Simple steps are all you need: Frank-Wolfe

and generalized self-concordant functions

Abstract

Generalized self-concordance is a key property present in the objective function of many important learning problems. We establish the convergence rate of a simple Frank-Wolfe variant that uses the open-loop step size strategy , obtaining a convergence rate for this class of functions in terms of primal gap and Frank-Wolfe gap, where is the iteration count. This avoids the use of second-order information or the need to estimate local smoothness parameters of previous work. We also show improved convergence rates for various common cases, e.g., when the feasible region under consideration is uniformly convex or polyhedral.

1 Introduction

Constrained convex optimization is the cornerstone of many machine learning problems. We consider such problems, formulated as:

| (1.1) |

where is a generalized self-concordant function and is a compact convex set. When computing projections onto the feasible regions as required in, e.g., projected gradient descent, is prohibitive, Frank-Wolfe (FW) [Frank & Wolfe, 1956] algorithms (a.k.a. Conditional Gradients (CG) [Levitin & Polyak, 1966]) are the algorithms of choice, relying on Linear Minimization Oracles (LMO) at each iteration to solve Problem (1.1). The analysis of their convergence often relies on the assumption that the gradient is Lipschitz-continuous. This assumption does not necessarily hold for generalized self-concordant functions, an important class of functions whose growth can be unbounded.

1.1 Related work

In the classical analysis of Newton’s method, when the Hessian of is assumed to be Lipschitz continuous and the function is strongly convex, one arrives at a convergence rate for the algorithm that depends on the Euclidean structure of , despite the fact that the algorithm is affine-invariant. This motivated the introduction of self-concordant functions in Nesterov & Nemirovskii [1994], functions for which the third derivative is bounded by the second-order derivative, with which one can obtain an affine-invariant convergence rate for the aforementioned algorithm. More importantly, many of the barrier functions used in interior-point methods are self-concordant, which extended the use of polynomial-time interior-point methods to many settings of interest.

Self-concordant functions have received strong interest in recent years due to the attractive properties that they allow to prove for many statistical estimation settings [Marteau-Ferey et al., 2019, Ostrovskii & Bach, 2021]. The original definition of self-concordance has been expanded and generalized since its inception, as many objective functions of interest have self-concordant-like properties without satisfying the strict definition of self-concordance. For example, the logistic loss function used in logistic regression is not strictly self-concordant, but it fits into a class of pseudo-self-concordant functions, which allows one to obtain similar properties and bounds as those obtained for self-concordant functions [Bach, 2010]. This was also the case in Ostrovskii & Bach [2021] and Tran-Dinh et al. [2015], in which more general properties of these pseudo-self-concordant functions were established. This was fully formalized in Sun & Tran-Dinh [2019], in which the concept of generalized self-concordant functions was introduced, along with key bounds, properties, and variants of Newton methods for the unconstrained setting which make use of this property.

Most algorithms that aim to solve Problem (1.1) assume access to second-order information, as this often allows the algorithms to make monotonic progress, remain inside the domain of , and often, converge quadratically when close enough to the optimum. Recently, several lines of work have focused on using Frank-Wolfe algorithm variants to solve these types of problems in the projection-free setting, for example constructing second-order approximations to a self-concordant using first and second-order information, and minimizing these approximations over using the Frank-Wolfe algorithm [Liu et al., 2020]. Other approaches, such as the ones presented in Dvurechensky et al. [2020] (later extended in Dvurechensky et al. [2022]), apply the Frank-Wolfe algorithm to a generalized self-concordant , using first and second-order information about the function to guarantee that the step sizes are so that the iterates do not leave the domain of , and monotonic progress is made. An additional Frank-Wolfe variant in that work, in the spirit of Garber & Hazan [2016], utilizes first and second order information about , along with a Local Linear Optimization Oracle for , to obtain a linear convergence rate in primal gap over polytopes given in inequality description. The authors in Dvurechensky et al. [2022] also present an additional Frank-Wolfe variant which does not use second-order information, and uses the backtracking line search of Pedregosa et al. [2020] to estimate local smoothness parameters at a given iterate. Other specialized Frank-Wolfe algorithms have been developed for specific problems involving generalized self-concordant functions, such as the Frank-Wolfe variant developed for marginal inference with concave maximization [Krishnan et al., 2015], the variant developed in Zhao & Freund [2023] for -homogeneous barrier functions, or the application for phase retrieval in Odor et al. [2016], where the Frank-Wolfe algorithm is shown to converge on a self-concordant non-Lipschitz smooth objective.

1.2 Contribution

The contributions of this paper are detailed below and summarized in Table 1.

Simple FW variant for generalized self-concordant functions.

We show that a small variation of the original Frank-Wolfe algorithm [Frank & Wolfe, 1956] with an open-loop step size of the form , where is the iteration count is all that is needed to achieve a convergence rate of in primal gap; this also answers an open question posed in Dvurechensky et al. [2022]. Our variation ensures monotonic progress while employing an open-loop strategy which, together with the iterates being convex combinations, ensures that we do not leave the domain of . In contrast to other methods that depend on either a line search or second-order information, our variant uses only a linear minimization oracle, zeroth-order and first-order information and a domain oracle for . The assumption of the latter oracle is very mild and was also implicitly assumed in several of the algorithms presented in Dvurechensky et al. [2022]. As such, our iterations are much cheaper than those in previous work, while essentially achieving the same convergence rates for Problem (1.1).

Moreover, our variant relying on the open-loop step size allows us to establish a convergence rate for the Frank-Wolfe gap, is agnostic, i.e., does not need to estimate local smoothness parameters, and is parameter-free, leading to convergence rates and oracle complexities that are independent of any tuning parameters.

| Algorithm | Convergence | Reference | -order / | Requirements | |

|---|---|---|---|---|---|

| Primal gap | FW gap | LS free? | |||

| FW-GSC | [1, Alg.2] | ✗ / ✓ | SOO | ||

| LBTFW-GSC | [1, Alg.3] | ✓ / ✗ | ZOO, DO | ||

| MBTFW-GSC | [1, Alg.5] | ✗ / ✓ | ZOO, SOO, DO | ||

| FW-LLOO | [1, Alg.7] | ✗ / ✓ | polyh. , LLOO, SOO | ||

| ASFW-GSC | [1, Alg.8] | ✗ / ✓ | polyh. , SOO | ||

| M-FW | This work | ✓ / ✓ | ZOO, DO | ||

| B-AFW / B-BPCG | This work | ✓ / ✗ | polyh. , ZOO, DO | ||

Faster rates in common special cases.

We also obtain improved convergence rates when the optimum is contained in the interior of , or when the set is uniformly or strongly convex, using the backtracking line search of Pedregosa et al. [2020]. We also show that the Away-step Frank-Wolfe [Wolfe, 1970, Lacoste-Julien & Jaggi, 2015] and the Blended Pairwise Conditional Gradients algorithms can use the aforementioned line search to achieve linear rates over polytopes. For clarity we want to stress that any linear rate over polytopes has to depend also on the ambient dimension of the polytope; this applies to our linear rates and those in Table 1 established elsewhere (see Diakonikolas et al. [2020]). In contrast, the rates are dimension-independent.

Numerical experiments.

We provide numerical experiments that showcase the performance of the algorithms on generalized self-concordant objectives to complement the theoretical results. In particular, they highlight that the simple step size strategy we propose is competitive with and sometimes outperforms other variants on many instances.

After publication of our initial draft, in a revision of their original work, Dvurechensky et al. [2022] added an analysis of the Away-step Frank-Wolfe algorithm which is complementary to ours (considering a slightly different setup and regimes) and was conducted independently; we have updated the tables to include these additional results.

1.3 Preliminaries and Notation

We denote the domain of as and the (potentially non-unique) minimizer of Problem (1.1) by . Moreover, we denote the primal gap and the Frank-Wolfe gap at as and , respectively. We use , , and to denote the Euclidean norm, the matrix norm induced by a symmetric positive definite matrix , and the Euclidean inner product, respectively. We denote the diameter of as . Given a non-empty set we refer to its boundary as and to its interior as . We use to denote the probability simplex of dimension . Given a compact convex set we denote:

We assume access to:

-

1.

Domain Oracle (DO): Given , return true if , false otherwise.

-

2.

Zeroth-Order Oracle (ZOO): Given , return .

-

3.

First-Order Oracle (FOO): Given , return .

-

4.

Linear Minimization Oracle (LMO): Given , return .

The FOO and LMO oracles are standard in the FW literature. The ZOO oracle is often implicitly assumed to be included with the FOO oracle; we make this explicit here for clarity. Finally, the DO oracle is motivated by the properties of generalized self-concordant functions. It is reasonable to assume the availability of the DO oracle: following the definition of the function codomain, one could simply evaluate at and assert , thereby combining the DO and ZOO oracles into one oracle. However, in many cases testing the membership of is computationally less demanding than the function evaluation.

Remark 1.1.

