Constant Regret, Generalized Mixability, and Mirror Descent

Abstract

We consider the setting of prediction with expert advice; a learner makes predictions by aggregating those of a group of experts. Under this setting, and for the right choice of loss function and “mixing” algorithm, it is possible for the learner to achieve a constant regret regardless of the number of prediction rounds. For example, a constant regret can be achieved for mixable losses using the aggregating algorithm. The Generalized Aggregating Algorithm (GAA) is a name for a family of algorithms parameterized by convex functions on simplices (entropies), which reduce to the aggregating algorithm when using the Shannon entropy . For a given entropy , losses for which a constant regret is possible using the GAA are called -mixable. Which losses are -mixable was previously left as an open question. We fully characterize -mixability and answer other open questions posed by [12]. We show that the Shannon entropy is fundamental in nature when it comes to mixability; any -mixable loss is necessarily -mixable, and the lowest worst-case regret of the GAA is achieved using the Shannon entropy. Finally, by leveraging the connection between the mirror descent algorithm and the update step of the GAA, we suggest a new adaptive generalized aggregating algorithm and analyze its performance in terms of the regret bound.

1 Introduction

Two fundamental problems in learning are how to aggregate information and under what circumstances can one learn fast. In this paper, we consider the problems jointly, extending the understanding and characterization of exponential mixing due to [19], who showed that not only does the “aggregating algorithm” learn quickly when the loss is suitably chosen, but that it is in fact a generalization of classical Bayesian updating, to which it reduces when the loss is log-loss [21]. We consider a general class of aggregating schemes, going beyond Vovk’s exponential mixing, and provide a complete characterization of the mixing behavior for general losses and general mixing schemes parameterized by an arbitrary entropy function.

In the game of prediction with expert advice a learner predicts the outcome of a random variable (outcome of the environment) by aggregating the predictions of a pool of experts. At the end of each prediction round, the outcome of the environment is announced and the learner and experts suffer losses based on their predictions. We are interested in algorithms that the learner can use to “aggregate” the experts’ predictions and minimize the regret at the end of the game. In this case, the regret is defined as the difference between the cumulative loss of the learner and that of the best expert in hindsight after rounds.

The Aggregating Algorithm (AA) [19] achieves a constant regret — a precise notion of fast learning — for mixable losses; that is, the regret is bounded from above by a constant which depends only on the loss function and not on the number of rounds . It is worth mentioning that mixability is a weaker condition than exp-concavity, and contrary to the latter, mixability is an intrinsic, parametrization-independent notion [9].

Reid et al. [12] introduced the Generalized Aggregating Algorithm (GAA), going beyond the AA. The GAA is parameterized by the choice of a convex function on the simplex (entropy) and reduces to the AA when is the Shannon entropy. The GAA can achieve a constant regret for losses satisfying a certain condition called -mixability (characterizing when losses are -mixable was left as an open problem). This regret depends jointly on the generalized mixability constant — essentially the largest such that is -mixable — and the divergence , where is a prior distribution over experts and is the th standard basis element of [12]. At each prediction round, the GAA can be divided into two steps; a substitution step where the learner picks a prediction from a set specified by the -mixability condition; and an update step where a new distribution over experts is computed depending on their performance. Interestingly, this update step is exactly the mirror descent algorithm [16, 11] which minimizes the weighted loss of experts.

Contributions.

We introduce the notion of a support loss; given a loss defined on any action space, there exists a proper loss which shares the same Bayes risk as . When a loss is mixable, one can essentially work with a proper (support) loss instead — this will be the first stepping stone towards a characterization of (generalized) mixability.

The notion of -mixable and the GAA were previously restricted to finite losses. We extend these to allow for the use of losses which can take infinite values (such as the -loss), and we show in this case that under the -mixability condition a constant regret is achievable using the GAA.

For an entropy and a loss , we derive a necessary and sufficient condition (Theorems 13 and 14) for to be -mixable. In particular, if and satisfy some regularity conditions, then is -mixable if and only if is convex on the simplex, where is the Shannon entropy and is essentially the largest such that is -mixable [19, 18]. This implies that a loss is -mixable only if it is -mixable for some . This, combined with the fact that -mixability is equivalently -mixability (Theorem 12), reflects one fundamental aspect of the Shannon entropy.

Then, we derive an explicit expression for the generalized mixability constant (Corollary 17), and thus for the regret bound of the GAA. This allows us to compare the regret bound of any entropy with that of the Shannon entropy . In this case, we show (Theorem 18) that ; that is, the GAA achieves the lowest worst-case regret when using the Shannon entropy — another result which reflects the fundamental nature of the Shannon entropy.

Finally, by leveraging the connection between the GAA and the mirror descent algorithm, we present a new algorithm — the Adaptive Generalized Aggregating Algorithm (AGAA). This algorithm consists of changing the entropy function at each prediction round similar to the adaptive mirror descent algorithm [16]. We analyze the performance of this algorithm in terms of its regret bound.

Layout.

In §2, we give some background on loss functions and present new results (Theorem 4 and 5) based on the new notion of a proper support loss; we show that, as far as mixability is concerned, one can always work with a proper (support) loss instead of the original loss (which can be defined on an arbitrary action space). In §3, we introduce the notions of classical and generalized mixability and derive a characterization of -mixability (Theorems 13 and 14). We then introduce our new algorithm — the AGAA — and analyze its performance. We conclude the paper by a general discussion and direction for future work. All proofs, except for that of Theorem 16, are deferred to Appendix C.

Notation.

Let . We denote and . We write for the standard inner product in Euclidean space. Let be the probability simplex in , and let . We will extensively make use of the affine map defined by

| (1) |

2 Loss Functions

In general, a loss function is a map where is an outcome set and is an action set. In this paper, we only consider the case , i.e. finite outcome space. Overloading notation slightly, we define the mapping by and denote . We further extend the new definition of to the set such that for and , . We define the effective domain of by , and the loss surface by . We say that is closed if is closed in . The superprediction set of is defined by . Let be its finite part.

Let . The prediction is said to be better than if the component-wise inequality holds and there exists some such that [23]. A loss is admissible if for any there are no better predictions.

For the rest of this paper (except for Theorem 4), we make the following assumption on losses;

Assumption 1.

is a closed, admissible loss such that .

It is clear that there is no loss of generality in considering only admissible losses. The condition that is closed is a weaker version of the more common assumption that is compact and that is continuous with respect to the extended topology of for all [8, 5]. In fact, we do not make any explicit topological assumptions on the set ( is allowed to be open in our case). Our condition simply says that if a sequence of points on the loss surface converges in , then there exists an action in whose image through the loss is equal to the limit. For example the 0-1 loss is closed, yet the map is not continuous on , for .

In this paragraph let be the -simplex, i.e. . We define the conditional risk by and the Bayes risk by . In this case, the loss is proper if for all in (and strictly proper if the inequality is strict). For example, the -loss is defined by , where the ‘’ of a vector applies component-wise. One can easily check that is strictly proper. We denote its Bayes risk.

The above definition of the Bayes risk is restricted to losses defined on the simplex. For a general loss , we use the following definition;

Definition 2 (Bayes Risk).

Let be a loss such that . The Bayes risk is defined by

| (3) |

The support function of a set is defined by , , and thus it is easy to see that one can express the Bayes risk as . Our definition of the Bayes risk is slightly different from previous ones ([8, 18, 5]) in two ways; 1) the Bayes risk is defined on all instead of ; and 2) the infimum is taken over the finite part of the superprediction set . The first point is a mere mathematical convenience and makes no practical difference since for all . For the second point, swapping for in (3) does not change the value of for mixable losses (see Appendix D). However, we chose to work with — a subset of — as it allows us to directly apply techniques from convex analysis.

Definition 3 (Support Loss).

We call a map a support loss of if

where (see (2)) is the sub-differential of the support function — — of the set .

Theorem 4.

Any loss such that , has a proper support loss with the same Bayes risk, , as .

Theorem 4 shows that regardless of the action space on which the loss is defined, there always exists a proper loss whose Bayes risk coincides with that of the original loss. This fact is useful in situations where the Bayes risk contains all the information one needs — such is the case for mixability. The next Theorem shows a stronger relationship between a loss and its corresponding support loss.

Theorem 5.

Let be a loss and be a proper support loss of . If the Bayes risk is differentiable on , then is uniquely defined on and

Theorem 5 shows that when the Bayes risk is differentiable (a necessary condition for mixability — Theorem 12), the support loss is almost a reparametrization of the original loss, and in practice, it is enough to work with support losses instead. This will be crucial for characterizing -mixability.

3 Mixability in the Game of Prediction with Expert Advice

We consider the setting of prediction with expert advice [19]; there a is pool of experts, parameterized by , which make predictions at each round . In the same round, the learner predicts , where , are outcomes of the environment, and is a merging strategy [18]. At the end of round , is announced and each expert [resp. learner] suffers a loss [resp. ], where . After rounds, the cumulative loss of each expert [resp. learner] is given by [resp. ]. We say that achieves a constant regret if . In what follows, this game setting will be referred to by and we only consider the case where .

3.1 The Aggregating Algorithm and -mixability

Definition 6 (-mixability).

For , a loss is said to be -mixable, if ,

| (4) |

where the applies component-wise. Letting , we define the mixability constant of by if ; and otherwise. is said to be mixable if .

If a loss is -mixable for , the AA (Algorithm 1) achieves a constant regret in the game[19]. In Algorithm 1, the map is a substitution function of the loss [19, 9]; that is, satisfies the component-wise inequality , for all .

