Approximating inverse cumulative distribution functions to produce approximate random variables

\datedayname \nth9 \monthname 2024)

For random variables produced through the inverse transform method, approximate random variables are introduced, which are produced by approximations to a distribution’s inverse cumulative distribution function. These approximations are designed to be computationally inexpensive, and much cheaper than library functions which are exact to within machine precision, and thus highly suitable for use in Monte Carlo simulations. The approximation errors they introduce can then be eliminated through use of the multilevel Monte Carlo method. Two approximations are presented for the Gaussian distribution: a piecewise constant on equally spaced intervals, and a piecewise linear using geometrically decaying intervals. The errors of the approximations are bounded and the convergence demonstrated, and the computational savings measured for C and C++ implementations. Implementations tailored for Intel and Arm hardwares are inspected, alongside hardware agnostic implementations built using OpenMP. The savings are incorporated into a nested multilevel Monte Carlo framework with the Euler-Maruyama scheme to exploit the speed ups without losing accuracy, offering speed ups by a factor of 5–7. These ideas are empirically extended to the Milstein scheme, and the non central distribution for the Cox-Ingersoll-Ross process, offering speed-ups of a factor of 250 or more.

- Keywords:

-

approximations, random variables, inverse cumulative distribution functions, random number generation, the Gaussian distribution, geometric Brownian motion, the Cox-Ingersoll-Ross process, the non central distribution, multilevel Monte Carlo, the Euler-Maruyama scheme, the Milstein scheme, and high performance computing.

- MSC subject classification:

-

65C10, 41A10, 65D15, 65C05, 62E17, 65Y20, 60H35, and 65C30.

1 Introduction

Random number generation is a fundamental building block of a wide range of computational tasks, in particular financial simulations [32, 7, 43, 72]. A frequent performance bottleneck is the generation of random numbers from a specific statistical distribution such as in Monte Carlo simulations. While computers have many excellent and fast implementations of random number generators for the uniform distribution on the interval , sampling random variables from a generic distribution is often computationally much more expensive.

We consider random variables produced using the inverse transform method [32], which enables sampling from any uni-variate distribution, and thus is very widely applicable. Additionally, the inverse transform method is crucial for quasi-Monte Carlo simulations [29, 47] as no samples are rejected and the low-discrepancy property is preserved [66]; such applications are common in financial simulations [43, 72]. Furthermore, we demonstrate how the inverse transform method is particularly well suited to analysis, and that it naturally provides a coupling mechanism for multilevel Monte Carlo applications for a range of stochastic processes, statistical distributions, and numerical schemes.

Our analysis focuses on the Gaussian distribution (a.k.a. the Normal distribution), and the motivations are threefold. Firstly, the distribution is representative of several continuous distributions, and due to the central limit theorem is often the limiting case. Secondly, it is analytically tractable and often admits exact results or is amenable to approximation. Lastly, it is ubiquitous in both academic analysis and scientific computation, with its role cemented within Itô calculus and financial simulations.

To produce Gaussian random variables will require the Gaussian distribution’s inverse cumulative distribution function. Constructing approximations accurate to machine precision has long been investigated by the scientific community [35, 54, 8, 69, 48, 27], where the de facto routine implemented in most libraries is by Wichura [69]. While some applications may require such accurate approximations, for many applications such accuracy is excessive and unnecessarily costly, as is typically the case in Monte Carlo simulations.

To alleviate the cost of exactly sampling from the Gaussian distribution, a popular circumvention is to substitute these samples with random variables with similar statistics. The bulk of such schemes follow a moment matching procedure, where the most well known is to use Rademacher random variables (which take the values with equal probability [44, page XXXII], giving rise to the weak Euler-Maruyama scheme), matching the mean and variance. Another is to sum twelve uniform random variables and subtract the mean [52, page 500], which also matches the mean and variance, and is still computationally cheap. The most recent work in this direction is by Müller et al. [51], who produce either a three or four point distribution, where the probability mass is positioned so the resulting distribution’s moments match the lowest few moments of the Gaussian distribution; as in this paper, they combine this with use of the multilevel Monte Carlo (MLMC) method but in a way which is not directly comparable.

The direction we follow in this paper is more closely aligned to the work by Giles et al. [31, 30], whose analysis proposes a cost model for producing the individual random bits constituting a uniform random number. They truncate their uniforms to a fixed number of bits and then add a small offset before using the inverse transform method. The nett result from this is to produce a piecewise constant approximation, where the intervals are all of equal width, and the values are the midpoint values of the respective intervals.

The work we present directly replaces random variables produced from the inverse transform method using the exact inverse cumulative distribution function, with those produced using an approximation to the inverse cumulative distribution function. While this is primarily motivated by computational savings, our framework encompasses the distributions produced from the various moment matching schemes and the truncated bit schemes.

Having a framework capable of producing various such distributions has several benefits. The first is that by refining our approximation, we can construct distributions resembling the exact distribution to an arbitrary fidelity. This allows for a trade-off between computational savings, and a lower degree of variance between the exact distribution and its approximation. This naturally introduces two tiers of simulations: those using a cheap but approximate distribution, and those using an expensive but near-exact distribution. This immediately facilitates the multilevel Monte Carlo setting of Giles [26], where fidelity and cost are balanced to minimise the computational time. As an example, we will see in section 4 that Rademacher random variables, while very cheap, are too crude to exploit any savings possible with multilevel Monte Carlo, whereas our higher fidelity approximations can fully exploit the possible savings.

The second benefit of our approach is that while the approximations are specified mathematically, their implementations are left unspecified. This flexibility facilitates constructing approximations which can be tailored to a specific hardware or architecture. We will present two approximations, whose implementations can gain speed by transitioning the work load from primarily using the floating point processing units to instead exploiting the cache hierarchy. Further to this, our approximations are designed with vector hardware in mind, and are non branching, and thus suitable for implementation using single instruction multiple data (SIMD) instructions, (including Arm’s new scalable vector extension (SVE) instruction set). Furthermore, for hardware with very large vectors, such as the wide vectors on Intel’s AVX-512 and Fujitsu’s Arm-based A64FX (such as those in the new Fugaku supercomputer), we demonstrate implementations unrivalled in their computational performance on the latest hardware. Previous work using low precision bit wise approximations targetted at reconfigurable field programmable gate arrays has previously motivated the related works by Brugger et al. [14], Omland et al. [55], and Cheung et al. [18].

We primarily focus our attention on the analysis and implementation of two approximations: a piecewise constant approximation using equally sized intervals, and a piecewise linear approximation on a geometric sequence of intervals. The former is an extension of the work by Giles et al. [31, theorem 1] to higher moments, while the latter is a novel analysis, capable of both the highest speeds and fidelities. Although we will demonstrate how these are incorporated into a multilevel Monte Carlo framework, the subsequent analysis is performed by Giles and Sheridan-Methven [28, 63] and omitted from this work.

Having outlined our approximation framework and the incorporation of approximate random variables within a nested multilevel Monte Carlo scheme, we quantify the savings a practitioner can expect. For a geometric Brownian motion process from the Black-Scholes model [11] using Gaussian random variables, savings of a factor of 5–7 are possible. Furthermore, for a Cox-Ingersoll-Ross process [19] using non-central random variables, savings of a factor of 250 or more are possible. These savings are benchmarked against the highly optimised Intel C/C++ MKL library for the Gaussian distribution, and against the CDFLIB library [13, 15] in C and Boost library [3] in C++ for the non-central distribution.

Section 2 introduces and analyses our two approximations, providing bounds on the error of the approximations. Section 3 discusses the production of high performance implementations, the code for which is collected into a central repository maintained by Sheridan-Methven [62, 61]. Section 4 introduces multilevel Monte Carlo as a natural application for our approximations, and demonstrates the possible computational savings. Section 5 extends our approximations to the non central distribution, representing a very expensive parametrised distribution which arises in simulations of the Cox-Ingersoll-Ross process. Lastly, section 6 presents the conclusions from this work.

2 Approximate Gaussian random variables

The inverse transform method [32, 2.2.1] produce univariate random variable samples from a desired distribution by first generating a uniform random variable on the unit interval , and then computing , where is the inverse of the distribution’s cumulative distribution function (sometimes called the percentile or quantile function). We will focus on sampling from the Gaussian distribution, whose inverse cumulative distribution function we denote by (some authors use ), and similarly whose cumulative distribution function and probability density function we denoted by and respectively.

