Vector Space and Matrix Methods in

Signal and System Theory

Chapter 1 Introduction

The tools, ideas, and insights from linear algebra, abstract algebra, and functional analysis can be extremely useful to signal processing and system theory in various areas of engineering, science, and social science including approximation, optimization, parameter identification, big data, etc. Indeed, many important ideas can be developed from the simple operator equation

| (1.1) |

by considering it in a variety of ways. If and are vectors from the same or, perhaps, different vector spaces and is an operator, there are three interesting questions that can be asked which provide a setting for a broad study.

-

1.

Given and , find . The analysis or operator problem or transform.

-

2.

Given and , find . The inverse or control problem or deconvolution or design or solving simultanious equations.

-

3.

Given and , find . The synthesis or design problem or parameter identification.

Much can be learned by studying each of these problems in some detail. We will generally look at the finite dimensional problem where (1.1) can more easily be studied as a finite matrix multiplication [1, 2, 3, 4]

| (1.2) |

but will also try to indicate what the infinite dimensional case might be [5, 6, 7, 8].

An application to signal theory is in [9], to optimization [10], and multiscale system theory [11]. The inverse problem (number 2 above) is the basis for a large study of pseudoinverses, approximation, optimization, filter design, and many applications. When used with the norm [12, 13] powerful results can be optained analytically but used with other norms such as , , (a pseudonorm), an even larger set of problems can be posed and solved [14, 15].

A development of vector space ideas for the purpose of presenting wavelet representations is given in [16, 17]. An interesting idea of unconditional bases is given by Donoho [18].

Linear regression analysis can be posed in the form of (1.1) and (3.6) where the rows of are the vectors of input data from experiments, entries of are the weights for the components of the inputs, and the values of are the outputs [14]. This can be used in machine learning problems [19, 20]. A problem similar to the design or synthesis problem is that of parameter identification where a model of some system is posed with unknown parameters. Then experiments with known inputs and measured outputs are run to identify these parameters. Linear regression is also an example of this [14, 19].

Dynamic systems are often modelled by ordinary differential equation where is set to be the time derivative of to give what are called the linear state equations:

| (1.3) |

or for difference equations and discrete-time or digital signals,

| (1.4) |

which are used in digital signal processing and the analysis of certain algorithms. State equations are useful in feedback control as well as in simulation of many dynamical systems and the eigenvalues and other properties of the square matix are important indicators of the performance [21, 22].

The ideas of similarity transformations, diagonalization, the eigenvalue problem, Jordon normal form, singular value decomposition, etc. from linear algebra [23, 1, 2, 24] are applicable to this problem.

This booklet is intended to point out relationships, interpretations, and tools in linear algebra, matrix theory, and vector spaces that scientists and engineers might find useful. It is not a stand-alone linear algebra book. Details, definitions, and formal proofs can be found in the references. A very helpful source is Wikipedia.

There is a variety of software systems to both pose and solve linear algebra problems. A particularly powerful one is Matlab [3] which is, in some ways, the gold standard since it started years ago as a purely numerical matrix package. But there are others such as Octave, SciLab, LabVIEW, Mathematica, Maple, R, Python, etc.

Chapter 2 A Matrix Times a Vector

In this chapter we consider the first problem posed in the introduction

| (2.1) |

where the matrix and vector are given and we want to interpret and give structure to the calculation of the vector . Equation (2.1) has a variety of special cases. The matrix may be square or may be rectangular. It may have full column or row rank or it may not. It may be symmetric or orthogonal or non-singular or many other characteristics which would be interesting properties as an operator. If we view the vectors as signals and the matrix as an operator or processor, there are two interesting interpretations.

-

•

The operation (2.1) is a change of basis or coordinates for a fixed signal. The signal stays the same, the basis (or frame) changes.

-

•

The operation (2.1) alters the characteristics of the signal (processes it) but within a fixed basis system. The basis stays the same, the signal changes.

An example of the first would be the discrete Fourier transform (DFT) where one calculates frequency components of a signal which are coordinates in a frequency space for a given signal. The definition of the DFT from [25] can be written as a matrix-vector operation by which, for and , is

| (2.2) |

An example of the second might be convolution where you are processing or filtering a signal and staying in the same space or coordinate system.

| (2.3) |

A particularly powerful sequence of operations is to first change the basis for a signal, then process the signal in this new basis, and finally return to the original basis. For example, the discrete Fourier transform (DFT) of a signal is taken followed by setting some of the Fourier coefficients to zero followed by taking the inverse DFT.

Another application of (2.1) is made in linear regression where the input signals are rows of and the unknown weights of the hypothesis are in and the outputs are the elements of .

2.1 Change of Basis

Consider the two views:

-

1.

The operation given in (2.1) can be viewed as being a set of weights so that is a weighted sum of the columns of . In other words, will lie in the space spanned by the columns of at a location determined by . This view is a composition of a signal from a set of weights as in (2.6) and (2.8) below. If the vector is the column of , it is illustrated by

(2.4) -

2.

An alternative view has being a signal vector and with being a vector whose entries are inner products of and the rows of A. In other words, the elements of are the projection coefficients of onto the coordinates given by the rows of A. The multiplication of a signal by this operator decomposes the signal and gives the coefficients of the decomposition. If is the row of we have:

(2.5) Regression can be posed from this view with the input signal being the rows of A.

These two views of the operation as a decomposition of a signal or the recomposition of the signal to or from a different basis system are extremely valuable in signal analysis. The ideas from linear algebra of subspaces, inner product, span, orthogonality, rank, etc. are all important here. The dimensions of the domain and range of the operators may or may not be the same. The matrices may or may not be square and may or may not be of full rank [5, 1].

2.1.1 A Basis and Dual Basis

A set of linearly independent vectors forms a basis for a vector space if every vector in the space can be uniquely written

| (2.6) |

and the dual basis is defined as a set vectors in that space allows a simple inner product (denoted by parenthesis: ) to calculate the expansion coefficients as

| (2.7) |

A basis expansion has enough vectors but none extra. It is efficient in that no fewer expansion vectors will represent all the vectors in the space but is fragil in that losing one coefficient or one basis vector destroys the ability to exactly represent the signal by (2.6). The expansion (2.6) can be written as a matrix operation

| (2.8) |

where the columns of F are the basis vectors and the vector a has the expansion coefficients as entries. Equation (2.7) can also be written as a matrix operation

| (2.9) |

which has the dual basis vectors as rows of . From (2.8) and (2.9), we have

| (2.10) |

Since this is true for all ,

| (2.11) |

or

| (2.12) |

which states the dual basis vectors are the rows of the inverse of the matrix whose columns are the basis vectors (and vice versa). When the vector set is a basis, F is necessarily square and from (2.8) and (2.9), one can show

| (2.13) |

Because this system requires two basis sets, the expansion basis and the dual basis, it is called biorthogonal.

2.1.2 Orthogonal Basis

2.1.3 Parseval’s Theorem

Because many signals are digital representations of voltage, current, force, velocity, pressure, flow, etc., the inner product of the signal with itself (the norm squared) is a measure of the signal energy .

| (2.15) |

Parseval’s theorem states that if the basis system is orthogonal, then the norm squared (or “energy”) is invarient across a change in basis. If a change of basis is made with

| (2.16) |

then

| (2.17) |

for some constant which can be made unity by normalization if desired.

