Multi-Criteria Dimensionality Reduction with

Applications to Fairness

Abstract

Dimensionality reduction is a classical technique widely used for data analysis. One foundational instantiation is Principal Component Analysis (PCA), which minimizes the average reconstruction error. In this paper, we introduce the multi-criteria dimensionality reduction problem where we are given multiple objectives that need to be optimized simultaneously. As an application, our model captures several fairness criteria for dimensionality reduction such as our novel Fair-PCA problem and the Nash Social Welfare (NSW) problem. In Fair-PCA, the input data is divided into groups, and the goal is to find a single -dimensional representation for all groups for which the minimum variance of any one group is maximized. In NSW, the goal is to maximize the product of the individual variances of the groups achieved by the common low-dimensional space.

Our main result is an exact polynomial-time algorithm for the two-criterion dimensionality reduction problem when the two criteria are increasing concave functions. As an application of this result, we obtain a polynomial time algorithm for Fair-PCA for groups and a polynomial time algorithm for NSW objective for groups. We also give approximation algorithms for . Our technical contribution in the above results is to prove new low-rank properties of extreme point solutions to semi-definite programs. We conclude with experiments indicating the effectiveness of algorithms based on extreme point solutions of semi-definite programs on several real-world data sets.

1 Introduction

Dimensionality reduction is the process of choosing a low-dimensional representation of a large, high-dimensional data set. It is a core primitive for modern machine learning and is being used in image processing, biomedical research, time series analysis, etc. Dimensionality reduction can be used during the preprocessing of the data to reduce the computational burden as well as at the final stages of data analysis to facilitate data summarization and data visualization [72, 41]. Among the most ubiquitous and effective of dimensionality reduction techniques in practice are Principal Component Analysis (PCA) [68, 43, 39], multidimensional scaling [57], Isomap [78], locally linear embedding [73], and t-SNE [61].

One of the major obstacles to dimensionality reduction tasks in practice is complex high-dimensional data structures that lie on multiple different low-dimensional subspaces. For example, Maaten and Hinton [61] address this issue for low-dimensional visualization of images of objects from diverse classes seen from various viewpoints. Dimensionality reduction algorithms may optimize one data structure well while performs poorly on the others. In this work, we consider when those data structures lying on different low-dimensional subspaces are subpopulations partitioned by sensitive attributes, such as gender, race, and education level.

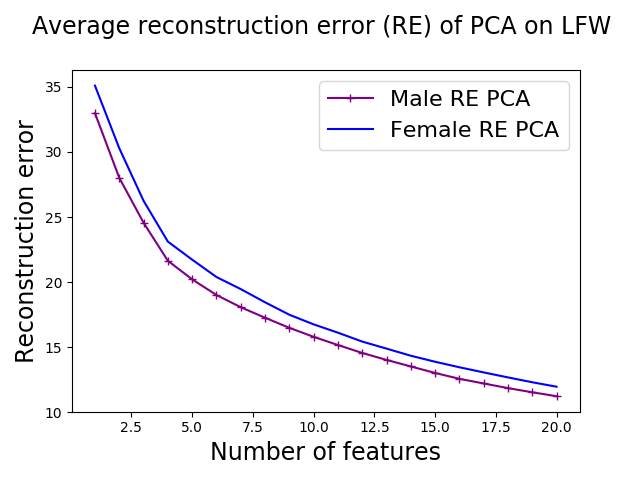

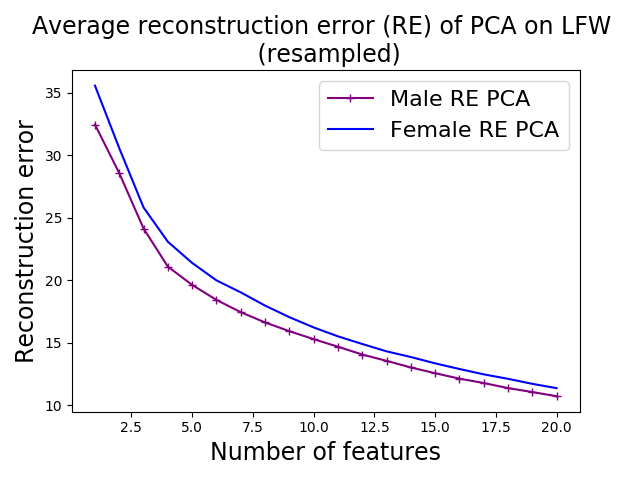

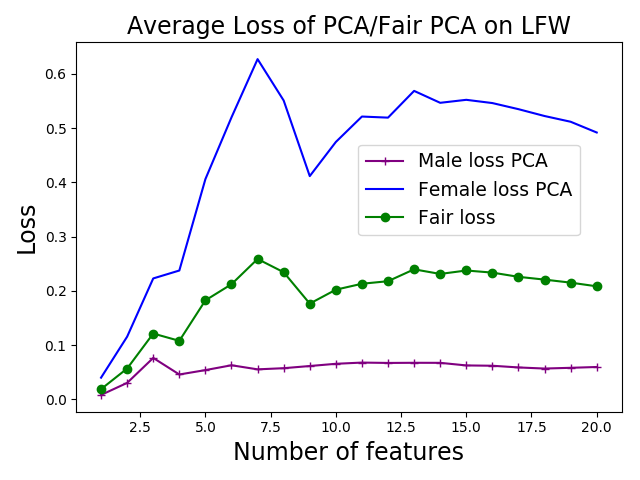

As an illustration, consider applying PCA on a high-dimensional data to do a visualization analysis in low dimensions. Standard PCA aims to minimize the single criteria of average reconstruction error over the whole data, but the reconstruction error on different parts of data can be different. In particular, we show in Figure 1 that PCA on the real-world labeled faces in the wild data set (LFW) [40] has higher reconstruction error for women than men, and this disparity in performance remains even if male and female faces are sampled with equal weight. We similarly observe difference in reconstruction errors of PCA in other real-world datasets. Dissimilarity of performance on different data structure, such as unbalanced average reconstruction errors we demonstrated, raises ethical and legal concerns whether outcomes of algorithms discriminate the subpopulations against sensitive attributes.

Relationship to fairness in machine learning.

In recent years, machine learning community has witnessed an onslaught of charges that real-world machine learning algorithms have produced “biased” outcomes. The examples come from diverse and impactful domains. Google Photos labeled African Americans as gorillas [79, 75] and returned queries for CEOs with images overwhelmingly male and white [53], searches for African American names caused the display of arrest record advertisements with higher frequency than searches for white names [77], facial recognition has wildly different accuracy for white men than dark-skinned women [17], and recidivism prediction software has labeled low-risk African Americans as high-risk at higher rates than low-risk white people [4].

The community’s work to explain these observations has roughly fallen into either “biased data” or “biased algorithm” bins. In some cases, the training data might under-represent (or over-represent) some group, or have noisier labels for one population than another, or use an imperfect proxy for the prediction label (e.g., using arrest records in lieu of whether a crime was committed). Separately, issues of imbalance and bias might occur due to an algorithm’s behavior, such as focusing on accuracy across the entire distribution rather than guaranteeing similar false positive rates across populations, or by improperly accounting for confirmation bias and feedback loops in data collection. If an algorithm fails to distribute loans or bail to a deserving population, the algorithm won’t receive additional data showing those people would have paid back the loan, but it will continue to receive more data about the populations it (correctly) believed should receive loans or bail.

Many of the proposed solutions to “biased data” problems amount to re-weighting the training set or adding noise to some of the labels; for “biased algorithms,” most work has focused on maximizing accuracy subject to a constraint forbidding (or penalizing) an unfair model. Both of these concerns and approaches have significant merit, but form an incomplete picture of the machine learning pipeline where unfairness might be introduced therein. Our work takes another step in fleshing out this picture by analyzing when dimensionality reduction might inadvertently introduce bias.

This work underlines the importance of considering fairness and bias at every stage of data science, not only in gathering and documenting a data set [33] and in training a model, but also in any interim data processing steps. Many scientific disciplines have adopted PCA as a default preprocessing step, both to avoid the curse of dimensionality and also to do exploratory/explanatory data analysis (projecting the data into a number of dimensions that humans can more easily visualize). The study of human biology, disease, and the development of health interventions all face both aforementioned difficulties, as do numerous economic and financial analysis. In such high-stakes settings, where statistical tools will help in making decisions that affect a diverse set of people, we must take particular care to ensure that we share the benefits of data science with a diverse community.

We also emphasize this work has implications for representational rather than just allocative harms, a distinction drawn by Crawford [25] between how people are represented and what goods or opportunities they receive. Showing primates in search results for African Americans is repugnant primarily due to its representing and reaffirming a racist painting of African Americans, not because it directly reduces any one person’s access to a resource. If the default template for a data set begins with running PCA, and PCA does a better job representing men than women, or white people over minorities, the new representation of the data set itself may rightly be considered an unacceptable sketch of the world it aims to describe.

Remark 1.1.

We focus on the setting where we ask for a single projection into dimensions rather than separate projections for each group, because using distinct projections (or more generally distinct models) for different populations raises legal and ethical concerns.111Lipton et al. [59] have asked whether equal treatment requires different models for two groups.

Instability of PCA.

