Rejection Sampling for Tempered Lévy Processes

Abstract

We extend the idea of tempering stable Lévy processes to tempering more general classes of Lévy processes. We show that the original process can be decomposed into the sum of the tempered process and an independent point process of large jumps. We then use this to set up a rejection sampling algorithm for sampling from the tempered process. A small scale simulation study is given to help understand the performance of this algorithm.

Keywords: tempered Lévy processes; tempered stable distributions; rejection sampling

MSC2010: 60G51; 60E07

1 Introduction

Tempered stable distributions are a class of models obtained by modifying the tails of stable distributions to make them lighter. This leads to models that are more realistic for a variety of applications, where real-world frictions prevent extremely heavy tails from occurring. Perhaps the earliest models of this type are Tweedie distributions, which were introduced in Tweedie (1984), see also Küchler and Tappe (2013) for a recent review. A more general approach is given in Rosiński (2007). This was further generalized in several directions in Rosiński and Sinclair (2010), Bianchi et al. (2011), and Grabchak (2012). A survey with many references, which discuss a variety of applications, including those to actuarial science, biostatistics, computer science, mathematical finance, and physics can be found in Grabchak (2016). Associated with every tempered stable distribution, is a tempered stable Lévy process, which behaves like a stable Lévy process in a small time frame, but it has fewer large jumps.

The purpose of this paper is two-fold. First, we extend the idea of tempering a stable Lévy process to tempering any Lévy process, and give results about the relationship between the original process and the tempered one. In particular, we show that the original process can be decomposed into the sum of the tempered process and an independent point process of large jumps. Our second purpose is to use this decomposition to set up a rejection sampling algorithm for simulating from the tempered process.

The problem of simulation has not been resolved even for tempered stable distributions. For these, rejection sampling techniques are currently known only for Tweedie distributions. For other tempered stable distributions, the only known exact simulation technique is the inversion method, which is computationally inefficient because it requires numerically calculating the quantile function, which can only be done by numerically inverting the cumulative distribution function (cdf). However, calculating the cdf is, itself, expensive, since, for most tempered stable distributions, it can only be evaluated by numerically applying an inverse Fourier transform to the characteristic function. Other simulation techniques are only approximate, and are based either on truncating a shot-noise representation (Imai and Kawai, 2011), or on approximations by a compound Poisson Process (Baeumer and Kovacs, 2012) or a Brownian motion (Cohen and Rosiński, 2007).

The basic idea of our rejection sampling approach is to start by sampling an increment of the original process. This increment is then rejected if it is too large, otherwise it is accepted. The procedure is in keeping with the motivation for defining tempered processes as having marginal distributions that are similar to those of the original process, but with lighter tails. In deciding if the observation is too large, we require the ability to evaluate the probability density functions of the marginal distributions of both the original and the tempered process. While this may be computationally challenging, in many situations it is more efficient than implementing the inversion method, see the simulation results in Section 7 below.

The rest of the paper is organized as follows. In Section 2, we recall basic facts about infinitely divisible distributions and their associated Lévy processes. In Section 3, we formally introduce tempered Lévy processes and give our main theoretical results. Then, in Section 4, we show how to use these results to set up a rejection sampling algorithm. In Section 5, we recall some basic facts about tempered stable distributions and give conditions under which our results hold. Then, in Section 6, we give detailed conditions for an important subclass of tempered stable distributions, which has additional structure and is commonly used. Finally, in Section 7, we give a small scale simulation study to illustrate how our method works in practice.

Before proceeding, we introduce some notation. Let be the set of natural numbers. Let be the space of -dimensional column vectors of real numbers equipped with the usual inner product and the usual norm . Let denote the unit sphere in . Let and denote the Borel sets in and , respectively. For a Borel measure on and , we write to denote the Borel measure on given by for every . If , we write and to denote, respectively, the maximum and the minimum of and . If is a probability measure on , we write to denote that is an -valued random variable with distribution . Finally, we write to denote the uniform distribution on and to denote the multivariate normal distribution with mean vector and covariance matrix .

