Everything You Always Wanted to Know About XVA Model Risk but Were Afraid to Ask

Abstract

Valuation adjustments, collectively named XVA, play an important role in modern derivatives pricing. XVA are an exotic pricing component since they require the forward simulation of multiple risk factors in order to compute the portfolio exposure including collateral, leading to a significant model risk and computational effort, even in case of plain vanilla trades.

This work analyses the most critical model risk factors, meant as those to which XVA are most sensitive, finding an acceptable compromise between accuracy and performance. This task has been conducted in a complete context including a market standard multi-curve G2++ model calibrated on real market data, both Variation Margin and ISDA-SIMM dynamic Initial Margin, different collateralization schemes, and the most common linear and non-linear interest rates derivatives. Moreover, we considered an alternative analytical approach for XVA in case of uncollateralized Swaps.

We show that a crucial element is the construction of a parsimonious time grid capable of capturing all periodical spikes arising in collateralized exposure during the Margin Period of Risk. To this end, we propose a workaround to efficiently capture all spikes. Moreover, we show that there exists a parameterization which allows to obtain accurate results in a reasonable time, which is a very important feature for practical applications. In order to address the valuation uncertainty linked to the existence of a range of different parameterizations, we calculate the Model Risk AVA (Additional Valuation Adjustment) for XVA according to the provisions of the EU Prudent Valuation regulation.

Finally, this work can serve as an handbook containing step-by-step instructions for the implementation of a complete, realistic and robust modelling framework of collateralized exposure and XVA.

JEL classifications: G10, G12, G13, G15, G18, G20, G33.

Keywords: Interest Rates, XVA, CVA, DVA, AVA, Prudent Valuation, Model Risk, Market Risk, Counterparty Risk, Model Validation, Credit Exposure, Variation Margin, Initial Margin, ISDA-SIMM, Swaps, Swaptions, Derivatives.

Acknowledgements: the authors acknowledge fruitful discussions with Marcello Terraneo, Andrea Principe, and many other colleagues in Intesa Sanpaolo Risk Management Department.

Disclaimer: the views expressed here are those of the authors and do not represent the opinions of their employers. They are not responsible for any use that may be made of these contents.

1 Introduction

The 2007 credit crunch crisis has made necessary to reconsider the methodologies used until that time to price over-the-counter (OTC) derivatives. For example, during the crisis a change of regime in the interest rate market was observed: basis spreads between interest rate derivatives characterised by different underlying rate tenors (e.g. IBOR 3M444IBOR denotes a generic Interbank Offered Rates., IBOR 6M, etc.) exploded and the spread between Overnight Indexed Swap (OIS) rates and rates of longer tenors widened significantly. This change of regime has lead to an evolution of market practice with the introduction of multiple interest rate yield curves (multi-curve framework) and OIS discounting. Literature is very extensive in this field, a non-exhaustive list of references is [1, 2, 3, 4, 5, 6, 7]. Such framework has been recently questioned by the interest benchmark reform and the progressive replacement of the old IBOR rates with the corresponding risk free rates. Benchmark reform impacts XVA as well, but in this paper it is not considered at all. We refer to [8] for a discussion around the impact of EONIA-€STR discounting switch on XVA.

Moreover, the crisis triggered the incorporation of additional risk factors within the usual risk-neutral valuation through a set of valuation adjustments, collectively named XVA. In particular, the Lehman Brothers bankruptcy triggered a greater awareness amongst market participants on counterparty credit risk, leading to its inclusion in derivatives pricing via Credit Valuation Adjustment (CVA)555Which actually was explored before the crisis, see e.g. [9] and references therein.. Post-crisis also the own risk of default began to be addressed (see e.g. [10, 11]) leading to bilateral CVA models and Debt Valuation Adjustment (DVA). Both CVA and DVA are also envisaged by the International Financial Reporting Standards (IFRS) 13 (see par. 42 and 56, [12]) In addition, the observed widening of funding spreads originated a parallel stream of literature (see e.g. [13, 14, 15]) focused on the inclusion of financing costs in derivatives pricing via Funding Valuation Adjustment (FVA) which, even nowadays, represents a source of debate in quantitative finance community given the possible overlap between its Funding Benefit Adjustment (FBA) component and DVA (see [16] and references therein). In a similar way, the Margin Valuation Adjustment (MVA) takes into account the costs of financing the Initial Margin (see e.g. [17]). Finally, due to the increasing regulatory capital requirements triggered by the crisis (Basel II, [18] and Basel III, [19]), the literature started to consider these capital costs in derivatives pricing through the Capital Valuation Adjustment (KVA) (see e.g. [20]). From regulatory capital requirements perspective, Basel III has set provisions only for CVA and DVA by introducing the CVA capital charge to cover potential losses associated with a deterioration in the credit worthiness of a counterparty, and by de-recognizing DVA from CET1 capital to ensure that an increase in the credit risk of a bank does not lead to an increase in its common equity due to a reduction in the value of its liabilities (see par. 14(b) and 75, [19]).

This paper focuses on CVA and DVA, whose calculation requires modelling the credit exposure along the lifetime of a derivative position. The credit crunch crisis has pushed regulators to mitigate the credit exposure for OTC derivatives. In particular, with regard to non-cleared OTC derivatives, in 2015 the Basel Committee on Banking Supervision (BCBS) and the International Organization of Securities Commissions (IOSCO) finalized a framework, introduced progressively from 2016, which requires institutions engaging in these transactions to bilaterally post Variation Margin (VM) and Initial Margin (IM) on a daily basis at a netting set level (see [21]). In particular, VM aims at covering the current exposure stemming from changes in the value of the portfolio by reflecting its current size, while IM aims at covering the potential future exposure that could arise, in the event of default of the counterparty, from changes in the value of the portfolio in the the period between last VM exchange and the close-out of the position. IM represented an element of innovation in bilateral derivatives markets and according to [21] shall be calculated through either a standardized schedule or an approved internal model. With the aim to prevent both potential disputes between counterparties related to IM determination with different internal models and the overestimation of margin requirements due to the non-risk-sensitive standard approach (see [22]), the International Swaps and Derivatives Association (ISDA) developed the Standard Initial Margin Model (SIMM), a uniform risk-sensitive model for calculating bilateral IM (see [23]), the first version of which was published in 2016.

These margin requirements mitigate credit exposure with impacts on CVA/DVA, therefore VM and IM have to be correctly modelled. Extensive literature exists regarding VM (see e.g. [24, 25, 16]). On the other hand, ISDA-SIMM dynamic IM modelling involves the simulation of several forward sensitivities and their aggregation according to a set of predefined rules, this poses difficult computation and implementation challenges. Different methods have been proposed to overcome such challenges: approximations based on normal distribution assumptions (see [26, 27]), approximated pricing formulas to speed up the calculation (see e.g. [28, 29]), adjoint algorithmic differentiation (AAD) for fast sensitivities calculation (see e.g. [30, 31]) and regression techniques to approximate IM (see e.g. [32, 33]). This paper focuses on the implementation of ISDA-SIMM avoiding as much as possible any approximation. Moreover, in calculating forward sensitivities we considered a finite-difference “bump-and-run” approach which, although computationally intensive compared to AAD, is still used in the financial industry when performances are not critical.

In general, XVA pricing is subject to significant model risk as it depends on many assumptions made for modelling and calculating the relevant quantities in a reasonable computation time. This model risk arises principally from the need to optimize the trade-off between accuracy and performance. In light of this, our paper is intended to answer to the following two interconnected questions:

-

1.

which are the most critical model risk factors, meant as those to which exposure modelling and thus CVA/DVA are most sensitive?

-

2.

Is there an acceptable compromise between accuracy and performance?

We address these questions by identifying all the relevant calculation parameters involved in the standard Monte Carlo approach for computing CVA/DVA and by analysing their impacts in terms of accuracy of the results and computational effort required. Specifically, we calculated CVA/DVA using real market data for both linear and non-linear interest rates derivatives for different collateralization schemes. Clearly, collateral simulation introduces a series of complexities which pose greater computational effort to obtain reliable results; we propose a possible solution which allows to obtain robust results in a reasonable time.

Our work extends the existing literature in the following regards. We consider a complete framework including different collateralization schemes and interest rates derivatives based on real market data. In this context, we generalize G2++ model to multi-curve framework also allowing for the time dependency of volatility parameters for both risk factor dynamics and pricing formulas for Swaps and Swaptions, reporting all mathematical details. Furthermore, we describe in depth the implementation of ISDA-SIMM dynamic IM with a particular focus on the principal methodological peculiarities, e.g. the calculation of Vega sensitivity in future scenarios. Regarding XVA pricing, we address the related model risk by analysing CVA and DVA sensitivities to the relevant calculation parameters and by applying the provisions of regulation [34, 35] regarding the calculation of Model Risk Additional Valuation Adjustment (MoRi AVA). Finally, we compare XVA for uncollateralized Swaps with those obtained through an alternative analytical approach.

The paper is organized as follows. In sec. 2 we introduce the notation, we briefly remind the basic theoretical framework and pricing formulas for the instruments analysed, we describe the model used for simulating interest rates, and we remind CVA/DVA formulas describing both Monte Carlo and analytical approaches for their numerical calculation. In sec. 3 we introduce collateral and we describe the assumptions made for modelling VM and IM along with their calculation methodologies. In sec. 4 we describe the parameterization optimizing the trade-off between accuracy and performance and we show the results both in terms of credit exposure and CVA/DVA for the selected instruments. In sec. 5 we report the analyses conducted on model parameters in order to answer the questions above and we describe the calculation of the MoRi AVA. In sec. 6 we draw the conclusions.

2 Theoretical Framework

2.1 Pricing Approach

Assuming no arbitrage and the usual probabilistic framework () with market filtration and risk-neutral probability measure , the general pricing formula of a financial instrument with payoff paid at time is

| (2.1) | ||||

| (2.2) | ||||

| (2.3) | ||||

| (2.4) |

where the base value666In order to ease the notation, for the rest of the paper we omit subscript 0 unless clearly necessary, denoting the base value simply with . (or mark to market) in eq. 2.2 is interpreted as the price of the financial instrument under perfect collateralization777An ideal Credit Support Annex (CSA) ensuring a perfect match between the price and the corresponding collateral at any time . This condition is realised in practice with a real CSA minimizing any friction between the price and the collateral, i.e. with daily margination, cash collateral in the same currency of the trade, flat overnight collateral rate, zero threshold and minimum transfer amount (see sec. 3 for further details)., the discount (short) rate in eq. 2.3 is the corresponding collateral rate, is the collateral bank account growing at rate , is the stochastic collateral discount factor, is the Zero Coupon Bond (ZCB) price, and is the -forward probability measure associated to the numeraire . Valuation adjustments in eq. 2.1, collectively named XVA, represent a crucial and consolidated component in modern derivatives pricing which takes into account additional risk factors not included among the risk factors considered in the base value in eq. 2.2. These risk factors are typically related to counterparties default, funding, and capital, leading, respectively, to Credit/Debt Valuation Adjustment (CVA/DVA), Funding Valuation Adjustment (FVA), often split into Funding Cost/Benefit Adjustment (FCA/FBA), Margin Valuation Adjustment (MVA), Capital Valuation Adjustment (KVA). A complete discussion on XVA may be found e.g. in [25, 16]. For XVA pricing we must consider the enlarged filtration where is the filtration generated by default events (see e.g. [24]). More details on XVA pricing are discussed in sec. 2.4 below.

2.2 Instruments

In this section we briefly describe the financial instruments subject to our analyses along with their corresponding pricing formulas. In particular, our analyses rely on Interest Rate Swaps and physically settled European Swaptions both characterized by the following time schedules for the fixed and floating leg of the Swap

| (2.5) |

2.2.1 Interest Rate Swap

We consider a generic Swap contract, which allows the exchange of a fixed rate against a floating rate, characterised by the time schedules S and T and the following payoffs for the fixed and floating legs, respectively,

| (2.6) |

where and are the year fractions for fixed and floating rate conventions, respectively, and is the underlying spot floating rate with tenor , consistent with the time interval .

The price of the Swap at time is given by the sum of the prices of fixed and floating cash flows occurring after ,

| (2.7) |

where is the notional amount, denotes a payer/receiver Swap (referred to the fixed leg), and are the first future cash flows in the Swap’s schedules, is the annuity, and is the forward rate observed at time , fixing at future time888If the rate has already fixed, hence . and spanning the future time interval , given by

| (2.8) |

By construction, the forward rate is a martingale under the forward measure associated to the numeraire .

The par Swap rate , i.e. the fixed rate such that the Swap is worth zero, is given by

| (2.9) |

The Swap’s price in terms of the par Swap rate can be expressed as

| (2.10) |

The underlying rate is an IBOR with a tenor consistent with the time interval (e.g. for EURIBOR 6M and semi-annual coupons). IBOR forward rates are computed from IBOR yield curves built from homogeneous market IRS quotes (i.e. with the same underlying IBOR tenor ), using the corresponding OIS yield curve for discounting, a procedure commonly called multi-curve bootstrapping999Since OIS and IBOR curves with different tenors are involved, see e.g. [36] for a detailed discussion.. We can write the usual expression of forward rates

| (2.11) |

where is the year fraction with the forward rate convention and can be interpreted as the price of a risky ZCB issued by an average IBOR counterparty101010Namely an issuer with a credit risk equal to the average credit risk of the IBOR panel, see e.g. [37]..

2.2.2 European Swaption

A physically settled European Swaption is a contract which gives to the holder the right to enter, at a given expiry time , into a Swap contract starting at and maturing at with time schedules S and T. The payoff can be written as

| (2.12) |

The market practice is to value physically settled European Swaptions through the Black formula, assuming a shifted log-normal driftless dynamics for the evolution of the Swap rate under its corresponding discounting Swap measure111111Since . associated to the numeraire . Formally, the price of a physically settled European Swaption at time is given by

| (2.13) |

where is the constant log-normal shift, is the shifted log-normal implied forward variance, with being the shifted log-normal implied forward volatility.

2.3 G2++ Model

As regards interest rate simulation, due to its analytical tractability, we considered the Shifted two-factor Gaussian (Vasicek) model G2++, equivalent to the Hull-White Two-Factor Model, introduced in [38]. We generalized G2++ model in multi-curve framework also allowing for the time dependency of volatility parameters. In following sections we describe the instantaneous short rate process dynamics, pricing formulas for Swaps and European Swaptions, and the methodologies used for calibrating model parameters and for implementing Monte Carlo simulation. Pricing formulas are further described in app. B.

2.3.1 Short-Rates Dynamics

The dynamics of the instantaneous short rate process under the risk-neutral measure is given by

| (2.14) |

where , with and denoting, respectively, the discount curve and the forward curve . The processes and are defined as follows

| (2.15) | ||||

| (2.16) |

where is a two dimensional Brownian motion with an instantaneous correlation such that

| (2.17) |

with , , positive constants, , , , with piece-wise constant function written as . The function is deterministic and well defined in the time interval . This modification of G2++ model represents the most parsimonious way to take into account the multi-curve dynamics of interest rates (see e.g. [6] for G1++ model).

By integrating eqs. 2.15 and 2.16 we obtain, for each

| (2.18) |

from which we can see that , conditional on the sigma-field generated by the pair up to time , is normally distributed with mean ad variance, respectively,

| (2.19) | ||||

| (2.20) |

where for the variance we assumed, without loosing generality, that and for a certain and with .

2.3.2 Interest Rate Swap and European Swaption Pricing

In [38] it is shown that in single-curve framework G2++ model admits closed pricing formulas for the price of Swaps and European Swaptions. In particular, Swap pricing is fairly straightforward since ZCB are known, while for an European Swaption it is necessary to compute an integral. We generalized G2++ pricing formulas in multi-curve framework also allowing for time dependent (piece-wise constant) volatility parameters in such a way to preserve the proofs in [38]. All details are reported in app. B.

2.3.3 Calibration

We calibrated G2++ model parameters on at-the-money (ATM) Swaption prices following a two-steps procedure:

-

1.

Constant volatility calibration: calibration of by minimizing the following objective function, which represents the distance between market prices and model prices for each combination of expiry and tenor

(2.21) -

2.

Time dependent volatility calibration: calibration of the function which multiplies and obtained from step above. We calibrated through an iterative calibration which minimizes the following objective function for each expiry using calibrated in the previous iterations

(2.22)

2.3.4 Monte Carlo Simulation

Since G2++ is analytically tractable, it is possible to avoid unnecessary workloads by simulating the processes and under the -forward measure (see e.g. [39, 38]). In [38] the dynamics of and are rewritten under the -forward measure and explicit solutions for the stochastic differential equations are shown. Following the authors, we considered the following simulation scheme by using the exact transition density and generalizing for time-dependent volatility parameters

| (2.23) | ||||

| (2.24) |

for , where and are the drift components (see app. B), and is a two-dimensional normal random vector with zero mean and covariance matrix (assuming and )

| (2.25) |

In detail, we defined a time grid and we calculated the price of each instrument at a future time step (or mark to future) by simulating forward market risk factors using the pair , , obtained from the previously generated , by applying eqs. 2.23 and 2.24, with and , for . It should be noticed that, for our purposes, we do not need to simulate since the price of a Swap or an European Swaptions can be obtained directly through and (see app. B).

2.4 XVA Pricing

As mentioned before, our paper is focused on Credit Valuation Adjustment (CVA) and Debt Valuation Adjustment (DVA) which take into account the risks related to counterparties default. In particular, CVA is related to counterparty default, while DVA is related to own default. In this section we define these valuation adjustments and we describe both the adopted Monte Carlo approach and an alternative analytical approach limited to CVA/DVA calculation of Swaps.

2.4.1 Definitions

Let us consider the two parts of the contract as the Bank (B) and the Counterparty (C) assuming that both can default at instant , .

In order to define CVA we suppose that , i.e. C defaults before B and contract maturity , and B has positive exposure with regard to C. In this case, B suffers a loss equal to the replacement cost of the position. CVA is therefore the discounted value of expected future loss suffered by B due to the default of C and it is a negative quantity in B’s perspective.

On the other hand, to define DVA we consider the opposite situation: , i.e. B defaults before C and contract maturity , and B has negative exposure with regard to C. In this case, C suffers a loss equal to the replacement cost of the position. DVA is therefore the discounted value of expected future loss suffered by C due to the default of B and it is a positive quantity in B’s perspective. Formally

| (2.26) | ||||

| (2.27) | ||||

| (2.28) |

where denotes the exposure at time in the event of default of X, is the base value121212We assume “risk free” close-out at the base value, without any adjustment. of the instrument at time , denotes generically the collateral available at time (see sec. 3 for a specific definition in relation with our purposes), and is the Loss Given Default at time , which represents the percentage amount of the exposure expected to be loss in case of X’s default, with denoting the Recovery Rate.