Our key proposal is to use the inverse transform method with an approximation to the inverse cumulative distribution function. As the resulting distribution will not exactly match the desired distribution, we call random variables produced in this way approximate random variables, and those without the approximation as exact random variables for added clarity. In general, we will denote exact Gaussian random variables by and approximate Gaussian random variables by . The key motivation for introducing approximate random variables is that they are computationally cheaper to generate than exact random variables. Consequently, our key motivating criterion in forming approximations will be a simple mathematical construction, hoping this fosters fast implementations. As such there is a trade-off between simplicity and fidelity, where we will primarily be targetting simplicity.

In this section, we present two approximation types: a piecewise constant, and a piecewise linear. For both we will bound the error, focusing on their mathematical constructions and analyses. Their implementations and utilisation will be detailed in sections 3 and 4. Both analyses will share and frequently use approximations for moments and tail values of the Gaussian distribution, which we gather together in section 2.1. Thereafter, the piecewise constant and linear approximations are analysed in sections 2.2 and 2.3.

2.1 Approximating tail values and high order moments

We require bounds on the approximations of tail values and high order moments. We use the notation of Giles et al. [31] that denotes . Our key results are lemmas 2.1 and 2.2 which bound the tail values and high order moments. Lemma 2.1 is an extension of a similar result by Giles et al. [31, lemma 7], extended to give enclosing bounds. Similarly, lemma 2.2 is partly an extension of a result by Giles et al. [31, lemma 9], but extended to arbitrarily high moments rather than just the second. As such, neither of these lemmas are particularly noteworthy in themselves and their proofs resemble work by Giles et al. [31, appendix A]. Similarly, our resulting error bounds for the piecewise constant approximation in section 2.2 will closely resemble a related result by Giles et al. [31, theorem 1]. However, our main result for the piecewise linear approximation in section 2.3 is novel and will require these results, and thus we include them here primarily for completeness.

Lemma 2.1.

Defining , then for we have the bounds and for .

Proof.

. Integrating by parts using gives

which proves that and hence we obtain the first inequality.

For , and so . The inequality then gives

Inserting the upper bound into the left hand term, and the lower bound in the right hand term, gives the desired second inequality. ∎

Lemma 2.2.

For integers we have and as .

Proof.

Applying L’Hôpital’s rule gives

Similarly, applying L’Hôpital’s rule times gives

2.2 Piecewise constant approximations on equal intervals

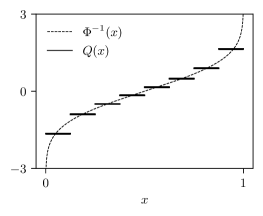

Mathematically it is straightforward to motivate a piecewise constant approximation as the simplest possible approximation to use, especially using equally spaced intervals. As the range of values will go from a continuous to a discrete set, we say the distribution has become quantised and denote our approximation as , where for a uniform random variable we have and . A preview of such an approximation is shown in figure 1(a), where the error will be measured using the norm .

Before presenting theorem 2.3, we can briefly comment on the error seen in figure 1(b). Specifically looking at the root mean squared error (RMSE), corresponding to the norm, we can see that increasing the number of intervals from 2 to gives a drop of in the RMSE. For our multilevel Monte Carlo applications in section 4, having approximately 1000 intervals gives a very good fidelity, whereas Rademacher random variables have a very low fidelity. Being able to achieve a reasonable fidelity from our approximation ensures that we achieve the largest portion of the possible computational savings offered by our approximations.

As we have already mentioned, the piecewise constant approximation is closely related to the resulting approximation produced by Giles et al. [31], whose approximation arises from considering uniform random variables truncated to a finite number of bits of precision. Thus our main result from this section, theorem 2.3, closely resembles a related result by Giles et al. [31, theorem 1]. To put our extension into context, we paraphrase the similar result from Giles et al. [31], which is that for a piecewise constant approximation using intervals, for some integer , then for constant values equal to each interval’s midpoint value they have . Our result from theorem 2.3 extends this to for , and numerous other possible constant values other than the midpoint’s. Our result enables us to increase the order of the error to arbitrarily high norms and is interesting in its own right. It shows that as the intervals become increasing small (corresponding to ), the dominant term effecting the error is the geometric decay due to the error in the two end intervals, and thus the convergence exists but is slower in higher norms, with the polynomial term being comparatively negligible (as we can see in figure 1(b)). Additionally, in the related analysis incorporating approximate random variables into a nested multilevel Monte Carlo framework by Giles and Sheridan-Methven [28, 63], their bounds on the variance of the multilevel Monte Carlo correction term (discussed more in section 4) rely on the existence of the error for . Hence, while this strengthening of the result may appear only slight, it is crucial for nested multilevel Monte Carlo.

We can now present our main result concerning piecewise constant approximations, namely theorem 2.3. In this we will leave the interval values largely unspecified, and later demonstrate in corollary 2.4 several choices fit within the scope of theorem 2.3.

Theorem 2.3.

Let a piecewise constant approximation use equally spaced intervals for some integer . Denote the intervals for where . On each interval the approximation constant is for . We assume there exists a constant independent of such that:

-

1.

for .

-

2.

for .

-

3.

.

Then for any even integer we have as .

Proof.

Defining for , then we have . We use condition (1) to reduce our considerations to the domain , where is strictly positive and convex, and thus obtain . As is convex, then from the intermediate value theorem there exists a such that . Noting that , then from the mean value theorem for any there exists an such that . Furthermore, as is monotonically decreasing in , then introducing we have . An identical argument follows for any giving the same bound. Using this to bound in our expression for gives

where the last bound comes from considering a translated integral. Changing integration variables the integral becomes , from which we can use lemma 2.2 to give

where the last bound follows from lemma 2.1. Turning our attention to the final interval’s contribution , then using Jensen’s inequality, condition (3), and lemmas 2.1 and 2.2 we obtain

Combining our two bounds for and into our expression for we obtain

where the coefficients inside the -notation are only a function of and not of . ∎

Corollary 2.4.

Proof.

As all three approximations are anti-symmetric about , and therefore all satisfy conditions (1, we consider the domain where and are both positive. Letting the interval lie in this domain, then from Jensen’s inequality and the law of iterated expectations we obtain

for any , where the last inequality is a standard result. Mirroring this result to the full domain , we can directly see that the moments of are uniformly bounded. Furthermore, as is increasing and convex in , then the value is an upper bound on and , and so these too have uniformly bounded moments.

It is immediately clear that all three choices satisfy condition 2) and the lower bound in 3). As is an upper bound for the other two choices, it will suffice to show that this satisfies the upper bound in 3). Inspecting the difference between the smallest value in the final interval, namely , and the average value , we obtain

where the first inequality follows from lemma 2.2, the second from lemma 2.1, and the last uses for . We bound the final term using lemma 2.1 for to give and therefore . ∎

We remark that the construction from corollary 2.4 is the same as the value used in the analysis of Giles et al. [31, (4)]. In any piecewise constant approximations we use, such as that in figure 1(a), we will use the constants defined by the construction from corollary 2.4. Furthermore, we can see that our bound from theorem 2.3 appears tight in figure 1(b).

2.3 Piecewise linear approximations on geometric intervals

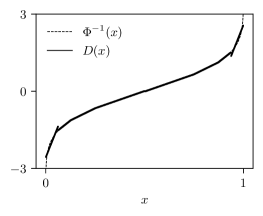

Looking at the piecewise constant approximation in figure 1(a), it is clear there are two immediate improvements that can be made. The first is to use a piecewise linear approximation, which is considerably more appropriate for the central region. Secondly, the intervals should not be of equal sizes, but denser near the singularities at either end. We will make both these modifications in a single step, where we will construct a piecewise linear approximation with geometrically decreasing intervals which are dense near the singularities. For brevity we will denote this just as the piecewise linear approximation. An example piecewise linear approximation using 8 intervals is shown in figure 2(a). The precise nature of the interval widths, and how the linear functions are fitted will be detailed shortly, but by direct comparison against figure 1(a) it is clear that the fidelity of a piecewise linear approximation is much better than the piecewise constant.

The main result from this section will be theorem 2.5, which will bound the error of our piecewise linear approximation. The proof will proceed in a similar fashion the proof of theorem 2.3, where we will bound the sum of the central intervals and the end intervals separately. For the central intervals we will use the Peano kernel theorem to bound the point wise error, and in the end intervals several results will be a mixture of exact results and bounds from lemmas 2.1 and 2.2.

Theorem 2.5.

For an approximation which is anti-symmetric about , with intervals in , we define the -th interval for and for some decay rate . Each interval uses a piecewise linear approximation for any . The gradient and intercept in each interval is set by the minimisation where is the set of all 1-st order polynomials. Then we have for any

Proof.

