MS-0001-1922.65

Greedy Algorithms for Many Armed Bandit

The Unreasonable Effectiveness of Greedy Algorithms in Multi-Armed Bandit with Many Arms

Mohsen Bayati\AFFGraduate School of Business, Stanford University,\EMAILbayati@stanford.edu \AUTHORNima Hamidi\AFFDepartment of Statistics, Stanford University, \EMAILhamidi@stanford.edu \AUTHORRamesh Johari\AFFDepartment of Management Science and Engineering, Stanford University, \EMAILrjohari@stanford.edu \AUTHORKhashayar Khosravi\AFFGoogle Research, NYC, \EMAILkhosravi@google.com

We study a Bayesian -armed bandit problem in many-armed regime, when , with the time horizon. We first show that subsampling is critical for designing optimal policies. Specifically, the standard UCB algorithm is sub-optimal while a subsampled UCB (SS-UCB), which samples arms and executes UCB on that subset, is rate-optimal. Despite theoretically optimal regret, SS-UCB numerically performs worse than a greedy algorithm that pulls the current empirically best arm each time. These empirical insights hold in a contextual setting as well, using simulations on real data. These results suggest a new form of free exploration in the many-armed regime that benefits greedy algorithms. We theoretically show that this source of free exploration is deeply connected to the distribution of a tail event for the prior distribution of arm rewards. This is a fundamentally distinct phenomenon from free exploration due to variation in covariates, as discussed in the recent literature on contextual bandits. Building on this result, we prove that the subsampled greedy algorithm is rate-optimal for Bernoulli bandits in many armed regime, and achieves sublinear regret with more general distributions. Taken together, our results suggest that practitioners may benefit from using greedy algorithms in the many-armed regime.

Greedy algorithms, free exploration, multi-armed bandit

1 Introduction

In this paper, we consider the standard stochastic multi-armed bandit (MAB) problem, in which the decision-maker takes actions sequentially over time periods (the horizon). At each time period, the decision-maker chooses one of arms (or decisions), and receives an uncertain reward. The goal is to maximize cumulative rewards attained over the horizon. Crucially, in the typical formulation of this problem, the set of arms is assumed to be “small” relative to the time horizon ; in particular, in standard asymptotic analysis of the MAB setting, the horizon scales to infinity while remains constant. In practice, however, there are many situations where the number of arms is large relative to the time horizon of interest. For example, drug development typically considers many combinations of basic substances; thus MABs for adaptive drug design inherently involve a large set of arms. Similarly, when MABs are used in recommendation engines for online platforms, the number of choices available to users is enormous: this is the case in e-commerce (many products available); media platforms (many content options); online labor markets (wide variety of jobs or workers available); dating markets (many possible partners); etc.

Formally, we say that an MAB instance is in the many-armed regime where . In our theoretical results, we show that the threshold is in fact the correct point of transition to the many-armed regime, at which behavior of the MAB problem becomes qualitatively different than the regime where . Throughout our paper, we consider a Bayesian framework, i.e., where the arms’ reward distributions are drawn from a prior. But we expect our analysis can be extended to the frequentist setting as well.

In §3.1, we first use straightforward arguments to establish a fundamental lower bound of on Bayesian regret in the many-armed regime. We note that prior Bayesian lower bounds for the stochastic MAB problem require to be fixed while (see, e.g., Kaufmann 2018, Lai et al. 1987, Lattimore and Szepesvári 2020), and hence, are not applicable in the many-armed regime.

Our first main insight (see §3.2) is the importance of subsampling. The standard UCB algorithm can perform quite poorly in the many-armed regime, because it over-explores arms: even trying every arm once leads to a regret of . Instead, we show that the bound is achieved (up to logarithmic factors) by a subsampled upper confidence bound (SS-UCB) algorithm, where we first select (e.g., ) arms uniformly at random, and then run a standard UCB algorithm (Lai and Robbins 1985, Auer et al. 2002) with just these arms.

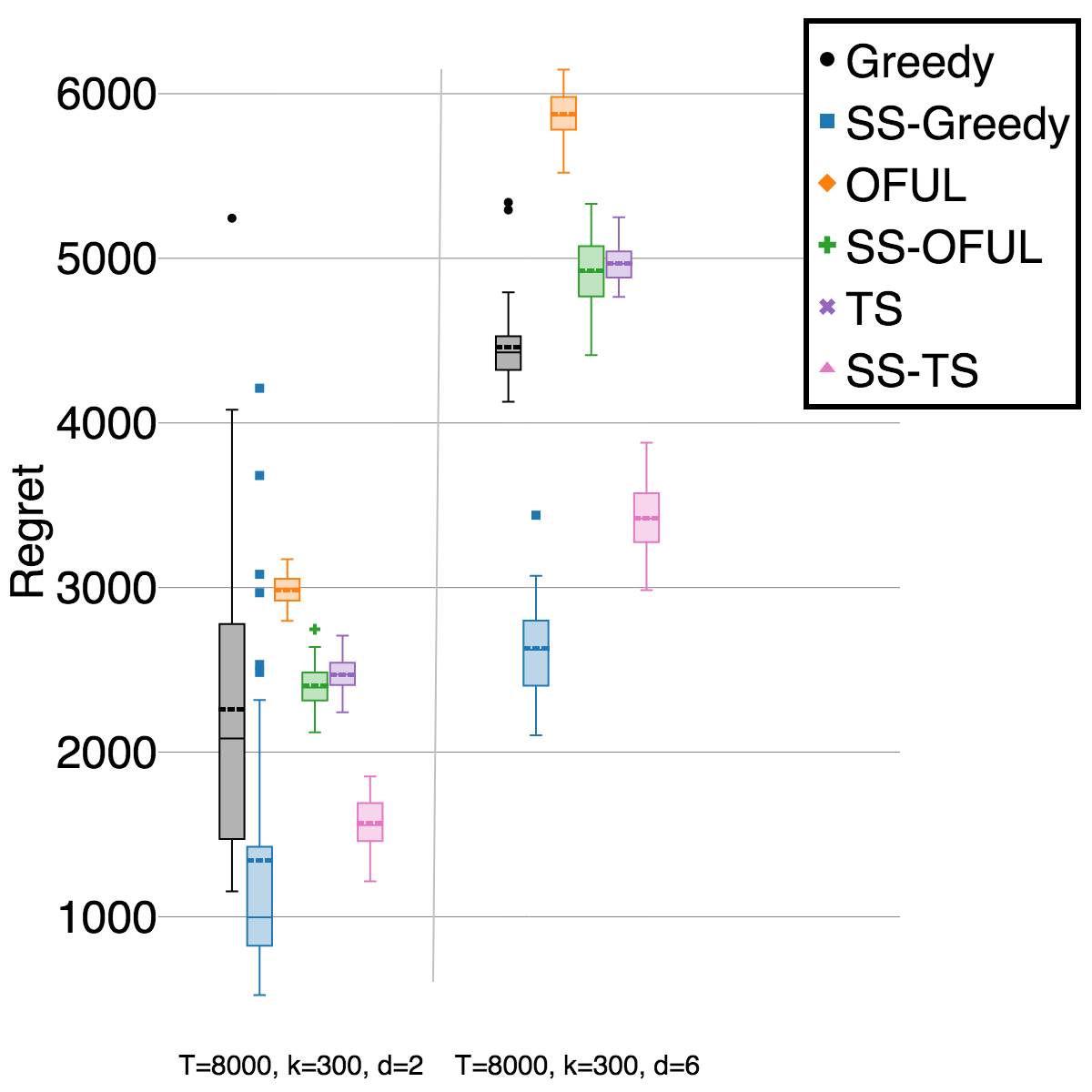

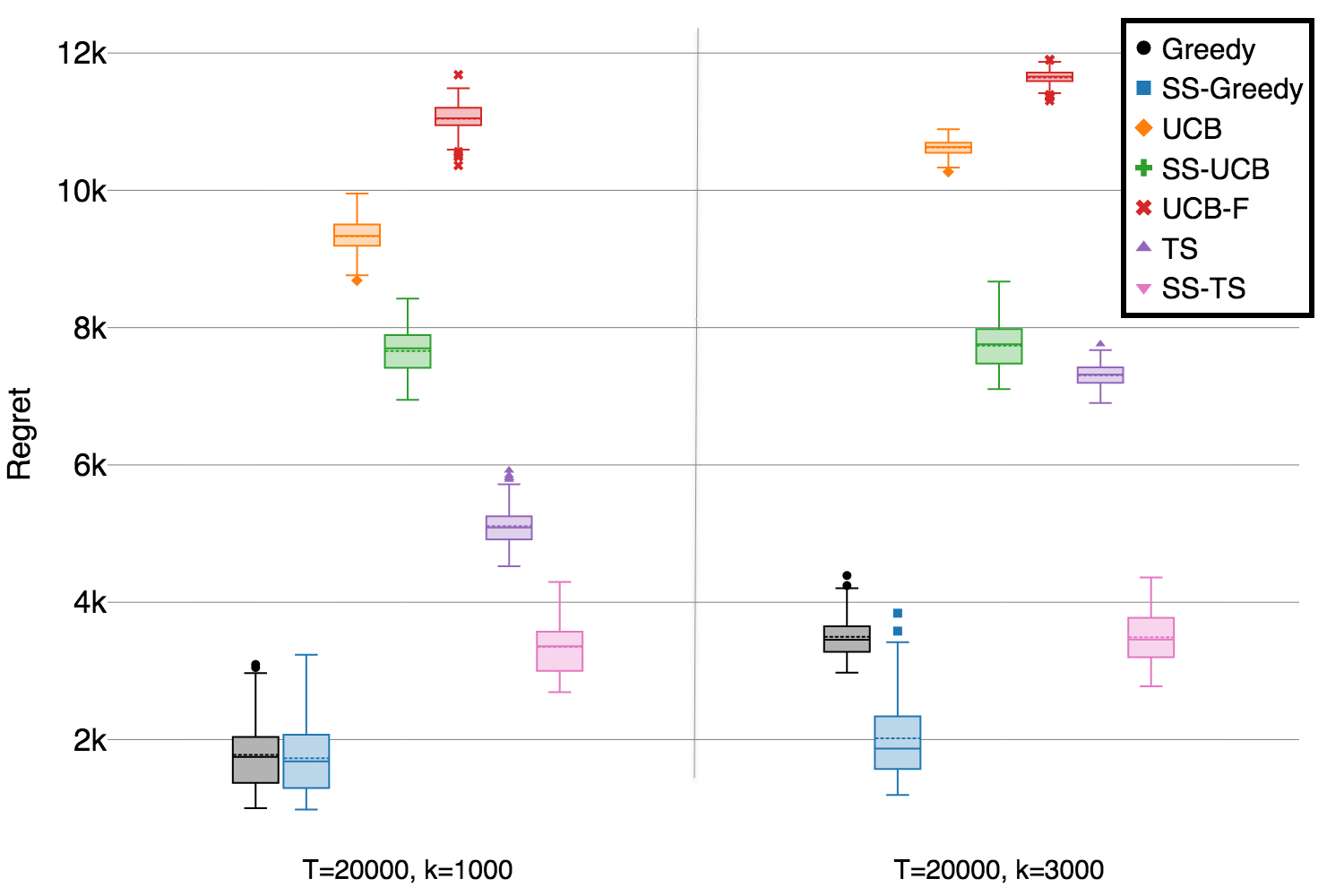

However, numerical investigation reveals more interesting behaviors. In Figure 1, we simulate several different algorithms over 400 simulations, for two pairs of in the many-armed regime. Notably, the greedy algorithm (Greedy) — i.e., an algorithm that pulls each arm once, and thereafter pulls the empirically best arm for all remaining times – performs extremely well. This is despite the well-known fact that Greedy can suffer linear regret in the standard MAB problem, as it can fixate too early on a suboptimal arm. Observe that in line with our first insight above, subsampling improves the performance of all algorithms, including UCB, Thompson sampling (TS), and Greedy. In particular, the subsampled greedy algorithm (SS-Greedy) outperforms all other algorithms.

