Quantification of Model Uncertainty on Path-Space via Goal-Oriented Relative Entropy

Abstract

Quantifying the impact of parametric and model-form uncertainty on the predictions of stochastic models is a key challenge in many applications. Previous work has shown that the relative entropy rate is an effective tool for deriving path-space uncertainty quantification (UQ) bounds on ergodic averages. In this work we identify appropriate information-theoretic objects for a wider range of quantities of interest on path-space, such as hitting times and exponentially discounted observables, and develop the corresponding UQ bounds. In addition, our method yields tighter UQ bounds, even in cases where previous relative-entropy-based methods also apply, e.g., for ergodic averages. We illustrate these results with examples from option pricing, non-reversible diffusion processes, stochastic control, semi-Markov queueing models, and expectations and distributions of hitting times.

Keywords uncertainty quantification; relative entropy; non-reversible diffusion processes; semi-Markov queueing models; stochastic control; option pricing; hitting times

1 Introduction

Probabilistic models are widely used in engineering, finance, physics, chemistry, and many other fields. Models of real-world systems inherently carry uncertainty, either in the value of model parameters, or more general non-parametric (i.e., model-form) uncertainty. Such uncertainty can stem from fitting a model to data or from approximating a more complicated, intractable model with one that is simpler and computationally tractable. It is often important to estimate or bound the effect of such uncertainties on quantities-of-interest (QoIs) computed from the model, i.e, to obtain uncertainty quantification (UQ) bounds. This can be especially difficult for dynamical/time-series problems over a long time-horizon, such as the computation of hitting times, reaction rates, cost functions, and option values. When the uncertainty is parametric and small, linearization and perturbative methods are effective tools for quantifying the impact of uncertainty on model predictions; see, e.g., [3, 4, 28, 21, 31, 36, 48, 49, 51]. However, new general methods are needed when the uncertainties are large or non-parametric. In this paper, we present a framework for addressing this problem for a wide range of path-space QoIs.

To illustrate the challenges inherent in model-form uncertainty on path-space, consider the following examples (see Section 5 below for further detail):

-

1.

In mathematical finance, the value of an asset, , in a variable-interest-rate environment may be modeled by a stochastic differential equation of the form

(1) Many QoIs, such as option values, involve hitting times for , and hence are naturally phrased on path-space with a potentially large time horizon. When the variable rate perturbation, , is influenced by some other process, , that is incompletely known (such as in the Vasicek model), one may wish to approximate Eq. (1) with a simpler, tractable model, e.g., geometric Brownian motion (obtained by setting ). If the true is potentially large or has an incompletely known structure then perturbative methods are unable to provide reliable error estimates. One needs new, non-perturbative methods to obtain bounds on option values, and other QoIs.

-

2.

In queuing systems, Markovian models are widely used due to their mathematical simplicity, even in cases where real-world data shows that waiting times are non-exponential, and hence the systems are non-Markovian [16]. To quantify the model uncertainty, one must estimate/bound the error incurred from using a Markovian approximation to a non-Markovian system. More generally, an approximate model may have a fundamentally different mathematical structure than the ‘true’ model; such scenarios can be difficult to study through perturbative methods.

Variational-principle-based methods, relating expectations of a quantity of interest to information-theoretic divergences, have proven to be effective tools for deriving UQ bounds. While they are applicable to parametric uncertainty, such methods are particularly powerful when applied to systems with model-form uncertainty. Methods have been developed using relative entropy [17, 15, 27, 39, 29] and Rényi divergences [6, 21]. For stochastic processes, the relative entropy rate has been used to derive UQ bounds on ergodic averages [46, 20, 30, 35, 10]. Ergodic averages constitute an important class of QoIs on path space, but many other key QoIs are not covered by these previous methods, such as the expectation of hitting times and exponentially discounted observables. Here, we develop a new general framework for path-space UQ by identifying a larger class of information-theoretic objects (the so-called goal-oriented relative entropies) and proving an accompanying new bound, Theorem 2. This framework can be applied to qualitatively new regimes, such as the aforementioned hitting times or to ergodic averages in the presence of unbounded perturbations. In addition, even when the previous methods apply (e.g., for ergodic averages with bounded perturbations), the framework developed here provides quantitatively tighter bounds.

In this work, UQ will refer to the following mathematical problem: One has a baseline model, described by a probability measure , and an alternative model, . For a given real-valued function (i.e., QoI), , one’s goal is to bound the error incurred from using in place of , i.e.,

| (2) |

(Here, and in the following, will denote the expectation under the probability measure .) is the quantity one is interested in, such as a hitting time or an ergodic average. The baseline model, , is typically an approximate but ‘tractable’ model, meaning one can calculate QoIs exactly, or it is relatively inexpensive to simulate. However, it generally contains many sources of error and uncertainty; it may depend on parameters with uncertain values (obtained from experiment, Monte-Carlo simulation, variational inference, etc.) or is obtained via some approximation procedure (coarse graining, neglecting memory terms, linearization, asymptotic approximation, etc.). Any QoI computed from therefore has significant uncertainty associated with it. In contrast, , is thought of as the ‘true’ (or at least, a more precise) model, but due to its complexity or a lack of knowledge, it is intractable. For instance, in the finance example discussed above, is the distribution on path space of the solution to Eq. (1), and one possible choice of is the distribution of geometric Brownian motion (i.e., the solution to Eq. (1) with ). In the queuing example, is the distribution of the ‘true’ non-Markovian model on path-space, while is the distribution of the Markovian approximation.

The results in [17, 15, 27, 39, 29] produce bounds on the general UQ problem (2) in terms of the relative entropy, i.e., Kullback-Leibler (KL) divergence, , which quantifies the discrepancy between the models and . When comparing stochastic processes, and , one often finds that their distributions on path-space, and , have infinite relative entropy. Hence, when dealing with an unbounded time horizon, these previous methods do not produce (nontrivial) UQ bounds. As we will see, this infinite relative entropy is often an indication that one is using the wrong information-theoretic quantity. In [20] it was shown how to overcome this issue when the QoI is an ergodic average; there, the relative entropy rate was found to be the proper information-theoretic quantity for bounding ergodic averages. See Section 2 for further discussion of this, and other background material. In this paper, we derive a general procedure for identifying information-theoretic quantities, matched to a particular QoI, that can then be used to obtain UQ bounds.

The intuition underlying our approach is conveyed by the following example: Suppose one wants to bound the -expectation of a stopping time, . Even if is unbounded, the QoI depends only on the path of the process up to time , and not on the path for all . Hence, one would expect UQ bounds on to only require knowledge of the dynamics up to the stopping time; a bound on should not be necessary. Rather, one should be able to construct UQ bounds using the relative entropy between the baseline and alternative processes up to the stopping time:

| (3) |

where is the filtration for the process up to the stopping-time ; intuitively, captures the information content of the process up to the stopping time. Eq. (3) is an example of a goal-oriented relative entropy, for the QoI .

| QoI | |

|---|---|

| 1 | |

| 2 | |

| 3 | |

| 4 |

Our results will make the above intuition rigorous and general, and we will provide appropriate information-theoretic objects for computing UQ bounds on a variety of path-space QoIs, generalizing Eq. (3). Moreover, we will show how partial information regarding the structure of the alternative model, , can be used to make such bounds computable. The method is developed in an abstract framework in Section 3, before being specializing to path-space QoIs in Section 4. The following list shows several classes of QoIs to which our methods apply (see also Table 1):

-

1.

Cumulative distribution function (CDF) of a stopping time.

-

2.

Expected value of a stopping time.

-

3.

Expectation of exponentially discounted QoIs.

-

4.

Expectation of time averages.

We will also show how one can bound goal-oriented relative entropies, such as Eq. (3), often a key step in obtaining computable UQ bounds. Finally, we illustrate these results through several examples in Section 5:

- 1.

-

2.

UQ bounds for invariant measures of non-reversible stochastic differential equations (SDEs); see Section 5.2.

-

3.

Robustness of linear-quadratic stochastic control under non-linear perturbations; see Section 5.3.

-

4.

Robustness of continuous-time queueing models under non-exponential waiting-time perturbations (i.e., semi-Markov perturbations); see Section 5.4.

- 5.

2 Background on Uncertainty Quantification via Information-Theoretic Variational Principles

In this section we record important background on the information-theoretic-variational-principle approach to UQ; the new methods presented in this paper (starting in Section 3) will be built upon these foundations.

First, we fix some notation. Let be a probability measure on a measurable space . will denote the extended reals and we will refer to a random variable as a quantity-of-interest (QoI). If we write

| (4) |

for the centered quantity of mean . The cumulant generating function of is defined by

| (5) |

where denotes the natural logarithm and we use the continuous extensions of to and of to .

