Discretized conformal prediction for efficient distribution-free inference

Abstract

In regression problems where there is no known true underlying model, conformal prediction methods enable prediction intervals to be constructed without any assumptions on the distribution of the underlying data, except that the training and test data are assumed to be exchangeable. However, these methods bear a heavy computational cost—and, to be carried out exactly, the regression algorithm would need to be fitted infinitely many times. In practice, the conformal prediction method is run by simply considering only a finite grid of finely spaced values for the response variable. This paper develops discretized conformal prediction algorithms that are guaranteed to cover the target value with the desired probability, and that offer a tradeoff between computational cost and prediction accuracy.

1 Introduction

In this paper, we examine the problem of efficiently computing conformal prediction intervals using models that are computationally expensive to fit. The conformal prediction method, introduced by Vovk et al. [6, 7, 5] and developed for the high-dimensional setting by Lei et al. [4], uses a training data set to provide a prediction interval for an unobserved response variable at the covariate point . The prediction interval’s coverage guarantees rely only on the assumption that the available training data is exchangeable with the test data point .

As originally proposed, this method requires refitting an expensive model for every possible value of the test point’s response variable —at least in theory, but of course in practice, if is real-valued, it is impossible to refit the model infinitely many times, and so instead it is common to round to a fine finite grid of values in .

Our work formalizes this rounding procedure, proving that rounding can be done without losing the coverage guarantee of the method. Our result also allows for the rounding to be as coarse or fine as desired, giving a principled way to trade off between computational cost and the precision of the prediction (as measured by the width of the prediction interval), while maintaining the coverage guarantee.

2 Background

Given a training data set , and a new feature vector , the goal of predictive inference is to provide an interval in that is likely to contain the unobserved response value . Imagine fitting a predictive model , where predicts the value of given , to the training points. If is within the interval for of the training data points , we might naively assume that is a -coverage prediction interval for , that is, that . However, for high dimensions , in general this will be completely untrue—the model , having been fitted to the training data points, by its construction will have low residuals on this same training data set, but may be wildly inaccurate on an independently drawn test point . In general, the constructed prediction interval will undercover, i.e. the probability of this interval containing (“covering”) the true response value will be lower than intended.

The problem is that while the training and test data ( total data points) may have been drawn from the same distribution initially, the resulting many residuals are not exchangeably distributed since was fitted on the training points without including the test point.

At first glance, this problem seems insurmountable—without observing the test point, how can we hope to include it into the process of fitting the model ? Remarkably, the conformal prediction method offers a way to do exactly this, which can be carried out using any desired model fitting algorithm for constructing . Here we summarize the steps of the conformal prediction method, as presented in the work of Lei et al. [4].

-

(1)

Without looking at the data, we choose any model fitting algorithm

that is required to treat the many input points exchangeably but is otherwise unconstrained.

-

(2)

Given the data, we compute

for every value —each is a possible value for the unseen test data point’s response value, .

-

(3)

Compute the desired quantile for the residuals,

where is the predefined desired error level.

-

(4)

The prediction interval111While the prediction set is labeled PI for “prediction interval”, and we often refer to it with this terminology, in some settings the set might not be equal to a single interval. is given by

The conformal prediction algorithm offers a coverage guarantee with no assumptions aside from exchangeability of the data points (for example, if the training and test points are i.i.d. draws from some distribution).

Theorem 1 (Lei et al. [4, Theorem 2.1]).

Assume exchangeability of the training and test data points

Then the conformal prediction algorithm satisfies

We reproduce a short proof of this result here, as this proof technique will be useful for proving the results presented later in this paper.

Proof of Theorem 1.

Define residuals for each . Since is a fitted model that was constructed using the many data points exchangeably, we therefore see that are themselves exchangeable, and so

By a simple calculation this event is equivalent to

where we use the definitions of and . In other words, the bound holds for . By definition, this means that , proving the theorem.∎

Computation for conformal prediction

Examining the conformal prediction algorithm, the reader may notice that for each possible value (that is, for each potential value for the test data point, ), we must refit a model using the algorithm . Depending on the setting, each run of may be fairly expensive—and even disregarding cost, in general we cannot hope to run infinitely many times, once for each .