The right panel in Figure 1 shows that Greedy and SS-Greedy benefit from a novel form of free exploration, that arises due to the availability of a large number of near-optimal arms. This free exploration helps the greedy algorithms to quickly discard sub-optimal arms that are substantially over-explored by algorithms with “active exploration” (i.e., UCB, TS, and their subsampled versions). We emphasize that this source of free exploration is distinct from that observed in recent literature on contextual bandits (see, e.g., Bastani et al. 2020, Kannan et al. 2018, Raghavan et al. 2018, Hao et al. 2020), where free exploration arises due to diversity in the context distribution. Our extensive simulations in Section 5 and in Appendix 10 show that these insights are robust to varying rewards and prior distributions. Indeed, similar results are obtained with Bernoulli rewards and general beta priors. Further, using simulations, we also observe that the same phenomenon arises in the contextual MAB setting, via simulations with synthetic and real-world data.

Motivated by these observations, in §4 and §6 we embark on a theoretical analysis of Greedy in the many-armed regime to complement our empirical investigation and shed light on the aforementioned source of free-exploration. We show that with high probability, one of the arms on which Greedy concentrates attention is likely to have a high mean reward (as also observed in the right panel of Figure 1). Our proof technique uses the Lundberg inequality to relate the probability of this event to distribution of the ruin event of a random walk, and may be of independent interest in studying the performance of greedy algorithms in other settings. Using this result we show that for Bernoulli rewards, the regret of Greedy is ; in particular, for SS-Greedy is optimal (and for , Greedy is optimal). For more general reward distributions we show that, under a mild condition, an upper bound on the regret of Greedy is . Thus theoretically, for general reward distributions, in the many-armed regime Greedy achieves sublinear, though not optimal, regret.

Our theoretical results illuminate why Greedy and SS-Greedy perform well in our numerical experiments, due to the novel form of free exploration we identify in the many-armed regime. Although our theoretical results do not establish universal rate optimality of SS-Greedy, this is clearly a case where regret bounds do not tell the whole story. Indeed, given the robust empirical performance of Greedy and SS-Greedy, from a practical standpoint the combination of our empirical and theoretical insights suggests that in applications it may be preferable to use greedy algorithms in the many-armed regime. This advice is only amplified when one considers that in contextual settings, such algorithms are likely to benefit from free exploration due to context diversity as well (as noted above).

1.1 Related Work

The literature on stochastic MAB problems with a finite number of arms is vast; we refer the reader to recent monographs by Lattimore and Szepesvári (2020) and Slivkins (2019) for a thorough overview. Much of this work carries out a frequentist regret analysis. In this line, our work is most closely related to work on the infinitely many-armed bandit problem, first studied by Berry et al. (1997) for Bernoulli rewards. They provided algorithms with regret, and established a lower-bound in the Bernoulli setting while a matching upper bound is proved by Bonald and Proutiere (2013). In (Wang et al. 2009), the authors studied more general reward distributions and proposed an optimal (up to logarithmic factors) algorithm called UCB-F that is constructed based on the UCB-V algorithm of Audibert et al. (2007). In fact, our results in §3 also leverage ideas from (Wang et al. 2009). The analysis of the infinitely many-armed bandit setting was later extended to simple regret (Carpentier and Valko 2015) and quantile regret minimization (Chaudhuri and Kalyanakrishnan 2018). Adjustments of confidence bounds in the setting where number of arms scales as was studied in (Chan and Hu 2019). In a related work, Russo and Van Roy (2018) proposed using a variant of Thompson Sampling for finding “satisficing” actions in the complex settings where finding the optimal arm is difficult.

Our results complement the existing literature on Bayesian regret analysis of the stochastic MAB. The literature on the Bayesian setting goes back to index policies of Gittins (1979) that are optimal for the infinite-horizon discounted reward setting. Bayesian bounds for a similar problem like ours, but when is fixed and were established in Kaufmann (2018); their bounds generalized the earlier results of Lai et al. (1987), who obtained similar results under more restrictive assumptions.

Several other papers provide fundamental bounds in the fixed setting. Bayesian regret bounds for the Thompson Sampling algorithm were provided in (Russo and Van Roy 2014b) and information-theoretic lower bounds on Bayesian regret for fixed were established in (Russo and Van Roy 2016). Finally, Russo and Van Roy (2014a) proposed to choose policies that maximize information gain, and provided regret bounds based on the entropy of the optimal action distribution.

Very recently, and building on our results, Jedor et al. (2021) provide additional support for our main recommendation that employing greedy algorithms in practice may be preferred when the number of arms is large.

2 Problem Setting and Notation

We consider a Bayesian -armed stochastic bandit setting where a decision-maker sequentially pulls from a set of unknown arms, and aims to maximize the expected cumulative reward generated. In this section we present the technical details of our model and problem setting. Throughout, we use the shorthand that denotes the set of integers . We also use the notations , , and to represent asymptotic scaling of different parameters (de Bruijn 1981). And we use instead of when the asymptotic relationship holds up to logarithmic factors.

Time.

Time is discrete, denoted by ; denotes the time horizon.

Arms.

At each time , the decision-maker chooses an arm from a set of arms.

Rewards.

Each time the decision maker pulls an arm, a random reward is generated. We assume a Bayesian setting that arm rewards have distributions with parameters drawn from a common prior. Let be a collection of reward distributions, where each has mean . Further, let be a prior distribution on for ; we assume is absolutely continuous w.r.t. Lebesgue measure in , with density . For example, might be the family of all binomial distributions with parameters , and might be the uniform distribution on .111Our results can be extended to the case where the support of is a bounded interval . The following definition adapted from the infinitely-many armed bandit literature (see, e.g. Wang et al. 2009, Carpentier and Valko 2015) is helpful in our analysis.

Definition 2.1 (-regular distribution)

Distribution defined over is called -regular if

when goes to . Equivalently, there exists positive constants such that

For simplicity, throughout the paper we assume that is -regular and discuss how our results can be generalized to an arbitrary in §6 and §12.1.

The distribution is -regular. Assumption 2 puts a constraint on , which quantifies how many arms are -optimal. The larger number of -optimal arm means it is more likely that Greedy concentrates on an -optimal arm which is one of main components of our theoretical analysis (see Lemma 4.1). We also assume that the reward distributions are -subgaussian as defined below and for notation simplicity we assume , but generalization of our results to any is straightforward. {assumption} Every is -subgaussian: for any and any , if is distributed according to , then

Given a realization of reward means for the arms, let denote the reward upon pulling arm at time . Then is distributed according to , independent of all other randomness; in particular, . Note that is the actual reward earned by the decision-maker. As is usual with bandit feedback, we assume the decision-maker only observes , and not for .

Policy.

Let denote the history of selected arms and their observed rewards up to time . Also, let denote the decision-maker’s policy (i.e., algorithm) mapping to a (possibly randomized) choice of arm . In particular, is a distribution over , and is distributed according to , independently of all other randomness.

Goal.

Given a horizon of length , a realization of , and the realization of actions and rewards, the realized regret is

We define to be the expectation of the above quantity with respect to randomness in the rewards and the actions, given the policy and the mean reward vector ,

Here the notation is shorthand to indicate that actions are chosen according to the policy , as described above; the expectation is over randomness in rewards and in the choices of actions made by the policy. In the sequel, the dependence of the above quantity on will be important as well; we make this explicit as necessary.

The decision-maker’s goal is to choose to minimize her Bayesian expected regret, i.e., where the expectation is taken over the prior as well as the randomness in the policy. In other words, the decision-maker chooses to minimize

| (1) |

Many arms.

In this work, we are interested in the setting where and are comparable. In particular, we focus on the scaling of in different regimes for and .

3 Lower Bound and an Optimal Algorithm

In this section, we first show that Bayesian regret of any policy is larger than the minimum of and up to constants, in §3.1. Then, in §3.2, we show how this lower bound can be achieved, up to logarithmic factors, by integrating subsampling into the UCB algorithm.

3.1 Lower Bound

Our lower bound on is stated next.

Theorem 3.1

This theorem shows that the Bayesian regret of an optimal algorithm should scale as when and as if . The proof idea is to show that for any policy , there is a class of “bad arm orderings” that occur with constant probability for which a regret better than is not possible. The complete proof is provided in §8.1. Interestingly, this theorem does not require any additional assumption on reward distributions beyond Assumption 2 on the prior distribution of reward means.

3.2 An Optimal Algorithm

In this section we describe an algorithm that achieves the lower bound of §3.1, up to logarithmic factors. Recall that we expect to observe two different behaviors depending on whether or ; Theorems 3.2 and 3.3 state our result for these two cases, respectively. In particular, Theorem 3.3 shows that subsampling is a necessary step in the design of optimal algorithms in the many-armed regime. Proofs of these theorems are provided in §8.2. Note that for Theorem 3.2, instead of Assumption 2, we require the density (of ) to be bounded from above.

We require several definitions. For , define:

where is the indicator function. Thus is the number of times arm is pulled up to time , and is the empirical mean reward on arm up to time . (We arbitrarily define if .) Also define,

3.2.1 Case .

In this case, we show that the UCB algorithm (see, e.g., Chapter 8 of (Lattimore and Szepesvári 2020)) is optimal, up to logarithmic factors. For completeness, this algorithm is restated as Algorithm 1.

Theorem 3.2

3.2.2 Case .

For large , because of the first time periods that each arm is pulled once, UCB incurs regret which is not optimal. This fact suggests that subsampling arms is a required step of any optimal algorithm. In fact, we show that in this case the subsampled UCB algorithm (SS-UCB) is optimal (up to logarithmic factors).

Theorem 3.3

4 A Greedy Algorithm

While in §3 we showed that SS-UCB enjoys the so called “rate optimal” performance, the simulations of Figure 1 in §1 suggest that a greedy algorithm and its subsampled version are superior. Motivated by this observation, in this section we embark on analyzing this greedy algorithm to shed some light on its empirical performance. The greedy algorithm pulls each arm once and from then starts pulling the arm with the highest estimated mean; the formal definition is shown in Algorithm 3. We can also define a subsampled greedy algorithm that randomly selects arms and executes Algorithm 3 on these arms. This subsampled form of greedy is stated as Algorithm 4. As in previous section, we denote the estimated mean of arm at time by .

Our road map to analyze the above algorithms is as follows. First, in §4.1 , we prove a general upper bound on regret of Algorithm 3 that depends on probability of a tail event for a certain random walk, with steps that are distributed according to the arms’ reward distribution . This result opens the door to prove potentially sharper regret bounds for specific families of reward distributions, if one can prove tight bounds for the aforementioned tail event. We provide two examples of this strategy in §4.2-4.1. In §4.2, we consider Bernoulli reward functions and prove a rate-optimal regret bound of for Greedy when and for SS-Greedy when . In the remaining parts we obtain sub-linear regrets for more general family of distributions.

4.1 A General Upper Bound on Bayesian Regret of Greedy

We require the following definition. For a fix and , let be a sequence of i.i.d. random variables with distribution . Let , and define as the probability that the sample average always stays above ,

| (2) |

In other words, is the probability of the tail event that the random walk with i.i.d. samples drawn from never crosses .

The following lemma (proved in §9.1) gives a general characterization of the Bayesian regret of Greedy, under the assumption that rewards are subgaussian (Assumption 2).

Lemma 4.1 (Generic bounds on Bayesian regret of Greedy)

Lemma 4.1 is the key technical result in the analysis of Greedy and SS-Greedy. This bound depends on several components, in particular, the choice of and the scaling of . To ensure sublinear regret, should be small, but that increases the first term as decreases. The scaling of is also important; in particular, the shape of will dictate the quality of the upper bound obtained.

Observe that is the only term in (3) that depends on the family of reward distributions . In the remainder of this section, we provide three upper bounds on Bayesian regret of Greedy and SS-Greedy. The first one is designed for Bernoulli rewards; here has a constant lower bound, leading to optimal regret rates. The second result requires -subgaussian rewards (Assumption 2); this leads to a which is quadratic in . The last bound makes an additional (mild) assumption on the reward distribution (covers many well-known rewards, including Gaussians); this leads to a that is linear in which leads to a better bound on regret compared to -subgaussian rewards.

The bounds that we establish on rely on Lundberg’s inequality, which bounds the ruin probability of random walks and is stated below. For more details on this inequality, see Corollary 3.4 of (Asmussen and Albrecher 2010).

