Hidden Geometry of Bi-Directional Grid Constrained Stochastic Processes

Abstract.

Bi-Directional Grid Constrained (BGC) stochastic processes (BGCSP) are constrained Itô diffusions with the property that the further they drift away from the origin, the more resistance to movement in that direction they undergo. We investigate the underlying characteristics of the BGC parameter by examining its geometric properties. The most appropriate convex form for , i.e. the parabolic cylinder is identified after extensive simulation of various possible forms. The formula for the resulting hidden reflective barrier(s) is determined by comparing it with the simpler Ornstein-Uhlenbeck process (OUP). Applications of BGCSP arise when a series of semipermeable barriers are present, such as regulating interest rates and chemical reactions under concentration gradients, which gives rise to two hidden reflective barriers.

Key words and phrases:

Bi-Directional grid constrained (BGC) stochastic processes (BGCSP), Wiener processes, hidden barriers, stochastic differential equation (SDE), surfaces, contour plots, Itô diffusions, convex functions, Ornstein-Uhlenbeck process (OUP), vector fields.1. Introduction

In Taranto et al., [26], the concept of Bi-Directional Grid Constrained (BGC) stochastic processes (BGCSP) was described as a general Itô diffusion in which the further it drifts away from the origin, the more constrained the Itô diffusion(s) becomes. We note that for an arbitrary stochastic function , that the following notations are equivalent,

and that the last of these is adopted here. We will also interchange , and depending on the specific context. The stochastic differential equation (SDE) of BGC stochastic processes was defined as follows.

Definition 1.1.

(Definition I of BGC Stochastic Processes). For a complete filtered probability space and a BGC function , , then the corresponding BGC Itô diffusion is expressed as,

| (1.1) |

where is the sign function defined in the usual sense, is the drift term, is the constraining term, is the diffusion term and , , are convex functions.

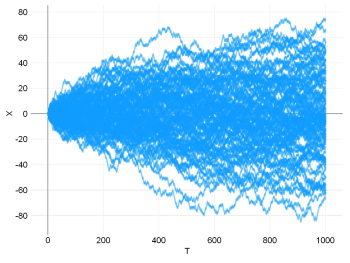

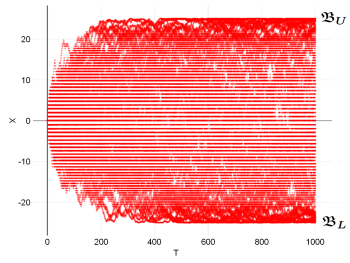

To visualize the impact of BGC stochastic processes, 1000 Itô diffusions were simulated both with and without BGC, with unit diffusion coefficient for negative, zero and positive drift coefficients. Figure 1 shows this when and , so that one can see the hidden upper barrier and hidden lower barrier emerge more clearly than is the case when using other coefficients.

(a). , , without BGC (b). , , with BGC

Remark 1.2.

The drift and diffusion (or volatility) terms reflect the instantaneous mean and standard deviation respectively. It must also be noted from Figure 1 that even when a generalized Itô diffusion is reduced to a single Wiener process by setting and , then BGC still impacts the the stochastic process.

It is from these observations that an alternative definition to (1.1) can be stated as follows.

Definition 1.3.

(Definition II of BGC Stochastic Processes). For a complete filtered probability space and a BGC function , , then the corresponding BGC Itô diffusion can be expressed as,

| (1.2) |

where is defined in the usual sense, is the drift term, is the diffusion term, is the constraining term and , , are convex functions.

Remark 1.4.

In Taranto et al., [26], only 2 decimal places were used and some readers may argue that this is a low level of precision for simulation results to be robust. To show that the discretization effect present in BGC stochastic processes is not due to such rounding errors, all our simulations were rerun to ten times more precision (i.e. to 20 decimal places) and it was found that the discretization or banding effect of BGC was still present, so it is a real phenomenon. More shall be discussed about this in the Results and Discussion section.

This paper will answer two main objectives;

-

(1).

What are the key properties of that are relevant in BGC stochastic processes?

-

(2).

What is the formula for the hidden reflective lower barrier and the hidden reflective upper barrier in relation to ?

Before these objectives are addressed in the Methodology section, the relevant research is examined in the Literature Review section.

2. Literature Review

Constraining Discrete Random Walks. Constrained stochastic processes have been applied to game theory (Feller, [9]) and conditional Markov chains of this type have also been applied to biology, branching processes (Ferrari et al., [10]), molecular physics (Novikov et al., [18]), medicine (Bell, [2]) and queuing theory (Böhm and Gopal, [3]) to name a few. Weesakul, [27] discussed the classical problem of random walks restricted between a reflecting and an absorbing barrier. Lehner, [15] studied 1-Dimensional random walks with a partially reflecting barrier using combinatorial methods. Gupta, [12] introduced the concept of a multiple function barrier (MFB) where a state can either absorb, reflect, let through (transmit) or hold for a moment along with their corresponding probabilities. Dua et al., [7] found the bivariate generating functions of the probabilities of a random variable reaching a certain state under different conditions. Percus, [20] considered asymmetric random walks, with one or two boundaries, on a 1-Dimensional lattice. El-Shehawey, [8] obtained absorption probabilities at the boundaries for random walks between one or two partially absorbing boundaries, using conditional probabilities.

Constraining Continuous Wiener Processes. Dirichlet studied the first boundary value problem, for the Laplace equation, proving the uniqueness of the solution and this type of problem in the theory of partial differential equations (PDEs). This was later named the Dirichlet problem after him (Gowers et al., [11]). Problems expressed within this framework were studied as early as 1840 by C.F. Gauss, and then by Dirichlet, [6]. Kurtz, [14] formulated a means for constraining Markov processes. L’epingle, [16] expanded upon previous research on barriers, which included boundary behavior of constrained Wiener processes between reflecting and repellent barriers. Majumdar et al., [17] derived the time taken to reach the maximum for a variety of constrained Wiener processes. Ormeci et al., [19] examined the constraining of Wiener processes via impulse control. Budhiraja and Dupuis, [4] added necessary and sufficient conditions for the stability of such constrained processes. The same authors studied large deviations for various metrics of reflecting Wiener processes under constraining (Budhiraja and Dupuis, [5]). Kharroubi et al., [13] constrained the jumps of Backward SDEs.

Whilst BGC stochastic processes are relatively new, they do have applications in many areas, most prominent being in mathematical finance, investment algorithms and quantitative trading (Taranto and Khan, [24], [22], [23], [25]).

We are now in a position to examine the geometry of the random variable as constrained by and its ramifications for BGCSP.

3. Methodology

3.1. Convexity of BGC

From (1.2), we know that needs to be a convex function and specifically, centered about the origin. This is to ensure that the constraining applies increasing monotonic resistance to the Itô diffusion in both directions (i.e. bi-directionally). For example, would not be sufficient because whilst is convex (as shown by having a line bisect any two points on its curve) does not increase as as it does when . This gives rise to the need for the following classification of convexity.

Definition 3.1.

(Types of Convexity). If and , then we can characterize (Zalinescu, [28], Bauschke and Combettes, [1]) its convexity as follows,

-

(1)

is convex if and only if , .

-

(2)

is strictly convex if and only if , .

