Conic Blackwell Algorithm: Parameter-Free Convex-Concave Saddle-Point Solving

Abstract

We develop new parameter-free and scale-free algorithms for solving convex-concave saddle-point problems. Our results are based on a new simple regret minimizer, the Conic Blackwell Algorithm+ (CBA+), which attains average regret. Intuitively, our approach generalizes to other decision sets of interest ideas from the Counterfactual Regret minimization (CFR+) algorithm, which has very strong practical performance for solving sequential games on simplexes. We show how to implement CBA+ for the simplex, norm balls, and ellipsoidal confidence regions in the simplex, and we present numerical experiments for solving matrix games and distributionally robust optimization problems. Our empirical results show that CBA+ is a simple algorithm that outperforms state-of-the-art methods on synthetic data and real data instances, without the need for any choice of step sizes or other algorithmic parameters.

1 Introduction

We are interested in solving saddle-point problems (SPPs) of the form

| (1) |

where are convex, compact sets, and is a subdifferentiable convex-concave function. Convex-concave SPPs arise in a number of practical problems. For example, the problem of computing a Nash equilibrium of a zero-sum games can be formulated as a convex-concave SPP, and this is the foundation of most methods for solving sequential zero-sum games (von Stengel, 1996; Zinkevich et al., 2007; Tammelin et al., 2015; Kroer et al., 2020). They also arise in imaging (Chambolle and Pock, 2011), -regression (Sidford and Tian, 2018), Markov Decision Processes (Iyengar, 2005; Wiesemann et al., 2013; Sidford and Tian, 2018), and in distributionally robust optimization, where the max term represents the distributional uncertainty (Namkoong and Duchi, 2016; Ben-Tal et al., 2015). In this paper we propose efficient, parameter-free algorithms for solving (1) in many settings, i.e., algorithms that do not require any tuning or choices of step sizes.

Repeated game framework

One way to solve convex-concave SPPs is by viewing the SPP as a repeated game between two players, where each step consists of one player choosing , the other player choosing , and then the players observe the payoff . If each player employs a regret-minimization algorithm, then a well-known folk theorem says that the uniform average strategy generated by two regret minimizers repeatedly playing an SPP against each other converges to a solution to the SPP. We will call this the “repeated game framework” (see Section 2). There are already well-known algorithms for instantiating the above repeated game framework for (1). For example, one can employ the online mirror descent (OMD) algorithm, which generates iterates as follows for the first player (and similarly for the second player):

| (2) |

where ( denotes here the set of subgradients as regards the variable ), is a Bregman divergence which measures distance between pairs of points, and is an appropriate step size. By choosing appropriately for , the update step (2) becomes efficient, and one can achieve an overall regret on the order of after iterations. This regret can be achieved either by choosing a fixed step size , where an upper bound on the norms of the subgradients visited , or by choosing adaptive step sizes , for . This is problematic, as 1) the upper bound may be hard to obtain in many applications and may be too conservative in practice, and 2) adequately tuning the parameter can be time- and resource-consuming, and even practically infeasible for very large instances, since we won’t know if the step size will cause a divergence until late in the optimization process. This is not just a theoretical issue, as we highlight in our numerical experiments (Section 4) and in the appendices (Appendices F). Similar results and challenges hold for the popular follow the regularized leader (FTRL) algorithm (see Appendix F).

The above issues can be circumvented by employing adaptive variants of OMD or FTRL, which lead to parameter- and scale-free algorithms that estimate the parameters through the observed subgradients, e.g., AdaHedge for the simplex setting (De Rooij et al., 2014) or AdaFTRL for general compact convex decisions sets (Orabona and Pál, 2015). Yet these adaptive variants have not seen practical adoption in large-sale game-solving, where regret-matching variants are preferred (see the next paragraph). As we show in our experiments, adaptive variants of OMD and FTRL perform much worse than our proposed algorithms. While these adaptive algorithms are referred to as parameter-free, this is only true in the sense that they are able to learn the necessary parameters. Our algorithm is parameter-free in the stronger sense that there are no parameters that even require learning. Formalizing this difference may be one interesting avenue for explaining the performance discrepancy on saddle-point problems.

Regret Matching

In this paper, we introduce alternative regret-minimization schemes for instantiating the above framework. Our work is motivated by recent advances on solving large-scale zero-sum sequential games. In the zero-sum sequential game setting, and are simplexes, the objective function becomes , and thus (1) reduces to a bilinear SPP. Based on this bilinear SPP formulation, the best practical methods for solving large-scale sequential games use the repeated game framework, where each player minimizes regret via some variant of counterfactual regret minimization (CFR, (Zinkevich et al., 2007)). Variants of CFR were used in every recent poker AI challenge, where poker AIs beat human poker players (Bowling et al., 2015; Moravčík et al., 2017; Brown and Sandholm, 2018, 2019). The CFR framework itself is a decomposition of the overall regret of the bilinear SPP into local regrets at each decision point in a sequential game (Farina et al., 2019a). The key to the practical performance of CFR-based algorithms seems to be three ingredients (beyond the CFR decomposition itself): (1) a particular regret minimizer called regret matching+ (RM+) (Tammelin et al., 2015) which is employed at each decision point, (2) aggressive iterate averaging schemes that put greater weight on recent iterates (e.g. linear averaging, which weights iterate at period by ), and (3) an alternation scheme where the updates of the repeated game framework are performed in an asymmetric fashion. The CFR framework itself is specific to sequential bilinear games on simplexes, but these last three ingredients could potentially be generalized to other problems of the form (1). That is the starting point of the present paper.

The most challenging aspect of generalizing the above ingredients is that RM+ is specifically designed for minimizing regret over a simplex. However, many problems of the form (1) have convex sets that are not simplexes, e.g., box constraints or norm-balls for distributionally robust optimization (Ben-Tal et al., 2015). In principle, regret matching arises from a general theory called Blackwell approachability (Blackwell, 1956; Hart and Mas-Colell, 2000), and similar constructions can be envisioned for other convex sets. However, in practice the literature has only focused on developing concrete implementable instantiations of Blackwell approachability for simplexes. A notable deviation from this is the work of Abernethy et al. (2011), who showed a general reduction between regret minimization over general convex compact sets and Blackwell approachability. However, their general reduction still does not yield a practically implementable algorithm: among other things, their reduction relies on certain black-box projections that are not always efficient. We show how to implement these necessary projections for the setting where and are simplexes, balls, and intersections of the ball with a hyperplane (with a focus on the case where an ball is intersected with a simplex, which arises naturally as confidence regions). This yields an algorithm which we will refer to as the conic Blackwell algorithm (CBA), which is similar in spirit to the regret matching algorithm, but crucially generalizes to other decision sets. Motivated by the practical performance of RM+, we construct a variant of CBA which uses a thresholding operation similar to the one employed by RM+. We call this algorithm CBA+.

Our contributions

We introduce CBA+, a parameter-free algorithm which achieves regret in the worst-case and generalizes the strong performances of RM+ for bilinear, simplex saddle-points solving to other more general settings. A major selling point for CBA+ is that it does not require any step size choices. Instead, the algorithm implicitly adjusts to the structure of the domains and losses by being instantiations of Blackwell’s approachability algorithm. After developing the CBA+ algorithm, we then develop analogues of another crucial components for large-scale game solving. In particular, we prove a generalization of the folk theorem for the repeated game framework for solving (1), which allows us to incorporate polynomial averaging schemes such as linear averaging. We then show that CBA+ is compatible with linear averaging on the iterates. This mirrors the case of RM and RM+, where only RM+ is compatible with linear averaging on the iterates. We also show that both CBA and CBA+ are compatible with polynomial averaging when simultaneously performed on the regrets and the iterates. Combining all these ingredients, we arrive at a new class of algorithms for solving convex-concave SPPs. As long as efficient projection operations can be performed (which we show for several practical domains, including the simplex, balls and confidence regions in the simplex), one can apply the repeated game framework on (1), where one can use either CBA or CBA+ as a regret minimizer for and along with polynomial averaging on the generated iterates to solve (1) at a rate of .

We highlight the practical efficacy of our algorithmic framework on several domains. First, we solve two-player zero-sum matrix games and extensive-form games, where RM+ regret minimizer combined with linear averaging and alternation, and CFR+, lead to very strong practical algorithms (Tammelin et al., 2015). We find that CBA+ combined with linear averaging and alternation leads to a comparable performance in terms of the iteration complexity, and may even slightly outperform RM+ and CFR+. On this simplex setting, we also find that CBA+ outperforms both AdaHedge and AdaFTRL. Second, we apply our approach to a setting where RM+ and CFR+ do not apply: distributionally robust empirical risk minimization (DR-ERM) problems. Across two classes of synthetic problems and four real data sets, we find that our algorithm based on CBA+ performs orders of magnitude better than online mirror descent and FTRL, as well as their optimistic variants, when using their theoretically-correct fixed step sizes. Even when considering adaptive step sizes, or fixed step sizes that are up to larger than those predicted by theory, our CBA+ algorithm performs better, with only a few cases of comparable performance (at step sizes that lead to divergence for some of the other non-parameter free methods). The fast practical performance of our algorithm, combined with its simplicity and the total lack of step sizes or parameters tuning, suggests that it should be seriously considered as a practical approach for solving convex-concave SPPs in various settings.

Finally, we make a brief note on accelerated methods. Our algorithms have a rate of convergence towards a saddle point of , similar to OMD and FTRL. In theory, it is possible to obtain a faster rate of convergence when is differentiable with Lipschitz gradients, for example via mirror prox (Nemirovski, 2004) or other primal-dual algorithms (Chambolle and Pock, 2016). However, our experimental results show that CBA+ is faster than optimistic variants of FTRL and OMD (Syrgkanis et al., 2015), the latter being almost identical to the mirror prox algorithm, and both achieving rate of convergence. A similar conclusion has been drawn in the context of sequential game solving, where the fastest CFR-based algorithms have better practical performance than the theoretically-superior -rate methods (Kroer et al., 2020, 2018). In a similar vein, using error-bound conditions, it is possible to achieve a linear rate, e.g., when solving bilinear saddle-point problems over polyhedral decision sets using the extragradient method (Tseng, 1995) or optimistic gradient descent-ascent (Wei et al., 2020). However, these linear rates rely on unknown constants, and may not be indicative of practical performance.

2 Game setup and Blackwell Approachability

As stated in section 1, we will solve (1) using a repeated game framework. The first player chooses strategies from in order to minimize the sequence of payoffs in the repeated game, while the second player chooses strategies from in order to maximize payoffs. There are iterations with indices . In this framework, each iteration consists of the following steps:

-

1.

Each player chooses strategies

-

2.

First player observes and uses when computing the next strategy

-

3.

Second player observes and uses when computing the next strategy

The goal of each player is to minimize their regret across the iterations:

The reason this repeated game framework leads to a solution to the SPP problem (1) is the following folk theorem. Relying on being convex-concave and subdifferentiable, it connects the regret incurred by each player to the duality gap in (1).

Theorem 2.1 (Theorem 1, Kroer (2020)).

Let for any . Then

Therefore, when each player runs a regret minimizer that guarantees regret on the order of , converges to a solution to (1) at a rate of . Later we will show a generalization of Theorem 2.1 that will allow us to incorporate more aggressive averaging schemes that put additional weight on the later iterates. Given the repeated game framework, the next question becomes which algorithms to employ in order to minimize regret for each player. As mentioned in Section 1, for zero-sum games, variants of regret matching are used in practice.

Blackwell Approachability

Regret matching arises from the Blackwell approachability framework (Blackwell, 1956). In Blackwell approachability, a decision maker repeatedly takes decisions from some convex decision set (this set plays the same role as or in (1)). After taking decision the player observes a vector-valued affine payoff function . The goal for the decision maker is to force the average payoff to approach some convex target . Blackwell proved that a convex target set can be approached if and only if for every halfspace , there exists such that for every possible payoff function , is guaranteed to lie in . The action is said to force . Blackwell’s proof is via an algorithm: at iteration , his algorithm projects the average payoff onto , and then the decision maker chooses an action that forces the tangent halfspace to generated by the normal , where is the orthogonal projection of onto . We call this algorithm Blackwell’s algorithm; it approaches at a rate of . It is important to note here that Blackwell’s algorithm is rather a meta-algorithm than a concrete algorithm. Even within the context of Blackwell’s approachability problem, one needs to devise a way to compute the forcing actions needed at each iteration, i.e., to compute .