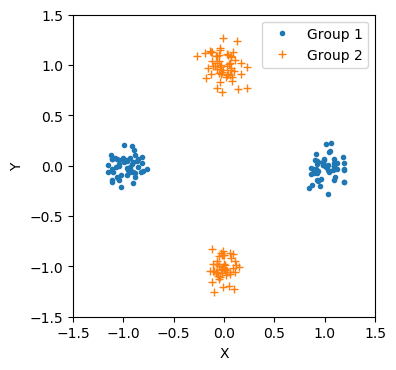

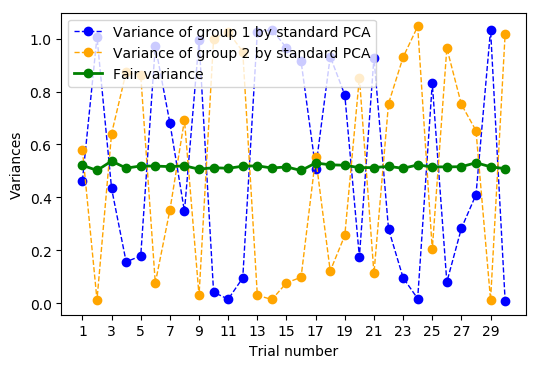

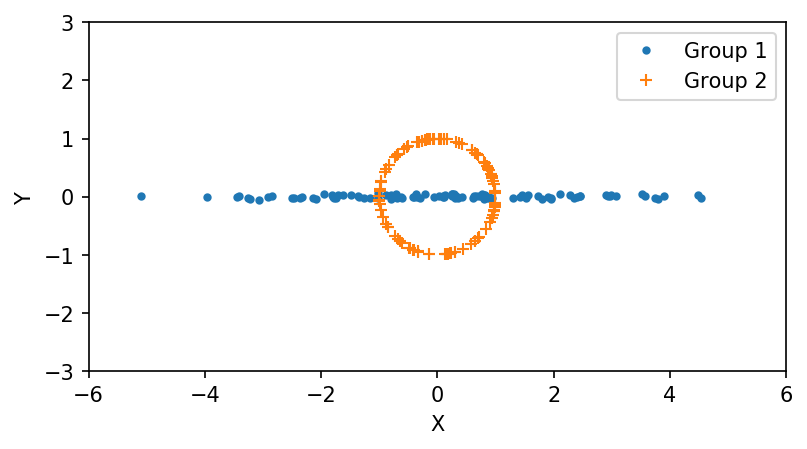

Disparity of performance in subpopulations of PCA is closely related to its instability. Maximizing total variance or equivalently minimizing total reconstruction errors is sensitive to a slight change of data, giving widely different outcomes even if data are sampled from the same distribution. An example is shown in Figure 2. Figure 2a shows the distribution of two groups lying in orthogonal dimensions. When the first group’s variance in the x-axis is slightly higher than the second group’s variance in the y-axis, PCA outputs the x-axis, otherwise it outputs the y-axis, and it rarely outputs something in between. The instability of performance can be shown in Figure 2b. Even though in each trial, data are sampled from the same distribution, PCA solutions are unstable and give oscillating variances to each group. However, solutions to one of our proposed formulations (Fair-PCA, which is to be presented later) are stable and give the same, optimal variance to both groups in each trial.

Our work presents a novel general framework that addresses all aforementioned issues: data lying on different low-dimensional structure, unfairness, and instability of PCA. A common difficulty in those settings is that a single criteria for dimensionality reduction might not be sufficient to capture different structures in the data. This motivates our study of multi-criteria dimensionality reduction.

Multi-criteria dimensionality reduction.

Multi-criteria dimensionality reduction could be used as an umbrella term with specifications changing based on the applications and the metrics that the machine learning researcher has in mind. Aiming for an output with a balanced error over different subgroups seems to be a natural choice, extending economic game theory literature. For example, this covers maximizing geometric mean of the variances of the groups, which is the well-studied Nash social welfare (NSW) objective [51, 63]. Motivated by these settings, the more general question that we would like to study is as follows.

Question 1.

How might one redefine dimensionality reduction to produce projections which optimize different groups’ representation in a balanced way?

For simplicity of explanation, we first describe our framework for PCA, but the approach is general and applies to a much wider class of dimensionality reduction techniques. Consider the data points as rows of an matrix . For PCA, the objective is to find an projection matrix that maximizes the Frobenius norm (this is equivalent to minimizing the reconstruction error ). Suppose that the rows of belong to different groups based on demographics or some other semantically meaningful clustering. The definition of these groups need not be a partition; each group could be defined as a different weighting of the data set (rather than a subset, which is a 0/1 weighting). Multi-criteria dimensionality reduction can then be viewed as simultaneously considering objectives on the different weightings of , i.e., . One way to balance multiple objectives is to find a projection that maximizes the minimum objective value over each of the groups (weightings):

More generally, let denote the set of all projection matrices , i.e., matrices with orthonormal columns. For each group , we associate a function that denotes the group’s objective value for a particular projection. We are also given an accumulation function . We define the -multi-criteria dimensionality reduction problem as finding a -dimensional projection which optimizes

In the above example of Fair-PCA, is simply the function and is the total squared norm of the projection of vectors in . The central motivating questions of this paper are the following:

-

•

What is the complexity of Fair-PCA?

-

•

More generally, what is the complexity of Multi-Criteria-Dimension-Reduction?

Framed another way, we ask whether these multi-criteria optimization problems force us to incur substantial computational cost compared to optimizing over alone.

Summary of contributions.

We summarize our contributions in this work as follows.

-

1.

We introduce a novel definition of Multi-Criteria-Dimension-Reduction.

-

2.

We give polynomial-time algorithms for Multi-Criteria-Dimension-Reduction with provable guarantees.

-

3.

We analyze the complexity and show hardness of Multi-Criteria-Dimension-Reduction.

-

4.

We present empirical results to show efficacy of our algorithms in addressing fairness.

We have introduced Multi-Criteria-Dimension-Reduction earlier, and we now present the technical contributions in this paper.

1.1 Summary of technical results

Let us first focus on Fair-PCA for ease of exposition. The problem can be reformulated as the following mathematical program where we denote by . A natural approach to solving this problem is to consider the SDP relaxation obtained by relaxing the rank constraint to a bound on the trace.

| Exact Fair-PCA | SDP relaxation of Fair-PCA (1) (2) (3) (4) |

Our first main result is that the SDP relaxation is exact when there are two groups. Thus finding an extreme point of this SDP gives an exact algorithm for Fair-PCA for two groups.

Theorem 1.2.

Any optimal extreme point solution to the SDP relaxation for Fair-PCA with two groups has rank at most . Therefore, -group Fair-PCA can be solved in polynomial time.

Given data points partitioned into groups in dimensions, the algorithm runs in time. is from computing and is from solving an SDP over PSD matrices [10]. Alternative heuristics and their analyses are discussed in Section 7.2. Our results also hold for the Multi-Criteria-Dimension-Reduction when is monotone nondecreasing in any one coordinate and concave, and each is an affine function of (and thus a special case of a quadratic function in ).

Theorem 1.3.

There is a polynomial-time algorithm for -group Multi-Criteria-Dimension-Reduction when is concave and monotone nondecreasing for at least one of its two arguments and each is linear in , i.e., for some matrix .

As indicated in the theorem, the core idea is that extreme-point solutions of the SDP in fact have rank , not just trace equal to . For , the SDP need not recover a rank- solution. In fact, the SDP may be inexact even for (see Section 6.2). Nonetheless, we show that we can bound the rank of a solution to the SDP and obtain the following result. We state it for Fair-PCA, although the same bound holds for Multi-Criteria-Dimension-Reduction under the same assumptions as in Theorem 1.3. Note that this result generalizes Theorems 1.2 and 1.3.

Theorem 1.4.

For any concave that is monotone nondecreasing in at least one of its arguments, there exists a polynomial time algorithm for Multi-Criteria-Dimension-Reduction with groups that returns a -dimensional embedding whose objective value is at least that of the optimal -dimensional embedding. If is only concave, then the solution lies in at most dimensions.

We note that the iterative rounding framework for linear programs [58] would give a rank bound of for the Fair-PCA problem (see [74] for details). Hence, we strictly improves the bound to . Moreover, if the dimensionality of the solution is a hard constraint, instead of tolerating extra dimension in the solution, one may solve Fair-PCA for target dimension to guarantee a solution of rank at most . Thus, we obtain an approximation algorithm for Fair-PCA of factor .

Corollary 1.5.

Let be data sets of groups and suppose . Then there exists a polynomial-time approximation algorithm of factor to Fair-PCA.

That is, the algorithm returns a projection of exact rank with objective at least of the optimal objective. More details on the approximation result are in Section 3.1. The runtime of Theorems 1.3 and 1.4 depends on the access to first order oracle to , and standard application of the ellipsoid algorithm would take oracle calls.

We also develop a general rounding framework for SDPs with eigenvalue upper bounds and other linear constraints. This algorithm gives a solution of desired rank that violates each constraint by a bounded amount. It implies that for Fair-PCA and some of its variants, the additive error is

where . The precise statement is Theorem 1.9 and full details are presented in Section 4.

It is natural to ask whether Fair-PCA is NP-hard to solve exactly. The following result implies that it is, even for target dimension .

Theorem 1.6.

The Fair-PCA problem for target dimension is NP-hard when the number of groups is part of the input.

This raises the question of the complexity for constant groups. For groups, we would have constraints, one for each group, plus the eigenvalue constraint and the trace constraint; now the tractability of the problem is far from clear. In fact, as we show in Section 6.2, the SDP has an integrality gap even for . We therefore consider an approach beyond SDPs, to one that involves solving non-convex problems. Thanks to the powerful algorithmic theory of quadratic maps, developed by Grigoriev and Pasechnik [36], it is polynomial-time solvable to check feasibility of a set of quadratic constraints for any fixed . As we discuss next, their algorithm can check for zeros of a function of a set of quadratic functions, and can be used to optimize the function. Using this result, we show that for , there is a polynomial-time algorithm for rather general functions of the values of individual groups.