-

(3)

is strongly convex if and only if , .

We will require a new type of (subset) convexity for BGCSP.

Definition 3.2.

(Bi-Directional Convexity). If and , then we can characterize its convexity as follows,

is bi-directionally convex if and only if , , .

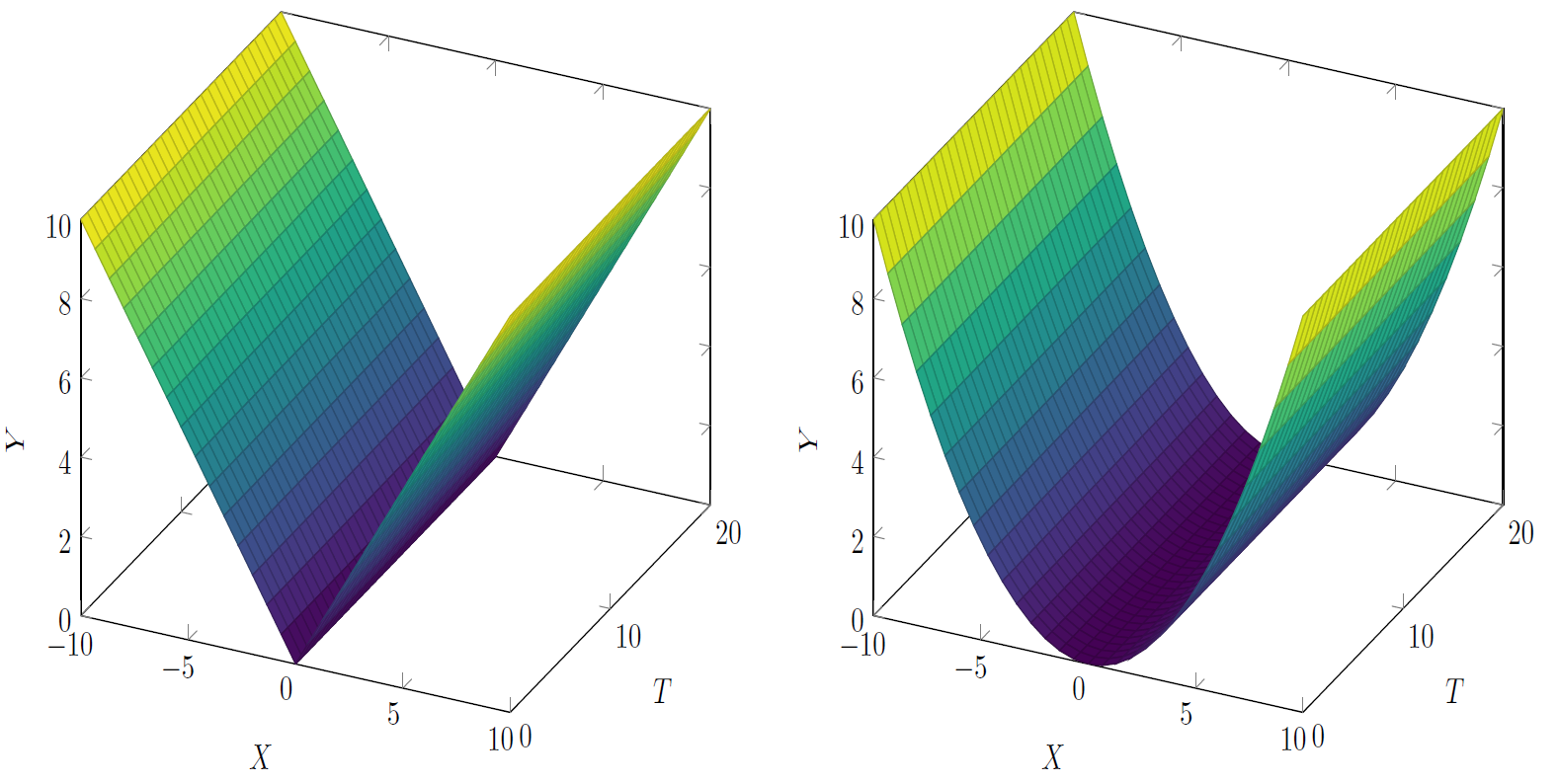

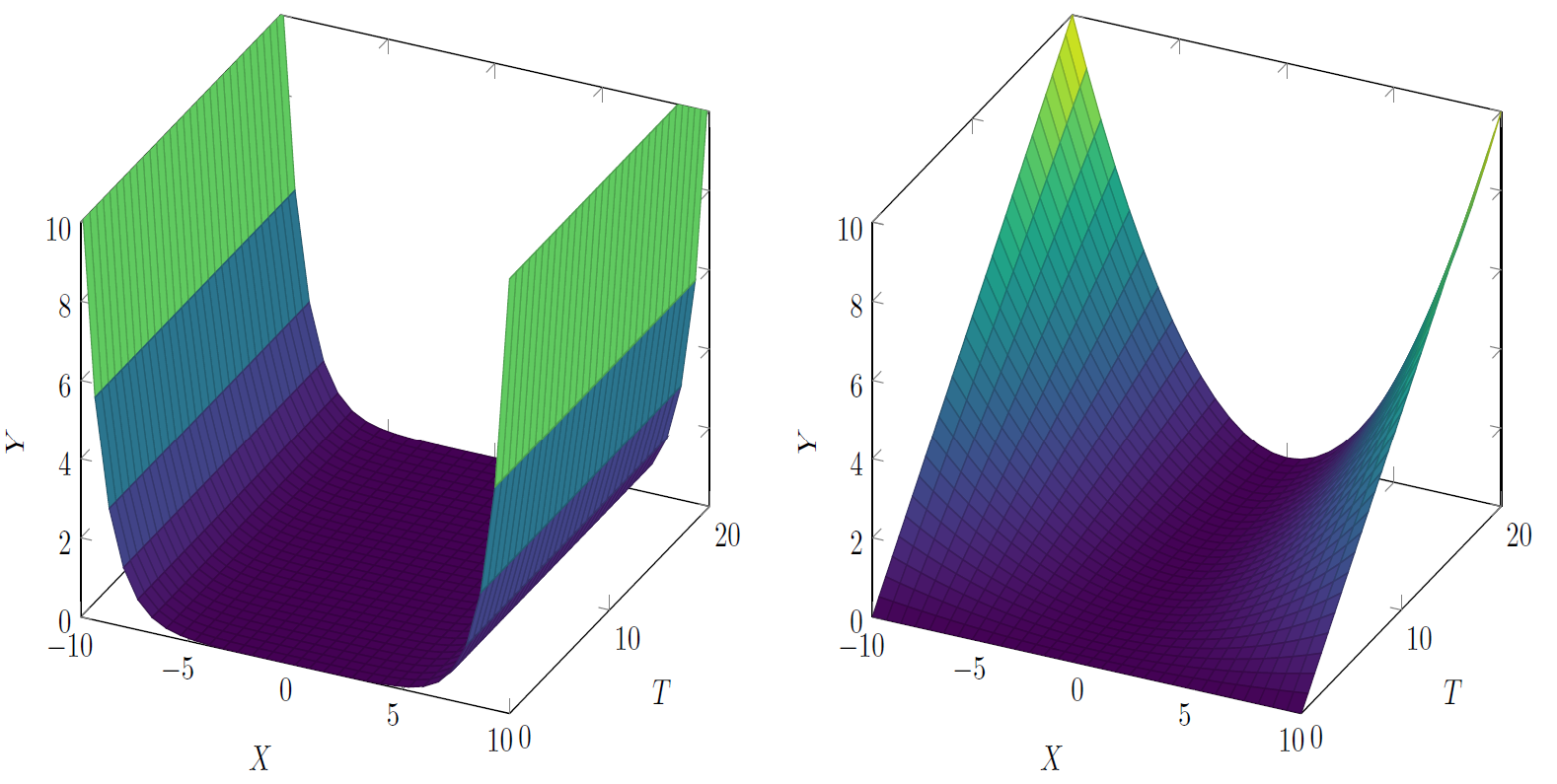

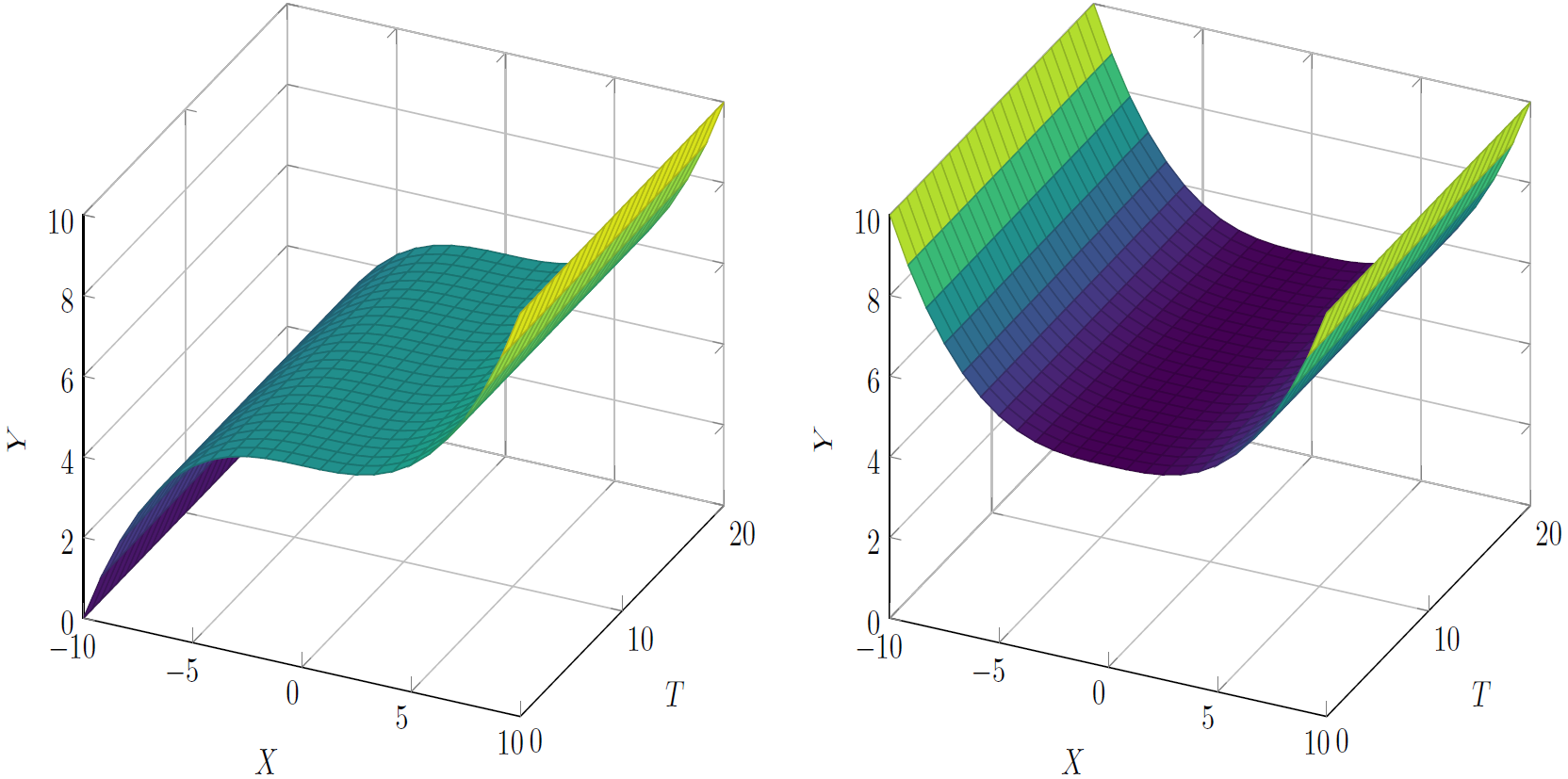

To establish some use cases to explore the convex geometry of potential BGC functions for , we plot their surfaces in Figures 2 and 3, and deduce which specific type of convexity definition is required for BGCSP.

-

(1)

Use Case I was not adopted because it constrains the Itô diffusion evenly and uniformly but not rapidly enough with the unconstrained Itô diffusions’ iterated logarithm bounds growth rate. This is to the point that the before and after BGC plots (see Figure 9(a)) look very similar and do not constitute a practical and worthwhile BGC process.

-

(2)

Use Case II is definitely the ideal function for BGC and so we will dedicate much of the Methodology, Results and Discussion sections to the parabolic cylinder.

-

(3)

Use Case III examines how the standard convex will not suffice because needs to be ‘Bi-Directional’, that is, it must be a mirror reflection about the origin over all time. Hence, was used, yet due to the fast growing nature of the exponential function, it constrains the Itô process too much for it to be a useful function for BGC (even when it is scaled down by a constant or many other possible variations of ), as will be elaborated further in the Results and Discussion section Figure 9(b).

-

(4)

