remarkRemark \newsiamremarkhypothesisHypothesis \newsiamthmclaimClaim \headersWasserstein Distance between 2D-Histograms by Minimum Cost FlowsF. Bassetti, S. Gualandi, and M. Veneroni

On the Computation of Kantorovich-Wasserstein Distances between 2D-Histograms by Uncapacitated Minimum Cost Flows

Abstract

In this work, we present a method to compute the Kantorovich-Wasserstein distance of order one between a pair of two-dimensional histograms. Recent works in Computer Vision and Machine Learning have shown the benefits of measuring Wasserstein distances of order one between histograms with bins, by solving a classical transportation problem on very large complete bipartite graphs with nodes and edges. The main contribution of our work is to approximate the original transportation problem by an uncapacitated min cost flow problem on a reduced flow network of size that exploits the geometric structure of the cost function. More precisely, when the distance among the bin centers is measured with the 1-norm or the -norm, our approach provides an optimal solution. When the distance among bins is measured with the 2-norm: (i) we derive a quantitative estimate on the error between optimal and approximate solution; (ii) given the error, we construct a reduced flow network of size . We numerically show the benefits of our approach by computing Wasserstein distances of order one on a set of grey scale images used as benchmark in the literature. We show how our approach scales with the size of the images with 1-norm, 2-norm and -norm ground distances, and we compare it with other two methods which are largely used in the literature.

keywords:

Kantorovich metric, Wasserstein distance, Transportation Problem, Network Simplex, Uncapacitated Minimum Cost Flow Problem90C06, 90C08

1 Introduction

The Transportation Problem, also called the Hitchcock-Koopmans transportation problem [17], is a historical problem for the mathematical programming community [42]. Indeed, the Transportation Problem is a particular case in the discrete setting of the more general Monge-Kantorovich Transportation Problem, largely studied in the functional analysis community (e.g., see [49, 3]), since the pioneering work of the French mathematician Gaspard Monge in 1781 [31], and later the fundamental work of L.V. Kantorovich on the theory of Linear Programming duality [48]. In the discrete setting, the Transportation Problem played a fundamental role in the development of the (Network) Simplex algorithm and of all the related network flows problems [42, 20, 1]. In the continuous setting, the Transportation Problem has recently gathered a renewed interest in computer science and applied mathematics, as an efficient method to compute distances between probability measures. We just mention here the attention gathered from the Machine Learning community in the use of the Wasserstein distances within Generative Adversarial Networks (GAN) [4], which was possible thanks to recent developments of very efficient numerical algorithms based on entropic regularization [13, 44, 11, 2].

In this paper, we focus on the Kantorovich metric, i.e. the Wasserstein (Vasershtein) distance of order 1, between two-dimensional histograms. By exploiting the geometric cost structure of the problem, we reduce the computation of Kantorovich distances to the problem of solving an uncapacitated minimum cost flow problem [34] on a graph with a prescribed topology. We consider three types of transportation costs among locations, induced by the -norms with , , and . For each norm, we build a flow network with a prescribed topology and given costs: our aim is to keep the size of the flow network as small as possible in order to accelerate the computation of Kantorovich distances, while limiting the use of computer memory. In addition, for the 2-norm, we provide a flow network that permits to find an approximate solution, and we derive a quantitative estimate on the error between optimal and approximate solution.

We stress the importance of having fast methods to compute exact and approximate Kantorovich distances. As discussed next, these distances are used as subproblems of more general tasks, and they are usually (re)computed again, and again, and again. Having a strongly polynomial algorithm of worst-case complexity (e.g., [20]), where is the number of locations of the transportation problem, it is definitely not enough. In addition, the size of Transportation Problems that must be solved is so large, that we need new numerical methods with strong mathematical foundations to solve such problems in practice. The contribution of our paper tackles exactly this numerical challenge.

Related Works

In mathematical programming, the Hitchcock-Koopmans transportation problem is considered a well–solved problem, since it can be solved with strongly polynomial algorithms or with Network Simplex algorithms [1, 20]. Recent work focused on the structure of the Transportation polytope [5, 9], on variations of the problem with nonlinear variables [47], or on mixed production transportation problems with concave costs [23]. However, our paper follows a different (numerical) line of research, which aims at solving very large instances of structured Hitchcock-Koopmans problems.

Our work is closely related to what, in the computer vision and image retrieval community, is known as the Earth Mover’s Distance (EMD) [38, 36]. In this context, the Kantorovich metric is used to compute the distance between images by precomputing so–called SIFT descriptors (special type of histograms, see [30]) and then by computing distances between such descriptors. The advantages of using a more computationally demanding metric instead of other simpler metrics is empirically demonstrated by the quality of the results, and in addition is elegantly supported by the mathematical theory that lays the foundation of the Kantorovich metric. Remarkable results were also obtained in the context of cell biology for comparing flow cytometry diagrams [8, 35] and in radiation therapy to improve the comparison of histograms related to tumor shape [25].

In statistics and probability, the Kantorovich distance is known as the Mallow’s distance [28]. It has been used for the assessment of goodness of fit between distributions [32, 46] as well as an alternative to the usual -divergences as cost function in minimum distance point estimation problems [6, 7]. It was used to compare 2D histograms, but only considering the 1-norm as a cost structure of the underlying Transportation Problem [29]. Another interesting application is the computation of the mean of a set of empirical probability measures based on the Kantorovich metric [14]. In machine learning, the use of Kantorovich distances is increasingly spreading in different contexts. Apart from the GAN networks [4], it has been used in unsupervised domain adaptation [12], in semi-supervised learning [45], and as a Loss Function for learning probability distributions [18]. For the theoretical foundations of the Monge-Kantorovich Transportation Problem, we refer the interested reader to [39, 49], while for a survey on recent applications of Optimal Transportation to [43].

Outline

In Section 2 we review the Kantorovich distance (i.e., the Wasserstein distance of order 1) in the discrete setting and we show its connection with Linear Programming (Section 2.2) and with uncapacitated minimum cost flow problems (Section 2.3 and Section 2.4). In Section 2.5, we discuss how to reduce the time complexity of evaluating the Kantorovich distance by approximating the transportation problem with a flow problem on a specific reduced network, we define the relative approximation error which is incurred upon by introducing a reduced flow network, and we provide a bound upon it.

Our main contributions are presented in Section 3, where we exploit the reduced flow networks to efficiently compute Kantorovich distances while using the 1-norm, the 2-norm, and the -norm as ground distances. In addition, for the 2-norm, we derive a quantitative estimate on the error between the optimal solution and an approximate solution on a reduced flow network (Theorem 3.4).

