Scalable Bayesian high-dimensional local dependence learning

Kyoungjae Lee

Department of Statistics, Sungkyunkwan university

Lizhen Lin

Department of Applied and Computational Mathematics and Statistics, University of Notre Dame

Abstract

In this work, we propose a scalable Bayesian procedure for learning the local dependence structure in a high-dimensional model where the variables possess a natural ordering. The ordering of variables can be indexed by time, the vicinities of spatial locations, and so on, with the natural assumption that variables far apart tend to have weak correlations. Applications of such models abound in a variety of fields such as finance, genome associations analysis and spatial modeling. We adopt a flexible framework under which each variable is dependent on its neighbors or predecessors, and the neighborhood size can vary for each variable. It is of great interest to reveal this local dependence structure by estimating the covariance or precision matrix while yielding a consistent estimate of the varying neighborhood size for each variable. The existing literature on banded covariance matrix estimation, which assumes a fixed bandwidth cannot be adapted for this general setup. We employ the modified Cholesky decomposition for the precision matrix and design a flexible prior for this model through appropriate priors on the neighborhood sizes and Cholesky factors. The posterior contraction rates of the Cholesky factor are derived which are nearly or exactly minimax optimal, and our procedure leads to consistent estimates of the neighborhood size for all the variables. Another appealing feature of our procedure is its scalability to models with large numbers of variables due to efficient posterior inference without resorting to MCMC algorithms. Numerical comparisons are carried out with competitive methods, and applications are considered for some real datasets.

The problem of covariance matrix or precision matrix estimation has been extensively studied over the last few decades. A typical model setup is to assume follows a -dimensional normal distribution , with mean zero and covariance matrix . The dependence structure among the variables is encoded by the covariance matrix or its inverse .

In high-dimensional settings where can be much larger than the sample size, the traditional sample covariance matrix or inverse-Wishart prior leads to inconsistent estimates of or , see Johnstone and Lu (2009) and Lee and Lee (2018). Restricted matrix classes with a banded or sparse structure are often imposed on the covariance or precision matrices as a common practice for consistent estimation (see, e.g., Bickel and Levina (2008), Cai et al. (2016) and Lee et al. (2019)).

In this paper, we focus on investigating the local dependence structure in a high-dimension model where the variables possess a natural ordering. An ordering on variables is often encountered for example in time series or genome data, where variables close to each other in time or location are more likely to be correlated than variables located far apart. More specifically, we assume that each variable depends on its neighboring variables or predecessors and more importantly, the the size of the neighborhood or bandwidth can vary with each variable. Therefore, the existing literature on banded covariance matrix estimation which deals with a fixed bandwidth cannot be adapted for this set up.

Our work employs the modified Cholesky decomposition (MCD) (Pourahmadi, 1999) of the precision matrix, which provides an efficient way to learn the local dependence structure of the data.

The MCD has been widely used for covariance or precision matrix estimation including in Rütimann and Bühlmann (2009), Shojaie and Michailidis (2010) and van de Geer and Bühlmann (2013), just to name a few. In more details, assume the variables are arranged according to a known ordering.

For any positive definite matrix , there uniquely exist lower triangular matrix and diagonal matrix such that , where and for all .

It is called the MCD of , and we call the Cholesky factor.

Based on the MCD, is equivalent to a set of linear regression models, and

(1)

In this paper, we assume local dependence structure by considering

(2)

for some instead of (1), which implies for any and .

It leads to a varying bandwidth structure for the Cholesky factor which means that is dependent only on closest variables, , and conditionally independent of others.

Our goal is to learn the local dependence structure of data based on model (2) by learning as well as the varying bandwidth or neighborhood size . Allowing a varying bandwidth in the above model is a more realistic assumption as the range and pattern of dependence can vary over time or spatial locations. See Figure 1 for an illustration of the Cholesky structure with varying bandwidth.

A number of work have been proposed for estimating sparse Cholesky factors based on penalized likelihood approaches, including Rothman et al. (2010), van de Geer and Bühlmann (2013) and Khare et al. (2019).

However, these methods are not suitable for modeling local dependence because they allow arbitrary sparsity patterns for Cholesky factors.

For example, can depend on but not on in their framework, which is not desirable in the context of local dependence.

An et al. (2014) considered a banded Cholesky factor and proposed a consistent test for bandwidth selection, but they assumed the same local dependence structure for all variables, that is, assumed a common instead of in (2). The most relevant work is Yu and Bien (2017) which developed a penalized likelihood approach for estimating the banded Cholesky factor in (2) using a hierarchical group lasso penalty.

Their approach is formulated as a convex optimization problem, and theoretical properties such as selection consistency and convergence rates were established.

However, they required relatively strong conditions to obtain theoretical results, which will be discussed in detail in Section 3.

From a Bayesian perspective, Banerjee and Ghosal (2014) and Lee and Lee (2021) suggested -Wishart priors and banded Cholesky priors for learning local dependence structure with a common bandwidth , and posterior convergence rates for precision matrices are derived assuming is known.

Lee et al. (2019) proposed the empirical sparse Cholesky prior for sparse Cholesky factors.

Under their model each variable can be dependent on distant variables, so it is not suitable for local dependence structure.

Lee and Lin (2020) suggested a prior distribution for banded Cholesky factors.

Although bandwidth selection consistency as well as consistency of Bayes factors were established in high-dimensional settings, again a common bandwidth is assumed in their model. Achieving selection consistency simultaneously for bandwidths of all the variables is a much more challenging problem as the number of bandwidths as well as the size of the bandwidth can diverge as the number of variables goes to infinity.

In this paper, we propose a prior tailored to Cholesky factors with local dependence structure.

The proposed prior allows a flexible learning of local dependence structure based on varying bandwidth .

This paper contributes in both theoretical and practical developments.

For theoretical advancement, we prove selection consistency for varying bandwidth and nearly optimal posterior convergence rates for Cholesky factors.

This is the first Bayesian method for local dependence learning with varying bandwidth in high-dimensional settings with theoretical guarantees.

Furthermore, we significantly weaken required conditions to obtain theoretical properties compared with those in Yu and Bien (2017).

On the other hand, from a practical point of view, the induced posterior allows fast computations, enabling scalable inference for large data sets. The posterior inference does not require Markov chain Monte Carlo (MCMC) algorithms and is easily parallelizable. Furthermore, our simulation studies show that the proposed method outperforms other competitors in various settings.

We find that the proposed cross-validation for the proposed method is much faster than the contenders and selects nearly optimal hyperparameter in terms of specificity and sensitivity.

Finally, it is worth mentioning that posterior inference for sparse Cholesky factors with an arbitrary sparsity pattern is computationally much more expensive than that for banded Cholesky factors, developing a statistical method for banded Cholesky factors is therefore of great importance independent of existing methods for sparse Cholesky factors.

The rest of paper is organized as follows.

In Section 2, model assumptions, the proposed local dependence Cholesky prior and the induced fractional posterior are introduced.

The main results including bandwidth selection consistency and optimal posterior convergence rates are established in Section 3.

In Section 4, the performance of the proposed method is illustrated based on simulated data and real data analysis.

Concluding remarks and discussions are given in Section 5, while the proofs of main results and additional simulation results are provided in the Appendix.

R codes for implementation of our empirical results are available at https://github.com/leekjstat/LANCE.

2 Preliminaries

2.1 Notation

For any and , we denote and as the minimum and maximum of and , respectively.

For any positive sequences and , denotes as .

We denote , or equivalently , if there exists a constant such that for all large . For any matrix , we denote and as the minimum and maximum eigenvalues, respectively.

Furthermore, we define the matrix -norm, Frobenius norm and element-wise maximum norm as follows:

, and . We denote as the inverse-Gamma distribution with shape parameter and scale parameter .

2.2 High-dimensional Gaussian Models

Throughout the paper, we assume a high-dimensional setting with , and that the variables have a known natural ordering.

Specifically, we assume we observe a sample of data with sample size from a -dimensional Gaussian model,

(3)

where is a precision matrix.

For the rest of the paper, we use subscript for any matrices to indicate that the dimension grows as .

Let be a data matrix, and for all .

We denote the Cholesky factor and the diagonal matrix from the MCD as and , respectively, i.e., .

Model (3) is related to a directed acyclic graph (DAG) model depending on the sparsity pattern of (van de Geer and Bühlmann, 2013; Lee et al., 2019), but we will not go into detail on DAG models.

In this paper, we assume has a banded structure with varying bandwidths, , which satisfies and for each .

Let and be sub-matrices of consisting of the th and th columns, respectively.

Under the varying bandwidths assumption, model (3) can be represented as

where .

The above representation implies that to predict the th variable, , it suffices to know its -nearest predecessors, .

Thus, the varying bandwidths assumption of directly induces the local dependence structure between variables.

As mentioned before, this is often natural given commonly encountered ordered variables in time series or genome data sets, and a more realistic and flexible assumption than the common bandwidth assumption.

2.3 Local Dependence Cholesky Prior

To conduct Bayesian inference, we need to impose a prior on and as well as , , which restricts to have a local dependence structure.

We propose the following prior

(4)

for some positive constants and , where .

We call the above prior LANCE (LocAl depeNdence CholEsky) prior.

The conditional prior for is a version of the Zellner’s g-prior (Zellner, 1986) and depends on the data.

By using the prior with sub-Gaussian tails and data-dependent center, we can obtain theoretical properties of posteriors without having to use priors with heavier tails or introducing redundant upper bound conditions on as discussed by Lee et al.(2019).

The prior for is improper and includes the Jeffreys’ prior (Jeffreys, 1946), , as a special case.

In fact, the proper prior , for some constant , can be used.

However, we proceed with the above improper prior to reduce the number of hyperparameters.

For posterior inference, we suggest using the fractional posterior, which has received increased attention recently (Martin and Walker, 2014; Martin et al., 2017; Lee et al., 2019).

Let be the likelihood function of model (3). For a given constant , the -fractional posterior is defined by .

Thus, -fractional posterior is a posterior distribution updated with the likelihood function raised to a power of instead of the usual likelihood.

We denote the -fractional posterior by to indicate the use of -fractional likelihood.

Theoretical properties of fractional posterior can often be established under weaker conditions compared with the usual posterior (Bhattacharya et al., 2019).

Under our model, the -fractional posterior has the following closed form:

(5)

where and .

Based on (5), one can notice that posterior inference for each is parallelizable.

Furthermore, a MCMC algorithm is not needed because direct posterior sampling from (5) is possible.

Note that the three posterior distributions in (5) form the joint posterior distributions of , which are independent for each .