Case IV was also presented here because it is a transition from no constraining to a gradual parabolic cylinder. Such a surface was proposed for applications in which Itô diffusions are not constrained so much initially and which become increasingly more constrained over time are required. However, as will be detailed further in the Results and Discussion section Figure 9(c), this did not produce the hidden barriers that bound an Itô diffusion from both above and below.

-

(5)

Use Case V is the final example that is worthwhile discussing, as shown in Figure 3.

From Figure 3, we note that , , will always result in a polynomial cylinder as will always be an even exponent. For odd exponents , , one can simply replace this with . In general, will be a polynomial cylinder that will always be convex and ‘Bi-Directional’, . As will be elaborated in the Results and Discussion section in Figure 9(d), the polynomial cylinder was not suitable as a BGC function for general unconstrained Itô diffusions, but can be scaled to suit one’s specific unconstrained Itô diffusion.

(a). (b). ,

(c). , (d). ,

(c). , (d). ,

(a). , , (b). , ,

(a). Cubic cylinder, (b). USE CASE V - Spliced polynomial cylinder(s).

(a). The cubic is concave for negative values and convex for positive values.

Remark 3.3.

It is clear by now that not any convex function can be appropriate for BGC. An example of this would be , where it is clearly and bi-directionally convex but not constant or ‘cylindrical’ over time and does not resemble any natural regime to constrain the stochastic processes uniformly over time. It is thus clear now that BGC requires the bi-directionally convex definition and in particular, bi-directionally convex cylinders.