Theorem 1.7.

Let where is a degree- polynomial in some computable subring of , and let each be quadratic for . Then there is an algorithm to solve -Multi-Criteria-Dimension-Reduction in time .

By choosing to be the product polynomial over the usual ring or the function which is degree in the ring, this applies to Fair-PCA discussed above and various other problems.

1.2 Techniques

SDP extreme points.

For , the underlying structural property we show is that extreme point solutions of the SDP have rank exactly . First, for , this is the largest eigenvalue problem, since the maximum obtained by a matrix of trace equal to can also be obtained by one of the extreme points in the convex decomposition of this matrix. This extends to trace equal to any , i.e., the optimal solution must be given by the top eigenvectors of . Second, without the eigenvalue bound, for any SDP with constraints, there is an upper bound on the rank of any extreme point, of , a seminal result of Pataki [67] (see also Barvinok [9]). However, we cannot apply this directly as we have the eigenvalue upper bound constraint. The complication here is that we have to take into account the constraint without increasing the rank.

Theorem 1.8.

Let and be real matrices, , and . Suppose the semi-definite program :

| (5) | |||||

| (6) | |||||

| (7) | |||||

| (8) |

where , has a nonempty feasible set. Then, all extreme optimal solutions to have rank at most . Moreover, given a feasible optimal solution, an extreme optimal solution can be found in polynomial time.

To prove the theorem, we extend Pataki [67]’s characterization of rank of SDP extreme points with minimal loss in the rank. We show that the constraints can be interpreted as a generalization of restricting variables to lie between and in the case of linear programming relaxations. From a technical perspective, our results give new insights into structural properties of extreme points of semi-definite programs and more general convex programs. Since the result of [67] has been studied from perspective of fast algorithms [16, 18, 19] and applied in community detection and phase synchronization [7], we expect our extension of the result to have further applications in many of these areas.

SDP iterative rounding.

Using Theorem 1.8, we extend the iterative rounding framework for linear programs (see [58] and references therein) to semi-definite programs, where the constraints are generalized to eigenvalue bounds. The algorithm has a remarkably similar flavor. In each iteration, we fix the subspaces spanned by eigenvectors with and eigenvalues, and argue that one of the constraints can be dropped while bounding the total violation in the constraint over the course of the algorithm. While this applies directly to the Fair-PCA problem, it is in fact a general statement for SDPs, which we give below.

Let be a collection of matrices. For any set , let the largest singular of the average of matrices . We let

Theorem 1.9.

Let be a real matrix and be a collection of real matrices, , and . Suppose the semi-definite program :

has a nonempty feasible set and let denote an optimal solution. The algorithm Iterative-SDP (see Algorithm 1 in Section 4) returns a matrix such that

-

1.

rank of is at most ,

-

2.

, and

-

3.

for each .

Moreover, Iterative-SDP runs in polynomial time.

1.3 Organization

We present related work in Section 1.4. In Section 2, we prove Theorem 1.8 and apply the result to Multi-Criteria-Dimension-Reduction to obtain Theorem 1.4. In Section 3, we present and motivate several fairness criteria for dimensionality reduction, including a novel one of our own, and apply Theorem 1.4 to get approximation algorithm of Fair-PCA, thus proving Corollary 1.5. In Section 4, we give an iterative rounding algorithm and prove Theorem 1.9. In Section 5, we show the polynomial-time solvability of Multi-Criteria-Dimension-Reduction when the number of groups and the target dimension are fixed, proving Theorem 1.7. In Section 6, we show NP-hardness and integrality gap of Multi-Criteria-Dimension-Reduction for . In Section 7, we show the experimental results of our algorithms on real-world data sets, evaluated by different fairness criteria, and present additional algorithms with improved runtime. We present missing proofs in Appendix A. In Appendix B, we show that the rank of extreme solutions of SDPs in Theorem 1.8 cannot be improved.

1.4 Related work

Optimization.

As mentioned earlier, Pataki [67] (see also Barvinok [9]) showed that low rank solutions to semi-definite programs with small number of affine constraints can be obtained efficiently. Restricting a feasible region of certain SDPs relaxations with low-rank constraints has been shown to avoid spurious local optima [7] and reduce the runtime due to known heuristics and analysis [18, 19, 16]. We also remark that methods based on Johnson-Lindenstrauss lemma can also be applied to obtain bi-criteria results for the Fair-PCA problem. For example, So et al. [76] give algorithms that give low rank solutions for SDPs with affine constraints without the upper bound on eigenvalues. Here we have focused on the single criteria setting, with violation either in the number of dimensions or the objective but not both. We also remark that extreme point solutions to linear programming have played an important role in design of approximation algorithms [58], and our result add to the comparatively small, but growing, number of applications for utilizing extreme points of semi-definite programs.

A closely related area, especially to Multi-Criteria-Dimension-Reduction, is multi-objective optimization which has a vast literature. We refer the reader to Deb [26] and references therein. We remark that properties of extreme point solutions of linear programs [70, 34] have also been utilized to obtain approximation algorithms to multi-objective problems. For semi-definite programming based methods, the closest works are on simultaneous max-cut [12, 13] that utilize sum of squares hierarchy to obtain improved approximation algorithms.

Fairness in machine learning.

The applications of multi-criteria dimensionality reduction in fairness are closely related to studies on representational bias in machine learning [25, 65, 15], for which there have been various mathematical formulations studied [23, 22, 55, 56]. One interpretation of our work is that we suggest using multi-criteria dimensionality reduction rather than standard PCA when creating a lower-dimensional representation of a data set for further analysis. Two most relevant pieces of work take the posture of explicitly trying to reduce the correlation between a sensitive attribute (such as race or gender) and the new representation of the data. The first piece is a broad line of work [85, 11, 21, 62, 86] that aims to design representations which will be conditionally independent of the protected attribute, while retaining as much information as possible (and particularly task-relevant information for some fixed classification task). The second piece is the work by Olfat and Aswani [66], who also look to design PCA-like maps which reduce the projected data’s dependence on a sensitive attribute. Our work has a qualitatively different goal: we aim not to hide a sensitive attribute, but to instead maintain as much information about each population after projecting the data. In other words, we look for representation with similar richness for population, rather than making each group indistinguishable.

Other work has developed techniques to obfuscate a sensitive attribute directly [69, 48, 20, 47, 60, 49, 50, 37, 30, 84, 31, 1]. This line of work diverges from ours in two ways. First, these works focus on representations which obfuscate the sensitive attribute rather than a representation with high fidelity regardless of the sensitive attribute. Second, most of these works do not give formal guarantees on how much an objective will degrade after their transformations. Our work gives theoretical guarantees including an exact optimality for two groups.

Much of other work on fairness for learning algorithms focuses on fairness in classification or scoring [27, 38, 54, 24], or in online learning settings [44, 52, 28]. These works focus on either statistical parity of the decision rule, or equality of false positives or negatives, or an algorithm with a fair decision rule. All of these notions are driven by a single learning task rather than a generic transformation of a data set, while our work focuses on a ubiquitous, task-agnostic preprocessing step.

Game theory applications.

2 Low-rank solutions of Multi-Criteria-Dimension-Reduction

In this section, we show that all extreme solutions of SDP relaxation of Multi-Criteria-Dimension-Reduction have low rank, proving Theorem 1.2-1.4. Before we state the results, we make the following assumptions. In this section, we let be a concave function, and mildly assume that can be accessed with a polynomial-time subgradient oracle. We are explicitly given functions which are affine in , i.e., we are given real matrices and constants , and .

We assume to be -Lipschitz. For functions that are -Lipschitz, we define an -optimal solution to -Multi-Criteria-Dimension-Reduction as a matrix of rank with whose objective value is at most away from the optimum. IWhen an optimization problem has affine constraints where is -Lipschitz for all , we also define an -feasible solution as a projection matrix of rank with that violates the th affine constraint by at most for all . Note that the feasible region of the problem is implicitly bounded by the constraint .

In this work, an algorithm may involve solving an optimization under a matrix linear inequality, whose exact optimal solutions may not be representable in finite bits of computation. However, we give algorithms that return an -feasible solution whose running time depends polynomially on for any . This is standard for computational tractability in convex optimization (see, for example, in [10]). Therefore, for ease of exposition, we omit the computational error dependent on this to obtain an -feasible and -optimal solution, and define polynomial time as polynomial in and .

We first prove Theorem 1.8 below. To prove Theorem 1.2-1.4, we first show that extreme point solutions in a general class of semi-definite cone under affine constraints and have low rank. The statement builds on a result of [67], and also generalizes to SDPs under a constraint for any given PSD matrix by the transformation of the SDP feasible region. We then apply our result to Multi-Criteria-Dimension-Reduction, which generalizes Fair-PCA, and prove Theorem 1.4, which implies Theorem 1.2 and 1.3.

Proof of Theorem 1.8: Let be an extreme point optimal solution to . Suppose rank of , say , is more than . Then we show a contradiction to the fact that is extreme. Let of the eigenvalues of be equal to one. If , then we have since , and we are done. Thus we assume that . In that case, there exist matrices , and a symmetric matrix such that

where , , , and that the columns of and are orthogonal, i.e. has orthonormal columns. Now, we have

and so that and are linear in .

Observe that the set of symmetric matrices forms a vector space of dimension with the above inner product where we consider the matrices as long vectors. If , then there exists a -symmetric matrix such that for each and .