Thus, LANCE prior leads to a fast and scalable posterior inference even in high-dimensions.

3 Main Results

In this section, we show that LANCE prior accurately unravels the local dependence structure.

More specifically, it is proved that LANCE prior attains bandwidth selection consistency for all bandwidths and nearly minimax posterior convergence rates for Cholesky factors. To obtain desired asymptotic properties of posteriors, we assume the following conditions:

(A1)

.

(A2)

For some constant ,

(A3)

for any , , where and

(A4)

The hyperparameters satisfy , , , and .

Condition (A1) allows the condition number to grow to infinity at a rate slower than .

This condition is weaker than the bounded eigenvalue conditions used in Banerjee and Ghosal(2015), Khare et al.(2019) and Lee et al.(2019), which assume for some constants and .

We note here that we require the bounded eigenvalue conditions for the (nearly) minimaxity of the posterior convergence rates in Theorems 3.2 and 3.3.

Condition (A2) determines the lower bound for the nonzero signals, .

This is called the beta-min condition.

It has been well known that the beta-min condition is essential for variable selection (Bühlmann and van de

Geer, 2011; Martin et al., 2017) and support recovery for sparse matrices (Yu and Bien, 2017; Cao et al., 2019).

Condition (A2) implies that the rate of nonzero should, at least, be , which has the same rate with under the bounded eigenvalue condition.

Condition (A3), together with condition (A4), provides an upper bound for the true bandwidth : they allow the maximum bandwidth, , to grow to infinity at a rate not faster than .

The rest of condition (A4) presents sufficient conditions for hyperparameters to obtain theoretical properties.

The conditions on and control the strength of penalty for large models, i.e., large bandwidths.

Note that condition is weaker than the condition used in Lee et al.(2019), which implies that the local dependence assumption requires a weaker penalty compared with arbitrary sparsity patterns.

In Section 4, we will give a practical guidance for the choice of hyperparameters.

Theorem 3.1 (Bandwidth selection consistency)

Consider model (3) and LANCE prior (4).

Under conditions (A1)–(A4), we have

Theorem 3.1 says that the posterior probability of incorrectly estimating local dependence structure, i.e., bandwidths, converges to zero in probability as .

Thus, the proposed method can consistently recover local dependence structure for each variable.

We compare the above result with existing theoretical results in other work.

First of all, we note here that Khare et al.(2019), Cao et al.(2019) and Lee et al.(2019) assumed arbitrary dependence structures for Cholesky factors, thus their methods are not tailored to local dependence structure considered in this paper.

Although Bickel and Levina(2008), Banerjee and Ghosal(2014) and Lee and Lee(2021) focused on banded Cholesky factors, which result in banded precision matrices, they assumed a common dependence structure, i.e., a common bandwidth, for each variable, and did not provide bandwidth selection consistency.

To the best of our knowledge, the state-of-the-art theoretical result for estimating local dependence structure is obtained by Yu and Bien(2017).

They proposed a penalized likelihood approach and obtained bandwidth selection consistency in a high-dimensional setting.

They assumed that the eigenvalues of lie in and the beta-min condition,

for some constants and , where denotes the sub-matrix of the true covariance matrix.

Note that these conditions are more restrictive than our conditions (A1) and (A2).

For example, holds under the bounded eigenvalue condition, so the beta-min condition in Yu and Bien(2017) implies that the minimum nonzero is bounded below by with respect to a constant multiple; in contrast, the rate of the lower bound in condition (A2) is under the bounded eigenvalue condition.

Furthermore, they assumed the so-called irrepresentable condition,

which is typically required for the lasso type methods with a random design matrix (e.g., see Wainwright(2009) and Khare et al.(2019)).

Yu and Bien(2017) proved the exact signed support recovery property under the above conditions and .

Note that condition (A3) together with (A4) implies for some constant .

Hence, stronger conditions are also required by Yu and Bien(2017) to establish bandwidth selection consistency compared with Theorem 3.1.

Next, we show that LANCE prior achieves nearly minimax posterior convergence rates for Cholesky factors.

The posterior convergence rates are obtained with or without beta-min condition (A2).

Under the beta-min condition, Theorem 3.2 presents posterior convergence rates based on various matrix norms.

Theorem 3.2 (Posterior convergence rates with beta-min condition)

Suppose that the conditions in Theorem 3.1 hold.

If , where , we have

for some constant not depending on unknown parameters.

Estimating each row of Cholesky factor can be considered as a linear regression problem with a random design matrix.

By assuming beta-min condition (A2), we can use the selection consistency result in Theorem 3.1, although a beta-min condition is usually not essential for obtaining convergence rates.

With a cost of the beta-min condition, we can focus only on the set for all in the posterior with high probability tending to 1.

Then the above posterior convergence rates for various matrix norms boil down to those related to for various vector norms , which makes the problem simpler.

Assume that for some small constant .

Then, the obtained posterior convergence rates in Theorem 3.2 under the matrix -norm and Frobenius norm are minimax if and for all , respectively, by Theorem 3.3 in Lee et al.(2019).

Therefore, the above posterior convergence rates are nearly or exactly minimax depending on the dimensionality and bandwidths under bounded eigenvalue conditions on .

Now, we establish posterior convergence rate of Cholesky factors without beta-min condition (A2).

To obtain the desired result, we consider a modified LANCE prior using for some constant instead of in (4).

This modification is mainly used to derive a lower bound of the likelihood ratio appearing in the denominator of posteriors (see Lemma 7.1 in Lee et al.(2019)).

Theorem 3.3 shows the posterior convergence rate under various matrix norms.

Theorem 3.3 (Posterior convergence rates without beta-min condition)

Consider model (3) and the modified LANCE prior described above.

Suppose that the conditions (A1), (A3) and (A4) hold.

If , and , we have

for some constant not depending on unknown parameters.

If we assume bounded eigenvalue conditions on , the above posterior convergence rates are slightly slower than those in Theorem 3.2 due to the absence of the beta-min condition. Suppose for some small constant .

Under these bounded eigenvalue conditions, Yu and Bien(2017) (Lemma 17) obtained the convergence rates , and under the element-wise maximum norm, matrix -norm and Frobenius norm, respectively, where for some constant .

Note that, as mentioned before, it holds that without further assumption.

Thus, their convergence rates are slower than or comparable to ours.

We would also like to mention that, under bounded eigenvalue conditions on , the posterior convergence rate under the matrix -norm in Theorem 3.3 is minimax if by Theorem 3.5 in Lee et al.(2019). For example, it is the case if for some .

Remark

By carefully modifying the proof of Theorem 3.6 in Lee et al.(2019), we can probably obtain posterior convergence rates for precision matrices.

However, it is not clear whether the obtained posterior convergence rates are minimax optimal.

Although Liu and Ren(2020) showed minimax rates for precision matrices with bandable Cholesky factors, they considered slightly different parameter spaces for Cholesky factors from what we consider.

To the best of our knowledge, minimax rates for precision matrices based on Cholesky factors with varying bandwidths have not been established.

4 Numerical Studies

4.1 Choice of hyperparameters

The proposed Bayesian method has hyperparameters that need to be determined, and we provide the following guidelines.

It is reasonable to use the hyperparameter close to 1 unless there is a strong evidence of model misspecification.

Thus, in our numerical studies, is used.

We use the hyperparameter , which leads to the Jeffreys’ prior (Jeffreys, 1946) for .

The upper bound for model sizes, , is set at .

The rest of hyperparameters and control the penalty for large models through : as the values of and increase, prefers smaller values of .

We suggest to determine using the Bayesian cross-validation method (Gelman et al., 2014), with the other hyperparameters and fixed.

Compared with the Bayesian cross-validation method for choosing , this approach significantly reduces computational time, while achieving nice performance in our simulation study.

To conduct Bayesian cross-validation, we repeatedly split the data times into a training set and a test set with size and , respectively.

Let and be indices for the th training set and test set, respectively, i.e., , and , for any .

Denote and as and , respectively.

Then for a given hyperparameter , the estimated out-of-sample log predictive density, , is

where , is the marginal likelihood for given , and is the fractional posterior based on and the hyperparameter .

The aim of the Bayesian cross-validation is to find the optimal maximizing .

The marginal likelihood is available in a closed form:

where is the estimated variance using .

The closed form of the marginal posterior is also available in (5), which requires the calculation of .

When calculating , the main computational burden comes from calculating and for each and .

Note that these quantities do not vary from different choices of .

For a given randomly split data, these quantities only need to be calculated once regardless of the value of .

Therefore, LANCE prior enables scalable cross-validation-based inference even in high-dimensions.

Throughout the numerical study, we split the data times.

4.2 Simulated data

Throughout the numerical studies in this section, we focus on the bandwidth selection performance, while additional simulation studies focusing on the estimation performance are given in the Appendix. We generated the true precision matrix for simulation studies.

The diagonal entries of were drawn independently from .

Next, the lower triangular entries of were generated as follows:

•

Model 1:

For , the bandwidth of the th row of is sampled from .

This produces a sparse Cholesky factor with the maximum bandwidth size 5. Each nonzero element in is drawn independently from , where the positive of negative sign is assigned with probability 0.5.

•

Model 2: is a block diagonal matrix consisting of 5 blocks with size , while the maximum size of bandwidths is 40.

This setting produces a moderately sparse Cholesky factor.

The length of the bandwidth of the th row in each block follows a mixture distribution, , where is a point mass at zero.

Each nonzero element in is drawn independently from , where the positive or negative sign is assigned with probability 0.5.

This setting corresponds to Model 2 in Yu and Bien(2017).

•

Model 3: is a block diagonal matrix consisting of 2 blocks with size , and the rest of the generation process is similar to that of Model 2.

This setting produces a denser Cholesky factor compared with Model 2.

This setting corresponds to Model 3 in Yu and Bien(2017).

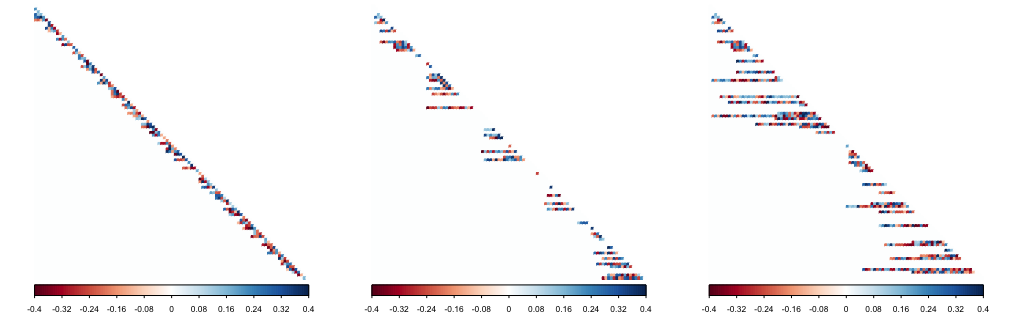

Figure 1 shows a simulated true Cholesky factors for Settings 1 and 2 with and .

