On moments of folded and doubly truncated multivariate extended skew-normal distributions

Abstract

This paper develops recurrence relations for integrals that relate the density of multivariate extended skew-normal (ESN) distribution, including the well-known skew-normal (SN) distribution introduced by [1] and the popular multivariate normal distribution. These recursions offer a fast computation of arbitrary order product moments of the multivariate truncated extended skew-normal and multivariate folded extended skew-normal distributions with the product moments as a byproduct. In addition to the recurrence approach, we realized that any arbitrary moment of the truncated multivariate extended skew-normal distribution can be computed using a corresponding moment of a truncated multivariate normal distribution, pointing the way to a faster algorithm since a less number of integrals is required for its computation which result much simpler to evaluate. Since there are several methods available to calculate the first two moments of a multivariate truncated normal distribution, we propose an optimized method that offers a better performance in terms of time and accuracy, in addition to consider extreme cases in which other methods fail. The R MomTrunc package provides these new efficient methods for practitioners.

Keywords Extended skew-normal distribution Folded normal distribution Product moments Truncated distributions.

1 Introduction

Many applications on simulations or experimental studies, the researches often generate a large number of datasets with restricted values to fixed intervals. For example, variables such as pH, grades, viral load in HIV studies and humidity in environmental studies, have upper and lower bounds due to detection limits, and the support of their densities is restricted to some given intervals. Thus, the need to study truncated distributions along with their properties naturally arises. In this context, there has been a growing interest in evaluating the moments of truncated distributions. These variables are also often skewed, departing from the traditional assumption of using symmetric distributions. For instance, [2] provided the formulas for the first two moments of truncated multivariate normal (TN) distributions. [3] gave the expressions for the moments of truncated bivariate log-normal distributions with applications to test the Houthakker effect ([4]) in future markets. [5] derived the truncated moments of several continuous univariate distributions commonly applied to hydrologic problems. [6] provided analytical formulas for moments of the truncated univariate Student-t distribution in a recursive form. [7] obtained expressions for the moments of truncated univariate skew-normal distributions ([8]) and applied the results to model the relative humidity data. [9] studied the moments of a doubly truncated member of the symmetrical class of univariate normal/independent distributions and their applications to the actuarial data. [10] presented a general formula based on the slice sampling algorithm to approximate the first two moments of the truncated multivariate Student- (TT) distribution under the double truncation. [11] provided explicit expressions for computing arbitrary order product moments of the TN distribution by using the moment generating function (MGF). However, the calculation of this approach relies on differentiation of the MGF and can be somewhat time consuming.

Instead of differentiating the MGF of the TN distribution, [12] recently presented recurrence relations for integrals that are directly related to the density of the multivariate normal distribution for computing arbitrary order product moments of the TN distribution. These recursions offer a fast computation of the moments of folded normal (FN) and TN distributions, which require evaluating -dimensional integrals that involve the Normal (N) density. Explicit expressions for some low order moments of FN and TN distributions are presented in a clever way, although some proposals to calculate the moments of the univariate truncated skew-normal distribution ([7]) and truncated univariate skew-normal/independent distribution ([7]) has recently been published. So far, to the best of our knowledge, there has not been attempt on studying neither moments nor product moments of the multivariate folded extended skew-normal (FESN) and truncated multivariate extended skew-normal (TESN) distributions. Moreover, our proposed methods allow to compute, as a by-product, the product moments of folded and truncated distributions, of the N ([12]), SN ([1]), and their respective univariate versions. The proposed algorithm and methods are implemented in the new R package “MomTrunc”.

The rest of this paper is organized as follows. In Section 2 we briefly discuss some preliminary results related to the multivariate SN, ESN and TESN distributions and some of its key properties. The section 3 presents a recurrence formula of an integral to be applied in the essential evaluation of moments of the TESN distribution as well as explicit expressions for the first two moments of the TESN and TN distributions. A direct relation between the moments of the TESN and TN distribution is also presented which is used to improved the proposed methods. In section 4, by means of approximations, we propose strategies to circumvent some numerical problems that arise on limiting distributions and extreme cases. We compare our proposal with others popular methods of the literature in Section 5. Finally, Section 6 is devoted to the moments of the FESN distribution, several related results are discussed. Explicit expressions are presented for high order moments for the univariate case and the mean vector and variance-covariance matrix of the multivariate FESN distribution. Finally, some concluding remarks are presented in Section 7.