For the discrete Fourier transform (DFT) of which is

| (2.18) |

the energy calculated in the time domain: is equal to the norm squared of the frequency coefficients: , within a multiplicative constant of . This is because the basis functions of the Fourier transform are orthogonal: “the sum of the squares is the square of the sum” which means means the energy calculated in the time domain is the same as that calculated in the frequency domain. The energy of the signal (the square of the sum) is the sum of the energies at each frequency (the sum of the squares). Because of the orthogonal basis, the cross terms are zero. Although one seldom directly uses Parseval’s theorem, its truth is what make sense in talking about frequency domain filtering of a time domain signal. A more general form is known as the Plancherel theorem [28].

If a transformation is made on the signal with a non-orthogonal basis system, then Parseval’s theorem does not hold and the concept of energy does not move back and forth between domains. We can get around some of these restrictions by using frames rather than bases for expansions.

2.1.4 Frames and Tight Frames

In order to look at a more general expansion system than a basis and to generalize the ideas of orthogonality and of energy being calculated in the original expansion system or the transformed system, the concept of frame is defined. A frame decomposition or representation is generally more robust and flexible than a basis decomposition or representation but it requires more computation and memory [29, 30, 28]. Sometimes a frame is called a redundant basis or representing an underdetermined or underspecified set of equations.

If a set of vectors, , span a vector space (or subspace) but are not necessarily independent nor orthogonal, bounds on the energy in the transform can still be defined. A set of vectors that span a vector space is called a frame if two constants, and exist such that

| (2.19) |

and the two constants are called the frame bounds for the system. This can be written

| (2.20) |

where

| (2.21) |

If the are linearly independent but not orthogonal, then the frame is a non-orthogonal basis. If the are not independent the frame is called redundant since there are more than the minimum number of expansion vectors that a basis would have. If the frame bounds are equal, , the system is called a tight frame and it has many of features of an orthogonal basis. If the bounds are equal to each other and to one, , then the frame is a basis and is tight. It is, therefore, an orthogonal basis.

So a frame is a generalization of a basis and a tight frame is a generalization of an orthogonal basis. If , , the frame is tight and we have a scaled Parseval’s theorem:

| (2.22) |

If , then the number of expansion vectors are more than needed for a basis and is a measure of the redundancy of the system (for normalized frame vectors). For example, if there are three frame vectors in a two dimensional vector space, .

A finite dimensional matrix version of the redundant case would have in (2.8) with more columns than rows but with full row rank. For example

| (2.23) |

has three frame vectors as the columns of but in a two dimensional space.

The prototypical example is called the “Mercedes-Benz” tight frame where three frame vectors that are apart are used in a two-dimensional plane and look like the Mercedes car hood ornament. These three frame vectors must be as far apart from each other as possible to be tight, hence the separation. But, they can be rotated any amount and remain tight [30, 31] and, therefore, are not unique.

| (2.24) |

In the next section, we will use the pseudo-inverse of to find the optimal for a given .

So the frame bounds and in (2.19) are an indication of the redundancy of the expansion system and to how close they are to being orthogonal or tight. Indeed, (2.19) is a sort of approximate Parseval’s theorem [6, 16, 32, 33, 28, 30, 34, 35].

The dual frame vectors are also not unique but a set can be found such that (2.9) and, therefore, (2.10) hold (but (2.13) does not). A set of dual frame vectors could be found by adding a set of arbitrary but independent rows to F until it is square, inverting it, then taking the first columns to form whose rows will be a set of dual frame vectors. This method of construction shows the non-uniqueness of the dual frame vectors. This non-uniqueness is often resolved by optimizing some other parameter of the system [16].

If the matrix operations are implementing a frame decomposition and the rows of F are orthonormal, then and the vector set is a tight frame [6, 16]. If the frame vectors are normalized to , the decomposition in (2.6) becomes

| (2.25) |

where the constant is a measure of the redundancy of the expansion which has more expansion vectors than necessary [16].

2.1.5 Sinc Expansion as a Tight Frame

The Shannon sampling theorem [36, 37] can be viewied as an infinite dimensional signal expansion where the sinc functions are an orthogonal basis. The sampling theorem with critical sampling, i.e. at the Nyquist rate, is the expansion:

| (2.27) |

where the expansion coefficients are the samples and where the sinc functions are easily shown to be orthogonal.

Over sampling is an example of an infinite-dimensional tight frame [38, 17]. If a function is over-sampled but the sinc functions remains consistent with the upper spectral limit , using as the amount of over-sampling, the sampling theorem becomes:

| (2.28) |

and we have

| (2.29) |

where the sinc functions are no longer orthogonal. In fact, they are no longer a basis as they are not independent. They are, however, a tight frame and, therefore, have some of the characteristics of an orthogonal basis but with a “redundancy” factor as a multiplier in the formula [17] and a generalized Parseval’s theorem. Here, moving from a basis to a frame (actually from an orthogonal basis to a tight frame) is almost invisible.

2.1.6 Frequency Response of an FIR Digital Filter

The discrete-time Fourier transform (DTFT) of the impulse response of an FIR digital filter is its frequency response. The discrete Fourier transform (DFT) of gives samples of the frequency response [36]. This is a powerful analysis tool in digital signal processing (DSP) and suggests that an inverse (or pseudoinverse) method could be useful for design [36].

2.1.7 Conclusions

Frames tend to be more robust than bases in tolerating errors and missing terms. They allow flexibility is designing wavelet systems [16] where frame expansions are often chosen.

In an infinite dimensional vector space, if basis vectors are chosen such that all expansions converge very rapidly, the basis is called an unconditional basis and is near optimal for a wide class of signal representation and processing problems. This is discussed by Donoho in [18].

Still another view of a matrix operator being a change of basis can be developed using the eigenvectors of an operator as the basis vectors. Then a signal can decomposed into its eigenvector components which are then simply multiplied by the scalar eigenvalues to accomplish the same task as a general matrix multiplication. This is an interesting idea but will not be developed here.

2.2 Change of Signal

If both and in (2.1) are considered to be signals in the same coordinate or basis system, the matrix operator is generally square. It may or may not be of full rank and it may or may not have a variety of other properties, but both and are viewed in the same coordinate system and therefore are the same size.

One of the most ubiquitous of these is convolution where the input to a linear, shift invariant system with impulse response is calculated by (2.1) if is the convolution matrix and is the input [36].

| (2.30) |

It can also be calculated if is the arrangement of the input and is the the impulse response.

| (2.31) |

If the signal is periodic or if the DFT is being used, then what is called a circulate is used to represent cyclic convolution. An example for is the Toeplitz system

| (2.32) |

One method of understanding and generating matrices of this sort is to construct them as a product of first a decomposition operator, then a modification operator in the new basis system, followed by a recomposition operator. For example, one could first multiply a signal by the DFT operator which will change it into the frequency domain. One (or more) of the frequency coefficients could be removed (set to zero) and the remainder multiplied by the inverse DFT operator to give a signal back in the time domain but changed by having a frequency component removed. That is a form of signal filtering and one can talk about removing the energy of a signal at a certain frequency (or many) because of Parseval’s theorem.

It would be instructive for the reader to make sense out of the cryptic statement “the DFT diagonalizes the cyclic convolution matrix” to add to the ideas in this note.

2.3 Factoring the Matrix

For insight, algorithm development, and/or computational efficiency, it is sometime worthwhile to factor into a product of two or more matrices. For example, the matrix [25] illustrated in (2.2) can be factored into a product of fairly sparce matrices. If fact, the fast Fourier transform (FFT) can be derived by factoring the DFT matrix into factors (if ), each requiring order multiplies. This is done in [25].