Figure 1:

The true Cholesky factors for Model 1 (left), Model 2 (middle) and Model 3 (right) with and .

We compare the performance of the proposed LANCE prior with the penalized likelihood approach in Yu and Bien(2017), which we call YB method.

Since the unweighted version outperformed the weighted version in the simulation studies in Yu and Bien(2017), we used the unweighted version of the penalized likelihood approach.

Furthermore, the convex sparse Cholesky selection (CSCS) (Khare et al., 2019), which is designed for sparse Cholesky factors, is also considered as a contender.

Let and be the estimated Cholesky factor based on the penalized likelihood approach proposed by Yu and Bien(2017) and Khare et al.(2019), respectively.

To estimate the local dependence structure, we set all of the estimated entries in whose absolute values are below to zero, as suggested by Yu and Bien(2017).

The receiver operating characteristic (ROC) curves for LANCE prior and the penalized likelihood approaches were drawn based on 100 hyperparameters selected from and 100 tuning parameters selected from , respectively.

Using these hyperparameter values, we also compare the performance of cross-validation for LANCE prior and YB method.

The Bayesian cross-validation described in Section 4.1 was used for LANCE prior.

For YB method, we used varband_cv function in R package varband.

The -fold cross-validation was used based on the unweighted version of the penalty.

We did not conduct a cross-validation for CSCS method due to heavy computation.

The three methods, the LANCE, YB and CSCS methods, can be run in parallel, although we did not use parallel computing in the numerical study.

