The Correlated Particle Hybrid Sampler for State Space Models.

Abstract

Particle Markov Chain Monte Carlo (PMCMC) is a general computational approach to Bayesian inference for general state space models. Our article scales up PMCMC in terms of the number of observations and parameters by generating the parameters that are highly correlated with the states with the states ‘integrated out’ in a pseudo marginal step; the rest of the parameters are generated conditional on the states. The novel contribution of our article is to make the pseudo-marginal step much more efficient by positively correlating the numerator and denominator in the Metropolis-Hastings acceptance probability. This is done in a novel way by expressing the target density of the PMCMC in terms of the basic uniform or normal random numbers used in the sequential Monte Carlo algorithm, instead of the standard way in terms of state particles. We also show that the new sampler combines and generalizes two separate particle MCMC approaches: particle Gibbs and the correlated pseudo marginal Metropolis-Hastings. We investigate the performance of the hybrid sampler empirically by applying it to univariate and multivariate stochastic volatility models having both a large number of parameters and a large number of latent states and show that it is much more efficient than competing PMCMC methods.

Keywords: Correlated pseudo-marginal Metropolis-Hastings; Factor stochastic volatility model; Particle Gibbs sampler.

1 Introduction

Our article proposes a novel particle Markov chain Monte Carlo (PMCMC) sampler for the general class of state space models defined in section 2. The sampler generates parameters that are highly correlated with the states, or are difficult to generate conditional on the states, using a pseudo marginal step with the states ‘integrated out’, while the rest of the parameters are generated by a particle Gibbs step. Mendes et al., (2020) shows that such an approach allows the sampler to scale up in terms of the number of parameters. Our main contribution is to make the pseudo marginal step much more efficient than in Mendes et al., (2020) as explained below.

In a seminal paper, Andrieu et al., (2010) propose two PMCMC methods for state space models. The first is the particle marginal Metropolis-Hastings (PMMH), where the parameters are generated with the unobserved states ‘integrated out’. The second is particle Gibbs (PG) which generates the parameters conditional on the states. The basic idea of PMCMC methods is to define a target distribution on an augmented space that includes all of the parameters and the particles generated by a sequential Monte Carlo (SMC) algorithm and has the joint posterior density of the parameters and states as a marginal density.

Mendes et al., (2020) propose the particle hybrid sampler (PHS) that combines the two approaches in Andrieu et al., (2010). Parameters that are efficiently generated by conditioning on the states are generated using a PG step(s); all the other parameters are generated by particle marginal Metropolis-Hastings steps. For example, the particle marginal Metropolis-Hastings is suitable for parameters that are highly correlated with the states, or parameters that very expensive to generate efficiently conditional on the states.

Deligiannidis et al., (2018) improve the efficiency of the PMMH sampler by proposing the correlated pseudo-marginal (CPMMH) method, which correlates the random numbers used in constructing the estimated likelihood at the current and proposed values of the parameters. They show that by inducing a high correlation in successive iterations between those random numbers, it is necessary to increase the number of particles in proportion to , where is the number of observations and is the state dimension. The computational complexity of the correlated pseudo-marginal method is , up to a logarithmic factor, compared to for the standard PMMH sampler. This shows that the correlated pseudo-marginal method can scale up with the number of observations more easily than standard pseudo-marginal methods, as long as the state dimension is not too large. A number of other papers, including Yıldırım et al., (2018) and Andrieu et al., (2018), also extend the literature on PMCMC methods.

Our article builds on the correlated pseudo-marginal (CPMMH) method of Deligiannidis et al., (2018) and the particle hybrid sampler (PHS) sampler of Mendes et al., (2020) and proposes a novel PMCMC sampler for state space models, which we call the correlated particle hybrid sampler (CPHS). It improves on both the CPMMH and PHS to allow for further improvements in scaling up particle MCMC in terms of the number of parameters and the length of the series. The CPHS expresses the target density of the PMCMC in terms of the basic uniform or standard normal random numbers used in the sequential Monte Carlo algorithm, rather than the state particles, as done in the rest of the literature. This novel representation allows the estimated likelihoods in the numerator and denominator of the acceptance probability of the MH step of the PMMH to be correlated as in the CPMMH, while still allowing the PMMH and PG steps to be combined in a hybrid form. Section 3 of our article also shows that the PG and CPMMH samplers are special cases of the CPHS sampler. While our CPHS and the PHS of Mendes et al., (2020) similarly combine PG and PMMH sampling, they technically involve quite different constructions of the target density. In particular, it is the use of the basic random numbers in the target density of the CPHS that allows us to correlate the numerator and denominator in the PMMH step.

We illustrate the CPHS empirically using a univariate stochastic volatility model with leverage and a multivariate factor stochastic volatility model with leverage using real and simulated datasets. We use these univariate and multivariate models to compare the performance of our sampling scheme to several competing sampling schemes currently available in the literature.

Kim et al., (1998) estimate the univariate SV model without leverage by modelling the log of the squared returns and approximating the distribution of the innovations by a seven component mixture of normals; the paper then corrects the approximation using importance sampling, which makes their approach simulation consistent. Current popular MCMC estimation approaches for estimating the factor stochastic volatility model without leverage proposed by Chib et al., (2006), Kastner et al., (2017), and Kastner, (2019) follow the approach proposed by Kim et al., (1998), but are neither exact nor flexible. The first drawback of the approaches for estimation of the factor SV models mentioned above is that they do not correct for their mixture of normals approximations and so their estimators are not simulation consistent, with the approximation errors increasing with the dimension of the state vector. Section 5.2 of Gunawan et al., (2022) reports that the MCMC sampler of Kastner et al., (2017) can give different results to the CPHS111Note that Gunawan et al., (2022) refer to the CPHS as PHS. The second drawback of the factor SV estimators using mixture of normals approximations is that they are inflexible because they require different approximations when applied to different factor SV models. For example, the factor stochastic volatility with leverage requires approximating the joint distribution of outcome and volatility innovations by a ten-component mixture of bivariate normal distributions as in Omori et al., (2007). The CPHS is simulation consistent and it does not need to make such approximations and is simulation consistent in the sense that as the number of MCMC samples tends to infinity, the PHS iterates converge to the true posterior distributions of the states and parameters.

We also consider a factor stochastic volatility model in which the log-volatilities of the idiosyncratic errors follow a GARCH diffusion continuous volatility time process which does not have a closed form transition density (Kleppe et al.,, 2010; Shephard et al.,, 2004). It is well known that the Gibbs-type MCMC and PMCMC samplers, including the MCMC sampler of Kastner et al., (2017) and particle Gibbs of Andrieu et al., (2010), perform poorly for generating parameters of a diffusion model (Stramer and Bognar,, 2011). We show in section 5.2 that the particle Gibbs performs poorly in estimating the parameters of the GARCH diffusion model.

The rest of the article is organized as follows. Section 2 outlines the basic state space model, the sequential Monte Carlo algorithm for this model, and the backward simulation method. Section 3 introduces the CPHS, its invariant distribution, the constrained conditional sequential Monte Carlo algorithm, which is an important component of the CPHS, and shows that the PG and the CPMMH samplers are special cases of the CPHS. Sections 4 and 5 compare the performance of the CPHS to competing PMCMC methods for estimating univariate and multivariate stochastic volatility models. Section 6 discusses how the CPHS can estimate some other factor stochastic volatility models that would be very difficult to estimate by existing methods. The paper has an online supplement containing some further technical and empirical results.

2 Preliminaries

This section introduces the state space model, sequential Monte Carlo (SMC) and backward simulation. We use the colon notation for collections of variables, i.e. and for , .

2.1 State Space Models

We consider the stochastic process with parameter . The are the observations and the form the latent state space process. The density of is the density of given is (), and the density of given is .

We assume that the parameter , where is a subset of , and is the prior for . The are valued and the are valued and and are densities with respect to dominating measures which we write as and . The dominating measures are frequently taken to be the Lebesgue measure if and , where is the Borel -algebra generated by the set . Usually and .

The joint density function of is

| (1) |

The likelihood is , where and for . By using Bayes rule, we can express the joint posterior density of and as

where the marginal likelihood of is . Section 2.2 discusses an example of popular univariate state space models.

2.2 Example: the univariate SV model with leverage

We consider the univariate stochastic volatility model with leverage discussed and motivated by Harvey and Shephard, (1996),

| (2) | ||||

is the latent volatility process and the sequence is independent. Hence, the observation densities and the state transition densities are:

| (3) | ||||

The persistence parameter is restricted to to ensure that the volatility is stationary. The correlation between and also needs to lie between . When in Eq. (2), we obtain the standard volatility model without leverage.

2.3 (Correlated) Sequential Monte Carlo

Exact filtering and smoothing are only available for some special cases, such as the linear Gaussian state space model. For non-linear and non-Gaussian state space models, a sequential Monte Carlo (SMC) algorithm can be used to approximate the joint filtering densities.

Unless stated otherwise, upper case letters indicate random variables and lower case letters indicate the corresponding values of these random variables. e.g., and , and .

We use SMC to approximate the joint filtering densities

sequentially using particles, i.e., weighted samples ,

drawn from some proposal densities

and

for .

Definition 1.

Let

The SMC for is implemented by using the resampling scheme

, which depends on

and for a given . The argument means that

is the ancestor of . Section S2 of the online supplement gives the assumptions for the proposal densities and resampling scheme.

Definition 2.

