Multiple block sizes and overlapping blocks for multivariate time series extremes

Abstract

Block maxima methods constitute a fundamental part of the statistical toolbox in extreme value analysis. However, most of the corresponding theory is derived under the simplifying assumption that block maxima are independent observations from a genuine extreme value distribution. In practice however, block sizes are finite and observations from different blocks are dependent. Theory respecting the latter complications is not well developed, and, in the multivariate case, has only recently been established for disjoint blocks of a single block size. We show that using overlapping blocks instead of disjoint blocks leads to a uniform improvement in the asymptotic variance of the multivariate empirical distribution function of rescaled block maxima and any smooth functionals thereof (such as the empirical copula), without any sacrifice in the asymptotic bias. We further derive functional central limit theorems for multivariate empirical distribution functions and empirical copulas that are uniform in the block size parameter, which seems to be the first result of this kind for estimators based on block maxima in general. The theory allows for various aggregation schemes over multiple block sizes, leading to substantial improvements over the single block length case and opens the door to further methodology developments. In particular, we consider bias correction procedures that can improve the convergence rates of extreme-value estimators and shed some new light on estimation of the second-order parameter when the main purpose is bias correction.

keywords:

[class=AMS]keywords:

and

T1Supported by the collaborative research center “Statistical modeling of nonlinear dynamic processes” (SFB 823) of the German Research Foundation (DFG). T2Supported by a Discovery Grant from the Natural Sciences and Engineering Research Council of Canada.

1 Introduction

Extreme-value theory provides a central statistical ingredient in various fields like hydrology, meteorology and financial risk management, which all have to deal with highly unlikely but important events, see, e.g., Beirlant et al., (2004) for an overview. Mathematically, the properties of such events can be understood by studying the (multivariate) tail of probability distributions and the potential temporal dependence of tail events. Respective statistical methodology typically relies on some version of one of two fundamental approaches: the peaks-over-threshold (POT) method which considers only observations that exceed a certain high threshold, or the block maxima (BM) method which is based on taking maxima of observed values over consecutive blocks of observations and treating those maxima as (approximate) data from an extreme value distribution.

While historically the BM approach was the first to be invented (Gumbel,, 1958), the mathematical interest soon shifted towards the POT approach. POT methods are by now well understood, and there is a rich and mature literature on various theoretical and practical aspects of such methods, see de Haan and Ferreira, (2006) for a review of many classical results and Drees and Rootzén,, 2010; Can et al.,, 2015; Fougères et al.,, 2015; Einmahl et al.,, 2016 for recent developments. In the last couple of years, there has been an increased interest in the theoretical aspects of the BM approach for univariate observations, and recent work in this direction includes Dombry, (2015); Ferreira and de Haan, (2015); Dombry and Ferreira, (2017); Bücher and Segers, 2018b ; Bücher and Segers, 2018a . The case of multivariate observations has received much less attention, and the only theoretical analysis of (component-wise) block maxima in the multivariate setting that we are aware of is due to Bücher and Segers, (2014). The present paper is motivated by this apparent imbalance of theoretical developments for BM methods as compared to POT methods in the multivariate case.

It is well known that the analysis of multivariate distributions can be decomposed into two distinct parts: the analysis of marginal distributions and the analysis of the dependence structure as described by the associated copula. Classical results from extreme-value theory further show that the possible dependence structures of extremes have to satisfy certain constraints, but do not constitute a parametric family. In fact, the possible dependence structures may be described in various equivalent ways (see, e.g., Resnick,, 1987; Beirlant et al.,, 2004; de Haan and Ferreira,, 2006): by the exponent measure (Balkema and Resnick,, 1977), by the spectral measure (de Haan and Resnick,, 1977), by the Pickands dependence function (Pickands,, 1981), by the stable tail dependence function (Huang,, 1992), by the tail copula (Schmidt and Stadtmüller,, 2006), by the madogram (Naveau et al.,, 2009), by the extreme-value copula (see Gudendorf and Segers, (2010) for an overview), or by other less popular objects.

Since statistical theory for estimators of, e.g., the Pickands dependence function, the stable tail dependence function, or the madogram may be derived from corresponding results for the empirical copula process (see, e.g., Genest and Segers,, 2009), we focus on constructing estimators for the extreme-value copula , which can in turn serve as a fundamental building block for subsequent developments. This approach was also taken in the above-mentioned reference Bücher and Segers, (2014), who analyse the empirical copula process based on (disjoint) block maxima, and then apply the results to obtain the asymptotic behavior of estimators for the Pickands dependence function.

The basic observational setting that we consider is the same as in Bücher and Segers, (2014): data are assumed to come from a strictly stationary multivariate time series, and we assume that the copula of the random vector of component-wise block-maxima converges, as the block length tends to infinity, to a copula which is our main object of interest. However, in contrast to Bücher and Segers, (2014), we base our estimators on overlapping instead of disjoint blocks. While the corresponding theoretical analysis is more involved due to the additional dependence introduced by overlaps in the blocks, we show that this always leads to a reduction in the asymptotic variance of the resulting empirical copula process and smooth functionals thereof. Another major difference with Bücher and Segers, (2014) is that we consider functional central limit theorems which explicitly involve the block size as a parameter. This generalization is crucial for various applications, some of which are considered in Section 3.

As a first simple but useful application, we consider estimators for which are based on aggregating over various block length parameters, thereby providing estimators which are less sensitive to the choice of a single block length parameter. The corresponding asymptotic theory is a straightforward consequence of the asymptotic theory mentioned before. A Monte Carlo simulation study reveals the superiority of the aggregated estimators over their non-aggregated versions in typical finite-sample situations.

A second more involved application concerns the construction of bias-reduced estimators for (see Fougères et al.,, 2015; Beirlant et al.,, 2016 for recent proposals in the multivariate POT approach for i.i.d. observations). As is typically done when tackling the problem of bias reduction in extreme value statistics, the estimators are obtained by explicitly taking into account the second order structure of the extreme value model in the estimation step. We are not aware of any results on bias-reduced estimators within the block maxima framework in general. In fact, even for POT methods such results do not seem to exist in the multivariate time series setting (some results on the univariate time series case can be found in de Haan et al.,, 2016). As a necessary intermediate step for bias correction, we need to consider estimation of a second order parameter which naturally shows up in the second order condition. We show that special care needs to be taken when estimating this parameter for its use in bias correction, and propose a penalized estimator which explicitly takes this specific aim into account.

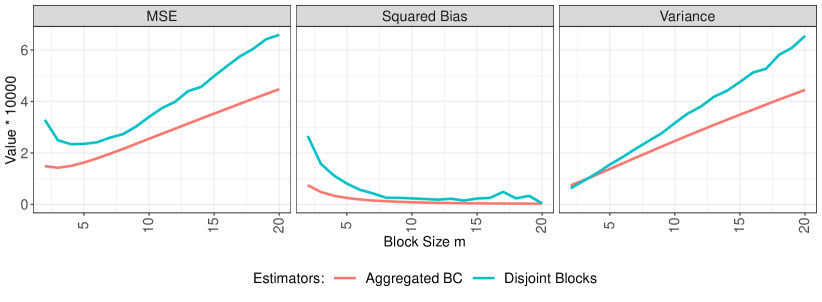

The improvement in both variance and bias of one of the estimators for proposed in this paper over the disjoint blocks estimator from Bücher and Segers, (2014) is illustrated in Figure 1.

The idea of using sliding/overlapping block maxima for statistical inference appears to be quite new to the extreme value community, whence similar results in the literature actually are rare, even in univariate situations. To the best of our knowledge, the idea first appeared in the context of estimating the extremal index of a univariate stationary time series, see Robert et al., (2009); Northrop, (2015); Berghaus and Bücher, (2018). The only paper we are aware of in the classical univariate case is Bücher and Segers, 2018a , which is restricted to the heavy tailed case. The idea of basing inference on multiple block sizes seems to be new, and is possibly transferable to the univariate case as well.

We further remark that there is a rich and mature literature that deals with estimation of extreme-value copulas and related objects when observations from an extreme-value copula are available (see, among many others, Pickands,, 1981, Capéraà et al.,, 1997 for early contributions and Genest and Segers,, 2009,Gudendorf and Segers,, 2010 for rank-based methods). However, the setting in that literature is different from ours since we do not assume that data from the extreme value copula are available directly.

The remaining parts of this paper are organized as follows: the sliding block maxima (empirical) copula process, including the block length as an argument of the process, is considered in Section 2. The applications on aggregated estimators, bias-reduced estimators and estimators of second order parameters are worked out in Section 3. Some theoretical examples, as well as a detailed Monte Carlo simulation study are presented in Section 4. All proofs are deferred to a supplementary material (Zou et al.,, 2019).

Throughout, for , let be the smallest integer greater or equal to . Let be the largest integer smaller or equal to if and the smallest integer greater or equal to if . For , write if for all , and if there exists such that . Let All convergences will be for , if not mentioned otherwise. The arrow denotes weak convergence in the sense of Hoffman-Jørgensen, see van der Vaart and Wellner, (1996).

2 Functional weak convergence of empirical copula processes based on sliding block maxima

Suppose is a multivariate strictly stationary process, and that is observable data. Let be a block size parameter and, for and , let be the maximum of the th sliding block of observations in the th coordinate. For , let

where denotes the left-continuous generalized inverse of a c.d.f. . Subsequently, we assume that the marginal c.d.f.s of are continuous. In that case, the marginal c.d.f.s of are continuous as well and

is the unique copula associated with . Throughout, we shall work under the following fundamental domain-of-attraction condition.

