A Free Boundary Characterisation of the Root Barrier for Markov Processes

Abstract

We study the existence, optimality, and construction of non-randomised stopping times that solve the Skorokhod embedding problem (SEP) for Markov processes which satisfy a duality assumption. These stopping times are hitting times of space-time subsets, so-called Root barriers. Our main result is, besides the existence and optimality, a potential-theoretic characterisation of this Root barrier as a free boundary. If the generator of the Markov process is sufficiently regular, this reduces to an obstacle PDE that has the Root barrier as free boundary and thereby generalises previous results from one-dimensional diffusions to Markov processes. However, our characterisation always applies and allows, at least in principle, to compute the Root barrier by dynamic programming, even when the well-posedness of the informally associated obstacle PDE is not clear. Finally, we demonstrate the flexibility of our method by replacing time by an additive functional in Root’s construction. Already for multi-dimensional Brownian motion this leads to new class of constructive solutions of (SEP).

1 Introduction

We study the Skorokhod embedding problem for Markov processes evolving in a locally compact space . That is, given measures and on , the task is to find a stopping time such that

| (SEP) |

Throughout this article we are interested in non-randomised stopping times, that is is a stopping time in the filtration generated by . When is a one-dimensional Brownian motion, this problem has received much attention, partly due to its importance in mathematical finance [42]. In this case, there exists a wealth of different stopping times that solve SEP, see [51] for an overview. One of the most intuitive solutions is due to Root [57]: for a one-dimensional Brownian motion and , in convex order, there exists a space-time subset – the so-called Root barrier – such that its hitting time by solves SEP. More recently, connections with obstacle PDEs [23, 28, 33, 34, 38], optimal transport [3, 5, 6, 7, 20, 37, 39, 40], and optimal stopping [23, 25] and extensions to the multi-marginal case [4, 22, 56] have been developed.

However, already for multi-dimensional Brownian motion much less is known about solutions to SEP, see for example work of Falkner [30] that highlights some of the difficulties that arise in the multi-dimensional Brownian case. For general Markov processes the literature gets even sparser: Rost [58, 59] developed a potential theoretic approach to previous work of Root, but in general this shows only the existence of a randomised stopping time for SEP when and are in balayage order. Subsequent works of Chacon, Falkner, and Fitzsimmons, [18, 30, 32], expand on these results and provide sufficient conditions for the existence of a non-randomised stopping time; however, in none of these works the question of how to compute these stopping times for a given sample trajectory is addressed. Another approach is the application of optimal transport to SEP as initiated by Beiglböck, Cox, Huesmann [3]. This covers Feller processes but verifying the assumptions can be non-trivial. More importantly, the optimal transport approach currently only addresses the existence and optimality of a stopping time but not its computation. Besides these two approaches – (Rost’s) potential theoretic approach and the optimal transport approach – we are not aware of a general methodology that produces solutions to SEP for Markov processes.

Contribution.

We focus on the large class of right-continuous transient standard Markov processes satisfying a duality assumption and absolute continuity of the semigroup. Our main result is Theorem 3.6 which extends Rost’s results and shows existence of a non-randomised Root stopping time and, more importantly, represents the Root barrier as a free boundary via the semigroup of the dual space-time process. This allows to apply classical dynamic programming to calculate the Root barrier for a large class of Markov processes. Theorem 3.6 also implies that if a PDE theory is available that ensures the well-posedness of the free boundary problem formulated as PDE problem, then numerical methods for PDEs can be used to compute the barrier. However, in general this requires much stronger assumptions on the Markov process, e.g. when the generator involves non-local terms as is already the case for one-dimensional Lévy processes, the well-posedness of such PDEs is an active research area.

We present a series of examples of processes to which our result applies. The most important one is arguably multi-dimensional Brownian motion (or more generally, hypoelliptic diffusions), but we also discuss stable Lévy processes and Markov chains on a discrete state space. In all these cases our result allows to compute the Root barrier, and we present several numerical experiments to illustrate this point.

Finally, we show that our approach is flexible enough to construct new classes of solutions to the Skorokhod embedding problem: instead of hitting times of the space-time process , we discuss hitting times of where is an additive functional of of the form . We expect that such an approach holds in much greater generality for other functionals and leave this for further research.

Outline.

The structure of the article is as follows: Section 2 introduces notation and basic results from potential theory, Section 3 contains the statement of our main result and Section 4 contains its proof. Section 5 then applies this to concrete examples of Markov processes and computations of Root barriers. Section 6 discusses how these results can be used to construct new solutions of SEP. In Appendix A and Appendix B we will present fundamental results from classical potential theory used throught this article and in Appendix C we discuss details around applying our result to Brownian motion in a Lie group.

2 Notations and assumptions

We briefly recall notations from potential theory, mostly following the presentation in Blumenthal and Getoor [12]. A detailed description can be found in Appendix A. Throughout, is a locally compact metric space with countable base and is the Borel--algebra on . In addition, we write for the -algebra of universally measurable sets and for the -algebra of nearly Borel sets, see Definition A.1.

Let denote a filtered probability space that carries a stochastic process . To allow for killing we add an absorbing cemetery state to the state space, that is we define and for all if , then for all . Denote with the lifetime of the process. Each is then a probability measure on paths with , -a.s for all . Furthermore, for let be the natural shift operator of the the process, i.e. for all . Throughout, we assume that is a standard process, see Definition A.2, in particular we assume that has càdlàg paths and satisfies the strong Markov property. We write for the Markovian transition semigroup of and for its potential and write as usual , , and for the actions on Borel functions and Borel measures on . For an -stopping time , we write and for first hitting times of A, we write . We write for the regular points of a nearly Borel set , see Table 3 in Appendix A.

A central role will be played by lifting to a space-time process , that is with , with the space-time semigroup acting on Borel functions and Borel measures on as follows:

where , , and .

Duality.

Throughout this paper we make the following assumption,

Assumption 2.1.

There exists a standard process with semigroup on the same probability space, and some -finite measure on such that for all and -measurable,

| (2.1) |

Furthermore, the semigroups of and are absolutely continuous with respect to ,

| (2.2) |

Remark 2.2.

Relation (2.1) is referred to in the literature as weak duality. The processes and are said to be in strong duality with respect to (as defined in [12, Ch. VI] or [19, Ch.13]), if, in addition to (2.1), the resolvent kernels are absolutely continuous with respect to . This is weaker than the absolute continuity of the semigroup, so that in particular, strong duality of and holds under Assumption 2.1.

We write and for the semigroup and potential kernel of , and we denote the actions of these operators on Borel functions and measures on the other side as for , i.e. , and . Furthermore, we use the prefix “co” for the corresponding properties relating to , e.g. coexcessive, copolar, cothin, etc., and we write and for the coregular points of a measurable set .

By [36, 65], absolute continuity of the semigroups implies that the corresponding space-time processes , and , where , are in strong duality with respect to the measure , where is the Lebesgue measure on the real line. We denote by the semigroup corresponding to the space-time process . For every and --measurable function ,

In addition, there exists a Borel function such that for all and in , and , and satisfies the Kolmogorov–Chapman relation

| (2.3) |

The function is excessive in (for each fixed ), coexcessive in , and is a density for and .

Note that the duality assumption implies by [12, Ch. IV, Prop. (1.11)]) that a measure is excessive if and only if it has a density which is coexcessive and finite -almost everywhere. Hence, the density of the potential with respect to is given by the (coexcessive) potential function .

| semigroup | ||||

|---|---|---|---|---|

| potential function | ||||

| potential measure | ||||

Remark 2.3.