But then we claim that is feasible for some small , which implies a contradiction to being extreme. Indeed, satisfies all the linear constraints by the construction of . Thus it remains to check the eigenvalues of . Observe that

with orthonormal . Thus it is enough to consider the eigenvalues of

Observe that eigenvalues of the above matrix are exactly ones and eigenvalues of . Since eigenvalues of are bounded away from and , one can find a small such that the eigenvalues of are bounded away from and as well, so we are done. Therefore, we must have which implies . By , we have .

To obtain the algorithmic result, given feasible , we iteratively reduce by at least one until . While , we obtain by Gaussian elimination. Now we want to find the correct value of so that takes one of the eigenvalues to zero or one. First, determine the sign of to find the correct sign to move that keeps the objective non-increasing, say it is in the positive direction. Since the feasible set of is convex and bounded, the ray intersects the boundary of feasible region at a unique . Perform binary search for up to a desired accuracy, and set . Since for each and , the additional tight constraint from moving to the boundary of the feasible region must be an eigenvalue constraint , i.e., at least one additional eigenvalue is now at 0 or 1, as desired. We apply eigenvalue decomposition to and update accordingly, and repeat.

The algorithm involves at most rounds of reducing , each of which involves Gaussian elimination and several iterations of checking (from binary search) which can be done by eigenvalue value decomposition. Gaussian elimination and eigenvalue decomposition can be done in time, and therefore the total runtime of SDP rounding is which is polynomial.

One can initially reduce the rank of given feasible using an LP rounding in time [74] before our SDP rounding. This reduces the number of iterative rounding steps; particularly, is further bounded by . The runtime complexity is then .

The next corollary is another useful fact of the low-rank property and is used in the analysis of iterative rounding algorithm in Section 4. The corollary can be obtained from the bound in the proof of Theorem 1.8.

Corollary 2.1.

The number of fractional eigenvalues in any extreme point solution to is bounded by .

We are now ready to prove the main result that we can find a low-rank solution for Multi-Criteria-Dimension-Reduction.

Proof of Theorem 1.4: Let . Given assumptions on , we write a relaxation of Multi-Criteria-Dimension-Reduction as follows:

| (9) | ||||

| (10) | ||||

| (11) |

Since is concave in and is affine in , we have that as a function of is also concave in . By concavity of and that the feasible set is convex and bounded, we can solve the convex program (9)-(11) in polynomial time, e.g. by ellipsoid method, to obtain a (possibly high-rank) optimal solution . (In the case that is linear, the relaxation is also an SDP and may be solved faster in theory and practice).

We first assume that is monotonic in at least one coordinate, so without loss of generality, we let be nondecreasing in the first coordinate. To reduce the rank of , we consider an :

| (12) | |||||

| (13) | |||||

| (14) | |||||

| (15) |

has a feasible solution of objective , and note that there are constraints in (13). Hence, we can apply the algorithm in Theorem 1.8 with to find an extreme solution of of rank at most . Since is nondecreasing in , an optimal solution to gives objective value at least the optimum of the relaxation and hence at least the optimum of the original Multi-Criteria-Dimension-Reduction.

If the assumption that is monotonic in at least one coordinate is dropped,

the argument holds by indexing constraints (13) in for all groups instead of groups.

Another way to state Theorem 1.4 is that the number of groups must reach before additional dimensions in the solution matrix is required to achieve the optimal objective value. For , no additional dimension in the solution is necessary to attain the optimum, which proves Theorem 1.3. In particular, it applies to Fair-PCA with two groups, proving Theorem 1.2. We note that the rank bound in Theorem 1.8 (and thus also the bound in Corollary 2.1) is tight. An example of the problem instance follows from [14] with a slight modification. We refer the reader to Appendix B for details.

3 Applications of low-rank solutions in fairness

In this section, we show applications of low-rank solutions of Theorem 1.4 in fairness applications of dimensionality reduction. We describe existing fairness criteria and motivate our new fairness objective, summarized in Table 1. The new fairness objective appropriately addresses fairness when subgroups have different optimal variances in a low-dimensional space. We note that all fairness criteria in this section satisfy the assumption in Theorem 1.4 that is concave and monotone nondecreasing in at least one (in fact, all) of its arguments, and thus these fairness objectives can be solved with Theorem 1.4. We also give approximation algorithm for Fair-PCA, proving Corollary 1.5.

3.1 Application to Fair-PCA

We prove Corollary 1.5 below. Recall that, by Theorem 1.4, additional dimensions for the projection are required to achieve the optimal objective. One way to ensure that the algorithm outputs -dimensional projection is to solve the problem in the lower target dimension , and then apply the rounding algorithm described in Section 2.

Proof of Corollary 1.5.

We find an extreme solution of the Fair-PCA problem of finding a projection from to target dimensions. By Theorem 1.4, the rank of is at most .

Denote the optimal value and an optimal solution to exact Fair-PCA with target dimension , respectively. Note that is a feasible solution to the Fair-PCA relaxation (1.1)-(4) on target dimension whose objective is at least , since the Fair-PCA relaxation objective scales linearly with . Therefore, the optimal value of Fair-PCA relaxation of target dimension , which is achieved by (Theorem 1.4), is at least . Hence, we obtain the -approximation. ∎

3.2 Welfare economic and NSW

| Name | Multi-Criteria-Dimension-Reduction | ||

|---|---|---|---|

| Standard PCA | sum | ||

| Fair-PCA (MM-Var) | min | ||

| Nash social welfare (NSW) | product | ||

| Marginal loss (MM-Loss) | min |

If we interpret in Fair-PCA as individual utility, then standard PCA maximizes the total utility of individuals, also known as a utilitarian objective in welfare economic. One other objective is egalitarian, aiming to maximize the minimum utility [45], which is equivalent to Fair-PCA in our setting. One other example, which lies between the two, is to choose the product function for the accumulation function . This is also a natural choice, famously introduced in Nash’s solution to the bargaining problem [63, 51], and we call this objective Nash Social Welfare (NSW). The three objectives are special cases of the th power mean of individual utilities, i.e. , with giving standard PCA, Fair-PCA, and NSW, respectively. Since the th power mean is concave for , the assumptions in Theorem 1.4 hold and our algorithms apply to these objectives.

Because the assumptions in Theorem 1.4 does not change under an affine transformation of , we may also take any weighting and introduce additive constants on the square norm. For example, we can take the average squared norm of the projections rather than the total, replacing by where is the number of data points in , in any of the discussed fairness criteria. This normalization equalizes weight of each group, which can be useful when groups are of very different sizes, and is also used in all of our experiments. More generally, one can weight each by a positive constant , where the appropriate weighting of objectives often depends on the context and application. Another example is to replace by , which optimizes the worst reconstruction error rather than the worst variance across all groups as in the Fair-PCA definition.

3.3 Marginal loss objective

We now present a novel fairness criterion marginal loss objective. We first give a motivating example of two groups for this objective, shown in Figure 3.

In this example, two groups can have very different variances when projected onto one dimension: the first group has a perfect representation in the horizontal direction and enjoys high variance, while the second has lower variance for every projection. Thus, asking for a projection which maximizes the minimum variance might incur loss of variance on the first group while not improving the second group. So, minimizing the maximum reconstruction error of these two groups fails to account for the fact that two populations might have wildly different representation variances when embedded into dimensions. Optimal solutions to such objective might behave in a counterintuitive way, preferring to exactly optimize for the group with smaller inherent representation variance rather than approximately optimizing for both groups simultaneously. We find this behaviour undesirable—it requires sacrifice in quality for one group for no improvement for the other group. In other words, it does not satisfy Pareto-optimality.

We therefore turn to finding a projection which minimizes the maximum deviation of each group from its optimal projection. This optimization asks that two groups suffer a similar decrease in variance for being projected together onto dimensions compared to their individually optimal projections ("the marginal cost of sharing a common subspace"). Specifically, we set the utility as the change of variance for each group and in the Multi-Criteria-Dimension-Reduction formulation. This gives an optimization problem

| (16) |

We refer to as the loss of group by a projection , and we call the objective (16) to be minimized the marginal loss objective.

For two groups, marginal loss objective prevents the optimization from incurring loss of variance for one subpopulation without improving the other as seen in Figure 3. In fact, we show that an optimal solution of marginal loss objective always gives the same loss for two groups. As a result, marginal loss objective not only satisfies Pareto-optimality , but also equalizes individual utilities, a property that none of the previously mentioned fairness criteria necessarily holds.

Theorem 3.1.

Let be an optimal solution to (16) for two groups. Then,

Theorem 3.1 can be proved by a "local move" argument on the space of all -dimensional subspaces equipped with a carefully defined distance metric. We define a new metric space since the move is not valid on the natural choice of space, namely the domain with Euclidean distance, as the set is not convex. We also give a proof using the SDP relaxation of the problem. We refer the reader to Appendix A for the proofs of Theorem 3.1. In general, Theorem 3.1 does not generalize to more than two groups (see Section 6.2).

Another motivation of the marginal loss objective is to check bias in PCA performance on subpopulations. A data set may show a small gap in variances or reconstruction errors of different groups, but a significant gap in losses. An example is the labeled faces in the wild data set (LFW) [40] where we check both reconstruction errors and losses of male and female groups. As shown in Figure 5, the gap between male and female reconstruction errors is about 10%, while the marginal loss of female is about 5 to 10 times of the male group. This suggests that the difference in marginal losses is a primary source of bias, and therefore marginal losses rather than reconstruction errors should be equalized.

