\pkgBeSS: An \proglangR Package for Best Subset Selection in Linear, Logistic and CoxPH Models

Canhong Wen, Aijun Zhang, Shijie Quan, Xueqin Wang \Plaintitle\pkgBeSS: An R Package for Best Subset Selection in GLM and CoxPH Model \Shorttitle\pkgBeSS: Best Subset Selection \Abstract

We introduce a new \proglangR package, \pkgBeSS, for solving the best subset selection problem in linear, logistic and Cox’s proportional hazard (CoxPH) models.

It utilizes a highly efficient active set algorithm based on primal and dual variables, and supports sequential and golden search strategies for best subset selection.

We provide a \proglangC++ implementation of the algorithm using \pkgRcpp interface.

We demonstrate through numerical experiments based on enormous simulation and real datasets that the new \pkgBeSS package has competitive performance compared to other \proglangR packages for best subset selection purposes.

\Keywordsbest subset selection, primal dual active set, model selection

\Plainkeywordsbest subset selection, primal dual active set, variable selection, R, C++, Rcpp \Address

Canhong Wen

Department of Statistics and Finance, School of Management

University of Science and Technology of China

230026 Hefei, AH, China

E-mail:

and

Department of Statistics, School of Mathematics

Southern China Center for Statistical Science

Sun Yat-sen University

510275 Guangzhou, GD, China

Aijun Zhang

Department of Statistics and Actuarial Science

The University of Hong Kong

Hong Kong, China

E-mail:

Shijie Quan

Department of Statistics, School of Mathematics

Southern China Center for Statistical Science

Sun Yat-sen University

510275 Guangzhou, GD, China

Xueqin Wang

Department of Statistics, School of Mathematics

Southern China Center for Statistical Science

Sun Yat-sen University

510275 Guangzhou, GD, China

E-mail:

1 Introduction

One of the main tasks of statistical modeling is to exploit the association between a response variable and multiple predictors. Linear model (LM), as a simple parametric regression model, is often used to capture linear dependence between response and predictors. The other two common models: generalized linear model (GLM) and Cox’s proportional hazards (CoxPH) model, can be considered as the extensions of linear model, depending on the types of responses. Parameter estimation in these models can be computationally intensive when the number of predictors is large. Meanwhile, Occam’s razor is widely accepted as a heuristic rule for statistical modeling, which balances goodness of fit and model complexity. This rule leads to a relative small subset of important predictors.

The canonical approach to subset selection problem is to choose out of predictors for each . This involves exhaustive search over all possible subsets of predictors, which is an NP-hard combinatorial optimization problem. To speed up, furnival1974regressions introduced a well-known branch-and-bound algorithm with an efficient updating strategy for LMs, which was later implemented by \proglangR packages such as the \pkgleaps (lumley2017leaps) and the \pkgbestglm (mcleod2010bestglm). Yet for GLMs, a simple exhaustive screen is undertaken in \pkgbestglm. When the exhaustive screening is not feasible for GLMs, fast approximating approaches have been proposed based on a genetic algorithm. For instance, \pkgkofnGA(wolters2015a) implemented a genetic algorithm to search for a best subset of a pre-specified model size , while \pkgglmuti (calcagno2010glmulti) implemented a genetic algorithm to automatically select the best model for GLMs with no more than 32 covariates. These packages can only deal with dozens of predictors but not high-dimensional data arising in modern statistics. Recently, bertsimas2016best proposed a mixed integer optimization approach to find feasible best subset solutions for LMs with relatively larger , which relies on certain third-party integer optimization solvers. Alternatively, regularization strategy is widely used to transform the subset selection problem into computational feasible problem. For example, \pkgglmnet (friedman2010regularization; simon2011regularization) implemented a coordinate descent algorithm to solve the LASSO problem, which is a convex relaxation by replacing the cardinality constraint in best subset selection problem by the norm.

In this paper, we consider a primal-dual active set (PDAS) approach to solve the best subset selection problem for LM, GLM and CoxPH models. The PDAS algorithm for linear least squares problems was first introduced by ito2013variational and later discussed by jiao2015primal, Huang-et-al-2017 and ghilli2017monotone. It utilizes an active set updating strategy and fits the sub-models through use of complementary primal and dual variables. We generalize the PDAS algorithm for general convex loss functions with the best subset constraint, and further extend it to support both sequential and golden section search strategies for optimal determination. We develop a new package \pkgBeSS (BEst Subset Selection, wen2017bess) in the \proglangR programming system (R) with \proglangC++ implementation of PDAS algorithms and memory optimized for sparse matrix output. This package is publicly available from the Comprehensive \proglangR Archive Network (CRAN) at https://cran.r-project.org/package=BeSS. We demonstrate through enormous datasets that \pkgBeSS is efficient and stable for high dimensional data, and may solve best subset problems with in 1000s and in 10000s in just seconds on a single personal computer.

