Autocovariance function estimation via difference schemes for a semiparametric change point model with -dependent errors

Abstract.

We discuss a broad class of difference-based estimators of the autocovariance function in a semiparametric regression model where the signal consists of the sum of an identifiable smooth function and another function with jumps (change points) while the errors are -dependent. We establish that the influence of the smooth part of the signal over the bias of our estimators is negligible; this is a general result as it does not depend on the distribution of the errors. We show that the influence of the unknown smooth function is negligible also in the mean squared error (MSE) of our estimators. Although we assume Gaussian errors to derive the latter result, our finite sample studies suggest that the class of proposed estimators still show small MSE when the errors are not Gaussian. Our simulation study also demonstrates that, when the error process is misspecified as an AR instead of an -dependent process, our proposed method can estimate autocovariances about as well as some methods specifically designed for the AR() case, and sometimes even better than them.

We also allow both the number of change points and the magnitude of the largest jump grow with the sample size. In this case, we provide conditions on the interplay between the growth rate of these two quantities, and the vanishing rate at zero of the modulus of continuity of the smooth part of the regression function, that ensure consistency of our autocovariance estimators.

As an application, we use our approach to provide a better understanding of the possible autocovariance structure of a time series of global averaged annual temperature anomalies. Finally, the R package dbacf complements this paper.

Key words and phrases:

autocovariance estimation and change point and semiparametric model and difference-based method and m-dependent and quadratic variation and total variation1. Introduction

Let us begin by considering the nonparametric regression model with correlated errors

| (1) |

where are the fixed sampling points, is an unknown mean function that can be discontinuous, e.g. a change point model or a signal with monotonic trend, and is a zero mean stationary time series error process. For such a model, the knowledge of the autocovariance function (ACF) , is essential. For instance, accounting for an appropriate estimate of the long-run variance () plays a crucial role for developing multiscale statistics aiming to either estimate the total number of change points, cf. Dette et al., (2020), or test for local changes in an apparent nonparametric trend, cf. Khismatullina and Vogt, (2020). Similar models have been considered in Davis et al., (2006), Jandhyala et al., (2013), Preuß et al., (2015), Vogelsang and Yang, (2016) and Chakar et al., (2017) among many others. Generally speaking, ACF estimates are important for bandwidth selection, confidence interval construction and other inferencial procedures associated with nonparametric modeling, cf. Opsomer et al., (2001). Some of these authors have considered parametric error structures such as ARMA(, ) or ARCH(1,1) models. In this manuscript, instead of considering a specific error process model, such as e.g. ARMA(,), we will consider an -dependent error structure and and a mean function that consists of both smooth and discontinuous parts. This is also the mean structure considered in Chan, (2022).

More specifically, we consider the general regression model with correlated errors

| (2) |

where we assume that is an unknown continuous function on , are sampling points, is the stepwise constant function

| (3) |

with and change points at ; the levels , the number of change points and their location are all unknown. We will assume that the errors form a zero mean, stationary, -dependent process, i.e., we assume that when . To ensure identifiability, we require that .

Somewhat similar partial linear regression models (where the function is a linear function of that does not contain jumps) with correlated errors have a fairly long history in statistical research. Engle et al., (1986) already established, in their study of the effect of weather on electricity demand that the data were autocorrelated at order one. Gao, (1995) was probably the first to study estimation of the partial linear model with correlated errors. You and Chen, (2007) obtained an improved estimator of the linear component in such a model using the estimated autocorrelation structure of the process .

A model where the mean structure is exactly the same as in (2) but the errors are iid is typically called a Nonparametric Jump Regression (NJRM) and was considered in Qiu and Yandell, (1998) who were concerned with the jump detection in that model. This model is often appropriate when the mean function in a regression model jumps up or down under the influence of some important random events. Good practical examples are stock market indices, physiological responses to stimuli and many others. Regression functions with jumps are typically more appropriate than continuous regression models for such data. A method that can be used to estimate the location curves and surfaces for - and - dimensional versions of NJRM was proposed in Chu et al., (2012). Further generalizations to the case where the observed image also experiences some spatial blur but the pointwise error remains serially uncorrelated are also available, see e.g. Kang and Qiu, (2014) and Qiu and Kang, (2015). With this background in mind, our model (2) effectively amounts to the generalization of the 1-dimensional NJRM to the case of serially correlated errors.

-dependency may be construed as a restrictive model for correlated structures, however, -dependency is an appropriate proxy for more elaborated dependency measures, within the framework of model (1), provided that the corresponding autocovariance function decays exponentially fast, see Section 4 of Dette et al., (2020). Since the appearence of the concept of physical dependence measure, cf. Wu, (2005), there has been an increasing theoretical interest for using -dependency to approximate general dependence structures, Berkes et al., 2009a , Berkes et al., 2009b , Dette and Quanz, (2023). Note also that there is a number of practically important cases where the value of may be known beforehand as in e.g. Hotz et al., (2013) and Pein et al., (2018). Thus the relevance of this work lies precisely in providing a family of ACF estimators that circumvent the difficult estimation of a mean function which consists of both a change point component and a smooth function . To this end we will focus on the family of difference-based estimators.

Difference-based estimators can be traced back to the mean successive difference of von Neumann et al., (1941). Since then this computationally efficient variance estimator has been studied with many different purposes in mind. For instance, in nonparametric regression with smooth signals and homoscedastic errors, it has been considered for improving bandwidth selection (Rice, (1984)) and asymptotic efficiency of variance estimators (Gasser et al., (1986) and Hall et al., (1990)); it has also been considered for variance estimation under heteroscedasticity of the errors (Müller and Stadtmüller, (1987)). Dette et al., (1998) have discussed that for a small sample size, a difference-based variance estimator may have a non-negligible bias and to overcome this issue, optimal sequences can be employed.

Difference-based estimators have also been considered in smooth nonparametric regression with correlated errors, e.g. Müller and Stadtmüller, (1988), Herrmann et al., (1992), Hall and Van Keilegom, (2003) and Park et al., (2006). More recently, and close to our work, optimal variance difference-based estimators have been proposed in the standard partial linear model under homoscedasticity of the errors, e.g. Wang et al., (2017) and Zhou et al., (2018), among others. Wang and Yu, (2017) studied the optimal difference-based estimator for variance. Dai et al., (2015) proposed difference-based variance estimator for repeated measurement data. Tecuapetla-Gómez and Munk, (2017) studied ACF estimation via difference-based estimators of second order and -gap in the model (2) when . To the best of our knowledge the ACF estimation problem via difference schemes in the Eq. (2), has not been considered.