Proposition 4.2 (Lundberg’s Inequality)

Let be a sequence of i.i.d. samples from distribution . Let and . For define the stopping time222Note that in risk theory, usually the random walk is considered and is probability of hitting , i.e., ruin.

and let denote the probability . Let satisfy and that , almost surely, on the set . Then, we have

4.2 Optimal Regret for Bernoulli Rewards

In this case, we can prove that there exists a constant lower bound on .

Lemma 4.3

Suppose is the Bernoulli distribution with mean , and fix . Then, for ,

The preceding lemma reveals that for and , for the choice we have . We can now state our theorem.

Theorem 4.4

Suppose that is Bernoulli distribution with mean and the prior distribution on satisfies Assumption 2. Then, for

Furthermore, Bayesian regret of SS-Greedy when executed with is .

This theorem shows that for , Greedy is optimal (up to log factors). Similarly, for , SS-Greedy is optimal. The proofs of both results is in Appendix 9.2.

4.3 Sublinear Regret for Subgaussian Rewards

Here we show that the generic bound of Lemma 4.1 can be used to obtain a sublinear regret bound in the general case of -subgaussian reward distributions. Specifically, first we can prove the following bound on .

Lemma 4.5

If is -subgaussian, then for we have

Next, from this lemma we obtain

Combining this and Lemma 4.1, we can prove the following result for Greedy and SS-Greedy.

Theorem 4.6

Proofs of Lemma 4.5 and Theorem 4.6 are provided in §9.3. While this upper bound on regret is appealing – in particular, it is sublinear regret when is large — we are motivated by the empirically strong performance of Greedy and SS-Greedy (cf. Figure 1) to see if a stronger upper bound on regret is possible.

4.4 Tighter Regret Bound for Uniformly Upward-Looking Rewards

To this end, we make progress by showing that the above results are further improvable for a large family of subgaussian reward distributions, including Gaussian rewards. The following definition describes this family of reward distributions.

Definition 4.7 (Upward-Looking Rewards)

Let be the reward distribution, and by abuse of notation, let be also a random variable with the same distribution. Also, assume and that is -subgaussian. Let be a sequence of i.i.d. random variables distributed according to and . For define and

We call the distribution upward-looking with parameter if for any one of the following conditions hold:

-

1.

-

2.

.

More generally, a reward family with is called uniformly upward-looking with parameters if for is upward-looking with parameter .

In §4.4.1 below, we show that a general class of reward families is uniformly upward-looking. In particular, class of reward distributions that for all satisfy are uniformly upward looking with parameters . This class includes the Gaussian rewards.

The preceding discussion reveals that many natural families of reward distributions are upward-looking. The following lemma shows that for such distributions, we can sharpen our regret bounds.

Lemma 4.8

Let be upward-looking with parameter which satisfies . Let be an iid sequence distributed as , and . Then for any ,

From this lemma, for we have

The following theorem shows that in small regime, this linear yields a strictly sharper upper bound on regret than a quadratic .

Theorem 4.9

It is worth noting that in the case where subsampling is inevitable, the results presented on SS-Greedy in Theorems 4.4 and 4.9 are still valid. The main reason is that our proof technique presented in Lemma 4.1 bounds the regret with respect to the “best” possible reward of which as stated in Lemma 4.1 allows for an immediate replacement of with the subsampling size .

4.4.1 Examples of Uniformly Upward-Looking Distributions

Here we show that two general family of distributions are uniformly upward-looking.

First, we start by showing that the Gaussian family is uniformly upward looking. Suppose . Then, for any the family is uniformly upward-looking with parameters . To see this, note that for any the random variable is distributed according to . Hence, using the second condition in Definition 4.7, for we have

More generally, suppose that is -subgaussian and consider the family of reward distributions . In other words, the family is shift-invariant, meaning that . The same argument as the above (Gaussian) case shows that for any choice of , is uniformly upward-looking with parameters with .

Second, we show that a family of reward distributions satisfying the following: there exist constants and such that for any integer exists such that:

| (4) |

Then, it is easy to observe that is upward-looking with parameters . For example, this also can be used to prove that the Gaussian rewards are uniformly upward-looking: take , then the above condition translates to

where is the CDF of the standard Gaussian distribution.

The proof of the above claim is as follows. The idea is to show that for any family satisfying Eq. (4) the first condition for the uniformly upward-looking distribution is satisfied. Indeed, consider and let . Then, we claim that the random walk crosses before crossing zero, with probability at least . Indeed, Eq. (4) implies that the probability that all observations are at least is at least . In this case, as , with probability , the random walk will not cross zero before and it crosses at . This proves our claim.