Requiring access to a zeroth-order and domain oracle are mild assumptions, that were also implicitly assumed in one of the three FW-variants presented in Dvurechensky et al. [2022] when computing the step size according to the strategy from Pedregosa et al. [2020]; see 5 in Algorithm 4. The remaining two variants ensure that by using second-order information about , which we explicitly do not rely on.

The following example motivates the use of Frank-Wolfe algorithms in the context of generalized self-concordant functions. We present more examples in the computational results.

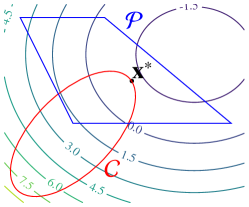

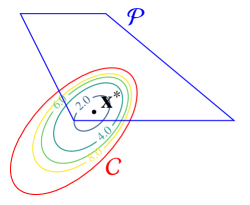

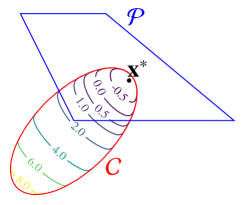

Example 1.2 (Intersection of a convex set with a polytope).

Consider Problem (1.1) where , is a polytope over which we can minimize a linear function efficiently, and is a convex compact set for which one can easily build a barrier function.

Solving a linear optimization problem over may be extremely expensive. In light of this, we can incorporate into the problem through the use of a barrier penalty in the objective function, minimizing instead where is a log-barrier function for and is a parameter controlling the penalization. This reformulation is illustrated in Figure 1. Note that if the original objective function is generalized self-concordant, so is the new objective function (see Proposition 1 in Sun & Tran-Dinh [2019]). We assume that computing the gradient of is roughly as expensive as computing the gradient for and solving an LP over is inexpensive relative to solving an LP over . The parameter can be driven down to after a solution converges in a warm-starting procedure similar to interior-point methods, ensuring convergence to the true optimum.

An additional advantage of this transformation of the problem is the solution structure. Running Frank-Wolfe on the set can select a large number of extremal points from if is non-polyhedral. In contrast, has a finite number of vertices, a small subset of which will be selected throughout the optimization procedure. The same solution as that of the original problem can thus be constructed as a convex combination of a small number of vertices of , improving sparsity and interpretability in many applications.

The following definition formalizes the setting of Problem (1.1).

Definition 1.3 (Generalized self-concordant function).

Let be a closed convex function with open. Then is generalized self-concordant if:

for any and , where .

2 Frank-Wolfe Convergence Guarantees

We establish convergence rates for a Frank-Wolfe variant with an open-loop step size strategy for generalized self-concordant functions. The Monotonic Frank-Wolfe (M-FW) algorithm presented in Algorithm 1 is a rather simple, but powerful modification of the standard Frank-Wolfe algorithm, with the only difference that before taking a step, we verify if , and if so, we check whether moving to the next iterate provides primal progress.

Note, that the open-loop step size rule does not guarantee monotonic primal progress for the vanilla Frank-Wolfe algorithm in general. If either of these two checks fails, we simply do not move: the algorithm sets in 8 of Algorithm 1. As customary, we assume short-circuit evaluation of the logical conditions in Algorithm 1, i.e., if the first condition in 7 is true, then the second condition is not even checked, and the algorithm directly goes to 8. This minor modification of the vanilla Frank-Wolfe algorithm enables us to use the monotonicity of the iterates in the proofs to come, at the expense of at most one extra function evaluation per iteration. Note that if we set , we do not need to call the FOO or LMO oracle at iteration , as we can simply reuse and . This effectively means that between successive iterations in which we search for an acceptable value of , we only need to call the zeroth-order and domain oracle.

In order to establish the main convergence results for the algorithm, we lower bound the progress per iteration with the help of Proposition 2.1.

Proposition 2.1.

(C.f., Sun & Tran-Dinh [2019, Proposition 10]) Given a generalized self-concordant function, then for , we have that:

| (2.1) |

where the inequality holds if and only if for , and we have that,

| (2.2) |

where:

The inequality shown in Equation (2.1) is very similar to the one that we would obtain if the gradient of were Lipschitz continuous, however, while the Lipschitz continuity of the gradient leads to an inequality that holds globally for all , the inequality in Equation (2.1) only holds for . Moreover, there are two other important differences, the norm used in Equation (2.1) is now the norm defined by the Hessian at instead of the norm, and the term multiplying the norm is instead of . We deal with the latter issue by bounding with a constant that depends on for any such that , as shown in Remark 2.2.

Remark 2.2.

As for and , then for .

Due to the fact that we use a simple step size , that we make monotonic progress, and we ensure that the iterates are inside , careful accounting allows us to bound the number of iterations until . Before formalizing the convergence rate we first review a lemma that we will need in the proof.

Lemma 2.3.

(C.f., [Sun & Tran-Dinh, 2019, Proposition 7]) Let be a generalized self-concordant function with . If and then . For the case we have that .

Putting all these things together allows us to obtain a convergence rate for Algorithm 1.

Theorem 2.4.

Suppose is a compact convex set and is a generalized self-concordant function with . Then, the Monotonic Frank-Wolfe algorithm (Algorithm 1) satisfies:

| (2.3) |

for , where and is defined as:

| (2.4) |

Otherwise it holds that for .

-

Proof.

Consider the compact set . As the algorithm makes monotonic progress and moves towards points such that , then for . As the smoothness parameter of is bounded over , we have from the properties of smooth functions that the bound holds for any . Particularizing for and noting that leads to . We then define as:

Using the definition shown in Equation (2.2) we have that for then . This fact, along with the fact that (by monotonicity) allows us to claim that , by application of Lemma 2.3. This means that the non-zero step size will ensure that in 7 of Algorithm 1. Moreover, it allows us to use the bound between the function value at points and in Equation (2.1) of Proposition 2.1, which holds for . With this we can estimate the primal progress we can guarantee for if we move from to :

where the second inequality follows from the upper bound on the primal gap via the Frank-Wolfe gap , the application of Remark 2.2 as for we have that , and from the fact that for all . With the previous chain of inequalities we can bound the primal progress for as

(2.5) From these facts we can prove the convergence rate shown in Equation (2.3) by induction. The base case holds trivially by the fact that using monotonicity we have that . Assuming the claim is true for some we distinguish two cases.

Case : Focusing on the first case, we can plug the previous inequality into Equation (2.5) to find that guarantees primal progress, that is, with the step size , and so we know that we will not go into 8 of Algorithm 1, and we have that . Thus using the induction hypothesis and plugging in the expression for into Equation (2.5) we have:where we use that for all and any .

Case : In this case, we cannot guarantee that the step size provides primal progress by plugging into Equation (2.5), and so we cannot guarantee if a step size of will be accepted and we will have , or we will simply have , that is, we may go into 8 of Algorithm 1. Nevertheless, if we reorganize the expression , by monotonicity we will have that:Where the last inequality holds as for any . ∎

One of the quantities that we have used in the proof of Theorem 2.4 is . Note that the function is -smooth over . One could wonder why we have bothered to use the bound on the Bregman divergence in Proposition 2.1 for a -generalized self-concordant function, instead of simply using the bounds from the -smoothness of over . The reason is that the upper bound on the Bregman divergence in Proposition 2.1 applies for any such that , and we can easily bound the number of iterations it takes for the step size to verify both and for . However, in order to apply the bound on the Bregman divergence from -smoothness we need , and while it is easy to show by monotonicity that , there is no straightforward way to prove that for some we have that for all , i.e., that from some point onward a step with a non-zero step size is taken (that is, we do not go into 8 of Algorithm 1) that guarantees primal progress.

Remark 2.5.

In the case where we can easily bound the primal gap , as in this setting , which leads to from Equation (2.5), regardless of if we set or . Moreover, as the upper bound on the Bregman divergence holds for regardless of the value of , we can modify the proof of Theorem 2.4 to obtain a convergence rate of the form for , which is reminiscient of the rate of the original Frank-Wolfe algorithm for the smooth and convex case.

Furthermore, with this simple step size we can also prove a convergence rate for the Frank-Wolfe gap, as shown in Theorem 2.6. More specifically, the minimum of the Frank-Wolfe gap over the run of the algorithm converges at a rate of . The idea of the proof is very similar to the one in Jaggi [2013]. In a nutshell, as the primal progress per iteration is directly related to the step size times the Frank-Wolfe gap, we know that the Frank-Wolfe gap cannot remain indefinitely above a given value, as otherwise we would obtain a large amount of primal progress, which would make the primal gap become negative. This is formalized in Theorem 2.6.

Theorem 2.6.

Suppose is a compact convex set and is a generalized self-concordant function with . Then if the Monotonic Frank-Wolfe algorithm (Algorithm 1) is run for iterations, we will have that:

where is defined as:

| (2.6) |

-

Proof.

In order to prove the claim, we focus on the iterations , where is defined in Equation (2.6). Note that as we assume that , we know that , and so for iterations we know that , and so:

(2.7) In a very similar fashion as was done in the proof of Theorem 2.4, we divide the proof into two different cases.

Case for some : Reordering the inequality above we therefore know that there exists a such that:where the second inequality follows from the fact that . This leads to .

