Logistic or not logistic?

Abstract

We propose a new class of goodness-of-fit tests for the logistic distribution based on a characterisation related to the density approach in the context of Stein’s method. This characterisation based test is a first of its kind for the logistic distribution. The asymptotic null distribution of the test statistic is derived and it is shown that the test is consistent against fixed alternatives. The finite sample power performance of the newly proposed class of tests is compared to various existing tests by means of a Monte Carlo study. It is found that this new class of tests are especially powerful when the alternative distributions are heavy tailed, like Student’s t and Cauchy, or for skew alternatives such as the log-normal, gamma and chi-square distributions.

1 Introduction

The logistic distribution apparently found its origin in the mid-nineteenth century in the writings of Verhulst, (1838, 1845). Since then it has been used in many different areas such as logistic regression, logit models and neural networks. The logistic law has become a popular choice of model in reliability theory and survival analysis (see e.g., Kannisto,, 1999) and lately in finance (Ahmad,, 2018). The United States Chess Federation and FIDE have recently changed its formula for calculating chess ratings of players by using the more heavy tailed logistic distribution instead of the lighter tailed normal distribution (Aldous,, 2017; Elo,, 1978). For a detail account on the history and application of the logistic distribution, the interested reader is referred to Johnson et al., (1995).

In the literature some goodness-of-fit tests for assessing whether the observed data are realisations from the logistic distribution have been developed and studied. These include tests based on the empirical distribution function (Stephens,, 1979), normalised spacings (Lockhart et al.,, 1986), chi-squared type statistics (Aguirre & Nikulin,, 1994), orthogonal expansions (Cuadras & Lahlou,, 2000), empirical characteristic and moment generating functions (Meintanis,, 2004; Epps,, 2005) and the Gini index (Alizadeh Noughabi,, 2017).

Balakrishnan, (1991) provides an excellent discussion on the logistic distribution including some of the goodness-of-fit tests mentioned above. Nikitin & Ragozin, (2019) recently proposed a test based on a characterisation of the logistic distribution involving independent shifts. In this paper the authors remarked that “no goodness-of-fit tests of the composite hypothesis to the logistic family based on characterizations are yet known”. Although, as mentioned, some tests exists for the logistic distribution, they are few in number compared to those for other distributions such as the normal, exponential and the Rayleigh distribution. In this paper we propose a new class of tests for the logistic distribution based on a new characterisation filling the gap reported by Nikitin & Ragozin, (2019). To be precise, we write shorthand L, , , for the logistic distribution with location parameter and scale parameter if the density is defined by

| (1) |

where is the hyperbolic secant. Note that L if, and only if, L and hence the logistic distribution belongs to the location-scale family of distributions, for a detailed discussion see Johnson et al., (1995), chapter 23. In the following we denote the family of logistic distributions by , a family of distributions which is closed under translation and rescaling. Let be real-valued independent and identically distributed (iid.) random variables with distribution defined on an underlying probability space . We test the composite hypothesis

| (2) |

against general alternatives based on the sample .

The novel procedure is based on the following new characterisation of the standard Logistic distribution, which is related to the density method in the broad theory of Stein’s method for distributional approximation, see for example Chen et al., (2011); Ley & Swan, (2013), and the Stein-Tikhomirov approach, see Arras et al., (2017).

Theorem 1.1.

Let be a random variable with absolutely continuous density and . Then follows a standard logistic distribution if, and only if

| (3) |

holds for all , where and is the imaginary unit.

Proof.

For direct calculation shows the assertion. Let be a random variable with absolutely continuous density function such that

holds for all . Note that since is the Fourier-Stieltjes transform of the derivative of we have

for all . By standard properties of the Fourier-Stieltjes transform, we hence note that must satisfy the ordinary differential equation

for all . By separation of variables it is straightforward to see, that the only solution satisfying is , , and follows. ∎

To model the standardisation assumption, we consider the so called scaled residuals , given by

Here, and denote consistent estimators of and such that

| (4) | |||||

| (5) |

holds for each and . By (4) and (5) it is easy to see that , do not depend on the location nor the scale parameter, so we assume and in the following. The test statistic

is the weighted -distance from (3) to the 0-function. Here, denotes a symmetric, positive weight function satisfying , that guaranties that the considered integrals are finite. Since under the hypothesis (2) should be close to 0, we reject for large values of .