2 Preliminaries

We start our exposition by defining some notation and presenting the basic concepts which are used throughout the development of our theory. As is usual in probability theory and its applications, we denote a random variable by an upper-case letter and its realization by the corresponding lower case and use boldface letters for vectors and matrices. Let and represent an identity matrix and a matrix of ones, respectively, both of dimension , be the transpose of , and mean the absolute value of each component of the vector . For multiple integrals, we use the shorthand notation

where and .

2.1 The multivariate skew-normal distribution

In this subsection we present the skew-normal distribution and some of its properties. We say that a random vector follows a multivariate SN distribution with location vector , positive definite dispersion matrix and skewness parameter vector, and we write if its joint probability density function (pdf) is given by

| (1) |

where represents the probability density distribution (pdf) of a -variate normal distribution with vector mean and variance-covariance matrix , and stands for the cumulative distribution function (cdf) of a standard univariate normal distribution. If then (1) reduces to the symmetric pdf. Except by a straightforward difference in the parametrization considered in (1), this model corresponds to the one introduced by [1], whose properties were extensively studied in [14] (see also, [13]).

Proposition 1 (cdf of the SN).

If , then for any

where and with

It is worth mentioning that the multivariate skew-normal distribution is not closed over marginalization and conditioning. Next, we present its extended version which holds these properties, called, the multivariate ESN distribution.

2.2 The extended multivariate skew-normal distribution

We say that a random vector follows a ESN distribution with location vector , positive definite dispersion matrix , a skewness parameter vector, and shift parameter , denoted by if its pdf is given by

| (2) |

with . Note that when , we retrieve the skew-normal distribution defined in (1), that is, . Here, we used a slightly different parametrization of the ESN distribution than the one given in [15] and [16]. Futhermore, [16] deals with the multivariate extended skew-t (EST) distribution, in which the ESN is a particular case when the degrees of freedom goes to infinity. From this last work, it is straightforward to see that

Also, letting , it follows that , with mean vector and variance-covariance matrix

with . Then, the mean vector and variance-covariance matrix of can be easily computed as and .

The following propositions are crucial to develop our methods. The proofs can be found in the Appendix A.

Proposition 2 (Marginal and conditional distribution of the ESN).

Let and is partitioned as of dimensions and (), respectively. Let

be the corresponding partitions of , , and . Then,

where , , , and .

Proposition 3 (Stochastic representation of the ESN).

Let . If it follows that , with and as defined in Proposition 1, and .

The stochastic representation above can be derived from Proposition 1 in [16].

Proposition 4 (cdf of the ESN).

If , then for any

Proof is direct from Proposition 3 by noting that . Hereinafter, for , we will denote to its cdf as for simplicity.

Let be a Borel set in . We say that the random vector has a truncated extended skew-normal distribution on when has the same distribution as . In this case, the pdf of is given by

where is the indicator function of . We use the notation . If has the form

then we use the notation , where and . Here, we say that the distribution of is doubly truncated. Analogously, we define and . Thus, we say that the distribution of is truncated from below and truncated from above, respectively. For convenience, we also use the notation .

3 On moments of the doubly truncated multivariate ESN distribution

3.1 A recurrence relation

For two -dimensional vectors and , let stand for , and let be a vector with its th element being removed. For a matrix , we let stand for the th row of with its th element being removed. Similarly, stands for the matrix with its th row and th columns being removed. Besides, let denote a vector with its th element equaling one and zero otherwise. Let

We are interested in evaluating the integral

| (3) |

The boundary condition is obviously . When and , we recover the multivariate normal case, and then

| (4) |

with boundary condition

| (5) |

Note that we use calligraphic style for the integrals of interest and when we work with the skewed version. In both expressions (4) and (5), for the normal case, we are using compatible notation with the one used by [12].