Details on Regret Matching

Regret matching arises by instantiating Blackwell approachability with the decision space equal to the simplex , the target set equal to the nonpositive orthant , and the vector-valued payoff function equal to the regret associated to each of the actions (which correspond to the corners of ). Here has one on every component. Hart and Mas-Colell (2000) showed that with this setup, playing each action with probability proportional to its positive regret up to time satisfies the forcing condition needed in Blackwell’s algorithm. Formally, regret matching (RM) keeps a running sum , and then action is played with probability , where denotes thresholding at zero. By Blackwell’s approachability theorem, this algorithm converges to zero average regret at a rate of . In zero-sum game-solving, it was discovered that a variant of regret matching leads to extremely strong practical performance (but the same theoretical rate of convergence). In regret matching+ (RM+), the running sum is thresholded at zero at every iteration: , and then actions are again played proportional to . In the next section, we describe a more general class of regret-minimization algorithms based on Blackwell’s algorithm for general sets , introduced in Abernethy et al. (2011). Note that a similar construction of a general class of algorithms can be achieved through the Lagrangian Hedging framework of Gordon (2007). It would be interesting to construct a CBA+-like algorithm and efficient projection approaches for this framework as well.

3 Conic Blackwell Algorithm

We present the Conic Blackwell Algorithm Plus (CBA+), a no-regret algorithm which uses a variation of Blackwell’s approachability procedure (Blackwell, 1956) to perform regret minimization on general convex compact decision sets . We will assume that losses are coming from a bounded set; this occurs, for example, if there exists (that we do not need to know), such that

| (3) |

CBA+ is best understood as a combination of two steps. The first is the basic CBA algorithm, derived from Blackwell’s algorithm, which we describe next. To convert Blackwell’s algorithm to a regret minimizer on , we use the reduction from Abernethy et al. (2011), which considers the conic hull where . The Blackwell approachability problem is then instantiated with as the decision set, target set equal to the polar of , and payoff vectors . The conic Blackwell algorithm (CBA) is implemented by projecting the average payoff vector onto , calling this projection with and , and playing the action .

The second step in CBA+ is to modify CBA to make it analogous to RM+ rather than to RM. To do this, the algorithm does not keep track of the average payoff vector. Instead, we keep a running aggregation of the payoffs, where we always add the newest payoff to the aggregate, and then project the aggregate onto . More concretely, pseudocode for CBA+ is given in Algorithm 1. This pseudocode relies on two functions: , which maps the aggregate payoff vector to a decision in , and which controls how we aggregate payoffs. Given an aggregate payoff vector , we have

If , we just let for some chosen .

The function is implemented by adding the most recent payoff to the aggregate payoffs, and then projecting onto . More formally, it is defined as

where is the weight assigned to the most recent payoff and the weight assigned to the previous aggregate payoff . Because of the projection step in , we always have , which in turn guarantees that , since .

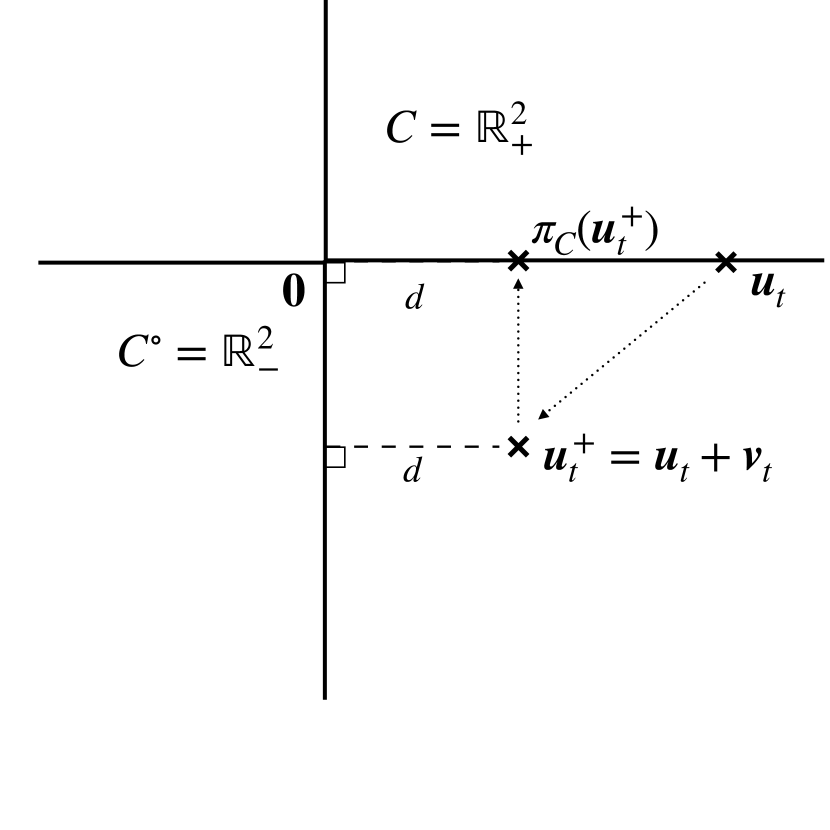

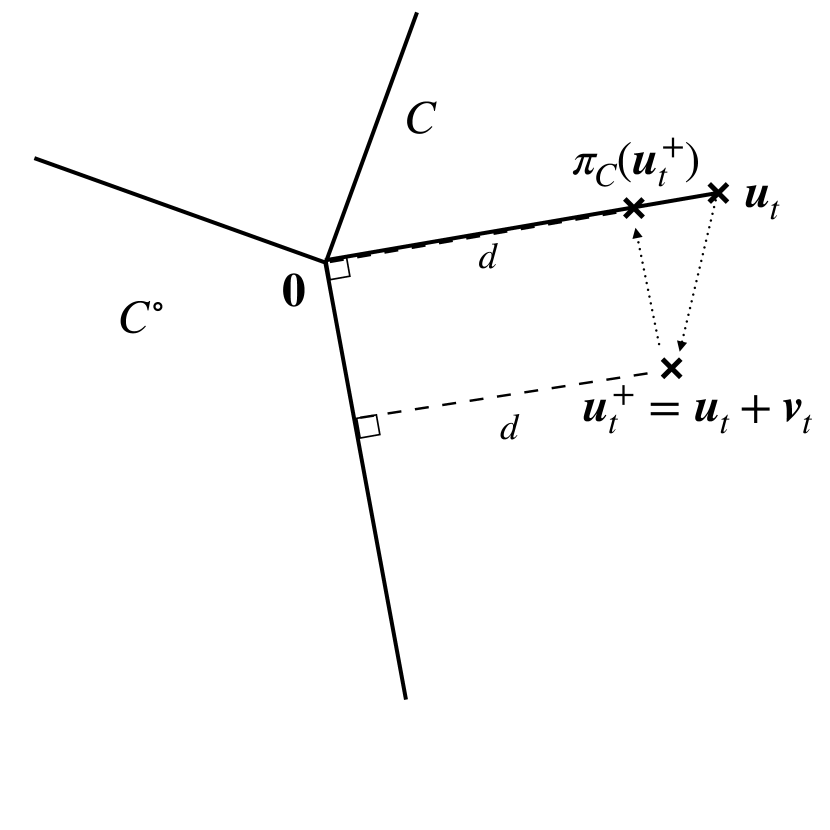

Let us give some intuition on the effect of projection onto . In a geometric sense, it is easier to visualize things in with and . The projection on moves the vector along the edges of , maintaining the distance to and moving toward the vector . This is illustrated in Figure 5 in Appendix B.1. From a game-theoretic standpoint, the projection on eliminates the components of the payoffs that are negative. It enables CBA+ to be less pessimistic than CBA, which may accumulate negative payoffs on actions for a long time and never resets the components of the aggregated payoff to , leading to some actions being chosen less frequently.

We will see in the next section that RM+ is related to CBA+ but replaces the exact projection step in by a suboptimal solution to the projection problem. Let us also note the difference between CBA+ and the algorithm introduced in Abernethy et al. (2011), which we have called CBA. CBA uses different UPDATEPAYOFF and CHOOSEDECISION functions. In CBA the payoff update is defined as

Note in particular the lack of projection as compared to CBA+, analogous to the difference between RM and RM+. The function then requires a projection onto :

Based upon the analysis in Blackwell (1956), Abernethy et al. (2011) show that CBA with uniform weights (both on payoffs and decisions) guarantees average regret. The difference between CBA+ and CBA is similar to the difference between the RM and RM+ algorithms. In practice, RM+ performs significantly better than RM for solving matrix games, when combined with linear averaging on the decisions (as opposed to the uniform averaging used in Theorem 2.1). In the next theorem, we show that CBA+ is compatible with linear averaging on decisions only. We present a detailed proof in Appendix B.

Theorem 3.1.

Consider generated by CBA+ with uniform weights: . Let and . Then

Note that in Theorem 3.1, we have uniform weights on the sequence of payoffs , but linearly increasing weights on the sequence of decisions. The proof relies on properties specific to CBA+, and it does not extend to CBA. Numerically it also helps CBA+ but not CBA. In Appendix B, we show that both CBA and CBA+ achieve convergence rates when using a weighted average on both the decisions and the payoffs (Theorems B.2-B.3). In practice, using linear averaging only on the decisions, as in Theorem 3.1, performs vastly better than linear averaging on both decisions and payoffs. We present empirical evidence of this in Appendix B.

We can compare the average regret for CBA+ with the average regret for OMD (Nemirovski and Yudin, 1983; Ben-Tal and Nemirovski, 2001) and FTRL (Abernethy et al., 2009; McMahan, 2011), where We can always recenter to contain , in which case the bounds for OMD/FTRL and CBA+ are equivalent since . Note that the bound on the average regret for Optimistic OMD (O-OMD, Chiang et al. (2012)) and Optimistic FTRL (O-FTRL, Rakhlin and Sridharan (2013)) is in the game setup, a priori better than the bound for CBA+ as regards the number of iterations . Nonetheless, we will see in Section 4 that the empirical performance of CBA+ is better than that of methods. A similar situation occurs for RM+ compared to O-OMD and O-FTRL for solving poker games (Farina et al., 2019b; Kroer et al., 2020).

The following theorem gives the convergence rate of CBA+ for solving saddle-points (1), based on our convergence rate on the regret of each player (Theorem 3.1). The proof is in Appendix C.

Theorem 3.2.

Let where are generated by the repeated game framework with CBA+ with uniform weights: . Let defined in (3) and . Then

3.1 Efficient implementations of CBA+

To obtain an implementation of CBA+ and CBA, we need to efficiently resolve the functions and . In particular, we need to compute , the orthogonal projection of onto the cone , where :

| (4) |

Even for CBA this problem must be resolved, since Abernethy et al. (2011) did not study whether (4) can be efficiently solved. It turns out that (4) can be computed in closed-form or quasi closed-form for many decision sets of interest. Interestingly, parts of the proofs rely on Moreau’s Decomposition Theorem (Combettes and Reyes, 2013), which states that can be recovered from and vice-versa, because We present the detailed complexity results and the proofs in Appendix D.

Simplex

is the classical setting used for matrix games. Also, for extensive-form games, CFR decomposes the decision sets (treeplexes) into a set of regret minimization problems over the simplex (Farina et al., 2019a). Here, is the number of actions of a player and represents a randomized strategy. In this case, can be computed in . Note that RM and RM+ are obtained by choosing a suboptimal solution to (4), avoiding the sorting operation, whereas CBA and CBA+ choose optimally (see Appendix D). Thus, RM and RM+ can be seen as approximate versions of CBA and CBA+, where (4) is solved approximatively at every iteration. In our numerical experiments, we will see that CBA+ slightly outperforms RM+ and CFR+ in terms of iteration count.

balls

This is when with or . This is of interest for instance in distributionally robust optimization (Ben-Tal et al., 2015; Namkoong and Duchi, 2016), regression (Sidford and Tian, 2018) and saddle-point reformulation of Markov Decision Process (Jin and Sidford, 2020). For , we can compute in closed-form, i.e., in arithmetic operations. For , we can compute in arithmetic operations using a sorting algorithm.

Ellipsoidal confidence region in the simplex

Here, is an ellipsoidal subregion of the simplex, defined as . This type of decision set is widely used because it is associated with confidence regions when estimating a probability distribution from observed data (Iyengar, 2005; Bertsimas et al., 2019). It can also be used in the Bellman update for robust Markov Decision Process (Iyengar, 2005; Wiesemann et al., 2013; Goyal and Grand-Clément, 2018). We also assume that the confidence region is “entirely contained in the simplex”: , to avoid degenerate components. In this case, using a change of basis we show that it is possible to compute in closed-form, i.e., in arithmetic operations.

Other potential sets of interests

Other important decision sets include sets based on Kullback-Leibler divergence , or, more generally, -divergence (Ben-Tal et al., 2013). For these sets, we did not find a closed-form solution to the projection problem (4). Still, as long as the domain is a convex set, computing remains a convex problem, and it can be solved efficiently with solvers, although this results in a slower algorithm than with closed-form computations of .

