework. The execution strategies are càdlàg semimartingales with and . As explained above, we need to allow for jumps (i.e., block trades). In particular, a possibility of a block trade at time means that can be different from . Notice that we do not require to have monotone paths, which means that we allow for trading in both directions within the execution strategy. We assume that the realized price of the asset is the sum of a martingale unaffected price and a deviation process that carries the price impact. The inputs are the price impact process driven by (3), which models market depth, and the resilience process . Both enter the dynamics of the deviation process (4). We see from (4) that the sign of determines whether the deviation process moves back to zero or moves further away from it. The optimal execution problem is given in (6).

This general setting is elaborated in Ackermann et al. [1], where the solution to the optimal execution problem is described via a solution to a challenging quadratic BSDE (characteristic BSDE). In [1] it is shown that the characteristic BSDE has a solution in two specific subsettings of this general framework. In this paper we also complement these results by establishing the existence for the characteristic BSDE in the subsetting, where the resilience process and the processes and in dynamics (3) for the price impact process are independent from the driving Brownian motion . It turns out that this subsetting is feasible enough to study some new qualitative effects of negative resilience and to explicitly construct pertinent examples.

It is worth noting that the majority of papers on models with finite resilience considers execution strategies of finite variation. In this stream of literature, strategies of infinite variation were first included by Lorenz and Schied [32], where they allow for a non-martingale dynamics in the unaffected price, and hence the execution strategies need to account for the fluctuations in it. Recently, strategies of infinite variation emerge in related frameworks of Horst and Kivman [28] and Fu et al. [25]. In the framework of [1] we need to include strategies of infinite variation, as they actually come out as optimal trading schedules, e.g., to account for the fluctuations in and . This comes with some adjustments in the conventional setting of the optimal execution problem, where the most important one is the term in the dynamics (4) of the deviation process . As the main theme of this paper is to discuss the effects of negative resilience, we withdraw from an extended discussion of the term in (4) but rather refer an interested reader to [1]. From this perspective, we mention that Carmona and Webster [19] provide a strong empirical evidence that trading strategies of large traders are of infinite variation nature.

We, finally, embed our paper into a broader set of related literature on optimal trade execution in models with finite resilience. After the pioneering paper444In SSRN it appeared already in 2005. [34] subsequent work either extends the framework in different directions or suggests alternative frameworks with similar features. Alfonsi et al. [5] study constrained portfolio liquidation in a model of the type as in [34]. There is a subgroup of models which include more general limit order book shapes, see Alfonsi et al. [6], Alfonsi and Schied [7], Predoiu et al. [35]. Models in another subgroup extend the exponential decay of the price impact to general decay kernels, see Alfonsi et al. [8], Gatheral et al. [26]. Finite player games with deterministic model parameters and transient impact were studied by Luo and Schied [33], Schied et al. [38], Schied and Zhang [39] and Strehle [40]. Models with transient multiplicative price impact have recently been analyzed in Becherer et al. [16, 17], whereas Becherer et al. [18] contains a stability result for the involved cost functionals. Superreplication and optimal investment in a block-shaped limit order book model with exponential resilience is discussed in Bank and Dolinsky [12, 13] and in Bank and Voß [15]. The present paper falls into the subgroup that studies time-dependent (possibly stochastic) market depth and resilience, see Ackermann et al. [2, 1], Alfonsi and Acevedo [3], Bank and Fruth [14], Fruth et al. [22, 23]. To point out the difference from our present paper, we notice that all mentioned papers except [2, 1] consider only positive resilience, the framework in [2] is in discrete time, while [1] does not study the question of what kind of new effects can arise when the (time-dependent) resilience process is allowed to take negative values.

The paper is organized as follows. Section 1 contains a precise description of our setting and formulates the problem of optimal trade execution in this setting. Section 2 describes the solution to this optimal trade execution problem based on the results from [1]. The key ingredient here is 2.1 that establishes existence of a solution to the characteristic BSDE in our setting. In Section 3 we present two general results about the possibility for optimal execution strategies in such models to overjump zero or to exhibit premature closure. Loosely speaking, a necessary condition for overjumping zero or premature closure is to have negative resilience at least for some time, while a sufficient condition for that is to have negative resilience for some time close to the time horizon . See Section 3 for the precise formulations and more detailed discussions. Via case studies in Section 4 we address several questions that arise in discussions in Section 3. For instance, one of the examples shows that the “close to ”-requirement in the sufficient condition mentioned above is essential. It is worth mentioning that Section 4 contains both examples with deterministic optimal strategies and examples with stochastic ones and, in the latter examples, the strategies are of infinite variation. In one of other examples we see that, with resilience that can take negative values, it is possible that the optimal execution strategy closes the position at a certain point in time and reopens it immediately. Finally, the paper is concluded with a more tricky example, where the position is kept closed during a time interval, after which it is reopened again.

1 Problem formulation

Let us introduce the stochastic order book model in which we analyze the effects of negative resilience. In Remark 1.2 below we explain in which sense the model is a special case of the model considered in [1] and in which sense not. Remark 1.1 provides information on where to find more detailed motivations and derivations of the order book model.

We fix a terminal time and consider trading in the time interval . Let be a filtered probability space that satisfies the usual conditions and supports a Brownian motion . Furthermore, we assume that has the structure , , , where denotes the filtration generated by , and is a right-continuous complete filtration such that and are independent. Throughout the paper, denotes the conditional expectation for , and denotes the Lebesgue measure on .

As input processes we require three -progressively measurable processes , , and such that there exist deterministic such that

| (1) | ||||

| (2) |

Here and in what follows, we write , , etc., to emphasize the presence of the time variable, i.e., we do so to indicate that we speak about the process as a whole. Assumption (1) is a structural condition on the input processes which, roughly speaking, ensures that the minimization problem under consideration (see (6) below) is convex. To see this, we refer to the alternative representation of the cost function provided in [1, Theorem 3.1]. Note that the process also shows up in the denominator of the driver of the characteristic BSDE (7). Assumption (2) is a boundedness condition that we need in order to ensure existence of a solution of BSDE (7). Please note that Assumption (1) in combination with Assumption (2) also implies boundedness of .

The two processes and are used to model price impact. More precisely, we define the price impact process to be the solution of

| (3) |

where is a positive -measurable random variable. Consequently, is the positive continuous -adapted process

Given an open position to be liquidated, an execution strategy is a càdlàg semimartingale such that and . For any , the quantity describes the remaining position to be closed during . As in [1] we follow the convention that a positive position means the trader has to sell an amount of shares, whereas requires to buy an amount of shares. Note that we do not require an execution strategy to have monotone paths and hence we allow for selling and buying within the same strategy. Moreover, the paths of execution strategies can exhibit jumps and thus so-called block trades are possible.

We assume that trading according to an execution strategy affects the asset price. To model this influence we associate to every execution strategy a deviation process with initial deviation . We assume that the actual price of the asset is the sum of an unaffected price and the price deviation . The unaffected price is assumed to be a martingale satisfying suitable integrability assumptions. This ensures that the optimal trade execution problem we are about to set up (see (6) below) does not depend on the unaffected price process and that we only need to focus on the deviation (see [1, Remark 2.2] for more detail). The deviation is modeled as follows. Given and an execution strategy , the deviation process associated to is defined by

| (4) |

i.e.,

When ignoring the effects of on at time we see from (4) that the sign of determines whether the deviation tends back to or further moves away from it. In the case , which is typically assumed in the literature, the deviation is always reverting to and the speed of reversion is determined by the magnitude of . The input process thus models how fast the order book recovers from past trades and is therefore called the resilience process. We allow to also take negative values and thereby enable the incorporation of signaling effects, where, e.g., a series of buy trades might indicate the arrival of further buy trades and therefore lead to a further growth of the deviation process.

For , we let be the set of all execution strategies (i.e., càdlàg semimartingales with and ) such that all three conditions

are satisfied.

Given and , we then consider the expected costs

| (5) |

The optimal trade execution problem considered here consists in minimizing the expected costs over . An optimal strategy is an execution strategy such that

| (6) |

We point out that possible jumps of the integrators at time contribute to the integrals , , and in the definition of the deviation (4) and the expected costs (5).

Remark 1.1.

We refer to the introduction of [1] as well as Sections 4, 5 and Appendix A therein for a discussion of the specific form of the deviation dynamics (4) and the expected costs (5). In short, they come from a block-shaped symmetric limit order book model, and, e.g., the term in (4) appears because execution strategies are not necessarily of finite variation. We also mention [19] for empirical evidence that, in related settings, trading strategies are of infinite variation nature.

Remark 1.2.

Let us briefly explain in which sense the setting outlined above is a special case of the model considered in [1]. In [1] we consider a general continuous local martingale instead of the Brownian motion to drive the price impact process in (3). Moreover, in [1] we do not require that the three input processes , , and are independent of the martingale .

