Global jump filters and quasi-likelihood analysis for volatility 111 This work was in part supported by CREST JPMJCR14D7 Japan Science and Technology Agency; Japan Society for the Promotion of Science Grants-in-Aid for Scientific Research No. 17H01702 (Scientific Research) and by a Cooperative Research Program of the Institute of Statistical Mathematics.

Revised version: September 17, 2020

Revised version 2: February 14, 2021 333The theoretical part has been extended by relaxing Condition . )

Summary.

We propose a new estimation scheme for

estimation of the

volatility parameters of a semimartingale with jumps based on a

jump-detection filter.

Our filter uses all of data to analyze the relative size of increments and to discriminate jumps more precisely.

We construct quasi-maximum likelihood estimators and quasi-Bayesian estimators,

and show limit theorems for them including

-estimates of the error

and asymptotic mixed normality based on the framework of the quasi-likelihood analysis.

The global jump filters do not need a restrictive condition for the distribution of

the small jumps.

By numerical simulation we show that our “global” method obtains better estimates of the volatility parameter than the previous “local” methods.

Keywords and phrases.

Volatility, jump, global filter,

high frequency data, quasi-likelihood analysis,

quasi-maximum likelihood estimator,

quasi-Bayesian estimator, semimartingale,

stochastic differential equation,

order statistic, asymptotic mixed normality,

polynomial type large deviation, moment,

stable convergence.

1 Introduction

We consider an -dimensional semimartingale admitting a decomposition

| (1.1) |

on a stochastic basis with a filtration . Here is an -dimensional càdlàg adapted process, is a -dimensional càdlàg adapted process, is an -dimensional standard -Wiener process, is a parameter in the closure of an open set in , and is a continuous function. is the jump part of , i.e., , where and . We assume and a.s. Model (1.1) is a stochastic regression model, but for example, it can express a diffusion type process with jumps contaminated by exogenous jump noise :

with , and as a special case, a jump-diffusion process. We want to estimate the true value of based on the data , where . Asymptotic properties of estimators will be discussed when . That is, the observations are high frequency data. The data of the processes and are not available since they are not directly observed.

Today a substantial amount of literature is available on parametric estimation of the diffusion parameter of diffusion type processes with/without jumps. In the ergodic diffusion case of and , the drift coefficient is parameterized as well as the diffusion coefficient. Certain asymptotic properties of estimators are found in Prakasa Rao [9, 8]. The joint asymptotic normality of estimators was given in Yoshida [15] and later generalized in Kessler [5]. The quasi-likelihood analysis (QLA, Yoshida [16]) ensures not only limit theorems but also moment convergence of the QLA estimators, i.e., the quasi-maximum likelihood estimator (QMLE) and the quasi-Bayesian estimator (QBE). The adaptive estimators (Uchida and Yoshida [12, 14]) and the hybrid multi-step estimators (Kamatani and Uchida [4]) are of practical importance from computational aspects. Statistics becomes non-ergodic under a finite time horizon . Dohnal [1] discussed estimation of the diffusion parameter based on high frequency data. Stable convergence of the quasi-maximum likelihood estimator was given by Genon-Catalot and Jacod [2]. Uchida and Yoshida [13] showed stable convergence of the quasi-Bayesian estimator and moment convergence of the QLA estimators. The methods of the QLA were essential there and will be applied in this article. The non-synchronous case is addressed by Ogihara and Yoshida [7] within QLA. As for inference for jump-diffusion processes, under ergodicity, Ogihara and Yoshida [6] showed asymptotic normality of the QLA estimators and moment convergence of their error. They used a type of optimal jump-filtered quasi-likelihood function in Shimizu and Yoshida [11].

The filter in the quasi-likelihood functions of Shimizu and Yoshida [11] is based on the magnitude of the absolute value of the increment: , where , and . If an increment is sufficiently large relative to the threshold, then it is classified as a jump. If, on the other hand, the size of the increment is “moderate”, it is regarded as coming from the continuous part. Then the parameters in the continuous and jump parts can optimally be estimated by respective data sets obtained by classification of increments. This threshold is natural and in fact, historically, the idea goes back to studies of limit theorems for semimartingales, even further back to Lévy processes.

However, this jump detection filter has a caveat. Though the efficiency of the estimators has been established theoretically, it is known that their real performance strongly depends on a choice of tuning parameters; see, e.g., Shimizu [10], Iacus and Yoshida [3]. The filter is each time based on only one increment of the data. In this sense, this filter can be regarded as a local method. This localism would cause misclassification of increments in practice, even though it should not occur mathematically by the large deviation principle in the limit, and estimated values’ instability and strong dependency on the tuning parameters. To overcome these problems, we introduce a global filtering method, which we call the -threshold method. It uses all of the data to more accurately detect increments having jumps, based on the order statistics associated with all increments. Another advantage of the global filter is that it does not need any restrictive condition on the distribution of small jumps. This paper provides efficient parametric estimators for the model (1.1) under a finite time horizon by using the -threshold method, while applications of this method to the realized volatility and other related problems are straightforward. Additionally, it should be remarked that though the -threshold method involves the tuning parameter to determine a selection rule for increments, it is robust against the choice of as we will see later.

The organization of this paper is as follows. In Section 2.2, we introduce the -quasi-log likelihood function , that is a truncated version of the quasi-log likelihood function made from local Gaussian approximation, based on the global filter for the tuning parameter . The -quasi-maximum likelihood estimator (-QMLE) is defined with respect to . Since the truncation is formulated by the order statistics of the increments, this filter destroys adaptivity and martingale structure. However, the global filtering lemmas in Section 2.4 enable us to recover these properties. Section 2.5 gives a rate of convergence of the -QMLE in sense. In order to prove it, with the help of the QLA theory (Yoshida [16]), the so-called polynomial type large deviation inequality is derived in Theorem 2.13 for an annealed version of the quasi-log likelihood of (2.11), where is the annealing index. Moreover, the -quasi-Bayesian estimator (-QBE) can be defined as the Bayesian estimator with respect to as (2.12). Then the polynomial type large deviation inequality makes it possible to prove -boundedness of the error of the -QBE (Proposition 2.15). The -QMLE and -QBE do not attain the optimal rate of convergence when the parameter is fixed though the fixed -method surely removes jumps as a matter of fact. In Section 3, we introduce a quasi-likelihood function depending on a moving level . The random field is more aggressive than with a fixed . Then a polynomial type large deviation inequality is obtained in Theorem 3.3 but the scaling factor is in this case so that we can prove -consistency in sense for both QMLE and QBE associated with the random field (Proposition 3.4). Stable convergence of these estimators and moment convergence are validated by Theorem 3.13. The moving threshold method attains the optimal rate of convergence in contrast to the fixed- method. However, the theory requires the sequence should keep a certain balance: too large causes deficiency and too small may fail to filter out jumps. To balance efficiency of estimation and precision in filtering by taking advantage of the stability of the fixed- scheme, in Section 4, we construct a one-step estimator for a fixed and the aggressive with the -QMLE as the initial estimator. Similarly, the one-step estimator is constructed for fixed and with the -quasi-Bayesian estimator for the initial estimator. By combining the results in Sections 2 and 3, we show that these estimators enjoy the same stable convergence and moment convergence as QMLE and QBE . It turns out in Section 6 that the so-constructed estimators are accurate and quite stable against , in practice. In Section 5, we relax the conditions for stable convergence by a localization argument. Section 6 presents some simulation results and shows that the global filter can detect jumps more precisely than the local threshold methods.

