Learning Hard Optimization Problems:

A Data Generation Perspective

Abstract

Optimization problems are ubiquitous in our societies and are present in almost every segment of the economy. Most of these optimization problems are NP-hard and computationally demanding, often requiring approximate solutions for large-scale instances. Machine learning frameworks that learn to approximate solutions to such hard optimization problems are a potentially promising avenue to address these difficulties, particularly when many closely related problem instances must be solved repeatedly. Supervised learning frameworks can train a model using the outputs of pre-solved instances. However, when the outputs are themselves approximations, when the optimization problem has symmetric solutions, and/or when the solver uses randomization, solutions to closely related instances may exhibit large differences and the learning task can become inherently more difficult. This paper demonstrates this critical challenge, connects the volatility of the training data to the ability of a model to approximate it, and proposes a method for producing (exact or approximate) solutions to optimization problems that are more amenable to supervised learning tasks. The effectiveness of the method is tested on hard non-linear nonconvex and discrete combinatorial problems.

1 Introduction

Constrained optimization (CO) is in daily use in our society, with applications ranging from supply chains and logistics, to electricity grids, organ exchanges, marketing campaigns, and manufacturing to name only a few. Two classes of hard optimization problems of particular interest in many fields are (1) combinatorial optimization problems and (2) nonlinear constrained problems. Combinatorial optimization problems are characterized by discrete search spaces and have solutions that are combinatorial in nature, involving for instance, the selection of subsets or permutations, and the sequencing or scheduling of tasks. Nonlinear constrained problems may have continuous search spaces but are often characterized by highly nonlinear constraints, such as those arising in electrical power systems whose applications must capture physical laws such as Ohm’s law and Kirchhoff’s law in addition to engineering operational constraints. Such CO problems are often NP-Hard and may be computationally challenging in practice, especially for large-scale instances.

While the AI and Operational Research communities have contributed fundamental advances in optimization in the last decades, the complexity of some problems often prevents them from being adopted in contexts where many instances must be solved over a long-term horizon (e.g., multi-year planning studies) or when solutions must be produced under time constraints. Fortunately, in many practical cases, including the scheduling and energy problems motivating this work, one is interested in solving many problem instances sharing similar patterns. Therefore, the application of deep learning methods to aid the solving of computationally challenging constrained optimization problems appears to be a natural approach and has gained traction in the nascent area at the intersection between CO and ML [5, 19, 31]. In particular, supervised learning frameworks can train a model using pre-solved CO instances and their solutions. However, learning the underlying combinatorial structure of the problem or learning approximations of optimization problems with hard physical and engineering constraints may be an extremely difficult task. While much of the recent research at the intersection of CO and ML has focused on learning good CO approximations in jointly training prediction and optimization models [3, 18, 22, 25, 32] and incorporating optimization algorithms into differentiable systems [1, 27, 34, 20], learning the combinatorial structure of CO problems remains an elusive task.

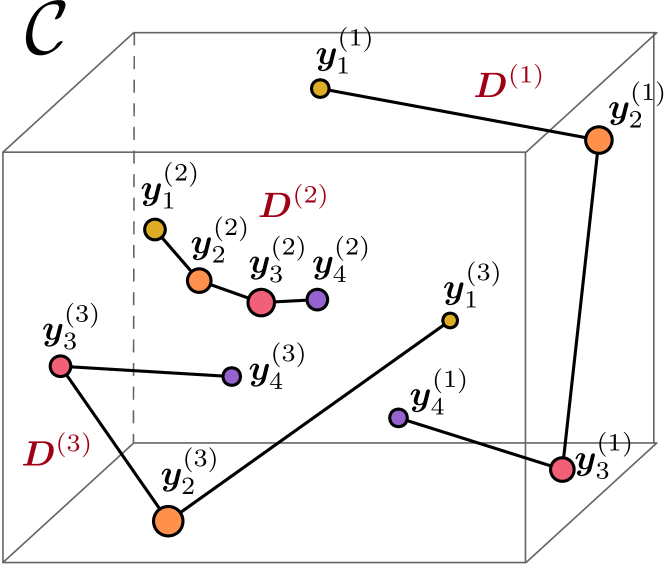

Beside the difficulty of handling hard constraints, which will almost always exhibit some violations, two interesting challenges have emerged: the presence of multiple, often symmetric, solutions, and the learning of approximate solution methods. The first challenge recognizes that an optimization problem may not have a optimal solution. This challenge is illustrated in Figure 1,

where the various represent optimal solutions to CO instances and the feasibility space. As a result, a combinatorial number of possible datasets may be generated. While equally valid as optimal solutions, some sets follow patterns which are more meaningful and recognizable. Symmetry breaking is of course a major area of combinatorial optimization and may alleviate some of these issues. But different instances may not break symmetries in the same fashion, thus creating datasets that are harder to learn.

The second challenge comes from realities in the application domain. Because of time constraints, the solution technique may return a sub-optimal solution. Moreover, modern combinatorial optimization techniques often use randomization and large neighborhood search to produce high-quality solutions quickly. Although these are widely successful, different runs for the same, or similar, instances may produce radically different solutions. As a result, learning the solutions returned by these approximations may be inherently more difficult. These effects may be viewed as a source of noise that obscures the relationships between training data and their target outputs. Although this does not raise issues for optimization systems, it creates challenging learning tasks.

This paper demonstrates these relations, connects the volatility of the training data to the ability of a model to approximate it, and proposes a method for producing (exact or approximate) solutions to optimization problems that are more amenable to supervised learning tasks. More concretely, the paper makes the following contributions:

-

1.

It shows that the existence of co-optimal or approximated solutions obtained by solving hard CO problems to construct training datasets challenges the learnability of the task.

-

2.