3.1.1 Univariate case

When , it is straightforward to use integration by parts to show that

where , , and .

When , we need a similar recurrence relation in order to compute which is presented in the next theorem.

3.1.2 Multivariate case

Theorem 1.

For and ,

| (6) |

where , , and is a -vector with th element

| (7) | |||||

where

Proof.

Let as in Proposition 2. From the conditional distribution of a multivariate normal, it is straightforward to show that and . Then it holds that

| (8) |

where we have used that . Now, taking the derivative of the ESN density, then

with and . Multiplying both sides by and integrating from

to , we have (after suppressing the arguments of

and ) that

and the th element of the left hand side is

by using integration by parts. Using Proposition 2, we know that

and we obtain

Finally, multiplying both sides by , we obtain (6). This completes the proof. ∎

This delivers a simple way to compute any arbitrary moments of multivariate TSN distribution based on at most lower order terms, with of them being -dimensional integrals, the rest being -dimensional integrals, and a normal integral that can be easily computed through our proposed R package MomTrunc available at CRAN. When , the first term in (7) vanishes. When , the second term vanishes, and when , the third term vanishes. When we have no truncation, that is, all the are and all the are , for , we have that

and in this case the recursive relation is

with .

3.2 Computing ESN moments based on normal moments

Theorem 2.

In particular, for , then

| (10) |

Proof.

The proof is straightforward by Proposition 3. Since a ESN variate can be written as , it follows that

since is distributed as .

∎

3.3 Mean and covariance matrix of multivariate TESN distributions

It follows that

| (11) |

where the -th element of and are

Denoting , we can write

where , that is a -variate truncated normal distribution on .

Besides, from Corollary 1, we have that the first two moments of can be also computed as

| (12) | ||||

| (13) |

with . Note that . Equations (12) and (13) are more convenient for computing and since all boils down to compute the mean and the variance-covariance matrix for a -variate TN distribution which integrals are less complex than the ESN ones.

3.4 Mean and covariance matrix of TN distributions

Some approaches exists to compute the moments of a TN distribution. For instance, for doubly truncation, [18] (method available through the tmvtnorm R package) computed the mean and variance of directly deriving the MGF of the TN distribution. On the other hand, [12] (method available through the MomTrunc R package) is able to compute arbitrary higher order TN moments using a recursive approach as a result of differentiating the multivariate normal density. For right truncation, [19] (see Supplemental Material) proposed a method to compute the mean and variance of also by differentiating the MGF, but where the off-diagonal elements of the Hessian matrix are recycled in order to compute its diagonal, leading to a faster algorithm. Next, we present an extension of [19] algorithm to handle doubly truncation.

3.5 Deriving the first two moments of a double TN distribution through its MGF

Theorem 3.

Let , with being a correlation matrix of order . Then, the first two moments of are given by

and consequently,

where , , with the -th element of and as

being a symmetric matrix of dimension , with off-diagonal elements given by

and diagonal elements

| (14) |

with , and .

Proof. See Appendix A.

The main difference of our proposal in Theorem 3 and other approaches deriving the MGF relies on (14), where the diagonal elements are recycled using the off-diagonal elements . Furthermore, for , we have that

| (15) | ||||

| (16) |

where being a positive-definite matrix, , and truncation limits and such that and .

4 Dealing with limiting and extreme cases

Let consider . As , we have that . Besides, as , we have that and consequently . Thus, for negative values small enough, we are not able to compute due to computation precision. For instance, in R software, for . The next proposition helps us to circumvent this problem.

Proposition 5.

(Limiting distribution for the ESN) As ,

Proof.