Considering the domain , we split the contribution into those from the intervals without the singularity, and that from the final interval with the singularity, where

where the factors of 2 correct for us only considering the lower half of the domain .

Beginning with the non-singular intervals, we express the pointwise error using the Peano kernel theorem [41, 57], which we will later bound. For notational simplicity, we denote the approximated function as , where , and a given interval as . The optimal linear approximation is for where and are functionals. The point wise error is a linear mapping acting on where . By construction annihilates linear functions, so the Peano kernel is for where we defined and similarly . The pointwise error is .

To determine the intercept and gradient, we use that they are optimal, and so the functional derivatives of with respect to and are zero, giving the simultaneous equations

It is important to notice that because we chose the norm, these are a set of linear simultaneous equations, and thus and are linear functionals, thus showing that is linear, (a requirement of the Peano kernel theorem). Evaluating these for the kernel function () gives

Thus, the pointwise error is

where to achieve the last equality we rescaled our interval and variables where . Taking the absolute value and applying Jensen’s inequality immediately gives

where for the first inequality we used that is maximal at the lower boundary, and for the second inequality we bound this by the maximum with respect to (which is at ). Using this expression for the pointwise error in our summation of the non-singular intervals gives (as )

We now consider the interval containing the singularity at 0, which has intercept and gradient and . These integrals can be calculated exactly (with a change of variables), where denoting we obtain

For the gradient, as the interval becomes ever smaller and , we can use lemma 2.1 to give

where in the first approximation we used . Interestingly, this means the range of values , and our approximation “flattens” relative to the interval as .

With the intercept and gradient in the singular interval known exactly, we define the two points and where the error is zero, where , and there are two as is concave in . Corresponding to these we define and , where . Thus in the singular interval we have

Using lemmas 2.1 and 2.2, then for the first of these integrals we obtain

and for the second integral we similarly obtain

Combining the results for the central intervals and the singular interval we obtain

where for the second equality we used lemma 2.1 in the limit . ∎

We can see from theorem 2.5 that the term comes from the central regions, and is reduced by taking , and the term is from the singular interval, and is reduced by taking . The key point of interest with this result is that the error from the central regions and the singular region is decoupled. In order to decrease the overall error, it is not sufficient to only increase the number of intervals (), which would only improve the error from the singular interval, but the decay rate must also be decreased (). The independence and interplay of these two errors is important for balancing the fidelity between the central and edge regions.

It is possible to generalise this construction and analysis to piecewise polynomial approximations, constructing the best approximation on each interval. We could also require the approximations to be continuous over the entire interval by turning our previous minimisation into a constrained minimisation, with a coupled set of linear constraints. While such a continuous approximation may be more aesthetically pleasing, it is of no practical consequence for the inverse transform method, and by definition will have a worse overall error than the discontinuous approximation from theorem 2.5, and thus we choose not to do this.

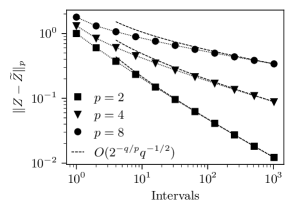

The errors from piecewise polynomial approximations for various polynomial orders and interval numbers are shown in figure 2(b), where we have set the decay rate . As we increase the number of intervals used, then for the piecewise linear function, the error plateaus to approximately for 16 intervals, which is approximately equal to the error for the piecewise constant approximation using intervals. Thus we can appreciate the vast increase in fidelity that the piecewise linear approximation naturally offers over the piecewise constant approximation. Furthermore, this plateau demonstrates that the central regions are limiting the accuracy of the approximation. Inspecting the approximation using 16 intervals in , we see that as we increase the polynomial order from linear to cubic there is a considerable drop in the error approximately equal to a factor of , where the piecewise cubic approximation is achieving errors of around . However, we see that increasing the polynomial order any further does not lead to any significant reduction in the error, indicating that in this regime it is the error in the singular interval which is dominating the overall error.

3 High performance implementations

Our motivation for presenting the piecewise constant and linear approximations was to speed up the inverse transform method, where the approximations were inherently simple in their constructions, with the suggestion that any implementations would likely be simple and performant. However, it is not obvious that the implementations from various software libraries, especially heavily optimised commercial libraries such as Intel’s Maths Kernel Library (MKL), should be slow. In this section, we will mention how most libraries implement these routines, and why many are inherently ill posed for modern vector hardware. Our two approximations capitalise on the features where most libraries stumble, avoiding division and conditional branching, which will be the key to their success. We give a brief overview of their implementations in C and showcase their superior speed across Intel and Arm hardwares. While we will briefly outline the implementations here in moderate detail, a more comprehensive suite of implementations and experiments, including Intel AVX-512 and Arm SVE specialisations, are hosted in a centralised repository by Sheridan-Methven [62].

3.1 The shortcomings in standard library implementations

Several libraries providers, both open source and commercial, offer implementations of the inverse Gaussian cumulative distribution function, (Intel, NAG, Nvidia, MathWorks, Cephes, GNU, Boost, etc.). The focus of these implementations is primarily ensuring near machine precision is achieved for all possible valid input values, and handling errors and edge cases appropriately. While some offer single precision implementations, most offer (or default to) double precision, and to achieve these precisions algorithms have improved over the years [35, 54, 8, 69, 48, 27]. The most widely used is by Wichura [69], which is used in GNU’s scientific library (GSL) [25], the Cephes library [50] (used by Python’s SciPy package [68]), and the NAG library [53] (NAG uses a slight modification).

These implementations split the function into two regions: an easy central region, and the difficult tail regions. Inside the central region a rational Padé approximation is used with seventh order polynomials [69]. In the tail regions, the square root of the logarithm is computed, and then a similar rational approximation performed on this. While these are very precise routines, they have several shortcomings with respect to performance.

The first shortcoming is the division operation involved in computing the rational approximation. Division is considerably more expensive than addition or multiplication, and with a much higher latency [71, 24]. Thus, for the very highest performance, avoiding division is preferable. (The implementation by Giles [27] already capitalises on this). Similarly, taking logarithms and square roots is expensive, making the tail regions very expensive, and so are best avoided too.

The second short coming is that the routine branches: requesting very expensive calculations for infrequent tail values, and less expensive calculations for more frequent central values. Branching is caused by using “if-else” conditions, but unfortunately this often inhibits vectorisation, resulting in compilers being unable to issue single instruction multiple data (SIMD) operations [67]. Even if a vectorised SIMD implementation is produced, typically the results from both branches are computed, and the correct result selected a posteriori by predication/masking. Thus, irrespective of the input, both the very expensive and less expensive calculations may be performed, resulting in the relatively infrequent tail values producing a disproportionately expensive overall calculation. This effect is commonly known as warp divergence in GPU programs, and in our setting we will call this vector divergence. The wider the vector and the smaller the data type, (and thus the greater the amount of vector parallelisation), the worse the impact of vector divergence. Noting that half precision uses only 16 bits, both Intel’s AVX-512 and Fujitsu’s A64FX are 512 bits wide, and Arm’s SVE vectors can be up to 2048 bits [56, 65], the degree of vector parallelisation can be substantial, and the impact of conditional branching becomes evermore crippling as vector parallelisation increases.

In light of these two shortcomings, we will see our approximations can be implemented in a vectorisation friendly manner which avoids conditional branching and are homogenous in their calculations. Furthermore, their piecewise constant and polynomial designs avoid division operations, and only require addition, multiplication, and integer bit manipulations, and thus result in extremely fast executables. We will see that our piecewise constant approximation will rely on the high speed of querying the cache. Furthermore, for the piecewise linear approximation using a decay rate and 16 intervals, then in single precision all the coefficients can be held in 512 bit wide vector registers, bypassing the need to even query the cache, and thus are extremely fast provided the vector widths are sufficiently large.

3.2 Implementing the piecewise constant approximation

Splitting the domain into the intervals zero indexed by , the values for each interval are easily computed a priori, and stored in a lookup table. An example of how this looks in C is shown in code 1, where we use OpenMP (omp.h) to signal to the compiler that the for loop is suitable for vectorisation. This relies on typecasting to an integer, where any fractional part is removed. The benefit to such an implementation is that on modern chips a copy of the lookup table can readily fit within either the L1 or L2 caches, where 1024 values stored in 64 bit double precision consume . As an example, an Intel Skylake Xeon Gold 6140 CPU has L1 and L2 caches which are and respectively, and thus the lookup table can exploit the fast speeds of the L1 cache, which typically has latencies of 2–5 clock cycles.