We define as the vector random variable used to generate given and , where is the ancestor index of , as defined above. We write,

| (4) |

Denote the distribution of as . Common choices for are iid or iid random variables. The function maps the random variable to .

We now discuss how Definition 2 is implemented for the univariate SV model with leverage using the bootstrap filter. At time , we first generate random variables , and define

| (5) |

for . At time , we generate random variables , and define

| (6) |

for .

Definition 3.

For , we define as the vector of random variables used to generate the ancestor indices using the resampling scheme and define as the distribution of . This defines the mapping . The function maps the random variable to given and . Common choices for are iid or iid random variables.

We now discuss how Definition 3 is implemented for the simple multinomial resampling scheme. In the usual resampling scheme, an empirical cumulative distribution function is first constructed based on the index of the particle that we want to sample. We then generate random variables , sample the ancestor indices , and then obtain the selected particles for . This shows an example of the mapping . Section 3.3 and section S3.1 of the online supplement show a more complex mapping function , which is required by the CPHS.

Next, we define the joint distribution of as

| (7) |

The SMC algorithm also provides an unbiased estimate of the likelihood

| (8) |

which we will often write concisely as .

For the Metropolis-within-Gibbs (MWG) steps in part 1 of the CPHS given in section 3.2 to be effective and efficient, we require that the SMC algorithm ensures that the logs of the likelihood estimates and are close when and are close, where is the proposed value of the parameters and is the current value. This requires implementing the SMC algorithm carefully as a naive implementation introduces discontinuities in the logs of the estimated likelihoods due to the resampling steps when and are even slightly different. The problem with the simple multinomial resampling described above is that particles whose indices are close are not necessarily close themselves. This breaks down the correlation between the logs of the likelihood estimates at the current and proposed values.

To reduce the variance of the difference in logs of the likelihood estimates

appearing in the MWG acceptance ratio in the one dimensional case, it is necessary to sort the particles from the smallest to largest before resampling the particles. Sorting the particles before resampling helps to ensure that the particles whose indices are close are actually close to each other (Deligiannidis et al.,, 2018). Hence, the correlation in the logs of likelihood estimates is more likely to be preserved. However, this simple

sorting method does not extend easily to the multivariate case,

because we cannot sort multivariate states in this manner and guarantee

closeness of the particles. Deligiannidis et al., (2018) use the Hilbert sorting method of Gerber and Chopin, (2015).

We follow Choppala et al., (2016) and use a simpler and faster Euclidean sorting procedure described in Algorithm S4 in section S3.3 of the online supplement.

Algorithm S1 in section S3.1 of the online supplement describes the correlated SMC algorithm that we use,

which is similar to that of Deligiannidis et al., (2018).

Algorithm S1 uses the

multinomial resampling scheme (Algorithm S2) in section S3.1 of the online supplement.

2.4 Backward simulation

The CPHS requires sampling from the particle approximation of . Backward simulation is one approach to sampling from the particle approximation. It was introduced by Godsill et al., (2004) and used in Olsson and Ryden, (2011); Algorithm S3 in section S3.2 of the online supplement describes the backward simulation algorithm.

We denote the selected particles and trajectory by and , respectively. Backward simulation samples the indices sequentially, and differs from the ancestral tracing algorithm of Kitagawa, (1996), which only samples one index and traces back its ancestral lineage. Backward simulation is also more robust to the resampling scheme (multinomial resampling, systematic resampling, residual resampling, or stratified resampling) used in the resampling step of the algorithm (see Chopin and Singh,, 2015).

3 The Correlated Particle Hybrid Sampler

This section presents the CPHS for the Bayesian estimation of a state space model. Section 3.1 presents the target distribution. Section 3.2 presents the sampling scheme. Section 3.3 presents the constrained conditional sequential Monte Carlo (CCSMC) algorithm. Sections 3.4 and 3.5 discuss the correlated pseudo marginal and the particle Gibbs with backward simulation (PGBS) samplers, respectively. The methods introduced in this section are used in the univariate models in section 4 and the multivariate models in section 5.

3.1 Target Distributions

The key idea of CPHS is to construct a target distribution on an augmented space that includes all the particles generated by the SMC algorithm and has the joint posterior density of the latent states and parameters as a marginal.

The CPHS targets the distribution

| (9) |

where . For brevity, in Eq. (9) and below, we write as . We now discuss some properties of the target distribution in Eq. (9). They are proved in section S1 of the online supplement.

Theorem 1.

The target distribution in Eq. (9) has the marginal distribution

and hence, with some abuse of notation, we write .

The target density in Eq. (9) involves densities of the basic standard normal and uniform distribution instead of the standard way in terms of densities of state particles. This is done to make the Metropolis-within-Gibbs step in Algorithm 1 more efficient; see section 3.2 for further details. Theorem 1 shows that the marginal distribution in Eq. (9) has the joint posterior density of the latent states and parameters as the marginal density.

Theorem 2.

The target distribution in Eq. (9) can also be expressed as

| (10) |

The target distribution in Eq. (2) is expressed in terms of the estimated likelihood . Corollary 1 below and Theorem 2 are used to derive the acceptance probability in Part 1 in our CPHS (Algorithm 1).

Corollary 1.

By integrating out of the target distribution in Eq. (2) we obtain

| (11) |

Corollary 2.

The conditional distribution is

| (12) |

3.2 The CPHS

We now outline a sampling scheme for the state space model that allows the user to generate those parameters that can be drawn efficiently conditional on the states by a particle Gibbs step(s); all the other parameters are drawn in a Metropolis-within-Gibbs step(s) by conditioning on the basic uniform or standard normal random variables; e.g., parameters that are highly correlated with states, or parameters whose generation is expensive when conditioning on the states. For simplicity, let partition the parameter vector into 2 components where each component may be a vector. The CPHS is given in Algorithm 1; it generates the vector of parameters using the Metropolis-within-Gibbs step and the vector of parameters using the PG step. The components and can be further partitioned and sampled separately in multiple Metropolis-within-Gibbs steps and multiple PG steps, respectively.

We note that the correlated pseudo-marginal method of Deligiannidis et al., (2018) correlates the random numbers, and used in constructing the estimators of the likelihood at the current and proposed values of the parameters. This correlation is set very close to 1 to reduce the variance of the difference in the logs of the estimated likelihoods appearing in the MH acceptance ratio. It is easy to see that part 1 (MWG sampling) of our sampling scheme is a special case of the correlated pseudo-marginal step with the correlation set to 1. We condition on the same set of random numbers that is generated using CCSMC in part 4 of Algorithm 1. That is, in our scheme, we deal with which is the difference in the logs of the estimated likelihoods at the proposed and current values of the parameters. The basic random numbers are fixed in the Metropolis-within-Gibbs step (part 1), but they are updated in part 4 of Algorithm 1. On the other hand, Part 1 (PMMH sampling) of PHS proposed by Mendes et al., (2020) is a special case of the correlated pseudo-marginal step with the correlation set to .

Given initial values for , , , and

-

Part 1:

MWG sampling.

-

(a)

Sample

-

(b)

Run the sequential Monte Carlo algorithm and evaluate .

-

(c)

Accept the proposed values with probability

(13)

-

(a)

- Part 2:

-

Part 3:

PG sampling.

-

(a)

Sample

-

(b)

Accept the proposed values with probability

(14)

-

(a)

-

Part 4:

Sample from using the constrained conditional sequential Monte Carlo algorithm (Algorithm 2) and evaluate .

Part 1 (MWG sampling): from corollary 1, we can show that

where is defined in Eq. (8). This leads to the acceptance probability in Eq. (0c). Part 2 follows from Corollary 2. Using theorem 1, we can show that the Metropolis-Hastings in Eq. (14) (Part 3: PG sampling) simplifies to

| (15) |

Part 4 updates the basic random numbers and using constrained conditional sequential Monte Carlo (section 3.3) and follows from Eq. (9) (the target), theorem 1 and Definitions 2 and 3.

Algorithm S8 in section S4 of the supplementary material gives a more general sampling scheme than Algorithm 1 with Part 1 having a Metropolis-within-Gibbs proposal that potentially moves the basic uniform and standard normal variables as well as the parameter of interest. Possible Metropolis-within-Gibbs proposals in Part 1 include the correlated pseudo-marginal approach in Deligiannidis et al., (2018), the block pseudo-marginal approach in Tran et al., (2016), and the standard pseudo-marginal approach in Andrieu and Roberts, (2009). The advantage of Algorithm 1 over Algorithm S8 in section S4 of the online supplement is that Part 1 has fewer tuning parameters that need to be chosen by the user and is computationally more efficient because the basic uniform and standard normal variables are fixed and not generated.

3.3 Constrained conditional sequential Monte Carlo

This section discusses the constrained conditional sequential Monte Carlo (CCSMC) algorithm (Algorithm 2), which is used in Part 4 of the CPHS (Algorithm 1). The CCSMC algorithm is a sequential Monte Carlo algorithm in which a particle trajectory and the associated sequence of indices are kept unchanged, which means that some elements of and are constrained. It is a constrained version of the conditional SMC sampler in Andrieu et al., (2010) that follows from the density of all the random variables that are generated by sequential Monte Carlo algorithm conditional on ,

| (16) |

which appears in the augmented target density in Eq. (9).

The CCSMC algorithm takes the number of particles , the parameters , and the reference trajectory as inputs. It produces the set of particles , ancestor indices , and weights ; it also produces the random variables used to propagate state particles and the random numbers used in the resampling steps . Both sets of random variables are used as the inputs of the sequential Monte Carlo algorithm in part (1b) of Algorithm 1.