To overcome this limitation, it introduces the problem of optimal dataset design, which is cast as a bilevel optimization problem. The optimal dataset design problem is motivated using theoretical insights on the approximation of functions by neural networks, relating the properties of a function describing a training dataset to the model capacity required to represent it.

-

3.

It introduces a tractable algorithm for the generation of datasets that are amenable to learning, and empirical demonstration of marked improvements to the accuracy of trained models, as well as the ability to satisfy constraints at inference time.

-

4.

Finally, it provides state-of-the-art accuracy results at vastly enhanced computational runtime on learning two challenging optimization problems: Job Shop Scheduling problems and Optimal Power Flow problems for energy networks.

To the best of the authors knowledge this work is the first to highlight the issue of learnability in the face of co-optimal or approximate solutions obtained to generate training data for learning to approximate hard CO problems. The observations raised in this work may result in a broader impact as, in addition to approximating hard optimization problems, the optimal dataset generation strategy introduced in this paper may be useful to the line of work on integrating CO as differentiable layers for predictive and prescriptive analytics, as well as for physics constrained learning problems such as when approximating solutions to systems of partial differential equation.

2 Related work

The integration of CO models into ML pipelines to meld prediction and decision models has recently seen the introduction of several nonoverlapping approaches, surveyed by Kotary et al. [19]. The application of ML to boost performance in traditional search methods through branching rules and enhanced heuristics is broadly overviewed by Bengio et al. [5]. Motivated also by the need for fast approximations to combinatorial optimization problems, the training of surrogate models via both supervised and reinforcement learning is an active area for which a thorough review is provided by Vesselinova et al. [31]. Designing surrogate models with the purpose to approximate hard CO problem has been studied in a number of works, including [6, 12, 15]. An important aspect for the learned surrogate models is the prediction of solutions that satisfy the problem constraints. While this is a very difficult task in general, several methodologies have been devised. In particular, Lagrangian loss functions have been used for encouraging constraint satisfaction in several applications of deep learning, including fairness [30] and energy problems [15]. Other methods iteratively modify training labels to encourage satifaction of constraints during training [12].

This work focuses on an orthogonal direction with respect to the literature reviewed above. Rather than devising a new methodology for effectively producing a surrogate model that approximate some hard optimization problem, it studies the machine learning task from a data generation perspective. It shows that the co-optimality and symmetries of a hard CO problem may be viewed as a source of noise that obscures the relationships between training data and the target outputs and proposes an optimal data generation approach to mitigate these important issues.

3 Preliminaries

A constrained optimization (CO) problem poses the task of minimizing an objective function of one or more variables , subject to the condition that a set of constraints are satisfied between the variables and where denotes a vector of input data that specifies the problem instance:

| (1) |

An assignment of values which satisfies is called a feasible solution; if, additionally for all feasible , it is called an optimal solution.

A particularly common constraint set arising in practical problems takes the form , where and . In this case, is a convex set. If the objective is an affine function, the problem is referred to as linear program (LP). If, in addition, some subset of a problem’s variables are required to take integer values, it is called mixed integer program (MIP). While LPs with convex objectives belong to the class of convex problems, and can be solved efficiently with strong theoretical guarantees on the existence and uniqueness of solutions [7], the introduction of integral constraints () results in a much more difficult problem. The feasible set in MIP consists of distinct points in , not only nonconvex but also disjoint, and the resulting problem is, in general, NP-Hard. Finally, nonlinear programs (NLPs) are optimization problems where some of the constraints or the objective function are nonlinear. Many NLPs are nonconvex and can not be efficiently solved [24].

The methodology introduced in this paper is illustrated on hard MIP and nonlinear program instances.

4 Problem setting and goals

This paper focuses on learning approximate solutions to problem (1) via supervised learning. The task considers datasets consisting of data points with being a vector of input data, as defined in equation (1), and being a solution of the optimization task. A desirable, but not always achievable, property is for the solutions to be optimal.

The goal is to learn a model , where is a vector of real-valued parameters, and whose quality is measured in terms of a nonnegative, and assumed differentiable, loss function . The learning task minimizes the empirical risk function (ERM):

| (2) |

with the desired goal that the predictions also satisfy the problem constraints: .

While the above task is difficult to achieve due to the presence of constraints, the paper adopts a Lagrangian approach [14], which has been shown successful in learning constrained representations, along with projection operators, commonly applied in constrained optimization to ensure constraint satisfaction of an assignment. For a given point , e.g., representing the model prediction, a projection operator finds the closest feasible point to under a -norm:

The full description of the Lagrangian based approach and the projection method adopted is delegated to the Appendix A.

5 Challenges in learning hard combinatorial problems

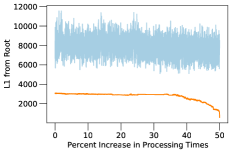

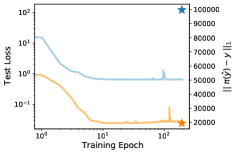

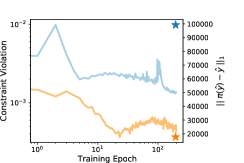

One of the challenges arising in this area comes from the recognition that a problem instance may admit a variety of disparate optimal solutions for each input . To illustrate this challenge, the paper uses a set of scheduling instances that differ only in the time required to process tasks on some machine. A standard approach to the generation of dataset in this context would consist in solving each instance independently using some SoTA optimization solver. However, this may create some significant issues that are illustrated in Figure 2 (more details on the problem are provided in Section 8). The blue curve in Figure 2 (left) illustrates the behavior of this natural approach. In the figure, the processing times in the instances increase from left to right and the blue curve represents the -distance between the obtained solution to each instance (i.e., the start times of the tasks) and a reference optimal solution for some instance. The volatile curve shows that meaningful patterns can be lost, including the important relationship between an increase in processing times and the resulting solutions. Figure 2 (center) shows that, while the solution patterns induced by the target labels appear volatile, the ERM problem appears well behaved, in the face of minimizing the test loss. However, when training loss converges, accuracy (measured as the distance between the projection of the prediction and the real label ) remains poor in models trained on the such data (blue star). Figure 2 (right) shows the average magnitude of the constraints violation during training, corresponding to the two target solution sets of Figure 2 (left), along with a comparison of the objective of the projection operator applied to the prediction: . It is worth emphasizing that these volatility issues are further exacerbated when time constraints prevent the solver from obtaining optimal solutions. Moreover, similar patterns can also be observed for the data generated while solving optimal power flow instances that exhibit symmetries.