Let . As , we have that , and (i.e., is (i.e., is degenerated on ). In light of Proposition 3, , and by the conditional distribution of a multivariate normal, it is straightforward to show that and , which concludes the proof. ∎

4.1 Approximating the mean and variance-covariance of a TN distribution for extreme cases

While using the normal relation (12) and (13), we may also face numerical problems for extreme settings of and due to the scale matrix does depend on them. Most common problem is that the normalizing constant is approximately zero, because the probability density has been shifted far from the integration region. It is worth mentioning that, for these cases, it is not even possible to estimate the moments generating Monte Carlo (MC) samples due to the high rejection ratio when subsetting to a small integration region.

For instance, consider a bivariate truncated normal vector , with and having zero mean and unit variance, and truncation limits and . Then, we have that the limits of are far from the density mass since . For this case, both the mtmvnorm function from the tmvtnorm R package and the Matlab codes provided in [12] return wrong mean values outside the truncation interval and negative variances. Values are quite high too, with mean values greater than and all the elements of the variance-covariance matrix greater than . When changing the first upper limit from to , that is , both routines return Inf and NaN values for all the elements.

Although the above scenarios seem unusual, extreme situations that require correction are more common than expected. Actually, the development of this part was motivated as we identified this problem when we fit censored regression models, with high asymmetry and presence of outliers. Hence, we present correction method in order to approximate the mean and the variance-covariance of a multivariate TN distribution even when the numerical precision of the software is a limitation.

Dealing with out-of-bounds limits

Consider the partition such that , , where . It is well known that

and

Now, consider to be partitioned as above. Also consider the corresponding partitions of , , and . We say that the limits of are out-of-bounds if . Let us consider the case where we are not able to compute any moment of , because there exists a partition of of dimension that is out-of-bounds. Note this happens because Also, we consider the partition such that . Since the limits of are out-of-bounds (and ), we have two possible cases: or . For convenience, let and . For the first case, as , we have that and . Analogously, we have that and as .

Then , (i.e., is degenerated on ) and . Given that and , it follows that

| (17) |

with and being the mean and variance-covariance matrix of a TN distribution, which can be computed using (15) and (16).

In the event that there are double infinite limits, we can partition the vector as well, in order to avoid unnecessary calculation of these integrals.

Dealing with double infinite limits

Let be the number of pairs in that are both infinite. We consider the partition , such that the upper and lower truncation limits associated with are both infinite, but at least one of the truncation limits associated with is finite. Since and , it follows that , and . This leads to

| (22) |

and

| (25) |

with and being the mean vector and variance-covariance matrix of a TN distribution, which can be computed using (15) and (16) as well.

As can be seen, we can use equations (22) and (25) to deal with double infinite limits, where the truncated moments are computed only over a -variate partition, avoiding some unnecessary integrals and saving some computational effort. On the other hand, expression (17) let us to approximate the mean and the variance-covariance matrix for cases where the computational precision is a limitation.

5 Comparison of computational times

Since this is the first attempt to compute the moments of a TESN, it is not possible to compare our approach with others methods already implemented in statistical softwares, for instance, R or Stata. However, this section intends to compare three possible approaches to compute the mean vector and variance-covariance matrix of a -variate TESN distribution based on our results. We consider our first proposal derived from Theorem 1 which is derived directly from the ESN pdf, as well as the normal relation given in Theorem 2. For the latter, we use different (some existent) methods for computing the mean and variance-covariance of a TN distribution. The methods that we compare are the following:

- Proposal 1:

- Proposal 2:

- Proposal 3:

- Proposal 4:

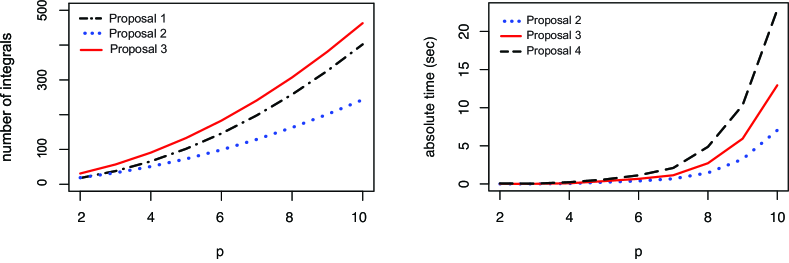

Left panel of Figure 1 shows the number of integrals required to achieve this for different dimensions . We compare the proposal 1 for a -variate TESN distribution and the equivalent -variate normal approaches K&R and proposal 2.