5 Simulations

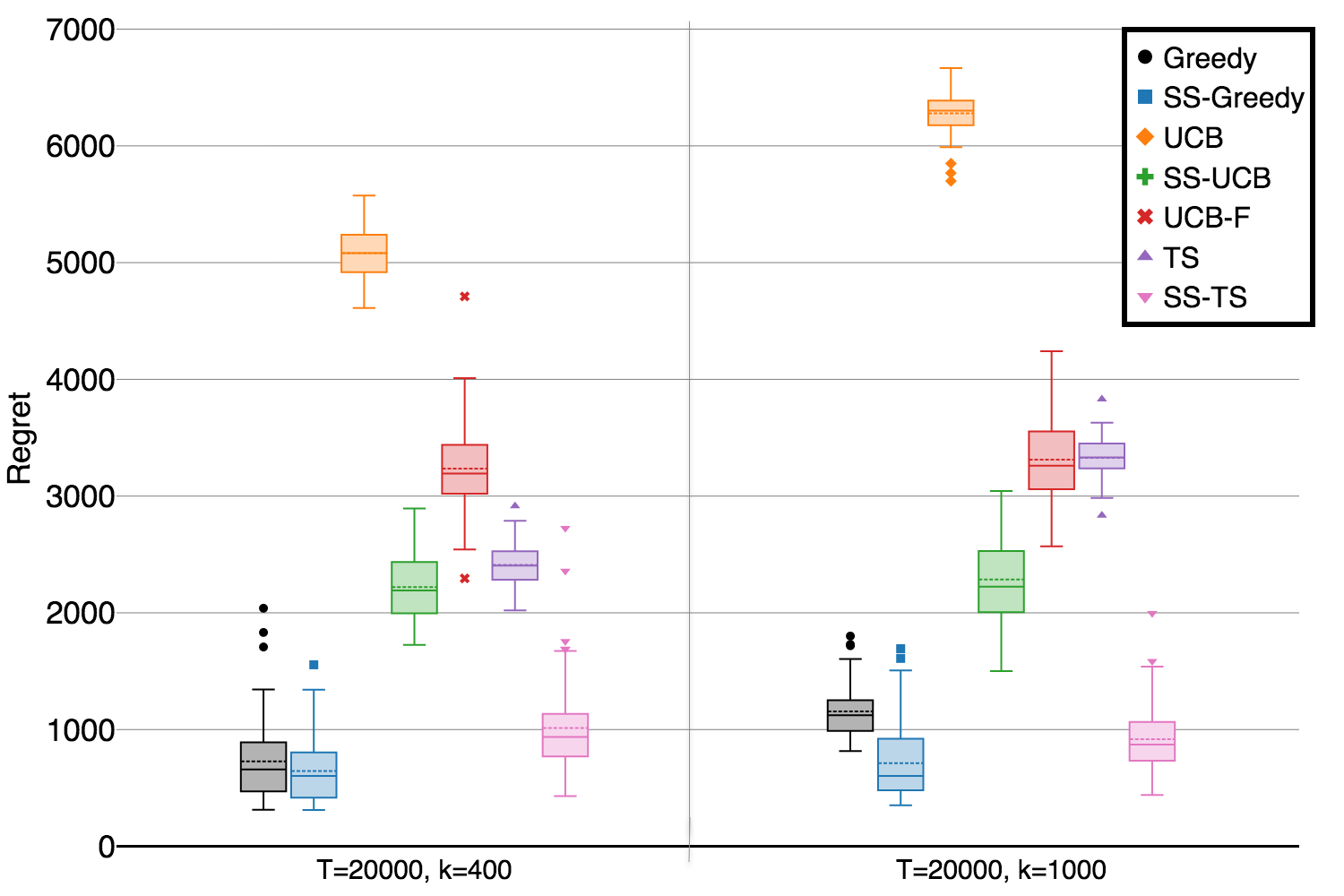

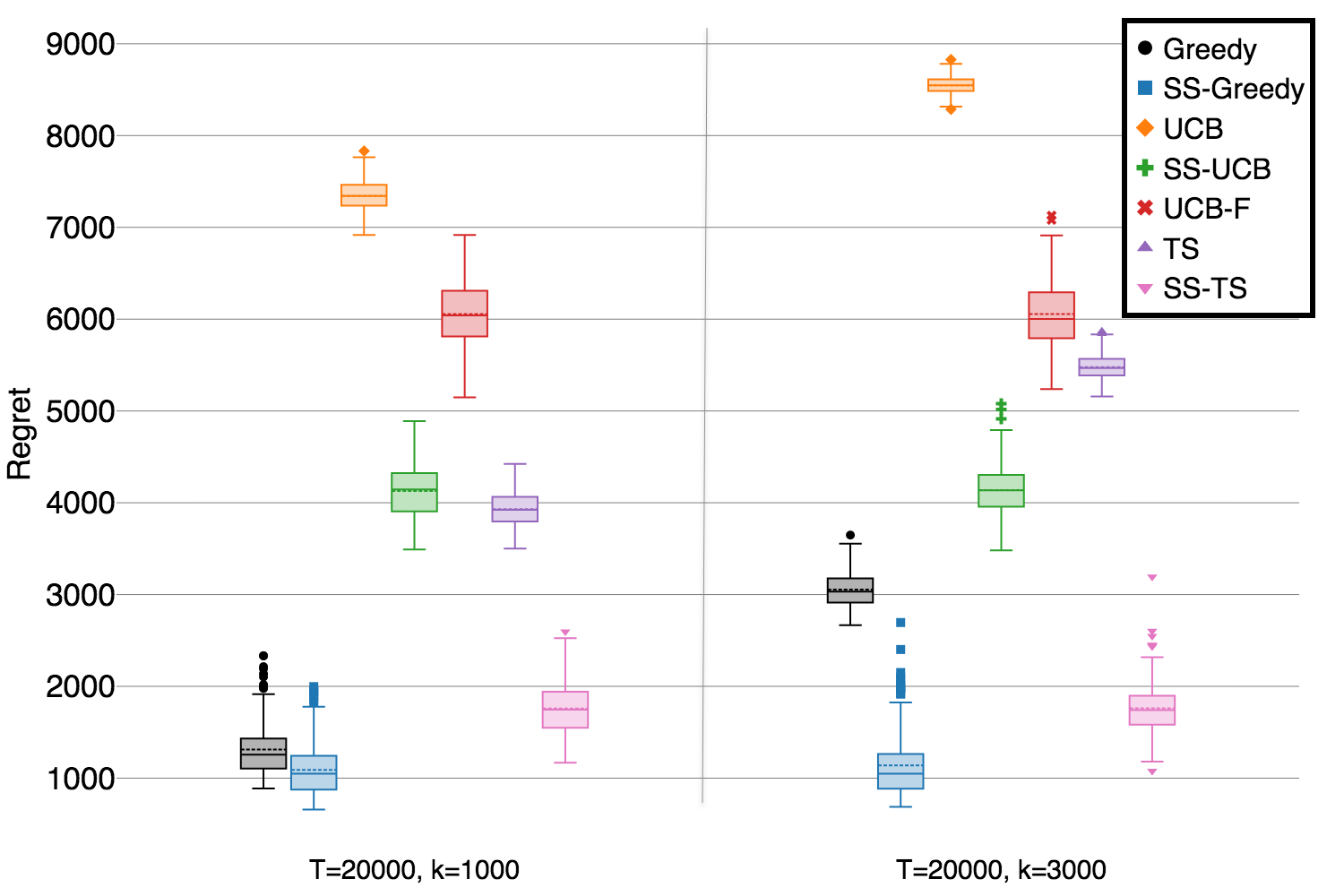

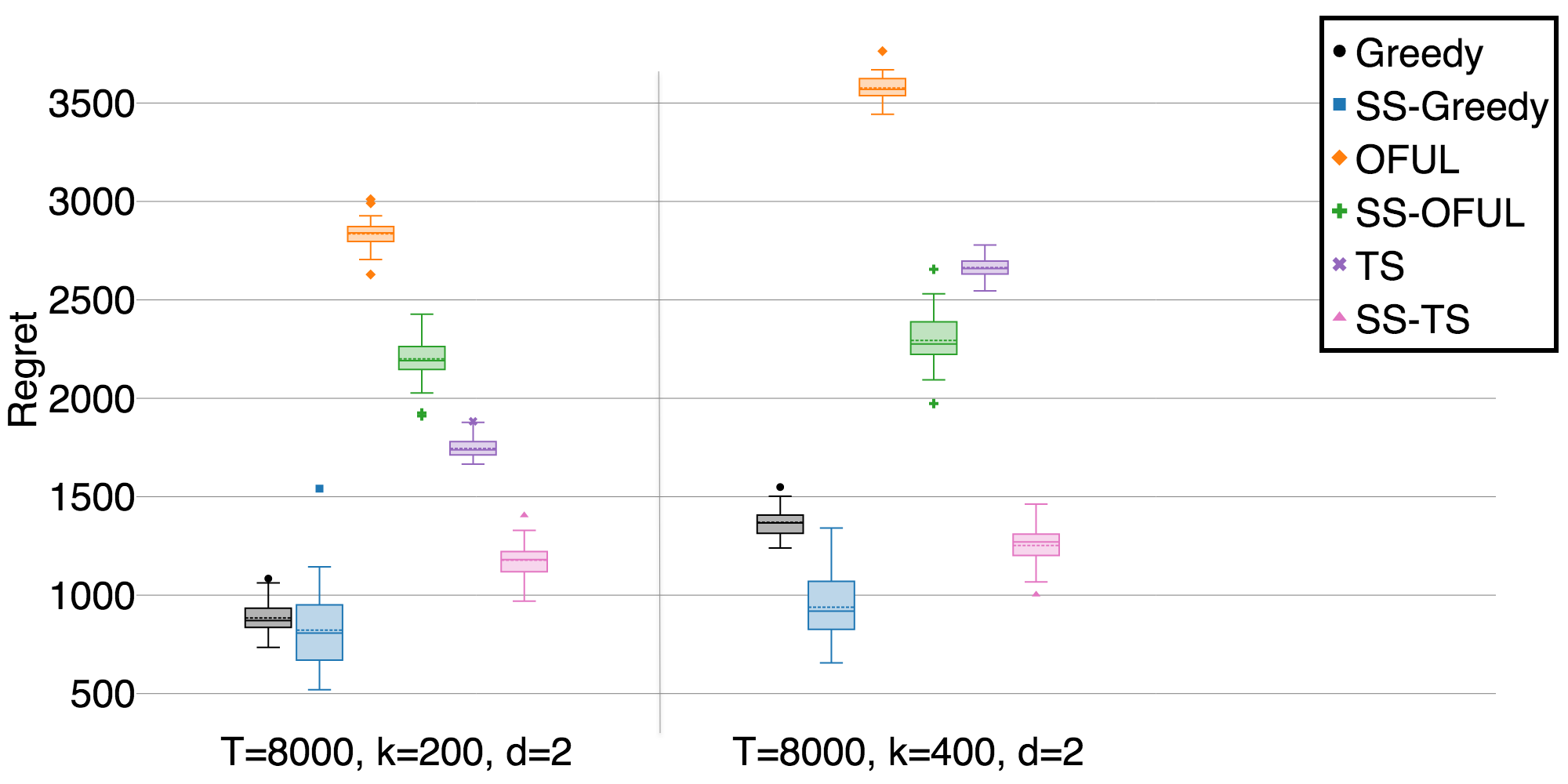

Recall Figure 1 with results of simulations for two pairs of in the many-armed regime where rewards were generated according to Gaussian noise and uniform prior. These results are robust when considering a wide range of beta priors as well as both Gaussian and Bernoulli rewards (see §10). In this section, motivated by real-world applications, we consider a contextual reward setting and show that our theoretical insights carry to the contextual setting as well.333Codes and data for reproducing all empirical results of the paper are available in this Github repository https://github.com/khashayarkhv/many-armed-bandit.

Data and Setup.

We use the Letter Recognition Dataset Frey and Slate (1991) from the UCI repository. The dataset is originally designed for the letter classification task ( classes) and it includes samples, each presented with covariates. As we are interested in values of , we only use the covariates from this dataset and create synthetic reward functions as follows. We generate arms with parameters ( will be specified shortly) and generate reward of arm at time via

where is the context vector at time and is iid noise.

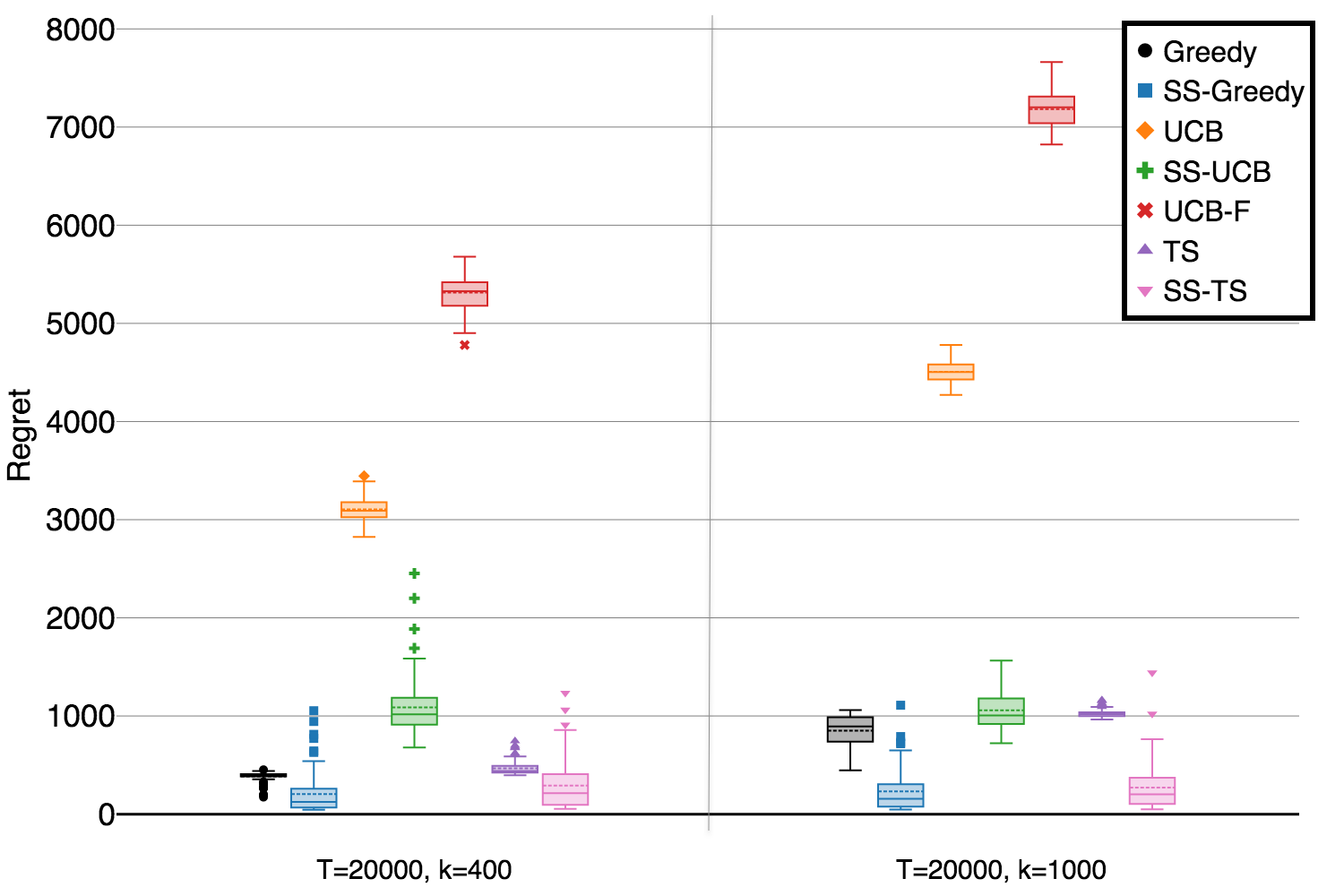

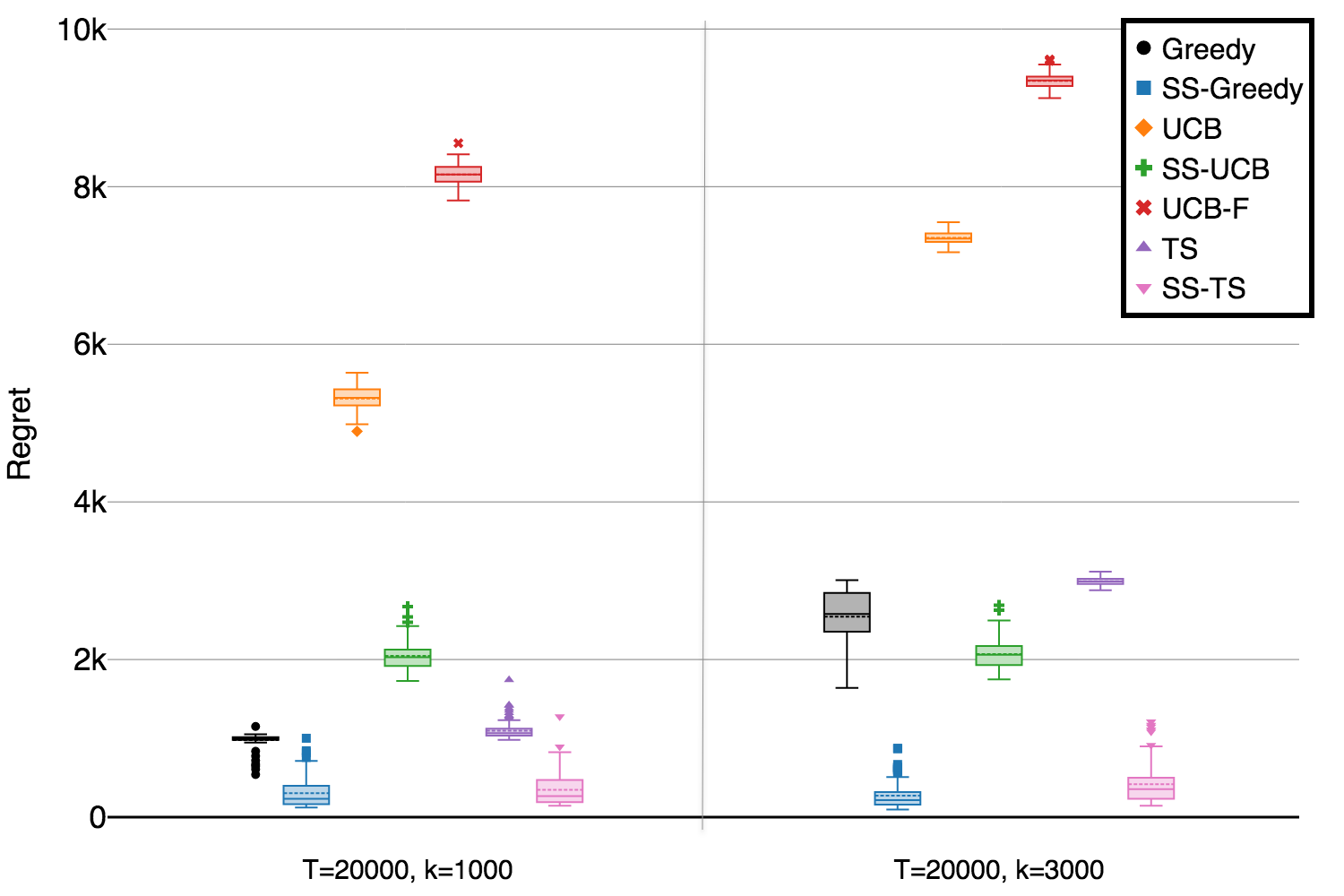

Our goal is to show that there are two distinct sources of free exploration. The first one is due to the variation in covariates, and the other one is due to having large number of arms. Therefore, we consider two experiments with and and compare the performance of several algorithms in these two cases. As contexts are -dimensional, we project them onto -dimensional subspaces using SVD.

