A Non-Iterative Quantile Change Detection Method in Mixture Model with Heavy-Tailed Components

Abstract.

Estimating parameters of mixture model has wide applications ranging from classification problems to estimating of complex distributions. Most of the current literature on estimating the parameters of the mixture densities are based on iterative Expectation Maximization (EM) type algorithms which require the use of either taking expectations over the latent label variables or generating samples from the conditional distribution of such latent labels using the Bayes rule. Moreover, when the number of components is unknown, the problem becomes computationally more demanding due to well-known label switching issues (Richardson and Green, 1997). In this paper, we propose a robust and quick approach based on change-point methods to determine the number of mixture components that works for almost any location-scale families even when the components are heavy tailed (e.g., Cauchy). We present several numerical illustrations by comparing our method with some of popular methods available in the literature using simulated data and real case studies. The proposed method is shown be as much as 500 times faster than some of the competing methods and are also shown to be more accurate in estimating the mixture distributions by goodness-of-fit tests.

1. Introduction

Determining the number of components in a finite mixture model is crucial in many application areas such as financial data (Hu, 2006; Wong et al., 2009; Si et al., 2013), bio-medical studies (Humphrey and Rajagopal, 2002; Yin et al., 2008) and low-frequency accident occurrence prediction (Wang et al., 2011; Park et al., 2014). Existing literature have witnessed numerous computational methods, and in particular Markov Chain Monte Carlo methods (Geweke, 2007; Carlin and Chib, 1995; Wang et al., 2016) and EM algorithms (McCallum, 1999; Muthén and Shedden, 1999; Ma et al., 2017) have been used with a lot of success. However, either these methods are computationally demanding and/or these methods are developed under the assumption of data being generated from mixtures of densities from the exponential family, in part because the family of exponential distribution has a sufficient statistic of constant dimension (i.e., the dimension of the sufficient statistic remains fixed for any sample size) and so the updates of the data augmentation type algorithm involve their smaller dimensional sufficient statistics (Fearnhead, 2005; Fraser, 1963; Neal and Kypraios, 2015). One the other hand, many heavy-tailed distributions (e.g., Cauchy, t etc.) do not have such nice properties and Gibbs or EM updates become much more involved and computationally demanding (Geman and Geman, 1984). However, we cannot always assume data being generated by a mixture of distributions with exponential tails which necessarily makes the mixture to be exponentially tailed. For example, financial data (e.g., log-returns of stock prices) often exhibit higher peaks and heavy tails (Grossman and Shiller, 1980) and it would be challenging for traditional MCMC or EM algorithms to detect the number of components if we fit a mixture model to such data.

The above-mentioned methods, including the EM algorithm (Dempster et al., 1977), determine the number of components in the mixture model by using non-nested statistical test and its variants. For example, (Zhang and Cheng, 2004) provided an extended KS test based on the EM procedure to determine the number of components in parallel. (Benaglia et al., 2011) provided a new selecting bandwidth method in kernel density estimation used by the nonparametric EM (npEM) algorithm of (Benaglia et al., 2009). Besides, (Roeder, 1994) used the diagnostic plot to estimate the number of components under the assumption that components are normally distributed with a common variance and there are only a few number of components. In recent years, (Rousseau and Mengersen, 2011) (RM) have demonstrated the asymptotic behavior of the number of components in overfitted model which tends to zero-out the extra components, and this stability can be realized by imposing restrictions on the prior. (Nasserinejad et al., 2017) illustrated the success of the RM method by applying it to hemoglobin values of blood donors.

More commonly, information criteria like AIC (Akaike, 1987), BIC (Burnham and Anderson, 2004) and DIC (Ward, 2008) have also been used for model selection for mixture models despite the fact that mixture models lead to so-called singular models that violates the standard regularity conditions required for the consistency of the criteria. (Drton and Plummer, 2017) proposed a modified singular Bayesian information criterion (sBIC) for models in which the Fisher information matrices may not be strictly positive definite (leading to singular model). However, the sBIC is difficult to construct especially when the components of the mixture models are assumed to arise from non-exponential families.

In this paper, we developed an easily implementable data-driven method that we call the Non-Iterative Quantile Change Detection (NIQCD) by using change-point detection methods applied to the quantiles of the component distributions of the mixture model. We adapt the RM (Rousseau and Mengersen, 2011) framework by starting with a relatively larger number of components (relative to the sample size) and empirically estimate the location and scale parameters of the components using quantiles conditioned on the subset of data assumed to be obtained from the corresponding components. The probability (mixing) weights assigned to each component are then estimated by constrained least squares method making the method computationally much faster. We use the change-point method (Killick et al., 2012) to reduce the redundancy of the location parameter and shrink it to a stable state. To summarize the three main highlights of the data-driven NIQCD are: (1) the quantile based estimation can be applied to any location-scale family (including heavy-tailed distributions); (2) the constrained least square method for estimating the weights makes the algorithm non-iterative; and finally (3) the change-point based method reduces the dimensionality of the mixture model to an optimal number.