Recall also that the relative entropy (i.e., KL divergence) of another probability measure, , with respect to is defined by

| (6) |

It has the property of a divergence, that is and if and only if ; see, for example, [19] for this and further properties.

The starting point of our approach to UQ on path-space is a KL-based UQ bound, which we here call the UQ information inequality. The bound was derived in [17, 20]; a similar inequality is used in the context of concentration inequalities, see e.g. [12], and was also used independently in [15, 27]. We summarize the proof in Appendix A for completeness: Let , . Then

| (7) |

If is also in then one can apply Eq. (7) to the centered QoI, to obtain centered UQ bounds, i.e., bounds on . Eq. (7) is to be understood as two formulas, one with all the upper signs and another with all the lower signs. This remark applies to all other uses of in this paper. The bounds (7) have many appealing properties, including tightness over relative-entropy neighborhoods [17, 20], a linearization formula in the case of small relative entropy [39, 20], and a divergence property [20]; see also [14, 15, 21].

In [20, 35, 10], Eq. (7) was used to derive UQ bounds for ergodic averages on path-space, both in discrete and continuous time. The goal of the present work is to extend these methods to apply to more general path-space QoIs. As motivation, here we provide a summary of one of the results from [20]: Let be a Polish space and consider two distributions, and , on path-space up to time , ; these are the baseline and alternative models respectively. Assuming that the alternative process starts in an invariant distribution, , and the baseline process starts in an arbitrary distribution, , one obtains the following UQ bound on ergodic averages (see Section 3.2 in [20] for this result and further generalizations):

Let be a bounded observable and for define the time average , where is evaluation at time for a path in . Then

| (8) |

where is the relative entropy rate:

| (9) |

To arrive at Eq. (8), one applies Eq. (7) to , divides by , and employs the chain-rule of relative entropy to write the result in terms of the relative entropy rate. Under appropriate assumptions, one can show that the upper bound remains finite as . In particular, the relative entropy rate between the alternative and baseline processes is positive and finite in many cases (see the online supplement to [20]), and hence provides an appropriate information-theoretic quantity for controlling ergodic averages in the long-time regime.

3 UQ Bounds via Goal Oriented Information Theory

Eq. (8) provides UQ bounds on ergodic averages, but there are many other classes of path-space QoIs that are important in applications; see Table 1. Naively applying the UQ information inequality, Eq. (7), to one of these other path-space QoIs that has an infinite time horizon (e.g., where is an unbounded stopping-time) will generally lead to trivial (i.e., infinite) bounds. This is due to the fact that is infinite in most cases (see Eq. (9) and the subsequent discussion). For ergodic averages, the argument leading to Eq. (8) circumvents this difficulty by expressing the bound in terms of the relative entropy rate. Although the derivation of (8) cannot be generalized to other QoIs, the idea of obtaining finite bounds by utilizing an alternative information theoretic quantity can be generalized, and we will do so in this section.

A naive application of Eq. (7) ignores a hidden degree of freedom: the choice of sigma algebra on which one defines the models. More specifically, if the QoI, , is measurable with respect to , a sub sigma-algebra of the full sigma algebra on , then one can write

| (10) |

where denotes the restriction of a measure to the sub sigma-algebra ; captures the information content of and working on will lead to UQ bounds that are targeted at the QoI. More specifically, one can apply Eq. (7) to the baseline model and alternative model , thereby obtaining a UQ bound in terms of a goal-oriented relative entropy . We use the term goal-oriented in order to emphasize the fact that the information-theoretic quantity is tailored to the QoI under consideration, through the use of . As we will show, the data-processing inequality (see [40]) implies

| (11) |

and there are many situations where the inequality is strict. Thus one often obtains tighter UQ bounds by using a goal-oriented relative entropy. The above idea is quite general, and so we develop the theory in this section without any reference to path-space. We also prove new (quasi)convexity properties regarding optimization problems of the form (7).

Theorem 1 (Goal-Oriented Information Inequality)

Let and be probability measures on and .

-

1.

Let be a sub sigma algebra of and be -measurable. Then

(12) (13) where we interpret . The objective function is quasiconvex and the objective function is convex.

-

2.

If are sub sigma-algebras then

(14)

Proof 1

-

1.

For a real-valued , write

(15) and then apply Eq. (7) to arrive at Eq. (12). The bound can then be extend to -valued by taking limits. Next, by changing variables in the infimum we arrive at Eq. (13). To see that the objective function in (13) is convex, first recall that the cumulant generating function is convex (this can be proven via Hölder’s inequality). The perspective of a convex function is convex (see, e.g., page 89 in [13] and note that the result can easily be exteded to -valued convex functions), and therefore is convex. Adding a linear term preserves convexity, hence is convex in . Finally, quasiconvexity of the objective function in (12) follows from the general fact that if is convex then is quasiconvex on . To see this, let and . Then for some . Therefore, convexity of implies

(16) -

2.

If are sub sigma-algebras then we can write (we let denote the identity on , thought of as a measurable map from to , and denotes the distribution of the random quantity ), and similarly for . The data processing inequality (see Theorem 14 in [40]) implies for any random quantity , and so we arrive at Eq. (14).

Remark 1

The objective functions in both (12) and (13) are unimodal, due to (quasi)convexity. In the majority of our theoretical discussions we will use the form (12) of the UQ bound, but the convex form (13) is especially appealing for computational purposes, as the optimization can be done numerically via standard techniques and with guarantees on the convergence. In the examples in Section 5 we will generally perform the optimization numerically, using either a line search or Nelder-Mead simplex method [43, 38].

Remark 2

Eq. (14) is a version of the data processing inequality, which holds in much greater generality than the form stated above. In particular, it holds for any -divergence [40]. For relative entropy, the data-processing inequality can be obtained from the chain rule, together with the fact that marginalization can only reduce the relative entropy.

In particular, one can bound the probability of an event by applying Theorem 1 to (see the example in Section 5.5.1):

Corollary 1

Let be a sub sigma-algebra of and . Then

| (17) | ||||

Remark 3

Theorem 1 is particularly useful because of the manner in which it splits the UQ problem into two sub-problems:

-

1.

Compute or bound the cumulant generating function of the QoI with respect to the baseline model, . (Note that there is no dependence on the alternative model, .)

-

2.

Bound the relative entropy of the alternative model with respect to the baseline model, , on an appropriate sub sigma-algebra, . (The primary difficulty here is the presence of the intractable/unknown model .)

We generally consider the baseline model, , and hence sub-problem (1), to be ‘tractable’. In practice, computing or bounding the CGF under may still be a difficult task. Bounds on CGFs are often used in the derivation of concentration inequalities; see [12] for an overview of this much-studied problem. For prior uses of CGF bounds in UQ, see [44, 29, 10]. With these points in mind, our focus will primarily be on the second problem; our examples in Section 5 will largely involve baseline models for which the CGF is relatively straightforward to compute.

Theorem 2, below, shows how one can use partial information/bounds on the intractable model, , to produce a computable UQ bound, thus addressing sub-problem 2. The key step is to select a sub sigma algebra and a -measurable for which the following relative entropy bound holds:

| (18) |

Theorem 2

Let , , be -measurable, where is a sub sigma-algebra, and suppose we have a -measurable real-valued that satisfies . Then

| (19) | ||||

| (20) |

The objective function , is quasiconvex and the objective function , is convex.

Remark 4

Proof 2

Given , apply Eq. (12) from Theorem 1 and the assumption (18) to the -measurable QoI, . Doing so yields

| (21) | ||||

In particular, bounding the right-hand-side by the value at , we can cancel the term (which is assumed to be finite) to find

| (22) |

Taking the infimum over all yields (19). Eq. (20) then follows by changing variables . To prove convexity of the objective function in Eq. (20), first note that the map is convex on for all positive measures, ; this can be proven using Hölder’s inequality in the same way that one proves convexity of the CGF. Applying this to we see that is convex in . Therefore, by again using convexity of the perspective of a convex function, we find that is convex. Finally, using the quasiconvexity property proven above in Eq. (16), we see that is quasiconvex, thus completing the proof.

Remark 5

Previously, a primary strategy for using the non-goal-oriented bound (7) in UQ was to find a function such that , compute an explicit upper bound , bound , and use this to obtain the (in principle) computable bounds

| (23) |

Of course, if is not bounded then the resulting UQ bound is uninformative. The new result (19) is tighter than the above described strategy, as can be seen by bounding in the exponent of Eq. (19). In addition, (19) can give finite results even when is not bounded, as we demonstrate in the examples in Sections 5.2 and 5.5.1.

Theorem 2 takes a relative entropy bound of the form (18) (which involves an expectation under the intractable model ) and produces a UQ bound which only involves expectations under the tractable model, (see Eq. (19)). However, in practice it is not enough to use just any that satisfies Eq. (18). If the relative entropy on is finite then the (trivial) choice of always satisfies Eq. (18) (with equality). Rather, the practical question is whether one can find a tractable that satisfies Eq. (18); the trivial choice typically does not satisfy this tractability requirement. Given the fact that may only be partially known, a tractable will generally need to incorporate bounds/partial information regarding .