For each , we generate different simulation instances, where we pick samples at random (from the original samples) and generate the arm parameters according to the uniform distribution on the -ball in , i.e., . We plot the distribution of the per-instance regret in each case, for each algorithm; note the mean of this distribution is (an estimate of) the Bayesian regret. We study the following algorithms and also their subsampled versions (with subsampling ; subsampling is denoted by “SS”):

-

1.

Greedy,

-

2.

OFUL Algorithm (Abbasi-Yadkori et al. 2011), and

- 3.

Results.

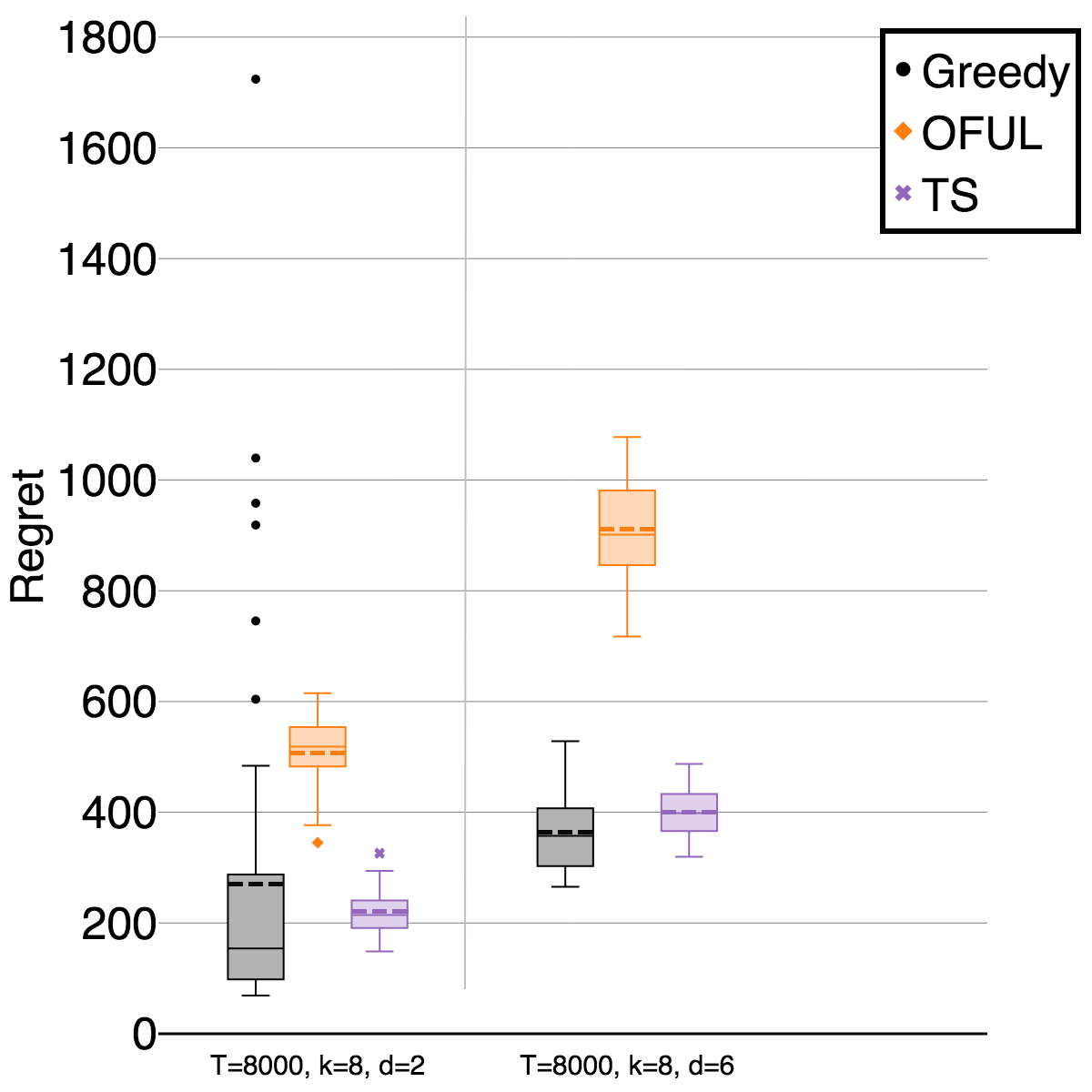

The results are depicted in Figure 2(a). We can make the following observations. First, subsampling is an important concept in the design of low-regret algorithms, and indeed, SS-Greedy outperforms all other algorithms in both settings. Second, Greedy performs well compared to OFUL and TS, and it benefits from the same free exploration provided by a large number of arms that we identified in the non-contextual setting: if it drops an arm due to poor empirical performance, it is likely that another arm with parameter close to is kept active, leading to low regret. Third, we find that SS-TS actually performs reasonably well; it has a higher average regret compared to SS-Greedy, but smaller variance. Finally, by just focusing on Greedy, OFUL, and TS (ignoring their SS versions) and comparing with Figure 2(b), we see empirical evidence that the aforementioned source of free exploration is different from that observed in recent literature on contextual bandits (see, e.g., (Bastani et al. 2020, Kannan et al. 2018, Raghavan et al. 2018, Hao et al. 2020)), where free exploration arises due to diversity in the context distribution. For example, simulations of Bastani et al. (2020) show that when is too small compared to , the context diversity is small and performance of Greedy deteriorates which leads to a high variance for its regret. Figure 2(b) which shows results of the above simulation, but using only arms, underscores the same phenomena – by reducing the number of arms, the performance of Greedy substantially deteriorates compared to TS and OFUL. But in the case of , even with , Greedy has the best average and median regret.

6 Generalizations

In this section we generalize results of §3-4 in two ways. First, in §6.1, we relax Assumption 2 and consider more general prior distributions. We prove that all results that appeared in §3-4 can be generalized to the broader family of -regular prior distributions, introduced in Definition 2.1. Second, in §6.2, we consider a more effective version of the SS-Greedy algorithm, called Seq-Greedy, and prove that our results for SS-Greedy also hold for Seq-Greedy.

6.1 General -regular Priors

Assume that the prior reward distribution is -regular per Definition 2.1. Before stating the results, we need to update the notion of “many armed regime” as well as subsampling rate of various algorithms.

Small versus large regime.

It can be shown (see §12 for details) that the transition from small to large regime, for lower bound, depends on whether or not. However, for the upper bounds, the transition point is algorithm dependent (depending on which term of the regret is dominant). For example, when and the reward is Gaussian, we saw in §3-4 that for the lower bounds (and even some upper bounds) the transition from small to large occurs at . However, our result for Greedy in §4 would give

which means the small versus large transition for this upper bound occurs at .

Subsampling rate.

Conditions on the density.

Similar to Theorem 3.2, for we require a bounded density for UCB and SS-UCB in the small regime. For , it is easy to observe that the density cannot be bounded near as . Hence, in this setting we instead assume that

A new notation for greedy algorithms.

We introduce a new notation, , that will be used for Greedy and SS-Greedy. To motivate the notation, recall that results in §4 qualitatively depend on the exponent of in . On the other hand, since the term by definition is of order , we could argue the exponent of in the expression

| (5) |

that appeared in Lemma 4.1, dictates the regret upper bounds. With that motivation in mind, let us define to be a lower bound on the exponent of in (5). More concretely, we assume is a constant that satisfies444One can be more precise and define to be the supremum of all constants that satisfy (6), but for our purposes this level of precision is not necessary. the following:

| (6) |

Clearly, any such constant must satisfy the inequality , given Definition 2.1. But for some reward distributions one may need to pick strictly larger than . In fact, we use the arguments of §4 and show that the constants

-

•

,

-

•

, and

-

•

satisfy (6).

6.1.1 Results for -regular priors

First, we show that a similar argument as in §3.1 can be used to show that regret of any policy is at least

This highlights that from the perspective of the lower bounds small versus large is determined when versus respectively. For the upper bounds, the results are presented in Table 1 below. Specifically, Table 1 shows upper bounds for each of UCB and Greedy and their subsampling versions, for both small versus large and when is smaller or larger than . A more detailed version of all these results with corresponding proofs is deferred to §12.

| small | large | small | large | |

| Algorithm | ||||

| UCB | ||||

| SS-UCB | ||||

| Greedy | ||||

| SS-Greedy | ||||

6.2 Sequential Greedy

When is large, allocating the first (or arms in case of subsampling) time-periods for exploration before exploiting the good arms may be inefficient. We can design a sequential greedy algorithm, in which an arm is selected and pulled until its sample average drops below a certain threshold, say . Once that happens, a new arm is selected and a similar routine is performed; we denote this algorithm by Seq-Greedy and its peseudo-code is shown in Algorithm 5.

In this section we show that for an appropriate choice of , Bayesian regret of Seq-Greedy is similar to that of SS-Greedy.

First, we state the following result on the regret of Seq-Greedy.

Lemma 6.1 (Bayesian Regret of Seq-Greedy)

Let Assumption 2 hold and suppose that Algorithm 5 is executed with parameter . Define as the probability that sample average of an i.i.d. sequence distributed according to never crosses (see also Eq. (2)). Then, for any integer , the following bound holds on the Bayesian regret of the Seq-Greedy algorithm:

| (7) |

Note that the above result shows that the Bayesian Regret of Seq-Greedy is at most

i.e., the best possible rate one can achieve by optimizing in the upper bound of regret of Greedy presented in Lemma 4.1.

While the above result can be used to prove similar results as those presented in Table 1, we only prove this for the case (similar to §3-4) as the proofs of other cases are similar.

Theorem 6.2 (Bayesian Regret of Seq-Greedy)

7 Conclusion

We first prove that in multi armed problems with many arms subsampling is a critical step in designing optimal policies. This is achieved by proving a lower bound for Bayesian regret of any policy and showing that it can be achieved when subsampling is integrated with a standard UCB algorithm. But surprisingly, through both empirical investigation and theoretical development we found that greedy algorithms, and a subsampled greedy algorithm in particular, can outperform many other approaches that depend on active exploration. In this way our paper identifies a novel form of free exploration enjoyed by greedy algorithms, due to the presence of many arms. As noted in the introduction, prior literature has suggested that in contextual settings, greedy algorithms can exhibit low regret as they obtain free exploration from diversity in the contexts. An important question concerns a unified theoretical analysis of free exploration in the contextual setting with many arms, that provides a complement to the empirical insights we obtain in the preceding sections. Such an analysis can serve to illuminate both the performance of Greedy and the relative importance of context diversity and the number of arms in driving free exploration; we leave this for future work.

Acknowledgements

This work was supported by the Stanford Human-Centered AI Institute, and by the National Science Foundation under grants 1931696, 1839229, and 1554140.

References

- Abbasi-Yadkori et al. (2011) Abbasi-Yadkori, Yasin, Dávid Pál, Csaba Szepesvári. 2011. Improved algorithms for linear stochastic bandits. Advances in Neural Information Processing Systems. 2312–2320.

- Agrawal and Goyal (2012) Agrawal, Shipra, Navin Goyal. 2012. Analysis of thompson sampling for the multi-armed bandit problem. Conference on learning theory. 39–1.

- Asmussen and Albrecher (2010) Asmussen, Søren, Hansjörg Albrecher. 2010. Ruin probabilities, vol. 14. World scientific Singapore.

- Audibert et al. (2007) Audibert, Jean-Yves, Rémi Munos, Csaba Szepesvári. 2007. Tuning bandit algorithms in stochastic environments. International conference on algorithmic learning theory. Springer, 150–165.

- Auer et al. (2002) Auer, Peter, Nicolo Cesa-Bianchi, Paul Fischer. 2002. Finite-time analysis of the multiarmed bandit problem. Machine learning 47(2-3) 235–256.

