Adversarial Estimation of Riesz Representers and Complexity-Rate Robustness

Abstract

Many causal and structural parameters are linear functionals of an underlying regression. The Riesz representer is a key component in the asymptotic variance of a semiparametrically estimated linear functional. We propose an adversarial framework to estimate the Riesz representer using general function spaces. We prove a nonasymptotic mean square rate in terms of an abstract quantity called the critical radius, then specialize it for neural networks, random forests, and reproducing kernel Hilbert spaces as leading cases. Furthermore, we use critical radius theory—in place of Donsker theory—to prove asymptotic normality without sample splitting, uncovering a “complexity-rate robustness” condition. This condition has practical consequences: inference without sample splitting is possible in several machine learning settings, which may improve finite sample performance compared to sample splitting. Our estimators achieve nominal coverage in highly nonlinear simulations where previous methods break down. They shed new light on the heterogeneous effects of matching grants.

Keywords: Neural network, random forest, reproducing kernel Hilbert space, critical radius, semiparametric efficiency.

Code: https://colab.research.google.com/github/vsyrgkanis/adversarial_reisz/blob/master/Results.ipynb

Acknowledgements: We thank William Liu for excellent RA work. NSF Grant 1757140 provided support.

1 Introduction and related work

Many parameters traditionally studied in econometrics and statistics are functionals, i.e. scalar summaries, of an underlying function [Hasminskii and Ibragimov, 1979, Pfanzagl, 1982, Klaassen, 1987, Robinson, 1988, Van der Vaart, 1991, Bickel et al., 1993, Newey, 1994, Andrews, 1994a, Robins and Rotnitzky, 1995, Ai and Chen, 2003]. For example, may be a regression function in a space , and the parameter of interest may be the average policy effect of transporting the covariates according to , so that the functional is [Stock, 1989]. Under regularity conditions, there exists a function called the Riesz representer that represents in the sense that for all For the average policy effect, it is the density ratio , where is the density of and is the density of . More generally, for any bounded linear functional , where and , there exists a Riesz representer such the functional can be evaluated by simply taking the inner product between and .

Estimating the Riesz representer of a linear functional is a critical building block in a variety of tasks. First and foremost, appears in the asymptotic variance of any semiparametrically efficient estimator of the parameter , so to construct an analytic confidence interval, we require an estimator [Newey, 1994]. Second, because appears in the asymptotic variance, can be directly incorporated into estimation of the parameter to ensure semiparametric efficiency [Robins et al., 1995, Robins and Rotnitzky, 1995, Van der Laan and Rubin, 2006, Zheng and Van der Laan, 2011, Belloni et al., 2012, Luedtke and Van der Laan, 2016, Belloni et al., 2017, Chernozhukov et al., 2018, Chernozhukov et al., 2022a]. Third, may admit a structural interpretation in its own right. In asset pricing, is the stochastic discount factor, and is used to price financial derivatives [Hansen and Jagannathan, 1997, Aït-Sahalia and Lo, 1998, Bansal and Viswanathan, 1993, Chen et al., 2023].

The Riesz representer may be difficult to estimate. Even for the average policy effect, its closed form involves a density ratio. A recent literature explores the possibility of directly estimating the Riesz representer, without estimating its components or even knowing its functional form, since the Riesz representer is directly identified from data [Robins et al., 2007, Avagyan and Vansteelandt, 2021, Chernozhukov et al., 2022c, Hirshberg and Wager, 2021, Chernozhukov et al., 2022b, Smucler et al., 2019, Hirshberg et al., 2019], generalizing what is known about balancing weights [Hainmueller, 2012, Imai and Ratkovic, 2014, Zubizarreta, 2015, Chan et al., 2016, Athey et al., 2018, Wong and Chan, 2018, Zhao, 2019, Kallus, 2020]. This literature proposes estimators in specific sparse linear or RKHS function spaces, and analyzes them on a case-by-case basis. In prior work, the incorporation of directly estimated into the tasks above appears to require either (i) the Donsker condition, which restricts the flexibility of the estimators, or (ii) sample splitting, which reduces the effective sample size and may depreciate finite sample performance.

This paper asks: is there a generic framework to construct an estimator over flexible function spaces, including machine learning function spaces that are not Donsker such as neural networks? Moreover, can we use the same framework to incorporate into the tasks listed above while avoiding both the Donsker condition and sample splitting? Finally, do these theoretical innovations shed new light in a highly influential empirical study where previous work is limited to parametric estimation?

1.1 Contributions

Our first contribution is a general Riesz estimator over nonlinear function spaces with fast estimation rates. Specifically, we propose and analyze an adversarial, direct estimator for the Riesz representer of any mean square continuous linear functional, using any function space that can approximate well. We prove a high probability, finite sample bound on the mean square error in terms of an abstract quantity called the critical radius , which quantifies the complexity of in a certain sense. Since the critical radius is a well-known quantity in statistical learning theory, we can appeal to critical radii of machine learning function spaces such as neural networks, random forests, and reproducing kernel Hilbert spaces (RKHSs).111Hereafter, a “general” function space is a possibly non-Donsker space that satisfies a critical radius condition. An “arbitrary” function space may not satisfy a critical radius condition. Unlike previous work on Riesz representers, we provide a unifying approach for general function spaces (and their unions), which allows us to handle new function spaces such as neural networks and random forests. These new function spaces achieve nominal coverage in highly nonlinear simulations where other function spaces fail.

Our use of critical radius theory goes beyond proving rates. Our second contribution is to incorporate our direct estimator, which may involve machine learning function spaces, into downstream tasks such as semiparametric estimation and inference while bypassing both the Donsker condition and sample splitting. In particular, we provide a new way to handle stochastic equicontinuity without sample splitting, which improves performance over the sample splitting counterpart in some Monte Carlo settings. This paper appears to be the first to articulate a general “complexity-rate robustness” using critical radii: we prove that a sufficient condition for Gaussian approximation is when the product of the complexity and the estimation rate is . Function spaces with well-behaved critical radii are an important intermediate case between Donsker spaces and arbitrary spaces, for which we attain quite strong “Donsker-style” conclusions. Critical radius conditions, which go well beyond Donsker conditions, imply both nonparametric estimation for the Riesz representer and asymptotic normality for the parameter without sample splitting.

In practice, adversarial estimators with machine learning function spaces involve computational techniques that may introduce computational error. As our third contribution, we analyze the computational error for some key function spaces used in adversarial estimation of Riesz representers. For random forests, we analyze oracle training and prove convergence of an iterative procedure. For the RKHS, we derive a closed form without computational error and propose a Nyström approximation with computational error. In doing so, we attempt to bridge theory with practice for empirical research.

Finally, we provide an empirical contribution by extending the influential analysis of [Karlan and List, 2007] from parametric estimation to semiparametric estimation. To our knowledge, semiparametric estimation has not been used in this setting before. The substantive economic question is: how much more effective is a matching grant in Republican states compared to Democratic states? The flexibility of machine learning may improve model fit, yet it may come at the cost of statistical power. Our approach appears to improve model fit relative to previous parametric and semiparametric approaches. At the same time, it recovers some of the statistical power by eliminating sample splitting, unlike previous approaches that allow for general machine learning but require sample splitting.

1.2 Key connections

A central insight of this work is that the adversarial approach for conditional moment models [Dikkala et al., 2020] may be adapted to the problem of learning the Riesz representer. In particular, the Riesz representation theorem implies a continuum of unconditional moment restrictions, similar to a conditional moment restriction [Newey and Powell, 2003, Ai and Chen, 2003, Blundell et al., 2007, Chen and Pouzo, 2009, Darolles et al., 2011, Chen and Pouzo, 2012, Chen and Pouzo, 2015, Chen and Christensen, 2018]. In an adversarial approach, the unconditional moment restrictions are enforced adversarially over a set of test functions [Goodfellow et al., 2014, Arjovsky et al., 2017, Kaji et al., 2020]. Since this paper was circulated on arXiv in 2020, this framework has been extended to Riesz representers of more functionals, e.g. proximal treatment effects [Kallus et al., 2021, Ghassami et al., 2022].

The fundamental advantage of the adversarial approach is its unified analysis over general function classes in terms of the critical radius [Koltchinskii and Panchenko, 2000, Bartlett et al., 2005]. The adversarial approach is a family of estimators adaptive to a variety of data settings with a unified guarantee [Negahban et al., 2012, Lecué and Mendelson, 2017, Lecué and Mendelson, 2018]. In semiparametric theory without sample splitting, the complexity of function classes has historically been quantified in more restrictive ways; see Section 2. For inference without sample splitting, previous work requires the function class to be Donsker [Andrews, 1994a, Van der Laan and Rubin, 2006, Luedtke and Van der Laan, 2016, Qiu et al., 2021], or to have slowly increasing entropy [Belloni et al., 2014a, Zhang and Zhang, 2014, Javanmard and Montanari, 2014, Van de Geer et al., 2014]. Machine learning function spaces may not satisfy these properties, however they may have well-behaved critical radii.

Our work complements [Hirshberg and Wager, 2021], who also use an adversarial approach to semiparametric estimation. However, their results are different in nature as they do not imply an rate for Riesz representers and hold only for Donsker function classes, ruling out machine learning. Another key predecessor is [Chernozhukov et al., 2022b] which only considers sparse linear function approximation of Riesz representers. Allowing for general function spaces may yield better finite sample performance due to a smaller approximation error. Finally, [Kaji et al., 2020] propose an adversarial estimation procedure for parametric models, whereas we study semiparametric models.