Assuming independence among credit and interest rate processes and even among default instants , and in absence of wrong way risk131313Risk arising when the exposure with the counterparty is inversely related to the creditworthiness of the counterparty itself., the expectations in eqs. 2.26 and 2.27 can be represented as integrals over time (see e.g. [25, 16]),

| (2.29) | ||||

| (2.30) |

where is the survival probability of X until time valued at such that , with denoting the stochastic hazard rate of X (see e.g. [38]); is the marginal default probability of X referred to the infinitesimal time interval valued at ; and denote respectively the market filtration and the filtration generated by default events. is assumed to be constant.

2.4.2 Calculation Methodology

Our work is based on the standard Monte Carlo simulation approach to solve eqs. 2.29 and 2.30, which allows to calculate CVA and DVA for any instrument, both at trade and at netting set level, also in the presence of collateral agreements. This approach, whilst the most time-consuming for exposure quantification, allows us to easily cope with the various complexities related to XVA calculation.

First of all, it is necessary to discretize the integral along a time grid , with being instrument’s maturity. Then, in order to simulate the relevant quantities over time, it is necessary to make assumptions regarding their stochastic dynamics. To this end, G2++ model admits closed pricing formulas for Swap and European Swaptions (see app. B) and as such, once simulated the processes and (see sec. 2.3.4), the exposure can be computed.

In light of what stated above, eqs. 2.29 and 2.30 can be discretized as follows (see e.g. [25, 16])

| (2.31) |

| (2.32) |

with

| (2.33) |

where is the Expected Positive Exposure (EPE) at time , discretized on interval , is the Expected Negative Exposure (ENE), is the exposure at time step for path (see eq. 3.1), is the survival probability of X at time , referred to time interval and is the marginal default probability of X at time , referred to interval .

2.4.3 Analytical Formulas

For some derivatives, such as Swaps, it is possible to analytically solve eqs. 2.29 and 2.30 with considerable benefits in terms of computational time, but limited to uncollateralized case and at trade level. Nevertheless, this approach can be used with the aim to validate the results obtained through a Monte Carlo model (see sec. 5.5).

Starting from eq. 2.29, the CVA of an uncollateralized Swap at time can be written as (see e.g. [16])

| (2.34) |

By rewriting the price of the Swap in terms of Swap rate (eq. 2.10) and rearranging the terms, the equation above becomes

| (2.35) |

where denotes the price at time of an European Swaption expiring at time on a Swap having tenor equal to .

Since , the analytical DVA can be obtained as

| (2.36) |

By discretizing the above integrals along a time grid , with being the maturity of the Swap one obtains

| (2.37) | ||||

| (2.38) |

Thus, the CVA of a payer (receiver) Swap at time can be written as a weighted sum with weights represented by the values of a strip of co-terminal payer (receiver) European Swaptions expiring at time to enter in a Swap with tenor . Symmetrically, DVA can be obtained as a weighted sum over the values of a strip of receiver (payer) European Swaptions.

3 Collateral Modelling

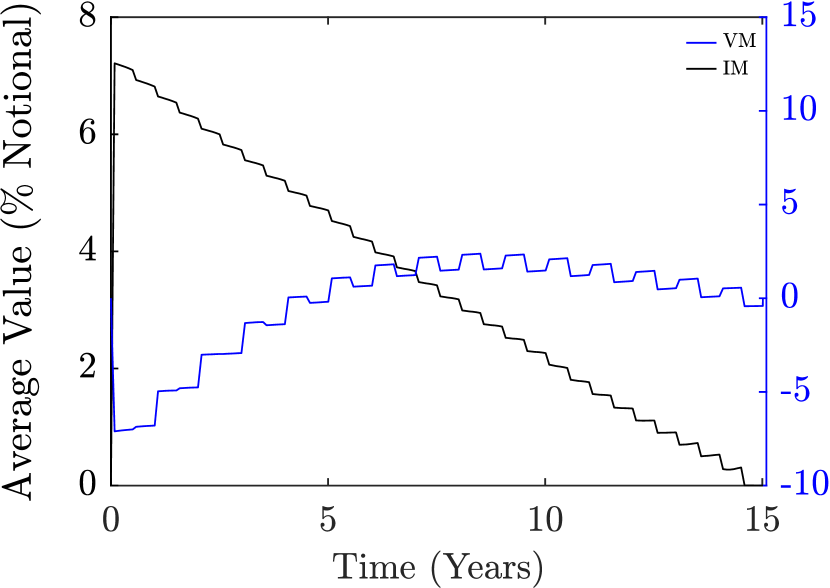

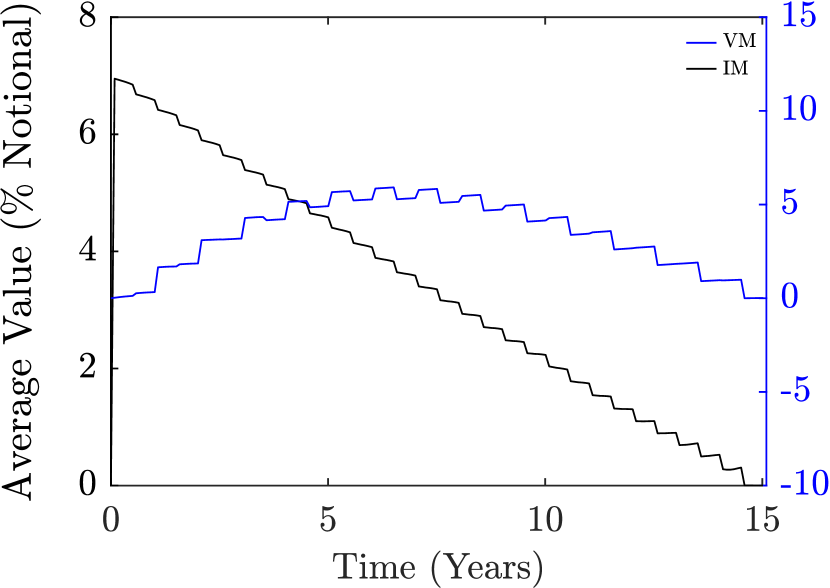

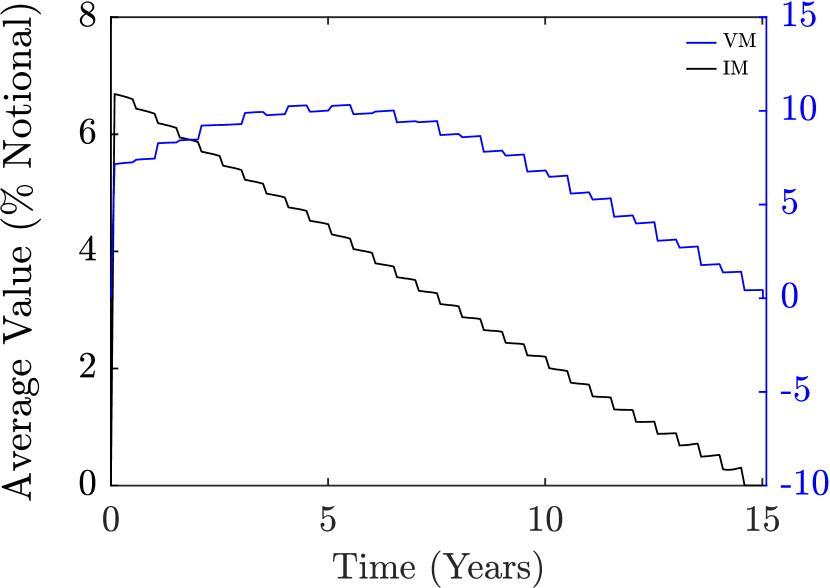

With the aim to reduce the systemic risk posed by non-cleared OTC derivatives, BCBS-IOSCO framework (see [21]) requires institutions engaging in these transactions to post bilaterally Variation Margin (VM) and Initial Margin (IM) on a daily basis at a netting set level. On the one hand, VM aims at covering the current exposure stemming from changes in instrument’s mark to market by reflecting its current size. On the other hand, IM aims at covering the potential future exposure that could arise, in the event of default of the counterparty, from changes in instrument’s mark to market in the the period between last VM exchange and the close-out of the position; this time interval is known as Margin Period of Risk (MPoR).

This section introduces collateral and describes the assumptions made for calculating VM and IM, with a particular focus on ISDA-SIMM dynamic IM.

3.1 Collateral Management

ISDA Master Agreement represents the most common legal framework which governs bilateral OTC derivatives transactions. In particular, the Credit Support Annex (CSA) to ISDA Master Agreement provides the terms under which collateral is posted, along with rules for the resolution of collateral disputes. Certain CSA parameters affect the residual exposure, namely: eligible assets (cash, cash equivalent, government bonds), margin call frequency, threshold (K), defined as the maximum amount of allowed unsecured exposure before any margin call is made, and minimum transfer amount (MTA), defined as the minimum amount that can be transferred for each margin call.

Under perfect collateralization, counterparty risk is suppressed resulting in null CVA/DVA. Theoretically, this corresponds to an ideal CSA ensuring a perfect match between the price and the corresponding collateral at any time .

This condition is approximated in practice with a CSA minimizing any friction between the mark to market and the collateral, i.e. cash collateral in the same currency of the trade, daily margination, flat overnight collateral rate, zero threshold and minimum transfer amount.

Nevertheless, real CSA introduces some frictions causing divergences between the price and the corresponding collateral and hence a not negligible counterparty risk. For example, collateral transfers are not instantaneous events and may also takes several days to complete in case of disputes; for this reason, in the event of default, the collateral actually available to the non-defaulting party at the close-out date may differ from the prescribed one.

A simple way to capture these divergences is assuming that VM and IM available at time step depend on the price computed at time , with being a lag parameter. In this way the time interval represents the MPoR, with being the last date for which collateral was fully posted and the close-out date. This implies that, while both counterparties stop simultaneously to post collateral for the entire MPoR, contractual cash flows are fully paid. Although simplistic, this assumption can be deemed appropriate in relation to the purposes of our work (advanced models can be found in [40, 27]).

In practical terms, the inclusion of MPoR requires a secondary time grid, built by defining for each of the principal time grid a look-back time point such that at which collateral is computed, with . Formally, from B’s perspective the collateralized exposure at time step for a generic path , can be written as

| (3.1) |

Here we assumed that a bilateral and symmetrical CSA is in place, VM is netted, and IM is posted into a segregated account as required by regulation (see [21]); therefore, from B’s perspective VM can be positive (if posted by C) or negative (if posted by B), while IM is always positive.

3.2 Variation Margin

VM modelling is fairly straightforward as it depends on instrument’s mark to market, together with K and MTA. We calculated VM available at time step for a generic path through the following formula

| (3.2) | |||

| (3.3) |

where is the value of VM just before its update at , and the second and the third terms of eq. 3.2 correspond to the amount of VM posted at time step by C and B respectively. In particular, in the second term, C will update VM for the amount exceeding the threshold and VM already in place, provided that this amount is greater than the minimum transfer amount; the same holds for B in case of negative exposure (third term). We imposed null VM for and .

3.3 Initial Margin

3.3.1 ISDA Standard Initial Margin Model

In 2013 ISDA, in cooperation with entities first impacted by bilateral margin requirements, started developing the Standard Initial Margin Model (SIMM) with the aim to provide market participant with a uniform risk-sensitive model for calculating bilateral IM (see [23]), preventing both potential disputes between counterparties related to IM determination with different internal models and the overestimation of margin requirements due to the use of the non-risk-sensitive standard approach (see [22]). The first version of the model was published in 2016. On an annual basis model parameters are recalibrated and the methodology is reviewed in order to ensure that regulatory requirements are met. Since our work relies on market data at 28 December 2018, we considered ISDA-SIMM Version 2.1 which was effective from 1 December 2018 to 30 November 2019 (see [41]).

In general, ISDA-SIMM is a parametric VaR model based on Delta, Vega and Curvature (i.e. “pseudo” Gamma) sensitivities, defined across risk factors by asset class, tenor and expiry, computed in line with specific definitions. More in detail, each trade of a portfolio (under a certain CSA agreement) is assigned to a Product Class among Interest Rates & FX, Credit, Equity and Commodity. Since a given trade may have sensitivity to different risk factors, six Risk Classes are defined among Interest Rate, FX, Credit (Qualifying), Credit (non-Qualifying), Equity and Commodity. The margin contributions stemming from the different Risk Classes are combined by means of an aggregation function taking account of Risk Classes correlations. Formally, IM for a generic instrument can be written as

| IM | (3.4) | |||

| (3.5) |

where Mx is the margin component for the Risk Class141414For Credit (Qualifying) Risk Class, which includes instruments whose price is sensitive to correlation between the defaults of different credits within an index or basket (e.g. CDO tranches), an additional margin component, i.e. the BaseCorrMargin shell be calculated (see [41]). , with , and is the correlation matrix between Risk Classes. IM at portfolio level is obtained by adding together IM contributions from each trade (see [42, 41] for a complete description of the model and underlying assumptions).

In our case, Swaps and European Swaptions are assigned to the Interest Rates & FX Product Class and exposed only to Interest Rate (IR) Risk Class, thus . Moreover, for a Swap given the linearity of its payoff. As discussed above, we imposed that collateral available at time step is function of instrument’s value (sensitivities in IM case) at time . Therefore, at time step and for a generic path the ISDA-SIMM dynamic IM is given by

| (3.6) | ||||

| (3.7) |

Finally, allowing for K and MTA

| (3.8) |

Similar to VM, we imposed null IM for and .

3.3.2 Calculation Methodology

The most challenging task underlying ISDA-SIMM dynamic IM is the simulation of forward sensitivities coherently with ISDA definitions, since the subsequent application of weights and aggregation functions is straightforward if we assume that parameters and aggregation rules do not change during the lifetime of the trade. In this section we report the methodology used for computing forward sensitivities, while the other steps to get the different margin components can be found in app. C.

According to ISDA, Delta for the IR Risk Class is defined as price change with respect to a 1 bp shift up in a given tenor151515ISDA defines for both OIS and IBOR curves the following 12 tenors at which Delta shall be computed: 2w, 1m, 3m, 6m, 1y, 2y, 3y, 5y, 10y, 15y, 20y, 30y. of the interest rate curve, expressed in monetary terms. Moreover, ISDA specifies that if computed by the internal system at different tenors, Delta shall be linearly re-allocated onto the SIMM tenors. In general, the price of an instrument which depends on an interest rate curve depends explicitly on the zero rates of the curve, which, in turn, depends on the market rates from which the curve is constructed via bootstrapping procedure (see e.g. [36]). Therefore, being and , respectively, the zero rates and the market rates in correspondence of the term structure of the same curve , we calculated the sensitivity with respect to the -th market rate at a generic time step as (to ease the notation we neglect subscripts referring to the path)

| (3.9) | |||||

| (3.10) |

where and denote, respectively, the forwarding curve and the discounting curve ,

| (3.11) |

is an element of the Jacobian matrix (with ), assumed to be constant for each , and

| (3.12) |

is the zero rate Delta sensitivity at . The last term of eq. 3.10 takes into account the indirect Delta sensitivity component of the forwarding zero curve to the discounting zero curve, due to the exogenous nature of the bootstrapping procedure. In line with ISDA prescriptions, for each tenor of the curve , we multiplied Delta sensitivity by shock size and linearly allocated this quantity onto the SIMM tenors, obtaining the (1-by-12) Delta vector

| (3.13) |

We then calculated and aggregated the Weighted Sensitivities in order to get Delta Margin (see eqs. C.4 and C.6).

According to ISDA, Vega for the IR Risk Class is defined as price change with respect to a 1% shift up in ATM Black implied volatility , formally

| (3.14) |

where we use superscript Blk to distinguish between Black implied volatility and G2++ parameter .

Vega sensitivity shall be multiplied by implied volatility to obtain the Vega Risk for expiry and linearly allocated onto the SIMM expiries, which correspond to the tenors defined for Delta sensitivity.

Since G2++ European Swaption pricing formula (see eq. B.12) does not provide for an explicit dependence on Black implied volatility, when performing time simulation Vega cannot be calculated according to the definition above. To overcome this limit we propose the following approximation

| (3.15) |

where and are shocks applied on G2++ model parameters governing the underlying process volatility, and implied volatilities and are obtained respectively from European Swaption’s prices and by solving the shifted Black pricing formula (see eq. 2.13). In sec. 5.3 we report the analyses conducted to validate this approach and to select the values for the shocks , and the Black shift . In line with ISDA prescriptions, we multiplied Vega sensitivity by implied volatility and linearly allocated the resulting Vega Risk onto the SIMM expiries, obtaining the (1-by-12) Vega Risk vector

| (3.16) |

We then calculated and aggregated the Vega Risk Exposures to get Vega Margin (see eqs. C.9 and C.11).

Curvature for the IR Risk Class is calculated by using an approximation of the Vega-Gamma relationship (see [42]). The (1-by-12) Curvature Risk Vector

| (3.17) |

is obtained multiplying the Vega Risk vector by a Scaling Function. We then aggregated the elements of Curvature Risk vector to get Curvature Margin (see eqs. C.14 and C.15).

4 Numerical Simulation

This section reports the results in terms of exposure and CVA/DVA obtained for various interest rate derivatives under three collateralization schemes: without collateral, with VM only and with both VM and IM. In particular, we considered 15 years payer Swaps, 30 years payer Swaps, 5x10 years payer and receiver Forward Swaps, and 5x10 years physically settled European payer and receiver Swaptions with different moneyness levels, listed in tab. 1.

| Instrument | Moneyness | ||

|---|---|---|---|

| 15Y Swap | 1 | out-of-the-money | |

| 1 | at-the-money | ||

| 1 | in-the-money | ||

| 30Y Swap | 1 | out-of-the-money | |

| 1 | at-the-money | ||

| 1 | in-the-money | ||

| 5x10Y Forward Swap | -1 | out-of-the-money | |

| 1 | at-the-money | ||

| 1 | out-of-the-money | ||

| 5x10Y Swaption | -1 | out-of-the-money | |

| 1 | at-the-money | ||

| 1 | out-of-the-money |

4.1 Summary of Numerical Steps

We report below a summary of the numerical steps followed for simulating the exposure and computing CVA/DVA.

-

1.

Discretization of the integrals in eqs. 2.29 and 2.30 along an equally spaced time grid with granularity (see eqs. 2.31 and 2.32). In order to capture all spikes arising in collateralized exposure we added to the time grid a point within the interval for each floating coupon date ()161616For the instruments considered, fixed coupon dates are a subset of floating ones since taking place at the same time, otherwise the corresponding coupon dates should have been added to the time grid., with being a lag parameter governing the length of MPoR (see sec. 5.1.2 for details).

-

2.

Construction of a secondary time grid by defining for each time step a look-back time point at which compute the collateral actually available at (see sec. 3.1 for details).

-

3.

Calibration of G2++ model parameters on market ATM European Swaption prices according to the procedure described in sec. 2.3.3.

-

4.

Generation of the pairs , and , for each time step of both the principal and the secondary time grids and simulated path according to the procedure described in sec. 2.3.4.

-

5.

Calculation of exposure for each time step and simulated path according to eq. 3.1. This requires to:

-

6.