The functions which are (co-)excessive with respect to , , and are actually Borel-measurable. Indeed, strong duality of the corresponding processes guarantees the existence of a so-called reference measure333a -finite measure is a reference measure for if for all Borel , ( for all ) . (for more details see [12, Ch. VI]). In this case Proposition (1.3) in [12, Ch. V] implies that excessive functions are Borel-measurable.

We repeatedly use the following classical result,

Proposition 2.4 (Hunt’s switching formula, [12, VI.1.16]).

Let , be standard processes in strong duality. Then for all Borel-measurable , one has , i.e. for all ,

Remark 2.5.

The dual process can be thought of as running backwards in time. In fact, strong duality implies that for non-negative bounded Borel functions and it holds

More generally and ignoring technicalities (see [19, Ch.13] for details), if we take to be the canonical probability space and let denote the right-continuous time reversal at time , that is is given as , then for any that is -measurable

Informally, strong duality of with another standard process requires that two conditions are met: (i) admits an excessive reference measure, (ii) the right-continuous version of its time reversal is a standard process and in particular satisfies the strong Markov property. We refer to [19, Ch. 15] and [62] for a detailed discussion.

Remark 2.6.

A practical approach to obtain Markov processes in duality is via Dirichlet forms. Given a Markov process with generator , this consists in considering the bilinear form

extended to a suitable class of functions . The theory of Dirichlet forms, see e.g. [49], then provides sufficient analytic criteria on so that it is associated to a pair of (standard) Markov processes in weak duality with respect to . It is also possible to obtain existence (and further properties) of transition densities for a Markov semigroup by considering functional inequalities (such as Nash inequality) satisfied by the associated Dirichlet form, see e.g. [17].

3 A free boundary characterisation

Definition 3.1 (Root barrier).

A subset of is called a Root barrier for if is nearly Borel-measurable with respect to the space-time process and

We call the first hitting time the Root stopping time associated with .

Dealing with the regularity of is a central theme of this article and it is useful to introduce “right-” and “left-”continuous modifications and of .

Definition 3.2.

For a Root barrier denote with

the section at time . We define as

Remark 3.3.

An equivalent definition of the barrier is that the mapping is non-decreasing. This also implies that and are barriers as well. As is nearly Borel-measurable with respect to then so are the shifted barriers for any , as then

Definition 3.4 (Balayage order).

Two probability measures and are in balayage order, if their potentials and satisfy

| (3.1) |

In this case we will write and say that is before .

Remark 3.5.

We now state our main result,

Theorem 3.6.

Let be a Markov process for which Assumption 2.1 holds. Let be two measures such that and are -finite measures and such that charges no semipolar set. If then there exists a Root barrier for such that

Moreover, if we set

| (3.3) |

then

-

(1)

,

-

(2)

for any Borel set and ,

-

(3)

in the above we may take

Besides existence and optimality of a Root stopping time, the main interest of Theorem 3.6 is that item (3) provides a way to compute the Root barrier for a large class of Markov processes ranging from Lévy processes to hypo-elliptic diffusions, see the examples in Section 5. Concretely, it allows to use classical optimal stopping and the dynamic programming algorithm to compute and hence . We state this as a corollary:

Corollary 3.7.

Using the same notation and assumptions as in Theorem 3.6 it holds that

-

(1)

is the value function of the optimal stopping problem

(3.4) where the supremum is taken over stopping times taking values in .

-

(2)

If we define for the function on by

then for each , ,

Informally, is the solution of the obstacle problem

| (3.5) |

where is the generator of the dual process . However, to make this rigorous is in general a subtle topic since the obstacle introduces singularities. Several notions of generalised PDE solutions ranging from variational inequalities to viscosity solutions address this, often together with numerical schemes [1, 44, 45, 52]. This PDE approach to Root’s barrier has been carried out in [23, 34] for one-dimensional diffusions. However, already in the one-dimensional case when the operator involves non-local terms as is the case for many Markov processes, the well-posedness of such obstacle PDEs is an active research area; see e.g. [2, 16]. In general, this PDE approach requires stronger assumptions than Assumption 2.1 for the well-posedness of (3.5); in stark contrast, Corollary 3.7 holds in full generality of Theorem 3.6.

Remark 3.8 (Minimal residual expectation).

Item (2) of Theorem 3.6 was named minimal residual expectation by Rost [60] with respect to . It implies that

This is actually an equivalent formulation of the minimal residual expectation property as soon as is finite as then this quantity is equal to for all solutions of SEP. Furthermore, Rost proved in [60] that any stopping time which is of minimal residual expectation with respect to necessarily satisfies -a.s.

Remark 3.9 (Recurrent Markov processes).

That and are -finite is a kind of transience assumption, and is usual in this context [32, 60]. In the case of one-dimensional Brownian motion or diffusions it is not necessary, see [23, 34]. We expect that our result could be extended to the recurrent case (at least in some special cases), but this would require a certain amount of work, see e.g. [30] for results for two-dimensional Brownian motion.

Remark 3.10 (Assumptions of Theorem 3.6).

From the counterexamples discussed in [30, 32], to obtain solutions to SEP as non-randomised stopping times, one needs to make:

-

(1)

an assumption on the process in order to avoid “deterministic portions” in the trajectory. In our case, this is reflected in the assumption of absolute continuity (2.2). This assumption is rather strong but can often be checked in practice. In the case of diffusions, the celebrated Hörmander’s criterion [43] gives a simple condition to ensure existence of transition densities with respect to Lebesgue measure. For jump-diffusions, there are also many results providing sufficient criteria for absolute continuity, see for instance [9, 53].

-

(2)

an assumption on the “small” sets charged by initial and target measures (to avoid issues as in the case of multidimensional Brownian motion and Dirac masses). This is why we assume that charges no semipolar sets. Without this assumption, it is not true that there exists a solution to SEP as hitting time of a barrier, or even as an non-randomised stopping time. In the case where all semipolar sets are polar, following [31], we can replace the assumption that charges no (semi)polar set by the assumption that

(3.6) Indeed, there exists then a polar set , and a measure supported on , supported on with , , and charges no polar sets (cf. [31, p.50]). Letting be a barrier embedding into as given by Theorem 3.6, let , then embeds into . In [31] is proven that (if semipolar sets are polar), (3.6) is a necessary condition for a non-randomised solution to SEP to exist (in the case where but (3.6) does not hold, randomisation of the stopping time at time is necessary).

4 Proof of Theorem 3.6

The proof of our main result, Theorem 3.6, is split into two parts:

- Existence.

-

We first show that a Root barrier exists such that and that items (1) and (2) of Theorem 3.6 hold. Here we rely on classic work of Rost, [60], that shows that SEP has as solution stopping time that lies between the hitting times of two barriers which differ only by a space-time graph. We show that these hitting times are necessarily equal; a similar approach was already followed in [3, 18, 34] under different assumptions.

- Free boundary characterisation.

-

We show item (3) of Theorem 3.6, that is that one can take the contact set of the obstacle problem (3.5) as the Root barrier. From a conceptual point of view, this is similar to the case of one-dimensional diffusions as studied with PDE methods in [23, 34]. However, there the analysis is greatly simplified due to the existence of local times. Since local times are not available in our setting, the situation becomes more delicate and requires the analysis of negligible sets via potential theory.

4.1 Existence

We prepare the proof of existence and optimality with two lemmas. The first lemma shows right-continuity of the semigroup when applied to bounded Borel-measurable functions.

Lemma 4.1.

Under Assumption 2.1, it holds for all Borel-measurable and bounded functions , for all and

| (4.1) |

Proof.

First, note that if is continuous then by a.s. right continuity of it is clear that is right continuous as a function of .