It was shown by Chernov et al. [5] that the -mixability condition (4) is equivalent to the convexity of the -exponentiated superprediction set of defined by . Using this fact, van Erven et al. [18] showed that the mixability constant of a strictly proper loss , whose Bayes risk is twice continuously differentiable on , is equal to

| (5) |

where is the Hessian operator and ( was defined in (1)). The next theorem extends this result by showing that the mixability constant of any loss is lower bounded by in (5), as long as satisfies Assumption 1 and its Bayes risk is twice differentiable.

Theorem 7.

Let and be a loss. Suppose that and that is twice differentiable on . If then is -mixable. In particular, .

We later show that, under the same conditions as Theorem 7, we actually have (Theorem 16) which indicates that the Bayes risk contains all the information necessary to characterize mixability.

Remark 8.

In practice, the requirement ‘’ is not necessarily a strict restriction to finite losses; it is often the case that a loss only takes infinite values on the relative boundary of (such is the case for the -loss defined on the simplex), and thus the restriction , where , satisfies . It follows trivially from the definition of mixability (4) that if is -mixable and is continuous with respect to the extended topology of — a condition often satisfied — then is also -mixable.

3.2 The Generalized Aggregating Algorithm and mixability

A function is an entropy if it is convex, its epigraph is closed in , and . For example, the Shannon entropy is defined by if , and

| (6) |

The divergence generated by an entropy is the map defined by

| (9) |

where (the limit exists since is convex [14]).

Definition 9 (-mixability).

Let be an entropy. A loss is -mixable for if , , such that

| (10) |

When , we simply say that is -mixable and we denote . Letting , we define the generalized mixability constant of by , if ; and otherwise.

Reid et al. [12] introduced the GAA (see Algorithm 2) which uses an entropy function and a substitution function (see previous section) to specify the learner’s merging strategy . It was shown that the GAA reduces to the AA when is the Shannon entropy . It was also shown that under some regularity conditions on , the GAA achieves a constant regret in the game for any finite, -mixable loss.

Our definition of -mixability differs slightly from that of Reid et al. [12] — we use directional derivatives to define the divergence . This distinction makes it possible to extend the GAA to losses which can take infinite values (such as the -loss defined on the simplex). We show, in this case, that a constant regret is still achievable under the -mixability condition. Before presenting this result, we define the notion of -differentiability; for , let . We say that an entropy is -differentiable if , , the map is linear on .

Theorem 10.

Let be a -differentiable entropy. Let be a loss (not necessarily finite) such that is twice differentiable on . If is -mixable then the GAA achieves a constant regret in the game; for any sequence ,

| (11) |

for initial distribution over experts , where is the th basis element of , and any substitution function .

Looking at Algorithm 2, it is clear that the GAA is divided into two steps; 1) a substitution step which consists of finding a prediction satisfying the mixability condition (10) using a substitution function ; and 2) an update step where a new distribution over experts is computed. Except for the case of the AA with the -loss (which reduces to Bayesian updating [21]), there is not a unique choice of substitution function in general. An example of substitution function is the inverse loss [22]. Kamalaruban et al. [9] discuss other alternatives depending on the curvature of the Bayes risk. Although the choice of can affect the performance of the algorithm to some extent [9], the regret bound in (11) remains unchanged regardless of . On the other hand, the update step is well defined and corresponds to a mirror descent step [12] (we later use this fact to suggest a new algorithm).

We conclude this subsection with two new and important results which will lead to a characterization of -mixability. The first result shows that -mixability is equivalent to -mixability, and the second rules out losses and entropies for which -mixability is not possible.

Theorem 11.

Let . A loss is -mixable if and only if is -mixable.

Proposition 12.

Let be an entropy and . If is -mixable, then the Bayes risk satisfies . If, additionally, is twice differentiable on , then must be strictly convex on .

3.3 A Characterization of -Mixability

In this subsection, we first show that given an entropy and a loss satisfying certain regularity conditions, is -mixable if and only if

| (12) |

Theorem 13.

Let , a -mixable loss, and an entropy. If is convex on , then is -mixable.

The converse of Theorem 13 also holds under additional smoothness conditions on and ;

Theorem 14.

Let be a loss such that is twice differentiable on , and an entropy such that is twice differentiable on . Then is -mixable only if is convex on .

As consequence of Theorem 14, if a loss is not classically mixable, i.e. , it cannot be -mixable for any entropy . This is because is not convex (where equality ‘*’ is due to Theorem 7).

We need one more result before arriving at (12); Recall that the mixability constant is defined as the supremum of the set { is -mixable}. The next lemma essentially gives a sufficient condition for this supremum to be attained when is non-empty — in this case, is -mixable.

Lemma 15.

Let be a loss. If , then either or .

Theorem 16.

Let and be as in Theorem 14 with . Then . Furthermore, is -mixable if and only if is convex on .

Proof.

Note that the condition ‘’ is in practice not a restriction to finite losses — see Remark 8. Theorem 16 implies that under the regularity conditions of Theorem 14, the Bayes risk [resp. ] contains all necessary information to characterize classical [resp. generalized] mixability.

Corollary 17 (The Generalized Mixability Constant).

3.4 The (In)dependence Between and and the Fundamental Nature of

So far, we showed that the -mixability of losses satisfying Assumption 1 is characterized by the convexity of , where (see Theorems 13 and 14). As a result, and contrary to what was conjectured previously [12], the generalized mixability condition does not induce a correspondence between losses and entropies; for a given loss , there is no particular entropy — specific to the choice of — which minimizes the regret of the GAA. Rather, the Shannon entropy minimizes the regret regardless of the choice of (see Theorem 18 below). This reflects one fundamental aspect of the Shannon entropy.

Nevertheless, given a loss and entropy , the curvature of the loss surface determines the maximum ‘learning rate’ of the GAA; the curvature of is linked to through the Hessian of the Bayes risk (see Theorem 49 in Appendix H.2), which is in turn linked to through (13).

Given a loss , we now use the expression of in (13) to explicitly compare the regret bounds and achieved with the GAA (see (11)) using entropy and the Shannon entropy , respectively.

Theorem 18.

Let , where is the Shannon entropy and is an entropy such that is twice differentiable on . A loss with twice differentiable on , is -mixable only if .

4 Adaptive Generalized Aggregating Algorithm

In this section, we take advantage of the similarity between the GAA’s update step and the mirror descent algorithm (see Appendix E) to devise a modification to the GAA leading to improved regret bounds in certain cases. The GAA can be modified in (at least) two immediate ways; 1) changing the learning rate at each time step to speed-up convergence; and 2) changing the entropy, i.e. the regularizer , at each time step — similar to the adaptive mirror descent algorithm [16, 11]. In the former case, one can use Corollary 17 to calculate the maximum ‘learning rate’ under the -mixability constraint. Here, we focus on the second method; changing the entropy at each round. Algorithm 3 displays the modified GAA — which we call the Adaptive Generalized Aggregating Algorithm (AGAA) — in its most general form. In Algorithm 3, is the entropic dual of .

Given a -mixable loss , we verify that Algorithm 3 is well defined; for simplicity, assume that and is twice differentiable on . From the definition of an entropy, on , and thus the entropic dual is defined and finite on all (in particular at ). On the other hand, from Proposition 12, is strictly convex on which implies that (and thus ) is differentiable on (see e.g. [7, Thm. E.4.1.1]). It remains to check that is -mixable. Since for , -mixability is equivalent to -mixability (by definition), Theorem 16 implies that is -mixable if and only if is convex on . This is in fact the case since is an affine transformation of , and we have assumed that is -mixable.

In what follows, we focus on a particular instantiation of Algorithm 3 where we choose , for some (arbitrary for now) . The vectors act as correction terms in the update step of the AGAA. Using standard duality properties (see Appendix A), it is easy to show that the AGAA reduces to the GAA except for the update step where the new distribution over experts at round is now given by

Theorem 19.

Let be a -differentiable entropy. Let be a loss such that is twice differentiable on . Let , where and . If is -mixable then for initial distribution and any sequence , the AGAA achieves the regret

| (14) |

where .

Theorem 19 implies that if the sequence is chosen such that is negative for the best expert (in hindsight), then the regret bound ‘’ of the AGAA is lower than that of the GAA (see (11)), and ultimately that of the AA (when ). Unfortunately, due to Vovk’s result [19, §5] there is no “universal” choice of which guarantees that is always negative. However, there are cases where this term is expected to be negative.

Consider a dataset where it is typical for the best experts (i.e., the ’s) to perform poorly at some point during the game, as measured by their average loss, for example. Under such an assumption, choosing the correction vectors to be negatively proportional to the average losses of experts, i.e. (for small enough ), would be consistent with the idea of making negative. To see this, suppose expert is performing poorly during the game (say at ), as measured by its instantaneous and average loss. At that point the distribution would put more weight on experts performing better than , i.e. having a lower average loss. And since is negatively proportional to the average loss of expert , the quantity would be negative — consistent with making . On the other hand, if expert performs well during the game (say close to the best) then , since would put comparable weights between and other experts (if any) with similar performance.

Example 1.

(A Negative Regret).

