A Power Analysis for Model-X Knockoffs with -Regularized Statistics

Abstract

Variable selection properties of procedures utilizing penalized-likelihood estimates is a central topic in the study of high dimensional linear regression problems. Existing literature emphasizes the quality of ranking of the variables by such procedures as reflected in the receiver operating characteristic curve or in prediction performance. Specifically, recent works have harnessed modern theory of approximate message-passing (AMP) to obtain, in a particular setting, exact asymptotic predictions of the type I–type II error tradeoff for selection procedures that rely on -regularized estimators.

In practice, effective ranking by itself is often not sufficient because some calibration for Type I error is required. In this work we study theoretically the power of selection procedures that similarly rank the features by the size of an -regularized estimator, but further use Model-X knockoffs to control the false discovery rate in the realistic situation where no prior information about the signal is available. In analyzing the power of the resulting procedure, we extend existing results in AMP theory to handle the pairing between original variables and their knockoffs. This is used to derive exact asymptotic predictions for power. We apply the general results to compare the power of the knockoffs versions of Lasso and thresholded-Lasso selection, and demonstrate that in the i.i.d. covariate setting under consideration, tuning by cross-validation on the augmented design matrix is nearly optimal. We further demonstrate how the techniques allow to analyze also the Type S error, and a corresponding notion of power, when selections are supplemented with a decision on the sign of the coefficient.

1 Introduction

Suppose that we observe a matrix of the measurements of predictor variables on each of subjects, and a response vector , and assume that

| (1.1) |

where and are unknown. In many modern applications where the linear model is appropriate, is large and we may have a reason to believe a priori that is small in magnitude for most . For example, in genetics might encode the state (presence or absence) of a specific genetic variant for individual , and measures a quantitative trait of interest. Typical cases entail the number of genetic variants in the millions but, for all we know about this kind of problems, only a small number of them may have significant explanatory power. Finding mutations which are in that sense important among the candidates, is key to investigating the causal mechanism regulating the trait.

Following recent literature [2, 9, for example], here we treat the problem formally as a multiple hypothesis testing problem with respect to the model (1.1), where the null hypotheses to be tested are

Denote by the (unknown) subset of nulls, and denote by the subset of nonnulls. In general, a multiple testing procedure uses the data to output an estimate of . For any such procedure we define the false discovery proportion and the true positive proportion as

respectively, with the convention . A good testing procedure is one for which TPP is large and FDP is small, meaning that the test is able to separate nonnulls from nulls. We will later be concerned with the concrete problem of controlling the false discovery rate,

below a prespecified level, and we say that a test is valid at level if for all . Note that, per definition, any variable selection procedure qualifies as a testing procedure and vice versa, and we will use the two terms interchangeably.

1.1 Selecting variables by thresholding regularized estimators

With a growing interest in high-dimensional (large ) settings, considerable attention has been given over the past two decades to variable selection procedures relying on the Lasso program,

| (1.2) |

The Lasso is appealing because it is relatively easy to solve and at the same time the solution to (1.2) tends to be sparse. Thus, for any , if denotes the solution to (1.2), variable selection is readily elicited by associating with the subset

| (1.3) |

which will be referred to as Lasso selection for the rest of this paper. Many works have studied the properties of Lasso selection, mostly establishing conditions on and for selection consistency, , e.g. [14, 27, 29, 20, 7, 12]. Such conditions turn out to be generally very stringent even in the noiseless case, ; in other words, the fundamental phenomenon is not a matter of insufficient signal-to-noise ratio. While the conditions for (1.3) to recover a superset of the true support , also referred to as screening, are considerably less restrictive, it tends to select too many null variables (see, e.g., [26, 7, 28]).

This rather discouraging fact has motivated practitioners and theoreticians alike to consider as an alternative the procedure that takes into account the magnitude of the estimate by setting

| (1.4) |

for some threshold [28, 26, 19, 8, 16], to which we refer from now on as thresholded-Lasso selection. Even more generally, one may consider, as in [22], replacing the Lasso estimator in (1.4) with some bridge estimator,

| (1.5) |

where , and we use the symbol from here on instead of the more standard notation (as in the title) because is already taken (denotes the number of columns in ). The optimization problem (1.5) retains computational convenience because it is still convex, and at the same time produces a richer family of thresholded-bridge selection procedures,

| (1.6) |

for some and a threshold . In [22] the above selection procedure is referred to as a two-stage variable selection technique, separating the ranking by the absolute value of the regularized regression estimator, and the thresholding at .

In principle, the parametric curve that associates the expectations of FDP and TPP with every for (1.3), and with every for (1.6), could be used to measure the quality of ranking for Lasso selection or for thresholded-bridge selection with different choices of . For fixed and , however, there are no tractable forms for in general (the special case is an exception), and the expected FDP and TPP are also intractable functions of and .

Remarkably, in a certain asymptotic regime and under some further modelling assumptions, it is possible to calculate the limits of FDP and TPP for (1.3) at any fixed , and for (1.6) at any fixed and . More specifically, in a special case where has i.i.d. Gaussian entries, and grow comparably, and the sparsity is linear, , [6] leveraged major advances from [3, 4] to first obtain exact asymptotic predictions of FDP and TPP for Lasso selection. In [15] a fundamental quantitative tradeoff between FDP and TPP for Lasso, valid uniformly in , was presented by extending the aforementioned results. Recently, [22] obtained predictions of FDP and TPP for thresholded-bridge selection with any , which covers in particular thresholded-Lasso selection.

The main purpose in [22] is to analyze the power corresponding to different choices of in (1.6), and compare them in different regimes of the signal. In particular, while the results of [15] imply that Lasso cannot achieve exact support recovery in this asymptotic setting, [22] show that using thresholded-Lasso can improve dramatically the separation between null and nonnulls if is chosen appropriately. This provides rigorous confirmation for the advantages of thresholded-Lasso, which have long been noticed by practitioners. Also, the analysis in [22] reinforces the results of [16], which imply that in the same asymptotic setting, thresholded-Lasso indeed achieves exact support recovery if the signal-to-noise ratio is high and the limiting signal sparsity is below the transition curve of [11].

1.2 A “vertical” look at the Lasso path

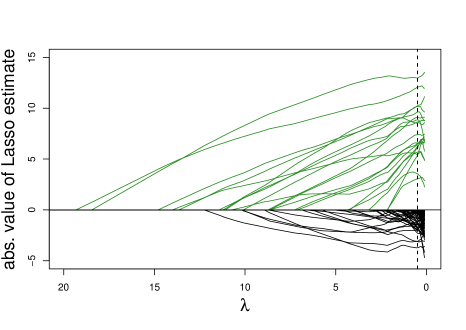

Before proceeding to describe the main focus of this paper, we take a moment to reflect on the basic differences between Lasso selection and thresholded-Lasso selection that account for the potential power increase reported in, e.g., [22]. At first glance, the two selection rules might not appear that different, because (1.3) is just (1.4) with . There is, however, a fundamental difference between Lasso and thresholded-Lasso. To illustrate this, we simulated data from the model with , , , and the coefficients are all zero except for . Figure 1 tracks the absolute value of the Lasso estimates as a function of , for null coefficients and for nonnull coefficients. In Lasso selection variables are collected in the order they become active, , as decreases; pictorially, this corresponds to looking at the selection path “horizontally” along the axis. We can see that false discoveries occur early on the Lasso path (as studied and confirmed in [15]). Consequently, (1.3) cannot keep FDP small unless is chosen large, which inevitably affects the power: in this example the maximum TPP for (1.3) subject to FDP is 0.45.

Nevertheless, it is also evident from the figure that the estimates corresponding to true signals maintain significantly larger size than most of the estimates for nulls, as decreases. This suggests that better separation between null and nonnulls can be achieved by looking further down the path (smaller ) and ordering the variables according to the magnitude of the corresponding estimates; pictorially, this corresponds to looking at the selection path “vertically”, as represented by the dashed line at . The additional flexibility in varying the threshold allows (1.4) to take advantage of this: basically, can be chosen freely, while setting appropriately large will ensure small FDP (by killing small estimates corresponding to null coefficients). The potential advantage is demonstrated in the figure by the broken line, indicating the 10-fold cross-validation estimate of . At this value of , for example, thresholded-Lasso has TPP equal to 0.95 when is selected such that FDP .