Assumption 2.1.

There exists a copula such that

Typically, the limit will be an extreme value copula (Hsing,, 1989; Hüsler,, 1990), that is, for all and and

for some stable tail dependence function satisfying

-

(i)

is homogeneous: for all ;

-

(ii)

for , where denotes the th unit vector;

-

(iii)

for all ;

-

(iv)

is convex;

see, e.g., Beirlant et al., (2004). By Theorem 4.2 in Hsing, (1989), this is for instance the case if the time series is beta-mixing. However, is in general different from the extreme value attractor, say , in case the observations are i.i.d. from the stationary distribution of the time series, see for instance Section 4.1 in Bücher and Segers, (2014). In fact, (block) maxima calculated from time series naturally incorporate information about the serial dependence (as, e.g., measured by the multivariate extremal index, see Section 10.5.2. in Beirlant et al.,, 2004), whence the BM approach is typically more suitable when it comes to, e.g., assessing return levels or periods. In the i.i.d. case, Assumption 2.1 is equivalent to the existence of a stable tail dependence function such that

where the copula is naturally extended to a c.d.f. on .

Assumption 2.1 does not contain any information about the rate of convergence of to . In many cases, more precise statements about this rate can be made, and it is even possible to write down higher order expansions for the difference . For some of the material in the paper, we will assume the validity of such expansions. Recall that a function defined on the integers is regularly varying if is regularly varying as a function .

Assumption 2.2 (Second order condition).

There exists a regularly varying function with coefficient of regular variation and a (necessarily continuous) non-null function on such that

uniformly in .

We refer to the accompanying paper Bücher et al., (2019) for a detailed account on second order conditions in the i.i.d. case. In particular, the latter paper shows that the block maxima second order condition above follows from the more common second order condition imposed on a POT-type convergence to under fairly general assumptions, see also Equation (6) in Fougères et al., (2015). It was further shown in Bücher et al., (2019) that, in the i.i.d. case, the function in the condition above must be regularly varying (the part can hence be removed from the assumption), that the function has certain homogeneity properties and that local uniform convergence on is sufficient for uniform convergence on . Specific examples in the i.i.d. and time series case are discussed in more detail in Section 4.1.

2.1 Estimation in the case of known marginal distributions.

We begin by estimating in the case of known marginal c.d.f.s , which, on the level of proofs, is a necessary intermediate step when considering the realistic case of unknown marginal c.d.f.s in the subsequent section. For block size , let

| (2.1) |

denote the empirical c.d.f. of the sample of standardized sliding block maxima . Subsequently, we will consider block sizes of the form with scaling parameter . The respective centred empirical process we are interested in is

where . For the functional weak convergence results to follow, we consider as an element of , the space of bounded function on equipped with the supremum norm, where is a fixed interval, the case being explicitly allowed. We impose the following assumptions on the block length parameter and the serial dependence of the time series.

Assumption 2.3.

Denote by and the and mixing coefficients of the process , respectively. Assume

-

(i)

-

(ii)

as , for some ,

-

(iii)

-

(iv)

Condition (i) is a typical condition in extreme value statistics, and in fact a necessary condition to allow for consistent estimation of . Condition (ii) is a short-range dependence condition that we introduce merely for technical reasons associated with our method of proof. At the cost of more sophisticated proofs, the condition may possibly be relaxed. However, since the condition is known to be satisfied for many common time series model, we feel that such a relaxation is not necessarily needed. Assumptions (iii) and (iv) relate the block length parameter to the serial dependence and allow for obtaining central limit theorems (alpha-mixing) and proofs of tightness based on coupling arguments (beta-mixing).

Theorem 2.4.

Perhaps surprisingly, the limiting covariance does not depend on the serial dependence of the original time series, except through itself. In the univariate case this was also observed in Bücher and Segers, 2018a .

Remark 2.5.

Under a slightly weaker version of Assumption 2.3, Bücher and Segers, (2014), Theorem 3.1, investigated the corresponding empirical process based on disjoint block maxima with , that is, the process in defined by

and with tight centred Gaussian limit denoted by . The covariance function of the limiting process is given by

A comparison between the covariance functionals and is worked out in Section 2.3 below, c.f. Section A.4 in the supplementary material Zou et al., (2019) for an alternative expression for .

Proof of Theorem 2.4.

Recall , let and define

The proof consists of several steps, which are explicitly taken care of in the supplementary material Zou et al., (2019):

-

(i)

In Lemma A.1 we prove that . Hence it suffices to prove weak convergence of .

-

(ii)

In Lemma A.2 we show that is asymptotically uniformly equicontinuous in probability with respect to the -norm on .

-

(iii)

In Lemma A.5 we prove that the finite-dimensional distributions of converge weakly to those of .

Weak convergence of then follows by combining (i)-(iii). ∎

The proofs of Step (ii) and Step (iii) are quite lengthy and technical, but it is instructive to present the main ideas within the next two remarks.

Remark 2.6 (Proving fidi-convergence).

The main steps for proving weak convergence of the finite-dimensional distributions (see Lemma A.5 for details) are as follows:

-

(i)

Calculation of the limiting covariance functional . This is treated in Lemma A.4, and bears similarities with common long run variance calculations in classical time series analysis. The integrals in are due to the fact that some of the sliding blocks are overlapping, with the integration variable controlling the relative position of two overlapping blocks, and with each of the three integrals corresponding to one of three possibilities for two blocks to overlap: (1) a block of length starts before a block of length and ends inside, (2) a block of length lies completely within a block of length , or (3) a block of length starts inside a block of length and ends outside. Consider for instance the latter case, which would correspond to and amounts to consideration of the event The main idea consist of rewriting this event as

We then use alpha mixing to show that the three events are asymptotically independent; this eventually gives rise to the three-fold product in the third integral in the definition of with each of the factors corresponding to the probability of one of the events above.

-

(ii)

Big-Blocks-Small-Blocks technique. The summands of the estimator of interest are collected in successive blocks of (block maxima) observations, with a ‘big block’ followed by a ‘small block’ followed by a ‘big block’ etc. The small blocks are then shown to be negligible, while the big blocks are shown to be asymptotically independent (via alpha mixing). Weak convergence of the sum corresponding to big blocks can finally be shown by an application of the Lyapunov Central Limit Theorem.

Remark 2.7 (Proving asymptotic tightness).

The main steps for proving the tightness part (see Lemma A.2) are as follows:

-

(i)

Getting rid of serial dependence. Based on a coupling lemma for beta mixing sequences by Berbee, (1979) and a blocking argument, proving tightness of may be reduced to proving tightness of two empirical processes based on row-wise i.i.d. observations. In contrast to classical time series settings where blocks are based on the original observations, we consider blocks of collections of block maxima corresponding to all block sizes considered. Blocking vectors of block maxima is needed to deal with the additional block length parameter in our setting.

-

(ii)

Proving tightness via a moment bound. After the reduction in step (i), we now deal with row-wise i.i.d. observations and the results in van der Vaart and Wellner, (1996) can be applied. Here, each ‘observation’ corresponds to a block of collections of block maxima mentioned in the previous step. The moment bound in Theorem 2.14.2 in the latter book allows to deduce tightness of the corresponding processes from controlling the bracketing numbers of certain function classes which map collections of block maxima to pieces in the sum defining .

-

(iii)

Bounding a certain bracketing number. The last step is based on some explicit lengthy calculations, which take the precise definition of the triangular arrays into account, and in particular the fact that the ‘observations’ are block maxima (with arguments similar to the one given in Remark 2.6 for the calculation of the limiting covariance).

2.2 Estimation in the case of unknown marginal c.d.f.s

The results in Section 2.1 are based on the assumption that the marginal c.d.f.s are known. In practice, this is not realistic and marginals are typically standardized by taking component-wise ranks of observed block maxima. For and block size , let

and consider observable pseudo-observations from defined as

The observable analog of the estimator in (2.1) is then given by

and we are interested in the asymptotic behavior of the associated empirical copula process, indexed by and block length scaling parameter , defined as

Subsequently, the process will be called extended empirical copula process based on sliding block maxima. Additional assumptions are needed for a corresponding weak convergence result.

Assumption 2.8.

For any , the th first order partial derivative of exists and is continuous on .

Recall that such an assumption is even needed for weak convergence of the classical empirical copula process based on i.i.d. observations from (Segers,, 2012). For completeness, define if . Following Bücher and Segers, (2014), we do not need differentiability of for finite . Instead, we will work with the functions

where and denotes the th canonical unit vector in . Note that is always defined and satisfies .

For the upcoming main theorem of this paper, we will need an additional assumption on the quality of convergence of to , which will eventually allow us to move from the known margins to the unknown margins case. Any of the following three conditions will be sufficient; the first two assumptions have also been considered in Bücher and Segers, (2014) (with in Part (a)), while the third part (a more refined version of (a)) is included specifically for the bias corrections worked out in Section 3.2, where (a) is typically not met.

Assumption 2.9 (Quality of convergence of to ).

-

(a)

A sequence of natural numbers with is said to satisfy if is relatively compact in (the space of continuous, real-valued functions on ).

-

(b)

For every , letting ,

-

(c)

A sequence of natural numbers with is said to satisfy if Assumption 2.2 holds, is uniformly Hölder-continuous of order , as and is relatively compact in .

We are now ready to state the main result of this section.

Theorem 2.10 (Functional weak convergence of the extended empirical copula process based on sliding block maxima).