In [1, Section 7] we establish existence of a solution to a characteristic BSDE (see [1, (3.2) & (3.3)]) for the trade execution problem in two subsettings: The first one assumes that , whereas the second one assumes that the underlying filtration is continuous (in the sense that every martingale is continuous). In the present paper we complement these results by establishing in 2.1 below existence of a solution to the BSDE in the subsetting outlined above. This is included in neither of the two subsettings considered in [1].

2 Solution of the trade execution problem

In this section we provide a probabilistic solution of the optimal trade execution problem (6). To this end, we establish in Section 2.1 an existence result for a characteristic BSDE associated to problem (6). Subsequently, in Section 2.2, we combine this result with the main results in [1] to obtain a representation of the optimal strategy for (6).

2.1 Characteristic BSDE

A representation of the minimal expected costs, a characterization for the existence of an optimal strategy as well as a formula for the optimal strategy in the general framework considered in [1] are provided as a main result in [1, Theorem 3.4]. This result is based on the existence of a solution of a certain BSDE [1, (3.2) & (3.3)].

In the setting of the present paper, where are independent of the Brownian motion , we consider the BSDE

| (7) |

By a solution of (7) we mean a pair such that

-

•

(7) is satisfied -a.s.,

-

•

is an -adapted, càdlàg, -valued process, and

-

•

is a càdlàg -martingale with , , and .

We show in 2.1 the existence555Uniqueness of the solution will follow as a byproduct of our analysis; see 2.2 below. of a solution of (7). Any such solution of (7) provides a solution of the BSDE [1, (3.2) & (3.3)] (in the sense that [1, (3.4)] is satisfied). In particular, we can invoke in Section 2.2 below the main results from [1, Section 3].

Proof.

Let be the truncation function defined by , . Let be the function defined by

| (8) |

We first consider BSDE (7) with its driver replaced by and on the filtered probability space , where denotes the probability measure restricted to the sigma algebra . Note that the expressions “-a.s.” and “-a.s.” have the same meaning. In the calculations below we assume without loss of generality that , , and satisfy (1) and (2) for all , as we can otherwise replace them in with -progressively measurable processes , , and that satisfy (1) and (2) for all and such that -a.e., -a.e., and -a.e. Observe that for all the function is continuous. Moreover, it is concave on and constant on the complement . This implies for all and that

It follows that for all and all it holds

Moreover, it holds for all that

This implies in particular that . By [30, Proposition 5.1] (see also [31, Theorem 1]) there exists a pair such that BSDE (7) on with its driver replaced by is satisfied a.s., is a càdlàg -adapted process with , and is a càdlàg -martingale with and .

Next, note that is a solution of the BSDE with driver and terminal condition . Then a comparison principle for BSDEs (e.g., [31, Proposition 4]) proves that for all a.s. Furthermore, it holds a.s. that for all

Again the comparison principle ensures that for all a.s. In particular, the truncation function in (8) is inactive. Therefore, also a.s. satisfies BSDE (7) and is -valued.

Since and are independent and for all , we have that is not only an -martingale, but also an -martingale. Furthermore, we can show that is an -martingale. It follows that . Since is continuous, it holds that is continuous, and hence . This completes the proof. ∎

2.2 Representation of the optimal strategy

For a solution of (7), we recall from [1, (3.5)] the process defined by, in the present set-up,

| (9) |

By (1), (2), and the fact that is -valued, we have that is -a.e. bounded. It thus follows from [1, Proposition 3.8] that the solution of (7) is unique up to indistinguishability. Furthermore, by boundedness of , under the condition that

| (10) |

we obtain from [1, Theorem 3.4] for any initial values (see also [1, Lemma 3.3] for the case ) the existence of an optimal strategy, which is unique up to -null sets. Notice that, in our present context, this is equivalent to uniqueness up to indistinguishability. Indeed, if and are optimal strategies, then they are indistinguishable, as and are càdlàg and -a.e. Note that condition (10) is in particular guaranteed if are deterministic and of finite variation, as in the examples in Section 4 below.

We extract the following representation for the optimal strategy and its associated deviation from [1, Theorem 3.4] provided that (10) holds true. Define

and denote by the stochastic exponential of , i.e.,

Let . Then the optimal strategy is given by the formulas

| (11) |

The associated deviation process is given by

| (12) |

We summarize the statements above in the following theorem.

Theorem 2.2.

3 Overjumping zero and premature closure

In this section we study qualitative effects of negative resilience on the optimal strategy. In particular, we examine effects that we call overjumping zero and premature closure. Roughly speaking, we are interested in market situations where it is optimal to change a buy program into a sell program (or vice versa), or where it is optimal to close the position strictly before the end of the execution period. More precisely, we intend to identify market conditions under which paths of optimal trade execution strategies with positive probability jump over the target level or already take the value prior to . To this end recall that under (1), (2), and (10), given an initial position and an initial deviation , the optimal strategy satisfies for all that

| (13) |

This representation allows to disentangle the contributions to the optimal strategy’s sign of the initial conditions and on the one side and the input processes , , and defining the market dynamics on the other side. Indeed, since the stochastic exponential is positive, the sign of for is determined by the signs of the two factors and . The first factor is determined by the initial conditions, does not depend on time, and thus can only contribute to a change of sign of at time . Note that has a different sign than the initial condition if and only if . A nonzero initial deviation can thus have the effect that changes its sign directly at time . In practice, one would typically assume that , in which case this factor does not contribute to a change of sign.

In the sequel we focus on the contribution of the second factor and provide definitions of the effects overjumping zero and premature closure which are only built upon . This factor and hence also these effects are determined by the input processes , , and driving the market dynamics and are independent of the initial conditions and .

For ease of notation, we extend the domain of to the point by setting . In what follows, we denote by the projection operator from onto .

Definition 3.1.

(i) We say that overjumping zero is optimal in the limit order book model driven by , , and , if .

(ii) We say that premature closure is optimal, if .

In relation with Definition 3.1 we need to make the following comments.

It is worth noting that the terms overjumping zero and premature closure could be equivalently defined with the help of stopping times:

Lemma 3.2.

Lemma 3.2 easily follows from the optional section theorem [36, Theorem IV.5.5], which applies because and are optional sets. We also remark that a simple attempt to define as, say, does not always work, as, for such that but the infimum is not attained, the expression will be zero.

We now turn to the question about new qualitative effects we can get if we allow for negative resilience. Informally, with positive resilience one will not be able to observe overjumping zero or premature closure in the optimal strategy. On the contrary, if we allow the resilience to take negative values, then overjumping zero and premature closure in the optimal strategy become possible. 3.3 and 3.4 contain precise mathematical formulations of these statements. After these propositions we also provide a more detailed informal 3.5.

Proposition 3.3.

(i) We have

(ii) Assume (10) and that -a.e. Then overjumping zero is not optimal.

(iii) Assume (10) and that there exists an -measurable random variable such that

| (14) |

Then neither overjumping zero nor premature closure is optimal.

In relation with 3.3 we make the following comments.

-

(a)

A rather widespread situation in today’s literature on resilient price impact is to assume a constant resilience. This falls into part (iii) of 3.3. To discuss the assumption in (iii) in more detail, we remark that, if

(15) then (14) is satisfied. Indeed, in this case we can take because, by the measurable projection theorem, for all we have

i.e., is -measurable. More precisely, (14) is slightly weaker than (15) and can be, in fact, equivalently expressed as follows: there exists an -measurable such that -a.e. and -a.s.

-

(b)

The observation in part (iii) of 3.3 is in line with [28], where in a different but related setting (with a positive stochastically varying resilience) it is observed that the optimal strategy never changes its sign (see [28, Theorem 2.2]), which means in our terminology that neither overjumping zero nor premature closure is optimal.

-

(c)

Comparison of (ii) and (iii) poses the question if premature closure can be optimal with nonnegative resilience. The answer is affirmative: e.g., if , then for all , and the optimal strategy is to close the position immediately (cf. [1, Proposition 3.7]). This is, however, a rather degenerate example. A much more interesting one, for which we, however, allow the resilience to be negative, is presented in Section 4.3.

Proof of 3.3.

(i) Define

and observe that . It is enough to show the claim for every . To this end, we fix an arbitrary . By (9) we have to show that

| (16) |

If , this inequality is evident. Therefore we assume in the sequel. Note that the fact that implies

This shows that

and hence establishes (16).

(ii) We first notice that (i) and (10) ensure that -a.e. As has càdlàg paths, by the standard Fubini argument, we infer that -a.s. it holds: for all , we have . This shows that overjumping zero is not optimal.

(iii) It suffices to show that premature closure is not optimal. Define

where is from (2), and notice that . It follows from (i) that

As and is càdlàg, we conclude that -a.s. it holds

(again by the Fubini argument), and hence premature closure is not optimal. ∎

In the sequel, for a set and , we use the notation

for the section of . We will permanently use the well-known statements that, if , then

-

•

for any , ,

-

•

and the mapping is -measurable.