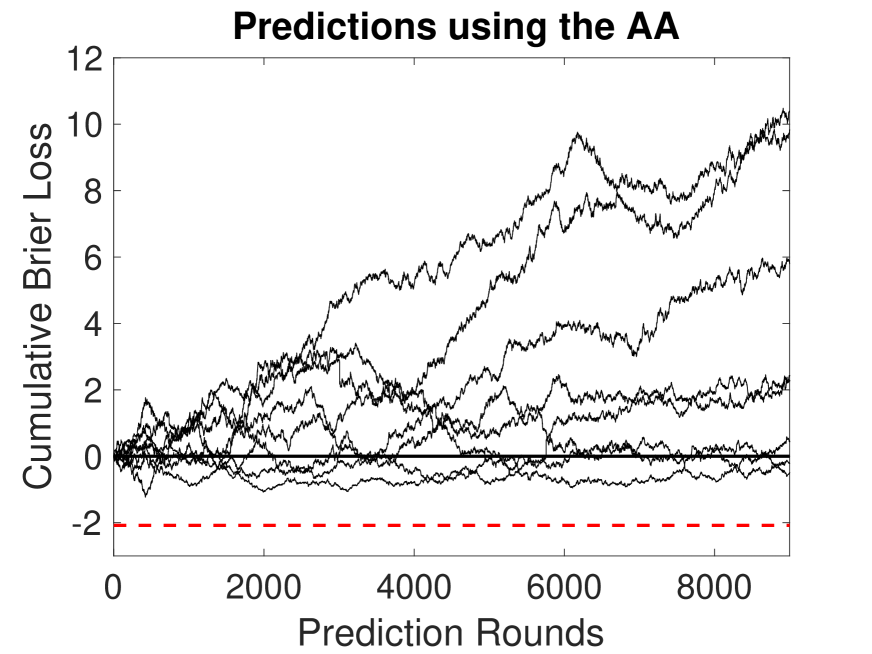

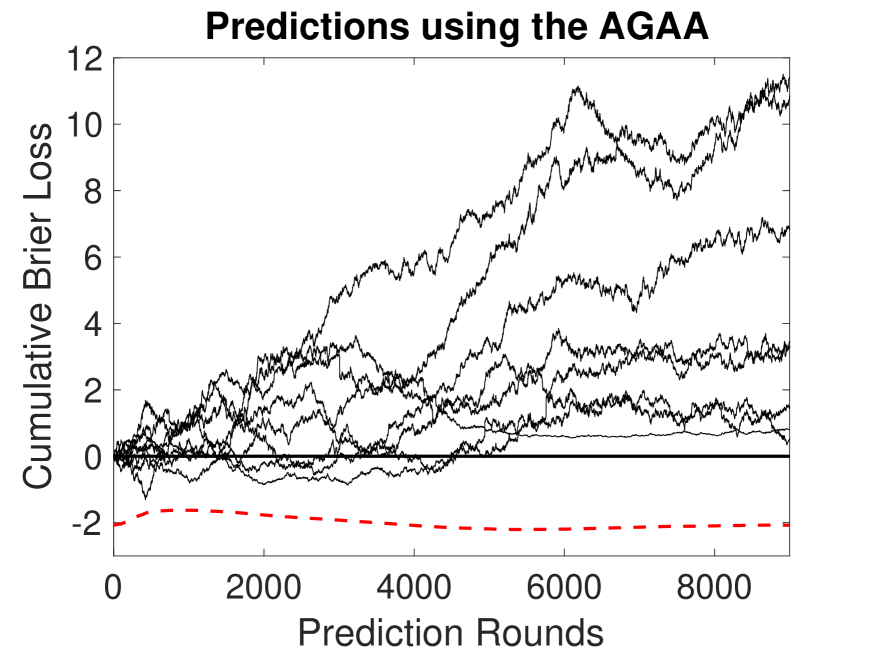

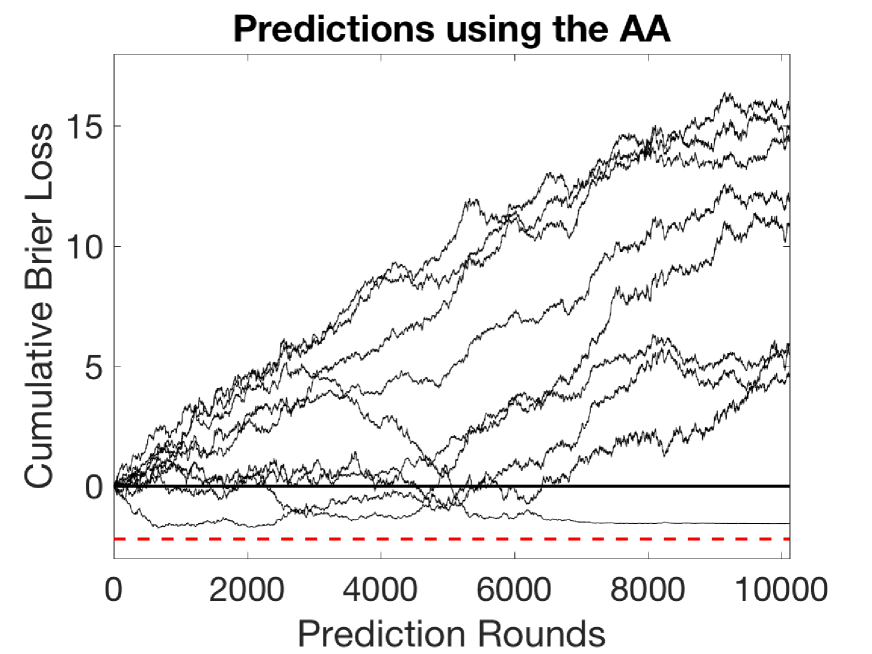

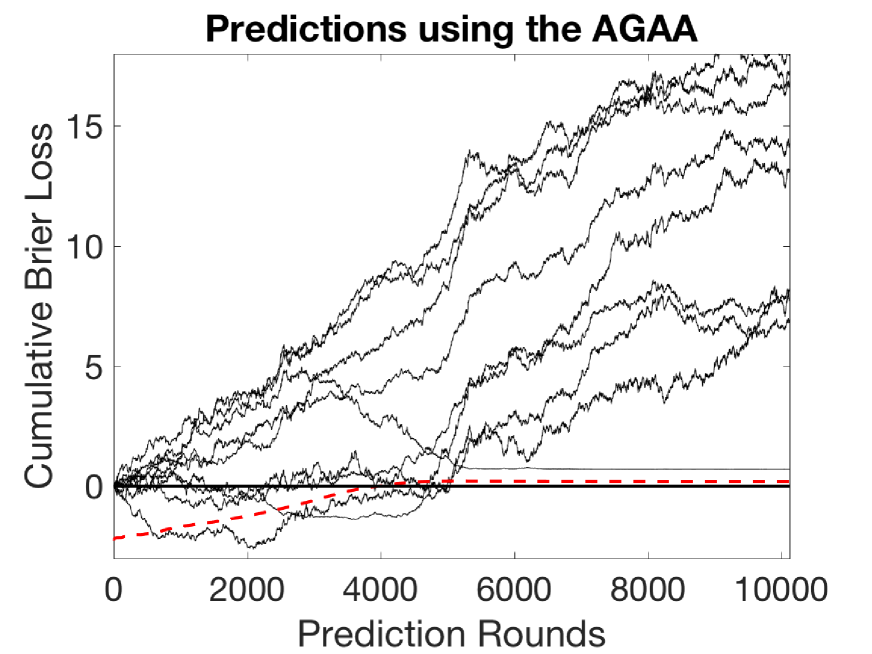

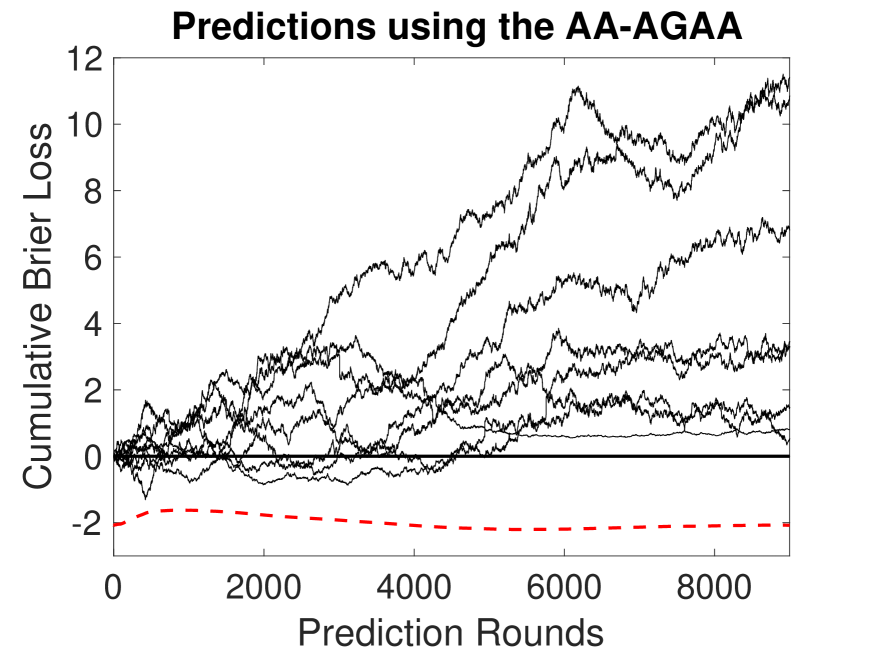

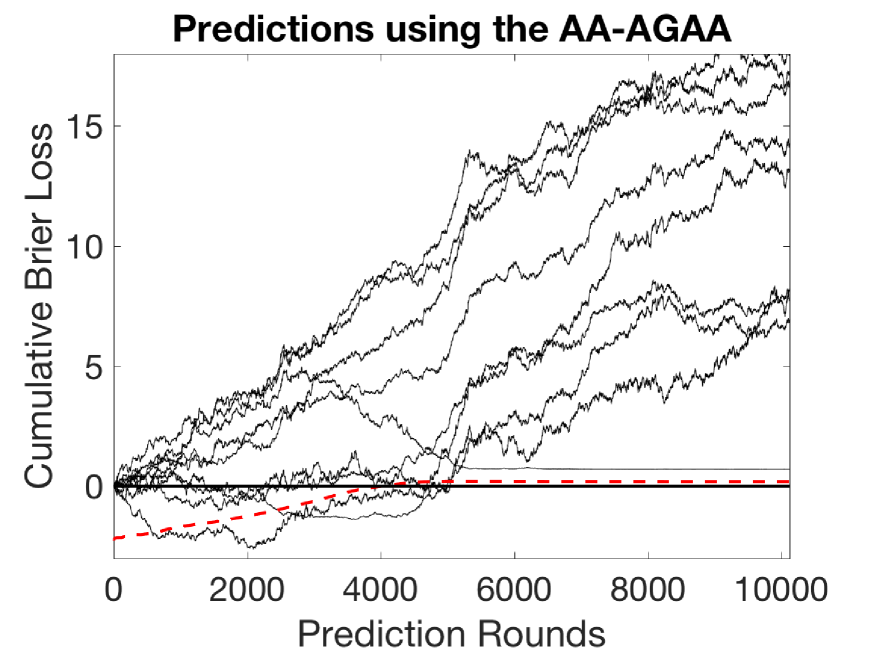

One can construct an example that illustrates the idea above. Consider the Brier game ; a probability game with 2 experts , 2 outcomes , and where the loss is the Brier loss [20] (which is -mixable). Assume that; expert consistently predicts ; expert predicts during the first rounds, then switches to predicting thereafter; the outcome is always . A straightforward simulation using the AGAA with the Shannon entropy, Vovk’s substitution function for the Brier loss [20], as in Theorem 19 with , yields , where in this case is the best expert for . The learner then does better than the best expert. If we use the AA instead, the learner does worse than by . ∎

In real data, the situation described above — where the best expert does not necessarily perform optimally during the game — is typical, especially when the number of rounds is large. We have tested the aggregating algorithms on real data as studied by Vovk [20]. We compared the performance of the AA with the AGAA, and found that the AGAA outperforms the AA, and in fact achieved a negative regret on two data sets. Details of the experiments are in Appendix J.

As pointed out earlier, there are situations where even for the choice of in Example 1, and this could potentially lead to a large positive regret for the AGAA. There is an easy way to remove this risk at a small price; the outputs of the AGAA and the AA can themselves be considered as expert predictions. These predictions can in turn be passed to a new instance of the AA to yield a meta prediction. The resulting worst case regret is guaranteed not to exceed that of the original AA instance by more than for an -mixable loss. We test this idea in Appendix J.

5 Discussion and Future Work

In this work, we derived a characterization of -mixability, which enables a better understanding of when a constant regret is achievable in the game of prediction with expert advice. Then, borrowing techniques from mirror descent, we proposed a new “adaptive” version of the generalized aggregating algorithm. We derived a regret bound for a specific instantiation of this algorithm and discussed certain situations where the algorithm is expected to perform well. We empirically demonstrated the performance of this algorithm on football game predictions (see Appendix J).

Vovk [19, §5] essentially showed that given an -mixable loss there is no algorithm that can achieve a lower regret bound than on all sequences of outcomes. There is no contradiction in trying to design algorithms which perform well in expectation (maybe better than the AA) on “typical” data while keeping the worst case regret close to . This was the motivation behind the AGAA. In future work, we will explore other choices for the correction vector with the goal of lowering the (expected) bound in (14). In the present work, we did not study the possibility of varying the learning rate . One might obtain better regret bounds using an adaptive learning rate as is the case with the mirror descent algorithm. Our Corollary 17 is useful in that it gives an upper bound on the maximal learning rate under the -mixability constraint. Finally, although our Theorem 18 states that worst-case regret of the GAA is minimized when using the Shannon entropy, it would be interesting to study the dynamics of the AGAA with other entropies.

| Symbol | Description |

|---|---|

| A loss function defined on a set and taking values in (see Sec. 2) | |

| The finite part of the superprediction set of a loss (see Sec. 2) | |

| The support loss of a loss (see Def. 3) | |

| The Bayes risk corresponding to a loss (see Definition 2) | |

| The composition of the Bayes risk with an affine function; (see (1)) | |

| The Shannon Entropy (see (6)) | |

| The mixability constant of (see Def. 6) ; essentially the largest s.t. is -mixable. | |

| Essentially the largest such that is convex (see (5) and [18]) | |

| The generalized mixability constant (see Def. 9); the largest s.t. is -mixable. | |

| A substitution function of a loss (see Sec. 3.1) | |

| The regret achieved by the GAA using entropy (see (11) and Algorithm 2) |

Acknowledgments

This work was supported by the Australian Research Council and DATA61.

References

- [1] Ravi P Agarwal, Maria Meehan, and Donal O’Regan. Fixed point theory and applications, volume 141. Cambridge university press, 2001.

- [2] Amir Beck and Marc Teboulle. Mirror descent and nonlinear projected subgradient methods for convex optimization. Operations Research Letters, 31(3):167–175, 2003.

- [3] Dennis S. Bernstein. Matrix Mathematics: Theory, Facts, and Formulas. Princeton University Press, second edition, 2011.

- [4] Jonathan M. Borwein, Jon D. Vanderwerff, et al. Convex functions: constructions, characterizations and counterexamples, volume 109. Cambridge University Press Cambridge, 2010.