Inputs: , , , and

Outputs: , , , , and

Fix , , and .

-

1.

For

-

(a)

Sample and set for .

-

(b)

Obtain such that .

-

(c)

Compute the importance weights , for , and normalize .

-

(a)

-

2.

For

-

(a)

Sort the particles using the simple sorting procedure of Choppala et al., (2016) and obtain the sorted index for and the sorted particles and weights and , for .

-

(b)

Use a constrained sampling algorithm, for example, the constrained multinomial sampler (Algorithm S5 in section S3.4 of the online supplement),

-

i.

Generate the random variables used in the resampling step and obtain the ancestor indices based on the sorted particles .

-

ii.

Obtain the ancestor indices in the original order of the particles .

-

i.

-

(c)

Sample for and obtain such that .

-

(d)

Set for .

-

(e)

Compute the importance weights,

and normalize the .

-

(a)

At , step (1a) samples the basic random numbers from the standard normal distribution for and obtains the set of particles using Eq. (5), except for the reference particles . We obtain the basic random number associated with the reference particle in step (1b) using

for the univariate SV model with leverage using the bootstrap filter and compute the weights of all the particles in step (1c).

Section 2.3 shows that when the parameters change, the resampling step creates discontinuities and breaks the relationship between the likelihood terms at the current and proposed values. Step (2a) sorts the particles from smallest to largest using the simple sorting procedure of Choppala et al., (2016) and obtains the sorted particles and weights. The particles are then resampled using constrained multinomial resampling given in Algorithm S5 in section S3.4 of the online supplement and the ancestor index in the original order of the particles in step (2b) is obtained. Step (2c) samples the basic random numbers from the standard normal distribution for and obtains the set of particles using Eq. (6), except for the reference particles . We obtain the basic random number associated with the reference particle in step (2d) using

for the univariate SV model with leverage and the bootstrap filter and compute the weights of all the particles in step (2e).

3.4 Correlated pseudo marginal Metropolis-Hastings (CPMMH) Algorithm

This section shows that the correlated pseudo marginal Metropolis-Hastings (CPMMH) algorithm of Deligiannidis et al., (2018) is a special case of Algorithm 1 in section 3.2. This approach is useful for generating parameters that are highly correlated with the state variables. Algorithm 3 is the CPMMH algorithm. One iteration of the CPMMH is now discussed.

Step 1 of Algorithm 3 generates the proposal for parameter and the random numbers and from the proposal density

| (18) |

Following Deligiannidis et al., (2018), the proposal for the random variables is

| (19) |

for and , where and is the correlation coefficient which is set very close to 1. For the uniform random numbers, , the transformation to normality is first applied to obtain and set , where . We then obtain for and . Step 2 runs the sequential Monte Carlo algorithm (Algorithm S1) in section S3.1 of the online supplement, estimates the likelihood evaluated at the proposed value , and samples the index using backward simulation (Algorithm S3) in section S3.2 of the online supplement. Finally, the proposed values are accepted with the probability in Eq. (17). Using the proposal in Eq. (18), the acceptance probability simplifies to

| (20) |

If the proposed values are accepted, then , for all , for all , , and the selected particles are updated to .

3.5 Particle Gibbs with backward simulation (PGBS) algorithm

This section shows that the particle Gibbs of Andrieu et al., (2010) is also a special case of the Algorithm 1 in section 3.2, with a few modifications. The basic idea of the PG algorithm is to generate the parameters conditional on the states and the states conditional on the parameters.

The particle Gibbs of Andrieu et al., (2010) uses ancestral tracing (Kitagawa,, 1996) to sample the particle approximation of . Ancestral tracing samples an index with probability , and then traces back its ancestral lineage , and selects the particle . Whiteley, (2010), Lindsten and Schön, (2012) and Lindsten and Schon, (2013) suggest that ancestor sampling leads to poor mixing of the Markov chain for the latent states. They use backward simulation to sample from and show that the mixing of the Markov chain improves appreciably. We call their sampler the particle Gibbs with backward simulation (PGBS). Backward simulation is discussed in section 2.4 and Algorithm S3 in section S3.2 of the online supplement.

The PG algorithm uses the standard conditional sequential Monte Carlo (CSMC) (Algorithm S6 in section S3.5 of the online supplement) of Andrieu et al., (2010) instead of constrained conditional sequential Monte Carlo (Algorithm 2). We note that the CSMC algorithm is a special case of the CCSMC algorithm. It does not need to (1) obtain for (steps 1b and 2c of the CCSMC algorithm) and (2) sort the particles before resampling (step 2a). The constrained multinomial resampling is replaced by the conditional multinomial resampler in Algorithm S7 in section S3.5 of the online supplement). The conditional multinomial resampling scheme takes the particles and weights as the inputs and produces the ancestor indices . The first step computes the cumulative weights of the particles; the second step generates the ancestor indices .

We now discuss a single iteration of the PGBS algorithm (Algorithm 4). The first step of Algorithm 4 generates the proposal for the parameter . The proposal is accepted with the probability in Eq. (22). These two steps are conditioned on the selected particles from the previous iteration. Using theorem 1, we can show that the Metropolis-Hastings ratio in Eq. (22) simplifies to

| (21) |

Step 3 is the CSMC algorithm (Algorithm S6 in section S3.5 of the online supplement) that generates new particles while keeping a particle trajectory and the associated indices fixed. Step 4 samples the new index vector using Algorithm S3 in section S3.2 of the online supplement to carry out backward simulation.

Given initial values for , , , and .

4 Univariate Example: The univariate stochastic volatility model with leverage

This section applies the CPHS defined in section 3.2 to the univariate SV model with leverage.

4.1 Preliminaries

To define our measure of the inefficiency of a sampler that takes computing time into account, we first define the integrated autocorrelation time (IACT) for a univariate function of as

where is the th autocorrelation of the iterates of in the MCMC after the chain has converged. We use the CODA package of Plummer et al., (2006) to estimate the IACT values of the parameters. A low value of the IACT estimate suggests that the Markov chain mixes well. Our measure of the inefficiency of a sampler for a given parameter based on is the time normalised variance (TNV), where CT is the computing time in seconds per iteration of the MCMC. The estimate of TNV is the estimate of the IACT times the computing time. The relative time normalized variance of the sampler for () is the TNV relative to the TNV for the CPHS.

For a given sampler and for a model with a large number of parameters, let and be the maximum and mean of the IACT values over all the parameters in the model. In addition, let and be the maximum and mean of the IACT values over the latent variables .

4.2 Empirical Results

We use the following notation from Mendes et al., (2020), means using PMMH to sample the parameter vector ; means sampling in the PMMH step and in the PG step; and means sampling using the PG sampler. Finally, means sampling in the MWG step in part 1 of Algorithm 1 and in the PG step.

Our approach for determining which parameters to estimate by MWG and which to estimate by PG in the sampling scheme is to first run the PG algorithm for all the parameters to identify which parameters have large IACT’s. We then generate these parameters in the MWG step.

Priors: We now specify the prior distributions of the parameters. We follow Kim et al., (1998) and choose the prior for the persistence parameter as , with and , i.e.,

The prior for is the half Cauchy, i.e., . The prior for . We reparametrize and put a flat prior on . We note that because of the large sample size, the results are insensitive to these prior choices.

We compare the performance of the following samplers: (I) CPHS, (II) the particle Gibbs with backward simulation approach of Whiteley, (2010) , (III) the particle Gibbs with data augmentation approach of Fearnhead and Meligkotsidou, (2016) , (IV) the correlated pseudo-marginal sampler of Deligiannidis et al., (2018) , and (V) the sampler of Mendes et al., (2020). The tuning parameters of the PGDA sampler are set optimally according to Fearnhead and Meligkotsidou, (2016). The correlation parameter in the CPMMH is set to 0.999. We apply these methods to a sample of daily US food industry stock returns data obtained from the Kenneth French website, using a sample from December 11th, 2001 to the 11th of November 2013, a total of observations, , , , and .

Empirical Results: We use particles for the CPHS and CPMMH sampler, particles for the PGBS sampler, and particles for the PGDA sampler and the PHS. In this example, we use the bootstrap particle filter to sample the particles for all samplers and the adaptive random walk Metropolis-Hastings of Roberts and Rosenthal, (2009) for the MWG step in the CPHS, the PMMH step in the PHS sampler, and the CPMMH sampler as the proposal density for the parameters. The particle filter and the parameter samplers are implemented in Matlab. We ran the five sampling schemes for iterations, discarding the initial iterations as warmup.

Table 4.2 shows the IACT, TNV and RTNV estimates for the parameters and the latent volatilities in the univariate SV model with leverage estimated using the five different samplers for the US food industry stock returns data with observations.