2 Global filter: -threshold method

2.1 Model structure

We will work with the model (1.1). To structure the model suitably, we begin with an example.

Example 2.1.

Consider a two-dimensional stochastic differential equation partly having jumps:

We can set , and . No jump filter is necessary for the component .

This example suggests that different treatments should be given component-wise. We assume that

for some nonnegative symmetric matrices , , and we further assume that with . Let . Then has the form of

for matrices , . According to the blocks of , we write

Let . We will pose a condition that a.s. The jump part of is defined by .

2.2 Quasi likelihood function by order statistics

In this section, we will give a filter that removes . [11] and [6] used certain jump detecting filters that cut large increments by a threshold comparable to diffusion increments. It is a local filter because the classification is done for each increment without using other increments. Contrarily, in this paper, we propose a global filter that removes increments when is in an upper class among all data .

We prepare statistics (; ; ) such that each is an initial estimator of up to a scaling constant, that is, there exists a (possibly unknown) positive constant such that every is approximated by , as precisely stated later. We do not assume that is -measurable.

Example 2.2.

Let be a positive integer. Let be a diverging sequence of positive integers, e.g., . Let

Here reads when or . An example of is

| (2.2) |

suppose that for some positive constant , where is the minimum eigenvalue of the matrix.

Let . Our global jump filter is constructed as follows. Denote by the set of such that

for and . If , then , that is, there is no filter for the -th component. The density function of the multi-dimensional normal distribution with mean vector and covariance matrix is denoted by . Let

equivalently,

for a random variable , the chi-squared distribution with degrees of freedom, where is determined by

Let . Now the -quasi-log likelihood function is defined by

where

| (2.3) |

and are arbitrarily given positive constants. For a tensor , we write

for , …, . We denote ( times). Brackets stand for a multilinear mapping. This notation also applies to tensor-valued tensors.

If , then , , and , so the -th component of essentially becomes the ordinary quasi-log likelihood function by local Gaussian approximation.

Remark 2.3.

(i) The cap can be removed if a suitable condition is assumed for the big jump sizes of , e.g., . It is also reasonable to use

if is uniformly -bounded. In any case, the factor only serves for removing the effects of too big jumps and the classification is practically never affected by it since the global filter puts a threshold of the order less than . As a matter of fact, the threshold of is of order , that is far looser than the ordinary local filters, and the truncation is exercised only with exponentially small probability. On the other hand, the global filter puts no restrictive condition on the distribution of the size of small jumps, like vanishing at the origin or boundedness of the density of the jump sizes, as assumed for the local filters so far. It should be emphasized that the difficulties in jump filtering are focused on the treatments of small jumps that look like the Brownian increments. (ii) The symmetry of is not restrictive because . On the other hand, we could introduce an random matrix approximating up to scaling, and use for , in order to remove the assumption of symmetry.

The -quasi-maximum likelihood estimator of (-QMLE) is any measurable mapping characterized by

We will identify an estimator of , that is a measurable mapping of the data, with the pull-back of it to since the aim of discussion here is to obtain asymptotic properties of the estimators’ distribution.

2.3 Assumptions

We assume Sobolev’s embedding inequality

for a bounded open set in , where is a constant, . This inequality is valid, e.g., if has a Lipschitz boundary. Denote by the set of continuous functions that have continuous derivatives for all such that and , and each of these derivatives satisfies

for some positive constant . Let for a vector-valued random variable and . Let and We shall consider the following conditions. Let for .

- [F1

-

]κ (i) For every , and there exists a constant such that

- (ii)

-

for every .

- (iii)

-

, is invertible a.s. for every , and

for every . - (iv)

-

and .

Let be a sequence of positive integers satisfying as . For , let . Let . Define the index set by

- [F2

-

] (i) are symmetric, invertible and for every and .

- (ii)

-

There exist positive constants and () such that

for every and .

Remark 2.4.

In (ii), we assumed that there exists a positive constant such that every is approximated by . In estimation of , we only assume positivity of but the values of them can be unknown since the function does not involve . When is a scalar matrix, Condition is satisfied simply by .

2.4 Global filtering lemmas

The -quasi-log likelihood function involves the summation regarding the index set . The global jump filter avoids taking jumps but it completely destroys the martingale structure that the ordinary quasi-log likelihood function originally possessed, and without the martingale structure, we cannot follow a standard way to validate desirable asymptotic properties the estimator should have. However, it is possible to recover the martingale structure to some extent by deforming the global jump filter to a suitable deterministic filter. In this section, we will give several lemmas that enable such a deformation.

As before, is a fixed vector in . We may assume that in . Let

By and , we have

for every , where

Remark that for a positive-definite matrix .

Denote and by and , respectively. denotes the -th ordered statistic of , and denotes the -th ordered statistic of . The rank of is denoted by . Denote by the -quantile of the distribution of . The number depends on .

Let . Let , where . Define the event by

Lemma 2.6.

Suppose that . Then as for every .

Proof.

We have

for every , where is a sequence of numbers such that (the existence of such can be proved by the mean value theorem). The last equality in the above estimates is obtained by the following argument. For and , by the Burkholder-Davis-Gundy inequality, Jensen’s inequality and , we obtain

for every .

Let

We can estimate , and so we have

| (2.4) |

for every .