Calculation of EPE and ENE for each time step according to eq. 2.33.

-

7.

Calculation of survival probabilities for each time step from default curves built from market CDS quotes through bootstrapping procedure.

- 8.

4.2 Model Setup

Aside from G2++ model parameters we can distinguish between calculation parameters and CSA parameters.

The former affect both the accuracy of the results and the calculation time required and are those related to Monte Carlo approach for calculating CVA/DVA. In particular, we are referring to the granularity of the time grid used for discretize the integrals, the number of simulated scenarios , and the parameters used for compute forward Vega sensitivities related to ISDA-SIMM dynamic IM (see eq. 3.15), namely the magnitude of the shocks on G2++ model parameters and , and the value of the Black shift for implied volatility calculation.

CSA parameters affect the residual credit exposure and consequently CVA/DVA with no impacts on the accuracy of the results, and are those related to collateral simulation. In particular, we are referring to threshold K, minimum transfer amount MTA, and to the length of MPoR .

In selecting calculation parameters it is necessary to cope with the trade-off between accuracy and computational effort. The parameterization considered in this section (see tab. 2) is the one that optimizes this trade-off on the basis of specific analyses reported in sec. 5.

| Parameters Class | Parameter | Value |

|---|---|---|

| Calculation parameters | month | |

| CSA parameters | days | |

| K | EUR | |

| MTA | EUR | |

| G2++ parameters | 1.1664 | |

| 0.0501 | ||

| 0.0304 | ||

| 0.0084 | ||

| -1.0000 | ||

| 0.9530 | ||

| 0.9781 | ||

| 1.0895 | ||

| 1.0709 | ||

| 1.0032 | ||

| 1.0776 | ||

| 1.0488 | ||

| 1.0186 | ||

| 1.1000 | ||

| 0.9608 | ||

| 1.0114 | ||

| 0.9553 | ||

| 0.9629 | ||

| 0.9340 |

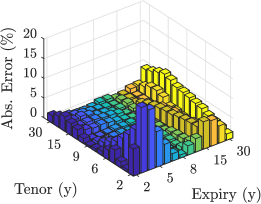

Regarding CSA parameters, in order to get as close as possible to perfect collateralization case, we considered bilateral CSA with both for VM and IM, with days. In sec. 5.4 the impact of these parameters is assessed. With regard to the calibration of G2++ model parameters, we considered the market ATM European Swaption prices matrix in correspondence of the following expiries = {2, 3, 4, 5, 6, 7, 8, 9, 10, 12, 15, 20, 25, 30} and tenors = {2, 3, 4, 5, 6, 7, 8, 9, 10, 15, 20, 25, 30}, both expressed in years (see app. A for details). Calibration errors in absolute percentage terms are shown in fig. 1.