The article is organized as follows. In Section 2, we provide a general primal-dual formulation for the best subset problem that includes linear, logistic and CoxPH models as special cases. Section 3 presents the PDAS algorithms and related technical details. Numerical experiments with enormous simulations and real datasets are conducted in Section 4. We conclude with a short discussion in Section 5.

2 Primal-dual formulation

The best subset selection problem with the subset size is given by the following optimization problem:

| (1) |

where is a convex loss function of the model parameters and is an unknown positive integer. The norm counts the number of nonzeros in .

It is known that the problem (1) admits non-unique local optimal solutions, among which the coordinate-wise minimizers possess promising properties. For a coordinate-wise minimizer , denote the vectors of gradient and Hessian diagonal by

| (2) |

respectively. For each coordinate , write while fixing the other coordinates. Then the local quadratic approximation of around is given by

| (3) |

which gives rise of an important quantity of the following scaled gradient form

| (4) |

Minimizing the objective function yields for .

The constraint in (1) says that there are components of that would be enforced to be zero. To determine which components, we consider the sacrifices of when switching each from to , which are given by

| (5) |

Among all the candidates, we may enforce those ’s to zero if they contribute the least total sacrifice to the overall loss. To realize this, let denote the decreasing rearrangement of for , then truncate the ordered sacrifice vector at position . Combining the analytical result by (3), we obtain that

| (6) |

In (6), we treat as primal variables, as dual variables, and as reference sacrifices. Next we provide their explicit expressions for three important statistical models.

Case 1: Linear regression. Consider the LM with design matrix and i.i.d. errors. Here and are standardized such that the intercept term is removed from the model and each column of has norm.

Take the loss function . For , it is easy to obtain

| (7) |

where denotes the th column of , so

| (8) |

Case 2: Logistic regression. Consider the GLM

with . Given the data with binary responses , the negative log-likelihood function is given by

| (9) |

We give only the primal-dual quantities for according to the constraint in (1), while leaving to be estimated by unconstrained maximum likelihood method. For ,

| (10) |

where denotes the -th predicted probability. Then,

| (11) |

Case 3: CoxPH regression. Consider the CoxPH model

with an unspecified baseline hazard . Given the data with observations of survival time and censoring indicator , by the method of partial likelihood (cox1972regression), the parameter can be obtained by minimizing the following convex loss

| (12) |

By writing , it can be verified that

| (13) | ||||

| (14) |

so that and for .

3 Active set algorithm

For the best subset problem (1), define the active set with cardinality and the inactive set with cardinality . For the coordinate-wise minimizer satisfying (6), we have that

-

(C1)

when ;

-

(C2)

when ;

-

(C3)

whenever and .

By (C1) and (C2), the primal variables ’s and the dual variables ’s have complementary supports. (C3) can be viewed as a local stationary condition. These three conditions lay the foundation for the primal-dual active set algorithm we develop in this section.

Let be a candidate active set. By (C1), we may estimate the -nonzero primal variables by standard convex optimization:

| (15) |

Given , the and vectors (2) can be computed, with their explicit expressions derived for linear, logistic and CoxPH models in the previous section. The and vectors are readily obtainable by (4), (5) and (C2). Then we may check if (C3) is satisfied; otherwise, update the active and inactive sets by

| (16) |

This leads to the following iterative algorithm.

Algorithm 1 Primal-dual active set (PDAS) algorithm

-

1.

Specify the cardinality of the active set and the maximum number of iterations . Initialize to be a random -subset of and .

- 2.

-

3.

Output .

Remark 1.

The proposed PDAS algorithm is close to the primal-dual active set strategy first developed by ito2013variational, but different from their original algorithm in two main aspects. First, our PDAS algorithm is derived from the quadratic argument (3) and it involves the second-order partial derivatives (i.e. Hessian diagonal ). Second, our algorithm extends the original linear model setting to the general setting with convex loss functions.

3.1 Determination of optimal

The subset size is usually unknown in practice, thus one has to determine it in a data-driven manner. A heuristic way is using the cross-validation technique to achieve the best prediction performance. Yet it is time consuming to conduct the cross-validation method especially for high-dimensional data. An alternative way is to run the PDAS algorithm from small to large values, then identify an optimal choice according to some criteria, e.g., Akaike information criterion (akaike1974new, AIC) and Bayesian information criterion (schwarz1978estimating, BIC) and extended BIC (chen2008extended; chen2012extended, EBIC) for small--large- scenarios. This leads to the sequential PDAS algorithm.

Algorithm 2 Sequential primal-dual active set (SPDAS) algorithm

-

1.

Specify the maximum size of the active set, and initialize .

-

2.

For , do

Run PDAS with initial . Denote the output by .

-

3.

Output the optimal choice that attains the minimum AIC, BIC or EBIC.