We illustrate the performance of two methods as compared to NIQCD for estimating the number of components for a mixture model with Cauchy components. It is also to be noticed that compared to distributions whose tails decay exponentially, Cauchy distribution is much heavy-tailed, which makes the detection of hidden components overlap much harder (see Section 2 for further details on this aspect). In our simulation studies we have not used certain Bayesian techniques, such as Reversible-jump Markov chain Monte Carlo (Richardson and Green, 1997) which we found computationally much slower compared to other methods that we have chosen to compare with the proposed NIQCD in terms of computational time and estimation accuracy. In particular we consider two Bayesian model selection methods in our experiment: RM (Rousseau and Mengersen, 2011), posterior deviance distribution (PDD) (Aitkin et al., 2015), and our proposed baseline model iterative QCD (IQCD).

The rest of this paper is organized as follows. In Section 2, we provide the general definition of mixture model. In Section 3, we give two definitions of measuring the overlap between multiple distributions. In Section 4, we describe two algorithms IQCD and NIQCD. In section 5, related literature is summarized. In Section 6, we present the simulation design and results for comparing R&M, PDD, IQCD, and NIQCD. In Section 7, we applied NIQCD to stock S&P 500 index return data. Finally, we discuss potential extensions of NIQCD.

2. Objectives and Notations

A -component mixture of location-scale families has the following density:

| (1) |

where is a known unimodal density from location-scale families, , , denotes the -dimensional simplex space, and .

Given a sample of observations for , the empirical cumulative distribution function (ecdf) is defined as . our goal is to estimate the true number of mixture components . As a secondary interest, we also want to estimate corresponding to the estimated value of .

3. Measure of overlapping and dispersion across components

In this section, we develop formal concepts of the degree of the overlapping and the amount of dispersion across different components. We use these concepts to build test cases for our simulation studies in Section 6.

When determining the number of components in a mixture model, the amount of difficulty often depends on the degree of overlapping (DOL) and between component dispersion (BCD). If the components have non-overlapping supports and large dispersion, it is generally easy to detect the number of components. However, if the components have heavy degree of overlapping supports and small dispersion, the detection of the number of components becomes harder (at least visually). When focusing on unimodal location-scale families, such DOL and BCD are manifested by location parameters. For example, if for all , the mixture density is unimodal and hence visually it is often infeasible to identify the mixture components and hence makes the estimation of more difficult (Nowakowska et al., 2014).

Below we present two criteria for a general class of mixture models which is not limited to location-scale components.

3.1. Weighted Degree of Overlapping

Consider the case of two components () in a mixture model, that is, , where , and are arbitrary densities. A measure of overlapping between and can be defined as:

| (2) |

where .

Clearly, and the boundary values and are achieved when and have disjoint supports (i.e., no overlapping) and (i.e., complete overlapping), respectively. However, such widely used measure of overlapping doesn’t take into account the weights assigned to each component and its generalization to can be difficult.

With above limitations, we propose weighted degree of overlapping (wDOL) for a mixture model as

| (3) |

where is the th component and is the corresponding weight for .

Without loss of generality, we assume . Since for arbitrary and each , we have

| (4) |

where the lower boundary is achieved when for almost all , i.e., when the intersection of the supports of is a null set, and the upper boundary is achieved when all components are all identical.

The well-defined wDOL also possesses the desired property that it is invariant under a class of transformation:

| (5) |

where is a strictly monotone differentiable function.

3.2. Robust Between Component Dispersion

The mixture model can also be expressed in a hierarchical form. That is, is equivalent to , where . Thus, the between component dispersion (BCD) can be defined as

| (6) |

where .

Since , BCD . The lower boundary is achieved when components’ location parameters are identical, whereas the upper boundary is achieved when there is almost no dispersion among components. However, such measure of between component dispersion doesn’t extend to the situation where the components are heavy-tailed densities (e.g., Cauchy distribution that doesn’t have the second moment).

Therefore, we propose a robust version of the between component dispersion (rBCD) using more robust measures of variability:

| (7) |

Note that the median of denoted by is always well defined and minimizes . Thus, we have because . It follows that rBCD when the dispersion between components is large, whereas rBCD when the dispersion between components is small.

4. Estimation using Quantile Change Detection (QCD) Method

In this section, we propose two methods to determine the number of components and estimate the parameters in the mixture model whose components are from the exponential family. The Iterative Quantile Change detection method (IQCD) is based on an iterative procedure to update the weight parameter and estimate the number of true latent classes by excluding tiny weight components. The Non-Iterative Quantile Change Detection method (NIQCD) determines the number of components by solving the change-point problem and estimates the parameters by using empirical cumulative distribution function (eCDF) to build up the linear equations. The coordinate descent method can also be integrated into NIQCD to refine the estimates of the location, scale, and weight parameters but with additional computational time.

For identifiability of the components, we further assume that .

4.1. Iterative QCD (IQCD)

The idea of IQCD is to select relatively large weights and use the cumulative sum criteria (cusum) (Page, 1954) to select the corresponding components followed by updating the parameters. By iterating this procedure, we could finally converge to a stable weight distribution and determine the number of components. The detailed steps are described as follows.

-

(1)

Initialize and . Rough estimates of and can be obtained by setting and

(8) where takes the integer value, and are the ordered statistics of the samples.