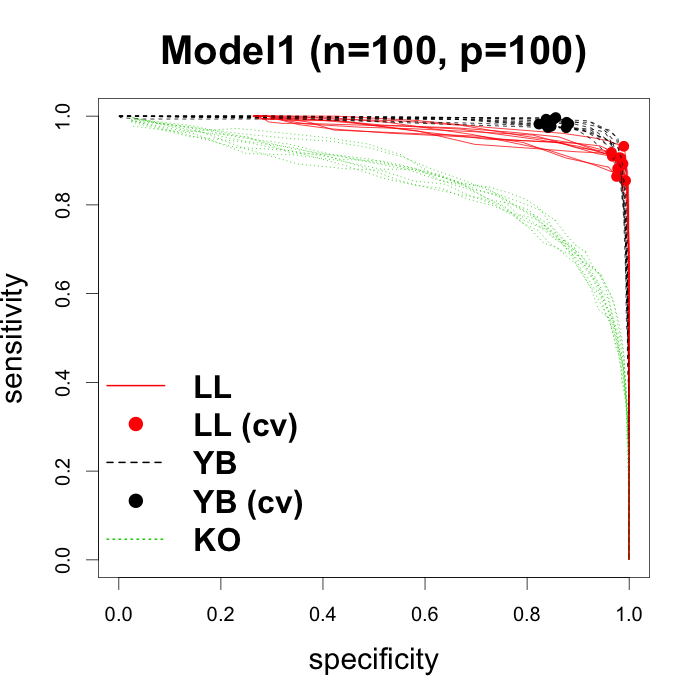

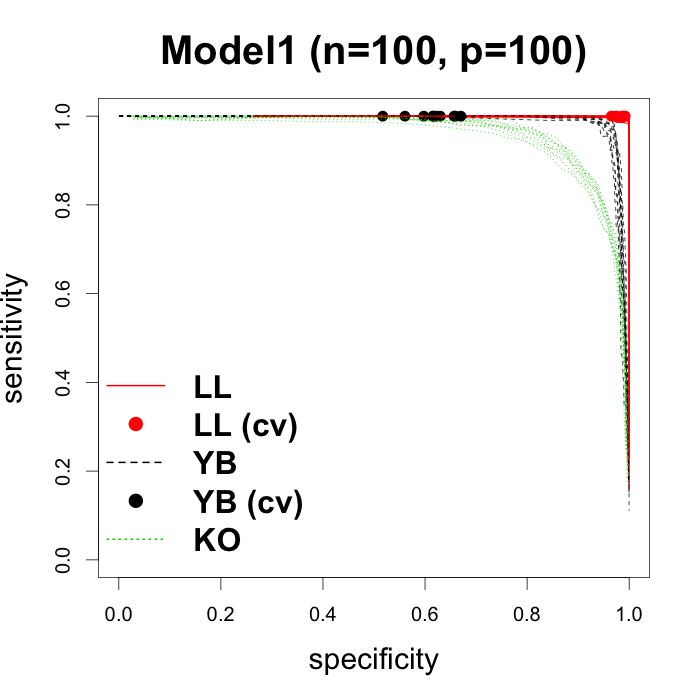

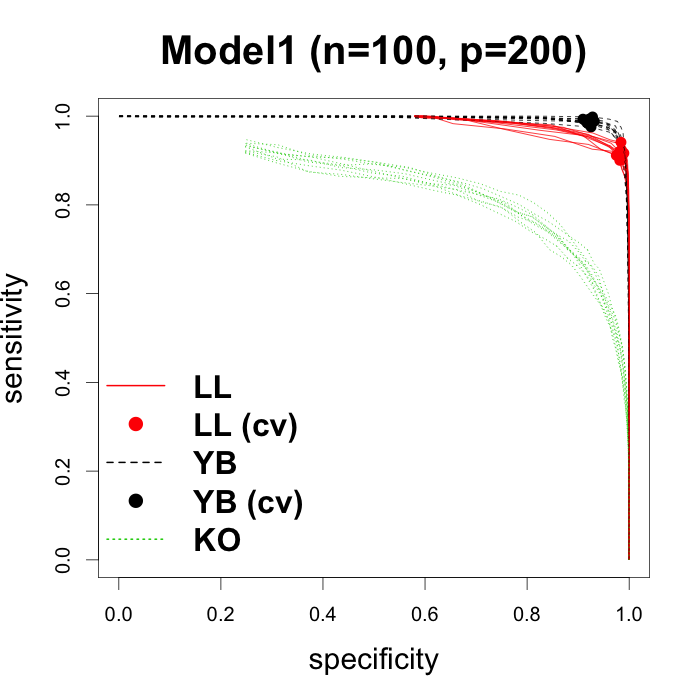

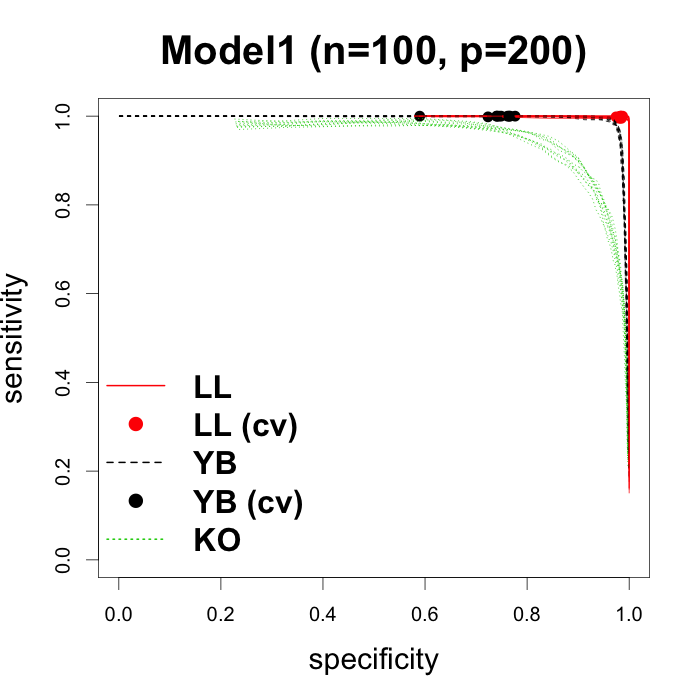

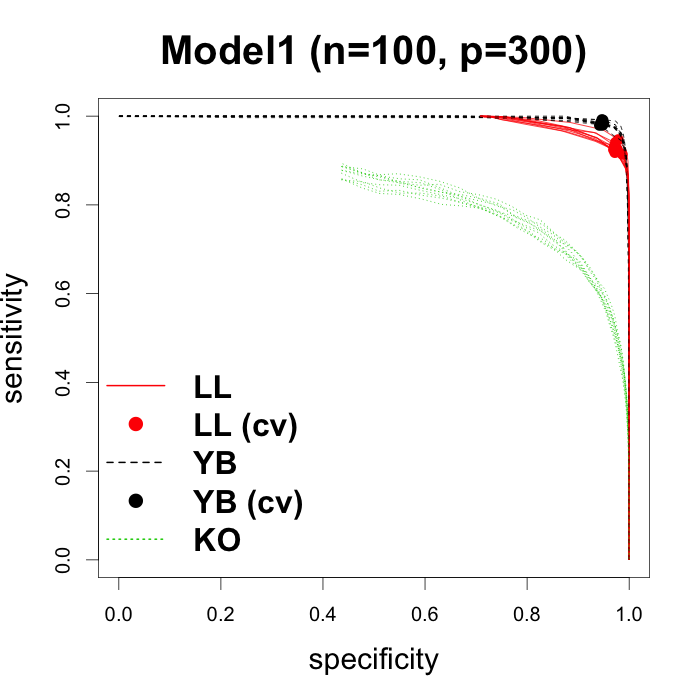

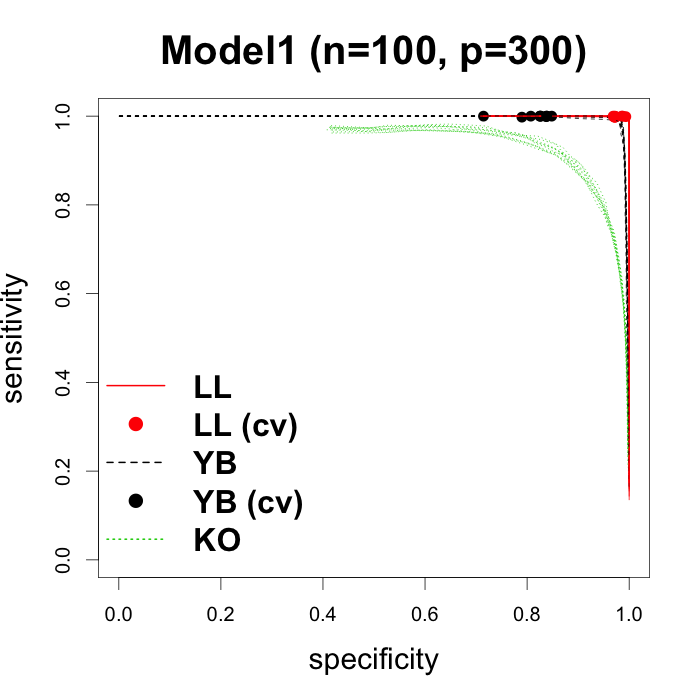

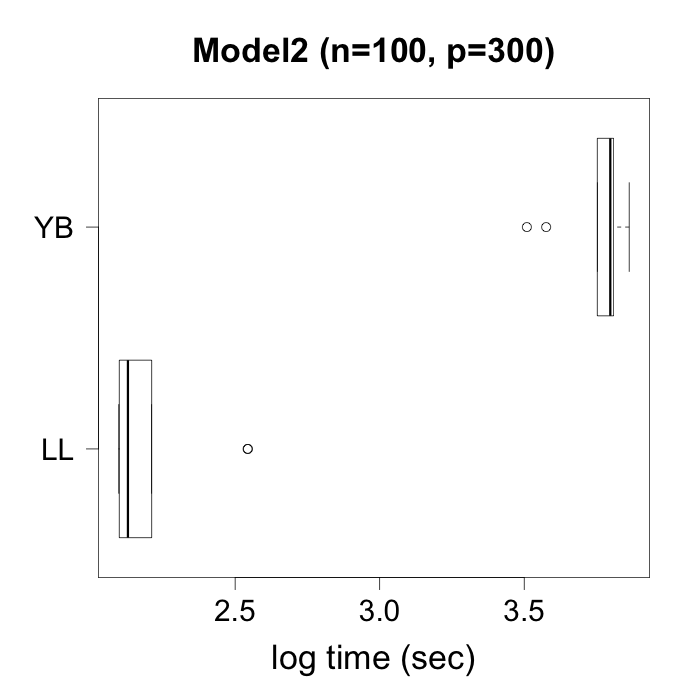

Figure 2:

ROC curves are represented based on 10 simulated data sets from Model 1 with and .

Left column and right column show the results for and , respectively.

LL and YB represent the methods proposed in this paper and Yu and Bien (2017), respectively.

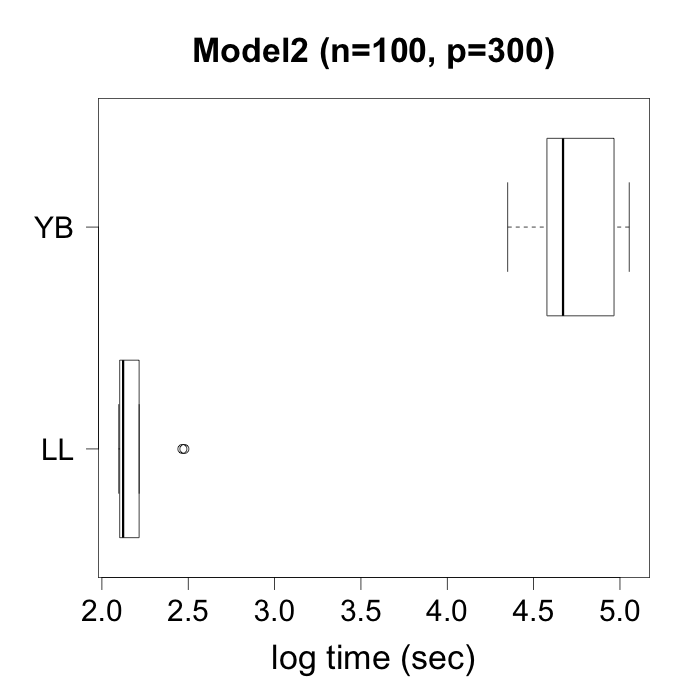

Figure 3:

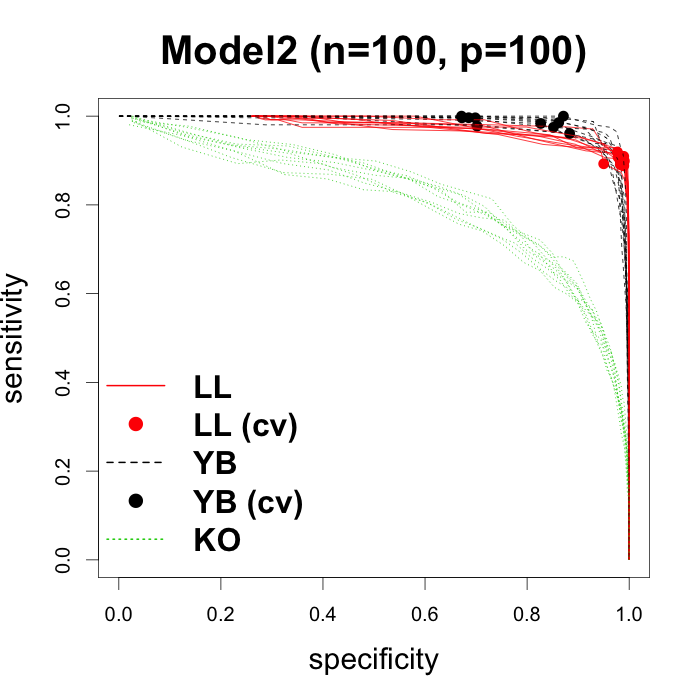

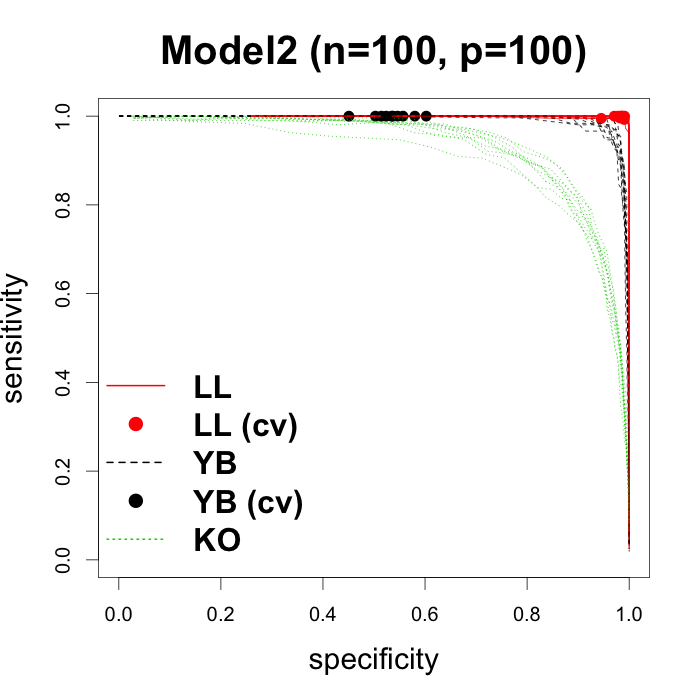

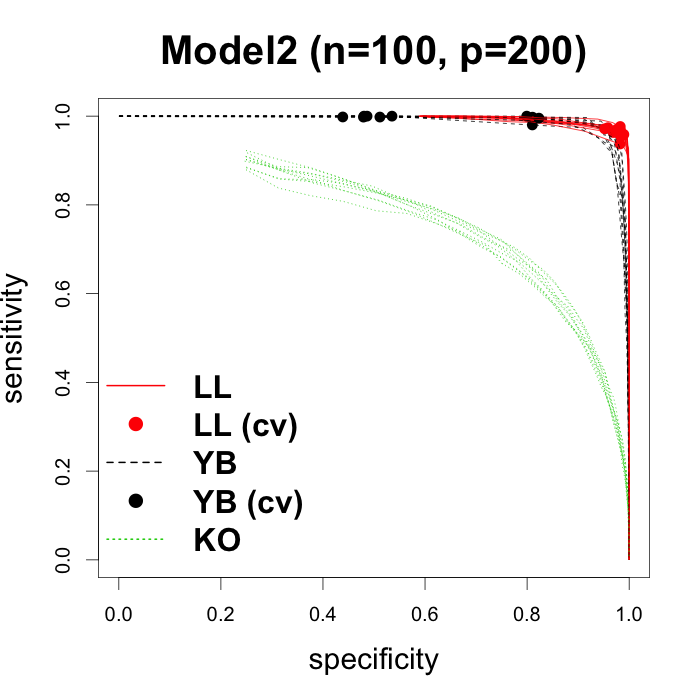

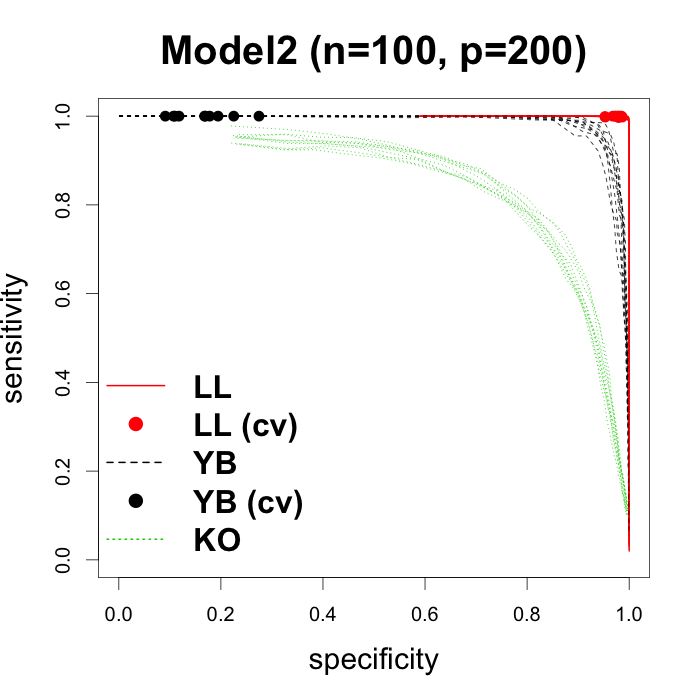

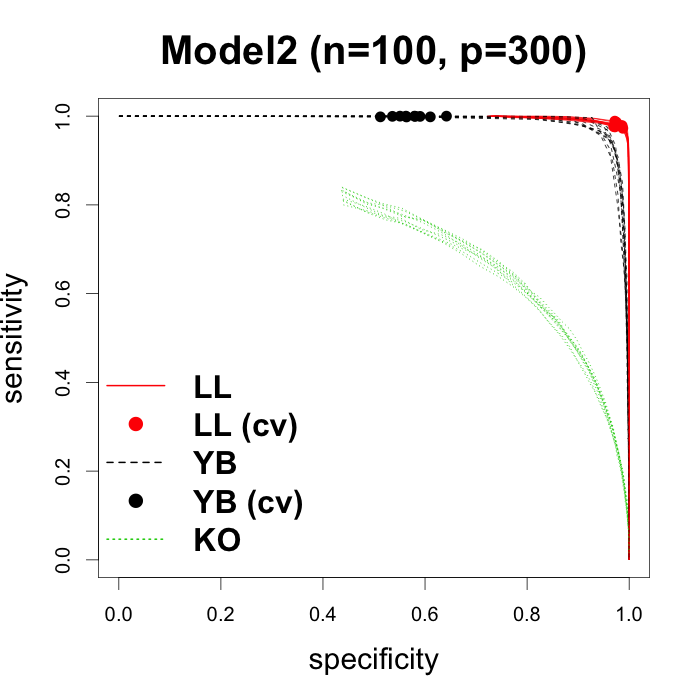

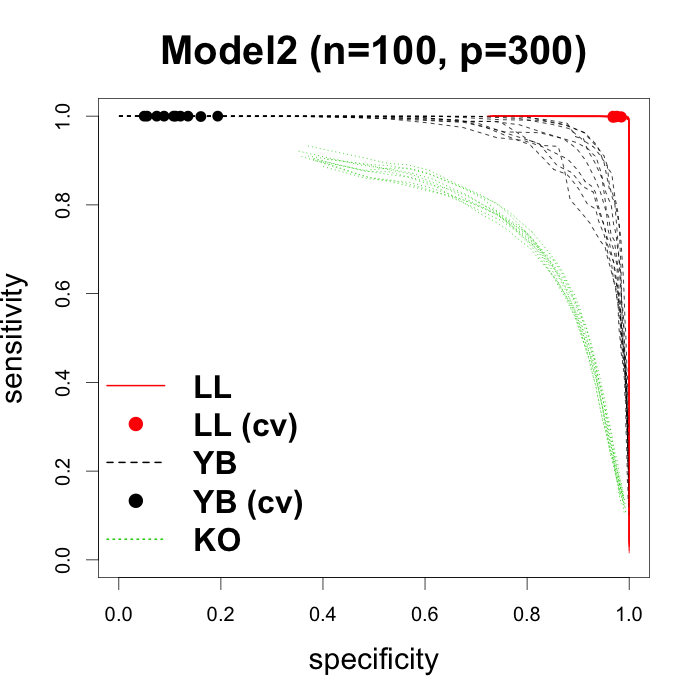

ROC curves are represented based on 10 simulated data sets from Model 2 with and .

Left column and right column show the results for and , respectively.

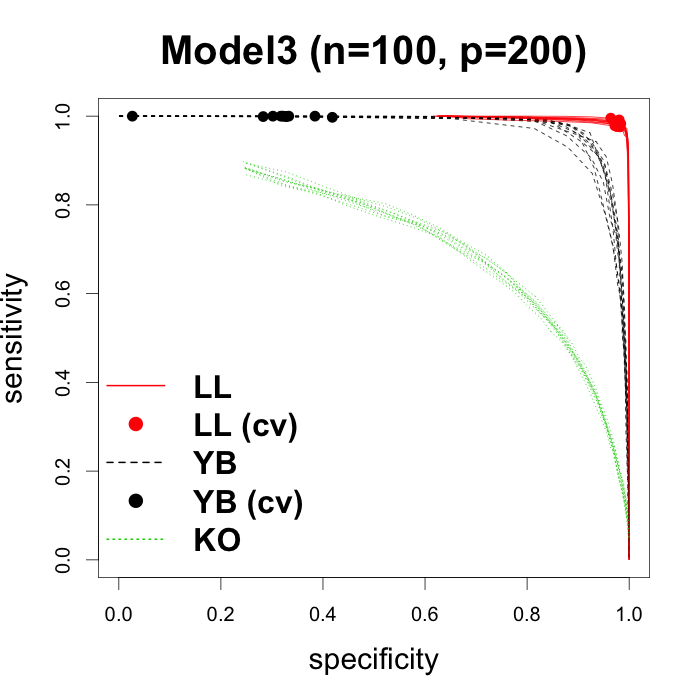

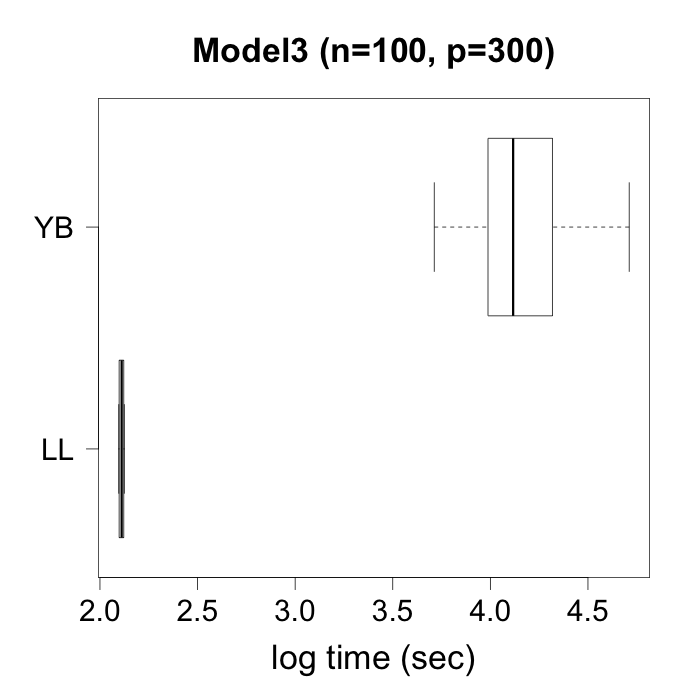

Figure 4:

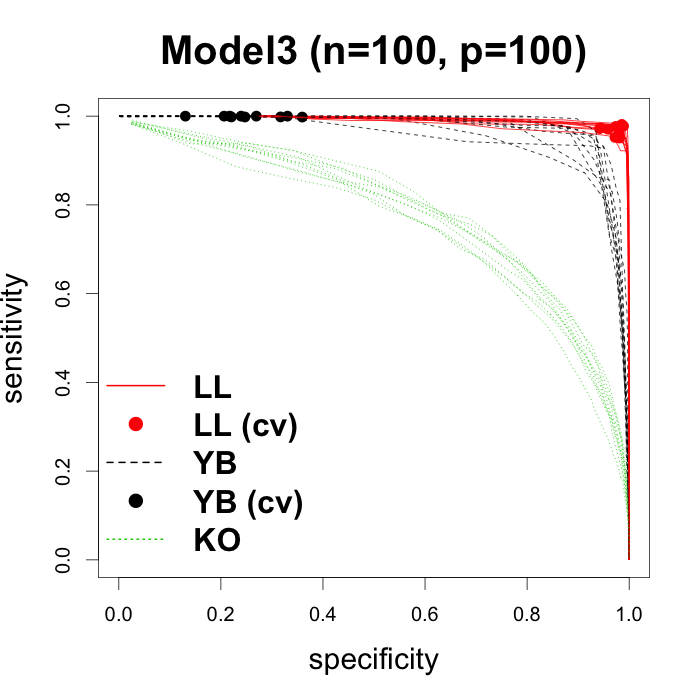

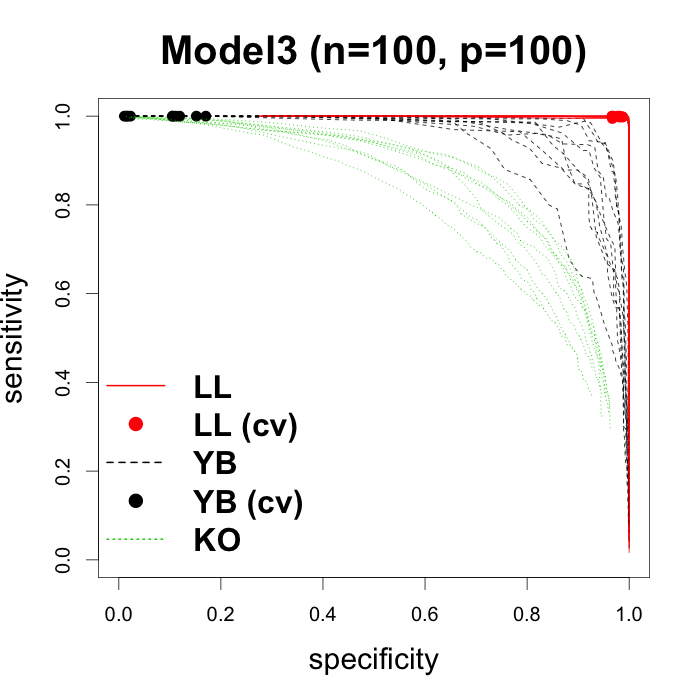

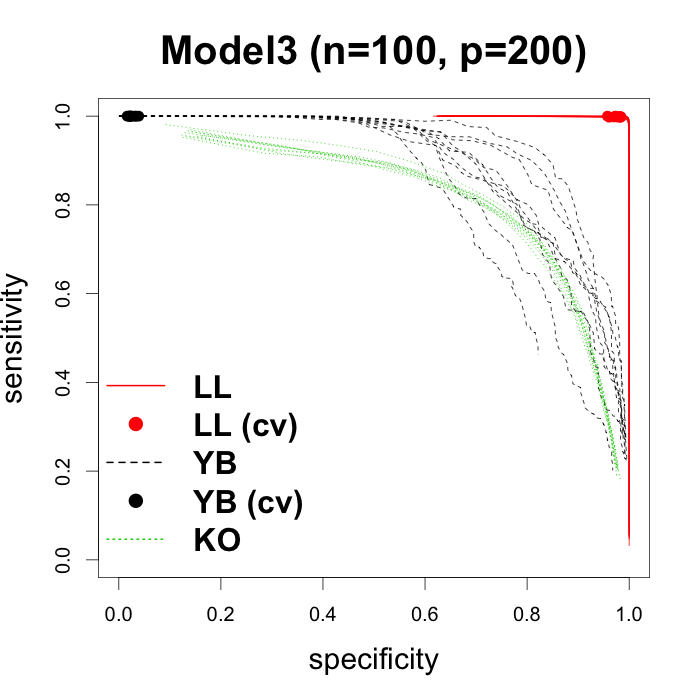

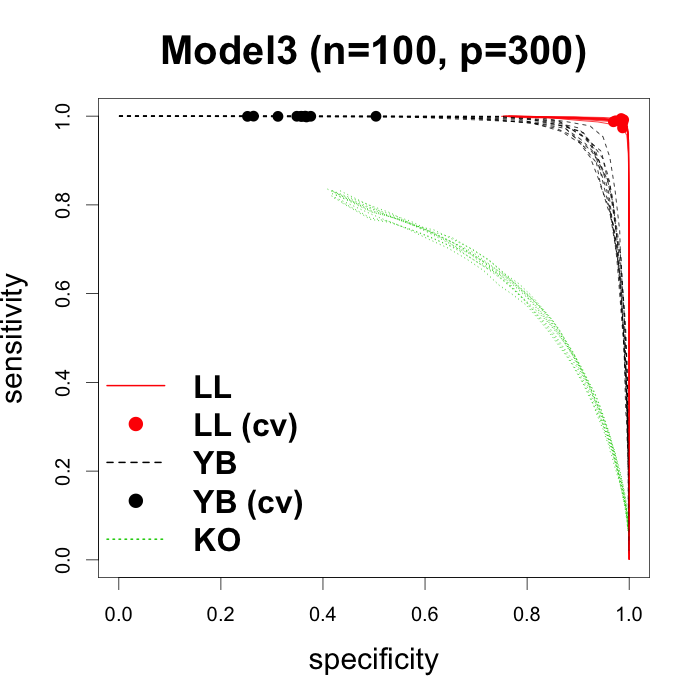

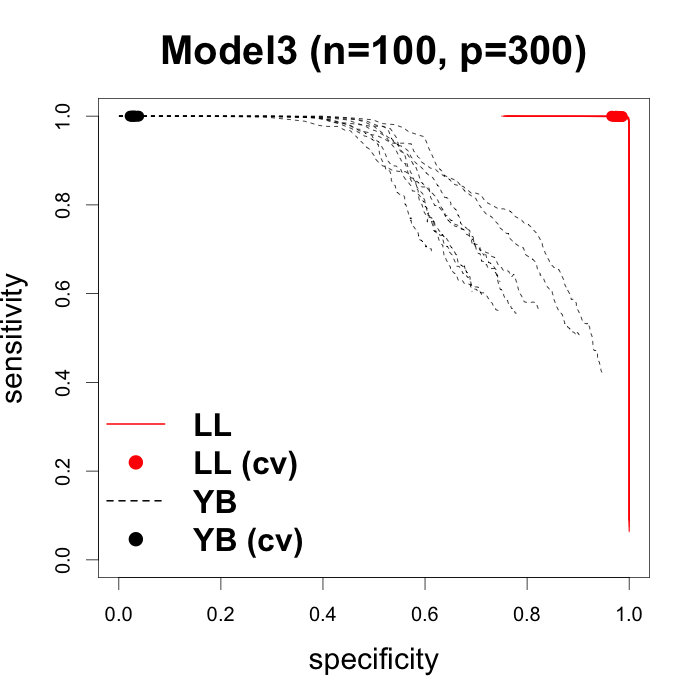

ROC curves are represented based on 10 simulated data sets from Model 3 with and .

Left column and right column show the results for and , respectively.

Figures 2, 3 and 4 represent ROC curves based on 10 simulated data sets for Model 1, Model 2 and Model 3, respectively.

For Model 3 with , we omit the results for CSCS method, because it did not converge for several days and caused a convergence problem.

As expected, CSCS method does not work well compared with other two methods tailored to local dependence structure.

The main reason for this phenomenon is that CSCS method does not guarantee local dependence structure.

Based on the simulation results, the performances of LANCE prior and YB method are comparable in Model 1 (i.e., when bandwidths are smaller than ), but LANCE prior tends to give larger area under the curves than those of YB method in Model 2 (i.e., when bandwidths are moderately large).

Especially in Model 3 (i.e., when bandwidths are large), LANCE prior significantly outperforms YB method especially for large .

Thus, it seems that YB method tends to work better with smaller bandwidths, which is consistent with the observations in Yu and Bien(2017). Furthermore, we found that LANCE prior works better under large signals, , compared with small signals, .

This makes sense because it is expected that large signals will easily satisfy the beta-min condition (A2).

The dots in Figures 2, 3 and 4 show the results based on cross-validation, where red dots and black dots represent those of LANCE prior and YB method, respectively.

We found that cross-validation based on LANCE prior gives nearly optimal result in the sense that the result of the cross-validation method is located close to on the ROC curve.

On the other hand, cross-validation based on YB method tends to produce high false positive, which results in low specificity.

In many cases, even when ROC curves of the two methods are similar, the performances of our cross-validation-based inference are much better than those of YB method.

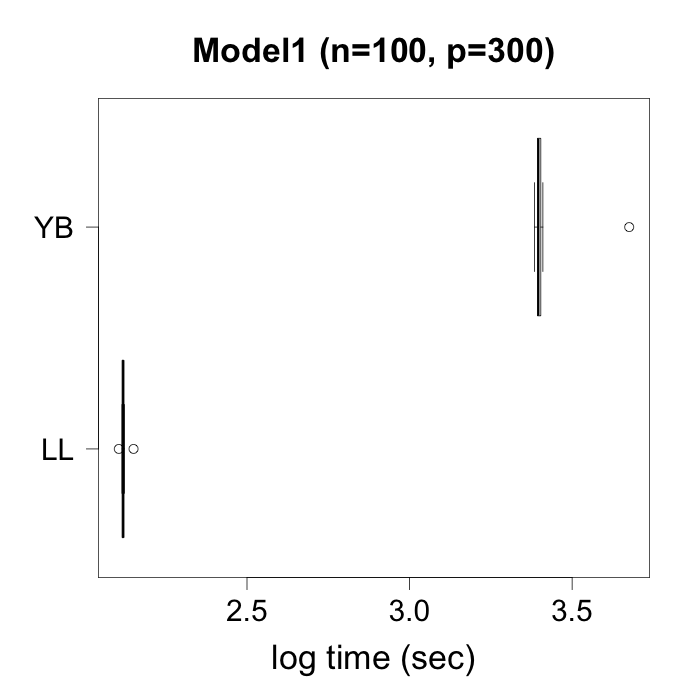

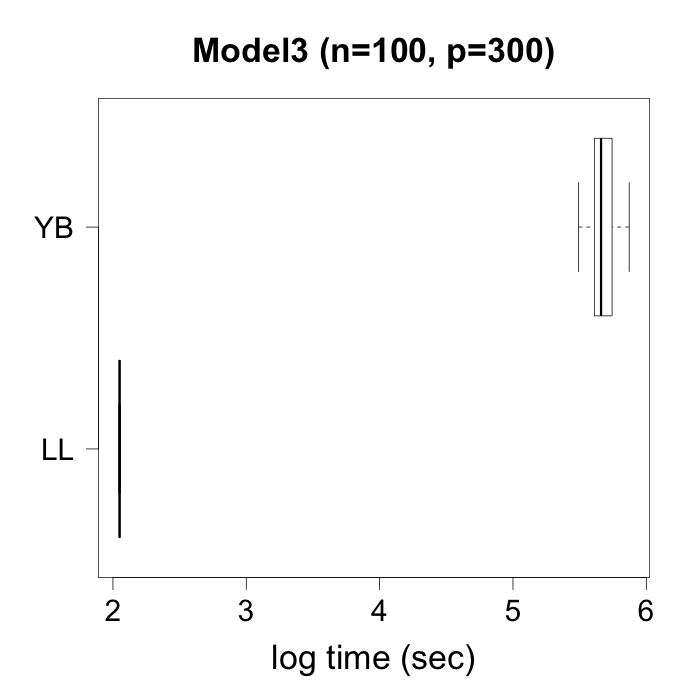

Figure 5:

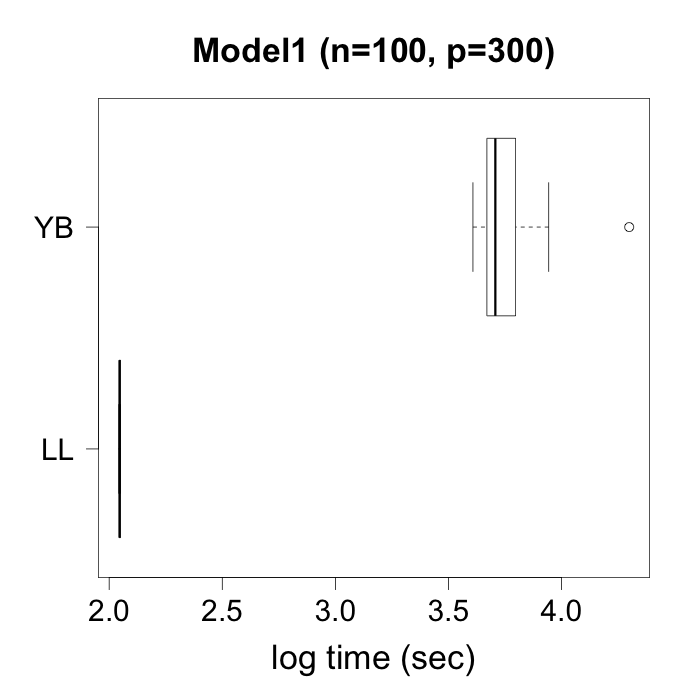

Logarithm of computation times for each method based on 10 simulated data sets.

Left column and right column show the results for and , respectively.

We also found that the proposed method is much faster than YB method in most settings.

Figure 5 shows box plots of the computation times for cross-validation using 100 hyperparameters.

For each method, box plots were drawn based on 10 simulated data sets with and .

The relative computational gain of LANCE prior can be summarized by dividing the computation time for the LANCE prior by that for YB method.

In our simulation settings, the mean and median of the relative computational gain of LANCE prior were 1539 and 208, respectively, which clearly show a computational advantage of the proposed method.

Also note that YB method was conducted using the R package varband providing C++ implementations, while LANCE prior was implemented using only R.

The main reason for this observation is that YB method requires solving a penalized likelihood problem for each value of the tuning parameter .

On the other hand, for LANCE prior, once the estimated error variance, , is calculated, there is no need to recalculate it for various values of .

As a result, the cross-validation for LANCE prior is much faster than the state-of-the-art contender, thus enables scalable inference even in high-dimensions.