Using eigenvalue theory [1], a full rank square matrix can be factored into a product

| (2.33) |

where is a matrix with columns of the eigenvectors of and is a diagonal matrix with the eigenvalues along the diagonal. The inverse is a method to “diagonalize” a matrix

| (2.34) |

If a matrix has “repeated eigenvalues”, in other words, two or more of the eigenvalues have the same value but less than indepentant eigenvectors, it is not possible to diagonalize the matrix but an “almost” diagonal form called the Jordan normal form can be acheived. Those details can be found in most books on matrix theory [23].

A more general decompostion is the singular value decomposition (SVD) which is similar to the eigenvalue problem but allows rectangular matrices. It is particularly valuable for expressing the pseudoinverse in a simple form and in making numerical calculations [4].

2.4 State Equations

If our matrix multiplication equation is a vector differential equation (DE) of the form

| (2.35) |

or for difference equations and discrete-time signals or digital signals,

| (2.36) |

an inverse or even pseudoinverse will not solve for . A different approach must be taken [39] and different properties and tools from linear algebra will be used. The solution of this first order vector DE is a coupled set of solutions of first order DEs. If a change of basis is made so that is diagonal (or Jordan form), equation (2.35) becomes a set on uncoupled (or almost uncoupled in the Jordan form case) first order DEs and we know the solution of a first order DE is an exponential. This requires consideration of the eigenvalue problem, diagonalization, and solution of scalar first order DEs [39].

Chapter 3 Solutions of Simultaneous Linear Equations

The second problem posed in the introduction is basically the solution of simultaneous linear equations [12, 14, 15] which is fundamental to linear algebra [24, 1, 3] and very important in diverse areas of applications in mathematics, numerical analysis, physical and social sciences, engineering, and business. Since a system of linear equations may be over or under determined in a variety of ways, or may be consistent but ill conditioned, a comprehensive theory turns out to be more complicated than it first appears. Indeed, there is a considerable literature on the subject of generalized inverses or pseudo-inverses. The careful statement and formulation of the general problem seems to have started with Moore [40] and Penrose [41, 42] and developed by many others. Because the generalized solution of simultaneous equations is often defined in terms of minimization of an equation error, the techniques are useful in a wide variety of approximation and optimization problems [13, 10] as well as signal processing.

The ideas are presented here in terms of finite dimensions using matrices. Many of the ideas extend to infinite dimensions using Banach and Hilbert spaces [43, 7, 6] in functional analysis.

3.1 The Problem

Given an by real matrix and an by vector , find the by vector when

| (3.1) |

or, using matrix notation,

| (3.2) |

If does not lie in the range space of (the space spanned by the columns of ), there is no exact solution to (3.2), therefore, an approximation problem can be posed by minimizing an equation error defined by

| (3.3) |

A generalized solution (or an optimal approximate solution) to (3.2) is usually considered to be an that minimizes some norm of . If that problem does not have a unique solution, further conditions, such as also minimizing the norm of , are imposed. The or root-mean-squared error or Euclidean norm is and minimization sometimes has an analytical solution. Minimization of other norms such as (Chebyshev) or require iterative solutions. The general norm is defined as where

| (3.4) |

for and a “pseudonorm” (not convex) for . These can sometimes be evaluated using IRLS (iterative reweighted least squares) algorithms [44, 45, 46, 47, 48].

If there is a non-zero solution of the homogeneous equation

| (3.5) |

then (3.2) has infinitely many generalized solutions in the sense that any particular solution of (3.2) plus an arbitrary scalar times any non-zero solution of (3.5) will have the same error in (3.3) and, therefore, is also a generalized solution. The number of families of solutions is the dimension of the null space of .

This is analogous to the classical solution of linear, constant coefficient differential equations where the total solution consists of a particular solution plus arbitrary constants times the solutions to the homogeneous equation. The constants are determined from the initial (or other) conditions of the solution to the differential equation.

3.2 Ten Cases to Consider

Examination of the basic problem shows there are ten cases [12] listed in Figure 1 to be considered. These depend on the shape of the by real matrix , the rank of , and whether is in the span of the columns of .

-

•

1a. : One solution with no error, .

-

•

1b. : : Many solutions with .

-

•

1c. : : Many solutions with the same minimum error.

-

•

2a. : : One solution .

-

•

2b. : : One solution with minimum error.

-

•

2c. : : Many solutions with .

-

•

2d. : : Many solutions with the same minimum error.

-

•

3a. : Many solutions with .

-

•

3b. : : Many solutions with

-

•

3c. : : Many solutions with the same minimum error.

Figure 1. Ten Cases for the Pseudoinverse.

Here we have:

-

•

case 1 has the same number of equations as unknowns (A is square, ),

-

•

case 2 has more equations than unknowns, therefore, is over specified (A is taller than wide, ),

-

•

case 3 has fewer equations than unknowns, therefore, is underspecified (A is wider than tall ).

This is a setting for frames and sparse representations.

In case 1a and 3a, is necessarily in the span of . In addition to these classifications, the possible orthogonality of the columns or rows of the matrices gives special characteristics.

3.3 Examples

Case 1: Here we see a 3 x 3 square matrix which is an example of case 1 in Figure 1 and 2.

| (3.6) |

If the matrix has rank 3, then the vector will necessarily be in the space spanned by the columns of which puts it in case 1a. This can be solved for by inverting or using some more robust method. If the matrix has rank 1 or 2, the may or may not lie in the spanned subspace, so the classification will be 1b or 1c and minimization of yields a unique solution.

Case 2: If is 4 x 3, then we have more equations than unknowns or the overspecified or overdetermined case.

| (3.7) |

If this matrix has the maximum rank of 3, then we have case 2a or 2b depending on whether is in the span of or not. In either case, a unique solution exists which can be found by (3.12) or (3.18). For case 2a, we have a single exact solution with no equation error, just as case 1a. For case 2b, we have a single optimal approximate solution with the least possible equation error. If the matrix has rank 1 or 2, the classification will be 2c or 2d and minimization of yelds a unique solution.

Case 3: If is 3 x 4, then we have more unknowns than equations or the underspecified case.

| (3.8) |

If this matrix has the maximum rank of 3, then we have case 3a and must be in the span of . For this case, many exact solutions exist, all having zero equation error and a single one can be found with minimum solution norm using (3.14) or (3.19). If the matrix has rank 1 or 2, the classification will be 3b or 3c.

3.4 Solutions

There are several assumptions or side conditions that could be used in order to define a useful unique solution of (3.2). The side conditions used to define the Moore-Penrose pseudo-inverse are that the norm squared of the equation error be minimized and, if there is ambiguity (several solutions with the same minimum error), the norm squared of also be minimized. A useful alternative to minimizing the norm of is to require certain entries in to be zero (sparse) or fixed to some non-zero value (equality constraints).

In using sparsity in posing a signal processing problem (e.g. compressive sensing), an norm can be used (or even an “pseudo norm”) to obtain solutions with zero components if possible [49, 50].

In addition to using side conditions to achieve a unique solution, side conditions are sometimes part of the original problem. One interesting case requires that certain of the equations be satisfied with no error and the approximation be achieved with the remaining equations.