4.3 Results

4.3.1 Exposure

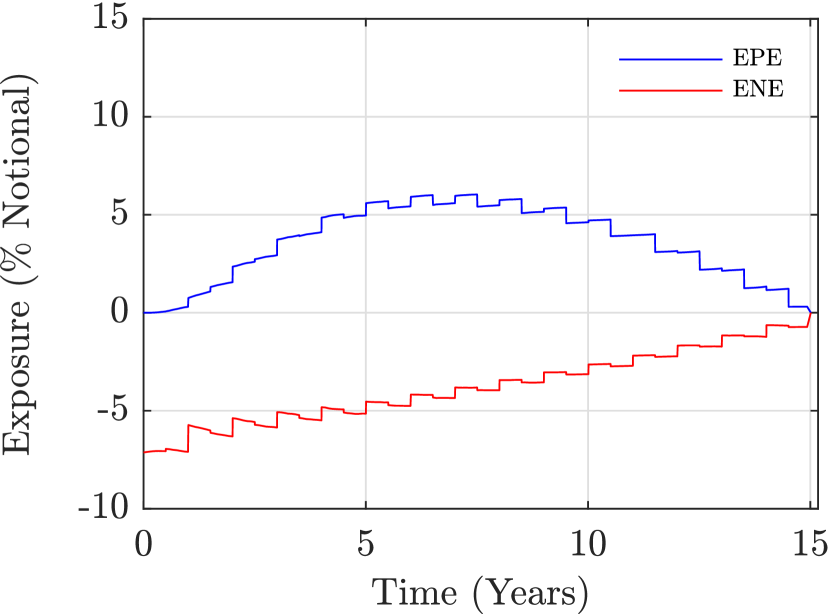

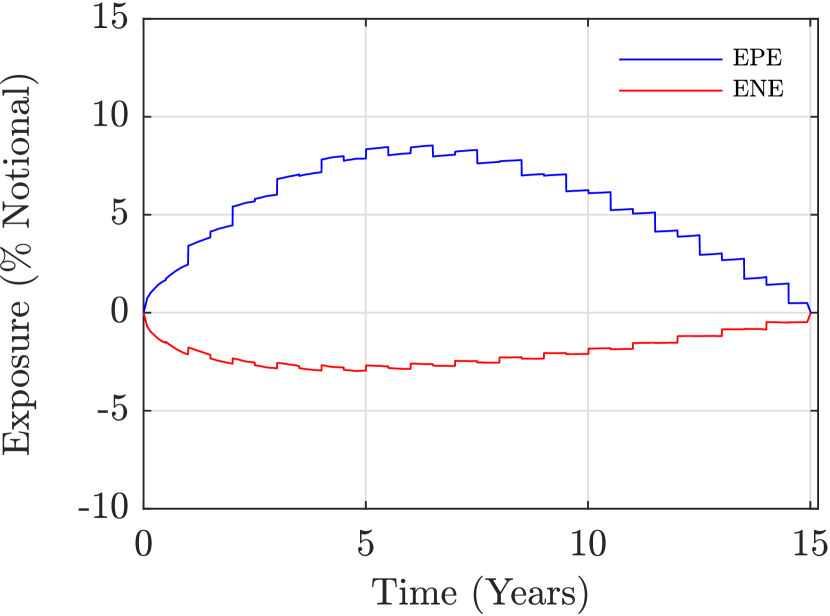

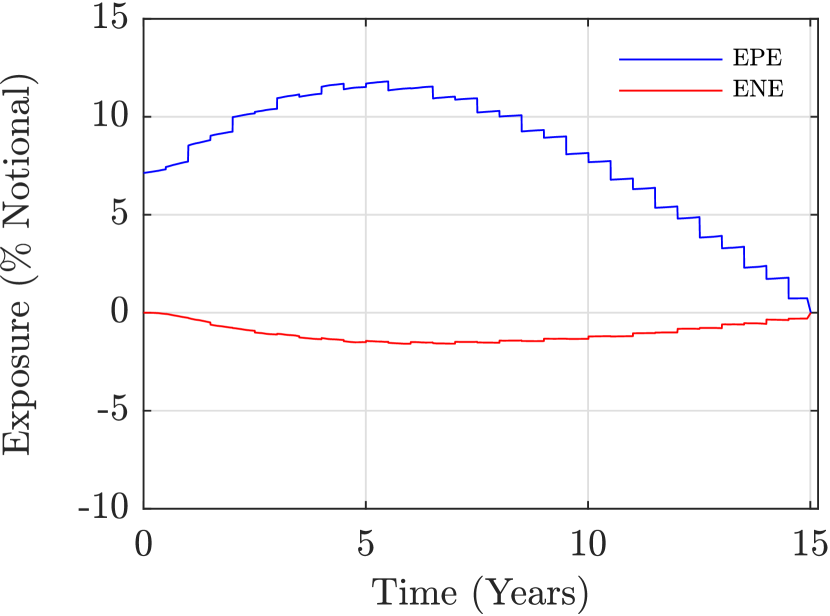

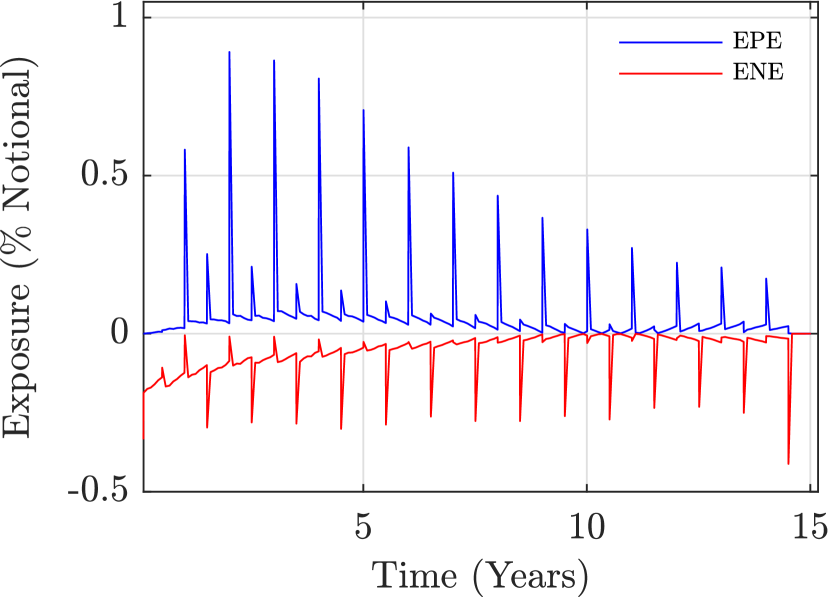

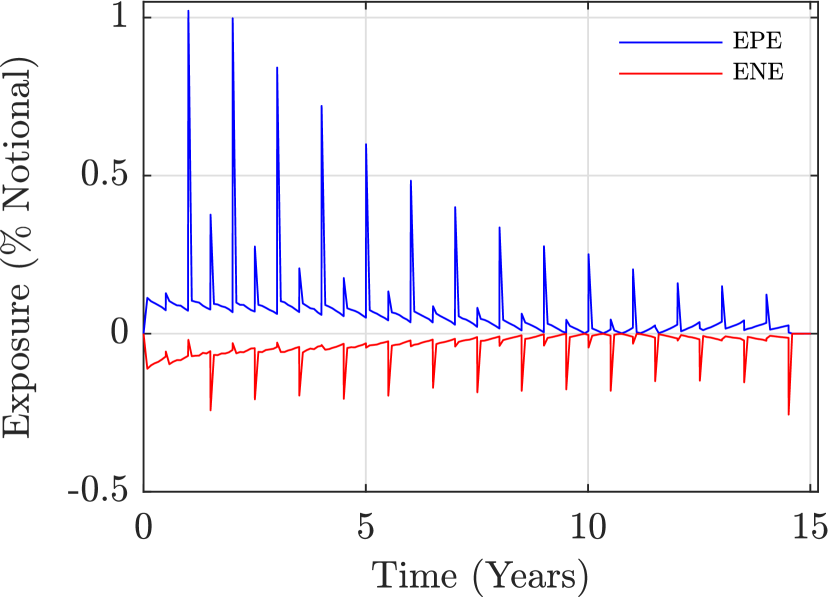

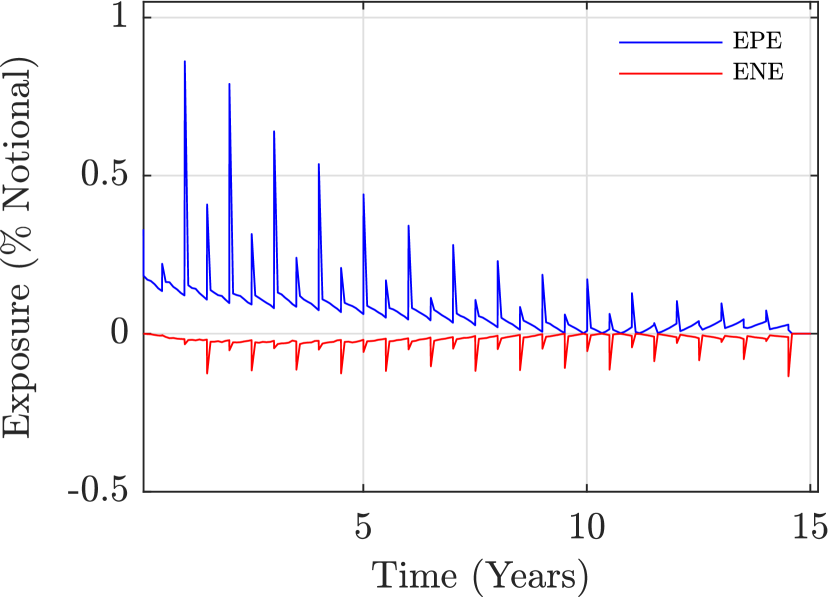

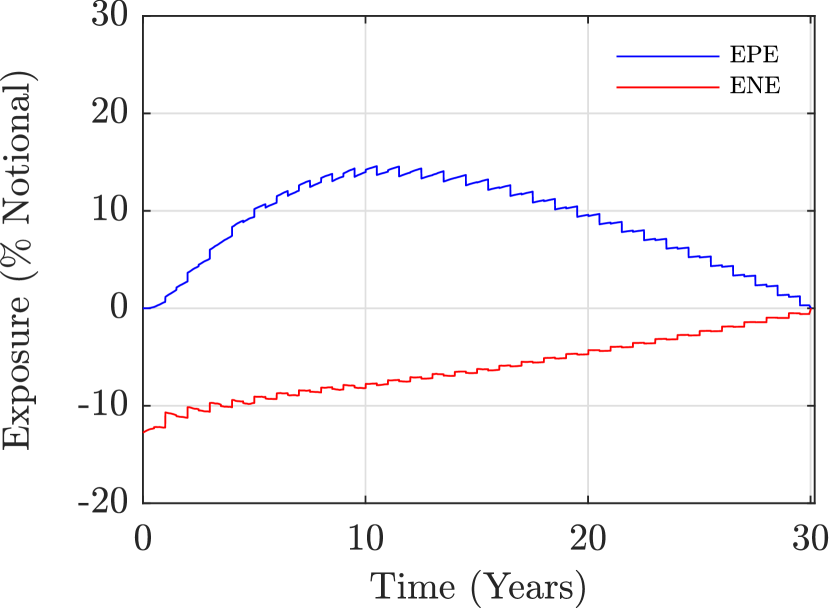

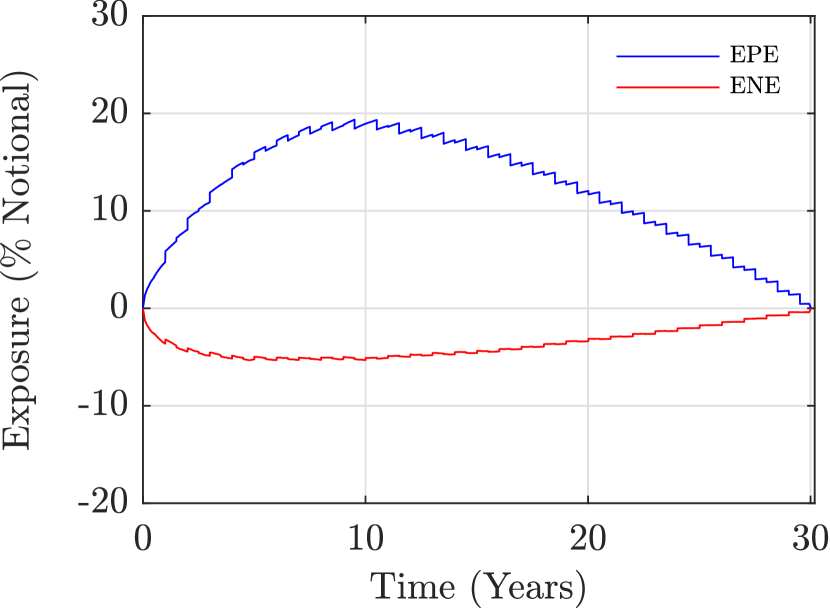

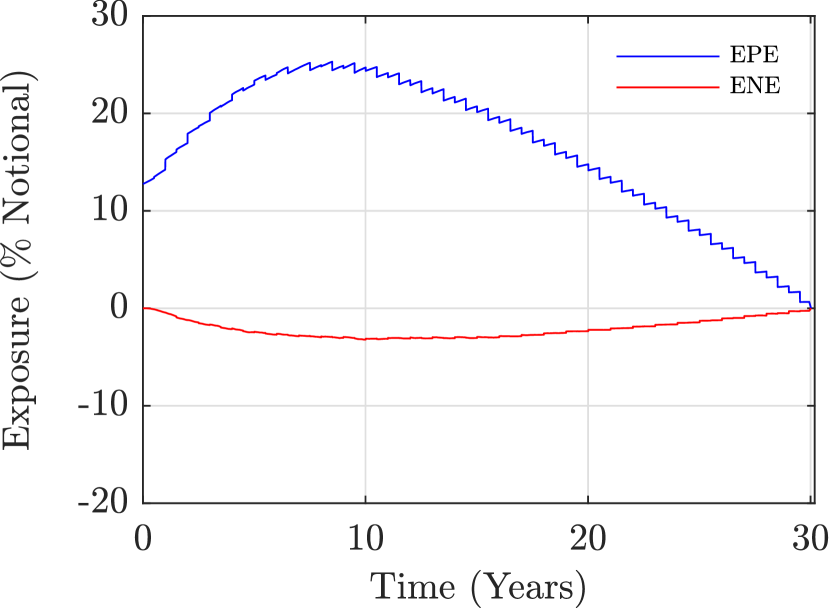

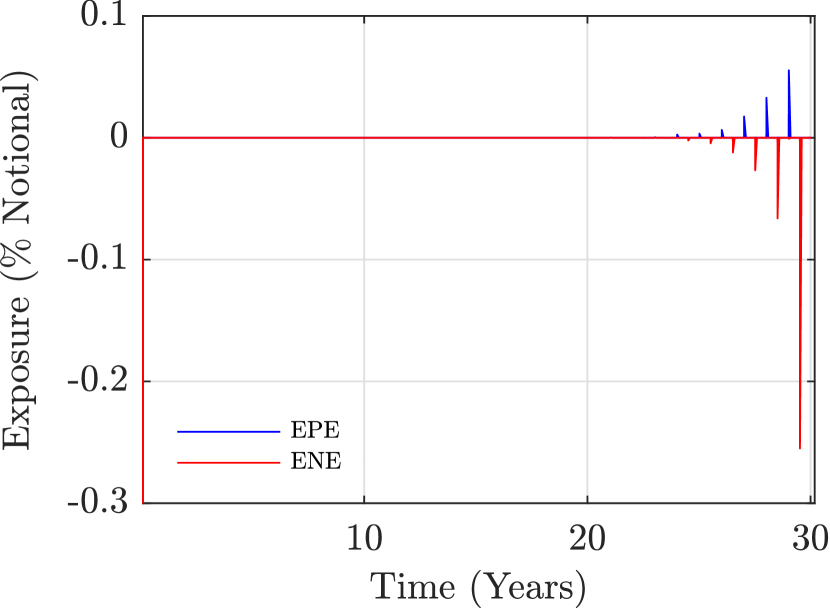

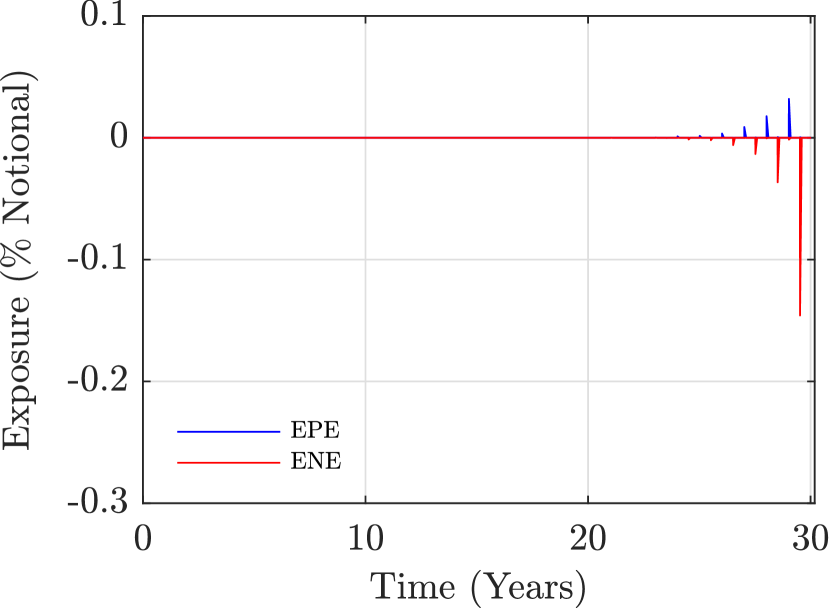

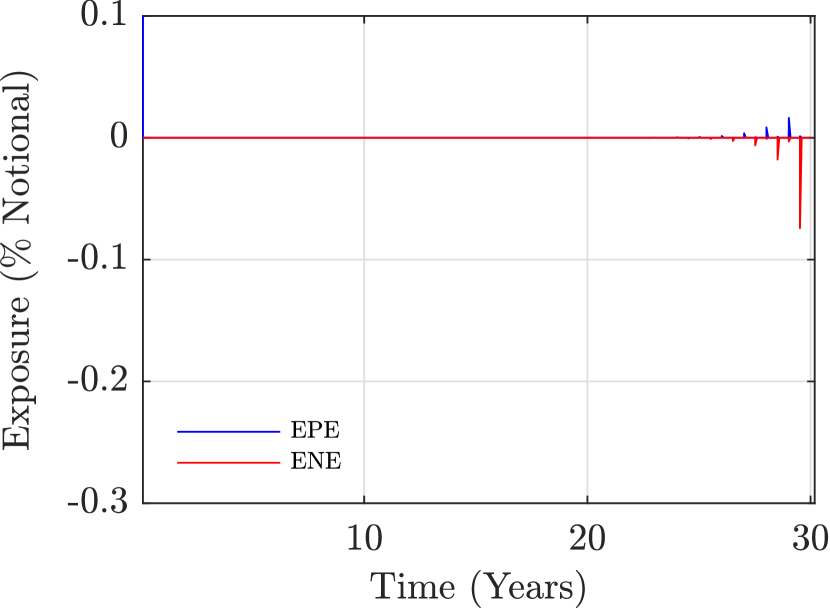

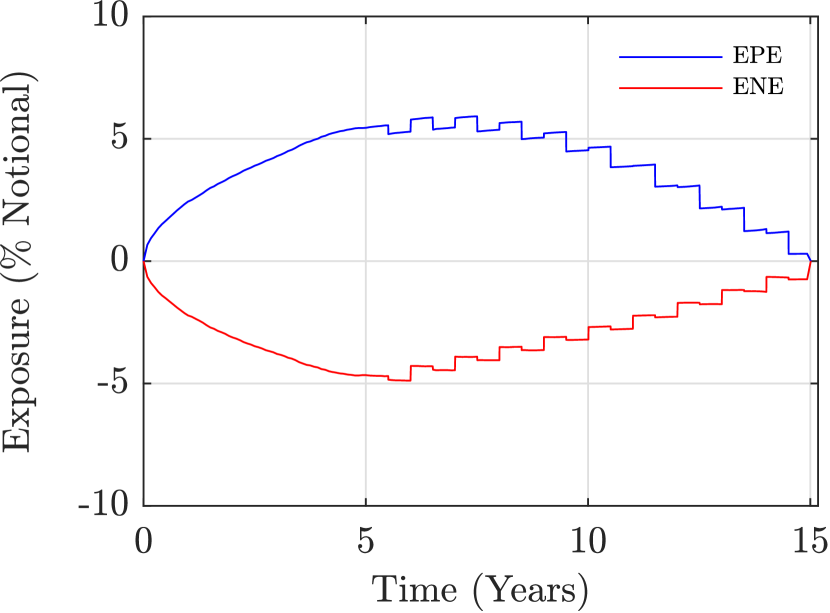

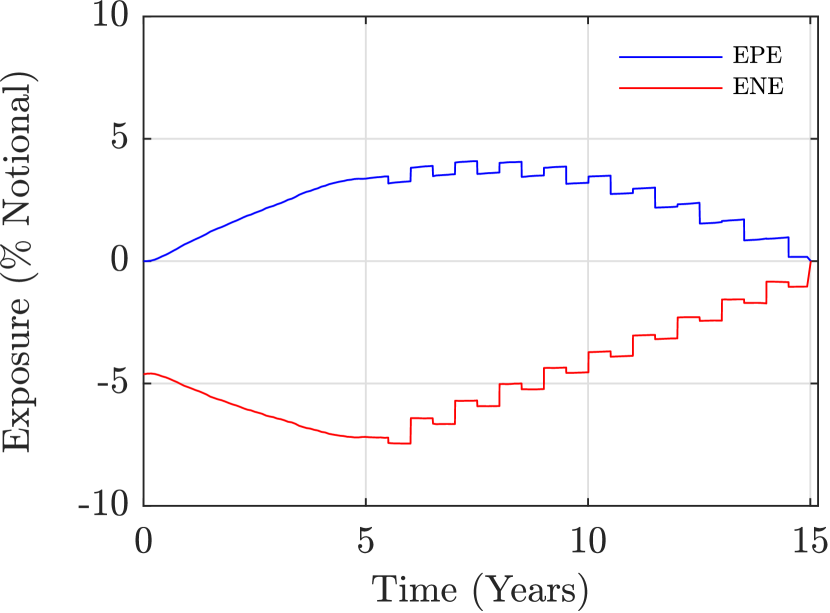

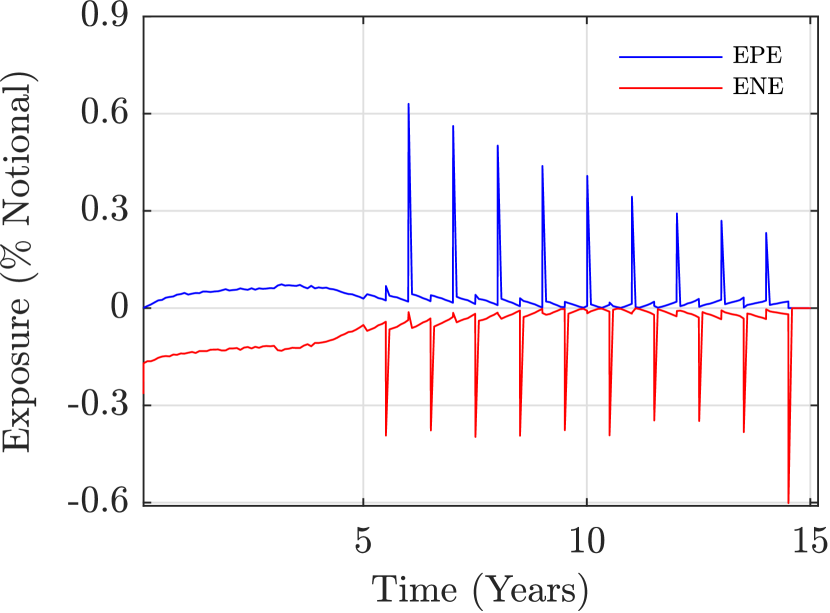

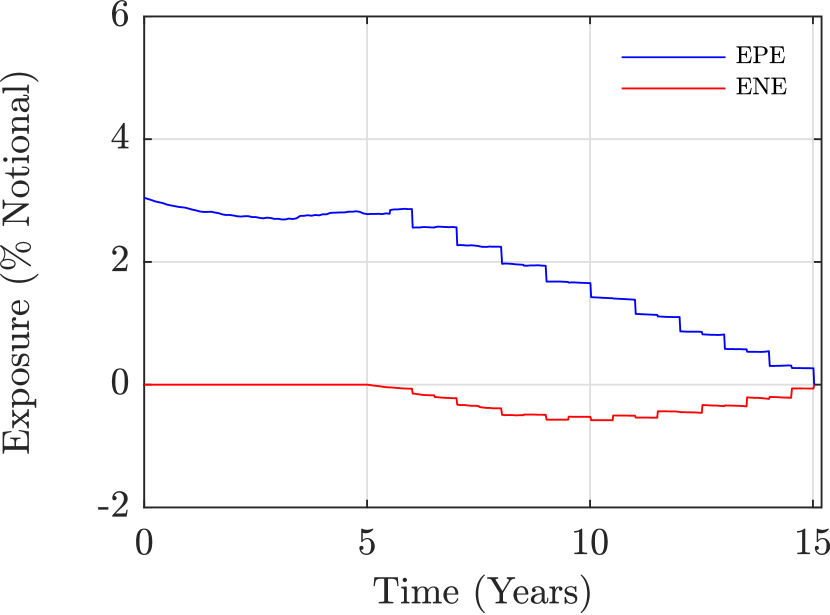

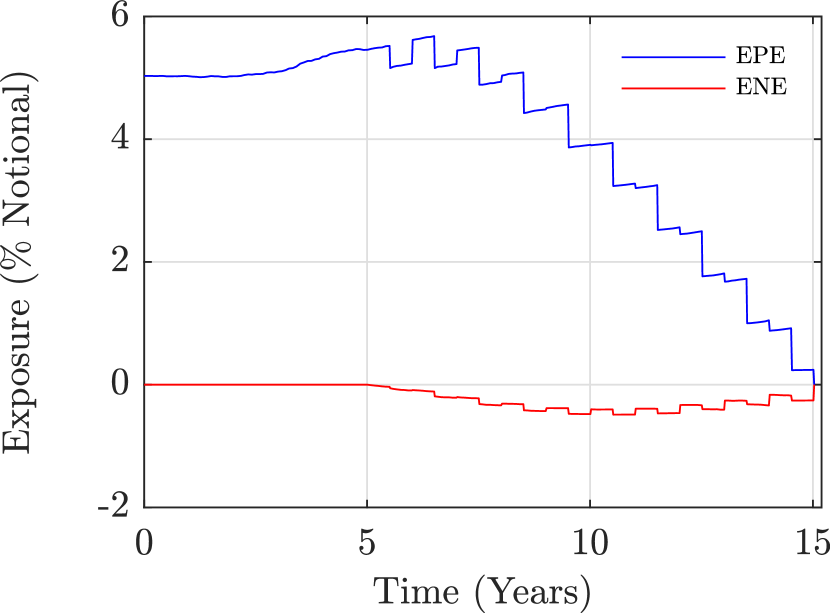

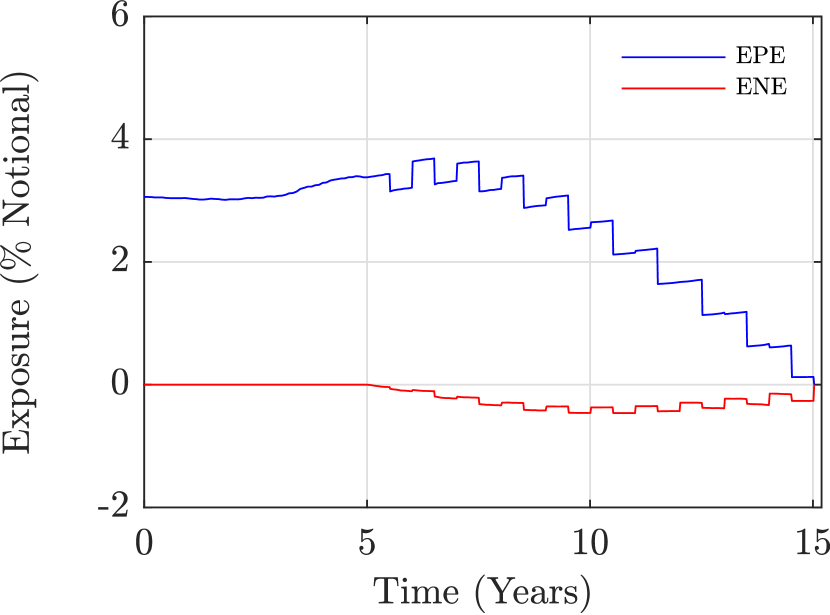

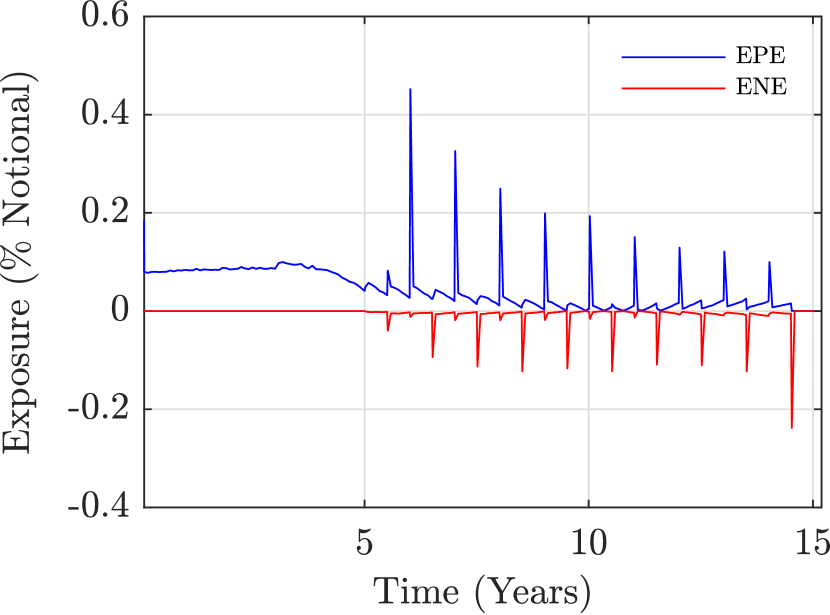

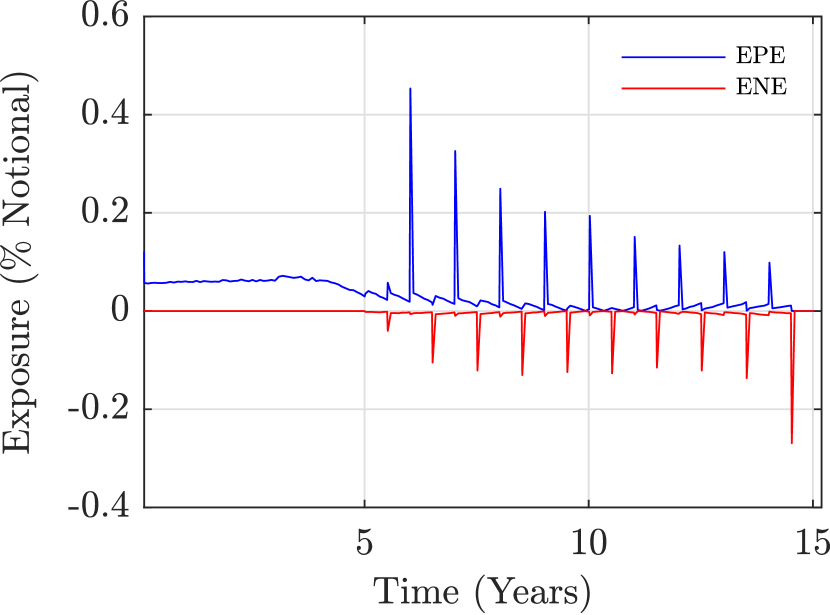

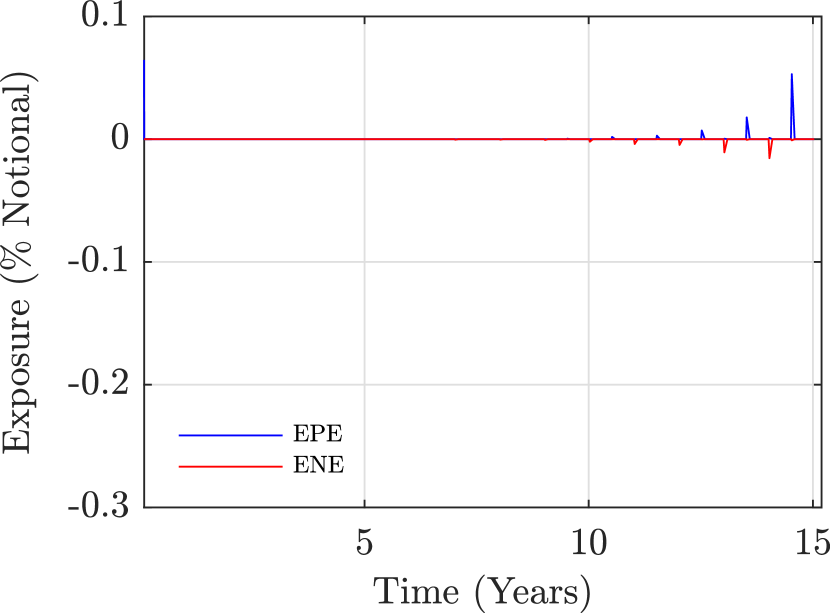

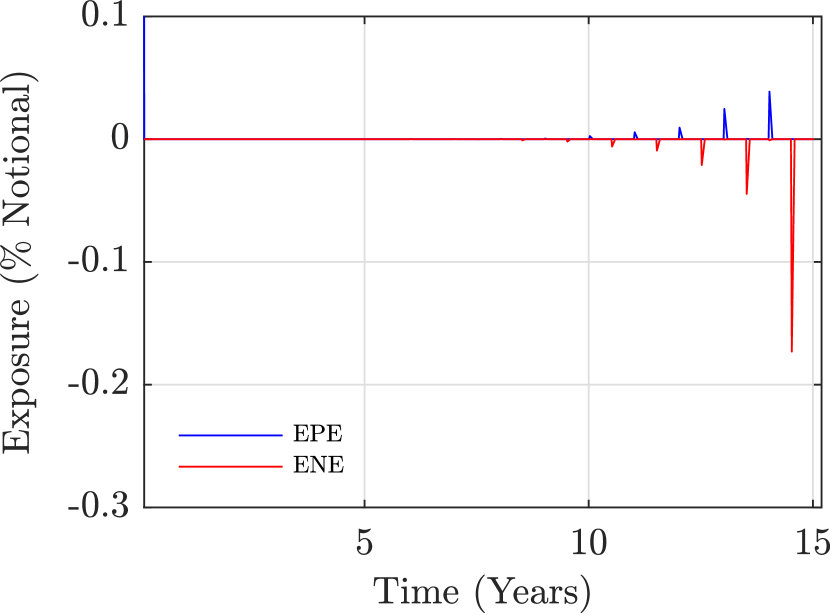

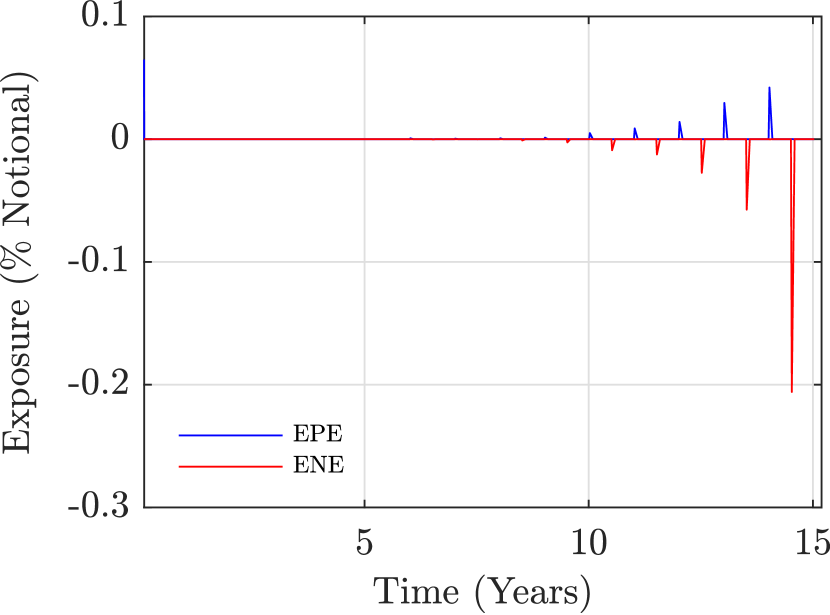

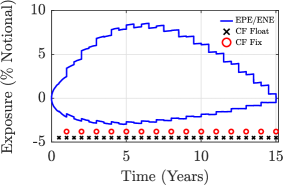

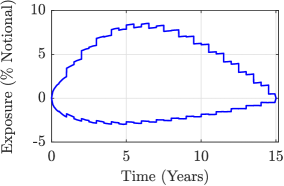

The results in terms of EPE and ENE profiles are reported in figs. 2-5 and are aligned on what can be found in the literature (see e.g. [16]).

