Piecewise linear processes with

Poisson-modulated exponential switching times111This is the peer reviewed version of the paper, which has been published

in final form at https://doi.org/10.1002/mma.5683. This article can be used for non-commercial purposes in accordance with Wiley Terms and

Conditions for use of Self-Archived versions.

Antonio Di Crescenzo

Dipartimento di Matematica,

Università degli Studi di Salerno, 84084 Fisciano (SA), Italy. e-mail: adicrescenzo@unisa.itBarbara Martinucci

Dipartimento di Matematica,

Università degli Studi di Salerno, 84084 Fisciano, SA, Italy. e-mail:

bmartinucci@unisa.itNikita

Ratanov

Facultad de Economía,

Universidad del Rosario, Bogotá, Colombia. e-mail:

nikita.ratanov@urosario.edu.co (corresponding author)

Abstract

We consider the jump telegraph process when

switching intensities depend on external shocks also accompanying

with jumps. The incomplete financial market model based on this process is studied.

The Esscher transform, which changes only unobservable parameters, is considered in detail.

The financial market model based on this transform

can price switching risks as well as jump risks of the model.

The piecewise linear processes have a long history and still receiving

attention in various aspects. This family of processes includes so-called

telegraph process which presumes alternating velocities with exponentially

distributed time intervals between switchings. The number of switchings

in this model is counted by homogeneous Poisson process.

This theory has been developing

since the seminal paper by Taylor [1] for almost a century.

In the 50s, this model has been studied by Goldstein [2]

and Kac [3].

See the history and the detailed description

in the monograph by Kolesnik and Ratanov [4].

The model which is based on the distribution of the inter-switching times

different from exponential is much less studied. Some examples could be found

in [5, 6, 7, 8, 9].

Another generalisation can be constructed as a piecewise linear process

with arbitrary consecutive

trends and switching intensities

see [10] and [11].

In this paper we study the piecewise linear processes

with exponentially distributed time intervals between successive tendency switchings, but here we assume

that the parameter of this distribution depends on

exogenous shocks (exogenous impacts, external interventions), arriving at a constant rate.

This approach reflects the well posed problem of financial market modelling,

when multiple agents are trying to break the trend by interventions,

but could affect only the switching rate.

Let be successive intensities of shocks.

That is, on a complete probability space

we consider the sequence of time intervals between the consecutive

shocks, which are independent and exponentially distributed,

We assume shocks do not come explosively, i. e. the

process is a simple point process,

which is equivalent to

(1.1)

see e. g.

[12]. This means that there is a finite accumulation of shocks at any finite time interval:

where is the corresponding counting process,

and is the indicator.

If (1.1) fails, then this process exibits explosive behaviour,

For example, if then

see [13, Example 6.3.1].

If all s are equal, then

is the homogeneous Poisson process.

Let

Consider the random variable which has the exponential distribution

with -modulated parameter,

the survivor function of is given by

(1.2)

where

(1.3)

is the accumulated intensity.

We call such a distribution a Poisson-modulated exponential distribution,

Here is the sequence

of parameters of the underlying process counting arrivals of shocks and

are the sequential parameters

of the main exponential distribution.

In this paper we study the piecewise linear process which follows two patterns

alternating at random instants

with Poisson-modulated exponential distribution of

inter-switching times.

To begin with, consider the sequence

of independent Poisson processes

based on the two alternating sets of parameters

and

(1.4)

Here

is a the sequence of alternating and which

indicates the current pattern.

Let these processes be non-explosive,

satisfying (1.1),

Let and

be two sequences of positive numbers.

Consider the sequence

of independent random variables ,

with alternating Poisson-modulated exponential distributions,

Consider the

point process formed by the times,

when the patterns are switched,

Since are non-explosive,

the process is non-explosive too, if

Let be

the counting process

(1.5)

The marginal distributions of the process

indicating the current pattern, are defined by

if

By we denote the corresponding filtration.

Process can be treated as a doubly stochastic Poisson process,

see [14, 15].

A similar approach is exploited in

[16], see there Example 6.3(e), Example 7.3(a) and Example 7.4(e)

(bivariate Poisson process).

Meanwhile this model differs from the model of mixed Poisson process

(when the parameter of Poisson process

is considered as the outcome of a positive -measurable

random variable)

widely exploited in actuarial applications, see e.g. [17, 18].