Then the ‘change point’ (Ebrahimi and Ghosh, 2001; Lee, 2010; Killick et al., 2012) method is used to identify the significant difference of the sudden change between those , which is implemented by minimizing a cost function to detect change points. Then we obtain the estimated number of component usually less than , and re-estimate based on , where .

-

(2)

Initialize . Notice that for the standard Cauchy, the CDF is , and . For the -th component, we want as the third quartile in the standard Cauchy distribution. So we get , leading to . Therefore, the scale parameters , can be estimated by quantiles of general Cauchy distribution

(9) So and which represents the hyperparameter and can be adjusted by the needs for more general conditions.111Default if Cauchy distribution.

-

(3)

Initialize . For the -th component, we simply use the difference of eCDF between two adjacent components, and , to represent the weight for the -th component,

(10) where , corresponds to the first component, and is for the last component.

-

(4)

Initialize latent variables. For each data point , it has a corresponding probability of belonging to the th component , which can be initialized using

(11) It’s easy to show that .

-

(5)

Update parameters iteratively. In the -th iteration, we update the parameters as follows:

(12) (13) where Med is the median and IQR is the interquartile range.

Based on cusum criteria222Cusum criteria: It uses the cumulative sum of estimated weights. One could obtain a distribution of over iteration if the accumulated sum of ordered weights is larger than a certain threshold e.g. . In other words, the (assumed) true number of non-empty classes () of iteration could be computed in each MCMC iteration as: , where is the iteration ’s th large weight and . We usually can set or . , the estimated component for at iteration is

(14) where is a threshold hyperparameter, usually can be set to .

4.2. Non Iterative QCD (NIQCD)

The estimated number of components, location, and scale parameters in NIQCD are obtained using the steps (1) and (2) in IQCD. That is, , , for .

-

(1)

Estimate weight parameters. We estimate the weight parameter by solving linear equations with constraints

(15) where , is an matrix and .

-

(2)

Update parameters by coordinate descent.333This step is optional. The estimated scale parameters could be large on two sides and be small in the middle (high bias). Define the negative log-likelihood of mixture model:

(16) Then the coordinate descent method is applied to minimize Equation (16) to update the parameters iteratively until they converge.

5. Related works

Here we present two related works and apply it to the Cauchy mixtue model.

1. Rousseau and Mengersen (RM)method: (Rousseau and Mengersen, 2011) proved that the posterior behavior of an overfitted mixture model depends on the chosen prior on the proportions . They showed that an overfitted mixture model converges to the true mixture, if the Dirichlet-parameters of the prior are smaller than .444 is the dimension of the class-specific parameters, for mixture of Cauchy Basically, a deliberately overfitted mixture model with , where is usually larger than . A sparse prior with Dirichlet distribution , on the proportions is then assumed to empty the superfluous classes during MCMC sampling.

In the overfitted mixture model, each data point is a tuple with and follows a multinomial distribution with for the simplex and represents for the class data where belongs. The joint distribution can be decomposed as , where . RM postulates that the observed data is comprised of components with proportions specified by . We see that is a mixture model by explicitly writing out this probability:

Then the corresponding likelihood of the mixture model is (Nasserinejad et al., 2017) claimed a class empty if the number of observations assigned to that latent class is smaller than a certain proportion of the observations in the data set , e.g. . In other words, the true number of non-empty classes could be computed in each MCMC iteration as , where is the estimated number of components in the -th iteration of MCMC sampling, is the number of observations allocated to class at iteration , is the sample size and is the indicator function. is the threshold which can be set to a predefined value, e.g. 0.01, 0.02, or 0.05. Then one can derive the number of non-empty classes based on the posterior mode of the number of non-empty classes based on MCMC iterations.

2. Posterior Distribution of Deviance (PDD) method: An alternative way is to use the posterior distribution of the deviance (Aitkin et al., 2015), by substituting random draws from the posterior distribution of model parameter into the deviance , where is the likelihood. Models are compared for the stochastic ordering of their posterior deviance distributions.

A random variable is stochastically less than another random variable if , , with a strict inequality for at least one , where and are CDFs of and respectively. If the CDF of the posterior deviance distribution for model is stochastically less than that of model , we can say that model fits the data better than model .

The CDFs of posterior deviances distribution for different models are compared initially by graphing them in the same plot. It may happen that the CDF curves cross, which indicates that the deviances for competing models are not stochastically ordered.

In this case, we can take the most often best criteria proposed by (Aitkin et al., 2015) to compare competing models. Let represents the index of models. At the -th deviance draw from each model we have deviances , , where is the number of samples drawn from each posterior sample.

For each , we define . Then can be viewed as samples from posterior distribution of who is a discrete random variable taking values on . The best model is the one with the largest frequency in the samples. We call this criteria most often best criteria.

