Matching methods for truncation by death problems

Abstract

Even in a carefully designed randomized trial, outcomes for some study participants can be missing, or more precisely, ill-defined, because participants had died prior to date of outcome collection. This problem, known as truncation by death, means that the treated and untreated are no longer balanced with respect to covariates determining survival. Therefore, researchers often utilize principal stratification and focus on the Survivor Average Causal Effect (SACE). The SACE is the average causal effect among the subpopulation that will survive regardless of treatment status. In this paper, we present matching-based methods for SACE identification and estimation. We provide an identification result for the SACE that motivates the use of matching to restore the balance among the survivors. We discuss various practical issues, including the choice of distance measures, possibility of matching with replacement, and post-matching crude and model-based SACE estimators. Simulation studies and data analysis demonstrate the flexibility of our approach. Because the cross-world assumptions needed for SACE identification can be too strong, we also present sensitivity analysis techniques and illustrate their use in real data analysis. Finally, we show how our approach can also be utilized to estimate conditional separable effects, a recently-proposed alternative for the SACE.

keywords:

principal stratification; average effect on the untreated, survivor average causal effect1 Introduction

Randomized controlled trials (RCTs) are considered by many the gold standard for estimating causal effects of treatments or interventions on an outcome of interest. However, even in a carefully designed trial, outcomes for some study participants can be missing, or more precisely, ill-defined, because participants had died prior to date of outcome collection. This problem is known as “truncation by death” (Zhang and Rubin, 2003; Hayden et al., 2005; Lee, 2009; Ding et al., 2011; Ding and Lu, 2017).

Examples of truncation by death in practice are ubiquitous: in clinical studies, when the outcome is Quality Of Life (QOL) index one year after initiating treatment for a terminal disease, but some study participants die earlier (Ding and Lu, 2017; Stensrud et al., 2022); in labor economics, when studying the effect of a training program on wage, but some remain unemployed (in this example, unemployment is the analogue of death) (Lee, 2009; Zhang et al., 2009); in education studies, different school programs are evaluated with respect to students’ achievements, but some students may drop out (Garcia Jaramillo and Hill, 2010).

In the presence of truncation by death, a naive comparison of the outcomes between the treated and untreated groups among the survivors does not correspond to a causal effect. Intuitively, those survived with the treatment might have died had they did not receive the treatment, hence the two treatment groups are not comparable, and are unbalanced with respect to covariates determining survival. An alternative composite outcome approach combines the two outcome types into one, often by setting the outcome to zero for those not surviving. This approach estimates a well-defined causal effect, but it entangles treatment effect on survival with treatment effect on the outcome.

To overcome the lack of causal interpretation for the comparison among the survivors, or the partial information gained by the composite outcome approach, researchers have utilized principal stratification (Robins, 1986; Frangakis and Rubin, 2002) to focus on a subpopulation among which a causal effect is well-defined. The Survivor Average Causal Effect (SACE) is the effect within the subpopulation who would survive regardless of treatment assignment; this subpopulation is often termed the always-survivors.

Identification and estimation of the SACE possess a challenge even in a RCT, as the standard assumptions of randomization and stable unit treatment value assumption (SUTVA) do not guarantee identification from the observed data distribution. As a result, there is a built-in tension between the strength of the assumptions researchers are willing to make and the degree to which causal effects can be identified from the observed data. Ordered by the increasing strength of the assumptions underpinning them, three main approaches have been considered for the SACE: constructing bounds (Zhang and Rubin, 2003; Lee, 2009; Nevo and Gorfine, 2021), conducting sensitivity analyses (Hayden et al., 2005; Chiba and VanderWeele, 2011; Ding et al., 2011; Chiba, 2012; Ding and Lu, 2017; Nevo and Gorfine, 2021) and leveraging additional assumptions for full identification (Hayden et al., 2005; Zhang et al., 2009; Chiba et al., 2011; Ding et al., 2011; Ding and Lu, 2017; Feller et al., 2017; Wang et al., 2017).

The practical use of SACE has been criticized because the underlying subpopulation for which the SACE is relevant can be an irregular subset of the population and because identification of the SACE relies on unfalsifiable assumptions (Robins, 1986; Stensrud et al., 2022). The approach of conditional separable effects (CSEs) (Stensrud et al., 2022), which is applicable to a setting more general than truncation by death, can be used as an alternative to the SACE. In the truncation by death setting, CSEs consider a mechanistic separation of the treatment to the component affecting survival and the component affecting the outcome. Interestingly, these effects can be identified even in a trial that only includes the original treatment, without its mechanistic separation.

Nevertheless, in practice, while researchers across a variety of disciplines increasingly recognize the invalidity of the aforementioned naive approaches (McConnell et al., 2008; Colantuoni et al., 2018), the novel methods and theory developed by causal inference researchers for truncation by death are not yet fully implemented in practice. Therefore, methods that are intuitive, simple to use, and with clear practical guidelines are of need.

The goal of this paper is to introduce matching procedures to analyses targeting the SACE or the CSEs. Traditionally, matching has been used to adjust for pre-treatment differences in observed covariates between the treated and untreated groups in observational studies (Stuart, 2010; Rosenbaum, 2011; Dehejia and Wahba, 1999, 2002; Ho et al., 2007). Here, we propose to use matching to restore the balance originally achieved by randomization, and broken by the differential survival.

With this in mind, the main contributions of the paper are as follows. First, we review and clarify SACE identification assumptions previously considered in the literature and show that weaker assumptions can be used to obtain identification of the SACE. Second, we explain how the obtained observed data functional motivates the use of matching methods. Third, we discuss how matching-based estimation can be used in practice to target the SACE or the CSEs, and discuss for the former how to tailor sensitivity analysis techniques for the presented assumptions when matching is used. Fourth, we demonstrate key ideas for SACE estimation and inference via simulations studies and data analysis.

The rest of the paper is organised as follows. Section 2 presents notations and the SACE causal estimand. Section 3 considers assumptions and the SACE identification result motivating the use of matching as described in detail in Section 4. Section 5 discusses how to tailor sensitivity analysis approaches for the assumptions, when matching is used, and in Section 6, we show how matching methods can be adapted to the recently-proposed CSEs. In Section 7, we present a simulation study, and in Section 8, we illustrate the utility of matching for SACE estimation in a real data analysis. Concluding remarks are offered in Section 9. Code and data analysis are available from https://github.com/TamirZe/Matching-methods-for-truncation-by-death-problems.

2 Preliminaries

Using the potential outcomes framework, for each individual in the population, we let and be the survival status and the outcome, respectively, under treatment value , at a pre-specified time after treatment assignment (e.g., one year). The outcome takes values in if . Truncation by death is introduced by setting whenever . Throughout the paper, we assume SUTVA, namely that there is no interference between units and no multiple versions of the treatment leading to different outcomes.

With these notations, one can define the following four principal strata (Frangakis and Rubin, 2002): always-survivors () , protected () , harmed () , and never-survivors () . Let also represent the stratum of unit and , be the stratum proportions. Because the causal contrast is well-defined only among the always-survivors, researchers often set the SACE,

as the target causal parameter (Rubin, 2006).

For a sample of size from the population, the observed data for each individual is , where is a vector of covariates that are either pre-treatment or unaffected by the treatment; is the treatment indicator ( for a treated individual, and for an untreated individual); is a vector of post-treatment covariates, that are affected by ; is the survival status; is the outcome of interest. From SUTVA it follows that , and . In addition to SUTVA, we assume that treatment was randomly assigned.

Assumption 1

Randomization for .

SUTVA and randomization suffice to identify the causal effect of on survival , but not the SACE or the CSEs (defined in Section 6). The covariates and play a key role in the identification of the SACE or the CSEs. Assumptions on these sets of covariates are necessary, because even though treatment was randomized, truncation by death forces researchers to consider shared causes of the variables and , and their relation to the treatment .

ns, pro as, har ns, har as, pro ns, pro as ns as, pro

3 SACE identification

Because the SACE is not point-identified from the observed data under SUTVA and randomization, additional assumptions have been considered. Possibly the most common assumption, which seems plausible in certain studies, is monotonicity (Zhang and Rubin, 2003; Chiba et al., 2011; Ding and Lu, 2017; Feller et al., 2017; Wang et al., 2017).

Assumption 2

Monotonicity. for all .

Monotonicity means that treatment could not cause death, that is, the harmed stratum is empty. Under monotonicity, SUTVA, and randomization, the proportion of always-survivors is identifiable from the data by . This proportion is crucial in practice, because it speaks to the proportion of the population for which the SACE is relevant. Table 1 presents the possible stratum membership for each unit according to its observed values, with and without the monotonicity assumption.

While the assertion that treatment cannot hurt survival may be reasonable in some studies, the monotonicity assumption is often criticized for being too strong (Ding et al., 2011; Yang and Ding, 2018). To describe a weaker assumption, consider the principal score , where (Ding and Lu, 2017; Feller et al., 2017). For example, the probability of being an always-survivor given the covariates is . We now ready to introduce the constant principal score ratio (CPSR) assumption.

Assumption 3

Constant principal score ratio (CPSR). For all possible values, for some possibly-unknown .