The problem of infinite accumulation of arrivals for doubly stochastic Poisson process

(when the interarrival times are Poisson-modulated) is more complicated than for a simple point process,

see Section 2 for the analysis of this problem.

The transport piecewise linear processes based on a mixed Poisson process

have been recently presented in

[19, 20].

For the D-case of such random motions

with jumps (and with constant intensity of switchings)

see [21].

The similar piecewise linear process with

the deterministically growing intensities

has been studied in [5].

In this paper we study

the piecewise linear renewal process based on the two alternating

sets of tendencies, and

with Poisson-modulated exponential distributions of patterns’ holding times.

First, consider the sequence of independent piecewise linear processes

which follows the sequence of tendencies

( or )

with switchings at Poisson random times.

Process successively follows the

two patterns alternating after holding times

(1.6)

Bearing in mind applications, we supply

with jumps. Properties of process with jumps and

with exponentially distributed time intervals

under the arbitrary set of tendencies

is recently studied by [10]. The processes with

renewal restarting points (instead of jumps) is studied by [22].

Here we analyse

properties of such processes

which follow the alternating patterns

with Poisson-modulated exponential distributions of switching times

and with jumps

and

accompanying the tendency switchings and the changes of patterns, respectively.

This approach could be used for financial market modelling

when log-returns are

determined by the inherent market forces, that is by and

by efforts of “small speculators” which create the tendency and volatility modulations.

Let jumps accompanying the patterns’ switchings occur

as “corrections” of the current trend :

In this case small players trying to change the trend affect only the volatility

and the probability of the next switching of the trend.

We derive coupled integral equations

for mean values of the process accompanied with jumps

(see Section 4). Further, the martingale condition is presented:

this process is a martingale if and only if

(1.7)

Here and are the expectations of the random jump values.

The same condition characterises martingales in a rather different model,

when holding times

are independent of the underlying Poisson processes

see [11, Corollary 3.1].

Condition (1.7) looks similar to the martingale condition for a simple jump-telegraph process, see [23]:

(1.8)

The text is organised as follows.

The detailed analysis of Poisson-modulated exponential distributions

is presented in Sections 2 and 3.

In Section 4 we study the

piecewise linear process with jumps.

In Section 5 we propose a financial market model based on these processes.

This model generalises the simple jump-telegraph market model, [23].

2 Poisson-modulated exponential distribution

In this section we present some properties of the Poisson modulated exponential distributions

which we will use later.

Let be the sequence

of independent and

exponentially distributed

random variables,

and be

the non-explosive, (1.1), renewal counting process.

Denote the probability mass function of

at by . If all are equal, then

in the case of distinct

by [10, formula (2.4), Proposition 2.1], we have

Due to identities (2.4), functions

satisfy the following conditions:

for

(2.5)

Consider the random variable

with Poisson-modulated exponential distribution,

See (1.2)-(1.3).

Let us begin by studying the properties of the accumulated intensity

based on the non-explosive counting process ,

(1.3).

Consider the moment generating function of

(2.6)

where

(2.7)

By definition we have

(2.8)

Assume that all linear -functions

(2.9)

are distinct,

(if )

one can easily obtain the explicit expression for

by means of Applying [10, Theorem 3.1],

we have

(2.10)

where and

are defined by (2.3) and (2.2)

with instead of .

We introduce the notation

(2.11)

assuming convergence of the series.

From (2.10)

one can obtain the representation of which is equivalent to (2.6):

if the series in (2.11) converge.

This representation is consistent with the identities

and :

Formula (3.8) can be simplified: by

[25, (9.14)]

using a

generalised hypergeometric function

where .

In particular, the mean of is given by

where is a confluent hypergeometric function,

see [25], formula (9.210).

By [25], formula (8.354.1),

could be written in the equivalent form:

where is the incomplete gamma-function.

4 Piecewise linear process with two alternating patterns and a double jump component

Let

be the sequence of independent Poisson processes

which are driven by two alternating sequences of parameters:

and

That is, see the definition in (1.4).

Here is a sequence of alternating and or

Let

be the sequence of independent

positive random variables,

and

be the associated process (1.5), that counts arrivals of

till time

Let be

the process, which indicates the current state as follows:

for .

We assume that random variable has

Poisson-modulated exponential distribution,

based on the Poisson process

Here

and

are the two sequences of switching intensities (see (1.2)-(1.3)).