\Description

\Description

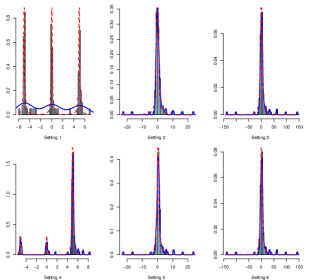

Histograms of randomly selected synthetic data sets with sample size , where the blue solid lines and the red dashed lines represent empirical densities and true densities respectively. The corresponding wDOL is from left to right, from top to bottom (0.01, 0.5, 0.89), (0, 0.09, 0.12) and the corresponding rBCD is (0.1083, 0.0024, 0.0004), (0.1083, 0.0024, 0.0004).

6. Simulation Study

\Description

\Description

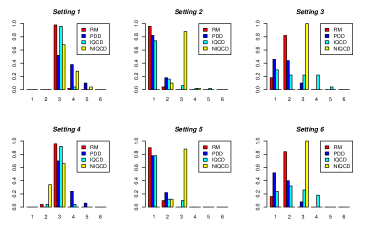

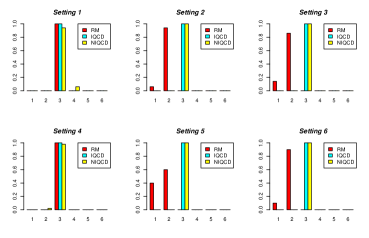

Sample size , given 50 data sets sampled from the mixture density, the correct detection rate. Setting 1 - Setting 6 are from left to right and from top to bottom corresponding. The yellow bar (NIQCD) is consistently good at S2, S3, S5, S5. NIQCD achieving the true detection rate is over . At S1 and S4, NIQCD achieves around and respectively. RM, PDD, IQCD perform not well at S2, S3, S5, S6 and nearly 0 correct detection rate.

Sample size , given 50 data sets sampled from the mixture density, the fitted lines used the estimated components, location, scale parameters in Cauchy mixture model. Setting 1 - Setting 6 are from left to right and from top to bottom corresponding. At S1 and S4, NIQCD both give the almost perfect fit though under the condition of unequal weighted scenario. At S2, S3, S5, and S6, NIQCD performs not bad at density fitting, which are close to the true density.

| Setting | Time[s] (se) | |||

|---|---|---|---|---|

| RM | PDD | IQCD | NIQCD | |

| S1 | 177.01 | 3591 | 105.84 | 0.32 |

| (6.96) | (1161) | (4.63) | (0.22) | |

| S2 | 177.55 | 1840 | 93.82 | 0.36 |

| (5.75) | (446) | (5.65) | (0.13) | |

| S3 | 167.32 | 775 | 95.71 | 0.28 |

| (2.36) | (227) | (4.59) | (0.09) | |

| S4 | 176.94 | 3020 | 102.57 | 0.47 |

| (9.14) | (1451) | (4.07) | (0.23) | |

| S5 | 172.72 | 2858 | 89.18 | 0.33 |

| (5.31) | (769) | (4.79) | (0.18) | |

| S6 | 166.96 | 830 | 96.11 | 0.28 |

| (2.27) | (283) | (3.37) | (0.09) | |

| Setting | P-value (se) | |||

|---|---|---|---|---|

| RM | PDD | IQCD | NIQCD | |

| S1 | 0.000 | 0.624 | 0.448 | 0.934 |

| (0.000) | (0.437) | (0.299) | (0.125) | |

| S2 | 0.177 | 0.618 | 0.013 | 0.910 |

| (0.206) | (0.346) | (0.016) | (0.184) | |

| S3 | 0.007 | 0.516 | 0.037 | 0.918 |

| (0.007) | (0.379) | (0.035) | (0.165) | |

| S4 | 0.012 | 0.621 | 0.138 | 0.612 |

| (0.052) | (0.394) | (0.092) | (0.323) | |

| S5 | 0.110 | 0.609 | 0.024 | 0.893 |

| (0.170) | (0.373) | (0.038) | (0.210) | |

| S6 | 0.006 | 0.547 | 0.040 | 0.880 |

| (0.007) | (0.371) | (0.050) | (0.205) | |

| Sample size | Criteria | S1 | S2 | S3 | S4 | S5 | S6 |

|---|---|---|---|---|---|---|---|

| Dectection Rate | RM | NIQCD | NIQCD | RM | NIQCD | NIQCD | |

| GOF by ADT | NIQCD | NIQCD | NIQCD | NIQCD | NIQCD | NIQCD | |

| CPU Time | NIQCD | NIQCD | NIQCD | NIQCD | NIQCD | NIQCD | |

| Dectection Rate | RM, IQCD | NIQCD | NIQCD | RM, IQCD | NIQCD | NIQCD | |

| GOF by ADT | NIQCD | NIQCD | NIQCD | NIQCD | NIQCD | NIQCD | |

| CPU Time | NIQCD | NIQCD | NIQCD | NIQCD | NIQCD | NIQCD |

In this section, we use for Cauchy mixture or any other density s.t. and . Besides, suppose there are components in the mixture model and .

6.1. Design

We compare the performance of these four methods, RM, PDD, IQCD, and NIQCD on simulated data. To evaluate the performance more objectively, we generate synthetic data with two sample sizes, and , from with components. We consider 6 different settings summarized below in our experiments with 50 synthetic data sets from each setting. For , the histograms of randomly selected synthetic data sets from each setting is present in figure (1).