1.3 Calibration for Type I error

The works of [15] and [22] are important because they facilitate a sharp theoretical comparison between Lasso selection and the thresholding selection procedures (1.6). In practice, however, the implications are limited: the analysis in these works will yield the achievable asymptotic FDP for a prescribed asymptotic TPP level at any given for (1.3), and at any given for (1.4), provided that and the empirical distribution of the true coefficients are known. In reality, such a priori knowledge about the signal and the noise level is rarely available, and the FDP needs to be estimated instead. This motivated [24] to study a knockoffs-augmented setup and obtain an operable counterpart to the “oracle” FDP-TPP curve of [15] for Lasso selection. By “operable” we mean that the power predictions of [24] apply to a procedure that provably controls the FDR for fixed without any knowledge about or .

Seeking to increase power while maintaining type I error control, in the present article we obtain an operable analog to the FDP and TPP predictions of [22] for the thresholding selection procedures (1.6), with special attention given to thresholded-Lasso selection. As in [24], we employ knockoffs to allow for FDR calibration, observing that the augmented setup can still be studied within the same AMP framework. However, there is a crucial point of departure between our work and [24] also in the type of knockoffs used: while the construction of [24], reviewed briefly in Section 2.3.1 and referred to as “counting” knockoffs in the sequel, is valid only when the entries of are i.i.d., here we use the more general prescription of Model-X knockoffs from [9]. The counting knockoffs scheme studied in [24] is something that the analyst would only implement if it were known that the covariates were i.i.d., as it controls FDR only in this limited setting. In contrast, the model-X knockoffs procedure is something that is widely used across a broad range of regimes, and has valid FDR control far beyond the i.i.d. design setting. While our power analysis for this method is, at present, restricted to the i.i.d. setting, the results in the current paper are far more useful since the analysis accommodates a much more general and broadly used kncokoff scheme (and the power analysis can hopefully be extended beyond the i.i.d. setting in future work).

To further justify studying Model-X knockoffs for i.i.d. covariates, it is important to emphasize that—perhaps not obviously so—the i.i.d. setting is very different from the orthogonal setting: for example, the discussions in [5, Section 3.2.1] and in [15, Section 3] regarding Lasso, imply that due to shrinkage, even small sample correlations between the realized columns of generate additional “noise” as an artifact, which increases the variance of the estimates. This makes the analysis quite different, and more involved, as compared to the orthogonal case. Specifically, the level of this noise increases with the ratio and depends non-monotonically on the tuning parameter , see also Figures 3 and 6 below. That explains, informally, why choosing an appropriate value of (i.e., a value that makes the power large) is far from trivial already in the i.i.d. covariate case under consideration here.

Regarding the comparison with [24], besides the main difference mentioned above in the type of knockoffs, it is worth emphasizing that by implementing Model-X knockoffs, we also obviate the problem of estimating the proportion of nonnulls (i.e., the sparsity), which was a nontrivial issue to handle with counting knockoffs and involved an extra tuning parameter. Table 1 indicates where our work fits in the context of existing literature analyzing variable selection with bridge-penalized statistics in the AMP framework.

1.4 Our contribution

As implied in the previous subsection, the thrust of this article is to develop mathematical tools enabling exact power analysis of Model-X knockoffs procedures, and to study consequences of the resulting analysis. We summarize below our main results.

-

I.

An extension of AMP theory. In the Model-X knockoffs framework the statistic used for ranking the variables will involve both and its knockoff counterpart. Therefore, we need to study aspects of their joint distribution, rather than just the marginal distribution of as in [24]. To accommodate this, we present a technical extension of existing AMP results, which underlies our analysis, but may be of independent interest and have broader implications. The challenge is, in essence, to extend the convergence results in [3] so they apply to functions (of the regression coefficients and their estimates) which are not symmetric with respect to all variables . This basic result is formulated in Theorem 1 (Section 3), and in turn facilitates calculation of the power curves in Corollaries 3.4 and 3.4.

selection by Lasso selection by thresholding Oracle setup Su et al (2017) Wang et al (2020) Knockoffs setup Weinstein et al. (2017+) current paper; Wang and Janson (2021) Table 1: Current paper in the context of related works analyzing variable selection in the approximate message-passing setting. -

II.

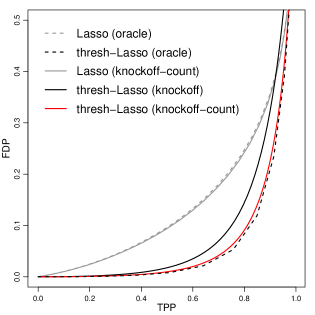

Asymptotic power predictions for Model-X knockoffs. To give an example of the consequences of the theoretical analysis in the current paper, the right panel of Figure 2 shows asymptotic FDP versus TPP as predicted by the theory for Lasso (1.3) and thresholded-Lasso (1.4) in both the oracle and knockoff versions. Here the undersampling ratio , the noise level , and has a mixture distribution of point mass at with probability , and at zero with probability . In the figure broken lines represent the oracle procedures, and solid lines correspond to knockoff procedures. For thresholded-Lasso curves are shown for both Model-X knockoffs (as proposed in the current paper, and depicted in solid black in the figure) and counting knockoffs with fake columns (solid red). For Lasso selection, predictions with Model-X knockoffs are actually harder to obtain, because (2.4) is not as useful an approximation when -statistics are considered, so only the curve for counting knockoffs is shown (solid grey). Importantly, the “oracle” version of thresholded-Lasso is implemented here with the optimal value for , see the discussion in Section 4. For the Model-X knockoffs version of thresholded-Lasso, the value of used here is the limit of the (10-fold) cross-validation estimate, denoted later by .

Comparing first the two oracles, it is clear that thresholded-Lasso has a significantly better tradeoff curve: for example, FDP is about 25% by the time Lasso detects 80% of the signals, whereas thresholded-Lasso is able to detect about 90% of the signal with the same FDP. Turning to the knockoff procedures, it can be seen that counting knockoffs performs slightly better than Model-X; the reason is that counting knockoffs use the lasso coefficient size itself instead of the difference , but this is a small price to pay for Model-X in return for a much more general method. More importantly, both knockoff versions for thresholded-Lasso perform substantially better than the knockoffs version of Lasso, in fact much better than the oracle version for Lasso, and even the universal lower bound of [15] on FDP (see the next paragraph). For example, knockoffs still attains TPP of about 80% with FDP just above 10%.

-

III.

Thresholded-Lasso selection breaks through the power-FDR tradeoff diagram of [15] also when knockoffs are used for calibration. In [15] a power-FDR tradeoff diagram is provided for Lasso selection, which specifies the upper limit on the asymptotic power subject to maintaining ; this diagram depends on the undersampling ratio and the sparsity , but holds independently of the magnitude of the nonzero regression coefficients. A consequence of the results in [15] is that, when the sparsity , Lasso selection will fail to exactly recover the true model. In a recent article [16] proved that the aforementioned tradeoff diagram does not apply to thresholded-Lasso selection. More specifically, it is shown that for any value of the tuning parameter , proper thresholding of the Lasso coefficient estimates identifies the true model as long as the signal is strong enough, and provided , where is the famous Donoho-Tanner phase transition curve. However, the appropriate threshold depends on unknown parameters such as the sparsity and the signal magnitude, hence the practical significance of the results in [16] is limited. In Theorem 2 we give a more quantitative result for the setting considered in the current paper, proving that a Model-X knockoffs analog of the thresholded-Lasso procedure still breaks through the tradeoff diagram of [15]. Thus, for any Model X-knockoffs equipped with the Lasso coefficient-difference [9, LCD hereafter] statistic, achieves power arbitrarily close to 1 if the signal is strong enough and the sparsity is below the transition curve corresponding to the augmented design.

-

IV.