3.3 Implementing the piecewise linear approximation

The piecewise linear approximation is a bit more involved than the piecewise constant approximation. Not only do we have a polynomial to evaluate (albeit only linear), but the varying widths of the intervals means identifying which interval a given value corresponds to is more involved. Once the appropriate interval’s polynomial’s coefficients are found, evaluating the polynomial is trivial, where the linear polynomial can be evaluated using a fused multiply and add (FMA) instruction. Higher order polynomials can be similarly computed (e.g. with Horner’s rule).

The primary challenge is determining which interval a given value corresponds to based on the construction from theorem 2.5 for a given decay rate . As floating point numbers are stored in binary using their sign, exponent, and mantissa, the natural choice most amenable for computation is , which we call the dyadic rate, producing the dyadic intervals shown in table 1. From table 1, we notice the intervals are only dense near the singularity at 0, but not at 1. This is not problematic, as we said in theorem 2.5 that the approximation is anti-symmetric about , and thus we can use the intervals in , and if our input value is within , it is straight forward to simply negate the value computed for the input reflected about (equivalent to using the inverse complementary cumulative distribution function).

| Index | 0 | 1 | 2 | ||||

|---|---|---|---|---|---|---|---|

| Interval |

Such an implementation can handle any value in , but unfortunately is not included within this. While a mathematician may say the individual value has zero measure, from a computational perspective such a value is perfectly feasible input, and quite likely to appear in any software tests. Thus our implementation will correctly handle this value. The reader will notice that when we reflect an input value about by using , then the value will not be in any of the intervals indexed between 1 and in table 1, but remains in the interval indexed by 0. Thus in our later implementations, the arrays of coefficients will always hold as their first entry (index 0) zero values () so is correctly handled. We found during the development of the implementation, being able to correctly handle this value is of considerable practical importance, so we encourage practitioners to also correctly handle this value.

If we are using the dyadic decay rate, then the interval an input belongs to is . However, to compute this we need not take any logarithms, which are expensive to compute. We can obtain the same result by reading off the exponent bits in the floating point representation, treating these as an integer, and then correcting for the exponent bias. This only involves simple bit manipulations, and interpreting the bits in a floating point representation as an integer. In C this is a technique called type punning, and can be achieved either by pointer aliasing, using a union, or using specialised intrinsic functions. Of these, pointer aliasing technically breaks the strict aliasing rule in C (and C++) [40, 6.5.2.3] [64, pages 163–164]. Similarly, type punning with a union in C89 is implementation defined, whereas in C11 the bits are re-interpreted as desired. In the presented implementation we will leave this detail undefined and just use a macro to indicate the type punning. (The implementation approximating the Gaussian distribution uses pointer aliasing, whereas the later approximation to the non central distribution in section 5 uses a union, to demonstrate both possibilities [62]).

Overall then, the general construction from theorem 2.5 is given in algorithm 1. Furthermore, a single precision C implementation is shown in code 2, where we assume the single precision floats are stored in IEEE 32 bit floating point format [39].

The reason why we decide to implement the approximation in single precision using coefficient arrays of 16 entries is because each requires only 512 bits ( bits) to store all the possible values for a given monomial’s coefficient. The significance of 512 bits cannot be overstated, as it is the width of an AVX-512 and A64FX vector register. Thus, instead of querying the cache to retrieve the coefficients, they can be held in vector registers, bypassing the cache entirely, and achieving extremely fast speeds. Recognising the coefficients can be stored in a single coalesced vector register is currently largely beyond most compilers’ capabilities using OpenMP directives and compiler flags alone. However, in the repository by Sheridan-Methven [62], specialised implementations using Intel vector intrinsics and Arm inline assembly code achieve this, obtaining the ultimate in performance.

3.4 Performance of the implementations

Both the piecewise constant and linear implementations in codes 1 and 2 are non branching, vector capable, and use only basic arithmetic and bit wise operations, and thus we anticipate their performance should be exceptionally good. Indeed, their performance, along with several other implementations’, is shown in table 2, with experiments performed on an Intel Skylake Xeon Gold CPU and an Arm based Cavium ThunderX2 [62].

| Description | Implementation | Hardware | Compiler | Precision | Clock cycles |

|---|---|---|---|---|---|

| Cephes [50] | — | Intel | icc | Double | |

| GNU GSL | — | Intel | icc | Double | |

| ASA241 [69, 16] | — | Intel | icc | Single | |

| Giles [27] | — | Intel | icc | Single | |

| Intel (HA) | MKL VSL | Intel | icc | Double | |

| Intel (LA) | MKL VSL | Intel | icc | Double | |

| Intel (HA) | MKL VSL | Intel | icc | Single | |

| Intel (LA) | MKL VSL | Intel | icc | Single | |

| Piecewise constant | OpenMP | Arm | armclang | Double | |

| Piecewise constant | OpenMP | Intel | icc | Double | |

| Piecewise cubic | OpenMP | Intel | icc | Single | |

| Piecewise cubic | Intrinsics | Intel | icc | Single | |

| Piecewise linear | Intrinsics | Intel | icc | Single | |

| Read and write | — | Intel | icc | Single |

Looking at the results from table 2, of all of these, the piecewise linear implementation using Intel vector intrinsics achieves the very fastest speeds, closely approaching the maximum speed of just reading and writing. Unsurprisingly, the freely available implementations from Cephes and GSL are not competitive with the commercial offerings from Intel. Nonetheless, even in single precision, our approximations, on Intel hardware, consistently beat the performance achieved from the Intel high accuracy (HA) or low accuracy (LA) offerings. Comparing the high accuracy Intel offering and the piecewise linear implementation, there stands to be a speed up by a factor of seven by switching to our approximation. These results vindicate our efforts, and that our simple approximations offer considerable speed improvements. It is also needless to say, that compared to the freely available open source offerings, the savings become even more significant.

4 Multilevel Monte Carlo

One of the core use cases for our high speed approximate random variables is in Monte Carlo applications. Frequently, Monte Carlo is used to estimate expectations of the form of functionals which act on solutions of stochastic differential equations of the form for given drift and diffusion processes and . The underlying stochastic process is itself usually approximated by some using a numerical method, such as the Euler-Maruyama or Milstein schemes [7, 44, 45]. These approximation schemes simulate the stochastic process from time to over time steps of size , where the incremental update at the -th iteration requires a Gaussian random variable to simulate the increment to the underlying Wiener process , where . Such types of Monte Carlo simulations are widespread, with the most famous application being to price financial options.

Approximate random variables come into this picture by substituting the exact random variable samples in the numerical scheme with approximate ones. This facilitates running faster simulations, at the detriment of introducing error. However, using the multilevel Monte Carlo method [26], this error can be compensated for with negligible cost. Thus, the speed improvements offered by switching to approximate random variables can be largely recovered, and the original accuracy can be maintained. A detailed inspection of the error introduced from incorporating approximate Gaussian random variables into the Euler-Maruyama scheme and the associated multilevel Monte Carlo analysis is presented by Giles and Sheridan-Methven [28, 63]. As such, we will only briefly review the key points of the setup, and focus on detailing the resultant computational savings that can be expected from using approximate random variables.

For the Euler-Maruyama scheme, the unmodified version using exact Gaussian random variables produces an approximation , whereas the modified scheme using approximate random variables produces an approximation , where the two schemes are respectively

where .

The regular multilevel Monte Carlo construction varies the discretisation between two levels, producing fine and coarse simulations. The functional would act on each path simulation, producing the fine and coarse approximations and respectively. If the path simulation uses the exact random variables we denote these as and , and alternatively if it uses approximate random variables as and . In general there may be multiple tiers of fine and coarse levels, so we use to index these, where increasing values of correspond to finer path simulations. Thus for a given we have and , and similarly and . If we have levels and use the convention , then Giles and Sheridan-Methven [28] suggest the nested multilevel Monte Carlo

where the first approximation is the regular Monte Carlo procedure [32], the first equality is the usual multilevel Monte Carlo decomposition [26], and the final equality is the nested multilevel Monte Carlo framework [28, 63]. Giles and Sheridan-Methven [28, 63] show that the two way differences in the regular and nested multilevel Monte Carlo settings behave almost identically, and the main result of their analysis is determining the behaviour of the final four way difference’s variance [28, lemmas 4.10 and 4.11] [63, corollaries 6.2.6.2 and 6.2.6.3]. They find that for Lipschitz continuous and differentiable functionals

for any such that , and that for Lipschitz continuous but non-differentiable functionals that

for any . We can see that in all circumstances covered by their analysis that there is a dependence on the approximation error for some norm where .