The CPSR assumption asserts that the ratio between the proportions of harmed and always-survivors is constant at all levels of . It is weaker than the monotonicity assumption, under which . An assumption similar to CPSR was previously considered by Ding and Lu (2017) to construct a sensitivity analysis for monotonicity.

To illustrate the interpretation of the two assumptions, consider the following data generating mechanism (DGM). Given a vector of covariates (that may include an intercept), assume that the potential survival status under treatment level follows the logistic regression

| (1) |

Then, among those who would not have survived under , the potential survival status under treatment level follows the logistic regression

| (2) |

and among those that would have survived under , equals to one under monotonicity and to under CPSR. We henceforth call this DGM the “sequential model”. The monotonicity and CPSR assumptions assert that any heterogeneity in survival under treatment, among those who would have survived under no treatment, is not captured by the covariates associated with survival status when untreated (i.e., ). Monotonicity further constraints that all of this subset will survive, while CPSR “allows” for a proportion of those to die. This would be the case, for example, in a trial studying treatment for lung cancer, with death under treatment being due to an adverse event, as a result of treatment damaging a different organ. If this adverse effect is only related to a genetic marker unrelated to lung cancer, it may be that this marker is independent of and hence is independent of . An alternative similar DGM is a multinomial regression for the strata with three categories: protected, never-survivors, and always-survivors or harmed (Section B of the Web Appendix). Then, monotonicity or CPSR constraint the proportion of harmed within the always-survivors or harmed group. We focus mainly on the sequential model because we find its interpretation clearer with respect to the causal assumptions.

We turn to assumptions on the relationship between the potential survival and non-survival outcomes. The first assumption is strongly related to the assumptions known as Principal Ignorability and General Principal Ignorability (Jo and Stuart, 2009; Feller et al., 2017; Ding and Lu, 2017). These assumptions, and their variants, state conditional independence between the potential non-survival outcomes and the principal stratum membership, conditionally on covariates. In this section, we consider an assumption we term partial principal ignorability (PPI) stating that for study participants who would have survived under treatment, conditionally on , the outcome under treatment is not informative about the survival status had those participants were untreated.

Assumption 4

Partial Principal Ignorability (PPI). .

The PPI assumption was considered by Chiba et al. (2011), who also showed that the SACE is identifiable under PPI and monotonicity. A slightly stronger assumption is Strong Partial Principal Ignorability (SPPI).

Assumption 5

Strong Partial Principal Ignorability (SPPI). for .

Hayden et al. (2005) combined SPPI with a strong survival status independence assumption to obtain identification for the SACE.

To illustrate the meaning of PPI, SPPI and the difference between the two assumptions, consider for example the case is QOL, and assume that whenever , the potential QOL is created by

where and are unobserved random variables, independent of all variables introduced so far. If , then both PPI and SPPI will hold. That will be the case if is, e.g., the baseline functionality of a muscle or group of muscles affecting the success in one of the tasks used to measure QOL, but is not informative about survival (at least not conditionally on , if we relax ). If and affects survival and QOL under either treatment status, then PPI and SPPI do not necessarily hold. If, however, for the entire population, the treatment improves the muscle functionality such that the task can be completed successfully, then , and thus, conditionally on , holds no information on , which is exactly PPI. However, does contain information about , even conditionally on . As an additional illustration, we describe in Section A of the Web Appendix a structural equation model under which both PPI and SPPI do not hold due to the post-treatment variables being common causes of and .

Considering each of the two sets of assumptions, it is clear that CPSR is weaker than monotonicity and PPI is weaker than SPPI. Chiba et al. (2011) showed that the SACE is identifiable under PPI and monotonicity. Here we extend this result by providing two new insights. First, the same identification result as in Chiba et al. (2011) holds when PPI is replaced with the stronger SPPI and monotonicity with the weaker CPSR.

Proposition 1

Under SUTVA, randomization, SPPI and CPSR (for any ), the SACE is identified from the observed data by

| (3) |

The proof is given in Section A of the Web Appendix. In this paper, the SACE is studied under randomization. Nevertheless, in Section A of the Web Appendix we extend Proposition 1 for scenarios randomization did not take place and conditional exchangeability is a more plausible assumption. Second, at face value, that the identification formula is the same under PPI and monotonicity, and under SPPI and CPSR, hints a trade-off exists with respect to the different cross-world assumptions. However, this trade-off does not exist, at least not for SACE point-identification.

Proposition 2

PPI and monotonicity together imply SPPI.

The proof is given in Section A of the Web Appendix. By Proposition 2, the combination of SPPI and CPSR is weaker than the combination of PPI and monotonicity. Proposition 1 means that the SACE is identifiable without assuming a value for . Nevertheless, assuming a specific value for has two important implications. First, the principal scores are only identifiable if is known, which means it cannot be used for estimation of the SACE unless a specific value of is assumed (see Section 4). Second, under PPI and CPSR, the SACE is only identifiable if a specific value is assumed (as well as a value for an additional sensitivity parameter, Table A1). We use this to construct a sensitivity analysis for monotonicity under PPI and CPSR as a function of (Section 5). Finally, while is not identifiable from the data, in Section A of the Web Appendix we show that whenever , is bounded within the range , where . When , only the lower bound is applicable.

4 Matching methods for SACE estimation

Proposition 1 implies that a consistent SACE estimator can be obtained by comparing the treated and untreated survivors at each level of , and then average the estimated differences according to the distribution of in the group. In Section A of the Web Appendix, we show that under monotonicity or CPSR, ignoring finite-sample variability, the conditional distribution of is identical to the conditional distribution of . Therefore, matching for SACE estimation seeks to create a matched sample with the following properties:

-

Property (a)

Survivors only. The matched sample includes only survivors .

-

Property (b)

Closeness. Within each matched pair or group of the matched sample, the values of should be close to each other.

-

Property (c)

Distribution preservation. The matched sample should have the distribution of as in the group.

The closeness property underpins having the differences between the treated and untreated at each matched pair/group being sensible estimators of . The distribution preservation property ensures the outer expectation in (1) could be correctly estimated nonparametrically.

In observational studies, we seek to create balance between the treated and the untreated with respect to pre-treatment confounders associated with the treatment and the outcome. For SACE estimation, we also seek to create balance between the treated and the untreated, but with respect to covariates that are associated with the non-mortality outcome and, due to selection bias caused by survival, are also associated with the treatment.

With the three properties in mind, we propose the following general matching procedure and analysis for SACE estimation, which parallels the use of matching in observational studies.

-

Step (i)

Identify covariates for which SPPI (or PPI) is a reasonable assumption.

-

Step (ii)

Choose a distance measure determining proximity of two units , with covariate vectors .

-

Step (iii)

Create matched pairs or groups by matching each unit from to a unit(s) from the group while minimizing the total distances within pairs/groups.

-

Step (iv)

Analyze the matched sample.

Step (i) pertains to SACE identification, discussed in the previous section. Regarding the distance measure (Step (ii)), for the standard use of matching for observational data, three common choices are exact distance (zero if covariate vectors are identical, infinity otherwise), Mahalanobis distance, or the difference in the (logit of) the propensity score. The exact or Mahalanobis distance can also be used for achieving balance on . However, the number of covariates needed for SPPI (or PPI) to hold can be non-small, making the exact and Mahalanobis distances less attractive as distance measures, especially when there are both discrete and continuous covariates on which one would like to match.

In observational studies, matching on the propensity score is justified by its balance properties (Rosenbaum and Rubin, 1983). Recently, analogous results for balance on covariates with respect to different principal strata were derived for functions of the principal scores (Ding and Lu, 2017; Feller et al., 2017). Let , and . Matching on seems attractive because given , always-survivors and protected in are balanced with respect to (Ding and Lu, 2017). Thus, due to randomization, conditionally on , the untreated always-survivors and units in are balanced with respect to . The principal score function can be estimated, e.g., using an EM algorithm (Ding and Lu, 2017). The details of the EM algorithms for the sequential model and for the multinomial regression model are given in Section B of the Web Appendix.

Taking the estimated principal score as the sole distance measure, i.e., , may suffer from disadvantages analogue to those of the propensity score in observational studies, namely, two units with very different covariate vectors can have similar . Furthermore, a potential disadvantage shared by both matching and weighting using is that the analysis relies on correct model specification for the principal scores. This challenge is amplified for principal score models, as they model a latent stratum which is not directly observable for all study participants. A third challenge is that is only identifiable if is known. Assuming (i.e., monotonicity) or any specific value of enables identification and estimation of , but the price is that assumptions stronger than what is needed for SACE estimation are imposed (Table A1 in the Web Appendix). Assuming the wrong value for will then result in bias, which is not expected for methods not using the principal scores. We illustrate this point in Section 7.

A possible compromise is to combine the Mahalanobis distance with a caliper (Rubin and Thomas, 2000; Stuart, 2010) on the principal score, namely

| (4) |

where and are subsets of key covariates from and , respectively, is the empirical covariance matrix of and is a user-specified threshold.

Turning to Step (iii) above, if all are matched, then if the closeness property was achieved, then distribution preservation holds in the matched sample. However, the number of always-survivors in the and groups might differ (e.g., if randomization probabilities are unequal). This may harm both closeness if inadequate matches are made, and distribution preservation if not all group members are matched. A remedy to this problem is found by considering matching with replacement, so potential always-survivors from can be chosen as matches for more than one individual from .