Perhaps the first contribution of this paper is the rather conceptual extension of model (1) (considered in Tecuapetla-Gómez and Munk, (2017)) to model (2). Note that the setup considered here is not a special case of the setup in Section 4 of Tecuapetla-Gómez and Munk, (2017). There, it is specified that there exists a positive number such that all of the jumps are greater than in absolute value. Thus, the mean function is guaranteed to have a certain number of discontinuities that may depend on . On the contrary, the setup consider in this work does not require the existence of such a constant and so the existence of a given number of discontinuities is not guaranteed. Moreover, in Section 4 of Tecuapetla-Gómez and Munk, (2017) it is required that, on every interval , the regression function must be Hölder continuous with some index whereas in our setup the smooth component of the regression function is only continuous. Additionally, the separation of signal in two parts, which contains jumps and which is rather smooth, allows us to establish all of our main results under the assumption that is continuous on .

The contributions of this paper continue with the explicit derivation of the expected value of difference-based variance estimator of arbitrary order and -gap, see Eq. (6) for a proper definition of this class of estimators and Theorem 1 for the result itself. An immediate consequence of this result is that, if in the semiparametric change point model given by (2) we assume that the largest jump is bounded (the bound does not depend on ) and the total variation of the function is of order , then any estimator within the class (6) is asymptotically unbiased. We stress that Theorem 1 does not require us to assume a specific distributional family for the error model. As explained in the remarks following Theorem 1, an increment in the (arbitrary) order increases the bias of any member of the variance estimator class (6); the magnitude of this increase is of the order of the product of times the quadratic variation of the function times an increasing function depending on . Observe that among the latter quantities we can only control the lag order . Consequently, we opt for studying some asymptotic properties of the member of class (6) with the smallest (finite sample) bias, namely, the variance estimator of order 1,

| (4) |

In order to estimate the remaining values of the autocovariance function we focus on the estimator

| (5) |

Also from the remarks of Theorem 1 it follows that in the semiparametric change point model with -dependent stationary errors given by (2) even when the number of change points grows at rate and the size of the largest jump grows at rate then, for any , our autocovariance estimators (4)-(5) are consistent provided that the modulus of continuity vanishes at zero at the rate as , see Theorem 2. Among our main results, this is the only one in which we utilized a distributional form for the error model (Gaussian). Theorem 2 is the second major contribution of this paper.

Section 3 contains preliminary calculations needed to establish the main results of this paper. In Section 4 we conducted several numerical studies to assess the accuracy and precision of our estimators in the setting of model (2)-(3); we also assess the robustness of our method by considering -dependent errors with heavy-tailed marginal distribution. Separately, we consider the robustness of our method to reasonably small violations of the -dependency requirement for the error process. This is done by using our method to estimate autocovariances when the true error process is an AR() process. This set-up is meaningful since the autocovariances of the AR() process at lag are proportional to . Thus, if is chosen to be small in absolute value, the autocovariances of AR() process decay quite quickly and become very small after a finite number of lags. We compare the performance of our method under the AR() error assumption to two alternative methods. First, introduced in the paper Hall and Van Keilegom, (2003), was designed specifically for the case of a smooth mean function. The second method is that of Chakar et al., (2017). That method was designed as a robust estimator of the autoregressive parameter of an AR(1) error process in a model with a mean that has a finite number of breakpoints. Since this method is not meant to provide a direct estimate of the autocovariance function at lag , this function has to be obtained using standard formulas that connect the autoregressive coefficient of an AR() process and its autocovariance at lag given in any introductory time series text e.g. Shumway and Stoffer, (2019) p. . All of our simulations are based on functions provided by the R package dbacf, available on The Comprehensive R Archive Network, of Tecuapetla-Gómez, (2023).

Section 5 shows that our method can be employed to provide a better understanding of the ACF structure of global, averaged, annual temperature anomalies spanning from 1808 to 2021. This dataset can be found in the package astsa by Stoffer and Poison, (2023) developed under the R language for statistical computing, cf. R Core Team, (2022). Finally, some technical details used in our proofs are relegated to Appendices A and B.

2. Main results

Before introducing the class of difference-based estimators we require some notation. First, for any we will use the notation for an index vector . Thus, for a generic vector , for , we define . Also, and will denote and . Thus, , and denote the vectors , and , respectively. The quadratic variation of the function will be denoted by . For vectors and , denotes their Euclidean inner product. From now on is a continuous function. Such a function is, of course, a uniformly continuous one. Due to this, there exists a function , called a modulus of uniform continuity, such that for all . This function is vanishing at zero, right-continuous at zero, and strictly increasing over the positive half of the real line. The function obeys (3).

Let be given such that . It is known that in the change point regression with -dependent errors model, which is a particular case of (2), in order to get a consistent variance estimator based on difference schemes it is necessary to consider observations which are separated in time by at least units, cf. Theorem 5 of Tecuapetla-Gómez and Munk, (2017). That is, a consistent variance difference-based estimator must consider gaps of size (at least) observations. Due to this we utilize the vector of weights and define a difference of order and a -gap as . We utilize this object to define a difference-based variance estimator of order and -gap as the quadratic form

| (6) |

Throughout the paper, in order to simplify notation, we may omit inside the parentheses for observation differences (and quadratic forms) and simply write (and ), unless any confusion results from such an omission.

Example 1.

For , , and , becomes . -dependence guarantees that for any . Hence, the expected value of the core statistic is equal to . For the general difference-based estimator given by Eq. (6), the expected value of is equal to .

In order to obtain a clear representation of the part of the bias of which is directly linked to the stepwise constant function we assume the following restriction on the distance between the jumps,

| (7) |

Observe that this condition ties up together the distance between change points, the depth of dependence and the lag order . Whether there exist alternative conditions to (7) which are less restrictive and allow us to get a simple description of this bias term is an interesting research question which is outside the scope of the present work.

Theorem 1.

Remark 1.

Note that the magnitude of the bias depends strongly on the quadratic variation . Note also that is effectively the total variation of the function and that one can guarantee that is growing relatively slowly with by imposing a condition on . Indeed, it is clear that the quadratic variation . Therefore, it is enough to impose a bound on the growth rate of and on the growth rate of the maximum jump size to guarantee a reasonably low rate of growth for .

Remark 2.

The normalization requirement 8 guarantees asymptotic unbiasedness of as an estimator of . Moreover, the result obtained in this Theorem is independent of the order of s in the vector .

Observe that these considerations carry over when in the model (2)-(3) we allow that the number of change points and maximum jump size depend on . More precisely,

Corollary 1.

Suppose that the conditions of Theorem 1 hold. Additionally, suppose that we allow the number of change points to depend on the sample size. Suppose further that is bounded by a constant not depending on , and . Then .

Remark 3.

Observe that thus far we have not made any distributional assumption on the errors ; null mean, stationarity and -dependence are sufficient to establish that, asymptotically, the influence of the smooth part of the regression function, i.e. , on the bias of the general difference-based variance estimator is negligible. Moreover, this result remains true regardless of the order .

Remark 4.