Let . Since , by de La Vallée Poussin’s theorem (see e.g. [26, Thm. II.22] 444The de La Vallée Poussin’s theorem in literature is given in finite measure spaces. That is infinite is clearly not a problem here. If necessary consider the finite measure , applying the theorem to that measure gives that for some superlinear , . there exists a function which is strictly convex and superlinear (i.e. ) such that

| (4.2) |

Then for all one has

where we first used Kolmogorov-Chapman’s equality (2.3), then Jensen’s inequality and that it holds by duality. Since is -finite, there exists a countable increasing family of open sets such that and for all .

Now fix . On the integrability condition as in (4.2) is satisfied for all functions in the family . By the de La Vallée Poussin’s theorem this is equivalent to being uniformly integrable in .

Then, by the Dunford-Pettis theorem (see e.g. [26, Thm. II.23]), uniform integrability of implies that it is weakly (relatively) compact in the finite measure space . By a diagonal argument there exists a subsequence and a measurable function such that for all , for all bounded and measurable one has for . If we take as a continuous function supported in , by right-continuity of the sample paths, we obtain that . In addition, since is closed, by a.s. right-continuity of , one has that

Hence if is measurable and bounded by ,

Letting , the right-hand side goes to by dominated convergence. Hence converges weakly in to . We can use the same line of argument for every subsequence of any sequence to argue the convergence of a subsubsequence. Therefore for all we have that converges weakly in to for which leads to the required statement.

∎

The second Lemma revisits Chacon’s idea of “shaking the barrier”, see also [3, 18] for similar statements under slightly stronger assumptions.

Lemma 4.2.

If the semigroup of a Markov process satisfies (4.1), then for all Root barriers one has almost surely

| (4.3) |

Proof.

Firstly, by replacing with if necessary, it is enough to show that almost surely. Secondly, if we define

we have . Put together, this implies that it is sufficient to show that for all , -a.s. and below we assume that for a given .

For define

| (4.4) |

That is, is the barrier that arises by shifting in time to the left if [resp. to the right if ]. Now since ,

and for any we also have

Now set and use the above identities to deduce that for every and every ,

From the right-continuity of the semigroup, Lemma 4.1, it follows that

But since -a.s. for all and for all , this already implies that

and we conclude that since ∎

For the proof of existence and optimality, we rely on the following result obtained by Rost:

Theorem 4.3 (Rost, Theorems 1 and 3 in [60]).

If , then there exists a (possibly randomised) stopping time which is of minimal residual expectation with respect to , i.e. and

| (4.5) |

In addition, the measure

is given by the -réduite of the measure

Furthermore, there exists a finely closed Root barrier such that -a.s.:

-

(1)

,

-

(2)

.

The key ingredients in the proof of Rost’s theorem are the filling scheme from [59], which allows to obtain the existence of satisfying the optimality property (4.5), and then a paths-swapping argument (see [42] for a heuristic description), which shows that is almost the hitting time of a Root barrier (i.e. (1) and (2) above). However, this does not imply that is the hitting time of a Root barrier.

In order to conclude item (1) from Theorem 3.6, we first see that Lemma B.3 yields

| (4.6) |

We will prove in Lemma 4.4 that is -excessive. Therefore, if we show that is -excessive then (4.6) holds everywhere. For this we need to show that satisfies as . But this follows from the definition since

Secondly, from , it also follows from Theorem 1 in [60] that is the unique stopping time minimising for all among all stopping times embedding in .

Furthermore, in (2) from Theorem 4.3 by Rost implies on . If we have and if then , so that combined we get

where we used that is semipolar and that by assumption charges no semipolar sets. Hence combined with item (2) from Theorem 4.3, one has , and we can conclude the existence of a solution satisfying items (1) and (2) in Theorem 3.6 with Lemma 4.2.

4.2 Free boundary characterisation

Let be the unique Root stopping time solving SEP from the previous section with the respective Root barrier . We want to prove with , where is defined as in Theorem 3.6

The proof is split into two inequalities given in Proposition 4.5 and Proposition 4.7. First, we show some useful properties of the Root barrier :

Lemma 4.4.

The function and the resulting Root barrier satisfy the following properties:

-

(1)

is -excessive and non-increasing in ,

-

(2)

is a Borel-measurable and -finely closed Root barrier.

Proof.

For (1), note that any function is -finely continuous if and only if the process is -a.s. right continuous for all (see e.g. [12, Theorem (4.8)]) . As in the obstacle , we have the -finely continuous functions and making (when ) and (when ) -a.s. right-continuous for all . Furthermore, is right continuous at which together makes -finely continuous. By Proposition B.2 it then follows that is -excessive. Further, is non-increasing in since is non-increasing.

For (2), note that the -excessive function is Borel-measurable, see Remark 2.3, and the barrier is a level set of the Borel-measurable function , hence it is Borel-measurable. Therefore is -finely closed since it is the set where the two finely-continuous functions and coincide, and it is a barrier by time monotonicity of .

∎

Proposition 4.5.

.

Proof.

Since by Lemma 4.2, we only need to prove . Since is -finite, is polar (cf. [12, (3.5)]). Let be such that and . One has

| (4.7) |

and since on as is non-decreasing, we can apply the Markov property to obtain

By the switching identity (Proposition 2.4) and since we have

| (4.8) |

for all and hence

| (4.9) |

Thus, we can conclude that .

Now for any , if , . Since is semipolar, and since charges no semipolar sets, it follows that a.s. . By the previous paragraph, this means that . Hence . ∎

Before we prove the inverse inequality, we first need a preliminary lemma:

Lemma 4.6.

Assume that for some measure which charges no semipolar sets, some stopping time and some nearly Borel-measurable set one has on . Then , almost surely.

Proof.

We first write

where we have used in the first inequality that is coexcessive and in the following equality, that the coexcessive functions and coincide on and therefore also on its cofine closure on which is supported. The last equality follows by the switching identity.

Therefore it holds that , i.e. the measures and are in balayage order. We then follow the proof of [60, Lemma p.8]. By [59], since , there exists a stopping time (possibly on an enlarged probability space) which is later than such that the process arrives in the measure at time , i.e. -a.s. and . We can assume without loss of generality that is finely closed and then this implies that . In particular, if , then we have -a.s. However, since it holds that -a.s., so that . Since would be a contradiction to , we conclude that , and therefore -almost surely.∎

Proposition 4.7.

.

Proof.

We first show that for all , one has . For this we first prove

| (4.10) |

where for fixed the stopping time is the hitting time of shifted in time by . This holds since for all Borel-measurable functions it holds

Since on , it holds that . Furthermore, we know that by definition of we have on , since is non-decreasing. As since does not charge semipolar sets, it holds that . Together this implies .

5 Examples

In this section we apply Theorem 3.6 to concrete Markov processes. The examples are

- Continuous-time Markov chains.

-

This is a toy example but we find it instructive since many abstract quantities from potential theory become very concrete and simple; e.g. the obstacle PDE reduces to a system of ordinary differential equations.

- Hypo-elliptic diffusions.

-

This is a large and important class of processes. In the one-dimensional case we recover the setting of [23, 34] but for the multi-dimensional case the results are new to our knowledge. As concrete example we give a Skorokhod embedding for two-dimensional Brownian motion and Brownian motion in a Lie group.

- -stable Lévy processes.

-

There is very little literature on the Skorokhod embedding problem for Lévy processes, see [27] for references. We apply our results to -stable Lévy processes which are of growing interest in financial modelling, see e.g. [63], as they are characterised uniquely as the class of Lévy processes possessing the self-similarity property. Due to the infinite jump-activity such processes are hard to analyse but potential theoretic tools are classic in this context and much is known about their potentials, see [8, 11, 14, 47].

