Optimal False Discovery Rate Control for Large Scale Multiple Testing with Auxiliary Information

Abstract

Large-scale multiple testing is a fundamental problem in high dimensional statistical inference. It is increasingly common that various types of auxiliary information, reflecting the structural relationship among the hypotheses, are available. Exploiting such auxiliary information can boost statistical power. To this end, we propose a framework based on a two-group mixture model with varying probabilities of being null for different hypotheses a priori, where a shape-constrained relationship is imposed between the auxiliary information and the prior probabilities of being null. An optimal rejection rule is designed to maximize the expected number of true positives when average false discovery rate is controlled. Focusing on the ordered structure, we develop a robust EM algorithm to estimate the prior probabilities of being null and the distribution of -values under the alternative hypothesis simultaneously. We show that the proposed method has better power than state-of-the-art competitors while controlling the false discovery rate, both empirically and theoretically. Extensive simulations demonstrate the advantage of the proposed method. Datasets from genome-wide association studies are used to illustrate the new methodology.

Keywords: EM algorithm, False discovery rate, Isotonic regression, Local false discovery rate, Multiple testing, Pool-Adjacent-Violators algorithm.

1 Introduction

Large scale multiple testing refers to simultaneously testing of many hypotheses. Given a pre-specified significance level, family-wise error rate (FWER) controls the probability of making one or more false rejections, which can be unduly conservative in many applications. The false discovery rate (FDR) controls the expected value of the false discovery proportion, which is defined as the ratio of the number of false rejections divided by the number of total rejections. Benjamini and Hochberg (BH) [5] proposed a FDR control procedure that sets adaptive thresholds for the -values. It turns out that the actual FDR level of the BH procedure is the multiplication of the proportion of null hypotheses and the pre-specified significance level. Therefore, the BH procedure can be overly conservative when the proportion of null hypotheses is far from one. To address this issue, [43] proposed a two-stage procedure (ST), which first estimates the proportion of null hypotheses and uses the estimated proportion to adjust the threshold in the BH procedure at the second stage. From an empirical Bayes perspective, [17] proposed the notion of local FDR (Lfdr) based on the two-group mixture model. [45] developed a step-up procedure based on Lfdr and demonstrated its optimality from the compound decision viewpoint.

The aforementioned methods are based on the premise that the hypotheses are exchangeable. However, in many scientific applications, particularly in genomics, auxiliary information regarding the pattern of signals is available. For instance, in differential expression analysis of RNA-seq data, which tests for difference in the mean expression of the genes between conditions, the sum of read counts per gene across all samples could be the auxiliary data since it is informative of the statistical power [35]. In differential abundance analysis of microbiome sequencing data, which tests for difference in the mean abundance of the detected bacterial species between conditions, the genetic divergence among species is important auxiliary information, since closely-related species usually have similar physical characteristics and tend to covary with the condition of interest [50]. In genome-wide association studies, the major objective is to test for association between the genetic variants and a phenotype of interest. The minor allele frequency and the pathogenicity score of the genetic variants, which are informative of the statistical power and the prior null probability, respectively, are potential auxiliary data, which could be leveraged to improve the statistical power as well as enhance interpretability of the results.

Accommodating auxiliary information in multiple testing has recently been a very active research area. Many methods have been developed adapting to different types of structure among the hypotheses. The basic idea is to relax the -value thresholds for hypotheses that are more likely to be alternative and tighten the thresholds for the other hypotheses so that the overall FDR level can be controlled. For example, [19] proposed to weight the -values with different weights, and then apply the BH procedure to the weighted -values. [23] developed a group BH procedure by estimating the proportion of null hypotheses for each group separately. [34] generalized this idea by using the censored -values (i.e., the -values that are greater than a pre-specified threshold) to adaptively estimate the weights that can be designed to reflect any structure believed to be present. [25, 26] proposed the independent hypothesis weighting (IHW) for multiple testing with covariate information. The idea is to use cross-weighting to achieve finite-sample FDR control. Note that the binning in IHW is only to operationalize the procedure and it can be replaced by the proposed EM algorithm below.

The above procedures can be viewed to some extent as different variants of the weighted-BH procedure. Another closely related method was proposed in [30], which iteratively estimates the -value threshold using partially masked -values. It can be viewed as a type of Knockoff procedure [BC2015] that uses the symmetry of the null distribution to estimate the false discovery proportion.

Along a separate line, Lfdr-based approaches have been developed to accommodate various forms of auxiliary information. For example, [9] considered multiple testing of grouped hypotheses. The authors proposed an optimal data-driven procedure that uniformly improves the pooled and separate analyses. [44] developed an Lfdr-based method to incorporate spatial information. [40, 47] proposed EM-type algorithms to estimate the Lfdr by taking into account covariate and spatial information, respectively.

Other related works include [18], which considers the two-group mixture models with side-information. [13] develops a method for estimating the constrained optimal weights for Bonferroni multiple testing. [7] proposes an FDR-controlling procedure based on the covariate-dependent null probabilities.

In this paper, we develop a new method along the line of research on Lfdr-based approaches by adaptively estimating the prior probabilities of being null in Lfdr that reflect auxiliary information in multiple testing. The proposed Lfdr-based procedure is built on the optimal rejection rule as shown in Section 2.1 and thus is expected to be more powerful than the weighted-BH procedure when the underlying two-group mixture model is correctly specified. Compared to existing work on Lfdr-based methods, our contributions are three-fold. (i) We outline a general framework for incorporating various forms of auxiliary information. This is achieved by allowing the prior probabilities of being null to vary across different hypotheses. We propose a data-adaptive step-up procedure and show that it provides asymptotic FDR control when relevant consistent estimates are available. (ii) Focusing on the ordered structure, where auxiliary information generates a ranked list of hypotheses, we develop a new EM-type algorithm [12] to estimate the prior probabilities of being null and the distribution of -values under the alternative hypothesis simultaneously. Under monotone constraint on the density function of -values under the alternative hypothesis, we utilize the Pool-Adjacent-Violators Algorithm (PAVA) to estimate both the prior probabilities of being null and the density function of -values under the alternative hypothesis (see [20] for early work on this kind of problems). Due to the efficiency of PAVA, our method is scalable to large datasets arising in genomic studies. (iii) We prove asymptotic FDR control for our procedure and obtain some consistency results for the estimates of the prior probabilities of being null and the alternative density, which is of independent theoretical interest. Finally, to allow users to conveniently implement our method and reproduce the numerical results reported in Sections 6-7, we make our code publicly available at https://github.com/jchen1981/OrderShapeEM.