- Bastani et al. (2020) Bastani, Hamsa, Mohsen Bayati, Khashayar Khosravi. 2020. Mostly exploration-free algorithms for contextual bandits. Management Science .

- Berry et al. (1997) Berry, Donald A, Robert W Chen, Alan Zame, David C Heath, Larry A Shepp. 1997. Bandit problems with infinitely many arms. The Annals of Statistics 2103–2116.

- Bonald and Proutiere (2013) Bonald, Thomas, Alexandre Proutiere. 2013. Two-target algorithms for infinite-armed bandits with bernoulli rewards. Advances in Neural Information Processing Systems. 2184–2192.

- Carpentier and Valko (2015) Carpentier, Alexandra, Michal Valko. 2015. Simple regret for infinitely many armed bandits. International Conference on Machine Learning. 1133–1141.

- Chan and Hu (2019) Chan, Hock Peng, Shouri Hu. 2019. Optimal ucb adjustments for large arm sizes. arXiv preprint arXiv:1909.02229 .

- Chaudhuri and Kalyanakrishnan (2018) Chaudhuri, Arghya Roy, Shivaram Kalyanakrishnan. 2018. Quantile-regret minimisation in infinitely many-armed bandits. UAI. 425–434.

- de Bruijn (1981) de Bruijn, N.G. 1981. Asymptotic Methods in Analysis. Bibliotheca mathematica, Dover Publications. URL https://books.google.com/books?id=Oqj9AgAAQBAJ.

- Frey and Slate (1991) Frey, Peter W, David J Slate. 1991. Letter recognition using holland-style adaptive classifiers. Machine learning 6(2) 161–182.

- Gittins (1979) Gittins, John C. 1979. Bandit processes and dynamic allocation indices. Journal of the Royal Statistical Society: Series B (Methodological) 41(2) 148–164.

- Hao et al. (2020) Hao, Botao, Tor Lattimore, Csaba Szepesvari. 2020. Adaptive exploration in linear contextual bandit. International Conference on Artificial Intelligence and Statistics. PMLR, 3536–3545.

- Jedor et al. (2021) Jedor, Matthieu, Jonathan Louëdec, Vianney Perchet. 2021. Be Greedy in Multi-Armed Bandits. arXiv e-prints arXiv:2101.01086.

- Kannan et al. (2018) Kannan, Sampath, Jamie H Morgenstern, Aaron Roth, Bo Waggoner, Zhiwei Steven Wu. 2018. A smoothed analysis of the greedy algorithm for the linear contextual bandit problem. Advances in Neural Information Processing Systems. 2227–2236.

- Kaufmann (2018) Kaufmann, Emilie. 2018. On bayesian index policies for sequential resource allocation. The Annals of Statistics 46(2) 842–865.

- Lai and Robbins (1985) Lai, Tze Leung, Herbert Robbins. 1985. Asymptotically efficient adaptive allocation rules. Advances in applied mathematics 6(1) 4–22.

- Lai et al. (1987) Lai, Tze Leung, et al. 1987. Adaptive treatment allocation and the multi-armed bandit problem. The Annals of Statistics 15(3) 1091–1114.

- Lattimore and Szepesvári (2020) Lattimore, Tor, Csaba Szepesvári. 2020. Bandit algorithms. Cambridge University Press.

- Raghavan et al. (2018) Raghavan, Manish, Aleksandrs Slivkins, Jennifer Wortman Vaughan, Zhiwei Steven Wu. 2018. The externalities of exploration and how data diversity helps exploitation. arXiv preprint arXiv:1806.00543 .

- Russo and Van Roy (2014a) Russo, Daniel, Benjamin Van Roy. 2014a. Learning to optimize via information-directed sampling. Advances in Neural Information Processing Systems. 1583–1591.

- Russo and Van Roy (2014b) Russo, Daniel, Benjamin Van Roy. 2014b. Learning to optimize via posterior sampling. Mathematics of Operations Research 39(4) 1221–1243.

- Russo and Van Roy (2016) Russo, Daniel, Benjamin Van Roy. 2016. An information-theoretic analysis of thompson sampling. The Journal of Machine Learning Research 17(1) 2442–2471.

- Russo and Van Roy (2018) Russo, Daniel, Benjamin Van Roy. 2018. Satisficing in time-sensitive bandit learning. arXiv preprint arXiv:1803.02855 .

- Slivkins (2019) Slivkins, Aleksandrs. 2019. Introduction to multi-armed bandits. Foundations and Trends® in Machine Learning 12(1-2) 1–286. 10.1561/2200000068. URL http://dx.doi.org/10.1561/2200000068.

- Thompson (1933) Thompson, William R. 1933. On the likelihood that one unknown probability exceeds another in view of the evidence of two samples. Biometrika 25(3/4) 285–294.

- Wang et al. (2009) Wang, Yizao, Jean yves Audibert, Rémi Munos. 2009. Algorithms for infinitely many-armed bandits. D. Koller, D. Schuurmans, Y. Bengio, L. Bottou, eds., Advances in Neural Information Processing Systems 21. 1729–1736.

8 Proofs of §3

8.1 Proof of the Lower Bound

Proof 8.1

Proof of Theorem 3.1. We start by proving that if , the Bayesian regret of any policy is at least for a constant .

Note that, without loss of generality, we can only consider the policies that first pull arm , then if needed arm , then if needed arm , and so on. This is because all arms have the same prior . More precisely, for any permutation on and any policy , let be the policy that pulls arm when policy pulls arm . Then, .

With this observation in hand, we define a class of “bad orderings” that happen with a constant probability, for which the Bayesian regret cannot be better than . This would prove our lower bound. More precisely, let and define event as the set of all realizations that satisfy the following conditions:

-

(i)

,

-

(ii)

,

-

(iii)

,

where and are the constants defined in Assumption 2.

First, we claim that the event happens with a constant probability. Note that if , then

| (8) |

using the lower bound in Assumption 2. Hence,

implying that event (i) happens with probability at least . Similar to Eq. (8), using the upper bound in Assumption 2, we have

where the right hand side inequality follows from the generalized Bernoulli inequality; therefore event (ii) holds with probability at least . Finally, we lower bound the probability of event (iii). In fact, using

we have . Hence, Hoeffding’s inequality implies that

when , i.e., if . This means (iii) occurs with probability at least . A union bound implies that,

In other words, the event happens at least for a constant fraction of realizations . We claim that on the realizations that are in , the expected regret of policy is lower bounded by , i.e.,

Note that given the assumption about the policy , the decision-maker starts by pulling arm , and continues pulling that arm for some number of rounds. At some point the decision-maker pulls arm (if needed), and then pulls only arms or for some number of rounds, until at some point she pulls arm (if needed); and so on. Although the choice of whether to try a new arm or keep pulling from the existing set of tried arms may depend on the observations , on any particular sample path one of these two possibilities arise:

-

•

Case 1. The decision-maker only pulls from the first arms during the -period horizon; or

-

•

Case 2. The decision-maker finishes pulling all arms in , and starts pulling some (or all) arms in the set .

We claim that in both cases, the decision-maker will incur regret. This is argued by considering each case in turn below.

Regret in Case 1.

In this case the regret incurred in each period , for , is at least . Therefore,

where the last inequality is true once .

Regret in Case 2.

In this case the algorithm pulls each of arms at least once and hence using

which holds when .

Thus regardless of the observations , and whether the decision-maker decides to try all arms in or only the arms in , the regret is lower bounded by , where . For finishing the proof note that we have

As a conclusion, if , then for any , the Bayesian regret of is at least .

Now if , then we can exploit the fact that the Bayesian regret is nondecreasing in time horizon. In other words, letting , we have and hence

as long as , meaning . Hence, letting and implies the result. \Halmos

8.2 Proofs for Upper Bound on SS-UCB

Proof 8.2

Proof of Theorem 3.2 The proof follows from the analysis of asymptotically optimal UCB algorithm which can be found in Lattimore and Szepesvári (2020) with slight modifications.

Suppose that are drawn from and let be a sorted version of these means. Denote and note that conditioned on , we can first derive an upper bound on the expected regret of the asymptotically optimal UCB algorithm and then take an expectation to derive an upper bound on the Bayes regret of this algorithm. Denote and decompose the expected regret as

where is the number of pulls of arm with mean till time . Theorem 8.1 of Lattimore and Szepesvári (2020) establishes an upper bound on . Specifically, for any , we have

Take and note that whenever , and . Hence,

Note that as the number of pulls for each arm is upper bounded by , we can write

Plugging this into the regret decomposition, we have

We need to take expectation of the above expression over the distribution of . As it can be observed from the above representation, only the distribution of matters. We separate the case of and , and also the terms from to write

Note that for the first term above, we can write

Lemma 11.5 shows that for any , we have , where is the upper bound on . Now looking at the term describing , we divide the expectation into two regimes: and . As it is shown in Lemma 11.5, has the following density

where we used the fact that together with the fundamental theorem of calculus. Note that here is the cumulative of distribution defined according to . Hence, we can write

Summing up all these terms, implies the following Bayesian regret bound for UCB:

as desired. \Halmos

Proof 8.3

Proof of Theorem 3.3 While this theorem can be proved from Theorem 3.2, here we provide a proof that does not require an upper bound on the density. First note that the regret on any instance , with subsampled arms can be written as

Taking an expectation implies that

Now, as arms have the same distribution as (i.e., ), the first term is Bayesian regret of UCB algorithm with arms. From here we replace them with for simplicity. Our goal is to prove that both terms are . For the second term, let and write

Hence,

We now proceed to proving that the first term is also small. Note that with probability at least , is larger than . Let this event be . Now note that for these instance in we can write

Furthermore, the upper bound on the pulls of UCB (see Theorem 8.1 of Lattimore and Szepesvári (2020)) for any arm with

Hence, we can write

Taking expectation with respect to (and hence ) implies that

Now, note that . Hence, Lemma 11.3 implies that

Replacing and implies the result. \Halmos

9 Proofs of Section 4

9.1 Proof of Lemma 4.1: A General Upper Bound for Greedy and SS-Greedy

Before proceeding with the proof, we need some notations. Note that we have

where is the suboptimality gap of arm . Define . In other words, is the regret of greedy when arms are compared to . Note that this implies that for any realization we have

Note that is the expectation of . Similarly, we can define the expectation of as which implies that

Our goal is to prove that satisfies the inequality given in the statement of Lemma 4.1 and hence the result. Note that the replacement of with a constant will be helpful in proving the second part of this lemma.

Fix the realization and partition the interval into sub-intervals of size . In particular, let be as and , for , where . For any , let denote the set of arms with means belonging to . Suppose that for each arm , a sequence of i.i.d. samples from is generated. Then, using definition of function in Eq. (2), for any arm we have

where is the empirical average of rewards of arm at time . Now, consider all arms that belong to . As the above events are independent, this implies that for the (bad) event we have

The above bounds the probability that , our bad event happens. Now note that if the (good) event happens, meaning that there exists an arm in such that its empirical average never drops below we can bound the regret as follows. First note that

Our goal is to bound for any arm that belongs to . Indeed, a standard argument based on subgaussianity of arm implies that

where we used the fact that a suboptimal arm (with mean less than ) only would be pulled for the time if its estimate after samples is larger than and that (centered version of) is -subgaussian. Now note that for any discrete random variable that only takes positive values, we have . Hence,

Now note that for any we have where . Hence, we have

which implies that

where we used the inequality which is true as . Note that the above is valid for any arm that belongs to . Furthermore, the expected number of pulls of arm cannot exceed . Hence,

As a result,

The last step is to take expectation with respect to the prior. Note that for the first term we can also be rewrite it as . Hence, taking expectation with respect to implies

as desired. The proof of second part follows from the fact that and that . \Halmos

9.2 Proofs for Bernoulli Rewards

9.2.1 Proof of Lemma 4.3.

Here we provide a more general version of Lemma 4.3 and prove it.

Lemma 9.1

Suppose is the Bernoulli distribution with mean and that exists such that . Then, for any we have

Furthermore, if the above quantity is at least .

First note that the above result implies Lemma 4.3 as condition ensures the existence of satisfying . Now we prove the above result.