If additionally Assumption 2.2 is met, then Theorem 2.10 shows that the uniform convergence rate of to is given by , where corresponds to the stochastic part, while is due to the deterministic difference between and . Assuming for simplicity that Assumption 2.2 holds with we find that the best possible convergence rate of is obtained by setting . In Section 3 we will show that this rate can in fact be improved by combining estimators for several values of . Establishing the asymptotic properties of those estimators will require the full power of Theorem 2.10, including the process convergence uniformly over the block length parameter .

2.3 A comparison of the asymptotic variances based on disjoint and sliding block maxima

The asymptotic variance of the sliding blocks version of the empirical copula with known and estimated margins will be shown to be less than or equal to the asymptotic variance of the corresponding disjoint blocks versions. Since the asymptotic bias of both approaches is the same, this suggests that the sliding blocks estimator, when available, should always be used instead of the disjoint blocks estimator.

Theorem 2.12.

Suppose is an extreme value copula satisfying Assumption 2.8. Let denote the weak limit of the empirical copula process based on sliding block maxima defined in (2.2). Similarly, recall as defined in Remark 2.5 and let

denote the weak limit of the corresponding disjoint blocks version (Theorem 3.1 in Bücher and Segers,, 2014). Then, for any ,

and

| (2.3) |

where denotes the Loewner-ordering between symmetric matrices.

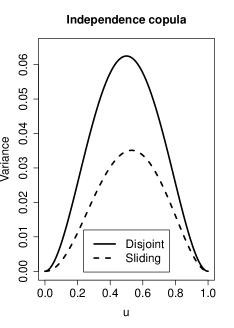

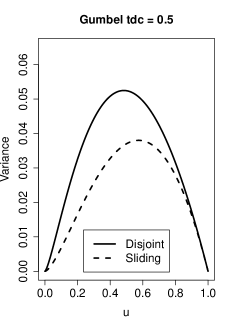

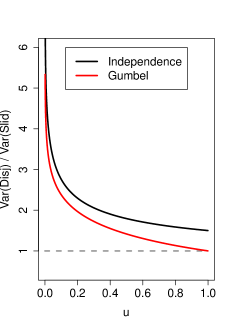

The proof is given in Section A.3. In Figure 2 we depict and , for with , for the Gumbel–Hougaard Copula in (4.1) with shape parameter and . Note that when , the Gumbel–Hougaard Copula degenerates to the independence copula on , i.e., while results in a tail dependence coefficient of . The analytical expressions of and for the Gumbel–Hougaard Copula are presented in Section A.4 in the supplementary material Zou et al., (2019). The difference between and is seen to be substantial, in particular for small values of .

As a consequence of the previous result, whenever is a continuous and linear (real-valued) functional on the space of continuous functions on (e.g., the Hadamard derivative of a functional at , tangentially to the subspace of continuous functions), then

Indeed, by the Riesz representation theorem (Dudley,, 2002, Theorem 7.4.1), for some finite signed Borel measure on , whence

The claim then follows by measure-theoretic induction. Examples of interesting functionals can for instance be found in Genest and Segers, (2010), Section 3, which comprise Blomqvist’s beta, Spearman’s footrule, Spearman’s rho and Gini’s gamma.

3 Applications of the functional weak convergence

The functional weak convergence result in Theorem 2.10 can be applied to large variety of statistical problems. Classical applications include the derivation of the asymptotic behavior of estimators for the Pickands dependence function, see, e.g., Section 3.3 in Bücher and Segers, (2014). Throughout this section, we discuss applications that explicitly make use of the fact that we allow for various block sizes, allowing one to aggregate over those block sizes, to derive bias reduced estimators or to even estimate second order characteristics.

Despite not being necessary for the bias correction to work, many of the results in this section can be formulated in a convenient explicit way under the assumption of a third order condition.

Assumption 3.1 (Third order condition).

Assumption 2.2 holds and there exists a regularly varying function with coefficient of regular variation and a (necessarily continuous) non-null function on , not a multiple of , such that, uniformly in ,

| (3.1) |

Under the additional assumption that is an i.i.d. sequence, it can be proved that in the above condition must be regularly varying under mild additional assumptions (it can hence be removed from the assumption).

Lemma 3.2.

Next we discuss an additional property of the function from Assumption 2.2 which allows to quantify the speed of convergence of

| (3.2) |

(note that convergence to zero of this difference follows from regular variation of ). This difference will be important in later parts of the manuscript as it will appear in several bounds that are related to bias correction.

Lemma 3.3.

Assume that is compact and that there exists a non-negative function with such that, uniformly in ,

| (3.3) |

for any , where . Under Assumption 3.1 we have, uniformly in ,

In the iid case, Equation (3.3) obviously holds with . The next result provides a bound on the difference in (3.3) under mixing conditions.

Lemma 3.4.

3.1 Improved estimation by aggregation over block lengths

Since the functional weak convergence result in Theorem 2.10 involves a scaling parameter for the block length, we may easily analyse estimators for which are based on aggregating over several blocks. More formally, we consider the following general construction: for a set of block length parameters and a set of weights satisfying for all , let

To derive the asymptotic distribution of this weighted aggregated estimator, we make the following assumption on the tuple .

Assumption 3.5.

Let denote the sequence from Assumption 2.3. For some closed interval of positive length, we have

and the weights satisfy uniformly over for some continuous on with .

For instance, given a continuous function on that integrates to unity, we may choose the weights .

Proposition 3.6.

Note that the asymptotic results in Theorem 2.10 imply that the asymptotic variance of is proportional to . For simplicity ignoring the dependence between for different , this motivates the choice , which is in fact the solution to the minimization problem ‘minimize over with ’. The corresponding function is , with a normalizing constant such that the integral over is one. Despite this being a crude approximation since will be strongly dependent for different values of , it performs reasonably well in simulations where we will see that in many cases it leads to an improvement in MSE. An alternative approach to choosing would consist of estimating the entire variance-covariance matrix of and minimize a corresponding quadratic form of . We leave a detailed investigation of this question to future research.

3.2 Bias correction

Before discussing the general methodology in this section, we comment on the notion of bias of as an estimator for the attractor copula . The difference can be naturally decomposed into two terms

The first term captures the stochastic part of and may be rewritten as

Recall that, by Theorem 2.10, converges to a centered Gaussian process. For this reason, throughout the remaining part of this paper, when discussing the bias of an estimator, we mostly concentrate on (versions of) the deterministic sequence , which might in fact be of larger order than and which we will call the approximation part of the bias. Note that this is a slight abuse of terminology as we never prove results about ; however, a similar approach has also been taken in Fougères et al., (2015).

Regarding the approximation part of the bias, note that the fundamental Assumption 2.1 only guarantees that . Under the second order condition from Assumption 2.2 however, we obtain a hold on both the size and the direction of the bias:

| (3.4) | ||||

It is the main purpose of this section to exploit the generality of Theorem 2.10 to construct estimators for with a smaller order approximation bias.

More precisely, in the current Section 3.2, we present three approaches on how to reduce the bias under either the preliminary assumption that the second order coefficient is known, or that an estimate is available. In the next section, we will then discuss how to obtain such an estimate. For the remaining parts of Section 3, suppose that the third order condition from Assumption 3.1 is met, which implies the expansion

| (3.5) |

for the approximation part of the bias of .

3.2.1 Naive bias-corrected estimator

The expansion in (3.5) implies that, assuming for simplicity for the moment,

This suggests that the leading bias term in Expansion (3.5) can be estimated by the plug-in version where is an integer and we set in the expansion above. Subtracting this estimated bias from the estimator naturally leads to the following naive bias-corrected estimator

Note that this estimator is infeasible in practice since is unknown. A feasible estimator denoted by , can be obtained by replacing with an estimator . In the result below we quantify the impact of such a replacement under the mild condition , estimators satisfying this assumption will be presented in Section 3.3 below. Furthermore, it is worthwhile to mention that as can be verified by a simple calculation.

Assuming that for some fixed value , the asymptotic distribution of this estimator is as follows.

Proposition 3.7.

3.2.2 Improving the naive bias-corrected estimator by aggregation

The naive bias-corrected estimator is fairly simple since it only considers two block length parameters and . One way to improve this estimator is to consider aggregation over different block lengths; an approach that was shown to work well in Fougères et al., (2015) for estimating the stable tail dependence function. Many kinds of aggregation are possible, but for the sake of brevity we will restrict our attention to the following version inspired by Section 3.1 (which works well in finite-sample settings as demonstrated in Section 4)

Here and are assumed to satisfy Assumption 3.5. Similarly to the discussion in Section 3.2.1, let denote a feasible version of , with replaced by .

3.2.3 Regression-based bias correction

A more sophisticated, regression-based estimator (inspired by Beirlant et al.,, 2016, where the POT-case is tackled) can be motivated by the following consequence of the expansion in (3.5) and the regular variation of :

| (3.7) |

for all , where . Letting for suitable values (to be determined below) we find that

| (3.8) |

where the remainder contains both the stochastic error and the deterministic error from expansion (3.7). This motivates the following weighted least square estimator for and :

| (3.9) |

where and are as in Section 3.1 with the additional assumption that the weights are non-negative. Note that, since the parameter is fixed in the above minimization problem, the value of does in fact not depend on and hence we do not need to consider as an index in . Similarly to the discussion in Section 3.2.1, let denote a feasible version of , where is replaced by .

Assuming that contains sufficiently many elements so that the inverse matrix in the next display exists, the minimization problem above has the unique closed-form solution

where we defined . To state the asymptotics of this estimator, define

and

Proposition 3.9.