By definition, on the event , the number of data on the interval is not less than . However,

| (2.5) | |||||

for every . Indeed, the family

is bounded in (this can be proved by the same argument as above). Since the estimate (2.5) is independent of , combining it with (2.4), we obtain

as for every . Now the desired inequality of the lemma is obvious. ∎

Let

where

Let

Lemma 2.7.

| (2.6) |

on . In particular

| (2.7) |

on , where is a positive constant. Here denotes the symmetric difference operator of sets.

Proof.

On , if a pair satisfies and , then . Therefore, if , then since one can find at least variables among that are larger than . Therefore (2.6) holds, and so does (2.7) as follows. From (2.6), we have for

Suppose that . In Case , since , we know the number of such is less than or equal to . In Case , as seen above, on for all satisfying , since and . The number of such s is at least . On the other hand, gives . Therefore

on . We obtain (2.7) on with if we use the inequality . ∎

Let . For random variables , let

Lemma 2.8.

(i) Let . Then

for .

- (ii)

-

Let and . Then

for .

Proof.

The estimate in (i) is obvious from (2.7). (ii) follows from (i). ∎

Let . Let

Lemma 2.9.

Let , where is a positive constant. Then

- (i)

-

For ,

- (ii)

-

For ,

Proof.

(i) follows from

and (ii) follows from (i). ∎

We take a sufficiently large . Then the term involving on the right-hand side of each inequality in Lemma 2.9 can be estimated as the proof of Lemma 2.6. For example, for any .

Lemma 2.10.

Let and let . Suppose that is fulfilled. Then

for every and .

Proof.

Use Sobolev’s inequality and Burkholder’s inequality as well as Lemmas 2.6, 2.8 (ii) and 2.9 (ii). More precisely, we have the following decomposition

We may assume since only remains when and it will be estimated below.

As for , we apply Lemma 2.8 (ii) to obtain

By taking small enough, we can verify that the right-hand side is since

Note that we have used the fact for any . A similar argument with Lemma 2.9 (ii) yields .

As for , applying the Burkholder-Davis-Gundy inequality for the discrete-time martingales as well as Jensen’s inequality, we have

for every and . Hence, by Sobolev’s inequality, we conclude

for every .

Finally, we will estimate . Since , there exists a positive constant such that

where for . Then by (i) and (ii), we obtain

for every . This completes the proof. ∎

By -estimate, we obtain the following lemma.

Lemma 2.11.

Let and let . Suppose that is fulfilled. Then

for every and .

Proof.

Let . Let . Let

Then

| (2.8) | |||||

as thanks to .

Let . Then, by the Burkholder-Davis-Gundy inequality, for any ,

In the last part, we used Taylor’s formula and Hölder’s inequality. Therefore, for any .

Expand with the formula

Then we have

Thus, we can see

for . Consequently,

| (2.9) | |||||

for every and .

2.5 Polynomial type large deviation inequality and the rate of convergence of the -QMLE and the -QBE

We will show convergence of the -QMLE. To this end, we will use a polynomial type large deviation inequality given in Theorem 2.13 below for a random field associated with . Proof of Theorem 2.13 will be given in Section 2.6, based on the QLA theory ([16]) with the aid of the global filtering lemmas in Section 2.4. Though the rate of convergence is less optimal, the global filter has the advantage of eliminating jumps with high precision, and we can use it as a stable initial estimator to obtain an efficient estimator later. We do not assume any restrictive condition of the distribution of small jumps though the previous jump filters required such a condition for optimal estimation.

We introduce a middle resolution (or annealed) random field. A similar method was used in Uchida and Yoshida [12] to relax the so-called balance condition between the number of observations and the discretization step for an ergodic diffusion model. For , let

| (2.11) |

The random field mitigates the sharpness of the contrast . Let

Let

The key index is defined by

Non-degeneracy of plays an essential role in the QLA.

- [F3

-

] For every positive number , there exists a constant such that

Remark 2.12.

An analytic criterion and a geometric criterion are known to insure Condition when is a non-degenerate diffusion process. See Uchida and Yoshida [13] for details. Since the proof of this fact depends on short time asymptotic properties, we can modify it by taking the same approach before the first jump even when has finitely active jumps. Details will be provided elsewhere. On the other hand, those criteria can apply to the jump diffusion without remaking them if we work under localization. See Section 5.

Let . Let . The quasi-likelihood ratio random field of order is defined by

The random field is “annealed” since the contrast function becomes a milder penalty than because .

The following theorem will be proved in Section 2.6.

Theorem 2.13.

Suppose that , and are fulfilled. Let . Then, for every positive number , there exists a constant such that

for all and .

Obviously, an -QMLE of with respect to is a QMLE with respect to . The following rate of convergence is a consequence of Theorem 2.13, as usual in the QLA theory.

Proposition 2.14.

Suppose that , and are satisfied. Then for every and every .

The -quasi-Bayesian estimator (-QBE) of is defined by

| (2.12) |

where is a continuous function on satisfying . Once again Theorem 2.13 ensures -boundedness of the error of the -QBE:

Proposition 2.15.

Suppose that , and are satisfied. Let . Then

for every .

2.6 Proof of Theorem 2.13

We will prove Theorem 2.13 by Theorem 2 of Yoshida [16] with the aid of the global filtering lemmas in Section 2.4. Choose parameters , , , and satisfying the following inequalities:

| (2.14) |

Let

Let

The symmetric matrix is defined by the following formula:

where , and by . We will need several lemmas. We choose positive constants () so that . Then we can choose parameters , , , and so that . Then there is an .

Lemma 2.16.

For every ,

Proof.

We have , where

and

Apply Lemma 2.11 to () to obtain

for every . Moreover, we apply Sobolev’s inequality, Lemma 2.8 (ii) and Lemma 2.9 (ii). Then it is sufficient to show that

| (2.15) |

for proving the lemma, where and are defined by the same formula as and , respectively, but with in place of . However, (2.15) is obvious. ∎

Lemma 2.17.

For every ,

Proof.

Consider the decomposition with

and

Since , we obtain

by Lemma 2.10, and also obtain

by Lemma 2.11 for every . Moreover, by Lemmas 2.8 (ii) and 2.9 (ii) applied to for “”, we replace in the expression of by and then apply the Burkholder-Davis-Gundy inequality to show

for every . This completes the proof. ∎

The following two lemmas are obvious under .

Lemma 2.18.

For every , there exists a constant such that

for all , where denotes the minimum eigenvalue of .

Lemma 2.19.

For every , there exists a constant such that

for all .

Lemma 2.20.

For every ,

Proof.