Note that is in the structural spirit of Section 5.4.2 in Anastasiou et al., (2021). It only depends on the scaled residuals , , and as a consequence it is invariant due to affine transformations of the data, i.e. w.r.t. transformations of the form , . This is indeed a desirable property, since the family is closed under affine transformations.

Direct calculations show with , , , that the integration-free and numerically stable version is

with , , and for . Here, is a so-called tuning parameter, which allows some flexibility in the choice of the right test statistic . A good choice of is suggested in Section 3.

The rest of the paper is organised as follows. In Section 2 the asymptotic behaviour of the new test is investigated under the null and alternative distribution, respectively. The results of a Monte Carlo study is presented in Section 3, while all the tests are applied to a real-world data set in Section 4. The paper concludes in Section 5 with some concluding remarks and an outlook for future research.

2 Limit distribution under the null hypothesis and consistency

In what follows let be iid. random variables, and in view of affine invariance of we assume w.l.o.g. . A suitable setup for deriving asymptotic theory is the Hilbert space of measurable, square integrable functions , where is the Borel--field of . Notice that the functions figuring within the integral in the definition of are -measurable random elements of . We denote by

the usual norm and inner product in . In the following, we assume that the estimators and allow linear representations

| (6) | ||||

| (7) |

where denotes a term that converges to 0 in probability, and und are measurable functions with

The interested reader finds formulas for the functions and in Appendix A for maximum-likelihood and moment estimators. By the symmetry of the weight function straightforward calculations show

where

and

Clearly, is a sum of dependent random variables. In order to find an asymptotic equivalent stochastic process we use a first order multivariate Taylor expansion and consider with

the helping process

In view of (6) and (7) we define the second helping process

which is a sum of centered iid. random variables. Note that using

| and |

we have by straightforward calculations and . In the following, we denote by weak convergence (or alternatively convergence in distribution), whenever random elements (or random variables) are considered, and in the same manner by convergence in probability.

Theorem 2.1.

Under the standing assumptions, we have

in , where is a centred Gaussian process having covariance kernel

Furthermore, we have , as .

Proof.

In a first step, we note that after some algebra using a multivariate Taylor expansion around we have

Furthermore using the linear representations in (6) and (7) and the law of large numbers in Hilbert spaces, it follows that

and by the triangular equation, we see that has the same limiting distribution as . Since by the central limit theorem in Hilbert spaces in , where is the stated Gaussian limit process with covariance kernel which gives the stated formula after a short calculation. The next statement is a direct consequence of the continuous mapping theorem. ∎

In the rest of this section we assume that the underlying distribution is a fixed alternative to and that the distribution is absolutely continuous, as well as in view of affine invariance of the test statistic, we assume and . Furthermore, we assume that

Theorem 2.2.

Under the standing assumptions, we have as ,

The proof of Theorem 2.2 follows the lines of the proof of Theorem 3.1 in Ebner et al., (2021) and since it does not provide further insights it is omitted. Notice that by the characterisation of the logistic law in Theorem 1.1, we have if and only if . This implies that , as , for any alternative with existing second moment. Thus we conclude that the test based on is consistent against each such alternative.

3 Simulation results

In this section the finite sample performance of the newly proposed test is compared to various existing tests for the logistic distribution by means of a Monte Carlo study. We consider the traditional tests (based on the empirical distribution function) of Kolmogorov-Smirnov (), Cramér-von Mises (), Anderson-Darling () and Watson (), a test proposed by Alizadeh Noughabi, (2017) based on an estimate of the Gini index (), as well as a test by Meintanis, (2004), based on the empirical characteristic function, with calculable form

where

We also include a new test () constructed similarly to that of , but setting , in Theorem 1.1. This new “moment generating” function based test is then given by the -statistic