Theorem 1 also provides a hint as to what class of autocovariance estimators may be useful in practice. More precisely, note that the quantity is always non-negative and monotonically increasing as a function of the order . The same is true for the first term of as well. This suggests that, especially for relatively small sample sizes , it is possible that the increase in the order of the difference-based estimator may increase its bias. Thus, from a practical viewpoint, it may not make a lot of sense to consider difference-based estimators of the variance (and autocovariances) of the error process for . Moreover, the condition (7) implies that, if we want to use larger , it is necessary to impose a more stringent condition on the change points to guarantee the same order of the bias. In other words, we would have to assume that change points are farther apart in such a case which may not always be a realistic assumption.

In light of the above, the rest of the paper will be devoted to establishing some asymptotic properties of the difference-based estimators of first order, -gap, and weight , . Note that this estimator is equivalent to introduced in Eq. (4):

| (9) |

The autocovariances with will be estimated using the following difference of random quadratic forms,

| (10) |

Remark 1 points at the direction on imposing conditions on the total variation of the stepwise constant function in order to obtain appropriate convergence rate of our estimators. The following result tells us a bit more. Indeed, we can allow the number of change points, to depend on the sample size and yet obtain appropriate rates of convergence for the estimators (9) and (10). This is possible through an interplay between the growth rate of the number of change points and the size of the largest jump. More precisely,

Theorem 2.

Let be given. Suppose that the conditions of Theorem 1 are satisfied with . Additionally, suppose that we allow the number of change points to depend on the sample size, say we have change points. Assume also that the errors are Gaussian and furthermore that

Then, for

In Theorem 2 we have utilized Gaussianity of the errors; this allows us to compute moments of fourth order of the quadratic forms , explicitly. Moreover, Gaussianity of the errors has been exploited in many influential publications in the change point literature, see Fryzlewicz, (2014) and Frick et al., (2014) among many others. More recently, Gaussianity has contributed to establishing an explicit form of the asymptotic minimax detection boundary for a change point model with dependent errors, cf. Enikeeva et al., (2020). Rather than being a limitation, these examples argue in favor of Gaussianity as a means to pave the way to obtain general results. In our work, assuming normal errors has allowed us to reveal that even when the number of change points tends to infinity (at the rate ), and the largest jump grows at the rate (), there is a -consistent class of autocovariance function estimators in the semiparametric change point model (2)-(3) provided that the rate at which the modulus of continuity vanishes at zero is .

3. Asymptotic properties of autocovariance difference-based estimators

The results of this section are proven in the Appendix A. We will denote and . The following proposition provides expressions for the bias of estimators , ; its proof is omitted as it can be deduced from that of Theorem 1.

Proposition 1.

Consequently, for ,

| (11) |

3.1. On the variance of

Now we focus on computing the variance of , or equivalently the variance of the difference-based estimator of order 1, gap and weights , see Eq. (9). To state the main result of this section, we first define an additional quantity of our model: , where .

Theorem 3.

Suppose that the conditions of Theorem 1 are satisfied and assume that . Additionally, assume that the errors are Gaussian. Then,

| (12) |

where

Remark 5.

If is finite, the main term of the expansion (3) converges to zero at the rate of . The higher order terms, however, depend, first, on the modulus of continuity of the smooth function and, second, quantities , , and . The latter three quantities reflect the behavior of the function ; for example, is its quadratic variation, is its absolute variation, and is closely related to the absolute variation. The behavior of the higher order terms is dependent on the interplay between these various quantities. As an example, the third of this terms suggests that one may have increasing relatively fast with if the modulus of continuity goes to zero sufficiently quickly as its argument goes to zero. If one is ready, however, to consider together with , the condition is absolutely necessary to guarantee consistency of the proposed estimator. The higher order terms may necessitate additional requirements, again depending on the relationship between the rate at which , , and go to infinity with , the rate at which goes to infinity with , and the behavior of the modulus of continuity of the smooth function .

3.2. On the variance of

In this section we characterize the asymptotic behavior of the autocovariance estimator introduced in (10). We stress that the proof of the main result of this section is based on derivations used in the proof of Theorem 3 presented in Section 3.1. Also, we utilize the series of Lemmas established in Appendix B. Now, we state a result about the variance of .

Theorem 4.

Remark 6.

Note, first, that the main term of the expansion has the rate of if is viewed is finite and consists of the first term and part of the third term in the sum (4). Taking into account higher order terms, the rate of convergence of this variance estimator depends, again, on the modulus of continuity of the smooth function and quantities , , and . If is viewed as infinite it is necessary, yet again, require that . Depending on the rates of growth of , , and additional assumptions may have to be imposed on .

4. Simulations

This section contains two simulation studies and in each one of them we will employ the autocovariance estimators (4)-(5) with , . The first simulation study assesses the performance of these autocovariance estimators for a semiparametric change point model with -dependent errors as defined in (2)-(3). The second study considers the performance of our estimators in the case where the error structure is not exactly -dependent but is described by an autoregressive process of order one (AR(1)) with a sufficiently small absolute value of the coefficient. This performance is then compared with the performance of the autocovariance structure estimator of Hall and Van Keilegom, (2003) and the estimator of Chakar et al., (2017). The estimator of Hall and Van Keilegom, (2003) has been designed specifically to handle the case of autoregressive errors in a nonparametric regression model with a smooth regression signal. The estimator of Chakar et al., (2017) has been designed as a robust estimator of the autoregressive parameter of an AR(1) error process in a model whose mean has a finite number of breakpoints. We utilized the functions of the R package dbacf, available on CRAN, to perform the calculations of this section.

4.1. Autocovariance structure estimation in a model with -dependent errors

We perform the first study with two possible stationary distributions of the error process: first, when this stationary distribution is zero mean Gaussian, and second, when that distribution is also zero mean but a non-Gaussian one. The second case is considered in order to assess the robustness of the proposed method against non-normally distributed errors. As an example of a non-Gaussian zero mean error distribution, we choose , a Student distribution with degrees of freedom.

Similarly to Park et al., (2006), we consider a -dependent error model: where s are i.i.d and distributed either normally or . It is assumed that and for a parameter Our aim is to estimate the variance and the autocovariance at lags 1 and 2, that is, , and , respectively, of the error process . The true values of these are clearly and .