The choice of an appropriate goes hand-in-hand with the choice of . The bounds in Theorem 1 become tighter as one makes smaller, with the tightest bound obtained when , where is the sigma algebra generated by (i.e., generated by ), in which case the relative entropy is . However, one must again balance the desire for tightness against the need for computable bounds. It is generally very difficult to find a tractable for the relative entropy on , and so a larger sub sigma-algebra must be used. While the task of finding a suitable and is problem specific, for QoIs on path space there are general strategies one can follow. We discuss such strategies in Section 4 and Appendix D below; see also the concrete examples in Section 5.

In some cases, the right-hand-side of the UQ bound (19) is still difficult to compute, and so it can be useful to first bound and then use the UQ bound from Theorem 1 directly; for example, see the analysis of the Vasicek model in Section 5.5.1. The following corollary, obtained by applying Theorem 2 to and then reparametrizing the infimum, is useful for this purpose:

Corollary 2

Suppose , is -measurable for some sub sigma-algebra , and . Then

| (24) |

Remark 6

Sensitivity analysis of a QoI to perturbations within a parametric family, , , was also studied in [20]. The extension to goal-oriented relative entropy proceeds similarly, assuming one can find a density for the restricted measure with respect to some common dominating measure: . Examples of such densities for various classes of Markov processes can be found in Appendix D. Once one has , the computation of sensitivity bounds proceeds as in [20], and so we make no further comments on sensitivity analysis here.

4 Goal-Oriented UQ for QoIs up to a Stopping Time

We now specialize the methods of Section 3 to the study of path-space QoIs. Concrete examples can be found in Section 5, but we first discuss the guiding principles and common themes that underlie these applications. Section 4.1 sets up the framework for UQ on path-space. Specifically, we consider QoIs up to a stopping time. Many important problem types fit under this umbrella, such as discounted observables, the CDF of a stopping time, expectation of a stopping time, as well as the previously studied ergodic averages (see Table 1); Sections 4.2 - 4.4 discuss several of these problem types in further detail.

4.1 General Setting for UQ on Path Space up to a Stopping Time

The general setting in which we derive path-space UQ bounds is as follows:

Assumption 1

Suppose:

-

1.

is a filtered probability space, where , or . We define .

-

2.

and are probability measures on .

-

3.

, written , is progressively measurable (progressive), i.e., is measurable and is -measurable for all (intervals refer to subsets of ).

-

4.

is a -stopping time.

We will derive UQ bounds for a process , stopped at , which we denote by . First recall:

Lemma 1

is -measurable, where

| (26) |

is the filtration up to the stopping-time , a sub sigma-algebra of .

For a general stopped QoI, , the following (uncentered) UQ bounds immediately follow from Theorems 1 and 2 with the choices or :

Corollary 3

Remark 8

Corollary 3 provides general-purpose UQ bounds for path-space QoIs up to a stopping time. In the following subsections, we discuss the nuances involved in deriving UQ bounds for several of the classes of QoIs from Table 1. In some cases we directly apply Corollary 3, while others benefit from a slightly altered approach. Not all of our examples in Section 5 below will fit neatly into one of these categories, but rather, they illustrate several important use-cases and strategies.

4.2 Expectation of a Stopping Time

Here we consider the expectation of a stopping time, . For , (the centered variant of) Eq. (27) in Corollary 3 applied to yields

| (29) |

For unbounded , it is often useful to use Lemma 3 from Appendix C to obtain:

| (30) |

To obtain a computable bound from Eq. (30), first note that a relative entropy bound of the following form often follows from Girsanov’s theorem (see Appendix D):

| (31) |

for some and all . One can then use Theorem 2 with and . Taking via the monotone and dominated convergence theorems and then reparameterizing the infimum results in the following:

Corollary 4

Assume the relative entropy satisfies a bound of the form Eq. (31) for all . Then

| (32) |

Again, note that the upper and lower bounds only involve the tractable model, . We illustrate this technique in a concrete example in Appendix G.

4.3 Time-Integral/Discounted QoIs

Here we consider exponentially discounted QoIs. In the language of Assumption 1, given a progressive process and some we define

| (33) |

and will consider the stopped process , with stopping-time . Such QoIs are often used in control theory (see page 38 in [37]) and economics (see page 64 in [45] and page 147 in [47]). Here we derive an alternative UQ bound to Corollary 3 that is applicable to such QoIs:

Theorem 3

Let and define . Suppose is progressively measurable and

| (34) |

Then

| (35) | ||||

Remark 9

Proof 3

First suppose . This allows us to use Fubini’s theorem to compute

| (36) |

and implies is finite for -a.e. . For each , is -measurable, hence Theorem 1 implies

| (37) |

for -a.e. . Integrating over gives the first inequality in Eq. (35). The second follows by pulling the infimum outside of the integral.

If then repeat the above calculations for and take , using the dominated and monotone convergence theorems.

The last line in Eq. (35) consists of two terms, a discounted moment generating function and a discounted relative entropy,

| (38) |

Eq. (38) is the same information-theoretic quantity that was defined in [47] (see page 147), where it was proposed as a measure of model uncertainty for control problems. Theorem 3 provides a rigorous justification for its use in UQ for exponentially discounted QoIs.

Remark 10

is a probability measure, and so one one could alternatively apply Theorem 1 to the product measures and . However, Jensen’s inequality implies that the bound Eq. (35) is tighter. Alternatively, one might attempt to use Corollary 3 in place of Theorem 3, in which case one generally finds that the relative-entropy term, , is infinite and so the corresponding UQ bound is trivial and uninformative. On the other hand, the bound Eq. (35) is often nontrivial; see the example in Section 5.3 below.

4.4 Time-Averages

Finally, we remark that ergodic averages are a special case of the current framework: Let , , and (one can similarly treat the discrete-time case). is -measurable and so, if , one can apply Corollary 3 to . Reparameterizing the infumum , one finds that the bound is the same as Eq. (8), which was previously derived in [20] and used in [10]. As we will demonstrate in the example in Section 5.2 below, one can often use Theorem 2 to obtain tighter and more general UQ bounds on ergodic averages than those obtained from Eq. (8).

5 Examples

We now apply the goal-oriented UQ methods developed above to several examples:

-

1.

Hitting times for perturbations of Brownian motion in Section 5.1.

-

2.

UQ bounds for invariant measures of non-reversible SDEs in Section 5.2.

-

3.

Expected cost in stochastic control systems in Section 5.3.

-

4.

Long-time behavior of semi-Markov perturbations of an queue in Section 5.4.

-

5.

Pricing of American put options with variable interest rate in Section 5.5.

5.1 Perturbed Brownian Motion

We first illustrate the use of our method, and several of its features, with a simple example wherein many computations can be done explicitly and exactly; the example consists of perturbations to Brownian-motion-with-constant-drift. Specifically, take the baseline model to be the distribution on path-space, , of a -valued Wiener process (Brownian motion), , with constant drift, , starting from , i.e., the distribution of the following process:

| Baseline Model: | (39) |

The alternative model will be the distribution of the solution to a SDE of the form:

| Alternative Models: | (40) |

where is also a Wiener process. We allow the drift perturbation, , to depend on an additional -valued process, , and also on independent external data, (see Appendix D.3 for further discussion of the type of perturbations we have in mind). More specific assumptions on will be stated later. We note that the methods developed here do not allow one to perturb the diffusion, as the corresponding relative entropy is infinite due to lack of absolute continuity (see, e.g., page 80 in [24]).

In Section 5.1.1 we will study the cumulative distribution function of , the level- hitting time:

| QoI 1: | (41) |

Note that is a stopping time on path-space, . denotes the distribution of on path-space and similarly for ; the superscript indicates that the initial condition is .

We will also derive UQ bounds for the expected level- hitting time,

| QoI 2: | (42) |

This second QoI is simpler, as we can use the general result of Section 4.2. Therefore we relegate the details to Appendix G.

5.1.1 Hitting Time Distribution: Benefits of Being Goal-Oriented

We use the QoI (41) to illustrate the benefits of using a goal-oriented relative entropy, versus a non-goal-oriented counterpart. Here we specialize to perturbed SDEs, Eq. (40), whose distributions, , satisfy the following.

| Alternative Models: | Perturbations by drifts, , such that, for some : | (43) | ||

For example, Eq. (43) holds if (assuming that the models satisfy the assumptions required to obtain the relative entropy via Girsanov’s theorem; see Appendix D.3 for details).