Case for all : Using the inequality above and plugging into Equation (2.7) allows us to conclude that all steps will produce primal progress using the step size , and so as we know that by Lemma 2.3, then for all we will take a non-zero step size determined by , as and in 7 of Algorithm 1. Consequently, summing up Equation (2.7) from to we have that:(2.8) (2.9) (2.10) (2.11) (2.12) Note that Equation 2.9 stems from the fact that for any , and from plugging , and Equation (2.10) follows from the fact that and for all . The last inequality, shown in Equation (2.11) and (2.12) arises from plugging in the upper bound on the primal gap from Theorem 2.4 and collecting terms. If we plug in the specific values of and this leads to:

(2.13) (2.14) We establish our claim using proof by contradiction. Assume that:

Then by plugging into the bound in Equation (2.14) we have that , which is the desired contradiction, as the primal gap cannot be negative. Therefore we must have that:

This completes the proof. ∎

Remark 2.7.

Note that the Monotonic Frank-Wolfe algorithm (Algorithm 1) performs at most one ZOO, FOO, DO, and LMO oracle call per iteration. This means that Theorems 2.4 and 2.6 effectively bound the number of ZOO, FOO, DO, and LMO oracle calls needed to achieve a target primal gap or Frank-Wolfe gap accuracy as a function of and ; note that is independent of . This is an important difference with respect to existing bounds, as the existing Frank-Wolfe-style first-order algorithms for generalized self-concordant functions in the literature that utilize various types of line searches may perform more than one ZOO or DO call per iteration in the line search. This means that the convergence bounds in terms of iteration count of these algorithms are only informative when considering the number of FOO and LMO calls that are needed to reach a target accuracy in primal gap, and do not directly provide any information regarding the number of ZOO or DO calls that are needed. In order to bound the latter two quantities one typically needs additional technical tools. For example, for the backtracking line search of Pedregosa et al. [2020], one can use Pedregosa et al. [2020, Theorem 1, Appendix C], or a slightly modified version of Lemma 4 in Nesterov [2013], to find a bound for the number of ZOO or DO calls that are needed to find an -optimal solution. Note that these bounds depend on user-defined initialization or tuning parameters provided by the user.

Remark 2.8.

In practice, a halving strategy for the step size is preferred for the implementation of the Monotonic Frank-Wolfe algorithm, as opposed to the step size implementation shown in Algorithm 1. This halving strategy, which is shown in Algorithm 2, helps deal with the case in which a large number of consecutive step sizes are rejected either because or , and helps avoid the need to potentially call the zeroth-order or domain oracle a large number of times in these cases. The halving strategy in Algorithm 2 results in a step size that is at most a factor of smaller than the one that would have been accepted with the original strategy, i.e., that would have ensured that and , in the standard Monotonic Frank-Wolfe algorithm in Algorithm 1. However, the number of zeroth-order or domain oracles that would be needed to find this step size that satisfies both and is logarithmic for the Monotonic Frank-Wolfe variant shown in Algorithm 2, when compared to the number needed for the Monotonic Frank-Wolfe variant with halving shown in Algorithm 1. Note that the convergence properties established throughout the paper for the Monotonic Frank-Wolfe algorithm in Algorithm 1 also hold for the variant in Algorithm 2; with the only difference being that we lose a very small constant factor (e.g., at most a factor of for the standard case) in the convergence rate.

In Table 2 we provide a detailed complexity comparison between the Monotonic Frank-Wolfe (M-FW) algorithm (Algorithm 1), and other comparable algorithms in the literature.

| Algorithm | SOO calls | FOO calls | ZOO calls | LMO calls | DO calls |

|---|---|---|---|---|---|

| FW-GSC [1, Alg.2] | |||||

| LBTFW-GSC‡ [1, Alg.3] | |||||

| MBTFW-GSC‡ [1, Alg.5] | |||||

| M-FW† [This work] |

We note that the LBTFW-GSC algorithm from Dvurechensky et al. [2022] is in essence the Frank-Wolfe algorithm with a modified version of the backtracking line search of Pedregosa et al. [2020]. In the next section, we provide improved convergence guarantees for various cases of interest for this algorithm, which we refer to as the Frank-Wolfe algorithm with Backtrack (B-FW) for simplicity.

2.1 Improved convergence guarantees

We will now establish improved convergence rates for various special cases. We focus on two different settings to obtain improved convergence rates; in the first, we assume that (Section 2.1.1), and in the second we assume that is strongly or uniformly convex (Section 2.1.2). The algorithm in this section is a slightly modified Frank-Wolfe algorithm with the adaptive line search technique of Pedregosa et al. [2020] (shown for reference in Algorithm 3 and 4). This is the same algorithm used in Dvurechensky et al. [2022], however, we show improved convergence rates in several settings of interest. Note that the adaptive line search technique of Pedregosa et al. [2020] requires user-defined inputs or parameters, which means that the algorithms in this section are not parameter-free.

2.1.1 Optimum contained in the interior

We first focus on the assumption that , obtaining improved rates when we use the FW algorithm coupled with the adaptive step size strategy from Pedregosa et al. [2020] (see Algorithm 4). This assumption is reasonable if for example , and . That is to say, we will have that if for example we use logarithmic barrier functions to encode a set of constraints, and we have that is a proper subset of . In this case the optimum is guaranteed to be in .

The analysis in this case is reminiscent of the one in the seminal work of Guélat & Marcotte [1986], and is presented in Subsection 2.1.1. Note that we can upper-bound the value of for by , where is the backtracking parameter and is the initial smoothness estimate in Algorithm 4. Before proving the main theoretical results of this section, we first review some auxiliary results that allow us to prove linear convergence in this setting.

Theorem 2.9 (Theorem 5.1.6, Nesterov [2018]).

Let be generalized self-concordant and not contain straight lines, then the Hessian is non-degenerate at all points .

Note that the assumption that does not contain straight lines is without loss of generality as we can simply modify the function outside of our compact convex feasible region so that it holds.

Proposition 2.10 (Guélat & Marcotte [1986]).

If there exists an such that , then for all we have that:

where and is the Frank-Wolfe gap.

With these tools at hand, we have that the Frank-Wolfe algorithm with the backtracking step size strategy converges at a linear rate.

Theorem 2.11.

Let be a generalized self-concordant function with and let not contain straight lines. Furthermore, we denote by the largest value such that . Then, the Frank-Wolfe algorithm (Algorithm 3) with the backtracking strategy of Pedregosa et al. [2020] results in a linear primal gap convergence rate of the form:

for , where , is the backtracking parameter, is the initial smoothness estimate in Algorithm 4, and

Proof.

Consider the compact set . As the backtracking line search makes monotonic primal progress, we know that for we will have that . Consequently we can define . As by our assumption does not contain any straight lines we know that for all the Hessian is non-degenerate, and therefore . This allows us to claim that for any we have that:

| (2.15) |

The backtracking line search in Algorithm 4 will either output a point or . In any case, Algorithm 4 will find and output a smoothness estimate and a step size such that for we have that:

| (2.16) |

In the case where we know by observing 7 of Algorithm 4 that , and so plugging into Equation (2.16) we arrive at . In the case where , we have that , which leads to , when plugging the expression for the step size in the progress bound in Equation 2.16. In this last case where we have the following contraction for the primal gap:

where we have used the inequality that involves the central term and the leftmost term in Proposition 2.10, and the last inequality stems from the bound for -strongly convex functions. Putting the above bounds together we have that:

which completes the proof. ∎

The previous bound depends on the largest positive such that , which can be arbitrarily small. Note also that the previous proof uses the lower bound of the Bregman divergence from the -strong convexity of the function over to obtain linear convergence. Note that this bound is local as this -strong convexity holds only inside , and is only of use because the step size strategy of Algorithm 4 automatically ensures that if and is a direction of descent, then . This is in contrast with Algorithm 1, in which the step size did not automatically ensure monotonicity in primal gap, and this had to be enforced by setting if , where . If we were to have used the lower bound on the Bregman divergence from Sun & Tran-Dinh [2019, Proposition 10] in the proof, which states that:

for any and any , we would have arrived at a bound that holds over all . However, in order to arrive at a usable bound, and armed only with the knowledge that the Hessian is non-degenerate if does not contain straight lines, and that , we would have had to write:

where the inequality follows from the definition of . It is easy to see that as by Remark 2.2, we have that . This results in a bound:

| (2.17) |

When we compare the bounds on Equation (2.15) and (2.17), we can see that the bound from -strong convexity is tighter than the bound from the properties of -generalized self-concordant functions, albeit local. This is the reason why we have used the former bound in the proof of Theorem 2.11.

2.1.2 Strongly convex or uniformly convex sets

Next, we recall the definition of uniformly convex sets, used in Kerdreux et al. [2021], which will allow us to obtain improved convergence rates for the FW algorithm over uniformly convex feasible regions.

Definition 2.12 (-uniformly convex set).

Given two positive numbers and , we say the set is -uniformly convex with respect to a norm if for any , , and with we have that .