We consider the decomposition with

and

We see by Lemma 2.11. Moreover by Lemmas 2.8 (ii) and 2.9 (ii) and the Burkholder-Davis-Gundy inequality. We note that symmetry between the components of is available. ∎

As a matter of fact, converges to , as seen in the proof of Lemma 2.20. The location shift of the random field asymptotically vanishes.

Lemma 2.21.

For every ,

Proof.

3 Global filter with moving threshold

3.1 Quasi likelihood function with moving quantiles

Though the threshold method presented in the previous section removes jumps surely, it is conservative and does not attain the optimal rate of convergence that is attained by the QLA estimators (i.e. QMLE and QBE) in the case without jumps. On the other hand, it is possible to give more efficient estimators by aggressively taking bigger increments while it may cause miss-detection of certain portion of jumps.

Let and . For simplicity, let with positive constants . Let and . Let

where

with some positive definite random matrix , and is the -th order statistic of .

We consider a random field by removing increments of including jumps from the full quasi-likelihood function. Define by

| (3.1) | |||||

Remark 3.1.

The truncation functional is given by (2.3). It is also reasonable to set it as

where is an arbitrarily given positive constant.

Remark 3.2.

The threshold is larger than . The truncation is for stabilizing the increments of , not for filtering. The factors , and can freely be chosen if and its inverse are uniformly bounded in and if and are sufficiently close to . , and are natural choices for , and , respectively. Asymptotic theoretically, the factors and can be replaced by , and one can take ; see Condition below. Thus a modification of is defined by

with for . The quasi-log likelihood function gives the same asymptotic results as .

We denote by a QMLE of with respect to given by (3.1). We should remark that defined by can differ from previously defined by . The quasi-Bayesian estimator (QBE) of is defined by

where is a continuous function on satisfying .

3.2 Polynomial type large deviation inequality

Let . Let . We define the quasi-likelihood ratio random field by

- [F2′

-

] (i) The positive-definite measurable random matrices () satisfy

for every .

- (ii)

-

Positive numbers and satisfy and .

A polynomial type large deviation inequality is given by the following theorem, a proof of which is in Section 3.3.

Theorem 3.3.

Suppose that , and are fulfilled. Let . Then, for every positive number , there exists a constant such that

for all and .

The polynomial type large deviation inequality for in Theorem 3.3 ensures -boundedness of the QLA estimators.

Proposition 3.4.

Suppose that , and are satisfied. Then

for every .

3.3 Proof of Theorem 3.3

Recall . Let

Lemma 3.5.

For every ,

| (3.2) |

as .

Proof.

Let

Let

For , there exists such that , and also there exists such that and . Then

and hence

where for a matrix . Since is bounded in , we obtain

as for every . Moreover, from the assumption for since

Thus

| (3.3) |

as for every .

Define by

where the indicator function controls the moment outside of . Then by (3.3), the cap and , we obtain

as for every . Indeed, we can estimate this difference of the two variables on the event and on , as follows. On , whenever . The cap also offers the estimate . On , after removing the factor from the expression of with the help of and the -estimate of , we can estimate the cross term in the difference with

for , as well as the term involving and admitting a similar estimate. Estimation is much simpler on thanks to (3.3). The cap helps.

We know that , and have assumed that and that . Then, with (3.3), it is easy to show

which implies (3.2) as for every . ∎

The following two estimates will play a basic role.

Lemma 3.6.

Let . Then under ,

for every and .

Proof.

One can validate this lemma in a quite similar way as Lemma 2.11. ∎

Lemma 3.7.

Let and . Let . Suppose that is satisfied. Then

Proof.

Let . By taking an approach similar to the proof of Lemma 3.6, we obtain

as . We also have the same estimate for in place of . Then the Sobolev inequality implies the result. ∎

We have the following estimates.

Lemma 3.8.

For every ,

Proof.

Applying Lemma 3.5 and Sobolev’s inequality, one can prove the lemma in a fashion similar to Lemma 2.16. ∎

Lemma 3.9.

For every ,

Proof.

Thanks to Lemma 3.5, it is sufficient to show that

| (3.4) |

where

Now taking a similar way as Lemma 2.17, one can prove the desired inequality by applying Lemmas 3.6 and 3.7 as well as the Burkholder-Davis-Gundy inequality. ∎

Lemma 3.10.

For every ,

Proof.

We have and

for every . Therefore

for every . In this situation, it suffices to show that

| (3.7) |

as for every .

Now, we have the equality

where

Define by

Then, by the same reason as in (3.7), and by Itô’s formula and the Burkholder-Davis-Gundy inequality,

and the last expression is not greater than

for since and by the continuity of the mapping for every . In a similar manner, we obtain

for every and . Finally, for ,

by the Burkholder-Davis-Gundy inequality. Therefore we obtained (3.7) and hence (3.5). ∎

Lemma 3.11.

For every ,

3.4 Limit theorem and convergence of moments

In this section, asymptotic mixed normality of the QMLE and QBE will be established.

- [F1′

-

]κ Conditions , and of are satisfied in addition to

- (i)

-

the process has a representation

where is a càdlàg adapted pure jump process, is an -dimensional -Wiener process, is a -dimensional càdlàg adapted process and is a progressively measurable processes taking values in . Moreover,

for every .

The Wiener process is possibly correlated with .

Recall that denotes the quasi-Bayesian estimator (QBE) of with respect to defined by (3.1). We extend the probability space so that a -dimensional standard Gaussian random vector independent of is defined on the extension . Define a random field on by

where . We write for .

Let for . Equip the space of continuous functions on with the sup-norm. Denote by the -stable convergence.

Lemma 3.12.

Suppose that , and are fulfilled. Then

| (3.8) |

as for every .

Proof.

Fix . Let

and let . We will show

| (3.9) |

for every . Let

Then

It is easy to see

| (3.10) |

For , we have

by the Burkholder-Davis-Gundy inequality and Hölder’s inequality. Therefore

| (3.11) |

since

Indeed, for any , there exists a number such that , where is the modulus of continuity defined by

where is the set of sequences such that and . Then

for , where

Thus we obtain and hence (3.11).

Itô’s formula gives

for . With Itô’s formula, one can show

Obviously

Moreover, for , we have

| (3.12) | |||||

Therefore

| (3.13) |

Similarly to (3.12), we know

and also

| (3.14) |

From (3.10), (3.11), (3.13), (3.14) and symmetry, we obtain (3.9). In particular, (3.9) and (3.6) give the approximation

and so as . Furthermore, Lemma 3.5 ensures

| (3.15) |

as .