- [5] Alexey Chernov, Yuri Kalnishkan, Fedor Zhdanov, and Vladimir Vovk. Supermartingales in prediction with expert advice. Theoretical Computer Science, 411(29-30):2647–2669, 2010.

- [6] A. Philip Dawid. The geometry of proper scoring rules. Annals of the Institute of Statistical Mathematics, 59(1):77–93, 2007.

- [7] J-B. Hiriart-Urruty and C. Lemaréchal. Fundamentals of convex analysis., 2001.

- [8] Yuri Kalnishkan, Volodya Vovk, and Michael V. Vyugin. Loss functions, complexities, and the legendre transformation. Theoretical Computer Science, 313(2):195–207, 2004.

- [9] Parameswaran Kamalaruban, Robert Williamson, and Xinhua Zhang. Exp-concavity of proper composite losses. In Conference on Learning Theory, pages 1035–1065, 2015.

- [10] Nelson Merentes and Kazimierz Nikodem. Remarks on strongly convex functions. Aequationes mathematicae, 80(1):193–199, 2010.

- [11] Francesco Orabona, Koby Crammer, and Nicolò Cesa-Bianchi. A generalized online mirror descent with applications to classification and regression. Machine Learning, 99(3):411–435, 2015.

- [12] Mark D. Reid, Rafael M. Frongillo, Robert C. Williamson, and Nishant Mehta. Generalized mixability via entropic duality. In Conference on Learning Theory, pages 1501–1522, 2015.

- [13] Joel W. Robbin and Dietmar A. Salamon. Introduction to differential geometry, eth, lecture notes. ETH, Lecture Notes, preliminary version, January, 2011.

- [14] R. Tyrrell Rockafellar. Convex analysis. Princeton University Press, Princeton, NJ, 1997.

- [15] Walter Rudin et al. Principles of mathematical analysis, volume 3. McGraw-hill New York, 1964.

- [16] Jacob Steinhardt and Percy Liang. Adaptivity and optimism: An improved exponentiated gradient algorithm. In International Conference on Machine Learning, pages 1593–1601, 2014.

- [17] John A. Thorpe. Elementary Topics in Differential Geometry. Springer Science & Business Media, 1994.

- [18] Tim van Erven, Mark D. Reid, and Robert C. Williamson. Mixability is Bayes risk curvature relative to log loss. Journal of Machine Learning Research, 13:1639–1663, 2012.

- [19] Vladimir Vovk. A game of prediction with expert advice. Journal of Computer and System Sciences, 56(2):153–173, 1998.

- [20] Vladimir Vovk and Fedor Zhdanov. Prediction with expert advice for the brier game. Journal of Machine Learning Research, 10(Nov):2445–2471, 2009.

- [21] Volodya Vovk. Competitive on-line statistics. International Statistical Review, 69(2):213–248, 2001.

- [22] Robert C. Williamson. The geometry of losses. In Conference on Learning Theory, pages 1078–1108, 2014.

- [23] Robert C. Williamson, Elodie Vernet, and Mark D. Reid. Composite multiclass losses. Journal of Machine Learning Research, 17:223:1–223:52, 2016.

Appendix A Notation and Preliminaries

For , we define . We denote the set of integers between and . Let denote the standard inner product in and the corresponding norm. Let and denote the identity matrix and the vector of all ones in . Let denote the standard basis for . For a set and , we denote , where and . We denote its transpose by . For two vectors , we write [resp. ], if [resp. ]. We also denote the Hadamard product of and . If is a sequence of vectors in , we simply write . For a sequence , we write or , if . For a square matrix , [resp. ] denotes its minimum [resp. maximum] eigenvalue. For , and , we define and .

Let be the probability simplex in . We also define . We will use the notations and . For , the set is a -face of . We denote the linear projection operator satisfying . If there is no ambiguity from the context, we may simply write instead of . It is easy to verify that and that is a bijection from to . In the special case where , we write and we define the affine operator by , where .

For and , we denote and . is a closed half space and is the -ball in centered at . Let be a non-empty set. We denote , , , and the interior, relative interior, boundary, and relative boundary of a set , respectively [7]. We denote the indicator function of by , where for , otherwise . The support function of is defined by

Let . We denote the effective domain of . The function is proper if . The function is convex if and , . When the latter inequality is strict for all , is strictly convex. When is convex, it is closed if it is lower semi-continuous; that is, for all , . The function is said to be 1-homogeneous if , and it is said to be 1-coercive if as . Let be proper. The sub-differential of is defined by

Any element is called a sub-gradient of at . We say that is directionally differentiable if for all the limit exists in . In this case, we denote the limit by . When is convex, it is directionally differentiable [14]. Let be proper and directionally differentiable. The divergence generated by is the map defined by

For and , it is easy to verify that . In this case, it holds that . If is differentiable [resp. twice differentiable] at , we denote [resp. ] its gradient vector [resp. Hessian matrix] at . A vector-valued function is differentiable at if for all , is differentiable at . In this case, the differential of at is the linear operator defined by . If has continuous derivatives on a set , we write .