4 Numerical experiments

In this section we investigate the practical performances of our algorithms on several instances of saddle-point problems. We start by comparing CBA+ with RM+ in the matrix and extensive-form games setting. We then turn to comparing our algorithms on instances from the distributionally robust optimization literature. The code for all experiments is available in the supplemental material.

4.1 Matrix games on the simplex and Extensive-Form Games

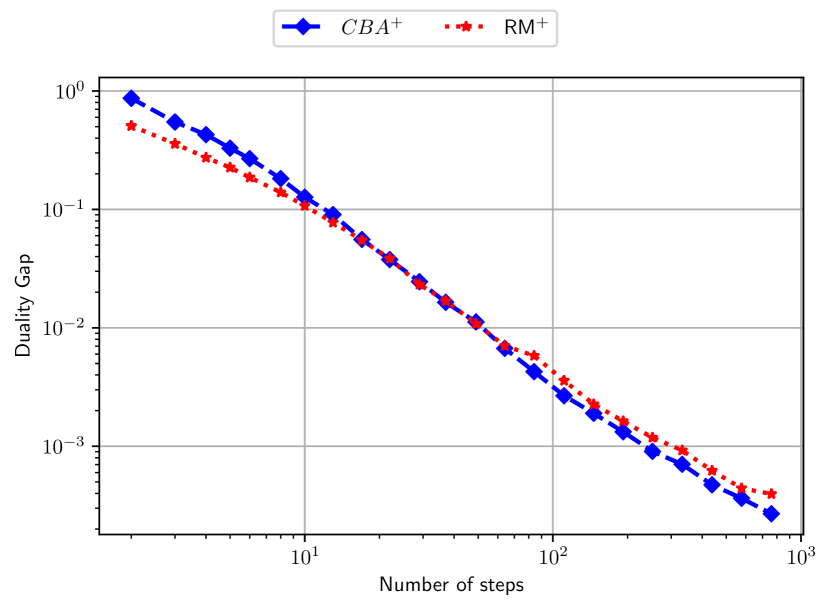

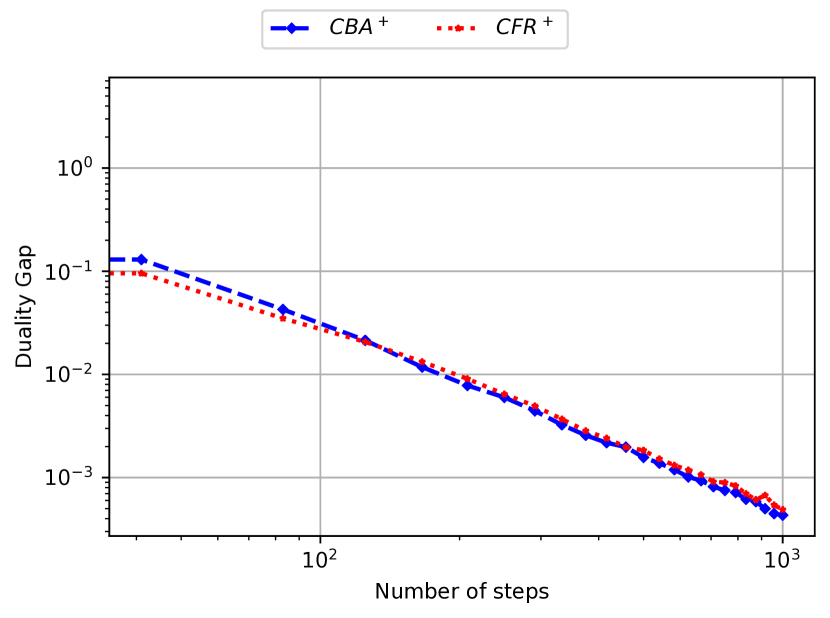

Since the motivation for CBA+ is to obtain the strong empirical performances of RM+ and CFR+ on other decision sets than the simplex, we start by checking that CBA+ indeed provide comparable performance on simplex settings. We compare these methods on matrix games