The simulated signal in this study is a sum of the piecewise constant signal used earlier by Chakar et al., (2017) and a smooth function Briefly, the first additive component is defined as a piecewise constant function with six change-points located at fractions and of the sample size . In the first segment, in the second and in the remaining segments alternates between and starting with in the third segment. The function is chosen to ensure that in order to satisfy the identifiability constraint. We consider three choices of : a linear function a quadratic function and a periodic function All of these functions are defined as zero outside interval. The functions are chosen to range from a simple linear function to a periodic function that may potentially increase the influence of the higher order terms in the risk expansions. Tables 1 and 2 summarize the results for observations obtained from replications for Gaussian and errors, respectively. The results seem to confirm that, in both cases, MSEs of proposed estimators are rather small and scarcely depend on the choice of the smooth function To check consistency of the method, we also performed the same experiment in the case of normal errors using a larger sample size of observations. The results of this experiment, available in the Table 3, show that MSEs decrease for every choice of the smooth function and for all possible choices of compared to the case of This result seems to confirm our conclusion that the main terms in both the squared bias and the variance of proposed estimators do not depend on the choice of Finally, it is known that the bias, although negligible asymptotically, may be rather noticeable in smaller sample sizes. This effect has been extensively illustrated in case of homoscedastic nonparametric regression with i.i.d. data in Dette et al., (1998). To study the bias magnitude numerically in our case, we also consider two smaller sample sizes and . For brevity, we only consider the situation where the error distribution is a zero mean Gaussian one. The results are illustrated in the Tables 4 and 5, respectively. First of all, one can see clearly that absolute magnitudes of MSEs in this case are noticeably larger than for larger sample sizes; however, as the sample size increases from to the magnitude of MSEs goes down noticeably, by a factor of about in many cases. The dependence on the choice of the function becomes a little more pronounced for a small sample size of especially when changing from the choice of to that of .

| 0.0402 | 0.0383 | 0.0181 | 0.0394 | 0.0379 | 0.0180 | 0.0393 | 0.0380 | 0.0181 | 0.0375 | 0.0387 | 0.0185 | 0.0383 | 0.0378 | 0.0181 | 0.0407 | 0.0396 | 0.0182 | 0.0418 | 0.0423 | 0.0200 | |

| 0.0390 | 0.0394 | 0.0174 | 0.0397 | 0.0388 | 0.0181 | 0.0405 | 0.0379 | 0.0182 | 0.0404 | 0.0381 | 0.0176 | 0.0406 | 0.0389 | 0.0180 | 0.0405 | 0.0398 | 0.0186 | 0.0408 | 0.0394 | 0.0183 | |

| 0.0420 | 0.0424 | 0.0193 | 0.0396 | 0.0441 | 0.0206 | 0.0429 | 0.0421 | 0.0197 | 0.0416 | 0.0422 | 0.0199 | 0.0418 | 0.0432 | 0.0203 | 0.0414 | 0.0432 | 0.0208 | 0.0417 | 0.0427 | 0.0201 | |

| 0.0764 | 0.0538 | 0.0250 | 0.0595 | 0.0514 | 0.0225 | 0.0990 | 0.0457 | 0.0227 | 0.0659 | 0.0422 | 0.0218 | 0.0876 | 0.0459 | 0.0233 | 0.0754 | 0.0518 | 0.0237 | 0.0707 | 0.0467 | 0.0212 | |

| 0.0935 | 0.0521 | 0.0225 | 0.1013 | 0.0568 | 0.0219 | 0.0868 | 0.0450 | 0.0228 | 0.0679 | 0.0430 | 0.0218 | 0.0677 | 0.0400 | 0.0203 | 0.0801 | 0.0514 | 0.0253 | 0.0786 | 0.0539 | 0.0230 | |

| 0.1088 | 0.0636 | 0.0247 | 0.0645 | 0.0528 | 0.0238 | 0.1059 | 0.0448 | 0.0234 | 0.0877 | 0.0446 | 0.0228 | 0.0789 | 0.0491 | 0.0245 | 0.0964 | 0.0555 | 0.0239 | 0.0818 | 0.0575 | 0.0257 | |

| 0.0117 | 0.0116 | 0.0055 | 0.0120 | 0.0111 | 0.0055 | 0.0120 | 0.0111 | 0.0053 | 0.0112 | 0.0112 | 0.0055 | 0.0116 | 0.0114 | 0.0054 | 0.0113 | 0.0114 | 0.0057 | 0.0119 | 0.0116 | 0.0056 | |

| 0.0124 | 0.0116 | 0.0058 | 0.0119 | 0.0114 | 0.0054 | 0.0120 | 0.0112 | 0.0053 | 0.0115 | 0.0114 | 0.0057 | 0.0116 | 0.0112 | 0.0052 | 0.0122 | 0.0116 | 0.0055 | 0.0121 | 0.0115 | 0.0054 | |

| 0.0122 | 0.0120 | 0.0055 | 0.0125 | 0.0119 | 0.0059 | 0.0119 | 0.0117 | 0.0058 | 0.0121 | 0.0118 | 0.0057 | 0.0123 | 0.0123 | 0.0060 | 0.0122 | 0.0123 | 0.0060 | 0.0127 | 0.0124 | 0.0058 | |

| 0.3974 | 0.3901 | 0.1764 | 0.3843 | 0.3876 | 0.1729 | 0.3859 | 0.3986 | 0.1758 | 0.3867 | 0.3880 | 0.1743 | 0.4003 | 0.3976 | 0.1778 | 0.3962 | 0.3940 | 0.1768 | 0.4035 | 0.4062 | 0.1848 | |

| 0.3970 | 0.3895 | 0.1760 | 0.3861 | 0.3957 | 0.1807 | 0.3918 | 0.3908 | 0.1823 | 0.3907 | 0.3930 | 0.1781 | 0.3938 | 0.3990 | 0.1838 | 0.3993 | 0.3954 | 0.1763 | 0.3910 | 0.3838 | 0.1709 | |

| 0.4587 | 0.5176 | 0.2441 | 0.4648 | 0.5125 | 0.2466 | 0.4681 | 0.5192 | 0.2461 | 0.4627 | 0.5206 | 0.2475 | 0.4666 | 0.5312 | 0.2511 | 0.4771 | 0.5159 | 0.2401 | 0.4629 | 0.5205 | 0.2493 | |

| 0.0997 | 0.0966 | 0.0452 | 0.0994 | 0.0979 | 0.0450 | 0.0971 | 0.0994 | 0.0451 | 0.0980 | 0.0990 | 0.0457 | 0.0975 | 0.0965 | 0.0449 | 0.1012 | 0.1002 | 0.0454 | 0.1016 | 0.1025 | 0.0477 | |

| 0.0948 | 0.1017 | 0.0456 | 0.0978 | 0.0988 | 0.0456 | 0.0957 | 0.0987 | 0.0441 | 0.1000 | 0.0988 | 0.0433 | 0.1034 | 0.1003 | 0.0454 | 0.1016 | 0.1005 | 0.0461 | 0.1018 | 0.1027 | 0.0477 | |

| 0.1050 | 0.1142 | 0.0535 | 0.1101 | 0.1118 | 0.0541 | 0.1065 | 0.1113 | 0.0538 | 0.1075 | 0.1151 | 0.0518 | 0.1073 | 0.1139 | 0.0538 | 0.1084 | 0.1144 | 0.0536 | 0.1090 | 0.1153 | 0.0544 | |

4.2. Autocovariance estimation in a model with AR() errors

We also conducted an additional experiment with the aim of comparing our method to a possible competitor. In particular, we considered a situation where the errors are generated by an AR() process where and independent. The method proposed in our manuscript is designed for the case where model errors are generated by an -dependent process with a finite however, for a causal AR(1) process with the autocovariance at lag is proportional to thus decreasing at an exponential rate. Due to this, we hypothesize that our method may perform reasonably well if the errors are generated by an AR() process with that is not too close to in absolute value. More specifically, we selected values of ranging from to with a step of As before, we compare the performance of our method when estimating variance and autocovariance at lags 1 and 2 of the process to that of Hall and Van Keilegom, (2003) and Chakar et al., (2017). The method of Chakar et al., (2017) assumes a mean function with a finite number of breakpoints and was designed to estimate the coefficient only and it does not provide a direct estimate of the autocovariance. Therefore, we proceed as follows. Let be the robust estimator of obtained using the method of Chakar et al., (2017). Then, we compute the estimated variance and autocovariance at lags and for this method as , and , respectively.