In order to prove convergence rate results for the case where the feasible region is -uniformly convex, we first review the definition of the -uniform convexity of a set (see Definition 2.13), as well as a useful lemma that allows us to go from contractions to convergence rates.

Definition 2.13 (-uniformly convex set).

Given two positive numbers and , we say the set is -uniformly convex with respect to a norm if for any , , and with we have that:

The previous definition allows us to obtain a scaling inequality very similar to the one shown in Theorem 2.10, which is key to proving the following convergence rates, and can be implicitly found in Kerdreux et al. [2021] and Garber & Hazan [2016].

Proposition 2.14.

Let be -uniformly convex, then for all :

where , and is the Frank-Wolfe gap.

The next lemma that will be presented is an extension of the one used in Kerdreux et al. [2021, Lemma A.1] (see also Temlyakov [2015]), and allows us to go from per iteration contractions to convergence rates.

Lemma 2.15.

We denote a sequence of nonnegative numbers by . Let , , and be positive numbers such that , and for , then:

where

This allows us to conveniently transform the per iteration contractions to convergence rates. Moving on to the proof of the convergence rate.

Theorem 2.16.

Suppose is a compact -uniformly convex set and is a generalized self-concordant function with . Furthermore, assume that . Then, the Frank-Wolfe algorithm with Backtrack (Algorithm 3) results in a convergence:

for , where:

and , where is the backtracking parameter, is the initial smoothness estimate in Algorithm 4, and

Proof.

At iteration , the backtracking line search strategy finds through successive function evaluations a such that:

Finding the that maximizes the right-hand side of the previous inequality leads to:

which is the step size ultimately taken by the algorithm at iteration . Note that if this means that , which when plugged into the inequality above leads to . Conversely, for we have that . Focusing on this case and using the bounds and from Proposition 2.14 leads to:

| (2.18) | ||||

| (2.19) |

where the last inequality simply comes from the bound on the gradient norm, and the fact that , for , where is the backtracking parameter and is the initial smoothness estimate in Algorithm 4. Reordering this expression and putting together the two cases we have that:

For the case where we get a linear contraction in primal gap. Using Lemma 2.15 to go from a contraction to a convergence rate for we have that:

for , where:

which completes the proof. ∎

However, in the general case, we cannot assume that the norm of the gradient is bounded away from zero over . We deal with the general case in Theorem 2.17

Theorem 2.17.

Suppose is a compact -uniformly convex set and is a generalized self-concordant function with for which domain does not contain straight lines. Then, the Frank-Wolfe algorithm with Backtrack (Algorithm 3) results in a convergence:

for , where:

and , where is the backtracking parameter, is the initial smoothness estimate in Algorithm 4,

Proof.

Consider the compact set . As the algorithm makes monotonic primal progress we have that for . The proof proceeds very similarly as before, except for the fact that now we have to bound using -strong convexity for points . Continuing from Equation (2.18) for the case where and using the fact that we have that:

where we have also used the bound in the last equation. This leads us to a contraction, together with the case where , which is unchanged from the previous proofs, of the form:

Using again Lemma 2.15 to go from a contraction to a convergence rate for we have that:

for , where:

which completes the proof. ∎

In Table 3 we provide an oracle complexity breakdown for the Frank-Wolfe algorithm with Backtrack (B-FW), also referred to as LBTFW-GSC in Dvurechensky et al. [2022], when minimizing over a -uniformly convex set.

| Algorithm | Assumptions | FOO/ZOO/LMO/DO calls | Reference |

|---|---|---|---|

| B-FW/LBTFW-GSC‡ | This work | ||

| B-FW/LBTFW-GSC‡ | , | This work | |

| B-FW/LBTFW-GSC‡ | , | This work | |

| B-FW/LBTFW-GSC‡ | No straight lines in | This work |

3 Away-step and Blended Pairwise Conditional Gradients

When the domain is a polytope, one can obtain linear convergence in primal gap for a generalized self-concordant function using the well known Away-step Frank-Wolfe (AFW) algorithm [Guélat & Marcotte, 1986, Lacoste-Julien & Jaggi, 2015] shown in Algorithm 5 and the more recent Blended Pairwise Conditional Gradients (BPCG) algorithm [Tsuji et al., 2022] with the adaptive step size of Pedregosa et al. [2020]. We use to denote the active set at iteration , that is, the set of vertices of the polytope that gives rise to as a convex combination with positive weights.

For AFW, we can see that the algorithm either chooses to perform what is know as a Frank-Wolfe step in 8 of Algorithm 5 if the Frank-Wolfe gap is greater than the away gap or an Away step in 11 of Algorithm 5 otherwise. Similarly for BPCG, the algorithm performs a Frank-Wolfe step in 8 of Algorithm 6 if the Frank-Wolfe gap is greater than the pairwise gap

Both proofs of linear convergence follow closely from Pedregosa et al. [2020] and Lacoste-Julien & Jaggi [2015], with the only difference that we need to take into consideration that the function is generalized self-concordant as opposed to smooth and strongly convex. One of the key inequalities used in the proof is a scaling inequality from Lacoste-Julien & Jaggi [2015] very similar to the one shown in Proposition 2.10 and Proposition 2.14, which we state next:

Proposition 3.1.

Let be a polytope, and denote by the set of vertices of the polytope that gives rise to as a convex combination with positive weights, then for all :

where , , and is the pyramidal width of .

Theorem 3.2.

Suppose is a polytope and is a generalized self-concordant function with for which the domain does not contain straight lines. Then, both the Away-step Frank-Wolfe (AFW) and the Blended Pairwise Conditional Gradients algorithms with Backtrack (Algorithm 5) achieve a convergence rate:

where is the pyramidal width of the polytope , , is the backtracking parameter, is the initial smoothness estimate in Algorithm 4, and

Proof.

Proceeding very similarly as in the proof of Theorem 2.11, we have that as the backtracking line search makes monotonic primal progress, we know that for we will have that . As the function is -strongly convex over , we can use the appropriate inequalities from strong convexity in the progress bounds. Using this aforementioned property, together with the scaling inequality of Proposition 3.1 results in:

| (3.1) | ||||

| (3.2) |

where the first inequality comes from the -strong convexity over , and the second inequality comes from applying Proposition 3.1 with .

For AFW, we can expand the expression of the numerator of the bound in (3.2):

| (3.3) |

Note that if the Frank-Wolfe step is chosen in 8, then

otherwise, if an away step is chosen in 11, then

In both cases, we have that:

| (3.4) |

For BPCG, we can directly exploit Tsuji et al. [2022, Lemma 3.5], which establishes the following bound at every iteration of Algorithm 6:

resulting in the same inequality (3.4).111Note the minus sign accounting for the difference in the definition of between our paper and Tsuji et al. [2022].

Note that using a similar reasoning, as , in both cases it holds that:

| (3.5) |

As in the preceding proofs, the backtracking line search in Algorithm 4 will either output a point or . In any case, for both AFW and BPCG, and regardless of the type of step taken, Algorithm 4 will find and output a smoothness estimate and a step size such that:

| (3.6) |

As before, we will have two cases differentiating whether the step size is maximal. If we know by observing 7 of Algorithm 4 that

which combined with Equation (3.6) results in:

In the case where , we have:

Plugging the expression of into Equation (3.6) yields

In any case, we can rewrite Equation (3.6) as:

| (3.7) |

We can now use the inequality in Equation (3.4) to bound the second term in the minimization component of Equation (3.7), and Equation (3.5) to bound the first term. This leads to:

| (3.8) | ||||

| (3.9) |

where in the last inequality we use and for all . It remains to bound away from zero to obtain the linear convergence bound. For Frank-Wolfe steps, we immediately have , but for away or pairwise steps, there is no straightforward way of bounding away from zero. One of the key insights from Lacoste-Julien & Jaggi [2015] is that instead of bounding away from zero for all steps up to iteration , we can instead bound the number of away steps with a step size up to iteration , which are steps that reduce the cardinality of the active set and satisfy . The same argument is used in Tsuji et al. [2022] to prove the convergence of BPCG. This leads us to consider only the progress provided by the remaining steps, which are Frank-Wolfe steps and away steps for AFW or pairwise steps for BPCG with . For a number of steps , only at most half of these steps could have been away steps with , as we cannot drop more vertices from the active set than the number of vertices we could have potentially picked up with Frank-Wolfe steps. For the remaining steps, we know that:

Therefore, we have that the primal gap satisfies:

This completes the proof. ∎

We can make use of the proof of convergence in primal gap to prove linear convergence in Frank-Wolfe gap. In order to do so, we recall a quantity formally defined in Kerdreux et al. [2019] but already implicitly used earlier in Lacoste-Julien & Jaggi [2015] as:

Note that provides an upper bound on the Frank-Wolfe gap as the first term in the definition, the so-called away gap, is positive.

Theorem 3.3.

Suppose is a polytope and is a generalized self-concordant function with for which the domain does not contain straight lines. Then, the Away-step Frank-Wolfe (AFW) algorithm with Backtrack (Algorithm 5) and the Blended Pairwise Conditional Gradients (BPCG) algorithm with Backtrack (Algorithm 6) both contract the Frank-Wolfe gap linearly, i.e., after iterations.