Optimal is well approximated by cross-validation. For a fixed , the performance in terms of achievable TPP of the oracle thresholding selection procedure (1.6) that has (asymptotic) FDP level , in general depends strongly on . For thresholded-Lasso () this is demonstrated in [22], where a characterization is also given for the value of that asymptotically maximizes TPP for a prescribed FDP level. When incorporating knockoffs, the analysis is more subtle because we operate with the difference in the estimate size between a variable and its knockoff counterpart, instead of the estimates themselves. While the dependence of the exact optimal on the unknown parameters of the problem is fairly complicated, we demonstrate that, at least in the case of i.i.d. , the optimal can be well estimated by cross-validation on the augmented design. To allow incorporating this into our asymptotic predictions, in Section 4 we derive the formula for the limiting value of chosen by cross-validation on the augmented design.

2 Setup and review

2.1 Setup

Adopting the basic setting from [15], our working hypothesis entails the linear model (1.1) with fixed and unknown, and we consider an asymptotic regime where such that . We assume that the matrix has i.i.d. entries, so that the columns are approximately normalized. The components of the coefficient vector are assumed to be i.i.d. copies of a mixture random variable,

| (2.1) |

where is a constant, and where . Here , so that . With some abuse of notation, we use to refer to either the random variable or its distribution, but the meaning should be clear from the context. Other than having a mass at zero, is completely unknown, which is to say that and are unknown. Finally, , and are all independent of each other.

Many selection rules first use the observed data to order the variables, that is, for some function , an “importance” statistic

is computed, where larger (say) values of presumably indicate stronger evidence against the null hypothesis that . We assume that has the natural symmetry property that if is obtained from by rearranging the columns, then rearranges the elements of the vector accordingly. 111Formally, the requirement is that for any permutation on , , where is defined to be the matrix with its -th column equal to the -th column of . This mild condition is needed also in [9]. Given a target FDR level , a final model can then be selected by taking

| (2.2) |

where is a threshold that may generally depend on the observed data. For any choice of the importance statistic (i.e., for any choice of ), we define

| (2.3) |

again with the convention 0/0 = 0. In the rest of the paper we will consider importance statistics that derive from the convex program (1.5). As presented in the Introduction, the case of in the bridge optimization program (1.5) is of particular interest here, because in the Lasso case the estimator itself is sparse and can be used directly for variable selection. Therefore, we generally focus on the case from now on, but, importantly, our new results are stated for any to match the generality in [22].

2.2 Basic AMP predictions

For the Lasso program (1.2), we start with noting that, on defining

| (2.4) |

we have , because only variables that drop out from the Lasso path—that is, for which but for —can contribute to the difference between the quantities; see discussion in [24]. Therefore, we treat the comparison between (1.3) and (1.4) as essentially a comparison between two procedures of the form (2.2), where is given by (2.4) for Lasso, and by

| (2.5) |

for thresholded-Lasso. In anticipation of Section 3, we call (2.4) the Lasso-max statistic, and we call (2.5) the Lasso-coefficient statistic.

Remarkably, under the working hypothesis, exact asymptotic predictions of FDP and TPP can be obtained for both Lasso and thresholded-Lasso. Stated informally, Theorem 1 in [3] asserts that under our modeling assumptions, in the limit as we can “marginally” treat

| (2.6) |

and we use a dot above the “” symbol to indicate that this holds only in that restricted sense. Above, is the soft-thresholding operator (acting coordinate-wise); and independent of ; and is the unique solution to

| (2.7) | ||||

Furthermore, is the unique root of the equation . This result underlies the analysis in [15], where it is formally shown (Lemma A.1) that

| (2.8) | ||||

with and as described above. For a general importance statistic , define

where the limits are in probability. We use special notation for the limiting FDP and TPP corresponding to the Lasso-max and to the Lasso-coefficient statistics: for the choice of in (2.4) we write and , and for the choice of in (2.5) we write and . In [24], (2.8) was used to approximate

| (2.9) | ||||

where are the solution to (2.7) on replacing by .

In a more recent work, [22] observed that the implications of [3] can, with the necessary adaptations, be used to analyze TPP and FDP also for selection rules of the form (1.6). In particular, for thresholded-Lasso, Lemma 2.2 in [22] asserts that

| (2.10) | ||||

It then follows that

| (2.11) | ||||

where are determined by through (2.7). Hence, the asymptotic TPP and FDP in (2.11) depend on the value of at which the Lasso estimates are computed. Theorem 3.2 in [22] further identifies the asymptotically optimal value of , proving that for any ,

where

| (2.12) |

By inspection, we see that an equivalent characterization of is the value of corresponding to the minimum in (2.7). This characterization is useful for computing as a function of .

2.3 Model-X knockoffs for FDR control

The choice of an adequate feature importance statistic is crucial for producing a good ordering of the ’s, from the most likely to be nonnull to the least likely to be nonnull. A separate question is how to set the threshold in (2.2) so that the FDR is controlled at a prespecified level. Inspired by [2], [9] proposed a general method for the random-X setting, Model-X knockoffs, that utilizes artificial null variables for finite-sample control of the FDR. Assuming that the distribution of the vector is known (but arbitrary), the basic idea is to introduce, for each of the original variables, a fake control so that, whenever , the importance statistic for the -th variable is indistinguishable from that corresponding to its fake copy. This property can then be exploited by keeping track of the number of fake variables selected as an estimate for the number of false positives.

Under our working assumptions, the components are i.i.d., in which case the construction of Model-X knockoffs is trivial. Thus, let be a matrix with i.i.d. entries drawn completely independently of , and , so that it holds in particular that and are independent conditionally on . We refer to as the augmented -matrix.

Ranking of the original features is based on contrasting the importance statistic for variable with that for its knockoff counterpart where, crucially, all importance statistics are computed on the augmented matrix. Thus, to obtain the analog of the selection procedure in (1.6), we first compute the -vector given by

| (2.13) |

instead of (1.5), and form the differences

| (2.14) |

Because is a valid matrix of Model-X knockoffs, we have from Lemma 3.3. in [9] that the signs of the , are i.i.d. coin flips (in fact, when , are i.i.d., as considered here, this is easy to see directly from symmetry). In the knockoffs framework, variables are selected when their is large, that is,

| (2.15) |

where is a data-dependent threshold. The idea is to rely on the “flip-sign” property of the to choose . Concretely, applying the knockoff filter by putting

| (2.16) |

ensures that the selection rule given by (2.15) controls the FDR at level by Theorem 3.4 in [9].

To obtain the knockoffs counterpart of thresholded-Lasso selection, we specialize (2.14) to , recovering the Lasso coefficient-difference (LCD) statistic introduced in [9],

| (2.17) |

where

| (2.18) |

is the Lasso solution for the augmented setup, i.e., the estimator (2.13) obtained for . The corresponding selection procedure in (2.15) will be referred to from now on as the level- LCD-knockoffs procedure.

Similarly to the notation in Section 2, we write , respectively, for and associated with the statistic (2.17). Finally, let

be the limit of the (knockoffs) estimate of FDP given in (2.16) for .

Before proceeding to the main section, we recall an alternative implementation of knockoffs for the special case of i.i.d. matrices.

2.3.1 “Counting” knockoffs for i.i.d. matrices

In the special case where are i.i.d., there is in fact a simpler approach to implementing a knockoff procedure, as proposed in [24]. Instead of pairing each original covariate with a designated knockoff copy ( with ), we can leverage the information that the covariates are i.i.d., and therefore exchangeable, to create a single pool of knockoff variables that act as a “control group” simultaneously for each .

To be concrete, for some integer , suppose we make the matrix of dimension instead of , still with i.i.d. entries as before. Then by the symmetry in the problem, the distribution of the fitted coefficient vector (conditional on ) is unchanged under any reordering of the indices in the “extended” null set,

where . This is a stronger notion of exchangeability (all null covariates are exchangeable with all knockoff variables), as compared to the pairwise exchangeability property of the general Model-X framework (where each null is only exchangeable with its own knockoff copy ). Exploiting this stronger form of exchangeability, [24] prove FDR control—for example, we could take the procedure that rejects whenever for222 We note that, while [24] focus on a different statistic, all of their results concerning FDR control apply equally well to what we call the Lasso-coefficient statistic in the following section.

| (2.19) |

and use AMP machinery to derive the appropriate formulas for the power. In particular, power is gained from the fact that, if we choose to be smaller than (e.g., for some ), the variable selection accuracy of the Lasso is better since we have observations and many covariates, rather than observations and covariates as with Model-X knockoffs.