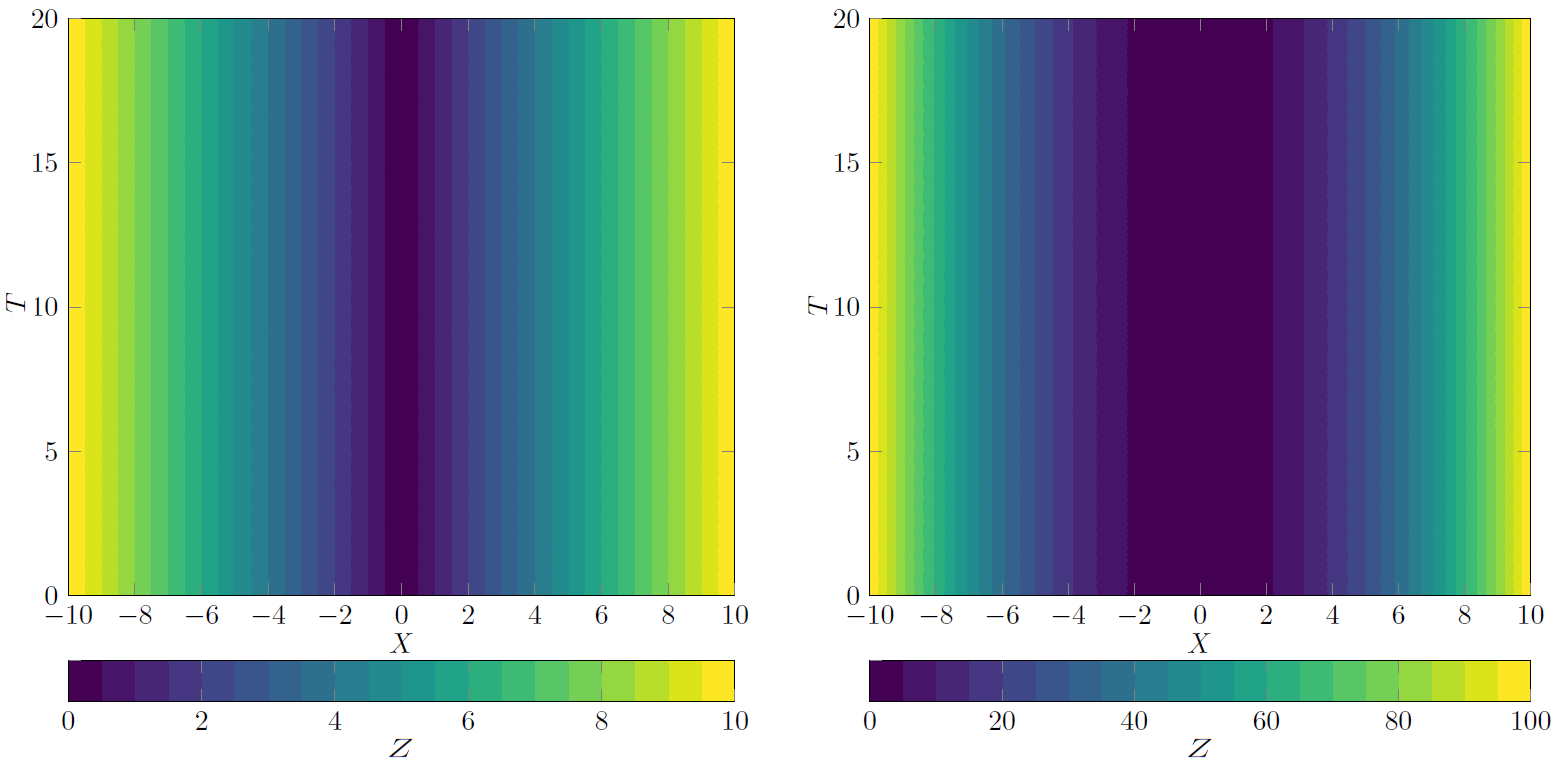

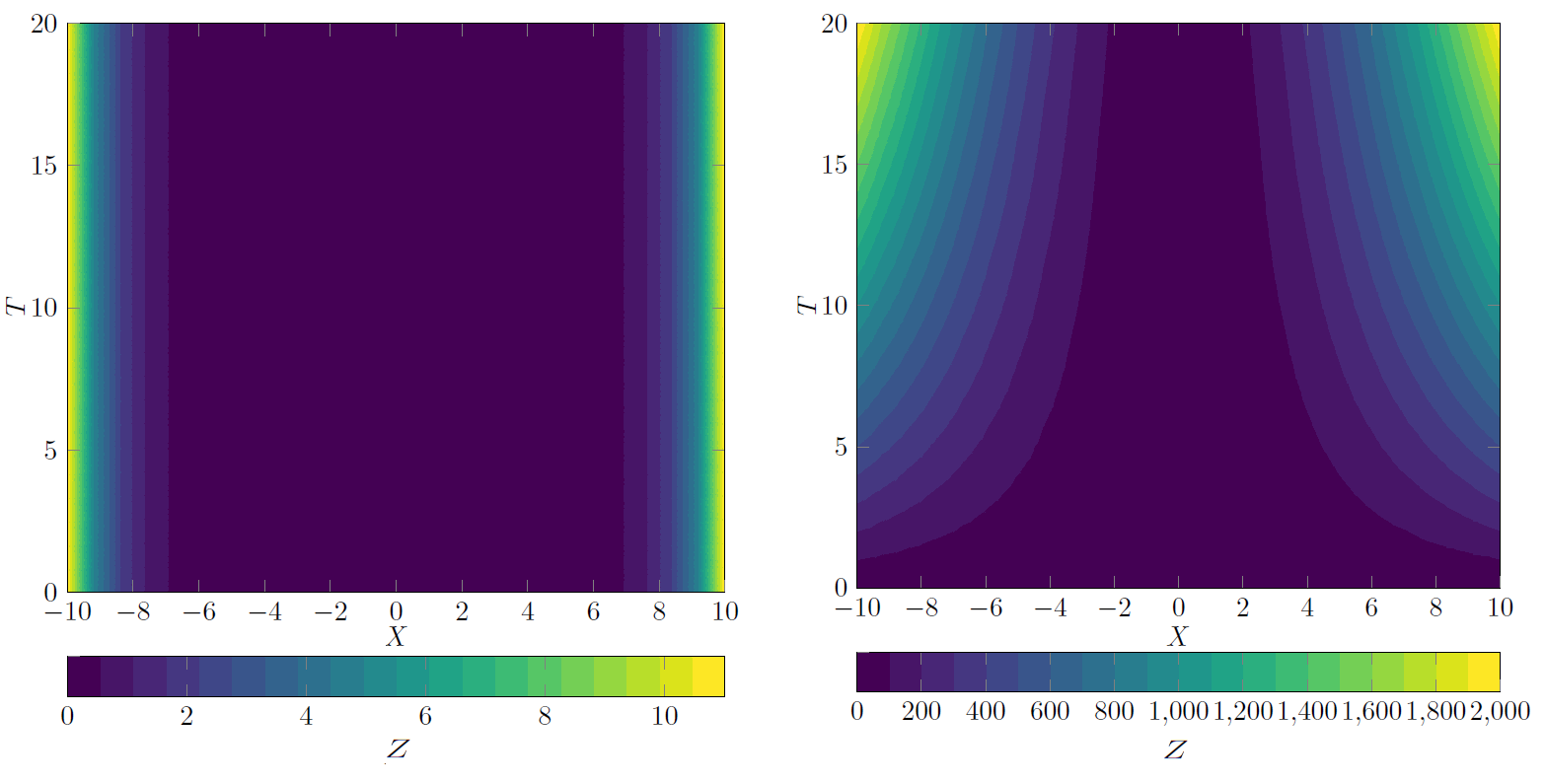

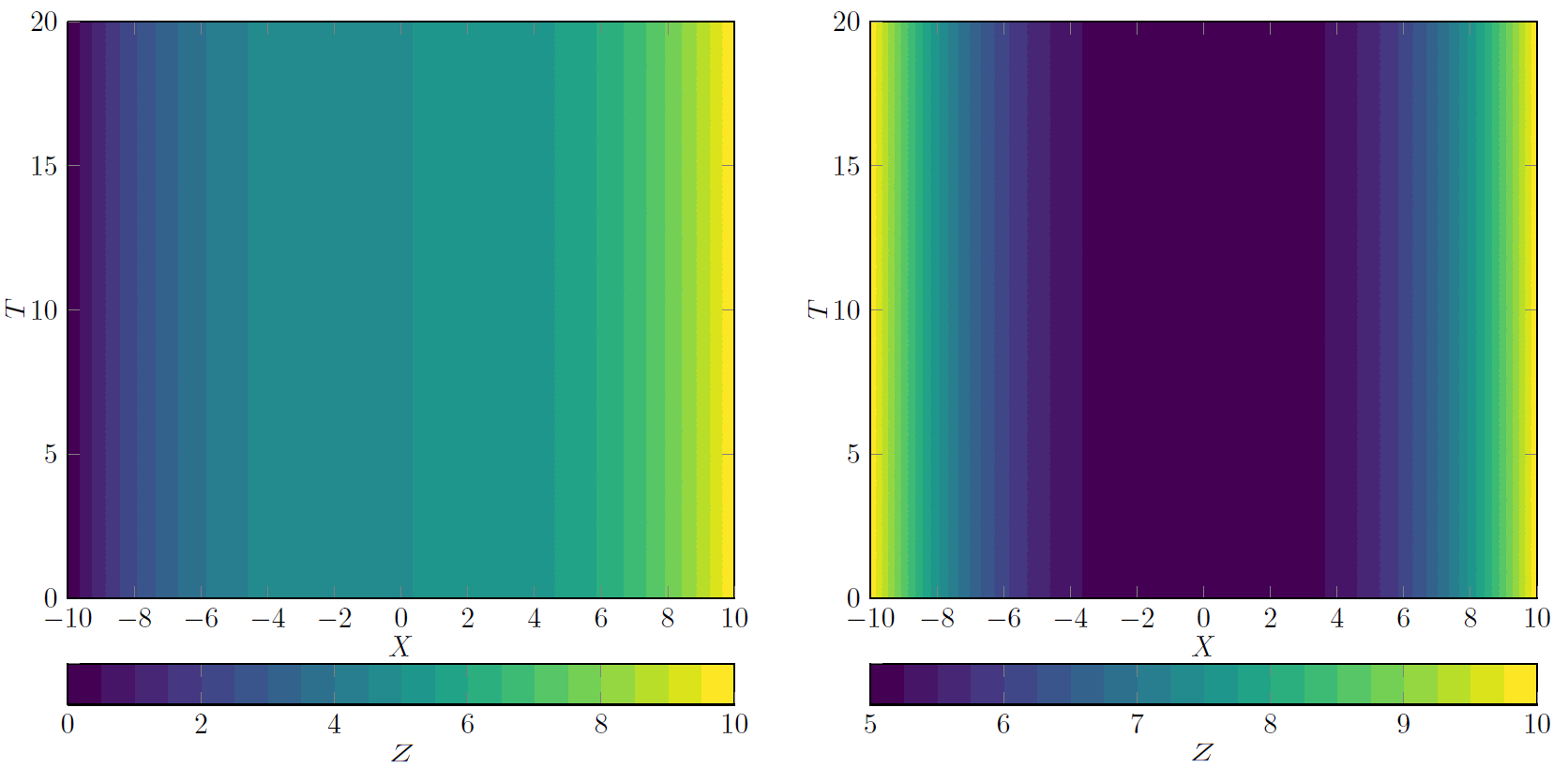

Having explored the nature of as determined by which lies in , we notice that our Itô process in is a 1-Dimensional stochastic process in , which when it propagates over time, it does so in . The way we can see how the 3-D constrains the 1-D Itô process in 2-D is via the projection of onto the plane is via contour plots, as shown in Figures 4 and 5.

(a). (b).

(c). (d).

(c). (d).

From Figure 4, it is much clearer to see how constrains the Itô process as propagates over time, where the lighter the colour, then the greater the resistance and hence the greater the constraining impact due to BGC. This is also shown in the contour plots of Figure 5.

(a). (b).

From these contour plots, we see how the convexity forms a series of decreasing semipermeable barriers (i.e. increasing reflection) on the Itô process. We now examine the effect that this has on the actual hidden reflective barriers, and .

Remark 3.4.