Proof 9.2

Proof of Lemma 9.1 The proof uses Lundberg’s inequality. Note that with probability we have . In this case, the ruin will not occur during the first rounds and as we can write:

where . The last term above falls into the framework defined by Proposition 4.2 for the sequence and . It is not very difficult to see that the other conditions are satisfied. Indeed, as and that is subgaussian, the moment generating function is defined for all values of . Furthermore, . Finally, we can assume that , which basically means that . Note that if we assume the contrary, then , which means that the probability that crosses is actually zero, making the claim obvious. Hence, due to continuity of there exists such that . Finally, note that on the set that (meaning that crossing never happens), using the fact that and that all moments of exist and are bounded, Strong Law of Large Numbers implies that almost surely. This shows that the conditions of Proposition 4.2 are satisfied. Hence,

where is the Lundberg coefficient of the distribution . Lemma 9.3 which is stated below provides a lower bound on . In particular, it shows that

Substituting this and noting that implies the first part.

For the second part, note that we have

Now note as we can write:

Hence, as which implies that

as desired.

Lemma 9.3

Let be distributed according to , with . Then, the following bound on , the Lundberg coefficient of distribution holds:

Proof 9.4

Proof. Note that is the non-zero solution of equation . Therefore, satisfies

Let . Then, solves , which implies that

Note that as , it implies that (this could also be derived from ). As a result

On the other hand, the AM-GM inequality implies that . Hence,

This concludes the proof. \Halmos

9.2.2 Proof of Theorem 4.4.

9.3 Proofs for Subgaussian Rewards

Proof 9.5

Proof of Lemma 4.5 The proof of this Lemma uses Lundberg’s inequality. Let and define . Then, we are interested in bounding the probability

We claim that the latter is upper bounded by . To prove this, first we claim that the conditions of Lundberg’s inequality stated in Proposition 4.2 are satisfied for . Denote and note that as is -subgaussian, exists for all values of . Further, without any loss in generality, we can assume , since otherwise is satisfied. Hence, as , we have that goes to . Furthermore, and . Therefore, we conclude that there exists a such that . Note that has finite moments and therefore the Strong Law of Large Numbers (SLLN) implies that diverges almost surely to . Therefore, looking at , diverges almost surely to on the set . Hence, the conditions of Lundberg’s inequality are satisfied and therefore

Now we claim that which concludes the proof. Note that and is -subgaussian. Hence,

hence . For finishing the proof, note that and that for any we have . \Halmos

Proof 9.6

Proof of Theorem 4.6 Note that the result of Lemma 4.5 holds for all -subgaussian distributions. Therefore, we can apply Lemma 4.1 for the choice . Note that for we have and as a result . Therefore, combining this with Lemma 11.3 and inequality implies that

Picking finishes the proof. The second part follows immediately. \Halmos

9.4 Proofs for Uniformly Upward-Looking Rewards

Similar to previous cases, we first prove the result stated in Lemma 4.8, providing a lower bound on for uniformly upward-looking rewards.

9.4.1 Proof of Lemma 4.8

Recall that and we are interested in bounding the probability that falls below . In Definition 4.7, pick and define and note that

Note that, without any loss in generality, we can assume that , since otherwise the above probability is which is of course less than . Note that is upward-looking, it implies that one of the following holds:

-

•

for .

-

•

.

We consider each of these cases separately.

Case 1. In this case, the random walk hits before going below with probability at least . Hence, denoting , letting , by conditioning on value we can write

where in the above we used the fact that only depends on and that the distribution of is independent of . For the last argument we want to use Lundberg’s inequality for the summation . First note that, . Therefore, by SLLN (note that has finite moments, as its centered version is sub-gaussian) almost surely. Hence, for using Lundberg’s inequality stated in Proposition 4.2, we only need to show the existence of such that . For proving this, let be the moment generating function of which exists for all values of (due to sub-gaussianity of ). Note that and . Note that as and as is defined for all values of , there exists such that . In other words, given the condition , goes to . Hence, due to the continuity of , there exists such that . Hence, we can apply Lundberg’s inequality which states that:

Now we claim that . This is true according to being -subgaussian and that

which proves our claim. Combining all these results and using we have

where we used the inequality for which is true for any (or equivalently, ).Thus, using inequality for we have

as desired.

Case 2. Proof of this part is similar and relies again on Lundberg’s inequality. Here, we are going to condition on the value of which is independent of for . Our goal is to relate the desired probability to . Hence,

where is the ultimate ruin probability for the random walk . Now we want to apply Proposition 4.2 to provide an upper bound on . Similar to the previous case, we can show that the conditions of Lundberg’s inequality holds and hence Proposition 4.2 implies that where is the Lundberg coefficient of distribution that satisfies . Similar to the previous case we can show that and therefore, holds for all . Hence,

Now we can use the inequality which is true for . Replacing , implies that for we have

Therefore,

Hence,

Our goal is to show that if , then

| (9) |

For proving this note that for we have . Hence, according to -subgaussianity of we have

We claim that the above probability is less than . In fact, a simple numerical calculation shows that for all we have

Hence, this implies that

The final inequality we need to show is that which is obvious as , meaning

as . Putting all these results together we have proved our claim in Eq. (9). Hence, using inequality and that we have

As , and that for all , the conclusion follows. \Halmos

9.4.2 Proof of Theorem 4.9

Note that the result of Lemma 4.8 holds for all upward-looking distributions. Note that as is uniformly upward-looking, this result holds if . Further, if , the distribution is upward-looking for as well. Suppose that . Then, we can apply Lemma 4.1 for the choice according to the inequality , for any . Therefore, combining this with Lemma 11.3 and inequality implies that

Picking finishes the proof. Note that the condition on also implies that , as desired. The second part follows from the second part of Lemma 4.1 together with

10 Additional Simulations

In this section, we provide a wide range of simulations to validate our claims in the paper. We first start by the stochastic case (which is the main focus of the paper) and then provide some additional simulations with the contextual case as well.

10.1 Stochastic reward

Setting.

We repeat the analysis described in the introduction and Figure 1 for the wide range of beta priors and for both Gaussian and Bernoulli rewards. We fix in all our simulations and use two different values for . For each setting, we generate instances, where in each instance the means . Denote our general prior to be (note that uniform corresponds to ). The subsampling rates chosen for various algorithms are based on our theory and Table 1. For SS-TS, we use a similar rate as of SS-UCB. Finally, TS and SS-TS use the correct prior information (i.e., ) for the Bernoulli setting. For the Gaussian case, TS and SS-TS suppose that the prior distribution of all arms are . In other words, for Gaussian rewards, TS uses a mismatched (but narrow) prior for all arms. The following algorithms are included in our simulations:

-

•

UCB: Asymptotically optimal UCB (Algorithm 1).

-

•

SS-UCB: Subsampled UCB algorithm in Algorithm 2, with if and if .

-

•

Greedy: Greedy (Algorithm 3).

- •

-

•

UCB-F algorithm Wang et al. (2009) with the choice of confidence set . Note that UCB-F also subsamples if and if arms.

- •

-

•

SS-TS: Subsampled TS with if and if .

Priors.

For each of Bernoulli and Gaussian case, we consider priors with and , leading to different choices of priors.

Results.

The following two tables summarize the results of these simulations. In fact, Table 2 contains the result for Gaussian rewards and Table 3 contains the result for Bernoulli rewards. For each simulation, we normalize the mean per-instance regret (an estimate of Bayesian regret) of all algorithms by that of SS-Greedy. In other words, each entry gives an estimate of .

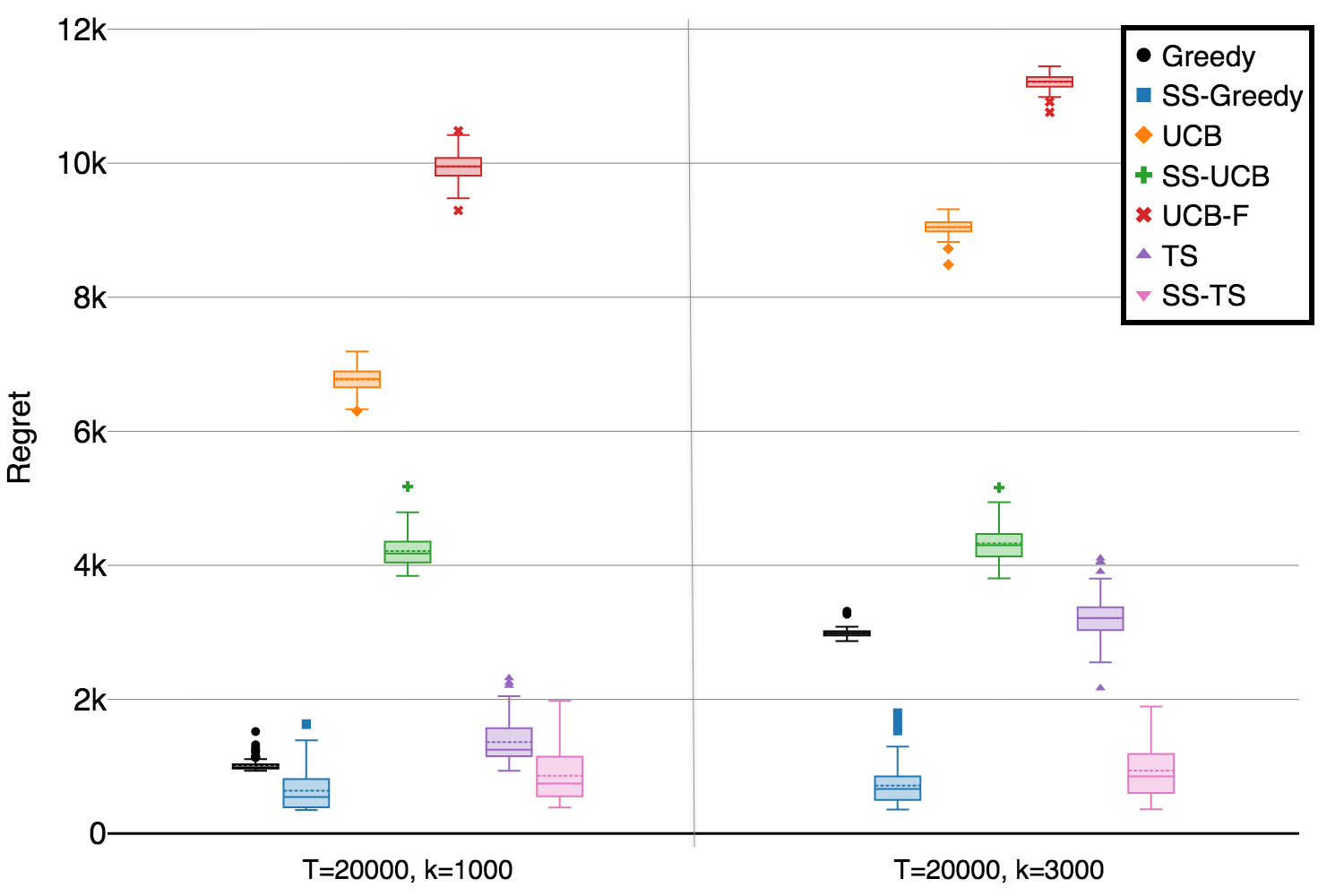

We also generate figures (Figures 3-8), similar to Figure 1, where we plot the distribution of per-instance regret of algorithms discussed above. As can be observed from Table 1, only the choice of changes the rates of various algorithms. For this reason, we only generate the plots for when is in for Bernoulli and Gaussian rewards ( in total).

As can be observed from Tables 2 and 3, SS-Greedy is the best performer in almost all the cases. Two other competitive algorithms are Greedy and SS-TS. It is clear from this table that subsampling leads to a great improvement (compare UCB with SS-UCB, Greedy with SS-Greedy, and TS with SS-TS) uniformly across all algorithms. For SS-TS, the performance in the Bernoulli case is much better. This is due to using correct information about prior and reward distributions. These two tables show that the superior performance of SS-Greedy is robust to the choice of prior and reward distributions.

| Setting | UCB | SS-UCB | Greedy | SS-Greedy | UCB-F | TS | SS-TS |

|---|---|---|---|---|---|---|---|

| Setting | UCB | SS-UCB | Greedy | SS-Greedy | UCB-F | TS | SS-TS |

|---|---|---|---|---|---|---|---|

10.2 Contextual reward

Setting.