4.1 Expected time savings

The regular multilevel estimator is

and the nested multilevel estimator is

where , , and are the number of paths generated, each with a computational time cost of , , and , and variance , , and respectively, and all terms with the same suffix are computed using the same uniform random numbers. Each of these estimators will have an error due to the finite number of paths used and the approximation scheme employed. The total error arising from these two factors is commonly referred to as the variance bias trade-off, where the mean squared error (MSE) of an estimator is given by [32, page 16]. Setting the desired MSE to and choosing the maximum simulation fidelity such that we just satisfy , then we can derive an expression for the total computational time . Forcing to be minimal is achieved by performing a constrained minimisation with an objective function . Considering the estimator , the corresponding objective function is , where is a Lagrange multiplier enforcing the constraint . Treating the number of paths as a continuous variable this is readily minimised to give

where the minimal number of paths required are given by

and hence an overall saving of

For modest fidelity approximations where , the term measures the potential time savings, and the term assesses the efficiency of realising these savings. A balance needs to be achieved, and the approximations should be sufficiently fast so there is the potential for large savings, but of a sufficient fidelity so the variance of the expensive four way difference is considerably lower than the variance of the cheaper two way difference.

Although we have estimates for the costs of each estimator from table 2, the variance will depend on the stochastic process being simulated, the numerical method being used, and the approximation employed. To make our estimates more concrete and quantify the possible variance reductions, we consider a geometric Brownian motion where and for two strictly positive constants and , where we take , , , and [26, 6.1]. The coarse level’s Weiner increments are formed by pair wise summing the fine level’s (which uses the fine time increment ). Importantly, the uniform random variable samples producing the exact Gaussian random variables will be the same as those used for producing the approximate Gaussian random variables, ensuring a tight coupling. Thus, for some approximation , such as those from section 2, for a single uniform sample , then and , where the is the same for both of these.

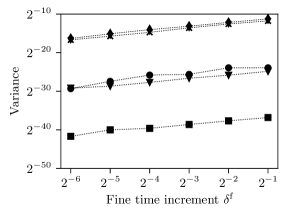

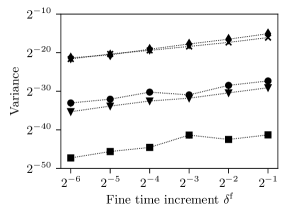

The variance for the various multilevel terms for different time increments for the Euler-Maruyama and Milstein schemes are shown in figure 3 for various approximations. We consider the underlying process itself, corresponding to the functional . The piecewise constant approximation uses 1024 intervals, which from figure 1(b) has an RMSE of approximately . The piecewise linear approximation uses 15 dyadic intervals (16 coefficients stored to correctly handle ), which from figure 2(b) has a similar RMSE of approximately . The piecewise cubic approximation uses the same number of intervals, which from figure 2(b) has an RMSE of approximately . We also include the approximation using Rademacher random variables for comparison.

We can see from figure 3 that the two way differences exhibit the usual strong convergence order and 1 of the Euler-Maruyama and Milstein schemes, as expected [44]. Furthermore, as the functional is differentiable and Lipschitz continuous, this strong convergence rate is preserved for the four way differences [28, 63]. Giles and Sheridan-Methven [28, 63] derive this result for the Euler-Maruyama scheme, but the analysis for the Milstein scheme remains an open problem. Aside from this, the key point to note from figure 3 is the substantial drop in the variance between the two way and four way variances using our approximations. This drop in the variance is large for the piecewise constant and linear approximations, and huge for the piecewise cubic approximation. The approximation using Rademacher random variables has only a very small drop in variance.

Estimating the best cost savings seen compared to Intel (HA) from table 2, the variance reductions from figure 3(a), and using the simplifications and , then the estimated speed ups and their efficiencies are shown in table 3. For the Rademacher random variables we use the optimistic approximations that this achieves the maximum speed set by reading and writing and that it offers a variance reduction of . We can see from this that the piecewise linear approximation would give the largest savings, although the savings from the piecewise constant and cubic approximations are quite similar. Notice that while the piecewise cubic is achieving near perfect efficiency, its cost savings are not substantial enough to beat the marginally less efficient piecewise linear approximation which offers the larger potential savings. For all of our approximations the four way difference simulations are required very infrequently. Lastly, while the Rademacher random variables may offer the best time savings, the absence of any considerable variance reduction caused by the extremely low fidelity approximation results in a very inefficient multilevel scheme, demonstrating the balance required between speed and fidelity.

| Approximation | Speed up | ||||||

|---|---|---|---|---|---|---|---|

| Rademacher | 9 | 0.86 | (9.5%) | 3.24 | 1 | .4 | |

| Piecewise constant | 6 | 5.66 | (94.4%) | 1.03 | 240 | ||

| Piecewise linear | 7 | 6.70 | (95.7%) | 1.02 | 360 | ||

| Piecewise cubic | 5 | 5.00 | (99.9%) | 1.00 | 14000 | ||

These cost savings are idealised in the respect that we have attributed the cost entirely to the generation of the random numbers. While this is quite a common assumption, the validity of this assumption will diminish the faster the approximations become, as the basic cost of the other arithmetic operations becomes significant. Thus, while a practitioner should have their ambitions set to achieve these savings, they should set more modest expectations.

5 The non central distribution

A second distribution of considerable practical and theoretical interest is the non-central distribution, which regularly arises from the Cox-Ingersoll-Ross (CIR) interest rate model [19] (and the Heston model [36]). The distribution is parametrised as , where denotes the degrees of freedom and the non-centrality parameter, where we denote the inverse cumulative distribution function as . Having a parametrised distribution naturally increases the complexity of any implementation, exact or approximate, and makes the distribution considerably more expensive to compute.

To gauge the procedure used, the associated function in Python’s SciPy package (ncx2.ppf) calls the Fortran routine CDFCHN from the CDFLIB library by Brown et al. [13] (C implementations available [15]). This computes the value by root finding [17, algorithm R] on the offset cumulative distribution function , where is itself computed by a complicated series expansion [2, (26.4.25)] involving the cumulative distribution function for the central distribution. Overall, there are many stages involved, and as remarked by Burkardt [15, cdflib.c]: “Very large values of [] can consume immense computer resources”. The analogous function ncx2inv in MATLAB, from its statistics and machine learning toolbox, appears to follow a similar approach based on its description [49, page 4301]. To indicate the costs, on an Intel core i7-4870HQ CPU the ratios between sampling from the non-central distribution and the Gaussian distribution (norm.ppf and norminv in Python and MATLAB respectively) are shown in table 6, from which it is clear that the non-central distribution can be vastly more expensive than the Gaussian distribution.