The problem we considered is related but different from the one in [21, 33], where the authors seek the largest cutoff so that one rejects the first hypotheses while accepts the remaining ones. So their method always rejects an initial block of hypotheses. In contrast, our procedure allows researchers to reject the th hypothesis but accept the th hypothesis in the ranked list. In other words, we do not follow the order restriction strictly. Such flexibility could result in a substantial power increase when the order information is not very strong or even weak, as observed in our numerical studies. Also see the discussions on monotonicity in Section 1.1 of [40].

To account for the potential mistakes in the ranked list or to improve power by incorporating external covariates, alternative methods have been proposed in the literature. For example, [36] extends the fixed sequence method to allow more than one acceptance before stopping. [32] modifies AdaPT in [30] by giving analysts the power to enforce the ordered constraint on the final rejection set. Though aiming for addressing a similar issue, our method is motivated from the empirical Bayes perspective, and it is built on the two-group mixture model that allows the prior probabilities of being null to vary across different hypotheses. The implementation and theoretical analysis of our method are also quite different from those in [32, 36].

Finally, it is also worth highlighting the difference with respect to the recent work [11] which is indeed closely related to ours. First of all, our Theorem 3.3 concerns about the two-group mixture models with decreasing alternative density, while Theorem 3.1 in [11] focuses on a mixture of Gaussians. We generalize the arguments in [48] by considering a transformed class of functions to relax the boundedness assumption on the class of decreasing densities. A careful inspection of the proof of Theorem 3.3 reveals that the techniques we develop are quite different from those in [11]. Second, we provide a more detailed empirical and theoretical analysis of the FDR-controlling procedure. In particular, we prove that the step-up procedure based on our Lfdr estimates asymptotically controls the FDR and provide the corresponding power analysis. We also conduct extensive simulation studies to evaluate the finite sample performance of the proposed Lfdr-based procedure.

The rest of the paper proceeds as follows. Section 2 proposes a general multiple testing procedure that incorporates auxiliary information to improve statistical power, and establishes its asymptotic FDR control property. In Section 3, we introduce a new EM-type algorithm to estimate the unknowns and study the theoretical properties of the estimators. We discuss two extensions in Section 5. Section 6 and Section 7 are devoted respectively to simulation studies and data analysis. We conclude the paper in Section 8. All the proofs of the main theorems and technical lemmas are collected in the Appendix.

2 Covariate-adjusted multiple testing

In this section, we describe a covariate-adjusted multiple testing procedure based on Lfdr.

2.1 Optimal rejection rule

Consider simultaneous testing of hypotheses for based on -values , where is the -value corresponding to the th hypothesis Let indicate the underlying truth of the th hypothesis. In other words, if is non-null/alternative and if is null. We allow the probability that to vary across . In this way, auxiliary information can be incorporated through

| (2.1) |

Consider the two-group model for the -values (see e.g., [15] and Chapter 2 of [16]):

| (2.2) |

where is the density function of the -values under the null hypothesis and is the density function of the -values under the alternative hypothesis. The marginal probability density function of is equal to

| (2.3) |

We briefly discuss the identifiability of the above model. Suppose is known and bounded away from zero and infinity. Consider the following class of functions:

Suppose , where the th components of and are given by and respectively. We show that if for all and , then and for all and . Suppose for some . If for some , then we have

| (2.4) |

which is a contradiction. Similarly, we get a contradiction when for some . Thus we have for all . As there exists a such that , it is clear that implies that .

In statistical and scientific applications, the goal is to separate the alternative cases () from the null cases (). This can be formulated as a multiple testing problem, with solutions represented by a decision rule It turns out that the optimal decision rule is closely related to the Lfdr defined as

In other words, is the posterior probability that a case is null given the corresponding -value is equal to . It combines the auxiliary information () and data from the current experiment. Information across tests is used in forming and

Optimal decision rule under mixture model has been extensively studied in the literature, see e.g., [46, 30, 3]. For completeness, we present the derivations below and remark that they follow somewhat directly from existing results. Consider the expected number of false positives (EFP) and true positives (ETP) of a decision rule. Suppose that follows the mixture model (2.2) and we intend to reject the th null hypothesis if The size and power of the th test are given respectively by

It thus implies that

where We wish to maximize ETP for a given value of the marginal FDR (mFDR) defined as

| (2.5) |

by an optimum choice of the cutoff value Formally, consider the problem

| (2.6) |

A standard Lagrange multiplier argument gives the following result which motivates our choice of thresholds.

Proposition 1.

Assume that is continuously non-increasing, and is continuously non-decreasing and uniformly bounded from above. Further assume that for a pre-specified

| (2.7) |

Then (2.6) has at least one solution and every solution satisfies

for some that is independent of

The proof of Proposition 1 is similar to that of Theorem 2 in [30] and we omit the details. Under the monotone likelihood ratio assumption [45, 10]:

| (2.8) |

we obtain that is monotonically increasing in Therefore, we may reduce our attention to the rejection rule as

| (2.9) |

for a constant to be determined later.

2.2 Asymptotic FDR control

To fully understand the proposed method, we gradually investigate its theoretical properties through several steps, starting with an oracle procedure which provides key insights into the problem. Assume that and are known. The proposed method utilizes auxiliary information through and information from the alternative through in addition to information from the null, upon which conventional approaches are based. In view of (2.9), the number of false rejections equals to

and the total number of rejections is given by

Write and . We aim to find the critical value in (2.9) that controls the FDR, which is defined as at a pre-specified significance level Note that

| (2.10) |

An estimate of the is given by

Let . Then reject if Below we show that the above (oracle) step-up procedure provides asymptotic control on the FDR under the following assumptions.

-

(C1)

Assume that for any ,

and

(2.11) where and are both continuous functions over .

-

(C2)

Write , where and are defined in (C1). There exists a such that

We remark that (C1) is similar to those for Theorem 4 in [42]. In view of (2.10), (2.11) follows from the weak law of large numbers. Note that (C1) allows certain forms of dependence, such as -dependence, ergodic dependence and certain mixing type dependence. (C2) ensures the existence of the critical value to asymptotically control the FDR at level The following proposition shows that the oracle step-up procedure provides asymptotic FDR control.

Proposition 2.

Under conditions (C1)-(C2),

The proof of Proposition 2 is relegated in the Appendix. In the following, we mimic the operation of the oracle procedure and provide an adaptive procedure. In the inference problems that we are interested in, the -value distribution under the null hypothesis is assumed to be known (e.g., the uniform distribution on , or can be obtained from the distributional theory of the test statistic in question). Below we assume is known and remark that our result still holds provided that can be consistently estimated. In practice, and are often unknown and replaced by their sample counterparts. Let and be the estimators of and respectively. Define

where A natural estimate of can be obtained through

Reject the th hypothesis if . This is equivalent to the following step-up procedure that was originally proposed in [45]. Let be the order statistics of and denote by the corresponding ordered hypotheses. Define

We show that this step-up procedure provides asymptotic control on the FDR. To facilitate the derivation, we make the following additional assumption.