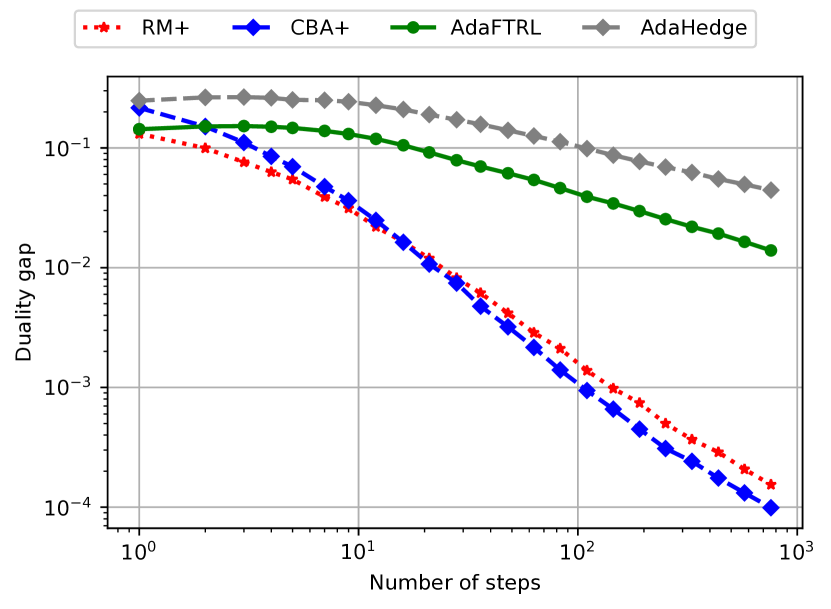

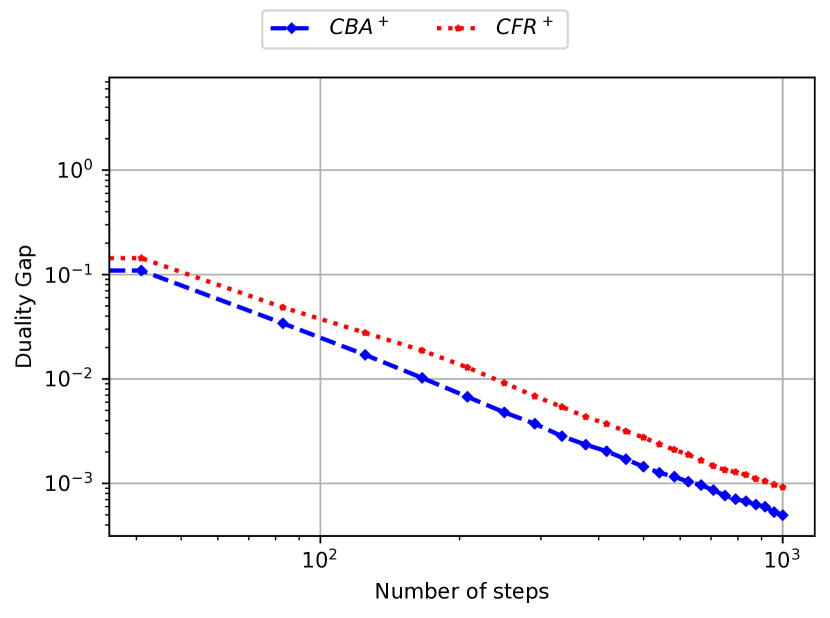

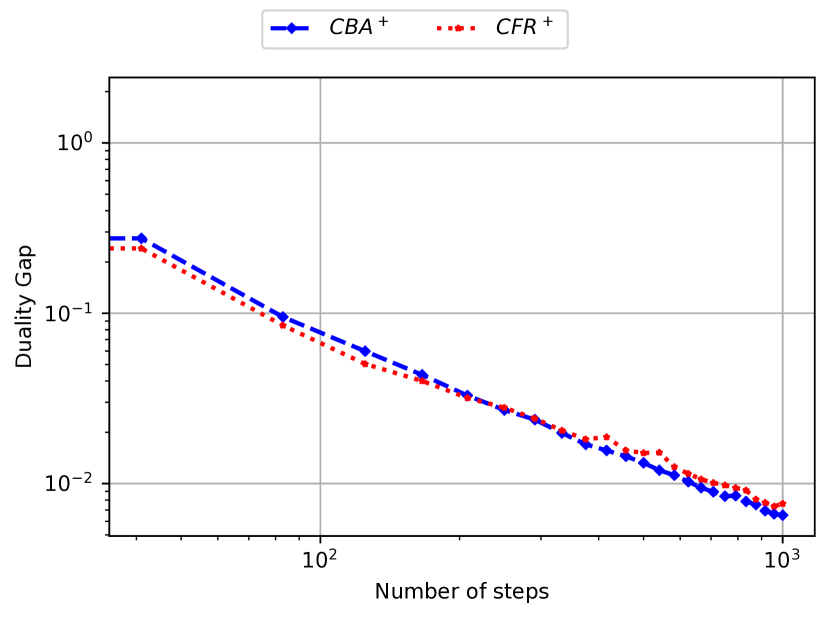

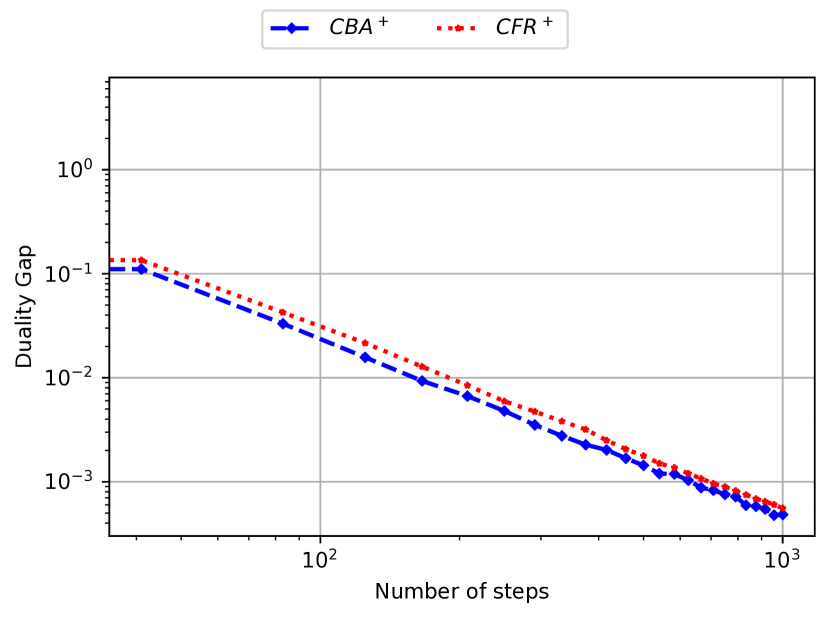

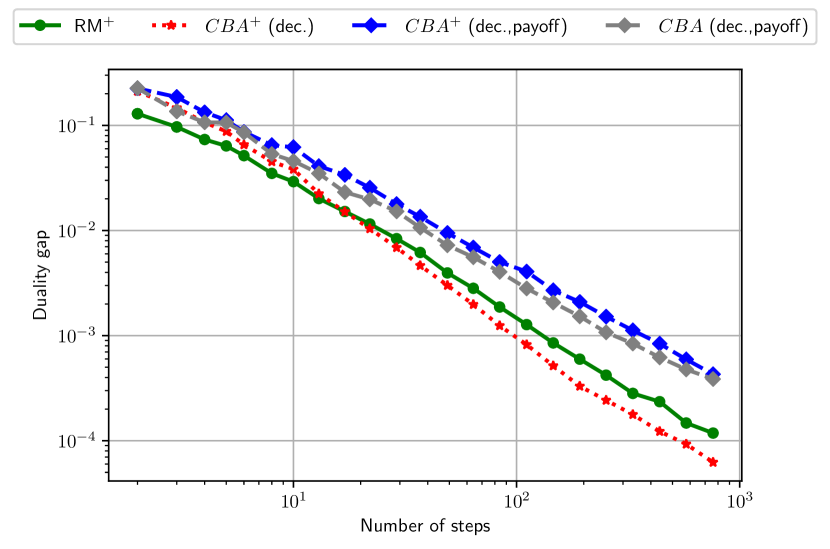

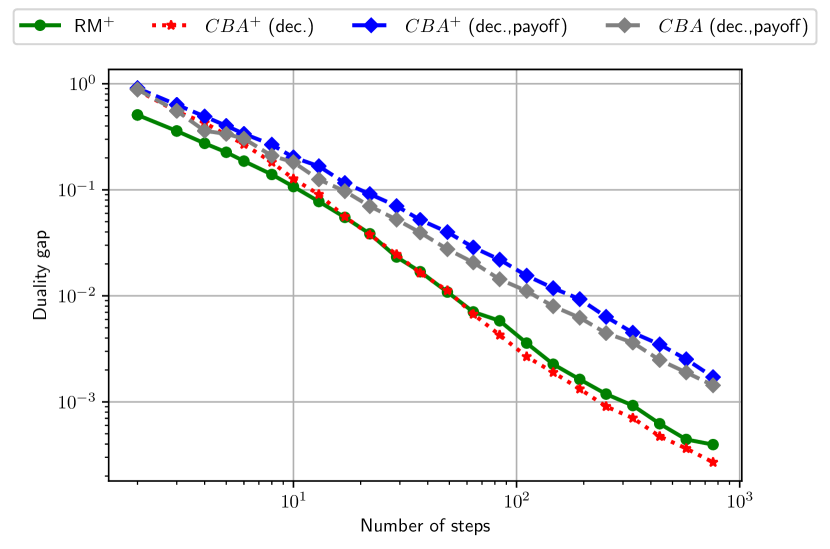

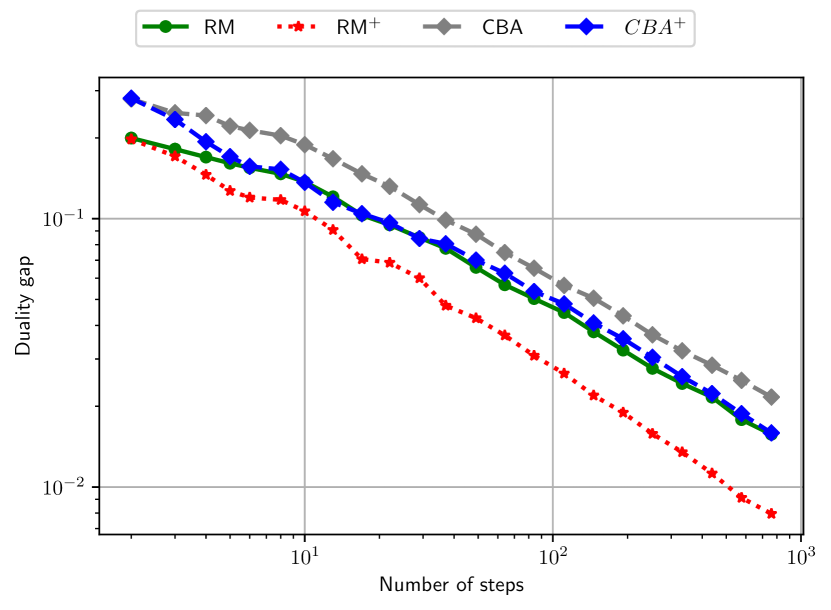

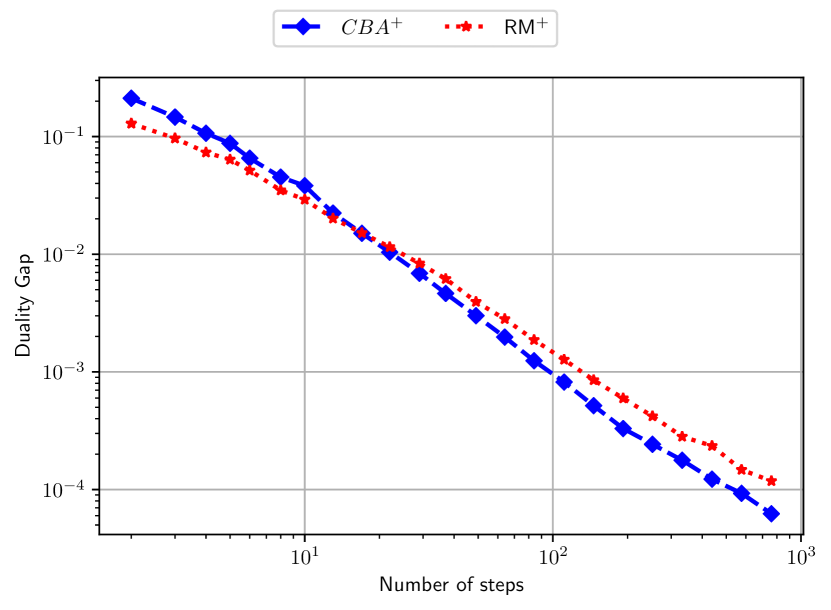

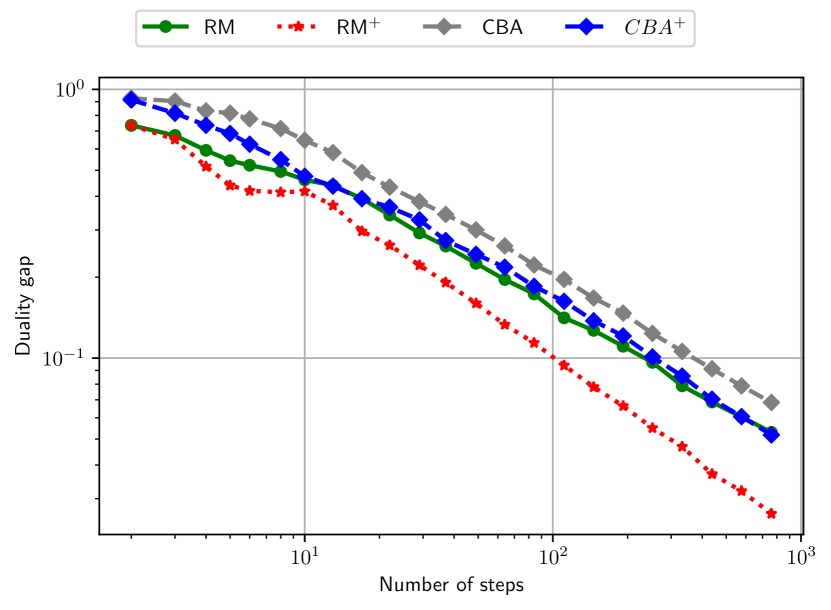

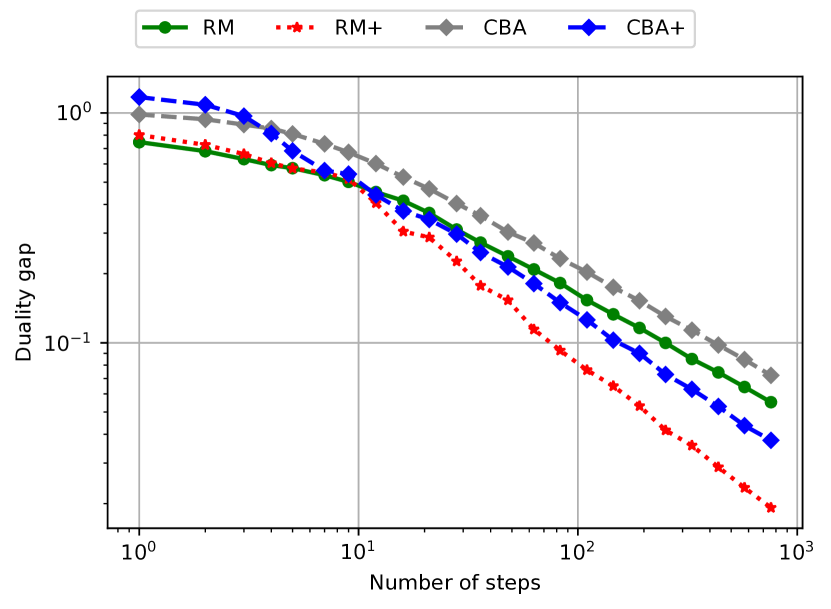

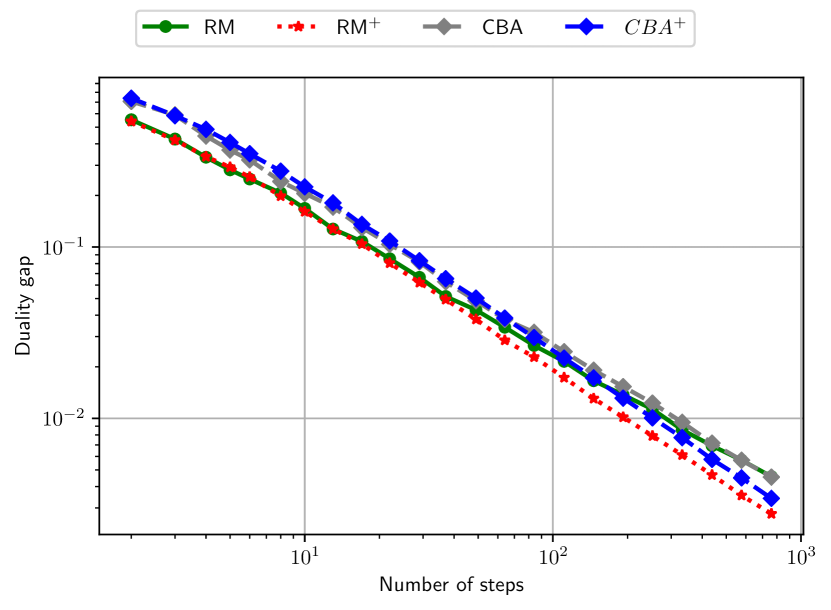

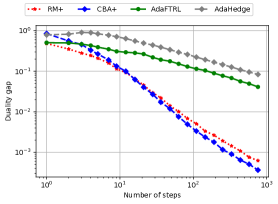

where is the matrix of payoff, and on extensive-form games (EFGs). EFGs can also be written as SPPs with bilinear objective and polytopes encoding the players’ space of sequential strategies (von Stengel, 1996). EFGs can be solved via simplex-based regret minimization by using the counterfactual regret minimization (CFR) framework to decompose regrets into local regrets at each simplex. Explaining CFR is beyond the scope of this work; we point the reader to (Zinkevich et al., 2007) or newer explanations (Farina et al., 2019c, a). For matrix games, we generate 70 synthetic -dimensional matrix games with and compare the most efficient algorithms for matrix games with linear averaging: CBA+ and RM+. We also compare with two other scale-free no-regret algorithms, AdaHedge (De Rooij et al., 2014) and AdaFTRL (Orabona and Pál, 2015). Figure 1(a) presents the duality gap of the current solutions vs. the number of steps. Here, both CBA+ and RM+ use alternation, which is a trick that is well-known to improve the performances of RM+ (Tammelin et al., 2015), where the repeated game framework is changed such that players take turns updating their strategies, rather than performing these updates simultaneously, see Appendix E.1 for details.111We note that RM+ is guaranteed to retain its convergence rate under alternation. In contrast, we leave resolving this property for CBA+ to future work.