4 Iterative rounding framework with applications to Fair-PCA

In this section, we give an iterative rounding algorithm and prove Theorem 1.9. The algorithm is specified in Algorithm 1. The algorithm maintains three subspaces of that are mutually orthogonal. Let denote matrices whose columns form an orthonormal basis of these subspaces. We will also abuse notation and denote these matrices by sets of vectors in their columns. We let the rank of and be and , respectively. We will ensure that , i.e., vectors in and span .

We initialize and . Over iterations, we increase the subspaces spanned by columns of and and decrease while maintaining pairwise orthogonality. The vectors in columns of will be eigenvectors of our final solution with eigenvalue . In each iteration, we project the constraint matrices orthogonal to and . We will then formulate a residual SDP using columns of as a basis and thus the new constructed matrices will have size . To readers familiar with the iterative rounding framework in linear programming, this generalizes the method of fixing certain variables to or and then formulating the residual problem. We also maintain a subset of constraints indexed by where is initialized to .

In each iteration, we formulate the following with variables which will be a symmetric matrix. Recall is the number of columns in .

It is easy to see that the semi-definite program remains feasible over all iterations if is declared feasible in the first iteration. Indeed the solution defined at the end of any iteration is a feasible solution to the next iteration. We also need the following standard claim.

Claim 4.1.

Let be a positive semi-definite matrix such that with . Let be a real matrix of the same size as and let denote the largest singular value of . Then

The following result follows from Corollary 2.1 and Claim 4.1. Recall that

where is the ’th largest singular value of . We let denote for the rest of the section.

Lemma 4.2.

Consider any extreme point solution of such that . Let be its eigenvalue decomposition and . Then there exists a constraint such that .

Proof.

Let . From Corollary 2.1, it follows that the number of fractional eigenvalues of is at most . Observe that since . Thus, we have . Moreover, , so from Claim 4.1, we obtain that

where the first inequality follows from Claim 4.1 and the second inequality follows since the sum of top singular values reduces after projection. But then we obtain, by averaging, that there exists such that

as claimed. ∎

Now we complete the proof of Theorem 1.9. Observe that the algorithm always maintains that at the end of each iteration, . Thus at the end of the algorithm, the returned solution has rank at most . Next, consider the solution over the course of the algorithm. Again, it is easy to see that the objective value is non-increasing over the iterations. This follows since defined at the end of an iteration is a feasible solution to the next iteration.

Now we argue a bound on the violation in any constraint . While the constraint remains in the SDP, the solution satisfies

where the inequality again follows since is feasible with the updated constraints.

When constraint is removed, it might be violated by a later solution. At this iteration, . Thus, . In the final solution, this bound can only go up as might only become larger. This completes the proof of the theorem.

We now analyze the runtime of the algorithm which contains at most iterations. First we note that we may avoid computing by deleting a constraint from with smallest instead of checking in step (9) of Algorithm 1. The guarantee still holds by Lemma 4.2. Each iteration requires solving an SDP and eigenvalue decompositions over matrices, computing , and finding with the smallest . These can be done in , , and time. However, the result in Section 2 shows that after solving the first , we have , and hence the total runtime of iterative rounding after solving for an extreme solution of the SDP relaxation) is .

Application to Fair-PCA.

For Fair-PCA, iterative rounding recovers a rank- solution whose variance goes down from the SDP solution by at most . While this is no better than what we get by scaling (Corollary 1.5) for the max variance objective function, when we consider the marginal loss, i.e., the difference between the variance of the common -dimensional solution and the best -dimensional solution for each group, then iterative rounding can be much better. The scaling solution guarantee relies on the max-variance being a concave function, and for the marginal loss, the loss for each group could go up proportional to the largest max variance (largest sum of top singular values over the groups). With iterative rounding applied to the SDP solution, the loss is the sum of only singular values of the average of some subset of data matrices, so it can be better by as much as a factor of .

5 Polynomial time algorithm for fixed number of groups

Functions of quadratic maps.

We briefly summarize the approach of [36]. Let be real-valued quadratic functions in variables. Let be a polynomial of degree over some subring of (e.g., the usual or ) The problem is to find all roots of the polynomial , i.e., the set

First note that the set of solutions above is in general not finite and is some manifold and highly non-convex. The key idea of Grigoriev and Paleshnik (see also Barvinok [8] for a similar idea applied to a special case) is to show that this set of solutions can be partitioned into a relatively small number of connected components such that there is an into map from these components to roots of a univariate polynomial of degree ; this therefore bounds the total number of components. The proof of this mapping is based on an explicit decomposition of space with the property that if a piece of the decomposition has a solution, it must be the solution of a linear system. The number of possible such linear systems is bounded as , and these systems can be enumerated efficiently.

The core idea of the decomposition starts with the following simple observation that relies crucially on the maps being quadratic (and not of higher degree).

Proposition 5.1.

The partial derivatives of any degree polynomial of quadratic forms , where , is linear in for any fixed value of .

To see this, suppose and write

Now the derivatives of are linear in as is quadratic, and so for any fixed values of , the expression is linear in .

The next step is a nontrivial fact about connected components of analytic manifolds that holds in much greater generality. Instead of all points that correspond to zeros of , we look at all “critical" points of defined as the set of points for which the partial derivatives in all but the first coordinate, i.e.,

The theorem says that will intersect every connected component of [35].

Now the above two ideas can be combined as follows. We will cover all connected components of . To do this we consider, for each fixed value of , the possible solutions to the linear system obtained, alongside minimizing . The rank of this system is in general at least after a small perturbation (while [36] uses a deterministic perturbation that takes some care, we could also use a small random perturbation). So the number of possible solutions grows only as exponential in (and not ), and can be effectively enumerated in time . This last step is highly nontrivial, and needs the argument that over the reals, zeros from distinct components need only to be computed up to finite polynomial precision (as rationals) to keep them distinct. Thus, the perturbed version still covers all components of the original version. In this enumeration, we check for true solutions. The method actually works for any level set of , and not just its zeros. With this, we can optimize over as well. We conclude this section by paraphrasing the main theorem from [36].

Theorem 5.2.

[36] Given quadratic maps and a polynomial over some computable subring of of degree at most , there is an algorithm to compute a set of points satisfying that meets each connected component of the set of zeros of using at most operations with all intermediate representations bounded by times the bit sizes of the coefficients of . The minimizer, maximizer or infimum of any polynomial of degree at most over the zeros of can also be computed in the same complexity.

5.1 Proof of Theorem 1.7

We apply Theorem 5.2 and the corresponding algorithm as follows. Our variables will be the entries of an matrix . The quadratic maps will be plus additional maps for and for columns of . The final polynomial is

We will find the maximum of the polynomial over the set of zeros of using the algorithm of Theorem 5.2. Since the total number of variables is and the number of quadratic maps is , we get the claimed complexity of operations and this times the input bit sizes as the bit complexity of the algorithm.

6 Hardness and integrality gap

6.1 NP-Hardness

In this section, we show NP-hardness of Fair-PCA even for , proving Theorem 1.6.

Theorem 6.1.

The Fair-PCA problem:

| (17) | ||||

| (18) | ||||

| (19) | ||||

for arbitrary symmetric real PSD matrices is NP-hard for and .

Proof of Theorem 6.1: We reduce another NP-hard problem MAX-CUT to Fair-PCA with . In MAX-CUT, given a simple graph , we optimize

| (20) |

over all subset of vertices. Here, is the size of the cut in . As common in NP-hard problems, the decision version of MAX-CUT:

| (21) |

for an arbitrary is also NP-hard. We may write MAX-CUT as an integer program as follows:

| (22) |

Here represents whether a vertex is in the set or not:

| (23) |

and it can be easily verified that the objective represents the desired cut function.

We now show that this MAX-CUT integer feasibility problem can be formulated as an instance of Fair-PCA (17)-(19). In particular, it will be formulated as a feasibility version of Fair-PCA by checking if the optimum of Fair-PCA is at least . We choose and for this instance, and we write . The rest of the proof is to show that it is possible to construct constraints in the form (18)-(19) to 1) enforce a discrete condition on to take only two values, behaving similarly as ; and 2) check an objective value of MAX-CUT.

Note that constraint (19) requires but . Hence, we scale the variables in MAX-CUT problem by writing and rearrange terms in (22) to obtain an equivalent formulation of MAX-CUT:

| (24) |

We are now ready to give an explicit construction of to solve MAX-CUT formulation (24). Let . For each , define

where and denote vectors of length with all zeroes except one at the th coordinate, and with all ones, respectively. It is clear that are PSD. Then for each , the constraints and are equivalent to

respectively. Combining these two inequalities with forces both inequalities to be equalities, implying that for all , as we aim.

Next, we set

where is the adjacency matrix of the graph . Since the matrix is diagonally dominant and real symmetric, is PSD. We have that is equivalent to

which, by , is further equivalent to

matching (24).

To summarize, we constructed so that checking whether an objective of Fair-PCA is at least is equivalent to checking whether a graph has a cut of size at least , which is NP-hard.

6.2 Integrality gap

We showed that Fair-PCA for groups can be solved up to optimality in polynomial time using an SDP. For , we used a different, non-convex approach to get a polynomial-time algorithm for any fixed . We show that the SDP relaxation of Fair-PCA has a gap even for and in the following lemma. Here, the constructed matrices ’s are also PSD, as required by for a data matrix in the Fair-PCA formulation. A similar result on tightness of rank violation for larger using real (non-PSD) matrices ’s is stated in Lemma B.1 in Appendix B.

Lemma 6.2.

The Fair-PCA SDP relaxation:

for , , and arbitrary PSD contains a gap, i.e. the optimum value of the SDP relaxation is different from one of exact Fair-PCA problem.