Equal weighted settings:

-

•

Setting 1: High separation (wDOL = , rBCD = ): classes with , , .

-

•

Setting 2: Medium separation (wDOL = , rBCD = ): classes with , , .

-

•

Setting 3: Low separation (wDOL = , rBCD = ): classes with , , .

Unequal weighted settings:

-

•

Setting 4: High separation (wDOL = , rBCD = ): classes with , , .

-

•

Setting 5: Medium separation (wDOL = , rBCD = ): classes with , , .

-

•

Setting 6: Low separation (wDOL = , rBCD = ): classes with , , .

6.2. Prior Distributions and Initial Values

-

•

RM: Vague priors for the location and scale parameters , for , where .

-

•

PDD: Truncated uniform prior on and and Dirichlet prior on are used in PDD method. The location and scale parameters , for , where .

-

•

IQCD: Initialize the number of components , the cutoff value (default).

-

•

NIQCD: Initialize the number of components , the relative error value is (default).

6.3. Results

For a small sample size , four methods, RM, PDD, IQCD, and NIQCD, are applied to estimate parameters in the mixture of Cauchy. In Figure (2), the histogram indicates that the ratio of each method correctly chooses over 50 times for each dataset. At S2, S3, S5, S6, NIQCD is consistently more accurate than other three methods when .

At Setting 1 (upper left) in Figure (2), two-sample binomial tests are conducted, given critical value of 0.05, corresponding to , between RMNIQCD, PDDNIQCD, and IQCDNIQCD. The P-Value results are 0.0001, 0.1052, 0.0005 respectively, which means that NIQCD is less effective than RM and IQCD under Setting 1. The possible reason is that NIQCD is very sensitive to abnormal values and allocates more weights on these small components. At Setting 4 (bottom left) in Figure (2), the corresponding P-values are 0.0003, 0.3639, 0.0024, which also shows that NIQCD is not so effective compared to other methods. But it does not bad at detecting the true number of components, which achieves around 0.7 at Setting 1 and Setting 4.

In Table (1) left, we show the computation time. NIQCD is around 500 times faster than RM, times faster than PDD and 300 times faster than IQCD.

Table (1) right shows the goodness of fit by Anderson Darling test (ADT) and the P-value of NIQCD is around 0.9 at all settings. RM method performs not good at Setting 2 and Setting 5 and P-value is around 0.1 for other settings. PDD’s P-value is around 0.6 at all settings. IQCD’s P-value ranges from 0.01 to 0.45.

In Figure (3), 50 estimated density lines of NIQCD method and the corresponding true density has been compared. The black line is the true density, settings from left to right and from top to bottom are Setting 1 to Setting 6 . We see that estimated density lines (colored dashed lines) capture the density line very well although there are few deviance.

In Table (2) top, , we combine three different criteria which are usually used together to evaluate one method, Detection Rate (DR), Goodness of Fit by ADT, and CPU Time. Under these criteria, NIQCD shows 16 times in overall 18 cells, around 89% better than other methods under different settings and criteria.

As sample size increases from to , in Figure (6) in Appendix B555For time saving, we only obtained the posterior samples from 1 to 6 Cauchy mixture components to compare for PDD method and simulated it just on , NIQCD is the best among all settings which achieves above 90% accuracy over 50 data sets. In Table (5) upper in Appendix B, NIQCD is around 500 times faster than the second place IQCD. In Table (5) bottom, NIQCD consistently shows great fit of the data. In Figure (7) in Appendix B, it shows 50 estimated density lines of NIQCD (colored dashed) and the true density is the black line. Compared with Figure (2), with sample size increasing, the goodness of fit becomes much better and with less noise.

7. Real Data Analysis

7.1. Data Description

Returns from financial assets are normally distributed underpin many traditional financial theories (Aparicio and Estrada, 2001), but the reality is that many asset returns do not conform to this law. Empirical distributions fitted on historical data exhibit that higher peaks and heavier tails returns are mostly clustered within a small range around the mean and extreme moves occur more frequently than a normal distribution would suggest. Robert Shiller (Grossman and Shiller, 1980) observed that fat-tailed distribution can help explain larger return fluctuations.

In this section, we empirically evaluate our algorithm on the real data from S&P 500 index between July 1st 2016 and July 1st 2018 with the number of transaction days . We use to denote the log return on day that is defined as , where and are closed stock price for day and , respectively.

Skewness is a measure of distortion or asymmetry of a distribution with a number of 0 indicates complete symmetry.666Sample Skewness: The sample skewness of the data is , implying that the underlying distribution is slightly skewed to the left and a mixture model could be a reasonable choice to estimate it. On the other hand, kurtosis refers to the degree to which a distribution is more or less peaked than a normal distribution whose kurtosis is 3.777Sample Kurtosis: A sample kurtosis of from the data justifies the use of heavy-tailed distribution as the components of the mixture model. Therefore, the mixture of Cauchy model was fitted to the data using NIQCD.