In this experiment, the three choices of the smooth function remain the same as in the previous one. When applying our estimator to an AR(1) error process, we choose the value The method of Hall and Van Keilegom, (2003) method is used with the choices of smoothing parameters recommended in Section of their paper: the first parameter and the second parameter We used the method of Chakar et al., (2017) with the default arguments of the R function AR1seg_func from the package AR1seq version 1.0. The results of the method comparison is given in Tables 6-7-8.

Comparing the performance of our approach to that of Hall and Van Keilegom, (2003) we note that, perhaps unsurprisingly, our method provides a universally better performance. In most cases, the MSEs of all estimators for our method are smaller by an order of magnitude compared to that of the method of Hall and Van Keilegom, (2003). That includes all three choices of the smooth function and all possible choices of the autoregressive coefficient This suggests that the method of Hall and Van Keilegom, (2003) is not at all resistant to the presence of breakpoints in the mean function of the regression model. Comparing the MSEs shown in Table 6 to those exhibited by our estimator under the assumption of -dependency for the same sample size, it appears that our method can also handle moderate departures from the assumption of -dependency in the error process of the model rather well.

| 0.0379 | 0.0377 | 0.0180 | 0.0346 | 0.0376 | 0.0177 | 0.0289 | 0.0356 | 0.0159 | 0.0178 | 0.0307 | 0.0127 | 0.0046 | 0.0158 | 0.0044 | |

| 0.0385 | 0.0375 | 0.0174 | 0.0367 | 0.0385 | 0.0178 | 0.0288 | 0.0339 | 0.0150 | 0.0168 | 0.0298 | 0.0122 | 0.0040 | 0.0156 | 0.0045 | |

| 0.0402 | 0.0429 | 0.0204 | 0.0376 | 0.0413 | 0.0193 | 0.0304 | 0.0388 | 0.0179 | 0.0181 | 0.0317 | 0.0132 | 0.0051 | 0.0185 | 0.0052 | |

| 3.1440 | 2.9200 | 2.7421 | 3.1255 | 2.9103 | 2.8207 | 3.1574 | 2.9350 | 3.0245 | 3.1482 | 2.9223 | 3.3461 | 3.0916 | 2.8666 | 3.9038 | |

| 3.1411 | 2.9141 | 2.7291 | 3.1225 | 2.9018 | 2.8076 | 3.1152 | 2.8872 | 2.9750 | 3.1342 | 2.9077 | 3.3323 | 3.0804 | 2.8685 | 3.9204 | |

| 5.0621 | 4.7845 | 4.5481 | 5.0719 | 4.7850 | 4.6989 | 5.0394 | 4.7565 | 4.9638 | 5.0202 | 4.7317 | 5.4616 | 4.9952 | 4.7178 | 6.3817 | |

At the same time, it appears that our method can, at least partially, holds its own against the method of Chakar et al., (2017) that, like ours, has been devised to account for a possibility of a finite number of breaks in the mean. This method exhibits better performance than our method for relatively small values of such as and . This better performance is observed for all choices of the function . Its performance deteriorates significantly, however, for larger values of . As a matter of fact, some of the MSEs of estimators obtained by this method for are an order or two orders of magnitude larger than those of our estimators under the same circumstances. This suggests that, in some cases, our approach can handle autocovariance estimation when the mean has a number of breakpoints better than the robust method of Chakar et al., (2017). Moreover, as opposed to our ACF estimation method, Chakar’s is very slow. For example, the results of the Table (8) were obtained using sec while those in Table 2 took only about sec to complete. All calculations were performed on a Dell Latitude laptop with GB RAM and a th Gen Intel(R) Core(TM) iU GHz processor. The reason for having such a long execution time in the estimation of the parameter is that this estimate is returned only when the method has estimated the entire change point model, which is known to be time-consuming. The user interested in Chakar’s robust estimation method, can reduce the execution time considerably by using the function dbacf_AR1 of the R package dbacf.

| 0.0005 | 0.0065 | 0.0005 | 0.0023 | 0.0179 | 0.0023 | 0.0078 | 0.0888 | 0.0078 | 0.0319 | 0.3981 | 0.0319 | 0.0713 | 1.6504 | 0.0713 | |

| 0.0006 | 0.0076 | 0.0006 | 0.0018 | 0.0187 | 0.0018 | 0.0053 | 0.0819 | 0.0053 | 0.0302 | 0.3806 | 0.0302 | 0.1388 | 1.6557 | 0.1388 | |

| 0.0006 | 0.0079 | 0.0006 | 0.0021 | 0.0182 | 0.0021 | 0.0086 | 0.0833 | 0.0086 | 0.0223 | 0.3819 | 0.0223 | 0.0811 | 1.6745 | 0.0811 | |

Finally, note that the choice of the estimator gap when applying our estimator to the model with AR() error process, is somewhat arbitrary. Our choice of the order was based on the fact that, for any difference sequence order the bias of the resulting estimator is proportional to which may play a fairly substantial role when the number of observations is not too large. To illustrate the benefits of this assumption, we also applied our method to the same model with an AR() error process, the same range of values of and the choice of the smooth function for any while choosing The results are given in the Table 9. Note that the resulting mean squared errors are mostly larger than those obtained the choice of although by less than the full order of magnitude. Note, however, that even in this misspecification case our estimator outperforms Hall and Van Keilegom, (2003)’s uniformly and Chakar et al., (2017) in a number of cases (especially for larger values of the coefficient ) when the sample size is the same.

| 0.0673 | 0.0662 | 0.0375 | 0.0666 | 0.0674 | 0.0381 | 0.0673 | 0.0675 | 0.0380 | 0.0563 | 0.0654 | 0.0370 | 0.0361 | 0.0528 | 0.0273 | |

5. Application

In this section we consider the dataset gtemp_land from the R package astsa by Stoffer and Poison, (2023). This dataset contains observations of annual temperature anomalies (in Celsius degree) averaged over the Earth’s land area from 1880 to 2021. We present a brief analysis of this dataset autocovariance structure.