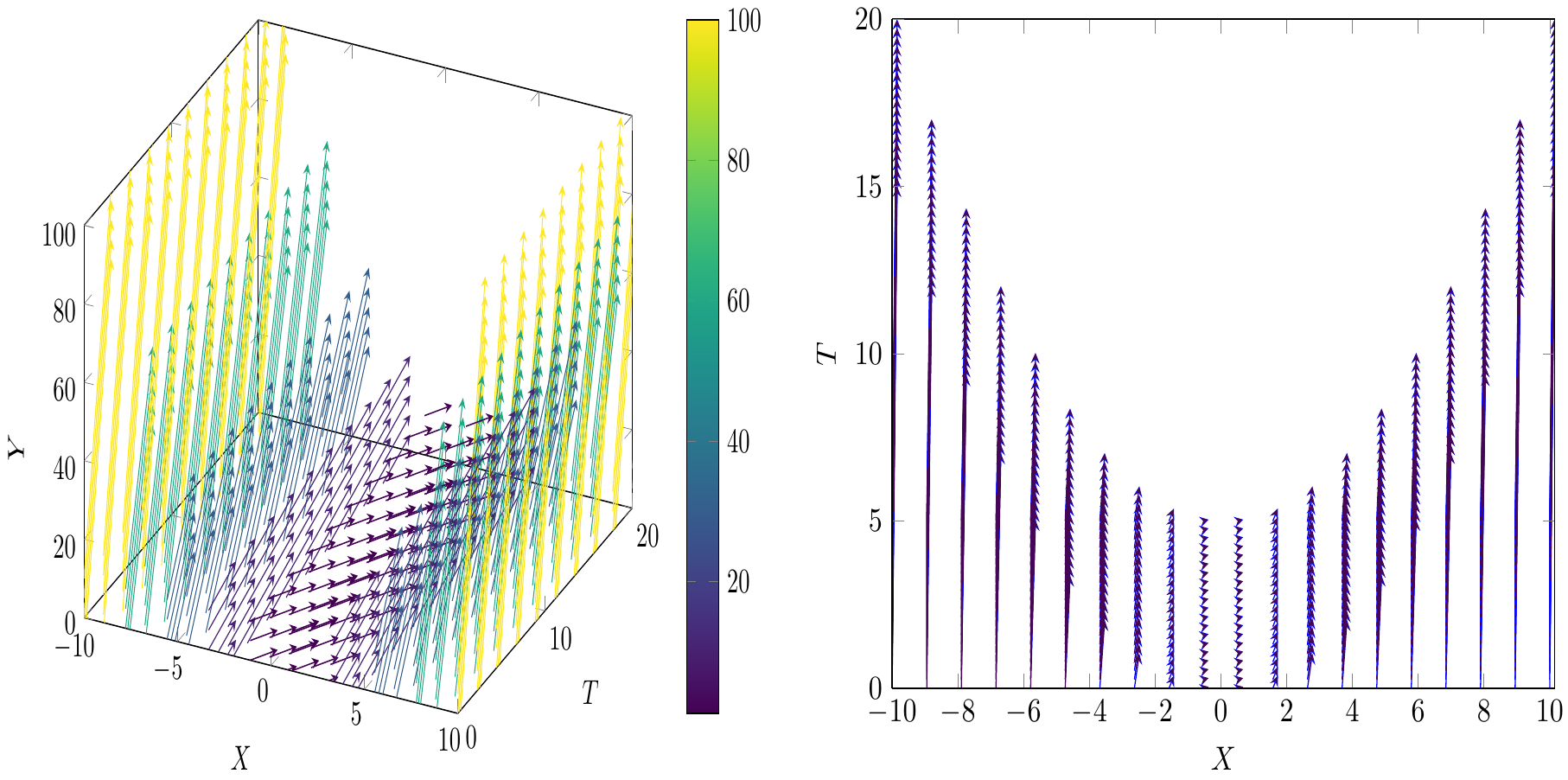

Note that an alternative to the 3-D surface inducing the 2-D contours, is the 3-D surface inducing the 3-D and 2-D vector fields, as shown in Figure 6.

(a). BGC Vector Field in , (b). BGC Vector Field in .

From Figure 6, we see that the constraining on (specifically ) can also be induced by the parabolic cylinder of and its associated vector field. As the Itô process propagates through the vector field, the greater the vector magnitudes, then the greater the resistance force of reflection back to the origin.

This novel concept has been researched recently, but in reverse by Simpson and Kuske, [21], by modelling a constant variable into a random vector field to induce a stochastic process. Specifically, they show how a Flippov system near a switching manifold (due to the meeting of vector fields) attracts orbits or constant variables in the abscence of randomness to create stochastic flow within the field.

3.2. Hidden Barriers of BGC Stochastic Processes

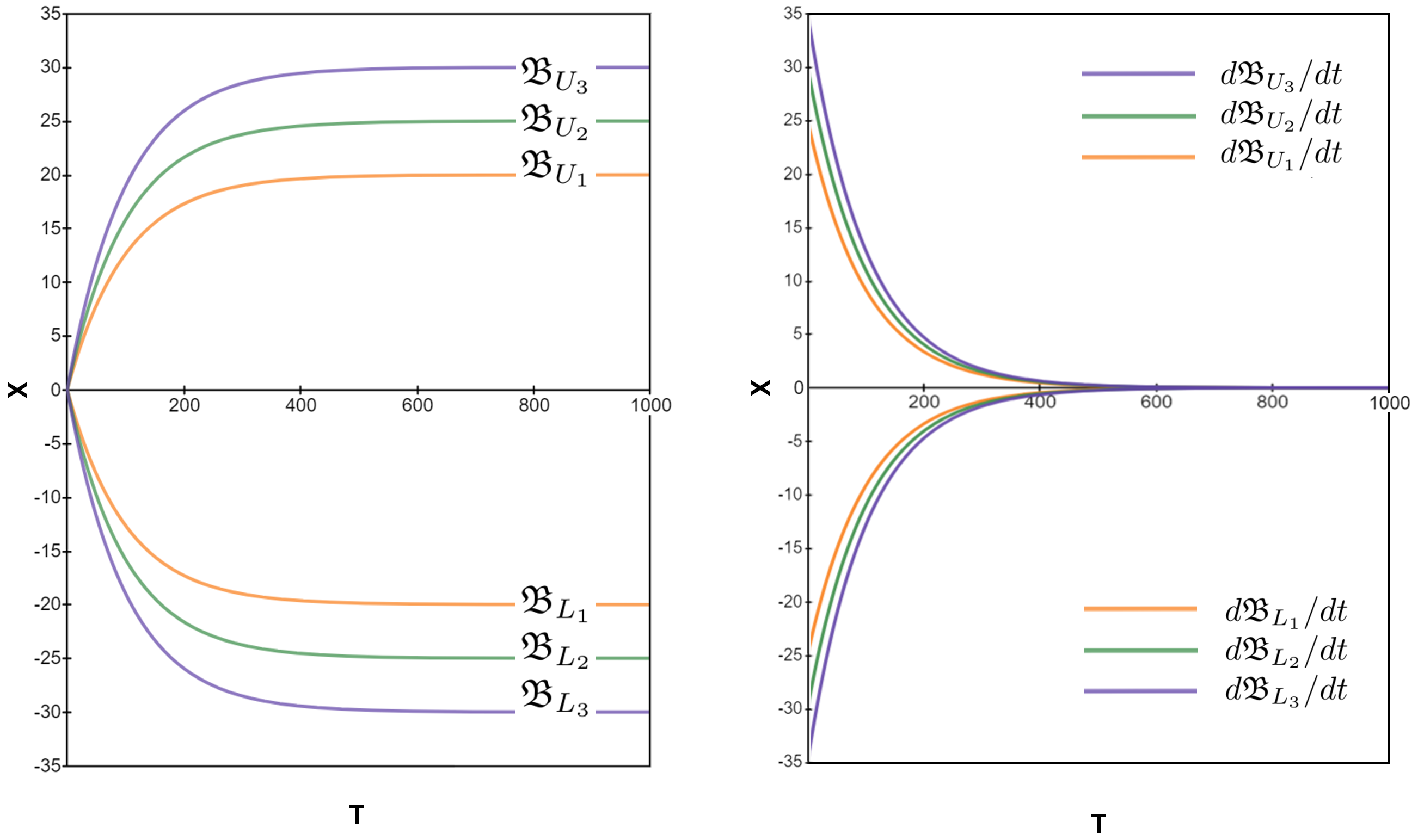

Whilst Figure 1(b) shows the detailed nature of the hidden reflective BGC varies, we only plot and to better help derive the formulation of the barriers, as shown in Figure 7.

From Figure 7, we see that the BGC hidden reflective barriers are regulated to one’s desired distance from the origin by altering the parameter and are regulated in their climb rate from the origin to the barrier by altering the parameter.

(a). (b).

Orange: , Green: , Purple: .

Remark 3.5.