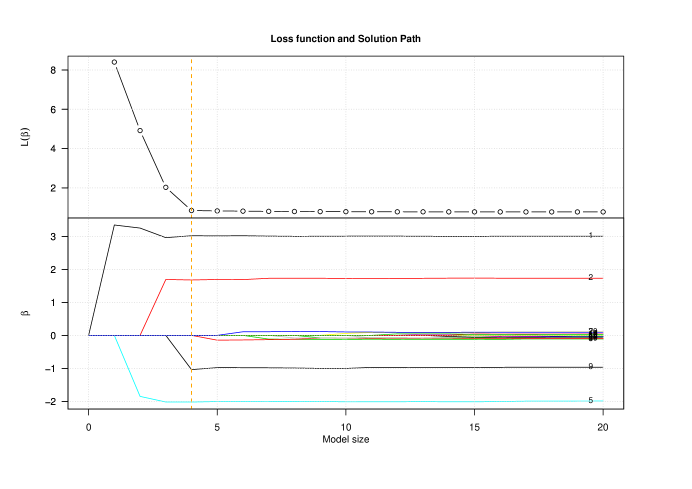

To alleviate the computational burden of determining as in SPDAS, here we provide an alternative method: the golden section search algorithm. We begin by plotting the loss function as a function of for a simulated data from linear model with standard Gaussian error. The true coefficient and the design matrix is generated as in Section 4.1 with . From Figure 1, it can be seen that the slope of the loss plot goes from steep to flat and there is an ‘elbow’ exists near the true number of active set, i.e., . The solution path for the same data is presented at the bottom of Figure 1 for a better visualization on the relationship between loss function and coefficient estimation. When a true active predictor is included in the model, the loss function drops dramatically and the predictors already in the model adjust their estimates to be close to the true values. When all the active predictors are included in the model, their estimates would not change much as becomes larger.

Motivated by this interesting phenomenon, we develop a search algorithm based on the golden section method to determine the location of such an elbow in the loss function. In this way, we can avoid to run the PDAS algorithm extensively for a whole sequential list. The golden section primal-dual active set (GPDAS) algorithm is summarized as follows.

Algorithm 3 Golden section primal-dual active set (GPDAS) algorithm

-

1.

Specify the number of maximum iterations , the maximum size of the active set and the tolerance . Initialize , and .

-

2.

For , do

-

(2.a)

Run PDAS with and initial . Output .

-

(2.b)

Run PDAS with and initial . Output .

-

(2.c)

Calculate . Run PDAS with and initial . Output .

-

(2.d)

Determine whether is an elbow point:

-

•

Run PDAS with and initial . Output .

-

•

Run PDAS with and initial . Output .

-

•

If and , then stop and denote as an elbow point, otherwise go ahead.

-

•

-

(2.e)

Update and :

-

•

If , then , ;

-

•

If , then , ;

-

•

Otherwise, and .

-

•

-

(2.f)

If , then stop, otherwise .

-

(2.a)

-

3.

Output .

3.2 Computational details

The proposed PDAS, SPDAS and SPDAS algorithms are much faster than existing methods reviewed in Section 1. For the exhaustive methods like \pkgleaps and \pkgbestglm, they essentially deal with sub-models in order to search for the best subset with size no more than . It is infeasible even when is moderate. That is why the greedy methods (e.g., \pkgglmuti) and the relaxed methods (e.g., \pkgglmnet) become popular. Our proposed algorithms belong to the greedy methods and their computational complexity is discussed below.

In general, consider one iteration in step (2) of the PDAS algorithm with a pre-specified . Denote by the computational complexity for solving on the active set; and denote by and the computational complexity for calculating and , respectively. The calculation of in steps (2.b)-(2.c) costs , and the calculation of in steps (2.b)-(2.c) costs . Then the overall cost of one iteration is .

The total number of iterations of the PDAS algorithm could depend on the signal-to-noise ratio, the dimensionality , and the sparsity level . The algorithm may usually converge in finite steps (otherwise capped by ). Denote by the complexity for each run of the PDAS algorithm, then the total complexity of the SPDAS and GPDAS algorithms are and , respectively.

Case 1: Linear regression. Since , . The matrix vector product in the computation of takes flops. For the least squares problem on the active set, we use Cholesky factorization to obtain the estimate, which leads to . Thus the total cost of one iteration in step (2) is , and the overall cost of the PDAS algorithm is the same since the number of iterations is often finite.

In particular, if the true coefficient vector is sparse with and , the cost of the PDAS algorithm is , a linear time with respective to the size . With an unknown , we can choose an appropriate value, e.g., , to speed up the SPDAS and GPDAS algorithms. Their costs become and , respectively. These rates are comparable with the sure independence screening procedure (fan2008sure) in handling ultrahigh-dimensional data. In fact, even if the true coefficient vector is not sparse, we could use a conjugate gradient (golub2012matrix) algorithm with a preconditioning matrix to achieve a similar computational rate.