However, the counting knockoffs strategy is extremely specific to the i.i.d. design setting: if the ’s are not themselves i.i.d. (or exchangeable), then we cannot hope to construct a single control group that can be shared by a heterogeneous set of covariates. The Model-X construction, with knockoff designed to pair with , is therefore substantially more interesting to study in terms of understanding the performance of this methodology in non-i.i.d. settings.

3 AMP predictions for knockoffs

The results presented thus far are not novel. In this section we find the asymptotic FDP and TPP for the Model-X knockoffs versions of the thresholded-bridge selection rules (1.6), in particular for the level- LCD-knockoffs procedure, and present new results. For the knockoffs procedure to control the FDR, the i.i.d. Gaussian assumption on the coordinates of is by no means necessary, and there is indeed no such assumption in [9]. In the current paper, on the other hand, the goal is to compare the (asymptotic) power of the “oracle” thresholded-bridge selection procedure (1.6) to that of its knockoffs version. In particular, for we ultimately want to compare the curves

| (3.1) |

where the quantities and are defined, respectively, as the values and for which

| (3.2) |

Of course, how the two curves in (3.1) compare on power at every given , depends on the underlying model, including the dependence structure among the coordinates of . We now proceed to obtaining power predictions for Model-X knockoffs under the asymptotic setting of Section 2.1.

The main technical challenge is to validate that the theory from [4] carries over to the knockoff setup involving -statistics. To overcome this technical challenge, we develop a “local” version of AMP theory that applies to the broad class of knockoff-calibrated selection procedures in (2.15). More specifically, as compared to (2.6), in order to analyze the knockoffs selection procedure (2.15) we need to study the triples rather than the pairs . Theorem 1 below asserts that, for our asymptotic FDP and TPP calculations, we can treat

| (3.3) |

which is an extension of (2.6). Above, and are independent random variables that are furthermore independent of , the operator with threshold level is defined as

| (3.4) |

and are the unique solution to the equation [25]

| (3.5) | ||||

In the special case , where the bridge estimator is just the Lasso estimator, the operator reduces to the soft-thresholding operator , and (3.5) becomes

| (3.6) | ||||

The following theorem formalizes the notion in which (3.3) holds, and is our main theoretical result.

Theorem 1.

Let be any bounded continuous function defined on . Then, we have

in probability. Here are the unique solution to (3.5), and and are two independent standard normal random variables, which are further independent of .

Remark 3.1.

Note that the generalized soft-thresholding operator (3.4) satisfies for any .

For the special Lasso case, , we actually have the stronger result below.

Proposition 3.2.

The proofs of Theorem 1 and Proposition 3.2 are deferred to Appendix A.2. For the Lasso case , a similar result was obtained in a simultaneous and independent work by [23, see their Theorem 6 and the corresponding analysis]. There are, however, some differences. First, our Theorem 1, of which the first assertion in Proposition 3.2 is a direct consequence, applies more generally to any bridge estimator with . Second, the techniques we use in the proof are quite different, and these allow us to establish uniform convergence in for the Lasso case in second assertion of Proposition 3.2. The uniform convergence is essential for our results to apply when selecting by cross-validation, as we recommend in Section 4. Proposition 3.2 is also closely related to Corollary 1 in [3], which can be viewed as a “marginal” version of the above assertion: in the Model-X knockoffs context, [3] implies the convergence of a sum over all pairs such that , as opposed to “diagonal” pairs for in Proposition 3.2 above. Corollary 1 in [3] then follows by making use of its conditional (hence stronger) counterpart, Proposition 3.2. More generally, just as Corollary 1 in [3] applies to a tuple of any number of indices, Proposition 3.2 can be readily extended to multiple knockoffs (where several knockoff copies are generated for each original variable). This extension would enable a theoretical comparison similar to that presented in the current paper except with multiple knockoffs, and we leave this interesting direction for future research.

Theorem 1 allows us to calculate the limits of and for the selection path of the -statistic (2.14) for any , which includes the LCD statistic as a special case.

Corollary 3.3.

For fixed and , consider the variable selection procedure given by (2.15). Then the asymptotic FDP and TPP at any fixed threshold are, respectively,

| (3.7) | ||||

Moreover, Theorem 1 allows us to calculate the limit of the corresponding knockoffs estimate of the FDP.

Corollary 3.4.

Fix and . Then for any , the limit of in Equation (2.16) is given by

| (3.8) |

Remark 3.5.

See the proofs of these two corollaries in Appendix A.2. It can be shown that the convergence is uniform in bounded .

In particular, from Corollaries 3.4 and 3.3 we can calculate , the asymptotic TPP achievable by the level- LCD-knockoffs procedure: setting , for a given first compute as the value of such that

and then plug it into the second equation in (3.7) to find . It is easy to verify the relationship

| (3.9) |

so that overestimates , the actual asymptotic FDP. However, the difference between the two is typically very small: because the random variable is designed to tend to large values when , the second term on the right hand side of (3.9) is typically much smaller than , for example it converges to zero when the magnitude of nonzero elements of increases. In other words, using the observable random variable in (2.16) instead of , does not make LCD-knockoffs overly conservative. We note that the conservativeness was a nuisance in the (alternative) “counting” knockoffs implementation in [24], where an estimate of that requires an extra (user-specified) tuning parameter, was incorporated to mitigate the effect. Here, conveniently, the use of -statistics obviates the need to estimate .

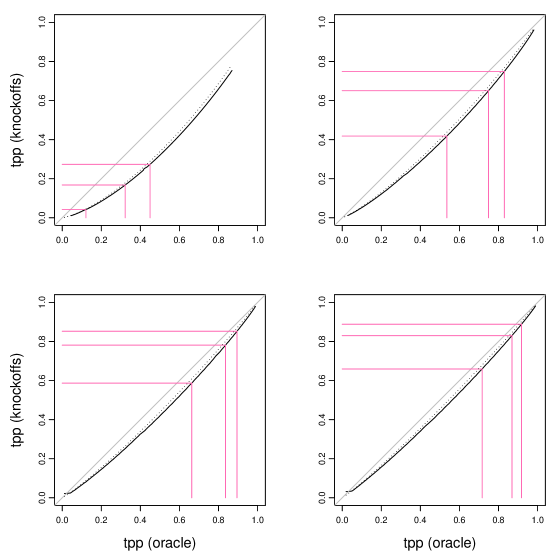

Figure 3 shows knockoffs power, , against “oracle” power ,, when the nominal FDR value varies. We took , and to be a mixture of mass at zero and mass at , while varies in the four panels. The tuning parameter is selected separately for each procedure: for the oracle, this is the optimal obtained by minimizing the value of ; for knockoffs, we use the limit of the (10-fold) cross-validation estimate, see Section 4. We can see that for , the powers obtained by knockoffs and the oracle are very similar for any . When is smaller, the loss of power is more pronounced. This is mainly because the Lasso estimate itself has larger variance for small values of ; see the left panel of Figure 5. However, for all considered values of the relative difference decreases with the power of the oracle (i.e., when or the magnitude of nonzero elements of increases). The dotted lines in Figure 4 are obtained by implementing “counting” knockoffs instead of Model-X knockoffs (); the power curve is slightly better as compared to Model-X knockoffs because the importance statistic itself is used for each feature rather than the -statistic.

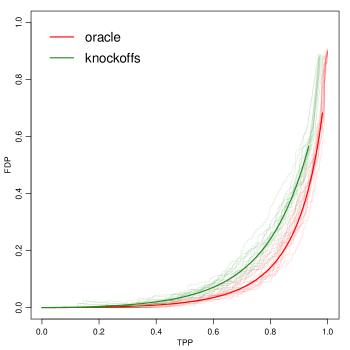

Figure 4 complements Figure 3 by showing FDP-TPP tradeoff paths from a simulation, with the theoretical asymptotic predictions superimposed. For both the oracle and the knockoffs versions of thresholded-Lasso we plotted the tradeoff curve in each of 15 realizations from an example with (the other parameters are as in Figure 4). To avoid crowding the figure, we plot only the paths for Model-X knockoffs (and not for counting knockoffs). We can see a good agreement between the empirical results and the theory.