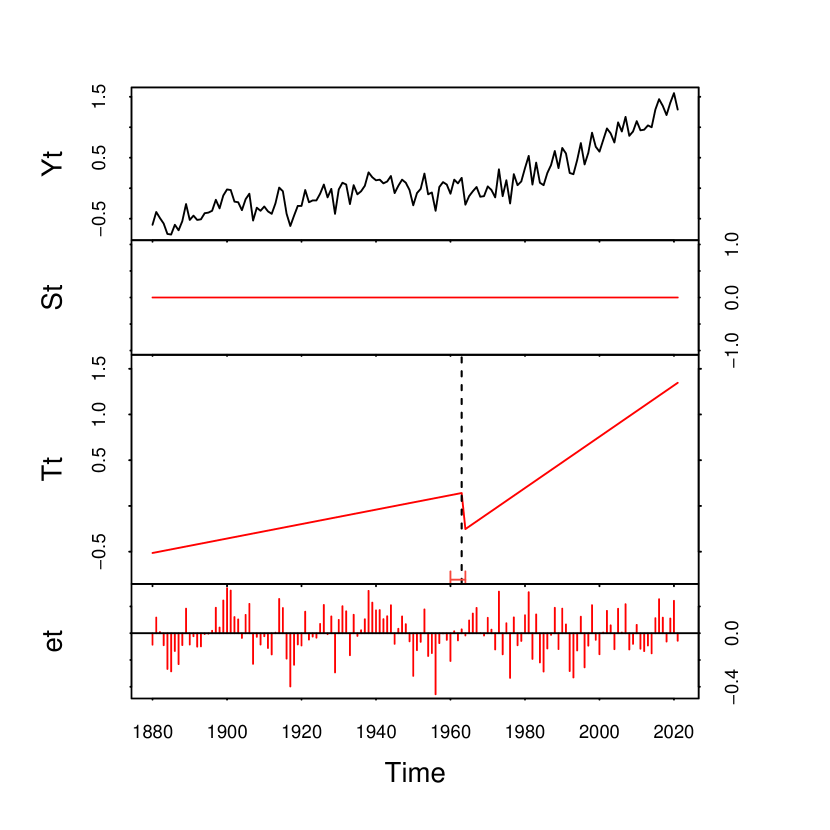

Figure 1 shows the gtemp_land (top panel) with a statistically significant breakpoint (at 1963) in its estimated trend (third panel from top to bottom); the second and fourth panels (from top to bottom) show the estimated seasonal component and the residuals, respectively. This breakpoint was estimated using the R package bfast by Verbesselt et al., (2010), with no seasonal argument and using default values for the remaining arguments of the procedure.

Verbesselt et al., (2010)’s allows for the estimation of unknown change points in the trend and seasonal component of time series. Statistically, this method is based on Chu et al., (1995)’s MOSUM test for no changes in the parameters of a sequence of local linear regressions, see also Zeileis et al., (2002) for further extensions to the method and its implementation. Computationally, bfast is an iterative algorithm allowing for fast computations due to the use of dynamic programming to keep track of both the number and positions of the estimated change points. The total number of change points, unknown a priori, is estimated through optimizing the BIC.

Due to the above, we believe that it is pertinent to analyze these observations with our approach. Apparently, Hall and Van Keilegom, (2003) analyzed this dataset with observations until 1985 and assumed AR(1) and AR(2) error processes. Like us, these authors did not consider a seasonal component. We did not consider a seasonal component because these are annually collected observations with no evident bi-, five-, etc., annual structure. In addition, a smooth seasonal component can be construed as a part of our smooth function . Table 10 shows Hall and Van Keilegom, (2003)’s ACF estimators as well as the bias-reducing, second-order, -gapped, autocovariance estimator of Tecuapetla-Gómez and Munk, (2017), and our estimator. For the latter two estimators, we assumed that .

| 0.035 | 0.035 | 0.025 | 0.028 | 0.023 | 0.027 | 0.025 | 0.029 | 0.026 | 0.031 | ||||

| 0.014 | 0.014 | 0.004 | 0.007 | 0.002 | 0.006 | 0.008 | 0.005 | 0.010 | 0.011 | ||||

| 0.010 | 0.003 | -0.002 | 0.002 | 0.001 | 0.006 | 0.007 | |||||||

| -0.005 | -0.002 | 0.002 | 0.004 | ||||||||||

| 0.003 | 0.007 | ||||||||||||

Although all estimates for are of the same order of magnitude, Hall and Van Keilegom, (2003)’s is slightly larger than the estimates obtained with the other two methods; the same can be said for the estimates of . This might be attributed to the fact that Hall and Van Keilegom’s method does not take into account the apparent breakpoint within the time series. It seems that independently of the value of , the bias-reducing, difference-based estimators shown in this section provide similar results.

Supplementary Materials for “Autocovariance estimation via difference schemes for a semiparametric change point model with -dependent errors” by Michael Levine and Inder Tecuapetla-Gómez

Appendix A Proof of Theorems 1, 2, 3, 4

In this section we will employ the following notation. For , . For , , where is a change point. For , . For the subset , denotes the indicator function on . We will write to denote and . For , .

Recall that any continuous function defined on a compact set is also uniformly continuous. That is, there exist an increasing function , called the modulus of continuity of , that is vanishing at zero and continuous at zero, such that for all .

Proof of Theorem 1.

Let denote an vector of zeros (this is a vector with rows and 1 column). This allows us to define the -dimensional row vector , the corresponding matrix

and the symmetric matrix .

It is not difficult to see that for ,

Therefore,

Proof of Theorem 2.

Next, observe that

Proof of Theorem 3.

We will write instead of . Writing , we get that

| (14) |

Note that we can write . In order to make the notation easier, we will suppress the vector from this point on hoping for this not to cause any confusion.

By direct calculation, we get that

| (15) |

Now, we compute the covariance between the terms. Since , we can see that

| (16) |

Due to Gaussianity it follows that for any and , In what follows we will need to use the following identities concerning central moments of the multivariate normal distribution (see e.g. Triantafyllopoulos, (2003)): for any integers , , , and

| (17) |

Next, observe that

Similar considerations allow us to obtain that

Due to -dependency provided that . Thus, taking expectation on both sides of (A) and utilizing the identities just derived we get

| (18) |

Proof of Theorem 4.

We will write instead of . We begin by using that for ,

| (20) |

Recall that was established above, cf. Theorem 3. Following the ideas and calculations leading to (14)-(A) we find that

We conclude this calculation by adapting Lemmas 5, 7 and 9 from the Appendix B to the current situation. More precisely, following the proof of each of those lemmas, line by line, we can show first that

Next, denote and verify directly that

and

An obvious adaptation of Lemma 10 allows us to see that the third term of above is bounded by .

Combining the above we get that

| (21) |

where

We now move on to the computation of the covariance between and . Let us write and . Since , and due to Proposition 1,

| (22) |

we must compute the expected value of in order to complete this part of the proof.

It is readily seen that

| (23) |

Appendix B Proofs of Lemmas used in Appendix A

In addition to the notation introduced in Appendix A, in this section for generic vectors and in , we will write to denote their inner product and for the norm of .

Lemma 1.

Suppose that the conditions of Theorem 1 hold. Then for

| (25) |

Proof.