Proposition 3.4.

Discussion 3.5.

(a) The meaning of (17) is that, with positive probability, resilience is assumed to be negative with positive Lebesgue measure in any neighbourhood of the terminal time .

(b) It is instructive to compare 3.4 with part (iii) of 3.3. The assumptions are “almost” complementary: compare (14) with (17)–(18). In both cases, we step a little away from (this is the role of in (14) and (18)) but in a “soft” sense (the bound can depend on ).

(c) In view of (a) and (b) we informally summarize part (iii) of 3.3 and 3.4 as follows. Positive resilience implies that neither overjumping zero nor premature closure is optimal; negative resilience “close to ” implies optimality of overjumping zero or premature closure. There arises the question of whether negative resilience “far from ” also implies overjumping zero or premature closure. The answer is negative: see 4.2 below.

Proof of 3.4.

1. In the first step of the proof we establish that (1), (2), and (17) imply , where

To this end, we first recall from [1, Lemma 8.1] that () -a.s., i.e., for the solution of (7), the orthogonal to martingale does not jump at terminal time . We define

where is from (2), and notice that , . Now we set

where is from (18), and observe that (17) holds with replaced by . As , we get , once we prove

| (19) |

To establish (19), we fix an arbitrary and make the following simple observation

This yields that, for , it holds

hence

| (20) |

Now we compute from (9) that, for , we have the equivalence

| (21) |

Moreover, (20) and (21) reveal that, for ,

| (22) |

Recalling that , the definition of the event in (19), and that (as implies that there exists with ), we conclude from (22) that there exists (which depends on ) such that

hence . We thus proved (19) and completed the first step of the proof.

2. The first step together with (10) yields . Define the stopping time (as usual, ). As , we get, by the Fubini argument, that . Since and is càdlàg, -a.s. on it holds and , which yields the result. ∎

4 Case studies on the effects of negative resilience

In this section we analyze the effects of negative resilience and discuss the results of 3.3 and 3.4 in several subsettings of Section 1.

4.1 A case study with piecewise constant resilience and deterministic optimal strategies

In this subsection we assume that there are different regimes of resilience. That is to say that is piecewise constant. Moreover, we assume that is deterministic, is constant and . These assumptions lead to deterministic optimal strategies. We summarize the results in the following proposition.

Proposition 4.1.

Assume that is deterministic and that666This assumption is only for ease of exposition. All statements hold also in the case with the suitable adjustments. . Suppose furthermore that , that is a deterministic constant, and that is piecewise constant in the sense that there exist , , and such that for all it holds Then, (1) and (2) are satisfied. The unique solution of (7) is given by

| (23) |

where . Moreover, (10) is satisfied with , The optimal strategy and the associated deviation are deterministic, for every they are continuous on , and for every they have a jump at if and only if has a jump at . Furthermore, for every the deviation is constant on and takes negative values, and the optimal strategy is monotone on : more precisely, if (resp., ; resp., ), then is strictly decreasing (resp., strictly increasing; resp., constant) on .

Proof.

Clearly, (1) and (2) are satisfied. Next note that from (23) satisfies for all that

From this it follows that is continuous and satisfies the Bernoulli ODE

Consequently, is the unique solution of (7). Moreover, defined by (9) is càdlàg and of finite variation and thus we have (10) with . In particular, is deterministic, and since and are deterministic, we have that the optimal strategy and its deviation are deterministic as well.

For every observe also that has a jump at if and only if has a jump at . This directly translates into jumps of the optimal strategy and jumps of the associated deviation via (11) and (12). To show that the deviation is constant on each , , observe that for all and it holds that

| (24) |

and hence

It thus follows from (12) that is constant on for . Moreover, since , , and , it holds that , and therefore (recall that we assume ). Next note that we have for all and that, using (24),

Since and , we conclude that if is positive, then in (11) is decreasing on , and if is negative, then is increasing on , . ∎