The alternating survivor functions of due to (2.12)

are given by

and the corresponding densities are defined by

In this section

we study a piecewise linear process which follows

two patterns alternating after the holding times . Precisely, we define the piecewise linear process

based on the two sequences of tendencies, and ,

alternating at the time instants such that

(4.1)

where

(4.2)

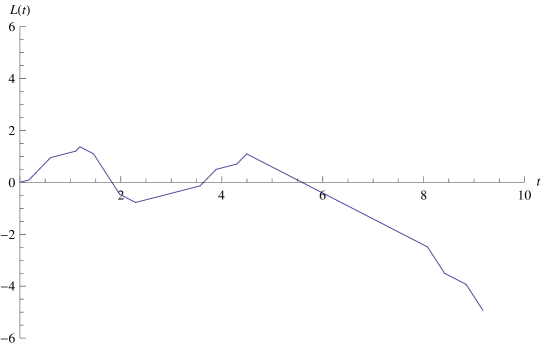

This definition coincides with (1.6). A simulated sample path is presented by

Figure 2.

Figure 2: A sample path the piecewise linear process

with two patterns of two pairs of alternating velocities.

The 0-pattern with and 2.0; the 1-pattern with

and -3.0. In both cases, the inter-switching times

are Poisson-modulated with

The jump component added to this process consists of two parts.

The first one calculates the jumps occurring at the arrival times

of the embedded Poisson processes. This corresponds to

the case that each tendency switching (inside the time interval ) is

accompanied with a jump of the magnitude .

The

compound Poisson processes

presents the summed jump component.

Here

are independent random jump amplitudes, independent of counting process .

Assume that the distributions of jumps are alternating,

such that the processes with even (odd)

are identically distributed.

Let

(4.3)

counts the total number of this type of jumps.

The second jump part is defined by jumps occurring

at times

when

the pattern changes.

We assume that the jump amplitudes depend on the number of interventions

during the elapsed time

(4.4)

Here independent random variables

are the jump magnitudes, which are independent of

and

.

Assume that are of the alternating distributions.

Summarising, the jump component

is defined by

(4.5)

Process is an alternating renewal process, see e.g. [26]. The behaviour of the paths of such a process

is illustrated by Figure 3.

Figure 3: A sample path of the piecewise linear process with two alternating patterns and jumps

In this paper we study the piecewise linear process accompanied

with the double jump component

defined by (4.3)-(4.5). Process

successively passes through

the alternating states

determined by the two sets of parameters

(4.6)

Jump processes and are of different nature. Under the given trend

the jump with the magnitude always

occurs just after each tendency switching, while

the jump with magnitude

occurs in the case when the process changes the pattern, (4.4).

We analyse the expectation of .

Denote by

the expectations of jump values,

alternating with respect to that is and .

Denote

(4.7)

Assume that for both the states,

the following series converge:

(4.8)

This condition extends condition (2.11)

fixing relations between

the sets of “observable” parameters

and “hidden” intensity parameters

.

Similarly to Eq. (2.11), conditions (4.8)

are sufficient for “finite accumulation of jumps” at any finite time interval.

Process is a martingale if and only if

for both states the parameters of the model satisfy

(4.18)

Proof.

By renewal character of the process

is a martingale if and only if

the expectations vanish,

or, equivalently,

for the both states,

see (4.9).

By (4.10) this is equivalent to

On the other hand, from (4.19) one can obtain

Indeed, summing up these equations by using

Vandermonde properties (2.4)

we have

Hence .

Then, we prove for both the states by induction.

This follows

by applying (2.4) to the sequential sums,

∎

Remark 4.1.

For some state of the process, let

the supports of jump amplitudes and and the tendency

be situated in the same semi-line.

In this case, by Theorem 4.2, the process is not a martingale.

Precisely, the equivalent martingale measure for

process does not exist

in the following cases: in some state of the process,

(4.20)

(4.21)

The problem of existence of equivalent martingale measures

is discussed in the next section.

Remark 4.2.

Theorem 4.2 seems natural.

For instance, if the holding times are independent of and

exponentially distributed

with alternating parameters

condition (4.18)

(with instead of )

characterises a martingale for the similar piecewise linear process with double jump component,

see [11], Corollary 3.1.