In Section 4, we give all the details of the results presented in Section 2.3-Section 2.5. Precisely, in Section 4.1, we recall the classical Strong Duality Theorem, which we use in Section 4.2 in order to establish a relation between the minimum of the cost flow problem and the infimum of Kantorovich’s transportation problem. The equivalence of these two problems is well known (Proposition 4.1), but we choose to give a proof here, as we were not able to find one in any reference. In Proposition 4.5 we state and prove the bound on the relative approximation error introduced in Eq. 12. This is key in the proof of the error estimate Eq. 16 in Theorem 3.4.

Finally, in Section 5 we conclude by reporting our extensive numerical experiments.

2 Background

In this section, we review the basic notions and we fix the notation used in this paper. Moreover, in Section 2.5 we state under which conditions Optimal Transportation and minimum cost flow problems yield the same optimal solutions, and we state a universal upper bound on the relative approximation error.

2.1 Kantorovich distance in the discrete setting

Let and be two discrete spaces. Given two probability vectors on and , denoted and , and a cost , the Kantorovich-Rubinshtein functional between and is defined as

| (1) |

where is the set of all the probability measures on with marginals and , i.e., of the probability measures such that

for every in . Such probability measures are sometimes called transportation plans or couplings for and . An important special case is when and the cost function is a distance on . In this case, which is our main interest in this article, is a distance on the simplex of probability vectors on , also known as Wasserstein distance of order . It is worth mentioning that a Wasserstein distance of order can be defined, more in general, for arbitrary probability measures on a metric space by

| (2) |

where now is the set of all probability measures on the Borel sets of that have marginals and , see, e.g., [3]. The infimum in Eq. 2 is attained and any probability which realizes the minimum is called an optimal transportation plan.

2.2 Linear Programming and Earth Mover’s Distance

The Kantorovich-Rubinshtein transportation problem in the discrete setting can be seen as a special case of the following Linear Programming problem, where we assume now that and are generic vectors of dimension and , with positive components,

| (3) | |||||

| (4) | s.t. | ||||

| (5) | |||||

| (6) | |||||

Note that the maximum flow quantity is equal to

If we have the so-called balanced transportation problem, otherwise the transportation problem is said to be unbalanced. For balanced optimal transportation problems, constraints Eq. 4 and Eq. 5 must be satisfied with equality, and the problem reduces to the Kantorovich transportation problem (up to normalization of the vectors and ). Problem (P) is also related to the so-called Earth Mover’s distance. In this case, and (, respectively) is the center of the data cluster (, respectively). Moreover, (, respectively) is the number of points in the cluster (, respectively) and, finally, is some measure of dissimilarity between and . Once the optimal transportation is determined, the Earth Mover’s distance between the signatures and is defined as

The Earth Mover’s distance (EMD) was first introduced by Rubner et al. for color and texture images in [37] and [38].

As noted in [38], the EMD is a true metric on distributions, and it is exactly the same as the Wasserstein distance, also known as Mallows distance. For more details on this, see e.g. [28] and the references therein. The cost function used in the EMD is typically a true distance, in general an distance.

2.3 Uncapacitated minimum cost flow problem on a graph

As we shall see in Section 2.4, a standard way to solve problem (P) is to recast it as an uncapacitated minimum cost flow problem. For this reason, we briefly recall the definition of minimum cost flow problem on a directed graph.

Let be a directed network with no self-loops, where is the vertex set and the set of edges. Consider a cost function and a function such that . A flow (or -flow) on is any function such that

| (7) |

In the following, we denote by the class of all the -flows on . The (uncapacitated) minimum cost flow problem associated to consists in finding a -flow which minimizes the cost

See, e.g., [1] or Chapter 9 in [26]. In what follows, we set

| (8) |

It is easy to see that if is a subgraph of , then

| (9) |

2.4 Wasserstein distance of order one as a minimum cost flow problem

It is easy to re-write as a minimum cost flow problem. Consider the bipartite graph

with , and define

It is plain to check that

| (10) |

Incidentally, an uncapacitated minimum cost flow problem of this kind is known as Hitchcock problem [17].

In general, given a network with nodes and arcs, Orlin’s algorithm [34] solves the uncapacitated minimum cost flow problem for integer supplies/demands in , where and is the complexity of finding a shortest path in . Using Dijkstra’s [16] algorithm . This gives, for general supplies/demands, the cost . Combining Eq. 10 with the previous observations, one obtains that can be computed exactly with a time complexity .

When , with , and is a distance, one can show that the flow problem associated with can be formulated on an auxiliary network, which is smaller than the bipartite graph . More precisely, set and let be the complete (directed) graph on (without self-loops). If is a distance, then

| (11) |

A detailed proof of this fact is given in Proposition 4.1 in Section 4.

Although is smaller than , the problem of determining is computationally demanding for relatively small . Using the previous considerations on the computational cost of a minimum flow problem, it is easy to see that the time complexity of computing is and hence it is of the same order of the complexity of computing .

Even if Eq. 11 is not satisfactory by itself, it is the starting point of our further developments. In Section 3 we shall exploit the cost structure (for some special costs) to reduce the number of edges in the graph on which the flow problem is formulated, and to largely simplify the complexity of the problem when is the space of base points of a 2D histogram.

2.5 Relaxation and Error bounds: main ideas

Before moving to our main results concerning the computation of the distance between 2D-histograms, let us briefly outline our main ideas in a more general setting. All the details are postponed to Section 4.

Let be a directed graph and consider the corresponding flow problem as an approximation of the original flow problem on the complete graph . One has that , which means that the relative error of approximation between the original minimum and its relaxation satisfies

| (12) |

If one is able to find a subgraph for which , one can reduce the problem of computing to a simpler minimum flow problem, i.e. to the evaluation of . Even if this is not possible, one can still use a subgraph to approximate and control the relative error of approximation .

This last goal is obtained by deriving a universal upper bound on . To this end define

| (13) |

where is the set of directed paths in from vertex to vertex and is the length of the path , composed of edges , and set

In Proposition 4.5 (Section 4) we prove that, if is a distance,

| (14) |

for any vector . Hence, combining Eq. 11 and Eq. 14 we get

for any couple of measures and any distance . In the light of these considerations, the key-point is to find a small graph for which is easy to compute and/or zero.