The QoI, , is -measurable, and so is an appropriate goal-oriented relative entropy; the bound Eq. (43) implies that we can take and in Theorem 2. This gives the following goal-oriented UQ bound:

| (44) |

For comparison, we also compute the non-goal-oriented bound that follows from the UQ information inequality (7). The QoI is a function of the path up to time , so we apply this proposition to the relative entropy (the subscript denotes taking the distribution on path-space ).

Remark 11

Repeating these computations under the assumption , but using the non-goal-oriented relative entropy bound (once again using Girsanov’s theorem), we obtain the UQ bound

| (45) |

Note that the goal-oriented bound on the right hand side of Eq. (44) is tighter than the non-goal-oriented bound (45), as can be seen by bounding in the exponent.

The -expectations in (44) and (45) can be computed using the known formula for the distribution of under the baseline model (see page 196 in [34] and also Appendix F). Assuming that and , the goal-oriented bound is

| (46) |

Similarly, one can compute the non-goal-oriented bound, Eq. (45), and the probability under the baseline model.

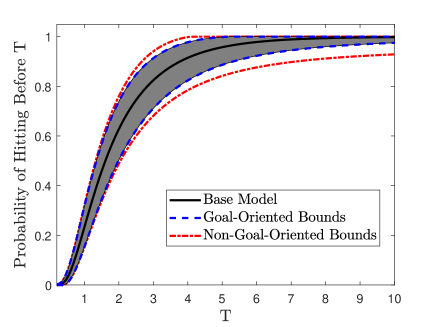

Figure 1 shows numerical results comparing these bounds, with parameter values , , ; we compute the integrals numerically using a quadrature method and, as discussed in Remark 1, we solve the 1-D optimization problems numerically. The black curve shows the distribution of under the baseline model. The blue curves show the goal-oriented bounds Eq. (46); these constrain to be within the gray region. The red curves show the non-goal-oriented bounds (45); we see that the non-goal-oriented bounds significantly overestimate the uncertainty, especially as approaches .

5.2 UQ for Time-Averages and Invariant Measures of Non-Reversible SDEs

In this example we show how Theorem 2 can be combined with the functional inequality methods from [10] to obtain improved UQ bounds for invariant measures of non-reversible SDEs. Specifically, consider the following class of SDEs on :

| Baseline Model: | (47) |

where the non-gradient portion of the drift, , satisfies

| (48) |

If then Eq. (47) is an overdamped Langevin equation with potential . In general, Eq. (47) is non-reversible but Eq. (48) ensures that remains the invariant measure for ; such non-reversible terms are used for variance reduction in Langevin samplers [50].

The alternative model will have a general non-reversible drift:

| Alternative Models: | (49) |

Denote their respective distributions on path-space, , by and . We will obtain UQ bounds for ergodic averages of some observable :

| QoI: | (50) |

Remark 12

While the invariant measure of the baseline process is known explicitly (up to a normalization factor; see Eq. (47)), the invariant measure of the alternative model (49) is not known for general ; physically, such non-reversible drifts model external forces. A general drift can be split into and via a Helmholz decomposition (i.e., is the divergence-free component). Such a decomposition can inform the choice of in the baseline model.

Assuming that Girsanov’s theorem applies (see Appendix D.3), we have the following expression for the relative entropy

| (51) |

The quantity is -measurable and if is finite and grows sufficiently slowly at infinity then and hence Theorem 2 implies

| (52) |

where we re-indexed .

We can now use the functional inequality approach of [10] to bound Eq. (52). First write

| (53) | |||

Utilizing a connection with the Feynman Kac semigroup, the cumulant generating function in (52) can be bounded as follows (see Theorem 1 in [53] or Proposition 6 in [10]):

| (54) | |||

where denotes the generator of the baseline SDE (47). Note that depends only on the symmetric part of , while the non-reversible component of the drift, , only contributes to the antisymmetric part of . Therefore, it suffices to consider the reversible case when bounding . (The precise form of will impact the quality of the final UQ bound; see Remark 13).

can be bounded using functional inequalities for (e.g., Poincaré, log-Sobolev, Liapunov functions). For example, a log-Sobolev inequality for ,

| (55) |

where , implies

| (56) |

(see Corollary 4 in [53] or Proposition 7 in [10]) and hence

| (57) |

If the alternative process is started in a known initial distribution, , for which is finite and can be computed (or bounded) then the right-hand-side of Eq. (57) only involves the baseline process and other known quantities. It therefore provides (in principle) computable UQ bounds on the expectations of time-averages at finite-times. Alternatively, by taking the dependence on the initial distribution in (52) disappears and we can obtain UQ bounds on the invariant measure of the alternative process. In the remainder of this subsection we explore this second direction.

By starting the alternative process in an invariant measure and taking in Eq. (57) we obtain the following UQ bounds on the invariant measure of the alternative model:

| (58) |

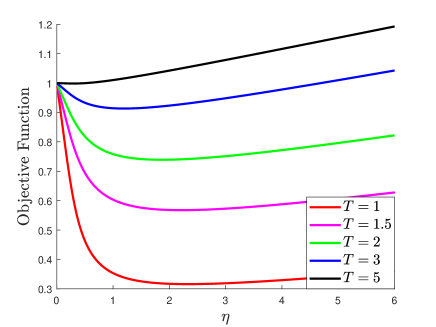

Note that the bounds (58) only involve expectations under the baseline invariant measure, , and are finite for appropriate unbounded and . The ability to treat unbounded perturbations is due to our use of Theorem 2, as opposed to Eq. (8), and constitutes a significant improvement on the results in [20, 10], which are tractable only when is bounded. In Figure 2 we compare Eq. (58) with the UQ bound (8) from [20], where in the latter we employ the relative entropy rate bound

| (59) |

i.e., we use the strategy described in Remark 5. Even in the case where is bounded, the new result (58) obtained using Theorem 2 is tighter than the bounds obtained from the earlier result (8).

5.3 Discounted Quadratic Observable for Non-Gaussian Perturbations of a Gaussian Process

Here we consider a -valued progressively measurable process, , that has a Gaussian distribution for every :

| Baseline Model: | (60) |

The mean and variance of the baseline model are considered to be known (i.e., obtained by some approximation or measurement). We will compute UQ bounds on non-Gaussian perturbations of (60). We assume is (strictly) positive-definite and study the discounted QoI:

| QoI: | (61) |

where is a positive-definite -matrix-valued function, is -valued, and is a probability measure. Without loss of generality (i.e., neglecting an overall constant factor and after a redefinition of ), we have chosen to express in terms of the centered process . The techniques involved here are those of Section 4.3.

At this point, we are being purposefully vague about the nature of the alternative model and even the details of the baseline model, as a large portion of the following computation is independent of these details. We also emphasize that the alternative models do not need to be Gaussian. In Section 5.3.1 we will make both base and alternative models concrete, as we study an application to control theory.

Assuming that the conditions of Theorem 4 of Appendix E are met, we obtain the following UQ bound (note that the appropriate sub sigma-algebras are ):

| (62) | ||||

is Gaussian under , so we can compute

| (63) | ||||

For small enough, is positive-definite. More specifically, is positive-definite, so we can compute a Cholesky factorization with nonsingular. is positive-definite if and only if for all nonzero , which is true if and only if (-matrix norm).

For , the integral in Eq. (63) can be computed in terms of the moment generating function of a Gaussian with covariance , resulting in the UQ bound

| (64) |

where and for the above ranges of we have

To make these bounds computable, one needs a bound on the relative entropy; this requires more specificity regarding the nature of the family of alternative models. We study an application to control theory in the following subsection.

5.3.1 Linear-Quadratic Stochastic Control

Here, Eq. (64) will be used to study robustness for linear-quadratic stochastic control (robustness under nonlinear perturbations). Specifically, suppose one is interested in controlling some nonlinear system,

| (65) |

where are matrices, and is a -valued Wiener process. We write the non-linear term with an explicit factor of to simplify the use of Girsanov’s theorem later on. The control variable is denoted by and is the state; we take to be an observable quantity that can be used for feedback.

The perturbation may be unknown and even when it is known, optimal control of Eq. (65) is a difficult problem, both analytically and numerically [37]. Therefore, one option is to consider the linear approximation

| (66) |

obtain an explicit formula for the optimal feedback control (under a cost functional to be specified below) for Eq. (66), and use that same feedback function to (suboptimally) control the original system Eq. (65). To evaluate the performance, one must bound the cost functional when the control for the linearized system is used on the nonlinear system.

To make the above precise, we must first specify the cost functional, which we take to be an exponentially discounted quadratic cost:

| (67) |

(and similarly with replaced by for the nonlinear system). Here, and are positive-definite -matrices.

The optimal feedback control for the the linear system Eq. (66) with cost Eq. (67) is given by where is obtained as follows (see [2, 9] for details): Define and solve the following algebraic Riccati equation for :

| (68) |

The optimal control is then

| (69) |

Having obtained Eq. (69), we can finally fit the above problem into our UQ framework:

| Baseline Model: | (70) | |||

| Alternative Models: | (71) | |||

| QoI: | (72) | |||

| where is the path of the state variable. |

Note that, by Girsanov’s theorem, the collection of alternative models contains all bounded-drift-perturbations of the baseline model with .