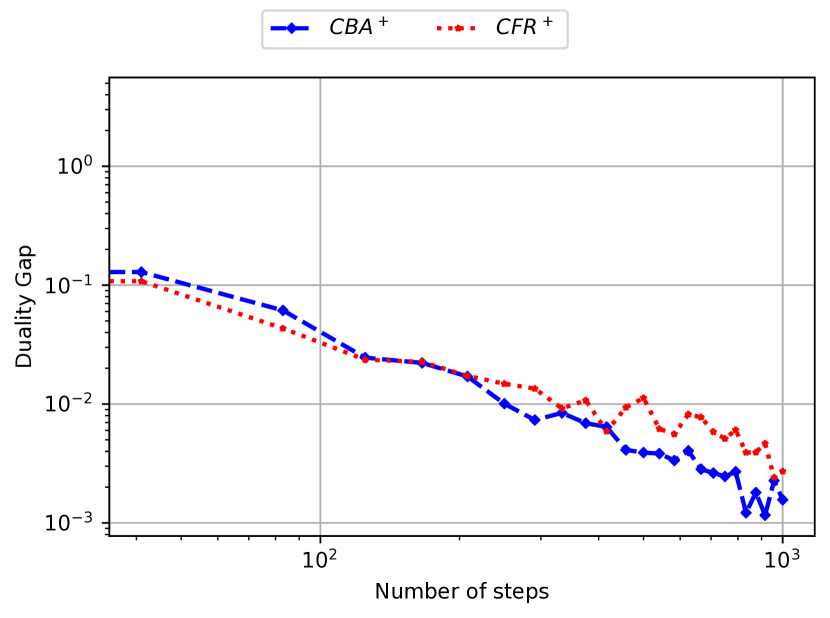

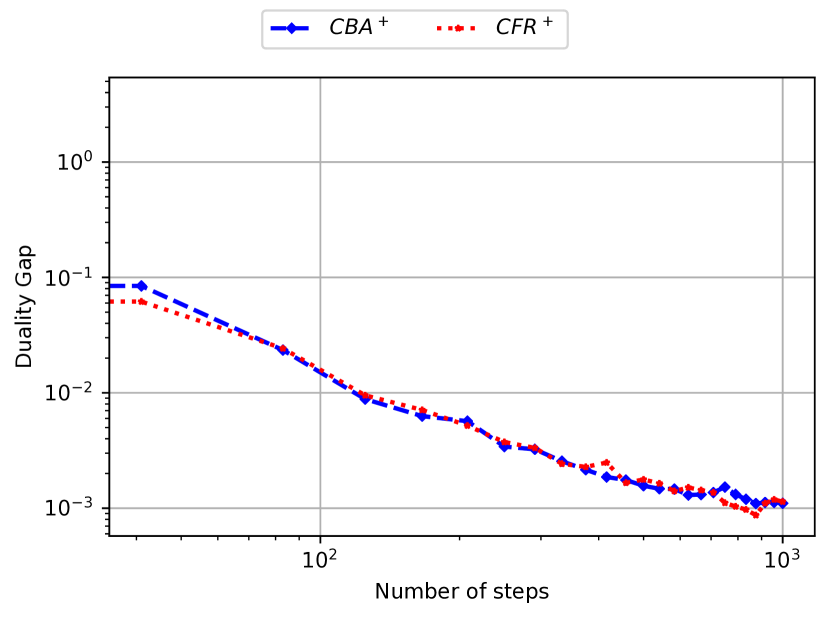

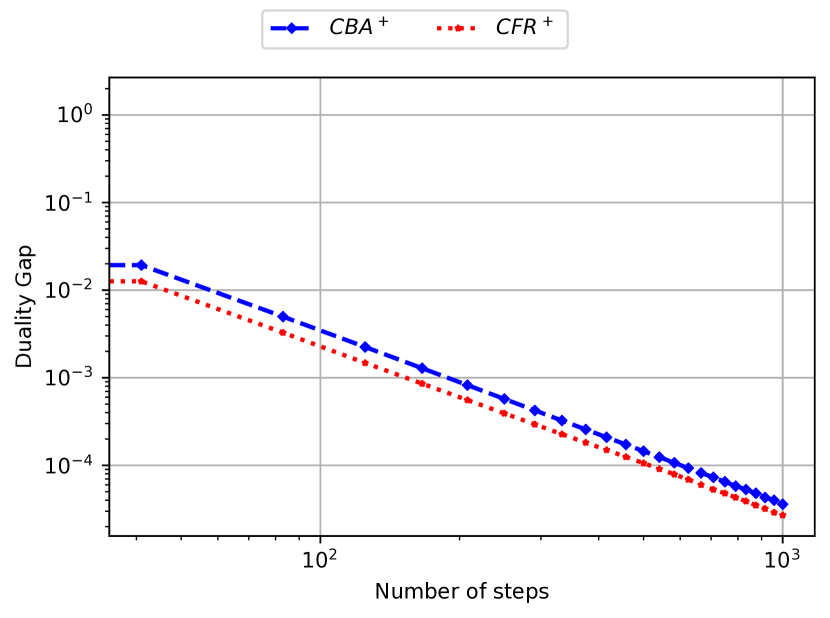

For EFGs, we compare CBA+and CFR+ on many poker AI benchmark instances, including Leduc, Kuhn, search games and sheriff (see Farina et al. (2021) for game descriptions). We present our results in Figures 1(b)-1(d). Additional details and experiments for EFGs are presented in Appendix E.4. Overall, we see in Figure 1 that CBA+may slightly outperform RM+ and CFR+, two of the strongest algorithms for matrix games and EFGs, which were shown to achieve the best empirical performances compared to a wide range of algorithms, including Hedge and other first-order methods (Kroer, 2020; Kroer et al., 2018; Farina et al., 2019b). For matrix games, AdaHedge and AdaFTRL are both outperformed by RM+ and CBA+; we present more experiments to compare RM+ and CBA+ in Appendix E.2, and more experiments with matrix games in Appendix E.3. Recall that our goal is to generalize these strong performance to other settings: we present our numerical experiments for solving distributionally robust optimization problems in the next section.

4.2 Distributionally Robust Optimization

Problem setup

Broadly speaking, DRO attempts to exploit partial knowledge of the statistical properties of the model parameters to obtain risk-averse optimal solutions (Rahimian and Mehrotra, 2019). We focus on the following instance of distributionally robust classification with logistic losses (Namkoong and Duchi, 2016; Ben-Tal et al., 2015). There are observed feature-label pairs , and we want to solve

| (5) |

where . The formulation (5) takes a worst-case approach to put more weight on misclassified observations and provides some statistical guarantees, e.g., it can be seen as a convex regularization of standard empirical risk minimization instances (Duchi et al., 2021).

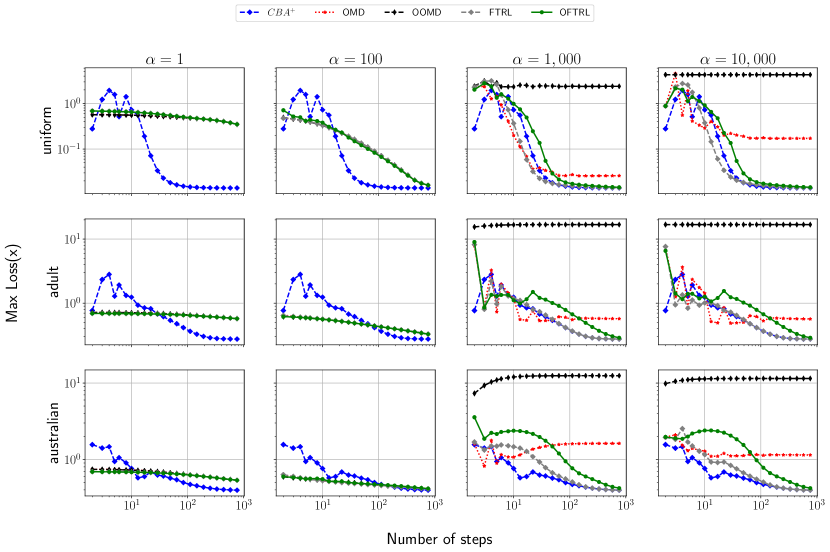

We compare CBA+ (with linear averaging and alternation) with Online Mirror Descent (OMD), Optimistic OMD (O-OMD), Follow-The-Regularized-Leader (FTRL) and Optimistic FTRL (O-FTRL). We provide a detailed presentation of our implementations of these algorithms in Appendix F. We compare the performances of these algorithms with CBA+ on two synthetic data sets and four real data sets. We use linear averaging on decisions for all algorithms, and parameters in eq. 5.

Synthetic and real instances

For the synthetic classification instances, we generate an optimal , sample for , set labels , and then we flip of them. For the real classification instances, we use the following data sets from the libsvm website222https://www.csie.ntu.edu.tw/cjlin/libsvmtools/datasets/: adult, australian, splice, madelon. Details about the empirical setting, the data sets and additional numerical experiments are presented in Appendix G.

Choice of step sizes

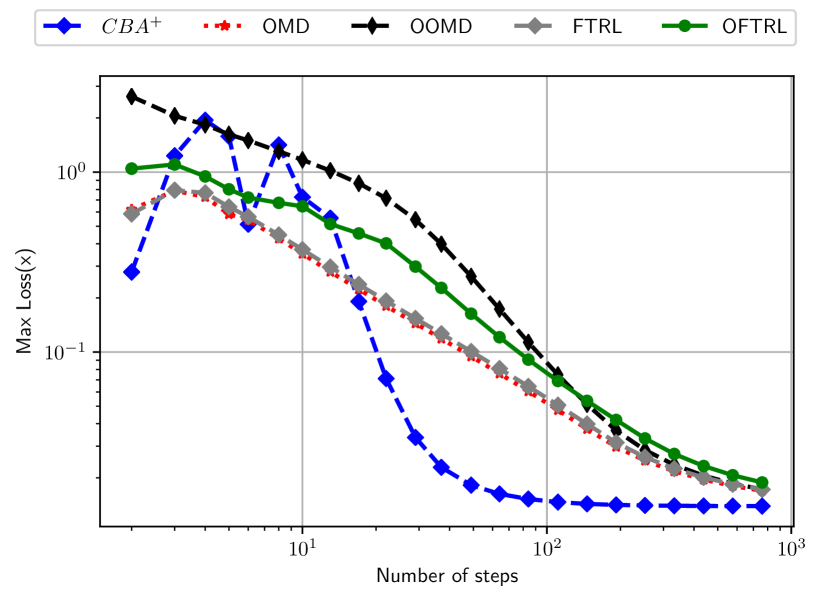

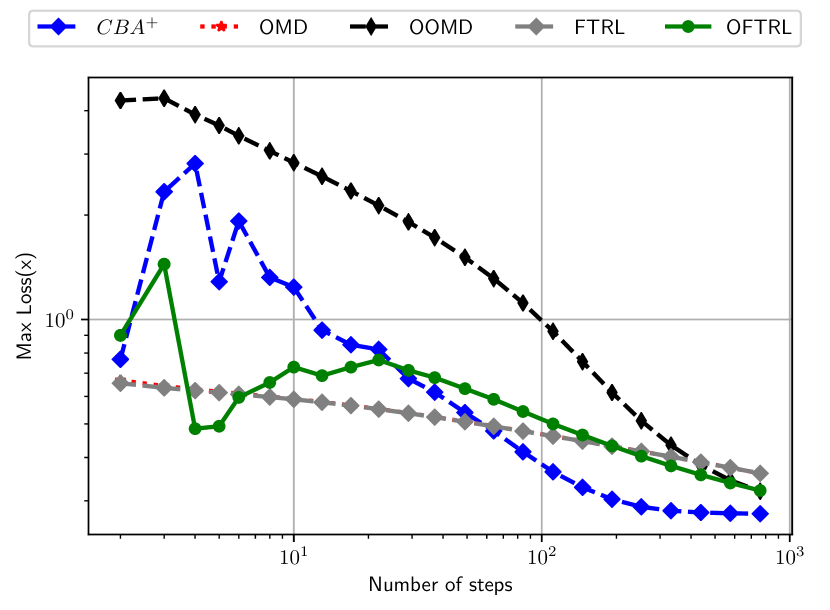

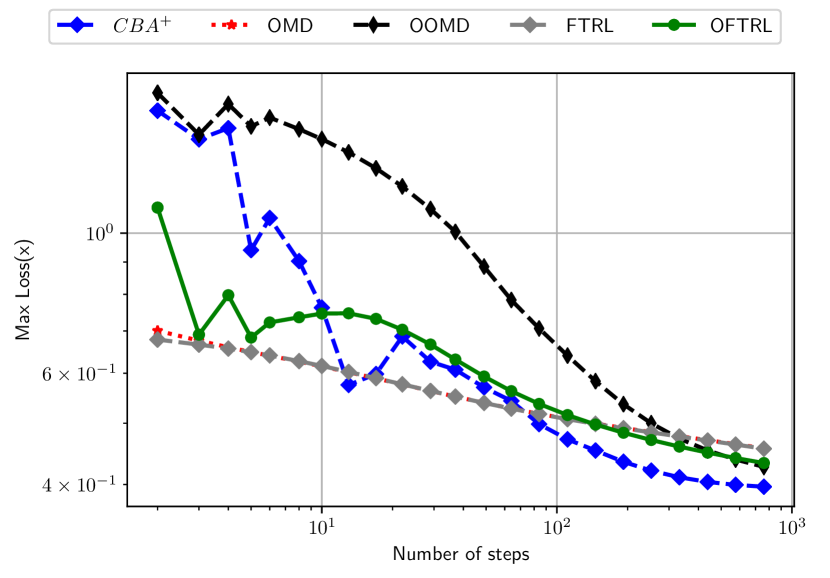

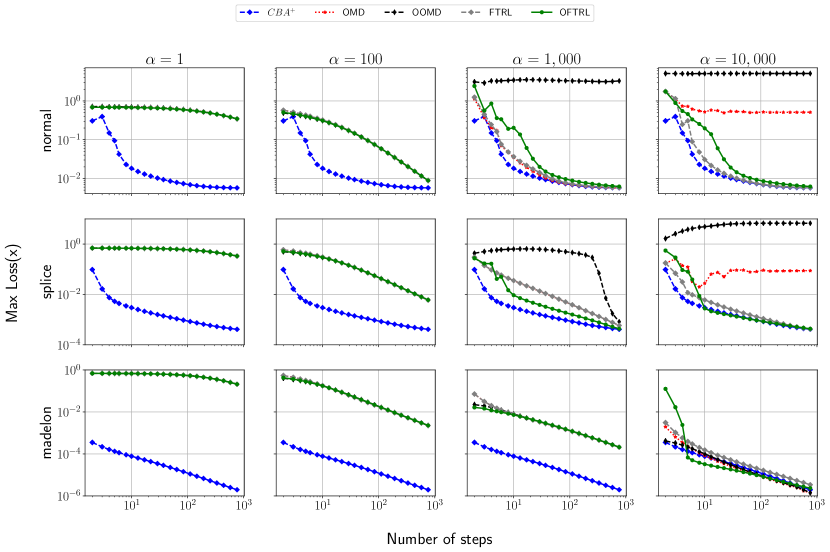

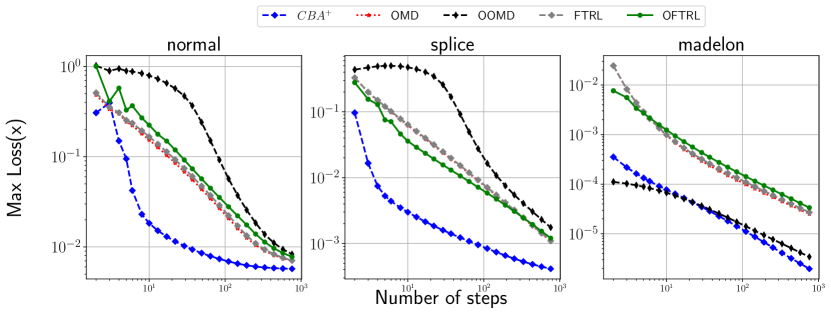

One of the main motivation for CBA+ is to obtain a parameter-free algorithm. Choosing a fixed step size for the other algorithms requires knowing a bound on the norm of the instantaneous payoffs (see Appendix F.2 for our derivations of this upper bound). This is a major limitation in practice: these bounds may be very conservative, leading to small step sizes. We highlight this by showing the performance of all four algorithms, for various fixed step sizes , where is a multiplier and is the theoretical step size which guarantees the convergence of the algorithms for each instance. We detail the computation of in Appendix F.2. We present the results of our numerical experiments on synthetic and real data sets in Figure 2. Additional simulations with adaptive step sizes (Orabona, 2019) are presented in Figure 3 and in Appendix G.