2 Infinitely Divisible Distributions and Lévy Processes

Recall that an infinitely divisible distribution on is a probability measure with a characteristic function of the form , where, for ,

Here, is a symmetric nonnegative-definite -dimensional matrix called the Gaussian part, is called the shift, and is a Borel measure, called the Lévy measure, which satisfies

| (1) |

The function , which we call the -function, can be any Borel function satisfying

| (2) |

for all . For a fixed -function, the parameters , , and uniquely determine the distribution , and we write

The choice of does not affect parameters and , but different choices of result in different values for , see Section 8 in Sato (1999).

Associated with every infinitely divisible distribution is a Lévy process, , which is stochastically continuous with independent and stationary increments, and the characteristic function of is . We denote the distribution of by . It follows that, for each , . For more on infinitely divisible distributions and their associated Lévy processes see Sato (1999).

3 Main Results

Let be any infinitely divisible distribution, and define the Borel measure by

where is a Borel function. Throughout, we make the following assumptions:

-

A1.

for all , and

-

A2.

Assumption A1 guarantees that satisfies (1) and (2). Thus is a valid Lévy measure, and we can use the same -function with as with . Let , where

We call the tempering of and we call the tempering function.

Remark 1.

The name “tempering function” comes from the fact that, when the additional assumption holds, the tails of the distribution are lighter than those of . In this sense, the distribution “tempers” the tails of . While this assumption is part of the motivation for defining such distributions, we do not require it in this paper.

Remark 2.

We can always take . In this case and Assumption A2 becomes . However, when we work with other -functions, we need Assumption A2 to be as given.

In light of Assumptions A1 and A2, we can define the finite Borel measure

Now, set

and define the probability measure

Let be independent and identically distributed (iid) random variables with distribution . Independent of these, let be a Poisson process with intensity , and set

| (3) |

This is a compound Poisson process and, by Proposition 3.4 in Cont and Tankov (2004), the characteristic function of is given by

Let and note that, by properties of Poisson processes, has an exponential distribution with rate , i.e.

| (4) |

We now give our main result, which generalizes a result about relativistic stable distributions222Relativistic stable distributions are the distributions of , where and are independent, has a Tweedie distribution, and , where is the identity matrix. given in Ryznar (2002).

Theorem 1.

Let and let be a Borel function satisfying Assumptions A1 and A2. Let , , and be as described above. Let be a Lévy process, independent of , with and set

1. The process is a Lévy process with .

2. If , then .

3. For any and we have

This theorem implies that the process is obtained from by throwing out the jumps that are governed by . We call the tempered Lévy process, and, in this context, we refer to as the original process.

Proof.

We begin with the first part. Since and are independent Lévy processes and the sum of independent Lévy processes is still a Lévy process, it suffices to check that the characteristic function of is the same as the characteristic function of . The characteristic function of can be written as , where for

as required. The second part follows immediately from the fact that when . We now turn to the third part. Since and are independent, for any we can use the second part to get

From here, the result follows by (4). ∎

4 Rejection Sampling

In this section, we set up a rejection sampling scheme for sampling from the tempered Lévy process , when we know how to sample from the original Lévy process . To begin with, assume that, for some we want to simulate . For our approach to work, we need the distributions of both and to be absolutely continuous with respect to Lebesgue measure on . Thus, each distribution must have a probability density function (pdf). This always holds, for instance, if is an invertible matrix or if both

More delicate conditions, in terms of the corresponding Lévy measures, can be found in Section 27 of Sato (1999).

Now assume that Assumptions A1 and A2 hold, and let and be the pdfs of and , respectively. Since the inequality in the third part of Theorem 1 holds for all Borel sets, it holds for pdfs as well. Thus, for Lebesgue almost every ,

where

This means that we can set up a rejection sampling algorithm (see Devroye (1986)) to sample from as follows.

Algorithm 1.

Step 1. Independently simulate and .

Step 2. If accept, otherwise reject and go back to Step 1.

Let be the probability of acceptance on a given iteration and let be the expected number of iterations until the first acceptance. By a simple conditioning argument, it follows that , and hence that . Note that both of these quantities approach as . On the other hand, when , we have and . Thus, this method works best for small .