Case 2: Logistic regression. It costs flop to compute the predicted probabilities ’s. Thus and . We use the iteratively reweighted least squares (IRLS) for parameter estimation on the active set. The complexity of each IRLS step is the same as that of the least squares, so with denoting the finite number of IRLS iterations. The total cost of one iteration in step (2) is .

Case 3: CoxPH regression. It costs flops to compute ’s. Assume the censoring rate is , then and . Like the \codecoxph command from the \pkgsurvival package, we adopt the standard Newton-Raphson algorithm for the maximum partial likelihood estimation on the active set. Its difficulty arises in the computation of the inverse of the Hessian matrix, which is full and dense. The Hessian matrix has entries and it requires flops for the computation of each entry. The matrix inversion costs via Gauss-Jordan elimination or Cholesky decomposition. Hence, for each Newton-Raphson iteration, the updating equation requires flops. We may speed up the algorithm by replacing the Hessian matrix with its diagonal, which reduces the computational complexity per updating to . Denote by the number of Newton-Raphson iterations, then and the total cost of one iteration in step (2) is

3.3 R package

We have implemented the active set algorithms described above into an \proglangR package called \pkgBeSS (BEst Subset Selection), which is publicly available from the CRAN at https://cran.r-project.org/package=BeSS. The package is implemented in \proglangC++ with memory optimized using sparse matrix output and it can be called from \proglangR by a user-friendly interface.

The package contains two main functions, i.e., \codebess.one and \codebess, for solving the best subset selection problem with or without specification of . In \codebess, two options are provided to determine the optimal : one is based on the SPDAS algorithm with criteria including AIC, BIC and EBIC; the other is based on the GPDAS algorithm. The function \codeplot.bess generates plots of loss functions for the best sub-models for each candidate , together with solution paths for each predictor. We also include functions \codepredict.bess and \codepredict.bess.one to make prediction on the new data.

4 Numerical examples

In this section we compare the performance of our new \pkgBeSS package to other well-known packages for best subset selection: \pkgleaps, \pkgbestglm and \pkgglmulti. We also include \pkgglmnet as an approximate subset selection method and use the default cross-validation method to determine an optimal tuning parameter. All parameters use the default values of the corresponding main functions in those packages unless otherwise stated. In presenting the results of \pkgBeSS, \codebess.seq represents \codebess with argument \codemethod = "sequential" and \codebess.gs represents \codebess with argument \codemethod = "gsection", two different ways to determine the optimal parameter . In \codebess.seq, we use AIC for examples with and EBIC for examples with . We choose for linear models and for logistic and CoxPH models.

All the \proglangR codes are demonstrated in Section 4.3. All computations are carried out on a 64-bit Intel machine with a single 3.30 GHz CPU and 4 GB of RAM.

4.1 Simulation data

We demonstrate the practical application of our new \pkgBeSS package on synthetical data under both low and high dimensional settings. For the low-dimensional data, \pkgBeSS has comparable performance with other state-of-the-art methods. For the high-dimensional data, while most state-of-the-art methods become incapable to deal with them, \pkgBeSS still performs fairly well. For an instance, \pkgBeSS is scalable enough to identify the best sub-model over all candidates efficiently in seconds or a few minutes when the dimension .

We compare the performances of different methods in three aspects. The first aspect is the run time in seconds (Time). The second aspect is the selection performance in terms of true positive (TP) and false positive (FP) numbers, which are defined by the numbers of true relevant and true irrelevant variables among the selective predictors. The third aspect is the predictive performance on a held out test data of size 1000. For linear regression, we use the relative mean squares error (MSE) as defined by . For logistic regression, we calculate the classification accuracy by the average number of observations being correctly classified. For CoxPH regression, we compute the median time on the test data, then derive the area under the receiver operator characteristic curve (i.e., AUC) using nearest neighbor estimation method as in heagerty2000time.

We generate the design matrix and the underlying coefficients as follows. The design matrix is generated with , where and were i.i.d. random samples drawn from standard Gaussian distribution and subsequently normalized to have norm. The true coefficient is a vector with nonzero entries uniformly distributed in , with and to be specified. In the simulation study, the sample size is fixed to be . For each scenario, 100 replications are conducted .

Case 1: Linear regression. For each and , we generate the response vector , with . We set and . Different choices of are taken to cover both the low-dimensional cases and the high-dimensional cases (). For \codeglmulti, we only present the result for and since it can only deal with at most 32 predictors. Since \codeleaps and \codebestglm cannot deal with high-dimensional case, we only report the results of \codeglmnet, \codebess.seq and \codebess.gs. The results are summarized in Table 1.