We define by . That is,

| (17) |

If is directionally differentiable, then , for . If is differentiable at , then . If, additionally, is differentiable at , the chain rule yields . Since , it also follows that .

The Fenchel dual of a (proper) function is defined by , and it is a closed, convex function on [7]. The following proposition gives some useful properties of the Fenchel dual which will be used in several proofs.

Proposition 20 ([7]).

Let . If and are proper and there are affine functions minorizing them on , then for all

A function is an entropy if it is closed, convex, and . Its entropic dual is defined by . For the remainder of this paper, we consider entropies defined on , where .

Let be an entropy and . In this case, . It is clear that is 1-coercive, and therefore, [7, Prop. E.1.3.8]. The entropic dual of can also be expressed using the Fenchel dual of defined by (17) after substituting by and by . In fact,

| (18) |

where (18) follows from the fact that . Note that when is an entropy, is a closed convex function on . Hence, it holds that [14].

The Shannon entropy by ,111The Shannon entropy is usually defined with a minus sign. However, it will be more convenient for us to work without it. if ; and otherwise.

We will also make use of the following lemma.

Lemma 21 ([3]).

, and .

Appendix B Technical Lemmas

This appendix presents technical lemmas which will be needed in various proofs of results from the main body of the paper.

For an open convex set in and , a function is said to be -strongly convex if is convex on [10]. The next lemma is a characterization of a generalization of -strong convexity, where is replaced by any strictly convex function.

Lemma 22.

Let be an open convex set. Let be twice differentiable.

If is strictly convex, then , is invertible, and for any

| (19) |

Furthermore, if , then the left hand side of (19) implies that is strictly convex.

Proof.

Suppose that . Since is strictly convex and twice differentiable on , is symmetric positive definite, and thus invertible. Therefore, there exists a symmetric positive definite matrix such that . Lemma 21 implies

where in the third and fifth lines we used the definition of minimum eigenvalue and performed the change of variable , respectively. To conclude the proof of (19), note that the positive semi-definiteness of is equivalent to the convexity of [7, Thm B.4.3.1].

Finally, note that the equivalences established above still hold if we replace , “”, and “ ” by , “”, and “” , respectively. The strict convexity of then follows from the positive definiteness of (ibid.). ∎

The following result due to [5] will be crucial to prove the convexity of the superprediction set (Theorem 48).

Lemma 23 ([5]).

Let be the set of distributions over some set . Let a function be such that is continuous for all . If for all it holds that , where is some constant, then

Note that when in the lemma above is , .

The next crucial lemma is a slight modification of a result due to [5].

Lemma 24.

Let be a continuous function in the first argument and such that . Suppose that , then

Proof.

Pick any such that , and such that . We define and . For a fixed , is continuous, since is continuous in the first argument. For a fixed , is linear, and thus concave. Since is convex and compact, satisfies Ky Fan’s minimax Theorem [1, Thm. 11.4], and therefore, there exists such that

| (20) |

For , let be such that and for (this is a legitimate distribution since by construction). Substituting for in (20) gives

Choosing , and gives the desired result.

∎

Lemma 25.

Let , where is an open interval containing . Suppose [resp. ] is continuous [resp. differentiable] at . Then is differentiable at if and only if is differentiable at , and we have

Proof.

We have

But since [resp. ] is continuous [resp. differentiable] at , the first term on the right hand side of the above equation converges to as . Therefore, admits a limit when if and only if admits a limit when . This shows that is differentiable at if an only if is differentiable at , and in this case the above equation yields

∎

Note that the differentiability of at does not necessarily imply the differentiability of at 0. Take for example , for , and

Thus, the function is differentiable at but is not. The preceding Lemma will be particularly useful in settings where it is desired to compute the derivative without any explicit assumptions on the differentiability of at . For example, this will come up when computing , where and is smooth curve on , with the only assumption that is twice differentiable at .

Lemma 26.

Let be a proper loss. For any , it holds that

.

This equivalence has been shown before by [23].

[] Since , for all , it follows that is differentiable at if and only if [7, Cor. D.2.1.4]. It remains to show that when is differentiable at . Let and , where is the standard basis of . For , the functions and satisfy the conditions of Lemma 25. Therefore, is differentiable at and

where the last equality holds because attains a minimum at due to the properness of . The result being true for all implies that . ∎

The next Lemma is a restatement of earlier results due to [18]. Our proof is more concise due to our definition of the Bayes risk in terms of the support function of the superprediction set.

Lemma 27 ([18]).

Let be a proper loss whose Bayes risk is twice differentiable on and let . The following holds

-

(i)

.

-

(ii)

, .

-

(iii)

.

We show (i) and (ii).

Let and , where the equality is due to Lemma 26. Since is twice differentiable , is differentiable on and we have . Since is proper, reaches a minimum at , and thus (this shows (i)). On the other hand, we have . By differentiating and using the chain the rule, we get . This means that , and thus . On the other hand, it follows from point (i) of the lemma that . Therefore, and, as a result, , . The last two equations can be combined as .

[We show (iii)] It follows from , since , for .

∎

In the next lemma we state a new result for proper losses which will be crucial to prove a necessary condition for -mixability (Theorem 14) — one of the main results of the paper.

Lemma 28.

Let be a proper loss whose Bayes risk is twice differentiable on . For and ,

| (21) |

where and is the Bayes risk of the loss.

Furthermore, if is a smooth curve in and satisfies and , then is differentiable at and we have

| (22) |

Proof.

We know from Lemma 27 that for , we have , where . Thus, we can write

| (23) |

Observe that . Thus,

| (24) |

where the last equality is due to Lemma 27. The desired result follows by combining (23) and (24).

[We show (22)] Let , we define , , and , where . Since is differentiable at and is continuous at , it follows from Lemma 22 that

where the second equality holds since, according to Lemma 27, we have . Since , , and , we get

| (25) | ||||

where the passage to (25) is due to . In the last equality we used the fact that . ∎

Proposition 29.

Let be an entropy and a closed admissible loss. If is -mixable, then with , is -mixable and

| (26) |

Given an entropy and a loss , we define

where , , , and . Reid et al. [12] showed that is mixable if and only if

Proof of Proposition 29.

[We show that is -mixable] Let , with , , and . Since is -mixable, the following holds

| (27) | ||||

| (28) | ||||

| (29) |

where in (27) we used the fact that . Given that [resp. ] is onto from to [resp. from to ], (29) implies that is -mixable.

[We show (26)] Suppose that there exists and such that . Let be defined by , where is such that . The function is closed and convex on and which is finite by assumption. Using this and the fact that , we have . Substituting by its expression in terms of in the latter equality gives

| (30) |

Let and be such that . Suppose that is an admissible, -mixable loss. The fact that is admissible implies that there exists such that [12]

| (31) |

In particular, it holds that . Fix , such that and for . Let

with as in (30). Note that exists since is closed.

If is such that , then taking puts all weights on experts predicting , while . Therefore,

This contradicts the -mixability of . Therefore, , which by (31) implies . For , with as in (27) and ,

Since () and , (27) implies that there exists small enough such that . But this implies that which contradicts the -mixability of . Therefore, is either equal to or . The former case is not possible. In fact, since is convex, it must have non-decreasing slopes; in particular, it holds that . Since is finite on (by definition of an entropy), we have . Therefore, we have just shown that

| (32) |

Lemma 30.

For , satisfies (26) for all such that , where is the Shannon entropy.

Proof.

Let such that . Let and for . Let and . We have

| (33) |

Observe that the limit of either summation term inside the bracket in (33) is equal to zero. Thus, using l’Hopital’s rule we get

| (34) |

where in (34) we used the fact that . Since for all , , the right hand side of (25) is equal to . Therefore satisfies (26). Since , it is clear that also satisfies (26).

∎

Lemma 31.

Let be an entropy satisfying (26) for all such that . Then for all such , it holds that

Proof.

Lemma 32.

Proof.

Let , , with , and . Then

| (35) | ||||

Lemma 33.

Proof.

Let . Since , the function is lower semicontinuous [14, Cor. 24.5.1]. Given that is a closed convex function, it is also lower semi-continuous. Therefore, the function

is lower semicontinuous, and thus attains its minimum on the compact set at some point . Using the fact that , we get that

| (39) |

If , then either is a vertex of or there exists such that . In the former case, it follows from (26) that for all , and thus the infimum of (36) is trivially attained at . Now consider the alternative — with . Using Corollary 31, we have for all . Therefore,

| (40) |

where . Since , we can use the same argument as the previous paragraph with and replaced by and , respectively, to show that the infimum in (40) is attained at some . Thus, attains the infimum in (36).

Now we show the second part of the lemma. Let and be the infimum of (36). Since is convex and , we have [14, Thm. 23.4]. This means that there exists such that [7, p.166]. We will now show that , which will imply that (ibid., Cor. D.1.4.4). Let . Thus, for all ,

where in the second line we used the fact that , and in third line we used the fact that (ibid.). This shows that .

Substituting by in the expression for , we get

where in the last line we used the fact that is a closed convex function, and thus , (ibid., Cor. E.1.4.4).

∎

Lemma 34.