Due to stationarity and -dependence, it can be seen that for any ,

| (26) |

Observe that for any , can be written as a pseudo telescopic sum. Indeed,

The last identity follows because . The same arguments used above yield

| (27) |

In what follows we will suppress the vector from the notation hoping to cause no confusion.

Using that for any sequence of real numbers ,

it follows that for any ,

| (28) |

Next, observe that for any and ,

and similarly, for any and ,

Therefore for any ,

| (29) |

Next, let us consider , see (27). Since for , , it follows that . Hence, . Similarly it can be proved that .

Lemma 2.

Suppose that the conditions of Theorem 1 hold. Then,

Proof.

Since for ,

| (31) |

in what follows we will consider only as the second term above can be handled similarly.

Lemma 3.

Proof.

From (31) it can be seen that

| (33) |

In what follows we will consider the first term only as the second term on the right-hand side above can be handled similarly. Occasionally, we will suppress from the notation hoping to cause no confusion.

It can be seen that

| (34) |

Now, we focus on the first term on the right-hand side of Eq. (34). For the following arguments, suppose that is a generic change-point (fixed). Observe that for any and any , , which implies that . Therefore, for and . Similarly, it can be seen that for , and .

Since the above holds true for any generic change-point , we conclude that

| (36) |

Next, we move to the second summand on the right-hand side of Eq. (34). For the following arguments, let us suppose that is a generic (and fixed) change-point. For define the sets

Note that when takes values on the set for then both and are equal to . Due to the definition of , when then takes the value of the next jump, that is . In summary,

Note also that by construction, for , .

In light of the above,

| (37) |

For , similar considerations yield

| (38) |

Lemma 4.

Proof.

It is straightforward that

where

It suffices to consider as the other term can be handled similarly.

We begin by noticing that for any ,

| (40) |

Next, following the ideas leading to Eq. (36), we get

| (41) |

Similarly as in (B), with , we can see that

| (42) |

Lemma 5.

Proof.

Since we get that

where the last equality follows from Lemma 4. The result follows after some algebra. ∎

Lemma 6.

Proof.

We begin by establishing (43). Recall that . First note that

| (45) |

For any with , let . We split the computation of in three ways, first we consider , then and finally .

Assume that . Note that for , which implies that . Note also that, implies that , i.e., . Since these arguments hold for any when we have shown that,

Assume now that . The arguments presented above allow us to get that for ,

Next, assume that . With the arguments utilized so far (basically inspection case by case), it is not difficult to see that

| (46) |

We can utilize the arguments presented above to show Eq. (44). Indeed, note first that since , it is not difficult to see that for ,

| (47) |

Lemma 7.

Proof.

Observe that due to -dependency,

Then, by definition

Because , . The uniform continuity of ensures that

Similarly, we find that

Consequently,

| (48) |

Next, for a generic and fixed change-point , set and use Lemma 6 to get that

| (49) |

Similarly, we get that

| (50) |

Lemma 8.

Proof.

We begin by establishing (51). Recall that . As in Lemma 6 here we also split the sum in three ways: let , first we consider , then and finally .

Assume that . It is not difficult to see that when , and , . Also, when and , . Hence,

Next, for any , it is straightforward to see that

Assume now that . We begin by studying the particular case . Then we get for and that . Also, when and , . Hence,

Similar arguments allow us to see that for where ,

| (53) |

Combining the arguments above, we have shown that the left-hand side of (51) is bounded by

Lemma 9.

Suppose that the conditions of Lemma 8 are satisfied. Then,

Proof.

In this proof, we will denote . For given , due to -dependency we get that when . Consequently,

This completes the proof. ∎

Lemma 10.

Let denote the autocovariance function of a stationary, -dependent process. Then

-

1.

,

-

2.

,

-

3.

.

Here .

Proof.

-

1.

. The inequality follows from the -dependency.

-

2.

First note that

Then, recall that when . Intersecting these two subsets we get that for . The rest of the proof is similar to that of 1.

-

3.

Follows from 1 and 2.

∎

References

- (1) Berkes, I., Gabrys, R., Horváth, L., and P., K. (2009a). Detecting changes in the mean of functional observations. Journal of the Royal Statistical Society: Series B, 71(5):927–946.

- (2) Berkes, I., Horváth, L., and Rice, G. (2009b). Weak invariance principles for sums of dependent random functions. Stochastic Processes and their Applications, 123(2):385–403.

- Chakar et al., (2017) Chakar, S., Lebarbier, E., Lévy-Leduc, C., Robin, S., et al. (2017). A robust approach for estimating change-points in the mean of an AR(1) process. Bernoulli, 23(2):1408–1447.

- Chan, (2022) Chan, K. W. (2022). Optimal difference-based variance estimators in time series: A general framework. The Annals of Statistics, 50(3):1376–1400.

- Chu et al., (2012) Chu, C.-K., Siao, J.-S., Wang, L.-C., and Deng, W.-S. (2012). Estimation of 2D jump location curve and 3D jump location surface in nonparametric regression. Statistics and Computing, 22(1):17–31.

- Chu et al., (1995) Chu, C.-S. J., Hornik, K., and Kaun, C.-M. (1995). MOSUM tests for parameter constancy. Biometrika, 82(3):603–617.

- Dai et al., (2015) Dai, W., Ma, Y., Tong, T., and Zhu, L. (2015). Difference-based variance estimation in nonparametric regression with repeated measurement data. Journal of Statistical Planning and Inference, 163:1–20.

- Davis et al., (2006) Davis, R. A., Lee, T. C. M., and Rodriguez-Yam, G. A. (2006). Structural break estimation for nonstationary time series models. Journal of the American Statistical Association, 101(473):223–239.

- Dette et al., (2020) Dette, H., Eckle, T., and Vetter, M. (2020). Multiscale change point detection for dependent data. Scandinavian Journal of Statistics, 47(4):1243–1274.

- Dette et al., (1998) Dette, H., Munk, A., and Wagner, T. (1998). Estimating the variance in nonparametric regression-what is a reasonable choice? J. R. Statist. Soc. B, 60 (3):751–764.

- Dette and Quanz, (2023) Dette, H. and Quanz, P. (2023). Detecting relevant changes in the spatiotemporal mean function. Journal of Time Series Analysis, 44(5-6 (Special issue in honour of Masanobu Taniguchi)):505–532.

- Engle et al., (1986) Engle, R. F., Granger, C. W., Rice, J., and Weiss, A. (1986). Semiparametric estimates of the relation between weather and electricity sales. Journal of the American statistical Association, 81(394):310–320.

- Enikeeva et al., (2020) Enikeeva, F., Munk, A., Pohlmann, M., and Werner, F. (2020). Bump detection in the presence of dependency: Does it ease or does it load? Bernoulli, 26(4):3280–3310.

- Frick et al., (2014) Frick, K., Munk, A., and Sieling, H. (2014). Multiscale change-point inference (with discussion and rejoinder by the authors). J. R. Statist. Soc. B, 76:495–580.