3.5 Moore-Penrose Pseudo-Inverse

If the norm is used, a unique generalized solution to (3.2) always exists such that the norm squared of the equation error and the norm squared of the solution are both minimized. This solution is denoted by

| (3.9) |

where is called the Moore-Penrose inverse [14] of (and is also called the generalized inverse [15] and the pseudoinverse [14])

Roger Penrose [42] showed that for all , there exists a unique satisfying the four conditions:

| (3.10) |

There is a large literature on this problem. Five useful books are [12, 14, 15, 51, 52]. The Moore-Penrose pseudo-inverse can be calculated in Matlab [53] by the pinv(A,tol) function which uses a singular value decomposition (SVD) to calculate it. There are a variety of other numerical methods given in the above references where each has some advantages and some disadvantages.

3.6 Properties

For cases 2a and 2b in Figure 1, the following by system of equations called the normal equations [14, 12] have a unique minimum squared equation error solution (minimum ). Here we have the over specified case with more equations than unknowns. A derivation is outlined in Section 3.8.1, equation (3.25) below.

| (3.11) |

The solution to this equation is often used in least squares approximation problems. For these two cases is non-singular and the by pseudo-inverse is simply,

| (3.12) |

A more general problem can be solved by minimizing the weighted equation error, where is a positive semi-definite diagonal matrix of the error weights. The solution to that problem [15] is

| (3.13) |

For the case 3a in Figure 1 with more unknowns than equations, is non-singular and has a unique minimum norm solution, . The by pseudoinverse is simply,

| (3.14) |

with the formula for the minimum weighted solution norm is

| (3.15) |

For these three cases, either (3.12) or (3.14) can be directly calculated, but not both. However, they are equal so you simply use the one with the non-singular matrix to be inverted. The equality can be shown from an equivalent definition [14] of the pseudo-inverse given in terms of a limit by

| (3.16) |

For the other 6 cases, SVD or other approaches must be used. Some properties [14, 51] are:

-

•

-

•

-

•

-

•

for else

-

•

-

•

It is informative to consider the range and null spaces [51] of and

-

•

-

•

-

•

-

•

3.7 The Cases with Analytical Soluctions

The four Penrose equations in (3.10) are remarkable in defining a unique pseudoinverse for any A with any shape, any rank, for any of the ten cases listed in Figure 1. However, only four cases of the ten have analytical solutions (actually, all do if you use SVD).

-

•

If is case 1a, (square and nonsingular), then

(3.17) -

•

If is case 2a or 2b, (over specified) then

(3.18) -

•

If is case 3a, (under specified) then

(3.19)

Figure 2. Four Cases with Analytical Solutions

Fortunately, most practical cases are one of these four but even then, it is generally faster and less error prone to use special techniques on the normal equations rather than directly calculating the inverse matrix. Note the matrices to be inverted above are all by ( is the rank) and nonsingular. In the other six cases from the ten in Figure 1, these would be singular, so alternate methods such as SVD must be used [12, 14, 15].

In addition to these four cases with “analytical” solutions, we can pose a more general problem by asking for an optimal approximation with a weighted norm [15] to emphasize or de-emphasize certain components or range of equations.

-

•

If is case 2a or 2b, (over specified) then the weighted error pseudoinverse is

(3.20) -

•

If is case 3a, (under specified) then the weighted norm pseudoinverse is

(3.21)

Figure 3. Three Cases with Analytical Solutions and Weights

These solutions to the weighted approxomation problem are useful in their own right but also serve as the foundation to the Iterative Reweighted Least Squares (IRLS) algorithm developed in the next chapter.

3.8 Geometric interpretation and Least Squares Approximation

A particularly useful application of the pseudo-inverse of a matrix is to various least squared error approximations [12, 13]. A geometric view of the derivation of the normal equations can be helpful. If does not lie in the range space of , an error vector is defined as the difference between and . A geometric picture of this vector makes it clear that for the length of to be minimum, it must be orthogonal to the space spanned by the columns of . This means that . If both sides of (3.2) are multiplied by , it is easy to see that the normal equations of (3.11) result in the error being orthogonal to the columns of and, therefore its being minimal length. If does lie in the range space of , the solution of the normal equations gives the exact solution of (3.2) with no error.

For cases 1b, 1c, 2c, 2d, 3a, 3b, and 3c, the homogeneous equation (3.5) has non-zero solutions. Any vector in the space spanned by these solutions (the null space of ) does not contribute to the equation error defined in (3.3) and, therefore, can be added to any particular generalized solution of (3.2) to give a family of solutions with the same approximation error. If the dimension of the null space of is , it is possible to find a unique generalized solution of (3.2) with zero elements. The non-unique solution for these seven cases can be written in the form [15].

| (3.22) |

where is an arbitrary vector. The first term is the minimum norm solution given by the Moore-Penrose pseudo-inverse and the second is a contribution in the null space of . For the minimum , the vector .

3.8.1 Derivations

To derive the necessary conditions for minimizing in the overspecified case, we differentiate with respect to and set that to zero. Starting with the error

| (3.23) |

| (3.24) |

and taking the gradient or derivative gives

| (3.25) |

which are the normal equations in (3.11) and the pseudoinverse in (3.12) and (3.18).

If we start with the weighted error problem

| (3.26) |

using the same steps as before gives the normal equations for the minimum weighted squared error as

| (3.27) |

and the pseudoinverse as

| (3.28) |

To derive the necessary conditions for minimizing the Euclidian norm when there are few equations and many solutions to (3.1), we define a Lagrangian

| (3.29) |

take the derivatives in respect to both and and set them to zero.

| (3.30) |

and

| (3.31) |

Solve these two equation simultaneously for eliminating gives the pseudoinverse in (3.14) and (3.19) result.

| (3.32) |

Because the weighting matrices are diagonal and real, multiplication and inversion is simple. These equations are used in the Iteratively Reweighted Least Squares (IRLS) algorithm described in another section.

3.9 Regularization

3.10 Least Squares Approximation with Constraints

The solution of the overdetermined simultaneous equations is generally a least squared error approximation problem. A particularly interesting and useful variation on this problem adds inequality and/or equality constraints. This formulation has proven very powerful in solving the constrained least squares approximation part of FIR filter design [57]. The equality constraints can be taken into account by using Lagrange multipliers and the inequality constraints can use the Kuhn-Tucker conditions [58, 1, 59]. The iterative reweighted least squares (IRLS) algorithm described in the next chapter can be modified to give results which are an optimal constrained least p-power solution [60, 61, 45].

3.11 Conclusions

There is remarkable structure and subtlety in the apparently simple problem of solving simultaneous equations and considerable insight can be gained from these finite dimensional problems. These notes have emphasized the norm but some other such as and are also interesting. The use of sparsity [50] is particularly interesting as applied in Compressive Sensing [62, 63] and in the sparse FFT [64]. There are also interesting and important applications in infinite dimensions. One of particular interest is in signal analysis using wavelet basis functions [16]. The use of weighted error and weighted norm pseudoinverses provide a base for iterative reweighted least squares (IRLS) algorithms.

Chapter 4 Approximation with Other Norms and Error Measures

Most of the discussion about the approximate solutions to are about the result of minimizing the equation error and/or the norm of the solution because in some cases that can be done by analytic formulas and also because the norm has a energy interpretation. However, both the and the [65] have well known applications that are important [48, 36] and the more general error is remarkably flexible [44, 45]. Donoho has shown [66] that optimization gives essentially the same sparsity as the true sparsity measure in .