Moreover, condition (4.18) is very similar

to the martingale condition for the simple jump-telegraph model, (1.8),

see [23, 27, 4].

In (4.18)

the term corresponds to the correction of tendency

which is provoked by jumps occurring at each tendency switching, whereas

the term corresponds to

the jumps accompanying the changes of patterns.

5 Market model

We consider the financial market model based on

the piecewise linear stochastic process with jumps

which is

defined on the filtered probability space

by (4.1), (4.3) and (4.4).

The alternating states of the process are described by the two sets of parameters

Here

and

are deterministic, and

independent random

jump amplitudes and

are greater then

Consider a market model of two risky primary assets,

stock and bond.

The bond price is based on the continuous

piecewise linear process

where and are continuously compounding interest rates

depending on the current market state.

The bond price dynamics is defined by

(5.1)

The stock price is defined by the stochastic exponential of .

Precisely, denote

(5.2)

the stochastic exponential of the independent

compound Poisson process .

The stock price is defined by

(5.3)

Model based on (5.1), (5.3)

is characterised by the multiple sources of uncertainty, the Poisson processes

and

which make the model incomplete.

Moreover, the model

has discontinuities of unpredictable type and size. This

makes the model essentially incomplete, see [28].

This model

generalises the jump-telegraph model studied by [23].

See [4] for the detailed presentation.

On the filtered probability space

we define the equivalent measure

by means of the following Girsanov transform.

Consider the numerical (nonrandom) sequences

such that Let

(5.4)

Define the piecewise linear process

with tendencies (as in Section 4)

based on process

counting the states’ switching, (4.1)-(4.2),

This means that for any ,

where is the natural filtration determined by ,

we have

(5.6)

It is easy to see that under measure defined by

(5.5),

only (unobservable) intensity parameters and

of process are changed. In this circumstances (5.5)-(5.6)

may be treated as the Esscher transform (see [29]).

The following result serves as a version of Cameron-Martin-Girsanov

Theorem for this measure transformation.

Theorem 5.1.

Under measure which is defined by (5.5)-(5.6),

the underlying state process

is governed by independent -distributed

inter-switching times,

with the alternating parameters

(5.7)

and

(5.8)

Notice that under measure the unobservable

intensity parameters and of

are transformed

in agreement with the traditional results, related to simple jump-telegraph process,

[4], see also [30].

Proof.

The distribution of the first switching time under measure

can be determined by the survivor functions

.

By definition (5.5)-(5.6)

Now, comparing (5.9) with (2.12) we found that under measure

the first switching time has Poisson-modulated exponential distribution,

with parameters , which

are defined by (5.7) and (5.8).

The joint distribution of the switching times,

could be represented similarly.

For instance, the joint distribution of and under measure

by independence of and is given by

On the other hand, under measure

by definition (5.5)-(5.6) we have for

(5.11)

Here

and

are independent.

By applying again Proposition 2.1 we

confirm (5.7)-(5.8).

∎

By the fundamental theorem of market modelling

the model is arbitrage-free when

the discounted stock price

is a martingale under suitable equivalent measure

(see [31, 32, 33] and [34]).

Note that the discounted stock price

is of the same form as (with the alternating trends

Hence, without loss of generality one can assume that the interest rates are zeros,

Meanwhile, Theorem 5.1 permits to change the intensity parameters arbitrarily.

Hence one can reach martingale condition (4.18)

by applying the Esscher transform (5.5)

only, if values

and are not of the same sign

(for all states and for all ).

If conditions (4.20) or (4.21) hold, then

model (5.3) has arbitrage opportunities.

Remark 5.1.

Market model (5.3) might be interpreted as follows.

Assume that the interest rates are zeros.

Let

(5.12)

be the essential component of asset price (5.3),

which is determined by inherent market forces.

This component takes into account only the jumps accompanying the pattern’s switchings.

We assume that in the both states the tendency and the accompanying

jump amplitude are of the opposite signs:

(5.13)

This assumption seems natural, since the market model with the stock price defined by

(5.12) is arbitrage-free if and only if this condition holds,

see [23, 4].

The jumps defined by (5.2),

accompanying each tendency fluctuation inside the current pattern,

can be considered as the result of external interventions of small markets players.

The stock price follows

If condition (5.13) is fulfilled, then

the model is still arbitrage-free, in spite of the efforts of small players.