4.1 Analysis of the matched data

Upon achieving reasonable balance, researchers can turn their attention to estimation of and inference about the SACE (Step (iv)). One key use of matching has been as a way to achieve balance so randomization-based inference and estimation can be carried out (Rosenbaum, 2011). Consider the sharp null hypothesis among the always-survivors

| (5) |

The proposed matching framework enables researchers to answer a basic question: is there evidence for a causal effect of the treatment on the non-mortality outcome for at least one person? Failure to reject the null (5) means the data do not support a positive answer to this question.

In a simple 1:1 matched set without replacement, the null hypothesis (5) can be tested using permutation tests, such as Wilcoxon signed-rank test. For 1:1 matching with replacement, the null of no causal effect can be non-parametrically tested by first grouping each treated survivor with all of their untreated matches, and then carrying out the aligned-rank test (Hodges and Lehmann, 1962; Heller et al., 2009).

We turn to estimation and inference based on the sampling distribution. For standard observational studies, the average treatment effect is often estimated by the crude difference between the treated and the untreated among the matched sample, and (paired or unpaired) Student’s -test is used for inference. However, because the analogue of closeness for matching in observational studies typically cannot be achieved with non-small and/or continuous confounders, bias is expected. Abadie and Imbens (2006) studied the magnitude of this bias, gave conditions under which the crude difference estimator is consistent, and derived the asymptotic distribution of this estimator.

It is generally recommended to consider covariate-adjusted treatment effects beyond the crude differences in the matched sample (Stuart, 2010). This may both reduce bias from inexact matching, and improve efficiency of estimators. In our case, one may consider the regression model

| (6) |

and non-linear terms, interactions and additional variables associated with can also be included. Easy to see from (3) that under model (6), the SACE equals to . More generally, given a model for , with parameters , we can write

| (7) |

for some induced by the model. Note that this model can be either non-parametric, semi-parametric or fully parametric. The analysis of the matched dataset starts with obtaining estimates , possibly using weighed estimation when matching is either 1: or with replacement. Then, the SACE can be estimated by , where . Consistency of depends on correctly specifying the model . Asymptotic normality and convergence rates of the estimators depend on the specific model and estimator for . When the model is misspecified, it has been argued that the matching step may reduce the bias due to misspecification (Ho et al., 2007).

A general variance estimator for is unavailable, as variance estimation for post-matching estimators is an active field of research. Even for the simple linear regression case, only recently Abadie and Spiess (2022) have shown that the variance of the estimated coefficients in post-matching regression can be consistently estimated by clustered standard errors (SEs). Their results are valid only for 1: matching without replacement. Furthermore, Abadie and Imbens (2008) showed that when matching is implemented with replacement, the standard bootstrap cannot be used. Abadie and Imbens (2006) derived large sample properties of matching estimators (when matching is with replacement), and proposed consistent variance estimators. They showed that matching estimators are not -consistent in general, and described the required conditions for the matching estimators to be -consistent.

As an alternative to the above-described estimators, we also consider a bias-corrected (BC) approach (Abadie and Imbens, 2011). The BC estimator combines any consistent regression model fitted in the original dataset, with a mean difference estimator. The idea is that the BC estimator adjusts for the bias resulting from inexact matching by adding a bias term to the difference of the means. Abadie and Imbens (2011) showed that the BC approach yields -consistent and asymptotically normal estimators for the average treatment effect and the average treatment effect in the treated, even when the outcome model is fitted using nonparametric series regression, as long as the number of parameters increases slowly enough. Their results can be naturally extended to our case, by recognizing that our proposed approach essentially estimates the average effect on the untreated among the survivors. This is reflected by the outer expectation in (3) being over .

The BC estimator for the SACE under 1:1 matching is constructed as follows. Prior to creating the matched sample, a regression estimator for is calculated. Let index the matched pair, and let and be the observed outcome and covariates for the unit with in matched pair . Then, following Abadie and Imbens (2011), let be the imputed outcome for the treated unit in matched pair . The BC SACE estimator is

| (8) |

As with , will be -consistent only if the model is correctly specified.

5 Sensitivity analyses

Causal inference identification relies on assumptions that are untestable from the data. Therefore, methods are often coupled with sensitivity analyses that relax one or more of the identifying assumptions to obtain an identification result as a function of a meaningful, but unknown, sensitivity parameter(s). Then, researchers can vary the value of this parameter to receive a curve of possible estimates as a function of this parameter. Sensitivity analyses of this type are often used for the SACE (Hayden et al., 2005; Chiba, 2012; Ding and Lu, 2017). Additionally, if these parameters can be bounded, bounds for the causal effect of interest can be estimated.

Here, we describe how the sensitivity analyses proposed by Ding and Lu (2017) for their weighting-based methods can be adapted for matching-based estimators. Like Ding and Lu (2017), our sensitivity parameters are based on the ratio of principal stratum proportions () and the ratio between the mean potential outcomes in different strata (defined below as and ). Because Ding and Lu (2017) developed a sensitivity analysis for a general principal stratum setup, our choice of sensitivity parameters slightly differs. For example, Ding and Lu (2017) uses the ratio for , while we took be the ratio between the harmed and always-survivors (at each level of .

Table A1 in the Web Appendix reviews identifiability of the SACE and of the principal scores, and summarizes the sensitivity parameters needed for identification under each combination of assumptions. Here we focus on sensitivity analysis for PPI/SPPI under monotonicity and for monotonicity under PPI and CPSR.

The first step of both sensitivity analyses carries out matching on among the survivors. The considerations in how to choose the distance measure for this step are the same as described in Section 4.

5.1 Sensitivity analysis for PPI/SPPI

Define to be the mean potential outcome under for units within the principal strata with covariate values . Consider the sensitivity parameter . In words, is the ratio between the mean outcomes under treatment of the protected and of the always-survivors at any value of . Because under PPI, values further away from one reflect a more substantial deviation from PPI. Whether values larger or smaller than one (or both) are taken for could be based on subject-matter expertise. For example, when higher outcome values reflect better health, the always-survivors might be expected to be healthier than the protected (at each level of ) and hence the sensitivity analysis would focus on values smaller than one. In Section A of the Web Appendix we show that can be bounded by . To reduce variance, model-based bounds can be used by fitting a regression model for , and then replacing the minimum and maximum expectations with the minimal and maximal model prediction in the data.

The following proposition provides the basis for the proposed sensitivity analysis.

Proposition 3

Under SUTVA, randomization, and monotonicity, the SACE is identified from the data as a function of by

The proof is given in Section A of the Web Appendix. Under PPI () we obtain the same identification formula as in Proposition 1. Following Proposition 3, matching-based SACE estimation for each value is as follows.

-

1.

Estimate the principal scores and subsequently as described in Section 4.

-

2.

Implement a matching procedure with the chosen distance measure, possibly, but not necessarily, using the estimated .

-

3.

Estimate for .

- 4.

We illustrate the use of this approach in Section 8. Although our proposed sensitivity parameter is identical to the one proposed by Ding and Lu (2017), and although it requires estimation of , it does offer the flexibility of not using it in the matching process, and thus it is expected to reduce, at least to some extent, the dependence of the final results on correct specification of the principal score model.

5.2 Sensitivity analysis for monotonicity

To develop a sensitivity analysis for monotonicity under PPI, without imposing the stronger SPPI, we present here an identification formula under PPI and CPSR, depending on two sensitivity parameters. The first is the previously-defined ratio . Larger values of reflect larger divergence from monotonicity. The second is . With a similar logic to the interpretation of , the sensitivity parameter represents the relative frailty of those at the harmed stratum compared to the always-survivors, as reflected by the ratio between mean outcome when untreated. Similarly to , model-based bounds for can be obtained; see Section A of the Web Appendix.

Unlike the results of Ding and Lu (2017), our proposed sensitivity analysis does not formally require estimation of the principal scores. However, if one wishes to use in the matching process, the principal scores need to be estimated. The following proposition provides the basis for the proposed sensitivity analysis.

Proposition 4

Under SUTVA, randomization, PPI, and CPSR, the SACE is identified from the data as a function of and by

The proof is given in Section A of the Web Appendix.

To utilize Proposition 4 for a sensitivity analysis, we can repeat the following analysis for different combinations of .

-

1.

Implement a matching procedure as previously described, with or without estimating the principal scores.

-

2.

Estimate for .

- 3.

If one chooses to use the principal scores in the matching procedure (e.g., with a caliper on ), the EM algorithm for estimating the principal scores should be revised, and implemented separately for each value of . The details are given in Section B of the Web Appendix.

6 Matching for CSEs and for SACE without PPI

CSEs have been recently proposed as an alternative to SACE. For complete motivation, definitions and theory, we refer the reader to Stensrud et al. (2022). Here we provide a summary of key points, before showing how the matching framework can be used for estimating CSEs.

Two key limitations of the SACE are often raised. First, the always-survivors stratum can be a non-trivial subset of the population, and it cannot be known, both for the observed data and for future individuals, who is an always-survivor and who is not. Second, identification of the SACE relies on cross-world assumptions, namely assumptions on the unidentifiable joint distribution of potential outcomes under different intervention values. Such assumptions cannot be tested from the data nor they can be guaranteed to hold by experimental design. Here, both monotonicity and PPI are cross-world assumptions.