Several subsequent works build on our work and propose other estimators for nonlinear function spaces [Singh, 2021, Chernozhukov et al., 2021, Kallus et al., 2021, Ghassami et al., 2022], but this paper was the first to give fast estimation rates for the Riesz representer with nonlinear function approximation, allowing neural networks and random forests to be used for direct Riesz estimation. See Sections 3 and 4 for detailed comparisons.

In summary, at the time the paper was initially circulated, it was the first to do the following: (i) propose direct Riesz representer estimators over general non-Donsker spaces; (ii) eliminate sample splitting for general non-Donsker spaces; (iii) provide a unified analysis in terms of critical radius theory to achieve both of these results.222Recall that a “general” function space is possibly non-Donsker yet satisfies a critical radius condition. None of (i), (ii), or (iii) appear to be contained in previous works.

The structure of this paper is as follows. Section 2 provides critical radius background. Section 3 analyzes our adversarial estimator of the Riesz representer over general and specific function spaces. Section 4 proves semiparametric inference without the Donsker condition and without sample splitting. Section 5 studies the computation error that arises in practice. Section 6 showcases settings where (i) eliminating sample splitting may improve finite sample performance; (ii) our flexible estimator achieves nominal coverage while previous methods do not; and (iii) these gains provide new, rigorous empirical evidence. Section 7 concludes. Appendix A proves the main results. Appendix B relates our results to empirical asset pricing, and Appendix C relates our results to the well-studied sparse linear case.

2 Critical radius background

2.1 Function space notation

The critical radius of a function class is a widely used quantity in statistical learning theory for deriving fast estimation rates that are nearly optimal. For instance, for parametric function classes, the critical radius is of order , leading to fast parametric rates. The slow rate would be achievable via looser uniform deviation bounds.

To use critical radius theory, we introduce the following notation. Let be the inner product associated with the norm, i.e. . Moreover, let denote the empirical average and the empirical norm, i.e. For any function space , let denote the star hull and let denote the space of differences.

We propose Riesz representer estimators that use a general function space , equipped with some norm . In particular, will be used for the minimization in our min-max approach. Given the notation above, we define the class which we will use for the adversarial maximization:

and we assume that the norm extends naturally to the larger space . We propose an adversarial estimator based on regularized variants of the following min-max criterion:

where is pinned down by the functional of interest

2.2 Abstract definition

A Rademacher random variable takes values in . Let be independent Rademacher random variables drawn equiprobably. Then the local Rademacher complexity of the function space over a neighborhood of radius is defined as . The local Rademacher complexity asks: for a draw of random signs on , how much can an adversarial choice of , within a certain radius, blow up the signed average in expectation? As an important stepping stone, we prove bounds on in terms of local Rademacher complexities.

These bounds can be optimized into fast rates by an appropriate choice of the radius , called the critical radius. Formally, the critical radius of a function class with range in is defined as any solution to the inequality . There is a sense in which balances bias and variance in the bounds.

The critical radius has been analyzed and derived for a variety of function spaces of interest, such as neural networks, reproducing kernel Hilbert spaces, high-dimensional linear functions, and VC-subgraph classes. The following characterization of the critical radius opens the door to such derivations [Wainwright, 2019, Corollary 14.3 and Proposition 14.25]: the critical radius of any function class , uniformly bounded in , is of the same order as any solution to the inequality:

| (1) |

In this expression, is the ball of radius and is the empirical -covering number at approximation level , i.e. the size of the smallest -cover of , with respect to the empirical metric. This expression foreshadows how a critical radius analysis will be similar in spirit to a metric entropy analysis, but will handle more function spaces; see (2) and the discussion below.

2.3 Illustration: Neural network

As a leading example, suppose that the function class can be expressed as a rectified linear unit (ReLU) activation neural network with depth and width , denoted as . Functions in can be expressed as neural networks with depth and width . Assume that functions in can also expressed by neural networks of depth and width . Finally, suppose that the covariates are distributed in a way that the outputs of and are uniformly bounded in . Then by the covering number for VC classes [Haussler, 1995] as well as the bounds of [Anthony and Bartlett, 2009, Theorem 14.1] and [Bartlett et al., 2019, Theorem 6], the critical radii of and are

See [Foster and Syrgkanis, 2023, Proof of Example 3] for a detailed derivation.

In summary, our general theorems provide rates, as well as rate conditions for inference without sample splitting, in terms of the critical radius. Thus our general theorems allow us to appeal to critical radius characterizations for a family of adversarial Riesz representer estimators over general function classes. In particular, we provide new results for function classes previously unused in direct Riesz representer estimation, e.g. neural networks.

2.4 Comparison to the Donsker condition

We use the critical radius condition, in place of the Donsker condition, to prove semiparametric inference in Section 4. We now clarify the similarities and differences between these concepts. A standard decomposition (restated in Appendix A) shows that

where is an empirical process indexed by nuisance functions. A central limit theorem gives , and a product rate condition gives . What remains to show is that , for which we provide a new argument.

The Donsker condition involves stochastic equicontinuity, which means that and , where , imply , so that the desired result holds [Andrews, 1994b]. A sufficient condition is Pollard’s entropy condition [Pollard, 1982], which we now state for the function class , uniformly bounded in :

| (2) |

where is the the set of all finite discrete probability measures. The standard analytic approach is to verify (2) for simple function spaces [Pakes and Pollard, 1989, Andrews, 1994a, Pakes and Olley, 1995, Ai and Chen, 2003, Chen et al., 2003]. While smooth Sobolev spaces satisfy this entropy condition, even rearranged Sobolev spaces do not [Chernozhukov et al., 2022c, Section 4.5], nor do balls for [Raskutti et al., 2011, Lemma 2].

By contrast, we use the less strict entropy condition (1) to find the critical radius . When and , we prove that .333We actually prove a more general result with limited mis-specification. We observe three key differences between our approach and the Donsker approach. First, the entropy integral in (1) is local in nature, with that appears in the integration bounds, in the radius of the ball , and in the upper bound. The entropy integral in (2) is global in its integration bounds, in considering all of , and in its upper bound. Second, the entropy integral in (1) is only in terms of the empirical covering number, whereas the entropy integral in (2) is for all covering numbers. Third, due to these differences between (1) and (2), we achieve a complexity-rate robustness: implies the desired result, so higher complexity can be compensated by better estimation rates. The Donsker approach does not have such a condition. In summary, we characterize a weaker sufficient condition for .

3 Adversarial estimation and fast rate

3.1 Estimator definition

We study linear and mean square continuous functionals of the form .

Assumption 1 (Mean square continuity).

There exists some constant such that , .

In Appendix D, we verify that a variety of functionals are mean square continuous under standard conditions, including the average policy effect, regression decomposition, average treatment effect, average treatment on the treated, and local average treatment effect.

Mean square continuity implies boundedness of the functional , since . By the Riesz representation theorem, any bounded linear functional over a Hilbert space has a Riesz representer in that Hilbert space. Therefore Assumption 1 implies that the Riesz representer estimation problem is well defined. We propose the following general estimator.

Estimator 1 (Adversarial Riesz representer).

For regularization , define

Corollary 1 (Population limit).

Consider the population limit of our criterion where and : This limit equals .

Thus our empirical criterion converges to the mean square error criterion in the population limit, even though an analyst does not have access to unbiased samples from .

Remark 1 (Comparisons).

Estimator 1 shares principles of adversarial estimation and ridge regularization of [Hirshberg and Wager, 2021], who propose an estimator

Some differences are (i) is a function while is a vector; (ii) directly regularizes the adversarial function , while does not; (iii) the criterion of is linear in the moment violation, while the criterion of is quadratic in it. More substantial than the difference in estimation will be the difference in theory: our analysis of avoids Donsker restrictions and provides rates, unlike the analysis of .

The vanishing norm-based regularization terms in Estimator 1 may be avoided if an analyst knows a bound on . In such case, one can impose a hard norm constraint on the hypothesis space and optimize over norm-constrained subspaces. By contrast, regularization allows the estimator to adjust to , without knowledge of it.

Our analysis allows for mis-specification, i.e. . In such case, the estimation error incurs an extra bias of where is the best-in-class approximation. Section 4 interprets as an approximating sequence of function spaces.

3.2 Mean square rate via critical radius

We now state our first main result: a fast, finite sample mean square rate for the adversarial Riesz representer in terms of the critical radius.

Assumption 2 (Critical radius for estimation).

Define the balls of functions and . Assume that there exists some constant such that the functions in and have uniformly bounded ranges in . Further assume that, for this , upper bounds the critical radii of and .

Our bound will hold with probability . To lighten notation, we define the following summary of the critical radii, approximation error, and low probability event:

where and are universal constants. We defer proofs to Appendices A and D.

Theorem 1 (Mean square rate).

Corollary 2 (Weaker metric rate).

Consider the weaker metric defined as . Then under the conditions of Theorem 1,

where the definition of replaces with .

Corollary 3 (Mean square rate without norm regularization).

