On the Optimal Reconstruction of Partially Observed Functional Data

Alois

Kneiplabel=e1]akneip@uni-bonn.de

[

Dominik

Liebl

label=e2]dliebl@uni-bonn.de

[

Alois Kneip and Dominik Liebl

Statistische Abteilung

University of Bonn

Adenauerallee 24-26

53113 Bonn, Germany

University of Bonn

Abstract

We propose a new reconstruction operator that aims to recover the missing parts of a function given the observed parts. This new operator belongs to a new, very large class of functional operators which includes the classical regression operators as a special case. We show the optimality of our reconstruction operator and demonstrate that the usually considered regression operators generally cannot be optimal reconstruction operators.

Our estimation theory allows for autocorrelated functional data and considers the practically relevant situation in which each of the functions is observed at , , discretization points. We derive rates of consistency for our nonparametric estimation procedures using a double asymptotic.

For data situations, as in our real data application where is considerably smaller than , we show that our functional principal components based estimator can provide better rates of convergence than conventional nonparametric smoothing methods.

62M20,

62H25,

62G05,

62G08,

functional data analysis,

functional principal components,

incomplete functions,

keywords:

[class=AMS]

keywords:

\newcites

appendixReferences\startlocaldefs\endlocaldefs

and

1 Introduction

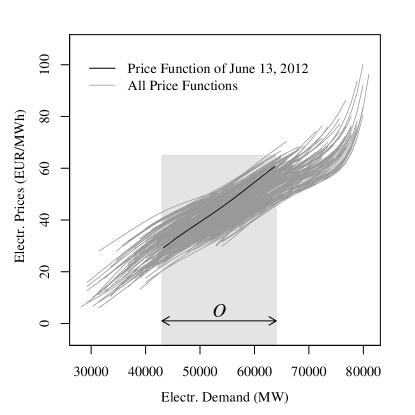

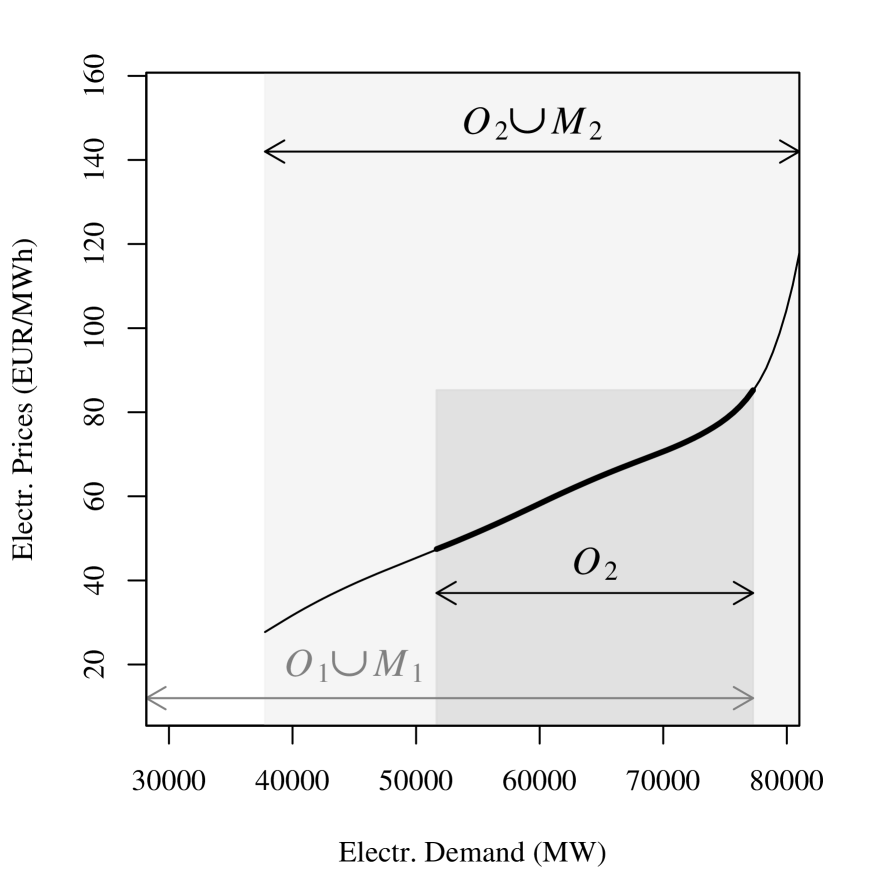

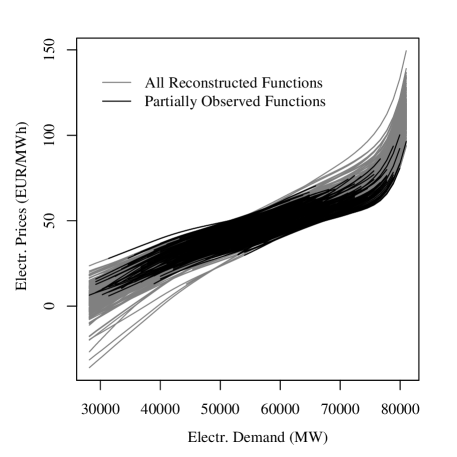

Our work is motivated by a data set from energy economics which is shown in Figure 1. The data consist of partially observed price functions. Practitioners use these functions, for instance, to do comparative statics, i.e., a ceteris-paribus analysis of price effects with respect to changes in electricity demand (cf. Weigt, 2009; Hirth, 2013). The possibilities of such an analysis, however, are limited by the extent to which we can observe the price functions. This motivates the goal of our work, which is to develop a reconstruction procedure that allows us to recover the total functions from their partial observations.

Figure 1: Partially observed electricity price functions with .

Let be an identically distributed, possibly weakly dependent sample of continuous random functions, where each function is an element of the separable Hilbert space with and , where . We denote the observed and missing parts of by and , where

and where is a random subinterval, independent from with almost surely. In our theoretical part (Section 2) we also allow for the general case, where consists of multiple subintervals of . In what follows we use “” and “” to denote a given realization of and . In addition, we use the following shorthand notation for conditioning on and :

typical realizations of and are shown in Figure 1. We denote the inner product and norm of as and ; their dependency on will be made obvious by writing, for instance, and for all , where . Throughout the introduction and Section 2, we consider centered random functions, that is, with for all .

Our object of interest is the following linear reconstruction problem:

(1)

which aims to reconstruct the unobserved missing parts given the partial observation . Our objective is to identify the optimal linear reconstruction operator which minimizes the mean squared error loss at any .

The case of partially observed functional data was initially considered in the applied work of Liebl (2013) and the theoretical works of Goldberg, Ritov and

Mandelbaum (2014) and Kraus (2015). The work of Gromenko

et al. (2017) is also related as it proposes an inferential framework for incomplete spatially and temporally correlated functional data. Goldberg, Ritov and

Mandelbaum (2014) consider the case of finite dimensional functional data and their results have well-known counterparts in multivariate statistics. Kraus (2015) starts by deriving his “optimal” reconstruction operator as a solution to the Fréchet-type normal equation, where he assumes the existence of a bounded solution. The theoretical results in our paper imply that this assumption generally holds only under the very restrictive case of linear regression operators, i.e., Hilbert-Schmidt operators. For showing consistency of his empirical reconstruction operator, Kraus (2015) restricts his work to this case of Hilbert-Schmidt operators. We demonstrate, however, that a Hilbert-Schmidt operator generally cannot be the optimal reconstruction operator.

In order to see the latter, we need some conceptional work. Hilbert-Schmidt operators on spaces correspond to linear regression operators,

(2)

However, such a regression operator generally does not provide the optimal solution of the reconstruction problem in (1). For instance, let us consider the “last observed”(=“first missing”) points, namely, the boundary points111The boundary of a subset is defined as , where and denote the closures of the subsets and . of . For any optimal reconstruction operator , it must hold that the “first reconstructed” value, , connects with the “last observed” value, , i.e., that

There is no hope, though, of finding a slope function that fulfills the equation (the Dirac- function is not an element of ). It is therefore impossible to identify the optimal reconstruction operator within the class of linear regression operators defined by (2).

Best possible linear reconstruction operators depend, of course, on the structure of the random function , and possible candidates have only to be well-defined for any function in the support of . We therefore consider the class of all linear operators with finite variance and thus for any . This class of reconstruction operators is much larger than the class of regression operators and contains the latter as a special case. A theoretical characterization is given in Section 2. We then show that the optimal linear reconstruction operator, minimizing for all , is given by

(3)

where denote the pairs of orthonormal eigenfunctions and nonzero eigenvalues of the covariance operator with , while

. Here denotes the covariance function of , and the covariance function .

The general structure of in (3) is similar to the structure of the operators considered in the literature on functional linear regression, which, however, additionally postulates that has an (restrictive) integral-representation as in (2); see, for instance, Cardot, Mas and Sarda (2007), Cai and Hall (2006), Hall and Horowitz (2007) in the context of functional linear regression, or Kraus (2015) in a setup similar to ours.

There is, however, no reason to expect that the optimal reconstruction operator satisfies (2). To see the point note that can be represented in the form (2) if and only if the additional square summability condition is satisfied for . Only then the series , , converge as and define a function such that .

But consider again the reconstruction at a boundary point , where simplifies to , since for boundary points we have and . Plugging this simplification into (3) and using the Karhunen-Loéve decomposition of implies that . This means that our reconstruction operator indeed connects the “last observed” value with the “first reconstructed” value . On the other hand, the sum will generally tend to infinity as , which violates the additional condition necessary for establishing (2). Therefore, in general, does not constitute a regression operator.222A frequently used justification of the use of regression operators relies on the Riesz representation theorem which states that any continuous linear functional can be represented in the form (2). This argument, however, does not necessarily apply to the optimal linear functional which may not be a continuous functional . In particular, although being a well-defined linear functional, the point evaluation is not continuous, since for two functions an arbitrarily small -distance may go along with a very large pointwise distance (see the example in Appendix B.1 of the supplementary paper Kneip and Liebl (2019)).

The above arguments indicate that methods for estimating should not be based on (2). Any theoretical justification of such procedures has to rely on non-standard asymptotics avoiding the restrictive assumption that . This constitutes a major aspect of our asymptotic theory given in Section 4.

The problem of estimating from real data is considered in Section 3. Motivated by our application, the estimation theory allows for an autocorrelated time series of functional data and considers the practically relevant case where the function parts are only observed at many discretization points with , , and .

We basically follow the standard approach to estimate through approximating the infinite series (3) by a truncated sequence relying only on the largest eigenvalues of the covariance operator. But note that our data structure implies that we are faced with two simultaneous estimation problems. One is efficient estimation of for , the other one is a best possible estimation of the function for from the observations . We consider two different estimation strategies; both allow us to accomplish these two estimation problems.