[H] Univariate SV model with leverage for the five samplers. Sampler I: , Sampler II: , Sampler III: , Sampler IV: , and Sampler V: for US stock returns data with . Time is the time in seconds for one iteration of the algorithm. The RTNV is the TNV relative to the CPHS with . The IACT, TNV, and RTNV are defined in section 4.1.

| Param | I | II | III | IV | V | ||||||||||

| 20 | 50 | 100 | 200 | 500 | 1000 | 1000 | 2000 | 5000 | 20 | 50 | 100 | 1000 | 2000 | 5000 | |

| 177.48 | 191.48 | 100.60 | 155.84 | 61.34 | 43.18 | 114.64 | 22.81 | 18.67 | 18.81 | 12.95 | 10.27 | ||||

| 1.26 | 1.08 | 1.20 | 91.75 | 42.88 | 38.29 | 109.06 | 31.27 | 46.93 | 1.06 | 1.09 | 1.14 | ||||

| 536.84 | 656.13 | 407.15 | 117.31 | 46.73 | 40.83 | 73.53 | 44.69 | 22.48 | 33.14 | 20.21 | 16.75 | ||||

| 284.07 | 281.14 | 270.43 | 91.57 | 38.83 | 25.94 | 141.27 | 20.54 | 17.99 | 25.17 | 15.77 | 12.10 | ||||

| 656.13 | 407.15 | 155.84 | 61.34 | 43.18 | 33.14 | 20.21 | 16.75 | ||||||||

| 249.91 | 282.46 | 194.85 | 114.12 | 47.45 | 37.06 | 19.55 | 12.50 | 10.07 | |||||||

| 17.08 | 20.93 | 11.80 | 58.99 | 25.90 | 15.24 | 419.10 | 334.76 | 387.20 | 4.42 | 2.92 | 2.43 | ||||

| 8.52 | 8.39 | 11.09 | 2.73 | 7.33 | 7.32 | 89.66 | 76.41 | 95.55 | 62.87 | 60.26 | 96.80 | 4.95 | 5.69 | 8.99 | |

| 1.02 | 1 | 1.32 | 0.33 | 0.87 | 0.87 | 10.69 | 9.11 | 11.39 | 7.49 | 7.18 | 11.54 | 0.59 | 0.68 | 1.07 | |

| 3.91 | 1.91 | 1.87 | 1.57 | 14.08 | 7.92 | 5.93 | 83.75 | 30.29 | 15.83 | 1.22 | 1.13 | 1.12 | |||

| 0.98 | 0.79 | 0.91 | 0.31 | 0.65 | 0.97 | 21.40 | 23.36 | 37.18 | 12.56 | 5.45 | 3.96 | 1.37 | 2.20 | 4.14 | |

| 1.24 | 1 | 1.15 | 0.39 | 0.82 | 1.23 | 27.10 | 29.57 | 47.06 | 15.09 | 6.90 | 5.01 | 1.73 | 2.78 | 5.24 | |

| Time | |||||||||||||||

The table shows that: (1) The PGBS sampler has large IACT values for parameters, and , and that putting the two parameters in the MWG step of the CPHS, and the PMMH step of the PHS improves the mixing significantly. The CPMMH sampler has similar IACT values for parameters and to CPHS and PHS. (2) Increasing the number of particles in PGBS does not improve the IACT of the parameters , , and . (3) PGDA requires more than particles to improve the IACT of the parameters , , and compared to PGBS. Increasing the number of particles in PGDA improves the mixing of the Markov chains. (4) In terms of , the CPHS with only particles is 10.20, 27.37, 30.09 times better than PGBS with particles, respectively, is 28.23, 21.57, 32.27 times better than the PGDA sampler with particles, and is 4.42, 4.70, and 7.39 times better than PHS with particles for estimating the parameters of the univariate SV model with leverage. Similar conclusions hold for . (5) The performance of the correlated PMMH sampler is comparable to the CPHS for this model. In terms of , the CPHS with particles is 3.39, 1.11, and 1.37 times better than the correlated PMMH sampler with particles. Similar conclusions hold for . (6) In terms of , the CPHS with particles is 10.69, 9.11, and 11.39 times better than the PGDA sampler with particles, and is 7.49, 7.18, and 11.54 better than the CPMMH sampler with particles for estimating the latent volatilities. The performance of the PHS sampler with particles and the PGBS sampler with particles are slightly better than the CPHS for estimating latent volatilities. (7) It is clear that the CPHS performs well for estimating the parameters and the latent volatilities for the univariate SV model with leverage for estimating the latent volatilities. The performance of CPHS is comparable to the CPMMH for estimating the parameters and is comparable to the PGBS for estimating the latent volatilities. Section S5 of the online supplement gives further results for univariate stochastic volatility model with leverage with different number of observations observations. The example shows that the CPHS is much better than CPMMH for estimating both the model parameters and the latent volatilities.

We now consider the univariate SV model with leverage and a large number of covariates. The measurement equation is

| (23) |

We compare the performance of the following samplers: (I) , (II) , (III) . We apply the methods to simulated data with observations, , , , , is generated from normal distribution with mean zero and standard deviation 0.1, for all . The covariates generated randomly from . The prior for is for .

| Param | I | II | III | ||

|---|---|---|---|---|---|

| 100 | 1000 | 100 | 500 | 1000 | |

| 5.20 | 39.45 | 223.78 | 99.50 | 149.60 | |

| 1.07 | 1.00 | 139.16 | 149.02 | 99.30 | |

| 12.84 | 179.30 | 97.15 | 134.03 | 99.78 | |

| 11.63 | 102.60 | 133.71 | 97.44 | 102.45 | |

| 1.56 | 1.54 | 98.13 | 88.97 | 85.19 | |

| 1.78 | 1.83 | 146.72 | 121.53 | 111.90 | |

| 12.84 | 179.30 | 223.78 | 149.02 | 149.60 | |

| 14.12 | 227.71 | 114.13 | 269.73 | 477.22 | |

| 1 | 16.13 | 8.08 | 19.10 | 33.80 | |

| 2.01 | 7.40 | 101.85 | 91.27 | 87.23 | |

| 2.21 | 9.40 | 51.94 | 165.20 | 278.26 | |

| 1 | 4.25 | 23.50 | 74.75 | 125.91 | |

| 4.21 | 2.17 | 127.76 | 68.63 | 25.73 | |

| 4.63 | 2.76 | 65.16 | 124.22 | 82.08 | |

| 1 | 0.60 | 14.07 | 26.83 | 17.73 | |

| 1.21 | 1.04 | 10.83 | 7.70 | 7.37 | |

| 1.33 | 1.32 | 5.52 | 13.94 | 23.51 | |

| 1 | 0.99 | 4.15 | 10.48 | 17.68 | |

| Time | 1.10 | 1.27 | 0.51 | 1.81 | 3.19 |

Table 1 reports the estimated IACT, TNV, and RTNV values for the parameters and the latent volatilities in the univariate SV model with leverage and covariates estimated using different samplers. The table suggests the following: (1) The CPHS is much better than the CPMMH and the PGBS samplers for estimating the parameters in the univariate SV model. This example shows very clearly how the flexibility of CPHS can be used to obtain good results. The vector of parameters are high-dimensional and not highly correlated with the states, so it is important to generate them in a PG step. Both and are generated in an MWG step because they are highly correlated with the states. In general, it is useful to generate the parameters that are highly correlated with the states using a MWG step. If there is a subset of parameters that is not highly correlated with the states, then it is better to generate them using a PG step that conditions on the states, especially when the number of parameters is large. In addition, using PG is preferable in general to MWG because it is easier to obtain better proposals within a PG framework. (2) The CPMMH performs much worse than CPHS because the adaptive random walk is inefficient in high dimensions.

5 Multivariate example

This section applies the CPHS to a model having a large number of observations, a large number of parameters, and a large number of latent states. Section 5.1 discusses the multivariate factor stochastic volatility model with leverage. Section 5.2 compares the performance of the CPHS to competing PMCMC methods to estimate a multivariate factor stochastic volatility model with leverage using real datasets having a medium and large number of observations.

5.1 The factor stochastic volatility model

The factor SV model is often used to parsimoniously model a vector of returns; see, e.g., Chib et al., (2006); Kastner et al., (2017); Kastner, (2019). However, estimating time-varying multivariate factor SV models can be very challenging because the likelihood involves computing an integral over a very high dimensional latent state and the number of parameters in the model can be very large. We use this complex model to illustrate the CPHS.

Suppose that is a vector of daily stock prices and define as the log-return of the stocks in period . We model as the factor SV model

| (24) |

where is a vector of latent factors (with ), is a factor loading matrix of the unknown parameters. Section S8 of the supplement discusses parametrization and identification issues for the factor loading matrix and the latent factors .

We assume that: the ; the idiosyncratic error volatility matrix is diagonal, with diagonal elements ; the log volatility processes are independent for , and each follows an independent autoregressive process of the form

| (25) | ||||

We also consider that the log-volatilities follow a GARCH diffusion continuous time volatility process, which does not have a closed form transition density. The continuous time GARCH diffusion process is (Kleppe et al.,, 2010; Shephard et al.,, 2004)

| (26) |

where the are independent Wiener processes. We use the GARCH diffusion model to show that the CPHS can be used to estimate state space models that do not have closed form transition densities. In this example, the CPHS is applied to an Euler approximation of the diffusion process driving the log volatilities. The Euler scheme places evenly spaced points between times and . We denote the intermediate volatility components by and set and . The equation for the Euler evolution, starting at is

| (27) |

for , where .

The factors are assumed independent with ; is a diagonal matrix with th diagonal element . Each log volatility is assumed to follow an independent autoregressive process of the form

| (28) |

Prior specification For and , we choose the priors for the persistence parameters and , the priors for and as in section 4.2. For every unrestricted element of the factor loadings matrix , we follow Kastner et al., (2017) and choose standard normal distributions. The priors for the GARCH parameters are , , where and , for . These prior densities cover most possible values in practice.