It is clear that the importance of the new proposed method since it reduces the number of integral involved almost to half, this compared to the TESN direct results from proposal 1, when we consider the double truncation. In particular, for left/right truncation, we have that the equivalent -variate normal approach along with [19] (now, a special case of proposal 2) requires up to 4 times less integrals than when we use the proposal 3. As seen before, the normal relation proposal 2 outperforms the proposal 1, that is, the equivalent normal approach always resulted faster even it considers one more dimension, that is a -variate normal vector, due to its integrals are less complex than for the ESN case.

Processing time when using the equivalent normal approach are depicted in the right panel of Figure 1. Here, we compare the absolute processing time of the mean and variance-covariance of a TN distribution under the methods in proposal 2, 3 and 4, for different dimensions . In general, our proposal is the fastest one, as expected. Proposal 3 resulted better only for , which confirms the necessity for a faster algorithm, in order to deal with high dimensional problems. Proposal 4 resulted to be the slowest one by far.

Computational time in real life:

For applications where a unique truncated expectation is required (for example, conditional tail expectations as a measure of risk in Finance), the computation cost may seem insignificant, however, iterative algorithms depending on these quantities become computationally intensive. For instance, in longitudinal censored models under a frequentist point of view, an EM algorithm reduces to the computation of the moments of multivariate truncated moments (Lachos et al., 2017) at each iteration, and for all censored observations along subjects. See that, 125K integrals will be required for an algorithm that converges in 250 iterations and a modest dataset with 100 subjects and only four censored observations. Other models as geostatistical models are even more demanding, so small differences in times may be significant between a tractable and non-tractable problem, even that without these expectations, these must be approximated invoking Monte Carlo methods.

6 On moments of multivariate folded ESN distributions

First, we established some general results for the pdf, cdf and moments of multivariate folded distributions (MFD). These extend the results found in [20] for a FN distribution to any multivariate distribution, as well as the multivariate location-scale family. The proofs are given in Appendix A.

Theorem 4 (pdf and cdf of a MFD).

Let be a -variate random vector with pdf and cdf , with being a set of parameters characterizing such distribution. If , then the joint pdf and cdf of that follows a folded distribution of are given, respectively, by

where is a cartesian product with elements, each of the form , and .

Corollary 2.

If belongs to the location-scale family of distributions, with location and scale parameters and respectively, then and consequently the joint pdf and cdf of are given by

Hence, the -th moment of follows as

where denotes the positive component of the random vector .

Let , we now turn our attention to discuss the computation of any arbitrary order moment of , a FESN distribution. Let define the function as

Note that is a special case of that occurs when and , . In this scenario we have

When and , that is, the normal case we write .

Proposition 6.

If , then and consequently the joint pdf, cdf and the th raw moment of are, respectively, given by

and

where , , and .

Proof.

Note that is suffices to show that,

if , then ,

since the rest of the corollary is straightforward. We have that

| (26) | ||||

| (27) | ||||

where due to .

In order to equalize (26) and (27), we see that it suffices to show that . This is equivalent to show that for and . We have that both matrices and are positive-definite matrices since and are too, as a consequence that they are obtained using Singular Value Decomposition (SVD). Finally, given that and any positive-definite matrix has an unique positive-definite square root, we conclude that by uniqueness, which concludes the proof. ∎

Remark 1.

As a consequence of Proposition 6, we also have the new vectors , , , , and , and matrix , while the constants , , ,, and remain invariant with respect to .

From Proposition 6, we can compute any arbitrary moment of a FESN distribution as a sum of integrals. In light of Theorem 1, the recurrence relation for can be written as

| (28) |

where

with and .

It is also possible to use the normal relation in Theorem 2 to compute in a simpler manner as in next proposition.

Proposition 7.