In some settings, this problem can be circumvented using special structure within the model fitting algorithm. For instance, if fits a linear model with a squared norm penalty (Ridge regression), the prediction interval PI in fact enjoys a closed form solution [1]. Recent work by Lei [3] provides an efficient method for computing PI for the Lasso, i.e. quadratic loss function + norm penalty.

In nearly any other setting, however, we must instead turn to approximations of the full conformal prediction method, since fully computing PI is impossible. A straightforward way to approximate the algorithm is to only fit for a finite set of values—for instance, taking a fine grid of values over some interval that includes the empirical range of the observed response values, —we give more details below. This range may be further reduced for greater computational efficiency via “trimming”, as in Chen et al. [2]. An alternate approach is to employ sample splitting, studied by Lei et al. [4], where half the training data is used to fit the model a single time, while the quantiles of the residual are then computed over the remaining data points. Split conformal prediction is highly efficient, requiring only a single run of the model fitting algorithm , but may produce substantially wider prediction intervals due to the effective sample size being reduced to half. (Of course, it is also possible to create a uneven split, using a larger portion of data for model fitting and a smaller set for the inference step. This will produce sharper prediction intervals, but the method will have higher variance; this tradeoff is unavoidable for data splitting methods.)

2.1 Approximation via rounding

As mentioned above, in most settings, in practice the model can only be fitted over some finite grid of values spanning some range . Specifically, a common approximate algorithm might take the form:

-

(1)

Choose as before, and a finite set of trial values, with spacing , i.e. .

-

(2)

,(3) As before, Compute and for each trial value, i.e. for

-

(4)

The rounded prediction interval is given by

Then extend by a margin of to each side:

In practice, this type of approximate conformal prediction algorithm performs well, but there are several drawbacks. First, from a theoretical point of view, coverage can no longer be guaranteed—in particular, if there is some value that lies between two grid points, , it is possible that neither nor gets selected by the discretized algorithm, but we would have placed itself into the prediction interval PI if had been one of the values tested. In general this can happen only if the true prediction interval (the PI from the original non-discretized method) does not consist of a single connected component—depending on the model fitting algorithm , this may or may not occur. Second, in practice, the spacing of the grid provides a lower bound on the precision of the method—the set PI will always be at least wide. Since , this forces us to use a large computational budget .

We will next propose two different approaches towards a discretized conformal prediction method, which will resolve these issues by allowing for theoretical coverage properties and, in one of the algorithms, for prediction intervals whose width may be narrower than the spacing of the discretized grid.

3 Main results

In this section we introduce two different versions of discretized conformal inference, with a coverage guarantee for both algorithms given in Theorem 2 below.

3.1 Conformal prediction with discretized data

We begin with a simple rounded algorithm for conformal prediction, where our analysis is carried out entirely on the rounded data—that is, all response values are rounded to some finite grid—before converting back to the original values as a final step.

-

(1)

Without looking at the data, choose any model fitting algorithm

where maps a vector of covariates to a predicted value for in . The model fitting algorithm is required to treat the many input points exchangeably but is otherwise unconstrained. Furthermore, choose a set containing finitely many points—this set is the “grid” of candidate values for the response variable at the test point. Select also a discretization function that rounds response values to values in the grid .

-

(2)

Next, apply conformal prediction to this rounded data set. Specifically, we compute

for possible value .

-

(3)

Compute the desired quantile for the residuals,

where is the predefined desired error level.

-

(4)

The discretized prediction interval is given by

This prediction interval is, by construction, likely to cover the rounded test response value, . To invert the rounding step, the final prediction interval is then given by

The reason for the notation , for the grid of candidate values, is that in practice the grid is generally determined as a function of the data (and, therefore, the same may be true for the discretization function ). Most commonly, the grid might be determined by taking equally spaced points from some minimum value to some maximum value , where are determined by the empirical range of response values in the training data, i.e. by the range of . The function would then simply round to the nearest value in this grid. (The number of points, , is more commonly independent of the data, and simply depends on our computational budget—how many times we are willing to refit the model.)