Direct calculations lead with to the numerical stable version

A significance level of was used throughout the study and empirical critical values were obtained from independent Monte Carlo replications, with unknown parameters estimated by method of moments (maximum likelihood estimation yielded similar results, therefore we only display results based on method of moments). The critical values for are given in Table 1 for different values of , and . The power estimates were calculated for sample sizes and using independent Monte Carlo simulations. The alternative distributions considered were the Normal (Student’s t (), Cauchy (C), Laplace (log-normal (gamma (), uniform (U), beta (B) and chi-square () distributions. Tables 2 and 3 contain these power estimates. Apart from the mentioned alternative distributions, we also considered some local alternatives. Table 4 contains the local power estimates for (top row) and (bottom row), where we simulated data from a mixture of the logistic and Cauchy distribution, i.e. we sample from a logistic distribution with probability and from a Cauchy distribution with probability . Similarly, Table 5 contains the local power estimates where we simulated data from a mixture of the logistic and log-normal distribution. The tables contain the percentage of times that the null hypothesis in (1) is rejected, rounded to the nearest integer. All calculations were performed in R (R Core Team,, 2020).

| 1.011 | 0.701 | 0.525 | 1.091 | 0.759 | 0.580 | |

| 0.684 | 0.459 | 0.339 | 0.714 | 0.487 | 0.363 | |

| 0.531 | 0.350 | 0.254 | 0.555 | 0.374 | 0.276 | |

| Alternative | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | |

| 3 | 3 | 2 | 1 | 6 | 7 | 9 | 4 | 4 | 4 | 4 | 5 | |

| 37 | 37 | 37 | 38 | 31 | 27 | 23 | 33 | 37 | 37 | 36 | 33 | |

| 9 | 9 | 9 | 10 | 9 | 8 | 7 | 7 | 8 | 8 | 8 | 8 | |

| 4 | 4 | 4 | 4 | 5 | 6 | 6 | 5 | 4 | 5 | 5 | 5 | |

| 76 | 75 | 74 | 69 | 62 | 58 | 53 | 76 | 79 | 79 | 79 | 75 | |

| 13 | 13 | 13 | 13 | 8 | 6 | 5 | 12 | 13 | 13 | 13 | 10 | |

| 87 | 87 | 87 | 76 | 48 | 39 | 33 | 75 | 85 | 87 | 80 | 28 | |

| 98 | 98 | 98 | 94 | 70 | 61 | 53 | 94 | 97 | 98 | 97 | 52 | |

| 99 | 99 | 99 | 98 | 81 | 73 | 64 | 98 | 100 | 100 | 99 | 72 | |

| 70 | 70 | 69 | 52 | 26 | 20 | 16 | 53 | 67 | 71 | 61 | 17 | |

| 41 | 41 | 40 | 28 | 17 | 14 | 12 | 28 | 36 | 38 | 31 | 15 | |

| 26 | 26 | 26 | 17 | 12 | 11 | 11 | 19 | 23 | 24 | 20 | 13 | |

| 16 | 8 | 5 | 0 | 48 | 55 | 58 | 13 | 21 | 28 | 27 | 30 | |

| 5 | 3 | 2 | 0 | 19 | 24 | 28 | 6 | 9 | 11 | 12 | 14 | |

| 13 | 11 | 10 | 4 | 11 | 13 | 14 | 11 | 13 | 14 | 13 | 13 | |

| 71 | 71 | 70 | 52 | 27 | 21 | 17 | 53 | 67 | 71 | 61 | 16 | |