Let any of the sufficient conditions in Theorem 2.10 be met. Additionally, suppose that Assumption 3.1 is met and that satisfies Assumption 3.5. Then, in ,

where the bias term satisfies

with as defined in (3.6). Moreover,

in , where the bias term satisfies

and the processes involving converge jointly. If moreover , then we have, uniformly in

3.3 Estimating the second order parameter

Estimators for can be obtained by considering the expansion in (3.7). A simple estimator can be based on the observation that, for any with and any ,

Letting denote a block length parameter (typically chosen of smaller order than the block length used for estimating , whence the different notation here), this suggests the following naive estimator for :

Proposition 3.10.

While the estimator defined above is easy to motivate and analyze theoretically, we found in simulations that it does not work well when the sample size is small or even moderate (up to ). This motivated us to consider alternative estimators by treating in equation (3.8) as unknown. Specifically, we considered estimators of the form

| (3.10) |

where and are as in Section 3.1 with the additional assumption that the weights are non-negative. This lead to some improvement in performance compared to using , but still did not lead to very satisfactory results, prompting us to refine the estimator even further.

To gain an intuitive understanding of the shortcomings of as plug-in estimators for bias correction, we take a closer look at the properties of the quantity

which is simply the naive bias-corrected estimator from Section 3.2.1 but with plugged in instead of the true . We next take a close look at the bias and variance of this ‘estimator’ as a function of under the third order condition from Assumption 3.1. The leading part of the bias is approximately given by

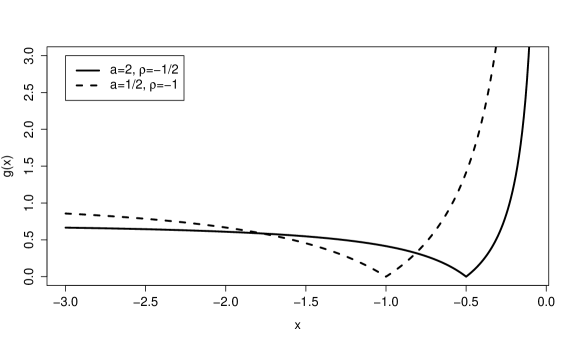

A close analysis reveals that is decreasing on with if and if and increasing on with for , see Figure 3 for a picture of the graph for two specific choices of . Hence the leading bias will never be increased compared to the original estimator if is smaller than , but can increase dramatically if , especially if gets close to zero. Similarly, the asymptotic variance of the ‘bias correction part’ can be found to be a strictly increasing function of .

In summary, the above findings suggest a very asymmetric behavior in the performance of the naive bias corrected estimator with respect to values of that are too large or too small relative to the true parameter . This apparent asymmetry is not taken into account in the minimization problem (3.10). It thus seems natural to introduce an additional penalty term which discourages the estimator of from being too close to . We hence consider the estimator

where are fixed constants (in the simulations, we choose and ), denotes a penalty parameter, and

To motivate the factor in the penalty, note that, provided this factor is non-zero, an equivalent representation for the corresponding minimization problem is to minimize

Since the minimal achievable value of the ratio equals , this automatically provides a scaling for the penalty part and makes this choice attractive in practice. Finally, observe that the procedure described above produces an estimator of for each value of . We hence propose to further aggregate estimators across different values of for some finite set to obtain the aggregated estimator

Next we prove consistency of the estimators defined above.

Proposition 3.11.

Suppose that Assumption 2.2 is met with and let be an increasing sequence of integers such that any of the sufficient conditions in Theorem 2.10 is met for that sequence. Further, assume that , that Assumption 3.5 is met with instead of , and that for all . Then, for any compact and any fixed ,

Also, for any finite set .

4 Examples and finite-sample properties

The proposed estimators will be compared in a simulation study. We begin by providing some details on several examples that will be used in the simulations. For the sake of simplicity, we only consider the case below. For a generic , see Examples D.1 and D.2 in the supplementary material Zou et al., (2019).

4.1 Examples

Example 4.1 (-Copula, iid case).

For degrees of freedom and correlation , the -copula is defined, for , as

where , is a correlation matrix with off-diagonal element , and is the cumulative distribution function of a standard univariate -distribution with degrees of freedom . Let and be the first-order and the second-order POT-type limits associated to . More specifically,

and is defined in Section 4 and 4.1 of Fougères et al., (2015). Recall that Let

By Theorem 2.6 of Bücher et al., (2019), Assumption 2.2 holds for with . Specifically, when , we have , , and

when , we have , , and

when , we have , , and

Example 4.2 (Outer-power transformation of Clayton Copula, iid case).

For and , the outer-power transformation of a Clayton Copula is defined as

which is to be interpreted as zero if . By Theorem 4.1 in Charpentier and Segers, (2009), is in the copula domain of attraction of the Gumbel–Hougaard Copula with shape parameter , defined by

| (4.1) |

which is again to be interpreted as zero if . Further, by Proposition 4.3 of Bücher and Segers, (2014), Assumption 2.2 is met with , , and

where, letting and ,

Example 4.3 (Moving-Maximum-Process).

Let denote a copula and let denote an iid sequence from . Fix and let denote nonnegative constants satisfying

The moving maximum process of order is defined as

with the convention that for . As suggested by the notation, the random variables are uniformly distributed on , whence a model with arbitrary continuous margins can easily be obtained by considering for some strictly increasing (quantile) function .

Assume that the copula is in the (iid) copula domain of attraction of an extreme-value copula , that is, for any ,

Note that is the copula of the componentwise block maximum of size , based on the sequence .

As a consequence of Proposition 4.1 in Bücher and Segers, (2014), if denotes the copula of the componentwise block maximum of size based on the sequence , then

as well, i.e., Assumption 2.1 is met. We prove in the Appendix that if Assumption 2.2 is met for (denote the auxiliary function by and ), then it is also met for provided that , with the same auxiliary functions. In case additional technical assumptions are needed and the functions and might differ. Details in the general case are omitted for the sake of brevity.

4.2 Finite-sample properties

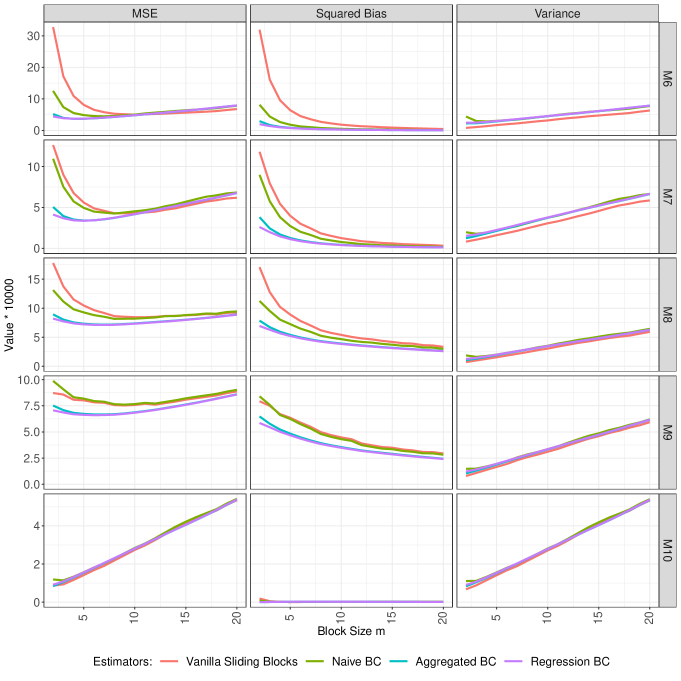

In this section we compare the estimators for introduced in the previous section by means of Monte-Carlo simulations. We focus on the case below; respective results in higher dimensions are quite similar and do not reveal additional deep insights, see the cases treated in Section D.1 in the supplementary material Zou et al., (2019). Results for all estimators are reported as follows: each estimator is computed for all values and block size (except for the aggregated versions, for which we specify the set of block length parameters below). Squared bias, variance and MSE of each estimator and in each point for sample size was estimated based on Monte Carlo replications. For the sake of brevity we only report summary results which correspond to taking averages of the squared bias, MSE and variance over all values . We present results on the following models.

-

(M1)

iid realizations from an Outer Power Clayton Copula with .

-

(M2)

A moving maximum process based on the outer Power Clayton Copula with and .

-

(M3)

iid realizations from a -Copula with .

-

(M4)

A moving maximum process based on a -Copula with and .

-

(M5)

A moving maximum process based on a -Copula with and .

For the sake of brevity, we do not include an iid version of Model (M5) because the findings are very similar to the time series case. Further note that we also investigated other parameter combinations, but chose to only present results for the above models as they provide, to a large extent, a representative subset of the results.

Following the heuristics after Proposition 3.6, weights are always chosen as

| (4.2) |

with block length sets as specified below, possibly depending on the specific estimator.