3 Efficient Computation of distance between 2D-Histograms

Histograms can be seen as discrete measures on a finite set of points in . Here we are interested in the case in which . To represent a two-dimensional histogram with equally spaced bins, we take without loss of generality

One can think of each point as the center of a bin.

In this case, and the complete directed graph has edges. Note that, according to last section’s notation, we are considering a set of points. To simplify notation, we write .

Following the idea sketched in Section 2.5, the goal is to approximate (or equivalently ), with for a suitable small graph .

When the distance among the bins is measured with the 1-norm or the infinity-norm , we provide an optimal solution using a graph with edges. When the distance between bins is measured with the -norm: (i) we show that an optimal solution can be obtained using a reduced network with around half the size of the complete bipartite graph, (ii) given an error, we provide an approximate solution using a reduced network of size .

In order to describe the subgraphs , we use the following notation. Given , define . If is a graph and , we denote the directed edge connecting to by . Let , . For , we define the following sets of vertices

The condition on the divisors of and implies that any point of coordinates is “visible” from the origin (0,0), in the sense that there is no point with integer coordinates on the line segment between the origin and .

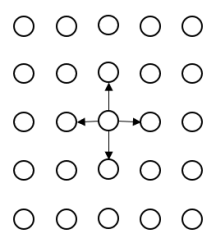

3.1 ground distance

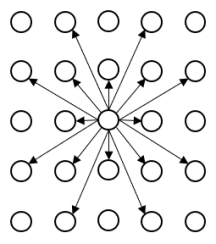

In this section we recover, as a special case of our approach, the method proposed in [29] to efficiently compute the -EMD by solving a flow problem on a graph with edges. Let us consider as ground distance the distance on , i.e. , where

In this case, as a subgraph of we choose

see Fig. 1.

Note that the set of (directed) edges of has cardinality .

It is a simple exercise to see that in this case for every . This means that one can compute the distance between two normalized histograms and without any error, by solving a minimum cost flow problem on the graph which has nodes and edges. We summarize the previous statements, recalling that was defined in Eq. 8, in the next

Proposition 3.1.

Under the previous assumptions, and hence

In particular,

for every couple of probability measures and on .

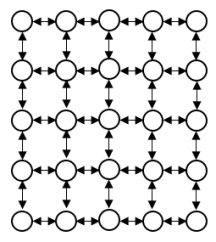

3.2 ground distance

In this section, we specialize our approach to deal with the ground distance. If , where , we consider the graph (see Fig. 2)

Also in this case it is easy to see that and the number of edges in is again , more precisely .

Proposition 3.2.

One has and hence . In particular,

for every couple of probability measures and on .

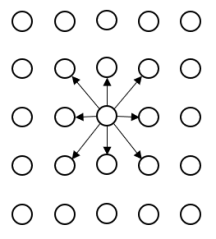

3.3 ground distance

Here we face the challenging problem of efficiently computing the Wasserstein distance of order 1 between 2D-histograms using the euclidean norm as ground distance. Let us consider , where

In order to build a suitable subgraph of , we further consider the vertices sets defined above. For , we define the graph

| (15) |

(we say that is the graph induced by ). See Fig. 3.

Our results concerning the ground distance are the following: in Proposition 3.3 we show that when (i.e., the induced subgraph is ) the approximation error is zero. Again, this means that one can compute by solving a minimum cost flow problem on a graph which is strictly contained in the complete graph . Unfortunately, in this case, the number of required edges is of order (Proposition 3.3). To conclude, in Theorem 3.4, we provide a sharp estimate on the error due to the approximation of with , for .

Proposition 3.3.

With the previous notation, if , then , hence and

for every couple of probability measures on . Moreover, if denotes the set of edges of , then

The next result, in combination with Eq. 14, shows that one can approximate the true value by computing with and obtain an explicit bound on the relative error.

Theorem 3.4.

Let , then for every

| (16) |

where and is monotone decreasing. Asymptotically,

| (17) |

3.4 Proofs of Section 3.3

Define the set

By restricting to , we consider only directions characterized by angles ranging between and ; all other directions may be obtained from by rotations of , for . To every element we associate the slope

The collection of these slopes, for , forms the so-called Farey sequence , see e.g. Section 4.5 in [21] or Chapter 6 in [33]. For example, for , we have

Since the elements in are pairwise coprime, the mapping

is one-to-one, i.e., there is a bijection between and . We will therefore use some known properties of the Farey sequence to prove an estimate on the graph induced by . Before proving Proposition 3.3, we need the following remark.

Lemma 3.5.

Each point in the square lattice can be written as

where is an integer and is in .

Proof 3.6.

Let . By definition of , . If and are coprime, then (i.e., we can choose , ). If they are not coprime, then there exists and such that .

We will also use known results on the asymptotic density of coprime numbers. Given a compact convex set D in containing the origin, the number of primitive lattice points in the “blow up” set , i.e. the number of coprime numbers in , diverges as goes to as , where is the area of . Under suitable regularity assumptions on , one can derive precise estimates on the remainder, see e.g. [24].

Lemma 3.7.

Let be the set of squares in containing with side of length 1. For any and set . Then, there is a constant such that for every

Proof 3.8.

One can write where

Set also . Combining these definitions with well-known properties of the Möbius function , one can prove that

See e.g. [24] or Lemma 4 in [50]. Since is a square of length containing the origin, then whenever . Moreover,

Combining these facts,

where, recalling also that ,

To conclude recall that to write, for ,

Proof 3.9.

(Proof of Proposition 3.3) Let us start by proving that

By definition Eq. 15,

Given , an admissible path connecting to in is a collection of edges , such that , , and . The length of a path is the sum of the lengths of its edges, that is

We denote by the set of all admissible paths connecting to . We want to prove that

that is, according to definition Eq. 13, that for every there exists such that . Let , since

then the vertex belongs to . By Lemma Lemma 3.5 there exists such that (the coordinates in are not restricted to positive integers). Choosing as admissible path

we compute

Since for all , we proved . Now we prove the second part of the statement. Let . The number of coprime integers in is , moreover , where belongs to . Hence, using Lemma 3.7,

with for every and . Hence,

and

so that

In order to prove Theorem 3.4 we need some preliminary results. Let and be two vectors in with . We say that and are adjacent if

We say that a vertex lies inside the convex cone defined by and if

| (18) |

Lemma 3.10.

Let . Given two adjacent vectors and in and a vector in that lies inside the convex cone defined by and , there are non-negative integers and such that

Proof 3.11.