The UQ bounds (64) applied to the above problem are bounds on the cost of controlling the nonlinear system (65) by using the feedback control function that was derived to optimally control the linear system (66). We can make the bounds explicit as follows: Eq. (70) has the solution

| (73) |

In particular, is Gaussian with mean and covariance

| (74) |

Next, compute a Cholesky factorization of , . The integrand in Eq. (67) is non-negative, hence the hypotheses of Theorem 3 are met and we can use Eq. (64) to obtain

| (75) | ||||

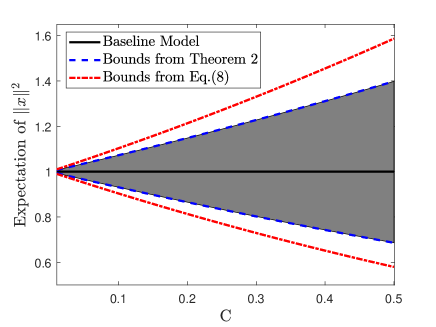

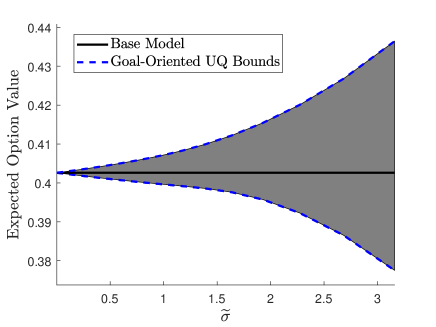

Figure 3 shows numerical results, corresponding to the following simple example system, with a 2-D state variable and a 1-D control variable:

| (76) |

, , , , , . Note that the size of the perturbation, , is not required to be ‘small’ for the method to produce non-trivial bounds, as this is a non-perturbative calculation. Finally, if one instead attempts to use the non-goal-oriented relative entropy to derive UQ bounds, the results are again trivial (infinite), due to the unbounded time-horizon.

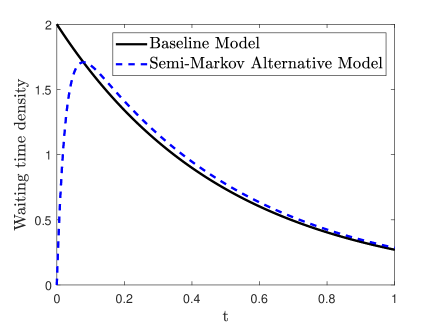

5.4 Semi-Markov Perturbations of a Queue

Continuous-time jump processes with non-exponential waiting times (i.e., waiting times with memory) are found in many real-world systems; see, for example, the telephone call-center waiting time distribution in Figure 2 of [16]. However, these systems are often approximated by a much simpler Markovian (i.e., exponentially-distributed waiting time) model. Here we derive robustness bounds for such approximations.

More specifically, we take the baseline model to be a queue (i.e., continuous-time birth-death process) with arrival rate and service rate :

| Baseline Model: | (77) |

The embedded jump Markov-chain has transition probabilities, , given by

| (78) |

and the waiting-times are exponentially distributed with jump rates

| (79) |

We consider the stationary case, i.e., is Poisson with parameter . Also, note that the jump chain with transition matrix (78) has the stationary distribution

| (80) |

The alternative models will be semi-Markov processes; these describe jump-processes with non-exponential waiting times (i.e., with memory). Mathematically, a semi-Markov model is a piecewise-constant continuous-time process defined by a jump chain, , and jump times, , and waiting times (i.e., jump intervals), , that satisfy

| Alternative Models: | (81) | |||

is called the semi-Markov kernel (see [33, 41] for further background and applications). Note that the baseline process (77) is described by the semi-Markov kernel

| (82) |

We emphasize that the alternative models (81) are not Markov processes in general; our methods make no such assumption on .

An important QoI in such a model is the average queue-length,

| QoI: | (83) |

More specifically, we will be concerned with the long-time behavior (limit of as ). Time-averages such as Eq. (83) were discussed in Section 4.4, and for these the UQ bound (27) implies

| (84) |

is the average queue-length in the (stationary) baseline process. Note that one does not need to first prove to obtain Eq. (84); non-negativity of the QoI allows one to first work with a truncated QoI and then take limits.

The cumulant generating function of the time-averaged queue-length has the following limit (see Section 4.3.4 in [10]):

| (85) |

Combining Eq. (84) and Eq. (85), we obtain the following UQ bound:

Proposition 1

A formula for the relative entropy rate between semi-Markov processes was obtained in [25] under the appropriate ergodicity assumptions:

| (88) | |||

where is the invariant distribution for the embedded jump chain of .

In particular, an alternative process with the same jump-chain as the base process but a different waiting-time distribution, , is described by the semi-Markov kernel

| (89) |

In this case, and can be expressed in terms of the relative entropy of the waiting-time distributions:

| (90) | ||||

| (91) |

where is the invariant distribution for ; recall the stationary distribution for the jump chain of the -queue was given in Eq. (80).

Remark 14

The quantity is the mean sojourn time under the invariant distribution, , and the expecation can be viewed as the mean relative entropy of a single jump (comparing the alternative and baseline model waiting-time distributions). The formula for , Eq. (90), therefore has the clear intuitive meaning of an information loss per unit time.

Other than , the formulas Eq. (86) and Eq. (90) include only baseline model quantities. Next we show one can bound for a particular class of semi-Markov processes, and thus obtain computable UQ bounds.

5.4.1 UQ Bounds for Phase Type Distributions

Phase-type distributions constitute a semi-parametric description of waiting-time distributions, going beyond the exponential case to describe systems with memory; see [23, 5, 16] for examples and information on fitting such distributions to data. Probabilistically, they can be characterized in terms the time to absorption for a continuous-time Markov chain with a single absorbing state. The density and distribution function of a phase type-distribution, , are characterized by a matrix , and a probability vector (see [11] for background):

| (92) |

where is the vector of all ’s and satisfies:

-

1.

for all ,

-

2.

for all ,

-

3.

has all non-negative entries.

Combining Eq. (92) with Eq. (90), we obtain a formula for the relative entropy rate of a semi-Markov perturbation:

Proposition 2

Let the baseline model consist of a queue (77) and let be a semi-Markov perturbation with state- waiting-time distributed as (and with the same jump-chain, , as the base process). Then the relative entropy rate is

| (93) | ||||

As a simple example, consider the case where the waiting-time at is distributed as a convolution of and -distributions (convolutions of exponential distributions are examples of phase-type distributions; again, see [11]), for some choices of . Recall the baseline model rates were given in Eq. (79). The semi-Markov kernel for the alternative process is then

| (94) |

Note that the Markovian limit occurs at , where the integrand is non-analytic. Hence, it appears unlikely that one could perform a perturbative study of this system. In contrast, our method will produce computable UQ bounds.

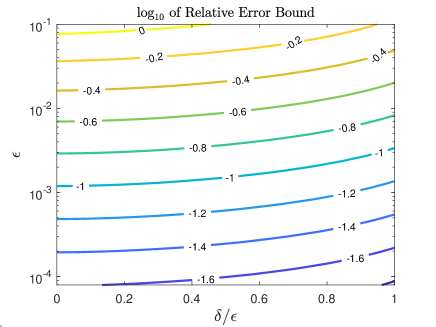

To proceed, one must assume some partial knowledge of . Here we consider the alternative family consisting of processes of the form Eq. (94) with the following parameter bounds (of course, other choices are possible):

| Alternative Models: | (95) |

where the jump-rates for the baseline model are . As a function of , Eq. (95) therefore constrains to lie between two lines. This set describes waiting-times that are approximately -distributed when is small (i.e., when ). The parameter is a lower-bound on the perturbation. See the left panel of Figure 4 for an illustrative example of this class of alternative models.

Using Eq. (95) we can bound

| (96) | ||||

To obtain the above, we used the inequality

| (97) |

Combining Eq. (96) and Eq. (97) with Eq. (86) gives the relative-error bounds

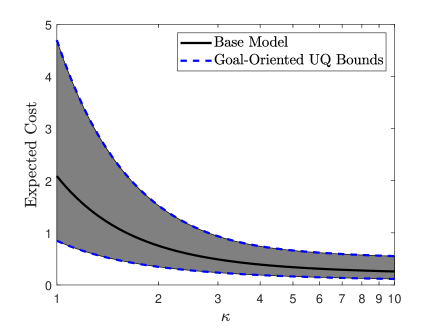

| (98) | ||||

These bounds depend only on the uncertainty parameters and , and not on the base-model parameters. See the right pane in Figure 4 for a contour plot of the logarithm of the upper bound Eq. (98). Note that the error decreases as increases, due to the decreasing uncertainty in the form of the perturbation (see Eq. (95)). As , the semi-Markov perturbation approaches the baseline model (see Eq. (94) and Eq. (95)) and so the relative error approaches . As previously noted, relative entropy based UQ methods are sub-optimal for risk-sensitive quantities (i.e., rare events); see [7] for a treatment of risk-sensitive UQ for queueing models.