In the low-dimensional cases, the performances of all best subset selection methods are comparable in terms of prediction accuracy and selection consistency. However, the regularization method \codeglmnet has much higher MSE and lower FP, which suggests that LASSO incurs bias in the coefficient estimation. In terms of computational times, both \codebess.seq and \codebess.gs have comparable performance with \codeglmnet, which cost much less run times than the state-of-the-art methods. Unlike \codeleaps, \codebestglm and \codeglmulti, the run times of \codebess.seq and \codebess.gs remain fairly stable across different dimensionality.

In the high-dimensional cases, both \codebess.seq and \codebess.gs work quite well and they have similar performance in prediction and variable selection. Furthermore, their performances become better as and increase (from left to right in Table 1). On the other hand, \codeglmnet has higher FP as increases. In particular, when and only nonzero coefficients are involved, the average TP equals and the average FP is less than 3.06. In contrast, the average FP of \codeglmnet increases to 30. As for the computational issues, both \codebess.seq and \codebess.gs seem to grow at a linear rate of , but \codebess.gs offers speedups by factors of 2 up to 10 and more.

| Low-dimensional | Method | ||||

|---|---|---|---|---|---|

| Time | \codeleaps | 0.00(0.01) | 0.39(0.13) | 58.79(28.78) | |

| \codebestglm | 0.02(0.01) | 0.51(0.15) | 69.39(32.27) | ||

| \codeglmulti | 11.91(2.60) | 18.41(4.13) | — | ||

| \codeglmnet | 0.08(0.02) | 0.09(0.02) | 0.08(0.01) | ||

| \codebess.seq | 0.18(0.01) | 0.23(0.02) | 0.25(0.03) | ||

| \codebess.gs | 0.16(0.01) | 0.18(0.02) | 0.17(0.02) | ||

| MSE | \codeleaps | 1.91(0.83) | 2.18(0.81) | 2.44(1.15) | |

| () | \codebestglm | 1.91(0.83) | 2.18(0.81) | 2.44(1.15) | |

| \codeglmulti | 1.87(0.72) | 2.16(0.79) | — | ||

| \codeglmnet | 3.90(1.30) | 3.51(1.23) | 3.51(1.37) | ||

| \codebess.seq | 1.93(0.82) | 2.12(0.76) | 2.43(1.21) | ||

| \codebess.gs | 2.14(2.45) | 2.06(1.78) | 2.80(3.37) | ||

| TP | \codeleaps | 3.97(0.17) | 3.99(0.10) | 3.97(0.17) | |

| \codebestglm | 3.97(0.17) | 3.99(0.10) | 3.97(0.17) | ||

| \codeglmulti | 3.99(0.10) | 4.00(0.00) | — | ||

| \codeglmnet | 3.96(0.20) | 3.97(0.17) | 3.95(0.22) | ||

| \codebess.seq | 3.96(0.20) | 3.91(0.35) | 3.84(0.44) | ||

| \codebess.gs | 3.78(0.42) | 3.73(0.51) | 3.63(0.61) | ||

| FP | \codeleaps | 2.37(1.83) | 3.92(2.39) | 5.53(2.66) | |

| \codebestglm | 2.37(1.83) | 3.92(2.39) | 5.53(2.66) | ||

| \codeglmulti | 2.29(1.63) | 4.15(2.29) | — | ||

| \codeglmnet | 0.73(0.80) | 0.82(0.83) | 0.78(1.10) | ||

| \codebess.seq | 3.75(4.25) | 4.98(5.80) | 7.59(8.64) | ||

| \codebess.gs | 1.35(2.94) | 4.31(6.93) | 5.42(8.74) | ||

| High-dimensional | Method | ||||

| Time | \codeglmnet | 0.16(0.03) | 1.77(0.09) | 14.82(1.73) | |

| \codebess.seq | 1.29(0.09) | 74.54(1.33) | 137.04(13.80) | ||

| \codebess.gs | 0.53(0.12) | 3.72(0.41) | 12.87(2.89) | ||

| MSE | \codeglmnet | 1.42(0.18) | 2.51(0.28) | 2.47(0.22) | |

| () | \codebess.seq | 1.65(0.41) | 1.20(0.62) | 0.70(0.23) | |

| \codebess.gs | 1.33(0.29) | 0.98(0.37) | 1.00(0.35) | ||

| TP | \codeglmnet | 39.74(0.54) | 39.80(0.45) | 39.75(0.46) | |

| \codebess.seq | 35.30(2.17) | 38.72(1.29) | 39.53(0.70) | ||

| \codebess.gs | 35.78(2.12) | 39.43(0.88) | 39.58(0.71) | ||

| FP | \codeglmnet | 15.45(3.65) | 12.73(5.50) | 29.82(11.91) | |

| \codebess.seq | 27.15(10.66) | 4.92(6.99) | 0.32(1.92) | ||

| \codebess.gs | 28.86(8.90) | 1.51(2.53) | 3.06(3.84) |

Case 2: Logistic regression. For each and , the binary response is generated by , where . The range of nonzero coefficients are set as . Different choices of are taken to cover both the low-dimensional cases and the high-dimensional cases . The number of true nonzero coefficients is chosen to be for low-dimensional cases and for high-dimensional cases. Since \codebestglm is based on complete enumeration, it may be used for low-dimensional cases yet it becomes computationally infeasible for high dimensional cases.