Let . Then there exists such that for all and all ,

| (3.16) |

where

with . Combining (3.15), Lemmas 3.9 and 3.8 with the representation (3.16), we conclude the finite-dimensional stable convergence

| (3.17) |

as . Since Lemma 3.8 validates the tightness of , we obtain the functional stable convergence (3.8). ∎

Theorem 3.13.

Suppose that , and are fulfilled. Then

as for , any continuous function of at most polynomial growth, and any -measurable random variable .

Proof.

To prove the result for , we apply Theorem 5 of [16] with the help of Lemma 3.12 and Proposition 3.4. For the case , we obtain the convergence

for any continuous function of at most polynomial growth, by applying Theorem 6 of [16]. For that, we use Lemma 3.12 and Theorem 3.3. Estimate with Lemma 2 of [16] ensures Condition (i) of Theorem 8 of [16], which proves the stable convergence as well as moment convergence. ∎

4 Efficient one-step estimators

In Section 3, the asymptotic optimality was established for the QMLE and the QBE having a moving threshold specified by converging to . However, in practice for fixed , these estimators are essentially the same as the -QMLE and -QBE for a fixed though they gained some freedom of choice of , and in the asymptotic theoretical context.

It was found in Section 2.5 that the -QMLE and the -QBE based on a fixed -threshold are consistent. However they have pros and cons. They are expected to remove jumps completely but they are conservative and the rate of convergence is not optimal. In this section, as the second approach to optimal estimation, we try to recover efficiency by combining these less optimal estimators with the aggressive random field given by (3.1), expecting to keep high precision of jump detection by the fixed filters.

Suppose that satisfies . We assume , , and . According to Proposition 2.14, attains -consistency for any , and then . For , there exists an open ball around . If is invertible, then Taylor’s formula gives

for . The second term on the right-hand side reads when . Here () are written by and (), respectively, and is by and (). Let

| (4.1) |

where

i.e., for . We write in the form

with

Next we write

with

Repeat this procedure up to

with

Let . Thus, the sequence of -valued random functions

are defined on is invertible. For example, when ,

Let

Define by

where is an arbitrary value in .

On the event , the QMLE for satisfies

| (4.3) |

Let

Then the estimate

for every follows from the representation (4.3), Propositions 2.14 and 3.4 and Lemma 2.18. Moreover, Lemmas 2.18, 3.9 and 3.8 together with -boundedness of the estimation errors yield for every .

Now on the event , we have

Therefore it follows from (4) that

for every . Inductively,

Consequently, using boundedness of on , we obtain

and this implies

for every . We note that in the above argument is a working parameter chosen so that .

Next, we will consider a Bayesian estimator as the initial estimator. We are supposing that , and furthermore we suppose satisfies . Remark that this is the parameter involved in the estimator , not a working parameter. Let

Define by

Then we obtain

and

for every .

Write for “” and “”. Thus, we have obtained the following result from Theorem 3.13 for .

Theorem 4.1.

Suppose that , , and are fulfilled. Let be any continuous function of at most polynomial growth, and let be any -measurable random variable in . Suppose that an integer satisfies . Then

-

as .

-

as , suppose that .

5 Localization

In the preceding sections, we established asymptotic properties of the estimators, in particular, -estimates for them. Though it was thanks to , verifying it is not straightforward. An analytic criterion and a geometric criterion are known to insure Condition when is a non-degenerate diffusion process (Uchida and Yoshida [13]). It is possible to give similar criteria even for jump-diffusion processes but we do not pursue this problem here. Instead, it is also possible to relax in order to only obtain stable convergences.

We will work with

- [F3♭

-

] a.s.

in place of .

Let . Then there exists a such that for . Define by

The way of modification of on is not essential in the following argument. Let

for . The random field is defined by

The limit of is now

The corresponding key index is

Then Condition holds for under the conditional probability given , that is,

for every . Now it is not difficult to follow the proof of Propositions 2.14 and 2.15 to obtain

for every and every , under and in addition to . Thus we obtained the following results.

Proposition 5.1.

Suppose that , and are satisfied. Then and as for every .

In a similar way, we can obtain the stable convergence of the estimators with moving , as a counterpart to Theorem 3.13.

Theorem 5.2.

Suppose that , and are fulfilled. Then

as for .

Moreover, a modification of the argument in Section 4 gives the stable convergence of the one-step estimators.

Theorem 5.3.

Suppose that , , and are fulfilled. Suppose that an integer satisfies . Then

-

as .

-

as , suppose that .

Suppose that the process satisfies the stochastic integral equation

with a finitely active jump part with . The first jump time of satisfies a.s. Suppose that is a solution to

and that on for the stopped process of at . This is the case where the stochastic differential equation has a unique strong solution. Furthermore, suppose that the key index defined for is non-degenerate for every in that for every . Then on the event , we have positivity of . This implies Condition . To verify non-degeneracy of , we may apply a criterion in Uchida and Yoshida [13].

6 Simulation Studies

6.1 Setting of simulation

In this section, we numerically investigate the performance of the global threshold estimator. We use the following one-dimensional Ornstein-Uhlenbeck process with jumps

| (6.1) |

starting from . Here is a one-dimensional Brownian motion and is a one-dimensional compound Poisson process defined by

where and is a Poisson process with intensity . The parameters , , and are nuisance parameters, whereas is unknown to be estimated from the discretely observed data .

There are already several parametric estimation methods for stochastic differential equations with jumps. Among them, Shimizu and Yoshida [11] proposed a local threshold method for optimal parametric estimation. They used method of jump detection by comparing each increment with , where is the time interval and . More precisely, an increment satisfying is regarded as being driven by the compound Poisson jump part, and is removed when constructing the likelihood function of the continuous part. The likelihood function of the continuous part is defined by

where . Obviously, the jump detection scheme is essentially different from our approach in this paper. They do not use any other increments to determine whether an increment has a jump or not. Our approach, however, uses all the increments.

Shimizu and Yoshida [11] proved that this estimator is consistent as the sample size tends to infinity; that is, asymptotic property of the local and the global threshold approaches are the same from the viewpoint of consistency. However, precision of jump detection may be different in the case of (large but) finite samples. Comparison of two approaches is the main purpose of this section.

In our setting, however, we assume that the jump size is normally distributed, the case of which is not dealt with in Shimizu and Yoshida [11]. In their original paper, they assume that the jump size must be bounded away from zero. Ogihara and Yoshida [6] accomodated a restrictive assumption on the distribution of jump size. They proved that the local threshold estimator works well under this assumption by using some elaborate arguments. Hence, the local estimator can be used in our setting and thus we can compare its estimates with the global threshold estimator.