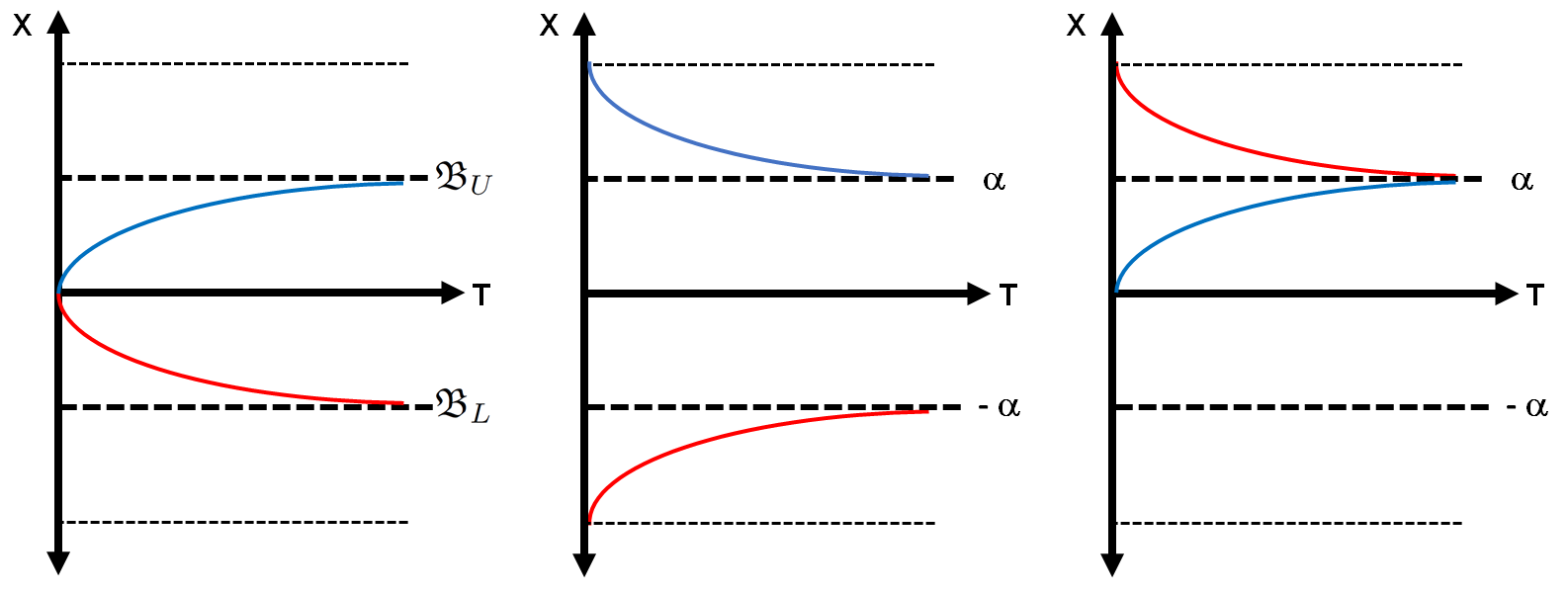

Note that these barriers are not the traditional constant reflective barriers such as or because the BGC Itô diffusions are bounded within these barriers even as they depart from the origin (i.e. the unconstrained Itô diffusions exceed these barriers, even near the origin), hence the initial curvature in the barriers. This is generalized in the following Thorem.

Theorem 3.6.

(Hidden Barriers of BGC Stochastic Processes). For a complete filtered probability space and a BGC function , and the corresponding BGC Itô diffusion expressed as,

| (3.1) |

for , where is the sign function defined in the usual sense, is a drift term, is the BGC term, is the diffusion term and , , are bi-directionally convex functions. Then the hidden lower barrier and hidden upper barrier are given by,

| (3.2) |

where , are constants, is the distance from the origin to the barrier(s) and is the rate of growth towards the barrier(s).

Proof.

To some readers, (3.2) is obvious just by looking at Figure 7(a) simply because the function must asymptote horizontally (exponentially) towards the barrier(s). However, this does not constitute a proof because we have a stochastic (and not a deterministic) process. Assume for a moment that the above BGC SDE is a simpler object in which and are constant, where the drift function and the diffusion function , , in the limit approach the typical constant expressions for the drift and diffusion coefficients, , . We now start to see the resembelence of our BGC Itô process with the simpler Ornstein–Uhlenbeck process (OUP),

| (3.3) |

where is the long-term mean, is the ‘attraction rate’ or speed of mean-reversion, both of which are constants, as depicted in Figure 8.

(a). (b). (c).

From Figure 8, we can see that the total number of paths (as shown in blue and red) is preserved in each of the three schemes. (3.1) is (1.1) repeated for convenience and (3.1) is similar to (3.2), where in OUP is replaced by in BGCSP (with and ), which caters for a much wider set of possible paths than is possible with OPU and yet BGCSP has instead of . Multiplying (3.3) by and expanding gives,

| (3.5) |

Having solved the OUP SDE, we wish to determine where is most likely to be for . Taking the expectation of both sides,

| (3.6) |

as is deterministic. Since for all BGCSPs, we will set all OUPs to start from the origin, giving,

| (3.7) |

We now have a stochastic argument that is a basis to justify (3.2). Assume that for greatest generality,

| (3.8) |

We know that since is bi-directional, it is symmetric about the origin and so . By comparing (3.8) with (3.7), we can see that,

where signifies a weak association. Since BGCSP do not ‘force’ the Itô diffusion to the long-term mean , the time taken to reach or under BGC would be greater than for OUP. Hence in terms of distance,

∎

Remark 3.7.

is intuitive because the greater the drift , then the greater , hence , ie. and . We also notice that the diffusion term doesn’t contribute as much to . We also know by some experimentation that .

To extend [26] further, the BGCSP Algorithm 1 is derived and simulated in the Results and Discussion section.

4. Results and Discussion

At this stage, we know that Use Cases I, III, IV and V -are not valid candidates for the correct type of convexity for general , but for various exotic forms of Itô diffusions, such as the Cox-Ingersoll-Ross (CIR) process, these use cases may be sufficient to BGC the Itô process within two hidden barriers. We also have a theoretical appreciation of what other forms of are valid and invalid candidates. On the other hand, we also know that Use Case II -the parabolic cylinder -is the ideal type of convexity for general Itô diffusions. To confirm this and further eliminate any remaining use cases, we simulate them in Figure 9.

From Figure 9, in (b) and (d), we see a certain amount of constraining is occuring and that the BGC never exceeds the original simulation paths. However, we also see in (d) that whilst there is some BGC initially, after some time the hidden barriers are unstable.

In (a) and (c), there is no real effective constraining since the BGCSP is now hyper-extended from the original simulation paths and so there are no hidden reflective barriers either. When (where is the unconstrained Ito diffusion and signifies domination), then there will be a point in time where will flip over the origin and the contribution from the drift will be eclipsed by the term. We thus have becoming the dominant drift term that will explode the Itô diffusion beyond where the unconstrained Itô diffusion would reach, away from the origin.

![[Uncaptioned image]](/html/2103.12859/assets/v2_2.png)

![[Uncaptioned image]](/html/2103.12859/assets/v5_2.png)

(a). (b). ,

![[Uncaptioned image]](/html/2103.12859/assets/v2_4.png)

![[Uncaptioned image]](/html/2103.12859/assets/v4_2.png)

(c). ,

(d). , ,

Blue = Without BGC, Red = With BGC

We now examine the parabolic cylinder in far greater detail, as shown in Figure 10.