-

(C3)

Assume that

Remark 1.

(C4) imposes uniform (weak) consistency on the estimators and Condition (C5) requires the joint empirical distribution function of and to converge to a continuous function. Both conditions are useful in showing that the empirical distribution functions based on and are uniformly close, which is a key step in the proof of Theorem 1. Notice that we do not require the consistency of the estimators at the boundaries. Such a relaxation is important when and are estimated using the shape-restricted approach. For example, [14] showed uniform consistency for the Grenander-type estimators on the interval with .

(C3) requires the Lfdr estimators to be consistent in terms of the empirical norm. We shall justify Condition (C3) in Section 3.3.

Theorem 1.

Under Conditions (C1)-(C3),

3 Estimating the unknowns

3.1 The density function is known

We first consider the case that and are both known. Under such setup, we need to estimate unknown parameters which is prohibitive without additional constraints. One constraint that makes the problem solvable is the monotone constraint. In statistical genetics and genomics, investigators can use auxiliary information (e.g., -values from previous or related studies) to generate a ranked list of hypotheses even before performing the experiment, where is the hypothesis that the investigator believes to most likely correspond to a true signal, while is the one believed to be least likely. Specifically, let Define the convex set

We illustrate the motivation for the monotone constraint with an example.

Example 3.1.

Suppose that we are given data consisting of a pair of values where represents the -value, represents auxiliary information and they are independent conditional on the hidden true state for Suppose

| (3.12) |

where if is alternative and if is null, is the density function of -values or auxiliary variables under the null hypothesis and is the density function of -values or auxiliary variables under the alternative hypothesis. Suppose for all Using the Bayes rule and the independence between and given we have the conditional distribution of as follows:

where

If is a monotonic function, so is . Therefore, the order of generates a ranked list of the hypotheses through the conditional prior probability .

We estimate by solving the following maximum likelihood problem:

| (3.13) |

It is easy to see that (3.13) is a convex optimization problem. Let . To facilitate the derivations, we shall assume that for all , which is a relatively mild requirement. Under this assumption, it is straightforward to see that for any , is a strictly concave function for Let be the unique maximizer. According to Theorem 3.1 of [37], we have

| (3.14) |

However, this formula is not practically useful due to the computational burden when is very large. Below we suggest a more efficient way to solve problem (3.13). A general algorithm when is unknown is provided in the next subsection. The main computational tools are the EM algorithm for two-group mixture model and the Pool-Adjacent-Violator-Algorithm from isotonic regression for the monotone constraint on the prior probability of null hypothesis [12, 38]. Our procedure is tuning parameter free and can be easily implemented in practice. The EM algorithm treats the hidden state as missing data. The isotonic regression problem is to

| (3.15) |

where and are given. By [22], the solution to (3.15) can be written as

| (3.16) |

We need a key result from [4] which we present below for completeness.

Proposition 3.

(Theorem 3.1 in [4]) Let be a proper convex function on and its derivative. Denote dimensional vectors and We call the problem

| (3.17) |

the generalized isotonic regression problem. Then

| (3.18) |

where

| (3.19) |

solves the generalized isotonic regression problem (3.17). The minimization function is unique if is strictly convex.

Observe that (3.16) and (3.19) have the same expression. In practice, we implement the Pool-Adjacent-Violator-Algorithm by solving (3.15) to get

Let be the solution at the th iteration. Define

At the th iteration, we solve the following problem,

| (3.20) |

To use Proposition 3, we first do a change of variable by letting We proceed by solving

which has the same solution to the problem

We write it as

By Proposition 3, we have

In practice, we obtain through the Pool-Adjacent-Violators Algorithm (PAVA) [38] by solving the following problem

| (3.21) |

Note that if , then the solution to (3.21) is simply given by for all As the EM algorithm is a hill-climbing algorithm, it is not hard to show that is a non-decreasing function of .

We study the asymptotic consistency of the true maximum likelihood estimator which can be represented as (3.14). To this end, consider the model

for some non-decreasing function Our first result concerns the point-wise consistency for each . For a set , denote by its cardinality.

Theorem 2.

Assume that for , and . Suppose For any , let such that Denote and . For we have

The condition on the cardinalities of and guarantees that there are sufficient observations around , which allows us to borrow information to estimate consistently. The assumption ensures that the maximizer is unique for It is fulfilled if the set has zero Lebesgue measure. As a direct consequence of Theorem 2, we have the following uniform consistency result of . Due to the monotonicity, the uniform convergence follows from the pointwise convergence.

Corollary 1.

For suppose there exists a set , where each satisfies the assumption for in Theorem 2 and that Then we have

Remark 3.1.

Suppose is Lipschitz continuous with the Lipschitz constant . Then we can set , and thus . Our result suggests that

which implies that

3.2 The density function is unknown

In practice, and are both unknown. We propose to estimate and by maximizing the likelihood, i.e.,

| (3.22) |

where is a pre-specified class of density functions. In (3.22), might be the class of beta mixtures or the class of decreasing density functions. Problem (3.22) can be solved by Algorithm 1. A derivation of Algorithm 1 from the full data likelihood that has access to latent variables is provided in the Appendix. Our algorithm is quite general in the sense that it allows users to specify their own updating scheme for the density components in (3.24). Both parametric and non-parametric methods can be used to estimate .

| (3.23) |

| (3.24) |

In the multiple testing literature, it is common to assume that

is a decreasing density function (e.g., smaller -values imply stronger

evidence against the null), see e.g. [29]. As an

example of the general algorithm, let denote the

class of decreasing density functions. We shall discuss how (3.24) can

be solved using the PAVA. The key recipe is to use Proposition 3 in obtaining evaluated at the observed -values.

Specifically, it can be accomplished by a series of steps outlined

below. Define the order statistics of as Let be the corresponding that is associated with .

Step 1: The objective function in (3.24) only looks at the value of at . The objective function increases if increases, and

the value of at has no impact on the objective

function (where ). Therefore, if maximizes the objective

function, there is a solution that is constant on .

Step 2: Let . We only need to find which maximizes

subject to and

. It can be formulated as a convex

programming problem which is tractable. In Steps 3 and 4 below, we further translate it into an isotonic regression problem.

Step 3: Write . Consider the problem:

The solution is given by

, which

satisfies the constraint in Step

2.