Proof.

We observed in the proof of Theorem 3.2 that regardless of the type of step chosen in AFW and BPCG, the following holds:

On the other hand, we also have that . Plugging these bounds into the right-hand side and the left hand side of Equation 3.7 in Theorem 3.2, and using the fact that we have that:

where the second inequality follows from the convergence bound on the primal gap from Theorem 3.2. Considering the steps that are not away steps with as in the proof of Theorem 3.2, leads us to:

∎

In Table 4 we provide a detailed complexity comparison between the Backtracking AFW (B-AFW) Algorithm 5, and other comparable algorithms in the literature. Note that these convergence rates assume that the domain under consideration is polyhedral.

| Algorithm | SOO calls | FOO calls | ZOO calls | LMO calls | DO calls |

|---|---|---|---|---|---|

| FW-LLOO [1, Alg.7] | * | ||||

| ASFW-GSC [1, Alg.8] | |||||

| B-AFW/B-BPCG†‡ [This work] |

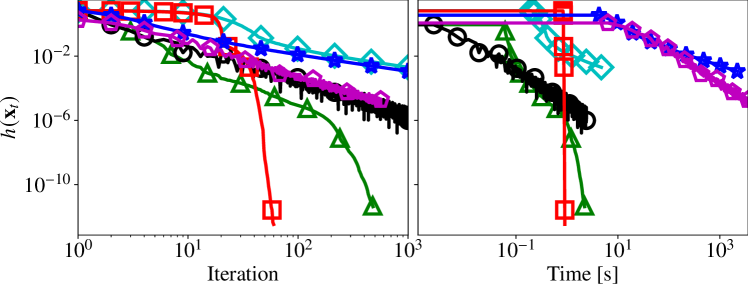

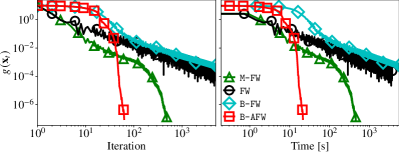

4 Computational experiments

We showcase the performance of the M-FW algorithm, the second-order step size and the LLOO algorithm from Dvurechensky et al. [2022] (denoted by GSC-FW and LLOO in the figures) and the Frank-Wolfe and the Away-step Frank-Wolfe algorithm with the backtracking stepsize of Pedregosa et al. [2020], denoted by B-FW and B-AFW respectively. We ran all experiments on a server with 8 Intel Xeon 3.50GHz CPUs and 32GB RAM. All computations are run in single-threaded mode using Julia 1.6.0 with the FrankWolfe.jl package [Besançon et al., 2022]. The data sets used in the problem instances can be found in Carderera et al. [2021], the code used for the experiments can be found on https://github.com/ZIB-IOL/fw-generalized-selfconcordant. When running the adaptive step size from Pedregosa et al. [2020], the only parameter that we need to set is the initial smoothness estimate . We use the initialization proposed in the Pedregosa et al. [2020] paper, namely:

with set to . The scaling parameters are left at their default values as proposed in Pedregosa et al. [2020] and also used in Dvurechensky et al. [2022]. The code can be found in the fw-generalized-selfconcordant repository.

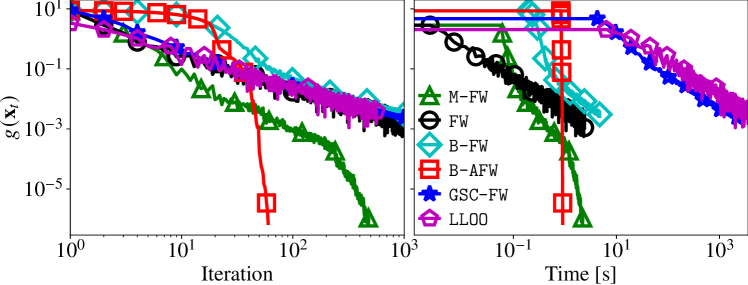

We also use the vanilla FW algorithm denoted by FW, which is simply Algorithm 1 without Lines 7 and 8 using the traditional open-loop step size rule. Note that there are no formal convergence guarantees for this algorithm when applied to Problem (1.1). All figures show the evolution of the and against and time with a log-log scale. As in Dvurechensky et al. [2022] we implemented the LLOO based variant only for the portfolio optimization instance ; for the other examples, the oracle implementation was not implemented due to the need to estimate non-trivial parameters.