The first consists in using a classical functional principal components based approximation of on , which is simply given by extending the operator in (3) by extending to . This way the empirical counterpart of the truncated sum

will simultaneously provide estimates of the true function on the observed interval and of the optimal reconstruction on the unobserved interval .

The second consists in estimating the true function on the observed interval directly from the observations using, for instance, a local linear smoother and to estimate for through approximating the infinite series (3) by its truncated version. But a simple truncation would result in a jump at a boundary point , with denoting the closest boundary point to the considered , i.e., if and otherwise. We know, however, that for any we must have for all , since for all boundary points . Therefore, we explicitly incorporate boundary points and estimate by the empirical counterpart of the truncated sum

The above truncation does not lead to an artificial jump at a boundary point , since continuously as for all .

For estimating the mean and covariance functions – the basic ingredients of our reconstruction operator – we suggest using Local Linear Kernel (LLK) estimators. These LLK estimators are commonly used in the context of sparse functional data (see, e.g., Yao, Müller and Wang, 2005a), though, we do not consider the case of sparse functional data. In the context of partially observed functional data, it is advisable to use LLK estimators, since these will guarantee smooth estimation results, which is not the case when using the empirical moment estimators for partially observed functions as proposed in Kraus (2015).

We derive consistency as well as uniform rates of convergence under a double asymptotic

which allows us to investigate all data scenarios from almost sparse to dense functional data. This leads to different convergence rates depending on the relative order of and . For data situations, as in our real data application where is considerably smaller than and all sample curves are of similar structure, we show that our functional principal components based estimator achieves almost parametric convergence rates and can provide better rates of convergence than conventional nonparametric smoothing methods, such as, for example, local linear regression.

Our development focuses on the regular situation where (with probability tending to 1) there exist functions that are observed over the total interval . Only then is it possible to consistently estimate the covariance function for all possible pairs . In our application this is not completely fulfilled, and there is no information on for very large values . Consequently, for some intervals and the optimal reconstruction operator cannot be identified. This situation corresponds to the case of so-called fragmentary observations, as considered by Delaigle and

Hall (2013), Delaigle and Hall (2016), Descary and Panaretos (2018), and Delaigle et al. (2018). To solve this problem we suggest an iterative reconstruction algorithm. Optimal reconstruction operators are determined for a number of smaller subintervals, and a final operator for a larger interval is obtained by successively plugging in the reconstructions computed for the subintervals. We also provide some inequality bounding the accumulating reconstruction error.

The rest of this paper is structured as follows: Section 2 introduces our reconstruction operator and contains the optimality result. Section 3 comprises our estimation procedure. The asymptotic results are presented in Section 4. Section 5 describes the iterative reconstruction algorithm. Section 6 contains the simulation study and Section 7 the real data application. All proofs can be found in the online supplement supporting this article (Kneip and Liebl, 2019).

2 Optimal reconstruction of partially observed functions

Let our basic setup be as described in Section 1. Any (centered) random function then adopts the well-known Karhunen-Loéve (KL) representation

(4)

with the principal component (pc) scores , where and for all and zero else and . We want to note that all arguments in this section also apply to the more general case where the observed subdomain consists of a finite number of mutually disjoint subintervals .

By the classical eigen-equations we have that

(5)

where . Equation (5) can obviously be generalized for all which leads to the following “extrapolated” th basis function:

(6)

where . Equation (6) leads to the definition of our reconstruction operator as a generalized version of the KL representation in (4):

(7)

Remark

Note that the KL representation provides the very basis of a majority of the works in functional data analysis (cf. Ramsay and

Silverman, 2005; Horváth and

Kokoszka, 2012). Functional Principal Component Analysis (FPCA) relies on approximating by its first principal components. This is justified by the best basis property, i.e., the property that for any

(8)

Remark

For later use it is important to note that the definitions of and in (6) and (7) can be extended for all by setting . Then by construction for all and, therefore, for all .

2.1 A theoretical framework for reconstruction operators

Before we consider the optimality properties of , we need to define a sensible class of operators against which to compare our reconstruction operator. We cannot simply choose the usual class of regression operators, since does generally not belong to this class, as pointed out in Section 1. Therefore, we introduce the following (very large) class of “reconstruction operators”:

Definition 2.1(Reconstruction operators).

Let the (centered) random function have a KL representation as in (4). We call every linear operator a “reconstruction operator with respect to ” if for all .

It is important to note that this definition of “reconstruction operators” is specific to the considered process . This should not be surprising, since a best possible linear reconstruction will of course depend on the structure of the relevant random function . The following theorem provides a useful representation of this class of linear operators:

Theorem 2.1(Representation of reconstruction operators).

Let be a “reconstruction operator with respect to ” according to Definition 2.1. Then there exists a unique (deterministic) parameter function such that almost surely

where is a Hilbert space with inner product for all and induced norm .

The space is the Reproducing Kernel Hilbert Space (RKHS) that takes the covariance kernel as its reproducing kernel. By construction, we obtain that the variance of equals the -norm of the parameter function , i.e., .

Let us consider two examples of possible reconstruction operators. While the first example does not belong the class of regression operators, the second example is a regression operator demonstrating the more restrictive model assumptions.

Example 1 - Point of impact:

Consider , i.e., a model with one “impact point” for all missing points . With we have , and hence

(9)

where with

.

Example 2 - Regression operator:

Let be a regression operator (see (2)). Then there exists a such that . Since eigenfunctions can be completed to an orthonormal basis of , we necessarily have that for . Then

(10)

where

with

. Also note that for any we have . This means that for the operator

constitutes a regression operator if and only if in addition to we also have that

(the latter is not satisfied in Example 1).

These examples show that Definition 2.1 leads to a very large class of linear operators which contains the usually considered class of regression operators as a special case. Of course, the class of reconstruction operators as defined by Definition 2.1 also contains much more complex operators than those illustrated in the examples.

Using Theorem 2.1, our reconstruction problem in (3) of finding a “best linear” reconstruction operator minimizing the squared error loss can now be restated in a theoretically precise manner: Find the linear operator which for all minimizes

with respect to all reconstruction operators satisfying for some . In the next subsection we show that the solution is given by the operator defined in (7) which can now be rewritten in the form

(11)

where for and . In particular, Theorem 2.2 below shows that for any , i.e., that is indeed a reconstruction operator according to Definition 2.1.

Remark

In the context of reconstructing functions, problems with the use of regression operators are clearly visible. But the above arguments remain valid for standard functional linear regression, where for some real-valued (centered) response variable with one aims to determine the best linear functional according to the model . Straightforward generalizations of Theorems 2.2 and 2.3 below then show that the optimal functional is given by

where for . Following the arguments of Example 2 it is immediately seen that it constitutes a restrictive, additional condition, to assume that can be rewritten in the form for some .

2.2 Theoretical properties

Result (a) of the following theorem assures that is a reconstruction operator according to Definition 2.1, and result (b) assures unbiasedness.

Theorem 2.2.

Let the (centered) random function have a KL representation as in (4).

(a)

in (7) has a continuous and finite variance function, i.e., for all .

(b)

is unbiased in the sense that for all .

The following theorem describes the fundamental properties of the reconstruction error

and contains the optimality result for our reconstruction operator . Result (a) shows that the reconstruction error is orthogonal to . This result serves as an auxiliary result for result (b) which shows that is the optimal linear reconstruction of . Finally, result (c) allows us to identify cases where can be reconstructed without any reconstruction error.

Theorem 2.3(Optimal linear reconstruction).

Under our setup it holds that:

(a)

For every and ,

(12)

(13)

(b)

For any linear operator

that is a reconstruction operator with respect to , according to Definition 2.1,

(c)

Assume that the underlying process is Gaussian, and let and be two independent copies of the random variable .

Then for all the variance of the reconstruction error can be written as

(14)

where means that for all .

Whether or not a sensible reconstruction of partially observed functions is possible, of course, depends on the character of the underlying process. For very rough and unstructured processes no satisfactory results can be expected. An example is the standard Brownian motion on which is a pure random process with independent increments. If Brownian motions are only observed on an interval , it is well known that the “best” (and only unbiased) prediction of for is the last observed value . This result is consistent with our definition of an “optimal” operator : The covariance function of the Brownian motion is given by , and hence for all and one obtains . Therefore, by (11) and (9) we have for all . Although in this paper we focus on processes that lead to smooth, regularly shaped sample curves, the Brownian motion is of some theoretical interest since it defines a reconstruction operator which obviously does not constitute a regression operator. Also note that

will provide perfect reconstructions if a.s. sample functions are constant for all .

Result (c) of Theorem 2.3 may be useful to identify cases that allow for a perfect reconstruction. By (14) there is no reconstruction error, i.e., for if the event implies that also . This might be fulfilled for very simply structured processes. It is necessarily satisfied for finite dimensional random functions , , as long as the basis functions are linearly independent over .

2.3 A deeper look at the structure of

Remember that the definition of can be extended to an operator . For elements of the observed part the best “reconstruction” of is obviously the observed value itself, and indeed for any (11) yields . Equation (7) then holds with

Since is a continuous function on it follows that the resulting “reconstructed” function is continuous on . In particular, is continuous at any boundary point , and

Equation (7) together with our definition of imply that the complete function on can be represented in the form

(15)

This sheds some additional light on result (14). We will have and if on the segment the process is essentially driven by the same random components as those determining its structure on . Additional random components , not present on , and uncorrelated with , then have to be of minor importance. If the observed interval is sufficiently long, then this may be approximately true for processes with smooth, similarly shaped trajectories. Note that even if for , the eigenfunctions of will usually not coincide with for , since there is no reason to expect that these functions are mutually orthogonal.