- Fryzlewicz, (2014) Fryzlewicz, P. (2014). Wild binary segmentation for multiple change-point detection. The Annals of Statistics, 42(6):2243–2281.

- Gao, (1995) Gao, J. (1995). Asymptotic theory for partly linear models. Communications in Statistics-Theory and Methods, 24(8):1985–2009.

- Gasser et al., (1986) Gasser, T., Sroka, L., and Jennen-Steinmetz, C. (1986). Residual variance and residual pattern in nonlinear regression. Biometrika, 73:625–633.

- Hall et al., (1990) Hall, P., Kay, J. W., and Titterington, D. M. (1990). Asymptotically optimal difference-based estimation of variance in nonparametric regression. Biometrika, 77 (3):521–528.

- Hall and Van Keilegom, (2003) Hall, P. and Van Keilegom, I. (2003). Using difference-based methods for inference in nonparametric regression with time series. J. R. Statist. Soc. B, 65 (2):443–456.

- Herrmann et al., (1992) Herrmann, E., Gasser, T., and Kneip, A. (1992). Choice of bandwidth for kernel regression when residuals are correlated. Biometrika, 79(4):783–795.

- Hotz et al., (2013) Hotz, T., Schütte, O. M., Sieling, H., Polupanow, T., Diederichsen, U., Steinem, C., and Munk, A. (2013). Idealizing ion channel recordings by a jump segmentation multiresolution filter. IEEE Transactions on Nanobioscience, 12 (4):376–386.

- Jandhyala et al., (2013) Jandhyala, V., Fotopoulos, S., MacNeill, I., and Liu, P. (2013). Inference for single and multiple change-points in time series. Journal of Time Series Analysis.

- Kang and Qiu, (2014) Kang, Y. and Qiu, P. (2014). Jump detection in blurred regression surfaces. Technometrics, 56(4):539–550.

- Khismatullina and Vogt, (2020) Khismatullina, M. and Vogt, M. (2020). Multiscale inference and long-run variance estimation in nonparametric regression with time series errors. J. R. Statist. Soc. B, 82:5–37.

- Müller and Stadtmüller, (1987) Müller, H.-G. and Stadtmüller, U. (1987). Estimation of heteroscedasticity in regression analysis. Ann. Statist., 15:610–635.

- Müller and Stadtmüller, (1988) Müller, H.-G. and Stadtmüller, U. (1988). Detecting dependencies in smooth regression models. Biometrika, 75 (4):639–50.

- Opsomer et al., (2001) Opsomer, J., Wang, Y., and Yang, Y. (2001). Nonparametric regression with correlated errors. Statistical Science, 16 (2):134–153.

- Park et al., (2006) Park, B. U., Lee, Y. K., Kim, T. Y., and Park, C. (2006). A simple estimator of error correlation in non-parametric regression models. Scandinavian Journal of Statistics, 33:451–462.

- Pein et al., (2018) Pein, F., Tecuapetla-Gómez, I., Schütte, O. M., Steinem, C., and Munk, A. (2018). Fully automatic multiresolution idealization for filtered ion channel recordings: flickering event detection. IEEE transactions on nanobioscience, 17(3):300–320.

- Preuß et al., (2015) Preuß, P., Puchstein, R., and Dette, H. (2015). Detection of multiple structural breaks in multivariate time series. Journal of the American Statistical Association, 110(510):654–668.

- Provost and Mathai, (1992) Provost, S. B. and Mathai, A. (1992). Quadratic forms in random variables: theory and applications. M. Dekker.

- Qiu and Kang, (2015) Qiu, P. and Kang, Y. (2015). Blind image deblurring using jump regression analysis. Statistica Sinica, pages 879–899.

- Qiu and Yandell, (1998) Qiu, P. and Yandell, B. (1998). Local polynomial jump-detection algorithm in nonparametric regression. Technometrics, 40(2):141–152.

- R Core Team, (2022) R Core Team (2022). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Rice, (1984) Rice, J. (1984). Bandwidth choice for nonparametric regression. Ann. Statist., 12:1215–1230.

- Shumway and Stoffer, (2019) Shumway, R. and Stoffer, D. (2019). Time series: a data analysis approach using R. CRC Press.

- Stoffer and Poison, (2023) Stoffer, D. and Poison, N. (2023). astsa: Applied Statistical Time Series Analysis. R package version 2.0.

- Tecuapetla-Gómez and Munk, (2017) Tecuapetla-Gómez, I. and Munk, A. (2017). Autocovariance estimation in regression with a discontinuous signal and -dependent errors: A difference-based approach. Scandinavian Journal of Statistics, 44(2):346–368.

- Tecuapetla-Gómez, (2023) Tecuapetla-Gómez, I. (2023). dbacf: Autocovariance Estimation via Difference-Based Methods. R package version 0.2.8.

- Triantafyllopoulos, (2003) Triantafyllopoulos, K. (2003). On the central moments of the multidimensional Gaussian distribution. The Mathematical Scientist, 28-1:125–128.

- Verbesselt et al., (2010) Verbesselt, J., Hyndman, R., Zeileis, A., and Culvenor, D. (2010). Phenological change detection while accounting for abrupt and gradual trends in satellite image time series. Remote Sensing of Environment, 114(12):2970–2980.

- Vogelsang and Yang, (2016) Vogelsang, T. J. and Yang, J. (2016). Exactly/nearly unbiased estimation of autocovariances of a univariate time series with unknown mean. Journal of Time Series Analysis, 37(6):723–740.

- von Neumann et al., (1941) von Neumann, J., Kent, R. H., Bellinson, H. R., and Hart, B. I. (1941). The mean square successive difference. The Annals of Mathematical Statistics, 12(2):153–162.

- Wang et al., (2017) Wang, W., Lin, L., and Yu, L. (2017). Optimal variance estimation based on lagged second-order difference in nonparametric regression. Computational Statistics, 32(3):1047–1063.

- Wang and Yu, (2017) Wang, W. and Yu, P. (2017). Asymptotically optimal differenced estimators of error variance in nonparametric regression. Computational Statistics & Data Analysis, 105:125–143.

- Wu, (2005) Wu, W. B. (2005). Nonlinear system theory: another look at dependence. Proc. Natl. Acad. Sci. USA, 102(40):14150–14154.

- You and Chen, (2007) You, J. and Chen, G. (2007). Semiparametric generalized least squares estimation in partially linear regression models with correlated errors. Journal of Statistical Planning and Inference, 137(1):117–132.

- Zeileis et al., (2002) Zeileis, A., Leisch, F., Hornik, K., and Kleiber, C. (2002). strucchange: An R package for testing for structural change in linear regression models. Journal of Statistical Software, Articles, 7(2):1–38.

- Zhou et al., (2018) Zhou, Y., Cheng, Y., Dai, W., and Tong, T. (2018). Optimal difference-based estimation for partially linear models. Computational Statistics, pages 1–23.