In some cases, one uses a different norm for the minimization of the equation error than the one for minimization of the solution norm. And in other cases, one minimizes a weighted error to emphasize some equations relative to others [15]. A modification allows minimizing according to one norm for one set of equations and another for a different set. A more general error measure than a norm can be used which used a polynomial error [45] which does not satisfy the scaling requirement of a norm, but is convex. One could even use the so-called norm for which is not even convex but is an interesting tool for obtaining sparse solutions.

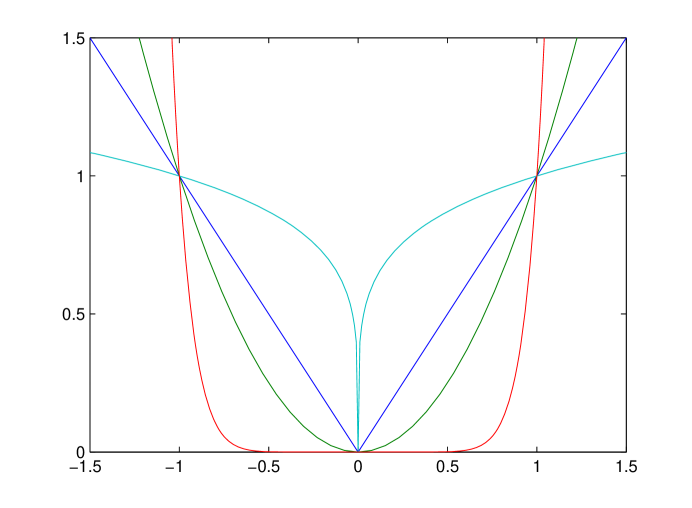

Note from the figure how the norm puts a large penalty on large errors. This gives a Chebyshev-like solution. The norm puts a large penalty on small errors making them tend to zero. This (and the norm) give a sparse solution.

4.1 The Norm Approximation

The IRLS (iterative reweighted least squares) algorithm allows an iterative algorithm to be built from the analytical solutions of the weighted least squares with an iterative reweighting to converge to the optimal approximation [13].

4.1.1 The Overdetermined System with more Equations than Unknowns

If one poses the approximation problem in solving an overdetermined set of equations (case 2 from Chapter 3), it comes from defining the equation error vector

| (4.1) |

and minimizing the p-norm

| (4.2) |

or

| (4.3) |

neither of which can we minimize easily. However, we do have formulas [15] to find the minimum of the weighted squared error

| (4.4) |

one of which is derived in Section 3.8.1, equation (3.25) and is

| (4.5) |

where is a diagonal matrix of the error weights, . From this, we propose the iterative reweighted least squared (IRLS) error algorithm which starts with unity weighting, , solves for an initial with (4.5), calculates a new error from(4.1), which is then used to set a new weighting matrix

| (4.6) |

to be used in the next iteration of (4.5). Using this, we find a new solution and repeat until convergence (if it happens!).

This core idea has been repeatedly proposed and developed in different application areas over the past 50 years with a variety of success [13]. Used in this basic form, it reliably converges for . In 1990, a modification was made to partially update the solution each iteration with

| (4.7) |

where is the new weighted least squares solution of (3.28) which is used to partially update the previous value using a convergence up-date factor which gave convergence over a larger range of around but but it was slower.

A second improvement showed that a specific up-date factor of

| (4.8) |

significantly increased the speed of convergence. With this particular factor, the algorithm becomes a form of Newton’s method which has quadratic convergence.

A third modification applied homotopy [60, 67, 68, 69] by starting with a value for which is equal to and increasing it each iteration (or each few iterations) until it reached the desired value, or, in the case of , decrease it. This made a significant increase in both the range of that allowed convergence and in the speed of calculations. Some of the history and details can be found applied to digital filter design in [44, 45].

A Matlab program that implements these ideas applied to our pseudoinverse problem with more equations than unknowns (case 2a) is:

% m-file IRLS1.m to find the optimal solution to Ax=b

% minimizing the L_p norm ||Ax-b||_p, using IRLS.

% Newton iterative update of solution, x, for M > N.

% For 2<p<infty, use homotopy parameter K = 1.01 to 2

% For 0<p<2, use K = approx 0.7 - 0.9

% csb 10/20/2012

function x = IRLS1(A,b,p,K,KK)

if nargin < 5, KK=10; end;

if nargin < 4, K = 2; end;

if nargin < 3, p = 10; end;

pk = 2; % Initial homotopy value

x = pinv(A)*b; % Initial L_2 solution

E = [];

for k = 1:KK % Iterate

if p >= 2, pk = min([p, K*pk]); % Homotopy change of p

else pk = max([p, K*pk]); end

e = A*x - b; % Error vector

w = abs(e).^((pk-2)/2); % Error weights for IRLS

W = diag(w/sum(w)); % Normalize weight matrix

WA = W*A; % apply weights

x1 = (WA’*WA)\(WA’*W)*b; % weighted L_2 sol.

q = 1/(pk-1); % Newton’s parameter

if p > 2, x = q*x1 + (1-q)*x; nn=p; % partial update for p>2

else x = x1; nn=2; end % no partial update for p<2

ee = norm(e,nn); E = [E ee]; % Error at each iteration

end

plot(E)

This can be modified to use different ’s in different bands of equations or to use weighting only when the error exceeds a certain threshold to achieve a constrained LS approximation [44, 45, 46]. Our work was originally done in the context of filter design but others have done similar things in sparsity analysis [47, 48, 70].

This is presented as applied to the overdetermined system (Case 2a and 2b) but can also be applied to other cases. A particularly important application of this section is to the design of digital filters.

4.1.2 The Underdetermined System with more Unknowns than Equations

If one poses the approximation problem in solving an underdetermined set of equations (case 3 from Chapter 3), it comes from defining the solution norm as

| (4.9) |

and finding to minimizing this p-norm while satisfying .

It has been shown this is equivalent to solving a least weighted norm problem for specific weights.

| (4.10) |

The development follows the same arguments as in the previous section but using the formula [71, 15] derived in (3.32)

| (4.11) |

with the weights, , being the diagonal of the matrix, , in the iterative algorithm to give the minimum weighted solution norm in the same way as (4.5) gives the minimum weighted equation error.

A Matlab program that implements these ideas applied to our pseudoinverse problem with more unknowns than equations (case 3a) is:

% m-file IRLS2.m to find the optimal solution to Ax=b

% minimizing the L_p norm ||x||_p, using IRLS.

% Newton iterative update of solution, x, for M < N.

% For 2<p<infty, use homotopy parameter K = 1.01 to 2

% For 0<p<2, use K = approx 0.7 to 0.9

% csb 10/20/2012

function x = IRLS2(A,b,p,K,KK)

if nargin < 5, KK= 10; end;

if nargin < 4, K = .8; end;

if nargin < 3, p = 1.1; end;

pk = 2; % Initial homotopy value

x = pinv(A)*b; % Initial L_2 solution

E = [];

for k = 1:KK

if p >= 2, pk = min([p, K*pk]); % Homotopy update of p

else pk = max([p, K*pk]); end

W = diag(abs(x).^((2-pk)/2)+0.00001); % norm weights for IRLS

AW = A*W; % applying new weights

x1 = W*AW’*((AW*AW’)\b); % Weighted L_2 solution

q = 1/(pk-1); % Newton’s parameter

if p >= 2, x = q*x1 + (1-q)*x; nn=p; % Newton’s partial update for p>2

else x = x1; nn=1; end % no Newton’s partial update for p<2

ee = norm(x,nn); E = [E ee]; % norm at each iteration

end;

plot(E)

This approach is useful in sparse signal processing and for frame representation.