Two remarks are in order: firstly, the question to characterise or even construct measures that are in balayage order for a given Markov process seems to be a difficult topic. In the case of one-dimensional Brownian motion this reduces to the convex order which is usually easy to verify but already for multi-dimensional Brownian motion it can be (numerically) difficult to check if two given measures are in balayage order. Secondly, we reiterate the discussion after Corollary 3.7 that the PDE formulation usually requires stronger assumptions whereas the discrete dynamic programming algorithm, Corollary 3.7, applies to Theorem 3.6 in full generality. All our examples were computed using the dynamic programming equation stated as item (2) in Corollary 3.7.

5.1 Continuous-time Markov chains

Let be a discrete-time Markov chain on a discrete state space and transition matrix such that for all and a probability measure . Imposing -distributed waiting times at each state, we arrive at the continuous-time Markov chain with transition function

| (5.1) |

The process is dual to the continuous-time Markov chain with transition matrix and the same transition rate at each state with respect to the counting measure. The potentials are given with respect to the function

| (5.2) |

and the potential function of a measure is given by

| (5.3) |

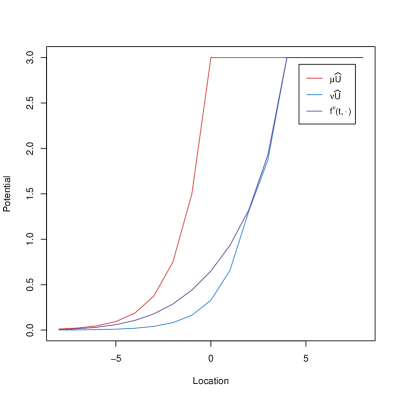

Example 5.1 (Asymmetric random walk on ).

Let be the asymmetric random walk on , that is and . By translation invariance and a standard result (see e.g. [54]) it then holds for the potential kernel of

| (5.4) |

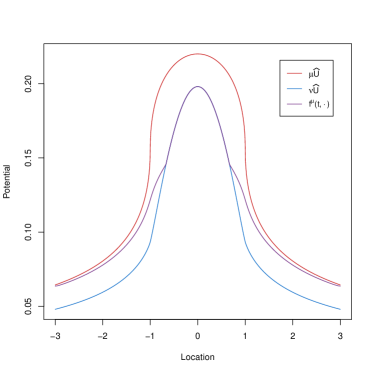

Now let and for some , , and . Then

| (5.5) |

Since , we have for all such . The generator of is given by

| (5.6) |

and the obstacle problem (3.5) reduces to the following set of ODEs:

Then either classical methods for solving this set of coupled ODEs can be applied or we can directly apply the dynamical programming approach as in Corollary 3.7 as follows: For small enough, we choose such that . We approximate the function on the set at discrete time points for fixed :

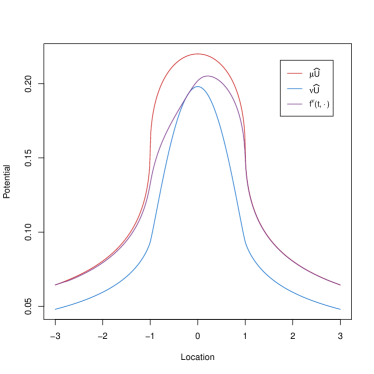

For example, we take , and . Figure 1 show the potentials , and the resulting Root barrier.

5.2 Hypo-elliptic diffusions

Let be the diffusion in obtained by solving an SDE formulated in the Stratonovich sense

| (5.7) |

where the , , are vector fields on which we assume to be smooth with all derivatives bounded, and is a standard Brownian motion in . We further assume that is killed at rate , where is a nonnegative smooth function. is then a standard Markov process on , with generator which acts on smooth functions via

where the and ’s are smooth functions which can be written explicitely in terms of the . The formal adjoint of with respect to Lebesgue measure is then given by

and we can choose smooth vector fields ’s such that . Assuming that

| (5.8) |

we can then identify with the generator of the Markov process consisting of the Stratonovich SDE

| (5.9) |

killed at rate .

In addition, assume that the vector fields satisfy the weak Hörmander conditions

| (5.10) |

| (5.11) |

then the classical Hörmander result [43] yields that the semigroups , associated to , admit (smooth) densities with respect to Lebesgue measure. Therefore, and are in duality with respect to Lebesgue measure, as seen by

which yields that , first for smooth with compact support and then for all Borel measurable by an approximation argument. In conclusion, we have obtained the following.

Proposition 5.2.

Example 5.3 (Brownian motion in ).

For , as Brownian motion is recurrent, for any positive Borel function we have either or . Therefore we consider the Brownian motion killed when exiting the unit ball , i.e. . For any probability measure with density supported on , the potential is the unique continuous solution of on vanishing on , and is given explicitely as , where

| (5.12) |

In dimensions , Brownian motion is transient, and the potential is the Newtonian potential on :

| (5.13) |

where . For the balayage order reduces to the convex order which is easy to verify. In higher dimensions it is in general non-trivial to find measures in balayage order.

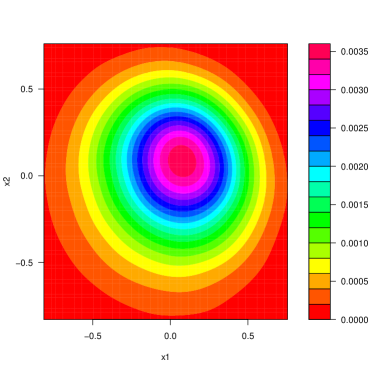

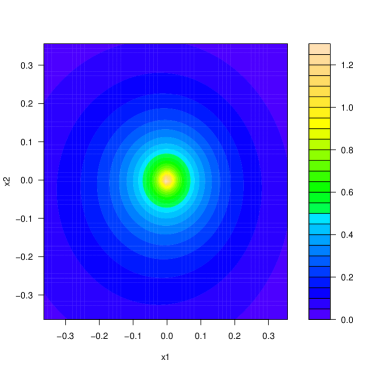

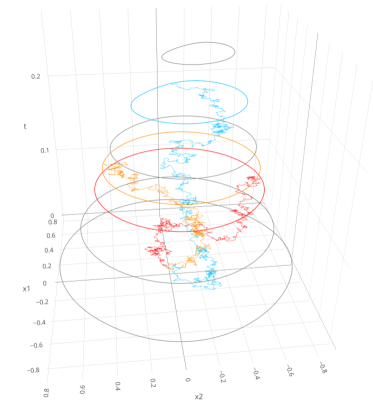

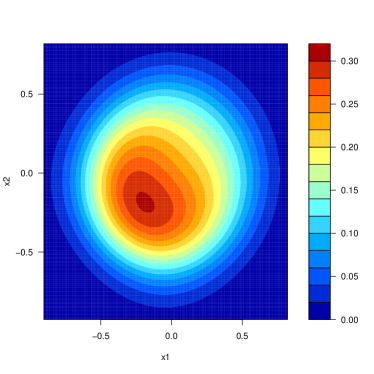

Now we consider the two-dimensional Brownian motion starting in 0. As an example for a measure which is not rotational symmetric and can be embedded in the two-dimensional Brownian motion, we take as the measure with the following density as an approximation of the marginal of the diffusion which is generated by the operator , here ,

where denotes a normalising constant, , and . The (empirical) density is respresented in Figure 2(a) on page 2. We take of this form since can be obtained as a time change via an additive functional of which implies (we will show this explicitly in Section 6) and we see in 2(b).

Example 5.4 (Lie-group valued Brownian motion).