3 Estimation

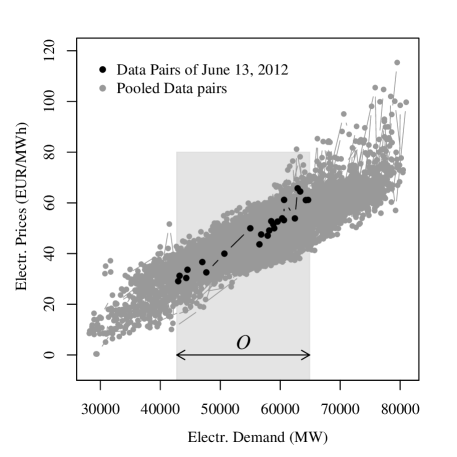

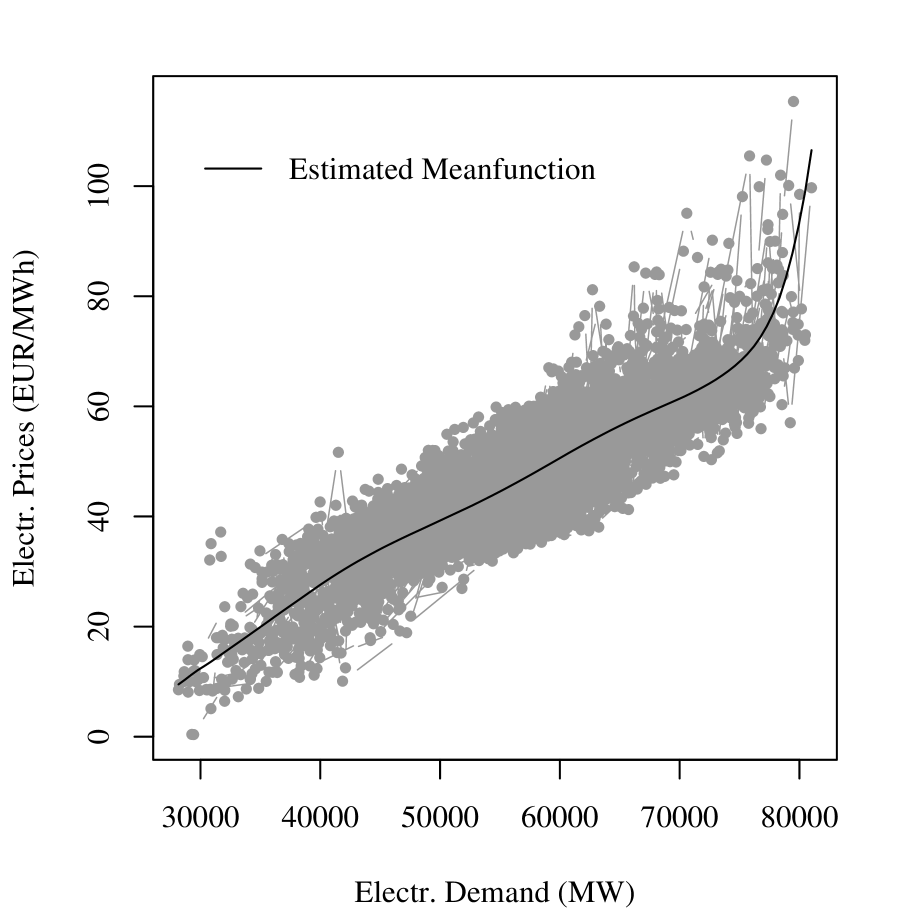

Figure 2: Scatter plot of the observed data pairs .

We typically do not observe a functional trajectory directly, but only its discretization with or without measurement errors. For instance, Figure 1 shows the pre-smoothed functions; however, the actual raw data is shown in Figure 2. Let denote the observable data pairs of a function , where

(16)

and .

For the rest of the paper, we focus on the case where as in our real data application. However, we give detailed descriptions on how to use our methods in the more general cases where consists of several mutually disjoint subintervals. We consider the case where are iid random variables with strictly positive density over the random subinterval , which in practice can be approximated by and . Let the error term be a real iid random variable that is independent from all other stochastic model components and has mean zero and finite (possibly zero) variance with . Motivated by our real data application we will concentrate on the case that is considerably larger than , which also holds in many other important applications.

So far, we have considered centered random functions . Henceforth, we consider non-centered functions and will make the empirical centering explicit in all estimators. As already outlined in Section 1, we propose to estimate by the empirical counterpart of the truncated sum

(17)

where the unknown true values of and are replaced by suitable estimates defined below.

Remember, however, that our data structure in (16) implies that we are faced with two simultaneous estimation problems. One is efficient estimation of for , the other one is the estimation of the underlying function for . There are two possible strategies which can be employed.

The first is motivated by the best basis property (2) and simply consists in using an FPCA-approximation of on . Recall that can be extended to an operator on . For we then obtain , and thus . That is, estimates of for will simultaneously provide estimates of the true function on the observed interval and of the optimal reconstruction on the unobserved interval .

The second approach is to rely on nonparametric curve estimation, e.g., local linear smoothers, to approximate on , while (17) is only used for reconstructing the unobserved part . We then, however, run into the boundary problem already mentioned in the introduction. Let be the boundary point closest to the considered , i.e., if and else. Usually nonparametric estimates of and reconstruction estimates based on (17) will not coincide for or . A correction, leading to continuous function estimates on may then be based on the identity and its truncated version

(18)

In this paper we propose to use the following empirical counterparts of and :

(19)

(20)

where

denotes the LLK estimator of (see (21)),

denotes the LLK estimator of (see (22)),

denotes the LLK estimator of the covariance function (see (23)),

and denote the estimators of the eigenfunctions and eigenvalues (see (24)), and

denote the estimators of the pc-scores (see (25)).

Remark

Estimator (19) can be directly applied in the general case, where consists of a union of finitely many mutually disjoint subintervals . Estimator (20), however, must be adjusted for this general case as follows.

First, consider a point located between the observed intervals and for any . In this case the quantities and in (20) have to be replaced by the linear interpolations

and

with .

Second, for replace

and

by

and

.

Third, for replace

and

by

and

.

In our asymptotic analysis (Section 4) we focus on the case of single subintervals which leads to comprehensible theorems and proofs.

For the LLK estimator is defined by , where

(21)

for . The kernel function is assumed to be a univariate symmetric pdf with compact support such as, e.g., the Epanechnikov kernel (see Assumption A5). The usual kernel constants are given by , and .

The LLK mean estimator is defined by , where

(22)

The LLK estimator is defined as , where

(23)

with raw-covariance points

. Like Yao, Müller and Wang (2005a), we do not include the diagonal raw-covariances for which as these would introduce an estimation bias through taking squares of the error term contained in .

Estimates of the eigenvalues and the eigenfunctions are defined by the corresponding solutions of the empirical eigen-equations

(24)

Remark

The implementation of (24) can be done as usually by discretizing the smoothed covariance using regular grid points , (see, for instance, Rice and Silverman, 1991). For approximating the eigenvalues and eigenfunctions of one needs to construct the matrix from the grid points falling into . In the case of several disjoint intervals the matrix must be assembled from the grid points falling into the intervals , .

Finally, the empirical pc-score is defined by the following integral approximation of :

(25)

where are ordered data pairs for which the ordering is determined through the order sample

In our theoretical analysis we consider as the sample size , where for all . In practice, the truncation parameter can be chosen by one of the usual procedures such as, for instance, Cross Validation or the Fraction of Variance Explained (FVE) criterion.

Alternatively, one can use an adapted version of the GCV criterion in Kraus (2015) in order to define an -specific GCV criterion. For this let denote the index set of the completely observed functions , , with , for instance, with and and define the following vectors by partitioning the complete data-vectors into pseudo-missing and pseudo-observed parts:

This allows us to compute the weighted sum of the residual sum of squares for reconstructions over

where is the number of elements in . The GCV criterion for reconstructing functions over is

(26)

where is the number of elements in , i.e., the number of complete functions.

4 Asymptotic results

Our theoretical analysis analyzes the reconstruction of an arbitrary sample function satisfying .

Our asymptotic results on the convergence of our nonparametric estimators are developed under the following assumptions which are generally close to those in Yao, Müller and

Wang (2005b) and Hall, Müller and

Wang (2006). We additionally allow for weakly dependent time series of random functions , and we consider a different asymptotic setup excluding the case of sparse functional data. Only second-order kernels are employed.

A1 (Stochastic)

For some the conditional random variables

,…, are iid with pdf for all and zero else. For the marginal pdf it is assumed that for all and zero else. The time series , , and are strictly stationary ergodic (functional) time series with finite fourth moments (i.e., in the functional case) and autocovariance functions with geometric decay. I.e., there are constants with and , such that

,

,

, and

for all , where

and

.

The error term is assumed to be independent from all other random variables. The random variables and are assumed to be independent from , which leads to the so-called “missing completely at random” assumption. The event has a strictly positive probability and almost surely.

A2 (Asymptotic scenario) with for all , where and with . Here, is used to denote that as , where is some constant .

A3 (Smoothness)

For : All second order derivatives of

on ,

on ,

on , and of

on

are uniformly continuous and bounded, where is the joint pdf of .

For : All second order derivatives of on

, on ,

on , and of on

are uniformly continuous and bounded, where

is the joint pdf of .

Finally, is a.s. continuously differentiable, and

, and is a.s. twice continuously differentiable.

A4 (Bandwidths)

For estimating :

and

as .

For estimating :

and

as .

For estimating :

and

as ,

where .

A5 (Kernel function)

is a second-order kernel with compact support .

In Assumption A2, we follow Zhang and Chen (2007) and consider a deterministic sample size , where for all . As Hall, Müller and

Wang (2006), Zhang and Chen (2007) and Zhang and Wang (2016) we do not consider random numbers , but if are random, our theory can be considered as conditional on .

While A1-A5 suffice to determine rates of convergence of mean and covariance estimators, it is well-known from the literature that rates of convergence of estimated eigenfunctions will depend on the rate of decay characterizing the convergence of to zero as .

We want to note that for a subinterval the decay of eigenvalues will usually be faster than the rate of decay of the eigenvalues of the complete covariance operator defined on . This is easily seen. Let denote the corresponding eigenfunctions on , and define by for and . For the special case , , inequality (2) then implies that for all we have , since for all .

To complete our asymptotic setup, we consider the reconstruction of arbitrary sample functions observed over an interval with length , where is an (arbitrary) constant. We then impose the following additional assumptions.

A6 (Eigenvalues)

For any subinterval with the ordered eigenvalues have all multiplicity one. Furthermore, there exist some and some , possibly depending on , such that with , and as well as as .

A7 (Eigenfunctions)

For any subinterval with there exists a constant such that (recall that for ).

Assumption A6 requires a polynomial decay of the sequence of eigenvalues. It cannot be tested, but it corresponds to the usual assumption characterizing a majority of work concerning eigenanalysis of functional data, although some authors also consider exponential decays. There exist various types of functional data, but this paper focuses on applications where the true sample functions are smooth and all possess a similar functional structure. This is quite frequent in practice, and in applied papers it is then often found that few functional principal components suffice to approximate sample functions with high accuracy. In view of the best basis property (2) one may then tend to assume that A6 holds for some very large . Indeed, for increasing eigenfunctions will become less and less “smooth” since the number of sign changes will necessarily tend to infinity. If observed trajectories are smooth, then the influence of such high-frequency components must be very small, indicating a very small eigenvalue for large . This is of substantial interest, since the theorems below show that rates of convergence of our final estimators are better the larger .