| 1 | 5 | 10 | 50 | 100 | |

|---|---|---|---|---|---|

| 1 | 37 | 36 | 40 | 54 | 73 |

| 5 | 40 | 46 | 48 | 62 | 85 |

| 10 | 54 | 56 | 63 | 69 | 97 |

| 50 | 101 | 103 | 103 | 144 | 143 |

| 100 | 191 | 190 | 192 | 189 | 185 |

| 200 | 243 | 246 | 240 | 233 | 221 |

| 500 | 465 | 474 | 465 | 446 | 416 |

| 1000 | 459 | 458 | 455 | 471 | 474 |

| 1 | 5 | 10 | 50 | 100 | |

|---|---|---|---|---|---|

| 1 | 168 | 214 | 259 | 456 | 294 |

| 5 | 651 | 782 | 840 | 1510 | 2046 |

| 10 | 935 | 1086 | 1050 | 1838 | 2496 |

| 50 | 3000 | 2969 | 2562 | 4118 | 5333 |

| 100 | 4929 | 3461 | 5039 | 6046 | 6299 |

| 200 | 9456 | 9603 | 10129 | 11524 | 12766 |

| 500 | 22691 | 22713 | 22702 | 23328 | 26273 |

| 1000 | 45872 | 43968 | 43807 | 44563 | 46780 |

| 1 | 5 | 10 | 50 | 100 | |

|---|---|---|---|---|---|

| 1 | 333 | 412 | 458 | 666 | 864 |

| 5 | 391 | 447 | 534 | 701 | 966 |

| 10 | 600 | 668 | 724 | 801 | 992 |

| 50 | 1411 | 1424 | 1231 | 1811 | 1811 |

| 100 | 2271 | 2174 | 2164 | 2207 | 2029 |

| 200 | 2539 | 2624 | 2791 | 2304 | 2113 |

| 500 | 5020 | 4912 | 4860 | 4908 | 4886 |

| 1000 | 4822 | 4859 | 4866 | 4791 | 4980 |

| 1 | 5 | 10 | 50 | 100 | |

|---|---|---|---|---|---|

| 1 | 671 | 1643 | 1534 | 1734 | 2093 |

| 5 | 1884 | 1831 | 1733 | 2037 | 2344 |

| 10 | 1924 | 1937 | 1863 | 2490 | 2490 |

| 50 | 2576 | 2565 | 2876 | 2945 | 2974 |

| 100 | 3238 | 3265 | 3255 | 3299 | 3354 |

| 200 | 4382 | 4384 | 4373 | 4356 | 4333 |

| 500 | 5260 | 5294 | 5243 | 5249 | 5224 |

| 1000 | 6101 | 6022 | 6026 | 6147 | 6093 |

| 1 | 5 | 10 | 50 | 100 | |

|---|---|---|---|---|---|

| 1 | 0.036 | 0.036 | 0.041 | 0.070 | 0.095 |

| 5 | 0.045 | 0.047 | 0.050 | 0.076 | 0.100 |

| 10 | 0.054 | 0.056 | 0.059 | 0.081 | 0.104 |

| 50 | 0.098 | 0.099 | 0.101 | 0.116 | 0.133 |

| 100 | 0.134 | 0.135 | 0.136 | 0.148 | 0.161 |

| 200 | 0.186 | 0.187 | 0.188 | 0.196 | 0.207 |

| 1 | 5 | 10 | 50 | 100 | |

|---|---|---|---|---|---|

| 1 | 0.004 | 0.005 | 0.006 | 0.007 | 0.006 |

| 5 | 0.004 | 0.004 | 0.005 | 0.010 | 0.015 |

| 10 | 0.006 | 0.005 | 0.005 | 0.009 | 0.014 |

| 50 | 0.006 | 0.007 | 0.005 | 0.010 | 0.011 |

| 100 | 0.013 | 0.008 | 0.009 | 0.011 | 0.014 |

| 200 | 0.009 | 0.012 | 0.011 | 0.012 | 0.015 |

| 1 | 5 | 10 | 50 | 100 | |

|---|---|---|---|---|---|

| 1 | 0.153 | 0.041 | 0.023 | 0.009 | 0.006 |

| 5 | 0.329 | 0.155 | 0.083 | 0.013 | 0.007 |

| 10 | 0.385 | 0.243 | 0.156 | 0.026 | 0.011 |

| 50 | 0.451 | 0.403 | 0.353 | 0.157 | 0.079 |

| 100 | 0.461 | 0.435 | 0.405 | 0.250 | 0.157 |

| 200 | 0.466 | 0.453 | 0.436 | 0.334 | 0.251 |

| 1 | 5 | 10 | 50 | 100 | |

|---|---|---|---|---|---|

| 1 | 0.031 | 0.021 | 0.009 | 0.006 | |

| 5 | 0.058 | 0.031 | 0.010 | 0.007 | |

| 10 | 0.121 | 0.057 | 0.034 | 0.012 | 0.007 |

| 50 | 0.030 | 0.025 | 0.020 | 0.012 | 0.009 |

| 100 | 0.015 | 0.014 | 0.012 | 0.009 | 0.008 |

| 200 | 0.008 | 0.007 | 0.007 | 0.006 | 0.006 |

5.1 Approximating the non-central distribution

There has been considerable research effort into quickly sampling from the non-central distribution by various approximating distributions [42, 59, 1, 70, 38, 60, 10, 58], with the most notable being an approximation using Gaussian random variables by Abdel-Aty [1], (and a similar type of approximation by Sankaran [59]). With the exception of Abdel-Aty [1] and Sankaran [59], the remaining methods do not directly approximate the inverse cumulative distribution function, so do not give rise to an obvious coupling mechanism for multilevel Monte Carlo simulations, whereas our framework does. The schemes by Abdel-Aty [1] and Sankaran [59], both of which require evaluating , are appropriate for comparison to our scheme. Hence, our approximation scheme, while modest in its sophistication, appears novel research in this direction.

For approximating the non-central distribution, we simplify our considerations by taking to be fixed, and thus the distribution then only has the parameter varying. While this may appear a gross simplification, in the financial applications is a model constant independent of the numerical method’s parameters, and thus this simplification is appropriate.

We define the function for and as

This is because is better scaled than for the range of possible parameters, with the limits

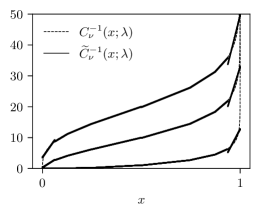

where , without the parameter , is the inverse cumulative distribution function of the central distribution. Thus to construct our approximation , we first construct the piecewise polynomial approximation , and then define . An example piecewise linear approximation of using 8 intervals is shown in figure 4(i) for various values of the non-centrality parameter with the degrees of freedom fixed at . We can see from figure 4(i) that the fidelity of the approximation appears quite high across a range of parameter values.

There are only two difficulties with constructing such an approximation. The first is that the distribution is no longer anti-symmetric about , which is easily remedied by constructing two approximations: one for and a second for . The second difficulty is the parametrisation. Noting that is dependent on the non-centrality parameter, we construct several approximations for various values of (knowing the limiting cases) and linearly interpolate. A good choice of knot points are equally spaced values of , where figure 4(i) uses 16 interpolation values.

The performance of C and C++ implementations are shown in table 6 on Intel Skylake hardware compiled with g++. Neither Intel, NAG, nor GSL offer an exact implementation of the inverse cumulative distribution function for the non-central distribution. Consequently, for our C implementation we compare against the cdfchn function from CDFLIB [13, 15], and for our C++ implementation the quantile function from the Boost library [3] acting on a non_central_chi_squared object (boost/math/distributions). Like the other implementations, Boost computes the inverse by a numerical inversion of the cumulative distribution function. We can see from table 6 that our approximation is orders of magnitude faster than the exact functions in both languages.

The fidelity of our non central approximations across the range of parameter values are quantified by the errors shown in table 6. A piecewise linear approximation achieves a consistently good RMSE, as seen in table 4(e). Similarly, the piecewise cubic approximation demonstrates the same behaviour in table 4(f), and has an RMSE which is typically an order of magnitude less than the piecewise linear approximation’s.

The approximations from Abdel-Aty [1] and Sankaran [59] are also shown in tables 4(g) and 4(h) respectively. We can see from table 4(g) that the approximation from Abdel-Aty, while improving for increasing , performs relatively poorly for large . Conversely, the approximation by Sankaran in table 4(h) is notably better than that by Abdel-Aty and often comparable to our piecewise cubic approximation, although demonstrating a much less consistent performance across the range of parameter values explored.

Having compared the error coming from the approximation by Sankaran [59], we can inspect the computational complexity of the approximation. The approximation can be expressed as

where , , and . Just as in our polynomial approximations, it contains an identical mix of basic arithmetic operations, but a evaluation. This can either be calculated exactly, or for improved speed it can potential be further approximated itself, but this then compounds a second level of approximation on top of the original. Furthermore, the expression contains an exponentiation by a factor of , which will not in general be an integer. It can be expected that such a non-integer exponentiation operation will be quite expensive. Consequently, we anticipate this would be measurably slower than our polynomial approximations.

Contrasting the approximations between Sankaran [59] and our piecewise cubic, the piecewise cubic demonstrates a more consistent RMSE alongside a simpler computational composition, makes our piecewise polynomial the more attractive of the two.

5.2 Simulating the Cox-Ingersoll-Ross process

We mentioned the non-central distribution arises from the Cox-Ingersoll-Ross (CIR) process: for strictly positive parameters , and . The distribution of is a scaled non-central distribution with and [19] [52, pages 67–68]. Simulating this with the Euler-Maruyama scheme forcibly approximates the non-central distribution as a Gaussian distribution, and can require very finely resolved path simulations to bring the bias down to an acceptable level, as explored by Broadie and Kaya [12]. Similarly the Euler-Maruyama scheme is numerically ill posed due to the term, and several adaptions exist to handle this appropriately [21, 46, 9, 37, 4, 5, 6, 22, 20, 34], especially when the Feller condition is not satisfied [23, 33]. The Feller condition is significant because [19, page 391]: “ can reach zero if . If , the upward drift is sufficiently large to make the origin inaccessible [see Feller [23]]”.