Step 4: Rewrite the problem in Step 3 as

This is the generalized isotonic regression problem considered in Proposition 3. We use (3.16) to obtain (3.19) as follows. Let

subject to The solution is given by the max-min formula

which can be obtained using the PAVA. By Proposition 3, we arrive at the solution to the original problem (3.24) by letting Therefore, in the EM-algorithm, one can employ the PAVA to estimate both the prior probabilities of being null and the -value density function under the alternative hypothesis. Because of this, our algorithm is fast and tuning parameter free, and is very easy to implement in practice.

3.3 Asymptotic convergence and verification of Condition (C3)

In this subsection, we present some convergence results regarding the proposed estimators in Section 3.2. Furthermore, we propose a refined estimator for , and justify Condition (C3) for the corresponding Lfdr estimator. Throughout the following discussions, we assume that

independently for and with . Let be the class of densities defined on . For , we define the squared Hellinger-distance as

Suppose the true alternative density belongs to a class of decreasing density functions . Let and assume that Consider and for , and . Define the average squared Hellinger-distance between and as

Suppose is an estimator of such that

where . Note that we do not require to be the global maximizer of the likelihood. We have the following result concerning the convergence of to in terms of the average squared Hellinger-distance.

Theorem 3.

Suppose , , and . Under the assumption that for some we have

for some and We remark that with satisfies for .

Theorem 3 follows from an application of Theorem 8.14 in [48]. By Cauchy-Schwarz inequality, it is known that

Under the conditions in Theorem 3, we have

| (3.25) |

However, and are generally unidentifiable without extra conditions. Below we focus on the case . The model is identifiable in this case if there exists an such that . If is decreasing, then for . Suppose . For a sequence such that

| (3.26) |

as , we define the refined estimator for as

Under (3.26), we have

| (3.27) |

Given the refined estimator , the Lfdr can be estimated by

As and thus are bounded from below, by (3.25) and (3.27), it is not hard to show that

| (3.28) |

Moreover, we have the following result which justifies Condition (C3).

Corollary 2.

Suppose , , and . Further assume in Condition (C1) is continuous at zero and (3.26) holds. Then Condition (C3) is fulfilled.

Remark 3.2.

Although needs to satisfy (3.26) theoretically, the rate condition is of little use in selecting in practice. We use a simple ad-hoc procedure that performs reasonably well in our simulations. To motivate our procedure, we let indicate the underlying truth of a randomly selected hypothesis from . Then we have

Without knowing the order information, the -values follow the mixture model The overall null proportion can be estimated by classical method, e.g., [41] (in practice, we use the maximum of the two Storey’s global null proportion estimates in the qvalue package for more conservativeness). Denote the corresponding estimator by . Also denote , where is the calibrated null probability and is the amount of calibration, which is a function of . Then it makes sense to choose such that the difference is minimized. This results in the procedure that if the mean of ’s from the EM algorithm (denote as is greater than the global estimate , , and if the mean is less than , then , where .

4 A general rejection rule

Given the insights from Section 2, we introduce a general rejection rule and also discuss its connection with the recent accumulation tests in the literature, see e.g. [21, 2, 33]. Recall that our (oracle) rejection rule is , which can be written equivalently as

Motivated by the above rejection rule, one can consider a more general procedure as follows. Let be a decreasing non-negative function such that . The general rejection rule is then defined as

| (4.29) |

for . Here serves as a surrogate for the likelihood ratio Set . Under the assumption that is symmetric about 0.5 (i.e. ), it is easy to verify that . We note that the false discovery proportion (FDP) for the general rejection rule is equal to

If we set for and for , then for and for Therefore, we have

where the approximation is due to the law of large numbers. With this choice of , one intends to follow the prior order restriction strictly. As suggested in [21, 2], a natural choice of is given by

which is designed to control the (asymptotic) upper bound of the FDP.222Finite sample FDR control has been proved for this procedure, see e.g. [33]. Some common choices of are given by

for , which correspond to the ForwardStop, SeqStep and HingeExp procedures respectively. Note that all procedures are special cases of the accumulation tests proposed in [33].

Different from the accumulation tests, we suggest to use and . Our procedure is conceptually sound as it is better motivated from the Bayesian perspective, and it avoids the subjective choice of accumulation functions.

Remark 4.1.

Our setup is different from the one in [21], where the authors seek for the largest cutoff so that one rejects the first hypothesis while accepts the remaining ones. In contrast, our procedure allows researchers to reject the th hypothesis but accept the th hypothesis. In other words, we do not follow the order restriction strictly. Such flexibility could result in a substantial power increase when the order information is not very strong or even weak as observed in our numerical studies.

Below we conduct power comparison with the accumulation tests in [33], which include the ForwardStop procedure in [21] and the SeqStep procedure in [2] as special cases. Let be a nonnegative function with and . Define

where if the above set is empty. The asymptotic power of the accumulation test in [33] is given by

Notice that the accumulation test rejects the first hypotheses in the ordered list, which is equivalent to setting the threshold for and otherwise. Suppose satisfies

Then after some re-arrangements, we have

which suggests that the accumulation test controls the mFDR defined in (2.5) at level By the discussion in Section 2.1, the optimal thresholds are the level surfaces of the Lfdr. Therefore the proposed procedure is more powerful than the accumulation test asymptotically.

4.1 Asymptotic power analysis

We provide asymptotic power analysis for the proposed method. In particular, we have the following result concerning the asymptotic power of the Lfdr procedure in Section 2.2.

Theorem 4.

Suppose Conditions (C1)-(C3) hold and additionally assume that

for a continuous function of on [0,1]. Let be the largest such that and for any small enough , Then we have

Recall that in Section 2.1, we have shown that the step-up procedure has the highest expected number of true positives amongst all -level FDR rules. This result thus sheds some light on the asymptotic optimal power amongst all -level FDR rules when the number of hypothesis tests goes to infinity.

Remark 4.2.

Under the two-group mixtue model (2.1)-(2.2) with for some non-decreasing function , we have as monotonic functions are Riemann integrable. Thus . Define and . Denote by the distribution function of . Then we have

where “” denotes the composition of two functions, and we have used the fact that is monotonic and thus Riemann integrable. So

5 Two extensions

5.1 Grouped hypotheses with ordering

Our idea can be extended to the case where the hypotheses can be divided into groups within which there is no explicit ordering but between which there is an ordering. One can simply modify (3.23) by considering the problem,

| (5.30) |

subject to , where is the group index for the th hypothesis. A particular example is about using the sign to improve power while controlling the FDR. Consider a two-sided test where the null distribution is symmetric and the test statistic is the absolute value of the symmetric statistic. The sign of the statistic is independent of the -value under the null. If we have a priori belief that among the alternatives, more hypotheses have true positive effect sizes than negative ones or vice versa, then sign could be used to divide the hypotheses into two groups such that (or ).