Proof of Lemma 6.2:

Let . It can be checked that are PSD. The optimum of the relaxation is (given by the optimal solution ).

However, an optimal exact Fair-PCA solution is

which gives an optimum (one way to solve for optimum rank-1 solution is by parameterizing for , ).

The idea of the example in Lemma 6.2 is that an optimal solution is close to picking the first axis as a projection, whereas a relaxation solution splits two halves for each of the two axes. Note that the example also shows a gap for marginal loss objective (16). Indeed, the numerical computation shows that optimal marginal loss (which is to be minimized) for the exact problem is 1.298 by and for relaxed problem is 1.060 by . This shows that equal losses for two groups in Theorem 3.1 cannot be extended to more than two groups. The same example also show a gap if the objective is to minimize the maximum reconstruction errors. Gaps for all three objectives remain even after normalizing the data by by numerical computation. The pattern of solutions across three objectives and in both unnormalized and normalized setting remains the same as mentioned: an exact solution is a projection close to the first axis, and the relaxation splits two halves for the two axes, i.e., picking close to .

7 Experiments

7.1 Efficacy of our algorithms to fairness

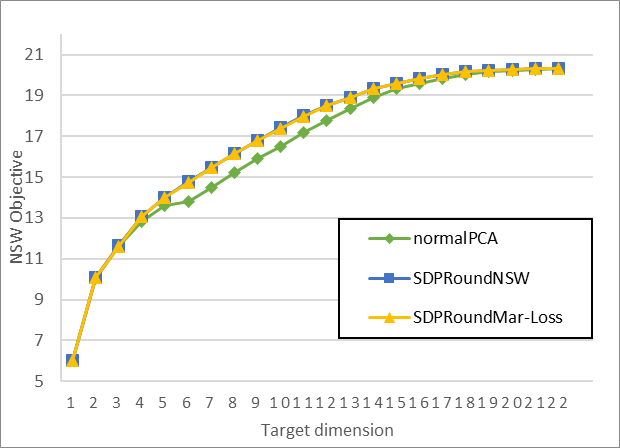

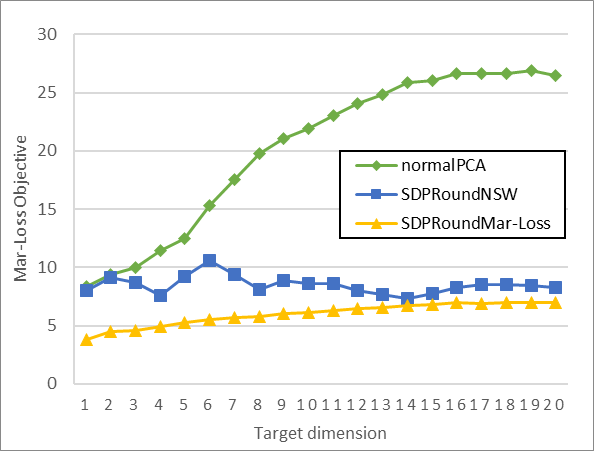

We perform experiments using the algorithm as outlined in Section 2 on the Default Credit data set [83] for different target dimensions , and evaluate the fairness performance based on marginal loss and NSW criteria (see Table 1 in Section 3 on definitions of these criteria). The data consists of 30K data points in 23 dimensions, partitioned into groups by education and gender, and then preprocessed to have mean zero and same variance over features. Our algorithms are set to optimize on either the marginal loss and NSW objective. The code is publicly available at https://github.com/uthaipon/multi-criteria-dimensionality-reduction.

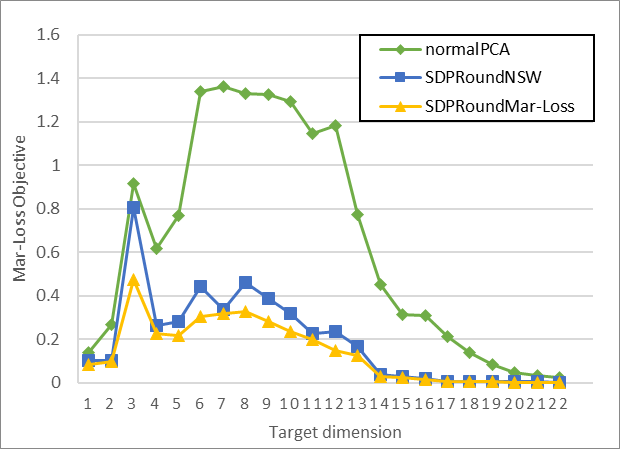

Figure 5 shows the marginal loss by our algorithms compared to standard PCA on the entire data set. Our algorithms significantly reduce disparity of marginal loss of PCA that the standard PCA subtly introduces. We also assess the performance of PCA with NSW objective, summarized in Figure 6. With respect to NSW, standard PCA performs marginally worse (about 10%) compared to our algorithms. It is worth noting from Figures 5 and 6 that our algorithms which try to optimize either marginal loss or NSW also perform well on the other fairness objective, making these PCAs promising candidates for fairness applications.

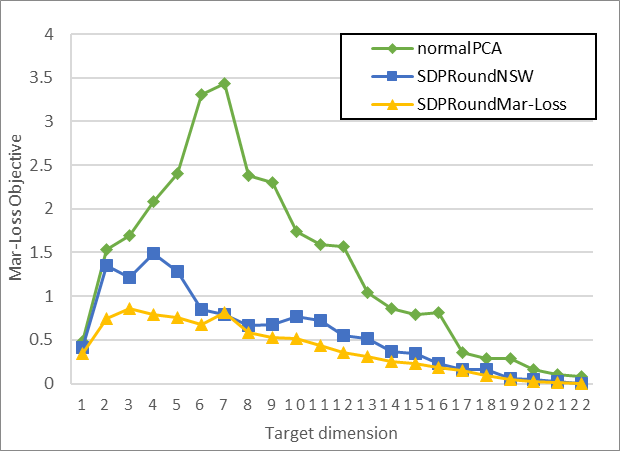

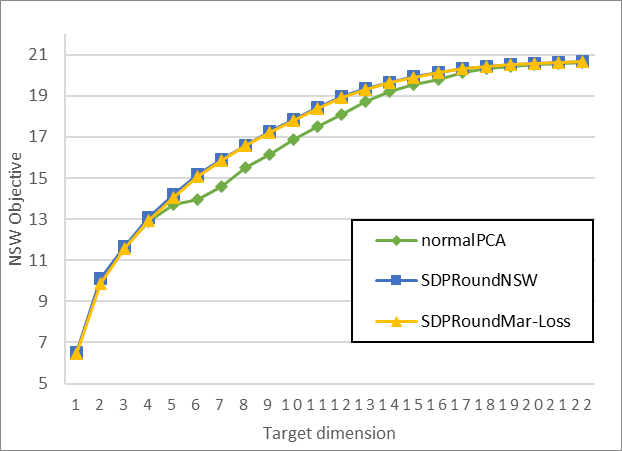

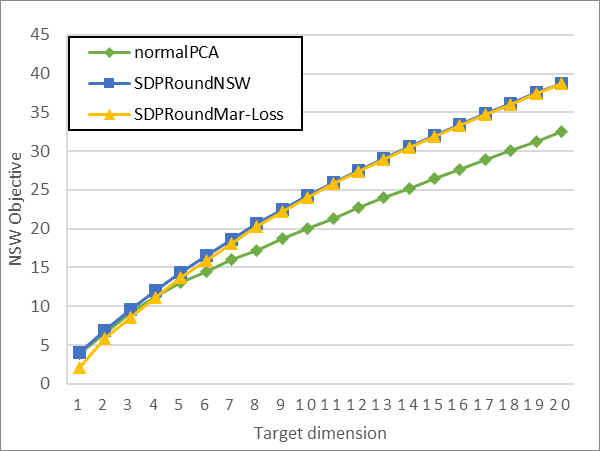

Same experiments are done on the Adult Income data [80]. Some categorial features are preprocessed into integers vectors and some features and rows with missing values are discarded. The final preprocessed data contains data points in dimensions and is partitioned into groups based on race. Figure 7 shows the performance of our SDP-based algorithms compared to standard PCA on marginal loss and NSW objectives. Similar to Credit Data, optimizing for either marginal loss or NSW gives a PCA solution that also performs well in another criterion and performs better than the standard PCA in both objectives.

We note details of the labeled faces in the wild data set (LFW) [40] used in Figures 1 and 4 here. The original data are in 1764 dimensions (4242 images). We preprocess all data to have mean zero and we normalize each pixel value by multiplying . The gender information for LFW was taken from Afifi and Abdelhamed [2], who manually verified the correctness of these labels. To obtain the fair loss in Figure 4, we solve using our SDP-based algorithm which, as our theory suggests, always give an exact optimal solution.

Rank violations in experiments.

In all of the experiments, extreme point solutions from SDPs enjoy lower rank violation than our worst-case guarantee. Indeed, while the guarantee is that the numbers of additional rank are at most for , almost all SDP solutions have exact rank, and in rare cases when the solutions are not exact, the rank violation is only one. As a result, we solve Multi-Criteria-Dimension-Reduction in practice by solving the SDP relaxation targeting dimension . If the solution is exact, then we are done. Else, we target dimension and check if the solution is of rank at most . If not, we continue to target dimension until the solution of the SDP relaxation has rank at most . While our rank violation guarantee cannot be improved in general (due to the integrality gap in Section 6.2; also see Lemma B.1 for tightness of the rank violation bound), this opens a question whether the guarantee is better for instances that arise in practice.

Extreme property of SDP relaxation solutions in real data sets.