Let . Since and are consecutive in the Farey set , by [33, Thm. 6.1] we have

| (19) |

The equation of the line that is parallel to and passes through is

The point where intersects is

Let . By Eq. 18 and Eq. 19 is integer and nonnegative. In the same way, the intersection between the line that is parallel to and passes by , and the line , is a point

We conclude that , with .

Lemma 3.12.

Let be fixed. Let

for . Then

| (20) |

Proof 3.13.

A straightforward computation shows that

Since , we conclude that is monotone increasing.

Proof 3.14.

(Proof of Theorem 3.4) In order to prove the upper bound in Eq. 16, we first draw an estimate on a continuous approximation of . Let

and

A straightforward computation shows

where . For fixed ,

| the mapping is a monotone increasing function |

and, since , one immediately gets the bound

On the other hand, for fixed we consider

Since

the line is a set of stationary points for . Setting , ,

we see that is the set of global minimum points for and thus for the mapping , with

| (21) |

For , denote , indexed in increasing slope order (i.e., so that ), and let be the angle between and . By Lemma 3.10 for all there exist two adjacent vectors and two integers such that , and therefore, by Eq. 21

| (22) |

We estimate

| (23) |

Let

Clearly , since the slopes include all elements in the Farey sequences . Define the sets of angles

Since the partitioning of induced by is finer than that of

Since the cosine function is monotone decreasing in , from Eq. 23 we obtain

which thus implies

The upper bound in Eq. 16 then follows by a simple algebraic manipulation, setting

In order to find the lower bound in Eq. 16, by Proposition 4.5, it is enough to evaluate the error for a specific choice of . We choose as a unit mass concentrated in , as a unit mass concentrated in , under the assumption that . A simple computation yields

and therefore

Finally, in order to estimate the asymptotic behaviour in Eq. 17, we compute the power expansions

Since the expansions are identical up to the term, owing to Eq. 16, we conclude Eq. 17.

4 Minimum flow on reduced graphs: general theory

In this section we give all the details of the results presented in Section 2.3-Section 2.5.

4.1 Dual formulation of a minimum flow problem

In what follows we need some basic results on the dual formulation of the minimum flow problem Eq. 8. Letting

the dual problem corresponding to Eq. 8 is

The Strong Duality theorem (see e.g. Thm. 9.6 in [1]) states that

Moreover, the so-called Complementary Slackness Optimality Conditions ensure that if a -flow is optimal for , then there exists a potential in such that whenever . Conversely, if is a -flow and there is a potential in such that whenever , and that if , then and are optimal solutions for the primal/dual problem. See e.g. Theorems 9.4 and 9.8 in [1].

4.2 Flows on Reduced Graphs

Assuming that , in place of considering the flow problem on a graph with nodes , we start by considering a flow problem for on the “reduced” set of nodes . Assuming that and for all , the set of nodes in this problem has cardinality while in has cardinality , where . For the reduced graph with nodes set , we choose, as a set of edges, the set of all possible directed links on , that is , being the complete (directed) graph on (without self-loops). Although this choice still considers a large number of edges (more precisely ) it will be useful in the sequel.

The next proposition summarizes some simple relations between the above defined problems.

Proposition 4.1.

Let and be two probability vectors on and .

-

(a)

If for every , then

-

(b)

If, in addition, for every in , then

In order to prove (a) and (b), we introduce an auxiliary bipartite graph with set of nodes , where and , and set of edges . Denoting by the bipartite graph , the corresponding minimum cost flow problem can be rewritten as

The cardinality of is , where is the fraction of vertexes with , respectively, hence , while the set of edges has cardinality .

The next Lemma specifies the relations between , the minimum of the cost flow problem , and the inf of Kantorovich’s transportation problem .

Lemma 4.2.

Let be any function.

-

(i)

If for every , then and, for ,

-

(ii)

If, in addition, for every in , then

Proof 4.3.

(i) Since , Eq. 9 implies that . If with , set

and, if and ,

Finally, define in all the remaining cases. It is easy to check that such a belongs to and again the inequality follows.

(ii) Let be an optimal -flow for . For in and in let be the set of directed paths in from to with no loops; for any in of length let be the flow through from to . The total flow from to can then be defined by

Doing this for any in , it is easy to see that the resulting is a -flow in . By the Complementary Slackness Conditions, since is an optimal -flow for , then there is in such that whenever . Now let in and in and in with . Since it must be that for , it follows that . Hence,

where the last inequality follows by triangle inequality. Summarizing, we have proved that if . Conversely, if , then necessarily . Since clearly belongs to , then and are optimal primal/dual solutions for by the Slackness Conditions. Using the Strong Duality theorem we conclude that .

Proof 4.4.

(Proof of Proposition 4.1.) (a) In order to prove that , note that if then for belongs to for . Since the inequality follows.

The previous result shows that one can compute the EMD between two normalized measures and (with respect to some ground distance ) by solving the minimum cost flow problem .

Although is smaller than , the problem of determining is computationally demanding for relatively small . Using the previous considerations on the computational cost of a minimum flow problem, it is easy to see that the time complexity of computing is and hence it is of the same order of the complexity of computing .

4.3 Error Bounds

In this Section we prove the universal upper bound Eq. 14, i.e. a bound on which depends only on the geometry of and not on the specific .

First of all, note that if is a distance, then (defined in Eq. 13) is a distance, and, since ,

| (26) |

Denote by any optimal path in connecting to , that is, any path such that

for any path in from to . Then

Note that clearly need not be unique. The constant

provides the bound we are looking for.

Proposition 4.5.

If is a distance, then for every

Proof 4.6.

Clearly, it suffices to prove that , i.e.,

First of all, we notice that by definition of

and therefore

| (27) |

Let be the set of edges of , for every , let be an optimal path (with no loops) in . Now let , then

where we used also Eq. 27 and that, by Eq. 26, . Letting

one can rewrite the previous inequality as

To conclude, one checks that belongs to , and hence

5 Numerical experiments

In this section, we report the results of our numerical experiments. The goal of our experiments is to address the following research questions:

-

1.

Which is the most efficient Minimum Cost Flow algorithm from those available in the literature, considering that our instances of optimal transport have a specific geometric cost function?

-

2.

How fast can we exactly compute the Wasserstein distance of order 1 as a function of the ground distance and as a function of the 2D histogram size?

-

3.

How tight is in practice the bound given in Theorem 3.4 as a function of the parameter ?

-

4.

How does our approach compare with other state-of-the-art algorithms?