Let . For any sequence in converging to coordinate-wise and any entropy satisfying (26) for such that ,

| (41) |

Proof of Lemma 34.

Let and be an entropy as in the statement of the Lemma. Let such that . in . Let . If then the result holds trivially since, on the one hand, and on the other hand .

Assume now that . Then

| (42) | ||||

| (43) | ||||

| (44) |

where the last inequality stems from the fact that is a finite vector in . Therefore, (44) implies that the sequence is bounded. We will show that converges in and that its limit is exactly . Let be any convergent subsequence of , and let be the corresponding subsequence of . Consider the infimum in (116) with is replaced by . From Lemma 33, this infimum is attained at some . Since is compact, we may assume without loss of generality that converges to some . Observe that must be ; suppose that such that . Then

This would contradict the fact that is bounded, and thus . Using this, we get

| (45) | ||||

| (46) |

where in (45) we use the fact that . Combining (46) with (43) shows that converges to . Since was any convergent subsequence of (which is bounded), the result follows. ∎

Appendix C Proofs of Results in the Main Body

C.1 Proof of Theorem 4

Theorem 4 Any loss such that , has a proper support loss with the same Bayes risk, , as .

Proof.

We will construct a proper support loss of .

Let (). Since the support function of a non-empty set is closed and convex, we have [7, Prop. C.2.1.2]. Pick any . Since [14], we can apply Proposition 20-(iv) with replaced by to obtain . The fact that and are both finite implies that . Therefore, and . Define .

Now let and . Since the is a closed concave function and , it follows that [7, Prop. B.1.2.5]. Note that . Now let , where is as constructed in the previous paragraph. If is bounded [resp. unbounded], we can extract a subsequence which converges [resp. diverges to ], where is an increasing function. By repeating this process for and so on, we can construct an increasing function , such that has a well defined (coordinate-wise) limit in . Define . By continuity of the inner product, we have

By construction, and . Therefore, is support loss of .

It remains to show that it is proper; that is , . Let . We just showed that and that . Using the fact that , we obtain .

Now let . Since is a support loss, we know that there exists a sequence such that . But as we established in the previous paragraph, . By passing to the limit , we obtain . Therefore is a proper loss with Bayes risk . ∎

C.2 Proofs of Theorem 5 and Proposition 12

For a set , we denote and its convex hull and closed convex hull, respectively.

Definition 35 ([7]).

Let be non-empty convex set in . We say that is an extreme point of if there are no two different points and in and such that .

We denote the set of extreme points of a set by .

Lemma 36.

Let be a closed loss. Then .

Proof.

Since is connected, : } [7, Prop. A.1.3.7].

We claim that . Let be a convergent sequence in , where , and are sequences in , , and , respectively. Since is compact, we may assume, by extracting a subsequence if necessary, that . Let . Since converges, is a bounded sequence in . Since is closed, we may assume, by extraction a subsequence if necessary, that , and , where and . Consequently,

where the last inequality is coordinate-wise. Therefore, there exists such that . This shows that , and thus which proves our first claim.

By definition of an extreme point, . Let and such that . If there exists such that or then would violate the definition of an extreme point. Therefore, the only possible extreme points are of the form . ∎

Theorem 5 Let be a loss and be a proper support loss of . If the Bayes risk is differentiable on , then is uniquely defined on and

Proof.

Let and suppose that is differentiable at . In this case, is differentiable at , which implies [7, Cor. D.2.1.4]

| (47) |

On the other hand, the fact that [7, Prop. C.2.2.1], implies . The latter being an exposed face of implies that every extreme point of is also an extreme point of [7, Prop. A.2.3.7, Prop. A.2.4.3]. Therefore, from (47), is the only extreme point of . From Lemma 36, there exists such that . In this paragraph, we showed the following

| (48) |

For the rest of this proof we will assume that is differentiable on . Let . Since is a support loss, there exists () in such that converges to . From (48) it holds that . Since converges and is closed, there exists such that .

Now let and . Since and is proper, we have for all and . Therefore, Lemma 24 implies that for all there exists , such that . On one hand, since is bounded (from the previous inequality), we may assume by extracting a subsequence if necessary, that converges. On the other hand, since , (48) implies that there exists such that . Since is closed and converges, there exists , such that . But since is admissible, the latter component-wise inequality implies that . ∎

Lemma 37.

Let be a loss satisfying Assumption 1. If is not differentiable at then there exist , such that and .

Proof.

Suppose is not differentiable at . Then from the definition of the Bayes risk, is not differentiable at . This implies that has more than one element [7, Cor. D.2.1.4]. Since (ibid.. Prop. C.2.2.1), is a subset of and every extreme point of is also an extreme point of (ibid., Prop. A.2.3.7). Thus, from Lemma 36, we have . On the other hand, since , is a compact, convex set [14, Thm. 23.4], and thus [7, Thm. A.2.3.4]. Hence, the fact that has more than one element implies there exists such that and . Since , Proposition 20-(iv) and the fact that imply that . ∎

Proposition 12 Let be an entropy and . If is -mixable, then the Bayes risk satisfies . If, additionally, is twice differentiable on , then must be strictly convex on .

Proof.

Let . Since is -mixable, it must be -mixable, where (Proposition 29). Let .

For and (see appendix E), we define . The value of does not depend on the choice of , and it holds that and [7, Prop. C.1.2.2]. In our case, we have (by definition of ), which implies that and . Therefore, . As a result cannot be affine. For all , let be defined by

Since is convex it must have non-decreasing slopes (ibid., p.13). Combining this with the fact that is not affine implies that

| (49) |

The fact that has non-decreasing slopes also implies that

Similarly, we have . Let . Since is a closed convex function the following equivalence holds (ibid., Cor. D.1.4.4). Thus, if , then , which is not possible since is -mixable (Lemma 32).

[We show ] We will now show that is continuously differentiable on . Since is 1-homogeneous, it suffices to check the differentiability on . Suppose is not differentiable at . From Lemma 37, there exists such that and . Let , , and as in (49). We denote and . Let and . From the fact that is -mixable, , and (10), there must exist such that for all ,

| and by letting be the sign function | ||||

| (50) | ||||

where in (50) we used the fact that has non-decreasing slopes and the definition of . When , (50) becomes . Otherwise, we have . Since is admissible, there must exist at least one such that . Combining this with the fact that (), implies that . This contradicts the fact that . Therefore, must be differentiable at . As argued earlier, this implies that must be differentiable on . Combining this with the fact that is concave on , implies that is continuously differentiable on (ibid., Rmk. D.6.2.6).

[We show ] Suppose that is not differentiable at some . Then there exists such that . Since , is finite and convex [7, Prop. D.1.1.2], and thus it is continuous on (ibid., Rmk. B.3.1.3). Consequently, there exists such that

| (51) |

Let be such that

Note that since has increasing slopes ( is convex), , where the last inequality holds because , and thus . Let . From (51), it is clear that .

Suppose that is twice differentiable on and let be a support loss of . By definition of a support loss, (where ). Thus, since is twice differentiable on , is differentiable on . Furthermore, is continuous on given that as shown in the first part of this proof. We may assume without loss of generality that is not a constant function. Thus, from Theorem 5, is not a constant function either. Consequently, the mean value theorem applied to (see e.g. [15, Thm. 5.10]) between any two points in with distinct images under , implies that there exists , such that . For the rest of the proof let and define . From Lemma 27, we have , which implies that there exists . Thus, the set

| (52) |

is non-empty. From this and the fact that , it follows that

| (53) |

Let . From Taylor’s Theorem (see e.g. [hardy2008, §151]) applied to the function , there exists and functions , , such that and

| (54) |

For , let and suppose that (we will define explicitly later). By shrinking if necessary, we may assume that

| (55) | |||

| (56) | |||

| (57) |

where (57) is satisfied for small enough because of (53) and the fact that

and (56) is also satisfied for small enough because , where the first equality is due to the fact that is uniformly bounded on compact subsets of (by continuity of the directional derivative ).

If , then by the positive homogeneity of the directional derivative, the definition of the function , and (57), we get

| (58) |

On the other hand, if , then from the monotonicity of the slopes of , the positive homogeneity of the directional derivative, and the definition of the function , it follows that

| (59) |

Let , for . From Theorem 5, there exists , such that

| (60) |

where for .

From the fact that is -mixable, it follows that there exists such that for all ,

| (61) |

For , we now define explicitly as

From (55), we have . Furthermore, from (60) and the fact that for all , , we have

| (62) |

Using this, together with (58) and (59), we get ,

| (63) |

Combining (61), (62), and (63) yields

| using (56) and the fact that (see Lemma 27), we get | ||||

| (64) | ||||

| (65) | ||||

where in (65) we used (53) and the fact that (see (61)). Equation 65 shows that , which is a contradiction. ∎

C.3 Proof of Theorem 7

Theorem 7 Let , and let a loss. Suppose that and that is twice differentiable on . If then is -mixable. In particular, .

Proof.

Let . We will show that is convex, which will imply that is -mixable [5].