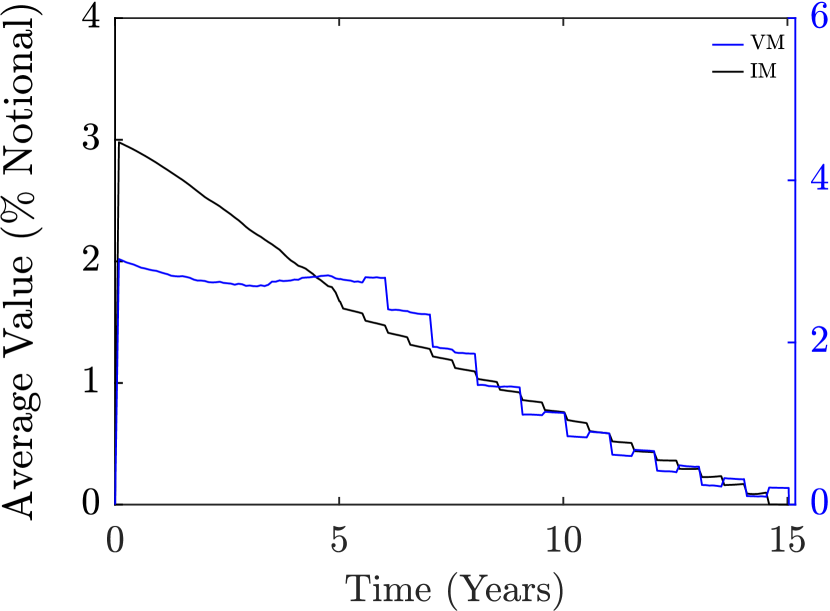

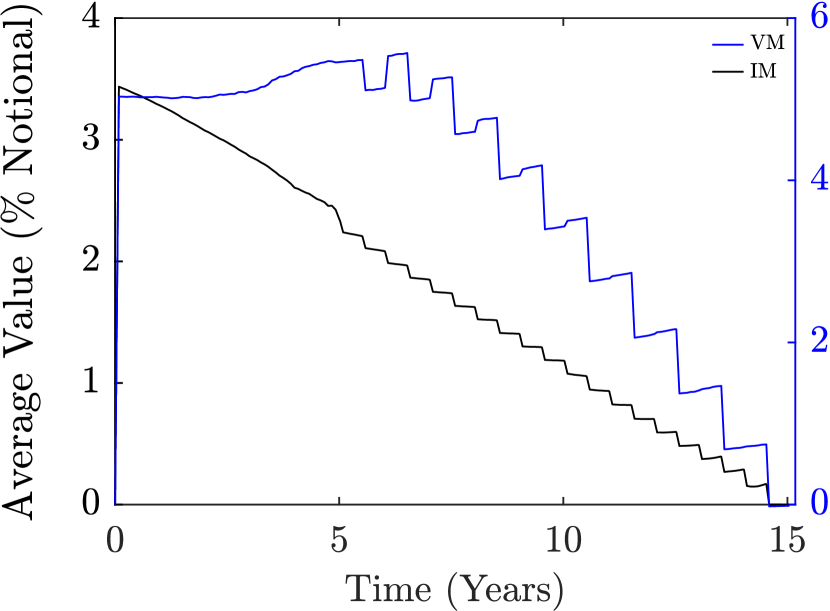

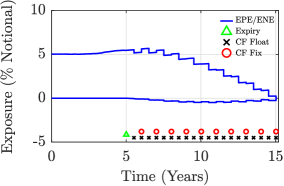

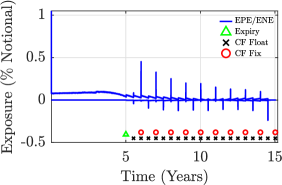

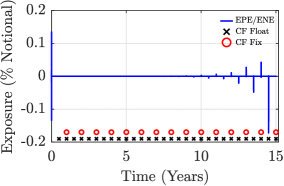

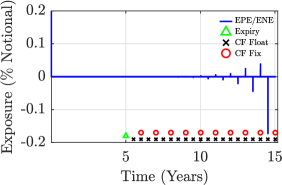

Focusing on uncollateralized exposures (top panels), the jagged shape observed for the Swaps (figs. 2 and 3) is due to the different coupons frequency (floating coupons received semi-annually, fixed coupons paid annually) which determines semi-annual jumps in instruments’ mark to future at coupon dates. EPE is larger than ENE, in absolute terms, except for the out-of-the-money (OTM) 15 years Swap, due to the forward rates structure which causes expected floating leg values greater than those of the fixed leg. This is evident for in-the-money (ITM) Swaps for which ENE is also almost flat given the low probability to observe negative mark to futures. By comparing the exposures for different maturities, 30 years Swaps are clearly riskier due to the greater number of coupons to be exchanged. The analogous shape for the exposure is observed for the Forward Swaps when coupons payment starts, i.e. from years (fig. 4). Here we can observe the asymmetric effect of forward rates on opposite transactions: the OTM payer Forward Swap displays larger EPE and less negative ENE compared to the OTM receiver one. Physically settled European Swaptions (fig. 5) are written on the same Forward Swaps, before the expiry the exposure is always positive and greater than the one of the corresponding underlying Forward Swap as the price is always positive. After the expiry, OTM paths are excluded as the exercise do not take place, determining smaller EPE and ENE (in absolute value) with respect to the corresponding underlying Forward Swap.

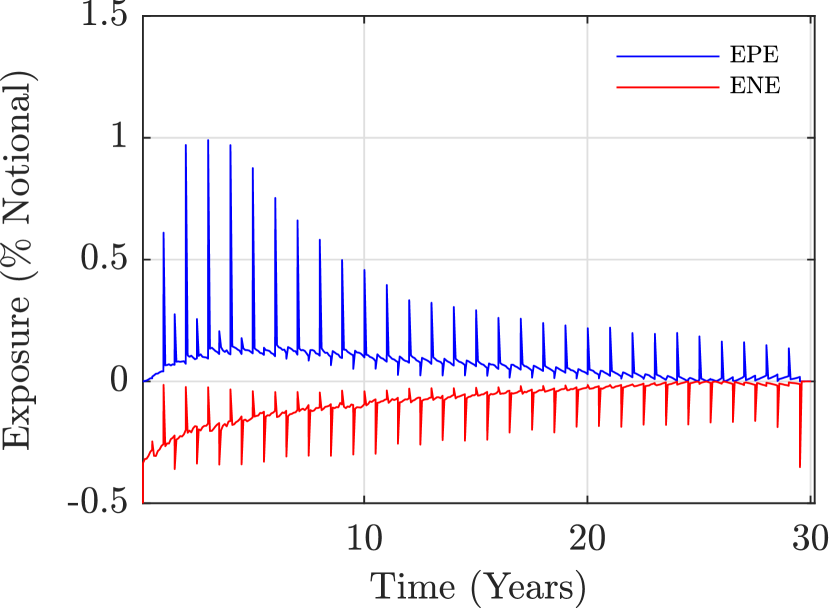

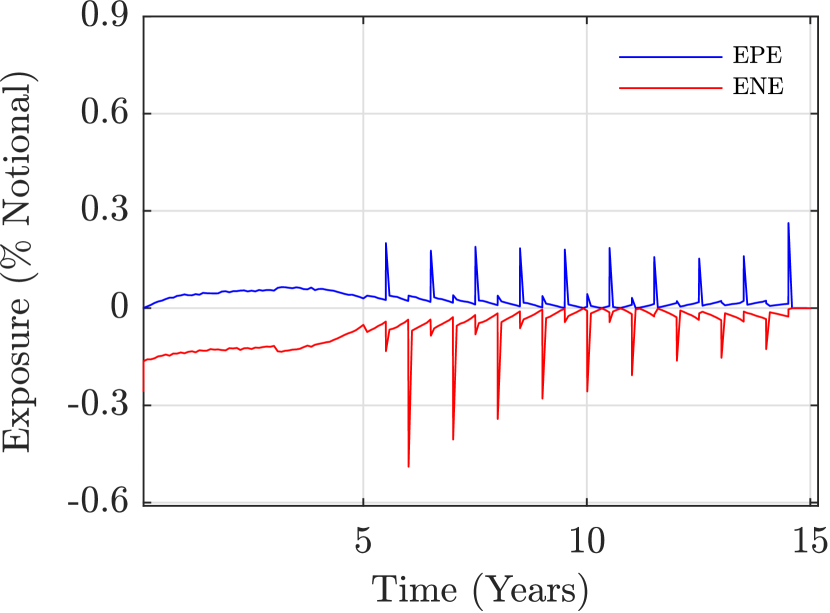

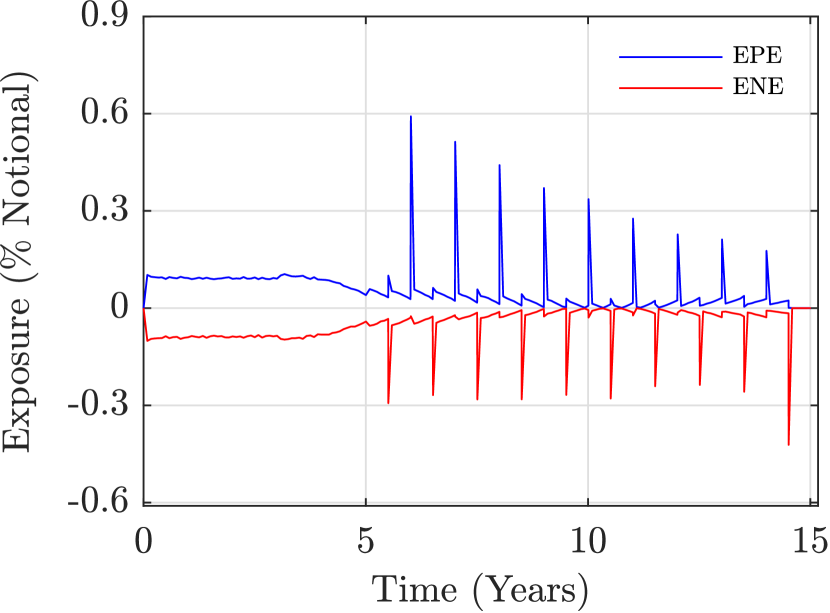

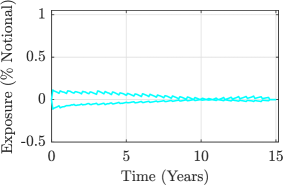

Focusing on exposures with VM (middle panels), a reduction of one order of magnitude can be observed. According to the assumptions made, VM tracks instrument’s mark to future with a delay equal to the length of MPoR (2 days), which represents the only element of friction. This delay causes a material residual exposure characterized by spikes at coupon dates. In general, when only floating coupons are received, one can expect to observe downward spikes due to the fact that the counterparty make a payment for which B still has not returned VM. Conversely, upward spikes arise when fixed cash flows occur and are offset by the downward ones stemming from floating coupons. The magnitude of these spikes is determined by the simulated forward rates structure, e.g. the large upward spikes displayed at the early stage of payer Swaps’ life are due to negative rates (see sec. 5.1.1 for details).