We repeat the analysis described in §5, where instead of real data, we work with synthetically generated data. We consider the contextual rewards given by , where is the (shared) context observed at time and is the parameter of arm . We fix and and consider two settings: and . We suppose that and draw all contexts according to . Note that the normalization with implies that . Also, the noise terms , where . We again compare, OFUL, Greedy, and TS, and their subsampled versions. We generate instances of the problem described above and compare the per-instance regret of these algorithms.

Results.

The results are depicted in Figure 9. As can be observed: (1) SS-Greedy is the best algorithm in both cases, and (2) subsampling improves the performance of all algorithms. These results are consistent with our findings throughout the paper.

11 Useful Lemmas

Lemma 11.1 (Gautschi’s Inequality)

Let be a positive real number and let . Then,

Lemma 11.2 (Rearrangement Inequality)

Let and be two sequence of real numbers. Then for any permutation the following holds:

Lemma 11.3

Let be given and let be -regular (See Definition 2.1).Then, the following holds:

In above, is a constant that only depends on .

Proof 11.4

Proof of Lemma 11.3. Divide the interval into subintervals of size . In particular, let and suppose intervals are defined according to , and for . Let , then the following holds:

Now we can write

Let and note that the sequence is decreasing in . Hence, applying Rearrangement Inequality (Lemma 11.2) to sequences and , together with inequalities above on probability terms implies

| (10) |

Note that for the right hand-side of above inequality turns into

For , we can write using the mean-value theorem on the function . Hence, by using which holds for any , the right hand-side of Eq. 10 is at most

where we used the fact that is bounded above by . Hence, letting , implies that our quantity of interest is bounded from above by .

For , we can still use the mean-value theorem for the function (here ), together with which is true for . Hence, the bound on the right hand-side of Eq. 10 turns into

where we used the fact that when , the summation is bounded above by a constant . Hence, letting implies half of the result for .

The only remaining part is to show that if we can show a similar bound for where is replaced with . In this case, the idea is to use the second term for terms that are closer to zero. In particular, we can write

where is chosen as the largest integer for which . Note that the first sum is upper bounded by

For the second term, we can use a similar analysis to the one we used above. The only difference here is that the summation of terms is from to (or ) and hence is upper bounded by .

Now using the fact that implies the the quantity of interest is at most

Letting finishes the proof.\Halmos

Lemma 11.5

Suppose that and which satisfies the conditions given in Assumption 2. Let denote the order statistics of and define . Then, we have

-

1.

has the following density function

where is the cumulative distribution function of , defined as

-

2.

If for all , then any ,

Proof 11.6

Proof of Lemma 11.5. The proof is as follows.

-

1.

The first part follows from basic probability calculations. In fact, conditioned on , the density of around can be computed according to the fact that we need of s to be less than and of them to belong to . Note that here is equal to . Considering all the different permutations that lead to the same realization of the order statistics and integrating from to (possible values for ) yields the desired formula.

-

2.

Note that for any we have

Now using this inequality we can write

where we used the fact that the last integral is equivalent to for which is true for .

12 Proofs of §6: -Regular Priors and Sequential Greedy

We prove results presented in §6 here. This section is divided into two parts. In the first part, we prove results for general -regular priors and in the second part, we prove results for the sequential greedy (Seq-Greedy) algorithm.

12.1 General -regular priors

Here, we prove results presented in Table 1. This includes generalizing the result of Theorem 3.1 on lower bounds, Theorems 3.2 and 3.3 for UCB and SS-UCB, and finally Theorems 4.4, 4.9, and 4.6 for Greedy and SS-Greedy. For each situation, we highlight the steps in the proofs that require significant changes and prove such modified results.

12.1.1 Lower Bounds

Note that the proof presented in §8.1 goes through without much change. Indeed, consider the large regime defined by , where only depends on and . Our goal is to prove that there exists a class of “bad orderings” that happen with a constant probability, for which the Bayesian is . Let and define the following class over orderings of arms:

-

(i)

,

-

(ii)

-

(iii)

.

Now one can follow the proof steps of Theorem 3.1 to prove the result. Indeed, it is not difficult to see that the upper bound on the probability of the events remain the same. For example, the first term happens with probability

Other events also hold with similar probabilities as in the proof Theorem 3.1 and one can follow the exact line of proof. Similarly, two things can happen: either the decision-maker only pulls from the first arms during the -period horizon or starts pulling some (or all) arms in the set . In the former case, the regret is at least

In the latter case, the regret is at least

as desired. Note that the values of and can be calculated from the above inequalities.

12.1.2 Upper Bounds

We divide the discussion of upper bounds into two parts. We first focus on the case of UCB and then consider SS-UCB. Note that for UCB, under the assumption that the density is bounded above by , the same proof goes through without any modification. However, an upper bound on the density is only possible when . In what follows we prove the bounds provided in Table 1 for small and large , when .

UCB with small .

We here provide a proof for under the assumption that for a constant . Our goal is to prove that an analogous form of Theorem 3.2 holds, which leads to regret. Recalling the proof of Theorem 3.2 we have

Now, we first need to derive a bound on when . In particular, we want to see how the result of Lemma 11.5 would change for under the assumption that . Suppose that integer exists such that . We claim that there exists a constant such that for any integer we have

Note that part 1 of Lemma 11.5 remains valid. However, for part 2, instead of we can write

This means that for we have . Replacing this in the upper bound and following same ideas as the proof of Lemma 11.5 implies

where is the gamma function defined by. Note that Gautschi’s Inequality (see Lemma 11.1) implies that if for an integer

Similarly, using the other direction in the Gautschi’s inequality one can show that

Therefore, for any index we have

Now moving back to the proof of Lemma 3.2, we can divide the arms into two sets, integer indices and . Hence,

As , the term is bounded from above by a constant. Hence, it only remains to bound the first term. For the first term we use the same technique as of proof of Theorem 3.2. In particular, we first want to establish an upper bound on the density. Note that for , using Lemma 11.5, the density of is upper bounded by

For , we can write

Having these upper bounds on the densities it is not difficult to see that the proof of Theorem 3.2 for indices goes through similarly and the contribution of each term is bounded above by . For the situation is a bit different, but we still can write

Putting all the terms together and factoring all constants together as we have

Note that for small , the term is dominant in above bound. However, once , the term is the dominant term.

UCB with large .

From the above regret bound it is clear that for large values of (specifically, ) the term is dominant which finishes the proof.

SS-UCB.

For SS-UCB, the results for small (in both cases and ) are under similar assumption as UCB, i.e., having a bounded density for and being bounded from above by , for . Hence, we only focus on proving that if the subsampling rate is chosen correctly, for large values of , is of order for and of order for . These results can be proved without putting an assumption on density, but rather under (more relaxed) -regular priors. The proof steps are similar to those of Theorem 3.3. We briefly explain which parts need to be changed below.

-

•

: In this case, we wish to prove that if then Bayesian regret of SS-UCB is upper bounded by . Similar to Theorem 3.3, we can upper bound as sum of and . Pick which implies again that

For the first term, we can follow the rest of the proof. In the last line, however, we need to use

and the result of Lemma 11.3 for a general . Note that the result follows from the result of Lemma 11.3 for general instead of . In particular, Lemma 11.3 shows that the difference between the upper bound on the term

for the cases and is only in , which translates to a factor . This finishes the proof.

-

•

: Proof is similar to the proof above (case ). Indeed, let and follow the steps provided in Theorem 3.3. Following these steps, we can see that and hence, . Our goal is to show that the other term, coming from is also . Note that again the last two lines of the proof of Theorem 3.3 need to be modified. Indeed, replacing and noting that shows that the term is . Finally, for the last term we can use Lemma 11.3. Here, note that as , this last term is upper bounded by

as desired.

12.1.3 Results for Greedy and SS-Greedy

Note that the proof of results for Greedy all follow from the generic bound presented in Lemma 4.1. Note that as discussed in §6, is lower bound for the exponent of in . In particular, Lemmas 4.3, 4.8, and 4.5 show that:

- •

- •

- •

Having these bounds on the first term and using inequality , the result of Lemma 4.1 can be written as:

| (11) |

where is a constant depending on the distribution and also . Furthermore, Lemma 4.1 also implies that for SS-Greedy the same upper bound holds, with being replaced with in Eq. 12.1.3. From here, the results can be proved by choosing the optimal value for . We explain these choices for and .

Case .

In this case, the best choice of is given by

Since , Lemma 11.3 implies that the last term is also upper bounded by . Therefore, the bound in Eq. 10 turns into

Now note that for small the first term is dominant, while for the large the second term is dominant. This proves the result presented in Table 1 for Greedy, for . For SS-Greedy, note that the same result applies, with being replaced with . Note that for , the optimal is given by , which proves the result for the SS-Greedy, when is large and .

Case .

In this case, the regret bound of Greedy has three regimes. Again pick according to

As , Lemma 11.3 implies that the last term in Eq. (12.1.3) is also upper bounded by . Therefore, the bound in Eq. (10) turns into

Now note that for small the first term is dominant and regret is while for the large , the second term is dominant. Note that between these two terms inside the minimum, for mid-range values for , the regret is , while for larger values of the term is smaller.

For SS-Greedy, note that as the regret in large is minimum of two terms, we need to carefully check at what the best regret is achieved. However, as , it is not difficult to see that the best regret is achieved when , or

which proves , as desired.

12.2 Sequential Greedy

Proof 12.1

Proof of Lemma 6.1 The proof is very similar to the proof of Lemma 4.1. In particular, the goal is to prove that, if is selected large enough (so that the probability of undesired events are much smaller than ), then with a very high probability the algorithm only tries the first and hence the term in the regret will be replaced with . To formally prove this, we show that on most problem instances only first arms are tried and in those cases we can replace in the bound of Lemma 4.1 with , and the contribution of problems where more than arms are pulled is at most times the probability of such events. While, the proof steps are very similar to that of Lemma 4.1, we provide a proof for completeness below.

Fix a realization and partition the interval into sub-intervals of size . In particular, let be as and , for , where . For any , let denote the set of arms with means belonging to . Suppose that for each arm , a sequence of i.i.d. samples from is generated. Furthermore, for each define the set , which includes the set of all arms among the first indices that belong to . Then, using definition of function in Eq. (2), for any arm we have

where is the empirical average of rewards of arm at time . Now, consider all arms that belong to . Define the bad event as meaning that the sample average of all arms in drops below at some time . Similarly, define the good event , as the complement of . We can write

| (12) |

The above bounds the probability that , our bad event happens. Now note that if the (good) event happens, meaning that there exists an arm in such that its empirical average never drops below we can bound the regret as follows. First note that in the case of good event, the algorithm only pulls the first arms and hence for all . Therefore,

Our goal is to bound for any arm that belongs to . Indeed, a standard argument based on subgaussianity of arm implies that

where we used the fact that a suboptimal arm (with mean less than ) only would be pulled for the time if its estimate after samples is larger than and that (centered version of) is -subgaussian. Now note that for any discrete random variable that only takes positive values, we have . Hence,

Now note that for any we have where . Hence, we have

which implies that

where we used the inequality which is true as . Note that the above is valid for any arm that belongs to . Furthermore, the expected number of pulls of arm cannot exceed . Hence,

As a result,

We can replace from Eq. (12) and take expectation with respect to the prior. Note that the first term we can also be rewritten as . Hence, taking an expectation with respect to implies

as desired. \Halmos

Proof 12.2

Proof of Theorem 6.2 We prove the result only for the Bernoulli case, the other cases use similar arguments. We want to show that when , Bayesian regret of Seq-Greedy is at most and if it is at most . Consider the first case and note that in this case . We claim that for this by selecting in Lemma 6.1, we have

and the conclusion follows similar to the proof of Theorem 4.4. Indeed, one can show that if , then the above rate becomes . Now consider the other case that , meaning that . In this case, by selecting , we have

which for the choice translates to the upper bound on , according to Theorem 4.4. The proof for -subgaussian and uniformly upward-looking rewards is similar. \Halmos