Let be a two-dimensional Brownian motion. Then can be identified (after taking the Lie algebra exponential), as a Brownian motion in the free nilpotent Lie group of order 2; see Appendix C for details and extension to general free nilpotent groups. The generator of the process is the sub-Laplacian on the Heisenberg group ; where in coordinates

As shown by [35, 48], the transition density equals

| (5.14) |

and by Brownian scaling . In this case, it is already non-trivial to find measures in balayage order, , even if is a Dirac at the origin. However, Proposition C.1 in the appendix shows that any measure on can be lifted to a measure on such that . This provides a rich class of probability measures in balayage order, and Theorem 3.6 allows to apply dynamic programming to compute the Root barrier solving SEP. However, this is computationally expensive since (5.14) is not available in closed form. In this case, the well-posedness of the obstacle PDE

can be shown by standard methods (such as viscosity solutions). Again this leads to non-trivial numerics555We would like to thank Oleg Reichmann and Christian Bayer on helpful conversations and numerical experiments., even after using the radial symmetry of (5.14) to reduce the space dimension to 2, namely radius and area. Nevertheless, both approaches (dynamic programming and PDE) are applicable to compute barriers for group-valued Brownian motion, although much work remains to be done to turn this into a stable numerical tool and we leave this for future research.

5.3 Symmetric stable Lévy processes

A right-continuous stochastic process is called an -stable Lévy process, if it has independent, stationary increments which are distributed according to an -stable distribution. We consider the symmetric case without drift. In this case, the characteristic component is given by , i.e. and hence satisfies the scaling property . Classic results, e.g. [41], show that has a transition density

which is absolutely continuous with respect to the Lebesgues measure. For further properties of symmetric stable processes, we refer to [11]. We are going to take , as in this case is transient, as shown in [14]. Furthermore, one-dimensional Lévy processes are dual to with respect to the Lebesgue measure (see [8]). Since the jumps are distributed according to the symmetric stable distribution, the symmetric stable process is self-dual. By [12] the potential equals

| (5.15) |

where in the one-dimensional case . In order to construct the Root stopping time, we construct the function as described in Theorem 3.6 as solution to the obstacle problem

where the generator of the process is given by the fractional Laplacian

| (5.16) |

with denoting a principal value integral.

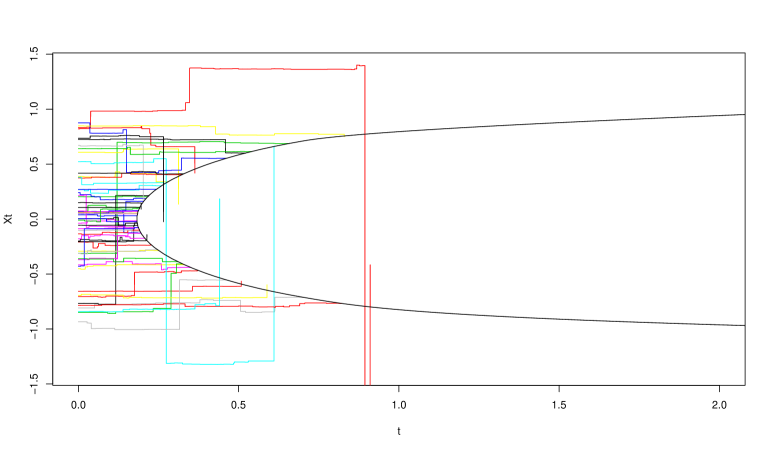

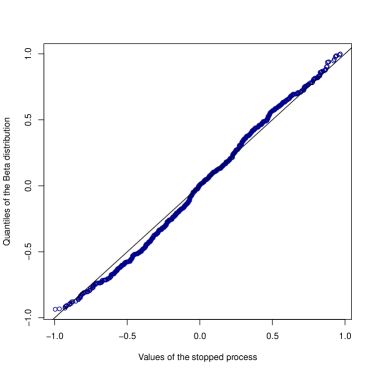

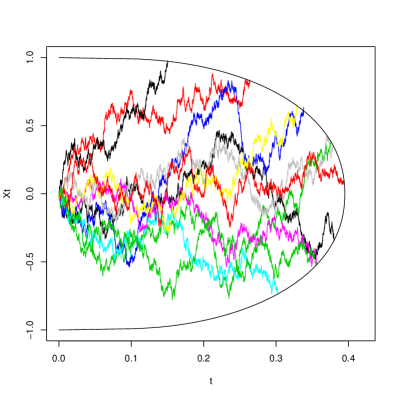

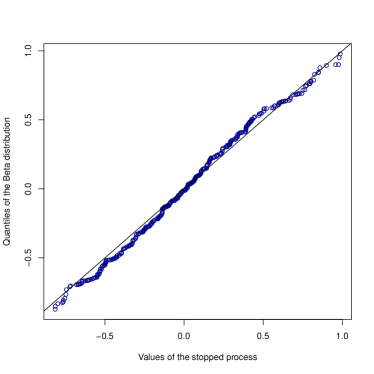

Example 5.5 (Embedding for , and ).

Let be the Uniform distribution on , then

| (5.17) |

We want to construct a solution for SEP where the density of is given by , where

| (5.18) |

is the density of a Beta distribution on the interval . Realisations of the resulting embedding will then give us that on the event where , the stopped values are distributed according to the Beta distribution. Studying general numerical methods for the fractional Laplacian is beyond the scope of this article, so we just discuss a quick method which is adapted to our case. We can rewrite (5.16) as

| (5.19) |

Define the set for large and , where , are chosen large enough. The space-time mesh grid is defined as

For the resulting minimal excessive majorant of we expect that never touches outside as this is the support of . Indeed, a straightforward calculation shows that starting in , for we have , i.e. the repeated action of the fractional Laplacian on outside an interval with large enough is negligible. For any we define the operator

where is the evaluation of the fractional Laplacian using a Gauß-Kronrod quadrature as described in [24] on . Then the minimal excessive majorant for Theorem 3.6 can be computed on as follows:

| (5.20) |

In Figure 3 on page 3, we can see a realisation of the embedding for SEP with and as given above. As for small values of , the trajectories of may have large jumps, for the simulations we need to take into consideration that may jump back in the barrier although it already left the support of . Following the results from [13, 46], the probability of not returning to after reaching level is

| (5.21) |

6 Towards generalised Root embeddings

The results of the previous sections, rely on Root’s and Rost’s approach to lift to a space-time process

and find a solutions of SEP that are given as a hitting time of . A natural generalisation is to replace the time-component by another real-valued, increasing process with , such that is again Markov and carry out a similar construction. That is, to construct a set such that its first hitting time by the lifted process

solves SEP. Again, one expects such a stopping time to be optimal in a minimal residual expectation sense, however, now formulated in terms of .

Carrying out this program in full generality is beyond the scope of this article. Instead, we focus on the case when is of the form where is strictly positive. Denote with the first hitting time of by and with the time-changed process. Since for every (sufficiently nice) set

this allows us to use the framework of the previous sections. Concretely, one needs to verify that the assumptions of Theorem 3.6 are met by . This already provides a new class of solutions for SEP. It can be seen as an interpolation between the Root embedding (when ) and the classical Vallois embedding [64], since when applied to a Brownian motion, the classical Vallois embedding can be identified as the limiting case when approaches a Dirac at .

6.1 Generalised Root embeddings

Below we restrict ourselves to additive functionals of the form

with a Borel measurable which is locally bounded and locally bounded away from , so that is one-to-one and the measure is -finite. This implies that is an additive functional of , i.e. satisfies

-

(1)

, is right continuous and non-decreasing, almost surely,

-

(2)

is -measurable,

-

(3)

almost surely for each .

We can then define the time-changed process as follows

By [29, Theorem 10.11], is a standard process. Its potential is given by

and we can define the potential operator for any non-negative Borel-measurable function which corresponds to the time-changed process , where we analogously define with . In addition, strong duality holds,

Theorem 6.1 (Revuz, Thm. V.5 and Thm. 2 in VII.3 in [55]).

The processes and are in strong duality with respect to the so-called Revuz measure .

Remark 6.2.

From the duality with respect to the Revuz measure , it follows for any Borel measure and that

Hence, , i.e. the potentials of the measures of the original and the time-changed process are equal. However, note that .