To formalize the setting where and depend on the data, we let

be any finite set, let

be any function mapping to that set, that depend arbitrarily on the training and test data; however, and are constrained to be exchangeable functions of the data. If and are nearly always equal to and —as is the case when depends only on the range of the ’s, and simply rounds to the nearest value—then the fact that and depend on the data will only slightly affect coverage.

3.2 A better way to round: conformal prediction with a discretized model

While the naive rounded algorithm presented above, where the data itself is discretized, will successfully provide the correct coverage guarantees, it may be overly conservative. In particular, the prediction intervals will always need to be at least as wide as the interval between two grid points (as was also the case with the rounding approximation presented in Section 2.1). We now modify our algorithm to more fully use the information in the data, and hopefully to attain narrower intervals. Specifically, instead of discretizing the response data (the ’s), we instead require only that the fitted model can only depend on the discretized ’s, but use the full information of the ’s when computing the residuals.

-

(1)

,(2) As in the naive rounded algorithm, choose , , and , and compute for each .

-

(3)

Compute the desired quantile for the unrounded residuals,

-

(4)

Finally, the prediction interval is given by

This prediction interval is, by construction, likely to cover the unrounded test response value, ; it is no longer necessary to invert the rounding step.

3.3 Coverage guarantee

The following theorem proves the coverage properties of the prediction intervals computed by our two discretized conformal prediction methods.222 In some settings, we may prefer a discretization function that is random—for instance, if rounds to the nearest value in , this introduces some bias, but with randomization we can remove this bias by setting (1) where are the nearest elements to in the trial set . With this construction, we obtain (at least for those values that are not outside the range of the entries of ). Our main result, Theorem 2, can be modified to prove the expected coverage guarantee in this setting as well, although we do not include the details here.

Theorem 2.

Assume exchangeability of the training and test data points

Let be any finite set, where is an exchangeable function of the data points. Let be a discretization function, , also assumed to be exchangeable in the data points. Then the rounded conformal prediction interval, constructed under either the Conformal Prediction with Discretized Data or Conformal Prediction with a Discretized Model algorithms (presented in Section 3.1 and Section 3.2, respectively), satisfies the coverage guarantee

Before proving this result, we pause to note two special cases regarding the choice of the set and (randomized) discretization function :

-

•

If and are fixed (do not depend on the data), then the coverage rate is , since we can define and always.

-

•

If depends on the data only via the range of the response values, i.e. is only a function of and , while depends only on (e.g. simply rounds any number to its nearest value in , or does randomized rounding as in (1)), then the coverage rate is . This holds because, by defining as the corresponding function of the range of the full data set, i.e. of and , we have

We now prove our main result.

Proof of Theorem 2.

Our proof closely follows the structure of the results on non-rounded conformal prediction in the earlier literature.

We begin with the naive rounded algorithm from Section 3.1, Conformal Prediction with Discretized Data. Let

be the fitted model when using the complete rounded data set (i.e. the training data as well as the test data point), using the rounding scheme . Define residuals

for . Then, by construction, we can see that are exchangeable, since and are both symmetric functions of the data , and thus

or equivalently,

Next, on the event , we have for all , and moreover, . Therefore,

Finally, if , then it holds trivially that .

Next, we turn to the second algorithm, Conformal Prediction with a Discretized Model, presented in Section 3.2. Define as above, and define residuals

for . As before, are exchangeable, and so, similarly to the calculations above, we have

Next, on the event , we have . Therefore,

∎

3.4 Computational tradeoffs

With our main theoretical result, Theorem 2, in place, we are now able to trade off between the computation time of the algorithm, and the precision of its resulting prediction intervals. Specifically, both algorithms developed in this paper guarantee exact coverage regardless of the number of values tested (or, if depend weakly on the data, for instance via the range of the data values, then coverage probability may decrease very slightly). Of course, with a smaller set , the discretization will be more coarse, so the residuals will in general be larger and our resulting prediction interval will be wider.