In Appendix C, we consider an another version of Estimator 1 without the term. We prove a fast rate on as long as can be decomposed into the union of symmetric function spaces, i.e. . See Proposition 4 for details.

Remark 2 (Technical contribution).

[Hirshberg and Wager, 2021, Theorem 2] and [Hirshberg et al., 2019, eq. 18] bound the empirical norm in terms of critical radii under Donsker and RKHS conditions, respectively. We instead bound the population norm in terms of critical radii without Donsker conditions, for function spaces beyond the RKHS. [Chernozhukov et al., 2022c, Theorem 4.3], [Chernozhukov et al., 2022b, Theorem 1], and [Smucler et al., 2019, Theorem 8] bound the population norm for sparse linear estimators in terms of approximate sparsity rates. We also bound the population norm, but for function spaces that may not be sparse and linear. In summary, we complement previous work by providing a unified analysis across function spaces, including new ones. See Appendix C for formal comparisons in the sparse linear special case.

Our proof uses similar ideas to [Dikkala et al., 2020, Theorem 1], which considers an adversarial estimator for nonparametric instrumental variable regression. [Dikkala et al., 2020, Theorem 1] bounds a weaker metric than mean square error and requires critical radius assumptions on more complicated function spaces.

Corollary 4 (Union of hypothesis spaces).

Suppose that and that the critical radius of each is in the sense of Assumption 2. Suppose that for some , . Then the critical radius of is , and the conclusions of the above results continue to hold.

By Corollary 4, our results allow an analyst to estimate the Riesz representer with a union of flexible function spaces, which is an important practical advantage. This is a specific strength of the critical radius approach and a contribution to the direct Riesz estimation literature, which appears to have studied one function space at a time.

3.3 Special cases: Neural network, random forest, RKHS

Recall from Section 1 that is the ReLU activation neural network with depth and width .

Corollary 5 (Neural network Riesz representer rate).

Take . Suppose that is representable as a neural network with depth and width . Finally, suppose that the covariates are such that functions in and are uniformly bounded in . Then with probability ,

If is representable as a ReLU neural network, then the first term vanishes and we achieve an almost parametric rate. If is representable as a nonparametric Holder function, then one may appeal to approximation results for ReLU activation neural networks [Yarotsky, 2017, Yarotsky, 2018]. Such results typically require that the depth and the width of the neural network grow as some function of the approximation error , leading to errors of the form . Optimally balancing leads to almost tight nonparametric rates. Corollary 5 for the Riesz representer is the same order as [Farrell et al., 2021, Theorem 1] for nonparametric regression.

Next, consider the oracle trained random forest estimator described in Section 5. Denote by the base space, with VC dimension , in which each tree of the forest is estimated. Denote by the linear span of the base space.

Corollary 6 (Random forest Riesz representer rate).

Take . Suppose that . Finally, suppose that the covariates are such that functions in and are uniformly bounded in . Then under after iterations of oracle training and under the regularity conditions described in Proposition 1, with probability ,

The second term is the computational error from Proposition 1. The third term follows from the complexity of oracle training and from analysis of VC spaces [Shalev-Shwartz and Ben-David, 2014]. We defer further discussion to Section 5.

Suppose that the base estimator is a binary decision tree with small depth. This example satisfies the requirement of [Mansour and McAllester, 2000], and we use it in practice. If , the bound simplifies to

Denote by the RKHS with kernel , so that is the RKHS norm. Define the empirical kernel matrix where . Let be the eigenvalues of . For a possibly different kernel , we define analogous objects with tildes. We arrive at the following result using [Wainwright, 2019, Corollary 13.18].

Corollary 7 (RKHS Riesz representer rate).

Take . Suppose that . Suppose that there exists some such that functions in and are uniformly bounded in . Let be any solution to the inequalities and . Then with probability ,

Our estimator does not need to know the RKHS norm . Instead it automatically adjusts to the unknown RKHS norm. The bound is based on empirical eigenvalues. These empirical quantities can be used as a data-adaptive diagnostic.

For particular kernels, a more explicit bound can be derived as a function of the eigendecay. For example, the Gaussian kernel has an exponential eigendecay. [Wainwright, 2019, Example 13.21] derives , thus leading to almost parametric rates: .

See Appendix C for sparse linear function spaces and further comparisons.

4 Semiparametric inference without sample splitting

4.1 Estimator definition

So far, we have analyzed a machine learning estimator for , the Riesz representer to the mean square continuous functional . As previewed in Section 1, a well known use of is to construct a consistent, asymptotically normal, and semiparametrically efficient estimator for a parameter . For example, when the parameter is the average policy effect, , , and . In this section, we provide new analysis for a well known estimator of the parameter . We quote the estimator then prove new semiparametric theory for it.

Estimator 2 (Doubly robust functional [Robins et al., 1995, Robins and Rotnitzky, 1995, Chernozhukov et al., 2022a]).

Estimate using all of the observations. Then set , where .

Our analysis in this section allows for machine learning estimators and , subject to critical radius (Theorem 2) or estimator stability (Theorem 3) conditions. One may choose Estimator 1 as , so that the same critical radius theory powers nonparametric rates and semiparametric inference.

Estimator 2 does not split the sample, as if often done in targeted [Zheng and Van der Laan, 2011] and debiased [Chernozhukov et al., 2018] machine learning. Sample splitting [Bickel, 1982, Schick, 1986, Klaassen, 1987] is a technique to bypass the Donsker condition while proving semiparametric inference. However, it may come at a finite sample cost since it reduces the effective sample size, as shown in simulations in Section 6. Our theoretical contribution in this section is to prove semiparametric inference of machine learning estimators without either the Donsker condition or sample splitting. See Appendix E for familiar results that use sample splitting.

4.2 Normality via critical radius

All of our results use a weak and well known condition for nuisance estimators and : the mixed bias vanishes quickly enough.

Assumption 3 (Mixed bias condition).

Suppose that .

By Cauchy-Schwarz inequality, Assumption 3 is implied by . The latter is the celebrated double rate robustness condition, also called the product rate condition, whereby either or may have a relatively slow estimation rate, as long as the other has a sufficiently fast estimation rate.

The mixed bias condition is weaker than double rate robustness: only needs to approximately satisfy Riesz representation for test functions of the form . Hence if , then it suffices for to be a local Riesz representer around rather than a global Riesz representer for all of . In Appendix E, we prove that Riesz estimation may become much simpler if the only aim is to satisfy Assumption 3.

Assumption 3 leaves limited room for mis-specification. In Appendix E, we allow for inconsistent nuisance estimation: the probability limit of may not be , or the probability limit of may not be , as long as the other nuisance is correctly specified and converges at the parametric rate [Benkeser et al., 2017]. Below, we focus on the thought experiment where, for a fixed , the best in class approximations are which may not coincide with . In the limit, the function spaces become rich enough to include .

We place a critical radius assumption for inference, slightly abusing notation by recycling the symbols and .

Assumption 4 (Critical radius for inference).

Assume that, with high probability, and . Moreover, assume that that there exists some constant such that the functions in , , and have uniformly bounded ranges in , and such that with high probability and . Further assume that, for this , upper bounds the critical radii of , , and . Finally, assume is lower bounded by , and that and are bounded almost surely.

In the special case that and , Assumption 4 simplifies to a bound on the critical radii of , , and . More generally, we allow the possibility that only the critical radii of subsets of function spaces, where the estimators are known to belong, are well behaved. This nuance is helpful for sparse linear settings, where is a restricted cone that is much simpler than .

As before, to lighten notation, we define the following summary of the critical radii: , where and are universal constants.

Theorem 2 (Normality via critical radius).

A special case takes and . More generally, we consider the possibility that and , where . For example, consider the thought experiment where are sequences of function spaces that approximate the nuisances increasingly well as the sample size increases. Then by Cauchy-Schwarz and triangle inequalities, a sufficient condition for Assumption 3 is that . In other words, for a fixed sample size, may not include ; it suffices that they do so in the limit, and that the product of their approximation errors vanishes quickly enough. In this thought experiment, is a sequence indexed by the sample size as well.

Remark 3 (Technical contribution).

Without sample splitting, inferential theory typically requires the Donsker condition or slowly increasing entropy, neither of which is satisfied by machine learning function spaces. We replace the Donsker condition with , a more permissive complexity bound in terms of the critical radius that allows for machine learning. We interpret as a new “complexity-rate robustness”. For general function spaces, the rate at which vanishes may be slower than what was previously required for inference, as long as vanishes quickly enough to compensate.

Remark 4 (Comparisons).

[Hirshberg and Wager, 2021, Theorem 2] prove a similar conclusion under Donsker conditions, which we avoid. [Farrell et al., 2021, Theorem 3] prove a similar conclusion for a smaller class of target parameters and one function space, under more stringent rate assumptions. In particular, the authors consider the average treatment effect and its variants, estimated using a neural network regression and neural network propensity score. [Farrell et al., 2021, Theorem 3, Assumption C] requires , which is not a product condition. By contrast, we require , which is a kind of product condition.

Take to be the maximum of the quantities called in Sections 3 and 4, multiplied by a slowly increasing factor. Theorem 1 proves that . Known results for nonparametric regression give . These results verify Assumption 3 as well as the joint rate condition when . In summary, critical radius theory alone, without sample splitting or Donsker conditions, delivers both of our main results: Theorems 1 and 2.