In order to answer these questions we have run several experiments using the Discrete Optimal Transport Benchmark (DOTmark) [41], which has 10 classes of grey scale images related to randomly generated images, classical images, and real data from microscopy images of mitochondria. In each class there are 10 different grey scale images. Every image is given at the following pixel resolutions: , , , , and . Table 1 show the Classical and the Microscopy images, respectively.

Implementation details

We run our experiments using the Network Simplex as implemented in the Lemon C++ graph library111http://lemon.cs.elte.hu (last visited on May, 2nd, 2019). The tests were executed on a Dell workstation equipped with an Intel Xeon W-2155 CPU working at 3.3 GHz and with 32 GB of RAM. All the code was compiled with the Microsoft Visual Studio 2017 compiler. Our C++ code is freely available at https://github.com/stegua/dotlib.

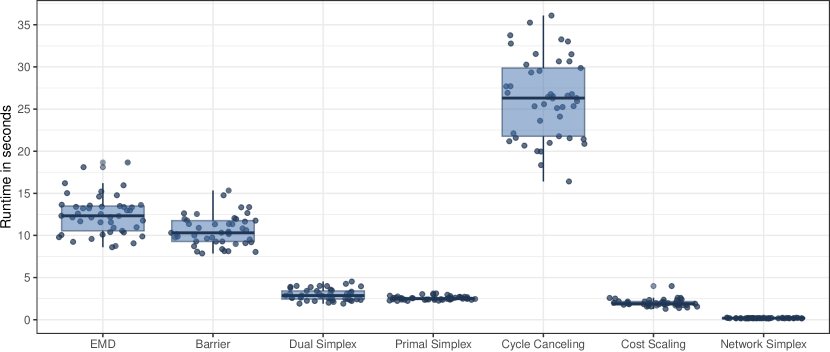

5.1 Comparison of Minimum Cost Flow Algorithms

As a first step, we run a set of experiments to select the fastest min cost flow algorithm for our geometric optimal transportation instances. We considered the following codes:

- 1.

-

2.

We test three different linear programming algorithms implemented in the commercial solver Gurobi v8.1: Primal Simplex, Dual Simplex, and Barrier. The barrier algorithm is the only parallel algorithms able to exploit the 10 physical cores of our CPU.

-

3.

We test three implementations of Minimum Cost Flow algorithms implemented in the Lemon Graph Library, corresponding to three different combinatorial algorithms: Cycle Cancelling [20], Cost Scaling [19, 10], and the Network Simplex [15]. For a deeper and more general comparison with other implementations among combinatorial algorithms, we refer to [27].

Figure 4 shows the results of our numerical tests. For each method, we compute the distance between any pair of images belonging the the Classic class (see Figure 1), with size , for a total of 45 problem instances. As ground distance, we use the Euclidean distance, and we solve the corresponding problem defined on a complete bipartite graph, that is the formulation used by the EMD algorithm.

The Network Simplex as implemented in the Lemon Graph library is clearly the fastest exact algorithm, and is able to solve every instance within a small fraction of a second. For this reason, in all our other numerical tests, we use that implementation.

5.2 Exact distance computations

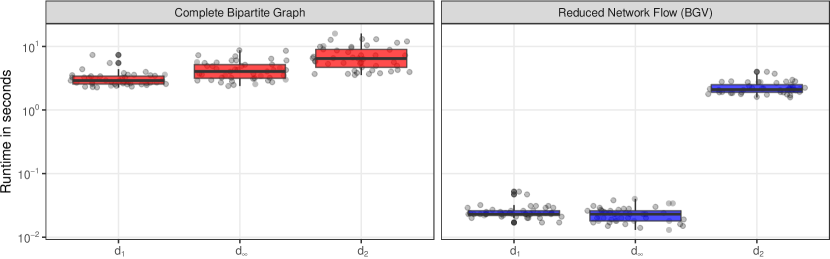

As second step, we have compared the running times of the flow models proposed in this paper computing the exact Wasserstein distance of order 1 using the , and ground distances.

First, we compare the running times for solving the models proposed in Section 3, with the running times of solving the equivalent problems formulated on bipartite graphs. Both type of problems are solved with the very efficient implementation of the Network Simplex algorithm provided by the Lemon Graph library. Figure 5 shows the boxplots that summarize our results on the classical images of size . While the bipartite graphs are all of the same size, the problems defined with the distance seem to be simpler, and those with the distance look slightly harder. By using our reduced network flow models, we get a speedup of two orders of magnitude for and : this is due to the significant reduction of the number of arcs. We recall that the bipartite graphs have arcs, where , while our equivalent models have only arcs. However, for the distance, the speedup is still present but more modest. In this case, our models have arcs, against the of the bipartite graphs. In order to get obtain a more significant speedup while controlling the error for the distance, we have numerically evaluated our approximation scheme, as discussed in the next subsection.

Once we have completely abandoned the bipartite model, we have run a large set of tests using images of size up to with the three different types of ground distances. Table 2 shows aggregate data elaborated from our results. For each combination of image size and ground distance, the table gives the size of the flow network in terms of number of nodes and number of arcs . Regarding the running times (in seconds), the same table reports the average, the standard deviation, and the maximum runtime over 450 tests (45 for each of the 10 class of images).

From Table 2, it is clear that the true challenge is to compute the Wasserstein distances using the ground distance, since with the and ground distances we can solve all the images in at most 1000 seconds (though, in average, it takes 2 or 3 minutes), while with the ground distance we cannot even solve the instances of size , since the code runs out of memory.

| Image size | Graph size | Ground | Running times (sec) | |||

|---|---|---|---|---|---|---|

| distance | Average | StdDev | Maximum | |||

| 1 024 | 3 968 | 0.002 | 0.001 | 0.009 | ||

| 7 812 | 0.002 | 0.001 | 0.009 | |||

| 638 692 | 0.075 | 0.016 | 0.154 | |||

| 4 096 | 16 128 | 0.023 | 0.008 | 0.059 | ||

| 32 004 | 0.024 | 0.006 | 0.053 | |||

| 10 205 236 | 2.011 | 0.573 | 4.401 | |||

| 16 384 | 65 024 | 0.35 | 0.13 | 0.82 | ||

| 129 540 | 0.32 | 0.08 | 0.63 | |||

| 163 207 372 | 57.73 | 20.17 | 146.33 | |||

| 65 536 | 261 120 | 6.7 | 3.0 | 23.7 | ||

| 521 220 | 5.5 | 1.7 | 12.9 | |||

| out of memory | - | - | - | |||

| 262 144 | 1 046 528 | 182.4 | 100.5 | 1056.5 | ||

| 2 091 012 | 139.6 | 58.3 | 405.0 | |||

| out of memory | - | - | - | |||

5.3 Approximation error : Theory vs. Practice

In this section, we present the numerical results on the error obtained in practice when we compute the Wasserstein distance of order 1 with our approximation scheme. The results are presented for the images of size , and , for which we can compute both the exact distance using and the approximate distance using , with ranging in the set .