One interesting phenomenon that we can observe is that, if the sample size is large, then our fitted models may be highly accurate (i.e. residuals are small) even if the added noise due to the rounding step is quite large. In other words, a low computational budget (a small set of trial values) can be offset by a large sample size. We explore these tradeoffs empirically in the next section.

4 Simulations

We now explore the effect of discretization in practice through a simulated data experiment.333Code to reproduce this experiment is available at http://www.stat.uchicago.edu/~rina/code/CP_rounded.R

Data

Our data is generated as

for noise level , where the features are generated from an i.i.d. Gaussian model, , with dimension . The mean function is given by

so that a linear model does not fit the data exactly, but is a fairly good approximation. The sample size is or . Our model fitting algorithm is given by fitting a Lasso,

for penalty parameter . We then generate a new data point from the same distribution, and set target coverage level at .

Methods

We compare the following methods:

-

•

Oracle: using the true coefficient vector and the Gaussian distribution of the noise, the prediction interval is given by .

-

•

Parametric: Let be the support of the Lasso solution. If we naively compute the confidence interval for the resulting least-squares model—that is, ignoring the fact that the feature set was selected as a function of the data—we would compute a prediction interval

Of course, since this computation ignores the selection event, we would expect this prediction interval to undercover.

-

•

Approximate Conformal Prediction (approximated via rounding)—the informal approximation to the conformal prediction algorithm, as presented in Section 2.1.

-

•

Conformal Prediction with Discretized Data (CPDD), as presented in Section 3.1.

-

•

Conformal Prediction with a Discretized Model (CPDM), as presented in Section 3.2.

For the rounded algorithms, we run the algorithm with grid size . The finite grid is then taken to be the set

where is the range of the observed response values in the training data. If the resulting prediction set is not an interval (which is seldom the case), we take the smallest interval containing the prediction set, for a simpler comparison.

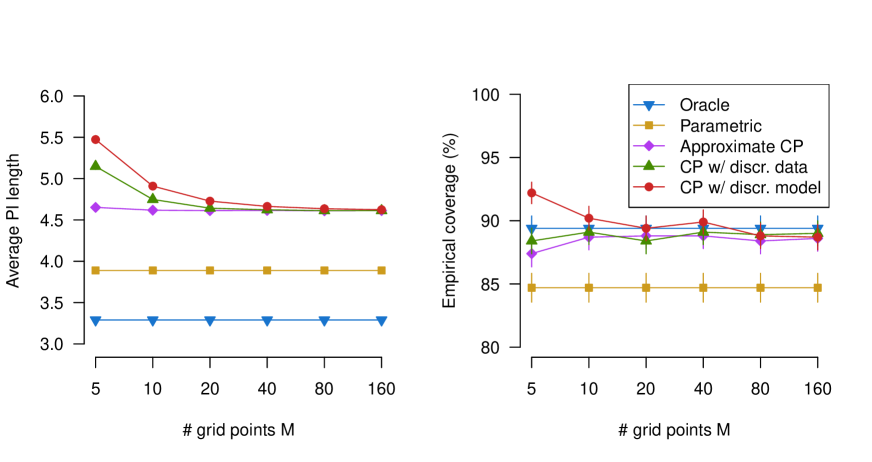

Results are averaged over 1000 trials.

Results

The resulting coverage probabilities and the average prediction interval lengths for each method are shown in Figure 1 (for sample size ) and Figure 2 (for ), across the different grid sizes . (Since the oracle method and parametric method do not use a discretized grid, reported values for these two methods are constant across .)