5.5 Value of American Put Options with Variable Interest Rate

As a final example, we consider the value of an asset in a variable-interest-rate environment, as compared to a constant-interest-rate baseline model. For background see, for example, Chapter 8 of [52] or Chapter 8 of [26]. This example does not fit neatly into any of the problem categories from Section 4, though the technique of Corollary 2 will play a critical role. In particular, we will see that the natural QoI for the base and alternative models is different; see Eq. (104) and Eq. (106).

Specifically, the baseline model in this example is geometric Brownian motion:

| Baseline Model: | (99) |

where are constants. This has the explicit solution

| (100) |

The variable-interest-rate alternative model has the general form

| Alternative Models: | (101) |

The initial values will be fixed (here, the superscript on will always denote the constant interest rate, , that is being used). will be thought of as a known, fixed value, while will be considered an unknown perturbation that depends on time, on the asset price, as well as on an additional driving process, , that solves some auxiliary SDE; see Appendix D.3 for more precise assumptions and [52] for discussion of various interest rate models. In Section 5.5.1 below, we will consider the Vasicek model.

The quantity of interest we consider is the value of a perpetual American put option: Let be the option strike price. The payout if the option is exercised at time is , where is the asset price at time . The relevant QoI is then the value, discounted to the present time. In the baseline model, this takes the form ,

| (102) |

while for the alternative model it is ,

| (103) |

The option-holder’s strategy is to exercise the option when the asset price hits some level , assumed to satisfy and , i.e., we consider the stopping time . Therefore the baseline model QoI is

| Baseline QoI: | (104) |

To evaluate this, one uses the fact that

| (105) |

is the level hitting time of a Brownian motion with constant drift , combined with the formula for the distribution of such hitting times (see [34] and also Appendix F).

The goal of our analysis is now to bound the expected option value in the alternative model:

| Alternative QoI: | (106) |

Note that both QoIs have unbounded time-horizon; therefore, to obtain non-trivial bounds one must again use a goal-oriented relative entropy.

Remark 15

The methods developed in this paper, applied to the goal oriented relative entropy , are still not capable of comparing the baseline model Eq. (99), with asset-price volatility , to an alternative model with perturbed asset-price volatility, , due to the loss of absolute continuity (again, see page 80 in [24]). It is likely that one does have absolute continuity on a smaller sigma algebra than , but we do not currently know how to bound the relative entropy on any such smaller sigma algebra. An alternative approach to robust option pricing under uncertainty in , utilizing -control methods, was developed in [42].

To obtain UQ bounds for Eq. (106), it is useful to define the modified QoI

| (107) |

and note that , where denotes the expectation with respect to the joint distribution of on path-space. (The notation will similarly be used below.) In the next subsection, we will bound for one class of rate perturbations.

5.5.1 Vasicek Interest Rate Model

Here we study a specific type of dynamical interest rate model, known as the Vasicek model (see, for example, page 150 in [52]):

| Alternative Models: | (108) | |||

| (109) |

where and are independent Brownian motions. The baseline model is still given by Eq. (99). Robustness bounds under such perturbations can be viewed as a model stress test for the type of financial instrument (QoI) studied here; see [22] for a detailed discussion of stress testing.

The SDE (109) defines a 2-dimensional parametric family of alternative models, parameterized by and . Infinite-dimensional alternative families of -models can also be considered; see Appendix I for one such class of examples. Eq. (109) has the exact solution

| (110) |

Note that is unbounded, and so a comparison-principle bound is is not possible here. Under the model (108), can become negative. Here, for both modeling and mathematical reasons, we eliminate this possibility by conditioning on the event , i.e., we only consider those paths with non-negative average interest rate up to the stopping time. This amounts to using the modified QoI

| (111) |

and bounding

| Alternative QoI: | (112) |

Other more complex interest rate models exist that enforce a positive rate via the dynamics; see, for example, page 275 in [52].

We also restrict to the parameter values , for which a negative average interest rate is sufficiently rare. More precisely, this assumption implies a.s.; see Appendix H for details. As a consequence, we also obtain a.s. (under both the base and alternative models). Therefore, Corollary 3 and Lemma 3 (see Appendix C) can both be used, yielding

| (113) |

For this example, we do not utilize Theorem 2, as the resulting expectation is difficult to evaluate. Instead, we work with the cumulant generating function and relative entropy terms separately and use Corollary 2 together with Theorem 1.

First we compute the cumulant generating function. and are independent, hence we can use the result of [1] to find

| (114) | ||||

The integral over in Eq. (114) can then be computed as discussed in the text surrounding Eq. (105), with and . (When , the inner integral should be interpreted as equaling .)

Remark 16

Note that if the integrated rate ( in Eq. (114)) is allowed to be negative (i.e., we remove from the exponential) then is infinite and the upper UQ bound is the trivial bound, . This is the mathematical reason for conditioning on the event .

The relative entropy can be computed via Girsanov’s theorem (Appendix H for a proof that the Girsanov factor is an exponential martingale)

| (115) |

Note that is -measurable and has finite expectation, as one can bound by and then use the fact that is normal with mean and variance . Hence, Corollary 2 is applicable, resulting in

| (116) |

Again using the independence of and , we have

| (117) |

Therefore

| (118) |

and the inner expectation can be evaluated using Theorem 1 (B) of [18]:

| (119) | ||||

By analytic continuation, this formula is valid for . Also, note that for the limit of Eq. (117) to be finite, we need -a.s., i.e., and must have the same signs.

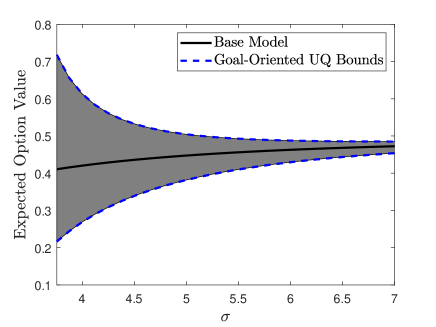

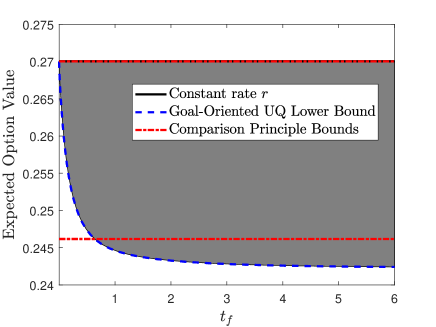

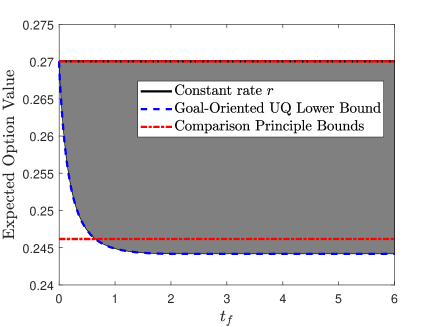

Figure 5 shows numerical results for the bounds on Eq. (112) that result from combining Eq. (113) through Eq. (121) (the full statement of the bound is quite lengthy so, rather than stating it here, we have placed it in Appendix H, Eq. (161)). The baseline model is shown in the black solid curves (see Eq. (104)) and the blue dashed curves show the bounds (161) on the alternative model QoI that result from our method, which constrain the QoI to the gray regions; we emphasize that the alternative model uses the modified QoI, Eq. (111)-(112). In the left plot we see that the uncertainty approaches zero as approaches zero, corresponding to zero rate perturbation. However, does not need to be small for our method to apply.

Remark 17

We are able to perturb the diffusion parameter, , without losing absolute continuity because, technically, the baseline model is the joint distribution of . Of course, is not coupled to , nor does the baseline QoI depend on it, but regardless, this makes it clear that there is no loss of absolute continuity between the distributions of and when is changed.

Appendix A Proof of the UQ Information Inequality

Proposition 3

Let , be probability measures and , . Then

| (122) |

Proof 4

The key tool is the Gibbs variational principle, which relates the cumulant generating function and relative entropy as follows: If is measurable and there exists such that then

| (123) |

A (slightly weaker) version of this result is found in Proposition 4.5.1 in [19], where it is assumed that is bounded above. However, the above variant can then easily be obtained by applying Eq. (123) to and then taking via the monotone convergence theorem (the assumption is necessary to ensure that for all with , where is the positive part of ).