Assumption A7 imposes a (typical) regularity condition on the structure of the eigenfunctions , since for . For condition is much weaker than the standard assumption of a regression operator which would go along with the requirement . But, for , theory only ensures that (see Theorem 2.3 (a)) and A7 is restrictive in so far as it excludes the possible case that for we have as . We are not sure whether the latter excluded case constitutes a realistic scenario in practical applications, since by (15) it would correspond to the fairly odd situation that for large the high-frequency components possess much larger influence on than on . Nevertheless, we want to emphasize that the arguments used in the proof of our theorems may easily be generalized to prove consistency of our estimators even in this excluded case; however, rates of convergence deteriorate and asymptotic expressions become much more involved.

Theorem 4.1(Preliminary consistency results).

Under Assumptions A1-A5 we have that:

(a)

(ã)

Conditional on :

(b)

, where

and where and for all (see A2 and A4).

If additionally Assumption A6 and A7 hold, we obtain for every subinterval with :

(c)

for all

(d)

where and

.

Related results can be found in Yao, Müller and Wang (2005a), Li and Hsing (2010), and Zhang and Wang (2016). Our proof of results (a)-(b) follows that of Yao, Müller and Wang (2005a), but is more restrictive as we allow only for compact second order kernels. Results (c) and (d) follow from standard arguments as used in Bosq (2000).

Theorem 4.2(Consistency results for ).

Consider an arbitrary and assume that satisfies . For some let . The following results hold then under Assumptions A1-A7, for , , and , as and with , . For any :

(27)

Furthermore, for all

(28)

The theorem tells us that for any the estimator achieves the same rate of convergence. But recall that for we have , and thus can be seen as a nonparametric estimator of . In contrast, for we have , and therefore the distance between and will additionally depend on the reconstruction error .

Note that by the above result the rates of convergence depend on and , and the optimal depends on these quantities in a complex way. However, the situation simplifies if is considerably smaller than such that for . The following corollary then is a direct consequence of (27).

Corollary 4.1.

Under the conditions of Theorem 4.2 additionally assume that . With

we obtain for all

(29)

Let us consider the simple case where for all , and recall that the main difference between and consists in the way of estimating on the observed interval . is based on local linear smoothing of the individual data , , and the associated estimation error of order appears in result (28). Twice continuously differentiable functions are assumed, and using only individual data it is well-known that constitutes the optimal rate of convergence of nonparametric function estimators with respect to this smoothness class.

In contrast, combines information from all sample curves in order to estimate for . If all samples curves are structurally similar in the sense that A6 holds for a very large , then (29) implies that the rate of convergence of is very close to the parametric rate . That is, under the conditions of Corollary 4.1 ( smaller than and ) it becomes advantageous to use instead of for estimating on the observed interval, since may provide faster rates of convergence than the rate achieved by nonparametric smoothing of individual data.. We believe that this is an interesting result in its own right, which to our knowledge has not yet been established in the literature.

5 Iterative reconstruction algorithm

So far we have focused on the regular situation where the covariance function is estimable for all points . Under this situation we can reconstruct the entire missing parts of the functions, such that the reconstructed functions with

(32)

are identifiable for all .

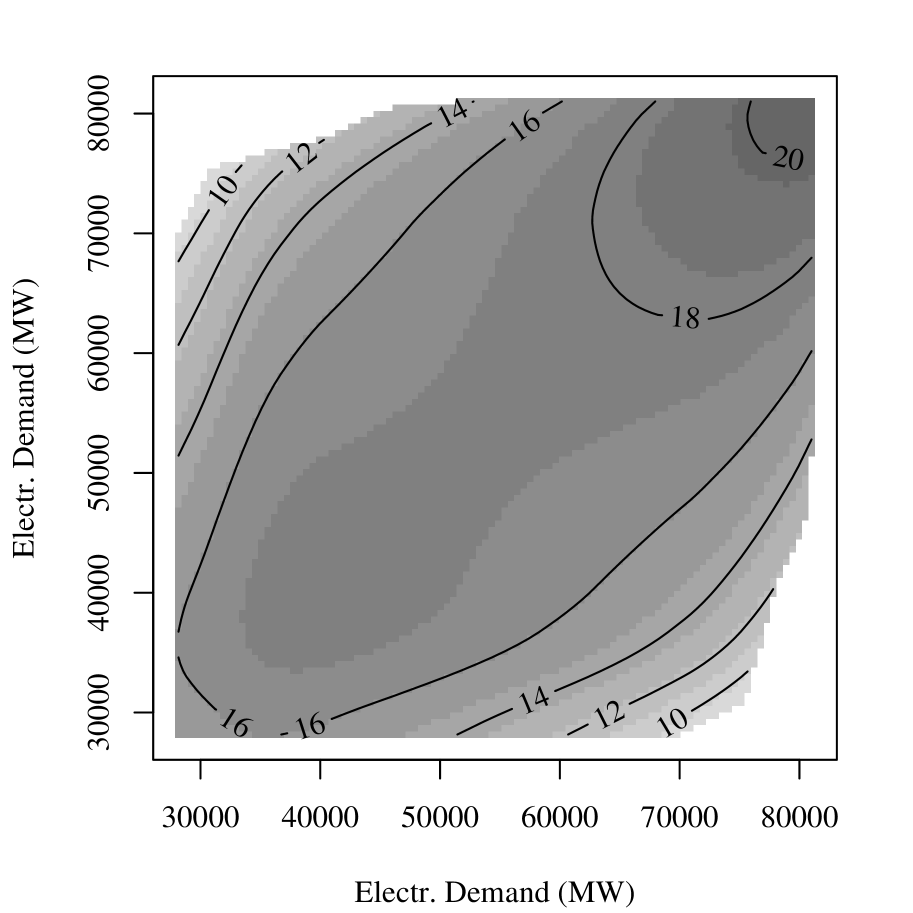

In our application, however, we face the more restrictive situation where the mean function can still be estimated for all , but where there is no information on for large values ; see Figure 5. This makes it impossible to reconstruct the entire missing part of a function, such that cannot be identified for all .

In order to reconstruct functions that cover the total interval , or at least a very large part of it, we propose successively plugging in the optimal reconstructions computed for subintervals. In the following we describe our iterative reconstruction algorithm:

Denote the originally observed interval as and compute

th Step ()

Choose a new “observed” interval and use with as the new “observed” fragment. Compute

Join the reconstructed fragments to form the new “observed” fragment on and repeat the th step.

Stopping

Stop if or if .

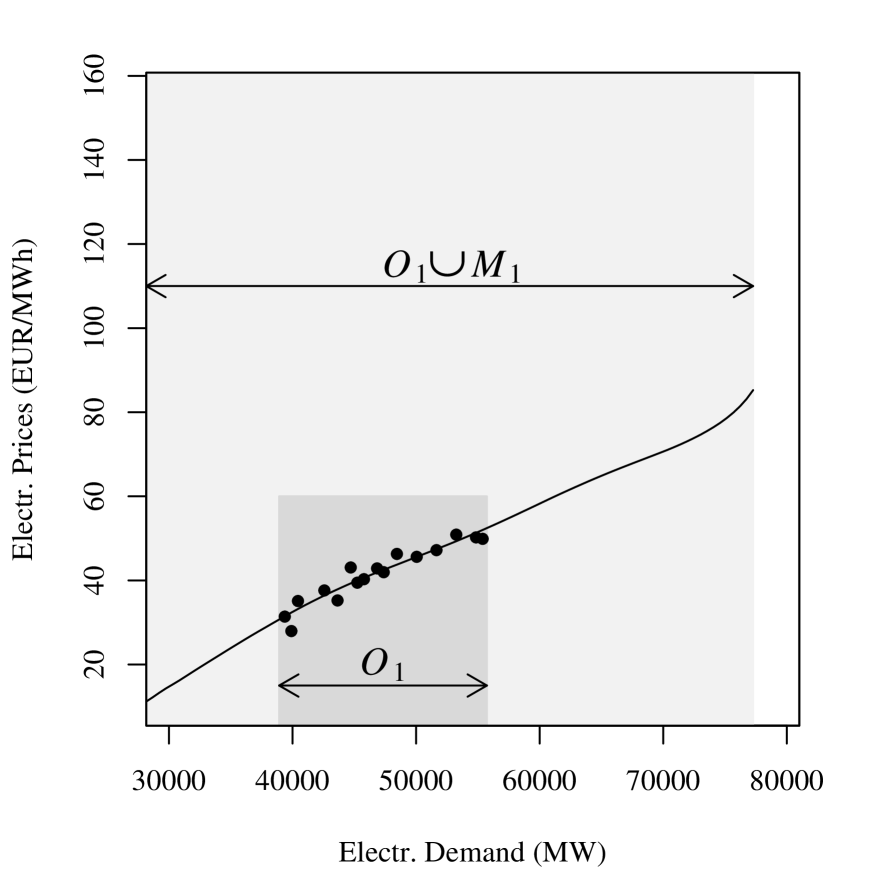

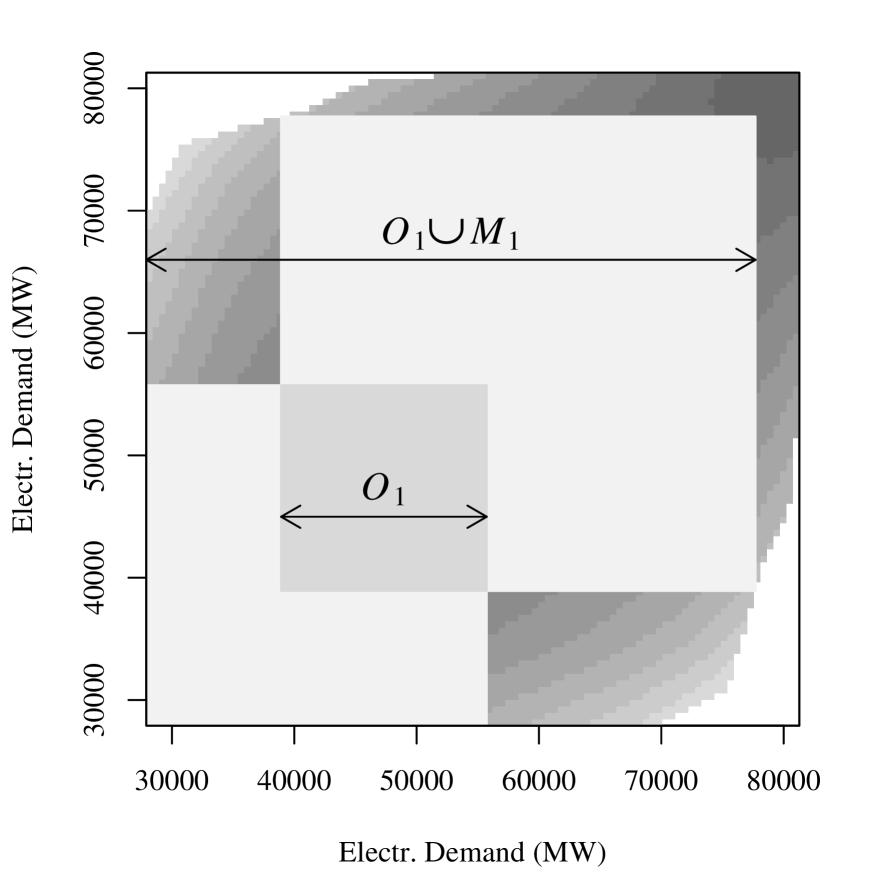

This algorithm has to be applied to every fragment . An exemplary first step of the reconstruction algorithm is shown in Figure 3. The subinterval is determined by the original interval and the extend to which can be estimated (see right panel). The function shown in the left panel still lacks the upper fragment for values such that a second step of the reconstruction algorithm is necessary.