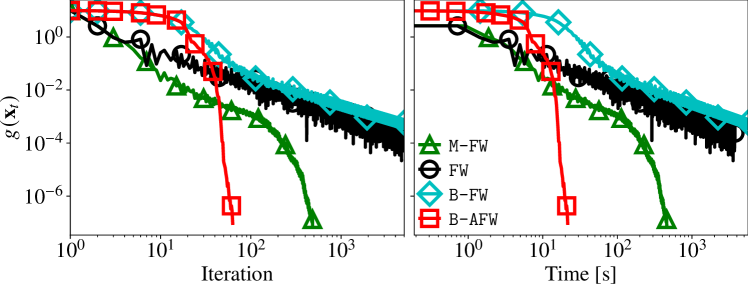

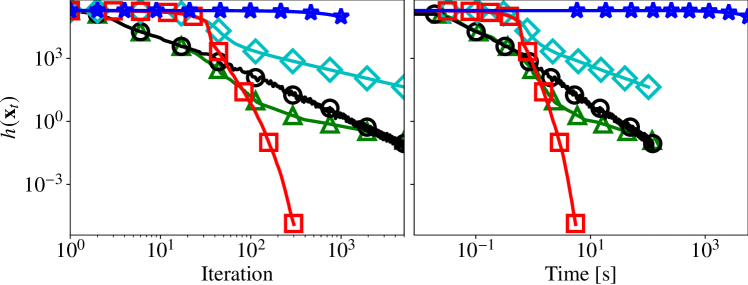

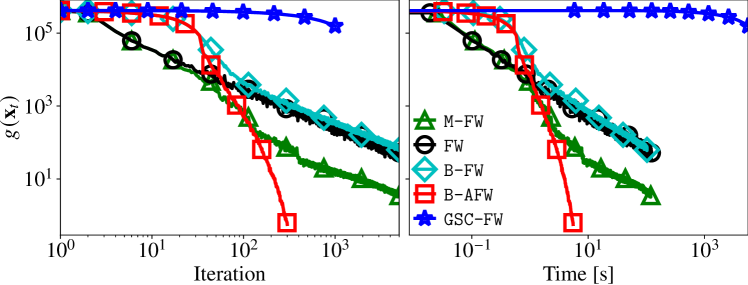

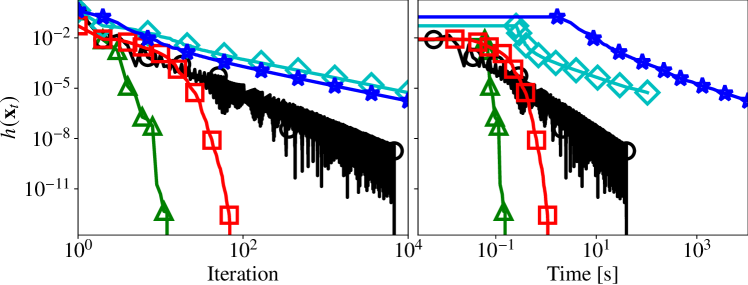

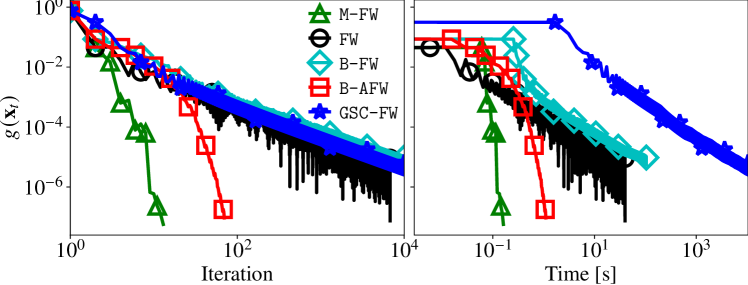

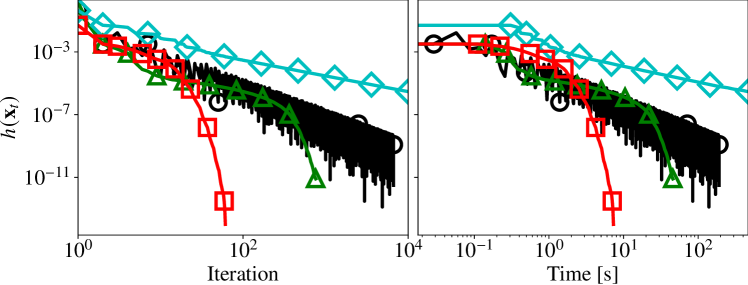

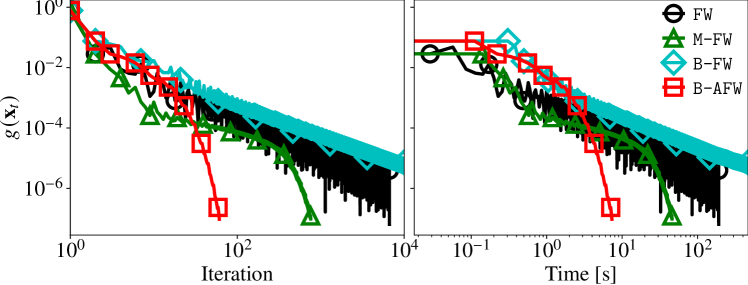

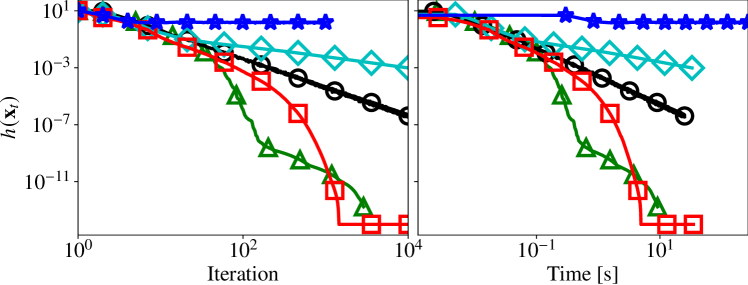

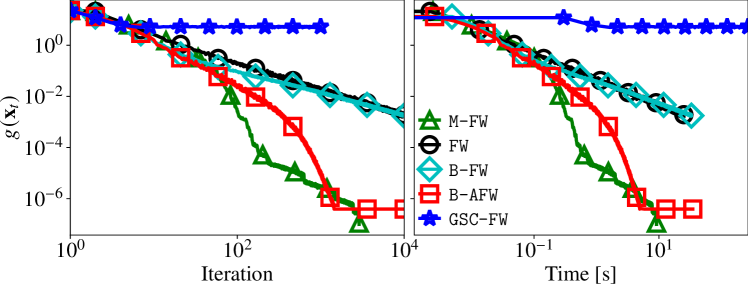

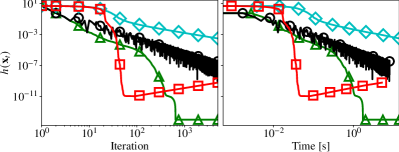

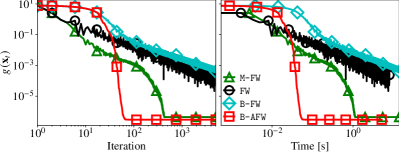

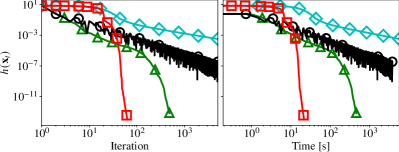

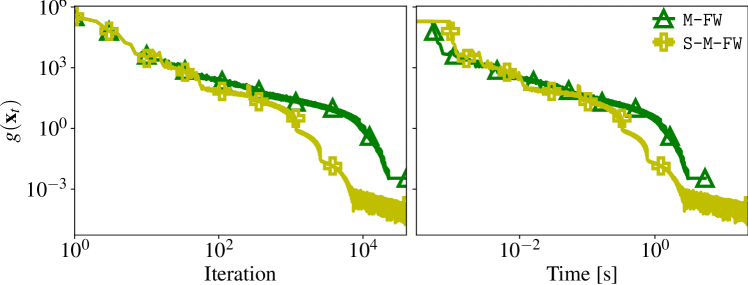

As can be seen in all experiments, the Monotonic Frank-Wolfe algorithm is very competitive, outperforming previously proposed variants in both in progress per iteration and time. The only other algorithm that is sometimes faster is the Away-step Frank-Wolfe variant, which however depends on an active set, and can induce up to a quadratic overhead, making iterations progressively more expensive; this can also be observed in our experiments as the advantage in time is much less pronounced than in iterations.

Portfolio optimization. We consider , where denotes the number of periods and . The results are shown in Figures 2, 3 and 4. We use the revenue data from Dvurechensky et al. [2022] and add instances generated in a similar fashion from independent Normal random entries with dimension 1000, 2000, and 5000, and from a Log-normal distribution with .

|

|

|

|

|

|

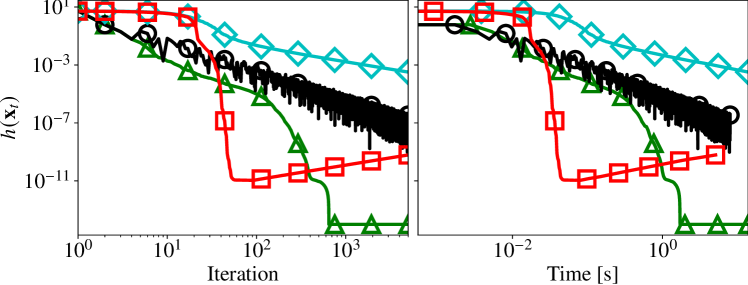

Signal recovery with KL divergence. We apply the aforementioned algorithms to the recovery of a sparse signal from a noisy linear image using the Kullback-Leibler divergence. Given a linear map , we assume a signal is generated by where is assumed to be a sparse unknown input signal and is a random error. Assuming and are entrywise positive, and that the signal to recover should also be entrywise positive, the minimizer of the KL divergence (or Kullback’s I-divergence [Csiszar, 1991]) can be used as an estimator for . The KL divergence between the resulting output signals is expressed as , where is the row of . In order to promote sparsity and enforce nonnegativity of the solution, we use the unit simplex of radius as the feasible set . The results are shown in Figure 5. We used the same choice for the second-order method as in Dvurechensky et al. [2022] for comparison; whether this choice is admissible is unknown (see Remark 4.1). We generate input signals with non-zeros elements following an exponential distribution of mean . The entries of are generated from a folded Normal distribution built from absolute values of Gaussian random numbers with standard deviation and mean . The additive noise is generated from a Gaussian centered distribution with a standard deviation equal to a fraction of the standard deviation of .

|

|

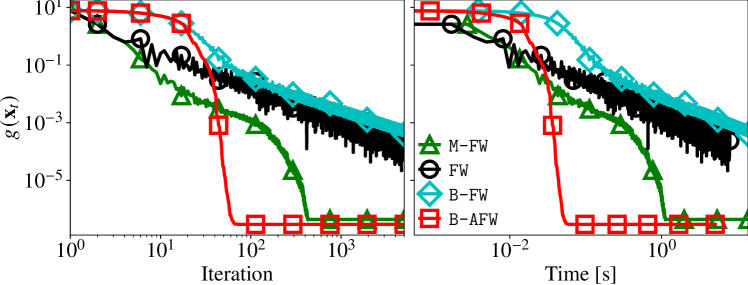

Logistic regression. One of the motivating examples for the development of a theory of generalized self-concordant function is the logistic regression problem, as it does not match the definition of a standard self-concordant function but shares many of its characteristics. We consider a design matrix with rows with and a vector and formulate a logistic regression problem with elastic net regularization, in a similar fashion as is done in Liu et al. [2020], with , and is the ball of radius , where and are two regularization parameters. The logistic regression loss is generalized self-concordant with . The results can be seen in Figures 6 and 7. We use the a1a-a9a datasets from the LIBSVM classification data.

|

|

|

|

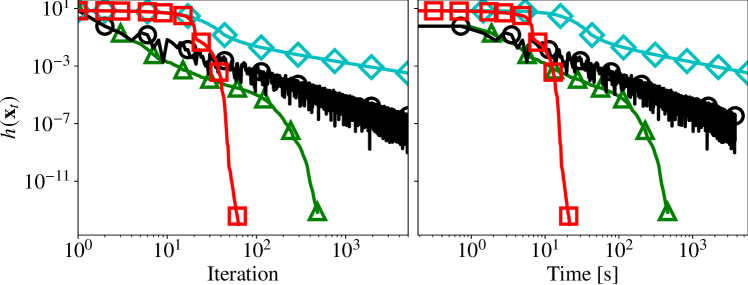

Birkhoff polytope. All applications previously considered all have in common a constraint set possessing computationally inexpensive LMOs (probability or unit simplex and norm ball). Additionally, each vertex returned from the LMO is highly sparse with at most one non-zero element. To complement the results we consider a problem over the Birkhoff polytope, the polytope of doubly stochastic matrices, where the LMO is implemented through the Hungarian algorithm, and is not as inexpensive as in the other examples considered. We use a quadratic regularization parameter where is the number of samples.

|

|

Remark 4.1.

Note that Proposition 2 in Sun & Tran-Dinh [2019], which deals with the composition of generalized self-concordant functions with affine maps, does not apply to the KL divergence objective function, reproduced here for reference:

Furthermore, the objective function is strongly convex if and only if , where is the dimension of the problem.

Proof.