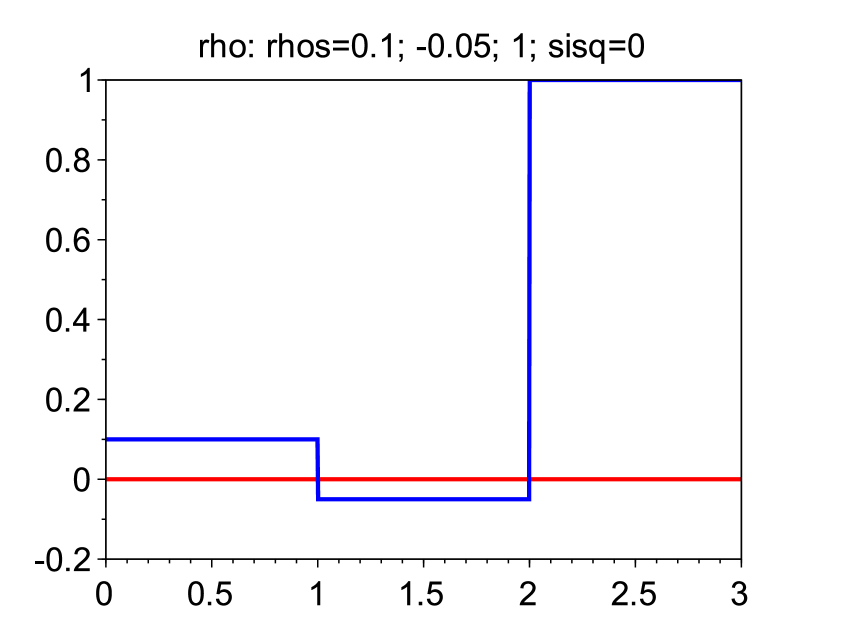

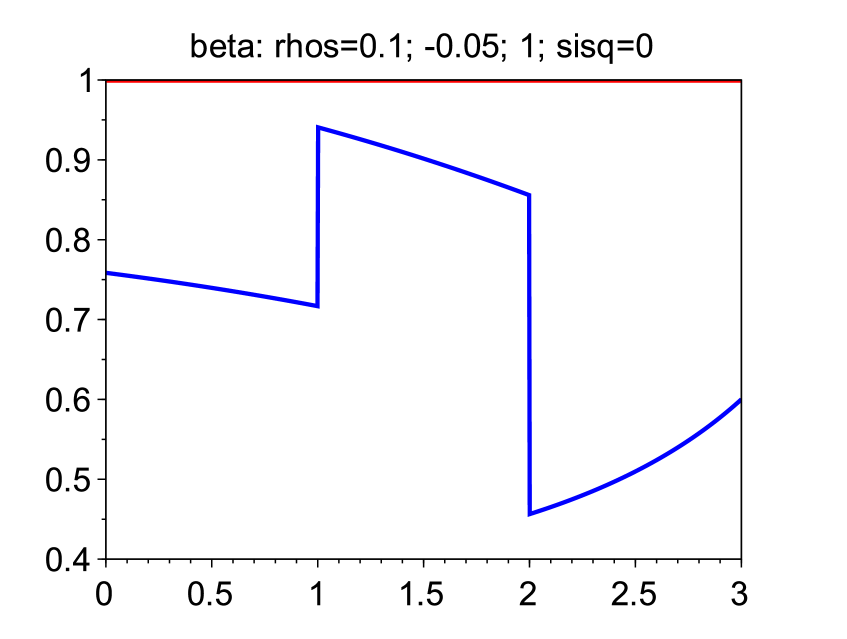

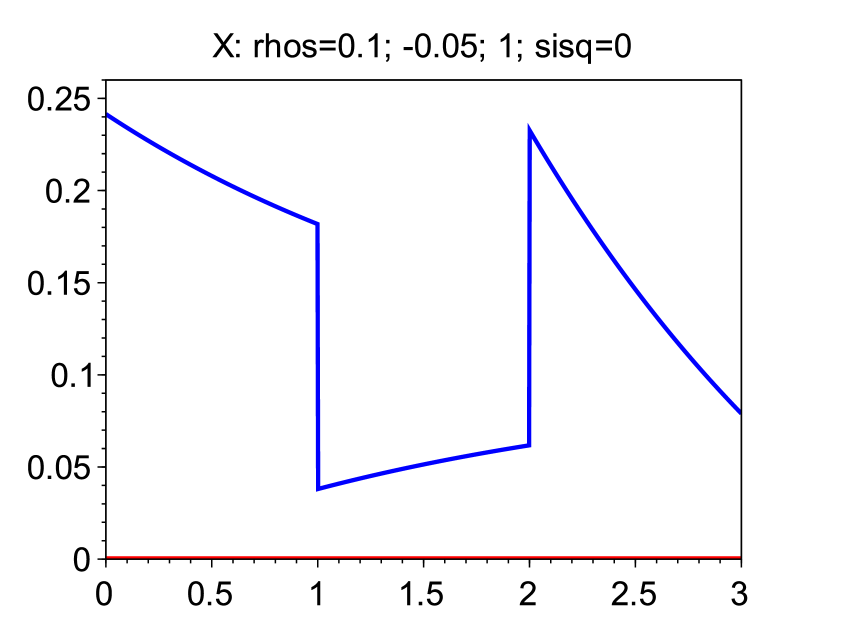

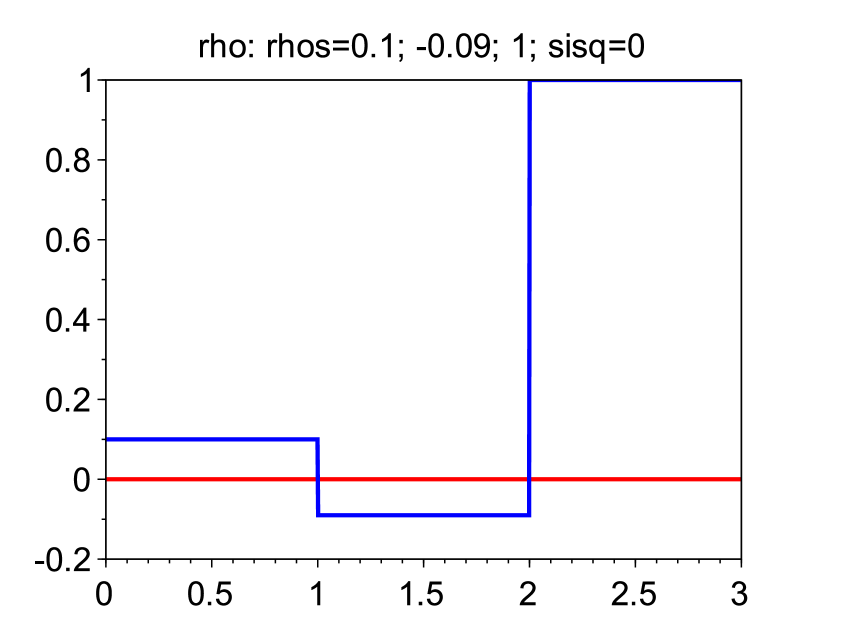

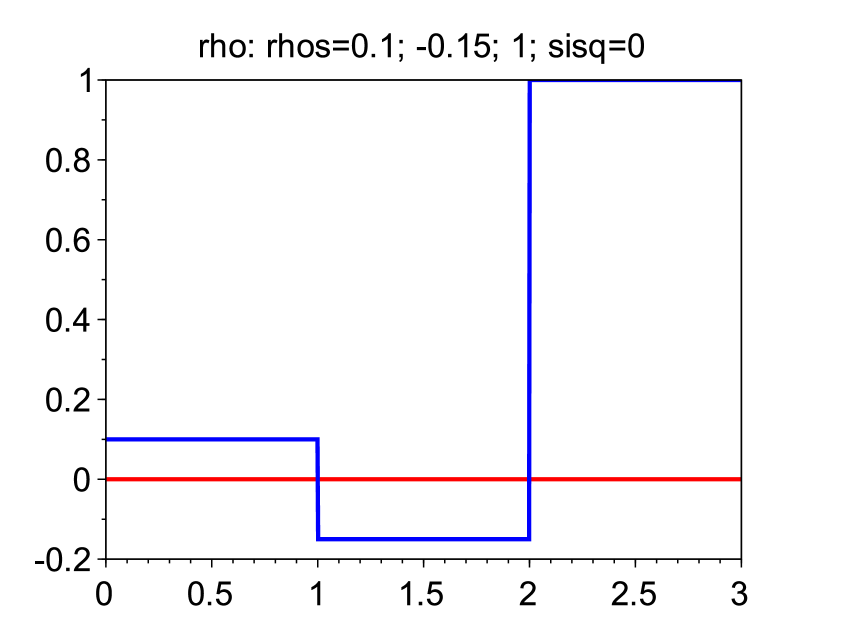

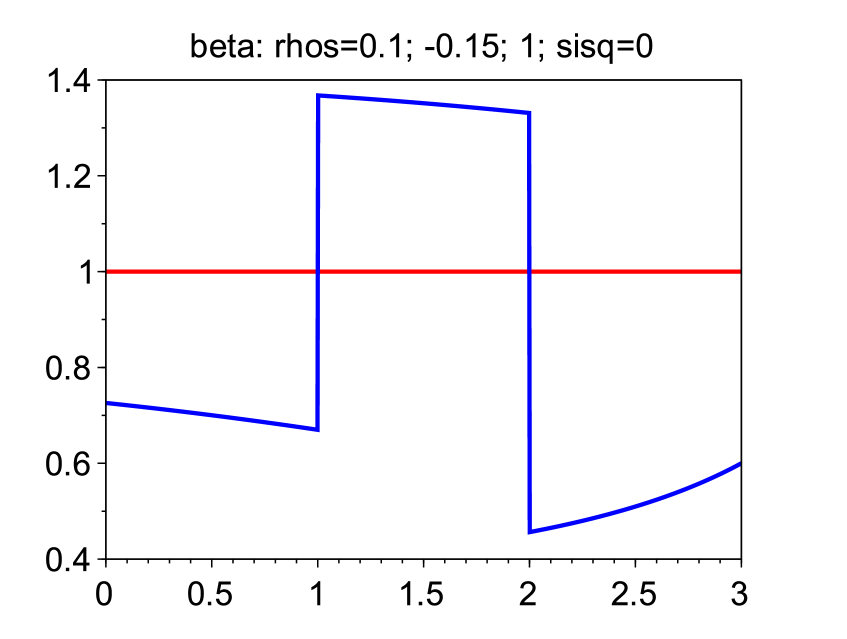

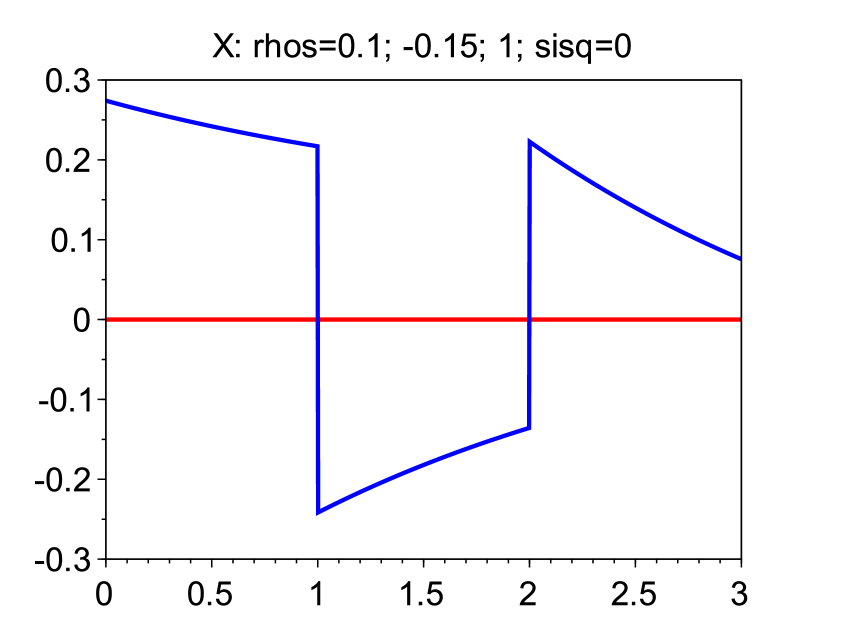

In 4.2, 4.3, and 4.4 below we consider the setting of 4.1 with different regimes of resilience. More precisely, we assume in the sequel of this subsection the setting of 4.1 with , , , , , and for .