4.2.1 Comparison of estimators without bias correction

We first focus on the performance of three estimators that do not involve any bias correction:

- •

-

•

the sliding blocks estimator from Section 2.2;

- •

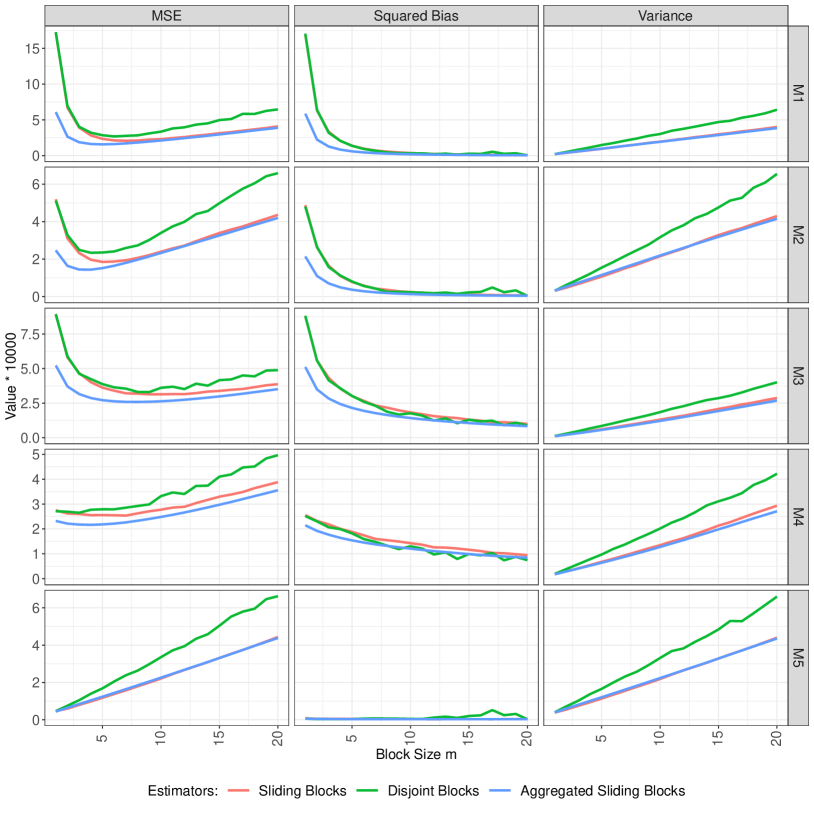

The respective results corresponding to Models (M1)-(M5) are shown in Figure 4. As predicted by the theory, the variance curves are linear in , with the disjoints blocks estimator always exhibiting the largest variance, while the variances of the aggregated and vanilla version of the sliding blocks estimator are both smaller and similar to each other. In terms of bias, the disjoint and vanilla sliding blocks estimators and show a very similar behavior, with only some smaller deviations (in particular visible for larger block sizes) which may possibly be explained by the fact that the disjoint blocks estimator does not make use of all observations in case the block length is not a divisor of the sample size . The aggregated sliding blocks estimator typically has the smallest bias among the three competitors. Finally, in terms of MSE, the aggregated sliding blocks estimator again shows the uniformly best performance. Except for Model (M5), the global minimum of the MSE-curve for is substantially smaller than the minima for the other two estimators.

When comparing the five models, we observe a qualitatively similar behavior for models (M1)-(M4), with the bias typically being larger in the iid case than in the time series setting. Model (M5) however exhibits little to no bias for all block sizes under consideration, even for . As a consequence, at their minimal MSE, the three estimators yield comparably good results. The observant reader might also note that the bias in the serially dependent models seems to be smaller than in the iid case. Intuitively, this is due to the fact that realizations from moving maximum processes are already based on maxima and thus it can be expected that their dependence structure is closer to that of a ‘limiting’ max-stable model described by .

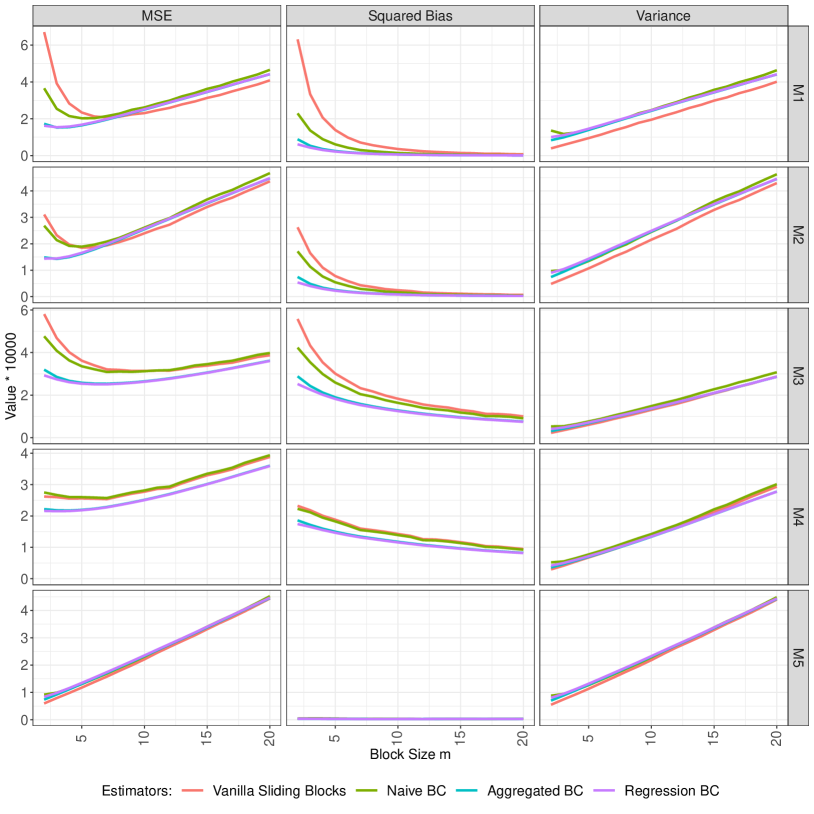

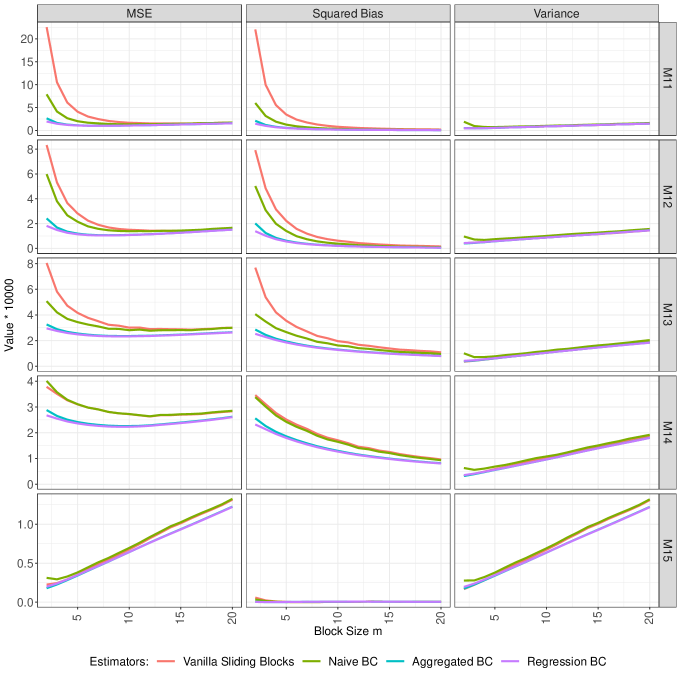

4.2.2 Comparison of bias corrected estimators

In this section, three bias corrected estimators for the vanilla sliding blocks estimator are compared with itself. In all cases, the second order parameter is estimated through , with the parameters of that estimator set to and weights as in (4.2). We consider the following estimators:

-

•

The naive bias corrected estimator with and .

-

•

The aggregated naive bias corrected estimator with (where is on the x-axis) and with weights as in (4.2).

- •

The choice of small block sizes for the bias correction, in particular , is motivated by the fact that this choice leads to the best performance in the simulations we tried. Similar observations were made in Fougères et al., (2015) who recommend using a very large value for the threshold in the POT setting.

The results are presented in Figure 5. We observe that the naive bias corrected estimator exhibits, at each fixed block size, a slightly larger variance and a slightly smaller squared bias than the plain sliding blocks empirical copula. In terms of MSE, no universal statement regarding the ordering between the two estimators can be made. Their minimal MSEs (for each separate model, over all block length parameters) are however quite similar. We further find that aggregating the naive bias-corrected estimator leads to substantial improvements for small values of and no major impact for larger values of . This is similar to the findings in the previous section. Compared with the vanilla sliding block estimator, the aggregated bias corrected estimator shows much less sensitivity to the parameter in Model (M1)-(M3) where there is a substantial bias. In Model (M5), where the bias is negligible compared to the variance, attempts to correct the bias introduce a bit of variance leading to a slight increase in MSE for all block sizes. Finally, the aggregated naive and regression-based bias corrected estimators show very similar performance.

Based on the simulation results, we would recommend using the aggregated bias corrected estimator among all bias corrected estimators since it leads to better results than the naive estimator, is reasonably fast to compute (see Section D.2), and is simpler to implement than the regression-based estimator. At the same time, it is less sensitive to the choice of the block size parameter compared to the estimator without bias correction.

Acknowledgments

The authors would like to thank Sebastian Engelke and Chen Zhou for fruitful discussions. We are also grateful to the Associate Editor and three anonymous Referees for detailed feedback which helped to improve the presentation of our results.

This research has been supported by the Collaborative Research Center “Statistical modeling of nonlinear dynamic processes” (SFB 823) of the German Research Foundation and by a Discovery Grant from the Natural Sciences and Engineering Research Council of Canada, which is gratefully acknowledged. Parts of this paper were written when A. Bücher was a post doctoral researcher at Ruhr-Universität Bochum.

[id=suppA] \stitleSupplement to: “Multiple block sizes and overlapping blocks for multivariate time series extremes” \slink[doi]COMPLETED BY THE TYPESETTER \sdatatype.pdf \sdescriptionThe supplement contains the proofs for the results in this paper.