From Figure 10, we see that the hidden reflective BGC barriers can constrain the Itô diffusion(s) indefinitely as it is ‘trapped’ within the barriers. This assumes that there are no sudden jumps (as is the case in jump-diffusion models) or changes in or in . To examine this in even further detail, we simulate again for different parameters, as shown in Figure 11.

From Figure 11, there is a region about the time axis where not many simulation paths visit, supporting the notion that as the paths approach the hidden barriers, they end up being ‘trapped’ near that boundary. Also notice how there is banding or discretization about various local times which get compressed the further they are from the origin. The local times seem to coincide or line up most near the time axis regardless of .

5. Conclusions

This paper has extended the available research on BGC stochastic processes by investigating the hidden geometry of BGC functions. The parabolic cylinder was found to be the ideal constraining mechanism for the parameter , for most general unconstrained Itô diffusions. Not any ordinary convex function will suffice and the novel ‘bi-directionally convex’ definition was defined and adopted. The formulas for the lower hidden reflective barrier and the upper hidden reflective barrier were derived. This helps establish a linkage between of the form and the resulting and . This research has applications in many fields, such as in finance where exchange rates can be constrained by ‘parabolic cylinder’ monetary policies, such as ‘keep the AUD/NZD exchange rate within a range by regulating the amount of Government debt, the more it approaches the range boundaries’. Future research in BGC can involve BGC of other important Itô diffusions from other research fields and finding estimates for the distribution of the first passage time (FPT) for when and are most likely to be first hit. We believe that there must be some mapping from to and to .

![[Uncaptioned image]](/html/2103.12859/assets/v1_10.png)

Blue = Unconstrained Itô process, Red = BGC Itô process.

![[Uncaptioned image]](/html/2103.12859/assets/v1_18.png)

Orange = Inner-most barriers, Green = Middle barriers, Purple = Outer-most barriers.

References

- Bauschke and Combettes, [2011] Bauschke, H. and Combettes, P. (2011). Convex Analysis and Monotone Operator Theory in Hilbert Spaces. Springer International Publishing, second edition edition.

- Bell, [1976] Bell, G. (1976). Models of carcinogenesis as an escape from mitotic inhibitors. Science, 192:569–572.

- Böhm and Gopal, [1991] Böhm, W. and Gopal, M. (1991). On random walks with barriers and their application to queues. Forschungsberichte / Institut für Statistik, 21.

- Budhiraja and Dupuis, [1999] Budhiraja, A. and Dupuis, P. (1999). Simple necessary and sufficient conditions for the stability of constrained processes. SIAM Journal on Applied Mathematics, 59(5):1686–1700.

- Budhiraja and Dupuis, [2003] Budhiraja, A. and Dupuis, P. (2003). Large deviations for the emprirical measures of reflecting brownian motion and related constrained processes in r+. Electronic Journal of Prob., 8.

- Dirichlet, [1850] Dirichlet, P. (1850). Abhandlungen der königlich preussischen akademie der wissenschaften. pages 99–116.

- Dua et al., [1976] Dua, S., Khadilkar, S., and Sen, K. (1976). A modified random walk in the presence of partially reflecting barriers. J. Appl. Prob., 13:169–175.

- El-Shehawey, [2000] El-Shehawey, M. (2000). Absorption probabilities for a random walk between two partially absorbing boundaries. I. J. Phys. A: Math. Gen., pages 9005–9013.

- Feller, [1968] Feller, W. (1968). An Introduction to Probability Theory and Its Applications, volume 1 of A Wiley publication in mathematical statistics. Wiley International Publishing, third edition edition.

- Ferrari et al., [1992] Ferrari, P., Martinez, S., and Picco, P. (1992). Existence of non-trivial quasi-stationary distributions in the birth-death chain. Advances in Applied Probability, 24(4):795–813.

- Gowers et al., [2008] Gowers, T., Barrow-Green, J., and Leader, I. (2008). The Princeton Companion to Mathematics. Princeton University Press.

- Gupta, [1966] Gupta, H. (1966). Random walk in the presence of a multiple function barrier. Journ. Math. Sci., 1:18–29.

- Kharroubi et al., [2010] Kharroubi, I., Ma, J., Pham, H., and Zhang, J. (2010). Backward sdes with constrained jumps and quasi-variational inequalities. The Annals of Probability, 38(2):794–840.

- Kurtz, [1991] Kurtz, T. (1991). A control formulation for constrained markov processes. Mathematics of Random Media, 27:139–150.

- Lehner, [1963] Lehner, G. (1963). One-dimensional random walk with a partially reflecting barrier. Ann. Math. Stat., 34:405–412.

- L’epingle, [2009] L’epingle, D. (2009). Boundary behavior of a constrained brownian motion between reflecting-repellent walls.

- Majumdar et al., [2008] Majumdar, S., Randon-Furling, J., Kearney, M., and Yor, M. (2008). On the time to reach maximum for a variety of constrained brownian motions. Journal of Physics A: Mathematical and Theoretical, 41(36):365005.

- Novikov et al., [2011] Novikov, D., Fieremans, E., Jensen, J., and Helpern, J. (2011). Random walks with barriers. Nature Physics, 7:508–514.

- Ormeci et al., [2008] Ormeci, M., Dai, J., and Vate, J. (2008). Impulse control of brownian motion: The constrained average cost case. Operations Research, 56(3):618–629.

- Percus, [1985] Percus, O. (1985). Phase transition in one-dimensional random walk with partially reflecting boundaries. Adv. Appl. Prob., 17:594–606.

- Simpson and Kuske, [2018] Simpson, D. and Kuske, R. (2018). Stochastically perturbed sliding motion in piecewise-smooth systems. arXiv preprint.

- [22] Taranto, A. and Khan, S. (2020a). Bi-directional grid absorption barrier constrained stochastic processes with applications in finance and investment. Risk Governance & Control: Financial Markets & Institutions, 10(3):20–33.

- [23] Taranto, A. and Khan, S. (2020b). Drawdown and drawup of bi-directional grid constrained stochastic processes. Journal of Mathematics and Statistics, 16(1):182–197.

- [24] Taranto, A. and Khan, S. (2020c). Gambler’s ruin problem and bi-directional grid constrained trading and investment strategies. Investment Management and Financial Innovations, 17(3):54–66.

- Taranto and Khan, [2021] Taranto, A. and Khan, S. (2021). Application of bi-directional grid constrained stochastic processes to algorithmic trading. Journal of Mathematics and Statistics, 17(1):22–29.

- Taranto et al., [2020] Taranto, A., Khan, S., and Addie, R. (2020). Iterated logarithm bounds of bi-diretional grid constrained stochastic processes. arXiv Preprint: Modern StochAstic Models & ProbleMs Of Actuarial MaTHematics (MAMMOTH) Conference, pages 1–21.

- Weesakul, [1961] Weesakul, B. (1961). The random walk between a reflecting and an absorbing barrier. Ann. Math. Statist., 32:765–769.

- Zalinescu, [2002] Zalinescu, C. (2002). Convex Analysis in General Vector Spaces.