How does our “complexity-rate robustness” compare to “double rate robustness” in a concrete example? Consider estimating and with constrained linear functions in dimensions. Suppose that are sparse linear functions with at most nonzero coefficients. Under a restricted eigenvalue condition on the covariates, a lasso estimator and a sparse linear adversarial estimator satisfy and . Thus a sufficient condition to use our theory above is . See Appendix C for formal statements.

For comparison, for the sample splitting estimator, a sufficient condition is double rate robustness, which amounts to double sparsity robustness: , where are the numbers of nonzero coefficients of .444More generally, for the sample splitting estimator, the well known sufficient condition is , where , , , and . Our requirement is slightly stronger. While it does not allow a setting in which one nuisance is quite dense while the other is quite sparse, it does show that if both nuisances are moderately sparse, then sample splitting can be eliminated, improving the effective sample size.

Our sufficient condition for the sparse linear setting, , recovers the sufficient conditions of [Belloni et al., 2014b, eq. 5.5] and [Belloni et al., 2014a, Condition 3(iv)] up to logarithmic factors. In this sense it appears relatively sharp. Our contribution is to characterize a general complexity-rate robustness condition that applies to a broad range of settings beyond the sparse linear case.

On the one hand, eliminating sample splitting may increase the effective sample size. On the other, it may increase “own observation” bias [Newey and Robins, 2018]. Section 6 shows that the former phenomenon may outweigh the latter in some cases. Future research may formalize this trade-off in finite samples.

4.3 Normality via estimator stability

In anticipation of Section 5, which addresses computational aspects, we present a different inference result that eliminates sample splitting, the Donsker condition, and now even the critical radius bound. Our motivation is that, in practice, the computational techniques used to fit machine learning estimators may defy critical radius analysis. For example, it could be the case that large neural network classes are trained via few iterations of stochastic gradient descent [Hardt et al., 2016], or that ensembles of overfitting estimators are sub-bagged [Elisseeff and Pontil, 2003]. For these scenarios where the critical radius may not be small, we instead appeal to the stability of the estimators.

Assumption 5 (Estimator stability for inference).

Let and let be the estimated function if sample were removed from the training set. Assume is symmetric across samples and satisfies , where returns the largest entry of the vector.

[Kale et al., 2011] propose Assumption 5 in order to derive improved bounds on -fold cross validation. It is formally called mean square stability, which is weaker than the well studied uniform stability [Bousquet and Elisseeff, 2002]. See [Elisseeff and Pontil, 2003, Celisse and Guedj, 2016, Abou-Moustafa and Szepesvári, 2019] for further discussion.

Theorem 3 (Normality via estimator stability).

Sub-bagging means using as an estimator the average of several base estimators, where each base estimator is calculated from a subsample of size . The sub-bagged estimator is stable with [Elisseeff and Pontil, 2003]. If the bias of the base estimator decays as some function , then sub-bagged estimators typically achieve [Athey et al., 2019, Khosravi et al., 2019, Syrgkanis and Zampetakis, 2020]. To use our results, it suffices that . As long as and , our joint rate condition holds.

Consider a high dimensional setting with . Suppose that only variables are strictly relevant, i.e. each decreases explained variance by least . [Syrgkanis and Zampetakis, 2020] show that the bias of a deep Breiman tree trained on observations decays as in this setting. A deep Breiman forest, where each tree is trained on samples drawn without replacement, achieves . Thus sub-bagged deep Breiman random forests satisfy the conditions of Theorem 3 in a sparse, high-dimensional setting.

5 Analysis of computational error

5.1 Oracle training for random forest

After studying in Section 3 and in Section 4, we attempt to bridge theory with practice by analyzing the computational error for some key function spaces used in adversarial estimation. For random forests, we prove convergence of an iterative procedure. For the RKHS, we derive a closed form without computational error. For neural networks, we describe existing results and directions for future work. This section aims to provide practical guidance for empirical researchers.

Consider Corollary 6, which uses random forest function spaces. We analyze an optimization procedure called oracle training to handle this case. In the context of random forests, it may be viewed as a particular criterion for fitting the random forest. More generally, it is an iterative optimization procedure based on zero sum game theory for when is a non-differentiable function space, hence gradient based methods do not apply.

In this exposition, we study a variation of Estimator 1 with , i.e. without norm-based regularization. Define . We view as the payoff of a zero sum game where the players are and . The game is linear in and concave in , so it can be solved when plays a no-regret algorithm at each period and plays the best response to each choice of .

Proposition 1 (Oracle training converges).

Suppose that has operator norm , and that is convex. Suppose that at each period , the players follow and , where . Then for , the function is an -approximate solution to Estimator 1 with .

Since is convex, a no-regret strategy for is follow-the-leader. At each period, the player maximizes the empirical past payoff . This loss may be viewed as a modification of the Riesz loss. In particular, construct a new functional that is the original functional minus then estimate its Riesz representer.

For any fixed , the best response for is to minimize . Since is linear in , this is the same as maximizing . In other words, wants to match the sign of . In summary, the best response for is equivalent to a weighted classification oracle, where the label is and the weight is .

Since is linear in , each is supported on only elements in the base space. In Corollary 6, we assume that each element of the base space has VC dimension at most . Hence each has VC dimension at most and therefore has VC dimension at most [Shalev-Shwartz and Ben-David, 2014]. Thus the entropy integral (1) is of order . Finally, since the player problem reduces to a modification of the Riesz problem, this bound applies to both of the induced function spaces in oracle training.

5.2 Closed form for RKHS

Consider the setting of Corollary 7, which uses RKHSs. We prove that Estimator 1 has a closed form solution without any computational error, and derive its formula. Our results extend the classic representation arguments of [Kimeldorf and Wahba, 1971, Schölkopf et al., 2001]. We use backward induction, first analyzing the best response of an adversarial maximizer, which we denote by , as a function of . Then we derive the minimizer that anticipates this best response.

Formally, let and , where is the RKHS with kernel . In what follows, we denote the usual empirical kernel matrix by , with entries given by , and the usual evaluation vector by , with entries given by . To express our estimator, we introduce additional kernel matrices and additional evaluation vectors . For readability, we reserve details on how to compute these additional matrices and vectors for Appendix F. At a high level, these additional objects apply the functional to the kernel and data in various ways. For any symmetric matrix , let denote its pseudo-inverse. If is invertible then .

Proposition 2 (Closed form of maximizer).

For a potential minimizer , the adversarial maximizer has a closed form solution with a coefficient vector . More formally, and . The coefficent vector is explicitly given by where

is defined such that , and is the vector of ones.

Proposition 3 (Closed form of minimizer).

The minimizer has a closed form solution with a coefficient vector . More formally, . The coefficient vector is explicity given by where .

Combining Propositions 2 and 3, it is possible to compute , and hence and . Therefore it is possible to compute the optimized loss in Estimator 1. While Theorem 1 provides theoretical guidance on how to choose , the optimized loss provides a practical way to choose .

Remark 5 (Comparisons).

Kernel balancing weights may be viewed as Riesz representer estimators for the average treatment effect functional , where , is the treatment, and is the covariate. Various estimators have been proposed, e.g. [Wong and Chan, 2018, Zhao, 2019, Kallus, 2020, Hirshberg et al., 2019] and references therein. Our results situate kernel balancing weights within a unified framework for semiparametric inference across general function spaces. It appears that the loss of Estimator 1, the closed form of Proposition 3, and the norm of our guarantee in Theorem 1 depart from and complement these works.

The closed form expressions above involve inverting kernel matrices that scale with . To reduce the computational burden, we derive a Nystrom approximation variant of our estimator in Appendix F. This variant incurs computational error.

5.3 Stochastic gradient descent for neural network

Consider the setting of Corollary 5, which uses neural network function spaces. When and are represented by deep neural networks, then the optimization problem in Estimator 1 is highly non-convex. Beyond the challenge of using a non-convex function space, which also appears in problems with square losses, we face the challenge of a non-convex and non-smooth min-max loss. We describe off-the-shelf optimization methods for generative adversarial networks (GANs) that apply to our problem, and describe a closely related approximate guarantee for stochastic gradient descent.

Similar to the optimization problem of GANs, our our estimator solves a non-convex, non-concave zero sum game, where the strategy of each player is a set of neural network parameters. A variety of recent iterative optimization algorithms for GANs inspired by zero sum game theory apply to our problem. See e.g. the “optimistic Adam” procedure [Daskalakis et al., 2017], which has been adapted to conditional moment models [Bennett et al., 2019, Dikkala et al., 2020]. The “extra gradient” procedures [Hsieh et al., 2019, Mishchenko et al., 2019] provide further options.

In practice, we find that a simple optimization procedure converges to the solution of Estimator 1 when using overparametrized neural networks. The procedure is to implement simultaneous gradient descent-ascent, then to obtain the average path by averaging over several iterations. We directly extend the main procedure of [Liao et al., 2020], who prove convergence for min-max losses that are similar to our own, building on principles used to study square losses [Allen-Zhu et al., 2018, Du et al., 2018, Soltanolkotabi et al., 2019].

Neural networks that are sufficiently wide and randomly initialized behave like linear functions in an RKHS called the neural tangent kernel space. As long as the error of this approximation is carefully accounted for, one can invoke the analysis of sparse linear function spaces given in Appendix C. Future work may formalize this intuition, generalizing the main result of [Liao et al., 2020].