References

- Balkema and Resnick, (1977) Balkema, A. A. and Resnick, S. I. (1977). Max-infinite divisibility. J. Appl. Probability, 14(2):309–319.

- Beirlant et al., (2016) Beirlant, J., Escobar-Bach, M., Goegebeur, Y., and Guillou, A. (2016). Bias-corrected estimation of stable tail dependence function. J. Multivariate Anal., 143:453–466.

- Beirlant et al., (2004) Beirlant, J., Goegebeur, Y., Segers, J., and Teugels, J. (2004). Statistics of extremes: Theory and Applications. Wiley Series in Probability and Statistics. John Wiley & Sons Ltd., Chichester.

- Berbee, (1979) Berbee, H. C. (1979). Random walks with stationary increments and renewal theory. MC Tracts, 112:1–223.

- Berghaus and Bücher, (2018) Berghaus, B. and Bücher, A. (2018). Weak convergence of a pseudo maximum likelihood estimator for the extremal index. Ann. Statist., 46(5):2307–2335.

- Bücher and Segers, (2014) Bücher, A. and Segers, J. (2014). Extreme value copula estimation based on block maxima of a multivariate stationary time series. Extremes, 17(3):495–528.

- (7) Bücher, A. and Segers, J. (2018a). Inference for heavy tailed stationary time series based on sliding blocks. Electron. J. Statist., 12(1):1098–1125.

- (8) Bücher, A. and Segers, J. (2018b). Maximum likelihood estimation for the Fréchet distribution based on block maxima extracted from a time series. Bernoulli, 24(2):1427–1462.

- Bücher and Volgushev, (2013) Bücher, A. and Volgushev, S. (2013). Empirical and sequential empirical copula processes under serial dependence. Journal of Multivariate Analysis, 119:61–70.

- Bücher et al., (2019) Bücher, A., Volgushev, S., and Zou, N. (2019). On second order conditions in the multivariate block maxima and peak over threshold method. J. Multivariate Anal., 173:604–619.

- Can et al., (2015) Can, S. U., Einmahl, J. H. J., Khmaladze, E. V., and Laeven, R. J. A. (2015). Asymptotically distribution-free goodness-of-fit testing for tail copulas. Ann. Statist., 43(2):878–902.

- Capéraà et al., (1997) Capéraà, P., Fougères, A.-L., and Genest, C. (1997). A nonparametric estimation procedure for bivariate extreme value copulas. Biometrika, 84(3):567–577.

- Charpentier and Segers, (2009) Charpentier, A. and Segers, J. (2009). Tails of multivariate archimedean copulas. Journal of Multivariate Analysis, 100(7):1521–1537.

- de Haan and Ferreira, (2006) de Haan, L. and Ferreira, A. (2006). Extreme value theory: an introduction. Springer.

- de Haan et al., (2016) de Haan, L., Mercadier, C., and Zhou, C. (2016). Adapting extreme value statistics to financial time series: dealing with bias and serial dependence. Finance Stoch., 20(2):321–354.

- de Haan and Resnick, (1977) de Haan, L. and Resnick, S. I. (1977). Limit theory for multivariate sample extremes. Z. Wahrscheinlichkeitstheorie und Verw. Gebiete, 40(4):317–337.

- Dehling and Philipp, (2002) Dehling, H. and Philipp, W. (2002). Empirical process techniques for dependent data. In Empirical process techniques for dependent data, pages 3–113. Springer.

- Dombry, (2015) Dombry, C. (2015). Existence and consistency of the maximum likelihood estimators for the extreme value index within the block maxima framework. Bernoulli, 21(1):420–436.

- Dombry and Ferreira, (2017) Dombry, C. and Ferreira, A. (2017). Maximum likelihood estimators based on the block maxima method. Bernoulli. Forthcoming, arXiv:1705.00465.

- Doukhan et al., (1995) Doukhan, P., Massart, P., and Rio, E. (1995). Invariance principles for absolutely regular empirical processes. In Annales de l’IHP Probabilités et statistiques, volume 31, pages 393–427. Elsevier.

- Drees and Rootzén, (2010) Drees, H. and Rootzén, H. (2010). Limit theorems for empirical processes of cluster functionals. Ann. Statist., 38(4):2145–2186.

- Dudley, (2002) Dudley, R. M. (2002). Real analysis and probability, volume 74 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge. Revised reprint of the 1989 original.

- Einmahl et al., (2016) Einmahl, J. H. J., de Haan, L., and Zhou, C. (2016). Statistics of heteroscedastic extremes. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 78(1):31–51.

- Ferreira and de Haan, (2015) Ferreira, A. and de Haan, L. (2015). On the block maxima method in extreme value theory: PWM estimators. Ann. Statist., 43(1):276–298.

- Fougères et al., (2015) Fougères, A.-L., de Haan, L., and Mercadier, C. (2015). Bias correction in multivariate extremes. Ann. Statist., 43(2):903–934.

- Genest and Segers, (2009) Genest, C. and Segers, J. (2009). Rank-based inference for bivariate extreme-value copulas. Ann. Statist., 37(5B):2990–3022.

- Genest and Segers, (2010) Genest, C. and Segers, J. (2010). On the covariance of the asymptotic empirical copula process. J. Multivariate Anal., 101(8):1837–1845.

- Gudendorf and Segers, (2010) Gudendorf, G. and Segers, J. (2010). Extreme-value copulas. In Jaworski, P., Durante, F., Härdle, W. K., and Rychlik, T., editors, Copula Theory and Its Applications, pages 127–145, Berlin, Heidelberg. Springer Berlin Heidelberg.

- Gumbel, (1958) Gumbel, E. J. (1958). Statistics of extremes. Columbia University Press, New York.

- Hsing, (1989) Hsing, T. (1989). Extreme value theory for multivariate stationary sequences. Journal of Multivariate Analysis, 29(2):274–291.

- Huang, (1992) Huang, X. (1992). Statistics of bivariate extreme values. PhD thesis, Tinbergen Institute Research Series, Netherlands.

- Hüsler, (1990) Hüsler, J. (1990). Multivariate extreme values in stationary random sequences. Stochastic Processes and their Applications, 35(1):99 – 108.

- Leadbetter, (1983) Leadbetter, M. R. (1983). Extremes and local dependence in stationary sequences. Probability Theory and Related Fields, 65(2):291–306.

- Naveau et al., (2009) Naveau, P., Guillou, A., Cooley, D., and Diebolt, J. (2009). Modelling pairwise dependence of maxima in space. Biometrika, 96(1):1–17.

- Northrop, (2015) Northrop, P. J. (2015). An efficient semiparametric maxima estimator of the extremal index. Extremes, 18(4):585–603.

- Pickands, (1981) Pickands, III, J. (1981). Multivariate extreme value distributions. In Proceedings of the 43rd session of the International Statistical Institute, Vol. 2 (Buenos Aires, 1981), volume 49, pages 859–878, 894–902. With a discussion.

- Resnick, (1987) Resnick, S. I. (1987). Extreme values, regular variation, and point processes, volume 4 of Applied Probability. A Series of the Applied Probability Trust. Springer-Verlag, New York.

- Robert et al., (2009) Robert, C. Y., Segers, J., and Ferro, C. A. T. (2009). A sliding blocks estimator for the extremal index. Electron. J. Stat., 3:993–1020.

- Schmidt and Stadtmüller, (2006) Schmidt, R. and Stadtmüller, U. (2006). Non-parametric estimation of tail dependence. Scand. J. Statist., 33(2):307–335.

- Segers, (2012) Segers, J. (2012). Asymptotics of empirical copula processes under non-restrictive smoothness assumptions. Bernoulli, 18(3):764–782.

- van der Vaart and Wellner, (1996) van der Vaart, A. W. and Wellner, J. A. (1996). Weak convergence and empirical processes. Springer Series in Statistics. Springer-Verlag, New York. With applications to statistics.

- Zou et al., (2019) Zou, N., Volgushev, S., and Bücher, A. (2019). Supplement to “Multiple block sizes and overlapping blocks for multivariate time series extremes”.

SUPPLEMENT TO THE PAPER:

“MULTIPLE BLOCK SIZES AND OVERLAPPING BLOCKS FOR

MULTIVARIATE TIME SERIES EXTREMES”

By Nan Zou, Stanislav Volgushev and Axel Bücher

University of Toronto and Heinrich-Heine-Universität Düsseldorf

Proofs from the main paper as well as additional simulations are provided. Appendix A contains proofs for Section 2, Appendix B those for Section 3, and Appendix C those for Section 4.1. Additional simulation results are presented in Appendix D.

Appendix A Proofs for Section 2

A.1 Proofs for Section 2.1

To keep things self-contained, we begin by repeating the proof of Theorem 2.4 from the main text.

Proof of Theorem 2.4.

Recall , and

where with . Below we provide technical details for the following steps:

-

(i)

In Lemma A.1, we will prove that . Hence it suffices to prove weak convergence of .

-

(ii)

In Lemma A.2 we will show that is asymptotically uniformly equicontinuous in probability with respect to the -norm on .

-

(iii)

We will prove in Lemma A.5 that the finite-dimensional distributions of converge weakly to those of .

Weak convergence of and hence the theorem then follows by combining (i)-(iii). ∎

A.1.1 Proof of Step (i)

Lemma A.1.

Under Assumption 2.3,

A.1.2 Proof of Step (ii): asymptotic equicontinuity.

Lemma A.2.

Under the conditions of Theorem 2.4, is asymptotically uniformly equicontinuous in probability with respect to the -norm on .