5.2 Varying alternative distributions

In model (2.1), we assume that the success probabilities vary with while is independent of . This assumption is reasonable in some applications but it can be restrictive in other cases. We illustrate this point via a simple example described below.

Example 5.2.

For , let be observations generated independently from . Consider the one sided -test with for testing

The -value is equal to and the -value distribution under the alternative hypothesis is given by

with the density

By prioritizing the hypotheses based on the values of , one can expect more discoveries. Suppose

One can consider the following problem to estimate and simultaneously,

This problem can again be solved using the EM algorithm together with the PAVA.

Generally, if the -value distribution under the alternative hypothesis, denoted by , is allowed to vary with , model (2.1)-(2.2) is not estimable without extra structural assumptions as we only have one observation that is informative about . On the other hand, if we assume that which varies smoothly over , then one can use non-parametric approach to estimate each based on the observations in a neighborhood of . However, this method requires the estimation of density functions at each iteration, which is computationally expensive for large . To reduce the computational cost, one can divide the indices into consecutive bins, say and assume that the density remains unchanged within each bin. In the M-step, we update via

| (5.31) |

for For small , the computation is relatively efficient. We note that this strategy is related to the independent hypothesis weighting proposed in [25, 26], which divides the p-values into several bins and estimate the cumulative distribution function (CDF) of the p-values in each stratum. Our method is different from theirs in the following aspect: the estimated densities will be used in constructing the optimal rejection rule, while in their procedure, the varying CDF is used as an intermediate quantity to determine the thresholds for p-values in each stratum. In other words, the estimated CDFs are not utilized optimally in constructing the rejection rule.

6 Simulation studies

6.1 Simulation setup

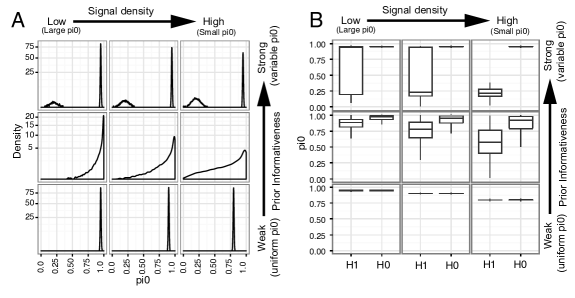

We conduct comprehensive simulations to evaluate the finite-sample performance of the proposed method and compare it to competing methods. For simplicity, we directly simulate -values for hypotheses. All simulations are replicated 100 times except for the global null, where the results are based on 2,000 Monte Carlo replicates. We simulate different combinations of signal density (the percentage of alternative) and signal strength (the effect size of alternative) since these are two main factors affecting the power of multiple testing procedures. We first generate the hypothesis-specific null probability (), upon which the truth, i.e., null or alternative, is simulated. Afterwards, we generate -values based on the truth of the hypothesis. We first use as the auxiliary covariate. Later, we will study the effect of using noisy as auxiliary covariate. Three scenarios, representing weakly, moderately and highly informative auxiliary information, are simulated based on the distribution of (Figure 1(a)), where the informativeness of the auxiliary covariate is determined based on its ability to separate alternatives from nulls (Figure 1(b)). In the weakly informative scenario, we make ’s similar for all hypotheses by simulating ’s from a highly concentrated normal distribution (truncated on the unit interval )

In the moderately informative scenario, we allow to vary across hypotheses with moderate variability. This is achieved by simulating ’s from a beta distribution

In the highly informative scenario, ’s are simulated from a mixture of a truncated normal and a highly concentrated truncated normal distribution

which represents two groups of hypotheses with strikingly different probabilities of being null.

Since the expected alternative proportion is

, we adjust the parameters and to

achieve approximately 5%, 10% and 20% signal density level. Figure 1(a) shows the distribution of for the three scenarios. Based on ,

the underlying truth is simulated from

Figure 1(b) displays the distribution of for and from one simulated dataset. As the difference in between and gets larger, the auxiliary covariate becomes more informative. Finally, we simulate independent -values using

where controls the signal strength and and are chosen to represent weak, moderate and strong signal, respectively. We convert -values to -values using the formula . The proposed method accepts -values and s as input. The specific parameter values mentioned above could be found in https://github.com/jchen1981/OrderShapeEM.

To examine the robustness of the proposed method, we vary the simulation setting in different ways. Specifically, we investigate:

-

1.

Skewed alternative distribution. Instead of simulating normal -values for the alternative group, we simulate -values from a non-central gamma distribution with the shape parameter . The scale and non-centrality parameters of the non-central gamma distribution are chosen to match the mean and variance of the normal distribution for the alternative group under the basic setting.

-

2.

Correlated hypotheses. Our theory allows certain forms of dependence. We then simulate correlated -values, which are drawn from a multivariate normal distribution with a block correlation structure. The order of is random with respect to the block structure. Specifically, we divide the hypotheses into blocks and each block is further divided into two sub-blocks of equal size. Within each sub-block, there is a constant positive correlation (). Between the sub-blocks in the same block, there is a constant negative correlation (). Hypotheses in different blocks are independent. We use to illustrate. The correlation matrix is

-

3.

Noisy auxiliary information. In practice, the auxiliary data can be very noisy. To examine the effect of noisy auxiliary information, we shuffle half or all the , representing moderately and completely noisy order.

-

4.

A smaller number of alternative hypotheses and a global null. It is interesting to study the robustness of the proposed method under an even more sparse signal. We thus simulate 1% alternatives out of 10,000 features. We also study the error control under a global null, where all the hypotheses are nulls. Under the global null, We increased the number of Monte Carlo simulations to 2,000 times to have a more accurate estimate of the FDR.

-

5.

Varying across alternative hypotheses. We consider the case where among the alternative hypotheses, the most promising 20% hypotheses (i.e., those with the lowest prior order) follow and the remaining p-values are derived from the z-values (see the setting of Figure 2).

-

6.

Varying across null hypotheses. Similar to the case of varying , we sample the p-values of 20% of the null hypotheses with the highest prior order from , which mimics the composite null situations. The remaining p-values are derived from the z-values as above.