Let , with . In light of Theorem 4, It follows that

where , and , with , , and standing for the block matrix with all its off-diagonal block elements signs changed.

Proof is direct from Theorem 2 as is a special case of . From Proposition 2, we have that the mean and variance-covariance matrix can be calculated as a sum of terms as well, that is

| (29) | ||||

| (30) |

where is the positive component of . Note that there are times more integrals to be calculated as compared to the non-folded case, representing a huge computational effort for high dimensional problems.

In order to circumvent this, we can use the fact that and the elements of are given by the second moments and . Thus, it is possible to calculate explicit expressions for the mean vector and variance-covariance matrix of the FESN only based on the marginal univariate means and variances of , as well as the covariance terms .

Next, we circumvent this situation by propose explicit expressions for the mean and the variance-covariance of the multivariate FESN distribution.

6.1 Explicit expressions for mean and covariance matrix of multivariate folded ESN distribution

Let . To obtain the mean and covariance matrix of boils down to compute , and . Consider to be the -th marginal partition of distributed as . In light of Proposition 6 it follows that

Thus, using the recurrence relation on in (28), and following the notation in Subsection 3.1.1, we can write explicit expressions for and . High order moments for the univariate FESN and others related distributions are detailed in Appendix B.

It remains to obtain for , which can be obtained as

| (31) |

as pointed in Proposition 6, with denoting an arbitrary bivariate partition of . Without loss of generality, let’s consider the partition and with . For simplicity, we denote , and the normalizing constants and .

Using the recurrence relation on in (28), we can obtain for and as

where , , , , and in light of Proposition 2 we have that , , and for .

Using Remark 1 along with (6.1), we finally obtain an explicit expression for as

with . Furthermore,

with () denoting the () matrix with all its signs of covariances (off-diagonal elements) changed. Here, we have simplified using the equivalences

with as in Theorem 4 and . It is worth mentioning that these expressions hold for the normal case, when and .

As expected, this approach is much faster than the one using equations (29) and (30). For instance, when we consider a trivariate folded ESN distribution, we have that it is approximately 56x times faster than using MC methods and 10x times faster than using equations (29) and (30). Time comparison (summarized in the Figure in the Supplementar material, right panel) as well as sample codes of our MomTrunc R package are provided in the Appendices C and D, respectively.

7 Conclusions

In this paper, we have developed a recurrence approach for computing order product moments of TESN and FESN distributions as well as explicit expressions for the first two moments as a byproduct, generalizing results obtained by [12] for the normal case. The proposed methods also includes the moments of the well-known truncated multivariate SN distribution, introduced by [1]. For the TESN, we have proposed an optimized robust algorithm based only in normal integrals, which for the limiting normal case outperforms the existing popular method for computing the first two moments, even computing these two moments for extreme cases where all available algorithms fail. The proposed method (including its limiting and special cases) has been coded and implemented in the R MomTrunc package, which is available for the users on CRAN repository.

During the last decade or so, censored modeling approaches have been used in various ways to accommodate increasingly complicated applications. Many of these extensions involve using Normal ([19]) and Student-t ([21, 22]), however statistical models based on distributions to accommodate censored and skewness, simultaneously, so far have remained relatively unexplored in the statistical literature. We hope that by making the codes available to the community, we will encourage researchers of different fields to use our newly methods. For instance, now it is possible to derive analytical expressions on the E-step of the EM algorithm for multivariate SN responses with censored observation asblur in [21].

Finally, we anticipate in a near future to extend these results to the extended skew-t distribution ([23]). We conjecture that our method can be extended to the context of the family of other scale mixtures of skew-normal distributions ([24]). An in-depth investigation of such extension is beyond the scope of the present paper, but it is an interesting topic for further research.

SUPPLEMENTARY MATERIAL

The Supplementary Materials, which is available upon request, contains the following two files:

- A

-

Proofs of propositions and theorems;

- B

-

Explicit expressions for moments of some folded univariate distributions;

- C

-

Figures;

- D

-

The R MomTrunc package.