Although the multivariate factor SV model can be written in standard state space form as in section 2.1, it is more efficient to take advantage its conditional independence structure and develop a sampling scheme on multiple independent univariate state space models.

Conditional Independence and sampling in the factor SV model: The key to making the estimation of the factor SV model tractable is that given the values of , the factor model given in Eq. (24) separates into independent components consisting of univariate SV models for the latent factors and univariate SV models with (or without) leverage for the idiosyncratic errors. That is, given , we have univariate SV models with leverage, with the th ‘observation’ on the th SV model, and we have univariate SV models without leverage, with the th observation on the th univariate SV model. Section S7 of the supplement discusses the CPHS for the factor SV model and makes full use of its conditional independence structure. Section S9 of the supplement also discusses a deep interweaving strategy for the loading matrix and the factor that helps the sampler mix better.

Target density: Section S6 of the supplement gives the target distribution for the factor SV model, which is a composite of the target densities of the univariate SV models for the idiosyncratic errors and the factors, together with densities for and .

5.2 Empirical Study

This section presents empirical results for the multivariate factor SV model with leverage model described in section 5.1.

Estimation details: We applied our method to a sample of daily US industry stock returns data. The data, obtained from the website of Kenneth French, consists of daily returns for value weighted US industry portfolios. We use a sample from November 19th, 2009 to 11th of November, 2013 a total of 1000 observations and a sample from December 11th, 2001 to the 11th of November, 2013, a total of 3001 observations. The computation is done in Matlab and is run on 28 CPU-cores of GADI high-performance computer cluster at the National Computing Infrastructure Australia222https://nci.org.au/.

We do not compare our method to the correlated pseudo-marginal method of Deligiannidis et al., (2018) which generates the parameters, with the factors and idiosyncratic latent log volatilities integrated out for two reasons. First, using a pseudo-marginal method results in a dimensional state space model and Mendes et al., (2020) show that it is very hard to preserve the correlation between the logs of the estimated likelihoods at the current and proposed values for such a model. Thus the correlated pseudo-marginal method would get stuck unless enough particles are used to ensure that the variance of log of the estimated likelihood is close to 1. Deligiannidis et al., (2018) also discuss the issue of how the correlation between the log of the estimated likelihoods at the current and proposed values decreases as the dimension increases. Second, the dimension of the parameter space in the factor SV model is large which makes it difficult to implement the pseudo-marginal sampler efficiently as it is difficult to obtain good proposals for the parameters because the first and second derivatives of the likelihood with respect to the parameters can only be estimated, while the random walk proposal is easy to implement but is very inefficient in high dimensions.

Kastner et al., (2017) develop the Gibbs-type MCMC algorithm to estimate multivariate factor stochastic volatility model. They use the approach proposed by Kim et al., (1998) to approximate the distribution of innovations in the log outcomes by a mixture of normals. Their estimator is not simulation consistent because it does not correct for these approximations. In addition, the Gibbs-type MCMC sampler cannot be used to estimate the factor SV model with the log volatility following diffusion processes with intractable state transition density. It is well known that the Gibbs sampler is inefficient for generating parameters of a diffusion model, in particular the variance parameter (Stramer and Bognar,, 2011).

We report results for a modified version of the PGDA sampler applied to the multivariate factor stochastic volatility model as

Mendes et al., (2020) shows that the PGDA sampler of Fearnhead and Meligkotsidou, (2016) does not work well when the model has many parameters

because the PGDA updates the pseudo observations of the parameters by MCMC and updates all of the latent states and parameters jointly using the particle filter.

We now extend the PGDA method to estimate the multivariate factor SV model and call it the refined PGDA method.

The sampler first generates the factor loading matrix and latent factors by a PG step and then,

conditioning on the latent factors and the factor loading matrix, we obtain univariate SV models with leverage and univariate SV models.

Then, for each of the univariate models, we can apply the Fearnhead and Meligkotsidou, (2016) approach by updating the pseudo observation of the SV parameters by MCMC

and updating the parameters and the latent states jointly by particle filter. The tuning parameters of the PGDA sampler are set optimally according to Fearnhead and Meligkotsidou, (2016).

We compare the following samplers:

(I) the ,

(II) the ,

(III) the refined ,

and

(IV) the .

Empirical Results Tables S2 to S5 in section S10 of the online supplement show the mean and maximum IACT values for each parameter in the factor SV model with leverage for observations, stock returns, and factor. We compare the CPHS with with the PGBS, the refined PGDA, and the PHS samplers with . The tables show that the factor loading matrix is sampled efficiently by all samplers with comparable IACT values. However, the CPHS has much smaller IACT values than the PGBS sampler for the , , and parameters for all (number of particles). The CPHS has much smaller IACT values for the , , and parameters than the PHS and the refined PGDA samplers when and and has comparable IACT values for the , , and parameters when and .

Table 5 summarises the estimation result for a factor SV model with leverage with observations, stock returns, and factor. The table shows that: (1) Increasing the number of particles from to does not seem to improve the performance of the PGBS sampler. This indicates that for the parameters that are highly correlated with the states, such as the , increasing the number of particles does not improve the mixing of the parameters. (2) Increasing the number of particles from to improves the performance of the PHS and the refined PGDA samplers significantly. They require at least particles to obtain comparable values of and as the CPHS. (3) The CPHS with particles is much more efficient than the PGBS sampler in terms of both and for all number of particles . (4) The CPHS is much more efficient than the PHS and the refined PGDA samplers for and , but only slightly more efficient for and .

We now compare the performance of the CPHS with when the number of observations is large, with PGBS, the refined PGDA, and the PHS with . Tables S6 to S8 in section S10 of the online supplement show the mean and maximum IACT values for each parameter in the factor SV model with leverage for observations, stock returns, factors, for the CPHS, the PHS, the PGBS and the refined PGDA samplers. Similarly to the case, the tables show that the factor loading matrix is sampled efficiently by all samplers, with comparable IACT values. The CPHS has much smaller IACT values than the PGBS sampler, the refined PGDA, and the PHS sampler for the , , and parameters for all cases. Note that even with , the PHS, PGBS, and refined PGDA samplers do not give comparable performance to the CPHS. Table 5 summarises the estimation result for a factor SV model with leverage with observations, stock returns, and factors. The table shows that: (1) It is necessary to greatly increase the number of particles for both the PHS and refined PGDA samplers to avoid the Markov chains from getting stuck. It is clear, however, that the CPHS works with only particles. This suggests that the CPHS scales up better than the other two samplers in both the number of observations and in the number of parameters. (2) The table clearly shows that the CPHS with particles is much more efficient than the PHS, the PGBS, and the refined PGDA samplers with particles in terms of both and .

GARCH Diffusion Models

This section considers the factor stochastic volatility models described in section 5, where the idiosyncratic log-volatilities follow a GARCH diffusion continuous volatility time process which do not have closed form state transition densities. The following samplers are compared: (I) The CPHS , (II) the , and (III) the PHS. We compare the PHS with with the PG and the PHS with .

Tables S9 and S10 in section S10 of the online supplement report the IACT estimates for all the parameters for the factor SV model with the idiosyncratic log-volatilities following GARCH diffusion models. The table clearly shows that the PG sampler has large IACT values for the GARCH parameters for both and particles. Putting those three parameters of the GARCH diffusion model in the PMMH step of the PHS sampler with particles and in the MWG step of the CPHS sampler with particles improves the mixing significantly. Table 2 summarises the estimation results and shows that in terms of , the CPHS is and times better than the PG sampler with and , respectively, and in terms of , the CPHS is and times better than the PG sampler with and , respectively. The table also shows that in terms of , the CPHS is and times better than the PHS sampler with and , respectively, and in terms of , the CPHS is and times better than the PHS sampler with and , respectively.

[H] Factor SV model with leverage for US stock return data with observations, stock returns, and factors. Comparing Sampler I: ; Sampler II: PHS ; Sampler III: ; Sampler IV: in terms of Time Normalised Variance. Time denotes the time taken in seconds per iteration of the method. The table shows the , , …, . The IACT, TNV, and RTNV are defined in section 4.1.

| I | II | III | IV | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 100 | 100 | 250 | 500 | 1000 | 100 | 250 | 500 | 1000 | 100 | 250 | 500 | 1000 | |

| 69.00 | 4454.61 | 493.83 | 88.33 | 75.54 | 1966.36 | 2158.37 | 2016.98 | 1781.30 | 6052.27 | 1111.59 | 192.41 | 98.03 | |

| 55.20 | 2316.40 | 340.74 | 83.03 | 109.53 | 845.53 | 1122.35 | 1311.04 | 1799.11 | 2602.48 | 578.03 | 126.99 | 99.99 | |

| 1 | 41.96 | 6.17 | 1.50 | 1.98 | 15.32 | 20.13 | 23.75 | 32.59 | 47.15 | 10.47 | 2.30 | 1.81 | |

| 19.47 | 140.20 | 32.78 | 22.32 | 19.98 | 237.77 | 259.93 | 237.88 | 245.48 | 545.18 | 81.01 | 29.25 | 17.78 | |

| 15.58 | 72.90 | 22.62 | 20.98 | 28.97 | 102.24 | 135.16 | 154.62 | 247.93 | 234.43 | 42.13 | 19.30 | 18.14 | |

| 1 | 4.68 | 1.45 | 1.35 | 1.86 | 6.56 | 8.68 | 9.92 | 15.91 | 15.05 | 2.70 | 1.24 | 1.16 | |

| Time | 0.80 | 0.52 | 0.69 | 0.94 | 1.45 | 0.43 | 0.52 | 0.65 | 1.01 | 0.43 | 0.52 | 0.66 | 1.02 |