We now describe how to use Algorithm 1 to simulate the tempered Lévy process on a finite mesh. For simplicity, assume that the mesh points are evenly spaced; the general case can be dealt with in a similar manner. Thus, fix and assume that we want to simulate for some . To do this, we begin by simulating independent increments using Algorithm 1. We expect this to take iterations. Now, to get values of the process, we set

| (5) |

Next, consider the case, when we only want to simulate for some fixed . While this can be done directly using Algorithm 1, when is large, the expected number of iterations, , is large as well. Instead, we can choose some and sample independent increments . Then the sum has distribution . In this case, we only expect to need iterations. This requires fewer iterations so long as . Since the function is minimized (on ) at , it follows that the optimal choice of is near this value. As an example, assume that we want to simulate one observation when and . To do this directly, we expect to need iterations. On the other hand, to simulate observations when and we only expect to need iterations. Thus, the second approach is much more efficient, in this case.

5 Tempered Stable Distributions

Most, if not all, tempered Lévy processes that have appeared in the literature, are those associated with tempered stable distributions. Before discussing these, we recall that an infinite variance stable distribution on is an infinitely divisible distribution with no Gaussian part and a Lévy measure of the form

| (6) |

where and is a finite Borel measure on . For these distributions we will use the -function

| (10) |

We denote the distribution by . For more on stable distributions, see the classic text Samorodnitsky and Taqqu (1994).

Now, following Rosiński and Sinclair (2010), we define a tempered stable distribution on as an infinitely divisible distribution with no Gaussian part and a Lévy measure of the form

where , is a Borel function, and is a finite Borel measure on . Here, the tempering function is . Using the -function given by (10), we denote the distribution by . In this case,

and Assumptions A1 and A2 become:

-

B1.

for all and , and

-

B2.

Note that Assumption B2 implies that, for almost every , we have

| (11) |

Next, we turn to the question of when both and are absolutely continuous with respect to Lebesgue measure on . Before characterizing when this holds, we recall the following definition. The support of is the collection of all points such that, for any open set with , we have .

Proposition 1.

If the support of contains linearly independent vectors, then both and are absolutely continuous with respect to Lebesgue measure on .

In particular, when , this holds so long as .

Proof.

In light of this proposition, we introduce the third assumption:

-

B3.

The support of contains linearly independent vectors.

We now specialize our main results to the case of tempered stable distributions.

Corollary 1.

Let , , where

If Assumptions B1 and B2 hold, then the results of Theorem 1 hold. If, in addition, Assumption B3 holds, then we can use Algorithm 1 to simulate from the Lévy process associated with .

In particular, this means that, when Assumptions B1 and B2 hold, if is a Lévy process with and is a Lévy process with , then for , where is as in Theorem 1. This strengthens the well-known fact that tempered stable Lévy processes behave like stable Lévy processes in a short time frame, see Rosiński and Sinclair (2010). Algorithm 1 requires the ability to sample from a stable distribution. In the one dimensional case, this is easily done using the classical method of Chambers, Mallows, and Stuck (1976). In the multivariate case, this problem has not been fully resolved, however a method for simulating from a dense class of multivariate stable distributions is given in Nolan (1998).

6 -Tempered -Stable Distributions

In the previous section, we allowed for tempered stable distributions with very general tempering functions. However, it is often convenient to work with families of tempering functions, which have additional structure. One such family, which is commonly used, corresponds to the case, where

| (12) |

Here and is a measurable family of probability measures on . For fixed , the corresponding tempered stable distributions are called -tempered -stable. For these were introduced in Rosiński (2007), for they were introduced in Bianchi et al. (2011), and the general case was introduced in Grabchak (2012). See also the recent monograph Grabchak (2016).

Now, consider the distribution , where is as in (12), and define the measures

and

We call the Rosiński measure of the distribution. For fixed and , uniquely determines and . Further, Proposition 3.6 in Grabchak (2016) implies that we can recover by

| (13) |

Due to the importance of the Rosiński measure, we sometimes denote the distribution , where is of the form (12), by . We now characterize when Assumptions B1 and B2 hold.

Proposition 2.

Consider the distribution , where is of the form (12) and let be the corresponding Rosiński measure. This distribution always satisfies Assumption B1. Further, it satisfies Assumption B2 if and only if and is a finite measure on . In this case

Proof.

The fact that Assumption B1 always holds follows from (12) and the fact that is a probability measure for every . We now turn to Assumption B2. First assume that . In this case, the fact that is a collection of probability measures implies that

where the second line follows by substitution and the third by integration by parts. It follows that

which is finite if and only if . Now assume that . We again have

To see that Assumption B2 does not hold in this case, observe that

where we use the fact that, for , , see e.g. 4.2.37 in Abramowitz and Stegun (1972). ∎

Remark 3.