Motivated by these limitations, Stensrud et al. (2022) proposed the CSEs approach. A key prerequisite for this approach is having an alternative to the single treatment , represented by two treatments , with potential outcomes and , such that joint interventions on and lead to the same results as interventions on . The latter is formalized by the modified treatment assumption, which implies that setting or lead to the same potential outcomes of and .

A second critical assumption is partial isolation, that states there are no causal paths between and . Under this assumption,

Under partial isolation, the CSEs for are

| (9) |

In a study of training program effect on employment () and earnings (), can include, for example, modules targeting directly salary negotiation skills and hence are not expected to affect , while represents the rest of the program contents (that affect and may or may not affect ). A detailed example involving cancer treatment () and QOL () is given by Stensrud et al. (2022).

Stensrud et al. (2022) make the point that unlike the members of the principal stratum , the members of the conditioning set can be observed from the data (under certain assumptions). Furthermore, there are scenarios under which the SACE is not identifiable and the CSEs are. Note that the interpretation of (9) as a direct effect of on is non-trivial, because, under the modified treatment assumption and partial isolation, there can still be causal paths between and which do not involve . Nevertheless, under the stronger full isolation assumption there are no such paths, and the CSEs retain an interpretation as a direct effect on . Further discussion of these estimands and their utility can be found in Stensrud et al. (2022).

The following Proposition provides an identification formula for , which resembles our identification formula for the SACE, and even coincides with it under certain conditions. It additionally relies on a positivity assumption and dismissible component conditions, all described in Section 7 of Stensrud et al. (2022).

Proposition 5

Under randomization, partial isolation, the modified treatment assumption, positivity, and the dismissible component conditions

The proof follows from Theorem 1 of Stensrud et al. (2022), and a few more lines given in Section A of the Web Appendix. Proposition 5 resembles the identification result for the SACE presented in (1). Note that for estimation of , the process is identical to SACE estimation by matching, with the only change is being that balance should be achieved with respect to both and . For the matching-based approach for estimation of , the distribution preservation property is revised to have the distribution of in the matched set to be the same as in .

7 Simulation studies

We conducted simulation studies to assess the performance of the matching-based approach and to compare the proposed estimators to naive approaches and to the weighting-based method (Ding and Lu, 2017). The number of simulation repetitions was 1,000 for each simulation scenario. The sample size of each simulated dataset was 2,000. The R package Matching (Sekhon, 2011) was used for the matching process. Technical details, simulation parameters, and additional results are given in Section C of the Web Appendix.

7.1 Data generating mechanism

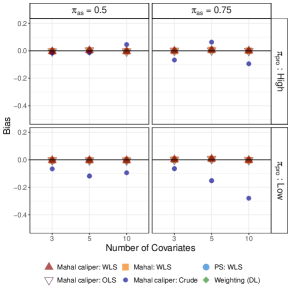

For each unit , a covariate vector of length was simulated from the multivariate normal distribution, , where is a vector of length with entries 0.5, and is the identity matrix of dimension . The stratum was generated according to the sequential logistic regression model (1)–(2) with . We set for a given under CPSR and set under monotonicity. In an additional simulation study, we considered the multinomial regression model for (Section B and Tables C4–C5 of the Web Appendix).

For the always-survivors, the potential outcomes were generated according to linear regression models with means , , and additive correlated normal errors with zero mean, unit variance, and correlation . For the protected or harmed, only or , respectively, were generated, and for the never-survivors, both potential outcomes were truncated by death. For the linear regression models, we considered scenarios including all - interactions and scenarios without including any interaction. The treatment assignment was randomized with probability . Finally, the observed survival status and outcomes were determined by , and .

7.1.1 Scenarios

To have a fair assessment of the finite-sample performance of the different methods, we considered a variety of scenarios under different number of covariates, stratum models and outcome models. In Scenario A, the always-survivors stratum comprised 50% of the population. In Scenario B, the always-survivors stratum comprised 75% of the population. In each of these scenarios, we considered the option of relatively high versus relatively low proportion of protected. These scenarios were created by choosing different values for the sequential logistic regression model coefficients (Tables C2 and C3). The coefficient values were chosen to obtain the desired stratum proportions. We also considered different values for .

In reality, the functional forms of the principal score and the outcome models are unknown to the researchers. Therefore, we conducted simulations under misspecification of the principal score model and/or the outcome model. When misspecified, the true outcome model included squared and exponential terms for two of the covariates, and the true principal score model included such terms and an interaction term of two covariates.

7.2 Analyses

For each of the simulated datasets, we calculated the two naive estimators – the mean difference in the survivors, and the mean difference in the composite outcomes. For the matching approach, we followed the procedure described in Section 4, by matching every untreated survivor to a treated survivor. For the matching-based estimators, we compared matching on ; matching on the Mahalanobis distance; and matching on Mahalanobis distance with a caliper on , taking (Equation (4)) to be 0.25 standard deviations (SDs) of the estimated . An EM algorithm was used to estimate under the sequential logistic regression model. For each of the above options, we considered matching with and without replacement of the treated survivors. Of note is that in practice, as we also illustrate in Section 8, one chooses the distance measure that achieves the best balance, so our assessment of the matching framework approach is likely to be pessimistic.

In the matched datasets, we considered the following estimators: crude difference estimators, linear regression estimators without and with all interactions, and the BC matching estimator (8) (with linear regression for ). The latter is implemented only for matching with replacement (Sekhon, 2011). Ordinary least squares (OLS) was used when matching was without replacement and weighted least squares (WLS) when matching was with replacement.

For matching without replacement, we used the simple SE estimator for the crude differences and clustered SEs for the OLS (Abadie and Spiess, 2022). For matching with replacement, we used SE estimators accounting for weights for the crude and BC estimators (Abadie and Imbens, 2006, 2011; Sekhon, 2011) and clustered weighted SEs for the WLS estimator.

We also considered the model-assisted weighting-based estimator of Ding and Lu (2017) (DL), which uses the estimated principal scores. This estimator was found by the authors to be more efficient than the simple weighting estimator.

As indicated in Section 7.1.1, we considered scenarios with misspecification of the functional form of the principal score model and/or the outcome model. Additionally, for analyses using the principal scores, we repeated the analyses under different (possibly incorrect) specified values for , denoted by .

7.3 Results

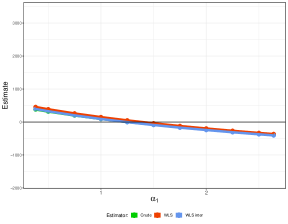

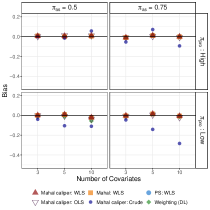

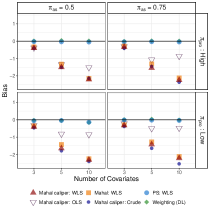

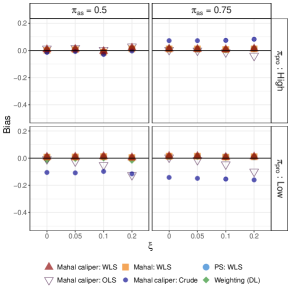

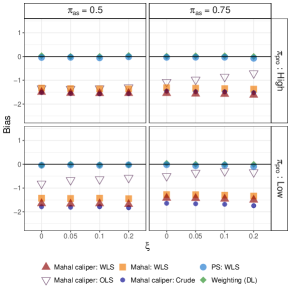

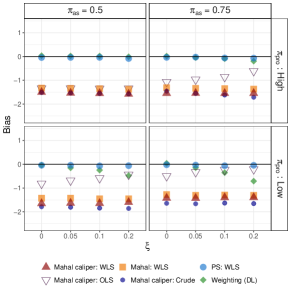

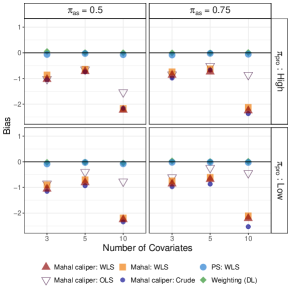

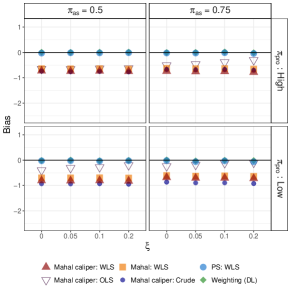

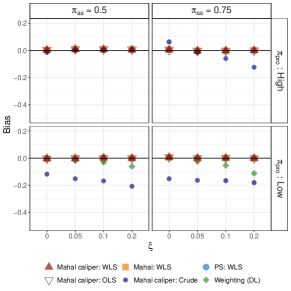

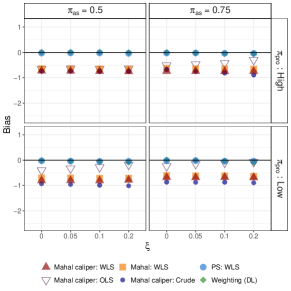

We first focus on the case the true outcome model included all interactions. Figure 1 presents the bias of selected matching estimators and of the DL estimator, under monotonicity. Table 2 presents more estimators and more detailed results on their performance for Scenarios A and B with covariates and low .