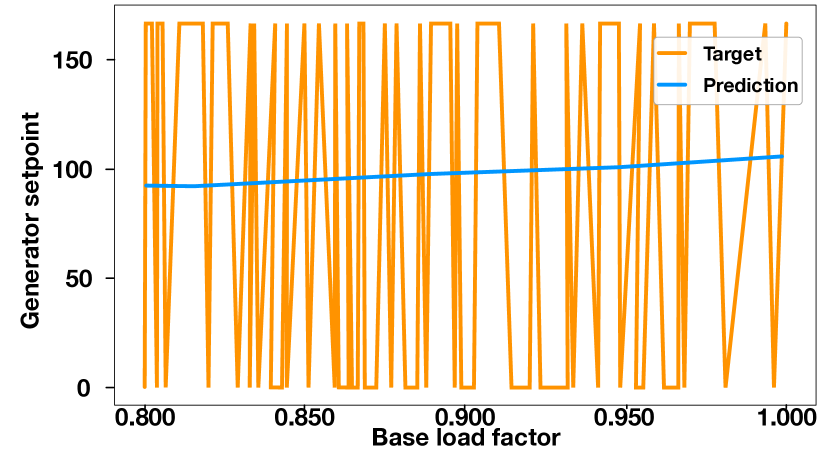

Additionally, extensive observations collected on the motivating applications of the paper show that, even when the model complexity (i.e., the dimensionality of the model parameters ) is increased arbitrarily, the resulting learned models tend to have low-variance. This is illustrated in Figure 3, where the orange and blue curves depict, respectively, a function interpolating the training labels and the associated learned solutions.

The goal of this paper is to construct datasets that are well-suited for learning the optimal (or near-optimal) solutions to optimization problems. The benefits of such an approach is illustrated by the orange curves and stars in Figure 2, which were obtained using the data generation methodology proposed in this paper. They considered the same instances and obtained (different) optimal solutions, but exhibit much enhanced behavior on all metrics.

6 Theoretical justification of the data generation

Although the data generation strategy is necessarily heuristic, it relies on key theoretical insights on the nature of optimization problems and the representation capabilities on neural networks. This section reviews these insights.

First, observe that, as illustrated in the motivating Figure 3, the solution trajectory associated with the problem instances on various input parameters can often be naturally approximated by piecewise linear functions. This approximation is in fact exact for linear programs when the inputs capture incremental changes to the objective coefficients or the right-hand side of the constraints. Additionally, ReLU neural networks, used in this paper to approximate the optimization solutions, have the ability to capture piecewise linear functions [17]. While these models are thus compatible with the task of predicting the solutions of an optimization problem, the model capacity required to represent a target piecewise linear function exactly depends directly on the number of constituent pieces.

Theorem 1 (Model Capacity [2]).

Let be a piecewise linear function with pieces. If is represented by a ReLU network with depth , then it must have size at least . Conversely, any piecewise linear function that is represented by a ReLU network of depth and size at most , can have at most pieces.

The solution trajectories may be significantly different depending on how the data is generated. Hence, the more volatile the trajectory, the harder it will be to learn. Moreover, for a network of fixed size, the more volatile the trajectory, the larger the approximation error will be in general. The data generation proposed in this paper will aim at generating solution trajectories that are approximated by small piecewise linear functions. The following theorem bounds the approximation error when using continuous piecewise linear functions: it connects the approximation errors of a piecewise linear function with the total variation in its slopes.

Theorem 2.

Suppose a piecewise linear function , with pieces each of width for , is used to approximate a piecewise linear with pieces, where . Then the approximation error

holds where is the slope of on piece and is the maximum width of all pieces.

Proof.

Firstly, the proof proceeds with considering the special case in which conincides in slope and value with at some point, and that each piece of overlaps with at most distinct pieces of . This is always possible when . Call the interval on which is defined by its piece. If overlaps with only one piece of , then for ,

| (3) |

If overlaps with pieces and of , then for ,

| (4) |

Each of the above follows from the assumption that and are equal in their slope and value at some point within . From this it follows that on ,

| (5) |

so that on the entire domain of and ,

| (6) |

Since removing the initial simplifying assumptions tightens this upper bound, the result holds. ∎

The final observation that justifies the proposed approach is the fact that optimization problems typically satisfy a local Lipschitz condition, i.e., if the inputs of two instances are close, then they admit solutions that are close as well, i.e., for and ,

| (7) |

for some and , where is a small value. This is obviously true in linear programming when the inputs vary in the objective coefficients or the right-hand side of the constraints, but it also holds locally for many other types of optimization problems. That observation suggests that, when this local Lipschitz condition holds, it may be possible to generate solution trajectories that are well-behaved and can be approximated effectively. Note that Lipschitz functions can be nicely approximated by neural networks as the following result indicates.

Theorem 3 (Approximation [9]).

If is -Lipschitz continuous, then for every , there exists some single-layer neural network of size such that , where

The result above illustrates that the model capacity required to approximate a given function depends to a non-negligible extent on the Lipschitz constant value of the underlying function.