7.2. Estimated Density

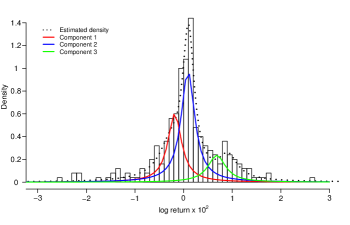

From the results obtained by NIQCD, the optimal number of components for the two years’ data is . The corresponding estimated weights, locations and scales for each component are shown in 3. The Anderson Darling Test was performed and the P-value of verifies that the fitted model matches the observations very well.

| Parameters | |||

|---|---|---|---|

| Component 1 (bear market) | -0.18 | 0.17 | 0.32 |

| Component 2 (neutral market) | 0.09 | 0.17 | 0.52 |

| Component 3 (bull market) | 0.68 | 0.22 | 0.16 |

The estimated number of components by NIQCD is in good agreement with the economical common knowledge that the stock market can be classified into three categories “bear market”, “neutral market” and “bull market”. In figure (4), we plot the fitted densities of each component. The component 1 (red curve) represents the bear market since its average log return rate is negative, the component 2 (blue curve) represents the neutral market with the log return rate not far away from zero, and the component 3 (green curve) corresponds to the bull market whose log return rate is positive.

\Description

\Description

Histogram of log return rate amplified 100 times. The black dashed curve is the estimated density based on NIQCD. Three components are denoted by the red, blue and the green curves.

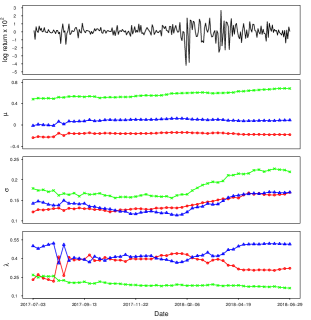

The scale parameters of the bull market (0.22) is slightly larger than the other two markets, which means that the bull market is more volatile. The estimated weight of the neutral market (0.52) shows that it occupies this market for a longer time during these two years compared to the bear market and the bull market, which meets the common knowledge that the market is usually at the neutral state. The possible reason for the relative large weight (0.32) of the bear market is that the market declined a lot and exhibited dramatic volatility from Feb 2018 to Apr 2018 as shown in Figure (5) (top).

\Description

\Description

Weekly updated parameters from 07/01/2017 to 07/01/2018. The series of updated parameters of the bear, neutral and bull markets are denoted in red, blue and green respectively. The top panel shows the log return amplified 100 times during this period.

To test the robustness of our algorithm, we update the estimated parameters weekly from July 2017 in an offline fashion as shown in Figure (5). That is, the training data accumulate weekly and are fitted with NIQCD as a whole. The second panel of Figure (5) indicates that the locations of the three market didn’t change significantly but the bull market did show slightly positive shift. From the updated scale parameters in the third panel, the volatility was relatively stable before Feb 2018 but increased considerably after that for all markets, which was probably caused by the huge fluctuation in technology stocks. The part Figure (5) shows the bull market moved down a little while the bear market moved up, implying that the whole market changed from relatively weak bear market to neutral market.

7.3. Prediction of Return Category

We use the NIQCD method to get corresponding estimated parameters and then apply the three components’ densities to calculate the corresponding probabilities from July 1, 2018 to August 1, 2018 with 20 transaction days. Then we get the index of each day with respect to the largest probability and assign category ’-1’ to component 1, category ’0’ to component 2, and category ’1’ to component 3,

| Date | Category | Date | Category |

|---|---|---|---|

| 2018-07-03 | -1 | 2018-07-18 | -1 |

| 2018-07-05 | 1 | 2018-07-19 | 0 |

| 2018-07-06 | 0 | 2018-07-20 | -1 |

| 2018-07-09 | 1 | 2018-07-23 | 0 |

| 2018-07-10 | 0 | 2018-07-24 | -1 |

| 2018-07-11 | 1 | 2018-07-25 | 0 |

| 2018-07-12 | 0 | 2018-07-26 | -1 |

| 2018-07-13 | 1 | 2018-07-27 | 0 |

| 2018-07-16 | -1 | 2018-07-30 | 0 |

| 2018-07-17 | 0 | 2018-07-31 | -1 |

The result is shown in Table (4). There are 7 days belonging to component 1, 9 days belonging to component 2, 4 days belonging to component 3, which indicates a shift from a neutral market to a bear market during this period.

8. Conclusion

Our study is a proof-of-concept study and provides a straightforward option for parameter estimation in mixture models with heavy-tailed components. Note that our algorithm is not limited to Cauchy mixture models, and can also be applied to other densities. The current work is not designed to be exhaustive in incorporating all potential mixture methods. We present the simulation results with six settings and prove that our algorithm show great performance even in the most difficult separation settings (Setting 2, Setting 3, Setting 5, Setting 6). Besides, our algorithm has relatively small computational complexity compared to other methods, the extension of NIQCD to an online version should not be difficult.

References

- (1)

- Aitkin et al. (2015) Murray Aitkin, Duy Vu, and Brian Francis. 2015. A new Bayesian approach for determining the number of components in a finite mixture. Metron 73, 2 (2015), 155–176.

- Akaike (1987) Hirotugu Akaike. 1987. Factor analysis and AIC. In Selected papers of hirotugu akaike. Springer, 371–386.