We conclude this section with Theorem 2 below, that applies to the Lasso case and formalizes the notion that the LCD-knockoffs procedure allows to break through the FDP-TPP diagram presented in [15]. Specifically, the following result says that for any nominal FDR level that is not too close to 1, if the signal is strong enough then the LCD-knocknoffs procedure has asymptotic power arbitrarily close to one, as long as the signal sparsity satisfies

| (3.10) |

where is a point on the Donoho–Tanner transition curve [11].

Definition 3.6.

A sequence of random variables is said to be -sparse and growing, if for all , and

as for every .

Theorem 2.

Fix and denote by the true positive proportion of the level- LCD-knockoffs procedure that uses parameter . Moreover, fix such that (3.10) holds. Then for any sequence that is -sparse and growing, it holds that for any fixed and any , there exist and such that

if and .

Remark 3.7.

4 Tuning by cross-validation

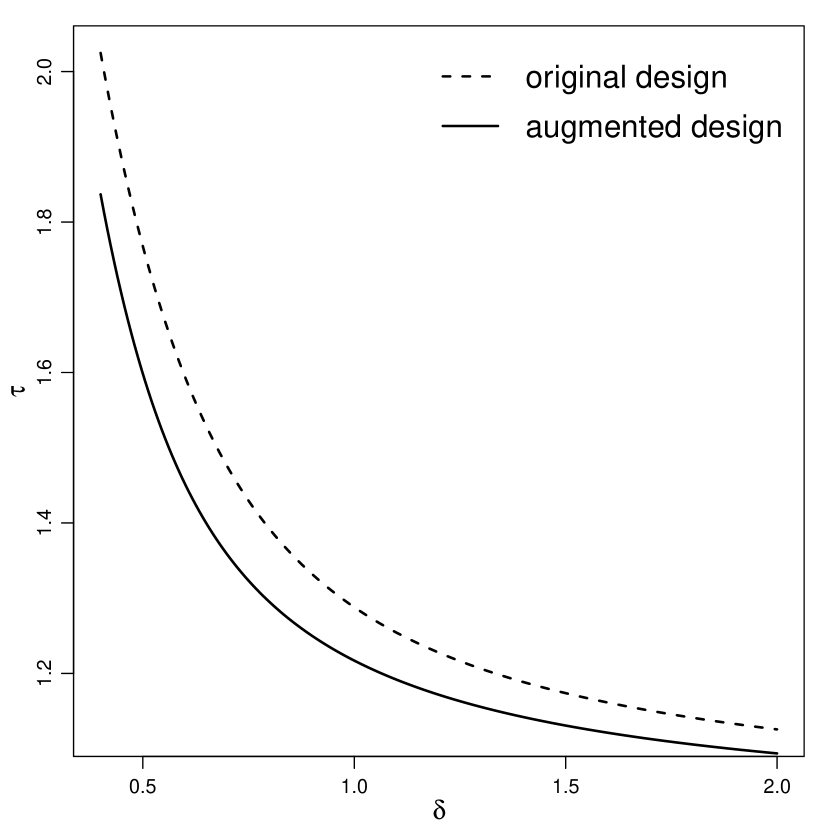

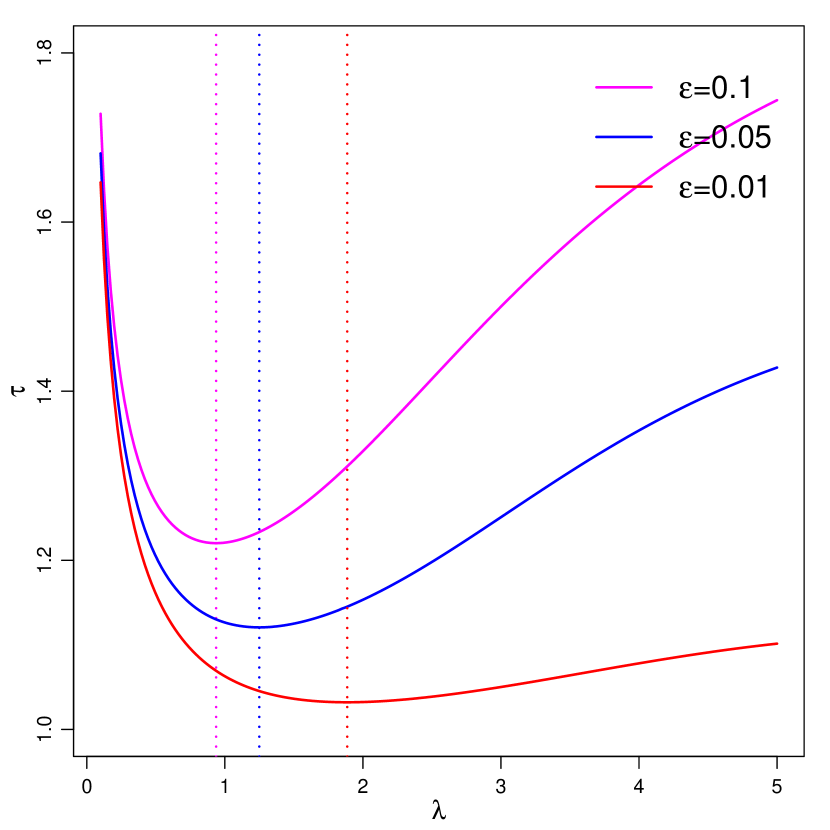

The choice of in the level- LCD-knockoffs procedure is critical. Unlike in the orthogonal situation, the value of substantially affects the ranking of the variables, because controls the shrinkage of the Lasso estimates. The advantage of the asymptotic theory is that it provides an analytic form for the relationship between and the parameter , so we can use this to characterize a good choice of by its consequences on the value of . Figure 5 below illustrates the dependence of on for and different values of . Here we can see clearly that the relationship is not monotone and that the choice (i.e., recovering the the Basis Pursuit criterion) as well as excessively large would result in an inflation of the variance of estimates.

Turning to the formal analysis, let , where is the smallest positive value such that . Then Theorem 3.2 in [22] asserts that, for any ,

In words, the value of minimizing the asymptotic estimation mean squared error (MSE) is also the optimal for the testing problem. [22] then observe that minimizing the asymptotic MSE, , is in turn equivalent to minimizing in (2.7) over . Because the minimizer of depends on and , [22] propose to estimate in practice by minimizing a consistent estimate of .

If the only difference between knockoffs and the oracle were the fact that the augmented -matrix is used instead of the original -matrix, we would be able to conclude immediately that the optimal tuning parameter for LCD-knockoffs is the value of minimizing in (3.6) instead of (2.7). This is, however, not the only difference, first because knockoffs use -statistics instead of , and secondly because knockoffs utilize an estimate of FDP instead of the actual FDP in setting the threshold. Admittedly, the exact value of that is optimal for knockoffs no longer has such a simple characterization, but we can still advocate the minimizing in (3.6) as a good approximation, and this is our target. Figure 6 demonstrates that this approximation is indeed a good one.

The value of minimizing in (3.6) again depends on the unknown and . To estimate it, instead of relying on a consistent estimator of as in [22], we propose to use cross-validation on the augmented design. This takes advantage of the fact that when the covariates are i.i.d., minimizing the estimation error is equivalent to minimizing the prediction error. Hence, from now on we write for the -fold cross-validation estimate of operating on the augmented -matrix. We can again predict the exact limit of as follows.

Lemma 4.1.

How to obtain is not immediate from Lemma 4.1: for any value of , is itself given implicitly as the solution to an equation system in two variables, which then needs to be minimized over . We can nevertheless define a simple procedure for solving this minimization problem, described in Appendix B and ultimately yielding the system of equations

| (4.2) | ||||

We call (4.2) the CV-AMP equations. To obtain , we solve the CV-AMP equations, and then use the second equation of (3.6) with substituted for and with substituted for .