| 32 | 32 | 31 | 21 | 15 | 13 | 12 | 23 | 27 | 29 | 24 | 14 | |

| 15 | 15 | 15 | 10 | 10 | 10 | 10 | 12 | 14 | 15 | 12 | 11 | |

| 12 | 11 | 11 | 7 | 8 | 9 | 10 | 9 | 10 | 11 | 10 | 9 |

| Alternative | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | |

| 5 | 3 | 3 | 0 | 4 | 7 | 10 | 5 | 6 | 6 | 7 | 9 | |

| 65 | 64 | 64 | 59 | 57 | 54 | 51 | 60 | 66 | 67 | 67 | 65 | |

| 11 | 12 | 12 | 15 | 14 | 13 | 12 | 9 | 11 | 11 | 10 | 11 | |

| 5 | 4 | 4 | 4 | 5 | 6 | 6 | 5 | 5 | 5 | 6 | 5 | |

| 98 | 98 | 97 | 91 | 91 | 90 | 88 | 98 | 99 | 99 | 99 | 98 | |

| 19 | 18 | 18 | 15 | 13 | 11 | 9 | 20 | 23 | 22 | 24 | 19 | |

| 100 | 100 | 100 | 96 | 83 | 76 | 70 | 99 | 100 | 100 | 100 | 48 | |

| 100 | 100 | 100 | 100 | 96 | 93 | 90 | 100 | 100 | 100 | 100 | 87 | |

| 100 | 100 | 100 | 100 | 99 | 98 | 96 | 100 | 100 | 100 | 100 | 98 | |

| 99 | 99 | 99 | 73 | 48 | 39 | 31 | 94 | 99 | 99 | 97 | 21 | |

| 87 | 87 | 87 | 39 | 27 | 22 | 19 | 67 | 81 | 86 | 73 | 28 | |

| 68 | 69 | 69 | 24 | 18 | 17 | 14 | 48 | 59 | 65 | 50 | 30 | |

| 78 | 66 | 51 | 0 | 93 | 97 | 98 | 44 | 68 | 84 | 77 | 74 | |

| 29 | 19 | 11 | 0 | 47 | 64 | 71 | 16 | 26 | 35 | 34 | 42 | |

| 46 | 43 | 40 | 1 | 12 | 18 | 21 | 30 | 39 | 45 | 37 | 40 | |

| 99 | 99 | 99 | 75 | 49 | 40 | 33 | 95 | 99 | 99 | 97 | 20 | |

| 78 | 79 | 79 | 30 | 22 | 19 | 16 | 57 | 70 | 75 | 61 | 30 | |

| 46 | 46 | 46 | 13 | 12 | 13 | 13 | 31 | 38 | 41 | 32 | 29 | |

| 31 | 31 | 30 | 8 | 8 | 10 | 11 | 22 | 26 | 28 | 22 | 24 |

| 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | |

| 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | |

| 12 | 12 | 12 | 12 | 12 | 11 | 11 | 11 | 12 | 12 | 11 | 11 | |

| 20 | 20 | 20 | 22 | 22 | 22 | 21 | 18 | 19 | 19 | 18 | 18 | |

| 17 | 18 | 18 | 19 | 17 | 16 | 15 | 16 | 17 | 17 | 16 | 16 | |

| 30 | 31 | 31 | 35 | 34 | 33 | 32 | 28 | 30 | 31 | 30 | 31 | |

| 24 | 24 | 24 | 25 | 23 | 21 | 20 | 21 | 23 | 23 | 22 | 22 | |

| 41 | 42 | 43 | 46 | 45 | 44 | 43 | 38 | 40 | 41 | 40 | 43 | |

| 28 | 29 | 29 | 31 | 28 | 26 | 24 | 25 | 27 | 27 | 26 | 27 | |

| 51 | 52 | 52 | 55 | 54 | 53 | 51 | 48 | 51 | 51 | 50 | 51 | |

| 38 | 38 | 38 | 39 | 36 | 33 | 31 | 34 | 36 | 37 | 35 | 37 | |

| 66 | 66 | 66 | 68 | 67 | 65 | 64 | 62 | 65 | 66 | 65 | 65 | |

| 46 | 47 | 47 | 47 | 42 | 39 | 36 | 42 | 45 | 45 | 44 | 43 | |

| 77 | 77 | 77 | 76 | 76 | 74 | 72 | 73 | 76 | 77 | 76 | 76 | |

| 55 | 55 | 55 | 54 | 49 | 46 | 42 | 51 | 54 | 54 | 53 | 51 | |

| 84 | 84 | 84 | 82 | 82 | 80 | 78 | 82 | 84 | 85 | 85 | 83 | |

| 60 | 60 | 60 | 58 | 52 | 48 | 45 | 57 | 60 | 60 | 59 | 57 | |

| 89 | 89 | 89 | 86 | 85 | 84 | 82 | 87 | 90 | 90 | 90 | 89 | |