To facilitate optimization, computational analysis increases the width of the neural network. Doing so deteriorates the statistical guarantee in Corollary 5, since the critical radius grows as a function of the width; see Section 1. Future work may improve the dependence on width, sharpening the results of [Liao et al., 2020], to alleviate this trade-off.

6 Simulated and real data analysis

6.1 Eliminating sample splitting may improve precision

To begin, we showcase how eliminating sample splitting may improve precision—a simple point with practical consequences for empirical economics. In this section, let , where is the treatment and are the covariates. In a baseline setting with , every variation of our estimator achieves nominal coverage when the sample size is sufficiently large. We document performance in 100 simulations for sample sizes , which are representative for empirical economic research.

We implement five variations of Estimator 2 for the average treatment effect, denoted by in Section 4. Crucially, for , we use our proposed adversarial Riesz representer, defined by Estimator 1 in Section 3. The five variations of are (i) sparse linear, (ii) RKHS, (iii) RKHS with Nystrom approximation, (iv) random forest, or (v) neural network. For comparison, we implement three previous estimators for the average treatment effect. These are (vi) logistic propensity score, (vii) random forest propensity score, and (viii) the adversarial estimator of [Hirshberg and Wager, 2021]. Across estimators, we use a boosted regression estimator of , except when implementing [Hirshberg and Wager, 2021], which requires to be Donsker. Across estimators, we report the coverage, bias, and interval length. We present simulation results with and without sample splitting. We leave table entries blank when previous work does not provide theoretical justification. See Appendix G for simulation details.

| Previous work | This paper | ||||||||

| Estimator | Prop. score | Adv. | Adversarial | ||||||

| Function space | logistic | R.F. | Donsker | sparse | RKHS | Nystrom | R.F. | N.N. | |

| coverage | 95 | 95 | - | 97 | 96 | 91 | 93 | 53 | |

| bias | -1 | 5 | - | 1 | 2 | 3 | 8 | -11 | |

| length | 138 | 99 | - | 118 | 113 | 93 | 106 | 34 | |

| coverage | 95 | 92 | - | 95 | 96 | 85 | 92 | 57 | |

| bias | 2 | 2 | - | 0 | 4 | 0 | 4 | -6 | |

| length | 80 | 65 | - | 77 | 98 | 63 | 68 | 33 | |

| coverage | 95 | 95 | - | 97 | 98 | 93 | 97 | 82 | |

| bias | -1 | 0 | - | -3 | 1 | -2 | 0 | -5 | |

| length | 48 | 42 | - | 46 | 64 | 41 | 44 | 34 | |

| coverage | 95 | 87 | - | 91 | 99 | 88 | 86 | 90 | |

| bias | 0 | 3 | - | 1 | 1 | 3 | 3 | 0 | |

| length | 34 | 30 | - | 32 | 42 | 29 | 30 | 32 | |

| coverage | 96 | 92 | - | 95 | 97 | 91 | 89 | 94 | |

| bias | 0 | 2 | - | 1 | 1 | 2 | 2 | 1 | |

| length | 23 | 21 | - | 22 | 28 | 21 | 21 | 23 | |

| Previous work | This paper | ||||||||

| Estimator | Prop. score | Adv. | Adversarial | ||||||

| Function space | logistic | R.F. | Donsker | sparse | RKHS | Nystrom | R.F. | N.N. | |

| coverage | 92 | - | 97 | 94 | 95 | 91 | 92 | 50 | |

| bias | 0 | - | 3 | 1 | 0 | 1 | 7 | -8 | |

| length | 94 | - | 103 | 94 | 96 | 86 | 88 | 32 | |

| coverage | 92 | - | 94 | 95 | 94 | 88 | 93 | 58 | |

| bias | 1 | - | 1 | -1 | 1 | 0 | 2 | -6 | |

| length | 68 | - | 70 | 68 | 73 | 58 | 65 | 34 | |

| coverage | 92 | - | 98 | 91 | 92 | 87 | 90 | 77 | |

| bias | -2 | - | -1 | -3 | -3 | -2 | -2 | -6 | |

| length | 41 | - | 43 | 41 | 43 | 37 | 40 | 33 | |

| coverage | 86 | - | 92 | 85 | 97 | 83 | 85 | 84 | |

| bias | 0 | - | 2 | 0 | 0 | 1 | 1 | 0 | |

| length | 27 | - | 30 | 26 | 32 | 25 | 26 | 28 | |

| coverage | 94 | - | 94 | 92 | 93 | 90 | 92 | 93 | |

| bias | -1 | - | 1 | 0 | 0 | 0 | 1 | 0 | |

| length | 20 | - | 21 | 19 | 20 | 19 | 19 | 20 | |

Tables 1 and 2 present results. We find that every version of our adversarial estimator (i-v) achieves nominal coverage with and without sample splitting, as long as the sample size is large enough. In particular, (i-iv) achieve nominal coverage with , but (v) requires . The previous estimators (vi-viii) also achieve nominal coverage. Comparing entries across tables, we see that eliminating sample splitting always reduces the confidence interval length. For example, with , (i) has length 1.18 with sample splitting and length 0.94 without sample splitting; eliminating sample splitting reduces the confidence interval length by 20%. Another general trend is that our estimators have the shortest confidence intervals among those implemented—tied with the parametric estimator (vi), and shorter than (vii-viii). For example, with , (i) has length 0.94 without sample splitting while the lengths of (vi-viii) are at best 0.94, 0.99, and 1.03, respectively.

6.2 Adversarial non-Donsker estimation may improve coverage

In highly nonlinear simulations with and , our estimators may achieve nominal coverage where previous methods break down. In high dimensional simulations with and , our estimators may have lower bias and shorter confidence intervals. These gains seem to accrue from, simultaneously, using flexible function spaces for nuisance estimation and directly estimating the Riesz representer. These simulation designs are challenging, and only particular variations of our estimator work well.

| Previous work | This paper | |||||||

| Estimator | Prop. score | Adv. | Adversarial | |||||

| Function space | logistic | R.F. | Donsker | sparse | RKHS | Nystrom | R.F. | N.N. |

| coverage | 83 | 76 | - | 74 | 95 | 83 | 91 | 69 |

| bias | -12 | -1 | - | -7 | -4 | -3 | 0 | -8 |

| length | 54 | 29 | - | 33 | 53 | 32 | 39 | 35 |

| Previous work | This paper | |||||||

| Estimator | Prop. score | Adv. | Adversarial | |||||

| Function space | logistic | R.F. | Donsker | sparse | RKHS | Nystrom | R.F. | N.N. |

| coverage | 79 | - | 0 | 73 | 88 | 79 | 90 | 72 |

| bias | -11 | - | 50 | -7 | -4 | -4 | -2 | -8 |

| length | 47 | - | 44 | 30 | 36 | 30 | 37 | 33 |

Tables 3 and 4 present results from 100 simulations of the highly nonlinear design, with and without sample splitting, respectively. We find that our adversarial estimators (ii) and (iv) achieve near nominal coverage with sample splitting (95% and 91%) and slightly undercover without sample splitting (88% and 90%). For readability, we underline these estimators. None of the previous methods (vi-viii) achieve nominal coverage, with or without sample splitting, and they undercover more severely (at best 83%, 76%, and 0%).

| Previous work | This paper | |||||||

| Estimator | Prop. score | Adv. | Adversarial | |||||

| Function space | logistic | R.F. | Donsker | sparse | RKHS | Nystrom | R.F. | N.N. |

| coverage | 92 | 91 | - | 93 | 89 | 88 | 84 | 3 |

| bias | 44 | 16 | - | 8 | 6 | 6 | -7 | -35 |

| length | 214 | 93 | - | 88 | 72 | 73 | 126 | 6 |

| Previous work | This paper | |||||||

| Estimator | Prop. score | Adv. | Adversarial | |||||

| Function space | logistic | R.F. | Donsker | sparse | RKHS | Nystrom | R.F. | N.N. |

| coverage | 79 | - | 91 | 88 | 88 | 87 | 91 | 3 |

| bias | 2 | - | 16 | 1 | 8 | 9 | 26 | -33 |

| length | 64 | - | 94 | 75 | 76 | 78 | 184 | 3 |

Tables 5 and 6 present analogous results from the high dimensional design. We find that our adversarial estimator (i) achieves close to nominal coverage with sample splitting (93%) and slightly undercovers without sample splitting (88%). For readability, we underline this estimator. The previous estimators (vi-viii) also achieve close to nominal coverage (92%, 91%, 91%). Comparing the instances of near nominal coverage, we see that our estimator (i) has half of the bias (0.08 versus 0.44, 0.16, 0.16) and shorter confidence intervals (0.88 versus 2.14, 0.93, 0.94) compared to the previous estimators (vi-viii).

In summary, in simple designs, every variation of our estimator works well when sample sizes are large enough; in the highly nonlinear design, some variations of our estimator achieve nominal coverage where previous methods break down; in the high dimensional design, a variation of our estimator achieves nominal coverage with smaller bias and length than previous methods. The different simulation designs illustrate a virtue of our framework: our results in Sections 3 and 4 apply to every variation of our estimator in a unified manner. Our inferential guarantees hold whenever a given design and a given variation of our estimator together satisfy the complexity-rate robustness condition of Remark 3.