When both the principal score and the outcome models were correctly specified, all matching-based estimators and the DL estimator had low or negligible bias in comparison to the naive estimators (Figure 1 and Table 2). The SEs of the regression-based post-matching estimators were generally well estimated (Table 2).

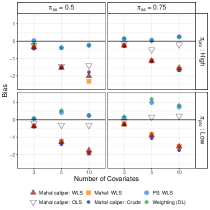

Interestingly, under the sequential regression model, misspecification of the principal score model, but not the outcome model, resulted in minimal bias, for both matching and weighting using . Under a misspecified multinomial regression model for the principal strata, more substantial bias was observed for the DL estimator than for matching using Mahalanobis distance with a caliper on (Figure C6 and Table C13). When only the outcome model was misspecified, methods that use were unbiased, while the model-based estimators after matching on Mahalanobis distance (with or without a caliper) were biased (Figure 1). Under misspecification of both the principal score and the outcome models, all methods showed bias under certain scenarios, with larger bias observed as the number of coefficients grew. A relatively robust estimator was the OLS estimator which followed matching without replacements on Mahalanobis distance with a caliper (Figure 1 and Table 2).

The empirical SDs of all estimators have increased as increased, and when the functional form of the outcome model was misspecified. Under correctly-specified outcome model, the SD of the post-matching model-based estimators were comparable to the SD of the DL estimator. Under a misspecified outcome model, the SD of the DL estimator was larger than those of Mahalanobis post-matching estimators.

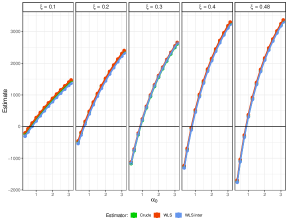

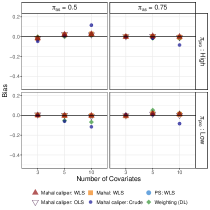

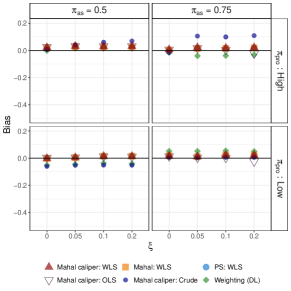

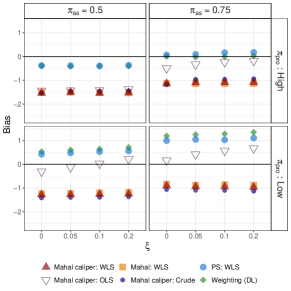

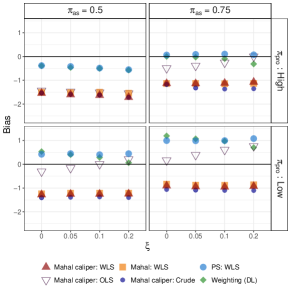

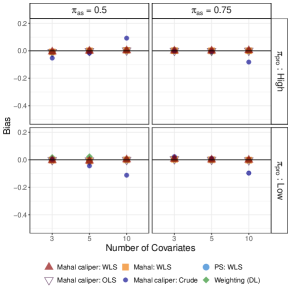

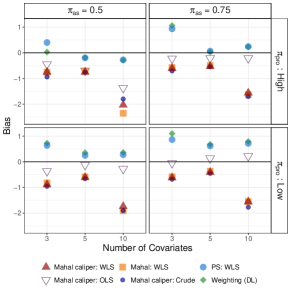

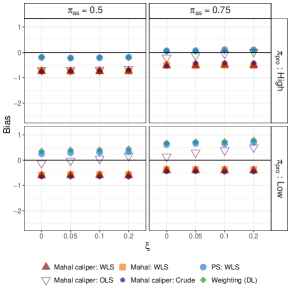

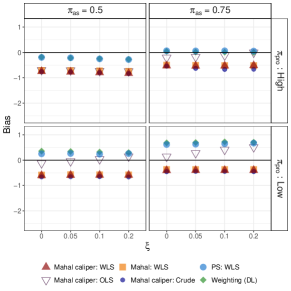

We turn to discuss simulations under , namely when monotonicity does not hold. When the chosen value of was correct (), the performance of nearly all estimators was not affected by the true value (Figure C1).

The post-matching model-based estimators were robust to wrongfully assumed values, even when the principal score model was misspecified, as long as the functional form of the outcome model was correctly specified. In this case, the DL estimator was more sensitive to wrong values, with some bias observed for larger values (Figure C2).

Under a misspecified outcome model and correctly-specified principal score model (but wrong ), the weighting and matching based on were generally less biased than estimators that followed matching on Mahalanobis (Figure C2). When both models were misspecified, results were qualitatively similar to the case where (Figure C1 and Figure C2). That taking impact only methods that use is not surprising, as methods that do not use the principal scores at all do not specify .

Correctly specified principal score and outcome models Misspecified principal score and outcome models Method Estimator Mean Emp.SD Est.SE MSE CP95 Mean Emp.SD Est.SE MSE CP95 Scenario A, SACE = 5 Scenario A, SACE = 10.91 Matching Crude:cal 4.92 0.23 0.20 0.06 0.90 10.16 0.54 0.44 0.85 0.54 Crude:PS 4.90 0.30 0.28 0.10 0.90 10.74 0.67 0.69 0.48 0.95 OLS:cal 4.99 0.17 0.18 0.03 0.97 10.61 0.57 0.42 0.41 0.76 OLS:PS 5.00 0.17 0.18 0.03 0.96 11.36 0.56 0.53 0.51 0.88 Matching Crude:cal 4.89 0.19 0.18 0.05 0.90 9.51 0.38 0.34 2.12 0.04 with Crude:PS 5.03 0.33 0.27 0.11 0.90 10.71 0.93 0.68 0.90 0.83 replacement WLS:cal 5.00 0.18 0.18 0.03 0.96 9.63 0.35 0.44 1.76 0.15 WLS:PS 5.01 0.18 0.18 0.03 0.95 11.33 0.71 0.68 0.68 0.94 BC:cal 5.00 0.18 0.22 0.03 0.98 9.63 0.35 0.41 1.76 0.11 Composite 4.93 0.64 0.64 0.41 0.95 10.76 0.88 0.88 0.80 0.94 Naive 3.94 0.42 0.41 1.28 0.27 10.98 0.67 0.69 0.45 0.96 DL 4.98 0.15 0.02 11.45 0.56 0.60 Scenario B, SACE = 5.77 Scenario B, SACE = 11.38 Crude:cal 5.70 0.22 0.16 0.05 0.83 11.37 0.57 0.39 0.33 0.81 Crude:PS 5.64 0.32 0.21 0.12 0.80 12.44 0.61 0.56 1.49 0.52 OLS:cal 5.78 0.14 0.14 0.02 0.96 11.55 0.52 0.36 0.29 0.82 OLS:PS 5.79 0.14 0.14 0.02 0.96 12.41 0.46 0.45 1.27 0.36 Matching Crude:cal 5.63 0.16 0.14 0.04 0.82 10.32 0.33 0.30 1.23 0.10 with Crude:PS 5.78 0.25 0.20 0.06 0.90 12.51 0.79 0.55 1.90 0.46 replacement WLS:cal 5.79 0.15 0.15 0.02 0.95 10.47 0.32 0.37 0.92 0.31 WLS:PS 5.78 0.14 0.15 0.02 0.95 12.38 0.56 0.56 1.31 0.59 BC:cal 5.79 0.15 0.17 0.02 0.98 10.47 0.32 0.36 0.92 0.28 Composite 6.56 0.56 0.57 0.93 0.73 15.96 0.78 0.76 21.55 0.00 Naive 4.50 0.33 0.33 1.73 0.02 11.80 0.59 0.57 0.52 0.88 DL 5.79 0.12 0.01 12.57 0.44 1.62

The empirical coverage rates of the confidence intervals of the regression post-matching estimators were close the desirable level, and were robust to wrong values, as long as the outcome model was correctly specified. When the outcome model was misspecified, the coverage rates of the confidence intervals for estimators that followed matching on Mahalanobis distance were dramatically lower when . In these situations, coverage rates of the regression estimators after matching on were noticeably closer to the desirable level than other matching estimators.

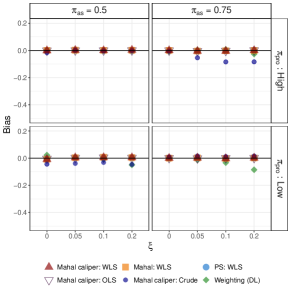

When the true outcome model did not include interactions (Figures C3–C5), the results were qualitatively similar, with the absolute bias being typically lower.

8 Illustrative data example

The National Supported Work (NSW) Demonstration was an employment training program, carried out in the United States during the early 1970s. The NSW aimed to provide work experience for disadvantaged workers and to help them acquire capabilities required at the labor market. Eligible candidates were randomized to participate in the program or to not receive assistance from the program. Further details about the program can be found elsewhere (LaLonde, 1986; Dehejia and Wahba, 1999). Descriptive data, and additional details and results are given in Section D of the Web Appendix. The dataset consists of participants in total, of which (41%) participated in the program and (59%) did not.