To apply our main result to the time-changed process we make the following assumption, which we will discuss later in this section.

Assumption 6.3.

For all and , the transition functions of and are absolutely continuous with respect to , i.e. and .

Combining the above duality results with our main Theorem 3.6 then gives us the following new solution of SEP.

Theorem 6.4.

Let be a Markov process and an additive functional for which Assumption 2.1 and Assumption 6.3 hold. Let be two measures with -finite potentials in balayage order, i.e. , and such that charges no semipolar set. Then there exists a Root barrier which embeds such that its first hitting time embeds into ,

Moreover, if we denote

| (6.1) |

where denotes the space-time semigroup associated with , then

-

(1)

,

-

(2)

for all Borel sets and ,

-

(3)

We may take .

Proof.

By Remark 6.2, implies for the time-changed process . We henceforth write for the visits of a nearly Borel set during the lifetime of . Then the set is semipolar if and only if the set is almost surely countable. Further we have

since the mapping is continuous and strictly increasing because is. Therefore, any set which is semipolar for is also semipolar for and does not charge sets which are semipolar for .

Due to Assumption 6.3, the processes and and the measures and satisfy the assumptions of Theorem 3.6. Then and defined as above are exactly the equivalent results from Theorem 3.6 for and the stopping time solving SEP is given by

Then for as in (6.1), we have is the density of the measure w.r.t. . If we define , then for any nearly Borel set we obtain and it follows that for any solution to SEP, we have that is a solution for SEP. The optimality of Property 2 then naturally follows.

Finally, since , for , we know that

which completes the proof. ∎

Remark 6.5.

Assumption 6.3 does not always hold, even under Assumption 2.1. For instance, let be the Markov process given by

where is non-negative, bounded, smooth with (for instance) strictly positive, and is a linear Brownian motion. Then by the weak Hörmander criterion, admits transition probabilities with respect to Lebesgue measure and satisfies Assumption 2.1. However taking the time-change corresponding to , the resulting process satisfies

which does not admit transition probabilities.

Remark 6.6.

Let be the diffusion with generator given in Hörmander form by

(with for instance the ’s with bounded derivatives of all order), then (assuming also smooth,say) the generator of is given by

for some vector field . In particular, if the following strong Hörmander condition holds for :

it also holds for the generator of , in which case admits transition probabilities with respect to Lebesgue measure. This condition is for instance satisfied when is multi-dimensional Brownian motion (or more generally, Brownian motion on a Carnot group).

Remark 6.7 (Obstacle PDE).

The generator of the time-changed process is given by , see [29]. Hence, we can again identify as the solution to the obstacle problem

provided additional regularity assumptions are made that guarantee well-posedness of the above PDE. However, analogous to Corollary 3.7, dynamic programming applies without any additionally assumptions on and .

Remark 6.8 (Vallois’ embedding as limit of Root type embedding).

6.2 Examples

We now apply Theorem 6.4 to concrete Markov processes.

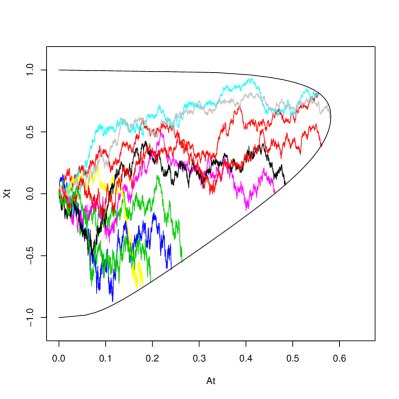

Example 6.9 (Brownian motion and ).

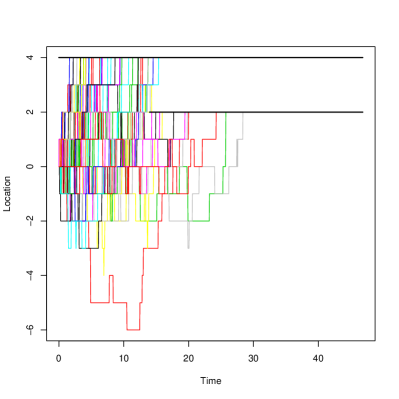

Taking as the one-dimensional Brownian motion, the additive functional has received much attention (see e.g. [50]) due to application in mathematical finance in the context of Asian options. Then , where is the Bessel process of index 0 for which the transition density is well known (see [50]). Figure 4 on page 4 shows the Root barriers for and .

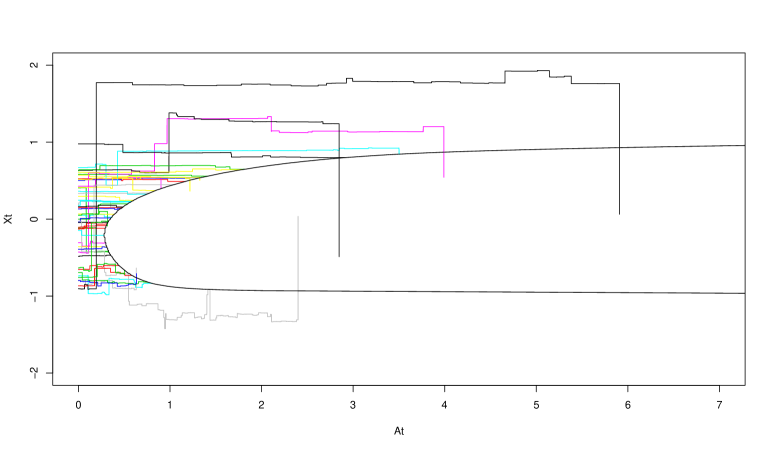

Example 6.10 (Symmetric stable Lévy process and ).

For smooth with for some , from [10, Theorem (2.5)], the time-changed process has absolutely continuous transition density with respect to the Lebesgue measure. Comparing the Root barriers for and for and , we can see that the barrier in Figure 5(b) on page 5 is not symmetric, unlike the barrier for in Figure 3(b). Due to the time change, the process runs faster past negative increments and more slowly through the positive parts which leads to hitting the barrier early on the negative parts and much later on the positive parts compared to .

Appendix A Basic definitions from potential theory

Below, we state some definitions taken from [12, Chapter 0 and 1]:

Definition A.1 (Universally measurable sets and nearly Borel sets).

Given a Borel -algebra , define the following -algebras on :

-

(1)

the -algebra of universally measurable sets given as intersection of completions of with respect to finite measures ,

-

(2)

the -algebra of nearly Borel sets. We call a set nearly Borel (with respect to ) if for each finite measure on , there exists Borel sets such that .

Definition A.2 (Standard process).

On a filtered probability space , the stochastic process with shift operator is called a Markov process with augmented state space , if for all , , and

-

(1)

is --measurable,

-

(2)

the map from to is -measurable and ,

-

(3)

, and

-

(4)

.

Furthermore, it is called a standard process, if additionally

-

(1)

is right-continuous and is complete with respect to the family of measures ,

-

(2)

the sample paths are càdlàg a.s.,

-

(3)

satisfies the strong Markov property, i.e. is --measurable and for all bounded measurable functions and -stopping times we have for all and , and

-

(4)

is quasi-left-continuous on , i.e. for any increasing sequence of -stopping times such that almost surely for a stopping time , it holds that almost surely on .

Semigroup and potential.

In Table 2 we let , , , be a -measurable function (extended to by ), be a Borel measure on , and be a stopping time.

| Markov process | ||

| semigroup of | ||

| potential of | ||

| Stopping times | ||

| semigroup at | ||

| first hitting time | , | |

The potential of a measure on a set describes the occupation of the set by over its lifetime when starting in the initial distribution ; on the other hand, evaluates the mass transported over the entire lifetime after starting in under . This explains the notation for the different actions and of the potential kernel on and as we start in and end in , respectively.