Proof. The proof is based on a blocking technique. For , let be defined by its entries

In words, denotes the block maximum of the observations starting at time with block length , in the th coordinate. Let (to be interpreted as a maximal block size) and let . For simplicity, we shall assume that and are integers. For , let

such that is a partition of . By the coupling lemma in Berbee, (1979) and Doukhan et al., (1995), we can construct inductively a triangular array , such that

| (A.1) | ||||

For and , let denote the ’th entry of ; note that . Further, let denote the ’th column of , and let

Finally, for , let

Later we will show that part (ii) of (A.1) implies

| (A.2) |

Hence it suffices to prove asymptotic equicontinuity of . To this end observe the representation

| (A.3) |

where and are stochastic processes on defined by

where

To prove asymptotic equicontinuity of it suffices to prove asymptotic equicontinuity and boundedness in probability of and (note that by assumption the set is bounded and bounded away from zero). Since the distribution of both terms is the same, we will focus on . For and , let be defined as

By (i) and (iii) of (A.1) and stationarity, is a row-wise i.i.d. triangular array. Let denote the empirical process corresponding to those observations. Then

where is defined by

| (A.4) |

For , consider the sequences of functions classes

Since for all and ,

we have, for sufficiently large so that ,

and similarly

Hence, the equicontinuity of will follow if we can prove that

| (A.5) |

while the corresponding boundedness in probability will follow from

| (A.6) |

To prove (A.5) and (A.6) we shall apply Theorem 2.14.2 in van der Vaart and Wellner, (1996) to the function classes , and the empirical process . Let denote the norm

Let be an envelope function for and note that is an envelope function for . Define

where denotes the bracketing number, see Definition 2.1.6 in van der Vaart and Wellner, (1996). Note that

| (A.7) |

By the middle part of Theorem 2.14.2 in van der Vaart and Wellner, (1996), if there exists such that for every ,

then

| (A.8) |

We begin by observing that, for any as defined in (A.4), we have

for all sufficiently large (using that , eventually). Hence, we can choose as an envelope function of . Later we shall prove that there exist such that

| (A.9) |

and, for all and all sufficiently large (such that ),

| (A.10) |

Now (A.8) together with some simple computations utilizing (A.7), (A.9) and (A.10) shows that for

For fixed the term is bounded away from uniformly in while as . This implies (A.5).

The bound in (A.6) follows by similar but simpler arguments utilizing the last part of Theorem 2.14.2 in van der Vaart and Wellner, (1996).

Proof of (A.2). By (i) of (A.1), we have . Hence,

Now, for fixed , since , we have

Similarly,

By (ii) of (A.1) and Assumption 2.3 (iii),

The result follows by Markov’s Inequality.

Further, is increasing in (coordinate-wise) and and decreasing in . Likewise, is increasing in (coordinate-wise) and and decreasing in . Subsequently, let . Lemma A.6 implies that there exist such that, for all sufficiently large , all and all with ,

Let and . Then we have, for all and ,

| (A.13) |

To simplify notation, we subsequently write . Begin by considering the case . For and define

Then we have, for sufficiently large ,

| (A.14) |

Let , , , , and

Then and are the corners of the cuboid in . For all , by (A.1.2), there exists such that . For such and , we have by the monotonicity properties of and . Therefore, is covered by the collection of brackets

| (A.15) |

By construction and by (A.13) [note that ] we have, for any ,

i.e., the collection in (A.15) provides a cover of by brackets. This implies

| (A.16) |

Next consider the case . For the constant from Lemma A.7 let . For , let , , and . Then is covered by the collection of brackets

| (A.17) |

By Lemma A.7, for sufficiently large ,

Hence, (A.17) is a collection of -brackets that covers . Notice the number of brackets in the collection (A.17) is bounded by , for sufficiently large . Combining this with (A.16) we have proved that for constants depending on only we have, for any (note that for constants can be absorbed into powers of by changing ),

Proof of (A.10). Suppose and . Then either or or . Now we discuss case by case. Begin by observing that

As a consequence,

| (A.18) | ||||

By Lemma A.6, when , we obtain the upper bound

| (A.19) |

When , select such that and . By (A.1.2) and Lemma A.6,

| (A.20) |

where the last inequality uses the fact that . Finally, by Lemma A.7, when ,

| (A.21) |

A combination of (A.19), (A.1.2), and (A.21) gives (A.10) where the constant can be dropped at the cost of changing the power of

A.1.3 Proof of Step (iii): fidi convergence

We begin by stating and proving two technical results.

Lemma A.3.

Proof of Lemma A.3.

Let be an arbitrary sequence in , and be an arbitrary sequence in . Lemma 2.1 of Leadbetter, (1983), together with a straightforward extension to multivariate time series, shows that if there exists a sequence such that

| (A.23) |

then we have

| (A.24) |

and

| (A.25) |

See also Lemma 4.1 of Hsing, (1989). Let . By (A.22) and Assumption 2.3(i),(ii), (A.23) holds. Now plug in . By (A.22) and (A.24),

Then plug in . By (A.22) and (A.25),

Hence we have shown (i) and (ii) of Lemma A.3. Finally, by part (i) and Assumption 2.1,

| (A.26) | ||||

and, on the other hand, by part (ii),

This implies (iii). ∎

Lemma A.4.

Proof of Lemma A.4.

For let

such that

| (A.27) |

where is defined as

Now, for sufficiently large ,

All but the first term on the right hand side of the previous equation vanish. Indeed

and, by Assumption 2.3(ii), ,

As a result,

| (A.28) |

Similarly,

| (A.29) |

and

| (A.30) |

Suppose . Notice

| (A.31) |

For and , let . Since we can write

| (A.32) | ||||

where

Now we seek to approximate by with a clipping technique; see also the proof of Lemma 5.1 of Bücher and Segers, 2018a . Let and define

be the clipped events; note that . First we show that clipping ‘does not hurt’. Applying (ii) of Lemma A.3 twice gives

| (A.33) | ||||

Similarly,

| (A.34) |

Now we apply the clipping technique. First, by (A.33) and (A.34),

| (A.35) | ||||

Second, by (A.33), (A.34), and since by Assumption 2.3(ii),

| (A.36) |

Next, similarly as in (A.26), by (i) and (iii) of Lemma A.3, Assumption 2.1 and continuity of ,

| (A.37) | ||||

Similarly,

| (A.38) |

By (A.32), (A.35), (A.36), (A.37), and (A.38), for ,

| (A.39) |

Similarly, for ,

| (A.40) | ||||

and for ,

| (A.41) | ||||

By Assumption 2.1 and the stationarity of ,

| (A.42) |

Recall (A.27). Now apply the Dominated Convergence Theorem to the right hand side of (A.28), (A.29), and (A.30). By (A.31), (A.39), (A.40), (A.41), (A.42), and (iii) of Lemma A.3, we get

with is defined in Theorem 2.4. ∎

Lemma A.5.

Proof of Lemma A.5.

We apply a big-blocks-small-blocks technique. Assume without loss of generality that is an integer (otherwise enlarge , this does not change any of the arguments). For chosen below, the block size of the big blocks will be proportional to , while the small blocks will have size proportional to . By Assumption 2.3(i) and (iv), we have and for some . Hence, there exists , which can be chosen to be integer-valued, such that

| (A.43) |

| (A.44) |

| (A.45) |

Let and for simplicity assume that is an integer. For consider big blocks

and small blocks

For , let

We may then write

We will now show that is negligible. Indeed, let

then, by stationarity,

Notice that . Hence, since by (A.44),

Moreover, for , by Lemma 3.9 in Dehling and Philipp, (2002),

Hence, since by (A.44) and by Assumption 2.3 (ii),

Therefore,

| (A.46) |

and since , we obtain that as asserted.

Next, we show finite-dimensional convergence of , i.e., for all in and all in ,

By the Cramér-Wold device, it suffices to show that for all ,

Recall

| (A.47) |

Let

By (A.46) and (A.47), to show the finite dimensional convergence, it suffices to show that

| (A.48) |

Let

and note that In addition, for , and are based on observations that are at least observations apart. As a consequence, and are asymptotically independent. Next, let and denote the characteristic functions of and , respectively. By the reasoning in p. 515 of Bücher and Segers, (2014) and (A.45), for any fixed ,

| (A.49) |

Let denote row-wise independent random variables with having the same distribution as for . Then is the characteristic function of . If we can prove that , then will converge the the characteristic function of , and then (A.49) will imply (A.48).

Now we apply the Lyapunov Central Limit Theorem to . By Lemma A.4, applied with and replaced by and , respectively (note that since and that ) is the length of a big block), we obtain that

| (A.50) | ||||

Now, if , then and we are left with the case . Let with from Assumption 2.3 (iv). By (A.43), . By stationarity,

By the Lyapunov Central Limit Theorem,

Since by (A.50), we obtain (A.48) and the proof is finished. ∎

A.1.4 Further technical Lemmas for the proof of Theorem 2.4

Throughout this section assume that the conditions of Theorem 2.4 hold. Recall that the functions are defined in (A.11), (A.12).

Lemma A.6.

Let denote an arbitrary closed interval in . There exist and , depending on the mixing coefficients , , the interval and the dimension only, such that, for all , all with and all , we have

Proof of Lemma A.6.