Note that, we do not impose too restrictive assumption about the distribution of jump sizes in our paper: we only assume natural moment conditions on the number of jumps. Versatility in this sense can be regarded as the advantage of our approach.

The setting of the simulation is as follows. The initial value is . The true value of the unknown parameter is 0.1. Other parameters are all known and given by , , and . The sample size is in Section 6.2 to see the accuracy of the jump detection of our filter and in Section 6.3 and thereafter to compare the estimates of each estimator. We assume the equidistant case, so that and . Since the time horizon is now finite and is not consistently estimable, we set in at the true value , that is the most preferable value for the estimator in Shimizu and Yoshida [11].

In applying the global estimator, we need to set several tuning parameters. we set for the truncation function in (2.3), that is used for the definition of -quasi-log likelihood function. For the one-step global estimator, we use the parameter and for the truncation function . Moreover, we set so that in the definition of the moving threshold quasi-likelihood function in (3.1).

Figure 1 shows a sample path of . The left panel is the sample path of and the right panel is its jump part . Note that the jump part is not observable and thus we need to discriminate the jump from the sample path of .

(a) Sample path of

(a) Sample path of

(b) Sample path of the jump part of

(b) Sample path of the jump part of

|

6.2 Accuracy of jump detection

Before comparing the results of parameter estimation, we check the accuracy of jump detection of each estimation procedure. If there are too many misjudged increments, the estimated value can have a significant bias. Hence it is important how accurately we can eliminate jumps from the observed data .

6.2.1 Local threshold method

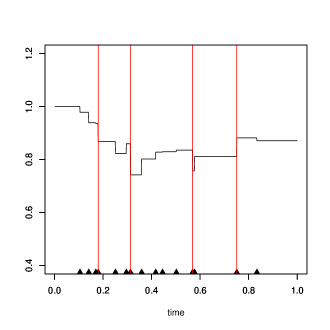

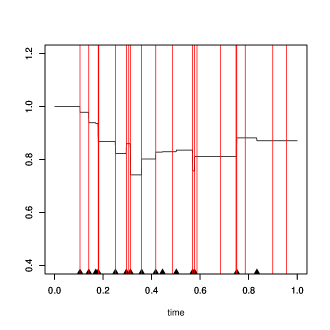

First, we check the accuracy of jump detection of the local threshold method. Figure 2 shows the results of jump detection by the local threshold method of Shimizu and Yoshida [11] for in panel (a) and in panel (b). The red vertical lines indicate the jump detected by each estimator, whereas the triangles on the horizontal axis indicate the true jumps. As these figures show, the accuracy of the jump detection heavily depend on a choice of the tuning parameter . For relatively small (say ), we cannot completely detect jumps: the estimator detects only one jump for . On the other hand, in the case of (theoretically banned) , the estimator detects the jumps better than the case of . Note that the case of is not dealt with in Shimizu and Yoshida [11], but it is useful for us to compare the local threshold method with the global threshold method later and so we show the result of the exceptional case.

(a)

(a)

(b)

(b)

|

6.2.2 Global threshold method

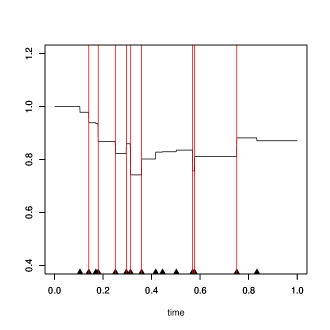

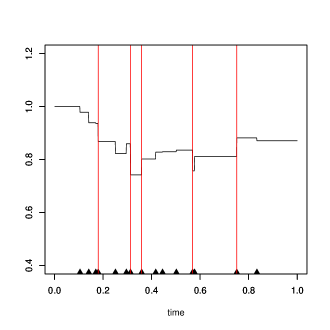

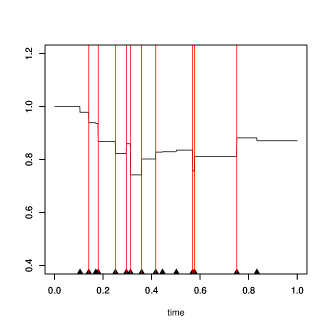

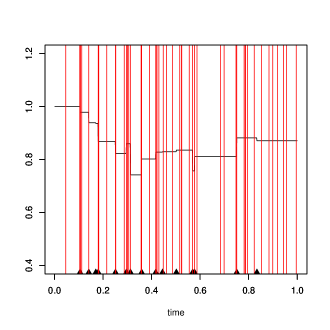

Next, we discuss the jump detection by global threshold method. The accuracy of jump detection depends on the tuning parameter , so we here show results of four cases, namely, the case .

From the figures, we see that the too small cannot detect jumps sufficiently, mistakenly judging some genuine jumps as increments driven by the continuous part, which is similar to the case of small of the Shimizu-Yoshida estimator. By setting a little larger, the accuracy of jump detection increases, as shown in panels (b) and (c). On the other hand, too large discriminate too many increments as jumps, as panel (d) shows. In this case, there are many increments that are regarded as jumps but are actually generated by the continuous part of the process only. These figures suggests that one should choose the tuning parameter carefully to detect jumps appropriately.

(a)

(a)

(b)

(b)

|

(c)

(c)

(d)

(d)

|

We show the false negative / positive ratio of jump detection in Table 1. Note that false negative means that our method did not judge an increment as a jump, despite it was actually driven by the compound Poisson jump part. The meaning of false positive is the opposite; that is, our method judged an increment which was not driven by the jump part as a jump.

The false negative ratio for small tends to be large because in this case the estimator judges only big increments as jumps, and ignores some jumps of intermediate size. On the other hand, the false positive ratio for large is high, since the estimator judges small increments as jumps, but almost increments are actually driven by the continous part. From this table as well, we can infer that there should be some optimal range of for jump detection. In any case, a large value of false negative may seriously bias the estimation, while a large value of false positive only decreases efficiency. Sensitivity of the local filter is also essentially observed by this experiment since each value of of the global filter corresponds to a value of the threshold of the local filter.

| alpha | 0.005 | 0.01 | 0.015 | 0.02 | 0.025 | 0.05 | 0.1 | 0.25 |

|---|---|---|---|---|---|---|---|---|

| False Negative | ||||||||

| False Positive |

6.3 Comparison of the estimators

Next, we investigate the estimation results of the global threshold method. In this section, we set the number of samples to let the biases of the estimators as small as possible. Since the estimator depends on the parameter , we check the stability of the estimator with respect to the parameter . Remember that too small is not able to detect jumps effectively, but too large mistakenly eliminates small increments driven by the Brownian motion which should be used to construct the likelihood function of the continuous part. So there would be a suitable level .