| 65 | 65 | 65 | 63 | 56 | 52 | 48 | 63 | 66 | 66 | 65 | 62 | |

| 93 | 92 | 92 | 88 | 87 | 86 | 84 | 91 | 93 | 93 | 94 | 92 | |

| 70 | 69 | 69 | 65 | 58 | 54 | 50 | 68 | 71 | 71 | 71 | 67 | |

| 96 | 95 | 95 | 90 | 89 | 88 | 86 | 95 | 96 | 96 | 96 | 95 | |

| 73 | 73 | 72 | 68 | 61 | 57 | 52 | 72 | 76 | 75 | 75 | 71 | |

| 97 | 97 | 96 | 91 | 91 | 90 | 88 | 96 | 98 | 98 | 98 | 97 | |

| 77 | 76 | 75 | 70 | 63 | 59 | 54 | 77 | 80 | 80 | 80 | 75 | |

| 98 | 98 | 98 | 92 | 91 | 90 | 88 | 98 | 99 | 99 | 99 | 98 |

| 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | |

| 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | |

| 7 | 7 | 7 | 7 | 7 | 6 | 6 | 6 | 7 | 7 | 7 | 5 | |

| 8 | 8 | 8 | 9 | 9 | 8 | 8 | 7 | 7 | 8 | 7 | 6 | |

| 8 | 8 | 8 | 9 | 8 | 7 | 6 | 7 | 8 | 8 | 7 | 6 | |

| 10 | 11 | 11 | 13 | 12 | 11 | 11 | 10 | 11 | 11 | 11 | 8 | |

| 10 | 10 | 10 | 11 | 9 | 8 | 7 | 8 | 9 | 9 | 9 | 7 | |

| 13 | 14 | 14 | 16 | 15 | 14 | 13 | 13 | 14 | 14 | 13 | 10 | |

| 11 | 12 | 12 | 12 | 10 | 9 | 8 | 11 | 11 | 11 | 11 | 8 | |

| 17 | 17 | 17 | 20 | 19 | 18 | 16 | 17 | 18 | 18 | 18 | 13 | |

| 15 | 15 | 15 | 16 | 13 | 11 | 9 | 15 | 15 | 15 | 15 | 10 | |

| 23 | 24 | 24 | 25 | 24 | 23 | 21 | 26 | 27 | 27 | 28 | 19 | |

| 19 | 19 | 19 | 20 | 14 | 12 | 10 | 19 | 20 | 19 | 19 | 13 | |

| 33 | 33 | 33 | 32 | 31 | 28 | 26 | 38 | 41 | 39 | 42 | 27 | |

| 25 | 25 | 25 | 25 | 18 | 15 | 12 | 26 | 28 | 26 | 27 | 16 | |

| 43 | 42 | 42 | 39 | 36 | 33 | 31 | 52 | 54 | 52 | 56 | 36 | |

| 31 | 31 | 31 | 29 | 21 | 17 | 14 | 32 | 35 | 34 | 35 | 20 | |

| 57 | 55 | 53 | 45 | 42 | 39 | 36 | 65 | 70 | 67 | 72 | 45 | |

| 41 | 40 | 40 | 36 | 26 | 21 | 17 | 41 | 46 | 44 | 46 | 25 | |

| 71 | 69 | 67 | 53 | 49 | 45 | 42 | 78 | 83 | 81 | 84 | 51 | |

| 51 | 50 | 49 | 44 | 30 | 25 | 20 | 51 | 57 | 56 | 56 | 28 | |

| 85 | 83 | 82 | 63 | 58 | 54 | 50 | 88 | 92 | 92 | 93 | 54 | |

| 66 | 66 | 65 | 56 | 37 | 30 | 26 | 61 | 69 | 69 | 67 | 28 | |

| 95 | 94 | 94 | 76 | 68 | 63 | 58 | 96 | 98 | 98 | 98 | 53 | |

| 87 | 87 | 87 | 77 | 48 | 39 | 33 | 75 | 85 | 87 | 80 | 29 | |

| 100 | 100 | 100 | 96 | 83 | 76 | 70 | 99 | 100 | 100 | 100 | 48 |

The newly proposed tests are especially powerful when the alternative distributions are heavy tailed, like the Student’s t and Cauchy, or for skew alternatives such as the log-normal, gamma and chi-square distributions. The test of Meintanis produces the highest estimated powers when the alternatives have lighter tails or have bounded support such as the uniform and Beta distributions. When comparing the traditional tests, it is clear that the Anderson-Darling test has superior estimated powers.