The outcome of interest was earnings (wage) in 1978. However, a challenge in considering the effect of the training program on earnings is that only participants () were employed during 1978, () in the treated and () in the untreated. Thus, unemployment at 1978 represents “truncation by death”. Table D14 provides the number and proportion of participants within the four values of . The causal effect of the program on the overall earnings, setting for the unemployed, quantifies the effect on earnings and employment status combined, and not on the earnings alone (Lee, 2009).

A number of pre-randomization variables that are possibly shared causes (or good proxies of shared causes) of employment status and earnings in 1978 are available (Dehejia and Wahba, 1999). These include age, years of education, not having a high school degree, race (white/black/hispanic), marital status (married or not married), and employment status and real earnings in 1975. A description of these covariates is given in Table D15. One may argue that for SPPI to hold, measured covariates should represent pre-trial skills and education, as these are common causes of both future employment status and earnings. While years of education is available, it does not capture the totality of pre-trial education and skills. For this reason, we consider the employment status and earnings in 1975 to be key proxies for these covariates. Nevertheless, it is possible that SPPI or PPI do not hold with the measured covariates, and we therefore also apply to the data the proposed sensitivity analysis.

The covariates were generally balanced due to randomization in the original sample, with the exception of years of education, having a high school degree and employment status in 1975 (Table 3). Looking at those employed in 1978 (), the imbalance got more substantial. Among the employed, compared to the untreated, the treated were older, less likely to be hispanic, and more likely to be married, to own a high school degree, and to be employed in 1975. At each treatment arm, earnings and employment rates in 1975 were higher among the employed, suggesting that participants who managed to acquire a position in 1978 were possibly more skilled before entering the program.

Full Employed Matched Untreated Treated SMD Untreated Treated SMD Untreated Treated SMD Continuous Age 24.4 (6.6) 24.6 (6.7) 0.03 24.1 (6.6) 24.6 (6.7) 0.09 24.1 (6.6) 23.9 (6.2) -0.02 Education 10.2 (1.6) 10.4 (1.8) 0.12 10.2 (1.6) 10.4 (1.9) 0.13 10.2 (1.6) 10.2 (1.5) 0.00 Earnings75 3.0 (5.2) 3.1 (4.9) 0.01 3.4 (5.7) 3.3 (5.1) -0.02 3.4 (5.7) 3.1 (5.2) -0.05 Discrete Black 340 (80%) 238 (80%) 0.00 224 (76%) 176 (77%) 0.02 224 (76%) 221 (75%) -0.02 Hispanic 48 (11%) 28 (9%) -0.06 41 (14%) 25 (11%) -0.09 41 (14%) 36 (12%) -0.05 Married 67 (16%) 50 (17%) 0.03 45 (15%) 44 (19%) 0.11 45 (15%) 54 (18%) 0.08 Nodegree 346 (81%) 217 (73%) -0.21 238 (80%) 167 (73%) -0.20 238 (80%) 241 (81%) 0.03 Employed75 247 (58%) 186 (63%) 0.09 182 (61%) 150 (65%) 0.08 182 (61%) 182 (61%) 0.00

8.1 Results

The composite outcome approach yielded an estimated difference of 886 US dollars (CI95%: -71, 1843) between those participated in the program and those who did not. However, because the program increases employment by approximately 8% (, one-sided test), the above estimates cannot be interpreted as a causal effect on the earnings, but as an effect on employment and earnings combined. The naive difference in the survivors was 409 (CI95%: -690, 1508).

The always-survivors (here always-employed) stratum proportion is identifiable under monotonicity and was estimated to be , which is quite high in comparison to and . Assuming the principal stratum proportions are relatively stable over time, this means the causal effect among the always-survivors stratum is of a high interest in this example, as the always-survivors comprise more than two thirds of the study population.

Turning to the matching, because we had several discrete covariates and a number of continuous covariates, we used the Mahalanobis distance with a caliper on . In our main analysis, we included the continuous covariates age, education and earnings in 1975 in the Mahalanobis distance. We used an EM algorithm to estimate the principal score model with the continuous covariates age and earnings in 1975, and the discrete covariates black, hispanic, marital status, and employment status in 1975. The estimated sequential regression coefficients for are given in Table D16.

As previously noted, a key advantage of matching is that balance can be optimized without looking at the outcome data, and hence without jeopardizing the validity of the analysis. Table D17 presents balance results under several caliper values. The best balance was obtained with (Equation (4)). In the matched sample, the covariates were generally balanced, and compared to the employed (survivors) sample, notable improvements were achieved in the balance of the covariates age, education, high-school degree and employment status in 1975 (Table 3).

Because there were less treated than untreated employed, we used matching with replacement, resulting in matching of all untreated employed participants. The alternative of matching without replacement resulted in only matches out of the () untreated (Table D18).

Turning to the analysis of the matched sample, beyond the crude difference, we also fitted a linear regression model (using WLS) for the outcome with the covariates age, education, black, hispanic, marital status, and earnings in 1975, and compared models with and without all treatment-covariates interactions. For the model with interactions, we estimated the SACE by plugging in the fitted model in (7), and then averaged the obtained quantities across the matched untreated employed. We also calculated the BC estimator, taking the same set of covariates for its regression model. Wald-type 95% confidence intervals were calculated with SEs estimated as described in Section 7.

The crude difference in the matched dataset was 59 (CI95%: -977, 1094). The weighted linear regression estimators were 114 (CI95%: -1226, 1453) without interactions and 55 (CI95%: -1269, 1379) with interactions. The BC estimator (8) was 68 (CI95%: -1376, 1512). The non-parametric aligned-rank test revealed no evidence for rejecting the sharp null hypothesis of no individual causal effect (). The model-assisted weighting approach using the principal scores (Ding and Lu, 2017) estimated the SACE to be 398 (CI95%: -711, 1280, using the bootstrap with 500 samples).

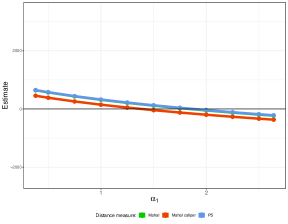

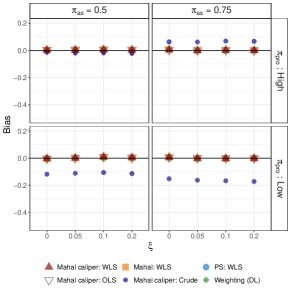

We turn to explore how relaxing the assumptions by using the sensitivity analyses described in Section 5 may affect the conclusions. We used the same matching procedure as in the main analysis. We present here results for the WLS estimator without interactions after matching on the Mahalanobis distance with a caliper.

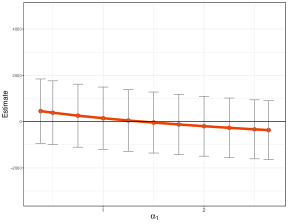

We start with sensitivity analysis for PPI/SPPI under monotonicity. Using a regression model as described in Section 5.1, we obtained . Values smaller than one (larger than one) might imply the always-survivors are believed to be more (less) skilled than the protected and hence are expected to have higher (lower) earnings had they participated in the program.

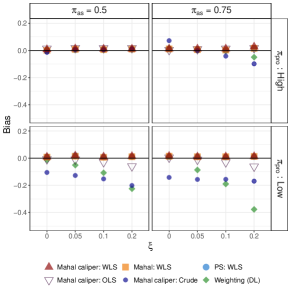

As can be seen from the left panel of Figure 2, as increases, the SACE decreases. For , the SACE was estimated to be negative, meaning that the program decreases the mean earnings among the always-survivors. For all values, the estimates were insignificant ( significance level). Taking the estimated most extreme values, bounds for the SACE under monotonicity are .

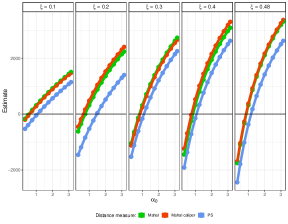

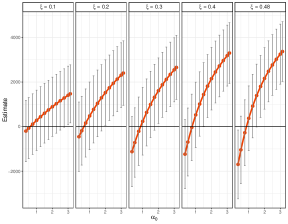

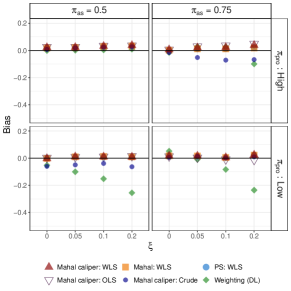

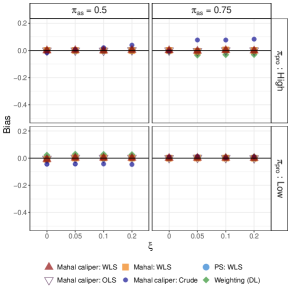

We now turn to sensitivity analysis for monotonicity (Section 5.2). A possible violation of monotonicity might be that program participants raise their reservation wages (the minimal wage they require before accepting a job) due to the program, and therefore may refuse low-earnings job offers they would have accepted had they did not participate in the program (Zhang et al., 2009). Under CPSR instead of monotonicity, the principal scores are identifiable from the data as a function of . In the NSW data, and , thus . Therefore, we considered . Using a regression model as described in Section 5.2, we obtained .