Perhaps, the most famous -tempered -distributions are Tweedie distributions, which were introduced in Tweedie (1984). These are sometimes also called classical tempered stable subordinators. These are one-dimensional distributions with , , , , and , where and is the point-mass at . In this case . It is not difficult to show that such distributions satisfy Assumptions B1, B2, and B3 and thus that Algorithm 1 can be used. Further, in this case, , and it can be shown that . Thus, in this case, Algorithm 1 is computationally easy to perform. In fact, it reduces to the standard rejection sampling algorithm for Tweedie distributions given in e.g. Kawai and Masuda (2011).

7 Simulations

In this section we perform a small scale simulation study to see how well Algorithm 1 works in practice. We focus on a parametric family of tempered stable distributions for which, up to now, there has not been an exact simulation method except for the inversion method. Specifically, we consider the family of -tempered -stable distribution on with Rosiński measures of the form

where is a parameter and

These distributions were introduced in Grabchak (2016) as a class of tempered stable distributions, which can have a finite variance, but still fairly heavy tails. If fact, if random variable has a distribution of this type, then, for ,

Thus, controls how heavy the tails of the distribution are. Distributions with tails of this type are useful, for instance, in modeling financial returns, since, as is well-known, returns tend to have heavy tails, but the fact that they exhibit aggregational Gaussianity suggests that their tails cannot be too heavy and that the variance should be finite, see e.g. Cont and Tankov (2004) or Grabchak and Samorodnitsky (2010).

Since is a finite measure, Proposition 2 implies that, when , Assumptions B1 and B2 hold and

By (13), it follows that we are tempering a symmetric stable distribution with

Let and . When , methods for evaluating the pdfs and related quantities of both of these distribution are available in the SymTS package (Grabchak and Cao, 2017) for the statistical software R. For this reason, we focus on the case . In this case, we are restricted to .

|

|

|

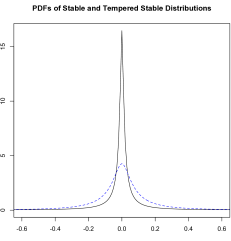

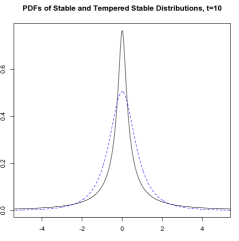

For our simulations, we took , , and . By numerical integration, we got . Let and let , where . Plots of the pdfs of and are given in Figure 1.

To get observations from using Algorithm 1, we expect to need iterations. For simplicity, we ran iterations. Thus, we began by simulating observations from . This was done using the method of Chambers, Mallows, and Stuck (1976). We then applied Algorithm 1 to see which observations should be rejected. Here, we used the SymTS package to evaluate the pdfs. In the end, we wound up with observations from .

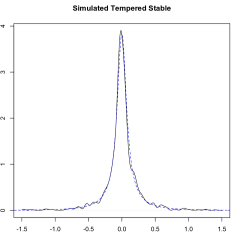

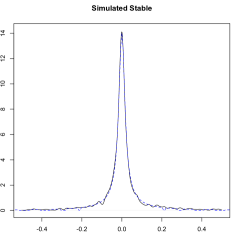

Figure 2 (left) plots the kernel density estimator (KDE) for our samples from . Here, KDE used a Gaussian kernel with a bandwidth of . The plot is overlaid with the pdf of smoothed by the Gaussian Kernel with this bandwidth. This verifies, numerically, that we are simulating from the correct distribution. For comparison, Figure 2 (right), plots the KDE of the original samples from . This is overlaid with the smoothed pdf of . Here, KDE used a Gaussian kernel with a bandwidth of .

|

|

|

|

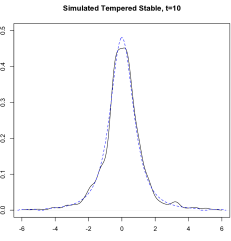

Next, consider the Lévy process , where . To simulate , we apply (5) to the iid increments, which we simulated above. A plot of this Lévy process is given in the left plot of Figure 3. For comparison, the right plot of Figure 3 gives the Lévy process based on the original iid increments from . Comparing the two processes, we see that all of the largest jumps have been rejected.