One concern for solving an SDP is whether the solver will not return an extreme solution; if so, the SDP-based algorithm requires an additional time to round the solution. We found that a solution from SDP relaxation is, in fact, always already extreme in practice. This is because with probability one over random data sets, SDP is not degenerate, and hence have a unique optimal solution. Since any linear optimization over a compact, convex set must have an extreme optimal solution, this optimal solution is necessarily extreme. Therefore, in practice, it is not necessary to apply the SDP rounding algorithm to the solution of SDP relaxation. As an application, any faster algorithm or heuristics which can solve SDP relaxation to optimality in practice will always obtain a low-rank solution immediately. We discuss some useful heuristics in Section 7.2.

7.2 Runtime improvement

We found that the running time of solving SDP, which depends on , is the bottleneck in all experiments. Each run (for one value of ) of the experiments is fast ( seconds) on Default Credit data (), whereas a run on Adult Income data () takes between 10 and 15 seconds on a personal computer. The runtime is not noticeably impacted by the numbers of data points and groups: larger only increases the data preprocessing time (the matrix multiplication ) to obtain matrices, and larger simply increases the number of constraints. SDP solver and rounding algorithms can handle moderate number of affine constraints efficiently. This observation is as expected from the theoretical analysis.

In this section, we show two heuristics for solving the SDP relaxation that run significantly faster in practice for large data sets: multiplicative weight update (MW) and Frank-Wolfe (FW). We also discuss several findings and suggestions for implementing our algorithms in practice. Both heuristics are publicly available at the same location as SDP-based algorithm experiments.

For the rest of this section, we assume that the utility of each group is for real , and that is a concave function of . When is other linear function in , we can model such different utility function by modifying without changing the concavity of . The SDP relaxation of Multi-Criteria-Dimension-Reduction can then be framed as the following SDP.

| (25) | ||||

| (26) | ||||

| (27) | ||||

| (28) |

7.2.1 Multiplicative Weight Update (MW)

One alternative method to solving (25)-(28) is multiplicative weight (MW) update [6]. Though this algorithm has theoretical guarantee, in practice the learning rate is tuned more aggressively and the algorithm becomes a heuristic without any certificate of optimality. We show the primal-dual derivation of MW which provides the primal-dual gap to certify optimality.

We take the Lagrangian with dual constraints in (26) to obtain that the optimum of the SDP equals to

By strong duality, we may swap and . After rearranging, the optimum of the SDP equals

| (29) |

The inner optimization

| (30) |

in (29) can easily be computed by standard PCA on weighted data projecting from to dimensions. The term (30) is also convex in , as it is a maximum of (infinitely many) linear functions. The term is also known as concave conjugate of , which we will denote by . Concave conjugate is concave, as it is a minimum of linear functions. Hence, (29) is a convex optimization problem.

Solving (29) depends on the form of . For each fairness criteria outlined in this paper, we summarize the form of below.

- Max-Min Variance (Fair-PCA or MM-Var)

-

: the fairness objective gives

- Min-Max Loss (MM-Loss)

-

: the fairness objective (recall (16)) , where is the optimal variance of the group , gives

More generally, the above form of holds for any constants ’s. For example, this calculation also captures min-max reconstruction error: (recall that , , and ).

- Nash Social Welfare (NSW)

-

: the fairness objective gives

For fairness criteria of the "max-min" type, such as MM-Var and MM-Loss, solving the dual problem is an optimization over a simplex with standard PCA as the function evaluation oracle. This can be done using mirror descent [64] with negative entropy potential function . The algorithm is identical to multiplicative weight update (MW) by [6], described in Algorithm 2, and the convergence bounds from mirror descent and [6] are identical. However, with primal-dual formulation, the dual solution obtained in each step of mirror descent can be used to calculate the dual objective in (29), and the optimum in (30) is used to calculate the primal objective, which gives the duality gap. The algorithm runs iteratively until the duality gap is less than a set threshold. We summarize MW in Algorithm 2.

Runtime analysis.

The convergence of MW is stated as follows and can be derived from the convergence of mirror descent [64]. A proof can be found in Appendix A.3.

Theorem 7.1.

Given PSD and , we consider a maximization problem of the function

over . For any , the -th iterate of multiplicative weight update algorithm with uniform initial weight and learning rate where satisfies

| (31) |

where is the optimum of the maximization problem.

Theorem 7.1 implies that MW takes iterations to obtain an additive error bound . For the Multi-Criteria-Dimension-Reduction application, is a scaling of the data input and can be bounded if data are normalized. In particular, suppose and each column of has mean zero and variance at most one, then

MW for two groups.

For MM-Var and MM-Loss objectives in two groups, the simplex is a one-dimensional segment. The dual problem (29) reduces to

| (32) |

The function is a maximum of linear functions in , and hence is convex on . Instead of mirror descent, one can apply ternary search, a technique applicable to maximizing a general convex function in one dimension, to solve (32). However, we claim that binary search, which is faster than ternary search, is also a valid choice.

First, because is convex, we may assume that achieves minimum at and that all subgradients for all and for all . In the binary search algorithm with current iterate , let

be any solution of the optimization (which can be implemented easily by standard PCA). Because a linear function is a lower bound of over and is convex, we have . Therefore, the binary search algorithm can check the sign of for a correct recursion. If , then ; if , then ; and the algorithm recurses in the left half or right half of the current segment accordingly. If , then is an optimum dual solution.

Tuning in practice.

In practice for MM-Var and MM-Loss objectives, we tune the learning rate of mirror descent much higher than in theory. In fact, we find that the last iterate of MW sometimes converges (certified by checking the duality gap), and in such case the convergence is much faster. For NSW, the dual is still a convex optimization, so standard technique such as gradient descent can be used. We found that in practice, however, the unboundedness of the feasible set is a challenge to tune MW for NSW to converge quickly.

7.2.2 Frank-Wolfe (FW)

Observe that while the original optimization (25)-(28), which is in the form

where the utility is a function of , is a nontrivial convex optimization, its linear counterpart

is easily solvable by standard PCA for any given matrix . This motivates Frank-Wolfe (FW) algorithm [32] which requires a linear oracle (solving the same problem but with a linear objective) in each step. The instantiation of FW to Multi-Criteria-Dimension-Reduction is summarized in Algorithm 3.

One additional concern for implementing FW is obtaining gradient . For some objectives such as NSW, this gradient can be calculated analytically and efficiently (some small error may need to be added to stabilize the algorithm from exploding gradient when the variance is close to zero; see -smoothing below). Other objectives, such as MM-Var and MM-Loss, on the other hand, are not differentiable everywhere. Though one may try to still use FW and calculate gradients at the present point (which is differentiable with probability one), there is no theoretical guarantee for the FW convergence when the function is non-differentiable (even when the feasible set is compact as in our SDP relaxation). Indeed, we find that FW does not converge in our experiment settings.

There are modifications of FW which has convergence guarantee for maximizing concave non-differentiable functions. The algorithm by White [82] (also used by Ravi et al. [71]) requires a modified linear oracle, namely a maximization of over in SDP feasible set where is the set of all subgradients at all points in the -neighborhood of . In our setting, if the neighborhood has at least two distinct subgradients, then the oracle reduces to the form at least as hard as the original problem, making the method unhelpful. Another method is by smoothing the function, and the natural choice is by replacing by where is the smoothing parameter. We find that the error from approximating by is significant for even moderate , and any smaller causes substantial numerical errors in computing the exponent. Hence, we do not find FW nor its modification useful in practice for solving MM-Var or MM-Loss objective.

Runtime analysis.

The NSW objective can be ill-conditioned or even undefined when matrices ’s span low dimensions and those dimensions are distinct. This is due to not defined at and having unbounded gradient when is small. To stabilize the objective, we solve the -smoothed NSW objective

| (33) |

Here, is a regularizer, and the regularization term normalizes the effect of each group when their variances are small, regardless of their original sizes . Since is now also Lipschitz, FW has the convergence guarantee as follows, which follows from the standard FW convergence bound [42]. The proof can be found in Appendix A.4.

Theorem 7.2.

Given and PSD as an input to -smooth NSW (33), the -th iterate of Frank-Wolfe with step sizes satisfies

| (34) |

where is the optimum of the optimization problem.

Theorem 7.2 implies that FW takes iterations to get an error bound for solving -smooth NSW.

Tuning in practice.

In practice, we experiment with more aggressive learning rate schedule and line search algorithm. We found that FW converges quickly for NSW objective. However, FW does not converge for MM-Var and MM-Loss for any learning rate schedule, including the standard and line search. This is consistent with, as we mentioned, that FW does not have convergence guarantee for non-differentiable objectives.

7.2.3 Empirical runtime result on a large data set

We perform MW and FW heuristics on a large 1940 Colorado Census data set [5]. The data is preprocessed by one-hot encoding all discrete columns, ignoring columns with N/A, and normalizing the data to have mean zero and variance one on each feature. The preprocessed data set contains 661k data points and 7284 columns. Data are partitioned into 16 groups based on 2 genders and 8 education levels. We solve the SDP relaxation of Multi-Criteria-Dimension-Reduction with MM-Var, MM-Loss, and NSW objectives until achieving the duality gap of no more than 0.1% (in the case of NSW, the product of variances, not the sum of logarithmic of variances, is used to calculate this gap). The runtime results, in seconds, are in shown in Table 2. When increases, the bottleneck of the experiment becomes the standard PCA itself. Since speeding up the standard PCA is not in the scope of this work, we capped the original dimension of data by selecting the first dimensions out of 7284, so that the standard PCA can still be performed in a reasonable amount of time. We note that the rank violation of solutions are almost always zero, and are exactly one when it is not zero, similarly to what we found for Adult Income and Credit data sets [80, 83].

| Original Dimensions | MM-Var (by MW) | MM-Loss (by MW) | NSW (by FW) | Standard PCA (by SVD) |

| 77 | 65 | 11 | 0.22 | |

| 585 | 589 | 69 | 1.5 |

Runtime of MW.