6.3 Heterogeneous effects by political environment

Finally, we extend the highly influential analysis of [Karlan and List, 2007] from parametric estimation to semiparametric estimation. To our knowledge, semiparametric estimation has not been used in this setting before; we provide an empirical contribution. We implement our estimators (i-v) as well as estimators from previous work (vi-vii) on real data. Compared to the parametric results of [Karlan and List, 2007], which do not allow for general nonlinearities, we find that our flexible approach both relaxes functional form restrictions and improves precision. Compared to semiparametric results obtained with previous methods, we find that our approach may improve precision by allowing for several machine learning function classes and by eliminating sample splitting.

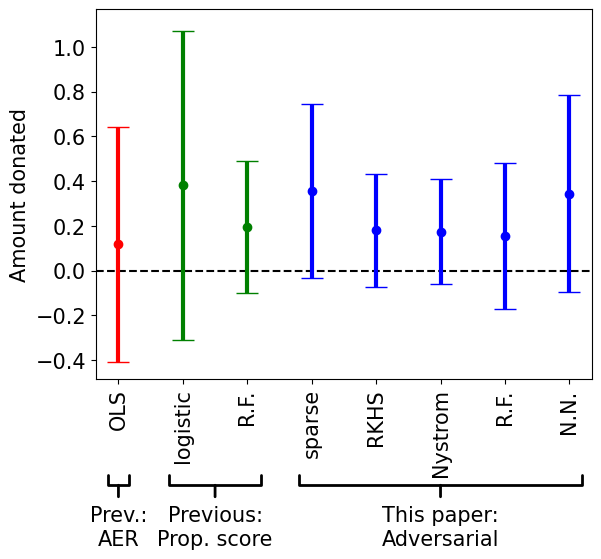

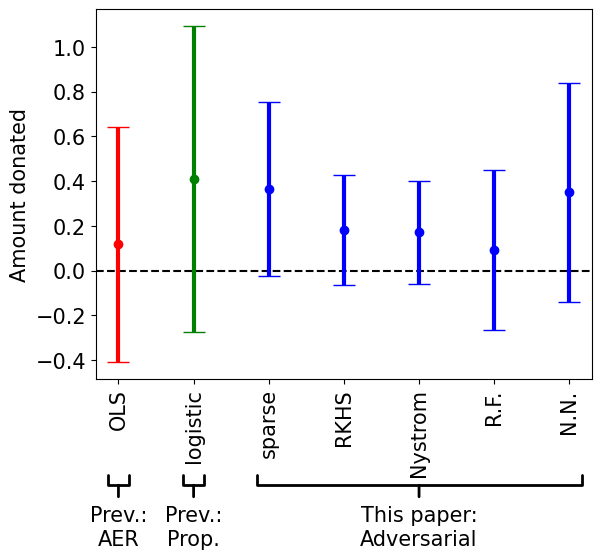

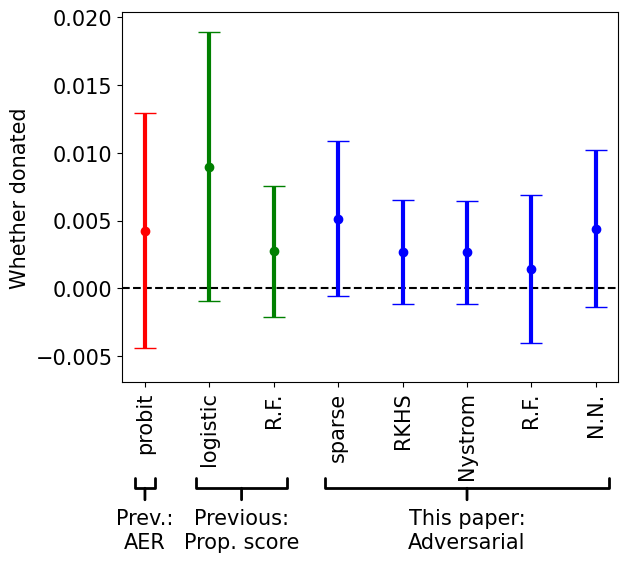

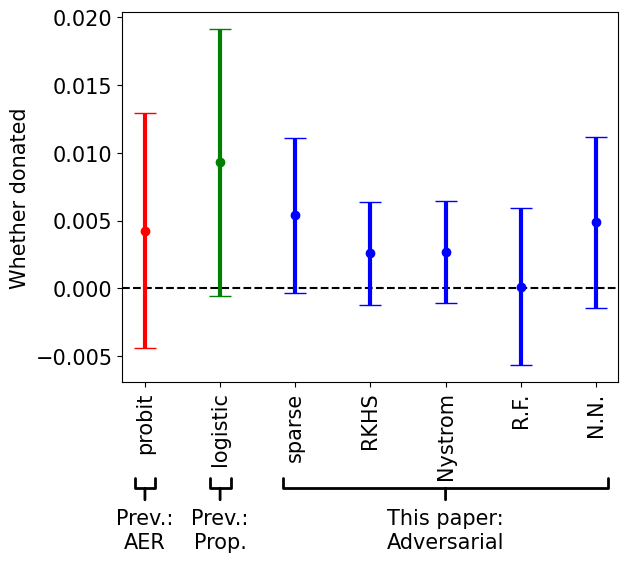

We study the heterogeneous effects, by political environment, of a matching grant on charitable giving in a large scale natural field experiment. We follow the variable definitions of [Karlan and List, 2007, Table 6]. In Figure 1, the outcome is dollars donated, while in Figure 2, indicates whether the household donated. The treatment indicates whether the household received a 1:1 matching grant as part of a direct mail solicitation. The covariates include political environment, previous contributions, and demographics. Altogether, and in our sample; see Appendix G.

A central finding of [Karlan and List, 2007] is that “the matching grant treatment was ineffective in [Democratic] states, yet quite effective in [Republican] states. The nonlinearity is striking…”, which motivates us to formalize a semiparametric estimand. The authors arrive at this conclusion with nonlinear but parametric estimation, focusing on the coefficient of the interaction between the binary treatment variable and a binary covariate which indicates whether the household was located in a state that voted for George W. Bush in the 2004 presidential election.555The authors write, “Upon interacting treatment with education, income, racial composition, age, household size, home ownership, number of children, and an urban/rural indicator, the coefficient on the interaction term [Republican]*treatment remains robust.” We generalize the interaction coefficient as follows. Denote the regression . We consider the parameter where . Intuitively, this parameter asks: how much more effective was the matching grant in Republican states compared to Democratic states? Its Riesz representer involves products and differences of the inverse propensity scores and , motivating our direct adversarial estimation approach. See Appendix G for derivations.

Figures 1 and 2 visualize point estimates and 95% confidence intervals for this semiparametric estimand. The former considers effects on dollars donated while the latter considers effects on whether households donated at all. Each figure presents results with and without sample splitting, using propensity score estimators from previous work (vi-vii) in green as well as the proposed adversarial estimators of this paper (i-v) in blue. As before, we leave entries blank when previous work does not provide theoretical justification. For comparison, we also present the parametric point estimate and confidence interval of [Karlan and List, 2007, Table 6, Column 9] in red.666The estimates in red slightly differ from [Karlan and List, 2007] since we drop observations receiving 2:1 and 3:1 matching grants and report the functional rather than the probit coefficient; see Appendix G.

Our estimates are stable across different estimation procedures and show that heterogeneity in the effect is positive, confirming earlier findings. The results are qualitatively consistent with [Karlan and List, 2007], who use a simpler parametric specification motivated by economic reasoning. Compared to the original parametric findings in red, which are not statistically significant, our findings in blue relax parametric assumptions and improve precision: our preferred confidence interval is more than 50% shorter in Figures 1 and 2. Compared to previous semiparametric methods in green, which require sample splitting to allow general machine learning, our preferred confidence interval is more than 20% shorter in Figures 1 and 2. In summary, our approach appears to improve model fit relative to previous parametric and semiparametric approaches. At the same time, it appears to recover some statistical power by eliminating sample splitting. As before, our results in Sections 3 and 4 apply to every variation of our estimator in a unified manner.

7 Discussion

This paper uses critical radius theory over general function spaces, in place of Donsker theory, to provide unified guarantees for nonparametric estimation of Riesz representers and semiparametric inference without sample splitting. The results in this paper complement and depart from previous work by allowing for non-Donsker spaces such as neural networks and random forests. Our analysis appears to forge new connections between statistical learning and semiparametrics. Simulations demonstrate that eliminating sample splitting may improve precision in some cases, and that non-Donsker approaches may achieve nominal coverage when Donsker approaches break down in other cases. Our method provides rigorous empirical evidence on heterogeneous effects of matching grants by political environment.

Appendix A Proof of main results

A.1 Adversarial estimation and fast rate

For convenience, throughout this appendix we use the notation

Thus We also lighten notation, setting .

Proof of Theorem 1.

We proceed in steps.

-

1.

Relating empirical and population regularization. By [Wainwright, 2019, Theorem 14.1], with probability , for our choice of , where upper bounds the critical radius of and are universal constants. Moreover, for any , with , we can consider the function , which also belongs to , since is star-convex. Thus we can apply the above lemma to this re-scaled function and multiply both sides by :

Thus overall, we have

(3) Hence with probability ,

Assuming that , the latter is at least

-

2.