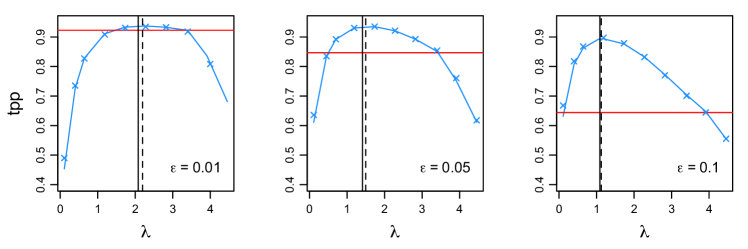

Figure 6 shows power against for the LCD-knockoffs procedure applied at level . For reference, horizontal lines indicate theoretical power for the knockoffs procedure utilizing the Lasso-max statistic (2.4) (computed on the augmented matrix). The latter is obtained from [24] and uses “counting” knockoffs with the true underlying value of . For LCD, the theoretical predictions are consistent with the simulation results (marker overlays), and demonstrate how drastically power can vary with the choice of the tuning parameter. In particular, bad choices of can lead to smaller power than even the knockoffs version of Lasso (1.3). Vertical solid lines indicate the value of , and they indeed seem close to optimal, i.e., close to the value that maximizes power. The broken vertical lines represent the simulation average for the -fold cross-validation . In accordance with the right panel of Figure 5, we can see that the optimal value of decreases when increases.

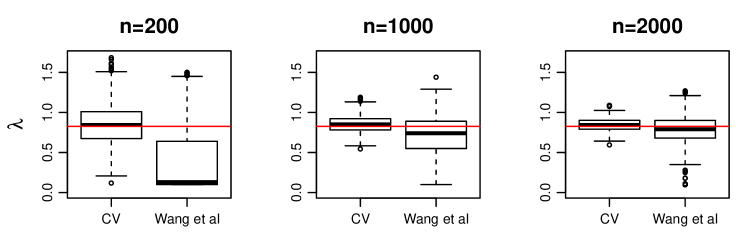

The boxplots in Figure 7 show sampling variability in simulation runs for the cross-validation estimate of and for the estimate of [22]. In all panels we used , , and has mass at zero and mass at . The red horizontal line indicates for . Sampling variability for cross-validation appears smaller. Another (unrelated) advantage of cross-validation is that we have an explicit characterization of through the CV-AMP equations, whereas the analog for the method of [22] is given implicitly as a minimizer of a certain estimate.

5 Extension to Type S errors

The classical paradigm, which was also adopted here, regards a predictor as important if the corresponding , and aims at controlling a Type I error rate. In practice, however, it is almost always the case that all are different from zero to some decimal, in which case the Type I error trivially vanishes. In the more general context of multiple comparisons, this has lead to adamant objection to focusing on testing of point null hypotheses [18, 17]. A reasonable way out is to consider a predictor as important only if for some , but this has the disadvantage that the definition depends on . Alternatively, Tukey [18] advocated procedures that classify the sign of “with confidence”, that is, declare or for as many as possible while keeping small some rate of incorrect decisions on the sign. Incorrectly declaring that when in fact , or that when in fact , is commonly referred to as a Type S [13] or Type III error. For hypothesis testing problems of the type considered in this paper, it is natural to ask what consequences supplementing each rejection with a directional decision has on the error rate.

As in [1], suppose that for each ‘rejection’ we further provide an estimate

of the sign of . We define the false sign proportion to be

where is 1,-1 or 0 according as or . In particular, we can see that

since any false discovery (i.e., selecting when in fact ) leads to a sign error, . The false sign proportion may often be much higher than the false discovery proportion—indeed, as demonstrated in [13], in a low signal-to-noise regime it is easy for a false discovery rate controlling procedure to have very high false sign rate.

In the sign-classification framework, we can apply our results to obtain exact asymptotic predictions of the FSP and a corresponding notion of power, for the knockoff procedures in our setting. Thus, write the nonzero component of the distribution of as

where and where . Now suppose that for the knockoffs version of the thresholded bridge selection procedure (1.5), we further estimate for each , where . Taking the Lasso case for example, we can apply Theorem 1 to conclude that the procedure that supplements LCD knockoffs with the sign estimates has

| (5.1) | ||||||

To quantify the power of a procedure in the sign problem, it may at first seem natural to consider the ratio of the number of correctly classified signs divided by the total number of nonzero ’s. But, in a regime where there are no exact zeros among the coefficients, this definition is not useful because the denominator will equal , the total number of coefficients, although most (usually, almost all) of the coefficients are still too close to zero in magnitude to be picked up by the selection procedure.

To overcome this difficulty, we consider a different model, where the distribution of is again a mixture between signals (the “slab”) and nulls (the “spike”), but now the null distribution is concentrated near zero instead of being a point mass at zero. In particular, let and indicate if is considered to be a “null” or “nonnull” coefficient, respectively, and assume the following distribution:

where, consistent with Tukey’s viewpoint mentioned earlier, we will assume that neither of has point mass at zero, but still represents a “spike” and is concentrated near zero and represents a “slab” component of the mixture. Notice that this “two group” model entails

| (5.2) |

as the distribution of , analogous to (2.1). The true sign proportion is then defined as

| (5.3) |

where .

Appealing again to Theorem 1, the limit of TSP for the knockoffs sign-classification version of (1.4) can be calculated as

| (5.4) | ||||

where , and where is the conditional distribution of given and is the conditional distribution of given .

We turn to discussing asymptotic FSP control under the assumption that has no point mass at zero. Recall that by the definition we use for FSP, which subsumes incorrect rejections of zero coefficients, FSP is formally at least as large as FDP in any setting—but, in this specific case, we will actually have FDP since there are no exact zeros. Nonetheless, we will now show that in our new model (5.2) that replaces exact zeros with approximate zeros, the Model X knockoffs at the nominal FDP level can control FSP at the level . The factor of 2 is due to the fact that, in this new model, for any we can only err in one direction, while in the idealized model where nulls are exactly zero, estimating either a positive or negative value for results in an error.

To show this formally, we will compare two different scenarios: first, we will consider the false sign rate under the model

where there are no exact zeros as in (5.2), and second, we will consider the false discovery rate under the model

where now there are exact zeros as in (2.1). To avoid confusion between these two distributions, we will write and for these two quantities of interest, respectively, to emphasize that we are working with two different distributions. Nevertheless, if the “spike” distribution is concentrated extremely close to zero, then the two resulting data distributions are essentially indistinguishable, which is why we can compare the two. Formally, below we will show that

which is approximately if . To make the argument clearer, for the rest of this section we denote , , and . Then

where in the last step we observe that for any . Notice that, since was arbitrary, this holds also for the asymptotic knockoff threshold . Moreover, observe that by continuity of the formula for , when the ”null” distribution converges to the point mass at zero. Thus, for and sufficiently concenrated around 0 it holds

which allows to conclude that knockoffs allow for the asymptotic FSP control under .

In fact, when is sufficiently concentrated around zero, and sufficiently dispersed, the formulas above will imply

| (5.5) |

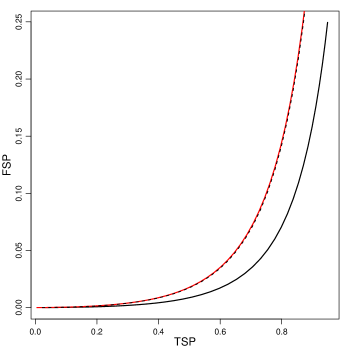

Figure 8 shows the parametric curve for a setting with , , and is point mass at . The red curve in the figure shows vs. , i.e., this is the curve from Figure 2. The relationship (5.5) is verified by plotting (dotted black line) the curve , which essentially coincides with the red curve.

Acknowledgement

A. W. is supported by ISF via grant 039-9325. W. J. S. is partially supported by NSF via grant CCF-1934876, and by the Wharton Dean’s Research Fund. M. B. is supported by the Polish National Center of Science via grant 2016/23/B/ST1/00454. R. F. B. is supported by NSF via grant DMS-1654076, and by the Office of Naval Research via grant N00014-20-1-2337. E. C. is partially supported by NSF via grants DMS 1712800 and DMS 1934578.

References

- [1] R. F. Barber and E. J. Candès. A knockoff filter for high-dimensional selective inference. The Annals of Statistics, 47(5):2504–2537, 2019.

- [2] R. F. Barber, E. J. Candès, et al. Controlling the false discovery rate via knockoffs. The Annals of Statistics, 43(5):2055–2085, 2015.

- [3] M. Bayati and A. Montanari. The dynamics of message passing on dense graphs, with applications to compressed sensing. IEEE Transactions on Information Theory, 57(2):764–785, 2011.