[H] Factor SV model with leverage for US stock return data with observations, stock returns, and factors. Comparing Sampler I: ; Sampler II: PHS ; Sampler III: ; Sampler IV: in terms of Time Normalised Variance. Time denotes the time taken in seconds per iteration of the method. The table shows the , , …, . The IACT, TNV, and RTNV are defined in section 4.1.

| I | II | III | IV | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 100 | 500 | 1000 | 2000 | 500 | 1000 | 2000 | 500 | 1000 | 2000 | |

| 119.37 | 5003.03 | 2467.29 | 908.42 | 2517.54 | 2233.80 | 1914.02 | 4815.88 | 2269.26 | 1379.56 | |

| 358.11 | 14808.97 | 11349.53 | 7721.57 | 7049.11 | 6768.41 | 9321.28 | 13725.26 | 7261.63 | 7008.06 | |

| 1 | 41.35 | 31.69 | 21.56 | 19.68 | 18.90 | 26.03 | 38.33 | 20.28 | 19.57 | |

| 24.02 | 138.21 | 85.71 | 41.14 | 217.58 | 215.24 | 247.47 | 395.05 | 140.35 | 72.56 | |

| 72.06 | 409.10 | 394.27 | 349.69 | 609.22 | 652.18 | 1205.18 | 1125.89 | 449.12 | 368.60 | |

| 1 | 5.68 | 5.47 | 4.85 | 8.45 | 9.05 | 16.72 | 15.62 | 6.23 | 5.12 | |

| Time | 3.00 | 2.96 | 4.60 | 8.50 | 2.80 | 3.03 | 4.87 | 2.85 | 3.20 | 5.08 |

| I | II | III | |||

|---|---|---|---|---|---|

| 100 | 500 | 1000 | 500 | 1000 | |

| 77.27 | 6610.81 | 9535.97 | 282.65 | 175.38 | |

| 554.80 | 52093.18 | 160395.02 | 4632.63 | 6696.01 | |

| 1 | 93.90 | 289.10 | 8.35 | 12.07 | |

| 19.76 | 436.58 | 516.13 | 37.31 | 28.38 | |

| 141.88 | 3440.25 | 8681.31 | 611.51 | 1083.55 | |

| 1 | 24.25 | 61.19 | 4.31 | 7.64 | |

| Time | 7.18 | 7.88 | 16.82 | 16.39 | 38.18 |

6 Discussion

Our article shows how to scale up the particle MCMC in terms of the number of parameters and the number of observations by expressing the target density of the PMCMC in terms of the basic uniform or standard normal random numbers used in the sequential Monte Carlo algorithm, rather than in terms of state particles. The parameters that can be drawn efficiently conditional on the particles are generated by a particle Gibbs step(s); all the other parameters are drawn in a Metropolis-within-Gibbs step(s) by conditioning on the basic uniform or standard normal random variables; e.g., parameters that are highly correlated with states, or parameters whose generation is expensive when conditioning on the states. The empirical results show that the CPHS is scalable in the number of parameters and the number of observations and is much more efficient than the competing MCMC methods. We also show that the particle Gibbs (PG) of Andrieu et al., (2010) and the correlated pseudo marginal Metropolis-Hastings (CPMMH) algorithm of Deligiannidis et al., (2018) are special cases of the CPHS.

The CPHS is useful when it is necessary estimate complex statistical models that are very difficult to estimate by existing methods. For example: complex factor stochastic volatility models where the factors and idiosyncratic errors follow mixture of normal distributions; multivariate financial time series model with recurrent neural network type architectures, e.g. the Long Short-term Memory Model of Hochreiter and Schmidhuber, (1997) and the statistical recurrent unit of Oliva et al., (2017); stochastic differential equation mixed effect models, which are used in psychology (Oravecz et al.,, 2011) and biomedical work (Leander et al.,, 2015).

7 Acknowledgement

The research of Robert Kohn and David Gunawan was partially supported by an ARC Center of Excellence grant CE140100049.

References

- Andrieu et al., (2010) Andrieu, C., Doucet, A., and Holenstein, R. (2010). Particle Markov chain Monte Carlo methods. Journal of the Royal Statistical Society, Series B, 72(3):269–342.

- Andrieu et al., (2018) Andrieu, C., Doucet, A., Yıldırım, S., and Chopin, N. (2018). On the utility of Metropolis-Hastings with asymmetric acceptance ratio. arXiv preprint arXiv:1803.09527.

- Andrieu and Roberts, (2009) Andrieu, C. and Roberts, G. (2009). The pseudo-marginal approach for efficient Monte Carlo computations. The Annals of Statistics, 37:697–725.

- Chan et al., (2018) Chan, J., Gonzalez, R. L., and Strachan, R. W. (2018). Invariant inference and efficient computation in the static factor model. Journal of the American Statistical Association, 113(522):819–828.

- Chib et al., (2006) Chib, S., Nardari, F., and Shephard, N. (2006). Analysis of high dimensional multivariate stochastic volatility models. Journal of Econometrics, 134(2):341–371.

- Chopin and Singh, (2015) Chopin, N. and Singh, S. S. (2015). On the particle Gibbs sampler. Bernoulli, 21(3):1855–1883.

- Choppala et al., (2016) Choppala, P., Gunawan, D., Chen, J., Tran, M. N., and Kohn, R. (2016). Bayesian inference for state space models using block and correlated pseudo marginal methods. Available from http://arxiv.org/abs/1612.07072.

- Conti et al., (2014) Conti, G., Fruhwirth-Schnatter, S., Heckman, J. J., and Piatek, R. (2014). Bayesian exploratory factor analysis. Journal of Econometrics, 183(1):31–57.

- Deligiannidis et al., (2018) Deligiannidis, G., Doucet, A., and Pitt, M. K. (2018). The correlated pseudo-marginal method. Journal of Royal Statistical Society, Series B, 80(5):839–870.

- Douc and Cappé, (2005) Douc, R. and Cappé, O. (2005). Comparison of resampling schemes for particle filtering. In Image and Signal Processing and Analysis, 2005. ISPA 2005. Proceedings of the 4th International Symposium on, pages 64–69. IEEE.

- Doucet et al., (2000) Doucet, A., Godsill, S., and Andrieu, C. (2000). On sequential Monte Carlo sampling methods for Bayesian filtering. Statistics and Computing, 10(3):197–208.

- Fearnhead and Meligkotsidou, (2016) Fearnhead, P. and Meligkotsidou, L. (2016). Augmentation schemes for particle MCMC. Statistics and Computing, 26(6):1293–1306.

- Gerber and Chopin, (2015) Gerber, M. and Chopin, N. (2015). Sequential quasi Monte Carlo. Journal of Royal Statistician Society Series B, 77(3):509–579.

- Geweke and Zhou, (1996) Geweke, J. F. and Zhou, G. (1996). Measuring the pricing error of the arbitrage pricing theory. Review of Financial Studies, 9:557–587.

- Godsill et al., (2004) Godsill, S., Doucet, A., and West, M. (2004). Monte Carlo smoothing for nonlinear time series. Journal of the American Statistical Association, 99(465):156–168.

- Gunawan et al., (2022) Gunawan, D., Kohn, R., and Tran, M. N. (2022). Flexible and robust particle tempering for state space models. Econometrics and Statistics.

- Harvey and Shephard, (1996) Harvey, A. C. and Shephard, N. (1996). The estimation of an asymmetric stochastic volatility model for an asset returns. Journal of Business and Economics Statistics, 14(4):429–434.

- Hochreiter and Schmidhuber, (1997) Hochreiter, S. and Schmidhuber, J. (1997). Long short-term memory. Neural computation, 9(8):1735–1780.

- Kastner, (2019) Kastner, G. (2019). Sparse Bayesian time-varying covariance estimation in many dimensions. Journal of Econometrics, 210(1):98–115.

- Kastner et al., (2017) Kastner, G., Fruhwirth-Schnatter, S., and Lopes, H. F. (2017). Efficient Bayesian inference for multivariate factor stochastic volatility models. Journal of Computational and Graphical Statistics, 26(4):905–917.

- Kim et al., (1998) Kim, S., Shephard, N., and Chib, S. (1998). Stochastic volatility: Likelihood inference and comparison with ARCH models. The Review of Economic Studies, 65(3):361–393.

- Kitagawa, (1996) Kitagawa, G. (1996). Monte Carlo filter and smoother for non-Gaussian nonlinear state space models. Journal of Computational and Graphical Statistics, 5(1):1–25.

- Kleppe et al., (2010) Kleppe, T. S., Yu, J., and Skaug, H. (2010). Estimating the GARCH diffusion: Simulated maximum likelihood in continuous time. SMU Economics and Statistics Working Paper Series, No. 13-2010, 13.

- Leander et al., (2015) Leander, J., Almquist, J., Ahlstrom, C., Gabrielsson, J., and Jirstrand, M. (2015). Mixed effects modeling using stochastic differential equations: illustrated by pharmacokinetic data of nicotinic acid in obese Zucker rats. The AAPS Journal, 17(3):586–596.