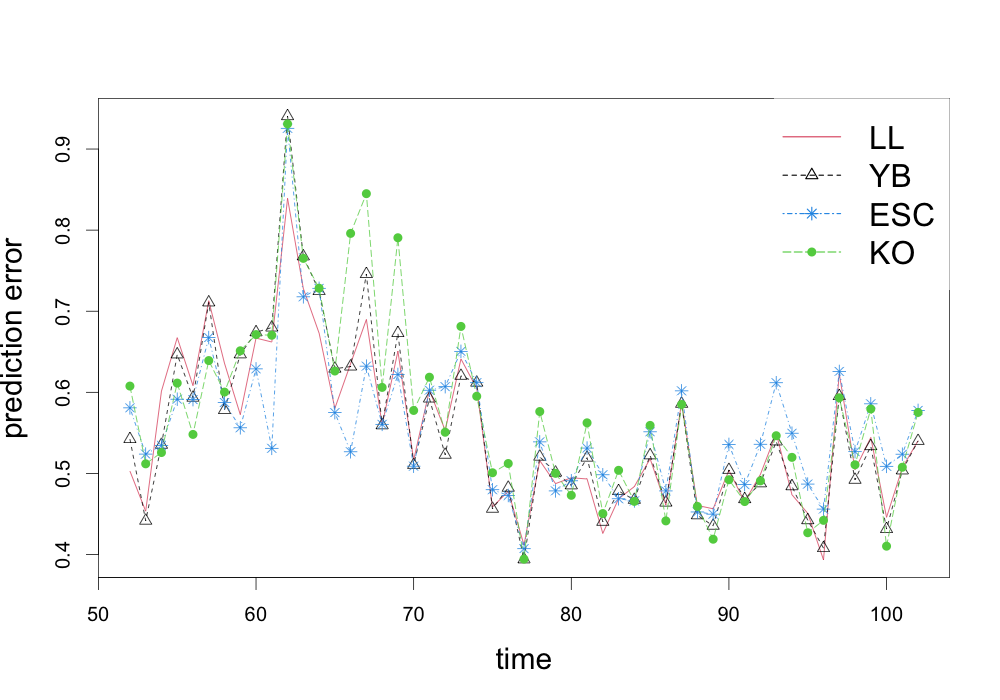

4.3 Real data analysis: phone call center and gun point data

We demonstrate the practical performance of LANCE prior by applying our model to two real data examples. We first consider the telephone call center data set, which was analyzed by Huang et al.(2006) and Bickel and Levina(2008).

This data set consists of phone calls for 239 days in 2002 from a call center of a major U.S. financial organization.

The phone calls were recorded from 7:00 am until midnight for every 10 minutes, resulting in 102 intervals for each day, except holidays, weekends and days when the recording system did not work properly.

The number of calls on the th time interval of the th day is denoted by for and .

The first days are used as a training set , and the last days are used a test set.

The data were transformed to as in Huang et al.(2006) and Bickel and Levina(2008).

The data were centered after the transformation.

Note that the data has a natural time ordering between the variables making it appropriate to apply LANCE prior.

The primary purpose is to predict the number of phone calls during a certain time period.

We divide 102 time intervals for each day into two groups: those before the 51st interval and those after 52nd interval.

For each , we predict using the best linear predictor based on ,

where , and .

The unknown parameters are estimated by and , where are estimated using various methods including LANCE prior: LANCE prior, YB method (Yu and Bien, 2017), ESC prior (Lee et al., 2019) and CSCS method (Khare et al., 2019).

For LANCE prior, and are used to construct , where is the posterior mode.

For ESC prior, instead of varying bandwidths, the posterior sample-based mode of the support of the Cholesky factor is used.

The absolute prediction error is calculated by for each , and the average of prediction errors, , is used to evaluate the performance of each method.

The hyperparameter in each method is chosen based on cross-validation, except ESC prior.

Because applying cross-validation to ESC prior is prohibitive due to heavy computation, we set the hyperparameters in ESC prior at , , and as suggested by Lee et al.(2019).

Figure 6 represents prediction errors at each time point.

Averages of prediction errors for the methods proposed in this paper, Yu and Bien(2017), Lee et al.(2019) and Khare et al.(2019) are , , and , respectively.

It suggests that a local dependence structure is more suitable for the call center data than an arbitrary dependence structure, which makes sense due to the nature of the data.

Figure 6:

Prediction errors at each time point for each method.

LL, YB, ESC and KO represent the methods proposed in this paper, Yu and Bien (2017), Lee et al. (2019) and Khare et al. (2019), respectively.

We further illustrate the performance of LANCE prior in a classification problem.

The GunPointAgeSpan data set, which is publicly available at http://timeseriesclassification.com, is used to conduct the quadratic discriminant analysis (QDA).

This consists of the two GunPoint data sets released in 2003 and 2018, respectively, and each year, the same two actors (one male and one female) participated in the experiment.

There are two classes in a data set: Gun and Point.

For the Gun class, the actors hold a gun and point the gun toward a target, while they point with just their fingers (without a gun) in the Point class.

The x-axis coordinates of centroid of the hand are recorded over five seconds of the movement based on 30 frames per second, which results in 150 frames per action. Thus, this data set also has a time ordering between the variables.

The GunPointAgeSpan has 135 training set and 316 test set, and the purpose of the analysis is to classify test observations into the two classes (Gun and Point).

The numbers of observations corresponding to the Gun class are 68 and 160 in the training and test data, respectively.

The training and test data sets are centered.

For each data in the test set, the quadratic discriminant score is calculated as follows:

where and are the mean vector and precision matrix for the class , respectively.

Here, is the number of observations for the class , thus we have and .

To conduct the QDA, we estimate the unknown parameters and using the training data set.

They are plugged into similarly to the phone call center data example, and is then classified as the class .

The performances of LANCE prior, YB method, ESC prior and CSCS method are compared, where cross-validation is used for each method except ESC prior.

Table 1: Classification errors for the test set in the GunPointAgeSpan data.

LL

YB

ESC

KO

Error

0.2310

0.3956

0.2437

0.3704

Table 1 represents classification errors for the test set based the QDA using estimated by each method.

For this data set, Bayesian methods seem to achieve lower classification errors than the penalized likelihood approaches, while LANCE prior achieves the lowest classification error.

Despite similar performance, LANCE prior has a clear advantage over ESC prior by enabling a scalable cross-validation to select the hyperparameter.

In practice, there is no guideline for choosing the hyperparameters in ESC prior, which can dramatically affect the performance.

5 Discussion

In this paper, we propose a Bayesian procedure for high-dimensional local dependence learning, where variables close to each other are more likely to be correlated.

The proposed prior, LANCE prior, allows an exact computation of posteriors, which enables scalable inference even in high-dimensional settings.

Furthermore, it provides a scalable Bayesian cross-validation to choose the hyperparameters.

We establish selection consistency for the local dependence structure and posterior convergence rates for the Cholesky factor.

The required conditions for these theoretical results are significantly weakened compared with the existing literature.

Simulation studies in various settings show that LANCE prior outperforms other contenders in terms of the ROC curve, cross-validation-based analysis and computation time.

Two real data analyses based on the phone call center and gun point data illustrate the satisfactory performance of the proposed method in linear prediction and classification problems, respectively.

It is worth mentioning that LANCE prior is only applicable when is smaller than due to term in the conditional prior for .

Although we rule out this situation by introducing condition (A3), in practice, we can modify LANCE prior to allow when needed.

Specifically, we can modify the conditional prior for to

(6)

for some constant , where .

Note that the above prior (6) has a variance stabilizing term .

Then, the resulting -fractional posterior has the following closed form:

where

Thus, the proposed LANCE prior can be modified to allow large bandwidths such that .

A sufficiently small would give similar results with (5) in practice, although theoretical properties of the resulting -fractional posterior should be further investigated.

An important and interesting future direction is to consider the estimation of covariance or precision structures with an unknown topological ordering on the variables of a DAG.

Assume one specifies an arbitrary label of the variables as which does not necessarily correspond to the ordered variables.

Let be an element in the permutation group of variables and is the corresponding true DAG structure.

If one is interested in learning both the DAG and the resulting covariance structure, a natural attempt is to impose a prior on the DAG along with a prior on the covariance structure given or the DAG, and then perform posterior inference.

However, some identifiability conditions need to be imposed for the identifiability of the DAG structure.

Please see Theorem 2.2 of Park and Kim(2020) for a state-of-the-art result on the identifiability of a Gaussian DAG, which essentially says that a Gaussian DAG is identifiable if the uncertainty level of a node is smaller than that of its descendants, given the non-descendants.

One can potentially design a prior for the variances (s in our notation) that satisfies this ordered constraint.

It would be interesting to study the posterior contraction and model selection properties of this model and design efficient MCMC algorithms.

If one does not impose any identifiability conditions (e.g., through the prior), another direction to deal with the unknown ordering case is to learn the equivalent class (or a representative of the class) of a DAG for all s, the so-called structure learning of DAGs which will learn the covariance structure of an equivalent class without learning the topological ordering of the variable or the underlying DAG structure.

A recent work Zhou and Chang(2021) is one such example. The key ideas are the following: Let be the distribution of some true Gaussian DAG model .

One can show that (see definition 7 in Zhou and Chang(2021) for example), for any , one can have the Cholesky factor matrix and the positive diagonal matrix such that .

That is, for any , one can find a unique pair (, which corresponds to some DAG called minimal I-map of the equivalent classes which has the same covariance structure as .

This minimal I-map can be viewed as a representative point of the equivalent class which can be uniquely constructed.

The structure learning problems boil down to the learnings of essentially.

One can design appropriate priors that can obtain posterior consistency over .

Another work that deals with unknown ordering is Cao and Zhang(2020) which proposed to sample permutation matrices or s under the MCD model.

They obtained the posterior estimates of the Cholesky factors and diagonal matrices for each permutation which are then averaged to obtain a final estimate of the precision matrix.

Acknowledgement

We are very grateful to the Associate Editor and the two reviewers for their valuable comments which have led to great improvement in our paper. We would also like to thank Guo (Hugo) Yu for very helpful discussions.

for all sufficiently large , where the first inequality follows from Corollary 5.35 in Eldar and Kutyniok(2012).

Since , we have

for all sufficiently large , by the concentration inequality for chi-square random variables in Lemma 1 of Laurent and Massart(2000).

Furthermore, because , where denotes the noncentral chi-square distribution with the degrees of freedom and the noncentrality parameter , we have

by Lemma 4 of Shin et al.(2018) and conditions (A1), (A3) and (A4).

The last inequality holds because

where is the unit vector whose the th element is 1 and the others are zero.

Thus, we have proved (7).

Now, we complete the proof by showing (8).

For a given , because for any , it can be shown that

where

Then, we have

on the event .