For a fixed , as increases, the SACE increases (Figure 2). As increases, changes in have larger impact on the SACE estimate, as expected from Proposition 4. For each value, the positive effect of the program becomes significant for large enough value. For example, for , meaning there are 2.5 times more always-survivors than harmed at each level of , the SACE is significantly different from zero if the ratio between the mean outcomes of the harmed and the always-survivors when untreated is at least 1.5. Taking the estimated most extreme values, bounds for the SACE under CPSR and PPI are . Sensitivity analyses under different distance measures and using several estimators were overall similar (Figures D7 and D8).

To summarize the conclusions from the data analysis, under monotonicity and PPI (or CPSR and SPPI), no significant causal effect was found on the earnings among those would have been employed regardless of the program participation. Sensitivity analyses revealed that under CPSR and PPI, a positive effect is possible if one believes that the proportion of the harmed stratum is non-negligible and is large enough.

9 Discussion

In this paper, we presented a matching-based approach for estimation of well-defined causal effects in the presence of truncation by death. Underpinning our approach is that the balance created by randomization and lost due to differential survival can be retrieved by a matching procedure achieving the three properties: survivors only, closeness, and distribution preservation.

To fix ideas, we focused in this paper on 1:1 matching with or without replacement, and on classical matching distance measures. In practice, 1:k matching can also be used. Other distance measures or newly-developed matching procedures are also possible to use, and might be more attractive, especially when rich data are available and is high-dimensional. Regardless of the quality of balance achieved on the observed covariates, researchers should be aware that the identifying assumptions for the SACE are strong and cannot be falsified. Hence, the analysis should be accompanied with the proposed sensitivity analyses. Nevertheless, the methods in this paper assume that all covariates in were measured, and without an error. The sensitivity analysis assumes that , for example, is not a function of . If this is not the case, bias is expected. Alternatively, can be replaced by a function specified by the researchers. Specifying such a function, however, might be challenging in practice.

A number of issues concerning matching methods should be highlighted. First, we focused on designs with point-treatment and without loss to follow up. The generalization of matching methods for time-varying treatment is limited compared to other methods, see e.g. Thomas et al. (2020) for a review of matching methods for time-varying treatments when the goal is to study a static treatment regime. A second issue is that standard matching methods typically do not achieve the semi-parametric efficiency bound (Abadie and Imbens, 2006) and can be asymptotically biased (Abadie and Imbens, 2011). The theoretical properties of matching-based methods are understudied compared to other methods, although they are actively studied (Abadie and Spiess, 2022).

Nevertheless, matching methods are one of the most popular tools in the causal inference toolbox of practitioners. We reviewed in this paper the theoretical basis and discussed implementation details for adapting matching methods to adequately overcome truncation by death.

References

- Abadie and Imbens (2006) Abadie, A. and G. W. Imbens (2006). Large sample properties of matching estimators for average treatment effects. econometrica 74(1), 235–267.

- Abadie and Imbens (2008) Abadie, A. and G. W. Imbens (2008). On the failure of the bootstrap for matching estimators. Econometrica 76(6), 1537–1557.

- Abadie and Imbens (2011) Abadie, A. and G. W. Imbens (2011). Bias-corrected matching estimators for average treatment effects. Journal of Business & Economic Statistics 29(1), 1–11.

- Abadie and Spiess (2022) Abadie, A. and J. Spiess (2022). Robust post-matching inference. Journal of the American Statistical Association 117(538), 983–995.

- Chiba (2012) Chiba, Y. (2012). Estimation and sensitivity analysis of the survivor average causal effect under the monotonicity assumption. J Biomet Biostat 3(07), e116.

- Chiba et al. (2011) Chiba, Y., M. Taguri, and Y. Uemura (2011). On the identification of the survivor average causal effect. Journal of Biometrics and Biostatistics 2(5), e104.

- Chiba and VanderWeele (2011) Chiba, Y. and T. J. VanderWeele (2011). A simple method for principal strata effects when the outcome has been truncated due to death. American journal of epidemiology 173(7), 745–751.

- Colantuoni et al. (2018) Colantuoni, E., D. O. Scharfstein, C. Wang, M. D. Hashem, A. Leroux, D. M. Needham, and T. D. Girard (2018). Statistical methods to compare functional outcomes in randomized controlled trials with high mortality. BMJ 360.

- Dehejia and Wahba (1999) Dehejia, R. H. and S. Wahba (1999). Causal effects in nonexperimental studies: Reevaluating the evaluation of training programs. Journal of the American statistical Association 94(448), 1053–1062.

- Dehejia and Wahba (2002) Dehejia, R. H. and S. Wahba (2002). Propensity score-matching methods for nonexperimental causal studies. Review of Economics and statistics 84(1), 151–161.

- Ding et al. (2011) Ding, P., Z. Geng, W. Yan, and X.-H. Zhou (2011). Identifiability and estimation of causal effects by principal stratification with outcomes truncated by death. Journal of the American Statistical Association 106(496), 1578–1591.

- Ding and Lu (2017) Ding, P. and J. Lu (2017). Principal stratification analysis using principal scores. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 79(3), 757–777.

- Feller et al. (2017) Feller, A., F. Mealli, and L. Miratrix (2017). Principal score methods: Assumptions, extensions, and practical considerations. Journal of Educational and Behavioral Statistics 42(6), 726–758.

- Frangakis and Rubin (2002) Frangakis, C. E. and D. B. Rubin (2002). Principal stratification in causal inference. Biometrics 58(1), 21–29.

- Garcia Jaramillo and Hill (2010) Garcia Jaramillo, S. and J. Hill (2010). Impact of conditional cash transfers on children’s school achievement: evidence from Colombia. Journal of Development Effectiveness 2(1), 117–137.

- Hayden et al. (2005) Hayden, D., D. K. Pauler, and D. Schoenfeld (2005). An estimator for treatment comparisons among survivors in randomized trials. Biometrics 61(1), 305–310.

- Heller et al. (2009) Heller, R., E. Manduchi, and D. S. Small (2009). Matching methods for observational microarray studies. Bioinformatics 25(7), 904–909.

- Ho et al. (2007) Ho, D. E., K. Imai, G. King, and E. A. Stuart (2007). Matching as nonparametric preprocessing for reducing model dependence in parametric causal inference. Political analysis 15(3), 199–236.

- Hodges and Lehmann (1962) Hodges, J. and E. L. Lehmann (1962). Rank methods for combination of independent experiments in analysis of variance. The Annals of Mathematical Statistics 33(2), 482 – 497.

- Jo and Stuart (2009) Jo, B. and E. A. Stuart (2009). On the use of propensity scores in principal causal effect estimation. Statistics in medicine 28(23), 2857–2875.

- LaLonde (1986) LaLonde, R. J. (1986). Evaluating the econometric evaluations of training programs with experimental data. The American economic review, 604–620.

- Lee (2009) Lee, D. S. (2009). Training, wages, and sample selection: Estimating sharp bounds on treatment effects. The Review of Economic Studies 76(3), 1071–1102.

- McConnell et al. (2008) McConnell, S., E. A. Stuart, and B. Devaney (2008). The truncation-by-death problem: what to do in an experimental evaluation when the outcome is not always defined. Evaluation Review 32(2), 157–186.

- Nevo and Gorfine (2021) Nevo, D. and M. Gorfine (2021). Causal inference for semi-competing risks data. Biostatistics.

- Robins (1986) Robins, J. (1986). A new approach to causal inference in mortality studies with a sustained exposure period—application to control of the healthy worker survivor effect. Mathematical modelling 7(9-12), 1393–1512.

- Rosenbaum (2011) Rosenbaum, P. R. (2011). Observational studies. Springer.

- Rosenbaum and Rubin (1983) Rosenbaum, P. R. and D. B. Rubin (1983). The central role of the propensity score in observational studies for causal effects. Biometrika 70(1), 41–55.

- Rubin (2006) Rubin, D. B. (2006). Causal inference through potential outcomes and principal stratification: application to studies with “censoring” due to death. Statistical Science 21(3), 299–309.

- Rubin and Thomas (2000) Rubin, D. B. and N. Thomas (2000). Combining propensity score matching with additional adjustments for prognostic covariates. Journal of the American Statistical Association 95(450), 573–585.

- Sekhon (2011) Sekhon, J. S. (2011). Multivariate and propensity score matching software with automated balance optimization: The Matching package for R. Journal of Statistical Software 42(7), 1–52.

- Stensrud et al. (2022) Stensrud, M. J., J. M. Robins, A. Sarvet, E. J. Tchetgen Tchetgen, and J. G. Young (2022). Conditional separable effects. Journal of the American Statistical Association (just-accepted), 1–29.

- Stensrud et al. (2022) Stensrud, M. J., J. G. Young, V. Didelez, J. M. Robins, and M. A. Hernán (2022). Separable effects for causal inference in the presence of competing events. Journal of the American Statistical Association 117(537), 175–183.

- Stuart (2010) Stuart, E. A. (2010). Matching methods for causal inference: A review and a look forward. Statistical science 25(1), 1.