Results and discussion

In Figure 2, we present the worst-case loss of the current solution in terms of the number of steps . We see that when the step sizes is chosen as the theoretical step sizes guaranteeing the convergence of the non-parameter free algorithms (), CBA+ vastly outperforms all of the algorithms. When we take more aggressive step sizes, the non-parameter-free algorithms become more competitive. For instance, when , OMD, FTRL and O-FTRL are competitive with CBA+ for the experiments on synthetic data sets. However, for this same instance and , O-OMD diverges, because the step sizes are far greater than the theoretical step sizes guaranteeing convergence. At , both OMD and O-OMD diverge. The same type of performances also hold for the splice data set. Finally, for the madelon data set, the non parameter-free algorithms start to be competitive with CBA+ only when . Again, we note that this range of step sizes is completely outside the values that guarantee convergence of the algorithms, and fine-tuning the algorithms is time- and resource-consuming. In contrast, CBA+ can be used without wasting time on exploring and finding the best convergence rates, and with confidence in the convergence of the algorithm. Similar observations hold for adaptive step sizes (see Figure 3 and Appendix G). The overall poor performances of the optimistic methods (compared to their average regret guarantees) may reflect their sensibility to the choice of the step sizes. Additional experiments in Appendix G with other real and synthetic EFG and DRO instances show the robustness of the strong performances of CBA+ across additional problem instances.

Running times compared to CBA+

We would like to emphasize that all of our figures show the number of steps on the -axis, and not the actual running times of the algorithms. Overall, CBA+ converges to an optimal solution to the DRO instance (5) vastly faster than the other algorithms. In particular, empirically, CBA+ is 2x-2.5x faster than OMD, FTRL and O-FTRL, and 3x-4x faster than O-OMD. This is because OMD, FTRL, O-OMD, and O-FTRL require binary searches at each step, see Appendix F. The functions used in the binary searches themselves require solving an optimization program (an orthogonal projection onto the simplex, see (33)) at each evaluation. Even though computing the orthogonal projection of a vector onto the simplex can be done in , this results in slower overall running time, compared to CBA+ with (quasi) closed-form updates at each step. The situation is even worse for O-OMD, which requires two proximal updates at each iteration. We acknowledge that the same holds for CBA+ compared to RM+. In particular, CBA+ is slightly slower than RM+, because of the computation of in operations at every iteration.

5 Conclusion

We have introduced CBA+, a new algorithm for convex-concave saddle-point solving, that is 1) simple to implement for many practical decision sets, 2) completely parameter-free and does not attempt to lear any step sizes, and 3) competitive with, or even better than, state-of-the-art approaches for the best choices of parameters, both for matrix games, extensive-form games, and distributionally robust instances. Our paper is based on Blackwell approachability, which has been used to achieved important breakthroughs in poker AI in recent years, and we hope to generalize the use and implementation of this framework to other important problem instances. Interesting future directions of research include developing a theoretical understanding of the improvements related to alternation in our setting, designing efficient implementations for other widespread decision sets (e.g., based on Kullback-Leibler divergence or -divergence), and novel accelerated versions based on strong convex-concavity or optimistim.

Societal impact

Our work enables faster and simpler computation of solutions of saddle-point problems, which have become widely used for applications in the industry. There is a priori no direct negative societal consequence to this work, since our methods simply return the same solutions as previous algorithms but in a simpler and more efficient way.

References

- Abernethy et al. [2011] Jacob Abernethy, Peter L Bartlett, and Elad Hazan. Blackwell approachability and no-regret learning are equivalent. In Proceedings of the 24th Annual Conference on Learning Theory, pages 27–46. JMLR Workshop and Conference Proceedings, 2011.

- Abernethy et al. [2009] Jacob D Abernethy, Elad Hazan, and Alexander Rakhlin. Competing in the dark: An efficient algorithm for bandit linear optimization. 2009.

- Beck and Teboulle [2003] Amir Beck and Marc Teboulle. Mirror descent and nonlinear projected subgradient methods for convex optimization. Operations Research Letters, 31(3):167–175, 2003.

- Ben-Tal and Nemirovski [2001] Aharon Ben-Tal and Arkadi Nemirovski. Lectures on modern convex optimization: analysis, algorithms, and engineering applications, volume 2. Siam, 2001.

- Ben-Tal et al. [2013] Aharon Ben-Tal, Dick Den Hertog, Anja De Waegenaere, Bertrand Melenberg, and Gijs Rennen. Robust solutions of optimization problems affected by uncertain probabilities. Management Science, 59(2):341–357, 2013.

- Ben-Tal et al. [2015] Aharon Ben-Tal, Elad Hazan, Tomer Koren, and Shie Mannor. Oracle-based robust optimization via online learning. Operations Research, 63(3):628–638, 2015.

- Bertsimas et al. [2019] Dimitris Bertsimas, Dick den Hertog, and Jean Pauphilet. Probabilistic guarantees in robust optimization. 2019.

- Blackwell [1956] David Blackwell. An analog of the minimax theorem for vector payoffs. Pacific Journal of Mathematics, 6(1):1–8, 1956.

- Bowling et al. [2015] Michael Bowling, Neil Burch, Michael Johanson, and Oskari Tammelin. Heads-up limit hold’em poker is solved. Science, 347(6218):145–149, 2015.

- Brown and Sandholm [2018] Noam Brown and Tuomas Sandholm. Superhuman AI for heads-up no-limit poker: Libratus beats top professionals. Science, 359(6374):418–424, 2018.

- Brown and Sandholm [2019] Noam Brown and Tuomas Sandholm. Superhuman AI for multiplayer poker. Science, 365(6456):885–890, 2019.

- Burch et al. [2019] Neil Burch, Matej Moravcik, and Martin Schmid. Revisiting cfr+ and alternating updates. Journal of Artificial Intelligence Research, 64:429–443, 2019.

- Chambolle and Pock [2011] Antonin Chambolle and Thomas Pock. A first-order primal-dual algorithm for convex problems with applications to imaging. Journal of mathematical imaging and vision, 40(1):120–145, 2011.

- Chambolle and Pock [2016] Antonin Chambolle and Thomas Pock. On the ergodic convergence rates of a first-order primal–dual algorithm. Mathematical Programming, 159(1-2):253–287, 2016.

- Chiang et al. [2012] Chao-Kai Chiang, Tianbao Yang, Chia-Jung Lee, Mehrdad Mahdavi, Chi-Jen Lu, Rong Jin, and Shenghuo Zhu. Online optimization with gradual variations. In Conference on Learning Theory, pages 6–1. JMLR Workshop and Conference Proceedings, 2012.

- Combettes and Reyes [2013] Patrick L Combettes and Noli N Reyes. Moreau’s decomposition in banach spaces. Mathematical Programming, 139(1):103–114, 2013.

- De Rooij et al. [2014] Steven De Rooij, Tim Van Erven, Peter D Grünwald, and Wouter M Koolen. Follow the leader if you can, hedge if you must. The Journal of Machine Learning Research, 15(1):1281–1316, 2014.

- Duchi et al. [2008] John Duchi, Shai Shalev-Shwartz, Yoram Singer, and Tushar Chandra. Efficient projections onto the L-1 ball for learning in high dimensions. In Proceedings of the 25th international conference on Machine learning, pages 272–279, 2008.

- Duchi et al. [2021] John C Duchi, Peter W Glynn, and Hongseok Namkoong. Statistics of robust optimization: A generalized empirical likelihood approach. Mathematics of Operations Research, 2021.

- Egozcue et al. [2003] Juan José Egozcue, Vera Pawlowsky-Glahn, Glòria Mateu-Figueras, and Carles Barcelo-Vidal. Isometric logratio transformations for compositional data analysis. Mathematical Geology, 35(3):279–300, 2003.

- Farina et al. [2019a] Gabriele Farina, Christian Kroer, and Tuomas Sandholm. Online convex optimization for sequential decision processes and extensive-form games. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 1917–1925, 2019a.

- Farina et al. [2019b] Gabriele Farina, Christian Kroer, and Tuomas Sandholm. Optimistic regret minimization for extensive-form games via dilated distance-generating functions. In Advances in Neural Information Processing Systems, pages 5222–5232, 2019b.

- Farina et al. [2019c] Gabriele Farina, Christian Kroer, and Tuomas Sandholm. Regret circuits: Composability of regret minimizers. In International Conference on Machine Learning, pages 1863–1872, 2019c.

- Farina et al. [2021] Gabriele Farina, Christian Kroer, and Tuomas Sandholm. Faster game solving via predictive blackwell approachability: Connecting regret matching and mirror descent. In Proceedings of the AAAI Conference on Artificial Intelligence. AAAI, 2021.

- Gao et al. [2019] Yuan Gao, Christian Kroer, and Donald Goldfarb. Increasing iterate averaging for solving saddle-point problems. arXiv preprint arXiv:1903.10646, 2019.

- Gordon [2007] Geoffrey J Gordon. No-regret algorithms for online convex programs. In Advances in Neural Information Processing Systems, pages 489–496. Citeseer, 2007.

- Goyal and Grand-Clément [2018] Vineet Goyal and Julien Grand-Clément. Robust Markov decision process: Beyond rectangularity. arXiv preprint arXiv:1811.00215, 2018.

- Grand-Clément and Kroer [2020a] Julien Grand-Clément and Christian Kroer. First-order methods for Wasserstein distributionally robust MDP. arXiv preprint arXiv:2009.06790, 2020a.

- Grand-Clément and Kroer [2020b] Julien Grand-Clément and Christian Kroer. Scalable first-order methods for robust mdps. arXiv preprint arXiv:2005.05434, 2020b.

- Hart and Mas-Colell [2000] Sergiu Hart and Andreu Mas-Colell. A simple adaptive procedure leading to correlated equilibrium. Econometrica, 68(5):1127–1150, 2000.

- Iyengar [2005] Garud Iyengar. Robust dynamic programming. Mathematics of Operations Research, 30(2):257–280, 2005.

- Jin and Sidford [2020] Yujia Jin and Aaron Sidford. Efficiently solving mdps with stochastic mirror descent. In International Conference on Machine Learning, pages 4890–4900. PMLR, 2020.

- Kroer [2020] Christian Kroer. Ieor8100: Economics, ai, and optimization lecture note 5: Computing Nash equilibrium via regret minimization. 2020.

- Kroer et al. [2018] Christian Kroer, Gabriele Farina, and Tuomas Sandholm. Solving large sequential games with the excessive gap technique. In Advances in Neural Information Processing Systems, pages 864–874, 2018.

- Kroer et al. [2020] Christian Kroer, Kevin Waugh, Fatma Kılınç-Karzan, and Tuomas Sandholm. Faster algorithms for extensive-form game solving via improved smoothing functions. Mathematical Programming, pages 1–33, 2020.

- McMahan [2011] Brendan McMahan. Follow-the-regularized-leader and mirror descent: Equivalence theorems and l1 regularization. In Proceedings of the Fourteenth International Conference on Artificial Intelligence and Statistics, pages 525–533. JMLR Workshop and Conference Proceedings, 2011.