Since , is convex on [18, Thm. 10]. Let and define

Since is equal to plus an affine function, it follows that is also convex on . On the one hand, since and are proper losses, we have and which implies that

| (66) |

On the other hand, since and are differentiable we have and , which yields . This implies that attains a minimum at [7, Thm. D.2.2.1]. Combining this fact with (66) gives , or equivalently . By Proposition 20-(iii), this implies

| (67) |

Using Proposition 20-(ii), we get for . Since and , Proposition 20-(v) implies . Similarly, we have . Therefore, (67) implies

This inequality implies that if , then . In particular, if then

| (68) |

To see the set inclusion in (68), consider , then by definition of the superprediction set there exists and , such that . Thus,

| (69) |

where the inequality is true because and . The above argument shows that , where . Furthermore, , since all elements of have non-negative, finite components. The latter set inclusion still holds for . In fact, from the definition of a support loss, there exists a sequence in converging to such that . Equation 69 implies that for , . Since the inner product is continuous, by passage to the limit, we obtain . Therefore,

| (70) |

Now suppose ; that is, for all ,

| (71) |

where the first equality is obtained merely by expanding the expression of the inner product, and the second inequality is simply Jensen’s Inequality. Since is strictly convex, the Jensen’s inequality in (71) is strict unless , such that

| (72) |

By substituting (72) into (71), we get , and thus . Furthermore, (72) together with the fact that imply that , and thus there exists such that (Theorem 5). Using this and rearranging (72), we get . Since , this means that . Suppose now that (72) does not hold. In this case, (71) must be a strict inequality for all . By applying the on both side of (71),

| (73) |

Since is a closed concave function, the map is also closed and concave, and thus upper semi-continuous. Since is compact, the function must attain its maximum in . Due to (73) this maximum is negative; there exists such that

| (74) |

Let , for . It follows from (74) that for all , and . Thus, Lemma 25 applied to with , implies that there exists , such that . From this inequality, , and therefore, there exists such that (Theorem 5). This shows that , which implies that . Therefore, . Combining this with (70) shows that . Since is the intersection of convex set, it is a itself convex set. Since by assumption, it follows that , and thus is convex. This last fact implies that is -mixable [5]. ∎

C.4 Proof of Theorem 10

We start by the following characterization of -differentiability (this was defined on page 5 of the main body of the paper).

Lemma 38.

Let be an entropy. Then is -differentiable if and only if such that , is differentiable on .

Proof.

This is a direct consequence of Proposition B.4.2.1 in [7], since 1) is convex; and 2)

for all and . ∎

Theorem 10 Let be a -differentiable entropy. Let be a loss (not necessarily finite) such that is twice differentiable on . If is -mixable then the GAA achieves a constant regret in the game; for any sequence ,

where is the th basis element of .

Proof.

For all such that , let and . From Lemma 33 the infimum involved in the definition of the expert distribution in Algorithm 2 is indeed attained. It remains to verify that this minimum is unique. This will become clear in what follows.

Let and . For , we define the non-increasing sequence of subsets of defined by . We show by induction that and

| (75) |

where , . Suppose that (75) holds true up to some . We will now show that it holds for . To simplify expressions, we denote for , and . From the definition of in Algorithm 2, we have

| Using the definition of , | ||||

| Now using the facts that , , is -differentiable, and Lemma 38, we have | ||||

| Using the facts that , for , and (since ) | ||||

| and since the last two terms are independent of , | ||||

| Now using Fenchel duality property in Proposition 20-(iv), | ||||

| Finally, due to Lemma 29 and Proposition 12, is differentiable on , and thus | ||||

| (76) | ||||

From (76), we obtain

| (77) |

Thus using the induction assumption and the fact that (since ), the result follows, i.e. (75) is true for all . Furthermore, , since . Using the same arguments as above, one arrives at

| Using the Fenchel duality property Proposition 20-(vi) and (76), | ||||

| (78) | ||||

On the other hand, -mixability implies that there exists , such that for all ,

| Summing this inequality for yields, | ||||

| and thus using (78) and (77) yields | ||||

| Finally, using (75) together with the fact that | ||||

Using the definition of the Fenchel dual and Proposition 20-(vi) again, the above inequality becomes

| (79) |

Using the fact that , (by definition of ), the right hand side of (79) becomes

Thus, we get

| Using the facts that and the definition of the divergence, | ||||

| which for implies | ||||

| (80) | ||||

When instead of -mixability, we have -mixability, the last term in (80) becomes and the desired result follows.

∎

C.5 Proof of Theorem 11

We require the following result:

Proposition 39.

For the Shannon entropy , it holds that , and .

Proof.

Given , we first derive the expression of the Fenchel dual . Setting the gradient of to gives . For , we have , and from appendix A we know that . Therefore,

where the right most equality is equivalent to . Since , we get . Therefore, the supremum in the definition of is attained at . Hence . Finally, using (18) we get , for . ∎

Theorem 11 Let . A loss is -mixable if and only if is -mixable.

Proof.

Claim 1.

For all , , and

| (81) |

Let . From Proposition 39, the Shannon entropy is such that is differentiable on , and thus it follows from Lemma 33 ((37)-(38)) that for any

| (82) |

By definition of , , and due to Proposition 39, . Therefore,

| (83) |

On the other hand, from [12] we also have

| (84) |

| (85) |

Suppose now that for such that . By repeating the argument above for , we get

| (86) |

It remains to check the case where is a vertex; Without loss of generality assume that and let . Then there exists , such that and by Lemma 30, . Therefore, , which implies

| (88) |

Combining (88) and (87) proves the claim in (81). The desired equivalence follows trivially from the definitions of -mixability and -mixability.

∎

C.6 Proof of Theorem 13

We need the following lemma to show Theorem 13.

Proof.

Let . Suppose that there exists such that . Since is convex, it must have non-decreasing slopes; in particular, it holds that . Therefore, since is finite on (by definition of an entropy), we have . Since by assumption is convex and finite on the simplex, we can use the same argument to show that . This is a contradiction since (Lemma 30). Therefore, it must hold that .

Suppose now that for , with . Let and . Since is convex on and is a linear function, is convex on . Repeating the steps above for and substituted by and , respectively, we get that . Since the proof is completed. ∎

Theorem 13 Let , a -mixable loss, and an entropy. If is convex on , then is -mixable.

Proof.

Assume is convex on . For this to hold, it is necessary that since is strictly concave. Let and . Then and is convex on , since is convex on and is affine.

Let , and . Suppose that and let be as in Proposition 33. Note that if , then the -mixability condition (10) is trivially satisfied. Suppose, without loss of generality, that . Let be any sequence such that . From Lemmas 30 and 34, for .

Let be defined by

| and it’s Fenchel dual follows from Proposition 20 (i+ii): | ||||

After substituting by in the expression of and rearranging, we get

| (89) |

Since and is a closed convex function, combining Proposition 20-(iv) and the fact that [7, Cor. E.1.3.6] yields . Thus, after substituting by in the expression of , we get

| (90) |

On the other hand, is convex on , since is equal to plus an affine function. Thus, , since and are both convex (ibid., Thm. D.4.1.1). Since is differentiable at , we have . Furthermore, since , then . Hence, attains a minimum at (ibid., Thm. D.2.2.1). Due to this and (90), , which implies that (Proposition 20-(iii)). Using this in (89) gives for all

where the implication is obtained by adding on both sides of the first inequality and using Proposition 33.

Suppose now that , with , and let and . Note that since is convex on and is a linear function, is convex on . Repeating the steps above for , , , and substituted by , , , and , respectively, yields

| (91) |

where the first implication follows from Lemma 32, since and both satisfy (26) (see Lemmas 30 and 40), and (91) is obtained by passage to the limit . Since , is -mixable, which implies that is -mixable (Theorem 11). Therefore, there exists , such that

| (92) |

To complete the proof (that is, to show that is -mixable), it remains to consider the case where is a vertex of . Without loss of generality assume that and let . Thus, there exists , with , such that , and Lemma 40 implies that . Therefore, , which implies

| (93) |

The -mixability condition (10) is trivially satisfied in this case. Combining (92) and (93) shows that is -mixable. ∎

C.7 Proof of Theorem 14

The following Lemma gives necessary regularity conditions on the entropy under the assumptions of Theorem 14.

Lemma 41.

Let and be as in Theorem 14. Then the following holds

-

(i)

is strictly concave on .

-

(ii)

is be continuously differentiable on .

-

(iii)

is twice differentiable on and .

-

(iv)

For the Shannon entropy, we have

Proof.

Since is -mixable and is twice differentiable on , is continously differentiable on (Proposition 12). Therefore, is strictly convex on [7, Thm. E.4.1.2].

The differentiability of and implies (ibid.). Since is twice differentiable on (by assumption), the latter equation implies that is twice differentiable on . Using the chain rule, we get . Multiplying both sides of the equation by from the right gives the expression in (iii). Note that is in fact invertible on since is strictly convex on . It remains to show that . This set equality follows from 1) (ibid., Cor. E.1.4.4); 2) ; and 3) (Lemma 32).

For the Shannon entropy, we have (Proposition 39) and , for . Thus ∎

To show Theorem 14, we analyze a particular parameterized curve defined in the next lemma.

Lemma 42.

Let be a proper loss whose Bayes risk is twice differentiable on , and let be an entropy such that and are twice differentiable on and , respectively. For , let be the curve defined by

| (94) |

where and . Then

| (95) |

Proof.

Since , and . As a result, , and thus . This shows that Let . For ,

From the definition of , , , and therefore, . By differentiating in (94) and using the chain rule, . By setting , . Thus, . Furthermore,

where in the third equality we used Lemma 25, in the fourth equality we used Lemma 28, and in the sixth equality we used Lemma 41-(iii).

∎

In next lemma, we state a necessary condition for -mixability in terms of the parameterized curve defined in Lemma 42.

Lemma 43.

Let , , and be as in Lemma 42. If such that the curve satisfies , then is not mixable. In particular, , such that lies outside .

Proof.

First note that for any triplet , the map is differentiable at . This follows from Lemmas 25 and 42. Let and . Then

Since is differentiable at 0, it follows from Lemma 25 that is also differentiable at , and thus

| (96) | ||||

| (97) |

where (96) and (97) hold because (see Lemma 42). According to Taylor’s theorem (see e.g. [hardy2008, §151]), there exists and such that

| (98) |

and . From Lemma 42, and . Therefore, and (98) becomes . Due to (97) and the fact that , we can choose small enough such that . This means that . Therefore, must lie outside the superprediction set. Thus, the mixability condition (10) does not hold for . This completes the proof.∎

Theorem 14 Let be a loss such that is twice differentiable on , and an entropy such that is twice differentiable on . Then is -mixable only if is convex on .