- Thomas et al. (2020) Thomas, L. E., S. Yang, D. Wojdyla, and D. E. Schaubel (2020). Matching with time-dependent treatments: A review and look forward. Statistics in medicine 39(17), 2350–2370.

- Wang et al. (2017) Wang, L., X.-H. Zhou, and T. S. Richardson (2017). Identification and estimation of causal effects with outcomes truncated by death. Biometrika 104(3), 597–612.

- Yang and Ding (2018) Yang, F. and P. Ding (2018). Using survival information in truncation by death problems without the monotonicity assumption. Biometrics 74(4), 1232–1239.

- Zhang and Rubin (2003) Zhang, J. L. and D. B. Rubin (2003). Estimation of causal effects via principal stratification when some outcomes are truncated by “death”. Journal of Educational and Behavioral Statistics 28(4), 353–368.

- Zhang et al. (2009) Zhang, J. L., D. B. Rubin, and F. Mealli (2009). Likelihood-based analysis of causal effects of job-training programs using principal stratification. Journal of the American Statistical Association 104(485), 166–176.

This web appendix includes four major sections. Section A presents theory and proofs. Section B provides details on the EM algorithms used for principal scores estimation. Section C includes further details on and results from the simulation study. The final Section D presents additional information and results from the NSW data analysis.

Appendix

Appendix A Additional theory and proofs

In Section A.1 we present a data generating mechanism (DGM), where PPI and SPPI might be violated due to the existence of common causes of survival and the non-survival outcome that are also affected by the treatment. In Section A.2, we provide proofs for propositions 1-4 from the main text, and present identification formula and proof when randomization is replaced by conditional exchangeability. In Section A.3, we summarizes the sensitivity parameters required for SACE and principal scores identification under different assumption combinations. In Section A.4, we provide derive the bounds for the sensitivity parameters. In Section A.5, we provide a proof of Proposition 5, namely a proof for the alternative presentation of the identification formula of the conditional separable effect .

A.1 Violation of PPI and SPPI due to

We present a DGM under which both PPI and SPPI might be violated because of being affected by the treatment. For simplicity, we consider both and to be univariate. We then show that under further restrictions, PPI holds but SPPI does not. Consider the following non-parametric structural equation model with independent errors (NPSEM-IE)

where are independent, and are binary and where due to truncation by death for all values. Under this NPSEM-IE we have that

| (A1) | ||||

Without further assumptions, PPI (and hence SPPI) are not imposed by this model, because even conditionally on , we may have that . This is because contains information about , which in turn may contain information on and hence on .

PPI will hold but not SPPI under this NPSEM-IE, for example, if we add the assumption that affects Y directly only when untreated (that is, the treatment inactivates the effect of on ). Formally this means that from equation (A1) can be written as

A.2 Proofs and further theory

Throughout the proofs in this section, we denote for either a probability density function, or a joint distribution function (including of a continuous and a binary variable) conditioned on the event . For simplicity of presentation only, we assume in all proofs below that all components of are continuous.

Before presenting the auxiliary lemmas and the proofs, we define two quantities that will be used. Let and be the analogue marginal (with respect to ) quantities of and .

A.2.1 Auxiliary lemmas

Our first lemma states that under randomization and SUTVA, the proportion of always-survivors among the group is the relative size of out of the proportion .

Lemma 1

Under randomization and SUTVA

Proof A.1.

By SUTVA and randomization, we have

The proof for the other claim about is analogous.

An immediate corollary of this Lemma is that the results also hold without conditioning on . That is,

The following Lemma would be useful for our proofs, and is also interesting by itself. It states that under randomization, SUTVA and CPSR, the distribution of the covariates in the untreated survivors is the same as the distribution of in the always-survivors . Since under monotonicity , this result also holds if we replace CPSR with monotonicity.

Lemma A.2.

Under randomization, SUTVA and CPSR

Proof A.3.

First, note that is also the ratio between the marginal stratum proportions. That is,

| (A2) |

Next, by Bayes’ theorem and CPSR, the distribution of in the harmed and in the always-survivors strata is the same,

| (A3) | ||||

Now, by law of total probability and Lemma 1 we may write

| (A4) | ||||

| (A5) |

where (A4) follows from SUTVA and randomization, and (A5) is by (A3).

A.2.2 Proof of Propositions 1 and 4

Proposition 1 is a special case of Proposition 4, when PPI is replaced with the stronger SPPI. Therefore, we first present the proof for Proposition 4, which does not assume SPPI, and then use the fact that under SPPI, , to derive the conclusion of Proposition 1.

First, by law of total expectation and Lemma A.2, we may write

| (A6) | ||||

for . Next, is identified by

| (A7) | ||||

where the first line is by PPI, the second by randomization, and the third by SUTVA. By setting , and substituting (A7) in (A6), it follows that

| (A8) |

Next, to identify , we turn to the identification of . Observe that by SUTVA, randomization, and the fact that are pre-treatment variables which are not affected by we may write

| (A9) |

for . Now,

where the first equality is by SUTVA, the second is by the law of total expectation, the third is by Lemma 1 and (A9), and last line is by the definition of . Reorganizing the terms, we obtain

| (A10) |

Finally, setting , and substituting (A10) in (A6), we get

| (A11) |

where in (A11) we used that . To complete the proof of Proposition 4, we note that the difference between (A8) and (A11) is exactly the SACE. Proposition 1 follows by setting .

A.2.3 Proof of Proposition 2

Formally, SPPI entails the two following statements:

-

1.

.

-

2.

.

Statement 1 is PPI. Statement 2 follows from monotonicity, because deterministically when .

A.2.4 Proof of Proposition 3

First, is identified by

| (A12) | ||||

where the first equality is by monotonicity, the second is by randomization, and the third by SUTVA.

Turning to , observe that by SUTVA, randomization, and the fact that are pre-treatment variables which are not affected by we may write

| (A14) |

for . Now,

where the first equality is by SUTVA, the second is by the law of total expectation, the third is by Lemma 1 and (A14), and the last line is by the definition of . Reorganizing the terms, we obtain that

| (A15) |

Finally, setting , and substituting (A15) in (A6) (Section A.2.2), we get

| (A16) |

To complete the proof, we note that the difference between (A16) and (A13) is exactly the SACE.

A.2.5 SACE identification under conditional exchangeability

In this Section we show that the SACE can be identified when replacing the randomization assumption by a weaker assumption, namely, the following conditional exchangeability (CE) assumption. We focus on the case the same covariates are needed for both SPPI and CE to hold.

Assumption 6

Conditional exchangeability. for .

As with the case of randomization, we start with a Lemma identifying the distribution of among the always survivors. The following Lemma is the analogue of Lemma A.2, under CE instead of randomization.

Lemma A.4.

Under SUTVA, CE, and CPSR

where denotes the probability density function

Proof A.5.

First, by Bayes’ theorem

| (A17) |

Starting with and , we have

Proposition A.6.

Under SUTVA, CE, SPPI and CPSR (for any ), the SACE is identified from the observed data by

| (A23) |

where is defined in Lemma A.4.

Proof A.7.

First, when replacing randomization with CE, (A6) (Section A.2.2), can be replaced, by Lemma A.4, with

| (A24) | ||||

for . Second, the inner expectations in (A6), i.e. , are identified by

| (A25) | ||||

for , where the first equality is by SPPI, the second is by CE, and the third is by SUTVA. Finally, for both and , we plug (A25) in (A24), and consider the contrast between the two, to obtain the identification formula presented in (A23).

A.3 Summary of parameters required for identification

Table A1 reviews identifiability of the SACE and of the principal scores, and summarizes the sensitivity parameters needed for SACE and principal scores identification under each combination of the assumptions. For instance, under PPI and monotonicity, both the SACE and the principal scores are point-identifiable, without specifying any further parameters. Under the weaker combination of SPPI and CPSR, the SACE is point-identifiable (Proposition 1) but the principal scores are not, unless a specific value is assumed for . The table shows that whenever monotonicity is assumed, the principal scores are identifiable. If CPSR is assumed instead, the principal scores becomes identifiable only as a function of . The table also presents a result not discussed in the main text. Under CPSR only, the SACE is identifiable as a function of all three sensitivity parameters.

Assumptions Identification parameters SACE Principal scores PPI monotonicity — — SPPI CPSR — Monotonicity — PPI CPSR CPSR

A.4 Bounds for the sensitivity parameters

A.4.1 Bounds for

We now show that is bounded by

First, it can be shown that the principal stratum proportions can be expressed as a function of and by

Note that because and , then that does not impose any restrictions on . Turning to the next two equations, it is easy to see that for any we have that and are equal to or lower than one. However and are non-negative only if

| (A26) | ||||

| (A27) |

From (A26) we obtain , which imposes a new restriction only if . From (A27) we obtain , as long as . When , might be zero, while is positive and hence it is not possible to obtain an upper bound for .

A.4.2 Bounds for and

We now show that can be bounded by

and can be bounded by

We start with . For , for , and for each value of , denoted by , on one hand we have

| (A28) | ||||

where second is due to randomization and SUTVA, and the last one is due to SUTVA. On the other hand, by similar considerations, it follows that

| (A29) | ||||

Finally, putting together (A28) and (A29), for it follows that for any value of , denoted by , we may write