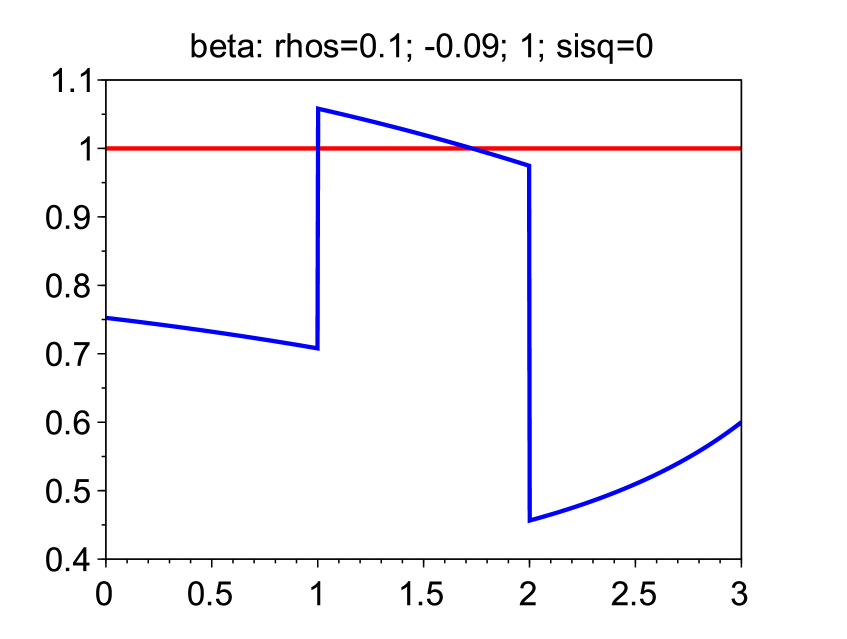

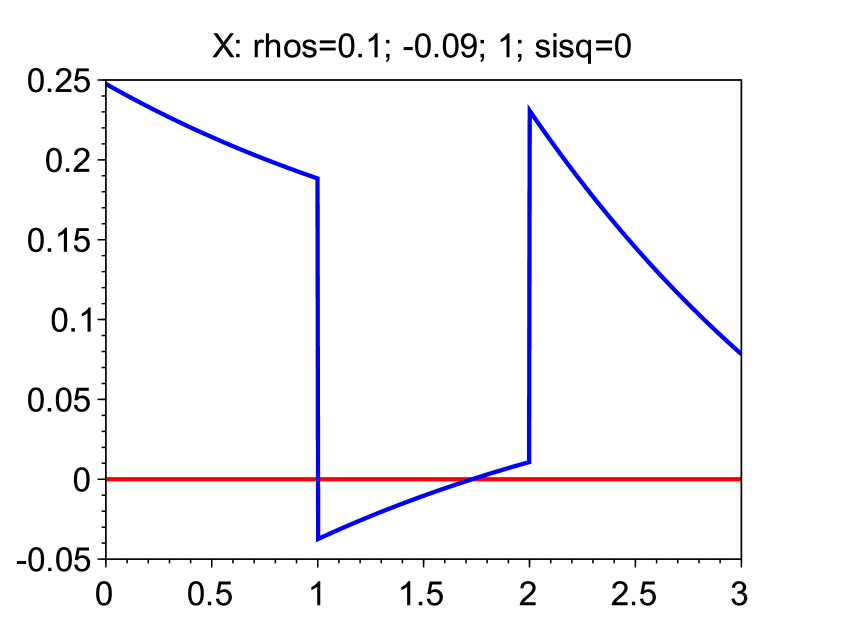

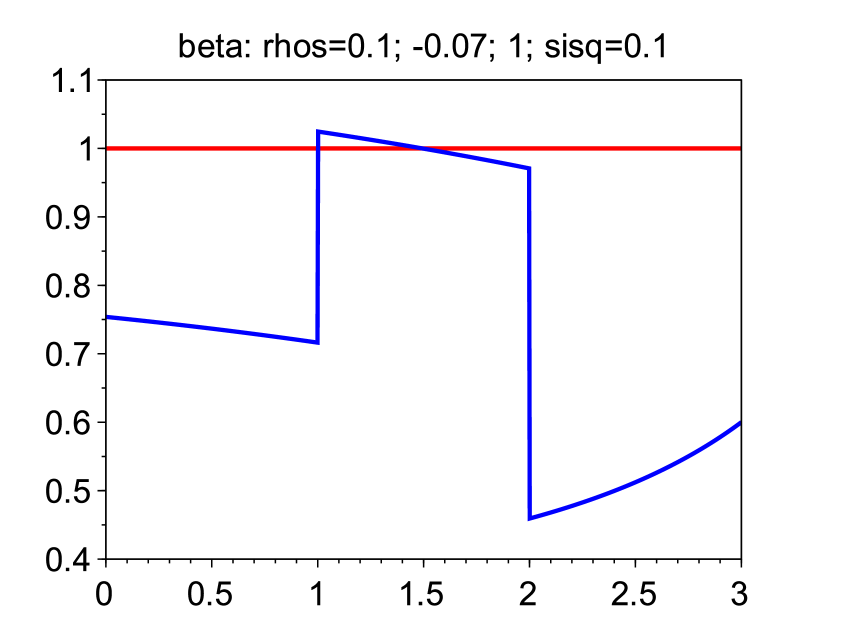

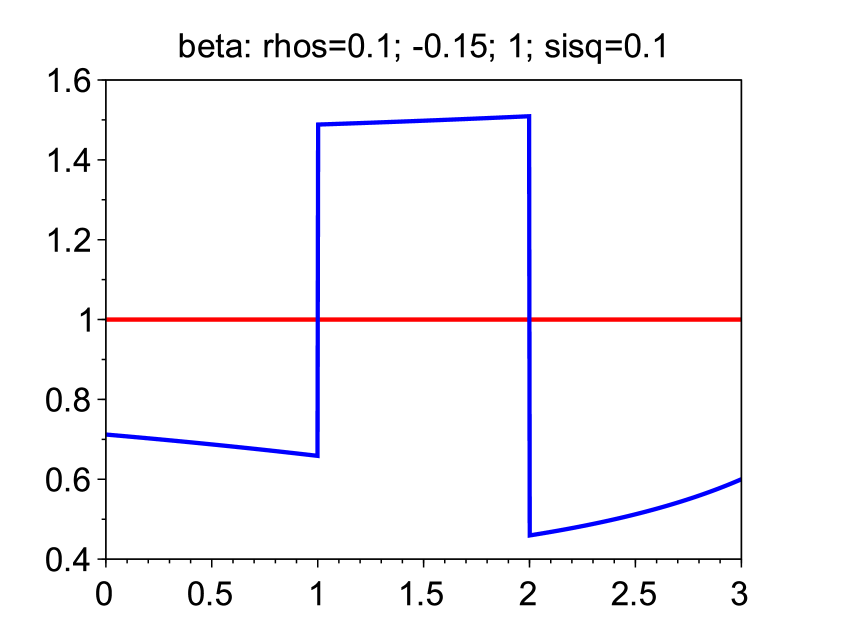

We already know from 3.4 that overjumping zero or premature closure is optimal if we have negative resilience in the last regime (i.e., ). In the three examples below we want to analyze under which conditions these effects occur in the case where the resilience is positive in the last (and also the first) regime. We choose and . 3.3 entails that we necessarily need to see these effects. Therefore we choose a different negative value for in each example.

For these choices of , , 4.1 shows that it is optimal to first sell during , change this to a buy program on to profit from the negative resilience during that time interval, and then sell again during . Moreover, since and are positive, we can already derive (e.g., by 3.3) that on and on , and hence that is strictly positive on and on due to . Between 4.2, 4.3, and 4.4 we vary the size of . This then determines if we get overjumping zero or premature closure for the optimal strategy. Recall that in all examples has jumps at and and is continuous on , , and , with values strictly smaller than on and . The facts that , , and yield that also . We moreover have that for all . This, continuity of on , , and imply that overjumping zero is optimal if and only if at least one of

| (25) |

and

| (26) |

is satisfied. Premature closure is optimal if and only if

| (27) |

The resilience , the function , and the optimal strategy for each of the examples below are shown in Figure 1.

Example 4.2.

We choose . The first row in Figure 1 shows that stays strictly smaller than one also on , and hence the optimal strategy is strictly positive on the time interval . We conclude that, in general, a period of negative resilience does not necessarily lead to overjumping zero or premature closure.

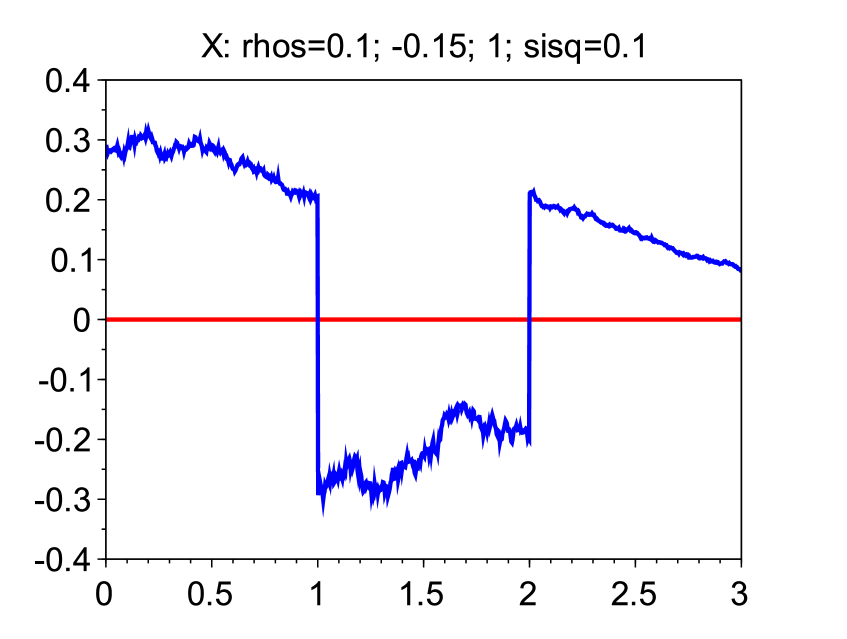

Example 4.3.