Write and . It is sufficient to consider the case . Recall that and . Then, since is decreasing in and increasing in and since for sufficiently large , we have

| (A.51) | ||||

where

For note that, by (A.1) (i),

| (A.52) | ||||

In what follows, define . Then

| (A.53) | ||||

Recall defined in Assumption 2.3 (ii) and note that the assumption continues to hold with instead of . Throughout the remaining proof we can thus assume without loss of generality that . For each , consider the three cases

| and | (A.54) | ||||

| and | (A.55) | ||||

| (A.56) | |||||

| (A.57) | ||||

Now bound the right hand side of (A.57). First, focus on (A.54). Then

| (A.58) |

Second, assume (A.55). Let . Then

| (A.59) | ||||

By (A.55) and Assumption 2.3 we have, for all sufficiently large , say ,

| (A.60) | ||||

where the second inequality follows from by Assumption 2.3(ii), which makes possible the values of the constants in this inequality.

By (A.55), (A.59), and (A.60), when

| (A.61) | ||||

where we used that for in the last inequality. Third, assume (A.56). Then, the right-hand side of (A.53) can be bounded as follows:

| (A.62) |

Since and we see that for

there exists such that for all and all

| (A.63) |

To see that the first inequality holds for sufficiently large , one may use that and the fact that to obtain the bound

The lower bound for the first expression in the definition of then follows from , which may be upper bounded by any constant multiple of for sufficiently large . A similar argument can be used to bound from below for sufficiently large since

Note that by construction as , so that we can assume (at the cost of potentially changing constants) that and are integers. Observe that for any with and any

Hence, for the particular choice

| (A.64) |

Now we bound the second and the third term on the right hand side of (A.64). By (A.63) and Assumption 2.3(ii) we have, for ,

| (A.65) |

By blocking arguments similar to (A.59), for any ,

| (A.66) |

By (A.66), Assumption 2.3(ii) and (A.63) we have, for ,

| (A.67) | ||||

By (A.64), (A.65), and (A.67) we can further bound the right-hand side of (A.1.4), for sufficiently large ,

| (A.68) | ||||

where we used that for the last inequality. By (A.52), (A.53), (A.58), (A.61), and (A.68) there exist such that, for ,

| (A.69) |

For , note that

| (A.70) |

For , by (A.1),

| (A.71) | ||||

To bound this term, consider the cases

| and | (A.72) | ||||

| and | (A.73) | ||||

| (A.74) | |||||

For the case (A.74) we have

In cases (A.72) and (A.73), we have similarly to (A.57)

and the right-hand side above can be bounded exactly as before. The right hand of (A.71) has the same form as the right hand of (A.52). Hence there exist such that for

| (A.75) |

Lemma A.6 follows from (A.51), (A.69), (A.70), and (A.75). ∎

Lemma A.7.

Let denote an arbitrary closed interval in . There exist and such that, for all , all and all , we have

A.2 Proofs for Section 2.2

The following notation is taken from the proof of Theorem 3.5 in Bücher and Segers, (2014). Let

denote by the set of all cdfs on whose marginals put no mass at zero and define

Consider the copula mapping

where denotes the left-continuous generalized inverse function, and let

In the proof of their Theorem 3.2, Bücher and Segers, (2014) established the following result under conditions (i) and (ii), the proof under condition (iii) is new to this paper.

Proposition A.8.

Proof.

The result under and was given in the proof of Theorem 3.2 in Bücher and Segers, (2014) and it remains to establish the statement under . We recall some additional notation from Bücher and Segers, (2014): let , be the identity function on , , and .

Similar to the proof of Theorem 3.5 in Bücher and Segers, (2014), it suffices to show that

which in turn follows if we show that

| (A.76) | ||||

| (A.77) | ||||

| (A.78) |

where . Note that (A.76) follows by exactly the same arguments as (A.8) in Bücher and Segers, (2014), while the proof of (A.77) is similar to the proof of (A.9) in Bücher and Segers, (2014), using that is relatively compact in . For (A.78), by Hölder-continuity of ,

By Vervaat’s Lemma, see also formula (4.2) in Bücher and Volgushev, (2013),

Hence,

by assumption. ∎

We will generalize this proposition by including the additional parameter . Define

Proposition A.9.

Assume that Assumption 2.1 is met, with satisfying Assumption 2.8. Further, let be a strictly increasing integer sequence with such that one of the following conditions is met:

-

(i)

from Assumption 2.9(a) holds for every converging sequence in ;

-

(ii)

Assumption 2.9(b) holds;

-

(iii)

from Assumption 2.9(c) holds for every converging sequence in .

Then, for any sequence in with in where , we have .

Proof of Proposition A.9.

We will proceed by contradiction. Assume that does not converge to . Then there exists , an increasing sequence of natural numbers and sequences in , in such that

| (A.79) |

By compactness of there further exists a sub-sequence such that, as , , . To simplify notation we shall abbreviate . Since uniformly and since is continuous (thus uniformly continuous as it is defined on a compact set) it follows that

i.e., with is a sequence in with uniformly. We may hence apply Proposition A.8 to obtain that

Now, the left-hand side of this display equals

while the right-hand side is equal to

As a consequence, since ,

uniformly on . Finally, since the mapping is continuous and since , it follows that so that

This contradicts (A.79), and thus as asserted. ∎

Proof of Theorem 2.10.

From Theorem 2.4 (for the continuity of sample paths) and a careful calculation (for the other condition imposed in the definition of ) it is easy to see that there exists a version of with sample paths that are in almost surely. Hence, Proposition A.9 combined with the extended continuous mapping theorem (Theorem 1.11.1 in van der Vaart and Wellner,, 1996) implies that

where

Following the lines of the proof of Lemma A.2 in Bücher and Segers, (2014) one can further show that

which implies the assertion. ∎

A.3 Proofs for Section 2.3

Before proving Theorem 2.12, we state the following lemma which provides a crucial technical ingredient.

Lemma A.10.

Suppose that, for any , is an excerpt from a univariate strictly stationary time series. Suppose is a sequence of positive integers such that and as . For , let and assume that . If there exists a sequence such that and for all and , then

Proof of Lemma A.10.

Without loss of generality, we may assume that . Observe that

By uniform boundedness and symmetry of ,

Hence

Similarly

From now on assume without loss of generality that is an integer and that . It suffices to prove that

| (A.80) |

where

To this end, for , let be a random variable uniformly distributed on and independent of , . For , let

where , . Note that, for any , is a second order stationary time series. More precisely, when ,

while, for ,

whence . Next, since is centered, we have

| (A.81) |

By the Dominated Convergence Theorem,

| (A.82) | ||||

which is (A.80). ∎

Proof of Theorem 2.12.

Since the proofs for the version with known and estimated margins are similar, we restrict our attention to the case of estimated margins. We need to show that, for any , and ,

For the ease of writing, we only consider the case and ; the general case follows along similar lines. Let denote an i.i.d. sequence with cdf . In that case, Assumptions 2.1, 2.3 and 2.9 are trivially met, provided and , whence we may apply all results from the proof of Theorem 2.10. Let us next show that

where

Indeed,

where . Now, the covariance matrix of converges by Lemma A.4, and the same is true for , since and since the are bounded by coordinate-wise. The claim then follows by simple linear algebra.

A similar argument can be used to show that

note that the summands on the right-hand side are independent due to the independence of

Finally, apply Lemma A.10 with (note that the condition on the autocovariances is trivially satisfied with ). ∎

A.4 Analytical expressions for the variances in Figure 2

A tedious but straightforward calculation shows that one may alternatively express from Theorem 2.4, for , as

and otherwise

For , the expression further simplifies to

For the bivariate Gumbel–Hougaard copula with shape parameter , it is then straightforward to show that, for

In particular, when , the Gumbel–Hougaard copula degenerates to the independent copula, and

Appendix B Proofs for Section 3

B.1 Proof of Lemma 3.2 and Lemma 3.3

Elementary calculations as in Lemma 2.2 in Bücher et al., (2019) show that, if Assumption 2.2 and the expansion in (3.3) is met, then

| (B.1) |

for all .

The following consequence of (3.1), holding for any with and for any , will be used repeatedly:

| (B.2) | ||||

| (B.3) |

For the proof of Lemma 3.3, note that the -terms in (B.3) are uniform in . Next, observe that

uniformly in , by (3.3) and (3.1). Take the difference of this expansion with (B.3) and note that by regular variation of we have, uniformly in , . We obtain

uniformly in , which implies Lemma 3.3.

Next let us prove Lemma 3.2. Note that under the i.i.d. assumption on we have

By linear independence of there exist points such that the vectors are linearly independent. By continuity of this implies the existence of an open interval with such that the determinant of the matrix with columns is bounded away from zero uniformly on .

A combination of (B.1) and (B.2) shows that (recall that )

Re-arrange terms, recall that and use regular variation of to obtain

| (B.4) |

where the remainder terms satisfy uniformly in .

Define the vectors

By construction of the points and the interval , there exists such that the determinant of the matrix with rows is bounded away from zero uniformly in for all . Define the vector

Applying (B.4) with we find that,

Since converges to an invertible matrix, we obtain that converges to a vector with entries where each entry is a continuous function of . Since for all , it follows that . This implies that the limit of with exists and is positive for all in an open set containing . Regular variation of the function follows by an application of Theorem B.1.3 in de Haan and Ferreira, (2006). ∎

B.2 Proof of Lemma 3.4

We begin by proving a couple of preliminary results. All results hold under Assumptions 2.1 and 2.3 and all convergences are for , if not mentioned otherwise.

Lemma B.1.

Let and with . If

| (B.5) |

then, for any ,

Proof of Lemma B.1.

Lemma B.2.

Let . Suppose and are -valued sequences with and , then

Lemma B.3.

Suppose is an -valued sequence satisfying and . Let