Now fix and consider the case of the upper signs in Eq. (122) (the proof for the lower signs proceeds similarly). If or then the claimed bound (at ) is trivial, so suppose not. In this case, we have and so we can apply Eq. (123) to . Bounding the supremum in Eq. (123) below by the value at , solving for , and then dividing by yields the result.

Appendix B Tightness of the Bounds from Theorem 2

The bounds (19) are tight, in the following sense:

Corollary 5

Proof 5

Let . The assumptions, together with Eq. (19), imply and we have

| (124) | ||||

Note that in the first line, we used the fact that are increasing on , as can be proven using Hölder’s inequality.

Appendix C Tools for Computing the Goal-Oriented Relative Entropy

In this appendix, we present several lemmas that are generally useful when computing the goal-oriented relative entropy. First, we address the question of processes with different initial distributions:

Lemma 2

Suppose that the base and alternative models are of the form

| (125) |

for some probability kernels, and , from to , and some probability measures (e.x. initial distributions), and , on .

In this case, one can use the chain-rule for relative entropy (see, for example, [19]) to bound

| (126) |

Remark 19

Note that without further assumptions, Eq. (126) is not an equality. For example, let be a probability measure on , (the projection onto the second component in ), and for define . Then for we have , and

| (127) |

Intuitively, inequality in Eq. (126) arises when the QoI ‘forgets’ some of the information regarding the discrepancy between the initial condition, as the right-hand-side in Eq. (126) incorporates the full discrepancy.

Remark 20

Recall that , where is the sigma algebra generated by . If is measurable with respect to a sub sigma algebra, , then and one can weaken the bound via , as discussed in Theorem 1.

The main tool we use to compute the relative entropy up to a stopping time, Lemma 4 below, requires one to work with bounded stopping times. This limitation can often be overcome by taking limits. For example:

Lemma 3

Suppose that one is working within the framework of Assumption 1 and one of the following two conditions holds:

-

1.

is finite -a.s. and -a.s.

-

2.

as , , both and -a.s.

Then

| (128) | ||||

Proof 6

Either condition implies that and weakly as . The result then follows from lower-semicontinuity of relative entropy (see [19]).

The general tool we use to compute relative entropy up to a stopping time is the optional sampling theorem (see, for example, [34]), as summarized by the following lemma:

Lemma 4

Let be probability measures on the filtered space such that for all .

Then is an -martingale. In the continuous-time case, we also assume that we have a right-continuous version of .

Given this, for any stopping time, , we have and

| (129) |

Appendix D Relative Entropy up to a Stopping Time for Markov Processes

Below, we use Lemma 4 to give explicit formulas for the relative entropy up to a stopping time for several classes of Markov processes in both discrete and continuous time.

D.1 Discrete-Time Markov Processes

Let be a Polish space, and be transition probabilities on and , be probability measures on . Let and be the induced probability measures on with transition probabilities and respectively, and initial distribution and . Let be the natural projections, , and be a -stopping time.

We have the following bound on the relative entropy, via the optional sampling theorem:

Lemma 5

Suppose that for some measurable and let . Then

| (130) |

D.2 Continuous-Time Markov Chains

Let be a countable set, and be probability measures on , and , , such that and are continuous-time Markov chains (CTMCs) with transition probabilities , , jump rates , , and initial distributions , respectively. Let be the natural filtration for , and be the embedded jump chain with jump times . We assume as for all .

Suppose and that whenever we also have (note that this also implies that whenever ). Then for all and

| (131) |

where is the number of jumps up to time (see, for example, [32]). Note that in defining the functions and , we use the convention .

Lemma 4 then yields the following:

Lemma 6

| (132) | ||||

D.3 Change of Drift for SDEs

Here we consider the case where and are the distributions on path-space, , of the solution flows and of a pair of SDEs starting at . More precisely:

Assumption 2

Assume:

-

1.

We have filtered probability spaces, , that satisfy the usual conditions [34] and are equipped with -valued Wiener processes and respectively (Wiener processes with respect to the respective filtrations).

-

2.

We have another probability space , a -measurable random quantity , and a -measurable random quantity , and they are both distributed as .

Remark 21

Intuitively, we are thinking of as representing some outside data, independent of , that is informing the model. can then be taken to be the completed sigma algebra generated by and the Wiener process up to time . Since and the Wiener process are independent, is still a Wiener process with respect to the resulting filtration.)

-

3.

We have and -valued processes and that are adapted to and respectively, and satisfy the SDEs

(133) (134) where , , and are measurable and the modified drift is

(135) -

4.

and the following process is a martingale under :

(136) This holds if the Novikov condition is satisfied; see, for example, page 199 of [34].

-

5.

The SDE Eq. (134) satisfies the following uniqueness in law property for all :

Suppose is a continuous, adapted process on another filtered probability space satisfying the usual conditions, , that is also equipped with -Wiener process and a -valued -measurable random quantity, , distributed as . Finally, suppose also that satisfies

(137) for . Then the joint distribution of equals the joint distribution of .

Given this, we define and , i.e., the distributions on path-space,

| (138) |

where denotes evaluation at time and is given the topology of uniform convergence on compact sets. For , we let and .

The relative entropy can be computed via Girsanov’s theorem, together with Lemma 4:

Lemma 7

Let and suppose Assumption 2 holds. For all we have

| (139) |

where . In terms of the base process, we have

| (140) |

where and

| (141) |

A class of alternative models that are of particular case of interest is covered by the following corollary:

Corollary 6

Suppose the baseline model is the solution to the following SDE on ,

| (142) |

and the alternative model is given by

| (143) |

which includes a modified drift that depends on external data, , and is also coupled to another SDE

| (144) |

on , where and are independent Wiener processes.

Suppose also we have such that

| (145) |

where is a Wiener process independent from .

If the base, , and alternative, , systems satisfy Assumption 2, we have

| (146) | ||||

for any stopping time on . Here denotes the map that takes a path in and returns the path of the -valued component.

Appendix E UQ for General Discounted Observables

Theorem 3 can be generalized beyond the case of exponential discounting. The proof is very similar and so it is omitted.

Theorem 4

Let be a sigma-finite positive measure on , be a -stopping time, be progressively measurable, and suppose we also have one of the following two conditions:

-

1.

is a finite measure and for -a.e. .

-

2.

.

For define the progressive process . Then

Appendix F Hitting Times of Brownian Motion with Constant Drift

For the reader’s convenience, here we recall the moment generating function and distribution of hitting times for Brownian motion with constant drift; see, for example, Chapter 8 of [52] and page 196 in [34].

Lemma 8

Let be a -valued Wiener process (i.e., Brownian motion) on , , . Let be Brownian motion with constant drift . Define the level- hitting time . For any measurable we have

| (147) |

In addition, for the MGF is

| (148) |

Appendix G Expected Hitting Times of Perturbed Brownian Motion

In this appendix we bound the expected hitting times (42) for perturbations of Brownain motion of the form (40), using the techniques of Section 4.2. We assume that and have the same sign in order to ensure the hitting time is a.s.-finite under the baseline model. For a given we specialize Eq. (40) to the following:

| Alternative Models: | (149) |

This example uses the technique of Section 4.2.

The optimal bounds can be obtained directly (i.e., without using the UQ methods developed above) by combining the known distribution of [34] with the comparison principle, i.e., with

| (150) |

We assume that so that the constant-drift lower bound, and hence also the perturbed model, have a.s.-finite hitting times. This yields

| (151) |

where upper and lower bounds are achieved in the cases of constant drift perturbations and respectively.

The optimal bounds Eq. (151) provide a useful test-case for our goal-oriented UQ bounds. Eq. (149) together with Girsanov’s theorem gives a bound on the relative entropy:

| (152) |

for all ; in the language of Theorem 2, we can take and .

Using the known formula for the cumulant generating function of (see Chapter 8 of [52]) and analytic continuation, the cumulant generating function in the baseline model can be computed:

| (153) |

Therefore Corollary 4 yields

| (154) | ||||

where . The above optimization problems can be solved explicitly, with minimizers and respectively. Computing the corresponding minimum values, one finds that the UQ bounds resulting from our method, Eq. (154), are the same as the optimal bounds, Eq. (151), that were obtained from the comparison principle. We also note that, while the comparison principle is only available in very specialized circumstances, our UQ method is quite general; in particular, our method is not restricted to 1-D systems. Finally, the non-goal-oriented UQ bounds, Eq. (7), are not effective here; the non-goal-oriented relative entropy over an infinite time-horizon is , which is infinite for the constant drift perturbations .

Appendix H Vasicek Model UQ Bounds

Here we record a pair of lemmas that are needed for the analysis of option values under the Vasicek interest rate model, as well as the final UQ bound obtained by our method. See Section 5.5.1 for definitions of the notation.

Lemma 9

Suppose . Then a.s. under both the base and the alternative models.