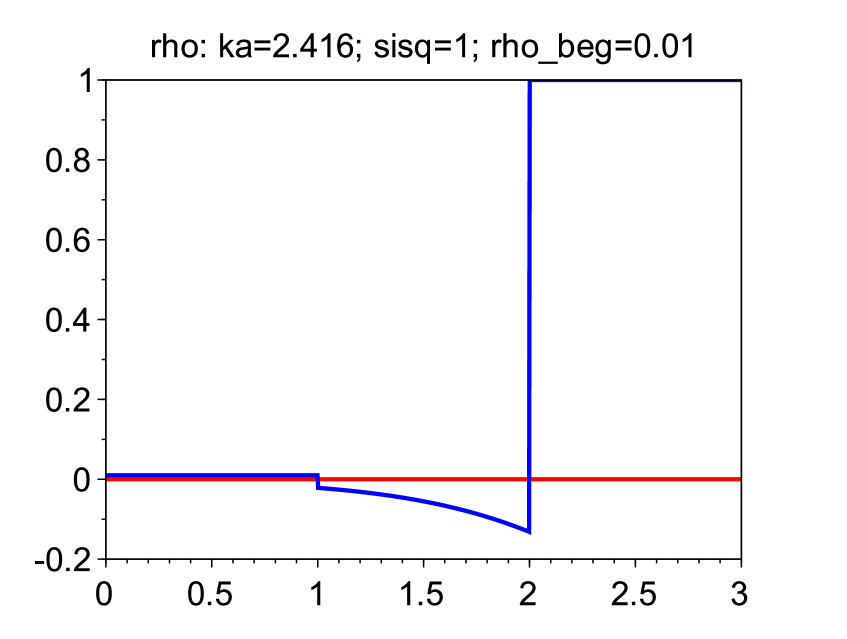

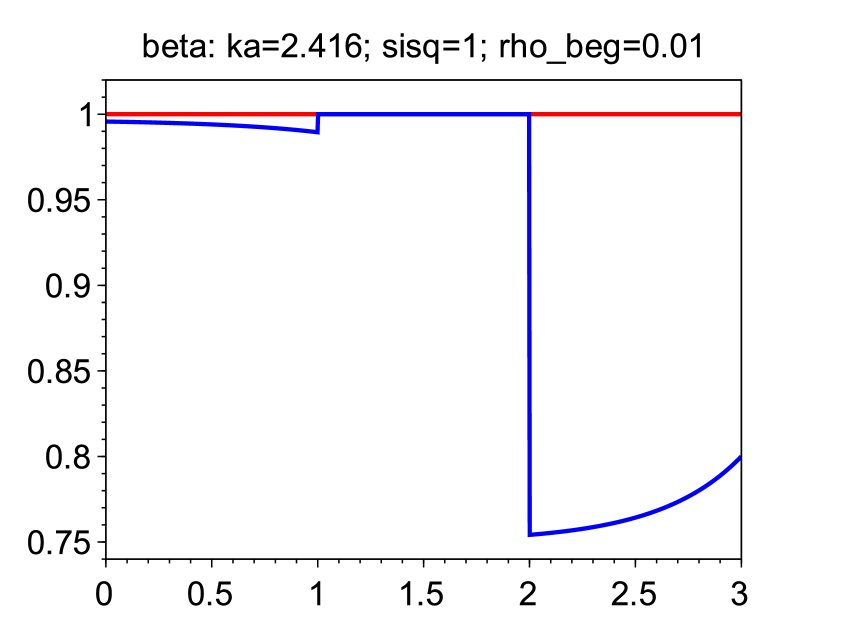

We next provide an example where negative resilience indeed leads to overjumping zero and premature closure. To this end we choose in the above set-up. From the second row of Figure 1 we observe that jumps above at time , but then decays continuously below already before its next jump at . It therefore holds that (25) and (27) are satisfied. We thus have overjumping zero as well as premature closure for the optimal strategy. This implies (recall ) that the optimal strategy jumps to a negative value at time and crosses within the time interval to become positive again. Note that the set of points in time for which we have is strictly included in the set where (which is ).

Example 4.4.

We finally provide an example where the set of points in time for which we have is equal to the set where . This means that the time periods with negative resilience exactly coincide with the time periods where the optimal strategy is negative. We achieve this for example for in the above set-up (see the third row of Figure 1). In particular, (25) is satisfied, i.e., overjumping zero is optimal. Furthermore, one can compute that (26) holds true as well. It follows that condition (27) is not met, and therefore, premature closure is not optimal. Note that the optimal strategy changes its sign twice, but does not continuously cross .