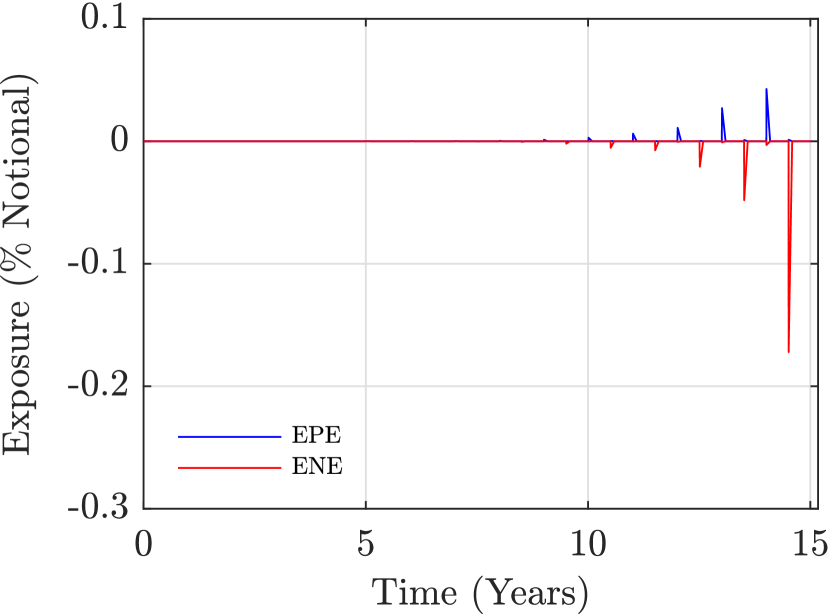

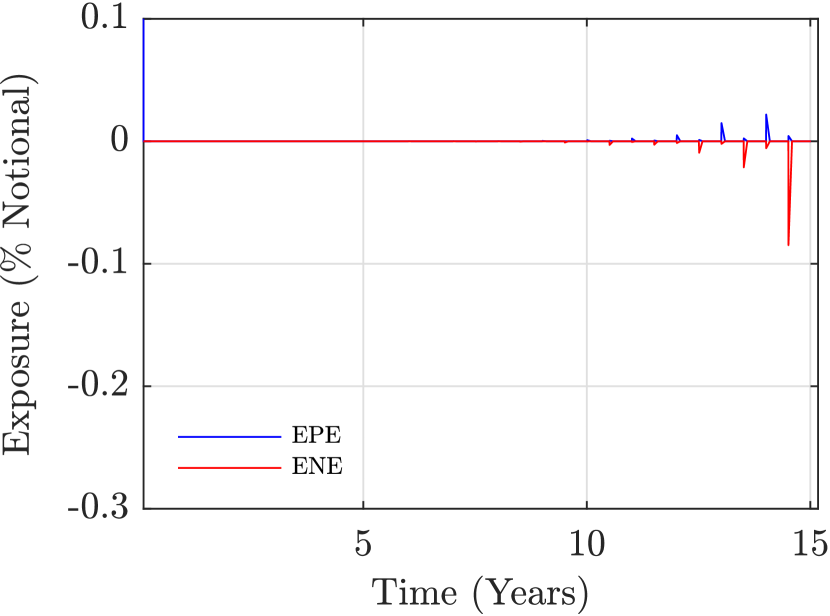

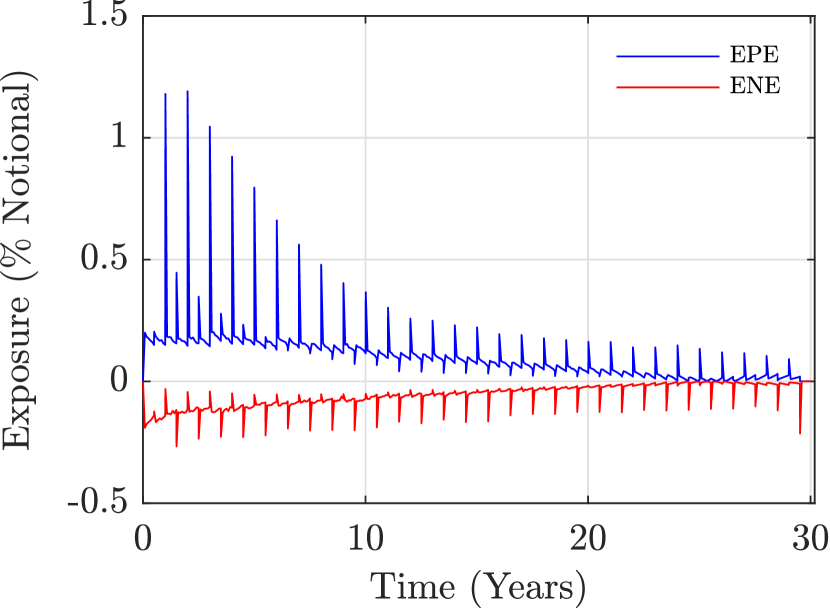

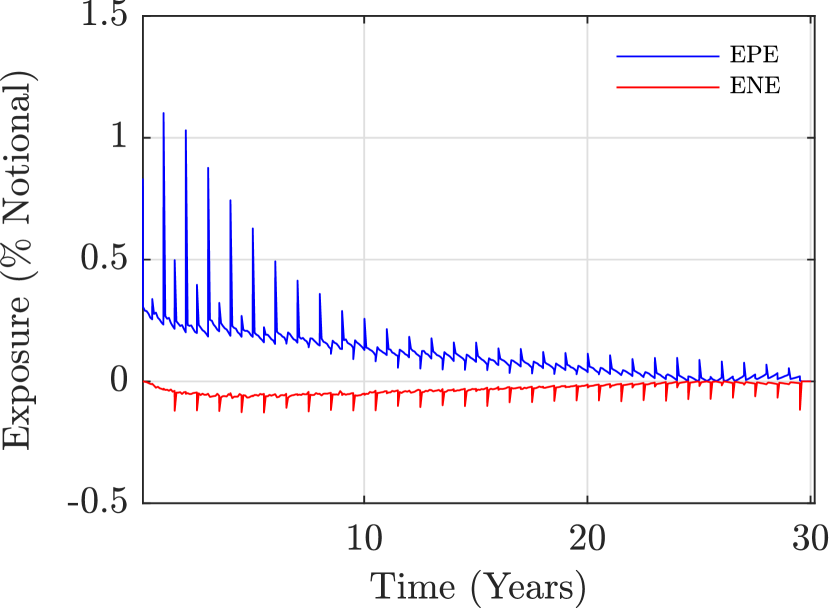

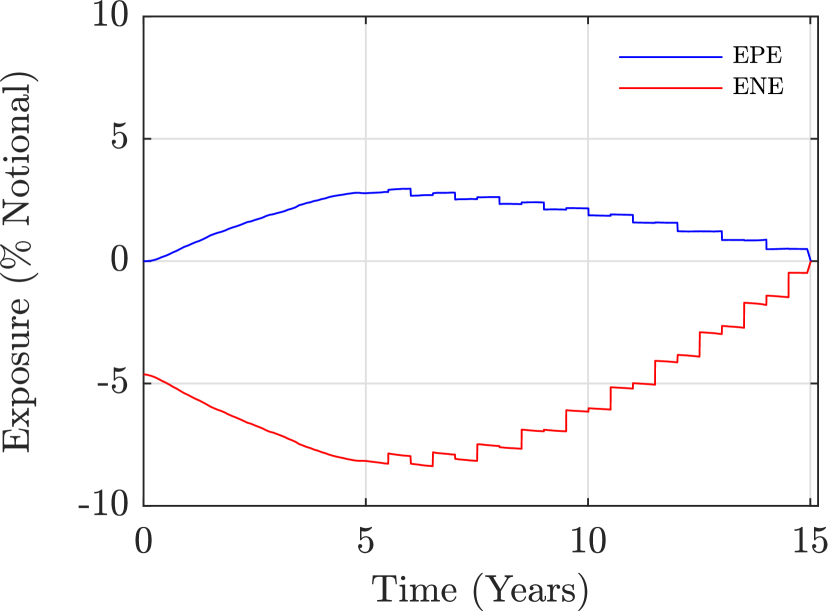

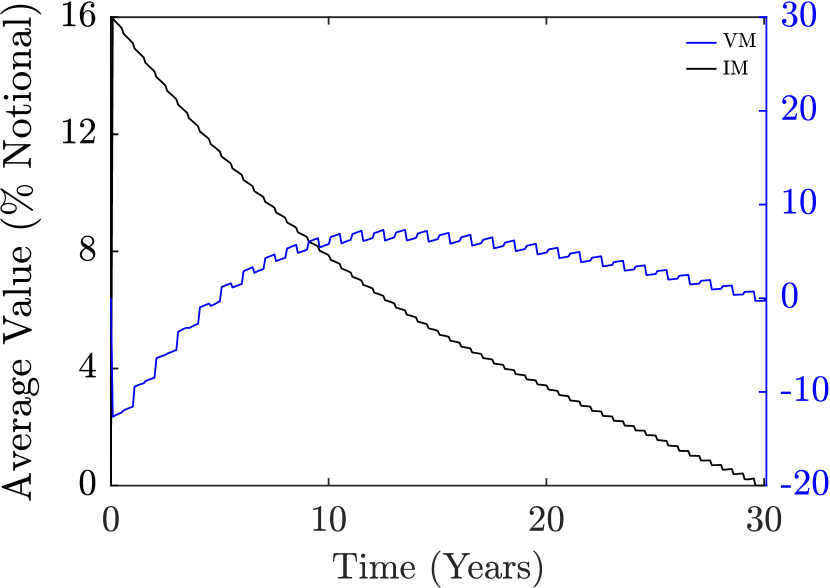

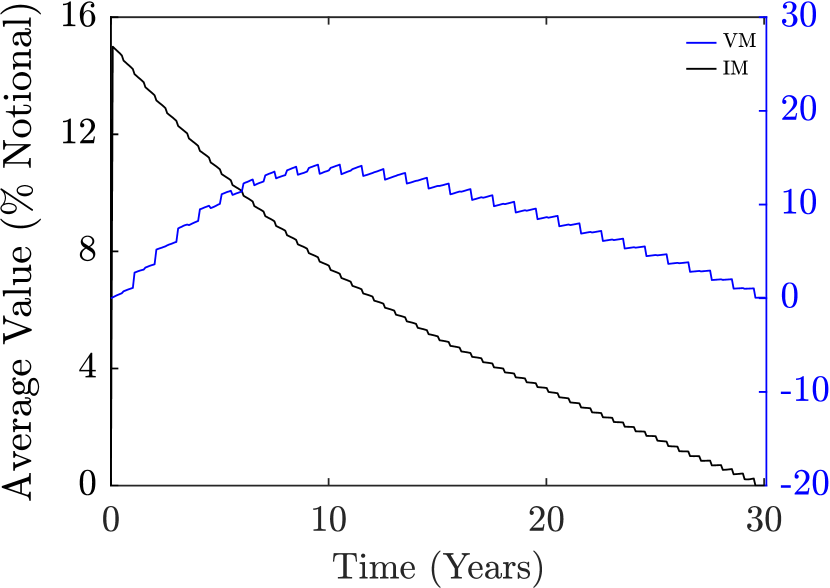

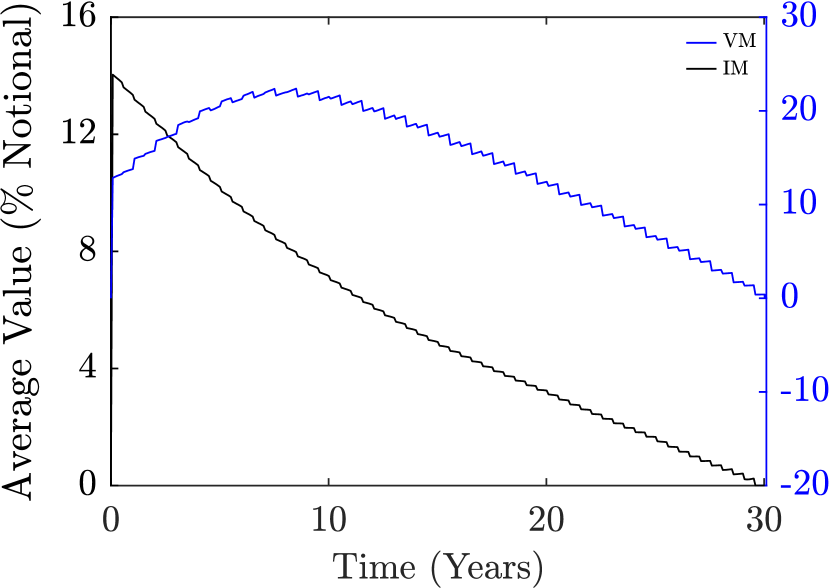

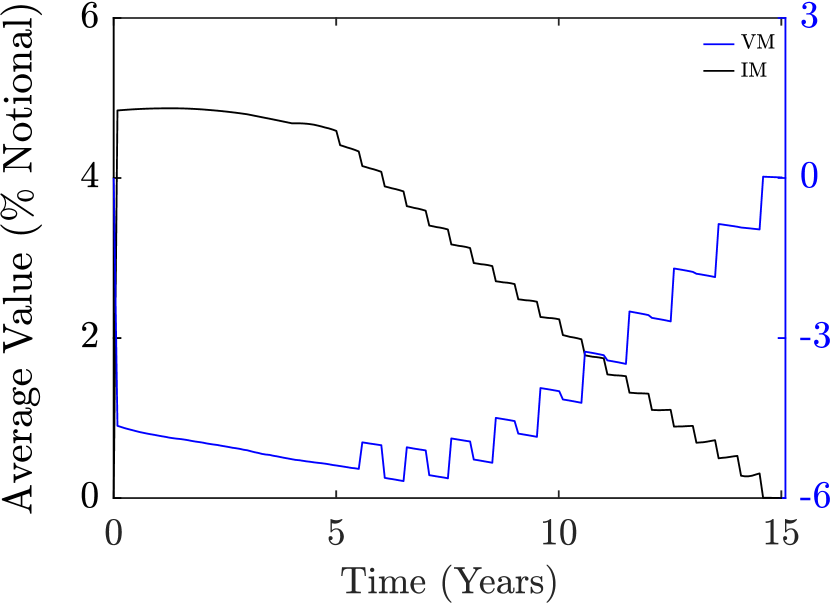

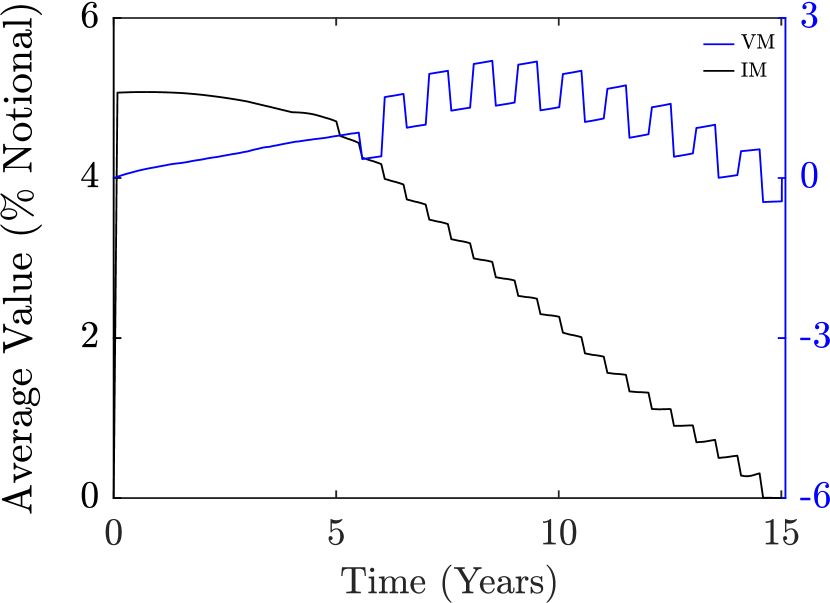

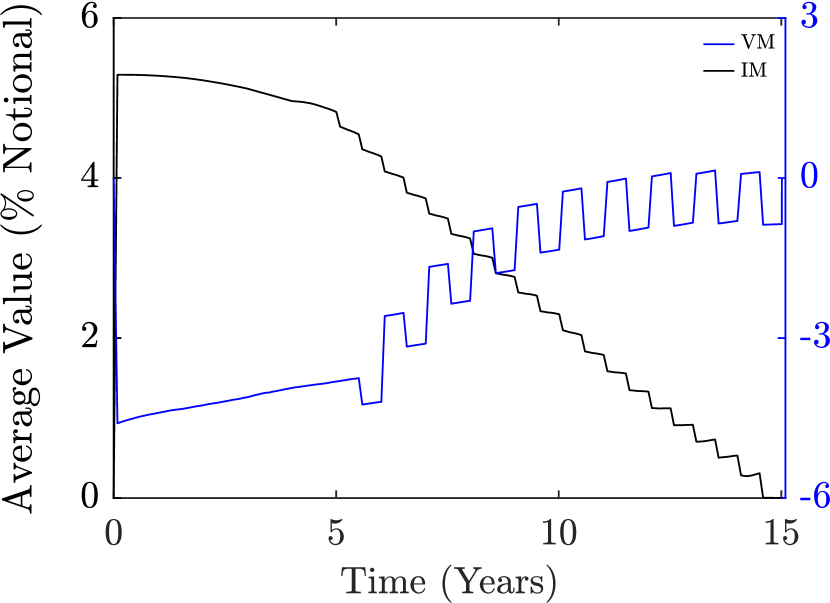

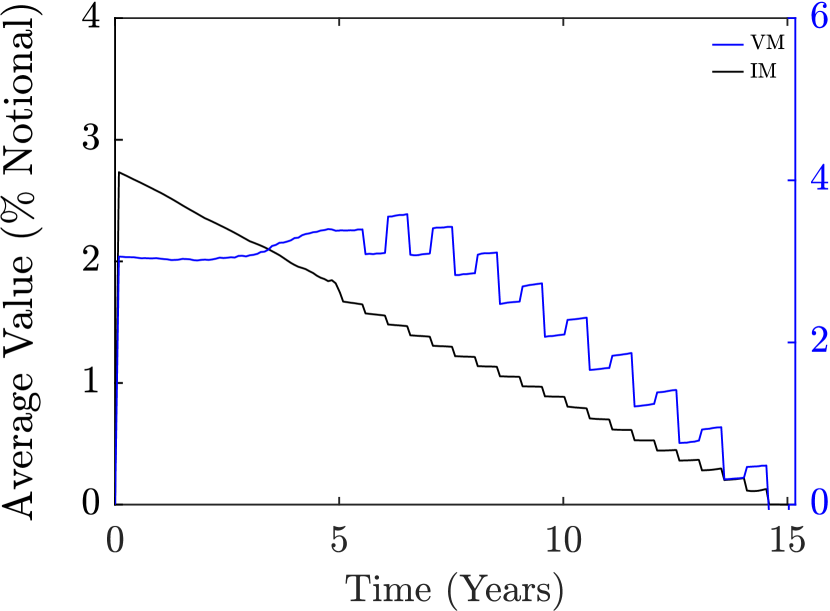

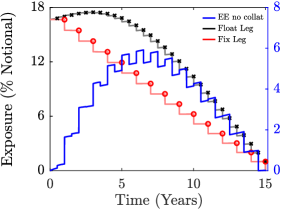

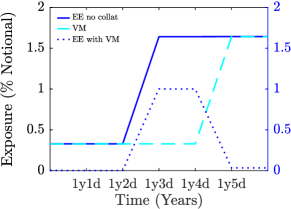

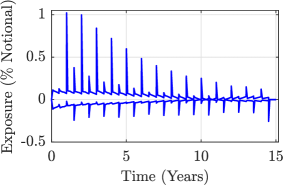

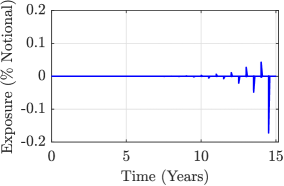

Focusing on exposures with VM and IM (bottom panels), EPE/ENE profiles display spikes with increasing magnitude approaching to maturity, which means that IM turns out to be inadequate to suppress completely the exposure due to its decreasing profile, as displayed in fig. 6.

4.3.2 XVA

The results in terms of CVA/DVA reported in tab. 3 are driven by the elements above discussed.

| Collateral | Instrument | Moneyness | CVA | DVA | |||

|---|---|---|---|---|---|---|---|

| None | 15Y Swap | OTM | 1 | ( | %) | ( | %) |

| 15Y Swap | ATM | 1 | ( | %) | ( | %) | |

| 15Y Swap | ITM | 1 | ( | %) | ( | %) | |

| 30Y Swap | OTM | 1 | ( | %) | ( | %) | |

| 30Y Swap | ATM | 1 | ( | %) | ( | %) | |

| 30Y Swap | ITM | 1 | ( | %) | ( | %) | |

| 5x10Y Fwd Swap | OTM | -1 | ( | %) | ( | %) | |

| 5x10Y Fwd Swap | ATM | 1 | ( | %) | ( | %) | |

| 5x10Y Fwd Swap | OTM | 1 | ( | %) | ( | %) | |

| 5x10Y Swaption | OTM | -1 | ( | %) | ( | %) | |

| 5x10Y Swaption | ATM | 1 | ( | %) | ( | %) | |

| 5x10Y Swaption | OTM | 1 | ( | %) | ( | %) | |

| VM | 15Y Swap | OTM | 1 | ( | %) | ( | %) |

| 15Y Swap | ATM | 1 | ( | %) | ( | %) | |

| 15Y Swap | ITM | 1 | ( | %) | ( | %) | |

| 30Y Swap | OTM | 1 | ( | %) | ( | %) | |

| 30Y Swap | ATM | 1 | ( | %) | ( | %) | |

| 30Y Swap | ITM | 1 | ( | %) | ( | %) | |

| 5x10Y Fwd Swap | OTM | -1 | ( | %) | ( | %) | |

| 5x10Y Fwd Swap | ATM | 1 | ( | %) | ( | %) | |

| 5x10Y Fwd Swap | OTM | 1 | ( | %) | ( | %) | |

| 5x10Y Swaption | OTM | -1 | ( | %) | ( | %) | |

| 5x10Y Swaption | ATM | 1 | ( | %) | ( | %) | |

| 5x10Y Swaption | OTM | 1 | ( | %) | ( | %) | |

| VM and IM | 15Y Swap | OTM | 1 | ( | %) | ( | %) |

| 15Y Swap | ATM | 1 | ( | %) | ( | %) | |

| 15Y Swap | ITM | 1 | ( | %) | ( | %) | |

| 30Y Swap | OTM | 1 | ( | %) | ( | %) | |

| 30Y Swap | ATM | 1 | ( | %) | ( | %) | |

| 30Y Swap | ITM | 1 | ( | %) | ( | %) | |

| 5x10Y Fwd Swap | OTM | -1 | ( | %) | ( | %) | |

| 5x10Y Fwd Swap | ATM | 1 | ( | %) | ( | %) | |

| 5x10Y Fwd Swap | OTM | 1 | ( | %) | ( | %) | |

| 5x10Y Swaption | OTM | -1 | ( | %) | ( | %) | |

| 5x10Y Swaption | ATM | 1 | ( | %) | ( | %) | |

| 5x10Y Swaption | OTM | 1 | ( | %) | ( | %) | |

Focusing on uncollateralized CVA/DVA, Swaps display larger CVA (DVA) figures for ITM (OTM) instruments due to the greater probability to observe positive (negative) mark to futures, also reflected in lower Monte Carlo errors. Moreover, CVA is larger than DVA except for the OTM 15 years Swap due to the simulated forward rates structure discussed above. Finally, analysing the results for different maturities, the higher risk of 30 years Swaps leads to larger adjustments compared to those maturing in 15 years. Analogous results are obtained for Forward Swaps. In this case, the asymmetric effect of simulated forward rates on opposite transactions causes larger CVA and smaller DVA for the OTM payer Forward Swap with respect to the OTM receiver one. Slightly lower (absolute) CVA values are observed for the corresponding physically settled European Swaptions since OTM paths are excluded after the exercise, while DVA values are considerably lower as negative exposure exists only after the expiry.