Note that the results in this section are bounds on the ability of neural networks to represent generic functions. In practice, these bounds themselves rarely guarantee the training good approximators, as the ability to minimize the empirical risk problem in practice is often another significant source of error. In light of these results however, it is to be expected that datasets which exhibit less variance and have small Lipschitz constants111The notation here is used to denote its discrete equivalent, as indicated in Equation (7). will be better suited to learning good function approximations. The following section presents a method for dataset generation motivated by these considerations.

7 Optimal CO training data design

Given a set of input data , the goal is to construct the associated pairs for each , that solve the following problem

| (8a) | ||||

| (8b) | ||||

One often equips the data point set with an ordering relation such that for some -norm. For example, in the scheduling domain, the data points represent task start times and the training data are often generated by “slowing down” some machine, which simulates some unexpected ill-functioning component in the scheduling pipeline. In the energy domain, represent the load demands and the training data are generated by increasing or decreasing these demands, simulating the different power load requests during daily operations in a power network.

From the space of co-optimal solutions to each problem instance , the goal is to generate solutions which coincide, to the extent possible, with a target function of low total variation and Lipschitz factor, as well as a low number of constituent linear pieces in the case of discrete optimization. While it may not be possible to produce a target set that simultaneously optimizes each of these metrics, they are confluent and can be improved simultaneously. Natural heuristics are available which reduce these metrics substantially when compared with naive approaches.

One heuristic aimed at satisfying the aforementioned properties reduces to the problem of determining a solution set for the inputs of problem (1) that minimizes their total variation:

| (9a) | ||||

| (9b) | ||||

In practice, this bi-level minimization cannot be achieved, due partially to its prohibitive size. It is possible, however, to minimize the individual terms of (9a), each subject to the result of the previous, by solving individual instances sequentially. Algorithm 1 ensures that solutions to subsequent instances have minimal distance with respect to the chosen -norm(the experiments of Section 8 use ). This method approximates a set of solutions with minimal total variation, while ensuring that the maximum magnitude of change between subsequent instances is also small. When the data represent the result of a discrete optimization, this coincides naturally with a representative function which requires less pieces, with less extreme changes in slope. The method starts by solving a target instance, e.g., the last in the given ordering (line 1). Therein, denotes the solution set of a (possibly approximated) minimizer for problem (1). In the case of the job shop scheduling, for example, represents a local optimizer with a suitable time-limit. The process then generates the next dataset instance in the ordering by solving the optimization problem given in line (3). The problem finds a solution to problem that is close to adjacent solution while preserving optimality, i.e., the objective of the sought is constrained to be at most that of .

The method hinges on the assumption that a bound on can be inferred from , as in the case studies analyzed in this paper. In addition, may be used to hot-start the solution of the subsequent problem, carrying forward solution progress between iterations of Algorithm 1. Therefore, a byproduct of this data-generation approach is that the optimization problem in line (3) can be well-approximated within a short timeout, resulting in enhanced efficiency which makes the data generation process viable in practice even for hard optimization problems that require substantial solving time when treated independently.

In addition to providing enhanced efficacy for learning, this method of generating target instances is generally preferable from a modeling point of view. When predicted solutions to related decision problems are close together, the resulting small changes are often more practical and actionable, and thus highly preferred in practice. For example, a small change in power demands should result in an updated optimal power network configuration which is easy to achieve given its previous state.

8 Application to case studies

The concepts introduced above are applied in this section to two representative case studies, Job Shop Scheduling (JSS) and Optimal Power Flow (OPF). Both are of interest in the optimization and machine learning communities as practical problems which must be routinely solved, but are difficult to approximate under stringent time constraints. The JSS problem represents the class of combinatorial problems, while the OPF problem is continuous but nonlinear and non convex. Both lack solution methods with strong guarantees on the rate of convergence, and the quality of solutions that can be obtained. In the studies described below, a deep neural ReLU network equipped with a Lagrangian loss function (described in details in Appendix A) is used to predict the problem solutions that are approximately feasible and close to optimal. Efficient projection operators are subsequently applied to ensure feasibility of the final output (See Appendix B and C).

Job shop scheduling

Job Shop Scheduling (JSS) assumes a set of jobs, each consisting of a list of tasks to be completed in a specified order. Each task has a fixed processing time and is assigned to one of machines, so that each job assigns one task to each machine. The objective is to find a schedule with minimal makespan, or time taken to process all tasks. The no-overlap condition requires that for any two tasks assigned to the same machine, one must be complete before the other begins. See the problem specification in Appendix B. The objective of the learning task is to predict the start times of all tasks given a JSS problem specification (task duration, machine assignments).

Data Generation Algorithms The experiments examine the proposed models on a variety of problems from the JSPLIB library [28]. The ground truth data are constructed as follows: different input data are generated by simulating a machine slowdown, i.e., by altering the time required to process the tasks on that machine by a constant amount which depends on the instance . Each training dataset associated with a JSS benchmark is composed of a total of 5000 instances. Increasing the processing time of selected tasks may also change the difficulty of the scheduling. The method of sequential solving outlined in Section 7 is particularly well-suited to this context. Individual problem instances can be ordered relative to the amount of extension applied to those processing times, so that when represents the time required to process task of job in instance , . In this case, any solution to instance is feasible to instance (tasks in a feasible schedule cannot overlap when their processing times are reduced, and start times are held constant). As such, the method can be made efficient by passing the solution between subsequent instances as a hot-start.