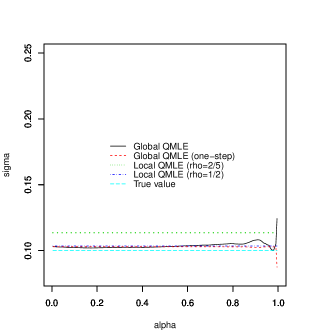

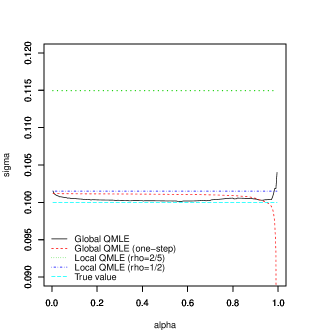

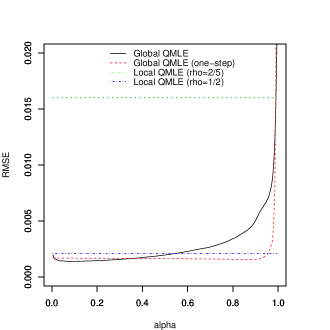

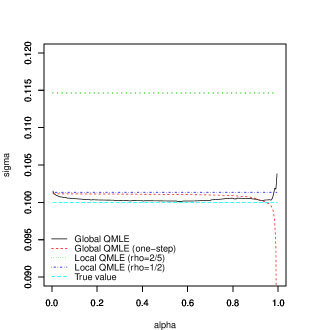

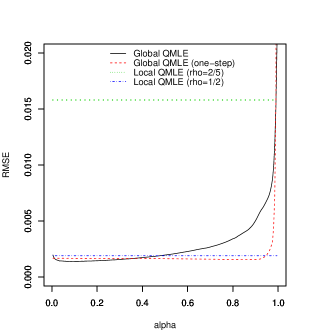

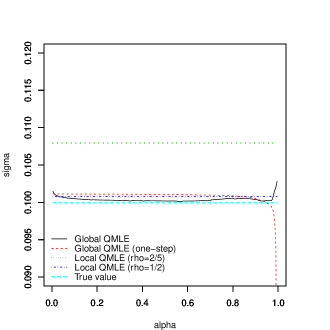

Figure 4 compares the global QMLEs with the local QMLE with , as is theoretically prohibited, and suggests that the global methods are superior to the local methods. Figure 4 also compares the performance of the global threshold estimator and the one-step estimator with ranging in , as well as that of the local filters. Here we used to construct the one-step estimator; that is, the one-step estimator is given by , where the adjustment term is defined in Section 4. As the figure shows, for suitably small , both the estimate and are well close to . However, as this figure indicates, the global threshold estimator may be somewhat unstable with respect to the choice of . Although the global estimator with moving and one-step global estimator are asymptotically equivalent, when we use the original global estimator, it would be recommended to use the one-step estimator as well and to try estimation for several ’s in order to check the stability of the estimates.

To compare statistical properties of the estimators, we used the 100 outcomes of Monte Carlo simulation to calculate the average estimates, the root mean square error (RMSE), and the standard deviation of this experiment. Looking at the average values of the estimators shown in the Figure 5 (a), we see the global threshold estimators outperform the local threshold estimator. It is concluded that the accuracy of the global estimator is not dependent on a sample path. High average accuracy can also be checked by RMSE. As shown in Figure 5 (b), RMSEs of the global estimators are smaller than those of the local estimators, except for the extreme choices of .

(a) Average estimates

(a) Average estimates

(b) RMSE

(b) RMSE

|

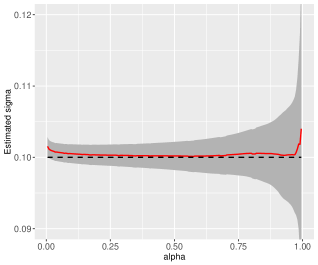

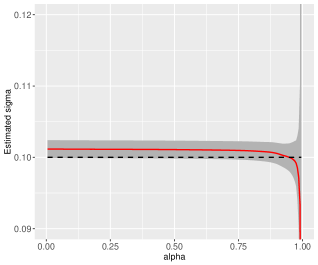

Figure 6 indicates the estimates for global QMLE estimator with standard error band. The standard errors are calculated by using 100 Monte carlo trials. It shows that the global QMLE estimator works very well with or without one-step adjustment. We can see, however, the one-step adjusted estimator is robust against the choice of the tuning parameter . For large , the global threshold tends to eliminate increments that are not driven by the jump part of the underlying process, and this could result in the large standard deviation of the estimate. The one-step estimator works well for such large .

(a) global QMLE

(a) global QMLE

(b) global QMLE (one-step)

(b) global QMLE (one-step)

|

A suitably chosen will yield a good estimate of the unknown parameter, although too small or too large might tends to bias the estimate. The global threshold estimator seems to generally be robust to the choice of the tuning parameters. The optimal choice of depends on the situation. Hence, it is desirable to use several values of and to compare the results to determine the preferable value of in using the global estimator. Moreover, it is worth considering of using one-step adjustment to get more robust estimates.

The global filter sets a number for the critical value of the threshold though it is determined after observing the data. In this sense, the global filter looks similar to the local filter, that has a predetermined number as its threshold. However, the critical values used by the two methods are fairly different in practice. We consider the situation where, for some , the local filter with threshold approximately performs as good as the global filter with . For simplicity, let us consider a one-dimensional case with constantly. Hence the critical value should approximately be near to the upper -quantile of . Moreover, let , and . Then the constant in the threshold of the local filter should satisfy , namely, approximately. Since is a predetermined common constant for different numbers , the critical value of the threshold of the local filter becomes when , while the threshold of the global filter is about . Some of jumps may not be detected by the local filter, since its critical value is not so small, compared with .

6.4 Asymmetric jumps

In the previous subsection, we assumed that the distribution of jump size was centered Gaussian and thus symmetric. In a real situations, however, the distribution of the size of jumps might be not symmetric. For example, stock prices have an asymmetric distribution with heavier tail in negative price changes. In this subsection, we show that our global estimator performs well for jumps with asymmetric distribution.