We found that MM-Var and MM-Loss objectives are solved efficiently by MW, whereas MW with gradient descent on the dual of NSW does not converge quickly. It is usual that the solution of the relaxation has rank exactly , and in all those cases we are able to tune learning rates so that the last iterate converges, giving a much faster convergence than the average iterate. For the Census data set, after parameter tuning, MW runs 100-200 iterations on both objectives. MW for both Credit and Income data sets () on 4-6 groups on both objectives finishes in 10-20 iterations whenever the last iterate converges, giving a total runtime of less than few seconds. Each iteration of MW takes 1x-2x of an SVD algorithm. Therefore, the price of fairness in PCA for MW-Var and MM-Loss objectives is 200-400x runtime for large data sets, and 20-40x runtime for medium data sets, as compared to the standard PCA without a fairness constraint.

Runtime of FW.

FW converges quickly for NSW objective, and does not converge on MM-Var or MM-Loss. FW terminates in 10-20 iterations for Census Data. In practice, each iteration of FW has an overhead of 1.5x-3x of an SVD algorithm. We suspect codes can be optimized so that the constant overhead of each iteration is closer to 1x, as the bottleneck in each iteration is one standard PCA. Therefore, the price of fairness in PCA for NSW objective is 15-60x runtime compared to the standard PCA without a fairness constraint.

References

- Adler et al. [2016] Philip Adler, Casey Falk, Sorelle Friedler, Gabriel Rybeck, Carlos Scheidegger, Brandon Smith, and Suresh Venkatasubramanian. Auditing black-box models for indirect influence. In Proceedings of the 16th International Conference on Data Mining, pages 1–10, 2016.

- Afifi and Abdelhamed [2017] Mahmoud Afifi and Abdelrahman Abdelhamed. Afif4: Deep gender classification based on adaboost-based fusion of isolated facial features and foggy faces. arXiv preprint arXiv:1706.04277, 2017.

- Ai et al. [2008] Wenbao Ai, Yongwei Huang, and Shuzhong Zhang. On the low rank solutions for linear matrix inequalities. Mathematics of Operations Research, 33(4):965–975, 2008.

- Angwin et al. [2018] Julia Angwin, Jeff Larson, Surya Mattu, and Lauren Kirchner. Machine bias - propublica. https://www.propublica.org/article/machine-bias-risk-assessments-in-cri%minal-sentencing, 2018.

- [5] The U.S. National Archives and Records Administration. https://1940census.archives.gov/index.asp. Accessed on March 27th, 2020.

- Arora et al. [2012] Sanjeev Arora, Elad Hazan, and Satyen Kale. The multiplicative weights update method: a meta-algorithm and applications. Theory of Computing, 8(1):121–164, 2012.

- Bandeira et al. [2016] Afonso S Bandeira, Nicolas Boumal, and Vladislav Voroninski. On the low-rank approach for semidefinite programs arising in synchronization and community detection. In Conference on learning theory, pages 361–382, 2016.

- Barvinok [1993] Alexander I Barvinok. Feasibility testing for systems of real quadratic equations. Discrete & Computational Geometry, 10(1):1–13, 1993.

- Barvinok [1995] Alexander I. Barvinok. Problems of distance geometry and convex properties of quadratic maps. Discrete & Computational Geometry, 13(2):189–202, 1995.

- Ben-Tal and Nemirovski [2001] Ahron Ben-Tal and Arkadi Nemirovski. Lectures on modern convex optimization: analysis, algorithms, and engineering applications, volume 2. Siam, 2001.

- Beutel et al. [2017] Alex Beutel, Jilin Chen, Zhe Zhao, and Ed Huai-hsin Chi. Data decisions and theoretical implications when adversarially learning fair representations. CoRR, abs/1707.00075, 2017.

- Bhangale et al. [2015] Amey Bhangale, Swastik Kopparty, and Sushant Sachdeva. Simultaneous approximation of constraint satisfaction problems. In International Colloquium on Automata, Languages, and Programming, pages 193–205. Springer, 2015.

- Bhangale et al. [2018] Amey Bhangale, Subhash Khot, Swastik Kopparty, Sushant Sachdeva, and Devanathan Thimvenkatachari. Near-optimal approximation algorithm for simultaneous max-cut. In Proceedings of the Twenty-Ninth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1407–1425. Society for Industrial and Applied Mathematics, 2018.

- Bohnenblust [1948] F Bohnenblust. Joint positiveness of matrices. Unpublished manuscript, 48, 1948.

- Bolukbasi et al. [2016] Tolga Bolukbasi, Kai-Wei Chang, James Y Zou, Venkatesh Saligrama, and Adam T Kalai. Man is to computer programmer as woman is to homemaker? debiasing word embeddings. In Advances in neural information processing systems, pages 4349–4357, 2016.

- Boumal et al. [2016] Nicolas Boumal, Vlad Voroninski, and Afonso Bandeira. The non-convex burer-monteiro approach works on smooth semidefinite programs. In Advances in Neural Information Processing Systems, pages 2757–2765, 2016.

- Buolamwini and Gebru [2018] Joy Buolamwini and Timnit Gebru. Gender shades: Intersectional accuracy disparities in commercial gender classification. In Conference on Fairness, Accountability and Transparency, pages 77–91, 2018.

- Burer and Monteiro [2003] Samuel Burer and Renato DC Monteiro. A nonlinear programming algorithm for solving semidefinite programs via low-rank factorization. Mathematical Programming, 95(2):329–357, 2003.

- Burer and Monteiro [2005] Samuel Burer and Renato DC Monteiro. Local minima and convergence in low-rank semidefinite programming. Mathematical Programming, 103(3):427–444, 2005.

- Calders and Verwer [2010] Toon Calders and Sicco Verwer. Three naive Bayes approaches for discrimination-free classification. Data Mining and Knowledge Discovery, 21(2):277–292, 2010.

- Calmon et al. [2017] Flavio Calmon, Dennis Wei, Bhanukiran Vinzamuri, Karthikeyan Natesan Ramamurthy, and Kush R Varshney. Optimized pre-processing for discrimination prevention. In Advances in Neural Information Processing Systems, pages 3992–4001, 2017.

- Celis et al. [2018] L Elisa Celis, Vijay Keswani, Damian Straszak, Amit Deshpande, Tarun Kathuria, and Nisheeth K Vishnoi. Fair and diverse dpp-based data summarization. arXiv preprint arXiv:1802.04023, 2018.

- Chierichetti et al. [2017] Flavio Chierichetti, Ravi Kumar, Silvio Lattanzi, and Sergei Vassilvitskii. Fair clustering through fairlets. In Advances in Neural Information Processing Systems, pages 5029–5037, 2017.

- Chouldechova [2017] Alexandra Chouldechova. Fair prediction with disparate impact: A study of bias in recidivism prediction instruments. Big data, 5(2):153–163, 2017.

- Crawford [2017] Kate Crawford. The trouble with bias, 2017. URL http://blog.revolutionanalytics.com/2017/12/the-trouble-with-bias-by-ka%te-crawford.html. Invited Talk by Kate Crawford at NIPS 2017, Long Beach, CA.

- Deb [2014] Kalyanmoy Deb. Multi-objective optimization. In Search methodologies, pages 403–449. Springer, 2014.

- Dwork et al. [2012] Cynthia Dwork, Moritz Hardt, Toniann Pitassi, Omer Reingold, and Richard Zemel. Fairness through awareness. In Proceedings of the 3rd innovations in theoretical computer science conference, pages 214–226. ACM, 2012.

- Ensign et al. [2017] Danielle Ensign, Sorelle A. Friedler, Scott Neville, Carlos Eduardo Scheidegger, and Suresh Venkatasubramanian. Runaway feedback loops in predictive policing. Workshop on Fairness, Accountability, and Transparency in Machine Learning, 2017.

- Fang and Bensaou [2004] Zuyuan Fang and Brahim Bensaou. Fair bandwidth sharing algorithms based on game theory frameworks for wireless ad hoc networks. In IEEE infocom, volume 2, pages 1284–1295. Citeseer, 2004.

- Feldman et al. [2015] Michael Feldman, Sorelle Friedler, John Moeller, Carlos Scheidegger, and Suresh Venkatasubramanian. Certifying and removing disparate impact. In Proceedings of the 21th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 259–268, 2015.

- Fish et al. [2016] Benjamin Fish, Jeremy Kun, and Ádám Dániel Lelkes. A confidence-based approach for balancing fairness and accuracy. In Proceedings of the 16th SIAM International Conference on Data Mining, pages 144–152, 2016.

- Frank and Wolfe [1956] Marguerite Frank and Philip Wolfe. An algorithm for quadratic programming. Naval research logistics quarterly, 3(1-2):95–110, 1956.

- Gebru et al. [2018] Timnit Gebru, Jamie Morgenstern, Briana Vecchione, Jennifer Wortman Vaughan, Hanna Wallach, Hal Daumeé III, and Kate Crawford. Datasheets for datasets. arXiv preprint arXiv:1803.09010, 2018.

- Grandoni et al. [2014] Fabrizio Grandoni, R Ravi, Mohit Singh, and Rico Zenklusen. New approaches to multi-objective optimization. Mathematical Programming, 146(1-2):525–554, 2014.