1st Step of the Reconstruction Algorithm

Figure 3: Explanatory plots for the first run of the reconstruction algorithm.

This second step is shown in Figure 4. There the new interval is chosen such that the still missing upper fragment becomes reconstructible. The new large interval contains the missing upper fragments, such that we can stop the algorithm.

2nd Step of the Reconstruction Algorithm

Figure 4: Explanatory plots for the second run of the reconstruction algorithm.

The choice of the subset in the th step is crucial. On the one hand, should be chosen as large as possible to contain as much information as possible. On the other hand, must be chosen such that contains a still missing fragment which is – in tendency – met by smaller intervals . That is, any efficient implementation of the algorithm and the choice of depends on the extend to which can be estimated. A simple practical implementation is described in our application in Section 7.

In each iteration of the reconstruction algorithm we accumulate reconstruction errors. The following proposition provides a theoretical description of this accumulation of reconstruction errors:

For simplicity, let for all and consider the second step of the reconstruction algorithm.

Let denote a missing value that we aim to reconstruct by using which is taken from the reconstruction of the st Step. The mean squared reconstruction error can then be approximated as following:

where and are the hypothetical reconstruction operators if were fully observed over , and were observable.

That is, the mean squared reconstruction error in the second run of the iterative algorithm is bounded from above by the two hypothetical mean squared reconstruction errors of and .

6 Simulation study

We compare the finite sample performance of our reconstruction operators (19) and (20) with that of the PACE method proposed by Yao, Müller and Wang (2005a) and the functional linear ridge regression model proposed by Kraus (2015). A further interesting comparison method might be the functional linear regression model for sparse functional data as considered by Yao, Müller and

Wang (2005b). Note, however, that this regression model becomes equivalent to the PACE method of Yao, Müller and Wang (2005a), when used to predict the trajectory of given its own sparse, i.e., irregular and noise contaminated measurements (see Appendix B.2 in the supplementary paper Kneip and Liebl (2019) for more detailed explanations regarding this equivalence).

The following acronyms are used to refer to the different reconstruction methods considered in this simulation study:

ANo

in (19) is denoted as ANo to indicate that this method involves No Alignment of the estimate of and the reconstruction of .

ANoCE

Equivalent to ANo, but with replacing the integral scores (25) using the following Conditional Exactions (CE) scores adapted from Yao, Müller and Wang (2005a)

(33)

where

,

,

, with if and zero else, and with and as defined in (24). The estimate of the error variance, , is computed using LLK estimators as described in equation (2) of Yao, Müller and Wang (2005a).

AYes

in (20) is denoted as AYes to indicate that this method involves an alignment of the estimate of and the reconstruction of .

AYesCE

Equivalent to AYes, but with replacing the integral scores (25) by the conditional exaction scores of (33).

PACE

The method of Yao, Müller and Wang (2005a), who approximate the missing and observed parts jointly using the truncated Karhunen-Loève decomposition with conditional expectation scores

The functional linear ridge regression model of Kraus (2015).

The idea of using the conditional expectation scores (33) in ANoCE and AYesCE as an alternative to the integral scores (25) in ANo and AYes is inspired by a comment of one of the anonymous referees, who correctly pointed out that the integral scores (25) might be instable for irregular and noisy data. PACE also uses condition expectation scores, but is fundamentally different from ANoCE and AYesCE. While PACE uses approximations of the classical eigenfunctions , the classical eigenvalues , and the classical scores , ANoCE and AYesCE use approximations of the reconstructive eigenfunctions , the eigenvalues , and the scores with respect to the partially observed domain .

The truncation parameters for ANo, ANoCE, AYes, AYesCE, and PACE are selected by minimizing the GCV criterion in (26). For PACE, we do not use the AIC-type criterion as proposed by Yao, Müller and Wang (2005a), since this criterion determines a “global” truncation parameter , which performs worse than our local, i.e., -specific truncation parameter . The ridge regularization parameter for KRAUS is determined using the GCV criterion as described in Kraus (2015).

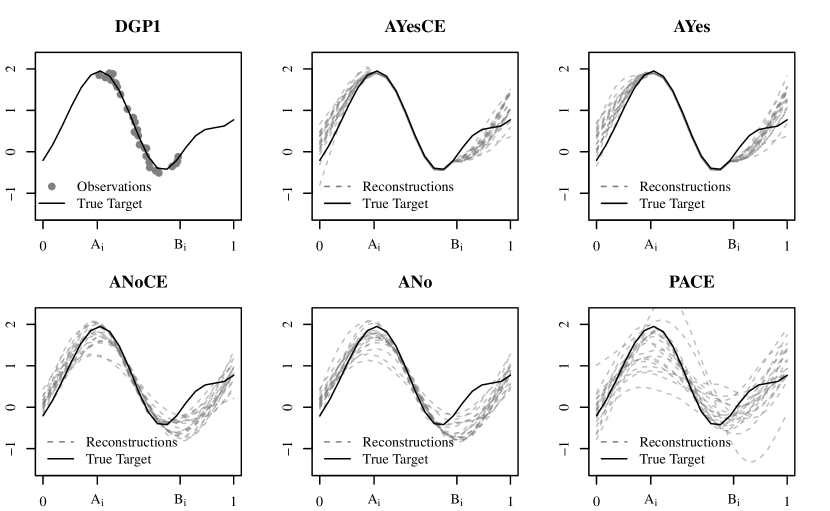

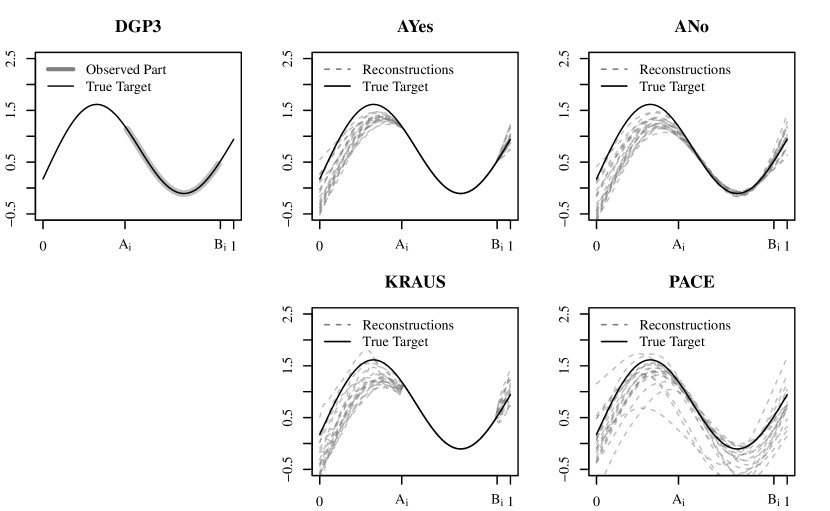

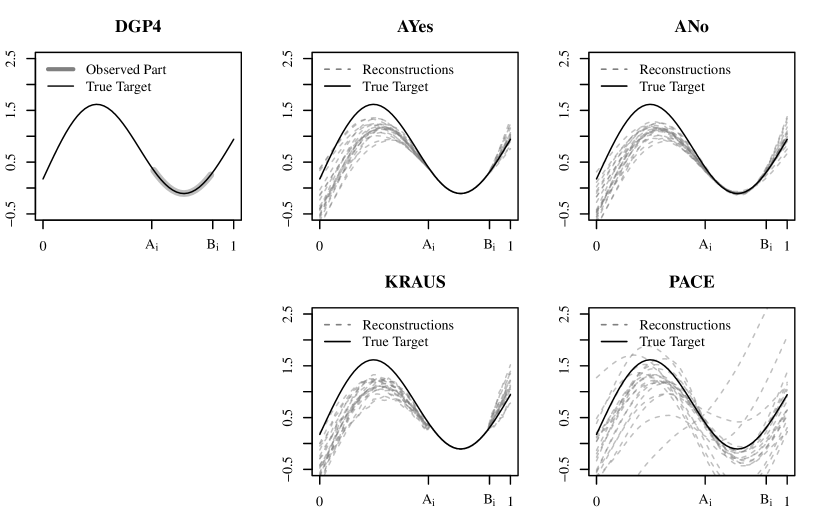

We consider four different Data Generating Processes (DGPs). DGP1 and DGP2 comprise irregular evaluation points and measurement errors which facilitates the comparison of ANo, ANoCE, AYes, AYesCE and the PACE method. DGP3 and DGP4 comprise regular evaluation points and no measurements errors which facilitates the comparison of ANo, AYes, PACE and the KRAUS method. For all simulations we set .

DGP1 The data points

are generated according to

with error term

and random function

,

where

,

, and

with

.

The evaluation points are generated as , where with probability , and and with probability , . That is, about one half of the sample consists of partially observed functions with mean interval-width .