Definition A.3 (Excessive functions and measures).

A non-negative -measurable function is called excessive if for all and pointwise.

Analogously, a Borel measure is called excessive if it is -finite and for all and .

Fine topology.

In Table 3, the set denotes a nearly Borel set.

| Fine topology | |

|---|---|

| polar set | is polar if , -a.s. for all |

| thin set | is thin if , -a.s. for all |

| semipolar set | is semipolar, if it is a countable union of thin sets |

| the regular points of ; a point is called regular if , -a.s. | |

| fine topology on | topology where the open sets are s.t. , -a.s. |

| fine closure of | the set |

Intuitively, the polar sets are those sets which are never visited at positive times by the process, while semipolar sets are those sets which are almost surely visited only countably many times by the process. Every polar set is semipolar, but the reverse implication is not true in general.

Appendix B Properties of the réduite

Definition B.1 (Réduite).

Given a Markov semigroup associated to a standard process, and given Borel-measurable and finely lower semicontinuous, we define the réduite (or smallest excessive majorant) of by

| (B.1) |

Proposition B.2 (Shiryaev, Lemma 3 and Theorem 1 in [61, Chapter 3]).

Let be a standard process with semigroup and finely lower semicontinuous. Then:

-

(1)

is excessive.

-

(2)

For all , it holds that

where the supremum ranges over stopping times taking values in .

-

(3)

Define for and Borel-measurable, Then it holds that

Given a (positive) Borel measure , we similarly define

| (B.2) |

(note that the infimum above is the infimum of a family of measures, namely the smallest measure dominated by all measures in the family).

Lemma B.3.

Assume that and are standard processes in strong duality with respect to a reference measure . Let be finely lower semi-continuous and . Then

Proof.

It is easy to see that is a -excessive measure, and it therefore admits a -excessive density . Since , it holds that -a.e. We then actually have the inequality everywhere since

using the semicontinuity of . Therefore .

For the opposite inequality, note that is a -excessive measure which dominates , so that -a.e., and then everywhere since both are excessive functions. ∎

Appendix C Hypo-elliptic Laplacian

Denote with the free nilpotent group of depth of generators. Denote with a basis of and identify it as left-invariant vector fields (the first level of the Lie algebra of ). If is a -dimensional Brownian motion, then it is well-known that the solution of the SDE

is a (left)-Brownian motion666A process taking values in Lie-group is called (left) Brownian motion in if is continuous, is independent of , and and are identical in law. on the Lie-group . Moreover, is a Markov process with generator . Following [15], there exists a homogeneous norm such that

with a constant ; moreover, is the fundamental solution to . In the case where and , is just given by the Euclidean norm on . For , can be identified as the Heisenberg group. It is more convenient to work in the associated Lie algebra which we identify in coordinates as . Then and

For any measure on we then define

Lemma C.1.

Let be any probability measure on . Define the measure

| (C.1) |

where is the open ball with respect to , is the surface measure and

Then is a probability measures on such that with respect to Brownian motion on .

Proof.

From [15, Theorems 3.4 and 4.1] we know that a upper semi-continous function is sub-harmonic on if and only if it satisfies the global-surface sub-mean property for any

| (C.2) |

where and . We write . Then is subharmonic. The fact that is a probability measure follows as we have equality in (C.2) for the harmonic function . For its potential we get

where we used equation (C.2) for in the last inequality. ∎

This in turns leads to an explicit density if we choose as the uniform measure on .

Corollary C.2.

Let . Then there exists a probability measure such that and that has a density with respect to Lebesgue measure given as

Acknowledgements

PG acknowledges the support of the ANR, via the ANR project ANR-16-CE40-0020-01. HO is grateful for support from the EPSRC grant “Datasig” [EP/S026347/1], the Oxford-Man Institute of Quantitative Finance, and the Alan Turing Institute. CZ was supported by the EPSRC grant EP/N509711/1, via the project No. 1941799.

References

- [1] Guy Barles and Panagiotis Souganidis. Convergence of approximation schemes for fully nonlinear second order equations. Asymptotic Analysis, 4(3):271–283, 1991.

- [2] Begoña Barrios, Alessio Figalli, and Xavier Ros-Oton. Free boundary regularity in the parabolic fractional obstacle problem. Communications on Pure and Applied Mathematics, 71(10):2129–2159, 2018.

- [3] Mathias Beiglböck, Alexander M.G. Cox, and Martin Huesmann. Optimal transport and Skorokhod embedding. Inventiones mathematicae, 208(2):327–400, 2017.

- [4] Mathias Beiglböck, Alexander M.G. Cox, and Martin Huesmann. The geometry of multi-marginal Skorokhod Embedding. arXiv preprint arXiv:1705.09505, 2017.

- [5] Mathias Beiglböck, Pierre Henry-Labordère, and Nizar Touzi. Monotone martingale transport plans and Skorokhod embedding. Stochastic Processes and their Applications, 127(9):3005–3013, 2017.

- [6] Mathias Beiglböck, Marcel Nutz, and Florian Stebegg. Fine Properties of the Optimal Skorokhod Embedding Problem. arXiv preprint arXiv:1903.03887, 2019.

- [7] Mathias Beiglböck, Marcel Nutz, and Nizar Touzi. Complete duality for martingale optimal transport on the line. The Annals of Probability, 45(5):3038–3074, 2017.

- [8] Jean Bertoin. Lévy processes, volume 121. Cambridge university press, 1998.

- [9] Klaus Bichteler, Jean-Bernard Gravereaux, and Jean Jacod. Malliavin Calculus for Processes with Jumps. volume 2. Gordon and Breach Publishers Singapore, 1987.

- [10] Klaus Bichteler and Jean Jacod. Calcul de malliavin pour les diffusions avec sauts: Existence d’une densite dans le cas unidimensionnel. In Séminaire de Probabilités XVII 1981/82, pages 132–157. Springer, 1983.

- [11] Robert M. Blumenthal and Ronald K. Getoor. Some theorems on stable processes. Transactions of the American Mathematical Society, 95(2):263–273, 1960.

- [12] Robert M. Blumenthal and Ronald K. Getoor. Markov processes and potential theory. Courier Corporation, 2007.

- [13] Robert M. Blumenthal, Ronald K. Getoor, and Daniel B. Ray. On the distribution of first hits for the symmetric stable processes. Transactions of the American Mathematical Society, 99(3):540–554, 1961.

- [14] Krzysztof Bogdan, Tomasz Byczkowski, Tadeusz Kulczycki, Michal Ryznar, Renming Song, and Zoran Vondracek. Potential analysis of stable processes and its extensions. Springer Science & Business Media, 2009.

- [15] Andrea Bonfiglioli and Ermanno Lanconelli. Subharmonic functions on Carnot groups. Mathematische Annalen, 325(1):97–122, 2003.

- [16] Luis Caffarelli, Xavier Ros-Oton, and Joaquim Serra. Obstacle problems for integro-differential operators: regularity of solutions and free boundaries. Inventiones mathematicae, 208(3):1155–1211, 2017.

- [17] Eric A. Carlen, Seiichiro Kusuoka, and Daniel W. Stroock. Upper bounds for symmetric Markov transition functions. Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, 23(2, suppl.):245–287, 1987.

- [18] Rene M. Chacon. Barrier stopping time and the filling scheme. PhD thesis, University of Washington, 1986.

- [19] Kai Lai Chung and John B. Walsh. Markov processes, Brownian motion, and time symmetry, volume 249. Springer Science & Business Media, 2006.

- [20] Alexander M.G. Cox and Goran Peskir. Embedding laws in diffusions by functions of time. The Annals of Probability, 43(5):2481–2510, 2015.