For the mixture of the logistic and Cauchy distribution, the newly proposed tests ( and ) as well as the test of Meintanis have the highest estimated powers for small values of the mixing parameter (i.e. closer to the null distribution). The more traditional tests have slightly higher estimated powers for increasing values of the mixing parameter. This trend is similar when considering the mixture of the logistic and log-normal distributions.

Overall, the newly proposed test performs favourably relative to the existing tests and to a lessor extend the test , which is based on the moment generating function. For practical implementation of the test, we advise choosing the tuning parameter as as this choice produced high estimated powers for most alternatives considered. Alternatively, one can use the methods described in Allison & Santana, (2015) or Tenreiro, (2019) to choose this parameter data dependently.

4 Practical application

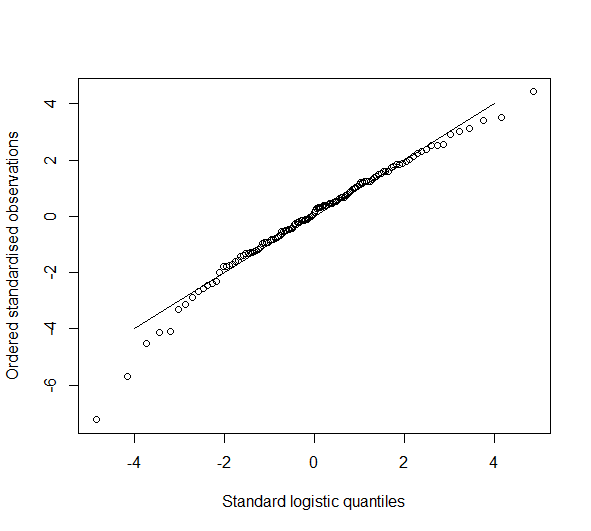

In this section all the tests considered in the Monte Carlo study are applied to the ’Bladder cancer’ data set. This data set contains the monthly remission times of 128 patients, denoted by , who were diagnosed with bladder cancer and can be found in Lee & Wang, (2003). The data was also studied and analysed by Noughabi, (2021) and Al-Shomrani et al., (2016). We are interested in testing whether the log of the remission times, , follow a logistic distribution. The method of moment estimates of and are and , respectively. Figure 1 represents the probability plot of vs , where denotes the quantile function of the standard logistic distribution and . This probability plot suggest that the underlying distribution of the data might be the logistic distribution. Table 6 contains the test statistic values as well as the corresponding estimated -values (calculated based on 10 000 samples of size 128 simulated from the standard logistic distribution) for the 8 tests for testing the goodness-of-fit for the logistic distribution. All the tests do not reject the null hypothesis that the log of the remission times is logistic distributed. These findings are in agreement with that of Al-Shomrani et al., (2016), where they concluded that the remission times follows a log-logistic distribution.

| Test | Test statistic value | value |

|---|---|---|

| 0.500 | 0.171 | |

| 19.75 | 0.329 | |

| 169.4 | 0.602 | |

| 0.061 | 0.404 | |

| 0.072 | 0.401 | |

| 0.440 | 0.421 | |

| 0.043 | 0.680 | |

| 0.325 | 0.147 |

5 Conclusion and open questions

We have shown a new characterisation of the logistic law and proposed a weighted affine invariant -type test. Monte Carlo results show that it is competitive to the state-of-the-art procedures. Asymptotic properties have been derived, including the limit null distribution and consistency against a large class of alternatives. We conclude the paper by pointing out open questions for further research.

Following the methodology in Baringhaus et al., (2017), we have under alternatives satisfying a weak moment condition , as where is a specified variance, for details, see Theorem 1 in Baringhaus et al., (2017). Since the calculations are too involved to get further insights, we leave the derivation of formulas open for further research. Note that such results can lead to confidence intervals for or approximations of the power function, for examples of such results see Dörr et al., (2021) and Ebner et al., (2020) in the multivariate normality setting.