4.2 The Chebyshev, Minimax, or Appriximation

The Chebyshev optimization problem minimizes the maximum error:

| (4.12) |

This is particularly important in filter design. The Remez exchange algorithm applied to filter design as the Parks-McClellan algorithm is very efficient [36]. An interesting result is the limit of an optimization as is the Chebyshev optimal solution. So, the Chebyshev optimal, the minimax optimal, and the optimal are all the same [65, 36].

A particularly powerful theorem which characterizes a solution to is given by Cheney [65] in Chapter 2 of his book:

-

•

A Characterization Theorem: For an by real matrix, with , every minimax solution is a minimax solution of an appropriate subsystem of the equations. This optimal minimax solution will have at least equal magnitude errors and they will be larger than any of the errors of the other equations.

This is a powerful statement saying an optimal minimax solution will have out of , at least maximum magnitude errors and they are the minimum size possible. What this theorem doesn’t state is which of the equations are the appropriate ones. Cheney develops an algorithm based on this theorem which finds these equations and exactly calculates this optimal solution in a finite number of steps. He shows how this can be combined with the minimum using a large , to make an efficient solver for a minimax or Chebyshev solution.

This theorem is similar to the Alternation Theorem [36] but more general and, therefore, somewhat more difficult to implement.

4.3 The Approximation and Sparsity

The sparsity optimization is to minimize the number of non-zero terms in a vector. A “pseudonorm”, , is sometimes used to denote a measure of sparsity. This is not convex, so is not really a norm but the convex (in the limit) norm is close enough to the to give the same sparsity of solution [66]. Finding a sparse solution is not easy but interative reweighted least squares (IRLS) [45, 46], weighted norms [47, 48], and a somewhat recent result is called Basis Pursuit [72, 73] are possibilities.

This approximation is often used with an underdetermined set of equations (Case 3a) to obtain a sparse solution .

Using the IRLS algorithm to minimize the equation error often gives a sparse error if one exists. Using the algorithm in the illustrated Matlab program with on the problem in Cheney [65] gives a zero error in equation 4 while using no larger gives any zeros.

Chapter 5 General Posing of Simultaneous Equations

Consider a mixture of the first and second problems posed in the introduction. The first problem assumed that is given and is to be found. The second problem assumed that is given and is to be found. We now again consider

| (5.1) |

but now let there be unknowns in the vector and givens or known values. The necessary balance of knowns and unknowns is maintained by having unknowns in the vector and givens or known values. With this generalization of the problem, we still have the same number of equations and unknowns but the unknowns are now divided to be on both sides of the equation. Note that this has the original problem-one as a special case for and problem-two results from but now allows a much more versatile mixture of the two. The integer with is the parameter that determines the mixture.

To show that we can solve for the unknowns, we now re-order the rows of in (5.1) so that the unknowns in are the first entries. We then re-order the columns so that the givens (knowns) in are the first entries. These reordered equations are partitioned in the form of

| (5.2) |

with the matrix being by and being by and with and being given and and being unknown.

Eliminating gives for

| (5.3) |

which requires to be

| (5.4) |

Equations (5.3) and (5.4) can be written in one partitioned matrix equation as

| (5.5) |

which is in the original form of having the knowns on the left hand side of the equation and the unknowns (to be calculated) on the right hand side.

Note that the original problem-1, which is the case for , causes (5.3) to become simply and problem-2 with gives .

This mixed formulation of simultaneous equations allows a linear algebra description of IIR (Infinite duration Impulse Response) digital filters and the use of partitions allows linear design of IIR filters which interpolate samples of a desired frequency response [36]. With the definition of an equation error, it also allows the optimal least squared equation error approximation. This is used in implementing Prony’s method, Pade’s method, and linear prediction [74].

Note also that this mixed formulation can also be stated in an over determined or under determined form which will require approximation in finding an optimal solution, see chapter 3.1.

The general posing of simultaneous equations also gives some interesting insights into sampling theory. For example, if the matirx is the discrete Fourier transform (DFT) matrix, and the signal is band limited, then (5.5) describes the case with implying that the total signal can be calculated from samples in by finding from (5.4). This can be viewed as a generalized sampling theorem.

A particularly interesting and important application of this formulation is the calculation of the sparse FFT (fast Fourier transform) [64, 75, 76]. In this problem, it is known that the signal has only non-zero spectral values (usually with ). In other words, from the specifics of the physical problem, it is known that values of the DFT (discrete Fourier transform) of the signal are zero. From (5.3), we see that the sparseness requires and the matrix in (5.1) is the DFT matrix. The desired DFT values are and are given by

| (5.6) |

which can be calculated from any samples of the -sparse signal requiring at most operations. is non-singular if is orthogonal (which the DFT matrix is) and may be in other cases.

From this formulation, it is seen that a length- -sparse signal lies in a dimensional subspace of the dimensional signal space. The DFT of any signal in the subspace can be calculated from samples of the signal using (5.6). Most of the recent work on sparse FFTs does not assume the location of the non-zero terms in is known ahead of time but are discovered as part of the solution. This seems to require more samples as well as more computation. The most common approach “filters” the signal and finds the solution in “bins” in the frequency domain [64, 77]. The number of operations for these approachs seems to be . Another approach uses the Chinese remainder theorem [75] to determine samples of or orthogonal polynomials [76]. These claim a number of operations of .

Chapter 6 Constructing the Operator

Solving the third problem posed in the introduction to these notes is rather different from the other two. Here we want to find an operator or matrix that when multiplied by gives . Clearly a solution to this problem would not be unique as stated. In order to pose a better defined problem, we generally give a set or family of inputs and the corresponding outputs . If these families are independent, and if the number of them is the same as the size of the matrix, a unique matrix is defined and can be found by solving simultaneous equations. If a smaller number is given, the remaining degrees of freedom can be used to satisfy some other criterion. If a larger number is given, there is probably no exact solution and some approximation will be necessary.

If the unknown operator matrix is of dimension by , then we take inputs for , each of dimension and the corresponding outputs , each of dimension and form the matrix equation:

| (6.1) |

where is the by unknown operator, is the by input matrix with columns which are the inputs and is the by output matrix with columns . The operator matrix is then determined by:

| (6.2) |

if the inputs are independent which means is nonsingular.

This problem can be posed so that there are more (perhaps many more) inputs and outputs than with a resulting equation error which can be minimized with some form of pseudoinverse.

Linear regression can be put in this form. If our matrix equation is

| (6.3) |

where is a row vector of unknown weights and is a column vector of known inputs, then is a scaler inter product. If a seond experiment gives a second scaler inner product from a second column vector of known inputs, then we augment to have two rows and to be a length-2 row vector. This is continued for experiment to give (6.3) as a 1 by row vector times an by matrix which equals a 1 by row vector. It this equation is transposed, it is in the form of (6.3) which can be approximately solved by the pesuedo inverse to give the unknown weights for the regression.

Alternatively, the matrix may be constrained by structure to have less than degrees of freedom. It may be a cyclic convolution, a non cyclic convolution, a Toeplitz, a Hankel, or a Toeplitz plus Hankel matrix.

A problem of this sort came up in research on designing efficient prime length fast Fourier transform (FFT) algorithms where is the data and is the FFT of . The problem was to derive an operator that would make this calculation using the least amount of arithmetic. We solved it using a special formulation [78] and Matlab.

This section is unfinished.

Chapter 7 Topics that might be Added

The following topics may added to these notes over time:

-

1.