We measure the relative percentage error, denoted by , as the following ratio:

where is equal to the optimal Wasserstein distance, and is the value of our approximation obtained by solving the uncapacitated min cost flow problem on the network built according to the parameter . Our goal is to compare the values of with the upper bound predicted by Theorem 3.4, that is

Table 3 reports the results for the images of size , and . The columns specify, in order, the image size, the value of the parameter , the cardinality of the arc set , the average runtime in seconds, the upper bound guaranteed by Theorem 3.4, the empirical average of the errors obtained in practice, and the maximum of such errors. Note that while from Theorem 3.4 in order to get an error smaller than we should use at least , in practice, we get on average such small errors already by using . Indeed, we can set the value of parameter in such a way to achieve the desired trade off between numerical precision in computing the Wasserstein distances and the running time we accept to wait. Table 4 details the maximum error obtained for each class of images. This shows that in practice a better trade off between the numerical precision of the distance and the running time can be obtained by considering the type of 2D histograms of interest.

| Size | Parameter | Runtime | mean | |||

|---|---|---|---|---|---|---|

| 257 556 | 0.446 | 2.675% | 1.291% | 2.646% | ||

| 510 556 | 0.748 | 1.291% | 0.463% | 1.153% | ||

| 1 254 508 | 1.153 | 0.486% | 0.121% | 0.447% | ||

| 16 117 244 | 2.424 | 0.124% | 0.019% | 0.109% | ||

| (exact) | 163 207 372 | 57.729 |

| Maximum Bound percentage error | ||||

|---|---|---|---|---|

| Class | L=2 | L=3 | L=5 | L=10 |

| CauchyDensity | 2.576% | 1.147% | 0.447% | 0.109% |

| ClassicImages | 1.813% | 0.716% | 0.246% | 0.053% |

| GRFmoderate | 2.365% | 0.937% | 0.348% | 0.065% |

| GRFrough | 1.918% | 0.780% | 0.279% | 0.039% |

| GRFsmooth | 2.248% | 1.069% | 0.338% | 0.068% |

| LogGRF | 2.546% | 1.019% | 0.370% | 0.076% |

| LogitGRF | 2.332% | 1.104% | 0.258% | 0.067% |

| MicroscopyImages | 2.069% | 0.900% | 0.272% | 0.045% |

| Shapes | 2.670% | 1.168% | 0.317% | 0.094% |

| WhiteNoise | 0.908% | 0.243% | 0.043% | 0.005% |

| 2.675% | 1.168% | 0.447% | 0.109% | |

Motivated by the results shown in Table 3, we measured how our approximation scheme scales for increasing image sizes, using and by restricting our test to the Cauchy images, since they are those with the larger error for and . For each combination of image size and value of , Table 5 reports the graph size and the basic statistics on the running time along the same line of the previous tables: average running time along with the respective standard deviations, and maximum running times.

| Image size | Param | Graph size | Running times (sec) | |||

|---|---|---|---|---|---|---|

| Average | StdDev | Maximum | ||||

| 2 | 65 536 | 1 039 380 | 8.6 | 2.5 | 14.8 | |

| 3 | 2 069 596 | 8.7 | 2.7 | 20.9 | ||

| 5 | 5 129 836 | 12.9 | 1.3 | 16.8 | ||

| 10 | 16 117 244 | 24.6 | 4.7 | 35.3 | ||

| 2 | 262 144 | 4 175 892 | 170.8 | 97.2 | 487.5 | |

| 3 | 8 333 404 | 148.0 | 70.6 | 361.6 | ||

| 5 | 20 744 812 | 171.9 | 29.7 | 236.3 | ||

| 10 | 65 782 268 | 471.5 | 139.4 | 950.6 | ||

5.4 Comparison with other approaches

We compare our solution method with other two approaches: the first is the algorithm proposed in [29] for the special case using the Manhattan as ground distance. The second approach is the (heuristic, with no guarantees) improved Sinkhorn’s algorithm [13] as implemented in [40].

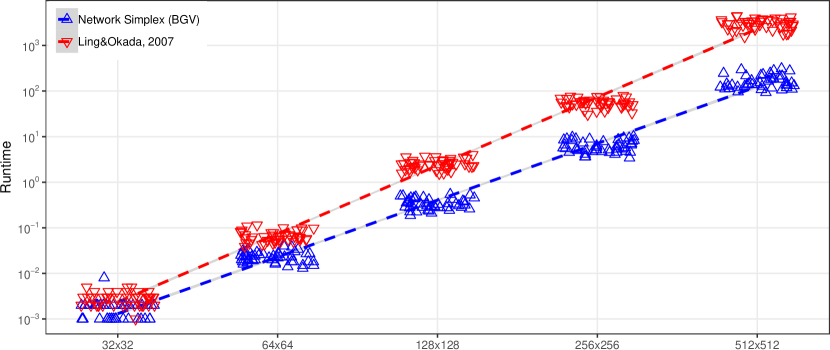

Manhattan ground distance [29]

Figure 6 shows the comparison of running time in seconds of our method with the algorithm proposed in [29]. The results refer to the running time for computing the distances between the 45 possible pairs of classical images, at resolution ranging from up to . Since both methods are exact, the distance value is always the same (indeed, it is the optimum). Note that apart from the very small case of size , our approach is always faster, with the difference increasing for the larger dimensions. While the two methods are using the same network flow model, they are using different solution algorithms: from these results, we can conclude that the Network Simplex implemented in [27] is faster than the implementation of combinatorial algorithm provided by the authors of [29], despite the fact that it has a lower worst-case time complexity.