The equivalent martingale measure can be provided

by the Esscher transform (5.5)

with parameters and satisfying

(5.4) in both the states.

To define this transform we first assume that

under the martingale measure the modulation intensity

can be determined

neglecting the influence of external interventions,

such that

is of the same sign

with :

By (5.7) . Hence, the parameters

satisfy the condition

Then, the Radon-Nikodym derivative (5.5) provides the martingale measure if

(see (4.18))

Let us consider the model with deterministic jump values and .

The model is arbitrage-free, if

for each and

the triplets

are not of the same sign.

In this case martingale measures are defined by

transform (5.5) with parameters and satisfying (5.4) and in both the states

Let the Poisson modulation in the model be unobservable. This can occur in the case

of constant trends and jumps : in both the states

with modulated hidden parameters and . We assume also that

the parameters’ modulation is not accompanied with jumps:

In this case the model is arbitrage-free, if

The martingale measures are defined by (5.4)

with arbitrary and unique

defined by

6 Concluding remarks

In this paper, we

introduce a rather new class of double stochastic piecewise linear processes

with a Poisson modulated exponential distributions of persistent epochs.

The first layer of stochasticity is a usual telegraph process

based on an alternating Poisson process ,

and the second one (driving the change of patterns)

is characterised by exponentially distributed holding times with a -modulated parameter.

This class of processes is exploited for the purposes of financial modelling.

In particular, we study

an incomplete financial market model

based on a jump-telegraph process.

The dynamics of the considered stochastic process is characterised

by two alternating types of tendencies,

whose holding times have Poisson-modulated exponential distribution.

Moreover, the model includes two different kinds of jumps,

one occurring at the tendency switchings

and the other at the changes of patterns.

A relevant aspect of this model is the presence of external shocks,

which affect the rates of the trend switchings.

This feature ensures that the model is largely flexible

and thus it is suitable to describe a wide family of financial market scenarios.

Specifically, it can be used to describe a financial market model

whose log-returns are influenced both by market forces and by efforts of speculators.

The main results provided for the piecewise linear process with jumps

include the determination of integral equations

for the conditional means and the martingale conditions.

The applications to the financial market model have been presented in detail,

including conditions leading to an arbitrage-free model.

Acknowledgements

The authors thank two anonymous referees for their

useful comments that improved the paper.

This research is partially supported by the group GNCS of INdAM, and by

MIUR (PRIN 2017, project “Stochastic Models for Complex Systems”).

There are no conflicts of interest to this work.

References

[1]

Taylor GI. Diffusion by continuous movements.

Proc Lond Math Soc. 1922; s2-20: 196–212.

https://doi.org/10.1112/plms/s2-20.1.196

[2]

Goldstein G.

On diffusion by discontinuous movements and on the telegraph equation.

Quart J Mech Appl Math. 1951; 4:129–156.

https://doi.org/10.1093/qjmam/4.2.129

[3]

Kac M.

A stochastic model related to the telegraphers equation.

Rocky Mountain J Math. 1974; 4:497–509.

https://doi.org/10.1216/RMJ-1974-4-3-497

Reprinted from: M. Kac,

Some stochastic problems in physics and mathematics,

Colloquium lectures in the pure and applied sciences,

No. 2, hectographed, Field Research Laboratory, Socony Mobil Oil Company, Dallas, TX,

1956, pp. 102-122.

[4]

Kolesnik AD, Ratanov N.

Telegraph Processes and Option Pricing.

Springer: Heidelberg, 2013.

https://doi.org/10.1007/978-3-642-40526-6

[5]

Di Crescenzo A, Martinucci B.

A damped telegraph random process

with logistic stationary distribution. J Appl Prob. 2010; 47:84–96.

https://doi.org/10.1017/S0021900200006410

[6]

Di Crescenzo A, Ratanov N. On jump-diffusion processes with regime

switching: martingale approach.

ALEA, Lat Am J Probab Math Stat. 2015; 12(2): 573–596.

[7]

Di Crescenzo A, Zacks S.

Probability law and flow function of Brownian

motion driven by a generalized telegraph process.

Methodol Comput Appl Probab. 2015; 17(3):761–780.

https://doi.org/10.1007/s11009-013-9392-1

[8]

Ratanov N. Damped jump-telegraph processes.