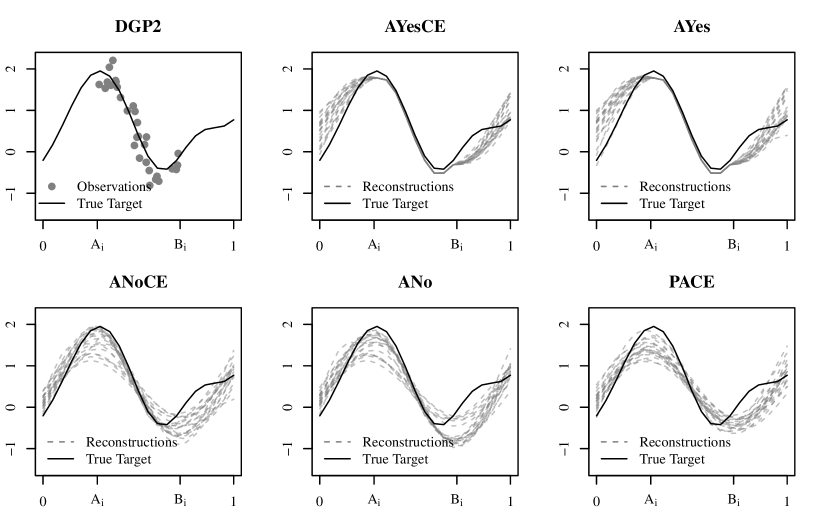

DGP2 Equivalent to DGP1, except for a larger noise component with .

DGP3 The data points

are generated according to

with random function

,

where

,

, and

with

.

The evaluation points are equidistant grid points , with , where all points are set to NA. With probability , and and with probability , .

DGP4 Equivalent to DGP3, but with and . That is, DGP4 has smaller and therefore more challenging fragments than DGP3.

For each DGP, we generate 50 different targets , , where each target is partitioned into a (non-degenerated) missing part and an observed part . Each of these targets are reconstructed in each of the simulation runs with sample sizes for DGP1-DGP4 and for DGP1 and DGP2.

Let denote the reconstructed function in simulation run using one of the reconstruction methods ANo, ANoCE, AYes, AYesCE, PCAE, or KRAUS. For each target , we compute the integrated mean squared error, the integrated squared bias, and the integrated variance,

where

. The finite sample performance is evaluated using the averages over all 50 targets,

Table 1: Simulation results for DGP1.

DGP

Method

MSE

MSE

Var

DGP1

50

15

AYesCE

1.00

0.161

0.135

0.025

DGP1

50

15

AYes

1.02

0.164

0.139

0.025

DGP1

50

15

ANoCE

1.38

0.222

0.199

0.023

DGP1

50

15

ANo

1.39

0.224

0.200

0.024

DGP1

50

15

PACE

10.49

1.685

0.259

1.426

DGP1

50

30

AYesCE

1.00

0.136

0.112

0.024

DGP1

50

30

AYes

1.00

0.137

0.113

0.024

DGP1

50

30

ANoCE

1.48

0.202

0.173

0.029

DGP1

50

30

ANo

1.53

0.209

0.180

0.029

DGP1

50

30

PACE

5.19

0.707

0.131

0.576

DGP1

100

15

AYesCE

1.00

0.131

0.112

0.018

DGP1

100

15

AYes

1.00

0.131

0.114

0.017

DGP1

100

15

ANoCE

1.58

0.207

0.191

0.017

DGP1

100

15

ANo

1.61

0.211

0.194

0.017

DGP1

100

15

PACE

8.74

1.145

0.154

0.991

DGP1

100

30

AYes

1.00

0.125

0.108

0.017

DGP1

100

30

AYesCE

1.01

0.126

0.109

0.017

DGP1

100

30

ANoCE

1.36

0.170

0.146

0.023

DGP1

100

30

ANo

1.45

0.181

0.158

0.023

DGP1

100

30

PACE

3.59

0.448

0.123

0.325

MSE

Table 2: Simulation results for DGP2.

DGP

Method

MSE

MSE

Var

DGP2

50

15

AYesCE

1.00

0.198

0.173

0.025

DGP2

50

15

AYes

1.04

0.207

0.179

0.027

DGP2

50

15

PACE

1.07

0.212

0.174

0.039

DGP2

50

15

ANoCE

1.14

0.227

0.203

0.023

DGP2

50

15

ANo

1.16

0.230

0.204

0.026

DGP2

50

30

AYesCE

1.00

0.189

0.167

0.022

DGP2

50

30

AYes

1.01

0.192

0.169

0.023

DGP2

50

30

PACE

1.09

0.206

0.167

0.039

DGP2

50

30

ANoCE

1.14

0.215

0.188

0.027

DGP2

50

30

ANo

1.16

0.219

0.190

0.028

DGP2

100

15

AYesCE

1.00

0.178

0.161

0.017

DGP2

100

15

AYes

1.01

0.180

0.162

0.018

DGP2

100

15

PACE

1.08

0.193

0.165

0.028

DGP2

100

15

ANoCE

1.20

0.213

0.198

0.015

DGP2

100

15

ANo

1.21

0.216

0.199

0.018

DGP2

100

30

AYesCE

1.00

0.177

0.159

0.018

DGP2

100

30

AYes

1.03

0.181

0.162

0.020

DGP2

100

30

PACE

1.03

0.183

0.153

0.029

DGP2

100

30

ANoCE

1.07

0.189

0.167

0.023

DGP2

100

30

ANo

1.12

0.197

0.174

0.024

MSE

The simulation study is implemented using the R-package ReconstPoFD which can be downloaded and installed from the second author’s GitHub account.

Table 1 shows the simulation results for DGP1. The methods (ANo, ANoCE, AYes, AYesCE and PACE) are ranked according to their MSE which is defined by the method’s MSE-value relative to the lowest MSE-value within the comparison group. The rankings are stable for all sample sizes and . The AYesCE reconstruction method shows the best performance. The AYes method, which uses integral scores instead of conditional expectation scores, is only marginally less efficient than AYesCE. Our non-alignment methods ANoCE and ANo are ranked third and fourth. The PACE method of Yao, Müller and Wang (2005a), originally proposed for sparse functional data analysis, shows a rather poor performance. The reason for this is that PACE adds the variance of the measurement error to the diagonal of the discretized covariance matrix, which has a regularization effect on the generally ill-posed inversion problem. For DGP1, however, the variance of the error term is rather small which results in a too small regularization of the inverse.

Table 2 shows the simulation results for DGP2. DGP2 is equivalent to DGP1 except for a larger variance of the error term. Our alignment methods AYesCE and AYes still show the best performance. However, having a larger variance leads to a better regularization of the inverse problem involved in the PACE method, such that PACE is ranked third. Our non-alignment methods ANoCE and ANo are ranked fourth and fifth. Figures 7 and 8 in Appendix C of the supplementary paper Kneip and Liebl (2019) provide graphical illustrations of the different reconstruction results as well as a visual impression of the different signal-to-noise ratios in DGP1 and DGP2.

Table 3: Simulation results for DGP3 and DGP4.

DGP

Method

MSE

MSE

Var

DGP3

50

AYes

1.00

0.168

0.131

0.037

DGP3

50

PACE

1.33

0.223

0.099

0.124

DGP3

50

ANo

1.40

0.234

0.178

0.056

DGP3

50

KRAUS

1.52

0.254

0.205

0.049

DGP3

100

AYes

1.00

0.142

0.120

0.022

DGP3

100

PACE

1.26

0.179

0.081

0.098

DGP3

100

KRAUS

1.29

0.184

0.151

0.033

DGP3

100

ANo

1.36

0.194

0.158

0.035

DGP4

50

AYes

1.00

0.276

0.220

0.056

DGP4

50

ANo

1.11

0.307

0.247

0.060

DGP4

50

KRAUS

1.20

0.330

0.269

0.061

DGP4

50

PACE

41.93

11.564

0.313

11.252

DGP4

100

AYes

1.00

0.232

0.202

0.030

DGP4

100

KRAUS

1.11

0.258

0.222

0.035

DGP4

100

ANo

1.12

0.261

0.227

0.034

DGP4

100

PACE

3.59

0.834

0.151

0.682

MSE

Table 3 shows the simulation results for DGP3 and DGP4 comparing the methods ANo, AYes, PACE and KRAUS. Here, the alignment method AYes shows by far the best performance for all sample sizes and for both DGPs. The partially very bad performance of PACE is due to the missing measurement error in DGP3 and DGP4, which results in a missing regularization of the inverse problem involved in the PACE method. Furthermore, PACE is designed for the case where one observes only a few noisy discretization points per function, but these points should be distributed over the total domain . For the considered DGPs, however, the discretization points are only observed within challenging small subdomains . Graphical illustrations of the different reconstruction results for DGP3 and DGP4 are provided in Figures 9 and 10 in Appendix C of the supplementary paper Kneip and Liebl (2019).

Summing up, in all DGPs the best performing reconstruction method are our alignment methods AYesCE and AYes. For discretized functional data plus measurement errors it is advantageous to use the alignment method AYesCE with involves conditional expectation scores.

7 Application

Our functional data point of view on electricity spot prices provides a practical framework that is useful for forecasting electricity spot prices (Liebl, 2013; Weron, 2014) and for testing price differences (Liebl, 2019). In the following, we focus on the problem of reconstructing the partially observed price-functions, which is highly relevant for practitioners who need complete price functions for doing comparative statics, i.e., a ceteris-paribus analysis of price effects with respect to changes in electricity demand (cf. Weigt, 2009; Hirth, 2013).

The data for our analysis come from three different sources. Hourly spot prices of the German electricity market are provided by the European Energy Power Exchange (EPEX) (www.epexspot.com), hourly values of Germany’s gross electricity demand, , and net-imports of electricity from other countries, , are provided by the European Network of Transmission System Operators for Electricity (www.entsoe.eu), and German wind and solar power infeed data are provided by the transparency platform of the European energy exchange (www.eex-transparency.com). The data dimensions are given by hours and working days between March 15, 2012 and March 14, 2013. Very few () data pairs with prices EUR/MWh and MW are considered as outliers and reset to .

The German electricity market, like many other electricity markets, provides purchase guarantees for Renewable Energy Sources (RES). Therefore, the relevant variable for pricing at the energy exchange is electricity demand minus electricity infeeds from RES (Nicolosi, 2010). Correspondingly, the relevant values of electricity demand are defined as electricity demand minus infeeds from RES and plus net-imports from other countries, i.e., , where . The effect of further RES such as biomass is still negligible for the German electricity market.

Figure 5: Left Panel: Estimated mean function plus a scatter plot of the data pairs . Right Panel: Contour plot of the estimated covariance function. The white regions reflect the outer off-diagonal parts which are infeasible to estimate.

The estimated mean and covariance functions are shown in Figure 5. The outer off-diagonal parts of the covariance function cannot be estimated, since these parts of the domain are not covered by data pairs , . In order to reconstruct the entire missing parts , we use the AYesCE estimator, which showed a very good performance in our simulation studies, and our iterative reconstruction Algorithm 5.1 implemented as follows. We use three iterations for each partially observed price function. In the first step, we use the information with respect to the original observations in order to reconstruct the missing parts as far as possible. In the second step, we use the upper half of the reconstructed curve and try to reconstruct possibly further missing upper fragments. In the final step we use the lower half of and try to reconstruct possibly further missing lower fragments.