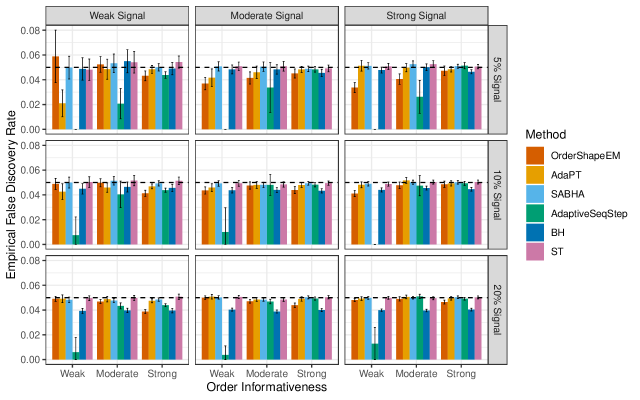

We compare the proposed method (OrderShapeEM) with classical multiple testing methods that do not utilize external covariates (BH and ST) and recent multiple testing procedures that exploit auxiliary information (AdaPT, SABHA, AdaptiveSeqStep). Detailed descriptions of these methods are provided in the appendix. The FDP estimate of AdaPT involves a finite-sample correction term +1 in the numerator. The +1 term yields a conservative procedure and could lose power when the signal density is low. To study the effect of the correction term, we also compared to AdaPT+, where we removed the correction term +1 in the numerator. However, we observed a significant FDR inflation when the signal density is low, see Figure LABEL:fig14 in the Appendix. We thus compared to AdaPT procedure with correction term throughout the simulations.

6.2 Simulation results

We first discuss the simulation results of Normal alternative distribution.

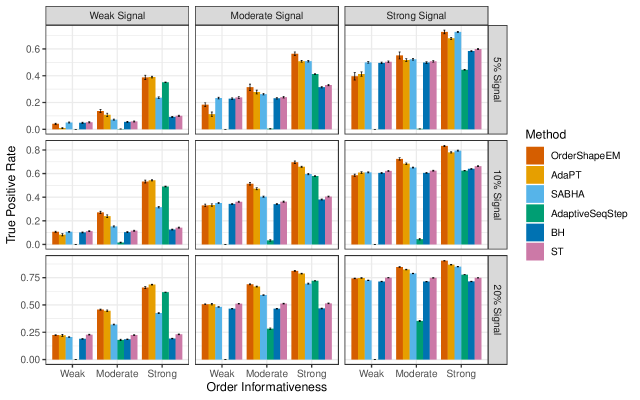

In Figure 2 and 3, we present FDR control and power comparison with different methods when -values under the null hypothesis follow and -values under the alternative hypothesis follow a normal distribution. In Figure 2, the dashed line indicates the pre-specified FDR control level and the error bars represent empirical confidence intervals. We observe that all procedures control the FDR sufficiently well across settings and no FDR inflation has been observed. Adaptive SeqStep is conservative most of the time especially when the signal is sparse and the auxiliary information is weak or moderate. AdaPT is conservative under sparse signal and weak auxiliary information. The proposed procedure OrderShapeEM generally controls the FDR at the target level with some conservativeness under some settings. As expected, ST procedure controls the FDR at the target level while BH procedure is more conservative under dense signal. In Figure 3, we observe that OrderShapeEM is overall the most powerful when the auxiliary information is not weak. When the auxiliary information is weak and the signal is sparse, OrderShapeEM could be less powerful than BH/ST. Close competitors are AdaPT and SABHA. However, AdaPT is significantly less powerful when the signal is sparse and the auxiliary information is weak. AdaPT is also computationally more intensive than the other methods. SABHA performs well when the signal is strong but becomes much less powerful than OrderShapeEM and AdaPT as the signal weakens. Adaptive SeqStep has good power for dense signal and moderate to strong auxiliary information. However, it is powerless when auxiliary information is weak. If auxiliary information is weak, SABHA, ST and BH have similar power, while Adaptive SeqStep has little power. Under this scenario, incorporating auxiliary information does not help much. All methods become more powerful with the increase of signal density and signal strength.

7 Data Analysis

We illustrate the application of our method by analyzing data from publicly available genome-wide association studies (GWAS). We use datasets from two large-scale GWAS of coronary artery disease (CAD) in different populations (CARDIoGRAM and C4D). CARDIoGRAM is a meta-analysis of CAD genome-wide association studies, comprising cases and controls of European descent [39]. The study includes million single nucleotide polymorphisms (SNP). In each of the studies and for each SNP, a logistic regression of CAD status was performed on the number of copies of one allele, along with suitable controlling covariates. C4D is a meta-analysis of heart disease genome-wide association studies, totaling CAD cases and controls [8]. The samples did not overlap those from CARDIoGRAM. The analysis steps were similar to CARDIoGRAM. A total of common SNPs were tested in both the CARDIoGRAM and C4D association analyses. Dataset can be downloaded from http://www.cardiogramplusc4d.org. Available data comprise of a bivariate -value sequence where represents -values from the CARDIoGRAM dataset and represents -values from the C4D dataset,

We are interested in identifying SNPs that are associated with CAD. Due to the shared genetic polymorphisms between populations, information contained in can be helpful in the association analysis of and vice versa. We thus performed two separate analyses, where we conducted FDR control on and respectively, using and as the auxiliary covariate.

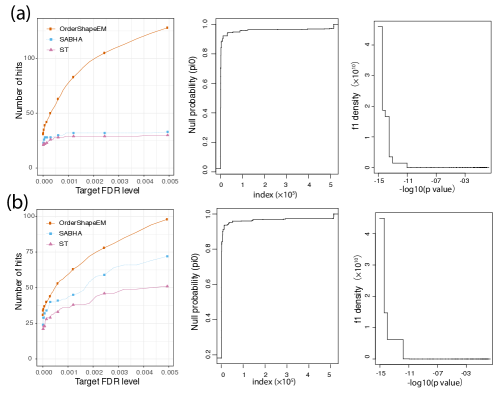

In the analysis, we compare the proposed OrderShapeEM, robust method that incorporates auxiliary information (SABHA) and method that does not incorporate auxiliary information (ST). As BH was outperformed by ST and Adaptive SeqStep by SABHA, we only included ST and SABHA in the comparison. AdaPT was not able to complete the analysis within 24 hours and was not included either. The results are summarized in Figure 4. From Figure 4(a), we observe that at the same FDR level, the proposed OrderShapeEM made significantly more discoveries than SABHA and ST. SABHA procedure, which incorporates the auxiliary information, picked up more SNPs than the ST procedure. The performance of OrderShapeEM is consistent with the weak signal scenario, where a significant increase in power has been observed (Figure LABEL:fig3(b)). Due to disease heterogeneity, signals in the genetic association studies are usually very weak. Thus, it can be extremely helpful to incorporate auxiliary information to improve power. The power difference becomes even larger at higher target FDR level. Figure 4(b) shows similar patterns.

(a) Analysis of C4D data with CARDIoGRAM data as auxiliary information; (b) Analysis of CARDIoGRAM data with C4D data as auxiliary information.