Upper bounding centered empirical sup-loss. We now argue that

is small. By the definition of ,

(4) By [Foster and Syrgkanis, 2023, Lemma 11], the fact that is -Lipschitz with respect to the vector (since ) and by our choice of , where is an upper bound on the critical radii of and , with probability

We have invoked Assumption 1. Thus, if , we can apply the latter inequality for the function , which falls in , and then multiply both sides by (invoking the linearity of the operator with respect to ):

(5) -

3.

Lower bounding centered empirical sup-loss. First observe that Let . Suppose that and let . Since and is star-convex, we also have that . Thus

-

4.

Combining upper and lower bound. Combining the upper and lower bound on the centered population sup-loss we get that with probability , either or

We now control the last part. Since ,

We then conclude that

Dividing by gives

Thus either or the latter inequality holds. In both cases, the latter holds.

-

5.

Upper bounding population sup-loss at minimum. By Riesz representation,

-

6.

Concluding. In summary,

By the triangle inequality,

Choosing and using the fact that gives

A.2 Semiparametric inference without sample splitting

Proof of Theorem 2.

We proceed in steps.

-

1.

If and then we can further decompose as

The latter two terms in form an empirical process.

-

2.

Critical radius theory. We derive a concentration inequality similar to (5) for the empirical process. Let . Recall [Foster and Syrgkanis, 2023, Lemma 11], which holds for any loss that is Lipschitz in , and when : fix , then with probability ,

In order to place critical radius assumptions on the centered function spaces, we take and we take . Notice that the loss is Lipschitz since

so its derivative is, in absolute value, . Here, are bounded by hypothesis, while , have uniformly bounded ranges in . Hence for all and for all , with probability , invoking Assumption 1,

Next consider and . We apply the previous result for and , then multiply both sides by and . Hence for all and for all , with probability ,

-

3.

Bounding the empirical process. Applying this concentration inequality, with probability

Let . Then

If and , then

Thus as long as , we have that

-

4.

Collecting results. We conclude that By the central limit theorem, the final expression is asymptotically normal with asymptotic variance . ∎

Proof of Theorem 3.

Define the notation and We argue that Then remainder of the proof is identical to the proof of Theorem 2. For the desired property to hold, it suffices to show that . First we rewrite the differences

By Assumption 1 and boundedness, for some constant . Moreover, since, for every : ,

For every we have

Thus we get that In summary, it suffices to assume that . ∎

References

- [Abou-Moustafa and Szepesvári, 2019] Abou-Moustafa, K. and Szepesvári, C. (2019). An exponential Efron-Stein inequality for stable learning rules. In Algorithmic Learning Theory, pages 31–63. PMLR.

- [Ai and Chen, 2003] Ai, C. and Chen, X. (2003). Efficient estimation of models with conditional moment restrictions containing unknown functions. Econometrica, 71(6):1795–1843.

- [Aït-Sahalia and Lo, 1998] Aït-Sahalia, Y. and Lo, A. W. (1998). Nonparametric estimation of state-price densities implicit in financial asset prices. The Journal of Finance, 53(2):499–547.

- [Allen-Zhu et al., 2018] Allen-Zhu, Z., Li, Y., and Liang, Y. (2018). Learning and generalization in overparameterized neural networks, going beyond two layers. arXiv:1811.04918.

- [Andrews, 1994a] Andrews, D. W. (1994a). Asymptotics for semiparametric econometric models via stochastic equicontinuity. Econometrica, pages 43–72.

- [Andrews, 1994b] Andrews, D. W. (1994b). Empirical process methods in econometrics. Handbook of Econometrics, 4:2247–2294.

- [Anthony and Bartlett, 2009] Anthony, M. and Bartlett, P. L. (2009). Neural network learning: Theoretical foundations. Cambridge University Press.

- [Arjovsky et al., 2017] Arjovsky, M., Chintala, S., and Bottou, L. (2017). Wasserstein generative adversarial networks. In International Conference on Machine Learning, pages 214–223. PMLR.

- [Athey et al., 2018] Athey, S., Imbens, G. W., and Wager, S. (2018). Approximate residual balancing: Debiased inference of average treatment effects in high dimensions. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80(4):597–623.

- [Athey et al., 2019] Athey, S., Tibshirani, J., and Wager, S. (2019). Generalized random forests. The Annals of Statistics, 47(2):1148–1178.

- [Avagyan and Vansteelandt, 2021] Avagyan, V. and Vansteelandt, S. (2021). High-dimensional inference for the average treatment effect under model misspecification using penalized bias-reduced double-robust estimation. Biostatistics & Epidemiology, pages 1–18.

- [Bansal and Viswanathan, 1993] Bansal, R. and Viswanathan, S. (1993). No arbitrage and arbitrage pricing: A new approach. The Journal of Finance, 48(4):1231–1262.

- [Bartlett et al., 2005] Bartlett, P. L., Bousquet, O., and Mendelson, S. (2005). Local Rademacher complexities. The Annals of Statistics, 33(4):1497–1537.

- [Bartlett et al., 2019] Bartlett, P. L., Harvey, N., Liaw, C., and Mehrabian, A. (2019). Nearly-tight VC-dimension and pseudodimension bounds for piecewise linear neural networks. Journal of Machine Learning Research, 20:63–1.

- [Belloni et al., 2012] Belloni, A., Chen, D., Chernozhukov, V., and Hansen, C. (2012). Sparse models and methods for optimal instruments with an application to eminent domain. Econometrica, 80(6):2369–2429.

- [Belloni et al., 2017] Belloni, A., Chernozhukov, V., Fernández-Val, I., and Hansen, C. (2017). Program evaluation and causal inference with high-dimensional data. Econometrica, 85(1):233–298.

- [Belloni et al., 2014a] Belloni, A., Chernozhukov, V., and Kato, K. (2014a). Uniform post-selection inference for least absolute deviation regression and other Z-estimation problems. Biometrika, 102(1):77–94.

- [Belloni et al., 2014b] Belloni, A., Chernozhukov, V., and Wang, L. (2014b). Pivotal estimation via square-root Lasso in nonparametric regression. The Annals of Statistics, 42(2):757–788.

- [Benkeser et al., 2017] Benkeser, D., Carone, M., Laan, M. V. D., and Gilbert, P. B. (2017). Doubly robust nonparametric inference on the average treatment effect. Biometrika, 104(4):863–880.

- [Bennett et al., 2019] Bennett, A., Kallus, N., and Schnabel, T. (2019). Deep generalized method of moments for instrumental variable analysis. In Advances in Neural Information Processing Systems, pages 3559–3569.

- [Bickel, 1982] Bickel, P. J. (1982). On adaptive estimation. The Annals of Statistics, pages 647–671.

- [Bickel et al., 1993] Bickel, P. J., Klaassen, C. A., Ritov, Y., and Wellner, J. A. (1993). Efficient and adaptive estimation for semiparametric models, volume 4. Johns Hopkins University Press.

- [Blundell et al., 2007] Blundell, R., Chen, X., and Kristensen, D. (2007). Semi-nonparametric IV estimation of shape-invariant Engel curves. Econometrica, 75(6):1613–1669.

- [Bousquet and Elisseeff, 2002] Bousquet, O. and Elisseeff, A. (2002). Stability and generalization. Journal of Machine Learning Research, 2:499–526.

- [Celisse and Guedj, 2016] Celisse, A. and Guedj, B. (2016). Stability revisited: New generalisation bounds for the leave-one-out. arXiv:1608.06412.

- [Chan et al., 2016] Chan, K. C. G., Yam, S. C. P., and Zhang, Z. (2016). Globally efficient non-parametric inference of average treatment effects by empirical balancing calibration weighting. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 78(3):673–700.

- [Chen et al., 2023] Chen, L., Pelger, M., and Zhu, J. (2023). Deep learning in asset pricing. Management Science. Advance online publication. https://doi.org/10.1287/mnsc.2023.4695.

- [Chen and Christensen, 2018] Chen, X. and Christensen, T. M. (2018). Optimal sup-norm rates and uniform inference on nonlinear functionals of nonparametric IV regression. Quantitative Economics, 9(1):39–84.

- [Chen et al., 2003] Chen, X., Linton, O., and Van Keilegom, I. (2003). Estimation of semiparametric models when the criterion function is not smooth. Econometrica, 71(5):1591–1608.

- [Chen and Ludvigson, 2009] Chen, X. and Ludvigson, S. C. (2009). Land of addicts? An empirical investigation of habit-based asset pricing models. Journal of Applied Econometrics, 24(7):1057–1093.

- [Chen and Pouzo, 2009] Chen, X. and Pouzo, D. (2009). Efficient estimation of semiparametric conditional moment models with possibly nonsmooth residuals. Journal of Econometrics, 152(1):46–60.

- [Chen and Pouzo, 2012] Chen, X. and Pouzo, D. (2012). Estimation of nonparametric conditional moment models with possibly nonsmooth generalized residuals. Econometrica, 80(1):277–321.

- [Chen and Pouzo, 2015] Chen, X. and Pouzo, D. (2015). Sieve, Wald, and QLR inferences on semi/nonparametric conditional moment models. Econometrica, 83(3):1013–1079.