- Aparicio and Estrada (2001) Felipe M Aparicio and Javier Estrada. 2001. Empirical distributions of stock returns: European securities markets, 1990-95. The European Journal of Finance 7, 1 (2001), 1–21.

- Benaglia et al. (2009) Tatiana Benaglia, Didier Chauveau, and David R Hunter. 2009. An EM-like algorithm for semi-and nonparametric estimation in multivariate mixtures. Journal of Computational and Graphical Statistics 18, 2 (2009), 505–526.

- Benaglia et al. (2011) Tatiana Benaglia, Didier Chauveau, and David R Hunter. 2011. Bandwidth selection in an EM-like algorithm for nonparametric multivariate mixtures. In Nonparametric Statistics And Mixture Models: A Festschrift in Honor of Thomas P Hettmansperger. World Scientific, 15–27.

- Burnham and Anderson (2004) Kenneth P Burnham and David R Anderson. 2004. Multimodel inference: understanding AIC and BIC in model selection. Sociological methods & research 33, 2 (2004), 261–304.

- Carlin and Chib (1995) Bradley P Carlin and Siddhartha Chib. 1995. Bayesian model choice via Markov chain Monte Carlo methods. Journal of the Royal Statistical Society: Series B (Methodological) 57, 3 (1995), 473–484.

- Dempster et al. (1977) Arthur P Dempster, Nan M Laird, and Donald B Rubin. 1977. Maximum likelihood from incomplete data via the EM algorithm. Journal of the royal statistical society. Series B (methodological) (1977), 1–38.

- Drton and Plummer (2017) Mathias Drton and Martyn Plummer. 2017. A Bayesian information criterion for singular models. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 79, 2 (2017), 323–380.

- Ebrahimi and Ghosh (2001) Nader Ebrahimi and Sujit K Ghosh. 2001. Bayesian and frequentist methods in change-point problems. Handbook of statistics 20 (2001), 777–787.

- Fearnhead (2005) Paul Fearnhead. 2005. Direct simulation for discrete mixture distributions. Statistics and Computing 15, 2 (2005), 125–133.

- Fraser (1963) DAS Fraser. 1963. On sufficiency and the exponential family. Journal of the Royal Statistical Society: Series B (Methodological) 25, 1 (1963), 115–123.

- Geman and Geman (1984) Stuart Geman and Donald Geman. 1984. Stochastic relaxation, Gibbs distributions, and the Bayesian restoration of images. IEEE Transactions on pattern analysis and machine intelligence 6 (1984), 721–741.

- Geweke (2007) John Geweke. 2007. Interpretation and inference in mixture models: Simple MCMC works. Computational Statistics & Data Analysis 51, 7 (2007), 3529–3550.

- Grossman and Shiller (1980) Sanford J Grossman and Robert J Shiller. 1980. The determinants of the variability of stock market prices.

- Hu (2006) Ling Hu. 2006. Dependence patterns across financial markets: a mixed copula approach. Applied financial economics 16, 10 (2006), 717–729.

- Humphrey and Rajagopal (2002) JD Humphrey and KR Rajagopal. 2002. A constrained mixture model for growth and remodeling of soft tissues. Mathematical models and methods in applied sciences 12, 03 (2002), 407–430.

- Killick et al. (2012) Rebecca Killick, Paul Fearnhead, and Idris A Eckley. 2012. Optimal detection of changepoints with a linear computational cost. J. Amer. Statist. Assoc. 107, 500 (2012), 1590–1598.

- Lee (2010) Tze-San Lee. 2010. Change-point problems: bibliography and review. Journal of Statistical Theory and Practice 4, 4 (2010), 643–662.

- Ma et al. (2017) Jiayi Ma, Junjun Jiang, Chengyin Liu, and Yansheng Li. 2017. Feature guided Gaussian mixture model with semi-supervised EM and local geometric constraint for retinal image registration. Information Sciences 417 (2017), 128–142.

- McCallum (1999) Andrew McCallum. 1999. Multi-label text classification with a mixture model trained by EM. In AAAI workshop on Text Learning. 1–7.

- Muthén and Shedden (1999) Bengt Muthén and Kerby Shedden. 1999. Finite mixture modeling with mixture outcomes using the EM algorithm. Biometrics 55, 2 (1999), 463–469.

- Nasserinejad et al. (2017) Kazem Nasserinejad, Joost van Rosmalen, Wim de Kort, and Emmanuel Lesaffre. 2017. Comparison of criteria for choosing the number of classes in Bayesian finite mixture models. PloS one 12, 1 (2017), e0168838.

- Neal and Kypraios (2015) Peter Neal and Theodore Kypraios. 2015. Exact Bayesian inference via data augmentation. Statistics and Computing 25, 2 (2015), 333–347.

- Nowakowska et al. (2014) Ewa Nowakowska, Jacek Koronacki, and Stan Lipovetsky. 2014. Tractable measure of component overlap for gaussian mixture models. arXiv preprint arXiv:1407.7172 (2014).

- Page (1954) Ewan S Page. 1954. Continuous inspection schemes. Biometrika 41, 1/2 (1954), 100–115.