Proof.

We will prove the contrapositive; suppose that is not convex on and we show that cannot be -mixable. Note first that from Lemma 41-(iii), is twice differentiable on . Thus Lemmas 42 and 43 apply. Let be a proper support loss of and suppose that is not convex on , This implies that is not convex on , and by Lemma 22 there exists , such that . From this and the definition of , there exists such that

| (99) |

where the equality is due to Lemma 41-(iv). For the rest of this proof let . By assumption, twice differentiable and concave on , and thus is symmetric positive semi-definite. Therefore, their exists a symmetric positive semi-definite matrix such that . From Lemma 41-(i), is strictly convex on , and so there exists a symmetric positive definite matrix such that . Let be the unit norm eigenvector of associated with . Suppose that . Since , it follows from the positive semi-definiteness of that , and thus . This implies that , which is not possible due to (99). Therefore, . Furthermore, the negative semi-definiteness of implies that

| (100) |

Let be the unit norm eigenvector of associated with , where the equality is due to Lemma 21. Let .

We will show that for , the parametrized curve defined in Lemma 42 satisfies , where . According to Lemma 43 this would imply that there exists , such that lies outside . From Theorem 5, we know that there exists , such that . Therefore, , and thus is not -mixable.

C.8 Proof of Lemma 15

Lemma 15 Let be a loss. If , then either or .

Proof.

Suppose . Let , . By definition of there exists such that is -mixable and . Therefore, such that

| (102) |

where the right-most inequality follows from the fact . Therefore, the sequence is bounded, and thus admits a convergent subsequence. If we let be the limit of this subsequence, then from (102) it follows that

| (103) |

On the other hand, since is closed (by Assumption 1), it follows that there exists such that . Combining this with (103) implies that is -mixable, and thus . ∎

C.9 Proof of Theorem 17

C.10 Proof of Theorem 18

Theorem 18 Let , where is the Shannon entropy and is an entropy such that is twice differentiable on . A loss , with twice differentiable on , is -mixable only if .

Proof.

Suppose is -mixable. Then from Theorem 16, is convex on , and thus (Corollary 17). Furthermore, is convex on , since is an affine function. It follows from Lemma 22 and Corollary 17 that

Let and . By definition of an entropy and the fact that the directional derivatives and are finite on [7, Prop. D.1.1.2], it holds that . Therefore, there exists such that . If we let , we get

| (105) |

Let . Observe that

We define similarly. Suppose that . Then, from Corollary 17, , This implies that , and from Lemma 22, must be strictly convex on . We also have and . Therefore, attains a strict minimum at (ibid., Thm. D.2.2.1); that is, , . In particular, for , we get , which contradicts (105). Therefore, , and thus

| (106) | ||||

| (107) |

where (106) is due to and . Equation 107, implies that , since [12]. Therefore,

| (108) |

It remains to consider the case where is in the relative boundary of . Let . There exists such that . Let and . It holds that and . Since is -mixable, it follows from Proposition 29 and the 1-homogeneity of [7, Prop. D.1.1.2] that

| Hence, | ||||

| (109) | ||||

Inequality 109 also applies to , since is -mixable. From (109) and (108), we conclude that . ∎

C.11 Proof of Theorem 19

Theorem 19 Let be a -differentiable entropy. Let be a loss such that is twice differentiable on . Let , where and . If is -mixable then for initial distribution and any sequence , the AGAA achieves the regret

Proof.

Recall that , where . From Theorem 16 and since is equal to plus an affine function, it is clear that if is -mixable then is -mixable. Thus, for all , there exists such that for any outcome

| Summing over from 1 to , we get | ||||

| (110) | ||||

ODue to the properties of the entropic dual [12] and the definition of , the following holds for all and in ,

| (111) | |||||

| (112) | |||||

| (113) |

Using (111)-(112), we get for all , , and in particular . Similarly, using (111)-(113), gives for all . Substituting back into (110) yields

| (114) |

To conclude the proof, we note that since is convex it holds that

| (115) |

which allows us to bound the sum on the right hand side of 114. To bound the rest of the terms, we use the fact that , and thus by letting ,

Substituting this last inequality and (115) back into (114) yields the desired bound. ∎

Appendix D Defining the Bayes Risk Using the Superprediction Set

In this section, we argue that when a loss is mixable, in the classical or generalized sense, it does not matter whether we define the Bayes risk using the full superprediction set or its finite part . Recall the definition of the Bayes risk;

Definition 2 Let be a loss such that . The Bayes risk is defined by

| (116) |

Note that the right hand side of (116) does not change if we substitute for its closure — — with respect to . Thus, it suffices to show that when the loss is mixable. We show this in Theorem 45, but first we give a characterization of the (finite part) of the superprediction set for a proper loss.

Proposition 44.

Let be a proper loss. If is differentiable on , then

| (117) |

Proof.

Let . Let be defined by . By the choice of , we have for all . Since is differentiable on , by assumption, is continuous on , and thus is continuous in the first argument. Since has finite components, the map satisfies all the conditions of Lemma 24. Therefore, there exists such that

| (118) |

Without loss of generality, we can assume by extracting a subsequence if necessary that converges to . By definition, we have , and from (118) it follows that coordinate-wise. Thus, is in .

The above argument shows that , and since is closed in we have , where is the closure of in . Now it suffice to show that to complete the proof.

Let and . Define by if ; and otherwise. Let . It follows that

| (119) |

Claim 2.

.

Suppose that Claim 2 is false. This means that there exists such that

| (120) |

We may assume, by extracting a subsequence if necessary ( is compact), that converges to . Taking the limit in (120) would lead to the contradiction ‘’, since from (119) we have . Therefore, Claim 2 is true. For let be as in Claim (2). The claim then implies that uniformly for . By the claim we also have that for all , and by construction of , we have . This shows that , which completes the proof.

∎

Theorem 45.

Let be a loss. If , then is not mixable.

Proof.

Suppose that is mixable and let be a proper support loss of . From Proposition 12, is differentiable on , and thus Theorem 5 implies that . Therefore, Lemma 44 implies that . Thus, if , there exists , , and such that

| (121) |

Note that cannot be in ; otherwise, (121) would imply that has all finite components, and thus would be included in , which is a contradiction. Assume from now on that . From the definition of the support loss, there exists a sequence such that and . Therefore, Theorem 5 implies that there exists such that

| (122) |

To see this, note that since , Theorem 5 guarantees the existence of a sequence such that . On the other hand, for any such that , we have — otherwise, would be infinite. It follows, by continuity of the inner product that , and thus it suffices to pick equal to for large enough.

Appendix E The Update Step of the GAA and the Mirror Descent Algorithm

In this section, we demonstrate that the update steps of the GAA and the Mirror Descent Algorithm are essentially the same (at least for finite losses) according to the definition of the MDA given by Beck and Teboulle [2];

Let be a loss and an entropy such that is differentiable on . Let be the update distribution of the GAA at round and . It follows from the definition of (see Algorithm 2) that

| (124) |

where . Update (124) is, by definition [2], the MDA with the sequence of losses on , ‘distance’ function , and learning rate . Therefore, the MDA is exactly the update step of the GAA.

Appendix F The Generalized Aggregating Algorithm Using the Shannon Entropy

The purpose of this appendix is to show that the GAA reduces to the AA when the former uses the Shannon entropy. In this case, generalized and classical mixability are equivalent. In what follows, we make use of the following proposition which is proved in C.5.

Proposition 39 For the Shannon entropy , it holds that , and .

Let be a loss and be as in Proposition 33 and suppose that and are differentiable on and , respectively. It was shown in [12] that

| (125) | |||

| (126) |

Let . By definition of , , and due to Proposition 39, . Therefore, and , . Thus,

| (127) |

Let . Then and [12].222Reid et al. [12] showed the equality , for any entropy differentiable on - not just for the Shannon Entropy. Then the left hand side of (127) can be written as . Using this fact, (125) and (127) show that the update distribution of the GAA (Algorithm 2) coincides with that of the AA after substituting , and by , and , respectively.

Appendix G Legendre , but no -mixable

In this appendix, we construct a Legendre type entropy [14] for which there are no -mixable losses satisfying a weak condition (see below).

Let be a loss satisfying condition 1. According to Alexandrov’s Theorem, a concave function is twice differentiable almost everywhere (see e.g. [4, Thm. 6.7]). Now we give a version of Theorem 14 which does not assume the twice differentiability of the Bayes risk. The proof is almost identical to that of Theorem 14 with only minor modifications.

Theorem 46.

Let be an entropy such that is twice differentiable on , and a loss satisfying Condition 1 and such that , where is a set of Lebesgue measure 1 where is twice differentiable, and define

| (129) |

Then is -mixable only if is convex on .

The new condition on the Bayes risk is much weaker than requiring to be twice differentiable on . In the next example, we will show that there exists a Legendre type entropy for which there are no -mixable losses satisfying the condition of Theorem 46.

Appendix H Loss Surface and Superprediction Set

In this appendix, we derive an expression for the curvature of the image of a proper loss function. We will need the following lemma.

Lemma 47.

Let be a 1-homogeneous, twice differentiable function on . Then is concave on if and only if is concave on .

Proof.

The forward implication is immediate; if is concave on , then is concave on , since is an affine function.

Now assume that is concave on . Let and . We need to show that

| (131) |