- Moravčík et al. [2017] Matej Moravčík, Martin Schmid, Neil Burch, Viliam Lisỳ, Dustin Morrill, Nolan Bard, Trevor Davis, Kevin Waugh, Michael Johanson, and Michael Bowling. Deepstack: Expert-level artificial intelligence in heads-up no-limit poker. Science, 356(6337):508–513, 2017.

- Namkoong and Duchi [2016] Hongseok Namkoong and John C Duchi. Stochastic gradient methods for distributionally robust optimization with f-divergences. In NIPS, volume 29, pages 2208–2216, 2016.

- Nemirovski [2004] Arkadi Nemirovski. Prox-method with rate of convergence O(1/t) for variational inequalities with lipschitz continuous monotone operators and smooth convex-concave saddle point problems. SIAM Journal on Optimization, 15(1):229–251, 2004.

- Nemirovski and Yudin [1983] Arkadi Nemirovski and David Yudin. Problem complexity and method efficiency in optimization. 1983.

- Orabona [2019] Francesco Orabona. A modern introduction to online learning. arXiv preprint arXiv:1912.13213, 2019.

- Orabona and Pál [2015] Francesco Orabona and Dávid Pál. Scale-free algorithms for online linear optimization. In International Conference on Algorithmic Learning Theory, pages 287–301. Springer, 2015.

- Rahimian and Mehrotra [2019] Hamed Rahimian and Sanjay Mehrotra. Distributionally robust optimization: A review. arXiv preprint arXiv:1908.05659, 2019.

- Rakhlin and Sridharan [2013] Alexander Rakhlin and Karthik Sridharan. Online learning with predictable sequences. In Conference on Learning Theory, pages 993–1019. PMLR, 2013.

- Shimkin [2016] Nahum Shimkin. An online convex optimization approach to blackwell’s approachability. The Journal of Machine Learning Research, 17(1):4434–4456, 2016.

- Sidford and Tian [2018] Aaron Sidford and Kevin Tian. Coordinate methods for accelerating l-infinity regression and faster approximate maximum flow. In 2018 IEEE 59th Annual Symposium on Foundations of Computer Science (FOCS), pages 922–933. IEEE, 2018.

- Syrgkanis et al. [2015] Vasilis Syrgkanis, Alekh Agarwal, Haipeng Luo, and Robert E Schapire. Fast convergence of regularized learning in games. arXiv preprint arXiv:1507.00407, 2015.

- Tammelin et al. [2015] Oskari Tammelin, Neil Burch, Michael Johanson, and Michael Bowling. Solving heads-up limit Texas hold’em. In Twenty-Fourth International Joint Conference on Artificial Intelligence, 2015.

- Tseng [1995] Paul Tseng. On linear convergence of iterative methods for the variational inequality problem. Journal of Computational and Applied Mathematics, 60(1-2):237–252, 1995.

- von Stengel [1996] Bernhard von Stengel. Efficient computation of behavior strategies. Games and Economic Behavior, 14(2):220–246, 1996.

- Wei et al. [2020] Chen-Yu Wei, Chung-Wei Lee, Mengxiao Zhang, and Haipeng Luo. Linear last-iterate convergence in constrained saddle-point optimization. In International Conference on Learning Representations, 2020.

- Wiesemann et al. [2013] W. Wiesemann, D. Kuhn, and B. Rustem. Robust Markov decision processes. Operations Research, 38(1):153–183, 2013.

- Zinkevich et al. [2007] Martin Zinkevich, Michael Johanson, Michael Bowling, and Carmelo Piccione. Regret minimization in games with incomplete information. In Advances in neural information processing systems, pages 1729–1736, 2007.

Appendix A Comparison to Shimkin (2016) and Farina et al. (2021)

The focus of our paper is on developing new algorithms for convex-concave saddle-point solving via Blackwell approachability algorithms for sets beyond the simplex domain. This is what motivated the development of CBA+, which attempts to generalize the ideas from RM+ and CFR+ beyond simplex settings. A complementary question is to consider the second construction of Abernethy et al. (2011), which is a way to convert a no-regret algorithm into an approachability algorithm. At a very high level, that construction ends up using the no-regret algorithm to select which hyperplane to force, and performing regret minimization on the choice of hyperplane. An observation made by both Shimkin (2016) and Farina et al. (2021) is that if one uses FTRL with the Euclidean regularizer, then it corresponds to Blackwell’s original approachability algorithm, and thus to regret matching on the simplex. This begs the question of what happens if one uses a different algorithm from FTRL. The most natural substitute would be OMD with a Bregman divergence derived from the Euclidean distance, which is also known as online gradient descent (OGD).

Shimkin (2016) considers OGD on a variation of the original construction of Abernethy et al. (2011) with the simplex as the decision set. This setup (and the original setup from Abernethy et al. (2011)) uses (a subset of) the unit ball as the feasible set for the regret minimizer, and thus OGD ends up projecting the cumulated payoff vector onto the unit ball after every iteration. Therefore, the OGD setup by Shimkin (2016) yields an algorithm that is reminiscent of RM+, but where we repeatedly renormalize the cumulated payoff vector. One consequence of this is that the stepsize used to add new payoff vectors becomes important. Farina et al. (2021) show that the Abernethy et al. (2011) construction can be extended to allow the regret minimizer to use any decision set such that , where is the target set and its polar cone, and is intersected with the unit ball. Then, Farina et al. (2021) consider the simplex regret-minimization setting, and show that OGD instantiated on is equivalent to RM+.

CBA+ does not generalize either of the two simplex approaches above. For Shimkin (2016), this can be seen because of the projection and subsequent dependence on stepsize required by Shimkin (2016)’s construction. For Farina et al. (2021), this can be seen by the fact that they obtain RM+ when applying their approach to the simplex setting, and CBA+ differs from RM+ (in fact, that paper does not attempt to derive new unaccelerated regret minimizers; the goal is to design accelerated, or predictive/optimistic, variants of RM and RM+). However, an alternative derivation of CBA+ can be accomplished by using the generalization from Farina et al. (2021) where OGD is run with the decision set . Instead of applying OGD on the no-regret formulation of the Blackwell formulation of regret-minimization on the simplex with target set as in Farina et al. (2021), we can apply the OGD-setup of Farina et al. (2021) to the Blackwell formulation of a general no-regret problem with decision set and target set where . Then, we would get an indirect proof of correctness of the CBA+ algorithm through the correctness of OGD and the two layers of reduction from regret minimization to Blackwell approachability to regret minimization. However, we believe that this approach is significantly less intuitive than understanding CBA+ directly in terms of its properties as a Blackwell approachability algorithm.

Appendix B Proofs of Theorem 3.1

Notations and classical results in conic optimization

We make use of the following facts. We provide a proof here for completeness.

Lemma B.1.

Let a closed convex cone and its polar.

-

1.

If , then , and .

-

2.

If then

where .

-

3.

If , then .

-

4.

Assume that with convex compact and . Then is a closed convex cone. Additionally, if we have .

-

5.

Let us write the order induced by . Then

(6) (7) -

6.

Assume that for . Then .

Proof.

-

1.

The fact that , follows from Moreau’s Decomposition Theorem (Combettes and Reyes, 2013). The fact that is a straightforward consequence of .

-

2.

For any we have

Conversely, since , we have

This shows that

-

3.

For any , by definition we have . Now if we have so .

-

4.

Let . Then for . We will show that . We have

and is true by Cauchy-Schwartz and the definition of .

-

5.

We start by proving (6). Let and assume that . Then . Because is a convex set, and a cone, we have . Therefore, , i.e., .

We now prove (7). Let and assume that . Then by definition . Additionally, by assumption. Since is convex, and is a cone, , i.e., . Therefore,

-

6.

Let such that . Then . We have

∎

Based on Moreau’s Decomposition Theorem, we will use and interchangeably.

Results for various linear averaging schemes

We now present our convergence results for various linear averaging schemes. As a warm-up, we start with two theorems, Theorem B.2 and Theorem B.3, which show that CBA and CBA+ are compatible with weighted average schemes, when both the decisions and the payoffs are weighted. The proofs for these theorems will be used in the proof of our main theorem, Theorem 3.1. For the sake of consiness, in all the proofs of this section we will always write . We start with the following theorem.

Theorem B.2.

Let the sequence of decisions generated by CBA with weights and let for any . Then

Additionally,

Overall,

Proof.

The proof proceeds in two steps. We start by proving

We have

| (8) | ||||

| (9) |

where (8) follows from Statement 1 in Lemma B.1, and (9) follows from CBA maintaining

We can conclude that

We now prove that

We have

| (10) | ||||

| (11) |

where (11) follows from

| (12) |

This is because:

-

•

. This is one of the crucial component of Blackwell’s approachability framework: the current decision is chosen to force a hyperplane on the aggregate payoff. To see this, first note that . Let us write . Note that by definition, , and . Therefore,

-

•

from Statement 3 of Lemma B.1 and .

We therefore have

This recursion directly gives

where the last inequality follows from the definition of and . ∎

Theorem B.3.

Let the sequence of decisions generated by CBA+ with weights and let for any . Then

Additionally,

Overall,

Proof of Theorem B.3.

The proof proceeds in two steps. We start by proving

Recall that , and let us consider . By definition of , similarly as in the proof of Theorem B.2, we have

Note that at any period , we have

| (13) |

This is simply because with

Now we have

From (6) in Lemma B.1, we can sum the inequalities (13). Noticing that , we can conclude that

From and Statement 6 in Lemma B.1, we have . This implies

We now turn to proving

We have

| (14) | ||||

| (15) | ||||

| (16) |

where (15) follows from Statement 1 in Lemma B.1. Therefore,

By construction and for the same reason as for (12), . Therefore, we have the recursion

By telescoping the inequality above we obtain

By definition of ,

∎

Linear averaging only on decisions

We are now ready to prove our main convergence result, Theorem 3.1. Our proof heavily relies on the sequence of payoffs belonging to the cone at every iteration (), and for this reason it does not extend to CBA. We also note that the use of conic optimization somewhat simplifies the argument compared to the proof that RM+is compatible with linear averaging (Tammelin et al., 2015).

Comparisons of different weighted average schemes

We conclude this section with an empirical comparisons of the different weighted average schemes (Theorem B.2, Theorem B.3, and Theorem 3.1). We also compare these algorithms with RM+. We present our numerical experiments on sets of random matrix game instances in Figure 4. The setting is the same as in our simulation section, Section 4. We note that CBA+ with linear averaging only on decisions outperforms both CBA+ and CBA with linear averaging on both decisions and payoffs, as well as RM+ with linear averaging on decisions.

B.1 Geometric intuition on the projection step of CBA+

Figure 5 illustrates the projection step of . At a high level, from to , an instantaneous payoff is first added to (where ), and then the resulting vector is projected onto . The projection moves the vector along the edges of the cone , preserving the (orthogonal) distance to .

Appendix C Proof of Theorem 3.2

Let , and

Since is convex-concave, we first have

Now,

Now since is convex-concave, we can use the following upper bound:

where (recall the repeated game framework presented at the beginning of Section 2).

Appendix D Proofs of the projections of Section 3.1

We will extensively use Moreau’s Decomposition Theorem (Combettes and Reyes, 2013): for any convex cone and , we can decompose , where is the polar cone of . Therefore, to compute , it is sufficient to compute , the orthogonal projection of onto . We will see that in some cases, it is simpler to compute and then use than directly computing via solving (4).

D.1 The case of the simplex

We consider . Note that in this case, . The next lemma gives a closed-form expression of .

Lemma D.1.

Let . Then

Proof of Lemma D.1.

Note that for we have

∎

For a given , computing is now equivalent to solving

| (18) |

Using the reformulation (18), we show that for a fixed , the optimal can be computed in closed-form. It is then possible to avoid a binary search over and to simply use a sorting algorithm to obtain the optimal . The next proposition summarizes our complexity result for .

Proposition D.2.

An optimal solution to (18) can be computed in time.

Proof.

Computing is equivalent to computing

Let us fix and let us first solve

| (19) | ||||

This is essentially the projection of on . So a solution to (19) is Note that in this case we have So overall the projection brings down to the optimization of such that

| (20) |

In principle, we could use binary search with a doubling trick to compute a -minimizer of the convex function in calls to . However, it is possible to a minimizer of using the following remark. By construction, we know that . Here, , and This proves that

which in turns imply that

| (21) |

We can use (21) to efficiently compute without using any binary search. In particular, we can sort the coefficients of in operations, and use (21) to find . ∎

Having obtained , we can obtain by using the identity . Note that RM and RM+ are obtained by choosing the closed-form feasible point corresponding to in (18).

D.2 The case of an ball

In this section we assume that with or . The next lemma provides a closed-form reformulation of the polar cone .

Lemma D.3.