- [4] M. Bayati and A. Montanari. The LASSO risk for Gaussian matrices. IEEE Transactions on Information Theory, 58(4):1997–2017, 2012.

- [5] M. Bogdan, E. van den Berg, C. Sabatti, W. J. Su, and E. J. Candès. Adaptive variable selection via convex optimization. Annals of Applied Statistics, 9(3):1103–1140, 2015.

- [6] M. Bogdan, E. van den Berg, W. J. Su, and E. J. Candès. Statistical estimation and testing via the sorted norm. arXiv preprint arXiv:1310.1969, 2013.

- [7] P. Bühlmann and S. van de Geer. Statistics for High-Dimensional Data: Methods, Theory and Applications. Springer, 2011.

- [8] P. Bühlmann and S. van de Geer. Statistics for High-Dimensional Data: Methods, Theory and Applications. Springer, New York, 2011.

- [9] E. Candes, Y. Fan, L. Janson, and J. Lv. Panning for gold: Model-x knockoffs for high dimensional controlled variable selection. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80(3):551–577, 2018.

- [10] N. L. Carothers. A short course on approximation theory. Department of Mathematics and Statistics, Bowling green State University, 1998. http://fourier.math.uoc.gr/~mk/approx1011/carothers.pdf.

- [11] D. L. Donoho and J. Tanner. Observed universality of phase transitions in high-dimensional geometry, with implications for modern data analysis and signal processing. Philosophical Trans. R. Soc. A, 367(1906):4273–4293, 2009.

- [12] C. Dossal. A necessary and sufficient condition for exact sparse recovery by l1 minimization. Comptes Rendus Mathematique, 350(1):117–120, 2012.

- [13] A. Gelman and F. Tuerlinckx. Type s error rates for classical and bayesian single and multiple comparison procedures. Computational Statistics, 15(3):373–390, 2000.

- [14] N. Meinshausen and P. Bühlmann. High-dimensional graphs and variable selection with the lasso. The Annals of Statistics, 34(3):1436–1462, 2006.

- [15] W. J. Su, M. Bogdan, and E. J. Candès. False discoveries occur early on the lasso path. The Annals of Statistics, 45(5):2133–2150, 2017.

- [16] P. J. C. Tardivel and M. Bogdan. On the sign recovery by LASSO, thresholded LASSO and thresholded Basis Pursuit Denoising. arXiv:1812.05723, to appear in Scandinavian Journal of Statistics, 2018.

- [17] J. W. Tukey. Conclusions vs decisions. Technometrics, 2(4):423–433, 1960.

- [18] J. W. Tukey. The philosophy of multiple comparisons. Statistical science, pages 100–116, 1991.

- [19] S. Van de Geer, P. Bühlmann, and S. Zhou. The adaptive and the thresholded lasso for potentially misspecified models (and a lower bound for the lasso). Electronic Journal of Statistics, 5:688–749, 2011.

- [20] M. J. Wainwright. Sharp thresholds for high-dimensional and noisy sparsity recovery using constrained quadratic programming (lasso). IEEE transactions on information theory, 55(5):2183–2202, 2009.

- [21] H. Wang, Y. Yang, and W. J. Su. The price of competition: Effect size heterogeneity matters in high dimensions. arXiv preprint arXiv:2007.00566, 2020.

- [22] S. Wang, H. Weng, and A. Maleki. Which bridge estimator is the best for variable selection? The Annals of Statistics, 48(5):2791–2823, 2020.

- [23] W. Wang and L. Janson. A high-dimensional power analysis of the conditional randomization test and knockoffs. Biometrika, 2021.

- [24] A. Weinstein, R. Barber, and E. J. Candès. A power and prediction analysis for knockoffs with lasso statistics. arXiv preprint arXiv:1712.06465, 2017.

- [25] H. Weng, A. Maleki, and L. Zheng. Overcoming the limitations of phase transition by higher order analysis of regularization techniques. The Annals of Statistics, 46(6A):3099–3129, 2018.

- [26] F. Ye and C. H. Zhang. Rate minimaxity of the lasso and Dantzig selector for the loss in balls. J. Mach. Learn. Res., 11:3519–3540, 2010.

- [27] P. Zhao and B. Yu. On model selection consistency of lasso. The Journal of Machine Learning Research, 7:2541–2563, 2006.

- [28] S. Zhou. Thresholding procedures for high dimensional variable selection and statistical estimation. In Advances in Neural Information Processing Systems, pages 2304–2312, 2009.

- [29] H. Zou. The adaptive lasso and its oracle properties. Journal of the American statistical association, 101(476):1418–1429, 2006.

Appendix A Proofs

We prove Theorems 1 and 2 in this appendix. The proofs rely heavily on some extensions of AMP theory and approximation results for continuous functions, which we first present in Section A.1 and the beginning of Section A.2, respectively.

A.1 Local AMP lemmas

Following the setting of AMP theory as specified earlier in Section 2, we present some extensions of AMP theory for the Lasso method. We call these results local AMP lemmas because these results apply to a subset of the coordinates of the coefficients, unlike the existing AMP results which apply to the entire set of coordinates.

Throughout this appendix, we use to denote convergence in probability. For simplicity, we also denote . Recall that are the unique solutions to the set of equations (3.5).

Lemma A.1.

Let and be two bounded continuous functions. We have

Lemma A.1 is the main contribution of this subsection. Its proof relies on the following three lemmas and we defer the proofs of these preparatory lemmas later in this subsection.

Lemma A.2.

Let be any bounded continuous function. We have

Lemma A.3.

Let be any bounded bivariate continuous function. We have

Lemma A.4.

For any numbers and , denote by and their respective means. Let be drawn from all permutations of uniformly at random. Then, we have

Proof of Lemma A.1.

By Lemma A.2, we have

and Lemma A.3 gives

Now, let us consider the distribution of

| (A.1) |

conditional on and the empirical distribution of . This -algebra is denoted as . Note that knowing the empirical distribution of is the same as knowing all values of except for the indices. By symmetry, the conditional distribution of (A.1) is the same as that of

where is a permutation of drawn uniformly at random. Then, first we know

which converges to the constant

Recognizing the boundedness of , which results from the boundedness of the terms of this sum, a consequence of the above implies

| (A.2) |

Moreover, due to the boundedness of , it must hold that

| (A.3) | ||||

Now, we consider the variance and write for the supremum of a function . To begin, we invoke Lemma A.4, from which we get

as . Therefore, its boundedness gives

| (A.4) |

Thus, from (A.2) and (A.4) we get

| (A.5) | ||||

∎

In the remainder of this subsection, we complete the proof of Lemmas A.2, A.3, and A.4. In the proof of Lemma A.2, we need the following preparatory lemma.

Lemma A.5.

Let be a triangular array of bounded random variables such that are exchangeable for every and as . If for a constant ,

as , for an arbitrary (deterministic) sequence satisfying and , we must have

Proof of Lemma A.5.

Fix any . We will show that

For any let be a random subset of of cardinality , drawn independently of the . Then by exchangeability, is equal in distribution to . Therefore we equivalently need to show that

We trivially have

The assumption implies that

Next we bound the remaining term. Recall that the ’s are bounded, so we can assume for some finite . We then have

since sampling uniformly with replacement always has variance no larger than sampling uniformly without replacement, and the ’s are bounded. Therefore,

almost surely. Marginalizing,

which tends to zero as since is fixed and . This completes the proof. ∎

Now, we are ready to prove Lemma A.2.

Proof of Lemma A.2.

It suffices to prove the lemma for any bounded Lipschitz continuous functions. To see this sufficiency, assume for the moment that

| (A.6) |

if is bounded and Lipschitz continuous. Let be a continuous function that satisfies for all . We show below that

| (A.7) |

Let be an arbitrary small number. As a consequence of Lemma A.7 presented in Section A.2 below, if is sufficiently large, then

| (A.8) |

with probability tending to one as . As is clear, one can find a Lipschitz continuous function defined on a compact set, for example, that satisfies

| (A.9) |

for all . We can extend to a bounded Lipschitz continuous function defined on . This can be done, for example, by setting if and let be linear on and . Hence, (A.6) holds for . Let be an upper bound of in the sense that for all (we can take ). To show (A.7), we first write

and

where the indicator function takes the value 1 if the event in the subscript happens and takes the value 0 otherwise. This gives

where in the second last inequality we use (A.9), and the last inequality follows from (A.8) and thus holds with probability tending to one. Similarly, we can show that the difference between and can be made arbitrarily small if is small enough. Taking , therefore, we see that (A.6) implies (A.7).