Sinkhorn’s algorithm [40]

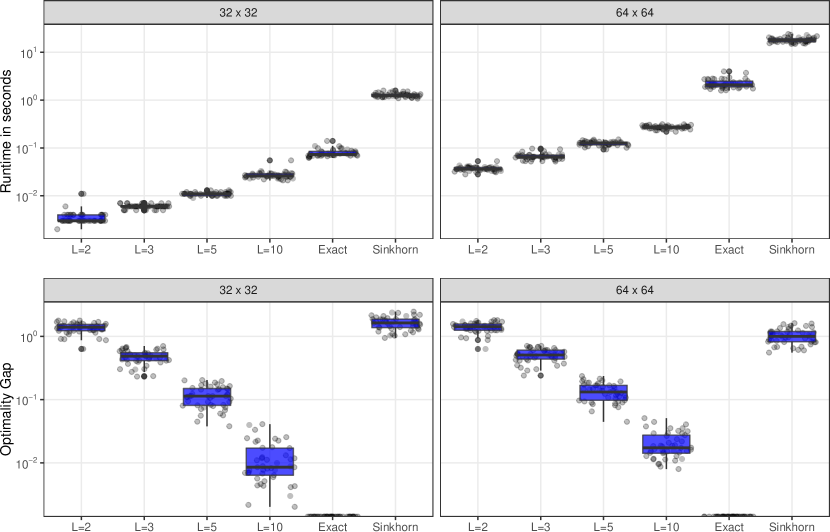

Figure 5 shows the result of comparing the stabilized Sinkhorn’s algorithm described in [40], with our approximation scheme for the Euclidean ground distance described in Section 3. We remark that the Sinkhorn’s algorithm, differently from our approach, is a heuristic method and it does not have any guarantee on the optimality gap of the solution it computes. The results refer to the classical images of size , , and . The exact solutions are computed using our approximation scheme with . For our approximation approach, we used the values . As expected, the running time grows with increasing values of and with increasing size of the images (note the log scale on the vertical axis). Our approach, is not only always faster, but, given the same value of empirical optimality gap, it can be two orders of magnitude faster. In addition, we remark that the Network Simplex runs in a single thread, while the implementation of the Sinkhorn’s algorithm we use runs in parallel on 20 threads.

6 Conclusion

Comparing two histograms, or establishing which histograms, in a given set, are more alike, is the crucial question in a number of applications with industrial and scientific scope. The staggering availability of data coming, e.g., from the Internet or from biological sampling and imaging, is undoubtedly encouraging the digitalization of data measures (e.g., images), while, at the same time, requiring a computational effort that, as of today, may not be within reach of modern workstations.

Motivated by these considerations, in this article we have addressed the problem of rapidly computing the Kantorovich distance (also known as Wasserstein distance of order 1) between 2D histograms. In our approach, we translate the original discrete optimal transportation problem Eq. 1 to an uncapacitated minimum cost flow problem on a directed graph Eq. 7. In Section 4 we prove that the two problems are equivalent when the Kantorovich cost is a distance.

The key observation is that, by reducing the size of the graph in the minimum cost flow, one can approximate the Kantorovich solution at a lower computational cost. Precisely, when the cost is the taxicab or the maximum distance, we are able to compute the optimal solution on a reduced flow network of size , where is number of pixels in the images, i.e., bins of a histogram. When the cost is the Euclidean distance, the size of the network that yields the exact optimal solution is . Our main contribution, in the Euclidean distance case, is that for any given error we can provide a reduced network of size that yields an approximate solution, which is at most away from the exact one. With our approximation method we were able to compute the distance between images, with an error lower than 0.12%, in less than 20 minutes.

Acknowledgments

This research was partially supported by the Italian Ministry of Education, University and Research (MIUR): Dipartimenti di Eccellenza Program (2018–2022) - Dept. of Mathematics “F. Casorati”, University of Pavia.

We are deeply indebted to Giuseppe Savaré, for introducing us to optimal transportation and for many stimulating discussions and suggestions. We thanks Rico Zenklusen for a useful discussion concerning the proof of Proposition 6. We thank Bernhard Schmitzer for suggesting the best parameters for his code.

References

- [1] R. K. Ahuja, T. L. Magnanti, and J. B. Orlin, Network flows: Theory, Algorithms, and Applications, Cambridge, Mass.: Alfred P. Sloan School of Management, Massachusetts Institute of Technology, 1988.

- [2] J. Altschuler, J. Weed, and P. Rigollet, Near-linear time approximation algorithms for optimal transport via Sinkhorn iteration, in Advances in Neural Inf. Process. Ser., 2017, pp. 1961–1971.

- [3] L. Ambrosio, N. Gigli, and G. Savaré, Gradient flows: in metric spaces and in the space of probability measures, Springer Science & Business Media, 2008.

- [4] M. Arjovsky, S. Chintala, and L. Bottou, Wasserstein GAN, arXiv preprint arXiv:1701.07875, (2017).

- [5] M. L. Balinski and F. J. Rispoli, Signature classes of transportation polytopes, Math. Program., 60 (1993), pp. 127–144.

- [6] F. Bassetti, A. Bodini, and E. Regazzini, On minimum Kantorovich distance estimators, Statist. Probab. Lett., 76 (2006), pp. 1298–1302.

- [7] F. Bassetti and E. Regazzini, Asymptotic properties and robustness of minimum dissimilarity estimators of location-scale parameters, Theory Probab. Appl., 50 (2006), pp. 171–186.

- [8] T. Bernas, E. K. Asem, J. P. Robinson, and B. Rajwa, Quadratic form: a robust metric for quantitative comparison of flow cytometric histograms, Cytometry Part A, 73 (2008), pp. 715–726.

- [9] S. Borgwardt, J. De Loera, and E. Finhold, The diameters of network-flow polytopes satisfy the Hirsch conjecture, Math. Program., (2017), pp. 1–27.

- [10] U. Bünnagel, B. Korte, and J. Vygen, Efficient implementation of the Goldberg–Tarjan minimum-cost flow algorithm, Optim. Methods Softw., 10 (1998), pp. 157–174.

- [11] L. Chizat, G. Peyré, B. Schmitzer, and F.-X. Vialard, Scaling algorithms for unbalanced optimal transport problems, Math. Comp., 87 (2018), pp. 2563–2609.

- [12] N. Courty, R. Flamary, D. Tuia, and A. Rakotomamonjy, Optimal transport for domain adaptation, IEEE Trans. on Pattern Analysis and Mach. Intell., 39 (2017), pp. 1853–1865.

- [13] M. Cuturi, Sinkhorn distances: Lightspeed computation of optimal transport, in Advances in †Neural Inf. Process. Ser., 2013, pp. 2292–2300.

- [14] M. Cuturi and A. Doucet, Fast computation of Wasserstein barycenters, in Intern. Conf. on Machine Learning, 2014, pp. 685–693.