- Park et al. (2014) Byung-Jung Park, Dominique Lord, and Chungwon Lee. 2014. Finite mixture modeling for vehicle crash data with application to hotspot identification. Accident Analysis & Prevention 71 (2014), 319–326.

- Richardson and Green (1997) Sylvia Richardson and Peter J Green. 1997. On Bayesian analysis of mixtures with an unknown number of components (with discussion). Journal of the Royal Statistical Society: series B (statistical methodology) 59, 4 (1997), 731–792.

- Roeder (1994) Kathryn Roeder. 1994. A graphical technique for determining the number of components in a mixture of normals. J. Amer. Statist. Assoc. 89, 426 (1994), 487–495.

- Rousseau and Mengersen (2011) Judith Rousseau and Kerrie Mengersen. 2011. Asymptotic behaviour of the posterior distribution in overfitted mixture models. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 73, 5 (2011), 689–710.

- Si et al. (2013) Jianfeng Si, Arjun Mukherjee, Bing Liu, Qing Li, Huayi Li, and Xiaotie Deng. 2013. Exploiting topic based twitter sentiment for stock prediction. In Proceedings of the 51st Annual Meeting of the Association for Computational Linguistics (Volume 2: Short Papers). 24–29.

- Wang et al. (2011) Chao Wang, Mohammed A Quddus, and Stephen G Ison. 2011. Predicting accident frequency at their severity levels and its application in site ranking using a two-stage mixed multivariate model. Accident Analysis & Prevention 43, 6 (2011), 1979–1990.

- Wang et al. (2016) Tingting Wang, Yi-Ping Phoebe Chen, Phil J Bowman, Michael E Goddard, and Ben J Hayes. 2016. A hybrid expectation maximisation and MCMC sampling algorithm to implement Bayesian mixture model based genomic prediction and QTL mapping. BMC genomics 17, 1 (2016), 744.

- Ward (2008) Eric J Ward. 2008. A review and comparison of four commonly used Bayesian and maximum likelihood model selection tools. Ecological Modelling 211, 1-2 (2008), 1–10.

- Wong et al. (2009) CS Wong, WS Chan, and PL Kam. 2009. A Student t-mixture autoregressive model with applications to heavy-tailed financial data. Biometrika 96, 3 (2009), 751–760.

- Yin et al. (2008) Dong Yin, Jia Pan, Peng Chen, and Rong Zhang. 2008. Medical image categorization based on gaussian mixture model. In 2008 International Conference on BioMedical Engineering and Informatics, Vol. 2. IEEE, 128–131.

- Zhang and Cheng (2004) Ming-Heng Zhang and Qian-Sheng Cheng. 2004. Determine the number of components in a mixture model by the extended KS test. Pattern recognition letters 25, 2 (2004), 211–216.

This appendix provides detailed supplementary information for the NIQCD algorithm and additional simulation results. Readers may refer to the publicly-available code for more implementation details.888https://github.com/Likelyt/Mixture-Model-tools.

Appendix A Algorithm

The detailed NIQCD algorithm is shown below.

Appendix B Additional Simulation Results

Additional simulation results for sample size are shown below including CPU Time, P-value of AD Test, estimation of number of components, and fitting lines for 50 data sets.

| Setting | Time[s] (se) | |||

|---|---|---|---|---|

| RM | PDD | IQCD | NIQCD | |

| S1 | 2021 | - | 522 | 0.96 |

| (51.81) | - | (9.00) | (0.41) | |

| S2 | 2263 | - | 505 | 1.24 |

| (118.95) | - | (12.47) | (0.17) | |

| S3 | 2073 | - | 500 | 1.50 |

| (60.80) | - | (9.81) | (2.14) | |

| S4 | 2010 | - | 505 | 2.33 |

| (88.32) | - | (7.82) | (1.39) | |

| S5 | 2200 | - | 493 | 1.34 |

| (107.80) | - | (8.38) | (0.29) | |

| S6 | 2084 | - | 496 | 1.26 |

| (48.91) | - | (7.34) | (0.64) | |

| Setting | P-value (se) | |||

|---|---|---|---|---|

| RM | PDD | IQCD | NIQCD | |

| S1 | 0.952 | - | 0.002 | 0.959 |

| (0.067) | - | (0.002) | (0.083) | |

| S2 | 0.000 | - | 0.000 | 0.928 |

| (0.001) | - | (0.000) | (0.132) | |

| S3 | 0.000 | - | 0.000 | 0.949 |

| (0.000) | - | (0.000) | (0.072) | |

| S4 | 0.000 | - | 0.000 | 0.108 |

| (0.000) | - | (0.000) | (0.282) | |

| S5 | 0.002 | - | 0.000 | 0.941 |

| (0.014) | - | (0.000) | (0.120) | |

| S6 | 0.000 | - | 0.000 | 0.952 |

| (0.000) | - | (0.000) | (0.067) | |

\Description

\Description

Histogram of the number of components detected, sample size n = 1000.

Fitted dashed lines by NIQCD method with 50 datasets sampled from true mixture model, sample size n = 1000.