Proof 7

The distribution of is the same under both the base and alternative models, so it does not matter which one we consider. As shown in [1], is normally distributed for all , with mean and variance

| (155) |

Using this, for any we can compute

| (156) | ||||

Therefore

| (157) |

Lemma 10

| (158) |

is a -martingale.

Proof 8

The final UQ bound on the Vasicek model obtained by the calculations in Section 5.5.1 is the following:

| (161) |

where

| (162) | |||

In creating Figure 5, the integrals over and were computed numerically via quadrature methods and the optimization over was also performed numerically; see Remark 1. Finally, note that and are, respectively, upper and lower bounds on a probability and they reflect that fact:

| (163) | |||

Appendix I American Put Options: Bounded Rate Perturbations

In this appendix, we derive UQ bounds on the value of American put options for another class of rate perturbations. This is a simpler example to analyze than the Vasicek model from Section 5.5.1 and provides a good benchmark case, as we will also have access to comparison principle bounds. We use the terminology and notation introduced in Section 5.5.

Specifically, here we consider interest rate perturbations of the following form:

| Alternative Models: | (164) |

where , , and . The parameters and define a fluctuation range, with allowing for specification of a time-dependent envelope on the fluctuation.

An elementary bound on follows from the uniform bounds together with the comparison principle:

| (165) |

Using only the information , the optimal UQ bounds can be obtained from Eq. (164) and Eq. (165), together with the exact value for the constant-rate processes, Eq. (104):

| (166) |

This provides a useful comparison for the UQ bounds derived via the methods developed above.

To use the goal-oriented method, first note the relative entropy bounds (obtained from Girsanov’s theorem):

| (167) |

is -measurable, hence we can use Theorem 2 to obtain

| (168) |

The above steps are justified by the bounds on .

The bounds on also allow us to take in Eq. (168) to obtain

| (169) | ||||

Bounding in terms of then yields

| (170) | ||||

where . The expectation can be evaluated using the known distribution of (see the discussion surrounding Eq. (105)):

| (171) | ||||

Note that all reference to the driving process , which is not coupled to , has been eliminated.

Remark 22

We show numerical results for the following scenario: Suppose the rate drops from to , and is certain to have completed this drop by time (one could also study a similar scenario where increases), but the timing and profile of the drop is otherwise unknown, i.e., we consider and to be known, and the only constraint on is . Using and , UQ bounds are obtained by combining Eq. (170) with Eq. (171).

In Figure 6 we show the resulting bounds on the option value, as a function of . Note that the bounds resulting from our UQ method are an improvement over the comparison-principle bound Eq. (166) for an initial range of , and stabilizes at a value near the comparison-principle bound for large . For large our method is sub-optimal, but still competitive. Minimizing over the parameters assigned to the baseline model (right plot) improves the bound. We find similar behavior when assuming other time-dependent envelopes of . It should again be noted that the comparison principle is available only in very special circumstances and is used here for benchmarking purposes; see Section 5.5.1 for a more realistic model where the comparison principle is not an effective tool.

Acknowledgments

The research of J.B., M.K., and L. R.-B. was partially supported by NSF TRIPODS CISE-1934846. The research of M.K and L. R.-B. was partially supported by the National Science Foundation (NSF) under the grant DMS-1515712 and the Air Force Office of Scientific Research (AFOSR) under the grant FA-9550-18-1-0214.

References

- [1] Mario Abundo, On the representation of an integrated Gauss-Markov process, Scientiae Mathematicae Japonicae 77 (2015), no. 3, 357–361.

- [2] B.D.O. Anderson and J.B. Moore, Optimal control: Linear quadratic methods, Dover Books on Engineering, Dover Publications, 2007.

- [3] David Anderson, An efficient finite difference method for parameter sensitivities of continuous time Markov chains, SIAM Journal on Numerical Analysis 50 (2012), no. 5, 2237–2258.

- [4] Georgios Arampatzis and Markos A. Katsoulakis, Goal-oriented sensitivity analysis for lattice kinetic Monte Carlo simulations, The Journal of Chemical Physics 140 (2014), no. 12, 124108.

- [5] Søren Asmussen, Olle Nerman, and Marita Olsson, Fitting phase-type distributions via the EM algorithm, Scandinavian Journal of Statistics 23 (1996), no. 4, 419–441.

- [6] R. Atar, K. Chowdhary, and P. Dupuis, Robust bounds on risk-sensitive functionals via Rényi divergence, SIAM/ASA Journal on Uncertainty Quantification 3 (2015), no. 1, 18–33.

- [7] Rami Atar, Amarjit Budhiraja, Paul Dupuis, and Ruoyu Wu, Robust bounds and optimization at the large deviations scale for queueing models via Rényi divergence, arXiv e-prints (2020), arXiv:2001.02110.

- [8] D. Bakry and M. Emery, Hypercontractivité do semi-groups de diffusion, C.R. Acad. Sci. Paris Sér I Math 299 (1984), 775–778.

- [9] Hildo Bijl and Thomas B. Schön, Optimal controller/observer gains of discounted-cost LQG systems, Automatica 101 (2019), 471 – 474.

- [10] Jeremiah Birrell and Luc Rey-Bellet, Uncertainty quantification for markov processes via variational principles and functional inequalities, SIAM/ASA Journal on Uncertainty Quantification 8 (2020), no. 2, 539–572.

- [11] M. Bladt and B.F. Nielsen, Matrix-exponential distributions in applied probability, Probability Theory and Stochastic Modelling, Springer US, 2017.

- [12] S. Boucheron, G. Lugosi, and P. Massart, Concentration inequalities, Oxford University Press, Oxford, 2013. MR 3185193

- [13] S. Boyd, S.P. Boyd, L. Vandenberghe, and Cambridge University Press, Convex optimization, Berichte über verteilte messysteme, no. pt. 1, Cambridge University Press, 2004.

- [14] T. Breuer and I. Csiszár, Measuring distribution model risk, Mathematical Finance 26 (2013), no. 2, 395–411.

- [15] , Systematic stress tests with entropic plausibility constraints, Journal of Banking & Finance 37 (2013), no. 5, 1552 – 1559.

- [16] Lawrence Brown, Noah Gans, Avishai Mandelbaum, Anat Sakov, Haipeng Shen, Sergey Zeltyn, and Linda Zhao, Statistical analysis of a telephone call center, Journal of the American Statistical Association 100 (2005), no. 469, 36–50.

- [17] K. Chowdhary and P. Dupuis, Distinguishing and integrating aleatoric and epistemic variation in uncertainty quantification, ESAIM: Mathematical Modelling and Numerical Analysis 47 (2013), no. 3, 635–662.

- [18] Thad Dankel, On the distribution of the integrated square of the Ornstein-Uhlenbeck process, SIAM Journal on Applied Mathematics 51 (1991), no. 2, 568–574.

- [19] P. Dupuis and R.S. Ellis, A weak convergence approach to the theory of large deviations, Wiley Series in Probability and Statistics, Wiley, 2011.

- [20] P. Dupuis, M.A. Katsoulakis, Y. Pantazis, and P. Plecháč, Path-space information bounds for uncertainty quantification and sensitivity analysis of stochastic dynamics, SIAM/ASA Journal on Uncertainty Quantification 4 (2016), no. 1, 80–111.

- [21] Paul Dupuis, Markos A. Katsoulakis, Yannis Pantazis, and Luc Rey-Bellet, Sensitivity analysis for rare events based on Rényi divergence, Ann. Appl. Probab. 30 (2020), no. 4, 1507–1533.

- [22] B. Engelmann and R. Rauhmeier, The Basel II risk parameters: Estimation, validation, stress testing - with applications to loan risk management, Springer Berlin Heidelberg, 2011.

- [23] M. J. Faddy, Examples of fitting structured phase–type distributions, Applied Stochastic Models and Data Analysis 10 (1994), no. 4, 247–255.

- [24] M.I. Freidlin, Functional integration and partial differential equations. (AM-109), volume 109, Annals of Mathematics Studies, Princeton University Press, 2016.

- [25] V. Girardin and N. Limnios, On the entropy for semi-Markov processes, Journal of Applied Probability 40 (2003), no. 4, 1060–1068.

- [26] P. Glasserman, Monte Carlo methods in financial engineering, Stochastic Modelling and Applied Probability, Springer New York, 2013.

- [27] P. Glasserman and X. Xu, Robust risk measurement and model risk, Quantitative Finance 14 (2014), no. 1, 29–58.

- [28] Peter W. Glynn, Likelihood ratio gradient estimation for stochastic systems, Commun. ACM 33 (1990), no. 10, 75–84.

- [29] K. Gourgoulias, M. A. Katsoulakis, L. Rey-Bellet, and J. Wang, How biased is your model? Concentration inequalities, information and model bias, IEEE Transactions on Information Theory 66 (2020), no. 5, 3079–3097.