- [15] G. Dantzig, Linear programming and extensions, Princeton university press, 2016.

- [16] E. W. Dijkstra, A note on two problems in connexion with graphs, Numer. Math., 1 (1959), pp. 269–271.

- [17] M. M. Flood, On the Hitchcock distribution problem, Pacific Journal of Mathematics, 3 (1953), pp. 369–386.

- [18] C. Frogner, C. Zhang, H. Mobahi, M. Araya, and T. A. Poggio, Learning with a Wasserstein loss, in Advances in †Neural Inf. Process. Ser., 2015, pp. 2053–2061.

- [19] A. V. Goldberg, An efficient implementation of a scaling minimum-cost flow algorithm, Journal of algorithms, 22 (1997), pp. 1–29.

- [20] A. V. Goldberg and R. E. Tarjan, Finding minimum-cost circulations by canceling negative cycles, Journal of the ACM (JACM), 36 (1989), pp. 873–886.

- [21] R. L. Graham, D. E. Knuth, and O. Patashnik, Concrete mathematics: A foundation for computer science. 2nd, 1994.

- [22] F. S. Hillier and G. J. Lieberman, Introduction to Operations Research, McGraw-Hill Science, Engineering & Mathematics, 1995.

- [23] K. Holmberg and H. Tuy, A production-transportation problem with stochastic demand and concave production costs, Math. Program., 85 (1999), pp. 157–179.

- [24] M. N. Huxley and W. G. Nowak, Primitive lattice points in convex planar domains, Acta Arith., 76 (1996), pp. 271–283.

- [25] M. Kazhdan, P. Simari, T. McNutt, B. Wu, R. Jacques, M. Chuang, and R. Taylor, A shape relationship descriptor for radiation therapy planning, in Intern. Conf. on Medical Image Computing and Computer-Assisted Intervention, Springer, 2009, pp. 100–108.

- [26] B. Korte, J. Vygen, B. Korte, and J. Vygen, Combinatorial Optimization, (5th Edition) Springer, 2012.

- [27] P. Kovács, Minimum-cost flow algorithms: an experimental evaluation, Optim. Methods Softw., 30 (2015), pp. 94–127.

- [28] E. Levina and P. Bickel, The Earth Mover’s Distance is the Mallows distance: Some insights from statistics, in IEEE Intern. Conf. Computer Vision, vol. 2, IEEE, 2001, pp. 251–256.

- [29] H. Ling and K. Okada, An efficient Earth Mover’s Distance algorithm for robust histogram comparison, IEEE Transactions on Pattern Analysis and Mach. Intell., 29 (2007), pp. 840–853.

- [30] D. G. Lowe, Distinctive image features from scale-invariant keypoints, International journal of computer vision, 60 (2004), pp. 91–110.

- [31] G. Monge, Mémoire sur la théorie des déblais et des remblais, Histoire de l’Académie Royale des Sciences de Paris, (1781).

- [32] A. Munk and C. Czado, Nonparametric validation of similar distributions and assessment of goodness of fit, J. R. Stat. Soc. Ser. B. Stat. Methodol., 60 (1998), pp. 223–241.

- [33] I. Niven, H. S. Zuckerman, and H. L. Montgomery, An introduction to the theory of numbers, vol. 5, (5th Edition) Wiley New York, 1991.

- [34] J. B. Orlin, A faster strongly polynomial minimum cost flow algorithm, Oper. Res., 41 (1993), pp. 338–350.

- [35] D. Y. Orlova, N. Zimmerman, S. Meehan, C. Meehan, J. Waters, E. E. Ghosn, A. Filatenkov, G. A. Kolyagin, Y. Gernez, S. Tsuda, et al., Earth Mover’s Distance (EMD): a true metric for comparing biomarker expression levels in cell populations, PloS one, 11 (2016), pp. 1–14.

- [36] O. Pele and M. Werman, Fast and robust Earth Mover’s Distances, in IEEE Intern. Conf. Computer Vision, IEEE, 2009, pp. 460–467.

- [37] Y. Rubner, C. Tomasi, and L. J. Guibas, A metric for distributions with applications to image databases, in IEEE Intern. Conf. Computer Vision, IEEE, 1998, pp. 59–66.

- [38] Y. Rubner, C. Tomasi, and L. J. Guibas, The Earth Mover’s Distance as a metric for image retrieval, Int. J. Comput. Vis., 40 (2000), pp. 99–121.

- [39] F. Santambrogio, Optimal transport for applied mathematicians, Birkäuser, NY, (2015), pp. 99–102.

- [40] B. Schmitzer, Stabilized sparse scaling algorithms for entropy regularized transport problems, arXiv preprint arXiv:1610.06519, (2016).

- [41] J. Schrieber, D. Schuhmacher, and C. Gottschlich, Dotmark–a benchmark for discrete optimal transport, IEEE Access, 5 (2017), pp. 271–282.

- [42] A. Schrijver, On the history of the transportation and maximum flow problems, Math. Program., 91 (2002), pp. 437–445.

- [43] J. Solomon, Optimal transport on discrete domains, AMS Short Course on Discrete Differential Geometry, (2018), https://arxiv.org/abs/1801.07745.

- [44] J. Solomon, F. De Goes, G. Peyré, M. Cuturi, A. Butscher, A. Nguyen, T. Du, and L. Guibas, Convolutional Wasserstein distances: Efficient optimal transportation on geometric domains, ACM Transactions on Graphics (TOG), 34 (2015), p. 66.

- [45] J. Solomon, R. Rustamov, L. Guibas, and A. Butscher, Wasserstein propagation for semi-supervised learning, in Intern. Conf. on Machine Learning, 2014, pp. 306–314.

- [46] M. Sommerfeld and A. Munk, Inference for empirical Wasserstein distances on finite spaces, J. R. Stat. Soc. Ser. B. Stat. Methodol., 80 (2018), pp. 219–238.

- [47] H. Tuy, S. Ghannadan, A. Migdalas, and P. Värbrand, A strongly polynomial algorithm for a concave production-transportation problem with a fixed number of nonlinear variables, Math. Program., 72 (1996), pp. 229–258.

- [48] A. M. Vershik, Long history of the Monge-Kantorovich transportation problem, TMath. Intelligencer, 35 (2013), pp. 1–9.

- [49] C. Villani, Optimal transport: old and new, vol. 338, Springer Science & Business Media, 2008.

- [50] D. Zagier, On the number of Markoff numbers below a given bound, Math. Comp., 39 (1982), pp. 709–723.