Due to the increasing popularity of the log-logistic distribution in survival analysis, another avenue for future research is to adapt our test for scenarios where censoring is present. One possibility is to estimate the expected value in (3) by estimating the law of the survival times by the well-known Kaplan-Meier estimate. Some work on this has been done in the case of testing for exponentiality (see, e.g., Cuparić & Milošević,, 2020 and Bothma et al.,, 2021).

References

- Aguirre & Nikulin, (1994) Aguirre, N. & Nikulin, M. (1994). Chi-squared goodness-of-fit test for the family of logistic distributions. Kybernetika, 30(3), 214–222.

- Ahmad, (2018) Ahmad, M. (2018). Analysis of financial data by generalized logistic distribution. 3(5), 69–72.

- Al-Shomrani et al., (2016) Al-Shomrani, A. A., Shawky, A., Arif, O. H., & Aslam, M. (2016). Log-logistic distribution for survival data analysis using mcmc. SpringerPlus, 5(1), 1–16.

- Aldous, (2017) Aldous, D. (2017). Elo ratings and the sports model: A neglected topic in applied probability? Statistical Science, 32(4), 616–629.

- Alizadeh Noughabi, (2017) Alizadeh Noughabi, H. (2017). Gini index based goodness-of-fit test for the logistic distribution. Communications in Statistics-Theory and Methods, 46(14), 7114–7124.

- Allison & Santana, (2015) Allison, J. & Santana, L. (2015). On a data-dependent choice of the tuning parameter appearing in certain goodness-of-fit tests. Journal of Statistical Computation and Simulation, 85(16), 3276–3288.

- Anastasiou et al., (2021) Anastasiou, A., Barp, A., Briol, F.-X., Ebner, B., Gaunt, R. E., Ghaderinezhad, F., Gorham, J., Gretton, A., Ley, C., Liu, Q., Mackey, L., Oates, C. J., Reinert, G., & Swan, Y. (2021). Stein’s method meets statistics: A review of some recent developments. arXiv preprint, arXiv:2105.03481.

- Arras et al., (2017) Arras, B., Mijoule, G., Poly, G., & Swan, Y. (2017). A new approach to the stein-tikhomirov method: with applications to the second Wiener chaos and Dickman convergence. arXiv preprint, arXiv:1605.06819.

- Balakrishnan, (1991) Balakrishnan, N. (1991). Handbook of the logistic distribution. CRC Press.

- Baringhaus et al., (2017) Baringhaus, L., Ebner, B., & Henze, N. (2017). The limit distribution of weighted -goodness-of-fit statistics under fixed alternatives, with applications. Annals of the Institute of Statistical Mathematics, 69(5), 969–995.

- Betsch & Ebner, (2020) Betsch, S. & Ebner, B. (2020). Testing normality via a distributional fixed point property in the Stein characterization. TEST, 29(1), 105–138.

- Bickel & Doksum, (2015) Bickel, P. J. & Doksum, K. A. (2015). Mathematical statistics : basic ideas and selected topics, volume 1. Boca Raton, Fla.: CRC Press, 2. edition.

- Bothma et al., (2021) Bothma, E., Allison, J., Cockeran, M., & Visagie, J. (2021). Characteristic function and laplace transform-based test for exponentiality in the presence of random right censoring. STAT, 10(1), e394.

- Chen et al., (2011) Chen, L. H. Y., Goldstein, L., & Shao, Q.-M. (2011). Normal approximation by Steins method. Probability and its applications. Berlin: Springer.

- Cuadras & Lahlou, (2000) Cuadras, C. M. & Lahlou, Y. (2000). Some orthogonal expansions for the logistic distribution. Communications in Statistics-Theory and Methods, 29(12), 2643–2663.

- Cuparić & Milošević, (2020) Cuparić, M. & Milošević, B. (2020). New characterization based exponentiality test for random censored data. arXiv preprint, arXiv:2011.07998.