This approach allows us to recover 91% of the price functions over the total support (Figure 6). Note that the price functions with negative electricity prices are perfectly plausible. Negative prices are an important market-feature of the EPEX (see, for instance, Nicolosi, 2010; Fanone, Gamba and Prokopczuk, 2013; Cludius et al., 2014). Electricity producers are willing to sell electricity at negative prices (i.e., to pay for delivering electricity) if shutting off and restarting their power plants is more expensive than selling their electricity at negative prices. That is, the reconstructed price functions are conform with the specific market design of the EPEX and may be useful for a variety of further subsequent analysis using classical methods of functional data analysis.

Figure 6: Recovered functions (gray) and the original partially observed functions (black).

Acknowledgements

We would like to thank the referees and the editors for their constructive feedback which helped to improve this research work.

{supplement}\stitle

Supplemental Paper

\slink[doi]COMPLETED BY THE TYPESETTER

\sdescriptionThe supplemental paper contains the proofs of our theoretical results.

References

Bosq (2000){bbook}[author]

\bauthor\bsnmBosq, \bfnmDenis\binitsD.

(\byear2000).

\btitleLinear Processes in Function Spaces: Theory and Applications

\bvolume149.

\bpublisherSpringer Verlag.

\endbibitem

Cai and Hall (2006){barticle}[author]

\bauthor\bsnmCai, \bfnmT Tony\binitsT. T. and \bauthor\bsnmHall, \bfnmPeter\binitsP.

(\byear2006).

\btitlePrediction in functional linear regression.

\bjournalThe Annals of Statistics

\bvolume34

\bpages2159–2179.

\endbibitem

Cardot, Mas and Sarda (2007){barticle}[author]

\bauthor\bsnmCardot, \bfnmHervé\binitsH.,

\bauthor\bsnmMas, \bfnmAndré\binitsA. and \bauthor\bsnmSarda, \bfnmPascal\binitsP.

(\byear2007).

\btitleCLT in functional linear regression models.

\bjournalProbability Theory and Related Fields

\bvolume138

\bpages325–361.

\endbibitem

Cludius et al. (2014){barticle}[author]

\bauthor\bsnmCludius, \bfnmJohanna\binitsJ.,

\bauthor\bsnmHermann, \bfnmHauke\binitsH.,

\bauthor\bsnmMatthes, \bfnmFelix Chr\binitsF. C. and \bauthor\bsnmGraichen, \bfnmVerena\binitsV.

(\byear2014).

\btitleThe merit order effect of wind and photovoltaic electricity generation

in Germany 2008–2016: Estimation and distributional implications.

\bjournalEnergy Economics

\bvolume44

\bpages302–313.

\endbibitem

Delaigle and

Hall (2013){barticle}[author]

\bauthor\bsnmDelaigle, \bfnmAurore\binitsA. and \bauthor\bsnmHall, \bfnmPeter\binitsP.

(\byear2013).

\btitleClassification using censored functional data.

\bjournalJournal of the American Statistical Association

\bvolume108

\bpages1269–1283.

\endbibitem

Delaigle and Hall (2016){barticle}[author]

\bauthor\bsnmDelaigle, \bfnmA\binitsA. and \bauthor\bsnmHall, \bfnmP\binitsP.

(\byear2016).

\btitleApproximating fragmented functional data by segments of Markov chains.

\bjournalBiometrika

\bvolume103

\bpages779–799.

\endbibitem

Delaigle et al. (2018){barticle}[author]

\bauthor\bsnmDelaigle, \bfnmAurore\binitsA.,

\bauthor\bsnmHall, \bfnmPeter\binitsP.,

\bauthor\bsnmHuang, \bfnmWei\binitsW. and \bauthor\bsnmKneip, \bfnmAlois\binitsA.

(\byear2018).

\btitleEstimating the covariance of fragmented and other incompletely observed

functional data.

\bjournalWorking Paper.

\endbibitem

Descary and Panaretos (2018){barticle}[author]

\bauthor\bsnmDescary, \bfnmMarie-Hélène\binitsM.-H. and \bauthor\bsnmPanaretos, \bfnmVictor M\binitsV. M.

(\byear2018).

\btitleRecovering covariance from functional fragments.

\bjournalarXiv:1708.02491.

\endbibitem

Fanone, Gamba and Prokopczuk (2013){barticle}[author]

\bauthor\bsnmFanone, \bfnmEnzo\binitsE.,

\bauthor\bsnmGamba, \bfnmAndrea\binitsA. and \bauthor\bsnmProkopczuk, \bfnmMarcel\binitsM.

(\byear2013).

\btitleThe case of negative day-ahead electricity prices.

\bjournalEnergy Economics

\bvolume35

\bpages22–34.

\endbibitem

Goldberg, Ritov and

Mandelbaum (2014){barticle}[author]

\bauthor\bsnmGoldberg, \bfnmY.\binitsY.,

\bauthor\bsnmRitov, \bfnmY.\binitsY. and \bauthor\bsnmMandelbaum, \bfnmA.\binitsA.

(\byear2014).

\btitlePredicting the continuation of a function with applications to call

center data.

\bjournalJournal of Statistical Planning and Inference

\bvolume147

\bpages53–65.

\endbibitem

Gromenko

et al. (2017){barticle}[author]

\bauthor\bsnmGromenko, \bfnmOleksandr\binitsO.,

\bauthor\bsnmKokoszka, \bfnmPiotr\binitsP.,

\bauthor\bsnmSojka, \bfnmJan\binitsJ. \betalet al.

(\byear2017).

\btitleEvaluation of the cooling trend in the ionosphere using functional

regression with incomplete curves.

\bjournalThe Annals of Applied Statistics

\bvolume11

\bpages898–918.

\endbibitem

Hall and Horowitz (2007){barticle}[author]

\bauthor\bsnmHall, \bfnmPeter\binitsP. and \bauthor\bsnmHorowitz, \bfnmJoel L\binitsJ. L.

(\byear2007).

\btitleMethodology and convergence rates for functional linear regression.

\bjournalThe Annals of Statistics

\bvolume35

\bpages70–91.

\endbibitem

Hall, Müller and

Wang (2006){barticle}[author]

\bauthor\bsnmHall, \bfnmP\binitsP.,

\bauthor\bsnmMüller, \bfnmHans-Georg\binitsH.-G. and \bauthor\bsnmWang, \bfnmJane-Ling\binitsJ.-L.

(\byear2006).

\btitleProperties of principal component methods for functional and

longitudinal data analysis.

\bjournalThe Annals of Statistics

\bvolume34

\bpages1493–1517.

\endbibitem

Hirth (2013){barticle}[author]

\bauthor\bsnmHirth, \bfnmLion\binitsL.

(\byear2013).

\btitleThe market value of variable renewables: The effect of solar wind power

variability on their relative price.

\bjournalEnergy Economics

\bvolume38

\bpages218–236.

\endbibitem

Horváth and

Kokoszka (2012){bbook}[author]

\bauthor\bsnmHorváth, \bfnmLajos\binitsL. and \bauthor\bsnmKokoszka, \bfnmPiotr\binitsP.

(\byear2012).

\btitleInference for Functional Data with Applications

\bvolume200.

\bpublisherSpringer.

\endbibitem

Kneip and Liebl (2019){barticle}[author]

\bauthor\bsnmKneip, \bfnmAlois\binitsA. and \bauthor\bsnmLiebl, \bfnmDominik\binitsD.

(\byear2019).

\btitleSupplement to “On the Optimal Reconstruction of Partially Observed

Functional Data”.

\endbibitem

Kraus (2015){barticle}[author]

\bauthor\bsnmKraus, \bfnmD\binitsD.

(\byear2015).

\btitleComponents and completion of partially observed functional data.

\bjournalJournal of the Royal Statistical Society: Series B (Statistical

Methodology)

\bvolume77

\bpages777–801.

\endbibitem

Li and Hsing (2010){barticle}[author]

\bauthor\bsnmLi, \bfnmYehua\binitsY. and \bauthor\bsnmHsing, \bfnmTailen\binitsT.

(\byear2010).

\btitleUniform convergence rates for nonparametric regression and principal

component analysis in functional/longitudinal data.

\bjournalThe Annals of Statistics

\bvolume38

\bpages3321–3351.

\endbibitem

Liebl (2013){barticle}[author]

\bauthor\bsnmLiebl, \bfnmD.\binitsD.

(\byear2013).

\btitleModeling and forecasting electricity spot prices: A functional data

perspective.

\bjournalThe Annals of Applied Statistics

\bvolume7

\bpages1562–1592.

\endbibitem

Liebl (2019){barticle}[author]

\bauthor\bsnmLiebl, \bfnmD.\binitsD.

(\byear2019).

\btitleNonparametric testing for differences in electricity prices: The case

of the Fukushima nuclear accident.

\bjournalThe Annals of Applied Statistics, accepted.

\endbibitem

Nicolosi (2010){barticle}[author]

\bauthor\bsnmNicolosi, \bfnmMarco\binitsM.

(\byear2010).

\btitleWind power integration and power system flexibility – An empirical

analysis of extreme events in Germany under the new negative price regime.

\bjournalEnergy Policy

\bvolume38

\bpages7257–7268.

\endbibitem

Ramsay and

Silverman (2005){bbook}[author]

\bauthor\bsnmRamsay, \bfnmJ O\binitsJ. O. and \bauthor\bsnmSilverman, \bfnmB W\binitsB. W.

(\byear2005).

\btitleFunctional Data Analysis,

\bedition2. ed.

\bseriesSpringer Series in Statistics.

\bpublisherSpringer.

\endbibitem

Rice and Silverman (1991){barticle}[author]

\bauthor\bsnmRice, \bfnmJohn A\binitsJ. A. and \bauthor\bsnmSilverman, \bfnmBernard W\binitsB. W.

(\byear1991).

\btitleEstimating the mean and covariance structure nonparametrically when the

data are curves.

\bjournalJournal of the Royal Statistical Society. Series B (Methodological)

\bpages233–243.

\endbibitem

Ruppert and Wand (1994){barticle}[author]

\bauthor\bsnmRuppert, \bfnmD.\binitsD. and \bauthor\bsnmWand, \bfnmM. P.\binitsM. P.

(\byear1994).

\btitleMultivariate locally weighted least squares regression.

\bjournalThe Annals of Statistics

\bvolume22

\bpages1346–1370.