Stat Probab Lett. 2013; 83:2282–2290.

https://doi.org/10.1016/j.spl.2013.06.018

[9]

Ratanov N.

Telegraph processes with random jumps and complete

market models.

Methodol Comput Appl Probab. 2015; 17(3): 677–695.

https://doi.org/10.1007/s11009-013-9388-x

[10]

Ratanov N.

On piecewise linear processes.

Stat Probab Lett. 2014; 90:60–67.

https://doi.org/10.1016/j.spl.2014.03.015

[11]

Ratanov N.

Self-exciting piecewise linear processes.

ALEA, Lat Am J Probab Math Stat. 2017; 14:445-471.

[12]

Jacobsen M. Point Process Theory and Applications.

Marked Point and Piecewise Deterministic Processes. Birkhäuser, Boston, Basel, Berlin, 2006.

[13]

Snyder DL, Miller MI.

Random Point Processes in Time and Space.

Second Edition. Springer, 1991.

[14]

Brémaud P.

Point Processes and Queues. Martingale dynamics. Springer, 1981.

[15]

Cox DR.

Some statistical methods connected with series of events.

Journal of Royal Statistical Society B. 1955; 17:129–164.

https://doi.org/10.2307/2983950.

[16]

Daley DJ, Vere-Jones D.

An Introduction to the

Theory of Point Processes,

Volume I: Elementary Theory and Methods

Springer, 2d edition, 2003.

[18]

Rolski T, Schmidli H, Schmidt V, Teugels J.

Stochastic Processes for

Insurance and Finance. John Wiley & Sons 1999.

https://doi.org/10.1002/ 9780470317044

[19]

De Gregorio A.

Transport processes with random jump rate.

Stat Probab Lett. 2016; 118:127–134.

http://dx.doi.org/10.1016/j.spl.2016.06.022

[20]

De Gregorio A.

A note on isotropic random flights moving in mixed Poisson environments.

Stat Probab Lett. 2017; 129:311–317.

http://dx.doi.org/10.1016/j.spl.2017.06.021

[21]

Garra R, Orsingher E, Ratanov N.

Planar piecewise linear random motions with jumps

Math Meth Appl Sci. 2017; 40:7673–7685.

http://dx.doi.org/10.1002/mma.4552

[22]

Ratanov N.

Piecewise linear process with renewal starting points.

Stat Probab Lett. 2017; 131:78–86.

https://doi.org/10.1016/j.spl.2017.08.010

[23]

Ratanov N.

A jump telegraph model for option pricing. Quant Fin.

2007; 7:575–583.

https://doi.org/10.1080/14697680600991226

[24]

Kuznetsov YI

Matrices and Polynomials. Part II. Special Theory.

(Inst. Comp. Math. and Math. Geoph. Publ., Novosibirsk, 2004), in Russian.

[25]

Gradshteyn IS, Ryzhik IM.

Table of Integrals, Series and Products

Academic Press, Boston, 1994.

[26]

Cox DR.

Renewal Theory, John Wiley & Sons: New York, 1962.

[27]

López O, Ratanov N.

Option pricing driven by a telegraph process with random jumps.

J Appl Prob. 2012; 49(3):838–849.

https://doi.org/10.1017/S0021900200009578

[28]

Bardhan I, Chao X.

On martingale measures when asset returns have

unpredictable jumps.

Stoch Proc Appl. 1996; 63:35–54.

[29]

Elliott RJ, Chan L, Siu TK.

Option pricing and Esscher transform under regime switching.

Ann Finance 2005; 1:423–432.

https://doi.org/10.1007/s10436-005-0013-z

[30]

Bardhan I, Chao X.

Martingale analysis for assets with discontinuous returns,

Math Oper Res. 1995; 20:243–256.

[31]

Harrison JM, Kreps DM.

Martingales

and arbitrage in multiperiod securities markets.

Journal of Economic Theory 1979; 20:381–408.

[32]

Harrison JM, Pliska SR.

Martingales and stochastic integrals in the theory of continuous trading.

Stoch Proc Appl. 1981; 11:215–280.

[33]

Harrison JM, Pliska SR.

A stochastic calculus model of continuous trading: complete markets.

Stoch Proc Appl. 1983; 15:313–316.

[34]

Delbaen F, Schachermayer W. What is a free lunch?

Notices of the American Mathematical Society 2004; 51(5):526–528.