Different norms on equation error and solution error and solution size

-

2.

exchange algorithm for Cheby approx from Cheney plus a program

-

3.

Freq. sampling [37], least squares, Chebyshev design of FIR filters

-

4.

Block formulation of FIR and IIR digital filters, Prony and Pade approximation

-

5.

Periodically time varying filters, Two-frequency formulation

-

6.

State variable modelling of dynamic systems; feedback control systems, sol by diagonalizing

-

7.

Regression, Machine Learning, Neural Networks (layers of linear and non-linear operators)

-

8.

The eigenvalue problem, eigenvector expansions, diagonalization of a matrix, and singular value decomposition (SVD)

-

9.

Quadratic forms, other optimizaion measures e.g. polynomials

-

10.

Other error definitions for approximate solutions. Sparsity [50] and approximation.

-

11.

Use of Matlab, Octave, SciLab, Mathematica, Maple, LabVIEW, R, Python, etc.

-

12.

Constrained approximation, Kuhn-Tucker.

-

13.

Expansion and completion of Chapter 6 on Constructing the Operator.

Please contact the author at [csb@rice.edu] with any errors, recommendations, or comments. Anyone is free to use these note in any way as long as attribution is given according to the Creative Commons (cc-by) rules.

Bibliography

- [1] Gilbert Strang. Introduction to Linear Algebra. Wellesley Cambridge, New York, 1986. 5th Edition, 2016.

- [2] Gilbert Strang. Linear Algebra and Learning from Data. Wellesley Cambridge, Wellesley, 2019. math.mit.edu/learningfromdata.

- [3] Cleve Moler. Numerical Computing with MATLAB. The MathWorks, Inc., South Natick, MA, 2008. available: http://www.mathworks.com/moler/.

- [4] Lloyd N. Trefethen and David Bau III. Numerical Linear Algebra. SIAM, 1997.

- [5] Paul R. Halmos. Finite-Dimensional Vector Spaces. Van Nostrand, Princeton, NJ, 1958. Springer 1974.

- [6] R. M. Young. An Introduction to Nonharmonic Fourier Series. Academic Press, New York, 1980.

- [7] J. Tinsley Oden and Leszek F. Demkowicz. Applied Functional Analysis. CRC Press, Boca Raton, 1996.

- [8] Todd K. Moon and Wynn C. Stirling. Mathematical Methods and Algorithms for Signal Processing. Prentice-Hall, Upper Saddle River, NJ, 2000. pdf available free on the Internet.

- [9] Lewis Franks. Signal Theory. Prentice–Hall, Englewood Cliffs, NJ, 1969.

- [10] D. G. Luenberger. Optimization by Vector Space Methods. John Wiley & Sons, New York, 1969, 1997.

- [11] A. Benveniste, R. Nikoukhah, and A. S. Willsky. Multiscale system theory. IEEE Transactions on Circuits and Systems, I, 41(1):2–15, January 1994.

- [12] C. L. Lawson and R. J. Hanson. Solving Least Squares Problems. Prentice-Hall, Inglewood Cliffs, NJ, 1974. Second edition by SIAM in 1987.

- [13] Åke Björck. Numerical Methods for Least Squares Problems. Blaisdell, Dover, SIAM, Philadelphia, 1996.

- [14] Arthur Albert. Regression and the Moore-Penrose Pseudoinverse. Academic Press, New York, 1972.

- [15] Adi Ben-Israel and T. N. E. Greville. Generalized Inverses: Theory and Applications. Wiley and Sons, New York, 1974. Second edition, Springer, 2003.

- [16] Ingrid Daubechies. Ten Lectures on Wavelets. SIAM, Philadelphia, PA, 1992. Notes from the 1990 CBMS-NSF Conference on Wavelets and Applications at Lowell, MA.

- [17] C. Sidney Burrus, Ramesh A. Gopinath, and Haitao Guo. Introduction to Wavelets and Wavelet Transforms: A Primer. Prentice Hall, Upper Saddle River, NJ, 1998. Also published in OpenStax in 2012’.

- [18] David L. Donoho. Unconditional bases are optimal bases for data compression and for statistical estimation. Applied and Computational Harmonic Analysis, 1(1):100–115, December 1993. Also Stanford Statistics Dept. Report TR-410, Nov. 1992.

- [19] Christopher M. Bishop. Pattern Recognition and Machine Learning. Springer, 2006.

- [20] Simon O. Haykin. Neural Networks and Learning Machines. Prentice Hall, 2008.

- [21] Lotfi A. Zadeh and Charles A. Desoer. Linear System Theory: The State Space Approach. Dover, 1963, 2008.

- [22] Paul M. DeRusso, Rob J. Roy, and Charles M. Close. State Variables for Engineers. Wiley, 1965. Second edition 1997.

- [23] Gilbert Strang. Linear Algebra and Its Applications. Academic Press, New York, 1976. 4th Edition, Brooks Cole, 2005.

- [24] Jim Hefferon. Linear Algebra. Virginia Commonwealth Univeristy Mathematics Textbook Series, 2011. Copyright: cc-by-sa, URL:joshua.smcvt.edu.

- [25] C. Sidney Burrus. Fast Fourier Transforms. OpenStax-Cnx, cnx.org, 2008. http://cnx.org/content/col10550/latest/.

- [26] Paul R. Halmos. Introduction to Hilbert Space and the Theory of Spectral Multiplicity. Chelsea, New York, 1951. second edition 1957.

- [27] N. Young. An Introduction to Hilbert Space. Cambridge Press, 1988.

- [28] Ole Christensen. An Introduction to Frames and Riesz Bases. Birkhäuser, 2002.

- [29] Christopher Heil, Palle E. T. Jorgensen, and David R. Larson, editors. Wavelets, Frames and Operator Theory. American Mathematical Society, 2004.

- [30] Shayne F. D. Waldron. An Introduction to Finite Tight Frames, Draft. Springer, 2010. http://www.math.auckland.ac.nz/ waldron/Harmonic-frames/Tuan-Shayne/book.pdf.

- [31] Jelena Kovacevic and Amina Chebira. Life beyond bases: The advent of frames (part ii). IEEE Signal Processing Magazine, 24(5):115–125, September 2007.

- [32] Soo-Chang Pei and Min-Hung Yeh. An introduction to discrete finite frames. IEEE Signal Processing Magazine, 14(6):84–96, November 1997.

- [33] Jelena Kovacevic and Amina Chebira. Life beyond bases: The advent of frames (Part I). IEEE Signal Processing Magazine, 24(4):86–104, July 2007.

- [34] Paulo J. S. G. Ferreira. Mathematics for multimedia signal processing II: Discrete finite frames and signal reconstruction. Signal Processing for Multimedia, pages 35–54, 1999. J. S. Byrnes (editor), IOS Press.

- [35] Martin Vetterli, Jelena Kovačević, and Vivek K. Goyal. Foundations of Signal Processing. Cambridge University Press, 2014. also available online: http://fourierandwavelets.org/.

- [36] C. Sidney Burrus. Digital Signal Processing and Digital Filter Design. OpenStax-Cnx, cnx.org, 2008. http://cnx.org/content/col10598/latest/.

- [37] Yonina C. Eldar. Sampling Theory, Beyond Bandlimited Systems. Cambridge University Press, 2015.

- [38] R. J. Marks II. Introduction to Shannon Sampling and Interpolation Theory. Springer-Verlag, New York, 1991.