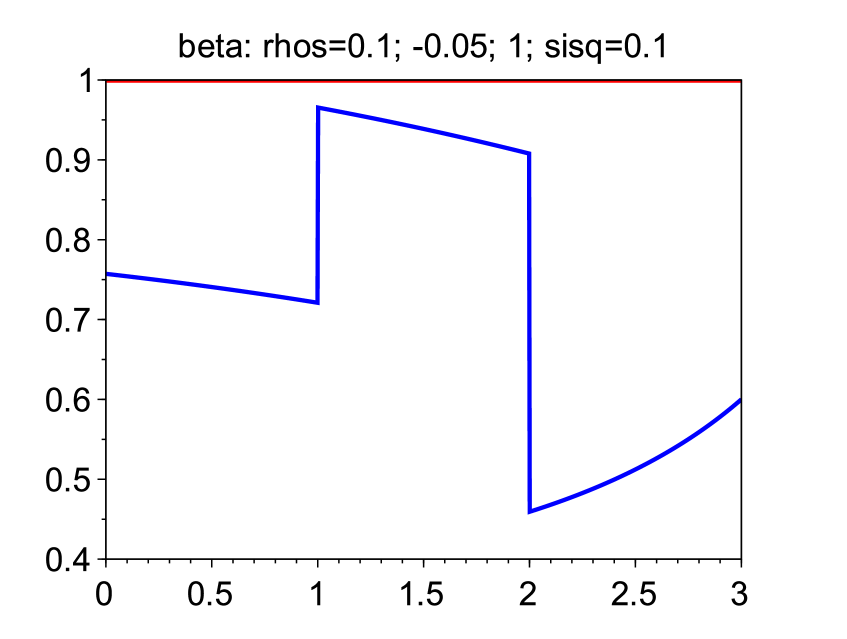

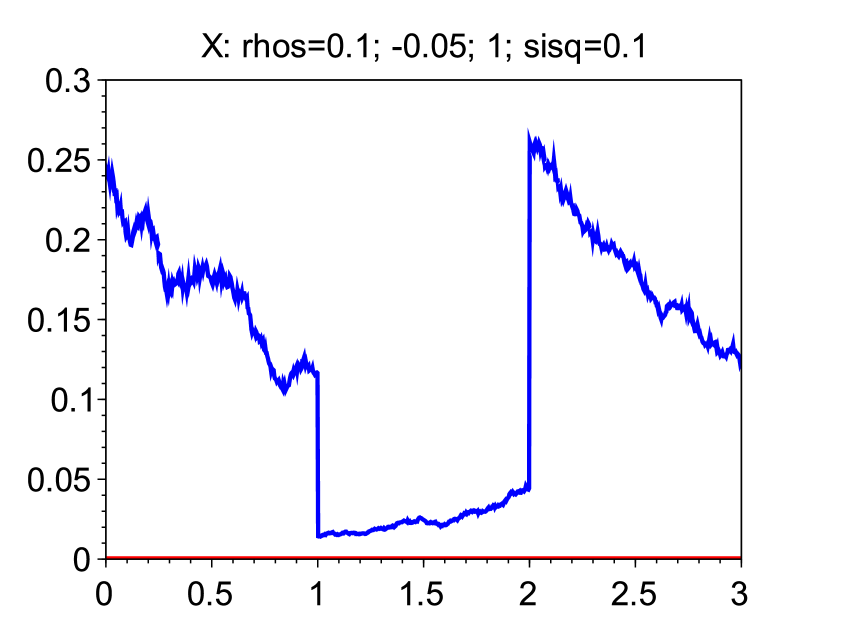

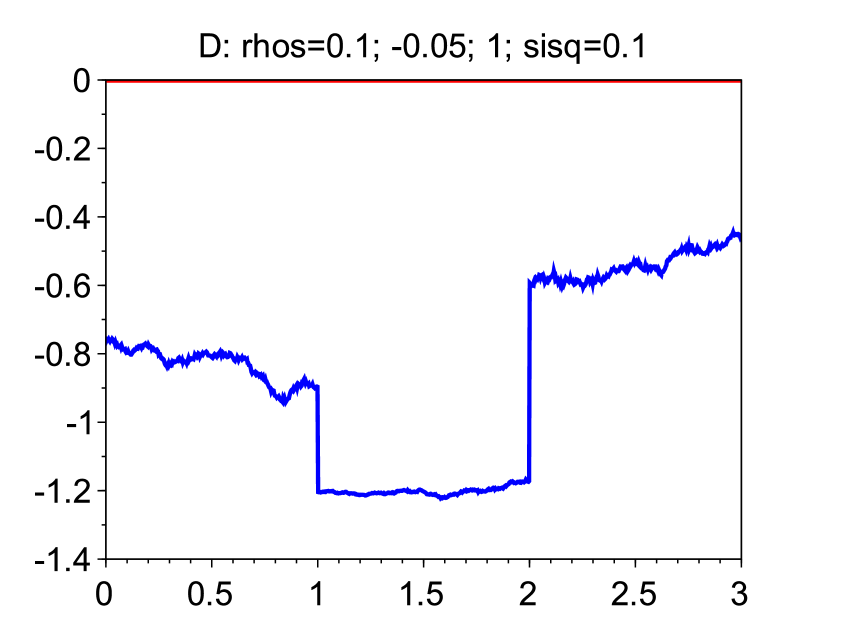

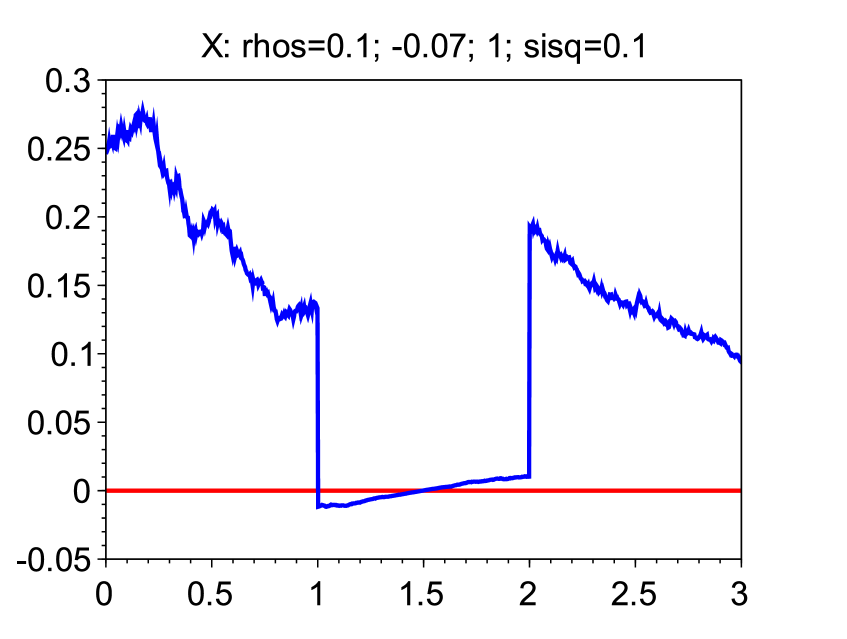

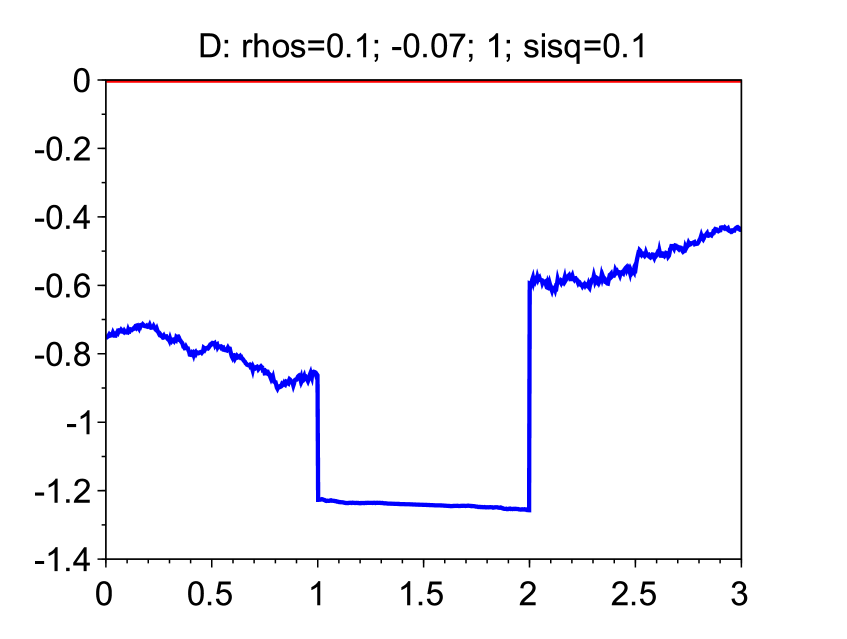

4.2 A case study with piecewise constant resilience and stochastic optimal strategies

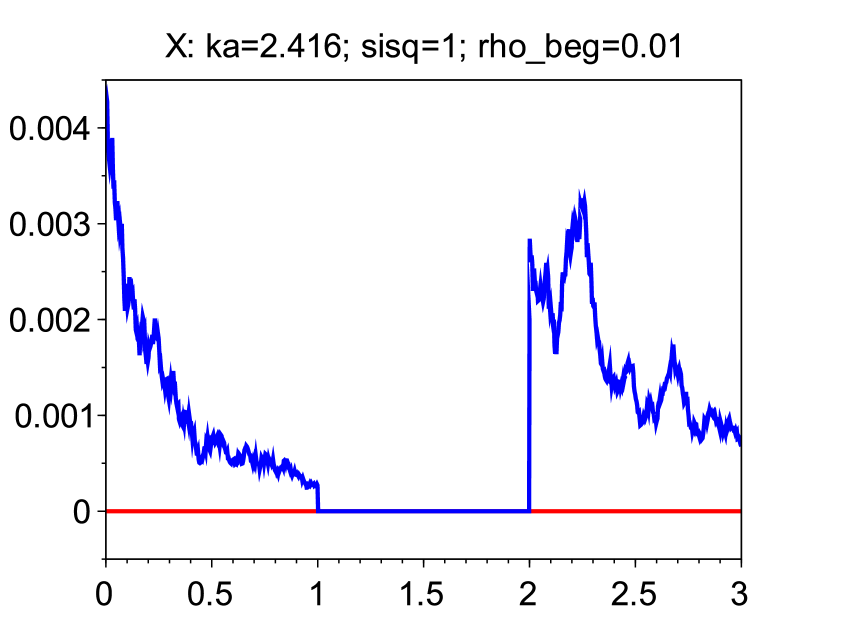

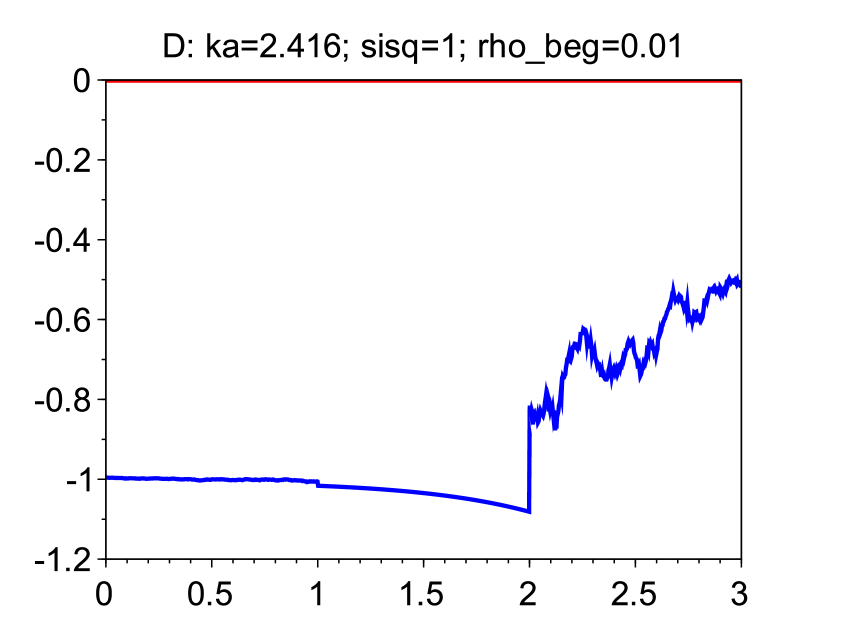

We here consider a similar setting as in Section 4.1, but now can be a deterministic constant different from . Although the solution of BSDE (7) and the process are still deterministic, the optimal strategy and its associated deviation in general become stochastic. The properties derived in 4.1 that is constant between jumps and that is monotone between jumps then no longer hold. However, we can produce the main effects discussed in 4.2, 4.3, and 4.4 also in the case with nonzero . Let , , , , , . Assume as in 4.1 with , , , , , , , and a chosen appropriately for each example. Then, for , we see that everywhere, which implies that neither overjumping zero nor premature closure is optimal (cf. the first row of Figure 2). This is just as in 4.2. In order to obtain the same effect as in 4.3, we consider . Then, , and jumps above in and goes through on (cf. the second row of Figure 2). Consequently, both overjumping zero and premature closure are optimal in this case. If we set , we observe that (cf. the third row of Figure 2), and that overjumping zero is optimal, but premature closure is not. This is the analogon of 4.4.