[Sun & Tran-Dinh, 2019, Proposition 2] establishes certain conditions under which the composition of a generalized self-concordant function with an affine map results in a generalized self-concordant function. The objective is of the form:

Note that generalized self-concordant functions are closed under addition, and so we only focus on the individual terms in the sum. As first-order terms are -generalized self-concordant for any , then we know that the composition of these first-order terms with an affine map results in a generalized self-concordant function Sun & Tran-Dinh [2019, Proposition 2]. We therefore focus on the entropy function which is generalized self-concordant. The conditions which ensure that the composition of a -generalized self-concordant function with an affine map results in a generalized self-concordant function requires in the case that [Sun & Tran-Dinh, 2019, Proposition 2]. In the case of the KL divergence objective, and is an outer product with only one positive eigenvalue, and 0 of multiplicity . Therefore we cannot guarantee that the function is generalized self-concordant by application of Proposition 2 in Sun & Tran-Dinh [2019].

Alternatively, in order to try to show that the function is generalized self-concordant we could consider . Assuming , then is positive definite, and only the generalized self-concordance of is left to prove.

Each term with the standard basis vector is the composition of a generalized self-concordant function composed with a rank-one affine transformation, this raises the same issues encountered in the paragraph above.

Regarding the strong-convexity of the objective function, we can express the gradient and the Hessian of the function as:

which is the sum of outer products, each corresponding to a single eigenvector . If , the Hessian is definite positive and the objective is strongly convex. Otherwise, it possesses zero as an eigenvalue regardless of , and the function Hessian is positive semi-definite. ∎

Strong convexity parameter for the LLOO.

The LLOO procedure explicitly requires a strong convexity parameter of the objective function, an underestimator of over . For the portfolio optimization problem, the Hessian is a sum of rank-one terms:

The only non-zero eigenvalue associated with each term is bounded below over by:

The denominator can be solved by two calls to the LMO, and we will denote it by for the term. Each summation term contributes positively to one of the eigenvalues of the Hessian matrix, an underestimator of the the strong convexity parameter is then given by:

The second-order method GSC-FW has been implemented with an in-place Hessian matrix updated at each iteration, following the implementation of Dvurechensky et al. [2022]. The Hessian computation nonetheless adds significant cost in the runtime of each iteration, even if the local norm and other quadratic expressions can be computed allocation-free. A potential improvement for future work would be to represent Hessian matrices as functional linear operators mapping any to .

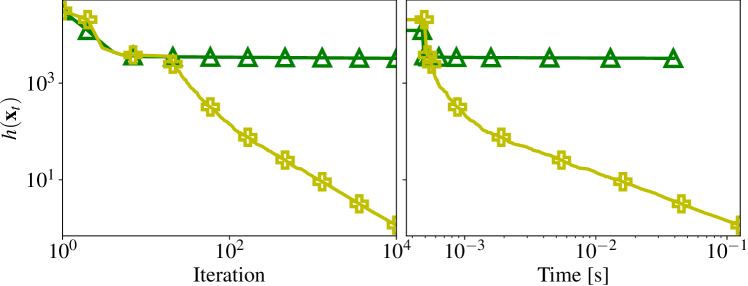

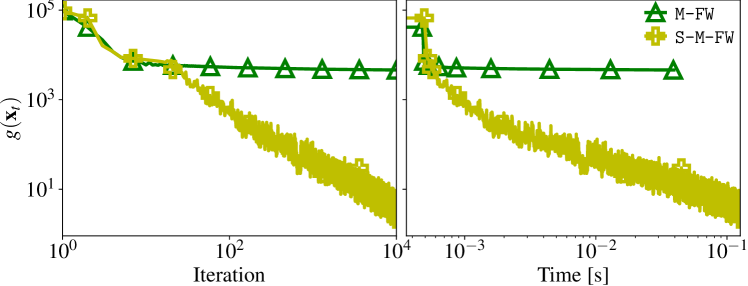

Monotonic step size: the numerical case.

The computational experiments highlighted that the Monotonic Frank-Wolfe performs well in terms of iteration count and time against other Frank-Wolfe and Away-step Frank-Wolfe variants. Another advantage of a simple step size computation procedure is its numerical stability. On some instances, an ill-conditioned gradient can lead to a plateau of the primal and/or dual progress. Even worse, some step-size strategies do not guarantee monotonicity and can result in the primal value increasing over some iterations. The numerical issue that causes this phenomenon is illustrated by running the methods of the FrankWolfe.jl package over the same instance using -bits floating-point numbers and Julia BigFloat types (which support arithmetic in arbitrary precision to remove numerical issues).

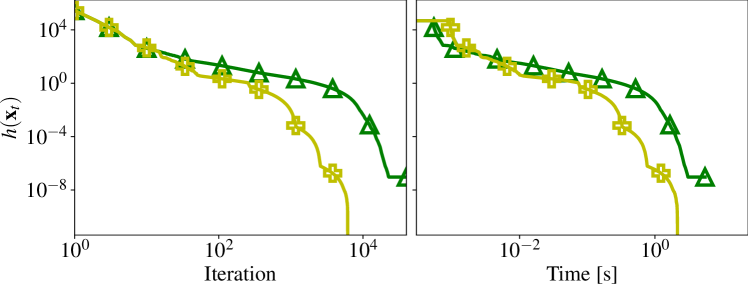

In Figure 9, we observe a plateau of the dual gap for both M-FW and B-AFW. The primal value however worsens after the iteration where B-AFW reaches its dual gap plateau. In contrast, M-FW reaches a plateau in both primal and dual gap at a certain iteration. Note that the primal value at the point where the plateau is hit is already below , the square root of the machine precision. The same instance and methods operating in arbitrary precision arithmetic are presented Figure 10. Instead of reaching a plateau or deteriorating, B-AFW closes the dual gap tolerance and terminates before other methods. Although this observation (made on several instances of the portfolio optimization problem) only impacts ill-conditioned problems, it suggests M-FW may be a good candidate for a numerically robust default implementation of Frank-Wolfe algorithms.

Function domain in the constraints

One of the arguments used to motivate the construction of FW algorithms for standard and generalized self-concordant minimization in prior work is the difficulty of handling objective functions with implicitly defined domains. We make several observations that highlight the relevance of this issue and justify the assumption of the availability of a Domain Oracle for . In the portfolio optimization example, all revenue vectors are assumed positive, and , it follows that all feasible points lie in . More generally ,for the logarithm of an affine function, verifying that a candidate lies in consists of a single affine transformation and element-wise comparison .

In the inverse covariance estimation problem, the information on can be added to the constraints by imposing , yielding a semi-definite optimization problem. The domain oracle consists of the computation of the smallest eigenvalue, which needs to be positive.

We can also modify the feasible region of the signal retrieval application using the KL divergence, resulting in a new feasible region so that . The objective is of the form:

where the data and are assumed to be entrywise positive, thus . Therefore we can define the set as the unit simplex. The domain of each function involved in the sum in has an open domain .

However, the positivity assumption on all these components could be relaxed. Without the positivity assumption on , the Domain Oracle would consist of verifying:

| (4.1) |

This verification can however be simplified by a preprocessing step if the number of data points is large by finding the minimal set of supporting hyperplanes in the polyhedral cone (4.1), which we can find by solving the following linear problem:

| (4.2a) | ||||

| s.t. | (4.2b) | |||

| (4.2c) | ||||

where is the dual variable associated with the inner product constraint. If the optimal solution of Problem (4.2a) is , the original problem is infeasible and the cone defined by (4.1) is empty. Otherwise the optimal will lie in the intersection of the closure of the polyhedral cone and the norm ball. Furthermore, the support of provides us with the non-redundant inequalities of the cone. Let be the matrix formed with the rows such that , then the Domain Oracle can be simplified to the verification that . The Distance Weighted Discrimination (DWT) model also considered in Dvurechensky et al. [2022] was initially presented in Marron et al. [2007], the denominator of each sum element is initially constrained to be nonnegative, which makes hold. Even without this additional constraint, the nonnegativity of all can be ensured with a minimum set of linear constraints in a fashion similar to the signal retrieval application, thus simplifying the Domain Oracle.

A stateless simple step variant.

The simple step-size strategy presented in Algorithm 2 ensures monotonicity and domain-respecting iterates by maintaining a “memory” which is the number of performed halvings. The number of halvings to reach an accepted step is bounded, but the corresponding factor is carried over in all following iterations, which may slow down progress. We propose an alternative step size that still ensures the monotonicity and domain-preserving properties, but does not carry over information from one iteration to the next.

Note that Algorithm 7, presented above, is stateless since it is equivalent to Algorithm 2 with reset to zero between every outer iteration. This resetting step also implies that the per-iteration convergence rate of the stateless step is at least as good as the simple step, at the potential cost of a bounded number of halvings, with associated ZOO and DOO calls at each iteration. Finally, we point out that the stateless step-size strategy can be viewed as a particular instance of a backtracking line search where the initial step size estimate is the agnostic step size .