The simulation results are summarized in Table 2. When is small, both \codebess.seq and \codebess.gs have comparable performance with \codebestglm, \codeglmulti and \codeglmnet, but have considerably faster speed in computation than \codebestglm and \codeglmulti. In the high-dimensional cases, we see that all three methods perform very well in terms of accuracy and TP. Yet both \codebess.seq and \codebess.gs have much smaller FP than \codeglmnet. Among them, the run time for \codebess.gs is around a quarter of that for \codebess.seq and is similar to that for \codeglmnet.

| Low-dimensional | Method | ||||

|---|---|---|---|---|---|

| Time | \codebestglm | 1.83(0.15) | 7.55(0.26) | 28.35(1.93) | |

| \codeglmulti | 2.08(0.11) | 13.91(2.43) | 21.61(4.54) | ||

| \codeglmnet | 0.49(0.07) | 0.56(0.09) | 0.63(0.17) | ||

| \codebess.seq | 0.70(0.33) | 0.79(0.35) | 0.78(0.52) | ||

| \codebess.gs | 0.52(0.20) | 0.78(1.14) | 0.65(0.23) | ||

| Acc | \codebestglm | 0.949(0.012) | 0.950(0.013) | 0.950(0.011) | |

| \codeglmulti | 0.949(0.012) | 0.950(0.013) | 0.950(0.011) | ||

| \codeglmnet | 0.949(0.013) | 0.951(0.013) | 0.950(0.011) | ||

| \codebess.seq | 0.949(0.012) | 0.950(0.013) | 0.950(0.011) | ||

| \codebess.gs | 0.948(0.013) | 0.951(0.012) | 0.949(0.013) | ||

| TP | \codebestglm | 3.99(0.10) | 4.00(0.00) | 3.99(0.10) | |

| \codeglmulti | 3.99(0.10) | 4.00(0.00) | 4.00(0.00) | ||

| \codeglmnet | 4.00(0.00) | 4.00(0.00) | 4.00(0.00) | ||

| \codebess.seq | 3.96(0.20) | 3.95(0.30) | 3.91(0.32) | ||

| \codebess.gs | 3.87(0.37) | 3.87(0.42) | 3.89(0.40) | ||

| FP | \codebestglm | 0.73(0.85) | 1.02(1.05) | 1.41(1.44) | |

| \codeglmulti | 0.73(0.85) | 1.02(1.05) | 1.37(1.20) | ||

| \codeglmnet | 1.62(0.96) | 2.07(1.16) | 2.83(1.44) | ||

| \codebess.seq | 1.77(1.59) | 2.19(2.20) | 2.39(2.40) | ||

| \codebess.gs | 0.15(0.41) | 0.31(0.93) | 0.64(1.57) | ||

| High-dimensional | Method | ||||

| Time | \codeglmnet | 4.75(0.89) | 4.38(0.49) | 17.01(0.24) | |

| \codebess.seq | 43.99(7.42) | 54.85(4.46) | 108.66(2.47) | ||

| \codebess.gs | 7.34(2.10) | 11.46(1.81) | 22.43(2.16) | ||

| Acc | \codeglmnet | 0.969(0.006) | 0.945(0.009) | 0.922(0.011) | |

| \codebess.seq | 0.963(0.012) | 0.972(0.011) | 0.979(0.006) | ||

| \codebess.gs | 0.970(0.010) | 0.976(0.008) | 0.978(0.009) | ||

| TP | \codeglmnet | 19.96(0.20) | 19.97(0.17) | 19.79(0.52) | |

| \codebess.seq | 16.50(2.38) | 19.34(1.23) | 19.92(0.34) | ||

| \codebess.gs | 18.62(1.15) | 19.81(0.49) | 19.82(0.61) | ||

| FP | \codeglmnet | 34.59(4.74) | 122.82(19.80) | 222.77(43.63) | |

| \codebess.seq | 5.61(3.37) | 1.82(2.03) | 0.49(0.67) | ||

| \codebess.gs | 3.16(2.46) | 0.95(1.34) | 0.54(0.92) |

Case 3: CoxPH regression. For each and , we generate data from the CoxPH model with hazard rate . The ranges of nonzero coefficients are set same as those in logistic regression, i.e., . Different choices of are taken to cover both the low-dimensional cases and the high-dimensional cases . The number of true nonzero coefficients is chosen to be for low-dimensional cases and for high-dimensional cases. Since \codeglmulti cannot handle more than 32 predictors, we only report the low dimensional result for \codeglmulti.