To conclude the proof of this lemma, therefore, it is sufficient to prove (A.6) for any bounded Lipschitz continuous function . For convenience, we write in place of and assume that is bounded by in magnitude and is -Lipschitz continuous. Consider the function

for . Our first step is to verify that this function is Lipschitz continuous and is, therefore, pseudo-Lipschitz continuous (see the definition in [4]). Writing for , we note that

This proves that is Lipschitz continuous. Using Theorem 2.1 of [25], therefore, we get

| (A.10) |

for any fixed , where the random variable with probability and otherwise . Note that Theorem 2.1 in its present form considers a bridge estimator of order and can be extended to any (personal communication).

Now we will take on the right-hand side of (A.10). Recognizing that

if and otherwise as , the boundedness of allows us to use Lebesgue’s dominated convergence theorem to obtain

| (A.11) | ||||

Turning to the left-hand side of (A.10), we use the fact that for any , one can find such that

| (A.12) |

with probability approaching one for each . To see this, note that

of which the expectation satisfies

since places no mass at zero, by definition. This inequality in conjunction with the Markov inequality reveals that (A.12) holds if is sufficiently small.

Writing

and taking , we get

from (A.11), (A.10), and (A.12). This is equivalent to

| (A.13) |

which makes use of the fact that

| (A.14) |

To conclude the proof of this lemma, we apply Lemma A.5 to (A.13). This is done by letting and and and . For completeness, we remark that the randomness of does not affect the validity of Lemma A.5 due to (A.14). Thus, we get

This completes the proof.

∎

Proof of Lemma A.3.

As with Lemma A.2, it is sufficient to prove the present lemma for any bounded Lipschitz continuous functions. By Theorem 1.5 of [4], we get

| (A.15) |

Note that the right-hand side can be written as

| (A.16) |

On the other hand, from Lemma A.2 we know

| (A.17) |

Plugging (A.17) into (A.15) and recognizing (A.16), we get

This completes the proof.

∎

A.2 Proofs of Theorem 1 and Proposition 3.2

We first prove Theorem 1 with a fixed , followed by a discussion showing that the theorem holds uniformly over in a compact set for the Lasso, thereby proving Proposition 3.2. In addition to Lemma A.1, the proof relies on Lemmas A.6 and A.7, which we state below.

Let denote the class of all real-valued continuous functions defined on a compact Hausdorff space .

Lemma A.6.

Let and be two compact Hausdorff spaces and be a continuous function, then for every there exist a positive integer and continuous functions on and continuous functions on such that

Lemma A.6 serves as an approximation tool for our proof. For information, this lemma follows from the Stone–Weierstrass theorem (see Corollary 11.6 in [10]).

Lemma A.7.

Proof of Lemma A.7.

Note that we have

It follows from [25] that

which tends to as . Second,

and third, we obtain

Last, note that these fractions are all bounded, so Lebesgue’s dominated convergence theorem can be applied here.

∎

Now we turn to the proof of Theorem 1.

Proof of Theorem 1.

Denote by an upper bound of in absolute value and let be a number that will later tend to infinity. It is easy to see that we can construct a continuous function defined on such that (1) on , (2) for all , and (3) exists. This can be done, for example, by letting

From the three properties of , it is easy to see that this is a continuous function on the product of two compact Hausdorff spaces, and . From Lemma A.6, therefore, we know that there exist continuous functions on and on such that

| (A.18) |

for any small constant .

Since and are continuous on the compactification of their domains for each , the two functions must be continuous and bounded on and , respectively. Thus, we get

by Lemma A.1, where and are i.i.d. standard normal random variables. This yields

| (A.19) | ||||

Taken together, (A.18) and (A.19) give

| (A.20) | ||||

as .

Next, we consider

| (A.21) |

and

| (A.22) |

Our aim is to show that both displays are small. For the first display, note that

Taking , we obtain

| (A.23) |

Likewise, we show below that (A.22) can be made arbitrarily small in absolute value. To this end, note that

| (A.24) | ||||

Finally, from (A.20), (A.23), and (A.24) it follows that the event

happens with probability tending to one as . Taking followed by letting , Lemma A.7 shows that

can be made arbitrarily small. This reveals that

thereby completing the proof.

∎

Proof of Corollaries 3.3 and 3.4.

Define

for . As is clear, is bounded and continuous. Therefore, by Theorem 1 we get

as . On the one hand, by the same argument for (A.10), we obtain

| (A.25) | ||||

On the other hand, note that the number of false discoveries at threshold value is

It is easy to see that

Thus, we have

Using Theorem 1 with appropriate bounded continuous functions, we can show that

in probability for a constant satisfying as . Together with (A.25), this gives

as . Similarly, one can show that

This proves the first identity in Corollary 3.3. The second identify of Corollary 3.3 and Corollary 3.4 can be proved similarly.

∎

The remaining part of this subsection is devoted to showing that Theorem 1 holds uniformly over all in a compact interval of when . As with the proof of Lemma A.2, we can assume that is bounded and -Lipschitz continuous. The uniformity extension is accomplished largely by using Lemma B.2 from [15] (see also [21]).

Lemma A.8 (Lemma B.2 in [15]).

Fix . Then, there exists a constant such that for any , the Lasso estimates satisfy

with probability tending to one.

Proof of Proposition 3.2.

To begin to establish the uniformity in , let be equally spaced points and set ; We will later take . Write

It follows from Theorem 1 that

| (A.26) |

Now, according to Corollary 1.7 from [4], both are continuous in and, therefore, is also continuous on . For any constant , therefore, the uniform continuity of ensures that

| (A.27) |

holds for all satisfying if is sufficiently large. Now we consider

Taking for some and , Lemma A.8 ensures that

with probability tending to one. Taking a union bound, we get

| (A.28) |

with probability tending to one as .

Now, for any , choose such that (set ). Then from (A.26), (A.27), and (A.28) we obtain

holds uniformly for all with probability tending to one. Taking , which allows us to set , gives

as .

∎

A.3 Proof of Theorem 2

The proof of Theorem 2 presented here applies more generally to the Model-X knockoffs procedure that uses, instead of the LCD statistic, any other statistic of the form , where the link function satisfies and as for any fixed ; we call such function faithful in what follows. From [15] we know that Lasso cannot obtain full power unless (3.10) holds, hence we consider only the case . For any such , it can be shown that the expressions in Equations (3.2) and (3.9) converge to when and is growing as in the assumption. We consider first the case .

Let be the unique value of satisfying

When the prior distribution is , denote by the solution to (3.6) and let be defined as above. Recognizing the assumption of a growing in Definition 3.6, one can show that converge to which are the solution to

That is, and as . As a consequence, tends to as as well, where the existence of is ensured by the fact that .

Following the proof of Lemma A.1 in [15], we can show that converges to

in probability uniformly over as , by making use of Theorem 1. Having demonstrated earlier that and converge to constants, the faithfulness of and the growing condition of reveal that

Moreover, the convergence of the probability as a smooth function of to its limit 1 is uniform over as . In particular, we can choose such that

| (A.29) |

for all . Furthermore, for any we can find such that

| (A.30) |

happens with probability at least when . Taken together, (A.29) and (A.30) ensure that, with probability at least , we have

for and . When , then for any , the procedure that selects whenever asymptotically attains full power with , and the assertion in the theorem holds. This concludes the proof.

As an aside, the proof above seamlessly carries over to any bridge-estimator-based knockoffs procedure that uses [25]. When the order , in particular, the nominal level can take any value in since the Donoho–Tanner phase transition does not occur once .

Appendix B Derivation of the CV-AMP equations

Denote the minimum value for by

and let be the corresponding value for (so is the solution in to the first equation in (3.6) when replaced by ). Note that we can characterize by requiring that for ,

does not have a solution in for . Therefore, on defining

we are looking to solve

| (B.1) |

It is easy to verify, on the other hand, that

Imposing now (B.1), we get the equation system

which simplifies to (4.2).