Focusing on CVA/DVA with VM only, the results show that the adjustments are reduced on average by approx. two orders of magnitude. In this case CVA/DVA are widely driven by spikes in exposure profiles which determine changes in certain relations previously identified. In particular, the 30 years OTM Swap displays greater DVA compared to CVA since ENE is larger than EPE between the spikes and their magnitude becomes larger for ENE by approaching the maturity (where default probability increases). The same can be observed for the 5x10 years ATM Forward Swap.

Focusing on CVA/DVA with VM and IM, the results show that the adjustments are reduced on average by approx. four orders of magnitude with respect to uncollateralized case. CVA/DVA are entirely due to the spikes closest to maturity which are not fully suppressed by IM. Largest DVA compared to CVA are observed for payer instruments for which wide spikes are observed in ENE as the difference between fixed rate and floating rate are greater. For the same reason receiver instruments display larger CVA figures.

5 Model Validation

Previous sections suggest that the numerical calculation of CVA/DVA requires various assumptions for modelling and computing the relevant quantities. Since affecting the stability of the results, these assumptions are source of model risk to be properly addressed.

The purpose of this section is twofold: on the one hand, we want to validate the framework adopted in sec. 4 by assessing its robustness and selecting a parameterization which optimizes the trade-off between accuracy and performance, on the other hand, we want to identify the most significant sources of model risk involved in exposure modelling and hence CVA/DVA calculation.

To ease the presentation we report the results only for a subset of the instruments in tab. 1, mainly the 15 years ATM payer Swap and the 5x10 years ATM physically settled European payer Swaption. Analogous results are obtained for the other instruments.

5.1 Time Grid Construction

The numerical solution of eqs. 2.29 and 2.30 involves the discretization of the integral along a grid of valuation dates in correspondence of which the exposure is computed. In selecting the length of time steps it is necessary to optimize the trade-off between precision and computational effort. In fact, an high granularity reduces the discretization error but makes the calculation unfeasible due to long time required. Furthermore, the inclusion in the model of the MPoR requires to discretize the aforementioned equations in such a way to capture all periodical spikes in Swap’s collateralized exposure which have material impact on CVA/DVA.

In this section we first analyse the nature of spikes in collateralized exposure when a daily grid is used and their impact on CVA/DVA. We then propose a possible workaround which allows to capture all spikes at lower granularities, at the end we report the results of a convergence analysis aimed at finding a granularity which ensures a good compromise between precision and computational time.

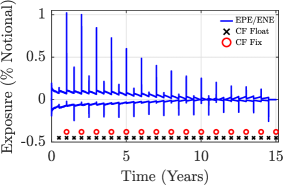

5.1.1 Spikes Analysis

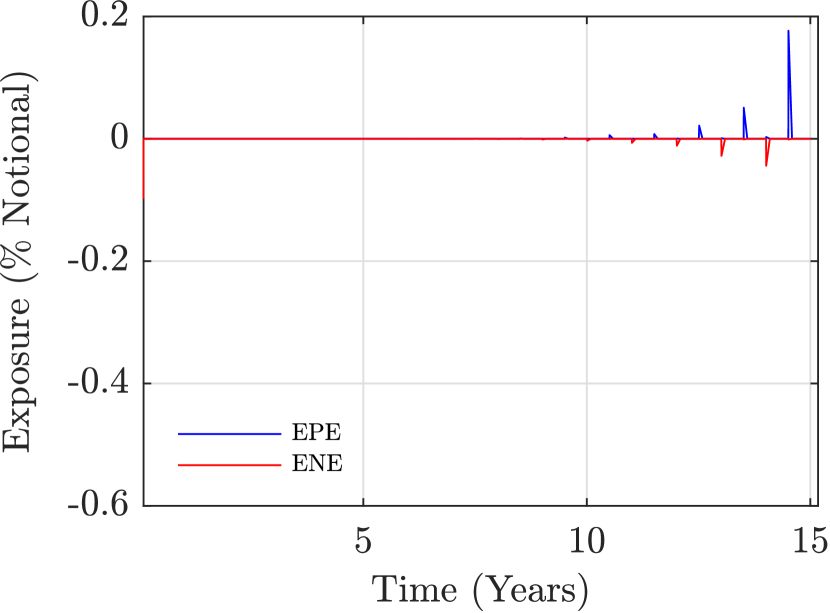

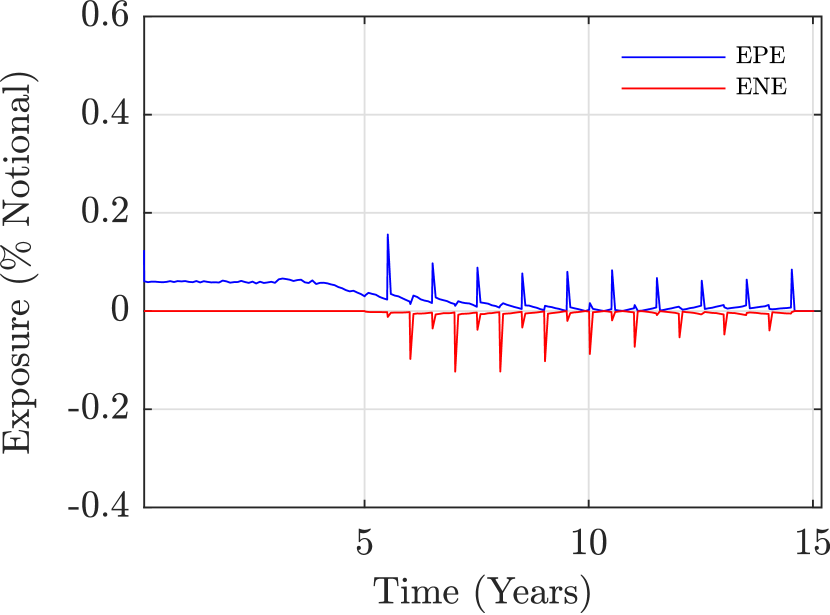

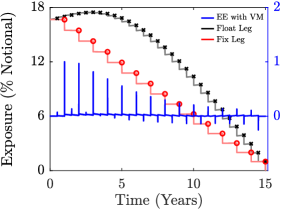

Spikes arising in collateralized exposure are due to the MPoR since it implies that the collateral available at time step depends on instrument’s mark to future at time step , assumed to be the last date for which VM and IM were fully posted (see sec. 3.1). The granularity of the time grid used to discretize the integrals in eqs. 2.29 and 2.30 determines the existence of spikes in collateralized exposure profile, in fact a time grid with daily granularity is able to capture all spikes as shown in fig. 7, which displays EPE/ENE profiles for the 15 years ATM payer Swap (left-hand side panel) and the 5x10 years ATM physically settled European payer Swaption (right-hand side panel) for the three collateralization schemes considered.

As can be seen, when only VM is considered, spikes emerge at inception as no collateral is posted, and at coupon dates as sudden changes in mark to future are captured by VM with a delay due to MPoR. When also IM is considered, spikes closest to maturity persist due to the downward profile of IM.

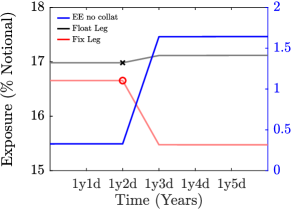

We further investigated the nature of these spikes by focusing on the 15 years ATM payer Swap’s Expected Exposure (EE)171717The Expected Exposure (EE) is defined as: . without collateral and with VM, displayed in fig. 8.

Left-hand side panels show that both the jagged shape of uncollalteralized EE (fig. 8(a)) and the spikes in EE with VM (fig. 8(b)) are determined by sudden changes in the average values of Swap legs right after coupon payments.

Right-hand side panels show a focus around y, when both fixed and floating coupons take place: after these cash flows, the average value of floating leg increases and fixed leg one decreases, resulting in a positive jump in uncollateralized EE at 1y3d (fig. 8(c)). This jump is captured by VM at 1y5d, this delay of 2 days due to MPoR causes an upward spike in EE with VM (fig. 8(d)). The direction and magnitude depend on the simulated forward rates structure and on whether fixed or floating coupon payments take place.

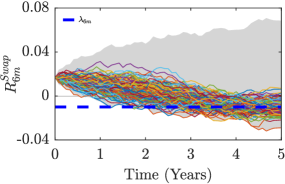

Focusing on semiannual floating coupons paid by C, two different behaviours can be observed during the lifetime of the Swap. The first three floating coupons determine positive jumps in uncollateralized EE and upward spikes in EE with VM. This is due to the fact that the simulated forward rates are on average negative until 2.5 years implying that, until that time, these coupons are actually paid by B. Once forward rates revert to positive values, negative jumps in uncollateralized EE and downward spikes in EE with VM arise in correspondence of the remaining floating coupons (figs. 8(a) and 8(b)).

When also annual fixed coupons paid by B take place, positive jumps in uncollateralized EE and upward spikes with decreasing magnitude in EE with VM can be observed. Negative rates cause wide spikes in correspondence of the first two fixed and floating coupons due to the simultaneous increase in the average value of floating leg and decrease in the fixed leg one, in B’s perspective, right after coupons payment (figs. 8(c) and 8(d)).

The impact of spikes on total CVA and DVA is significant: with only VM the contribution is respectively of and for the 15 years ATM payer Swap and of and for the 5x10 years ATM physically settled European payer Swaption. With also IM the exposure between spikes is suppressed, therefore CVA and DVA are completely attributable to spikes.

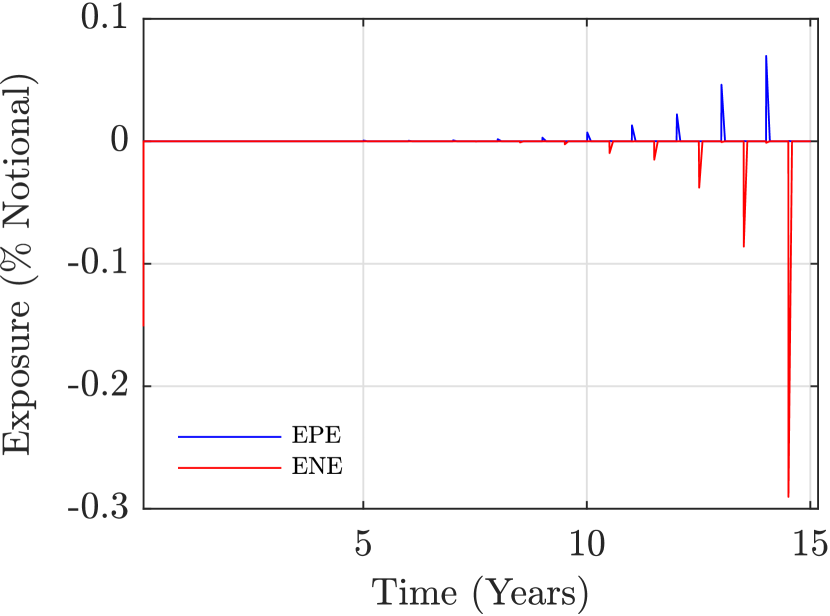

5.1.2 Parsimonious Time Grid

Although a daily grid represents the best discrete approximation of the integrals in eqs. 2.29 and 2.30, it is very limited in terms of computational time required, as can be seen from the last column of tab. 4. The most time consuming component is represented by IM which involves the calculation of several forward sensitivities for each path (see sec. 3.3.2). Computational time lengthens further for Swaptions due to the numerical resolution of G2++ pricing formula (see eq. B.12). The calculation of CVA/DVA using a daily grid is clearly unfeasible, this forced us to consider a lower granularity.

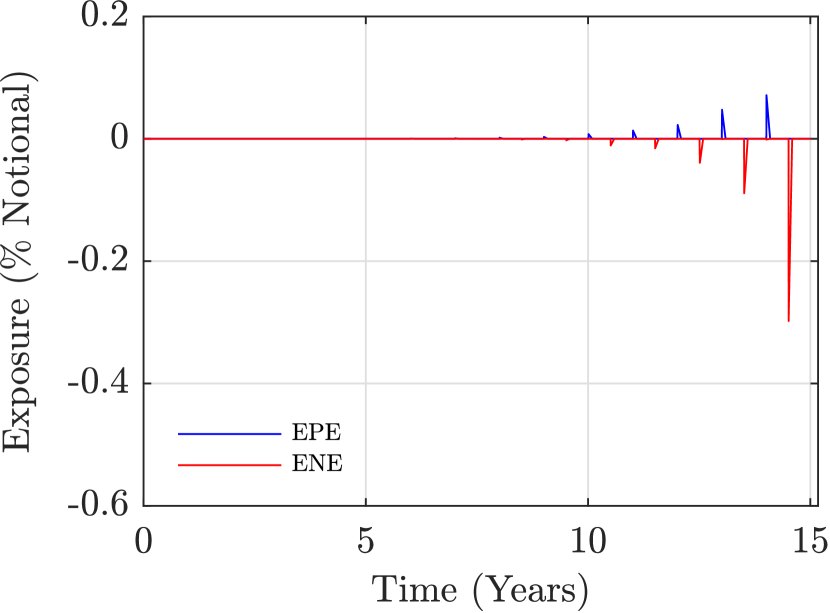

A standard less granular evenly spaced time grid may produce biased CVA/DVA values if not capable of capturing all spikes in collateralized exposure. In fact, the spike due to the coupon occurring at time would emerge only if the time grid includes a point falling within the interval . A possible workaround to make sure to capture all spikes could be to add to a standard time grid the set of points , where is the -th floating coupon date and is the number of floating coupons181818For the instruments considered, fixed coupon dates are a subset of floating ones since taking place at the same time, otherwise the corresponding coupon dates should have been added to the time grid.; we will refer to this augmented grid as the joint grid. The comparison between EPE/ENE for the 15 years ATM payer Swap, obtained through standard and joint grids with monthly granularity for the three collateralization schemes considered, is shown in fig. 9. The 5x10 years ATM physically settled European payer Swaption displays same results and is not reported.

As can be seen, uncollateralized exposure is similar for both grids, while standard grid fails to capture spikes in collateralized exposure since no time point within the interval is included for each coupon date . Moreover, with no spikes, IM suppresses completely the residual exposure resulting in null CVA/DVA. Instead, all spikes are captured by the joint grid which allows to correctly model the collateralized exposure with considerable time-saving benefits.

With the aim to optimize the trade-off between precision and computation time, we investigated CVA/DVA convergence with respect to different granularities for the joint grid, setting the results obtained with the daily grid as benchmark. In particular, we considered monthly, quarterly, semiannual and annual time steps. The results for the 15 years ATM payer Swap and the 5x10 years ATM physically settled European payer Swaption, for the three collateralization schemes considered are reported in tab. 4.

| Instrument | Collateral | CVA | DVA | Time (min) | |||

|---|---|---|---|---|---|---|---|

| 12M | ( | %) | ( | %) | |||

| 6M | ( | %) | ( | %) | |||

| None | 3M | ( | %) | ( | %) | ||

| 1M | ( | %) | ( | %) | |||

| 1D | ( | %) | ( | %) | |||

| 12M | ( | %) | ( | %) | |||

| 6M | ( | %) | ( | %) | |||

| Swap | VM | 3M | ( | %) | ( | %) | |

| 1M | ( | %) | ( | %) | |||

| 1D | ( | %) | ( | %) | |||

| 12M | ( | %) | ( | %) | |||

| 6M | ( | %) | ( | %) | |||

| VM and IM | 3M | ( | %) | ( | %) | ||

| 1M | ( | %) | ( | %) | |||

| 1D | ( | %) | ( | %) | |||

| 12M | ( | %) | ( | %) | |||

| 6M | ( | %) | ( | %) | |||

| None | 3M | ( | %) | ( | %) | ||

| 1M | ( | %) | ( | %) | |||

| 1D | ( | %) | ( | %) | |||

| 12M | ( | %) | ( | %) | |||

| 6M | ( | %) | ( | %) | |||

| Swaption | VM | 3M | ( | %) | ( | %) | |

| 1M | ( | %) | ( | %) | |||

| 1D | ( | %) | ( | %) | |||

| 12M | ( | %) | ( | %) | |||

| 6M | ( | %) | ( | %) | |||

| VM and IM | 3M | ( | %) | ( | %) | ||

| 1M | ( | %) | ( | %) | |||

| 1D | ( | %) | ( | %) | |||

For uncollateralized case, CVA and DVA converge for both instruments at low granularities, i.e. M. In case of collateralization, reliable results are obtained with M. Focusing on performance, a monthly grid allows on average a 95% reduction in computational time compared to a daily grid. In light of this analysis we set M since offering a good compromise between accuracy and performance.

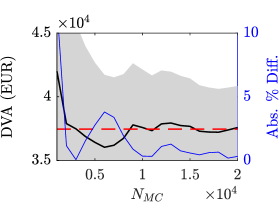

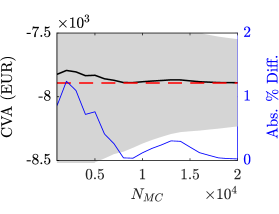

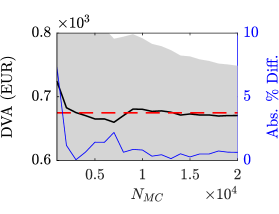

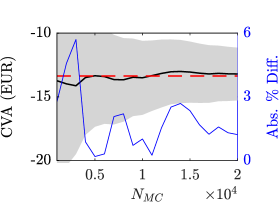

5.2 XVA Monte Carlo Convergence

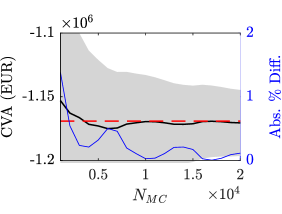

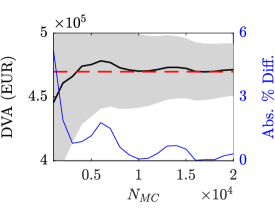

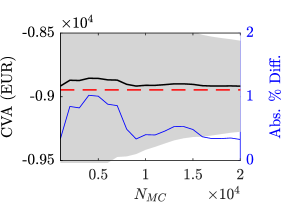

Monte Carlo method for quantifying EPE/ENE in eq. 2.33, although the most complex and computational intensive approach, allows to easily cope with the complexities inherent XVA calculation such as collateralization. Also in this case it is necessary to avoid unnecessary workloads by selecting a number of paths that optimizes the trade-off between precision and computational time. For this reason we investigated CVA/DVA convergence with respect to the number of simulated scenarios.