The simulation results are summarized in Table 3. Our findings about \codebess.seq and \codebess.gs are similar to those for the logistic regression.

| Low-dimensional | Method | ||||

|---|---|---|---|---|---|

| Time | \codeglmulti | 1.53(0.06) | 10.11(1.75) | 15.20(2.86) | |

| \codeglmnet | 1.07(0.20) | 1.09(0.20) | 1.16(0.23) | ||

| \codebess.seq | 0.42(0.20) | 0.49(0.23) | 0.52(0.22) | ||

| \codebess.gs | 0.35(0.15) | 0.46(0.19) | 0.51(0.18) | ||

| AUC | \codeglmulti | 0.973(0.012) | 0.972(0.010) | 0.974(0.010) | |

| \codeglmnet | 0.973(0.012) | 0.972(0.010) | 0.974(0.010) | ||

| \codebess.seq | 0.973(0.012) | 0.972(0.010) | 0.974(0.010) | ||

| \codebess.gs | 0.972(0.012) | 0.972(0.010) | 0.974(0.011) | ||

| TP | \codeglmulti | 4.00(0.00) | 3.99(0.10) | 4.00(0.00) | |

| \codeglmnet | 4.00(0.00) | 4.00(0.00) | 4.00(0.00) | ||

| \codebess.seq | 4.00(0.00) | 4.00(0.00) | 4.00(0.00) | ||

| \codebess.gs | 3.89(0.35) | 3.96(0.20) | 3.99(0.10) | ||

| FP | \codeglmulti | 0.60(0.77) | 1.06(1.17) | 1.14(1.21) | |

| \codeglmnet | 1.17(1.01) | 1.56(1.04) | 1.82(1.14) | ||

| \codebess.seq | 1.62(1.69) | 1.98(2.25) | 2.38(2.69) | ||

| \codebess.gs | 0.11(0.35) | 0.04(0.20) | 0.06(0.37) | ||

| High-dimensional | Method | ||||

| Time | \codeglmnet | 16.61(1.90) | 297.01(62.83) | 832.69(73.26) | |

| \codebess.seq | 20.57(1.77) | 72.53(2.58) | 233.53(11.94) | ||

| \codebess.gs | 4.86(1.59) | 15.36(1.69) | 63.23(7.21) | ||

| AUC | \codeglmnet | 0.993(0.005) | 0.992(0.006) | 0.991(0.007) | |

| \codebess.seq | 0.993(0.005) | 0.992(0.006) | 0.991(0.007) | ||

| \codebess.gs | 0.990(0.008) | 0.992(0.006) | 0.991(0.007) | ||

| TP | \codeglmnet | 20.00(0.00) | 20.00(0.00) | 20.00(0.00) | |

| \codebess.seq | 18.06(1.67) | 19.70(0.70) | 20.00(0.00) | ||

| \codebess.gs | 17.09(2.03) | 19.93(0.33) | 19.99(0.10) | ||

| FP | \codeglmnet | 41.26(4.10) | 245.82(19.41) | 541.13(34.33) | |

| \codebess.seq | 11.80(9.25) | 1.64(3.78) | 0.02(0.14) | ||

| \codebess.gs | 13.65(11.84) | 0.19(0.60) | 0.05(0.22) |

4.2 Real data

We also evaluate the performance of the \pkgBeSS package in modeling several real data sets. Table 4 lists these instances and their descriptions. All datasets are saved as \proglangR data objects and available online with this publication.

| Dataset | Type | Data source | ||

|---|---|---|---|---|

| \codeprostate | 97 | 9 | Continuous | \proglangR package \pkgElemStatLearn |

| \codeSAheart | 462 | 8 | Binary | \proglangR package \pkgElemStatLearn |

| \codetrim32 | 120 | 18975 | Continuous | scheetz2006regulation |

| \codeleukemia | 72 | 3571 | Binary | \proglangR package \pkgspikeslab |

| \codegravier | 168 | 2905 | Binary | https://github.com/ramhiser/ |

| \codeer0 | 609 | 22285 | Survival | https://www.ncbi.nlm.nih.gov/geo/ |

We randomly split the data into a training set with two-thirds observations and a test set with remaining observations. Different best subset selection methods are used to identify the best sub-model. For each method, the run time in seconds (Time) and the size of selected model (MS) are recorded. We also include measurements of the predictive performance on test data according to the metrics as in Section 4.1. For reliable evaluation, the aforementioned procedure is replicated for 100 times.