Further note that

where and under given .

Then,

where the third inequality follows from the moment generating function of normal distribution.

Note that

for and .

Let be the set defined at the proof of Theorem 3.2.

Note that by similar arguments used in (11), the proof of Lemma 6.5 in Lee et al.(2019) and page 29 of Boucheron et al.(2013),

for some constant and any integer on the event .

Therefore, we have

Now, we can show that (14) is of order if we show that

(16)

Let

where

and be a -dimensional vector such that and otherwise.

For any integer ,

for some positive constants and depending only on , by the proofs of Lemmas 6.5 and 7.1 in Lee et al.(2019).

Since under , we have

(17)

because and .

By the proof of Lemma 7.2 in Lee et al.(2019),

for some positive constant and large constant depending only on .

Note that the fourth inequality holds because .

Thus, it implies that (14) is of order .

We can complete the proof if we show that (14) is of order .

Note that

where

Recall that .

Let and .

Then, by the same arguments used in (15), we have

for some constants ,

by the proof of Lemma 7.3 of Lee et al.(2019).

Thus,

Thus, it implies that

for some large constant depending only on .

The posterior convergence rate under the element-wise maximum norm.

Note that

Because we showed that (14) and (A) are of order , it implies that (A) is of order .

The posterior convergence rate under the Frobenius norm.

Because , we have

The last term is of order by the similar arguments used in (A).

Appendix B Numerical Studies: Estimation of Cholesky Factors

In this section, we illustrate the performance of LANCE prior in terms of the estimation of Cholesky factors.

We consider Models 1–3 described in Section 4.2 of the main manuscript and compare the performance of LANCE prior with that of YB method (Yu and Bien, 2017).

The sample size and number of variables are varied as follows: and

.

To demonstrate the estimation performance of each method, cross-validation is used as described in Section 4.2.

For LANCE prior, the posterior means of Cholesky factors given the posterior mode of bandwidths are used for estimation purpose.

Tables 2 and 3 show the results under various loss functions when the signal sizes are between (small signal setting) and (large signal setting), respectively.

Note that LL in the tables represents LANCE prior.

In the small signal setting, YB method tends to outperform LANCE prior when , while LANCE prior tends to outperform YB method when .

Although the performances of both of the methods are improved as increases, LANCE prior offers a more significant performance improvement.

On the other hand, in the large signal setting, LANCE prior works better than YB method regardless of the sample size .

Compared with the small signal setting, LANCE prior shows slightly larger errors in the large signal setting.

However, relatively, YB method produces much larger errors in the large signal setting.

This is consistent with previous observations that under large signals, the performance of YB method is not satisfactory in terms of sensitivity and specificity.

Table 2:

The mean and standard deviation (in parentheses) of the Frobenius norm, spectral norm and matrix -norm when based on 10 simulated data sets.

Model 1

LL

YB

Model 2

LL

YB

Model 3

LL

YB

Table 3:

The mean and standard deviation (in parentheses) of the Frobenius norm, spectral norm and matrix -norm when based on 10 simulated data sets.

Model 1

LL

YB

Model 2

LL

YB

Model 3

LL

YB

References

(1)

An et al. (2014)

An, B., Guo, J. and Liu, Y. (2014).

Hypothesis testing for band size detection of high-dimensional banded

precision matrices, Biometrika101(2): 477–483.

Arias-Castro and Lounici (2014)

Arias-Castro, E. and Lounici, K. (2014).

Estimation and variable selection with exponential weights, Electronic Journal of Statistics8(1): 328–354.

Banerjee and Ghosal (2014)

Banerjee, S. and Ghosal, S. (2014).

Posterior convergence rates for estimating large precision matrices

using graphical models, Electronic Journal of Statistics8(2): 2111–2137.

Banerjee and Ghosal (2015)

Banerjee, S. and Ghosal, S. (2015).

Bayesian structure learning in graphical models, Journal of

Multivariate Analysis136: 147–162.

Bhattacharya et al. (2019)

Bhattacharya, A., Pati, D., Yang, Y. et al. (2019).

Bayesian fractional posteriors, The Annals of Statistics47(1): 39–66.

Bickel and Levina (2008)

Bickel, P. J. and Levina, E. (2008).

Regularized estimation of large covariance matrices, The Annals

of Statistics36(1): 199–227.

Boucheron et al. (2013)

Boucheron, S., Lugosi, G. and Massart, P. (2013).

Concentration Inequalities: A Nonasymptotic Theory of

Independence, OUP Oxford.

https://books.google.co.kr/books?id=koNqWRluhP0C

Bühlmann and van de

Geer (2011)

Bühlmann, P. and van de Geer, S. (2011).

Statistics for High-Dimensional Data: Methods, Theory and

Applications, Springer Series in Statistics, Springer Berlin Heidelberg.

Cai et al. (2016)

Cai, T. T., Liu, W. and Zhou, H. H. (2016).

Estimating sparse precision matrix: Optimal rates of convergence and

adaptive estimation, The Annals of Statistics44(2): 455–488.

Cao et al. (2019)

Cao, X., Khare, K. and Ghosh, M. (2019).

Posterior graph selection and estimation consistency for

high-dimensional bayesian dag models, The Annals of Statistics47(1): 319–348.

Cao and Zhang (2020)

Cao, X. and Zhang, S. (2020).

A permutation-based bayesian approach for inverse covariance

estimation, Communications in Statistics - Theory and Methods49(14): 3557–3571.

https://doi.org/10.1080/03610926.2019.1590601

Eldar and Kutyniok (2012)

Eldar, Y. C. and Kutyniok, G. (2012).

Compressed sensing: theory and applications, Cambridge

University Press.

Gelman et al. (2014)

Gelman, A., Hwang, J. and Vehtari, A. (2014).

Understanding predictive information criteria for bayesian models,

Statistics and computing24(6): 997–1016.

Huang et al. (2006)

Huang, J. Z., Liu, N., Pourahmadi, M. and Liu, L. (2006).

Covariance matrix selection and estimation via penalised normal

likelihood, Biometrika93(1): 85–98.

Jeffreys (1946)

Jeffreys, H. (1946).

An invariant form for the prior probability in estimation problems,

Proceedings of the Royal Society of London. Series A. Mathematical and

Physical Sciences186(1007): 453–461.

Johnstone and Lu (2009)

Johnstone, I. M. and Lu, A. Y. (2009).

On consistency and sparsity for principal components analysis in high

dimensions, J. Amer. Statist. Assoc.104(486): 682–693.

Khare et al. (2019)

Khare, K., Oh, S.-Y., Rahman, S. and Rajaratnam, B. (2019).

A scalable sparse cholesky based approach for learning

high-dimensional covariance matrices in ordered data, Machine Learning108(12): 2061–2086.

Laurent and Massart (2000)

Laurent, B. and Massart, P. (2000).

Adaptive estimation of a quadratic functional by model selection,

The Annals of Statistics28(5): 1302–1338.

Lee and Lee (2018)

Lee, K. and Lee, J. (2018).

Optimal bayesian minimax rates for unconstrained large covariance

matrices, Bayesian Analysis13(4): 1215–1233.

Lee and Lee (2021)

Lee, K. and Lee, J. (2021).

Estimating large precision matrices via modified cholesky

decomposition, Statistica Sinica31(1): 173–196.

Lee et al. (2019)

Lee, K., Lee, J. and Lin, L. (2019).

Minimax posterior convergence rates and model selection consistency

in high-dimensional dag models based on sparse cholesky factors, The

Annals of Statistics47(6): 3413–3437.

Lee and Lin (2020)

Lee, K. and Lin, L. (2020).

Bayesian bandwidth test and selection for high-dimensional banded

precision matrices, Bayesian Anal.15(3): 737–758.

Liu and Ren (2020)

Liu, Y. and Ren, Z. (2020).

Minimax estimation of large precision matrices with bandable cholesky

factor, The Annals of Statistics48(4): 2428–2454.

Martin et al. (2017)

Martin, R., Mess, R. and Walker, S. G. (2017).

Empirical bayes posterior concentration in sparse high-dimensional

linear models, Bernoulli23(3): 1822–1847.

Martin and Walker (2014)

Martin, R. and Walker, S. G. (2014).

Asymptotically minimax empirical bayes estimation of a sparse normal

mean vector, Electronic Journal of Statistics8(2): 2188–2206.

Park and Kim (2020)

Park, G. and Kim, Y. (2020).

Identifiability of gaussian structural equation models with

homogeneous and heterogeneous error variances, Journal of the Korean

Statistical Society volume49: 276–292.

Pourahmadi (1999)

Pourahmadi, M. (1999).

Joint mean-covariance models with applications to longitudinal data:

Unconstrained parameterisation, Biometrika86(3): 677–690.

Rothman et al. (2010)

Rothman, A. J., Levina, E. and Zhu, J. (2010).

A new approach to cholesky-based covariance regularization in high

dimensions, Biometrika97(3): 539–550.

Rütimann and Bühlmann (2009)

Rütimann, P. and Bühlmann, P. (2009).

High dimensional sparse covariance estimation via directed acyclic

graphs, Electronic Journal of Statistics3: 1133–1160.

Shin et al. (2018)

Shin, M., Bhattacharya, A. and Johnson, V. E. (2018).

Scalable bayesian variable selection using nonlocal prior densities

in ultrahigh-dimensional settings, Statistica Sinica28(2): 1053.

Shojaie and Michailidis (2010)

Shojaie, A. and Michailidis, G. (2010).

Penalized likelihood methods for estimation of sparse

high-dimensional directed acyclic graphs, Biometrika97(3): 519–538.

van de Geer and Bühlmann (2013)

van de Geer, S. and Bühlmann, P. (2013).

-penalized maximum likelihood for sparse directed acyclic

graphs, The Annals of Statistics41(2): 536–567.

Wainwright (2009)

Wainwright, M. J. (2009).

Sharp thresholds for high-dimensional and noisy sparsity recovery

using -constrained quadratic programming (lasso), IEEE

transactions on information theory55(5): 2183–2202.

Yu and Bien (2017)

Yu, G. and Bien, J. (2017).

Learning local dependence in ordered data, Journal of Machine

Learning Research18(42): 1–60.

Zellner (1986)

Zellner, A. (1986).

On assessing prior distributions and bayesian regression analysis

with g-prior distributions, Bayesian inference and decision techniques:

Essays in Honor of Bruno De Finetti6: 233–243.

Zhou and Chang (2021)

Zhou, Q. and Chang, H. (2021).

Complexity analysis of bayesian learning of high-dimensional dag

models and their equivalence classes.