References

- [1] A. Azzalini and A. Dalla-Valle. The multivariate skew-normal distribution. Biometrika, 83(4):715–726, 1996.

- [2] G. M. Tallis. The moment generating function of the truncated multi-normal distribution. Journal of the Royal Statistical Society. Series B (Statistical Methodology), 23(1):223–229, 1961.

- [3] Da-Hsiang Donald Lien. Moments of truncated bivariate log-normal distributions. Economics Letters, 19(3):243–247, 1985.

- [4] HJ Houthakker. The scope and limits of futures trading. Cowles Foundation for Research in Economics at Yale University, 1959.

- [5] James W Jawitz. Moments of truncated continuous univariate distributions. Advances in Water Resources, 27(3):269–281, 2004.

- [6] H. M. Kim. A note on scale mixtures of skew normal distribution. Statistics and Probability Letters, 78, 2008. 1694-1701.

- [7] Cedric Flecher, Denis Allard, and Philippe Naveau. Truncated skew-normal distributions: moments, estimation by weighted moments and application to climatic data. Metron, 68:331–345, 2010.

- [8] A. Azzalini. A class of distributions which includes the normal ones. Scandinavian Journal of Statistics, 12:171–178, 1985.

- [9] Ali İ Genç. Moments of truncated normal/independent distributions. Statistical Papers, 54:741–764, 2013.

- [10] H. J. Ho, T. I. Lin, H. Y. Chen, and W. L. Wang. Some results on the truncated multivariate t distribution. Journal of Statistical Planning and Inference, 142:25–40, 2012.

- [11] Juan Carlos Arismendi. Multivariate truncated moments. Journal of Multivariate Analysis, 117:41–75, 2013.

- [12] Raymond Kan and Cesare Robotti. On moments of folded and truncated multivariate normal distributions. Journal of Computational and Graphical Statistics, 25(1):930–934, 2017.

- [13] Arellano-Valle, R. B. and M. G. Genton. On fundamental skew distributions. Journal of Multivariate Analysis, 96, 93–116, 2005.

- [14] A. Azzalini and A. Capitanio. Statistical applications of the multivariate skew-normal distribution. Journal of the Royal Statistical Society, 61:579–602, 1999.

- [15] R. B. Arellano-Valle and A. Azzalini. On the unification of families of skew-normal distributions. Scandinavian Journal of Statistics, 33(3):561–574, 2006.

- [16] Reinaldo B Arellano-Valle and Marc G Genton. Multivariate extended skew-t distributions and related families. Metron, 68(3):201–234, 2010.

- [17] Alan Genz. Numerical computation of multivariate normal probabilities. Journal of Computational and Graphical Statistics, 1(2):141–149, 1992.

- [18] B.G. Manjunath and S. Wilhelm. Moments calculation for the double truncated multivariate normal density. Available at SSRN 1472153, 2009.

- [19] F. Vaida and L. Liu. Fast implementation for normal mixed effects models with censored response. Journal of Computational and Graphical Statistics, 18:797–817, 2009.

- [20] Ashis Kumar Chakraborty and Moutushi Chatterjee. On multivariate folded normal distribution. Sankhya B, 75(1):1–15, 2013.

- [21] L. A. Matos, M. O. Prates, M. H. Chen, and V. H. Lachos. Likelihood-based inference for mixed-effects models with censored response using the multivariate-t distribution. Statistica Sinica, 23:1323–1342, 2013.

- [22] Victor H Lachos, Edgar J López Moreno, Kun Chen, and Celso Rômulo Barbosa Cabral. Finite mixture modeling of censored data using the multivariate student-t distribution. Journal of Multivariate Analysis, 159, 2017. 151-167.

- [23] A. Azzalini and A. Capitanio. Distributions generated and perturbation of symmetry with emphasis on the multivariate skew-t distribution. Journal of the Royal Statistical Society, Series B, 61:367–389, 2003.

- [24] M. D. Branco and D. K. Dey. A general class of multivariate skew-elliptical distributions. Journal of Multivariate Analysis, 79:99–113, 2001.