- [21] Alexander M.G. Cox and D.G. Hobson. A unifying class of Skorokhod embeddings: connecting the Azéma-Yor and Vallois embeddings. Bernoulli, 13(1):114–130, 2007.

- [22] Alexander M.G. Cox, Jan Obłój, and Nizar Touzi. The Root solution to the multi-marginal embedding problem: an optimal stopping and time-reversal approach. Probability Theory and Related Fields, 173(1-2):211–259, 2019.

- [23] Alexander M.G. Cox and Jiajie Wang. Root’s barrier: Construction, optimality and applications to variance options. The Annals of Applied Probability, 23(3):859–894, 2013.

- [24] Philip J. Davis and Philip Rabinowitz. Methods of numerical integration. Courier Corporation, 2007.

- [25] Tiziano De Angelis. From optimal stopping boundaries to Rost’s reversed barriers and the Skorokhod embedding. In Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, volume 54, pages 1098–1133. Institut Henri Poincaré, 2018.

- [26] Claude Dellacherie and Paul-André Meyer. Probabilités et potentiel, Hermann, 1966.

- [27] Leif Döring, Lukas Gonon, David J. Prömel, Oleg Reichmann, et al. On Skorokhod embeddings and Poisson equations. The Annals of Applied Probability, 29(4):2302–2337, 2019.

- [28] Bruno Dupire. Arbitrage bounds for volatility derivatives as free boundary problem. Presentation at PDE and Mathematical Finance, KTH, Stockholm, 2005.

- [29] Evgeniĭ Borisovich Dynkin. Markov processes. Springer, 1965.

- [30] Neil Falkner. The distribution of Brownian motion in Rn at a natural stopping time. Advances in Mathematics, 40(2):97–127, 1981.

- [31] Neil Falkner. Stopped distributions for Markov processes in duality. Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete, 62(1):43–51, 1983.

- [32] Neil Falkner and Patrick J. Fitzsimmons. Stopping distributions for right processes. Probability Theory and Related Fields, 89(3):301–318, 1991.

- [33] Paul Gassiat, Aleksandar Mijatović, and Harald Oberhauser. An integral equation for Root’s barrier and the generation of Brownian increments. The Annals of Applied Probability, 25(4):2039–2065, 2015.

- [34] Paul Gassiat, Harald Oberhauser, and Gonçalo dos Reis. Root’s barrier, viscosity solutions of obstacle problems and reflected FBSDEs. Stochastic Processes and their Applications, 125(12):4601–4631, 2015.

- [35] Bernard Gaveau. Principe de moindre action, propagation de la chaleur et estimees sous elliptiques sur certains groupes nilpotents. Acta Mathematica, 139:95–153, 1977.

- [36] Ronald K. Getoor and Michael J. Sharpe. Excursions of dual processes. Advances in Mathematics, 45(3):259–309, 1982.

- [37] Nassif Ghoussoub, Young-Heon Kim, and Aaron Zeff Palmer. A solution to the Monge transport problem for Brownian martingales. arXiv preprint arXiv:1903.00527, 2019.

- [38] Nassif Ghoussoub, Young-Heon Kim, and Aaron Zeff Palmer. PDE methods for optimal Skorokhod embeddings. Calculus of Variations and Partial Differential Equations, 58(3):113, 2019.

- [39] Gaoyue Guo, Xiaolu Tan, and Nizar Touzi. On the monotonicity principle of optimal Skorokhod embedding problem. SIAM Journal on Control and Optimization, 54(5):2478–2489, 2016.

- [40] Gaoyue Guo, Xiaolu Tan, and Nizar Touzi. Optimal Skorokhod embedding under finitely many marginal constraints. SIAM Journal on Control and Optimization, 54(4):2174–2201, 2016.

- [41] Philip Hartman and Aurel Wintner. On the infinitesimal generators of integral convolutions. American Journal of Mathematics, 64(1):273–298, 1942.

- [42] David Hobson. The Skorokhod embedding problem and model-independent bounds for option prices. In Paris-Princeton Lectures on Mathematical Finance 2010, pages 267–318, Springer 2011.

- [43] Lars Hörmander. Hypoelliptic second order differential equations. Acta Mathematica, 119(1):147–171, 1967.

- [44] Espen R. Jakobsen and Kenneth H. Karlsen. Continuous dependence estimates for viscosity solutions of integro-PDEs. Journal of Differential Equations, 212(2):278–318, 2005.

- [45] David Kinderlehrer and Guido Stampacchia. An introduction to variational inequalities and their applications, volume 31. Siam, 1980.

- [46] Andreas E. Kyprianou, Juan Carlos Pardo, and Alexander R. Watson. Hitting distributions of -stable processes via path censoring and self-similarity. The Annals of Probability, 42(1):398–430, 2014.

- [47] Andreas E. Kyprianou and Alexander R. Watson. Potentials of stable processes. In Séminaire de Probabilités XLVI, pages 333–343. Springer, 2014.

- [48] Paul Lévy. Wiener’s Random Function, and Other Laplacian Random Functions. In Proceedings of the Second Berkeley Symposium on Mathematical Statistics and Probability, pages 171–187, Berkeley, Calif., 1951. University of California Press.

- [49] Zhi Ming Ma and Michael Röckner. Introduction to the theory of (nonsymmetric) Dirichlet forms. Universitext. Springer-Verlag, Berlin, 1992.

- [50] Hiroyuki Matsumoto, Marc Yor, et al. Exponential functionals of Brownian motion, I: Probability laws at fixed time. Probability surveys, 2:312–347, 2005.

- [51] Jan Obłój et al. The Skorokhod embedding problem and its offspring. Probability Surveys, 1:321–392, 2004.

- [52] Arshak Petrosyan, Henrik Shahgholian, and Nina Nikolaevna Uraltseva. Regularity of free boundaries in obstacle-type problems, volume 136. American Mathematical Society, 2012.

- [53] Jean Picard. On the existence of smooth densities for jump processes. Probability Theory and Related Fields, 105(4):481–511, 1996.

- [54] Pál Révész. Random walk in random and non-random environments. World Scientific, 2005.

- [55] Daniel Revuz. Mesures associées aux fonctionnelles additives de Markov. I. Transactions of the American Mathematical Society, 148(2):501–531, 1970.

- [56] Alexandre Richard, Xiaolu Tan, and Nizar Touzi. On the Root solution to the Skorokhod embedding problem given full marginals. arXiv preprint arXiv:1810.10048, 2018.

- [57] David H. Root. The existence of certain stopping times on Brownian motion. The Annals of Mathematical Statistics, 40(2):715–718, 1969.

- [58] Hermann Rost. Die Stoppverteilungen eines Markoff-Prozesses mit lokalendlichem Potential. manuscripta mathematica, 3(4):321–329, 1970.

- [59] Hermann Rost. The stopping distributions of a Markov process. Inventiones mathematicae, 14(1):1–16, 1971.

- [60] Hermann Rost. Skorokhod stopping times of minimal variance. In Séminaire de Probabilités X Université de Strasbourg, pages 194–208. Springer, 1976.

- [61] Albert N. Shiryaev. Optimal Stopping Rules, volume 8. Springer Science & Business Media, 2007.

- [62] Robert T. Smythe and John B. Walsh. The existence of dual processes. Inventiones mathematicae, 19(2):113–148, 1973.

- [63] Peter Tankov and Rama Cont. Financial modelling with jump processes. Chapman and Hall/CRC, 2003.

- [64] Pierre Vallois. Quelques inégalités avec le temps local en zero du mouvement brownien. Stochastic Processes and their Applications, 41(1):117–155, 1992.

- [65] Rainer Wittmann. Natural densities of Markov transition probabilities. Probability Theory and Related Fields, 73(1):1–10, 1986.