Examining the coverage plots first, the oracle method has 90% coverage as expected, and the two conformal prediction methods proposed here also show 90% (or higher) coverage. The “parametric” method, by ignoring the multiple testing problem inherent in the sparse model selection step, shows undercoverage for the smaller sample size . At , the selected model is more deterministic (as the signal-to-noise ratio is much stronger), so the selection event has less of an effect, and the coverage is closer to 90%. Finally, for the approximate conformal prediction method (i.e. the informal rounding scheme), this method shows the appropriate 90% coverage for higher values of , but can undercover when is low, particularly for the higher sample size . The reason is that if the grid points are spaced far apart, while residuals tend to be fairly small, then it may be the case that none of the grid point values are “plausible” enough to get included into the prediction interval. Therefore, this method is not reliable when the computational budget (i.e. the number of grid points ) is very low.

Next, we turn to the prediction interval length results—this length represents the precision of each procedure, as an extremely wide prediction interval is not informative. The oracle method of course yields the lowest possible PI length, providing a lower bound for the other methods. The approximate conformal prediction method (informal rounding) has somewhat lower PI length than the other rounded methods, but as discussed earlier, it fails to provide the guaranteed coverage rate. Comparing the two rounding algorithms proposed here, which do offer the desired coverage rate both in theory and empirically, at we see similar performance, with slightly better precision (lower PI width) for the Conformal Prediction with Discretized Data (CPDD) method. At , however, Conformal Prediction with a Discretized Model (CPDM) gives far better performance. To understand why, recall that for CPDD, when we discretize the data, the length of the PI will always be at least as large as the gap between two grid points; a small will therefore lead to an unfavorable lower bound on the PI length, regardless of the sample size . If we use CPDM, then coarse rounding (i.e. a low ) effectively adds noise to the values, but with a sufficiently high sample size , our fitted model will be highly accurate in spite of the high effective noise level, and we can obtain low PI lengths.

5 Summary

In this paper, we have formalized the role of rounding and discretization in the conformal prediction framework. These discretized algorithms allow conformal prediction methods to be used in practice when computational resources are limited, while providing rigorous guarantees that the right level of coverage will be maintained. Our simulations demonstrate that the level of discretization can be used to trade off between computation time and the precision of the prediction (i.e. the width of the prediction interval), enabling the user to obtain meaningful guarantees at any computational budget.

Acknowledgements

This work was partially supported by NSF award DMS1654076, by an Alfred P. Sloan fellowship, and by a J. and J. Neubauer Faculty Development Fellowship. The authors thank Jing Lei, Ryan Tibshirani, and Larry Wasserman for helpful discussions on the conformal prediction method, and Lin Gui for catching an error in an earlier draft of this paper.

References

- Burnaev and Vovk [2014] Evgeny Burnaev and Vladimir Vovk. Efficiency of conformalized ridge regression. In Conference on Learning Theory, pages 605–622, 2014.

- Chen et al. [2016] Wenyu Chen, Zhaokai Wang, Wooseok Ha, and Rina Foygel Barber. Trimmed conformal prediction for high-dimensional models. arXiv preprint arXiv:1611.09933, 2016.

- Lei [2017] Jing Lei. Fast exact conformalization of lasso using piecewise linear homotopy. arXiv preprint arXiv:1708.00427, 2017.

- Lei et al. [2016] Jing Lei, Max G’Sell, Alessandro Rinaldo, Ryan J Tibshirani, and Larry Wasserman. Distribution-free predictive inference for regression. arXiv preprint arXiv:1604.04173, 2016.

- Vovk et al. [2009] Vladimir Vovk, Ilia Nouretdinov, and Alex Gammerman. On-line predictive linear regression. The Annals of Statistics, 37(3):1566–1590, 2009.

- Vovk et al. [1999] Volodya Vovk, Alex Gammerman, and Craig Saunders. Machine-learning applications of algorithmic randomness. Proceedings of the 16th International Conference on Machine Learning, pages 444–453, 1999.

- Vovk et al. [2005] Volodya Vovk, Alex Gammerman, and Glenn Shafer. Algorithmic learning in a random world. Springer, New York, 2005.