We compare the two strategies on a random and badly conditioned problem with objective function:

where is a symmetric positive definite matrix with log-normally distributed eigenvalues and is the log-barrier function of the positive orthant. We optimize instances of this function over the -norm ball in dimension and . The results are shown in Figure 11 and 12 for and , respectively. On both of these instances, the simple step progress is slowed down or even seems stalled in comparison to the stateless version because a lot of halving steps were done in the early iterations for the simple step size, which penalizes progress over the whole run. The stateless step-size does not suffer from this problem, however, because the halvings have to be performed at multiple iterations when using the stateless step-size strategy, the per iteration cost of the stateless step-size is about three times that of the simple step-size. Future work will consider additional restart conditions, not only on of Algorithm 2, but also on the base step-size strategy employed, similar to Kerdreux et al. [2019].

|

|

|

|

Conclusion

We present in this paper a simple Frank-Wolfe variant that utilizes the open-loop step size strategy to obtain a convergence rate for generalized self-concordant functions in terms of primal gap and Frank-Wolfe gap, where is the iteration count. This algorithm neither requires second-order information, nor line searches. Moreover, the simple nature of the algorithm allows us to precisely bound the number of zeroth-order oracle, first-order oracle, domain oracle and linear optimization oracle calls that are needed to obtain a target accuracy in primal gap or Frank-Wolfe gap. This is in contrast to other existing bounds, which are only informative with respect to first-order and linear optimization oracle calls, and hide the zeroth-order and domain oracle complexity in line search procedures.

We also show improved convergence rates for several variants in various cases of interest and prove that the Away-step Frank-Wolfe algorithm [Wolfe, 1970, Lacoste-Julien & Jaggi, 2015] coupled with the backtracking line search of Pedregosa et al. [2020] can achieve linear convergence rates over polytopes when minimizing generalized self-concordant functions.

Acknowledgements

Research reported in this paper was partially supported through the Research Campus Modal funded by the German Federal Ministry of Education and Research (fund numbers 05M14ZAM,05M20ZBM) and the Deutsche Forschungsgemeinschaft (DFG) through the DFG Cluster of Excellence MATH+. We would like to thank the anonymous reviewers for their suggestions and comments.

References

- Bach [2010] Bach, F. Self-concordant analysis for logistic regression. Electronic Journal of Statistics, 4:384–414, 2010.

- Besançon et al. [2022] Besançon, M., Carderera, A., and Pokutta, S. FrankWolfe.jl: a high-performance and flexible toolbox for Frank-Wolfe algorithms and conditional gradients. INFORMS Journal on Computing, 34(5):2611–2620, 2022.

- Carderera et al. [2021] Carderera, A., Besançon, M., and Pokutta, S. Frank-Wolfe for Generalized Self-Concordant Functions - Problem Instances, May 2021. URL https://doi.org/10.5281/zenodo.4836009.

- Csiszar [1991] Csiszar, I. Why least squares and maximum entropy? An axiomatic approach to inference for linear inverse problems. The annals of statistics, 19(4):2032–2066, 1991.

- Diakonikolas et al. [2020] Diakonikolas, J., Carderera, A., and Pokutta, S. Locally accelerated conditional gradients. In Proceedings of the 23th International Conference on Artificial Intelligence and Statistics, pp. 1737–1747. PMLR, 2020.

- Dvurechensky et al. [2020] Dvurechensky, P., Ostroukhov, P., Safin, K., Shtern, S., and Staudigl, M. Self-concordant analysis of Frank-Wolfe algorithms. In Proceedings of the 37th International Conference on Machine Learning, pp. 2814–2824. PMLR, 2020.

- Dvurechensky et al. [2022] Dvurechensky, P., Safin, K., Shtern, S., and Staudigl, M. Generalized self-concordant analysis of Frank–Wolfe algorithms. Mathematical Programming, pp. 1–69, 2022.

- Frank & Wolfe [1956] Frank, M. and Wolfe, P. An algorithm for quadratic programming. Naval research logistics quarterly, 3(1-2):95–110, 1956.

- Garber & Hazan [2016] Garber, D. and Hazan, E. A linearly convergent variant of the conditional gradient algorithm under strong convexity, with applications to online and stochastic optimization. SIAM Journal on Optimization, 26(3):1493–1528, 2016.

- Guélat & Marcotte [1986] Guélat, J. and Marcotte, P. Some comments on Wolfe’s ‘away step’. Mathematical Programming, 35(1):110–119, 1986.

- Jaggi [2013] Jaggi, M. Revisiting Frank-Wolfe: Projection-free sparse convex optimization. In Proceedings of the 30th International Conference on Machine Learning, pp. 427–435. PMLR, 2013.

- Kerdreux et al. [2019] Kerdreux, T., d’Aspremont, A., and Pokutta, S. Restarting Frank-Wolfe. In Proceedings of the 22nd International Conference on Artificial Intelligence and Statistics, pp. 1275–1283. PMLR, 2019.

- Kerdreux et al. [2021] Kerdreux, T., d’Aspremont, A., and Pokutta, S. Projection-free optimization on uniformly convex sets. In Proceedings of the 24th International Conference on Artificial Intelligence and Statistics, pp. 19–27. PMLR, 2021.

- Krishnan et al. [2015] Krishnan, R. G., Lacoste-Julien, S., and Sontag, D. Barrier Frank-Wolfe for Marginal Inference. In Proceedings of the 28th Conference in Neural Information Processing Systems. PMLR, 2015.

- Lacoste-Julien & Jaggi [2015] Lacoste-Julien, S. and Jaggi, M. On the global linear convergence of Frank-Wolfe optimization variants. In Proceedings of the 29th Conference on Neural Information Processing Systems, pp. 566–575. PMLR, 2015.

- Levitin & Polyak [1966] Levitin, E. S. and Polyak, B. T. Constrained minimization methods. USSR Computational Mathematics and Mathematical Physics, 6(5):1–50, 1966.

- Liu et al. [2020] Liu, D., Cevher, V., and Tran-Dinh, Q. A newton frank–wolfe method for constrained self-concordant minimization. Journal of Global Optimization, pp. 1–27, 2020.

- Marron et al. [2007] Marron, J. S., Todd, M. J., and Ahn, J. Distance-weighted discrimination. Journal of the American Statistical Association, 102(480):1267–1271, 2007.

- Marteau-Ferey et al. [2019] Marteau-Ferey, U., Ostrovskii, D., Bach, F., and Rudi, A. Beyond least-squares: Fast rates for regularized empirical risk minimization through self-concordance. In Proceedings of the 32nd Conference on Learning Theory, pp. 2294–2340. PMLR, 2019.

- Nesterov [2013] Nesterov, Y. Gradient methods for minimizing composite functions. Mathematical Programming, 140(1):125–161, 2013.

- Nesterov [2018] Nesterov, Y. Lectures on convex optimization, volume 137. Springer, 2018.

- Nesterov & Nemirovskii [1994] Nesterov, Y. and Nemirovskii, A. Interior-point polynomial algorithms in convex programming. SIAM, 1994.

- Odor et al. [2016] Odor, G., Li, Y.-H., Yurtsever, A., Hsieh, Y.-P., Tran-Dinh, Q., El Halabi, M., and Cevher, V. Frank-wolfe works for non-lipschitz continuous gradient objectives: scalable poisson phase retrieval. In 2016 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP), pp. 6230–6234. Ieee, 2016.

- Ostrovskii & Bach [2021] Ostrovskii, D. M. and Bach, F. Finite-sample analysis of M-estimators using self-concordance. Electronic Journal of Statistics, 15(1):326–391, 2021.

- Pedregosa et al. [2020] Pedregosa, F., Negiar, G., Askari, A., and Jaggi, M. Linearly convergent Frank–Wolfe with backtracking line-search. In Proceedings of the 23rd International Conference on Artificial Intelligence and Statistics. PMLR, 2020.

- Rothvoß [2017] Rothvoß, T. The matching polytope has exponential extension complexity. Journal of the ACM (JACM), 64(6):1–19, 2017.

- Sun & Tran-Dinh [2019] Sun, T. and Tran-Dinh, Q. Generalized self-concordant functions: a recipe for Newton-type methods. Mathematical Programming, 178(1):145–213, 2019.

- Temlyakov [2015] Temlyakov, V. Greedy approximation in convex optimization. Constructive Approximation, 41(2):269–296, 2015.

- Tran-Dinh et al. [2015] Tran-Dinh, Q., Li, Y.-H., and Cevher, V. Composite convex minimization involving self-concordant-like cost functions. In Modelling, Computation and Optimization in Information Systems and Management Sciences, pp. 155–168. Springer, 2015.

- Tsuji et al. [2022] Tsuji, K. K., Tanaka, K., and Pokutta, S. Pairwise conditional gradients without swap steps and sparser kernel herding. In International Conference on Machine Learning, pp. 21864–21883. PMLR, 2022.

- Wolfe [1970] Wolfe, P. Convergence theory in nonlinear programming. In Integer and Nonlinear Programming, pp. 1–36. North-Holland, Amsterdam, 1970.

- Zhao & Freund [2023] Zhao, R. and Freund, R. M. Analysis of the Frank–Wolfe method for convex composite optimization involving a logarithmically-homogeneous barrier. Mathematical Programming, 199(1-2):123–163, 2023.