- [39] Richard C. Dorf. Time-Domain Analysis and Design of Control Systems. Addison-Wesley, 1965.

- [40] E. H. Moore. On the reciprocal of the general algebraic matrix. Bulletin of the AMS, 26:394–395, 1920.

- [41] R. Penrose. A generalized inverse for matrices. Proc. Cambridge Phil. Soc., 51:406–413, 1955.

- [42] R. Penrose. On best approximate solutions of linear matrix equations. Proc. Cambridge Phil. Soc., 52:17–19, 1955.

- [43] Frigyes Riesz and Béla Sz.–Nagy. Functional Analysis. Dover, New York, 1955.

- [44] C. S. Burrus and J. A. Barreto. Least -power error design of FIR filters. In Proceedings of the IEEE International Symposium on Circuits and Systems, volume 2, pages 545–548, ISCAS-92, San Diego, CA, May 1992.

- [45] C. S. Burrus, J. A. Barreto, and I. W. Selesnick. Iterative reweighted least squares design of FIR filters. IEEE Transactions on Signal Processing, 42(11):2926–2936, November 1994.

- [46] Ricardo Vargas and C. Sidney Burrus. Iterative design of digital filters. arXiv, 2012. arXiv:1207.4526v1 [cs.IT] July 19, 2012.

- [47] Irina F. Gorodnitsky and Bhaskar D. Rao. Sparse signal reconstruction from limited data using FOCUSS: a re-weighted minimum norm algorithm. IEEE Transactions on Signal Processing, 45(3), March 1997.

- [48] Ingrid Daubechies, Ronald DeVore, Massimo Fornasier, and C. Sinan Gunturk. Iteratively reweighted least squares minimization for sparse recovery. Communications on Pure and Applied Mathematics, 63(1):1–38, January 2010.

- [49] David L. Donoho and Michael Elad. Optimally sparse representation in general (non-orthogonal) dictionaries via minimization. Technical report, Statistics Department, Stanford University, 2002.

- [50] Ivan Selesnick. Introduction to sparsity in signal processing. Connexions Web Site, May 2012. Available: http://cnx.org/content/m43545/latest/.

- [51] S. L. Campbell and C. D. Meyer, Jr. Generalized Inverses of Linear Transformations. Pitman, London, 1979. Reprint by Dover in 1991.

- [52] C. R. Rao and S. K. Mitra. Generalized Inverse of Matrices and its Applications. John Wiley & Sons, New York, 1971.

- [53] Cleve Moler, John Little, and Steve Bangert. Matlab User’s Guide. The MathWorks, Inc., South Natick, MA, 1989.

- [54] Gene H. Golub and Charles F. Van Loan. Matrix Computations. The John Hopkins University Press, Baltimore, MD, 1996. 3rd edition, 4th edition is forthcoming.

- [55] A. Neumaier. Solving ill-conditioned and singular linear systems: A tutorial on regularization. SIAM Reiview, 40:636–666, 1998. available: http://www.mat.univie.ac.at/ neum/.

- [56] Christian Hansen. Regularization Tools. Informatics and Mathematical Modelling, Technical University of Denmark, 2008. A Matlab package for analysis and solution of discrete ill-posed problems.

- [57] Ivan W. Selesnick, Markus Lang, and C. Sidney Burrus. Constrained least square design of FIR filters without explicitly specified transition bands. IEEE Transactions on Signal Processing, 44(8):1879–1892, August 1996.

- [58] R. Fletcher. Practical Methods of Optimization. John Wiley & Sons, New York, second edition, 1987.

- [59] D. G. Luenberger. Introduction to Linear and Nonlinear Programming. Springer, third edition, 2008.

- [60] C. S. Burrus, J. A. Barreto, and I. W. Selesnick. Reweighted least squares design of FIR filters. In Paper Summaries for the IEEE Signal Processing Society’s Fifth DSP Workshop, page 3.1.1, Starved Rock Lodge, Utica, IL, September 13–16 1992.

- [61] C. Sidney Burrus. Constrained least squares design of FIR filters using iterative reweighted least squares. In Proceedings of EUSIPCO-98, pages 281–282, Rhodes, Greece, September 8-11 1998.

- [62] Richard G. Baraniuk. Compressive sensing. IEEE Signal Processing Magazine, 24(4):118–124, July 2007. also: http://dsp.rice.edu/cs.

- [63] David L. Donoho. Compressed sensing. Technical report, Statistics Department, Stanford University, September 2004. http://www-stat.stanford.edu/ donoho/ Reports/2004/CompressedSensing091604.pdf.

- [64] Haitham Hassanieh, Piotr Indyk, Dina Katabi, and Eric Price. Nearly optimal sparse Fourier transform. arXiv:1201.2501v2 [cs.DS] 6 April 2012. Also, STOC 2012, 2012.

- [65] E. W. Cheney. Introduction to Approximation Theory. McGraw-Hill, New York, 1966. Second edition, AMS Chelsea, 2000.

- [66] David L. Donoho. For most large underdetermined systems of linear equations the minimal -norm solution is also the sparsest solution. Communications on Pure and Applied Mathematics, 59(6):797–829, June 2006. http://stats.stanford.edu/ donoho/Reports/2004/l1l0EquivCorrected.pdf.

- [67] Virginia L. Stonick and S. T. Alexander. Globally optimal rational approximation using homotopy continuation methods. IEEE Transactions on Signal Processing, 40(9):2358–2361, September 1992.

- [68] Virginia L. Stonick and S. T. Alexander. A relationship between the recursive least squares update and homotopy continuation methods. IEEE Transactions on Signal Processing, 39(2):530–532, Feburary 1991.

- [69] Allan J. Sieradski. An Introduction to Topology and Homotopy. PWS–Kent, Boston, 1992.

- [70] Andrew E. Yagle. Non-iterative reweighted-norm least-squares local minimization for sparse solutions to underdetermined linear systems of equations, 2008. preprint at http://web.eecs.umich.edu/ aey/sparse/sparse11.pdf.

- [71] Ivan W. Selesnick. Least squares solutions to linear system of equations, 2009. to be published in Connexions.

- [72] S. S. Chen, D. L. Donoho, and M. A. Saunders. Atomic decomposition by basis pursuit. SIAM Journal of Sci. Compt., 20:33–61, 1998.

- [73] Scott S. Chen, David L. Donoho, and Michael A. Saunders. Atomic decomposition by basis pursuit. SIAM Review, 43(1):129–159, March 2001. http://www-stat.stanford.edu/ donoho/reports.html.

- [74] C. Sidney Burrus. Prony, Padé, and linear prediction. OpenStax, 2012. http://cnx.org/content/m45121/latest/.

- [75] Sameer Pawar and Kannan Ramchandran. Computing a k-sparse n-length discrete Fourier transform using at most 4k samples and o(k log k) complexity. arXiv:1305.0870v1 [cs.DS] 4 May 2013, 2013.

- [76] Sung-Hsien Hsieh, Chun-Shien Lu, and Soo-Chang Pei. Sparse fast Fourier transform by downsampling. In Proceedings of ICASSP-13, pages 5637–5641, Vancouver, British Columbia, May 28-31 2013.

- [77] Haitham Hassanieh, Piotr Indyk, Dina Katabi, and Eric Price. Simple and practical algorithm for sparse fourier transform, 2012.

- [78] Howard W. Johnson and C. S. Burrus. On the structure of efficient DFT algorithms. IEEE Transactions on Acoustics, Speech, and Signal Processing, 33(1):248–254, February 1985.