Rather than approximating the non-central distribution with an exact Gaussian distribution when using the Euler-Maruyama scheme, we propose using approximate non-central random variables, such as those from a piecewise linear approximation. This has the benefit of offering vast time savings, whilst introducing far less bias than the Euler-Maruyama scheme. The piecewise linear approximation is on average hundreds of times faster than the exact function, as was seen in table 6, giving vast savings, while still achieving a high fidelity, as was seen from table 6.

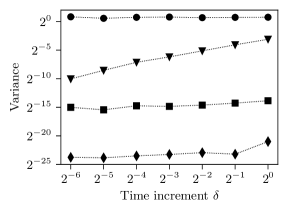

We can generate path simulations of the CIR process using the exact non-central distribution, piecewise linear and cubic approximations, and the truncated Euler-Maruyama scheme from Higham et al. [37] (where ), where we set and (just satisfying the Feller condition111In this case for which there is a finite and non zero probability density at zero.). These respectively give rise to the exact underlying process and the three approximations , , and . The variances of the underlying process and the differences between this and the approximations are shown in figure 4(j). Note that the difference terms are evaluated using the same time increments, and there is no mixing of coarse and fine paths in these two-way differences. The results of figure 4(j) do not change if we instead satisfy the Feller condition with strict inequality by setting e.g. .

From figure 4(j) we can see the exact underlying process’ variance does not vary with the discretisation, which is to be expected as the simulation is from the exact distribution, and thus has no bias. We can see that the Euler-Maruyama approximation to the process exhibits a strong convergence order , as expected [37, 33]. For the piecewise linear approximation, as the fidelity will not vary with the discretisation, then subsequently the variance also does not vary. Furthermore, given the high fidelity seen in table 4(e), the drop in the variance is approximately . Similarly, the even higher fidelity cubic approximation demonstrates the same behaviour in table 4(f), but with a drop in variance of . These findings demonstrate that the most substantial variance reductions come from using our piecewise polynomial approximations to the non central distribution’s inverse cumulative distribution function, rather than using the Gaussian distribution with the Euler-Maruyama scheme.

We can repeat these same variance comparisons with a different functional of the terminal value which is path dependent. A common example in financial simulations to consider the arithmetic average of the path, (an Asian option in mathematical finance [32]). Doing so produces an exactly identical variance structure as seen in figure 4(j). From this we conclude that our findings seen and explained thus far appear to carry over immediately to simulations requiring an entire path simulation, not only a terminal value, justifying the use of our approximations in time marching schemes.

Quantifying the savings that can be expected, we conservatively approximate the cost savings for both the linear and cubic approximations as a factor of 300 using table 6. Coupling this with the variance reductions seen in figure 4(j), the anticipated cost savings are shown in table 7. We can see from this that both offer impressive time savings, and the piecewise cubic again achieves a near perfect efficiency. However, the piecewise linear approximation’s efficiency, while good, is losing an appreciable fraction, making the piecewise cubic the preferred choice. Ultimately, both offer vast time savings by factors of 250 or higher.

| Approximation | Speed up | |||||

|---|---|---|---|---|---|---|

| Piecewise linear | 300 | 249 | (83.3%) | 1.09 | 2900 | |

| Piecewise cubic | 300 | 298 | (99.4%) | 1.00 | 100000 | |

6 Conclusions

The expense of sampling random variables can be significant. In the work presented, we proposed, developed, analysed, and implemented approximate random variables as a means of circumventing this for a variety of modern hardwares. By incorporating these into a nested multilevel Monte Carlo framework we showcased how the full speed improvements offered can be recovered with near perfect efficiency without losing any accuracy. With a detailed treatment, we showed that even for basic simulations of geometric Brownian motions requiring Gaussian random variables, speedups of a factor 5 or more can be expected. The same framework was also applied to the more difficult Cox-Ingersoll-Ross process and its non-central distribution, offering the potential for vast speedups of a factor of 250 or more.

For sampling from a wide class of univariate distributions, we based our work on the inverse transform method. Unfortunately, this method is expensive as it relies on evaluating a distribution’s inverse cumulative distribution function. We showed that many implementations for the Gaussian distribution, while accurate to near machine precision, are ill-suited in several respects for modern vectorised hardware. To address this, we introduced a generalised notion of approximate random variables, produced using approximations to a distribution’s inverse cumulative distribution function. The two major classes of approximations we introduced were: piecewise constant approximations using equally spaced intervals, and piecewise linear approximations using geometrically small intervals dense near the distribution’s tails. These cover a wide class of possible approximations, and notably recover as special cases: Rademacher random variables and the weak Euler-Maruyama scheme [32], moment matching schemes by Müller et al. [51], and truncated bit approximations by Giles et al. [31]. For piecewise constant and linear approximations, we analysed and bounded the errors for a range of possible norms. The significance of these bounds is that they are valid for arbitrarily high moments, which extends the results from Giles et al. [31], and crucially is necessary for the nested multilevel Monte Carlo analysis by Giles and Sheridan-Methven [28]. Lastly, these approximations were able to achieve very high fidelities, with the piecewise linear approximation using a geometric sequence of intervals providing high resolution of singularities.

With the approximations detailed from a mathematical perspective, we highlighted two possible implementations in C [62]. The benefit of these approximations is that they are by design ideally suited for modern vector hardware and achieve the highest possible computational speeds. They can be readily vectorised using OpenMP SIMD directives, have no conditional branching, avoid division and expensive function evaluations, and only require simple additions, multiplications, and bit manipulations. The piecewise constant and linear implementations were orders of magnitude faster than most freely available open source libraries, and typically a factor of 5–7 times faster than the proprietary Intel Maths Kernel Library, achieving close to the maximum speed of reading and writing to memory. This speed comes from the simplicity of their operations, and heavy capitalisation on the fast speeds of querying the cache and vector registers.

Incorporating approximate random variables into the nested multilevel Monte Carlo framework by Giles and Sheridan-Methven [28], the low errors and fast speeds of the approximations can be exploited to obtain their full speed benefits without losing accuracy. Inspecting the appropriate multilevel variance reductions, we demonstrated how practitioners can expect to obtain speed improvements of a factor of 5–7 by using approximate Gaussian random variables, where the fastest approximation was the piecewise linear approximation. This appears to be the case when using either the Euler-Maruyama or Milstein schemes.

Considering the Cox-Ingersoll-Ross process [19], this is known to give rise to the non-central distribution, which is an example of a parametrised distribution, and is also extremely expensive to sample from, as we demonstrated. We applied our approximation framework to this to produce a parametrised approximation. The error of using our approximate random variables was orders of magnitude lower than approximating paths using the Euler-Maruyama scheme, showing our approximate random variables are considerably more suitable for generating path simulations than the Euler-Maruyama scheme. This circumvents the problem of the Euler-Maruyama scheme having a very large bias for the Cox-Ingersoll-Ross process [12]. Furthermore, our implementation was substantially quicker than those by CDFLIB and Boost, offering a speed improvement of 250 times or higher.

7 Acknowledgements

We would like to acknowledge and thank those who have financially sponsored this work. This includes the Engineering and Physical Sciences Research Council (EPSRC) and Oxford University’s centre for doctoral training in Industrially Focused Mathematical Modelling (InFoMM), with the EP/L015803/1 funding grant. Furthermore, this research stems from a PhD project [63] which was funded by Arm and NAG. Funding was also provided by the EPSRC ICONIC programme grant EP/P020720/1, the Hong Kong Innovation and Technology Commission (InnoHK Project CIMDA), and by Mansfield College, Oxford.

References

- Abdel-Aty [1954] S.H. Abdel-Aty. Approximate formulae for the percentage points and the probability integral of the non-central distribution. Biometrika, 41(3/4):538–540, 1954.

- Abramowitz and Stegun [1948] Milton Abramowitz and Irene A. Stegun. Handbook of mathematical functions with formulas, graphs, and mathematical tables, volume 55. US government printing office, 1948. (6 printing, November 1967).

- Agrawal et al. [2020] Nikhar Agrawal, Anton Bikineev, Paul A. Bristow, Marco Guazzone, Christopher Kormanyos, Hubert Holin, Bruno Lalande, John Maddock, Jeremy Murphy, Matthew Pulver, Johan Råde, Gautam Sewani, Benjamin Sobotta, Nicholas Thompson, Thijs van den Berg, Daryle Walker, Xiaogang Zhang, et al. The Boost C++ library, 2020. URL https://www.boost.org/. Version 1.74.0.