- Lindsten and Schön, (2012) Lindsten, F. and Schön, T. B. (2012). On the use of backward simulation in the particle Gibbs sampler. In Proceedings of the 37th International Conference on Acoustics, Speech, and Signal Processing, pages 3845–3848. ICASSP.

- Lindsten and Schon, (2013) Lindsten, F. and Schon, T. B. (2013). Backward simulation methods for Monte Carlo statistical inference. Foundations and Trends in Machine Learning, 6(1):1–143.

- Mendes et al., (2020) Mendes, E. F., Carter, C. K., Gunawan, D., and Kohn, R. (2020). A flexible particle Markov chain Monte Carlo method. Statistics and Computing, 30:783–798.

- Oliva et al., (2017) Oliva, J. B., Póczos, B., and Schneider, J. (2017). The statistical recurrent unit. In International Conference on Machine Learning, pages 2671–2680. PMLR.

- Olsson and Ryden, (2011) Olsson, J. and Ryden, T. (2011). Rao-Blackwellization of particle Markov chain Monte Carlo methods using forward filtering backward sampling. IEEE Transactions on Signal Processing, 59(10):4606–4619.

- Omori et al., (2007) Omori, Y., Chib, S., Shephard, N., and Nakajima, J. (2007). Stochastic volatility with leverage: Fast and efficient likelihood inference. Journal of Econometrics, 140:425–449.

- Oravecz et al., (2011) Oravecz, Z., Tuerlinckx, F., and Vandekerckhove, J. (2011). A hierarchical latent stochastic differential equation model for affective dynamics. Psychological Methods, 16(4):468.

- Plummer et al., (2006) Plummer, M., Best, N., Cowles, K., and Vines, K. (2006). CODA: Convergence Diagnosis and Output Analysis of MCMC. R News, 6(1):7–11.

- Roberts and Rosenthal, (2009) Roberts, G. O. and Rosenthal, J. S. (2009). Examples of adaptive MCMC. Journal of Computational and Graphical Statistics, 18(2):349–367.

- Scharth and Kohn, (2016) Scharth, M. and Kohn, R. (2016). Particle efficient importance sampling. Journal of Econometrics, 190(1):133–147.

- Shephard et al., (2004) Shephard, N., Chib, S., Pitt, M. K., et al. (2004). Likelihood-based inference for diffusion-driven models. technical report, https://www.nuff.ox.ac.uk/economics/papers/2004/w20/chibpittshephard.pdf.

- Stramer and Bognar, (2011) Stramer, O. and Bognar, M. (2011). Bayesian inference for irreducible diffusion processes using the pseudo-marginal approach. Bayesian Analysis, 6(2):231–258.

- Tran et al., (2016) Tran, M. N., Kohn, R., Quiroz, M., and Villani, M. (2016). Block-wise pseudo marginal Metropolis-Hastings. preprint arXiv:1603.02485v2.

- Van Der Merwe et al., (2001) Van Der Merwe, R., Doucet, A., De Freitas, N., and Wan, E. (2001). The unscented particle filter. Advances in neural information processing systems, 13:584–590.

- Whiteley, (2010) Whiteley, N. (2010). Discussion on particle Markov chain Monte Carlo methods. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 72(3):306–307.

- Yıldırım et al., (2018) Yıldırım, S., Andrieu, C., and Doucet, A. (2018). Scalable Monte Carlo inference for state-space models. arXiv preprint arXiv:1809.02527.

Online Supplementary material

We use the following notation in the supplement. Eq. (1), algorithm 1, and sampling scheme 1, etc, refer to the main paper, while Eq. (S1), algorithm S1, and sampling scheme S1, etc, refer to the supplement.

S1 Proofs

Lemma S1.

-

(i)

-

(ii)

For ,

-

(iii)

For ,

Proof.

The proof of parts (i) and (ii) is straightforward. The proof of part (iii) follows from assumption S2. ∎

Proof of Theorem 1.

To prove the theorem we carry out the marginalisation by building on the proof of Theorem 3 of Olsson and Ryden, (2011). Let . The marginal of is obtained by integrating it over . We start by integrating over to get

Now, integrate over using part (ii) of lemma S1 to obtain,

Then, integrate over using part (iii) of lemma S1 and then sum over to obtain

We repeat this for , to obtain,

Finally, integrate over and then integrate over using part (i) of lemma S1 to obtain the result. ∎

Proof of theorem 2.

We have that,

∎

Proof of corollary 1.

S2 Assumptions

This section outlines the assumptions required for the PMCMC algorithms.

For , we define , and

.

We follow Andrieu et al., (2010) and assume that

Assumption S1.

for any and .

Assumption S1 ensures that the proposal densities can be used to approximate for . If is a mixture of some general proposal density and , with having nonzero weight, and for all , then assumption S1 is satisfied. In particular, if we use the bootstrap filter then . Furthermore, for all for the univariate stochastic volatility model in section 2.2. We follow Andrieu et al., (2010) and assume that

Assumption S2.

For any and , the resampling scheme satisfies .

Assumption S2 is used in section 3.1 to prove theorem 1 and is satisfied by all the popular resampling schemes, e.g., multinomial, systematic and residual resampling. We refer to Douc and Cappé, (2005) for a comparison between resampling schemes and Doucet et al., (2000); Van Der Merwe et al., (2001); Scharth and Kohn, (2016) for the choice of proposal densities.

S3 Algorithms

S3.1 The SMC algorithms

This section describes how to implement the SMC algorithm described in sections 2.3 and 3.2. The SMC algorithm takes the number of particles , the parameters , the random variables used to propagate state particles , and the random numbers used in the resampling steps as the inputs; it outputs the set of particles , ancestor indices , and weights . At , we obtain the particles as a function of the basic random numbers using Eq. (5); we then compute the weights of all particles in step (2).

Step (3a) sorts the particles from smallest to largest using the Euclidean sorting procedure of Choppala et al., (2016) to obtain the sorted particles and weights. Algorithm S2 resamples the particles using multinomial sampling to obtain the ancestor index in the original order of the particles in steps (3b) and (3c). Steps (3a) - (3c) define the mapping . Steps (3d) generates the particles as a function of the basic random numbers using Eq. (6) for the univariate stochastic volatility with leverage and then computes the weights of all particles in step (3e).

Inputs: , and .

Outputs: .

-

1.

For , set for .

-

2.

Compute the importance weights

and normalize for .

-

3.

For ,

-

(a)

Sort the particles using the Euclidean sorting of Choppala et al., (2016) and obtain the sorted index for and the sorted particles and weights and , for .

-

(b)

Obtain the ancestor index based on the sorted particles using a resampling scheme e.g. the multinomial resampling in Algorithm S2.

-

(c)

Obtain the ancestor index based on the original order of the particles for .

-

(d)

Generate and set for .

-

(e)

Compute the importance weights

for and normalize to obtain for .

-

(a)

Input: , , and

Output:

-

1.

Compute the cumulative weights based on the sorted particles

-

2.

Set for , and note that for is the ancestor index based on the sorted particles.

S3.2 The backward simulation algorithm

-

1.

Sample conditional on , with probability proportional to , and choose ;

-

2.

For , sample , conditional on

, and choose with probability proportional to .

S3.3 Multidimensional Euclidean Sorting Algorithm

This section discusses the multidimensional Euclidean sorting algorithm used in Algorithms 2 and S1. Let be the - dimensional particle at a time , . Let be the Euclidean distance between two multidimensional particles. Algorithm S4 is the multidimensional Euclidean sorting algorithm that generates the sorted particles and weights with associated sorted indices. The first sorted index is the index of the particle having the smallest value along its first dimension. The other particles are chosen in a way that minimises the Euclidean distance between the last selected particle and the set of all remaining particles.

Input: ,

Output: sorted particles , sorted weights , sorted indices

Let be the index set.

When ,

-

•

Obtain the index , for all .

For

-

•

Set .

-

•

Update the index by removing from the index set.

-

•

Obtain the index .

Sort the particles and weights according to the indices to obtain the sorted particles , and sorted weights .

S3.4 Constrained conditional multinomial resampling algorithm

Algorithm S5 describes the constrained multinomial resampling algorithm used in CCSMC. It takes the sorted particles and weights as the inputs and produces the basic random numbers and the ancestor indices based on the sorted particles and weights . The first step computes the cumulative weights based on the sorted particles; the second step generates the random numbers and ancestor indices .

Input: , and

Output: and .

-

1.

Compute the cumulative weights based on the sorted particles ,

-

2.

Generate uniform random numbers for , such that , and set . For ,

S3.5 The conditional sequential Monte Carlo algorithm

Inputs: , , , and

Outputs: , , .

Fix , , and .

-

1.

For

-

(a)

Sample and set for .

-

(b)

Compute the importance weights , for , and normalize .

-

(a)

-

2.

For

-

(a)

Use a conditional multinomial sampler in algorithm S7 and obtain the ancestor indices of the particles .

-

(b)

Sample for .

-

(c)

Set for .

-

(d)

Compute the importance weights,

and normalize the .

-

(a)

Input: , and

Output: .

-

1.

Compute the cumulative weights based on the particles ,

-

2.

Generate uniform random numbers for , such that , and set . For ,

S4 The CPHS with a general proposal in part 1

Algorithm S8 is a version of the CPHS with a general Metropolis-within-Gibbs proposal for the parameter and the basic uniform and standard normal variables; part 1 includes the correlated pseudo-marginal proposal in Deligiannidis et al., (2018), the block pseudo-marginal in Tran et al., (2016), the standard pseudo marginal of Andrieu and Roberts, (2009), and the proposal in part 1 of Algorithm 1 as special cases. It is unnecessary to move the basic uniform and standard normal variables in part 1 to obtain a valid sampling scheme because they are generated in a Gibbs step in part 4 of Algorithms 1 and S8.