- Dörr et al., (2021) Dörr, P., Ebner, B., & Henze, N. (2021). Testing multivariate normality by zeros of the harmonic oscillator in characteristic function spaces. Scandinavian Journal of Statistics, 48(2), 456–501.

- Ebner et al., (2021) Ebner, B., Eid, L., & Klar, B. (2021). Cauchy or not Cauchy? new goodness-of-fit tests for the Cauchy distribution. arXiv preprint, arXiv:2106.13073.

- Ebner et al., (2020) Ebner, B., Henze, N., & Strieder, D. (2020). Testing normality in any dimension by fourier methods in a multivariate Stein equation. arXiv preprint, arXiv:2007.02596.

- Elo, (1978) Elo, A. (1978). The Rating of Chessplayers, Past and Present. Arco Pub.

- Epps, (2005) Epps, T. W. (2005). Tests for location-scale families based on the empirical characteristic function. Metrika, 62(1), 99–114.

- Johnson et al., (1995) Johnson, N. L., Kotz, S., & Balakrishnan, N. (1995). Continuous univariate distributions, volume 2. John Wiley & Sons.

- Kannisto, (1999) Kannisto, V. (1999). Trends in the mortality of the oldest-old. Statistics, Registers and Science, J. Alho, ed, (pp. 177–194).

- Lee & Wang, (2003) Lee, E. T. & Wang, J. (2003). Statistical methods for survival data analysis, volume 476. John Wiley & Sons.

- Ley & Swan, (2013) Ley, C. & Swan, Y. (2013). Stein’s density approach and information inequalities. Electronic Communications in Probability, 18, 1– 14.

- Lockhart et al., (1986) Lockhart, R. A., O’Reilly, F., & Stephens, M. A. (1986). Tests of fit based on normalized spacings. Journal of the Royal Statistical Society: Series B (Methodological), 48(3), 344–352.

- Meintanis, (2004) Meintanis, S. G. (2004). Goodness-of-fit tests for the logistic distribution based on empirical transforms. Sankhyā: The Indian Journal of Statistics, 66(2), 306–326.

- Millard, (2013) Millard, S. P. (2013). EnvStats: An R Package for Environmental Statistics. New York: Springer.

- Nikitin & Ragozin, (2019) Nikitin, Y. Y. & Ragozin, I. (2019). Goodness-of-fit tests based on a characterization of logistic distribution. Vestnik St. Petersburg University, Mathematics, 52(2), 169–177.

- Noughabi, (2021) Noughabi, H. A. (2021). A new goodness-of-fit test for the logistic distribution. to appear in Sankhyā B: The Indian Journal of Statistics, (pp. 1–17).

- R Core Team, (2020) R Core Team (2020). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Stephens, (1979) Stephens, M. A. (1979). Tests of fit for the logistic distribution based on the empirical distribution function. Biometrika, 66(3), 591–595.

- Tenreiro, (2019) Tenreiro, C. (2019). On the automatic selection of the tuning parameter appearing in certain families of goodness-of-fit tests. Journal of Statistical Computation and Simulation, 89(10), 1780–1797.

- Verhulst, (1838) Verhulst, P.-F. (1838). Notice sur la loi que la population suit dans son accroissement. Corresp. Math. Phys., 10, 113–126.

- Verhulst, (1845) Verhulst, P.-F. (1845). Recherches mathématiques sur la loi d’accroissement de la population. Nouveaux mémoires de l’Académie Royale des Sciences et Belles-Lettres de Bruxelles, 18, 14–54.

Appendix A Asymptotic representation of estimators

In this section we derive explicit formulae for the linear representations of the estimators in (6) and (7), for comparison we refer to Meintanis, (2004), p.313.

A.1 Maximum-likelihood estimators

The maximum-likelihood estimators and of the parameters and in (1) satisfy the equations, see displays (23.35) and (23.36) in Johnson et al., (1995),

An implementation is found in the R-package EnvStats, see Millard, (2013). Direct calculations show that the score vector of , , , is

where stands for the transpose of a vector . The Fisher information matrix is

which is easily inverted due to the diagonal form. By Bickel & Doksum, (2015), Section 6.2.1, we hence have for and the asymptotic expansions