The modeling results are displayed in Table 5. Again in low-dimensional cases, \codebess has comparable performance with the state-of-art algorithms (branch-and-bound algorithm for linear models and complete enumeration algorithm and genetic algorithm for GLMs). Besides, \codebess.gs has comparable run time with \codeglmnet and is considerably faster than \codebess.seq especially in high-dimensional cases.

| Data | Method | \codeleaps | \codebestglm | \codeglmulti | \codeglmnet | \codebess.seq | \codebess.gs |

|---|---|---|---|---|---|---|---|

| \codeprostate | Time | 0.00(0.01) | 0.01(0.01) | 0.61(0.05) | 0.07(0.01) | 0.22(0.01) | 0.22(0.01) |

| PE | 0.61(0.14) | 0.61(0.14) | 0.61(0.14) | 0.65(0.19) | 0.60(0.13) | 0.60(0.14) | |

| MS | 4.27(1.11) | 4.25(1.12) | 4.25(1.12) | 3.58(0.87) | 4.29(1.17) | 6.11(0.87) | |

| \codeSAheart | Time | — | 1.58(0.07) | 4.03(0.53) | 0.13(0.01) | 0.27(0.04) | 0.26(0.04) |

| Acc | — | 0.72(0.03) | 0.72(0.03) | 0.70(0.04) | 0.72(0.03) | 0.72(0.03) | |

| MS | — | 5.68(0.98) | 5.68(0.98) | 4.61(0.84) | 5.68(0.99) | 6.29(1.09) | |

| \codetrim32 | Time | — | — | — | 3.23(0.15) | 1.95(0.53) | 1.08(0.19) |

| PE | — | — | — | 0.01(0.01) | 0.01(0.01) | 0.01(0.00) | |

| MS | — | — | — | 24.89(11.79) | 1.60(0.62) | 7.82(2.26) | |

| \codeleukemia | Time | — | — | — | 0.38(0.01) | 1.74(0.77) | 1.14(0.53) |

| Acc | — | — | — | 0.93(0.05) | 0.90(0.06) | 0.91(0.06) | |

| MS | — | — | — | 11.76(4.40) | 1.54(0.77) | 2.00(0.00) | |

| \codegravier | Time | — | — | — | 0.68(0.03) | 6.64(4.09) | 2.93(2.50) |

| Acc | — | — | — | 0.71(0.07) | 0.72(0.06) | 0.72(0.06) | |

| MS | — | — | — | 10.83(7.39) | 9.23(1.05) | 10.80(2.47) | |

| \codeer0 | Time | — | — | — | 154.97(15.75) | 184.51(86.15) | 55.20(22.07) |

| AUC | — | — | — | 0.52(0.04) | 0.53(0.05) | 0.60(0.05) | |

| MS | — | — | — | 3.06(7.35) | 1.02(0.14) | 56.85(6.90) |

4.3 Code demonstration

We demonstrate how to use the package \pkgBeSS on a synthesis data as discussed in Section 3.1 and a real data in Section 4.2. Firstly, load \pkgBeSS and generate data with the \codegen.data function.

R> require("BeSS") R> set.seed(123) R> Tbeta <- rep(0, 20) R> Tbeta[c(1, 2, 5, 9)] <- c(3, 1.5, -2, -1) R> data <- gen.data(n = 200, p = 20, family = "gaussian", beta = Tbeta, + rho = 0.2, sigma = 1)

We may call the \codebess.one function to solve the best subset selection problem with a specified cardinality. Then we can \codeprint or \codesummary the \codebess.one object. While the \codeprint method allows users to obtain a brief summary of the fitted model, the \codesummary method presents a much more detailed description.

R> fit.one <- bess.one(datay, s = 4, family = "gaussian") R> print(fit.one) {Soutput} Df MSE AIC BIC EBIC 4.0000000 0.8501053 -24.4790117 -11.2857422 12.6801159 {Sinput} R> summary(fit.one) {Soutput} ———————————————————————- Primal-dual active algorithm with maximum iteration being 15

Best model with k = 4 includes predictors:

X1 X2 X5 X9 3.019296 1.679419 -2.021521 -1.038276

log-likelihood: 16.23951 deviance: -32.47901 AIC: -24.47901 BIC: -11.28574 EBIC: 12.68012 ———————————————————————-

The estimated coefficients of the fitted model can be extracted by using the \codecoef function, which provides a sparse output with the control of argument \codesparse = TRUE. It is recommended to output a non-sparse vector when \codebess.one is used, and to output a sparse matrix when \codebess is used.

R> coef(fit.one, sparse = FALSE) {Soutput} (intercept) X1 X2 X3 X4 X5 -0.07506287 3.01929556 1.67941924 0.00000000 0.00000000 -2.02152109 X6 X7 X8 X9 X10 X11 0.00000000 0.00000000 0.00000000 -1.03827568 0.00000000 0.00000000 X12 X13 X14 X15 X16 X17 0.00000000 0.00000000 0.00000000 0.00000000 0.00000000 0.00000000 X18 X19 X20 0.00000000 0.00000000 0.00000000

To make prediction on new data, the \codepredict function can be used as follows.

R> pred.one <- predict(fit.one, newdata = datakk