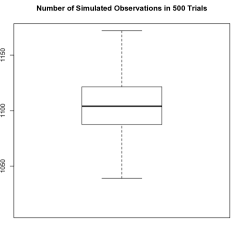

In our simulation, we used observations from to get observations from . Of course, due to the structure of the algorithm, if we run the simulation again, we may get a different number of observations from . We performed the simulation times to see how many observations from are obtained. Figure 4 gives a boxplot and a histogram for all resulting values. The smallest value observed was and the largest was . The mean was with a standard deviation of . Note that the observed mean is very close to the theoretical mean of .

Now, consider the case, where we want to simulate from , which is the distribution of . A plot of this distribution is given in Figure 5 (left). We have two choices. First, we can use Algorithm 1 directly, which requires, on average, iterations to get one observation. Second, we can use Algorithm 1 to simulate independent observations from , and then aggregate these by taking the sum. This requires, on average, iteration to get one observation. Clearly, the second approach is more efficient, and, hence, it is the one that we use.

|

|

Say that we want independent observations from . This requires independent observations from , and we expect to need iterations. We performed iterations, which gave us observations from . These, in turn, gave observations from . In Figure 5 (right), we plot the KDE of the simulated data. This is overlaid with the pdf of smoothed by the appropriate kernel and bandwidth. Here, KDE used the Gaussian kernel with bandwidth .

| Algorithm 1 | Inversion Method | |||||

|---|---|---|---|---|---|---|

| t | run time | iterations | obs | run time | obs | ratio |

| 1 | 24.711 sec | 3000 | 1121 | 285.210 sec | 1000 | 0.087 |

| 2 | 47.399 sec | 6000 | 1105 | 255.879 sec | 1000 | 0.185 |

| 5 | 118.563 sec | 15000 | 1104 | 224.227 sec | 1000 | 0.529 |

| 10 | 237.747 sec | 30000 | 1084 | 193.319 sec | 1000 | 1.230 |

| 20 | 443.286 sec | 56000 | 1024 | 191.004 sec | 1000 | 2.321 |

| Algorithm 1 | Inversion Method | |||||

|---|---|---|---|---|---|---|

| run time | observations | run time | observations | ratio | ||

| .50 | 0.5 | 66.841 sec | 1057 | 785.870 sec | 1000 | 0.085 |

| .50 | 1.0 | 30.531 sec | 1116 | 338.867 sec | 1000 | 0.090 |

| .50 | 5.0 | 47.035 sec | 1090 | 509.506 sec | 1000 | 0.092 |

| .75 | 0.5 | 53.346 sec | 1124 | 668.588 sec | 1000 | 0.080 |

| .75 | 1.0 | 23.844 sec | 1082 | 282.788 sec | 1000 | 0.084 |

| .75 | 5.0 | 37.353 sec | 1093 | 448.820 sec | 1000 | 0.083 |

| .95 | 0.5 | 51.121 sec | 1101 | 601.804 sec | 1000 | 0.084 |

| .95 | 1.0 | 23.444 sec | 1096 | 278.804 sec | 1000 | 0.084 |

| .95 | 5.0 | 38.190 sec | 1100 | 470.784 sec | 1000 | 0.081 |

For a comparison, we also performed simulations using the inversion method, which is implemented in the SymTS package. First, we fixed , , and considered . Computation times for both approaches are reported in Table 1. Not surprisingly, when is small, Algorithm 1 is more efficient, but for large the inversion method works better. Second, we fixed and considered and . Computation times are reported in Table 2. Both sets of simulations were performed on a desktop PC with a 3.40GHz Intel Core i7-6700 CPU. The computer was running Ubuntu 16.04.4 LTS and R version 3.2.3.

For the above simulations, we attempted to cover a large part of the parameter space. However, while the parameter can, in principle, take any value in , we did not consider the case . This is because we found it difficult to numerically evaluate the pdfs with enough accuracy in this case. We conjecture that this difficulty is due to the fact that, for such values of , stable distributions are extremely heavy tailed. On the other hand, there is no difficulty with values near , as is illustrated by the simulations for .