4.3 A case study with premature closure over a time interval

In 4.3 the optimal strategy entails to close the position at a certain point in time and reopen it immediately. On the other hand, in the case , it is optimal to close the position immediately and not to reenter trading (cf. [1, Proposition 3.7]). In the same way we can show that if, say, on , for some , then the optimal strategy satisfies on (and it can involve non-trivial trading on depending on behaviour of the model parameters on ). Keeping the position closed during a time interval and reopening again is more tricky, but also possible, as we show next. For an illustration, we refer to Figure 3.

Let such that . Suppose that is a deterministic constant and that . For deterministic , , and let

| (28) |

Note that (1) and (2) are satisfied. Let be the unique solution of the ODE (cf. (7) in the current setting)

| (29) |

We have (10) with

This implies that

In the sequel we establish that if is chosen such that , then on . To this end, suppose777Observe that to determine it suffices to consider only on . In particular, does not depend on the choice of . Moreover, as , we have (via a straightforward comparison argument for (29)). Therefore, we can set . It follows for this that . that and define on . We show that is a solution of (29) on . It holds for all that

On the other hand, we obtain for all that

In order to show that

| (30) |

note first that this is equivalent to

Denoting , , and using , , we can rewrite this as

The right hand side equals , . We thus obtain the equivalent equation

which clearly holds true. This proves (30). Thus, by uniqueness of the solution of (29) and , we have on . This implies that on . It follows that for all , almost all paths of the optimal strategy (cf. (11)) equal on . Finally, observe that if with , then almost all paths of are nonzero everywhere on because, on , we have , as , i.e., holds nowhere on .

Acknowledgement: We thank two anonymous referees for suggestions that helped improve the manuscript.

References

- [1] J. Ackermann, T. Kruse, and M. Urusov. Càdlàg semimartingale strategies for optimal trade execution in stochastic order book models. Finance Stoch., 25(4):757–810, 2021.

- [2] J. Ackermann, T. Kruse, and M. Urusov. Optimal trade execution in an order book model with stochastic liquidity parameters. SIAM J. Financial Math., 12(2):788–822, 2021.

- [3] A. Alfonsi and J. I. Acevedo. Optimal execution and price manipulations in time-varying limit order books. Applied Mathematical Finance, 21(3):201–237, 2014.

- [4] A. Alfonsi and P. Blanc. Dynamic optimal execution in a mixed-market-impact Hawkes price model. Finance Stoch., 20(1):183–218, 2016.

- [5] A. Alfonsi, A. Fruth, and A. Schied. Constrained portfolio liquidation in a limit order book model. Banach Center Publ, 83:9–25, 2008.

- [6] A. Alfonsi, A. Fruth, and A. Schied. Optimal execution strategies in limit order books with general shape functions. Quantitative Finance, 10(2):143–157, 2010.

- [7] A. Alfonsi and A. Schied. Optimal trade execution and absence of price manipulations in limit order book models. SIAM Journal on Financial Mathematics, 1(1):490–522, 2010.

- [8] A. Alfonsi, A. Schied, and A. Slynko. Order book resilience, price manipulation, and the positive portfolio problem. SIAM Journal on Financial Mathematics, 3(1):511–533, 2012.

- [9] R. Almgren. Optimal trading with stochastic liquidity and volatility. SIAM Journal on Financial Mathematics, 3(1):163–181, 2012.

- [10] R. Almgren and N. Chriss. Optimal execution of portfolio transactions. Journal of Risk, 3:5–40, 2001.

- [11] S. Ankirchner, M. Jeanblanc, and T. Kruse. BSDEs with singular terminal condition and a control problem with constraints. SIAM Journal on Control and Optimization, 52(2):893–913, 2014.

- [12] P. Bank and Y. Dolinsky. Continuous-time duality for superreplication with transient price impact. Ann. Appl. Probab., 29(6):3893–3917, 2019.

- [13] P. Bank and Y. Dolinsky. Scaling limits for super-replication with transient price impact. Bernoulli, 26(3):2176–2201, 2020.

- [14] P. Bank and A. Fruth. Optimal order scheduling for deterministic liquidity patterns. SIAM Journal on Financial Mathematics, 5(1):137–152, 2014.

- [15] P. Bank and M. Voß. Optimal investment with transient price impact. SIAM J. Financial Math., 10(3):723–768, 2019.

- [16] D. Becherer, T. Bilarev, and P. Frentrup. Optimal asset liquidation with multiplicative transient price impact. Applied Mathematics & Optimization, 78(3):643–676, 2018.

- [17] D. Becherer, T. Bilarev, and P. Frentrup. Optimal liquidation under stochastic liquidity. Finance and Stochastics, 22(1):39–68, 2018.

- [18] D. Becherer, T. Bilarev, and P. Frentrup. Stability for gains from large investors’ strategies in / topologies. Bernoulli, 25(2):1105–1140, 2019.

- [19] R. Carmona and K. Webster. The self-financing equation in limit order book markets. Finance Stoch., 23(3):729–759, 2019.

- [20] A. Cartea, S. Jaimungal, and J. Ricci. Algorithmic trading, stochastic control, and mutually exciting processes. SIAM Rev., 60(3):673–703, 2018. Revised reprint of “Buy low, sell high: a high frequency trading perspective” [ MR3233098].

- [21] T. Cayé and J. Muhle-Karbe. Liquidation with self-exciting price impact. Math. Financ. Econ., 10(1):15–28, 2016.

- [22] A. Fruth, T. Schöneborn, and M. Urusov. Optimal trade execution and price manipulation in order books with time-varying liquidity. Math. Finance, 24(4):651–695, 2014.

- [23] A. Fruth, T. Schöneborn, and M. Urusov. Optimal trade execution in order books with stochastic liquidity. Math. Finance, 29(2):507–541, 2019.

- [24] G. Fu, U. Horst, and X. Xia. Portfolio liquidation games with self-exciting order flow. Preprint, arXiv:2011.05589, 2020.

- [25] G. Fu, U. Horst, and X. Xia. A mean-field control problem of optimal portfolio liquidation with semimartingale strategies. Preprint, arXiv:2207.00446, 2022.

- [26] J. Gatheral, A. Schied, and A. Slynko. Transient linear price impact and Fredholm integral equations. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 22(3):445–474, 2012.

- [27] P. Graewe and U. Horst. Optimal trade execution with instantaneous price impact and stochastic resilience. SIAM Journal on Control and Optimization, 55(6):3707–3725, 2017.

- [28] U. Horst and E. Kivman. Optimal trade execution under small market impact and portfolio liquidation with semimartingale strategies. Preprint, arXiv:2103.05957, 2021.

- [29] U. Horst and X. Xia. Multi-dimensional optimal trade execution under stochastic resilience. Finance and Stochastics, 23(4):889–923, 2019.

- [30] T. Klimsiak and M. Rzymowski. Nonlinear BSDEs in general filtration with drivers depending on the martingale part of a solution. Preprint, arXiv:2103.07536, 2021.

- [31] T. Kruse and A. Popier. BSDEs with monotone generator driven by Brownian and Poisson noises in a general filtration. Stochastics, 88(4):491–539, 2016.

- [32] C. Lorenz and A. Schied. Drift dependence of optimal trade execution strategies under transient price impact. Finance and Stochastics, 17(4):743–770, 2013.

- [33] X. Luo and A. Schied. Nash equilibrium for risk-averse investors in a market impact game with transient price impact. Market Microstructure and Liquidity, 5(01n04):2050001, 2019.

- [34] A. A. Obizhaeva and J. Wang. Optimal trading strategy and supply/demand dynamics. Journal of Financial Markets, 16:1–32, 2013.

- [35] S. Predoiu, G. Shaikhet, and S. Shreve. Optimal execution in a general one-sided limit-order book. SIAM Journal on Financial Mathematics, 2(1):183–212, 2011.

- [36] D. Revuz and M. Yor. Continuous martingales and Brownian motion, volume 293 of Grundlehren der Mathematischen Wissenschaften. Springer-Verlag, Berlin, third edition, 1999.

- [37] A. F. Roch. Optimal liquidation through a limit order book: a neural network and simulation approach. Preprint, SSRN 4057478, 2022.

- [38] A. Schied, E. Strehle, and T. Zhang. High-frequency limit of Nash equilibria in a market impact game with transient price impact. SIAM J. Financial Math., 8(1):589–634, 2017.

- [39] A. Schied and T. Zhang. A market impact game under transient price impact. Math. Oper. Res., 44(1):102–121, 2019.

- [40] E. Strehle. Optimal execution in a multiplayer model of transient price impact. Market Microstructure and Liquidity, 3(03n04):1850007, 2017.