- [Chernozhukov et al., 2018] Chernozhukov, V., Chetverikov, D., Demirer, M., Duflo, E., Hansen, C., Newey, W., and Robins, J. (2018). Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21(1).

- [Chernozhukov et al., 2022a] Chernozhukov, V., Escanciano, J. C., Ichimura, H., Newey, W. K., and Robins, J. M. (2022a). Locally robust semiparametric estimation. Econometrica, 90(4):1501–1535.

- [Chernozhukov et al., 2021] Chernozhukov, V., Newey, W. K., Quintas-Martinez, V., and Syrgkanis, V. (2021). Automatic debiased machine learning via neural nets for generalized linear regression. arXiv:2104.14737.

- [Chernozhukov et al., 2022b] Chernozhukov, V., Newey, W. K., and Singh, R. (2022b). Automatic debiased machine learning of causal and structural effects. Econometrica, 90(3):967–1027.

- [Chernozhukov et al., 2022c] Chernozhukov, V., Newey, W. K., and Singh, R. (2022c). De-biased machine learning of global and local parameters using regularized Riesz representers. The Econometrics Journal, 25(3):576–601.

- [Christensen, 2017] Christensen, T. M. (2017). Nonparametric stochastic discount factor decomposition. Econometrica, 85(5):1501–1536.

- [Darolles et al., 2011] Darolles, S., Fan, Y., Florens, J.-P., and Renault, E. (2011). Nonparametric instrumental regression. Econometrica, 79(5):1541–1565.

- [Daskalakis et al., 2017] Daskalakis, C., Ilyas, A., Syrgkanis, V., and Zeng, H. (2017). Training GANs with optimism. arXiv:1711.00141.

- [De Vito and Caponnetto, 2005] De Vito, E. and Caponnetto, A. (2005). Risk bounds for regularized least-squares algorithm with operator-value kernels. Technical report, MIT CSAIL.

- [Dikkala et al., 2020] Dikkala, N., Lewis, G., Mackey, L., and Syrgkanis, V. (2020). Minimax estimation of conditional moment models. In Advances in Neural Information Processing Systems. Curran Associates Inc.

- [Du et al., 2018] Du, S. S., Zhai, X., Poczos, B., and Singh, A. (2018). Gradient descent provably optimizes over-parameterized neural networks. arXiv:1810.02054.

- [Elisseeff and Pontil, 2003] Elisseeff, A. and Pontil, M. (2003). Leave-one-out error and stability of learning algorithms with applications. NATO Science Series, III: Computer and Systems Sciences, 190:111–130.

- [Farrell et al., 2021] Farrell, M. H., Liang, T., and Misra, S. (2021). Deep neural networks for estimation and inference. Econometrica, 89(1):181–213.

- [Foster and Syrgkanis, 2023] Foster, D. J. and Syrgkanis, V. (2023). Orthogonal statistical learning. The Annals of Statistics, 51(3):879–908.

- [Freund and Schapire, 1999] Freund, Y. and Schapire, R. E. (1999). Adaptive game playing using multiplicative weights. Games and Economic Behavior, 29(1):79–103.

- [Ghassami et al., 2022] Ghassami, A., Ying, A., Shpitser, I., and Tchetgen Tchetgen, E. (2022). Minimax kernel machine learning for a class of doubly robust functionals with application to proximal causal inference. In International Conference on Artificial Intelligence and Statistics, pages 7210–7239. PMLR.

- [Goodfellow et al., 2014] Goodfellow, I., Pouget-Abadie, J., Mirza, M., Xu, B., Warde-Farley, D., Ozair, S., Courville, A., and Bengio, Y. (2014). Generative adversarial nets. Advances in Neural Information Processing Systems, 27:2672–2680.

- [Hainmueller, 2012] Hainmueller, J. (2012). Entropy balancing for causal effects: A multivariate reweighting method to produce balanced samples in observational studies. Political Analysis, 20(1):25–46.

- [Hansen and Jagannathan, 1997] Hansen, L. P. and Jagannathan, R. (1997). Assessing specification errors in stochastic discount factor models. The Journal of Finance, 52(2):557–590.

- [Hardt et al., 2016] Hardt, M., Recht, B., and Singer, Y. (2016). Train faster, generalize better: Stability of stochastic gradient descent. In International Conference on Machine Learning, pages 1225–1234. PMLR.

- [Hasminskii and Ibragimov, 1979] Hasminskii, R. Z. and Ibragimov, I. A. (1979). On the nonparametric estimation of functionals. In Prague Symposium on Asymptotic Statistics, volume 473, pages 474–482. North-Holland Amsterdam.

- [Haussler, 1995] Haussler, D. (1995). Sphere packing numbers for subsets of the Boolean -cube with bounded Vapnik-Chervonenkis dimension. Journal of Combinatorial Theory, Series A, 69(2):217–232.

- [Hirshberg et al., 2019] Hirshberg, D. A., Maleki, A., and Zubizarreta, J. R. (2019). Minimax linear estimation of the retargeted mean. arXiv:1901.10296.

- [Hirshberg and Wager, 2021] Hirshberg, D. A. and Wager, S. (2021). Augmented minimax linear estimation. The Annals of Statistics, 49(6):3206–3227.

- [Hsieh et al., 2019] Hsieh, Y.-G., Iutzeler, F., Malick, J., and Mertikopoulos, P. (2019). On the convergence of single-call stochastic extra-gradient methods. arXiv:1908.08465.

- [Imai and Ratkovic, 2014] Imai, K. and Ratkovic, M. (2014). Covariate balancing propensity score. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(1):243–263.

- [Javanmard and Montanari, 2014] Javanmard, A. and Montanari, A. (2014). Confidence intervals and hypothesis testing for high-dimensional regression. Journal of Machine Learning Research, 15(1):2869–2909.

- [Kaji et al., 2020] Kaji, T., Manresa, E., and Pouliot, G. (2020). An adversarial approach to structural estimation. arXiv:2007.06169.

- [Kale et al., 2011] Kale, S., Kumar, R., and Vassilvitskii, S. (2011). Cross-validation and mean-square stability. In International Conference on Supercomputing, pages 487–495.

- [Kallus, 2020] Kallus, N. (2020). Generalized optimal matching methods for causal inference. Journal of Machine Learning Research, 21(1):2300–2353.

- [Kallus et al., 2021] Kallus, N., Mao, X., and Uehara, M. (2021). Causal inference under unmeasured confounding with negative controls: A minimax learning approach. arXiv:2103.14029.

- [Karlan and List, 2007] Karlan, D. and List, J. A. (2007). Does price matter in charitable giving? evidence from a large-scale natural field experiment. American Economic Review, 97(5):1774–1793.

- [Khosravi et al., 2019] Khosravi, K., Lewis, G., and Syrgkanis, V. (2019). Non-parametric inference adaptive to intrinsic dimension. arXiv:1901.03719.

- [Kimeldorf and Wahba, 1971] Kimeldorf, G. and Wahba, G. (1971). Some results on Tchebycheffian spline functions. Journal of Mathematical Analysis and Applications, 33(1):82–95.

- [Klaassen, 1987] Klaassen, C. A. (1987). Consistent estimation of the influence function of locally asymptotically linear estimators. The Annals of Statistics, pages 1548–1562.

- [Koltchinskii and Panchenko, 2000] Koltchinskii, V. and Panchenko, D. (2000). Rademacher processes and bounding the risk of function learning. High Dimensional Probability II, 47:443–459.

- [Lecué and Mendelson, 2017] Lecué, G. and Mendelson, S. (2017). Regularization and the small-ball method II: Complexity dependent error rates. Journal of Machine Learning Research, 18(146):1–48.

- [Lecué and Mendelson, 2018] Lecué, G. and Mendelson, S. (2018). Regularization and the small-ball method I: Sparse recovery. The Annals of Statistics, 46(2):611–641.

- [Liao et al., 2020] Liao, L., Chen, Y.-L., Yang, Z., Dai, B., Wang, Z., and Kolar, M. (2020). Provably efficient neural estimation of structural equation model: An adversarial approach. In Advances in Neural Information Processing Systems. Curran Associates Inc.

- [Luedtke and Van der Laan, 2016] Luedtke, A. R. and Van der Laan, M. J. (2016). Statistical inference for the mean outcome under a possibly non-unique optimal treatment strategy. Annals of Statistics, 44(2):713.

- [Mansour and McAllester, 2000] Mansour, Y. and McAllester, D. A. (2000). Generalization bounds for decision trees. In Conference on Learning Theory, pages 69–74.

- [Maurer, 2016] Maurer, A. (2016). A vector-contraction inequality for rademacher complexities. In Algorithmic Learning Theory, pages 3–17. Springer.

- [Mishchenko et al., 2019] Mishchenko, K., Kovalev, D., Shulgin, E., Richtárik, P., and Malitsky, Y. (2019). Revisiting stochastic extragradient. arXiv:1905.11373.

- [Negahban et al., 2012] Negahban, S. N., Ravikumar, P., Wainwright, M. J., and Yu, B. (2012). A unified framework for high-dimensional analysis of -estimators with decomposable regularizers. Statistical Science, 27(4):538–557.

- [Newey, 1994] Newey, W. K. (1994). The asymptotic variance of semiparametric estimators. Econometrica, pages 1349–1382.