The analysis compares two datasets: One consisting of target solutions generated independently with a solving time limit of seconds using the state-of-the-art IBM CP Optimizer constraint programming software (denoted as Standard), and one whose targets are generated according to algorithm 1, called the Optimal Design dataset (denoted as OD).

| Instance | Size | Total Variation () | |

|---|---|---|---|

| Standard Data | OD Data | ||

| ta25 | |||

| yn02 | |||

| swv03 | |||

| swv07 | |||

| swv11 | |||

Figure 4 presents a comparison of the total variation resulting from the two datasets. Note that the OD datasets have total variation which is orders of magnitude lower than their Standard counterparts. Recall that a small total variation is perceived as a notion of well-behaveness from the perspective of function approximation. Additionally, it is noted that the total computation time required to generate the OD dataset is at least an order of magnitude smaller than that required to generate the standard dataset (h vs. h).

| Instance | Size | Prediction Error | Constraint Violation | Optimality Gap (%) | Time SoTA Eq. (s) | ||||

|---|---|---|---|---|---|---|---|---|---|

| Standard | OD | Standard | OD | Standard | OD | Standard | OD | ||

| ta25 | |||||||||

| yn02 | |||||||||

| swv03 | |||||||||

| swv07 | |||||||||

| swv11 | |||||||||

Prediction Errors and Constraint Violations Table 1 reports the prediction errors as -distance between the (feasible) predicted variables, i.e., the projections and their original ground-truth quantities (), the average constraint violation degrees, expressed as the -distance between the predictions and their projections, and the optimality gap, which is the relative difference in makespan (or, equivalently objective values) between the predicted (feasible) schedules and target schedules. All these metrics are averaged over all perturbed instances of the dataset and expressed in percentage. In the case of the former two metrics, values are reported as a percentage of the average task duration per individual instance. Notice that for all metrics the methods trained using the OD datasets result in drastic improvements (i.e., one order of magnitude) with respect to the baseline method. Additionally, Table 1 (last column) reports the runtime required by CP-Optimizer to find a value with the same makespan as the one reported by the projected predictions (projection times are also included). The values are to be read as the larger the better, and present a remarkable improvement over the baseline method. It is also noted that the worst average time required to obtain a feasible solution from the predictions is 0.02 seconds. Additional experiments, reported in Appendix D also show that the observations are robust over a wide range of hyper-parameters adopted to train the learning models.

The results show that the OD data generation can drastically improve predictions qualities while reducing the effort required by a projection step to satisfy the problem constraints.

AC Optimal Power Flow

Optimal Power Flow (OPF) is the problem of finding the best generator dispatch to meet the demands in a power network. The OPF is solved frequently in transmission systems around the world and is increasingly difficult due to intermittent renewable energy sources. The problem is required to satisfy the AC power flow equations, that are non-convex and nonlinear, and are a core building block in many power system applications. The objective function captures the cost of the generator dispatch, and the Constraint set describes the power flow operational constraints, enforcing generator output, line flow limits, Kirchhoff’s Current Law and Ohm’s Law for a given load demand. The OPF receives its input from unit-commitment algorithms that specify which generators will be committed to deliver energy and reserves during the 24 hours of the next day. Because many generators are similar in nature (e.g., wind farms or solar farms connected to the same bus), the problem may have a large number of symmetries. If a bus has two symmetric generators with enough generator capacities, the unit commitment optimization may decide to choose one of the symmetric generators or to commit both and balance the generation between both of them. The objective of the learning task is to predict the generator setpoints (power and voltage) for all buses given the problem inputs (load demands).

Data Generation Algorithms The experiments compare this commitment strategy and its effect on learning on Pegase-89, which is a coarse aggregation of the French system and IEEE-118 and IEEE-300, from the NESTA library [10]. All base instances are solved using the Julia package PowerModels.jl [11] with the nonlinear solver IPOPT [33]. Additional data is reported in Appendix C. A number of renewable generators are duplicated at each node to disaggregate the generation capabilities. The test cases vary the load data by scaling the (input) loads from 0.8 to 1.0 times their nominal values. Instances with higher load pattern are typically infeasible. The unit-commitment strategy sketched above can select any of the symmetric generators at a given bus (Standard data). The optimal objective values for a given load are the same, but the optimal solutions vary substantially. Note that, when the unit-commitment algorithm commits generators by removing symmetries (OD data), the solutions for are typically close to each other when the loads are close. As a result, they naturally correspond to the generation procedure advocated in this paper.

| Instance | Size | Prediction Error | Constraint Violation | Optimality Gap (%) | |||

|---|---|---|---|---|---|---|---|

| No. buses | Standard | OD | Standard | OD | Standard | OD | |

| Pegase-89 | 89 | ||||||

| IEEE-118 | 118 | ||||||

| IEEE-300 | 300 | ||||||

Prediction Errors and Constraint Violations As shown in Table 2, when compared the OD approach to data generation results in predictions that are closer to their optimal target solutions (error expressed in MegaWatt (MW)), reduce the constraint violations (expressed as -distance between the predictions and their projections), and improve the optimality gap, which is the relative difference in objectives between the predicted (feasible) solutions and the target ones.

9 Limitations and Conclusions

Aside from the inherent difficulty of learning feasible CO solutions, a practical challenge is represented by the data generation itself. Generating training datasets for supervised learning tasks requires solving many instances of hard CO problems, which can be time consuming and imposes a toll on energy usage and CO2 emissions. In this respect, an advantage of the proposed method, is its ability to use hot-starts to generate instances incrementally, resulting in enhanced efficiency even for hard optimization problems that require substantial solving time when treated independently.

A challenge posed by the proposed data generation methodology its restriction to classes of CO problems that do not necessarily require diverse solutions over time. For example, in timetabling applications, as in the design of employees shifts, a desired condition may be for shifts to be diverse for different but similar inputs. The proposed methodology may, in fact, induce a learner to predict similar solutions across similar input data. A possible solution to this problem may be that of generating various trajectories of solutions, learn from them with independent models, and then randomize the model selection to generate a prediction.

Aside these limitations, the observations raised in this work may be significant in several areas: In addition to approximating hard optimization problems, the optimal dataset generation strategy introduced in this paper may be useful to the line of work on integrating CO and machine learning for predictive and prescriptive analytics, as well as for physics constrained learning problems, two areas with significant economic and societal impacts.