Let with or . Then , with such that .

Proof of Lemma D.3.

Let us write . Note that for we have

since is the dual norm of . ∎

The orthogonal projection problem onto becomes

| (22) |

For , (22) has a closed-form solution. For , a quasi-closed-form solution to (22) can be obtained efficiently using sorting. For , it is more efficient to directly compute . This is because the dual norm of is .

Proposition D.4.

-

•

For , can be computed in arithmetic operations.

-

•

For , can be computed in arithmetic operations.

-

•

For , can be computed in closed-form.

Proof.

The case . Assume that . Then . We want to compute the projection of on :

| (23) | ||||

For a fixed , we want to compute

| (24) | ||||

The projection (24) can be computed in closed-form as

| (25) |

since this is simply the orthogonal projection of onto the ball of radius . Let us call such that

Because of the closed-form expression for as in (25), we have

Finding a minimizer of can be done in , with the same methods as in the proof in the previous section (Appendix D.1).

The case . Let . The problem of computing , the orthogonal projection onto the cone , is equivalent to

| (26) | ||||

Note the similarity between (26) (computing the orthogonal projection onto when ), and (23) (computing the orthogonal projection onto when ). From Lemma D.3, we know that this is the case because and are dual norms to each other.

Therefore, the methods described for computing for can be applied to the case for directly computing . This gives the complexity results as stated in Proposition D.4: can be computed in operations.

The case . Let , then . Let us fix and consider solving

| (27) | ||||

The projection (27) can be computed in closed-form as

since this is just the orthogonal projection of the vector onto the -ball of radius . Let us call such that

Note that here, is differentiable. Therefore is also differentiable. First-order optimality conditions yield a closed-form solution for computing , as

| (28) |

∎

D.3 The case of an ellipsoidal confidence region in the simplex

In this section we assume that is . We also assume that , so that we can write where

Suppose we made a sequence of decisions , which can be written as for Then it is clear that for any sequence of payoffs , we have

| (29) |

Therefore, if we run CBA+ on the set to obtain growth of the right-hand side of (29), we obtain a no-regret algorithm for . We now show how to run CBA+ for the set . Let We use the following orthonormal basis of : let be the vectors where the component is repeated times. The vectors are orthonormal and constitute a basis of (Egozcue et al., 2003). Writing , and noting that , we can write Now, if with , we have , for and . Finally,

| (30) |

Therefore, to obtain a regret minimizer for the left-hand side of (30) with observed payoffs , we can run CBA+ on the right-hand side, where the decision set is an ball and the sequence of observed payoffs is . In the previous section we showed how to efficiently instantiate CBA+ in this setting (see Proposition D.4).

Appendix E Additional details and numerical experiments for matrix games and EFGs

E.1 Numerical setup

Numerical setup for matrix games

For the experiments on matrix games, we sample at random the matrix of payoffs and we let , where represent the number of actions of each player. We average our results over instances. The decision sets and are given as and .

Alternation

Alternation is a method which improves the performances of RM and RM+ (Burch et al., 2019). We leave proving this for CBA and CBA+ to future works. Using alternation, the players play in turn, instead of playing at the same time. In particular, the -player may observe the current decision of the -player at period , before choosing its own decision . For CBA and CBA+, it is implemented as follows. At period ,

-

1.

The -player chooses using its payoff

-

2.

The -player observes and updates :

-

3.

The -player chooses using

-

4.

The -player observes and updates :

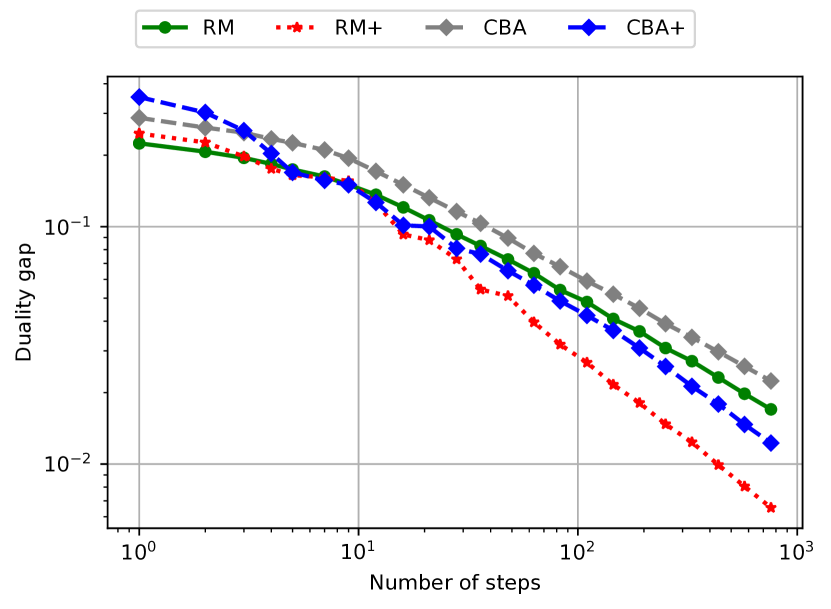

E.2 Comparing RM, RM+, CBA, and CBA+ on matrix games

In Figure 6 and Figure 7, we show the performances of RM, RM+, CBA and CBA+ with and without alternation, and with and without linear averaging. On the -axis we show the duality gap of the current averaged decisions . On the -axis we show the number of iterations.

- •

- •

- •

-

•

Finally, in Figure 6(d) and Figure 7(d), RM+ and CBA+ use linear averaging on decisions and alternation. We see that the strongest performances are achieved by CBA+. Recall that RM and CBA are not known to be compatible with linear averaging (on decisions only), so we do not show their performances here.

-

•

Conclusion of our experiments. We see that it is both alternation and linear averaging that enable the strong empirical performances of CBA+, rendering it capable to outperform RM+. Crucially, it is the “ operation” that enables CBA+ (and RM+) to be compatible with linear averaging on the decisions only and to outperform CBA and RM.

E.3 Additional numerical experiments for matrix games

We have seen in Appendix E.2 that RM+ and CBA+ with alternation and linear averaging are outperforming RM and CBA. In Figure 1(a), we have compared both RM+ and CBA+ with AdaFTRL (Orabona and Pál, 2015) and AdaHedge (De Rooij et al., 2014), two algorithms that also enjoy the desirable scale-free property, i.e., their sequences of decisions remain invariant when the losses are scaled by a constant factor. In the next figure, we provide additional comparisons of RM+, CBA+, AdaHedge and AdaFTRL when the coefficients of the matrix of payoff are normally distributed. We found that RM+ and CBA+ are both outperforming AdaHedge and AdaFTRL, a situation similar to the case of uniform payoffs (Figure 1(a).)

E.4 Additional numerical experiments for EFGs

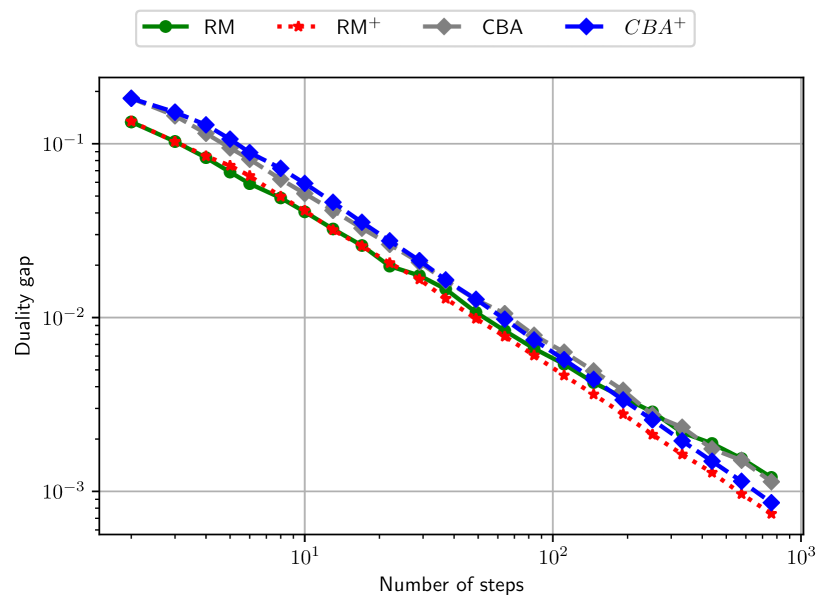

In Section 4.1 , we have compared CBA+ (using alternation and linear averaging) and CFR+ on various EFGs instances. We present in Figure 9 additional simulations where CBA+ and CFR+ performs similarly. A description of the games can be found in Farina et al. (2021). On the -axis we show the duality gap of the current averaged decisions . On the -axis we show the number of iterations.

Appendix F OMD, FTRL and optimistic variants

F.1 Algorithms

Let us fix some step size . For solving our instances of distributionally robust optimization, we compare Algorithm CBA+ with the following four state-of-the-art algorithms:

- 1.

- 2.

Note that a priori these algorithms can be written more generally using Bregman divergence (e.g., Ben-Tal and Nemirovski (2001)). We choose to work with instead of Kullback-Leibler divergence as this -setup is usually associated with faster empirical convergence rates (Chambolle and Pock, 2016; Gao et al., 2019). Additionally, following Chiang et al. (2012); Rakhlin and Sridharan (2013), we use the last observed loss as the predictor for the next loss, i.e., we set .

F.2 Implementations

When is the simplex or a ball based on the -distance and centered at , there is a closed-form solution to the proximal updates for FTRL, OMD, O-FTRL and O-OMD. However, it is not clear how to compute these proximal updates for different settings, e.g., when is a subset of the simplex or an -ball. We present the details of our implementation below. The results in the rest of this section are reminiscient to the novel tractable proximal setups presented in Grand-Clément and Kroer (2020a, b).

Computing the projection steps for min-player

For , and a step size , the prox-update becomes

| (31) |

This is the same arg min as

We can change by to solve the equivalent program

The solution to the above program is

From we obtain the solution to (31)

Computing the projection steps for max-player

For , the proximal update of the max-player from a previous point and a step size of becomes

| (32) |

If we dualize the constraint with a Lagrangian multiplier we obtain the relaxed problem where

| (33) |

Note that the in

is the same as in

| (34) |

Note that (34) is an orthogonal projection onto the simplex. Therefore, it can be solved efficiently (Duchi et al., 2008). We call an optimal solution of (34). Then can be rewritten

We can therefore binary search as in the previous expression. An upper bound for can be computed as follows. Note that

Since is concave we can choose such that . Using the previous inequality this yields

We choose a precision of in our simulations. Note that these binary searches make OMD, FTRL, O-FTRL and O-OMD slower than CBA+ in terms of running times, since the updates in CBA+ only requires to compute the projection , and we have shown in Proposition D.4 and Appendix D.2 how to compute this in when is an ball .

Computing the theoretical step sizes

We now give details about the choice of choice of theoretical step sizes. In theory (e.g., Ben-Tal and Nemirovski (2001)), for a player with decision set , we can choose with , and an upper bound on the norm of any observed loss : . Note that this requires to know 1) the number of steps , and 2) the upper bound on the norm of any observed loss , before the losses are generated. We now show how to compute and (for the -player and the -player) for an instance of the distributionally robust optimization problem (5).

-

1.

For the -player, the loss is , with . For each we have so that

-

2.

For the -player we have , where is the matrix of subgradients of at :

Therefore, , because . Now we have . From we use

Appendix G Additional details and numerical experiments for distributionally robust optimization

We compare CBA+ with alternation and linear averaging, OMD,FTRL,O-OMD and O-OMD for various step sizes where for , on additional synthetic and real data sets. We also add a comparison with adaptive step sizes.

Data sets

We present here the characteristics of the data sets that we use in our DRO simulations. All data sets can be downloaded from the libsvm classification libraries333https://www.csie.ntu.edu.tw/cjlin/libsvmtools/datasets/

-

•

Adult data set: two classes, samples with features.

-

•

Australian data set: two classes, samples with features.

-

•

Madelon data set: two classes, samples with features.

-

•

Splice data set: two classes, samples with features.

Additional experiments with fixed step sizes

In this section we present additional numerical experiments for solving distributionally robust optimization instances in Figure 10. We use a synthetic data set, where we sample the features as uniform random variables in . We also present results for the adult and the australian data sets from libsvm. We vary the aggressiveness of the step sizes by multiplying the theoretical step sizes by a multiplicative step factor . The empirical setting is the same as in Section 4. We note that our algorithm still outperforms or performs on par with the classical approaches after iterations, without requiring a single choice of parameter.

Additional experiments with adaptive step sizes

We present our additional results with adaptive step sizes in Figure 11. Given the payoff observed by the player at period , and following Orabona (2019), we choose the step sizes as

| (35) |

We note that CBA+ still outperforms, or performs on par, with the state-of-the-art approaches.