Although there are many asymmetric jumps in applications, we use just a normal distribution with a negative average because heavier tails would make jump detection easier. More precisely, we assume that the jump process is given by

where and . In this setting, as shown in Figure 7, negative jumps appear more frequently than positive ones.

(a) Sample path of

(a) Sample path of

(b) Sample path of the jump part of

(b) Sample path of the jump part of

|

As Figure 8 shows, the global estimator performs well even in the case of asymmetric jumps. The estimates are well similarly to those in the case of symmetric jumps in the previous subsection. This example implies that out estimator will work very well under realistic circumstances, like financial time series where changes in asset prices have an symmetric distribution with heavy tail in negative price changes.

(a) Average estimates

(a) Average estimates

(b) RMSE

(b) RMSE

|

6.5 Location-dependent diffusion coefficient

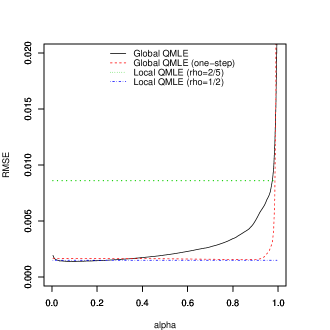

Here we assume that the diffusion coefficient is given by , where is an unknown positive parameter to be estimated. Other settings are entirely the same as those given in the Section 6.1. In particular, we assume that the distribution of jump size is centered, contrary to the previous subsection.

In this example, we have to set an estimator of the volatility matrix, , which satisfies the condition [F2](ii). It is obvious that we can choose to satisfy the condition. The results are shown in Figure 9. Like in the case of constant coefficient, the global estimators perform well. Except for too small or large for which the estimates are unstable and different from those of the case of constant diffusion coefficient, our estimators yield a good estimate even in the case of location-dependent diffusion coefficient.

(a) Average estimates

(a) Average estimates

(b) RMSE

(b) RMSE

|

7 Further topics and future work

In this paper, we payed main attention to removing jumps and to obtaining stable estimation of the diffusion parameter. The removed data consist of relatively large Brownian increments and the increments having jumps. Then it is possible to apply a suitable testing procedure to the removed data, e.g., the goodness-of-fit test for the cut-off normal distribution, in order to test existence of jumps.

It is also possible to consider asymptotics where the intensity of jumps goes to infinity at a moderate rate that does not essentially change the argument of removing jumps. In such a situation, estimation of jumps becomes an issue. Probably, some central limit theorem holds for the error of the estimators of the structure of jumps. Furthermore, a statistical test of the existence of jumps will be possible in this framework. The ergodic case as will be another situation where the parameters of jumps are estimable.

The global filtering methods can apply to the realized volatility to estimate the integrated volatility. The superiority of the global filter to the several existing filtering methods used in this context is numerically observed as well as a mathematical proof. For details, see the forthcoming paper by the authors.

The global jump filter was motivated by data analysis. This scheme is to be implemented on YUIMA, a comprehensive R package for statistical inference and simulation for stochastic processes.

References

- [1] Dohnal, G.: On estimating the diffusion coefficient. J. Appl. Probab. 24(1), 105–114 (1987)

- [2] Genon-Catalot, V., Jacod, J.: On the estimation of the diffusion coefficient for multi-dimensional diffusion processes. Ann. Inst. H. Poincaré Probab. Statist. 29(1), 119–151 (1993)

- [3] Iacus, S.M., Yoshida, N.: Simulation and inference for stochastic processes with YUIMA. Springer (2018)

- [4] Kamatani, K., Uchida, M.: Hybrid multi-step estimators for stochastic differential equations based on sampled data. Statistical Inference for Stochastic Processes 18(2), 177–204 (2014)

- [5] Kessler, M.: Estimation of an ergodic diffusion from discrete observations. Scand. J. Statist. 24(2), 211–229 (1997)

- [6] Ogihara, T., Yoshida, N.: Quasi-likelihood analysis for the stochastic differential equation with jumps. Stat. Inference Stoch. Process. 14(3), 189–229 (2011). DOI 10.1007/s11203-011-9057-z. URL http://dx.doi.org/10.1007/s11203-011-9057-z

- [7] Ogihara, T., Yoshida, N.: Quasi-likelihood analysis for nonsynchronously observed diffusion processes. Stochastic Processes and their Applications 124(9), 2954–3008 (2014)

- [8] Prakasa Rao, B.: Statistical inference from sampled data for stochastic processes. Statistical inference from stochastic processes (Ithaca, NY, 1987) 80, 249–284 (1988)

- [9] Prakasa Rao, B.L.S.: Asymptotic theory for nonlinear least squares estimator for diffusion processes. Math. Operationsforsch. Statist. Ser. Statist. 14(2), 195–209 (1983)

- [10] Shimizu, Y.: A practical inference for discretely observed jump-diffusions from finite samples. J. Japan Statist. Soc. 38(3), 391–413 (2008)

- [11] Shimizu, Y., Yoshida, N.: Estimation of parameters for diffusion processes with jumps from discrete observations. Stat. Inference Stoch. Process. 9(3), 227–277 (2006). DOI 10.1007/s11203-005-8114-x. URL http://dx.doi.org/10.1007/s11203-005-8114-x

- [12] Uchida, M., Yoshida, N.: Adaptive estimation of an ergodic diffusion process based on sampled data. Stochastic Process. Appl. 122(8), 2885–2924 (2012). DOI 10.1016/j.spa.2012.04.001. URL http://dx.doi.org/10.1016/j.spa.2012.04.001

- [13] Uchida, M., Yoshida, N.: Quasi likelihood analysis of volatility and nondegeneracy of statistical random field. Stochastic Processes and their Applications 123(7), 2851–2876 (2013)

- [14] Uchida, M., Yoshida, N.: Adaptive Bayes type estimators of ergodic diffusion processes from discrete observations. Statistical Inference for Stochastic Processes 17(2), 181–219 (2014)

- [15] Yoshida, N.: Estimation for diffusion processes from discrete observation. J. Multivariate Anal. 41(2), 220–242 (1992)

- [16] Yoshida, N.: Polynomial type large deviation inequalities and quasi-likelihood analysis for stochastic differential equations. Ann. Inst. Statist. Math. 63(3), 431–479 (2011). DOI 10.1007/s10463-009-0263-z. URL http://dx.doi.org/10.1007/s10463-009-0263-z