For both Algorithm 1 and the inversion method, the most expensive part of the calculation involves evaluating the required functions. These are and for Algorithm 1 and the quantile function for the inversion method. When we are simulating many observations from the same distribution, both methods can be improved by precomputing these functions on a grid and then using interpolation.

References

- Abramowitz and Stegun (1972) Abramowitz, M., Stegun, I.A.: Handbook of Mathematical Functions 10th ed. Dover Publications, New York (1972).

- Baeumer and Kovacs (2012) Baeumer, B., Kovács, M.: Approximating multivariate tempered stable processes. Journal of Applied Probability 49, 167–183 (2012).

- Bianchi et al. (2011) Bianchi, M.L., Rachev, S.T., Kim, Y.S., Fabozzi, F.J.: Tempered infinitely divisible distributions and processes. Theory of Probability and Its Applications 55, 2–26 (2011).

- Chambers, Mallows, and Stuck (1976) Chambers, J.M., Mallows, C.L., Stuck, B.W.: A method for simulating stable random variables. Journal of the American Statistical Association 71, 340–344 (1976).

- Cohen and Rosiński (2007) Cohen, S., Rosiński, J.: Gaussian approximation of multivariate Lévy processes with applications to simulation of tempered stable processes. Bernoulli 13, 195–210 (2007).

- Cont and Tankov (2004) Cont, R., Tankov, P.: Financial Modeling With Jump Processes. Chapman & Hall, Boca Raton (2004)

- Devroye (1986) Devroye, L.: Non-Uniform Random Variate Generation. Springer, New York (1986)

- Grabchak (2012) Grabchak, M.: On a new class of tempered stable distributions: Moments and regular variation. Journal of Applied Probability 49, 1015–1035 (2012).

- Grabchak (2016) Grabchak, M.: Tempered Stable Distributions: Stochastic Models For Multiscale Processes. Springer, Cham, Switzerland (2012).

- Grabchak and Cao (2017) Grabchak, M., Cao, L: SymTS: Symmetric tempered stable distributions. Ver. 1.0, R Package. https://cran.r-project.org/web/packages/SymTS/index.html (2017).

- Grabchak and Samorodnitsky (2010) Grabchak, M., Samorodnitsky, G.: Do financial returns have finite or infinite variance? A paradox and an explanation. Quantitative Finance 10, 883–893 (2010).

- Imai and Kawai (2011) Imai, J., Kawai, R.: On finite truncation of infinite shot noise series representation of tempered stable laws. Physica A 390, 4411–4425 (2011).

- Kawai and Masuda (2011) Kawai, R., H. Masuda, H.: On simulation of tempered stable random variates. Journal of Computational and Applied Mathematics 235, 2873–2887 (2011).

- Küchler and Tappe (2013) Küchler, U., S. Tappe, S.: Tempered stable distributions and processes. Stochastic Processes and their Applications 123, 4256–4293 (2013).

- Nolan (1998) Nolan, J.P.: Multivariate stable distributions: Approximation, estimation, simulation and identification. In Adler, R.J, Feldman, R.E., Taqqu, M.S. (Eds.), A Practical Guide to Heavy Tails, pp. 509–526. Birkhauser, Boston (1998).

- Rosiński (2007) Rosiński, J.: Tempering stable processes. Stochastic Processes and their Applications 117, 677–707 (2007)

- Rosiński and Sinclair (2010) Rosiński, J., Sinclair, J.L., Generalized tempered stable processes. Banach Center Publications 90, 153–170 (2010).

- Ryznar (2002) Ryznar, M.: Estimates of Green function for relativistic -stable process. Potential Analysis 17, 1-23 (2002).

- Samorodnitsky and Taqqu (1994) Samorodnitsky, G., Taqqu, M.S.: Stable Non-Gaussian Random Processes: Stochastic Models with Infinite Variance. Chapman & Hall, New York (1994).

- Sato (1999) Sato, K.: Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press, Cambridge (1999).

- Tweedie (1984) Tweedie, M.C.K.: An index which distinguishes between some important exponential families. In Ghosh, J.K., Roy, J. (eds.), Statistics: Applications and New Directions. Proceedings of the Indian Statistical Institute Golden Jubilee International Conference. Indian Statistical Institute, Calcutta, pg. 579–604 (1984).