- Alfonsi [2005] Aurélien Alfonsi. On the discretization schemes for the CIR (and Bessel squared) processes. Monte Carlo methods and applications, 11(4):355–384, 2005.

- Alfonsi [2008] Aurélien Alfonsi. A second-order discretization scheme for the CIR process: application to the Heston model. Preprint CERMICS hal-00143723, 14, 2008.

- Alfonsi [2010] Aurélien Alfonsi. High order discretization schemes for the CIR process: application to affine term structure and Heston models. Mathematics of computation, 79(269):209–237, 2010.

- Asmussen and Glynn [2007] Søren Asmussen and Peter W. Glynn. Stochastic simulation: algorithms and analysis, volume 57. Springer science & business media, 2007.

- Beasley and Springer [1977] J.D. Beasley and S.G. Springer. Algorithm AS 111: the percentage points of the normal distribution. Journal of the royal statistical society. Series C (applied statistics), 26(1):118–121, March 1977.

- Berkaoui et al. [2008] Abdel Berkaoui, Mireille Bossy, and Awa Diop. Euler scheme for SDEs with non-Lipschitz diffusion coefficient: strong convergence. ESAIM: probability and statistics, 12:1–11, 2008.

- Best and Roberts [1975] D.J. Best and D.E. Roberts. Algorithm AS 91: The percentage points of the distribution. Journal of the royal statistical society. Series C (applied statistics), 24(3):385–388, 1975.

- Black and Scholes [1973] Fischer Black and Myron Scholes. The pricing of options and corporate liabilities. Journal of political economy, 81(3):637–654, 1973.

- Broadie and Kaya [2006] Mark Broadie and Özgür Kaya. Exact simulation of stochastic volatility and other affine jump diffusion processes. Operations research, 54(2):217–231, 2006.

- Brown et al. [1994] Barry W. Brown, James Lovato, and Kathy Russell. CDFLIB: library of Fortran routines for cumulative distribution functions, inverses, and other parameters, February 1994.

- Brugger et al. [2014] Christian Brugger, Christian de Schryver, Norbert Wehn, Steffen Omland, Mario Hefter, Klaus Ritter, Anton Kostiuk, and Ralf Korn. Mixed precision multilevel Monte Carlo on hybrid computing systems. In 2104 IEEE conference on computational intelligence for financial engineering & economics (CIFEr), pages 215–222. IEEE, 2014.

- Burkardt [2019] John Burkardt. C source codes for CDFLIB, June 2019. URL https://people.sc.fsu.edu/~jburkardt/c_src/cdflib/cdflib.html. Accessed Wednesday \nth2 September 2020.

- Burkardt [2020] John Burkardt. MATLAB source codes for ASA241 and ASA111, April 2020. URL https://people.sc.fsu.edu/~jburkardt/m_src/m_src.html. Accessed Thursday \nth18 June 2020.

- Bus and Dekker [1975] Jacques C.P. Bus and Theodorus Jozef Dekker. Two efficient algorithms with guaranteed convergence for finding a zero of a function. ACM transactions on mathematical software (TOMS), 1(4):330–345, 1975.

- Cheung et al. [2007] R.C.C. Cheung, D-U Lee, W. Luk, and J.D. Villasenor. Hardware generation of arbitrary random number distributions from uniform distributions via the inversion method. IEEE Transactions on Very Large Scale Integration (VLSI) Systems, 15(8):952–962, 2007.

- Cox et al. [1985] John C. Cox, Jonathan E. Ingersoll Jr, and Stephen A. Ross. A theory of the term structure of interest rates. Econometrica, 53(2):385–408–164, March 1985.

- Cozma and Reisinger [2018] Andrei Cozma and Christoph Reisinger. Strong order 1/2 convergence of full truncation Euler approximations to the Cox-Ingersoll-Ross process. IMA journal of numerical analysis, 40(1):358–376, October 2018.

- Deelstra and Delbaen [1998] Griselda Deelstra and Freddy Delbaen. Convergence of discretized stochastic (interest rate) processes with stochastic drift term. Applied stochastic models and data analysis, 14(1):77–84, 1998.

- Dereich et al. [2012] Steffen Dereich, Andreas Neuenkirch, and Lukasz Szpruch. An Euler-type method for the strong approximation of the Cox-Ingersoll-Ross process. Proceedings of the royal society A: mathematical, physical and engineering sciences, 468(2140):1105–1115, 2012.

- Feller [1951] William Feller. Two singular diffusion problems. Annals of mathematics, pages 173–182, 1951.

- Fog [2018] Agner Fog. Instruction tables: lists of instruction latencies, throughputs and micro-operation breakdowns for Intel, AMD and VIA CPUs, 2018. URL https://www.agner.org/optimize/instruction_tables.pdf. Updated 9 April 2018, Copenhagen University college of engineering.

- Galassi et al. [2017] Mark Galassi, Jim Davies, James Theiler, Brian Gough, Gerard Jungman, Patrick Alken, Michael Booth, Fabrice Rossi, Rhys Ulerich, et al. GNU scientific library 2.4, June 2017.

- Giles [2008] Michael B. Giles. Multilevel Monte Carlo path simulation. Operations research, 56(3):607–617, 2008.

- Giles [2011] Michael B. Giles. Approximating the erfinv function. In GPU computing gems, jade edition, volume 2, pages 109–116. Elsevier, 2011.

- Giles and Sheridan-Methven [2020] Michael B. Giles and Oliver Sheridan-Methven. Analysis of nested multilevel Monte Carlo using approximate normal random variables, 2020. in preparation.

- Giles and Waterhouse [2009] Michael B. Giles and Benjamin J. Waterhouse. Multilevel quasi-Monte Carlo path simulation. Advanced financial modelling, Radon series on computational and applied mathematics, 8:165–181, 2009.

- Giles et al. [2019a] Michael B. Giles, Mario Hefter, Lukas Mayer, and Klaus Ritter. Random bit multilevel algorithms for stochastic differential equations. Journal of complexity, 2019a.

- Giles et al. [2019b] Michael B. Giles, Mario Hefter, Lukas Mayer, and Klaus Ritter. Random bit quadrature and approximation of distributions on Hilbert spaces. Foundations of computational mathematics, 19(1):205–238, 2019b.

- Glasserman [2013] Paul Glasserman. Monte Carlo methods in financial engineering, volume 53 of Stochastic modelling and applied probability. Springer science & business media, 1 edition, 2013.

- Gyöngy [1998] István Gyöngy. A note on Euler’s approximations. Potential analysis, 8(3):205–216, 1998.

- Gyöngy and Rásonyi [2011] István Gyöngy and Miklós Rásonyi. A note on Euler approximations for SDEs with Hölder continuous diffusion coefficients. Stochastic processes and their applications, 121(10):2189–2200, 2011.

- Hastings Jr et al. [1955] Cecil Hastings Jr, Jeanne T. Wayward, and James P. Wong Jr. Approximations for digital computers. Princeton University press, 1955.

- Heston [1993] Steven L. Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. The review of financial studies, 6(2):327–343, 1993.

- Higham et al. [2002] Desmond J. Higham, Xuerong Mao, and Andrew M. Stuart. Strong convergence of Euler-type methods for nonlinear stochastic differential equations. SIAM journal on numerical analysis, 40(3):1041–1063, 2002.

- Hoaglin [1977] David C. Hoaglin. Direct approximations for chi-squared percentage points. Journal of the American statistical association, 72(359):508–515, 1977.

- IEEE [2008] IEEE. IEEE standard for binary floating-point arithmetic, 2008. Computer society standards committee. Working group of the microprocessor standards subcommittee.

- International organization for standardization (2012) [ISO] International organization for standardization (ISO). ISO/IEC 9899:2011: programming languages–C. ISO working group, 14, 2012.

- Iserles [1996] Arieh Iserles. A first course in the numerical analysis of differential equations. Cambridge University press, 1996.

- Johnson et al. [1995] Norman L. Johnson, Samuel Kotz, and Narayanaswamy Balakrishnan. Continuous univariate distributions. John Wiley & sons, Ltd, 1995.

- Joy et al. [1996] Corwin Joy, Phelim P. Boyle, and Ken Seng Tan. Quasi-Monte Carlo methods in numerical finance. Management science, 42(6):926–938, 1996.

- Kloeden and Platen [1999] Peter E. Kloeden and Eckhard Platen. Numerical solution of stochastic differential equations, volume 23 of Stochastic modelling and applied probability. Springer, 1999. Corrected 3 printing.