In this analysis we assumed CVA/DVA calculated with as proxies for “exact” values to be used as benchmark and assessed the convergence by computing CVA/DVA with a smaller number of scenarios using the same seed. Furthermore, in order to investigate Monte Carlo error we built for each time step the following upper and lower bounds on EPE/ENE

| (5.1) | ||||

| (5.2) |

with

| (5.3) |

Therefore, we used these quantities to get the following confidence interval for CVA/DVA

| (5.4) | ||||

| (5.5) |

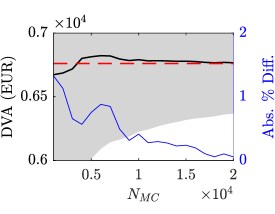

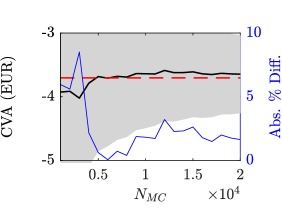

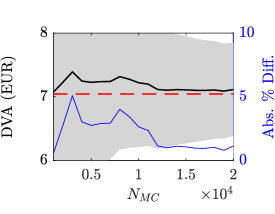

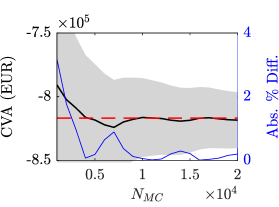

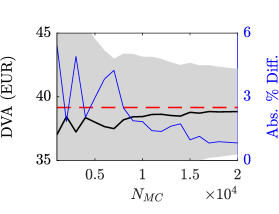

Figs. 10 and 11 display convergence diagrams of CVA (left-hand side) and DVA (right-hand side) showing the dependence of Monte Carlo error upon the number of simulated scenarios for the 15 years ATM payer Swap and the 5x10 years ATM physically settled European payer Swaption respectively, for the three collateralization schemes considered. Furthermore, we show the convergence rate in terms of absolute percentage difference with respect to “exact” value proxies. As can be seen, for both instruments CVA/DVA converge to “exact” values proxies for all collateralization schemes, with small absolute percentage differences even for few paths (i.e. ). Higher differences can be observed for VM and IM case (bottom panels) due to small CVA/DVA values; nevertheless, ensures an absolute percentage difference below the 5% for the Swap and 6% for the Swaption. As regards computational time, since it scales linearly with the number of simulated paths, with the benefits in terms of precision would be exceeded by the costs in terms of time required for the calculation, particularly for IM. In light of this, we set since offering a good compromise between accuracy and performance.

5.3 Forward Vega Sensitivity Calculation

In this section we report the analyses conducted to validate the approach adopted for calculating Vega sensitivity when simulating ISDA-SIMM dynamic IM. The results are shown for the 5x10 years ATM physically settled European payer Swaption, same considerations apply to the other Swaptions in tab. 1.

5.3.1 Shocks on G2++ Parameters

ISDA defines Vega sensitivity as the price change with respect to a 1% shift up in ATM Black implied volatility. Since G2++ European Swaption pricing formula does not provide for an explicit dependence on Black implied volatility (see eq. B.12), Vega cannot be calculated according to ISDA definition for future time steps.

The approximation proposed in sec. 3.3.2 allows to calculate forward Vega by shifting up G2++ model parameters governing the underlying process volatility.

In order validate this approach we compared Vega obtained at time step (i.e. valuation date) through eq. 3.15 with a “market” Vega and a “model” Vega, both consistent with ISDA prescriptions.

Specifically, for the 5x10 years ATM physically settled European payer Swaption we computed the following three Vega sensitivities

| (5.6) | ||||

| (5.7) | ||||

| (5.8) |

where denotes “market” Vega obtained by shifting up ATM Black implied volatility quote by 1% and re-pricing the Swaption via Black pricing formula; denotes “model” Vega obtained by shifting up the ATM Black implied volatility matrix by 1%, re-pricing market Swaptions via Black pricing formula, re-calibrating G2++ parameters on these prices, and computing the price of the Swaption using re-calibrated parameters . denotes Vega obtained according to the approximation outlined in sec. 3.3.2, i.e. by applying the shocks and on G2++ parameters governing the underlying process volatility and computing Black implied volatilities by inverting Black pricing formula.

| Approach | G2++ parameters | VR | |||

|---|---|---|---|---|---|

| eq. 5.6 | None | ||||

| eq. 5.7 | |||||

| eq. 5.8 | |||||

In addition, we tested eq. 5.8 for different values of and , considering both and . In the latter case, we recovered shocks values from the re-calibrated parameters and of eq. 5.7, which correspond respectively to and . The results of the comparison are reported in tab. 5. As can be seen, Vega sensitivities are aligned among the three approaches and the different shocks values examined. This means that at time step the approximation proposed produces Vega sensitivity and Vega Risk191919Vega Risk is the product between Vega sensitivity and Black implied volatility (see eq. C.8). values consistent with those obtained by applying ISDA definition, therefore we assumed that it can be adopted also for future time steps. As regards the choice of shocks sizes, in order to avoid any arbitrary elements, we computed forward Vega by using the re-calibrated and , corresponding to and .

5.3.2 Implied Volatility Calculation

When performing time simulation it may happen that for some extreme paths the value of the Black shift observed at time step results to be too small to retrieve positive Swap rates in future time steps avoiding Black formula inversion (see fig. 12).

In order to ensure Vega sensitivity calculation for each time step and path, we propose to consider Black shift values larger than those observed on the market at time step . To this end, we analysed the impact of different Black shift values on Black implied volatility, Vega sensitivity and Vega Risk. The results for the 5x10 years ATM physically settled European payer Swaption are reported in tab. 6.

| VR | |||

|---|---|---|---|

As can be seen, although a large impact on Black implied volatility and Vega sensitivity, the impact on Vega Risk is negligible as it is given by the product of the two quantities (see eq. C.8). More in detail, compared to the value observed at time step , i.e. , the various Black shifts considered produce Vega Risk values differing up to a maximum of 2%. This leads us to conclude that values larger than those observed at ensure the inversion of the Black formula for each path with an acceptable loss of accuracy in Vega Risk. For this reason we set .

5.4 XVA Sensitivities to CSA Parameters

The aim of this section is to analyse the impacts of CSA parameters on XVA figures by assessing if collateralized CVA/DVA converges to uncollateralized ones for increasing values of threshold K and minimum transfer amount MTA, keeping other model parameters as in tab. 2.

The results with respect to the length of MPoR are not reported since no significant impacts were found.

In carrying out the analysis we distinguished between the following three collateralization schemes:

-

1.

CVA/DVA with VM only;

-

2.

CVA/DVA with VM and IM, with K and MTA applied on VM only;

-

3.

CVA/DVA with VM and IM, with K and MTA applied on both VM and IM.

Convergence diagrams for the 15 years ATM payer Swap are shown in figs. 13

and 14.

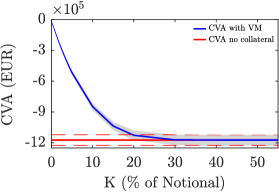

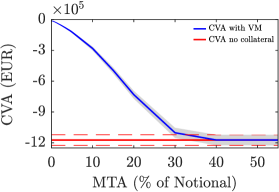

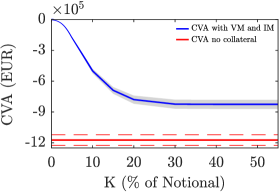

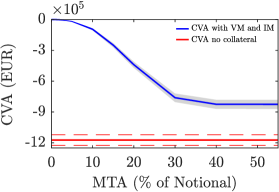

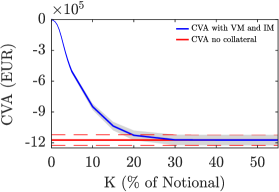

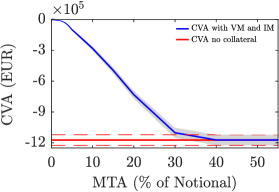

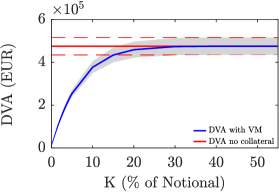

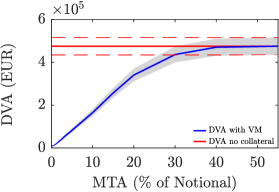

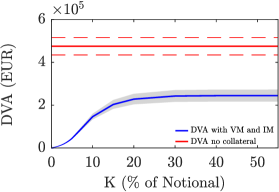

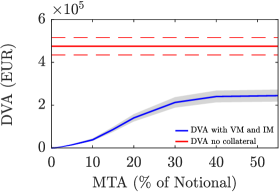

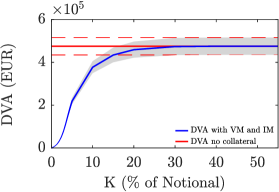

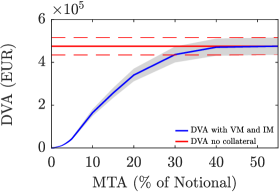

In particular, left-hand side panels show CVA/DVA convergence with respect to K, with EUR and days; conversely, right-hand side panels show the convergence with respect to MTA, with EUR and days. As can be seen, case 1. (top panels) and case 3. (bottom panels) display similar results except for small values of K and MTA, thus IM is ineffective when significant frictions are considered. Instead, case 2. (middle panels) displays collateralized CVA/DVA not converging to uncollateralized ones, this means that without frictions IM is effective in reducing residual credit exposure. Furthermore, the results suggest that K leads to a faster convergence to uncollateralized figures compared to MTA; e.g. in case 1. Mio EUR leads to an increase in absolute terms of approx. 5700% in CVA and 3600% in DVA with respect to the reference case (see tab. 2), while Mio EUR leads to an increase of approx. 1300% in CVA and 1100% in DVA. As expected, K introduces an higher degree of friction since determining the maximum amount of allowed unsecured exposure; on the other hand, MTA governs only the minimum amount for each margin call, therefore significant impacts can be observed only for large values (see eqs. 3.2 and 3.8). The 5x10 years ATM physically settled European payer Swaption displays same results and is not reported.

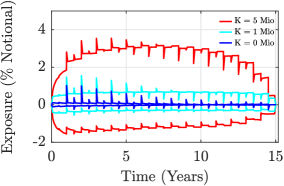

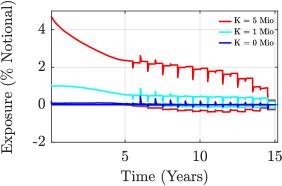

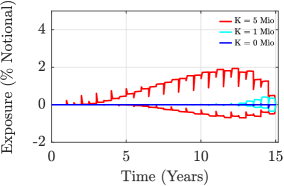

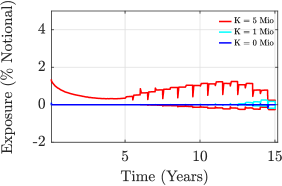

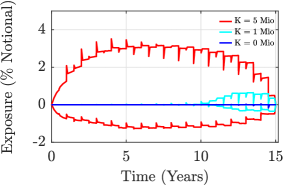

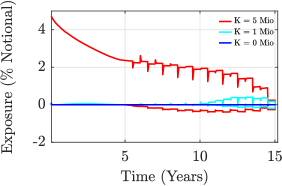

A focus on the effects of K on collateralized exposure is shown in fig. 15, which displays EPE/ENE for the 15 years Swap (left-hand side panels) and the 5x10 years ATM physically settled European payer Swaption (right-hand side panels) for the three collateralization schemes above, for different values of K (with EUR and days).

Focusing on the Swap with VM (top panel), the average EPE (ENE) over the time steps, expressed as a percentage of the notional, is equal to , and (, and ), respectively for threshold values of 0, 1 and 5 EUR Mio. By adding IM with no threshold (middle panel), large part of residual exposure is suppressed: average EPE (ENE) is equal to , and (, and ) of the notional. By considering threshold also on IM (bottom panel), average EPE (ENE) is equal to , and (, and ) of the notional meaning that, as K increases, IM looses its effectiveness and EPE/ENE approach to those with only VM.

5.5 Monte Carlo Versus Analytical XVA

In sec. 2.4.3 we have shown that analytical solutions for eqs. 2.29 and 2.30 are available for uncollateralized Swaps. In particular, CVA and DVA of a payer (receiver) Swap can be represented as an integral over the values of a strip of co-terminal European payer (receiver) Swaptions and European receiver (payer) Swaptions respectively (see eqs. 2.35 and 2.36).

| Item | Analytical G2++ | Analytical Black | MC | ||

|---|---|---|---|---|---|

| CVA ATM Swap | 12M | * | ( | %) | |

| 6M | * | ( | %) | ||

| 3M | * | ( | %) | ||

| 1M | * | ( | %) | ||

| 1D | * | ( | %) | ||

| DVA ATM Swap | 12M | * | ( | %) | |

| 6M | * | * | ( | %) | |

| 3M | * | * | ( | %) | |

| 1M | * | * | ( | %) | |

| 1D | * | * | ( | %) | |

| CVA OTM Swap | 12M | * | * | ( | %) |

| 6M | * | ( | %) | ||

| 3M | * | ( | %) | ||

| 1M | * | ( | %) | ||

| 1D | * | ( | %) | ||

| DVA OTM Swap | 12M | ( | %) | ||

| 6M | * | * | ( | %) | |

| 3M | * | * | ( | %) | |

| 1M | * | * | ( | %) | |

| 1D | * | * | ( | %) | |

The numerical solution of eqs. 2.35 and 2.36 involves the discretization of the integrals on a grid of time points (see eqs. 2.37 and 2.38), with impacts in terms of precision of the results related to its granularity. Therefore, as for Monte Carlo model, we tested analytical formulas for different time steps frequencies. Moreover, given the model independent nature of this approach, we calculated Swaptions prices through both G2++ and Black formulas. The purpose is twofold: one one hand we want to test the results of the Monte Carlo approach, on the other hand we want to quantify the model risk stemming from the use of two alternative pricing formulas. More in detail, we calculated G2++ Swaptions prices by applying eq. B.12 and G2++ parameters in tab. 2. Regarding Black pricing formula, the most complex step regards the determination of implied volatility for the strip of co-terminal Swaptions. Starting from market Swaptions prices cube, we calibrated SABR parameters (see [43]) on each smile section (i.e. tenor-expiry combination) obtaining a SABR parameters cube; hence, we determined the implied volatility for each co-terminal Swaption using the SABR approximated closed formula linearly interpolating/extrapolating on calibrated parameters cube in correspondence of the tenor-expiry combination of each co-terminal Swaption.

The analysis has been carried out considering the 15 years ATM payer Swap and the 15 years OTM payer Swap. The results shown in tab. 7 suggest that, with respect to Monte Carlo approach (last column), analytical formulas underestimate CVA and DVA values in absolute terms. Moreover, the results obtained with analytical G2++ (third column) are always included in Monte Carlo error (marked with an asterisk), with the only exception represented by the DVA of the OTM Swap with annual time grid granularity, to confirm the robustness of the results of the Monte Carlo model. As regards the results obtained with a different dynamic (fourth column), considerable differences are observed, particularly in CVA which is included in Monte Carlo error only in one case, to demonstrate that a not negligible model risk exists. In terms of computational performance, the advantage of the analytical approach is several orders of magnitude greater than that of Monte Carlo approach: with a daily grid robust results can be obtained in only 1 minute, meaning that, for an uncollateralized Swap, the analytical approach can replace the Monte Carlo approach whereas performance is critical.

5.6 XVA Model Risk

According to the Regulation (EU) No 575/2013 (see [34]), financial institutions are required to apply prudent valuation to fair-valued positions (Art. 105). For prudent valuation is meant the calculation of specific Additional Valuation Adjustments (AVA), to be deducted from the Common Equity Tier 1 (CET1) capital (Art. 34), necessary to adjust the fair-value of a financial instrument in order to achieve a prudent value with an appropriate degree of certainty.

The prudent value has to be computed considering the valuation risk factors listed in Art. 105 (par. 10-11) in order to mitigate the risk of losses deriving from the valuation uncertainty of the exit price of a financial instrument.

These valuation risk factors are linked to the corresponding AVA described in the Commission Delegated Regulation (EU) 2016/101 (see [35]), where the degree of certainty is set at 90%.

In particular, the Model Risk (MoRi) AVA is envisaged in Art. 11 of [35] and comprises the valuation uncertainty linked to the potential existence of a range of different models or model calibrations used by market participants.

This may occur e.g. when a unique model recognized as a clear market standard for computing the price of a certain financial instrument does not exist, or when a model allows for different parameterizations or numerical solution algorithms. Accordingly, for MoRi AVA the prudent value at a 90% confidence level corresponds to the 10th percentile of the distribution of the plausible prices obtained from different models/parameterizations202020Notice that we conventionally adopt positive/negative prices for assets/liabilities..

In this section we apply this framework to XVA by calculating a MoRi AVA based on the different models and parameterizations discussed in the sections above. In particular, we computed MoRi AVA at time starting from the following definition and avoiding the aggregation coefficient

| (5.9) |

where:

-

-

is the fair-value of the instrument, intended as the price obtained from the target XVA framework , i.e. the model and the corresponding parameters which optimizes the trade-off between accuracy and performance (as reported in tab. 2);

-

-

is the prudent value obtained from the alternative XVA framework , which produces the price corresponding to the 10th percentile of the prices distribution obtained from the set of XVA frameworks. In other words, ensures that one can exit the position at a price equal to or larger than with a degree of certainty equal to or larger than 90%212121Notice that, according to our conventions, ..

In light of this, and since we are not considering the valuation uncertainty related to the base value , eq. 5.9 becomes

| (5.10) |

We built the XVA distribution by leveraging on the outcomes of the analyses described in the sections above. In particular, we considered XVA obtained from both standard and joint grids with different granularities (see sec. 5.1), different numbers of simulated paths (see sec. 5.2), and analytical approach for uncollateralized Swaps with different time steps frequencies and pricing formulas for the strip of co-terminal Swaptions (see sec. 5.5).

We report in tabs. 8 and 9 the XVA distributions for the uncollateralized 15 years ATM payer Swap and for the uncollateralized 5x10 years ATM physically settled European payer Swaption, respectively. Similar results were obtained for the other collateralization schemes.

| XVA framework | |||||||

| Model | Parameters | CVA | DVA | XVA | |||

| Time grid | |||||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | ** | ||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1D | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | * | ||||

| MC | Joint | 1M | |||||

| MC | Standard | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 3M | |||||

| MC | Standard | 3M | |||||

| MC | Joint | 6M | |||||

| MC | Standard | 6M | |||||

| Analytical G2++ | Standard | 1D | NA | ||||

| Analytical G2++ | Standard | 6M | NA | ||||

| Analytical G2++ | Standard | 1M | NA | ||||

| Analytical G2++ | Standard | 3M | NA | ||||

| Analytical G2++ | Standard | 12M | NA | ||||

| MC | Joint | 12M | |||||

| MC | Standard | 12M | |||||

| Analytical Black | Standard | 6M | NA | ||||

| Analytical Black | Standard | 1D | NA | ||||

| Analytical Black | Standard | 1M | NA | ||||

| Analytical Black | Standard | 3M | NA | ||||

| Analytical Black | Standard | 12M | NA | ||||

| XVA | |||||||

| XVA | |||||||

| AVA | |||||||

| XVA framework | |||||||

| Model | Parameters | CVA | DVA | XVA | |||

| Time grid | |||||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | ** | ||||

| MC | Joint | 1D | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | * | ||||

| MC | Standard | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 3M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Standard | 3M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||

| MC | Joint | 1M | |||||