Given initial values for , , , and

-

Part 1:

General Metropolis-within-Gibbs move.

-

(a)

Sample .

-

(b)

Run the sequential Monte Carlo algorithm and evaluate .

-

(c)

Accept the proposed values with probability

(S1)

-

(a)

- Part 2:

-

Part 3:

PG sampling.

-

(a)

Sample .

-

(b)

Accept the proposed values with probability

(S2)

-

(a)

-

Part 4:

Sample from using constrained conditional sequential Monte Carlo (Algorithm 2) and evaluate .

S5 Further empirical results for the univariate SV model with leverage

This section gives further empirical results for the univariate SV model with leverage. Table S1 shows the IACT, TNV and RTNV estimates for the parameters in the univariate SV model with leverage estimated using the five different samplers for the simulated data with observations. The table shows that: (1) The PGDA sampler requires around particles to ensure that the Markov chains do not get stuck. (2) The PHS sampler requires at least particles to obtain similar IACT values for the parameters compared to the CPHS and the CPMMH sampler with particles. (3) In terms of , the CPHS with only particles is 18.82 times better than PGBS sampler with particles, is 15.70 times better than the PGDA sampler with particles, and is 670.57, 49.12, and 19.32 times better than the PHS sampler with particles for estimating the parameters of the univariate SV model. Similar conclusions hold for . (4) In terms of , the CPHS with particles is 39.37 times better than the PGDA sampler with particles, and is 12.56 times better than the CPMMH sampler for estimating the latent volatilities of the univariate SV model. The PGBS sampler is 1.72 times better than CPHS for estimating the latent volatilities of the univariate SV model.

| Param | I | II | III | IV | V | ||||

|---|---|---|---|---|---|---|---|---|---|

| 100 | 1000 | 1000 | 2000 | 5000 | 100 | 1000 | 2000 | 5000 | |

| 4.68 | 25.02 | NA | NA | 36.52 | 23.61 | 94.06 | 26.44 | 5.69 | |

| 1.41 | 3.97 | NA | NA | 34.09 | 17.80 | 1.11 | 4.06 | 1.99 | |

| 11.80 | 156.59 | NA | NA | 28.73 | 18.61 | 1931.35 | 79.89 | 14.94 | |

| 14.24 | 221.50 | NA | NA | 33.49 | 20.67 | 4441.36 | 163.42 | 35.92 | |

| 14.24 | 221.50 | NA | NA | 36.52 | 23.61 | 4441.36 | 163.42 | 35.92 | |

| 14.24 | 268.01 | NA | NA | 223.50 | 12.28 | 9548.92 | 699.44 | 275.15 | |

| 1 | 18.82 | NA | NA | 15.70 | 0.86 | 670.57 | 49.12 | 19.32 | |

| 8.03 | 101.77 | NA | NA | 33.21 | 20.17 | 1616.97 | 68.45 | 14.64 | |

| 8.03 | 123.14 | NA | NA | 202.69 | 10.49 | 3476.49 | 292.97 | 112.14 | |

| 1 | 15.33 | NA | NA | 25.24 | 1.31 | 432.94 | 36.48 | 13.97 | |

| 3.26 | 1.56 | NA | NA | 20.97 | 78.73 | 1.31 | 2.26 | 1.25 | |

| 3.26 | 1.89 | NA | NA | 128.34 | 40.94 | 2.82 | 9.67 | 9.57 | |

| 1 | 0.58 | NA | NA | 39.37 | 12.56 | 0.87 | 2.97 | 2.94 | |

| 1.19 | 1.02 | NA | NA | 9.82 | 10.76 | 1.01 | 1.02 | 1.01 | |

| 1.19 | 1.23 | NA | NA | 60.10 | 5.60 | 2.17 | 4.37 | 7.74 | |

| 1 | 1.03 | NA | NA | 50.50 | 4.71 | 1.82 | 3.67 | 6.50 | |

| Time | 1.00 | 1.21 | NA | NA | 6.12 | 0.52 | 2.15 | 4.28 | 7.66 |

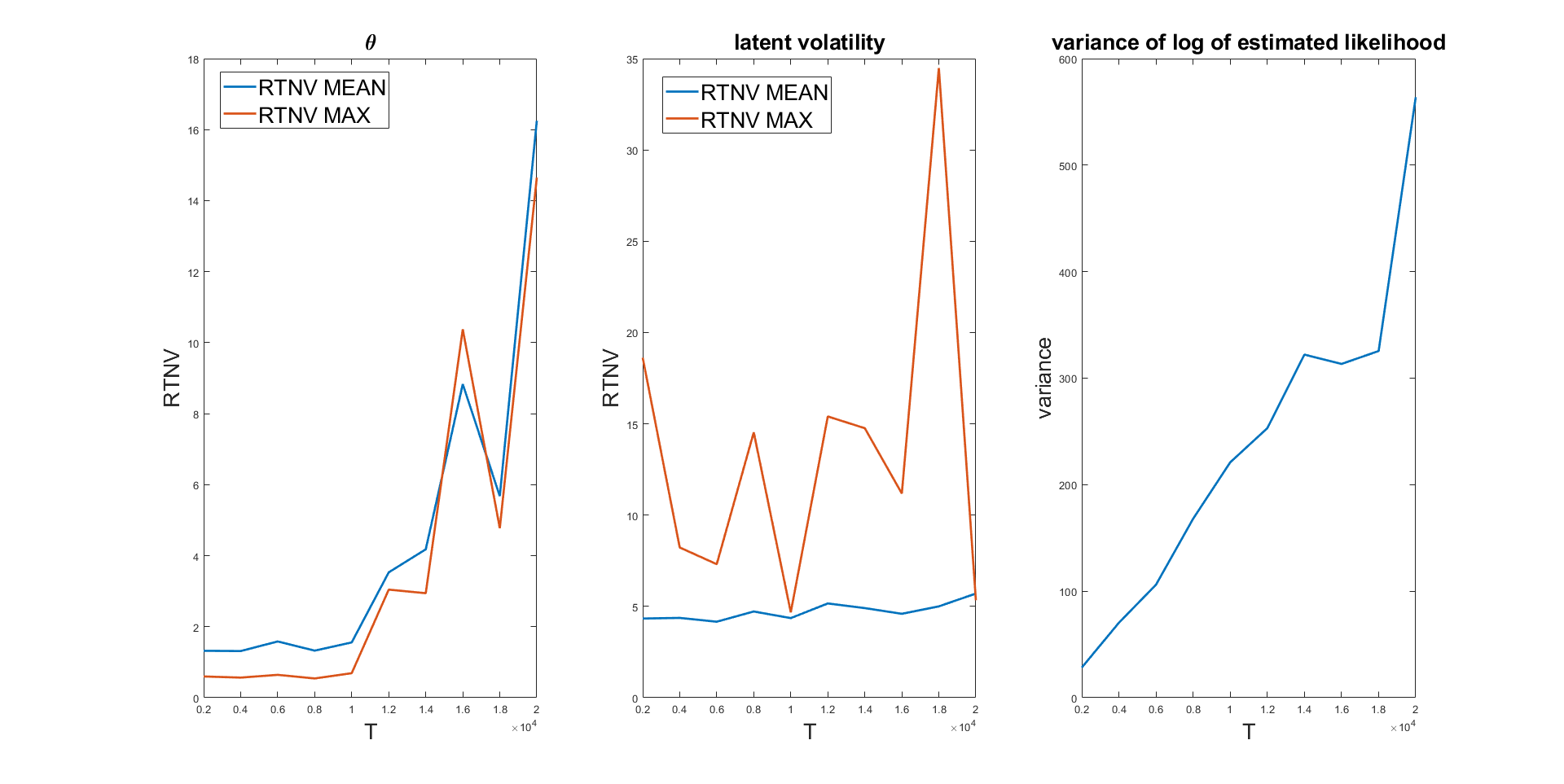

Figure S1 shows the and of the parameters and the latent volatilities estimated using CPHS and the CPMMH with particles for the univariate SV model. The RTNV is the TNV of the CPMMH relative to the TNV of the CPHS.

The data is generated from the univariate SV model with observations, , , , and . The figure also shows the variance of log of estimated likelihood evaluated at the true values of the parameters, with the variance increasing with the length of the time series. The figure suggests that the CPHS is much better than the CPMMH sampler for estimating both the parameters and the latent volatilities. This suggests that CPHS performs better than CPMMH at estimating an SV model with a large number of observations.

S6 Target distribution for the factor SV model

This section defines the target density for the factor SV model in section 5.1; it includes all the random variables produced by univariate SMC methods that generate the factor log-volatilities for and the idiosyncratic log-volatilities for , as well as the latent factors , the parameters of the individual idiosyncratic error SV’s , the parameters of the factor SV’s , and the factor loading matrix . We define . We use equations Eq. (28) to specify the univariate particle filters that generate the factor log-volatilities for without leverage and Eq. (25) to specify the particle filters for the idiosyncratic SV log-volatilities with leverage for . We denote the weighted samples at time for the factor log volatilities by and for the idiosyncratic errors log volatilities. The corresponding proposal densities are , , , and for and are the same as in the univariate case.