Acknowledgments

This research is partially supported by NSF grant 2007164. Its views and conclusions are those of the authors only and should not be interpreted as representing the official policies, either expressed or implied, of the sponsoring organizations, agencies, or the U.S. government.

References

- Amos and Kolter [2017] B. Amos and J. Z. Kolter. Optnet: Differentiable optimization as a layer in neural networks. In International Conference on Machine Learning (ICML), pages 136–145. PMLR, 2017.

- Arora et al. [2016] R. Arora, A. Basu, P. Mianjy, and A. Mukherjee. Understanding deep neural networks with rectified linear units. arXiv preprint arXiv:1611.01491, 2016.

- Balcan et al. [2018] M.-F. Balcan, T. Dick, T. Sandholm, and E. Vitercik. Learning to branch. In International conference on machine learning, pages 344–353. PMLR, 2018.

- Baran and Wu [1989] M. E. Baran and F. F. Wu. Optimal capacitor placement on radial distribution systems. IEEE TPD, 4(1):725–734, Jan 1989.

- Bengio et al. [2020] Y. Bengio, A. Lodi, and A. Prouvost. Machine learning for combinatorial optimization: a methodological tour d’horizon. European Journal of Operational Research, 2020.

- Borghesi et al. [2020] A. Borghesi, G. Tagliavini, M. Lombardi, L. Benini, and M. Milano. Combining learning and optimization for transprecision computing. In Proceedings of the 17th ACM International Conference on Computing Frontiers, pages 10–18, 2020.

- Boyd et al. [2004] S. Boyd, S. P. Boyd, and L. Vandenberghe. Convex optimization. Cambridge university press, 2004.

- Cain et al. [2012] M. B. Cain, R. P. O’neill, and A. Castillo. History of optimal power flow and formulations optimal power flow paper 1. https://www.ferc.gov/industries/electric/indus-act/market-planning/opf-papers.asp, 2012.

- Chong [2020] K. F. E. Chong. A closer look at the approximation capabilities of neural networks. In 8th International Conference on Learning Representations, ICLR 2020, Addis Ababa, Ethiopia, April 26-30, 2020. OpenReview.net, 2020. URL https://openreview.net/forum?id=rkevSgrtPr.

- Coffrin et al. [2014] C. Coffrin, D. Gordon, and P. Scott. NESTA, the NICTA energy system test case archive. CoRR, abs/1411.0359, 2014. URL http://arxiv.org/abs/1411.0359.

- Coffrin et al. [2018] C. Coffrin, R. Bent, K. Sundar, Y. Ng, and M. Lubin. Powermodels.jl: An open-source framework for exploring power flow formulations. In PSCC, June 2018.

- Detassis et al. [2020] F. Detassis, M. Lombardi, and M. Milano. Teaching the old dog new tricks: supervised learning with constraints. In A. Saffiotti, L. Serafini, and P. Lukowicz, editors, Proceedings of the First International Workshop on New Foundations for Human-Centered AI (NeHuAI), volume 2659 of CEUR Workshop Proceedings, pages 44–51, 2020.

- Deutche-Energue-Agentur [2019] Deutche-Energue-Agentur. The e-highway2050 project. http://www.e-highway2050.eu, 2019. Accessed: 2019-11-19.

- Fioretto et al. [2020a] F. Fioretto, P. V. Hentenryck, T. W. Mak, C. Tran, F. Baldo, and M. Lombardi. Lagrangian duality for constrained deep learning. arXiv:2001.09394, 2020a.

- Fioretto et al. [2020b] F. Fioretto, T. W. Mak, and P. Van Hentenryck. Predicting ac optimal power flows: Combining deep learning and lagrangian dual methods. In Proceedings of the AAAI Conference on Artificial Intelligence (AAAI), pages 630–637, 2020b.

- Fisher et al. [2008] E. B. Fisher, R. P. O’Neill, and M. C. Ferris. Optimal transmission switching. IEEE Transactions on Power Systems, 23(3):1346–1355, Aug 2008.

- Huang [2020] C. Huang. Relu networks are universal approximators via piecewise linear or constant functions. Neural Computation, 32(11):2249–2278, 2020.

- Khalil et al. [2016] E. Khalil, P. Le Bodic, L. Song, G. Nemhauser, and B. Dilkina. Learning to branch in mixed integer programming. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 30, 2016.

- Kotary et al. [2021] J. Kotary, F. Fioretto, P. Van Hentenryck, and B. Wilder. End-to-end constrained optimization learning: A survey. arXiv preprint arXiv:2103.16378, 2021.

- Mandi et al. [2020] J. Mandi, P. J. Stuckey, T. Guns, et al. Smart predict-and-optimize for hard combinatorial optimization problems. In Proceedings of the AAAI Conference on Artificial Intelligence (AAAI), volume 34, pages 1603–1610, 2020.

- Monticelli et al. [1987] A. Monticelli, M. Pereira, and S. Granville. Security-constrained optimal power flow with post-contingency corrective rescheduling. IEEE TPS, 2(1):175–180, 1987.

- Nair et al. [2020] V. Nair, S. Bartunov, F. Gimeno, I. von Glehn, P. Lichocki, I. Lobov, B. O’Donoghue, N. Sonnerat, C. Tjandraatmadja, P. Wang, et al. Solving mixed integer programs using neural networks. arXiv preprint arXiv:2012.13349, 2020.

- Niharika et al. [2016] Niharika, S. Verma, and V. Mukherjee. Transmission expansion planning: A review. In International Conference on Energy Efficient Technologies for Sustainability, pages 350–355, 2016.

- Nocedal and Wright [2006] J. Nocedal and S. Wright. Numerical optimization. Springer Science & Business Media, 2006.