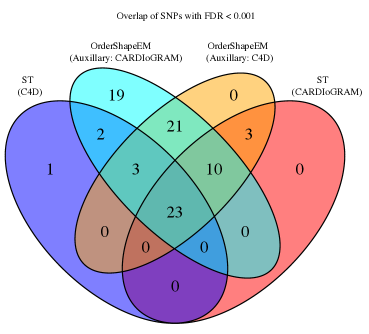

To further examine the identified SNPs based on different methods, Figure 5 shows the overlap of significant SNPs via the Venn diagram at FDR level We observe that there was a significant overlap of associated SNPs between the two datasets, indicating a shared genetic architecture between the two populations. By using auxiliary information, OrderShapeEM recovered almost all the SNPs by ST procedure, in addition to many other SNPs that were missed by the ST procedure. Interestingly, for the SNPs that were identified by OrderShapeEM only, most of them were located in genes that had been reported being associated with phenotypes or diseases related to the cardiovascular or metabolic system. It is well known that metabolic disorders such as high blood cholesterol and triglyceride levels are risk factors for CAD.

8 Summary and discussions

We have developed a covariate-adjusted multiple testing procedure based on the Lfdr and shown that the oracle procedure is optimal in the sense of maximizing the ETP for a given value of mFDR. We propose an adaptive procedure to estimate the prior probabilities of being null that vary across different hypotheses and the distribution function of the -values under the alternative hypothesis. Our estimation procedure is built on the isotonic regression which is tuning parameter free and computationally fast. We prove that the proposed method provides asymptotic FDR control when relevant consistent estimates are available. We obtain some consistency results for the estimates of the prior probabilities of being null and the alternative density under shape restrictions. In finite samples, the proposed method outperforms several existing approaches that exploit auxiliary information to boost power in multiple testing. The gain in efficiency of the proposed procedure is due to the fact that we incorporate both the auxiliary information and the information across -values in an optimal way.

Our method has a competitive edge over competing methods when the signal is weak while the auxiliary information is moderate/strong, a practically important setting where power improvement is critical and possible with the availability of informative prior. However, when the auxiliary information is weak , our procedure could be less powerful than the BH/ST procedure. The power loss is more severe under strong and sparse signals. To remedy the power loss under these unfavorable conditions, we recommend testing the informativeness of the prior order information before the application of our method using, for example, the testing method from [24]. We could also examine the plot after running our algorithm. If ’s lack variability, which indicates the auxiliary information is very weak, our method could be less powerful than BH/ST and we advise against using it.

Our method is also robust across settings with a very moderate FDR inflation under small feature sizes. However, there are some special cases where our approach does not work well due to the violation of assumptions. In the varying alternative scenario, as suggested by one of the reviewers, we did observe some FDR inflation. We found this only happens when the order information has inconsistent effects on the and (i.e., the more likely the alternative hypothesis, the smaller the effect size). We did not find any FDR inflation if the order information has consistent effects (i.e., the more likely the alternative hypothesis, the larger the effect size). We believe such inconsistent effects may be uncommon in practice. In the varying null scenario, we observed a severe deterioration of the power of our method and it has virtually no power when the signal is sparse. This is somewhat expected since our approach assumes a uniformly distributed null p-value. Therefore, we should examine the p-value distribution before applying our method. We advise against using our method if we see a substantial deviation from the uniform assumption based on the right half of the p-value distribution.

There are several future research directions. For example, it is desirable to extend our method to incorporate other forms of structural information such as group structure, spatial structure or tree/hierarchical structure. Also, the proposed method is marginal based and it may no longer be optimal in the presence of correlations. We leave these interesting topics for future research.

Acknowledgements

The authors would like to thank the Associate Editor and the reviewers for their constructive comments and helpful suggestions, which substantially improved the paper. Data on coronary artery disease/myocardial infarction have been contributed by CARDIoGRAMplusC4D investigators and have been downloaded from www.cardiogramplusc4d.org. Cao acknowledges partial support from NIH 2UL1TR001427-5, Zhang acknowledges partial support from NSF DMS-1830392 and NSF DMS-1811747 and Chen acknowledges support from Mayo Clinic Center for Individualized Medicine.

References

- [1] Ayer, M., Brunk, H. D., Ewing, G. M., Reid, W. T., and Silverman, E. (1955). An empirical distribution function for sampling with incomplete information. Annals of Mathematical Statistics, 26, 641-647.

- [2] Barber, R. F., and Candès, E. J. (2015). Controlling the false discovery rate via knockoffs. Annals of Statistics, 43, 2055-2085.

- [3] Basu, P., Cai, T. T., Das, K., and Sun, W. (2018). Weighted false discovery rate control in large scale multiple testing. Journal of the American Statistical Association, 113, 1172–1183.

- [4] Barlow, R. E., and Brunk, H. D. (1972). The isotonic regression problem and its dual. Journal of the American Statistical Association, 67, 140-147.

- [5] Benjamini, Y., and Hochberg, Y. (1995). Controlling the false discovery rate: a practical and powerful approach to multiple testing. Journal of the Royal Statistical Society, Series B, 57, 289-300.

- [6] Birgé, L. (1987). Estimating a density under order restrictions: Nonasymptotic minimax risk. Annals of Statistics, 15, 995-1012.

- [7] Boca, S. M., and Leek, J. T. (2018). A direct approach to estimating false discovery rates conditional on covariates. PeerJ, 6, e6035.

- [8] Coronary Artery Disease (C4D) Genetics Consortium. (2011). A genome-wide association study in Europeans and South Asians identifies five new loci for coronary artery disease. Nature Genetics, 43, 339-344.

- [9] Cai, T. T., and Sun, W. (2009). Simultaneous testing of grouped hypotheses: finding needles in multiple haystacks. Journal of the American Statistical Association, 104, 1467–1481.

- [10] Cao, H., Sun, W., and Kosorok, M. R. (2013). The optimal power puzzle: scrutiny of the monotone likelihood ratio assumption in multiple testing. Biometrika, 100, 495–502.

- [11] Deb, N., Saha, S., Guntuboyina, A., and Sen, B. (2019). Two-component mixture model in the presence of covariates. arXiv preprint arXiv:1810.07897.

- [12] Dempster, A. P., Laird, N. M., and Rubin, D. B. (1977). Maximum likelihood from incomplete data via the EM algorithm. Journal of the Royal Statistical Society: Series B, 39, 1-22.

- [13] Dobriban, E. (2017). Weighted mining of massive collections of -values by convex optimization. Information and Inference: A Journal of the IMA, 7, 251-275.

- [14] Durot, C., Kulikov, V. N., and Lopuhaä, H. P. (2012). The limit distribution of the -error of Grenander-type estimators. Annals of Statistics, 40, 1578-1608.

- [15] Efron, B. (2008). Microarrays, empirical Bayes and the two-groups model. Statistical science, 23, 1-22.

- [16] Efron, B. (2012). Large-scale inference: empirical Bayes methods for estimation, testing, and prediction. Cambridge University Press.