\endbibitem

Weigt (2009){barticle}[author]

\bauthor\bsnmWeigt, \bfnmHannes\binitsH.

(\byear2009).

\btitleGermany’s wind energy: The potential for fossil capacity replacement

and cost saving.

\bjournalApplied Energy

\bvolume86

\bpages1857–1863.

\endbibitem

Weron (2014){barticle}[author]

\bauthor\bsnmWeron, \bfnmRafał\binitsR.

(\byear2014).

\btitleElectricity price forecasting: A review of the state-of-the-art with a

look into the future.

\bjournalInternational Journal of Forecasting

\bvolume30

\bpages1030–1081.

\endbibitem

Yao, Müller and Wang (2005a){barticle}[author]

\bauthor\bsnmYao, \bfnmF\binitsF.,

\bauthor\bsnmMüller, \bfnmHans-Georg\binitsH.-G. and \bauthor\bsnmWang, \bfnmJane-Ling\binitsJ.-L.

(\byear2005a).

\btitleFunctional data analysis for sparse longitudinal data.

\bjournalJournal of the American Statistical Association

\bvolume100

\bpages577–590.

\endbibitem

Yao, Müller and

Wang (2005b){barticle}[author]

\bauthor\bsnmYao, \bfnmFang\binitsF.,

\bauthor\bsnmMüller, \bfnmHans-Georg\binitsH.-G. and \bauthor\bsnmWang, \bfnmJane-Ling\binitsJ.-L.

(\byear2005b).

\btitleFunctional linear regression analysis for longitudinal data.

\bjournalThe Annals of Statistics

\bvolume33

\bpages2873–2903.

\endbibitem

Zhang and Chen (2007){barticle}[author]

\bauthor\bsnmZhang, \bfnmJin-Ting\binitsJ.-T. and \bauthor\bsnmChen, \bfnmJianwei\binitsJ.

(\byear2007).

\btitleStatistical inferences for functional data.

\bjournalThe Annals of Statistics

\bvolume35

\bpages1052–1079.

\endbibitem

Zhang and Wang (2016){barticle}[author]

\bauthor\bsnmZhang, \bfnmXiaoke\binitsX. and \bauthor\bsnmWang, \bfnmJane-Ling\binitsJ.-L.

(\byear2016).

\btitleFrom sparse to dense functional data and beyond.

\bjournalThe Annals of Statistics

\bvolume44

\bpages2281–2321.

\endbibitem

\printaddressnum

1

Supplementary paper for:

On the Optimal Reconstruction of Partially Observed Functional Data

by Alois Kneip and Dominik Liebl

Content

In the following we give the proofs of our theoretical results. The main steps in our proofs of Theorems 4.1 and 4.2 are as in Yao, Müller and Wang (2005a). Though, by contrast to Yao, Müller and Wang (2005a), we allow for a time series context (see Assumption A1), impose more restrictive assumptions on the kernel function (see Assumption A5), and consider a different asymptotic setup (see Assumption A2). Appendix B contains further explanations and Appendix C contains visualizations of our simulation results.

Appendix A Proofs

Proof of Theorem 2.1:

For every linear operator that is a reconstruction operator with respect to according to Def. 2.1, we have that

(35)

Existence: Writing as for some and computing again the variance of yields that

(36)

Since (35) and (36) must be equal, we have that for all , which establishes that there exits a for every reconstruction .

Uniqueness: Assume that there is an alternative such that for all . Then

for all or equivalently

for all which shows that .

Proof of Theorem 2.2, part (a):

First, note that continuity of implies continuity of . Second, note that for any and every , we have

(37)

But this implies that converges to a fixed limit as for all .

Part (b): Follows directly from observing that for all .

Proof of Theorem 2.3, part (a):

For all we have that

From the definition in (6) we get that , which leads to for all .

This proves (12), while (13) directly follows from the definition of .

Part (b):

By Theorem 2.1 there exists a unique such that

By (12) and the orthogonality property of the least squares projection we thus obtain

Part (c):

Observe that for all and . Rearranging and using that for all and all yields . From result (a) we know that and are orthogonal and therefore uncorrelated for all and all , that is, . Under the assumption of an independent Gaussian process, we have then independence between and , such that

where means that for all . For the two random functions and we can write and . It follows from the definition of in (6) that for all , if and only if . Therefore,

for all .

Proof of Theorem 4.1

Note that under Assumption A2, the asymptotic rates of convergence of the LLK estimators

(see (21)),

(see (22)), and

(see (23)) are asymptotically equivalent to the scenario, where . Therefore, we consider the simplified case of a common number of discretization points .

For proofing the results in Theorem 4.1 we make use of the following two lemmas:

Lemma A.1.

Define

(38)

where

Then, under Assumptions A1-A5,

where , ,

,

, and .

Lemma A.2.

Define

(39)

where

Then, under Assumptions A1-A5,

where , ,

,

, and

.

Proof of Lemma A.1: Remember that implies that

, therefore, we focus in the

following on , where . Adding a zero and applying the

triangle inequality yields that

(40)

Let us first focus on the second summand in (A).

The next steps will make use of the Fourier transformation

of the kernel function \citepappendix[see, e.g.,][Ch. 1.3]tsybakov2009intro:

with . By Assumption A5,

has a compact support . The inverse transform gives then

Furthermore, we can use that \citepappendix[see][Ch. 1.3, (1.34)]tsybakov2009intro

which yields

Using further that is symmetric, since is

symmetric by Assumption A5, and that

leads to

where

(42)

such that

(43)

In order to simplify the notation we will denote

such that

As takes only values within the compact interval , there

exist constants and such that, uniformly for all ,

, for all , and

, for all . Together with the

triangle inequality, this yields that

From our moment assumptions (Assumption

A1) and the fact that is compact, we can conclude that there must

exist a constant such that, point-wise for every ,

(44)

for all and .

“Within function” dependencies: By the same reasoning there

must exist a constant such that, point-wise for every ,

(45)

for all and all .

“Between function” dependencies: Our weak dependency assumption (Assumption A1) and the fact that

is compact yields that point-wise for every

Plugging

(47) into (43) and integration by substitution

leads to

(48)

Let us now focus on the first summand in (A).

From standard arguments in nonparametric statistics (see, e.g., Ruppert and Wand (1994)) we know that

for each and for all

. Under our smoothness Assumption A3, the “”

term becomes uniformly valid for all and all , since all of the involved functions have uniformly bounded second order derivatives.

We can conclude with respect to the first summand

in (A) that

(49)

Finally, plugging our results (48) and

(49) into (A) leads to

(50)

for all .

Proof of Lemma A.2:

Analogously to that of Lemma A.1.

Proof of Theorem 4.1, part (a):

Let us rewrite the estimator using matrix notation

as in Ruppert and Wand (1994), i.e.,

(51)

where , is a dimensional data matrix with typical rows , the

dimensional diagonal weighting matrix

holds the kernel weights

. The objects and

are filled in correspondence with the

dimensional vector

.

This way we can decompose the estimator as

(52)

with matrix

and vector

Using the notation and the results from Lemma A.1 we have that

(53)

(54)

where we write

in order to denote that

. Taking

the inverse of (53) gives

Let us rewrite the estimator using matrix notation

as in Ruppert and Wand (1994), i.e.,

(56)

where , is a

dimensional data matrix with typical rows

, the dimensional diagonal weighting

matrix holds the bivariate kernel weights

. For the bivariate kernel weights

we use a

multiplicative kernel function

with as defined

above. The usual kernel constants are then

and

. The rows of the matrices

and are

filled in correspondence with the elements of the vector of raw-covariances

.

Let us initially consider the infeasible estimator that is

based on the infeasible “clean” raw-covariances instead of the estimator in

(56) that is based on the “dirty” raw-covariances

.

Equivalently to the estimator above, we can write the estimator as

(57)

with

(58)

and

(59)

where we use the notation and the results from Lemma A.2,

and where we write

in order to denote that

.

It remains to consider the additional estimation error, which comes from

using the “dirty” response variables instead of

“clean” dependent variables .

Observe that we can expand as following:

Using our finite moment assumptions on (Assumption A1) and

our result in Theorem

4.1, part (a), we have that

uniformly for all and . Therefore

Proof of Theorem 4.1, parts (c) and (d):

Part (c) follows directly from inequality ; see inequality (4.43) in Bosq (2000). Part (d) follows directly from Lemma 4.3 in Bosq (2000).

In the following let for some . By assumption of Theorem 4.2 we have , and recall that by Assumption (A1) the structure of a function , to be observed on , does not depend on the specific interval .

For the proof of Theorem 4.2 we need some additional lemmas. Generally note that under the assumed choice of bandwidths we have for , since for all and sufficiently large we have .

Recall that and for , where in the particular case of we additionally have and . Also recall that and that by (A6) we have as well as .

Lemma A.3.

Under the assumptions of Theorem 4.2 we have for all

(61)

Proof of Lemma A.3: Using results (b) and (c) of Theorem 4.1 we obtain

(62)

But by the established properties (in particular (12) in Theorem 2.3) of our operator we have for all and .

Hence

(63)

Now note that for all

(64)

Let . By the orthonormality of the system of eigenfunctions, the Cauchy-Schwarz inequality, and Theorem 4.1 we have

(65)

And since by Assumption (A7) the Cauchy-Schwarz inequality yields

(66)

By (c) of Theorem 4.1, (64), (66), for , and relation (63) can thus be rewritten in the form

and, similar to (66), the Cauchy-Schwarz inequality leads to

(69)

By our assumptions on the sequence of eigenvalues we have for all

When combining this result with (68), a further application of the Cauchy-Schwarz inequality yields

(70)

Since as , the desired result is an immediate consequence of (62) - (70).

A technical difficulty in the proof of Theorem 4.2 consists in the fact that and the observations corresponding to the selected . But let denote the estimate of the covariance matrix when eliminating the observations from the sample, and let and , , denote eigenvalues and eigenfunctions of the corresponding covariance operator.

Although in our time series context there may still exist dependencies between and , our assumptions imply that then all are independent of the particular samples and . The following Lemma now provides bounds for the differences between and , where .

Lemma A.4.

Under the assumptions of Theorem 4.2 we have for all

a)

.

b)

,

c)

Proof of Lemma A.4: Based on the definitions and techniques introduced in the proof of Theorem 4.1 and Lemma A.2 it is immediately seen that uniform rates of convergence of can be derived by considering the following difference:

Using similar arguments as in the proof of Lemma

A.1, leads to

which implies

and assertion a) of the Lemma is an immediate consequence.

The inequalities used to prove (c) and (d) of Theorem 4.1 now lead to

and

, where

.

By (c) of Theorem 4.1, our assumptions on , and with