- Nowak et al. [2018] A. Nowak, S. Villar, A. S. Bandeira, and J. Bruna. Revised note on learning algorithms for quadratic assignment with graph neural networks, 2018.

- Pache et al. [2015] C. Pache, J. Maeght, B. Seguinot, A. Zani, S. Lumbreras, A. Ramos, S. Agapoff, L. Warland, L. Rouco, and P. Panciatici. Enhanced pan-european transmission planning methodology. In IEEE Power Energy Society General Meeting, July 2015.

- Pogančić et al. [2020] M. V. Pogančić, A. Paulus, V. Musil, G. Martius, and M. Rolinek. Differentiation of blackbox combinatorial solvers. In International Conference on Learning Representations (ICLR), 2020.

- tamy0612 [2014] tamy0612. Jsplib: Benchmark instances for job-shop scheduling problem, Nov 2014. URL https://github.com/tamy0612/JSPLIB.

- Tong and Ni [2011] J. Tong and H. Ni. Look-ahead multi-time frame generator control and dispatch method in PJM real time operations. In IEEE Power and Energy Society General Meeting, July 2011.

- Tran et al. [2021] C. Tran, F. Fioretto, and P. V. Hentenryck. Differentially private and fair deep learning: A lagrangian dual approach. In Proceedings of the AAAI Conference on Artificial Intelligence (AAAI), 2021.

- Vesselinova et al. [2020] N. Vesselinova, R. Steinert, D. F. Perez-Ramirez, and M. Boman. Learning combinatorial optimization on graphs: A survey with applications to networking. IEEE Access, 8:120388–120416, 2020.

- Vinyals et al. [2015] O. Vinyals, M. Fortunato, and N. Jaitly. Pointer networks. In Advances in Neural Information Processing Systems (NeurIPS, pages 2692–2700, 2015.

- Wächter and Biegler [2006] A. Wächter and L. T. Biegler. On the implementation of an interior-point filter line-search algorithm for large-scale nonlinear programming. Mathematical Programming, 106(1):25–57, 2006.

- Wilder et al. [2019] B. Wilder, B. Dilkina, and M. Tambe. Melding the data-decisions pipeline: Decision-focused learning for combinatorial optimization. In Proceedings of the AAAI Conference on Artificial Intelligence (AAAI), volume 33, pages 1658–1665, 2019.

Appendix A Lagrangian Dual-based approach

In both case studies presented below, a constrained deep learning approach is used which encourages the satisfaction of constraints within predicted solutions by accounting for the violation of constraints in a Lagrangian loss function

| (10) |

where is a standard loss function (i.e., mean squared error), are Lagrange multipliers and represent the constraints of the optimization problem under the generic representation

| (11) |

Training a neural network to minimize the Lagrangian loss for some value of is anologous to computing a Lagrangian Relaxation:

| (12) |

and the Lagrangian Dual problem maximizes the relaxation over all possible :

| (13) |

The Lagrangian deep learning model is trained by alternately carrying out gradient descent for each value of , and updating the based on the resulting magnitudes of constraint violation in its predicted solutions.

Appendix B Job Shop Scheduling

The Job Shop Scheduling (JSS) problem can be viewed as an integer optimization program with linear objective function and linear, disjunctive constraints. For JSS problems with jobs and machines, a particular instance is fully determined by the processing times , along with machine assignments , and its solution consists of the resulting optimal task start times . The full problem specification is shown below in the system (14). The constraints (14c) enforce precedence between tasks that must be scheduled in the specified order within their respective job. Constraints (14d) ensure that no two tasks overlap in time when assigned to the same machine.

B.1 Problem specification

| (14a) | |||||

| subject to: | (14b) | ||||

| (14c) | |||||

| (14d) | |||||

| (14e) | |||||

Given a predicted, possibly infeasible schedule , the degree of violation in each constraint must be measured in order to update the multipliers of the Lagrangian loss function. The violation of task-precedence constraints (14c) and no-overlap constraint (14d) are calculated as in (15a) and (15b), respectively. Note that the violation of the disjunctive no-overlap condition between two tasks is measured as the amount of time at which both tasks are scheduled simultaneously on some machine.

| (15a) | ||||

| (15b) | ||||

where

The Lagrangian-based deep learning model does not necessarily produce feasible schedules directly. An additional operation is required for the construction of feasible solutions, given the direct neural network outputs representing schedules. The model presented below is used to construct solutions that are integral, and feasible to the original problem constraints. Integrality follows from the total unimodularity of constraints (16a, 16b), which converts the no-overlap condition of the problem (14) into addition task-precedence constraints following the order of predicted start times , denoted . By minimizing the makespan as in (14), this procedure ensures optimality of the resulting schedules subject to the imposed ordering.

| subject to: | |||||

| (16a) | |||||

| (16b) | |||||

B.2 Dataset Details

The experimental setting, as defined by the training and test data, simulates a situation in which some component of a manufacturing system ’slows down’, causing processing times to extend on all tasks assigned to a particular machine. Each experimental dataset is generated beginning with a root problem instance taken from the JSPLIB benchmark library for JSS instances. Further instances are generated by increasing processing times on one machine, uniformly over new instances, to a maximum of percent increase over the initial values. To accommodate these incremental perturbations in problem data while keeping all values integral, a large multiplicative scaling factor is applied to all processing times of the root instance. Targets for the supervised learning are generated by solving the individual instances according to the methodology proposed in Section 7. A baseline set of solutions is generated for comparison, by solving individual instances in parallel with a time limit per instance of seconds.