- [17] Efron, B., Tibshirani, R., Storey, J. D., and Tusher, V. (2001). Empirical Bayes analysis of a microarray experiment. Journal of the American Statistical Association, 96, 1151-1160.

- [18] Ferkingstad, E., Frigessi, A., Rue, H., Thorleifsson, G., and Kong, A. (2008). Unsupervised empirical Bayesian testing with external covariates. Annals of Applied Statistics, 2, 714–735.

- [19] Genovese, C. R., Roeder, K., and Wasserman, L. (2006). False discovery control with -value weighting. Biometrika, 93, 509–524.

- [20] Grenander, U. (1956). On the theory of mortality measurement: part ii. Scandinavian Actuarial Journal, 1956, 125-153.

- [21] G’Sell, M. G., Wager, S., Chouldechova, A., and Tibshirani, R. (2016). Sequential selection procedures and false discovery rate control. Journal of the Royal Statistical Society, Series B, 78, 423-444.

- [22] Henzi, A., M’́osching, A. and Dümbgen, L. (2020). Accelerating the Pool-Adjacent-Violators Algorithm for isotonic distributional regression. arXiv:2006.05527

- [23] Hu, J. X., Zhao, H., and Zhou, H. H. (2010). False discovery rate control with groups. Journal of the American Statistical Association, 105, 1215–1227.

- [24] Huang, J.Y., Bai, L., Cui, B.W., Wu, L., Wang, L.W., An, Z.Y,, Ruan, S.L. Yu, Y., Zhang, X.Y., and Chen, J. (2020). Leveraging biological and statistical covariates improves the detection power in epigenome-wide association testing. Genome biology, 21: 1-19.

- [25] Ignatiadis, N., Klaus, B., Zaugg, J. B., and Huber, W. (2016). Data-driven hypothesis weighting increases detection power in genome-scale multiple testing. Nature Methods, 13, 577–580.

- [26] Ignatiadis, N., and Huber, W. (2017). Covariate-powered weighted multiple testing with false discovery rate control. arXiv preprint arXiv:1701.05179.

- [27] Jaffe, A. E., Murakami, P., Lee, H., Leek, J. T., Fallin, M. D., Feinberg, A. P., Irizarry, R. A. (2012). Bump hunting to identify differentially methylated regions in epigenetic epidemiology studies. International Journal of Epidemiology, 41, 200–209.

- [28] Kristensen, V. N., Lingjarde, O. C., Russnes, H. G., Vollan, H. K. M., Frigessi, A., and Borresen-Dale, A.-L. (2014). Principles and methods of integrative genomic analyses in cancer. Nature Review Cancer, 14, 299–313.

- [29] Langaas, M., Lindqvist, B. H., and Ferkingstad, E. (2005). Estimating the proportion of true null hypotheses, with application to DNA microarray data. Journal of the Royal Statistical Society, Series B, 67, 555–572.

- [30] Lei, L., and Fithian, W. (2018). AdaPT: An interactive procedure for multiple testing with side information. Journal of the Royal Statistical Society, Series B, 80, 649–679.

- [31] Lei, L., and Fithian, W. (2016). Power of Ordered Hypothesis Testing. arXiv preprint arXiv:1606.01969.

- [32] Lei, L., Ramdas, A., and Fithian, W. (2020). STAR: A general interactive framework for FDR control under structural constraints. Biometrika, to appear.

- [33] Li, A., and Barber, R. F. (2017). Accumulation tests for FDR control in ordered hypothesis testing. Journal of the American Statistical Association, 112, 837–849.

- [34] Li, A., and Barber, R. F. (2019). Multiple testing with the structure adaptive Benjamini-Hochberg algorithm. Journal of the Royal Statistical Society, Series B, 81, 45–74.

- [35] Love, M., Huber, W., and Anders, S. (2014). Moderated estimation of fold change and dispersion for RNA-seq data with DESeq2. Genome Biology, 15, 550.

- [36] Lynch, G., Guo, W., Sarkar, S., and Finner, H. (2017). The control of the false discovery rate in fixed sequence multiple testing. Electronic Journal of Statistics, 11, 4649–4673.

- [37] Robertson, T., and Waltman, P. (1968). On estimating monotone parameters. Annals of Mathematical Statistics, 39, 1030–1039.

- [38] Robertson, T., Wright, F. T., and Dykstra, R. (1988). Order restricted statistical inference, Wiley.

- [39] Schunkert, H., Konig, IR., Kathiresan, S., Reilly, MP., Assimes, TL., Holm, H., et al. (2011). Large-scale association analysis identifies 13 new susceptibility loci for coronary artery disease. Nature Genetics, 43, 333–338.

- [40] Scott, J. G., Kelly, R. C., Smith, M. A., Zhou, P., and Kass, R. E. (2015). False discovery rate regression: an application to neural synchrony detection in primary visual cortex. Journal of the American Statistical Association, 110, 459–471.

- [41] Storey, J. D. (2002). A direct approach to false discovery rates. Journal of the Royal Statistical Society, Series B, 64, 479-498.

- [42] Storey, J. D., Taylor, J. E., and Siegmund, D. (2004). Strong control, conservative point estimation and simultaneous conservative consistency of false discovery rates: a unified approach. Journal of the Royal Statistical Society, Series B, 66, 187–205.

- [43] Storey, J. D., and Tibshirani, R. (2003). Statistical significance for genome-wide studies. Proceedings of the National Academy of Sciences, 100, 9440–9445.

- [44] Sun, W., Reich, B. J., Cai, T. T., Guindani, M., and Schwartzman, A. (2015). False discovery control in large-scale multiple testing. Journal of the Royal Statistical Society, Series B, 77, 59–83.

- [45] Sun, W., and Cai, T. T. (2007). Oracle and adaptive compound decision rules for false discovery rate control. Journal of the American Statistical Association, 102, 901-912.

- [46] Tang, W., and Zhang, C. (2005). Bayes and empirical bayes approaches to controlling the false discovery rate. Technical report, Dept. Statistics and Biostatistics, Rutgers Univ.

- [47] Tansey, W., Koyejo, O., Poldrack, R. A., and Scott, J. G. (2018). False discovery rate smoothing. Journal of the American Statistical Association, 13, 1156–1171.

- [48] van de geer, S. (2000). Empirical Processes in M-Estimation. Cambridge University Press.

- [49] van der vaart, A., and Wellner, J. (2000). Weak convergence and empirical processes: with applications to statistics. Springer Series in Statistics, New York.

- [50] Xiao, J., Cao, H., and Chen, J. (2017). False discovery rate control incorporating phylogenetic tree increases detection power in microbiome wide multiple testing. Bioinformatics, 33, 2873-2881