The results presented in Section 8 are taken from the best-performing models, with respect to optimality of the predicted solutions following application of the model (16), among the results of a hyperparameter search. The model training follows the selection of parameters presented in Table 3.

| Parameter | Value | Parameter | Value |

|---|---|---|---|

| Epochs | 500 | Batch Size | 16 |

| Learning rate | Batch Normalization | False | |

| Dual learning rate | Gradient Clipping | False | |

| Hidden layers | 2 | Activation Function | ReLU |

B.3 Network Architecture

The neural network architecture used to learn solutions to the JSS problem takes into account the structure of its constraints, organizing input data by individual job, and machine of the associated tasks. When and represent the input array indices corresponding to job and machine , the associated subarrays and are each passed from the input array to a series of respective Job and Machine layers. The resulting arrays, one for every job and machine, are concatenated to form a single array and passed to further Shared Layers. Each shared layer has size in the case of jobs and machines, and a final layer maps the output to an array of size , equal to the total number of tasks. This architecture improves accuracy significantly in practice, when compared with fully connected networks of comparable size.

Appendix C AC Optimal Power Flow

C.1 Problem specification

| variables: | ||||

| minimize: | (17) | |||

| subject to: | (18) | |||

| (19) | ||||

| (20) | ||||

| (21) | ||||

| (22) | ||||

| (23) | ||||

| (24) |

Optimal Power Flow (OPF) is the problem of finding the best generator dispatch to meet the demands in a power network, while satisfying challenging transmission constraints such as the nonlinear nonconvex AC power flow equations and also operational limits such as voltage and generation bounds. Finding good OPF predictions are important, as a 5% reduction in generation costs could save billions of dollars (USD) per year [8]. In addition, the OPF problem is a fundamental building bock of many applications, including security-constrained OPFs [21]), optimal transmission switching [16], capacitor placement [4], and expansion planning [23].

Typically, generation schedules are updated in intervals of 5 minutes [29], possibly using a solution to the OPF solved in the previous step as a starting point. In recent years, the integration of renewable energy in sub-transmission and distribution systems has introduced significant stochasticity in front and behind the meter, making load profiles much harder to predict and introducing significant variations in load and generation. This uncertainty forces system operators to adjust the generators setpoints with increasing frequency in order to serve the power demand while ensuring stable network operations. However, the resolution frequency to solve OPFs is limited by their computational complexity. To address this issue, system operators typically solve OPF approximations such as the linear DC model (DC-OPF). While these approximations are more efficient computationally, their solution may be sub-optimal and induce substantial economical losses, or they may fail to satisfy the physical and engineering constraints.

Similar issues also arise in expansion planning and other configuration problems, where plans are evaluated by solving a massive number of multi-year Monte-Carlo simulations at 15-minute intervals [26, 13]. Additionally, the stochasticity introduced by renewable energy sources further increases the number of scenarios to consider. Therefore, modern approaches recur to the linear DC-OPF approximation and focus only on the scenarios considered most pertinent [26] at the expense of the fidelity of the simulations.

A power network can be represented as a graph , where the nodes in represent buses and the edges in represent lines. The edges in are directed and is used to denote those arcs in but in reverse direction. The AC power flow equations are based on complex quantities for current , voltage , admittance , and power , and these equations are a core building block in many power system applications. Model 1 shows the AC OPF formulation, with variables/quantities shown in the complex domain. Superscripts and are used to indicate upper and lower bounds for variables. The objective function captures the cost of the generator dispatch, with denoting the vector of generator dispatch values . Constraint (18) sets the reference angle to zero for the slack bus to eliminate numerical symmetries. Constraints (19) and (20) capture the voltage and phase angle difference bounds. Constraints (21) and (22) enforce the generator output and line flow limits. Finally, Constraints (23) capture Kirchhoff’s Current Law and Constraints (24) capture Ohm’s Law.

The Lagrangian-based deep learning model is based on the model reported in [15].

C.2 Dataset Details

| Instance | Size | Total Variation | ||

|---|---|---|---|---|

| Standard Data | OD Data | |||

| 30_ieee | 30 | 82 | ||

| 57_ieee | 57 | 160 | ||

| 89_pegase | 89 | 420 | ||

| 118_ieee | 118 | 372 | ||

| 300_ieee | 300 | 822 | ||

Table 4 describes the power network benchmarks used, including the number of buses , and transmission lines/transformers . Additionally it presents a comparison of the total variation resulting from the two datasets. Note that the OD datasets have total variation which is orders of magnitude lower than their Standard counterparts.

C.3 Network Architecture

The neural network architecture used to learn solutions to the OPF problem is a fully connected ReLU network composed of an input layer of size proportional to the number of loads in the power network. The architecture has 5 hidden layers, each of size double the number of loads in the power network, and a final layer of size proportional to the number of generators in the network. The details of the learning models are reported in Table 5.

| Parameter | Value | Parameter | Value |

|---|---|---|---|

| Epochs | 20000 | Batch Size | 16 |

| Learning rate | Batch Normalization | True | |

| Dual learning rate | Gradient Clipping | True | |

| Hidden layers | 5 | Activation Function | LeakyReLU |

Appendix D Additional Results

| Instance | Size | Prediction Error | Constraint Violation | Optimality Gap (%) | |||

|---|---|---|---|---|---|---|---|

| No. buses | Standard | OD | Standard | OD | Standard | OD | |

| IEEE-30 | 30 | ||||||

| IEEE-57 | 57 | ||||||

| Pegase-89 | 89 | ||||||

| IEEE-118 | 118 | ||||||

| IEEE-300 | 300 | ||||||

Table 6 compares prediction errors and constraint violations for the OD and Standard approach to data generation for the Optimal Power Flow problems. As expressed in the main paper, the results show that the models trained on the OD datset present predictions that are closer to their optimal target solutions (error expressed in MegaWatt (MW)), reduce the constraint violations (expressed as -distance between the predictions and their projections), and improve the optimality gap, which is the relative difference in objectives between the predicted (feasible) solutions and the target ones.